Attached files

| file | filename |

|---|---|

| EX-32 - EXHIBIT 32 - WESTERN CAPITAL RESOURCES, INC. | g081935_ex32.htm |

| EX-31.2 - EXHIBIT 31.2 - WESTERN CAPITAL RESOURCES, INC. | g081935_ex31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - WESTERN CAPITAL RESOURCES, INC. | g081935_ex31-1.htm |

| EX-21.1 - EXHIBIT 21.1 - WESTERN CAPITAL RESOURCES, INC. | g081935_ex21-1.htm |

| EX-14 - EXHIBIT 14 - WESTERN CAPITAL RESOURCES, INC. | g081935_ex14.htm |

| EX-10.4 - EXHIBIT 10.4 - WESTERN CAPITAL RESOURCES, INC. | g081935_ex10-4.htm |

| EX-4.1 - EXHIBIT 4.1 - WESTERN CAPITAL RESOURCES, INC. | g081935_ex4-1.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

☒

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended

December 31, 2019

or

☐

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from

_______________________ to ___________________

Commission File Number 000-52015

WESTERN CAPITAL RESOURCES, INC.

(Exact name of registrant as specified in its charter)

|

Delaware |

47-0848102 |

|

(State of incorporation) |

(I.R.S. Employer Identification No.) |

|

|

|

|

11550 “I” Street, Suite 150 Omaha, Nebraska |

68137 |

|

(Address of principal executive offices) |

(Zip Code) |

Registrant’s telephone number, including area code: (402) 551-8888

Securities registered pursuant to Section 12(b) of the Act: |

|||||

Title of Each Class |

Trading Symbol(s) |

|

Name of Each Exchange on which Registered |

||

None |

N/A |

|

N/A |

||

Securities registered pursuant to Section 12(g) of the Act: Common Stock, par value $0.0001 per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐ Yes ☒ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to the filing requirements for the past 90 days ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of “accelerated filer,” large accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ Accelerated filer ☐ Non-accelerated filer ☒ Smaller reporting company ☒ Emerging Growth Company ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ☐ Yes ☒ No

The aggregate market value of the voting stock held by persons other than officers, directors and more than 5% shareholders of the registrant as of June 30, 2019 was approximately $11,057,000 based on the closing sales price of $3.75 per share as reported on the OTCQB. As of March 30, 2020, there were 9,265,778 shares of our common stock, $0.0001 par value per share, outstanding.

DOCUMENTS INCORPORATED IN PART BY REFERENCE

None.

Western Capital Resources, Inc.

Form 10-K

Table of Contents

OVERVIEW

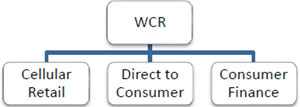

Western Capital Resources, Inc. (“WCR” or “Western Capital”), a Delaware corporation originally incorporated in Minnesota in 2001 and reincorporated in Delaware in 2016, is a holding company having a controlling interest in subsidiaries operating in the following industries and operating segments:

Our “Cellular Retail” segment is comprised of an authorized Cricket Wireless dealer and involves the retail sale of cellular phones and accessories to consumers through our wholly owned subsidiary PQH Wireless, Inc. and its controlled but less than 100% owned subsidiaries. Our “Direct to Consumer” segment consists of a wholly owned online and direct marketing distribution retailer of live plants, seeds, holiday gifts and garden accessories selling its products under Park Seed, Jackson & Perkins and Wayside Gardens brand names and home improvement and restoration products operating as Van Dyke’s Restorers as well as a wholesaler under the Park Wholesale brand. Our “Consumer Finance” segment consists of retail financial services conducted through our wholly owned subsidiaries Wyoming Financial Lenders, Inc. and Express Pawn, Inc. Our investment holdings are included with WCR. Throughout this report, we collectively refer to WCR and its consolidated subsidiaries as “we,” the “Company,” and “us.”

RECENT EVENTS

Cellular Retail Segment

During 2019 we made many strategic changes to our portfolio of Wireless Retail locations. We completed three joint venture transactions with other Cricket Wireless authorized retailers acquiring a total of 61 locations, sold 43 locations to other authorized retailers and purchased, launched or closed several others. In total in 2019, we added 69 locations and sold or closed 52 locations, ending the year operating 222 locations compared to 205 in operation at the beginning of the year.

Consumer Finance Segment

The payday lending industry continues to suffer from the perception and widespread belief that payday lenders are by their nature, predatory lenders. Consumer advocacy groups in many states are activity seeking state law changes which would effectively end the viability of a payday loan business, including Nebraska where we generate approximately 30% of our payday lending revenue or approximately 2% of our consolidated revenue. If these groups are successful in Nebraska, we will likely cease payday lending activities in Nebraska.

Release of Escrow Funds

In October 2019, we received $3,367,940, the scheduled release of the remaining 50% of the funds held in escrow relating to the 2017 sale of our Franchise segment, together with interest earned.

Common Stock Repurchases

During 2019, the Company repurchased 122,899 shares of its common Stock. Repurchases were made in the open market and through privately negotiated transactions.

Acquisitions

We are actively searching for acquisition opportunities. We are industry agnostic and target leaders in niche industries or geographies as well as opportunistic purchases of businesses that we believe we can improve operationally. We have a particular interest in companies facing succession dilemmas, corporate divestitures and businesses in out-of-favor industries. In addition, we seek to grow our subsidiaries through add-on acquisitions in the e-commerce, cellular retail and consumer finance segments. Our overall strategy continues to focus on building a diversified portfolio of strong cash flow generating businesses. Our financial strength, long-term view and operating expertise allow subsidiary companies to focus on growing and maximizing return on investment. We expect to be patient and move upon what we believe to be the right investment opportunities.

1

CELLULAR RETAIL SEGMENT

General Description

We operate cellular retail stores as an authorized Cricket Wireless retailer, selling cellular phones and accessories, activating Cricket Wireless customers on the Cricket network, providing ancillary services and accepting service payments from Cricket customers. As an authorized Cricket Wireless dealer, we are only permitted to sell the Cricket line of no-contract cellular phones and service at our Cricket retail stores.

We generate revenue in this business through retail sales of cellular phones, receipt of back-end compensation from Cricket, sales of phone accessories (e.g., cases, car chargers and bluetooth speakers), fees charged when a customer changes services (service activations and reactivations, adding lines, phone number changes, etc.), or whenever a customer whom we activated on the Cricket network pays his or her no-contract cellular bill.

A summary table of the number of cellular retail stores we operated during the periods ended December 31, 2019 and 2018 follows:

|

|

|

2019 |

|

|

2018 |

|

||

|

Beginning |

|

|

205 |

|

|

|

278 |

|

|

Acquired / Launched / Managed |

|

|

69 |

|

|

|

2 |

|

|

Closed |

|

|

(52 |

) |

|

|

(75 |

) |

|

Ending |

|

|

222 |

|

|

|

205 |

|

Market Information and Marketing

Cricket Wireless service offers customers simple, no-contract, predictable and affordable nationwide flat rate wireless plans. Cricket Wireless customers have the added advantage of unlimited minutes, text and data access on the AT&T network.

