Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

[X]

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2019

[ ]

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the

transition period from _______________ to

_______________

000-54416

(Commission

File Number)

Scandium International Mining Corp.

(Exact

Name of Registrant as specified in its charter)

|

British Columbia, Canada

|

|

98-1009717

|

|

(State

or other Jurisdiction of Incorporation or

organization)

|

|

(I.R.S.

Employer

Identification

No.)

|

|

1430 Greg Street, Suite 501

Sparks, Nevada

|

|

89431

|

|

(Address

of Principal Executive Offices)

|

|

(Zip

Code)

|

Registrant’s

Telephone Number, including area code: (775) 355-9500

Securities

registered pursuant to Section 12(b) of the Act: None

Securities to be

registered pursuant to Section 12(g) of the Act: Common Shares

without par value

(Title of class)

Indicate

by check mark if the registrant is a well-known seasoned issuer, as

defined in Rule 405 of the Securities Act. Yes [ ] No

[X]

Indicate

by check mark if the registrant is not required to file reports

pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No

[X]

Indicate

by check mark whether the registrant (1) has filed all reports

required to be filed by Section 13 or 15(d) of the Securities

Exchange Act of 1934 during the preceding 12 months (or for such

shorter period that the registrant was required to file such

reports), and (2) has been subject to such filing requirements for

the past 90 days. Yes [X] No [ ]

Indicate

by check mark whether the registrant has submitted electronically

every Interactive Data File required to be submitted pursuant to

Rule 405 of Regulation S-T (§

232.405 of this chapter) during the preceding

12 months (or for such shorter period that the registrant was

required to submit such files). Yes [X] No [ ]

Indicate

by check mark whether the registrant is a large accelerated filer,

an accelerated filer, a non-accelerated filer, a smaller reporting

company or an emerging

growth company. See the definitions of “large

accelerated filer,” “accelerated filer”

“smaller reporting company” and “emerging

growth company” in Rule 12b-2 of the Exchange Act (Check

one):

|

Large

Accelerated Filer ☐

|

|

Accelerated

Filer ☐

|

|

Non-Accelerated

Filer ☐

|

|

Smaller

Reporting Company☒

|

|

|

|

Emerging

Growth Company ☐

|

If an

emerging growth company, indicate by check mark if the registrant

has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided

pursuant to Section 13(a) of the Exchange Act [ ]

Indicate

by check mark whether the registrant is a shell company (as defined

in Rule 12b-2 of the Exchange Act). Yes [ ] No [X]

State

the aggregate market value of the voting and non-voting common

equity held by non-affiliates computed by reference to the price at

which the common equity was sold, or the average bid and asked

price of such common equity, as of the last business day of the

registrant’s most recently completed second fiscal quarter:

$16,990,618 as at June 30, 2019.

Indicate

the number of shares outstanding of each of the registrant’s

classes of common equity, as of the latest practicable

date: 312,482,595 common shares as at February 25, 2020.

DOCUMENTS

INCORPORATED BY REFERENCE

Portions

of the registrant's Proxy Statement for the Annual Meeting of

Stockholders are incorporated by reference into Part III of this

Form 10-K, which Proxy Statement is to be filed within 120 days

after the end of the registrant's fiscal year ended December 31,

2019.

TABLE OF CONTENTS

PART I

Note about Forward-Looking

Statements

Certain

statements contained in this annual report on Form 10-K and the

documents incorporated by reference herein constitute

"forward-looking statements.” Forward-looking statements may

include, but are not limited to, statements with respect to the

future price of commodities, the estimation of mineral resources,

the realization of mineral resource estimates, the timing and

amount of estimated future production, costs of production, capital

expenditures, costs and timing of the development of new deposits,

success of exploration activities, our ability to fund property

acquisition costs, our ability to reach targeted time frames for

establishing feasibility, permitting time lines, currency

fluctuations, requirements for additional capital, government

regulation of mining operations, environmental risks, unanticipated

reclamation expenses, title disputes or claims, our ability to

raise funds necessary for ongoing and planned expenditures and

operations, and regulatory approvals. In certain cases,

forward-looking statements can be identified by the use of words

such as "plans,” "expects" or "does not expect,” "is

expected,” "scheduled,” "estimates,” "intends,

"anticipates" or "believes,” or variations of such words and

phrases or state that certain actions, events or results

"may,” "could,” "would" or "will be taken,”

"occur" or "be achieved.” Forward-looking statements involve

known and unknown risks, uncertainties and other factors which may

cause our actual results, performance or achievements to be

materially different from any future results, performance or

achievements expressed or implied by the forward-looking

statements. Such factors may include, among others, risks related

to our joint venture operations; actual results of current

exploration activities or production technologies that we are

currently testing; actual results of reclamation activities; future

metal prices; accidents, labour disputes and other risks of the

mining industry; delays in obtaining governmental or regulatory

approvals or financing or in the completion of development

activities, as well as those factors discussed in the section

entitled "Risk Factors" and elsewhere in this Form 10-K. Although

we have attempted to identify important factors that could cause

actual actions, events or results to differ materially from those

described in forward looking statements, there may be other factors

that cause actions, events or results not to be as anticipated,

estimated or intended. There can be no assurance that

forward-looking statements will prove to be accurate, as actual

results and future events could differ materially from those

anticipated in such statements. Accordingly, readers should not

place undue reliance on forward-looking statements.

Glossary of Terms

“Company,”

“SCY,” “we,” “us,”

“our” and similar words of similar meaning refer to

ScandiumInternational Mining Corp.

$, A$, C$

mean

respectively, United States dollars, Australian dollars and

Canadian dollars.

Alteration

Usually referring

to chemical reactions in a rock mass resulting from the passage of

hydrothermal fluids.

Assay

An analysis to

determine the presence, absence or quantity of one or more

components, elements or minerals.

Core

The long

cylindrical piece of a rock, up to several inches in diameter,

brought to the surface by Diamond drilling.

Diamond drilling

A drilling method

in which the cutting is done by abrasion using diamonds embedded in

a matrix rather than by percussion. The drill cuts a core of rock,

which is recovered in long cylindrical sections.

Fractures

Breaks in a rock,

usually due to intensive folding or faulting.

Grade

The

concentration of a valuable mineral within an Ore.

Hydrothermal

Hot fluids, usually

water, which may or may not carry metals and other compounds in

solution to the site of mineral deposition or wall rock

alteration.

Igneous

A rock formed by

the cooling of molten silicate material.

Intrusion

A general term for

a body of igneous rock formed below the surface of the

earth.

4

Kg

Kilogram which is

equivalent to approximately 2.20 pounds.

Km

Kilometer which is

equivalent to approximately 0.62 miles.

Mineralization

A term used to

describe the presence of minerals of possible economic value. Also

used to describe the process by which concentration of economic

minerals occurs.

Net Smelter

A share of the net

revenues generated from the sale of metal produced by a

mine.

Returns

Royalty

NI 43-101

National Instrument

43-101 – Standards for

Disclosure of Mineral Projects, being the regulation adopted

by Canadian securities regulators that governs the public

disclosure of technical and scientific information concerning a

mineral property.

Ore

A

naturally occurring solid material from which a metal or valuable

mineral can be profitably extracted.

Outcrop

An exposure of rock

at the earth’s surface.

ppm

Parts per

million.

Pyrite

Iron sulphide

mineral. The most common and abundant sulphide mineral and often

found in association with copper and gold.