No-contract cellular products and services were historically targeted primarily only to market segments that were underserved by traditional communications companies requiring credit approval, a contractual commitment from the subscriber for a period of at least one year, and often included overage charges for minute and data usage in excess of a specified limit. We believe that a large portion of the U.S. cellular market consists of customers who are price-sensitive and prefer not to enter into these fixed-term contracts. We believe that the Cricket Wireless cellular retail product and service offerings we offer appeal strongly to both the underserved markets and the greater U.S. cellular market and believe we are positioned to benefit as a Cricket Wireless dealer.

Market Strategy

We believe that our business model is scalable and we can apply our operational protocols and administrative office functions to continue expanding our cellular retail business. We will continue to evaluate strategic and opportunistic acquisitions of existing Cricket dealerships and will actively close, dispose or consolidate locations that do not meet our operating criteria in order to streamline operations.

Products and Services

Our authorized Cricket retail stores offer the following products and services:

|

|

● |

Cricket Wireless service plans, each designed to attract customers by offering simple, predictable and affordable talk, text and high-speed data services that are a competitive alternative to traditional wireless and wireline services (e.g., flat-rate and unlimited talk/text plans, without fixed-term contracts, early termination fees or credit checks); |

|

|

● |

Cricket Wireless plan upgrades, such as Cricket International, individual country add-ons, Deezer (an independent music service on a no-contract basis), Cricket Protect and mobile hotspots; and |

2

|

|

● |

Cricket handsets and accessories. |

When purchasing a phone, our customers have options among the latest in Apple, Samsung and other Android-based and Windows OS-based smartphones. Because there is no contract for the monthly service, customer phone purchases are paid in full at the time of purchase.

Seasonality

Our Cellular Retail segment operations are influenced by seasonal effects related to traditional retail selling periods and other factors affecting our customer base. In particular, we generally expect sales activity to be highest in the first and fourth quarters. Nevertheless, our revenues can be strongly affected by the launch of new markets, new or improved products such as release of the latest smartphone edition, promotional activity, the timing of federal tax-refunds and the actions of our competitors, any of which have the ability to offset or exacerbate the seasonality we normally experience.

Competition

There is substantial and ever-increasing competition in the wireless phone industry where customers can choose between many other postpaid and no-contract resellers, including AT&T, Verizon, Sprint/Boost Mobile, T-Mobile/Metro PCS and a larger number of regional providers. We compete for customers based principally on Cricket’s service/device offerings, price, call quality and coverage area.

Competition for the no-contract customers is primarily among MetroPCS, Virgin Mobile and Boost Mobile, but also includes the traditional postpaid carriers that have introduced no-contract products. There is also competition with other no-contract phone service providers such as Straight Talk by Wal-Mart or Wal-Mart’s Family Mobile powered by T-Mobile, an increase of national retailers offering similar or identical products and services that we provide, such as Cricket phones sold at Game Stop and Wal-Mart, and an increase in mobile virtual network operator (“MVNO”) offerings.

Our Cricket store business also competes with other current or potential authorized Cricket Wireless dealers and direct-to-consumer sales through the Cricket Wireless website. The authorization to sell Cricket products and services is granted by Cricket Wireless, LLC, a wholly owned subsidiary of AT&T. Our ability to compete with other sellers of Cricket products and services will depend on the success with which we operate our stores and the attractiveness of their locations.

DIRECT TO CONSUMER SEGMENT

General Description

Our direct to consumer segment is a direct marketer of roses, plants, seeds, holiday gifts and home restoration products. The business is composed of: 1) a multi-channel retailer of garden and living gift products; 2) a wholesale seed business; and 3) a multi-channel retailer of home hardware and restoration products. Our garden products brands are highly recognizable in the rose and garden space as both the Jackson & Perkins and Park Seed brands were founded more than 149 years ago.

Products and Services

Our direct to consumer segment sells product through catalogs and online under the following brands:

● Jackson & Perkins, approximately 150 years of history and is the most recognized brand of premium garden roses. Jackson and Perkins is one of the largest direct to consumer retailers of bare root roses in the United States, selling over 150 active varieties of bare root roses, of which 87 varieties are patented by Jackson and Perkins. In addition to bare root roses, we sell perennials, flower bulbs, outdoor living products as well as living holiday gifts plants. Holiday gifts include fresh evergreen wreathes, live decorative Christmas trees and holiday amaryllis.

● Park Seed, over 150 years in the business and one of America’s oldest and largest direct to consumer seed retailers. As a leader within the direct to consumer seed business, Park Seed sells over 2,500 premium vegetable and flower seed varieties, as well as various gardening supplies. The wholesale seed business sells seeds, plants and other horticultural products in larger quantities to small-medium sized growers, nurseries and garden centers. Plants and seeds sales are concentrated during the spring months.

● Wayside Gardens, sells unique, hard to find high-end flowers, plants and gardening supplies to the master gardener. The Wayside Gardens customer is extremely selective, very knowledgeable, and seeks high quality plants. Approximately 60% of sales occur in the three months from March to May, during the spring planting season.

3

● Van Dyke’s, an online and catalog retailer with a vast assortment of vintage home restoration wood products, hardware and antique furniture, many of which are hard to find. Van Dyke’s focus is on hardware, decorative wood, home accents, knobs and pulls and kitchen, bath and other décor.

Seasonality

Demand for live goods and holiday products is cyclical in nature, sensitive to seasonal growing patterns, general weather conditions, holiday sales patterns and competitive influences. As such, the direct to consumer segment’s results of

operations, financial condition and cash flows could fluctuate significantly from period to period. The majority of segment revenue is derived in three selling periods, spring, fall, and the December holiday season, while the summer season accounts for a small portion of sales.

Market Strategy

As a direct to consumer retailer, we focus our marketing spending on mail order catalogs, internet advertising, and traditional advertising mediums (i.e., public relations, magazines, social media, etc.). We are focused on niche markets and direct our advertising to repeat and new customers through internet marketing strategies.

Competition

In the retail garden business, within the bare root rose category, we compete against brick and mortar garden centers and nurseries (approximately 10,000 across the United States), as well as other online and mail-order retailers, including David Austin Roses and Regan Nursery. Across other plant categories, we compete against Gardens Alive and their portfolio of brands, and other competitors. Our biggest competitive advantages are our recognizable Jackson & Perkins brand name proprietary patented rose varieties and exclusive garden seed products. The most direct competitor for Wayside Gardens is White Flower Farms, which also focuses on high-end, premium plants.

Within the holiday gift segment, we compete against larger competitors including Harry and David and 1-800 Flowers, among others. Within the seed business, our primary competitor is Burpee which, in addition to having an online presence, supplies lower-end seed products to mass market retailers, including Wal-Mart.

Our Van Dyke’s Restorers brand competes primarily with other online retailers since brick and mortar stores cannot afford to carry Van Dyke’s breadth of SKUs. Our competitors are Signature Hardware, House of Antique Hardware, and Rejuvenation Hardware (part of Williams Sonoma). The above-mentioned competitors compete primarily in the hardware, lighting and kitchen and bath categories. The decorative wood portion of the Van Dyke’s business is in a very fragmented industry niche and there are no big decorative wood competitors. Van Dyke’s competes primarily through the breadth of its product variety as well as through its established brand name and customer list.

CONSUMER FINANCE SEGMENT

General Description

The majority of short-term consumer loans we provide are commonly referred to as “payday loans” or “cash advance” loans. Such loans are referred to as “payday loans” because they are typically made to borrowers who have no available cash and promise to repay the loan out of their next paycheck. We also provide short-term installment and pawn loans as part of this operating segment.