Qualified Person

Means a Qualified

Person as defined in National Instrument 43-101, including an

engineer or geoscientist in good standing with their professional

association, with at least five years of relevant

experience.

Quartz

The second most common rock forming mineral in

the earth’s crust. SiO2.

Resource

Means any of a

measured, indicated or inferred resource as used in NI 43-101, and

having the following meanings:

“measured resource” is that part of a Mineral Resource

for which quantity, grade or quality, densities, shape, and

physical characteristics are so well established that they can be

estimated with confidence sufficient to allow the appropriate

application of technical and economic parameters, to support

production planning and evaluation of the economic viability of the

deposit. The estimate is based on detailed and reliable

exploration, sampling and testing information gathered through

appropriate techniques from locations such as outcrops, trenches,

pits, workings and drill holes that are spaced closely enough to

confirm both geological and grade continuity.

“indicated resource” is that part

of a Mineral Resource for which quantity, grade or quality,

densities, shape and physical characteristics, can be estimated

with a level of confidence sufficient to allow the appropriate

application of technical and economic parameters, to support mine

planning and evaluation of the economic viability of the deposit.

The estimate is based on detailed and reliable exploration and

testing information gathered through appropriate techniques from

locations such as outcrops, trenches, pits, workings and drill

holes that are spaced closely enough for geological and grade

continuity to be reasonably assumed.

“inferred resource” is that part of

a Mineral Resource for which quantity and grade or quality can be

estimated on the basis of geological evidence and limited sampling

and reasonably assumed, but not verified, geological and grade

continuity. The estimate is based on limited information and

sampling gathered through appropriate techniques from locations

such as outcrops, trenches, pits, workings and drill

holes.

For the

purposes of the above a “mineral resource” means a

concentration or occurrence of diamonds, natural solid inorganic

material, or natural solid fossilized organic material including

base and precious metals, coal, and industrial minerals in or on

the Earth’s crust in such form and quantity and of such a

grade or quality that it has reasonable prospects for economic

extraction. The location, quantity, grade, geological

characteristics and continuity of a Mineral Resource are known,

estimated or interpreted from specific geological evidence and

knowledge.

(Please

refer to “Item 2. Properties -

Cautionary Note to U.S. Investors Regarding Resource

Estimates” in regards to the use of the above terms in this

Form 10-K.)

5

Sulphide

A class of minerals

characterized by the linkage of sulphur with a metal (such as

Pyrite (FeS2)).

Tpd/Tpa

Tonnes per

day/tonnes per annum.

Tonne

A metric ton which

is equivalent to approximately 2,204 pounds.

Sediments

The debris

resulting from the weathering and breakup of rocks that have been

deposited by or carried by runoff, streams and rivers, or left over

from glacial erosion or sometimes from wind action.

Vein

A geological

feature comprised of minerals (usually dominated by quartz) that

are found filling openings in rocks created by faults or replacing

rocks on either side of faults or fractures.

6

ITEM 1. BUSINESS

General

We were

incorporated on July 17, 2006 under the laws of British Columbia,

Canada under the name

Golden Predator Mines Inc. We were incorporated as a wholly owned

subsidiary of Energy Metals Corp. for the purpose of holding

precious metals and certain specialty metals assets. In order to

focus on specialty metals, during February 2009 we transferred most

of our precious mineral assets to our then wholly-owned subsidiary

Golden Predator Corp., and on March 6, 2009 we completed a spin-out

of Golden Predator Corp. to our shareholders. Effective March 12,

2009, we changed our name to EMC Metals Corp. In order to reflect a

new emphasis on mining for scandium minerals, effective November

19, 2014, we changed our name to Scandium International Mining Corp

(“SCY” or the “Company”).

We are

a reporting issuer in the Canadian Provinces of British Columbia,

Alberta and Ontario and our common shares are listed for trading on

the Toronto Stock Exchange under the trading symbol

“SCY.”

Our

head office is located at 1430 Greg Street, Suite 501, Sparks,

Nevada 89431. The address of our registered office is 1200 - 750

West Pender Street, Vancouver, British Columbia, Canada,

V6C 2T8.

Our

focus of operations is the development of the Nyngan scandium

project located in New South Wales, Australia (the “Nyngan

Scandium Project”). We also hold a scandium mineral property

located nearby Nyngan known as the “Honeybugle Scandium

property” and a reservation on an exploration license in

Finland, known as the “Kiviniemi Scandium

property.”

Our

plan of operation for the remainder of 2020 is to obtain offtake

sales agreements with counterparties for Nyngan Scandium Project

product and seek additional funding for project construction and

corporate working capital. We also plan to continue to test and

develop unique scandium recovery and finishing techniques,

including the processing of intermediate scandium aluminum

products.

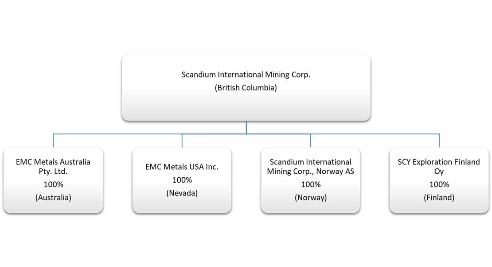

Intercorporate Relationships

The

chart below illustrates our corporate structure on December 31,

2019, including our subsidiaries, the jurisdictions of

incorporation, and the percentage of voting securities

held.

7

Recent History

Nyngan Feasibility Study

On

April 18, 2016, the Company announced the results of an

independently-prepared feasibility study on the Nyngan Scandium

Project. The technical report on the feasibility study entitled

“Feasibility Study –

Nyngan Scandium Project, Bogan Shire, NSW, Australia”

is dated May 4, 2016 and was independently compiled pursuant to the

requirements of NI 43-101. The report was filed on May 6, 2016 and

is available on SEDAR (www.sedar.com)

and on the Company’s website (www.scandiummining.com)

and the SEC’s website (www.sec.gov). A summary of the report

is provided herein under “Item 2. Properties – Description of

Mineral Projects – Nyngan Scandium Project – Nyngan

Feasibility Study.”

Transactions with Scandium Investments LLC

In June of 2017, the Company entered into a share exchange

agreement with Scandium Investments LLC (“SIL”) for the

purchase of SIL’s 20% interest in EMC Metals Australia Pty

Ltd (“EMC Australia”) in exchange for 57,371,565 common

shares of SCY as well as an additional 1,459,080 common shares as a

royalty adjustment payment. Closing of the purchase of the EMC

Australia shares was subject to shareholder approval, which the

Company obtained at a special meeting of shareholders held on

September 11, 2017. The transaction subsequently closed on October

9, 2017, with SCY holding a

100% ownership interest of EMC Australia. Under the terms of the

share exchange agreement, SIL was granted the right to nominate two

individuals to the board of the Company for so long as SIL held at

least 15% of SCY’s issued and outstanding shares, and one

director for so long as SIL held at least 5% but less than 15% of

SCY’s issued and outstanding shares. Pursuant to the

nomination rights, Peter Evensen and R. Christian Evensen were

appointed as directors to the SCY Board on closing of the

transaction.

Business Operations

Company Summary

We are

a mineral exploration and development company that is primarily

focused on the development of scandium mineral resources, and

scandium end-use markets, through identification of value-added

applications for scandium in aluminum alloys and end products. The

Company has also considered exploration and development interest in

rare earth minerals, and other specialty metals, including nickel,

cobalt, boron, manganese, tantalum, titanium and zirconium. We have

not commenced development of any of our scandium projects, and as a

result we are an exploration stage company.