We provide short-term consumer loans in amounts that typically range from $100 to $500 with the average loan amount, including fee, being approximately $432. Cash advance loans provide customers with cash in exchange for a promissory note with a maturity of generally two to four weeks and the customer’s post-dated personal check for the aggregate amount of the cash advance, plus a fee. The fee varies from state to state based on applicable regulations, and generally ranges from $15 to $22 for each whole or partial increment of $100 borrowed. To repay the cash advance loan, a customer may pay with cash, in which case their personal check is returned to them, or allow the check to be presented to the bank for collection. Approximately 91% and 89% of our lending revenue (comprised of payday loan fees and installment and pawn loan interest and fees) in the Consumer Finance segment was derived from payday lending in 2019 and 2018, respectively. Payday lending revenue made up approximately 76% and 74% of our total revenue (comprised of lending revenue, check cashing fees, pawn fees and miscellaneous other revenue) in the Consumer Finance segment in 2019 and 2018, respectively.

4

We currently offer short-term installment loans only in Wisconsin but also offered short-term installment loans in Colorado until February 2019. Approximately 3% and 6% of our total revenue in the Consumer Finance segment was derived from installment lending in 2019 and 2018, respectively. We provide our installment loan customers with cash in exchange for a promissory note with a maturity of generally six months. The fee and interest rate on installment loans vary based on applicable regulations. Like cash advance or payday loans, installment loans are unsecured.

We operate three pawn stores in our Consumer Finance segment. Our pawn stores provide collateralized non-recourse loans, commonly known as “pawn loans” with maturities of one to four months. Allowable service charges vary by state and loan size. The loan amount varies depending on our valuation of each item pawned. We generally lend from 30% to 55% of our estimate of the collateral’s resale value. Customers have the option to redeem the pawned merchandise during the term or at maturity, or else forfeit the merchandise to us on maturity. At our pawn stores we sell merchandise that was acquired through either customer forfeiture of pawn collateral, second-hand merchandise purchased from customers or consigned to us, or new merchandise purchased from vendors. Pawn store revenues made up approximately 17% of our total revenue in the Consumer Finance segment in 2019 and 2018.

All of our Consumer Finance lending activities and other services are subject to state regulations (which vary from state to state), federal regulations and local regulations, where applicable.

As part of each payday and installment loan transaction, we enter into a standardized written promissory note with the borrowing customer and obtain proof of income and identity, a personal post-dated check for the principal loan amount plus a specified fee if a payday loan, and other documentation. Our standardized contracts vary based on state laws, but all of our contracts plainly state in simple terms the annual percentage rate (assuming the fees we charge are computed as interest) in compliance with Regulation Z, the borrower’s right to rescind the transaction, a dispute-resolution clause, a notice of financial privacy rights, an affirmative representation about whether the borrower is a member of the U.S. military, and the consequences of defaulting on the loan. We retain copies of our written contracts and provide a signed copy to our customers.

In general, our lending process and standards are extraordinarily different from those used by banks. To our knowledge, banks typically order and carefully review credit reports on all loans, engage in extensive underwriting analysis, and will typically make independent verification of earnings history through phone calls, reviews of tax returns and other processes. As a result, we generally experience a higher default rate on our personal loans than banks do on their personal loans (see caption below, “Risks Associated with Our Loans—Default and Collection”). At December 31, 2019, we had an aggregate (of all loan types) of approximately:

|

|

● |

$3.70 million in current outstanding loan principal, fees and interest due to us; and |

|

|

● |

$0.83 million of late loans (customers’ repayment checks deposited and returned as NSF within the last 180 days or installment loan balances not past the final installment due date with one or more payments delinquent). |

A summary table of the number of Consumer Finance locations operated during the periods ended December 31, 2019 and 2018 follows:

| 2019 | 2018 | |||||||

| Beginning | 41 | 41 | ||||||

| Acquired / Launched | — | — | ||||||

| Closed | (2 | ) | — | |||||

| Ending | 39 | 41 | ||||||

The Fees We Charge

The fee we charge for a payday loan varies from state to state, based on applicable regulations, and generally ranges from $15 to $22 for each whole or partial increment of $100 borrowed. We do not charge interest in connection with our payday loans but do charge interest and fees where allowable on our short-term installment loans made in Wisconsin. If, however, we calculate the loan fees we charge as an annual percentage rate of interest (“APR”), such rate would range from 177% for a 31-day loan transacted in Kansas (on the low end) to approximately 536% for a 14-day loan in Wyoming (on the high end), with the actual average loan amount and average actual loan fees we charge involving an imputed annual percentage rate of approximately 439% and 198% for a 14-day and 31-day loan, respectively. The term of a loan significantly affects the imputed APR of the fees we charge for our loans. For instance, when a $15 fee is charged for a two-week loan of $100, the resulting APR is 391%. When the same fee on $100 is charged for a four-week loan, the resulting APR is 195%. Currently, we do not charge the maximum fee permitted in all of the states where we operate. We do, however, charge a uniform fee for all transactions processed in any particular state that involve the same range of payday loan amounts and the same term.

5

Of the six states in which we presently operate, only one state (Wisconsin) does not limit the loan fees we may charge or the term (i.e., the length) of the loan we may offer our customers.

In Wisconsin, we generally offer short-term installment loans in amounts from $300 to $750 payable in six equal monthly payments. Wisconsin installment loans are payable over four to six months at an annual percentage rate of approximately 480%.

We also offer pawn loans in Nebraska and Iowa. Allowable service charges for pawn loans vary by state and loan size. Our pawn loans earn 20% per month for loans under $1,000 and our average pawn loan amount typically ranges between $10 and $250, although may range as high as $5,000. The loan amount varies depending on our estimated value of each item pawned.

Many states have laws limiting the amount of fees that may be charged in connection with any lending transaction (including payday and pawn lending transactions) when calculated as an APR, and some states expressly prohibit payday lending. These limitations, combined with other limitations and restrictions, effectively prohibit us from utilizing our present business model for cash advance or “payday” lending in those jurisdictions. In addition, the federal “2007 Military Authorization Act” prohibits lenders from offering or making payday loans (or similar lending transactions) to members of the U.S. military when the interest or fees exceed a 36% APR. Like the state limitations discussed above, this limitation effectively prohibits us from providing our cash advance or “payday” lending to members of the U.S. military. As a result of these restrictions, we do not conduct business with U.S. military personnel.

The above-described payday fees are the only fees we assess and collect from our customers for payday loans. Nevertheless, we also charge a flat fee that ranges from $15 to $40 (depending on the state) for returned checks in the event that a post-dated check we attempt to cash as repayment for our loan is returned.

Extensions or “Rollovers” of Payday Loans

Most states prohibit payday lenders from extending or refinancing a payday loan. Nevertheless, one state in which we presently provide payday loans (North Dakota) permits a loan to be extended or “rolled over” once.