We have

established a 16.9 million tonne measured and indicated resource on

the Nyngan property (grading 235ppm at a 100ppm cut-off) and we

have also established a 1.43 million tonne mineral reserve

(combined proven and probable) on the Nyngan Scandium Project,

based on economics presented in our 2016 feasibility

study.

Our

principal project is the Nyngan Scandium Project located in New

South Wales, Australia, in which we own 100% of the mineral rights,

including exploration licenses and a mining lease grant on the

portion of the property that corresponds to the feasibility study

development. In April 2014, we also acquired an exploration license

referred to as the Honeybugle Scandium property, a prospective

scandium exploration property located 24 kilometers from the Nyngan

Scandium Project. During August

2018, we were granted an exploration license for the Kiviniemi

Scandium property in central Finland from the Finnish regulatory

body governing mineral exploration and mining in

Finland.

Corporate Objectives and Strategy

Our

corporate focus is to produce and sell scandium (Sc) and

scandium-based products. None of our current properties have

advanced to the development or production stage and we are

currently an exploration stage company. We have completed an

independently prepared definitive feasibility study

(“DFS”) of the Nyngan Scandium Project. Subject to

successfully financing of construction costs, we intend to develop

the Nyngan Scandium Project for production, with a view to

supplying anticipated demand for scandium oxide and

scandium-content materials. For further information on the Nyngan

Scandium Project, please refer to “Item 2. Properties - Description of Mineral Projects –

Nyngan Scandium Project” and

“Item 1A. Risk Factors.”

Concurrently

with our analysis of the Nyngan Scandium Project, we are developing

and testing unique mineral recovery techniques as well as

techniques to produce high quality intermediate scandium-content

aluminum alloy products. If effective at a commercial level, these

mineral recovery techniques, scandia finishing techniques and

intermediate product developments are expected to provide increased

economic margins and returns on capital on any future scandium

production.

Presently

our recovery and finishing technology is completed to a degree that

supports engineering and flow sheet design for our +15%/-5% DFS,

although further development work will continue in both areas.

There is no guarantee that we will be able to benefit from the

commercial application of such techniques or that we will have

scandium production in the future.

8

Global Scandium Production and Market

Scandium

is the 31st most abundant

element in the earth’s crust (average 33 ppm), which makes it

more common than lead, mercury and precious metals, but less common

than copper. Scandium has characteristics that are similar to rare

earth elements, and it is often classified as a member of that

group, although it is technically a light transition metal.

Scandium occurs in nature as an oxide, rarely occurs in

concentrated quantities because it does not selectively combine

with the common ore-forming anions, and is very difficult to reduce

to a pure metal state. Scandium is typically produced and sold as

scandium oxide (Sc2O3), more properly

known as scandia.

Global

annual production estimates of scandium range from 15 tonnes to 20

tonnes, but accurate statistics are not available due to the lack

of public information from countries in which scandium is currently

being produced. There are five known, primary production sources

globally today: stockpiles from the former Zhovti Voty uranium mine

in Ukraine, the rare earth mine at Bayan Obo in China, apatite

mines on the Kola Peninsula in Russia, by-product production from

titanium dioxide (TiO2) pigment refiners

in China, and recent start-up production of scandium oxide

concentrates from the Taganito Nickel Mine in the Philippines

(Sumitomo Metal Mining Co., Ltd.).

There

is no reliable pricing data on global scandium oxide trading. The

U.S. Geological Survey (“USGS”) in its latest available

report (dated January 2020) documents the 2019 price of scandium

oxide (99.99% grade) at US$3,900/kg, indicating a reduction from

the 2018 price estimate of US$4,600/kg. Small quantities of

scandium oxide, suitable for laboratory investigations, are

currently offered on the internet by traders for prices at this

level. Larger quantities of oxide product at varying purities are

available at considerably lower prices, typically below

US$2,000/kg. Scandium oxide grades of 95% or greater are considered

commercially suitable, with 99.9% grade used for electrical

applications, and grades higher than 99.9% reserved for science and

new technical applications. Scandium oxide grades of 95-99% are

generally considered suitable for aluminum alloy

applications.

Scandium

oxide is typically traded in small quantities, between private

parties, and pricing is not transparent to other buyers or sellers

as there is no clearing facility as is more common with

commercially traded metals and commodities. Prices do vary, based

on purity and quantity supplied. Small sale quantities tend to

command premium prices, and large quantities (over one tonne) are

simply not available to establish appropriate commercial

pricing.

Scandium

can also be effectively purchased in the form of aluminum-scandium

(Al-Sc) master alloy, typically containing 2% scandium by weight.

This product is the preferred form for manufacture of aluminum

alloys containing scandium. The latest available 2019 USGS report

indicates the 2018 price for Al-Sc 2% master alloy at US$360/kg,

slightly higher than the 2017 USGS average. Recent USGS estimated

prices for Al-Sc 2% master alloy have also been high relative to

commonly available prices, which have trended under US$100/kg and

are available in one tonne lots or greater today.

Principal

uses for scandium are in high-strength aluminum alloys,

high-intensity metal halide lamps, electronics, and laser research.

Recently developed applications include welding wire and fuel cells

which are expected to be in future demand. Approximately 15

different commercial aluminum-scandium alloys have been developed,

and some of them are used for aerospace applications. In Europe and

the U.S., scandium-containing alloys have been evaluated for use in

structural parts in commercial airplanes and high stress parts in

automobile engines and brake systems. Military and aerospace

applications are known to be of interest, although with less

specificity. The combination of high strength, weldability and

ductility makes aluminum-scandium alloys potentially attractive

replacements for existing aluminum alloys in a number of

applications where improved alloy properties can add value to final

products.

Competitive Conditions

We compete with numerous other companies and individuals in the

search for and the acquisition or control of attractive rare earth

and specialty metals mineral properties. Our ability to acquire

further properties will depend not only on our ability to operate

and develop our properties but also on our ability to select and

acquire suitable properties or prospects for development or mineral

exploration.

In regard to our plan to produce scandium, there are a limited

number of scandium producers presently. If we are successful at

becoming a producer of scandium, our ability to be competitive will

require that we establish a reliable supply of scandium to the

market, delivered at purity levels demanded by various

applications, and that our operating costs generate margins at

prices that will be set by customers and competitors in a market

yet to mature.

Governmental Regulations and Environmental Laws

The

development of any of our properties, and specifically the Nyngan

Scandium Project, will require numerous local and national

government approvals and environmental permits. For further

information about governmental approvals and permitting

requirements, please refer to “Item 1A. Risk

Factors”.

Employees

As at January 1, 2020, we have 5 full and part time employees and 5

individuals working on a consulting basis. Our operations are

managed by our officers with input from our directors. We engage

geological, metallurgical, and engineering consultants from time to

time as required to assist in evaluating our property interests and

recommending and conducting work programs.

ITEM 1A. RISK FACTORS

In

addition to the factors discussed elsewhere in this Form 10-K, the

following are certain material risks and uncertainties that are

specific to our industry and properties that could materially

adversely affect our business, financial condition and results of

operations.

9

Risks Associated with the Nyngan Scandium Project

There are technical challenges to scandium production that may

render the Nyngan Scandium Project not economic. The

economics of scandium recovery are known to be challenging. There

are very few facilities producing scandium and the existing

scandium producers are secretive in their techniques for recovery.

In addition, the recovery of scandium product from laterite

resources, such as are found on the Nyngan property, has not been

demonstrated at an operating facility. The Nyngan processing

facility design, if constructed, will be the first of its kind for

scandium production. These factors increase the possibility that we

will encounter unknown or unanticipated production and processing

risks. Should we encounter any of these risks, they could increase

the cost of production thereby reducing margins on the Nyngan

Scandium Project or rendering it uneconomic.

There is no guarantee that we will be able to finance the Nyngan

Scandium Project for production. Any decision to proceed

with production on the Nyngan Scandium Project will require

significant production financing. Scandium projects are uncommon,

and economic and production uncertainty may limit our ability to

attract the required amount of capital to put the project into

production. If we are unable to source production financing on

commercially viable terms, we may not be able to proceed with the

project and may have to write off our investment in the

project.

If we are successful at achieving production, we may have

difficulty selling scandium. Scandium is characterized by

unreliable supply, resulting in limited development of markets for

scandium oxide. Markets may take longer to develop than

anticipated, and Nyngan and other potential scandium producers may

have to wait for products and applications to create adequate

demand. Certain applications may require lengthy certification

processes that could delay usage or acceptance. In addition,

certain scandium applications require very high purity scandium

product, which is much more difficult to produce than lower grade

product. If we commence production, our inability to supply

scandium in sufficient quantities, in a reliable and timely manner,

and in the correct quality, could reduce the demand for any

scandium produced from our projects and possibly render the project

uneconomic.

General Risks Associated with our Mining Activities and

Company

We may not receive permits necessary to proceed with the

development of a mining project. The development of any of

our properties, including the Nyngan Scandium Project, will require

the acquisition and sustained possession of numerous local and

national government approvals and permits. Our ability to secure

all necessary permits required to develop any of our projects is

unknown until such permits are received. If we cannot obtain or

retain all necessary permits, the Nyngan Scandium Project cannot be

developed, and our investment in the project will potentially be

lost. While the critical permits for the Nyngan Scandium Project

have been received, other permits remain outstanding at this time

and continuing compliance with the terms of the permits is

required. Our future market value will likely be significantly

reduced to the extent one or more of our projects cannot proceed to

the development or production stage due to an inability to secure

all required permits.

Mineral Resource Estimates on our properties are subject to

uncertainty and may not reflect what may be economically

extracted. Resource estimates

included for scandium on our Nyngan property are estimates only and

no assurances can be given that the estimated levels of scandium

minerals will actually be produced or that we will receive the

metal prices assumed in determining our resources. Such estimates

are expressions of judgment based on knowledge, mining experience,

analysis of drilling and exploration results and industry

practices. Estimates made at any given time may change

significantly when new information becomes available or when

parameters that were used for such estimates change. By their

nature resource estimates are imprecise and depend, to a certain

extent, upon statistical inferences which may ultimately prove

unreliable. Furthermore, market price fluctuations in scandium, as

well as increased capital or production costs or reduced recovery

rates, may limit our ability to establish reserves at some future

point on Nyngan, or on any of our properties. The extent to which

more Nyngan project resources may ultimately be reclassified as

proven or probable reserves is dependent upon the demonstration of

their profitable recovery. The evaluation of reserves or resources

is always influenced by economic and technological factors, which

may change over time. Accordingly, further current resource

estimates on our material properties may never be converted into

reserves, or be economically extracted, and we may have to write

off such properties or incur a loss on sale of our interest on such

properties, which will likely reduce the value of our

shares.

Our potential for a competitive advantage in specialty and rare

metals production depends on the availability of our technical

processing abilities, as currently provided by our Chief Technology

Officer. We

are dependent upon the personal efforts and commitment of Willem

Duyvesteyn, our CTO, a director and significant shareholder of the

Company, for the continued development of new extractive

technologies related to scandium and other rare and specialty

metals production. The loss of the services of Mr. Duyvesteyn would

likely limit our ability to use or continue the development of such

technologies, which would remove the potential competitive and

economic benefit of such technologies.

Our operations are subject to losses due to exchange rate

fluctuation. We

maintain accounts in Canadian, Australian, Euro and U.S. currency.

Our equity financings have to date been priced in Canadian dollars.

All of our material projects and non-cash assets are located

outside of both Canada and the USA, however, and require regular

currency conversions to local currencies where such projects and

assets are located. Our operations are accordingly subject to

foreign currency fluctuations and such fluctuations may materially

affect our financial position and results. We do not engage in

currency hedging activities.

We do not currently earn any revenue and without additional

funding, we will not be able to carry out our business plan, and if

we raise additional funding existing security holders may

experience dilution. As an

exploration stage mining company, none of our principal properties

are in operation and we do not currently earn any revenue. In order

to continue our exploration activities and to meet our obligations

on the Nyngan Scandium Project, we will need to raise additional

funds. Recently, we have relied entirely on the sale of our

securities to raise funds for operations. Our ability to continue

to raise funds from the sale of our securities is subject to

significant uncertainty due to volatility in the mineral

exploration marketplace. If we are able to raise funds from the

sale of our securities, existing security holders may experience

significant dilution of their ownership interests and possibly to

the value of their existing securities.

10

ITEM 2.

PROPERTIES

Cautionary Note to U.S. Investors Regarding Resource

Estimates

Certain terms used in this section are those used in accordance

with the requirements of the securities laws in effect in Canada,

which differ from the requirements of U.S. securities laws.

Canadian requirements, including NI 43-101, differ significantly

from the requirements of the U.S. Securities and Exchange

Commission (the “SEC”), and resource information

contained herein may not be comparable to similar information

disclosed by U.S. companies.

In particular, and without limiting the generality of the

foregoing, the term “resource” does not equate to the

term “reserves.” The requirements of NI 43-101 for

identification of “reserves” are not the same as those

of the SEC, and reserves reported in compliance with NI 43-101 may

not qualify as “reserves” under SEC standards. Under

U.S. standards, mineralization may not be classified as a

“reserve” unless the determination has been made that

the mineralization could be economically and legally produced or

extracted at the time the reserve determination is

made.

The SEC’s disclosure standards normally do not recognize

information concerning “measured mineral resources.”

“indicated mineral resources” or “inferred

mineral resources” or other descriptions of the amount of

mineralization in mineral deposits that do not constitute

“reserves” by U.S. standards, in documents filed with

the SEC. In addition, resources that are classified as

“inferred mineral resources” have a great amount of

uncertainty as to their existence and great uncertainty as to their

economic and legal feasibility. It cannot be assumed that all or

any part of an “inferred mineral resource” will ever be

upgraded to a higher category. Under Canadian rules, estimated

“inferred mineral resources” may not generally form the

basis of feasibility or pre-feasibility studies. Investors are

cautioned not to assume that all or any part of an “inferred

mineral resource” exists or is economically or legally

mineable.

Disclosure of “contained ounces” in a resource is

permitted disclosure under Canadian regulations, however, the SEC

normally only permits issuers to report mineralization that does

not constitute “reserves” by SEC standards as in-place

tonnage and grade without reference to unit measures.

Accordingly, information concerning mineral deposits set forth

herein may not be comparable with information presented by

companies using only U.S. standards in their public

disclosure.