When a customer “rolls over” or extends the term of an outstanding loan, when permitted by state law, we treat that rollover or extension as a brand new loan and we again charge the above-described loan fee for that transaction. This rollover has no effect on the imputed APR of the loan in those cases where the extended term is equal to the initial term of the loan. For example, a $100 four-week loan that costs $20 to obtain is the APR equivalent of 261%. If a customer extends the term of that loan for an additional four-week period, the customer will have paid $40 total in fees to obtain the $100 eight-week loan—which is again the APR equivalent of 261%. In cases where a customer (1) extends or rolls over a loan for a length of time that is less than the original loan or (2) repays the extended loan prior to the expiration of the fully extended term, the imputed APR will increase. For example, if a customer who obtained an initial $100 four-week loan for $20 in loan fees (the APR equivalent of 261%) later extends the term of that loan for only two additional weeks and pays the additional $20 loan fee, that customer will have borrowed $100 for a six-week period at a total cost of $40—which is the APR equivalent of 347%. We do not charge any interest on the unpaid fee from the initial term of the loan because, as a condition to agreeing to a loan extension, we will only accept cash payment of the fee for extending the loan.

Risks Associated With Our Loans—Default and Collection

Ordinarily, our customers approach us for a loan because they currently have insufficient funds to meet their present obligations, and so rarely if ever do our customers have sufficient funds in their checking accounts to cover the personal post-dated checks they provide us at the time of the loan transaction. The nature of our payday loan transactions presents a number of risks, including the ultimate risk that the loan will not be paid back. In addition, we do not obtain security for our payday loans principally because, even assuming our customers would have potential collateral to offer as security for a payday loan, the small size of each particular lending transaction does not justify the time, effort and expense of identifying the collateral and properly obtaining a security interest in such collateral. As a consequence, all of our payday loans are unsecured. This means that, absent court or other legal action compelling a customer to repay our loans, we rely principally on the willingness and ability of our customers to repay amounts they owe us. In this regard, in many cases the costs of merely attempting to collect the amounts owed to us exceed the amounts we would seek to collect—making it impractical to take formal legal action against a defaulted borrower.

6

When a customer defaults on a loan, we engage in collection practices that include contacting the customer for repayment and the customer’s bank to determine whether funds are available to satisfy their personal post-dated check. If funds are available, we present the check to the bank for repayment and an official check from the bank is obtained to pay off the item. The costs involved in these initial collection efforts are minimal and involve some employee time and possibly a flat $15-30 bank fee to cover the cost of the cashier’s check. If funds are not available, we generally attempt to collect returned checks for up to 90 days (or up to 180 days in cases where a bank account is still active and the customer has not initiated a stop payment on the postdated check provided), principally through continued attempts to contact the customer. If our attempts remain unsuccessful after 90 (or 180) days, we generally assign the item to a collection agency. Assignment to a collection agency may cost us 30-40% of the amount eventually collected (if any) from the customer. Ordinarily, we do not recoup any costs of collection from our customers.

Historically, we collect approximately 60% of the amount of all returned checks, which results in approximately 2.56% of our total payday loan principal and fee volume being uncollectible. In 2019, we generated approximately 126,000 payday loan transactions.

Industry Information

According to a December 2017 study by the Center for Financial Services Innovation (“2017 Financially Underserved Market Size Study”) consumers spent approximately $3.2 billion on fees for single payment loan products from storefront payday lenders in 2016, compared to $3.6 million in 2015. This year over year decline continues a trend that is expected to continue going forward. According to the Community Financial Services Association of America (“CFSA”) website, industry analysts estimate that 19 million U.S. households use short-term payday advances and estimate that there are 20,600 payday advance locations across the United States, which extend approximately $38.5 billion in short-term credit to households experiencing cash-flow shortfalls. In addition to being a valuable source of credit for many consumers, the payday loan industry makes significant contributions to the U.S. and state economies employing more than 50,000 Americans who earn $2 billion in wages and generating more than $2.6 billion in federal, state, and local taxes. Industry trends indicate that there will likely be a net decrease in total payday lending stores over the next few years due to store closings resulting from a combination of regulatory or legal changes, regulatory pressures, a slowdown in new store growth, and general economic conditions.

Predatory Lending and Regulatory Concerns

In general, the payday lending industry suffers from the perception and widespread belief that payday lenders are by their nature, predatory lenders, offering loans to low income and poorly educated consumers at costs that are too high to be good for consumers. This perception and belief results in frequent efforts in the U.S. Congress and various state legislatures, often proposed by consumer advocacy groups and lobbyists for traditional financial institutions such as banks, to further regulate and restrict or prohibit payday lending outright. See “Item 1A – Risk Factors” for further information regarding regulatory risks.

We do not believe the payday lending is predatory, nor do we believe that our loans are too costly for consumers if they are judiciously obtained. In fact, we believe that bank overdraft fees by themselves are typically far more costly for consumers, and bouncing a check can often involve other negative consequences such as independent fees levied by the parties to whom a bad check is written, negative publicity, etc. In this regard, the FDIC released a November 2008 report called “Study of Bank Overdraft Programs.” The report indicates that the average amount obtained when bank customers overdraw their accounts is $60, and the average overdraft fee charged by the bank is $27. This equates to an APR of 1,173% and 587% for a two-week and four-week $60 bank “loan,” respectively. In sum, we believe that many of the bad perceptions about our industry are fueled primarily by:

|

|

● |

the effects of our loans on consumers who do not judiciously obtain payday loans; |

|

|

● |

a lack of genuine understanding about the choices faced by low and middle-income people facing a critical cash shortage; and |

|

|

● |

anti-payday lending lobbying campaigns, often funded by traditional financial institutions such as banks and credit unions that would economically benefit from the elimination of payday lending. |

Seasonality

Our Consumer Finance segment results are subject to seasonality, with the first and fourth quarters typically being our strongest periods as a result of broader economic factors, such as holiday spending habits at the end of each year and income tax refunds during the first quarter.

7

Competition

Like most other payday lenders, we believe that the primary competitive factors in our business are location and customer service. We face intense competition in an industry with relatively low barriers to entry, and we believe that the payday lending markets are becoming more competitive as the industry matures and consolidates. We compete with other payday lending and check cashing stores, and with financial service entities and retail businesses that offer payday loans or similar financial services. For example, we consider credit card companies that offer payday features, credit unions, banks that offer small loans, and creditors and loan services that can extend payment terms on outstanding loans to be our competitors. In addition, we compete in part with services offered by traditional financial institutions, most particularly with respect to the “overdraft protection” services those institutions may offer and the charges they levy for checks written with insufficient funds.

Additional areas of competition have arisen. Businesses offer loans over the Internet as well as “loans by phone,” and these services compete with the services we offer. There also has been increasing penetration of electronic banking and related services into the check cashing and money transfer industry, including direct deposit of payroll checks, payroll or debit cards, stored-value cards, prepaid credit and debit cards, and electronic transfer of government benefits.

We also believe that customer service is critical to developing loyalty. In our industry, we believe that quality customer service means:

|

|

● |

assisting with the loan application process and helping our customers understand the loan terms; |

|

|

● |

treating customers respectfully; and |

|

|

● |

processing transactions with accuracy, efficiency and speed. |

Our competitors for pawn store merchandise sales include numerous retail and wholesale stores, including jewelry stores, discount retail stores, consumer electronics stores, other pawn stores, other resale stores, electronic commerce retailers and auction sites.

The pawn industry in the United States is large and highly fragmented. The industry consists of approximately 13,000 pawn stores owned primarily by independent operators who own one to three locations. We consider the industry relatively mature. The three largest pawn store operators account for approximately 10% of the total estimated pawn stores in the United States.