Description of Mineral Projects

Nyngan Scandium Project

Property Description and Location

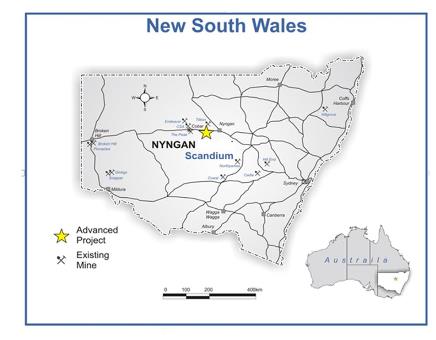

The

Nyngan Scandium Project site is located approximately 450

kilometres northwest of Sydney, NSW, Australia and approximately 20

kilometres due west from the town of Nyngan, a rural town of

approximately 2,900 people. The deposit is located 5 kilometres

south of Miandetta, off the Barrier Highway that connects the town

of Nyngan to the town of Cobar. The license area can be reached via

the paved Barrier Highway, which allows year-round access, but

final access to the site itself is reached by clay farm tracks. The

general area can be characterized as flat countryside and is

classified as agricultural land, used predominantly for wheat

farming and livestock grazing. Infrastructure in the area is good,

with available water and electric power in close proximity to the

property boundaries.

The Nyngan property is classified as an Australia Property

for purposes of financial statement segment

information.

The

scandium resource is hosted within the lateritic zone of the Gilgai

Intrusion, one of several Alaskan-type mafic and ultramafic bodies

which intrude Cambrian-Ordovician metasediments collectively called

the Girilambone Group. The laterite zone, locally up to 40 meters

thick, is layered with hematitic clay at the surface followed by

limonitic clay, saprolitic clay, weathered bedrock and finally

fresh bedrock. The scandium mineralization is concentrated within

the hematitic, limonitic, and saprolitic zones with values up to

350 ppm scandium.

11

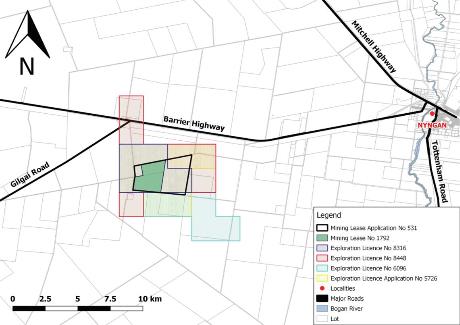

The

general location of the Nyngan Scandium Project is provided in

Figure 1 below. The specific location of the exploration licenses

that we may earn an interest in are provided in Figure 2

below.

Figure 1: Location of Nyngan Scandium Project

Note:

None of the Existing Mines identified in Figure 1 produce

scandium.

12

Figure 2: Location of the Exploration Licenses and Mining Lease for

the Nyngan Scandium Project

Mineral License Details

The

scandium resource is held under Exploration License (EL) 8316

(Block Number 3132, units d, e, j, k and Block no. 3133, unit f)

and EL 6096 (Block 3132, unit p, and Block 3133, units l, m, r and

s); a total of ten (10) graticular units. The exploration licenses

allow the license holder to conduct exploration on private land

(with landowner consents and signed compensation agreements in

place) and public lands not including wildlife reserves, heritage

areas or National Parks. The scandium resource is fully enclosed on

private agricultural land.

The

Company’s Australian subsidiary holds legal title to both the

surface and mineral exploration rights on the Nyngan Scandium

Project.

During

2017, an additional EL (EL 8448) was granted. Figure 2 provides

details of the location of EL 8448 and the locations of Mining

Lease 1792 and Mining Lease Application 531, both of which overlay

the exploration license area.

The exploration licenses cover 29.25 square kilometers (2,925

hectares). The resource site is located at geographic

coordinates MGA zone 55, GDA 94, Lat: - 31.5987, Long: 146.9827,

Map Sheets 1:250k – Cobar (SH/55-14) and 1:100k Hermidale

(8234).

The project surface rights (freehold) total 810 acres (370

hectares) on the portion of the exploration license area

corresponding to the Mine Lease 1792 area. The freehold

property boundaries are defined by standard land survey techniques

undertaken by the Lands Department and currently presented in the

form of Cadastral Deposited Plans (DP) and Lots. The land

associated with the project rights is DP 752879, Lots 6 and 7

(Appendix 2, Lots 6 and 7 - Nyngan).

The Company is required to lodge individual A$10,000 environmental

bonds with the NSW Mines Department for each license, and must meet

total minimum work requirements annually of approximately A$65,000,

covering both licenses.

Royalties attached to the properties include a 1.5% Net Profits

Interest royalty to private parties involved with the early

exploration on the property, a 1.7% Net Smelter Returns Royalty

payable to Jervois for 12 years after production commences, subject

to terms in the settlement agreement, and a 0.7% royalty on gross

mineral sales to a private investor. Another revenue royalty is

payable to private interests of 0.2%, subject to a US$370k cap. A

NSW minerals royalty will also be levied on the project, subject to

negotiation, currently 4% on revenue.

13

Metallurgy Development

The

Company has invested in and developed methodology for extracting

scandium from the Nyngan property resource since 2010. A portion of

the work done over this period has been superseded by work that

followed, but subsequent test programs universally benefitted from

prior efforts. In summary, the programs have been as

follows:

●

2010 – The

Company inherited work done on Nyngan from the previous property

owner, and applied that work to a quick flowsheet and capital

estimate done for management by Roberts & Schaefer of Salt Lake

City, Utah;

●

2011 – The

Company employed Hazen Research, Inc., of Golden, Colorado, USA

(“Hazen”) to test acid baking techniques and solvent

extraction (“SX”) processes with Nyngan resource

material. The Company also employed SGS-Lakefield (Ontario) to test

pressure acid leach techniques on Nyngan resource, as a replacement

for or an enhancement to acid bake techniques done earlier in the

year by Hazen;

●

2012 – The

Company engaged SNC-Lavalin to do an economic study for management,

utilizing an acid bake flowsheet and SX work from the Hazen test

program;

●

2014 – The

Company published a preliminary economic assessment

(“PEA”) entitled NI 43-101F1 Technical Report on the

Feasibility of the Nyngan Scandium Project, authored by Larpro Pty

Ltd, utilizing both Hazen and SGS-Lakefield test work results;

and

●

2015 – The

Company amended and refiled the 2014 PEA Report as the “Amended Technical Report and

Preliminary Economic Analysis on the Nyngan Scandium Project, NSW,

Australia.”

●

2016 – The

Company published an independently prepared definitive feasibility

study (“DFS”) on the Nyngan Scandium Project. The

technical report on the feasibility study entitled

“Feasibility Study –

Nyngan Scandium Project, Bogan Shire, NSW, Australia”

was independently compiled pursuant to the requirements of NI

43-101 and incorporated the results of current and previous test

work.

Nyngan Feasibility Study

On

April 18, 2016, the Company announced the results of an independent

definitive feasibility study on the Nyngan Scandium Project. The

technical report on the feasibility study entitled

“Feasibility Study –

Nyngan Scandium Project, Bogan Shire, NSW, Australia”

is dated May 4, 2016 and was independently compiled pursuant to the

requirements of NI 43-101 (the “Feasibility Study” or

“DFS”). The report was filed on May 6, 2016 and is

available on SEDAR (www.sedar.com)

and on the Company’s website (www.scandiummining.com)

and the SEC’s website (www.sec.gov). A full discussion on the

technical report was provided in the Company’s Form 10Q for

the quarterly period ending March 31, 2016, as filed with the SEC

and on SEDAR on May 13, 2016.

The

Feasibility Study concluded that the Nyngan Scandium Project has

the potential to produce an average of 37,690 kilograms of scandium

oxide (scandia) per year, at grades of 98.0%-99.8%, generating an

after-tax cumulative cash flow over a 20 year project life of

US$629 million, with an NPV10% of US$177

million. The average process plant feed grade over the 20 year

project life is 409ppm of scandium.