Effect of General Economic Conditions on our Consumer Finance Segment

Our business has experienced fluctuating changes in our provision for loan losses in recent years. For example, our provision for loan losses as a percentage of payday, installment and pawn loan revenue was 11.5%, 13.9%, and 12.3% in 2019, 2018, and 2017, respectively. We are uncertain how the current economic conditions will affect demand for our services or our loan losses after 2019.

Credit and financing available to us and our industry has been negatively impacted by recent federal and state legislation and regulation, including the overall negative perception associated with payday lending. For example, we are aware of federal and state regulatory pressures being exerted on our banking relationships due to the negative perception about payday lending. For more information, see “Regulation - Regulation of Consumer Financing Activities” below.

REGULATION

We are subject to regulation by federal, state and local governments that affect the products and services we provide. Generally, these regulations are designed to protect consumers who use our services and are not designed to protect our shareholders.

Regulation of Consumer Financing Activities

In those states where we currently operate consumer finance activities, we are licensed as a payday lender or pawn broker where required and are subject to various state regulations regarding the terms and conditions of our payday, installment and pawn loans and our lending policies, procedures and operations. In some states, payday lending is referred to as “deferred presentment,” “cash advance loans,” “deferred deposit loans” or “consumer installment loans.” State regulations normally limit the amount that we may lend to any single consumer and may limit the number of loans that we may make to any consumer at one time or in the course of a single year. State regulations also limit the amount of fees that we may assess in connection with any loan transaction and may limit a customer’s ability to extend or “rollover” a loan with us. Often, state regulations also specify minimum and maximum maturity dates for payday loans and, in some cases, specify mandatory cooling-off periods between transactions.

8

Our payday lending practices must also comply with the disclosure requirements of the Federal Truth-In-Lending Act and Regulation Z under that Act. Our collection activities for delinquent loans are generally subject to consumer protection laws regulating debt-collection practices. Finally, our payday lending business subjects us to the Equal Credit Opportunity Act and the Gramm-Leach-Bliley Act.

During the last few years, legislation has been introduced and passed in the U.S. Congress and in certain state legislatures proposing or effecting various restrictions or an outright prohibition on payday or certain installment lending. Currently, state laws in Arizona, Colorado, Montana, Oregon, South Dakota and Georgia have effectively eliminated the ability to conduct payday and certain installment lending in those states. In 2010, Congress passed the Dodd-Frank Wall Street Reform and Consumer Protection Act, which consolidated most federal regulation of financial services offered to consumers, and replaced the Office of Thrift Supervision’s seat on the FDIC Board. Almost all credit providers, including mortgage lenders, providers of payday loans, other nonbank financial companies, and banks and credit unions with assets over $10 billion, are subject to regulations and oversight by the Consumer Financial Protection Bureau (“CFPB”). While the CFPB does not have authority to make rules limiting interest rates or fees charged, the scope and extent of its authority is broad enough to impose limits on rollovers and extensions of payday loans, as well as compliance with federal rules and regulations.

After several years of research, debate, and public hearings, in October 2017 the CFPB issued new rules for payday lending. The proposed rules, originally scheduled to go into effect in August 2019, would impose significant restrictions on the industry, and it is expected that a large number of lenders would be forced to close their stores. The CFPB’s studies projected a reduction in the number of lenders by 50%, while industry studies forecast a much higher attrition rate. Included in the new rules are requirements for vetting borrowers (i.e., obtaining a credit report and performing basic underwriting procedures), limits on the number of loans a consumer could obtain in a 12-month period, limiting to two the number of times a consumer’s check may be presented to the consumer’s bank for payment, and provisions requiring paydowns by the consumer on successive loans. However, in January 2018, the CFPB issued a statement that it intends to “reconsider” the regulation. The most current information from the CFPB website states the proposals it is considering includes rescinding the mandatory underwriting provisions contained in the rule and to delay the August 19, 2019 compliance date for the other provisions to November 19, 2020. At this time it is uncertain whether the rule will be implemented as announced, rewritten with more favorable terms for the industry, or thrown out altogether. If the rule is implemented as written, it could have a significant and negative impact on business conducted within our Consumer Finance segment.

In addition, our Consumer Finance segment activities are subject to the following federal consumer laws, regulations and CFPB guidance:

|

|

● |

Unfair, Deceptive or Abusive Acts or Practices (“UDAAP”) |

|

|

● |

Fair Debt Collections Practice Act (“FDCPA”) |

|

|

● |

Consumer Complaint Management |

|

|

● |

Electronic Fund Transfer Act (“EFTA”) (Reg. E) |

|

|

● |

Fair Credit Reporting Act (“FCRA”) |

|

|

● |

Service Members Civil Relief Act |

For more information, see “PAYDAY LENDING BUSINESS—Predatory Lending and Regulatory Concerns” above.

Financial Reporting Regulation

Regulations promulgated by the United States Department of the Treasury under the Bank Secrecy Act require us to report all transactions involving currency in an amount greater than $10,000. Generally, every financial institution must report each deposit, withdrawal, exchange of currency or other payment or transfer that involves an amount greater than $10,000. In addition, multiple currency transactions must be treated as a single transaction if we have knowledge that the transactions are by or on behalf of any one person and result, in a single business day, in the transfer of cash in or out totaling more than $10,000. In addition, the regulations require us to maintain information concerning sales of monetary instruments for cash in amounts from $3,000 to $10,000. The Bank Secrecy Act requires us, under certain circumstances, to file a suspicious activity report.

9

The Money Laundering Suppression Act of 1994 requires us, as a money service business (“MSB”), to register with the United States Department of the Treasury. MSBs include check cashers and sellers of money orders. MSBs must renew their registrations every two years, maintain a list of their agents, update the agent list annually, and make the agent list available for examination.

Finally, we have established various procedures designed to comply, and we continue to monitor and evaluate our business methods and procedures to ensure compliance, with the USA PATRIOT Act.

Privacy Regulation

We are subject to a variety of federal and state laws and regulations restricting the use and seeking to protect the confidentiality of customer identity and other personal nonpublic customer information. We have identified our systems that capture and maintain nonpublic personal information, as that term is understood under the Gramm-Leach-Bliley Act and associated regulations. We disclose our public information policies to our customers as required by that law. We also have systems in place intended to safeguard this information as required by the Gramm-Leach-Bliley Act, which specifically governs certain aspects of our payday lending business.

TECHNOLOGY AND INFORMATION

We maintain an integrated system of retail points of sale and management software applications and platforms for processing the various types of financial transactions we offer. These systems provide us with customer service, internal control mechanisms, record-keeping and reporting information. These systems are designed to provide summary, detailed and exception information to various levels of management.

SECURITY

We believe the principal security risks to our Consumer Finance and Cellular Retail segments are robbery and employee theft. We have established extensive security and management information systems to address both areas of potential loss. To protect against robbery, most payday lending store employees work behind bullet-resistant glass, and the back office, safe and computer areas are locked and closed to customers. Security measures utilized in our retail locations include mechanical safes, electronic alarm systems monitored by third parties or remote controlled systems, control over entry to customer service representative, motion detection devices, locked cases, and, at times, the use of professional security services. Consumer Finance segment employees also use cellular phones to ensure safety and security whenever they are outside secured areas.

We implemented critical safeguarding controls, including daily cash and deposit monitoring, unannounced audits of cash and inventory items, and requiring immediate responses from our staff when irregularities in cash balances are discovered. We primarily self-insure for employee theft and dishonesty at the store level.