The

financial results of the Feasibility Study are based on a

conventional flow sheet, employing continuous high pressure acid

leach (HPAL) and solvent extraction (SX) techniques. The flow sheet

was modeled and validated from METSIM modeling and considerable

bench scale/pilot scale metallurgical test work utilising Nyngan

resource material. A number of the key elements of this flowsheet

work have been protected by the Company under US patent

applications.

The

Feasibility Study has been developed and compiled to an accuracy

level of +15%/-5%, by a globally recognized engineering firm that

has considerable expertise in laterite deposits and process

facilities, as well as in smaller mining and processing projects,

and has excellent familiarity with the Nyngan Scandium Project

location and environment.

Nyngan Scandium Project Highlights

●

Capital cost

estimate for the project is US$87.1 million,

●

Annual scandium

oxide product volume averages 37,690 kg, over 20

years,

●

Annual revenue of

US$75.4 million (oxide price assumption of

US$2,000/kg),

●

Operating cost

estimate for the project is US$557/kg scandium oxide,

●

Project Constant

Dollar NPV10% is US$177 million, (NPV8% is US$225

million),

●

Project Constant

Dollar IRR is 33.1%,

●

Oxide product

grades of 98-99.8%, as based on customer requirements,

●

Project resource

increases by 40% to 16.9 million tonnes, grading 235ppm Sc, at a

100ppm cut-off in the measured and indicated categories,

and

●

Project Reserve

totalling 1.43 million tonnes, grading 409ppm Sc was established on

part of the resource.

14

DFS Conclusions and Recommendations

The

production assumptions in the Feasibility Study are backed by solid

independent flow sheet test work on the planned process for

scandium recovery. The Feasibility Study consolidates a significant

amount of metallurgical test work and prior study on the Nyngan

Scandium Project, including important test work results completed

since the PEA was generated in 2014. The entire body of work

demonstrates a viable, conventional process flow sheet utilizing a

continuous-system HPAL leaching process, and good metallurgical

recoveries of scandium from the resource. The metallurgical

assumptions are supported by various bench and pilot scale

independent test work programs that are consistent with known

outcomes in other laterite resources. A number of the key elements

of this flowsheet work have been protected by the Company under US

Patent Applications. The continuous autoclave configuration, as

opposed to batch systems explored in previous flow sheets, is also

a more conventional and current design choice.

The

level of accuracy established in the Feasibility Study

substantially reduces the uncertainty levels inherent in earlier

studies, specifically the PEA. The greater confidence intervals

around the Feasibility Study were achieved by reliance on

significant project engineering work, a capital and operating cost

estimate supported by detailed requirements and vendor pricing,

plus one conditional offtake agreement and an independent marketing

assessment, both supportive of the marketing assumptions for the

business.

The

Feasibility Study delivered a positive result on the Nyngan

Scandium Project, and recommends the Nyngan Scandium Project owners

seek finance and proceed to construction. Recommendations were made

therein for additional immediate work, notably to win additional

offtake agreements with customers, complete some optimizing flow

sheet studies, and to initiate as early as possible detailed

engineering required on certain long-lead capital items. The

Company intends to act on these recommendations as financing

permits.

Confirmatory Metallurgical Test Results

On June

29, 2016, we announced the results of a confirmatory metallurgical

test work report from Altrius Engineering Services (AES) of

Brisbane, Australia. The test work results directly relate to the

list of recommended programs included in the Feasibility Study. AES

devised and supervised these test work programs at the SGS

laboratory in Perth, Australia and at the Nagrom laboratory in

Brisbane, Australia.

The

project DFS recommended a number of process flowsheet test work

programs be investigated prior to commencing detailed engineering

and construction. Those study areas included pressure leach

(“HPAL”), counter-current decant circuits

(“CCD”), solvent extraction (“SX”), and

oxalate precipitation, with specific work steps suggested in each

area. This latest test work program addresses all of these

recommended areas, and the results confirm recoveries and

efficiencies that either meet or exceed the parameters used in the

DFS. Highlights of the testing are:

●

Pressure leach test

work achieved 88% recoveries, from larger volume

tests,

●

Settling

characteristics of leach discharge slurry show substantial

improvement,

●

Residue

neutralization work meets or exceeds all environmental requirements

as presented in the DFS and the environmental impact

statement,

●

Solvent extraction

circuit optimization tests generated improved performance,

exceeding 99% recovery in single pass systems, and

●

Product finish

circuits produced 99.8% scandium oxide, completing the recovery

process from Nyngan ore to finished scandia product.

Engineering, Procurement and Construction Management

Contract

On May

30, 2017, the Company announced that its subsidiary EMC Australia

signed an Engineering, Procurement and Construction Management

("EPCM") contract with Lycopodium Minerals Pty Ltd ("Lycopodium"),

to build the Nyngan Scandium Project in New South Wales, Australia.

The EPCM contract also provides for start-up and commissioning

services.

The

EPCM contract appoints Lycopodium (Brisbane, QLD, Australia) to

manage all aspects of project construction. Lycopodium is the

principal engineering firm involved with the DFS. Lycopodium's

continued involvement in project construction and commissioning

ensures valuable technical and management continuity for the

project during the construction and start-up of the

project.

On

October 19, 2017, we announced that Lycopodium has been instructed

to initiate critical path engineering for the Nyngan Scandium

Project. Lycopodium commenced work on select critical path

components for the project, including design and specification

engineering on the high-pressure autoclave unit, associated flash

and splash vessels and several specialized high-pressure input

pumps. The engineering work was completed in 2018 and will enable

final supplier selection, firm component pricing and delivery dates

for these key process components.

15

Environmental Permitting/Development Consent/Mining

Lease

On May

2, 2016, the Company announced the filing of an Environmental

Impact Statement (“EIS”) with the New South Wales,

Australia, Department of Planning and Environment, (the

“Department”) in support of the planned development of

the Nyngan Scandium Project. The EIS was prepared by R.W. Corkery

& Co. Pty. Limited, on behalf of the Company’s 80% owned

subsidiary, EMC Australia, to support an application for

Development Consent for the Nyngan Scandium Project. The EIS is a

complete document, including a Specialist Consultants Study

Compendium, and was submitted to the Department on April 29,

2016.

EIS

Highlights:

●

The EIS finds

residual environmental impacts represent negligible

risk.

●

The proposed

development design achieves sustainable environmental

outcomes.

●

The EIS finds

net-positive social and economic outcomes for the

community.

●

Nine independent

environmental consulting groups conducted analysis over five years,

and contributed report findings to the EIS.

●

The Nyngan project

development is estimated to contribute A$12.4M to the local and

regional economies, and A$39M to the State and Federal economies,

annually

●

The EIS is fully

aligned with the DFS and with a NSW Mining License Application for

the Nyngan project.

Conclusion

statement in the EIS:

“In

light of the conclusions included throughout this Environmental Impact Statement, it is

assessed that the Proposal could be constructed and operated in a

manner that would satisfy all relevant statutory goals and

criteria, environmental objectives and reasonable community

expectations.”

EIS

Discussion:

The EIS

is the foundation document submitted by a developer intending to

build a mine facility in Australia. The Nyngan Scandium Project is

considered a State Significant Project, in that capital cost

exceeds A$30million, which means State agencies are designated to

manage the investigation and approval process for granting a

Development Consent, from the Minister of Planning and Environment.

This Department will manage the review of the Proposal through a

number of State and local governmental agencies.