We regularly receive and store information about our customers, vendors and other third parties. We have programs in place to detect, contain, and respond to data security incidents. However, because the techniques used to obtain unauthorized access, disable or degrade service, or sabotage systems change frequently and may be difficult to detect for long periods of time, we may be unable to anticipate these techniques or implement adequate preventive measures. In addition, hardware, software, or applications we develop or procure from third parties or through open source solutions may contain defects in design or manufacture or other problems that could unexpectedly compromise information security. Unauthorized parties may also attempt to gain access to our systems or facilities, or those of third parties with whom we do business, through fraud, trickery, or other forms of deceiving our team members, contractors, and vendors.

EMPLOYEES

At December 31, 2019, we had approximately 980 employees. We believe our relationship with our employees is good, and we have not suffered any work stoppages or labor disputes. We do not have any employees that operate under collective-bargaining agreements.

CORPORATE INFORMATION

Our principal offices are located at 11550 “I” Street, Suite 150, Omaha, Nebraska 68137, our telephone number at that office is (402) 551-8888 and our internet website is https://www.westerncapitalresources.com.

10

Our fiscal year ends December 31. Neither we nor any of our predecessors have been in bankruptcy, receivership or any similar proceeding.

You should consider the following risk factors, in addition to the other information presented or incorporated by reference into this Annual Report on Form 10-K, in evaluating our business and your investment in us.

Investment Risks

Acquisitions and strategic investments may fail to meet our expectations, and any such failure could have a negative impact on our results of operation or financial condition, and could ultimately result in dilution to our shareholders.

Our long-term growth strategy includes acquisitions. We may not successfully execute this strategy. An acquisition strategy includes numerous risks, including, among others, the risk that our financial projections relating to our acquisitions may turn out to be incorrect and our investment may fail to positively impact our results and growth as anticipated (and may in fact negatively impact our results), the risk of unexpected or unidentified issues not discovered in the due diligence process which could harm our financial condition, risks related to our ability to successfully integrate an acquisition target into the Company, and the need for substantial additional capital which may result in dilution to our shareholders.

Acquisitions and strategic investments made wholly or partly on the basis of our issuance of securities to the target companies, or acquisitions made with cash that is obtained from outside investors or lenders, will result in dilution to our shareholders.

The structuring of future acquisitions, whether through share exchanges, merger acquisitions or otherwise, may result in dilution to existing shareholders. In addition, cash-based transactions may not be financed from corporate cash flows and reserves, and may themselves be financed through borrowing arrangements or the sale of equity or equity-linked securities, the latter of which would be dilutive to our shareholders.

Acquisitions and strategic investments may be disruptive to our business.

The time and expense associated with finding suitable acquisitions or with integrating acquired entities and operations with our Company can be disruptive to our ongoing business and divert our management’s attention. In addition, the financing of acquisitions may impact our ability to obtain or renew financing for existing operations, or subject us to covenants restricting certain activities. Any of these outcomes could have a short- or long-term adverse effect on our results of operation and our ability to further execute our acquisition strategy.

Unpredictability in financing and other markets could impair our ability to grow our business through acquisitions

We anticipate that opportunities to acquire businesses will materially depend on the availability of financing alternatives with acceptable terms as well as acceptable market valuations of prospective acquisitions. As a result, poor credit and other market conditions, mergers and acquisitions market valuations, any uncertainty in the financing markets, or the adverse regulatory pressures of being involved in the payday lending business in particular, could materially limit our ability to grow through acquisitions since such conditions and uncertainty make obtaining financing and finding attractive opportunities more difficult and more expensive.

Our controlling shareholder possesses controlling voting power with respect to our common stock, which will limit other shareholders’ influence on corporate matters.

Our controlling shareholders, WCR, LLC and BC Alpha Holdings I, LLC, which are under common control (see Item 12), had beneficial ownership of approximately 60.42% of our common stock as of March 20, 2020. As a result, the controlling shareholders have the ability to outright control our affairs through the election and removal of our entire Board of Directors and all other matters requiring shareholder approval, including a future merger or consolidation of the Company, or a sale of all or substantially all of our assets. This concentrated control limits the Company’s public float and could discourage others from initiating any such potential merger, consolidation or sale or other change-of-control transaction that may otherwise be beneficial to our shareholders. Furthermore, this concentrated control will limit the practical effect of your participation in Company matters, through shareholder votes and otherwise.

We are subject to risks associated with public health crises and epidemics/pandemics, such as the novel strain of coronavirus that recently originated in China.

We are exposed to risks associated with public health crises and epidemics/pandemics, such as the novel strain of coronavirus that recently originated in China (COVID-19). COVID-19 may have an adverse impact on our operations, supply chains and distribution systems and increase our expenses, including as a result of impacts associated with preventive and precautionary measures that we, other businesses and governments are taking. Due to these impacts and measures, we may experience significant and unpredictable reductions or increases in demand for certain of our products and services. In addition to existing travel restrictions, the United States, states or municipalities may impose prolonged quarantines or further restrict travel, which may significantly impact the ability of our employees to get to their places of work, or may significantly hamper our products from moving through the supply and distribution chains. As a result, given the rapid and evolving nature of the virus, COVID-19 could negatively affect our sales, and it is uncertain how COVID-19 will affect our operations generally if these impacts persist or exacerbate over an extended period of time. Any of these impacts could have a material adverse effect on our business, financial condition and results of operations.

11

Our certificate of incorporation grants our Board of Directors the power to issue additional shares of common and preferred stock and to designate other classes of preferred stock, all without shareholder approval.

Our authorized capital consists of 12.5 million shares of capital stock. Pursuant to authority granted by our certificate of incorporation, our Board of Directors, without any action by our shareholders, may designate and issue shares in such classes or series (including other classes or series of preferred stock) as it deems appropriate and establish the rights, preferences and privileges of such shares, including dividends, liquidation and voting rights, provided they are consistent with Delaware law. The rights of holders of other classes or series of stock that may be issued could be superior to the rights of holders of our common shares. The designation and issuance of shares of capital stock having preferential rights could adversely affect other rights appurtenant to shares of our common stock. Furthermore, any issuances of additional stock (common or preferred) will dilute the percentage of ownership interest of then-current holders of our capital stock and may dilute our book value per share.

Our common stock trades only in an illiquid trading market.

Trading of our common stock is conducted on the OTCQB, a tier of the OTC Markets (symbol: WCRS). This has an adverse effect on the liquidity of our common stock, not only in terms of the number of shares that can be bought and sold at a given price, but also through delays in the timing of transactions and reduction in security analysts’ and the media’s coverage of us and our common stock. This may result in lower prices for our common stock than might otherwise be obtained and could also result in a larger spread between the bid and asked prices for our common stock.

There is not now and there may not ever be an active market for shares of our common stock.

In general, there has been minimal trading volume in our common stock. During 2019, the average daily trading volume was under 1,500 shares. The small trading volume will likely make it difficult for our shareholders to sell their shares as and when they choose. Furthermore, small trading volumes are generally understood to depress market prices. As a result, you may not always be able to resell shares of our common stock publicly at the time and prices that you feel are fair or appropriate.

Failure to achieve and maintain effective internal controls could limit our ability to detect and prevent fraud and thereby adversely affect our business and stock price.

Effective internal controls are necessary for us to provide reliable financial reports. Nevertheless, all internal control systems, no matter how well designed, have inherent limitations. Even those systems determined to be effective can provide only reasonable assurance with respect to financial statement preparation and presentation. As we continue executing on our acquisition strategy, our fraud risks will change and likely increase as the acquired entity may be unfamiliar or uncooperative with proper internal controls and procedures. Our inability to maintain an effective control environment may cause investors to lose confidence in our reported financial information, which could in turn have a material adverse effect on our stock price.

Our reliance on information management and transaction systems to operate our business exposes us to potential security breaches of our sensitive information from cyber incidents and hacking.

Effective information security internal controls are necessary for us to protect our sensitive information from illegal activities and unauthorized disclosure. Despite our efforts to maintain the highest level of security around our information systems, the sophistication of hackers continues to increase. Our inability to maintain effective controls or utilization of information technology providers that also maintain effective controls may increase our vulnerability to cyber-attacks. Breaches of our information management systems could adversely affect our business reputation. We could also be subject to lawsuits or fines relating to the unauthorized disclosure of information. Any of these outcomes could negatively affect our results of operations and the price of our common stock.

Any disruption in the availability of our information systems could adversely affect our operations.

We rely upon our information systems to manage and operate our business. Our security measures could fail to prevent a disruption in the availability of our information systems, our back-up systems could fail to operate properly, or we may experience denial of service attacks or corruption of our data. Any disruption in the availability of our information systems could adversely affect our results of operations by impairing our ability to efficiently effect transactions.

12

A significant portion of our assets consists of goodwill and other intangible assets.

As of December 31, 2019, 10.7% of our assets consisted of goodwill and other intangible assets. Under generally accepted accounting principles, the carrying value of goodwill is subject to periodic review and testing to determine if it is impaired. The value of our assets will depend on market conditions, regulatory environment, the availability of buyers and similar factors. While the value of these assets is based on management projections and assumptions and is determined by using the discounted cash flow method for purposes of our impairment testing, those values may differ from what could ultimately be realized by us in a sales transaction or otherwise and that difference, while not affecting cash flow, could have a material adverse impact on our operating results and financial position.

Industry Risks

The payday loan industry is highly regulated under federal, state and local laws and regulations. Changes in federal, state or local laws and regulations governing lending practices, or changes in the interpretation of such laws and regulations, could negatively affect our business.

Our Consumer Finance segment activities are highly regulated under numerous federal, state and local laws, regulations and rules, which are subject to change. New laws, regulations or rules could be enacted or issued, interpretations of existing laws, regulations or rules may change and enforcement action by regulatory agencies may intensify.

Although states provide the primary regulatory framework under which we offer payday loans, certain federal laws also affect our business. For example, because payday loans are viewed as extensions of credit, we must comply with the federal Truth-in-Lending Act and Regulation Z under that Act. Additionally, we are subject to the Equal Credit Opportunity Act, the Gramm-Leach-Bliley Act and certain other federal laws.

From a federal standpoint, anti-payday loan legislation has occasionally been introduced in the U.S. Congress. Over the past several years, consumer advocacy groups and certain media reports have advocated governmental and regulatory action to prohibit or severely restrict sub-prime lending activities such as those we conduct. As outlined under “BUSINESS – REGULATION – Regulation of Consumer Financing Activities,” the CFPB released their final rule in October 2017 but announced in January 2018 that it is reconsidering the rule. If implemented in substantially its present form, the rule may put in question the viability of the entire industry and result in mass store closures.

In the states, there are nearly always bills pending to alter the current laws governing payday lending. There is also a current trend for consumer activist groups to seek law changes through a ballot initiative. Any of these bills or ballot initiatives, or future proposed legislation or regulations prohibiting payday loans or making them less profitable, could be passed in any state at any time, or existing laws permitting payday lending could expire. From time to time legislation banning payday loans has been introduced in Nebraska but has not been passed into law and there is currently an active ballot initiative in Nebraska to include on the 2020 ballot an initiated state statute capping annual interest on payday lenders to 36%. Since we derive a significant percentage of our payday revenues in Nebraska, the passage of any such legislation in Nebraska would have a highly material and negative effect on our consumer finance business.

Statutes authorizing payday loans typically provide state agencies that regulate banks and financial institutions with significant regulatory powers to administer and enforce the laws relating to payday lending. Under statutory authority, state regulators have broad discretionary power and may impose new licensing requirements, interpret or enforce existing regulatory requirements in different ways or issue new administrative rules, even if not contained in state statutes, that affect the way we do business and may force us to terminate or modify our operations in those jurisdictions. They may also impose rules that are generally adverse to our industry. Finally, in many states, the attorney general has scrutinized or continues to scrutinize the payday loan statutes and the interpretations of those statutes.

In sum, the passage of federal or state laws and regulations that govern or otherwise affect lending, or changes in interpretations of them, could, at any point, result in our curtailment or cessation of operations in certain or all jurisdictions or locations essentially prohibiting us from conducting our lending business in its current form. Any such legal or regulatory change would certainly have a material and adverse effect on us, our operating results, financial condition and prospects, and perhaps even our viability. Furthermore, any failure to comply with any applicable federal, state or local laws or regulations could result in fines, litigation, closure of one or more store locations and negative publicity.

13

Adverse changes in laws or regulations relating to pawn lending services could negatively impact our financial results and/or limit our ability to expand into new markets.

Our pawn lending products and services are subject to extensive regulation and supervision under various federal, state and local laws, ordinances and regulations. We face the risk that restrictions or limitations on pawn loan amounts, pawn loan yields and customer acceptance of pawn loan products resulting from the enactment, change or interpretation of laws and regulations could have a negative effect on our business activities. In particular, short-term consumer loans have come under increased scrutiny and increasingly restrictive regulation in recent years. Adoption of such federal, state or local regulation or legislation could restrict, or even eliminate, our ability to conduct our pawn lending operations at a profit level we consider reasonable at some or all of our stores, and could prevent us from expanding into new markets.

Litigation and regulatory actions directed toward the consumer finance industry or our Company could adversely affect our operating results, particularly in certain key states.

During the last few years, the consumer finance industry has been subject to regulatory proceedings, class action lawsuits and other litigation regarding the offering of payday loans, and we could suffer losses resulting from interpretations of state laws in those lawsuits or regulatory proceedings, even if we are not a party to those proceedings. The losses we could suffer could be directly incurred through our involvement in litigation or regulatory proceedings, or could be indirectly incurred through negative publicity regarding the industry in general that is generated by litigation on regulatory proceedings involving third parties.

In addition, regulatory actions or enforcement efforts taken with respect to money services businesses could negatively affect our ability to operate our consumer finance segment in our current form. For example, federal bank regulators are imposing significant costs and regulatory pressure on banks that do business with money services businesses, even though our business is conducted in a manner compliant with applicable law. As a result, fewer and fewer banks are willing to accept or even retain customers in the MSB industry. We may be forced to change long-standing banking relationships and change the way we operate our consumer finance operations, incurring additional capital expenditures and paying higher banking fees.

Public perception of payday lending as being predatory or abusive could adversely affect our business.