The EIS

is a self-contained set of documents used to seek a Development

Consent. It is however, supported in many ways by the recently

completed DFS.

On

November 10, 2016, the Company announced that the Development

Consent had been granted. This Development Consent represents an

approval to develop the Nyngan Scandium Project and is based on the

EIS. The Development Consent follows an in-depth review of the EIS,

the project plan, community impact studies, public EIS exhibition

and commentary, and economic viability, and involved more than 12

specialized governmental agencies and groups.

Mining

Lease:

During

July 2019, EMC Australia received notice of approval for its Mining

Lease application. The Mining Lease (“ML 1792”)

overlays select areas previously covered by Exploration Licenses.

The ML represents the final major development approval required

from the NSW Government to begin construction on the

project. The ML 1792

grant is issued for a period of 21 years and is based on the

development plans and intent submitted in the ML Application. The

ML can be modified by NSW regulatory agencies, as requested by EMC

Australia over time, to reflect changing operating

conditions.

16

In

addition to these two key governmental approvals, other required

licenses and permits must be acquired but are considered routine

and require only compliance with fixed standards and objective

measurements. These remaining approvals include submittal of

numerous plans and reports supporting compliance with Development

Consent and Mining Lease. In addition, the following water, roads,

dam and electrical access reviews and arrangements must be

finalized:

●

Water Supply Works

and Use Approval and Water Access License,

●

State and local

approval for construction of the intersection of the Site Access

Road and Gilgai Road,

●

An approval from

the NSW Dams Safety Committee for the design and construction of

the Residue Storage Facility, and

●

A high voltage

connection agreement with Essential Energy.

The ML

1792 grant covers 810 acres (370

hectares) of surface area fully owned by the Company, an

area adequate to construct and operate a scandium mine of a scale

outlined in the definitive feasibility study. The Company had

originally filed a mining lease application (MLA 531) covering an

area of 874 hectares, providing for significant project expansion

capacity. However, due to an objection by a landowner who holds

freehold surface ownership over a portion of the 874 hectare area,

the original MLA 531 remains in review by the New South Wales

Department of Planning and Environment. The landowner objection

claims the property is “Agricultural Land”, with

meaning as defined in the relevant law.

The NSW

Department of Planning and Environment has recently sought and

received independent consultant input that the landowner objection

should qualify as “Agricultural Land”, as defined in

the relevant law. The Company has rights of comment on that

finding, which have been exercised, in a formal comment package

delivered to the Department on February 1, 2019. With receipt and

consideration of comment documents from the parties, and further

Department input, the Department Secretary will make a

determination on the validity of the affected portion of the MLA

531.

If the

Department Secretary’s decision upholds the landowner

objection, the Company believes that outcome will not delay or

prevent the development of the Nyngan Scandium Project., as is

generally characterized in the 2016 feasibility study.

As of

the date of this Form 10-K, the Department Secretary has not made a

decision on the validity of the landowner objection. In January

2020, the Company made a formal request to the Deputy Premier and

Minister for NSW Industry and Trade, urging for action and a final

decision in this matter, accompanied by a review of the facts,

status and Company position on the matter.

Patent Application Filings

The

Company is in the process of establishing a significant portfolio

of intellectual property through the filing of scandium related

patents both in the US and abroad.

To

date, the following five US patents have been granted to the

Company:

|

10450634

|

Scandium-Containing

Master Alloys And Method For Making The Same

|

|

10378085

|

Recovery

Of Scandium Values Through Selective Precipitation Of Hematite And

Basic Iron Sulfates From Acid Leachates

|

|

10260127

|

Method

For Recovering Scandium Values From Leach Solutions

|

|

9982326

|

Solvent

Extraction Of Scandium From Leach Solutions

|

|

9982325

|

Systems

And Methodologies For Direct Acid Leaching Of Scandium-Bearing

Ores

|

Below

is a list of ten US patents that haven filed, but have not been

granted yet:

|

US20200001407

|

Control Of Recrystallization In Cold-Rolled AlMn(Mg)ScZr Sheets For

Brazing Applications

|

|

US20190161827

|

Extraction Of Scandium Values From Copper Leach

Solutions

|

|

US20160289795

|

Systems and Processes for Recovering Scandium Values From Laterite

Ores

|

|

US20190218645

|

Direct Scandium Alloying

|

|

US20190218644

|

Scandium Master Alloy Production

|

|

US20120305452

|

Dry, Stackable Tailings and Methods for Producing the

Same

|

|

US20110298270

|

In Situ Ore Leaching Using Freeze Barriers

|

|

Provisional

|

Title not publicly disclosed.

|

|

Provisional

|

Title not publicly disclosed.

|

|

Provisional

|

Title

not publicly disclosed.

|

17

Patent Applications Discussion:

●

These patents and

patent applications cover novel, unique flowsheet designs,

applicable to scandium extraction, from scandiferous

resources;

●

The patented

designs are largely supported by test work done with Nyngan

Scandium Project resource material and known design

parameters;

●

The patents cover

HPAL system material flows, solvent extraction (SX), ion exchange

systems (“IX”), atmospheric tank and heap leaching

systems and techniques, and processes for directly making select

master alloys containing scandium; and

●

Most of the designs

are incorporated as part of the DFS.

●

Recovery by-product

scandium from certain mineral resources is also

covered.

These

patent applications, filed with the US Patent Office, protect the

Company’s position and rights to the intellectual property

(IP) contained and identified in the applications as of the date

filed, within the worldwide jurisdiction limits of the US patent

system. Review by the US Patent Office will take further time, but

the dates of filing these patents define the basis of IP ownership

claims, as is generally afforded U.S. patentholders.

The

Company intends to utilize the IP contained in these process

patents in the development of process flowsheets for recovery of

scandium from its Nyngan Scandium Project, as well as its

Honeybugle project, and potentially from future by-product

opportunities.

The

Company believes that patent protection of these specific, novel

process designs will be granted. Many of the basic design elements

contemplated in the Nyngan Scandium Project flowsheet are commonly

applied to other specialty metals, particularly nickel. However,

the application of these basic design elements has not been

commonly applied to scandium extraction from laterite resources,

and there are enough intended and required operational differences

in the application to permit the Company to patent-protect IP on

those differences.

These

patent claims are the result of several years of metallurgical test

work with independent resource laboratories and specific design

work by Willem Duyvesteyn, the Company’s Chief Technology

Officer. This work is ongoing. Patent protection on flowsheet

intellectual property will serve to limit or prevent the

unauthorized use of that IP by others without the Company’s

consent. We believe these filings are an important action to

protect the ownership of a Company asset, on behalf of all SCY

shareholders.

Downstream Scandium Products

In

February 2011 we announced results of a series of laboratory-scale

tests investigating the production of aluminum-scandium master

alloys directly from aluminum oxide and scandium oxide feed

materials. The overall objective of this research was to

demonstrate and commercialize the production of aluminum-scandium

master alloy using impure scandium oxide as the scandium source,

potentially significantly improving the economics of

aluminum-scandium master alloy production. In 2014, the Company

announced it applied for a US patent on master alloy production,

which is still in the application phase.

During

the 2015-2017 timeframe, we continued our own internal

laboratory-scale investigations into the production of

aluminum-scandium master alloys, furthering our understanding of

commercial processes, and achievable recoveries. We advanced our

abilities to make a standard-grade 2% scandium master alloy product

typical of commercially available products offered

today.

On

March 2, 2017, we announced the signing of a Memorandum of

Understanding ("MOU") with Weston Aluminium Pty Ltd. ("Weston") of

Chatswood, NSW, Australia. The MOU defines a cooperative commercial

alliance to jointly develop the capability to manufacture

aluminum-scandium master alloy. The intended outcome of this

alliance will be to develop the capability to offer Nyngan Scandium

Project aluminum alloy customers scandium in form of Al-Sc master

alloy, should customers prefer that product form.

The MOU

outlines steps to jointly establish the manufacturing parameters,

metallurgical processes, and capital requirements to convert Nyngan

Scandium Project scandium product into Master Alloy, on Weston's

existing production site in NSW. The MOU does not include a binding

contract with commercial terms at this stage, although the intent

is to pursue the necessary technical elements to arrive at a

commercial contract for conversion of scandium oxide to master

alloy, and to do so prior to first mine production from the Nyngan

Scandium Project.

18

On

March 5, 2018, the Company announced that it had initiated a small

scale pilot program (4kg scale) at the Alcereco Inc. metallurgical

research facilities in Kingston, Ontario, to confirm and refine

previous lab-scale work on the manufacture of aluminum-scandium 2%

master alloy (MA). The program advanced the process understanding

for commercial scale upgrade of Nyngan scandium oxide product to

master alloy product.

The

2018 pilot program consisted of 5 separate trials on two MA product

types, production of MA in various forms, and dross analysis to

ascertain scandium recoveries to product. The mass of master alloy

and product variants produced in the program totaled approximately

20kg and was completed in December of 2018. The results of the

program included the successful production of 2% grade MA, with

recoveries of scandium to product of 85%.

A

second phase of the small-scale pilot program was initiated in the

first half of 2019, again at 4kg scale, building on the work done

in phase I. The results of this second program included successful

production of 2% grade MA, with improvements in form of rapid

kinetics, and recoveries of scandium to product of

+90%.

On

March 5, 2018, the Company also announced that it filed for patent

protection on certain process refinements for master alloy

manufacture that it believes are novel methods, and also on certain

product variants that it believes represent novel forms of

introducing scandium more directly into aluminum

alloys.

Focus on Aluminum Alloy Applications for Scandium

Products

The

Company is in the process of obtaining sales agreements for

scandium products produced from our Nyngan Scandium Project. Our

focus is on the use of scandium as an alloying ingredient in

aluminum-based products. The specific scandium product forms we

intend to sell from the Nyngan project include both scandium oxide

(Sc2O3) and

aluminum-scandium master alloys (Al-Sc 2%).

Scandium

as an alloying agent in aluminum allows for aluminum metal products

that are much stronger, more easily weldable and exhibit improved

performance at higher temperatures than current aluminum-based

materials. This also means lighter structures, lower manufacturing

costs and improved performance in areas that aluminum alloys do not

currently compete.

Aluminum Alloy Research Partner – Alcereco

In

2015, the Company entered into a memorandum of understanding

(“MOU”) with Alcereco Inc. of Kingston, Ontario

(“Alcereco”), forming a strategic alliance to develop

markets and applications for aluminum alloys containing scandium.

To further that alliance, and to reinforce the capability of both

companies to deliver product developed for scandium aluminum alloy

markets, Scandium International and Alcereco also signed an offtake

agreement governing sales terms of scandium oxide product produced

from the Nyngan Scandium Project. The offtake agreement specifies

prices, delivery volumes and timeframes for commencement of

delivery of scandium oxide product. The offtake agreement does not

provide for a mandatory annual minimum purchase volume of scandium

oxide by Alcereco, and there is no requirement for payment in lieu

of purchase.

The MOU

represented keen mutual interest in foundry-based test work on

aluminum alloys containing scandium, based on understandings that

Alcereco’s team had gained from prior work with Alcan

Aluminum, and based on SCY’s twin goals of understanding and

identifying quality applications for scandium, and also

understanding the scandium value proposition for

customers.

During

December 2017, the Company revised and renewed the scandium product

offtake agreement with Alcereco. The revised agreement extends the

deadline for initial production and shipments from the Nyngan

Scandium Project from December 1, 2017, to as late as December 1,

2020. The defined sale product was changed to an aluminum scandium

2% master alloy from scandium oxide in the prior agreement. The

revised sales agreement covers approximately the same scandium

oxide volume as the prior agreement, representing 55% of

Nyngan’s initial twelve month forecast production, and

approximately 20% of nameplate capacity, as established by the

Definitive Feasibility Study. The revised offtake agreement does

not provide for a mandatory annual minimum purchase volume of

scandium oxide by Alcereco, and there is no requirement for payment

in lieu of purchase.

The

Company has sponsored research work as contemplated by the MOU with

Alcereco and with multiple other unrelated entities in separate

locations. This work develops and documents the improvement in

strength characteristics scandium can deliver to aluminum alloys

without degrading other key properties. The team has run multiple

alloy mix programs where scandium loading is varied, in order to

look at response to scandium additions on a cost/benefit basis.

This work has been done in the context of industries and

applications where these particular alloys are popular

today.

19

These

programs are focused on 1000 series, 3000 Series, 5000 Series and

7000 Series Al-Sc alloys, and have served to make independent data

and volume samples available for sales efforts.

The

results of our research work are positive, and consistent with the

body of published literature available today on aluminum scandium

alloys. We are observing noteworthy strengthening effects with

scandium additions above 0.1%, and dramatic strengthening

improvements with additions of 0.35%, while preserving or enhancing

other alloy properties and characteristics. We have also

demonstrated that altering the combinations of scandium loads and

alloy hardening process techniques has significant effect on the

final alloy properties, offering the opportunity to tune alloy

characteristics to suit specific applications. These findings are considered

commercially sensitive, and the data is not intended for public

disclosure at this time, although the findings and data are being

shared with select potential customers under specific

non-disclosure agreement protections, as is deemed relevant to

their specific areas of commercial interest.

Letters of Intent with Potential Customers

During

2018 and 2019, the Company announced that it entered into letter of

intent (“LOI”) agreements with nine unrelated

partnering entities. In each LOI, we have agreed to contribute

scandium samples, either in form of scandium master alloy product,

or aluminum-scandium alloy product, for trial testing by the

partners in their downstream manufacturing applications. Each of

the parties to the LOI agreements have agreed to report the

parameters and general results of the testing program utilizing

these scandium-containing alloys, upon completion of testing. The

Company plans to continue this LOI program of introducing scandium

for trial testing by partners through agreements with more

potential customers in 2020.

These

formal LOI agreements, with distinct industry segment leaders,

represent a key marketing program demonstrating precisely how

scandium will perform in specific products, and in

production-specific environments. Potential scandium customers

insist on these sample testing opportunities, directly in their

research facilities or on their shop floor, to ensure their full

understanding of the impacts, benefits, and costing implications of

introducing scandium into their traditional aluminum

feedstocks.

The

partnering entities in these LOI agreements are set out

below:

Austal

Ltd. (“Austal”), headquartered in Henderson, Western

Australia, (Australia). Austal is a public corporation, listed on

the Australian Stock Exchange (ASB.ASX), with shipbuilding

facilities in Perth, Australia, Mobile, Alabama (USA), Vung Tau,

Vietnam and Balamban, Cebu (Philippines). The company maintains a

focus on research and development of emerging maritime technologies

and cutting-edge ship designs, and is a recognized world leader in

the design and construction of large aluminum commercial and

defense vessels.

Impression

Technologies Ltd. (“ITL”), based in Coventry, UK. ITL