In recent years, consumer advocacy groups and media reports have advocated governmental action to prohibit or severely restrict payday loans. The consumer groups and media reports typically focus on the cost to a consumer for this type of loan, which is higher than the interest typically charged by credit card issuers. The consumer groups and media reports typically characterize these transactions as predatory or abusive toward consumers. If this negative characterization of payday lending becomes widely accepted by consumers, demand for our payday loans could significantly decrease, which could adversely affect our results of operations primarily by decreasing our revenues. Negative perception of payday lending activities could also result in our industry being subject to more restrictive laws and regulations and greater exposure to litigation.

Competition in the consumer finance industry is intense and could cause us to lose market share and revenues.

We believe that the primary competitive factors in the payday loan industry are store location and customer service. We face intense competition in the payday and pawn lending industry, and we believe that those markets are becoming more competitive as these industries mature and begin to consolidate. The payday loan industry has low barriers to entry, and new competitors, such as Wal-Mart, may easily enter the market. The pawn lending industry has medium level barriers to entry, however, there are several large pawn lending companies with which we directly compete. We also currently compete with services, such as overdraft protection offered by traditional financial institutions, and with other payday loan and check cashing stores and other financial service entities and retail businesses that offer payday loans or other similar financial services, as well as a rapidly growing internet-based payday loan market. Some of our competitors have larger and more established customer bases and substantially greater financial, marketing and other resources than we have. As a result, we could lose market share and our revenues could decline, thereby affecting our earnings and potential for growth.

We face significant cellular retail competition that may reduce our market share and lower our profits.

We face significant competition in our Cellular Retail segment. We compete with the four national wireless service providers (AT&T, Sprint, T-Mobile and Verizon Wireless) as well as other smaller brands or carriers such as U.S. Cellular, Boost Mobile and Metro by T-Mobile and with many mobile virtual network operators (“MVNOs”) such as Walmart’s Straight Talk and Family Mobile plans. We also compete with government-financed “lifeline assurance” programs that offer free or reduced-cost cellular services to individuals and families receiving many types of public assistance. Our ability to compete effectively will depend on, among other things, the pricing of cellular services and equipment, the quality of our customer service, the reach and quality of our sales and distribution channels and our capital resources. It will also depend on how successfully we anticipate and respond to various factors affecting our industry, including new technologies and business models, changes in consumer preferences, demographic trends and economic conditions.

14

The cellular retail industry also faces competition from other communications and technology companies seeking to capture customer revenue and brand dominance with respect to the provision of cellular accessories and services. For example, Apple Inc. packages software applications and content with its handsets, and Google Inc. has developed and deployed an operating system and related applications for mobile devices.

Free shipping pressure in the e-commerce industry could decrease our direct to consumer segment’s revenues and profitability.

The abundance of free shipping offers from Amazon.com and other online retailers is putting pressure on our Direct to Consumer segment shipping revenues, currently representing 15% of Direct to Consumer revenues. If market forces lead to the elimination of this revenue stream, it may be difficult for the Direct to Consumer segment to make up that lost revenue.

General economic conditions affect our loan losses, and accordingly, our results of operations could be adversely affected by a general economic slowdown or other negative economic conditions such as high unemployment.

Provision for loan losses, net of recoveries, is one of our largest Consumer Finance segment operating expenses, constituting approximately 11% of our loan fee revenues for the year ended December 31, 2019, with payday loan losses comprising most of the losses. Any changes in economic factors that adversely affect our customers, such as an economic downturn or high unemployment, could result in higher loan loss experiences than anticipated, which could in turn adversely affect our loan charge-offs and operating results.

A sustained deterioration in the economy could reduce demand for our products and services and result in reduced earnings.

A sudden or sustained deterioration in the economy could result in decreased demand for our seed, live plant, holiday gifts and home restoration products. This could result in decreased revenue and, because a significant portion of our sales in the Direct to Consumer segment are of live goods, inventory losses on live product acquired prior to a seasonal selling period could be significant.

In addition, a sudden or sustained deterioration in the economy could cause worsening performance of our pawn loans and in consumer demand for and resale value of pre-owned merchandise that we sell in our stores. This, in turn, could reduce the amount that we could effectively lend on an item of collateral. Such reductions could adversely affect pawn loan balances, pawn loan redemption rates, inventory balances, revenues and gross profit margins.

Company Risks

The concentration of our Consumer Finance revenues in certain states could adversely affect us.

We currently provide payday or installment lending services in six states. For the year ended December 31, 2019, Consumer Finance revenues from our locations in Nebraska represented approximately 35.4% of our total Consumer Finance segment revenues. For the foreseeable future, we expect that a material portion of our Consumer Finance revenues will continue to be generated in Nebraska. In addition, for the year ended December 31, 2019, Consumer Finance revenues from our North Dakota, Iowa and Wyoming stores represented approximately 25.3%, 16.4% and 14.5% of our total Consumer Finance revenues, respectively. Changes to prevailing economic, demographic, competitive, regulatory or any other conditions, including the legislative, regulatory or litigation risks mentioned above, in the markets in which we operate, and in Nebraska in particular, could lead to a reduction in demand for our services and result in a decline in our revenues or an increase in our provision for doubtful accounts, or even an outright legal prohibition on the conduct of our business. In this regard, we are aware of pending legislation in Nebraska that is aimed at eliminating payday lending in that state and permitting short-term loans in the nature of installment loans and of a ballot initiative capping annual interest on payday lenders to 36%. Any of these outcomes could in turn result in a material and swift deterioration of our Consumer Finance segment financial condition principally by impairing its revenues and affecting its ability to obtain financing and operating liquidity, its operating results and its business prospects.

15

If estimates of our loan losses are not adequate to absorb actual losses, our financial condition and results of operations may be adversely affected.

We maintain an allowance for loan losses at levels to cover the estimated incurred losses in the collection of our payday and installment loan portfolios outstanding at the end of each applicable period. At the end of each period, management considers recent collection history to develop expected loss rates, which are used to establish the allowance for loan losses. Our allowance for loan losses was $0.67 million on December 31, 2019. Our allowance for loan losses is an estimate, and if actual loan losses are materially greater than our allowance for losses, our financial condition and results of operations could be adversely affected.

We face substantial risk through reliance on a single wireless retail carrier.

We operate our Cellular Retail segment exclusively as an authorized dealer for Cricket, which means that this segment of our operations is entirely dependent upon continued operations as a Cricket dealer under our dealer agreement with Cricket Wireless, the commitment of Cricket Wireless to advertise and offer competitive product and service offerings in our markets, and the health of our relationship with Cricket Wireless. If Cricket Wireless were to change certain aspects of its dealer arrangements, including items such as pricing, product supply, credit terms and dealer compensation structure (all of which are primarily determined by Cricket Wireless) in a manner that is adverse to us, our margins and results of operations would likely suffer. In addition, if Cricket Wireless were to begin growing its relationship with other operators, or were to embark upon an effort to significantly grow corporate-owned locations, our prospects for growth in this segment would suffer.

Managing our inventory is complex and may include write-downs of excess or obsolete inventory.

Managing our inventory, across our segments, is complicated by a number of factors, including the need to maintain a significant inventory of finished goods to support our cellular retail locations and online orders for our products that we anticipate but may not be received. These issues may cause us to purchase and maintain significant amounts of inventory. If this inventory is not used as expected based on anticipated requirements, it may become excess or obsolete. The existence of excess or obsolete inventory can result in sales price reductions or inventory write-downs, which could adversely affect our business and results of operations.