Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - RAIT Financial Trust | d401268d8k.htm |

1

R

A

I

T

RAIT Financial Trust

Investor Presentation

Second Quarter 2012

Exhibit 99.1 |

2

R

A

I

T

Forward Looking Statements &

Non-GAAP Financial Measures

This document and the related presentation may contain forward-looking statements within

the meaning of the Private Securities Litigation Reform Act of 1995. These

forward-looking statements include, but are not limited to, statements about RAIT

Financial Trust’s (“RAIT”) plans, objectives, expectations and intentions with respect to future operations,

products, dividends, cash from investments and services and other statements that are not

historical facts. Forward- looking statements are sometimes identified by the words

“may”, “will”, “should”, “potential”, “predict”, “continue”,

“project”, “guide”, or other similar words or expressions. These

forward-looking statements are based upon the current beliefs and expectations of

RAIT's management and are inherently subject to significant business, economic and

competitive uncertainties and contingencies, many of which are difficult to predict and

generally not within RAIT’s control. In addition, these forward-looking

statements are subject to assumptions with respect to future business strategies and

decisions that are subject to change. RAIT does not guarantee that the assumptions underlying such

forward looking statements are free from errors. Actual results may differ materially from the

anticipated results discussed in these forward-looking statements. The

following factors, among others, could cause actual results to differ materially from the anticipated results or other

expectations expressed in the forward-looking statements: the risk factors discussed and

identified in filings by RAIT with the Securities and Exchange Commission

(“SEC”), including, without limitation, RAIT’s most recent annual and

quarterly reports filed with SEC. You are

cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of

this presentation. All subsequent written and oral forward-looking statements attributable

to RAIT or any person acting on its behalf are expressly qualified in their entirety by

the cautionary statements contained or referred to in this document and the related

presentation. Except to the extent required by applicable law or regulation, RAIT undertakes

no obligation to update these forward-looking statements to reflect events or

circumstances after the date of this presentation or to reflect the occurrence of

unanticipated events. This document and the related presentation may contain non-U.S. generally accepted

accounting principles (“GAAP”) financial measures. A reconciliation of

these non-GAAP financial measures to the most directly comparable GAAP financial

measure is included in this document and/or RAIT’s most recent annual and quarterly reports.

RAIT’s SEC filings are available on RAIT’s website at www.raitft.com. |

3

R

A

I

T

About RAIT

RAIT Financial Trust (“RAIT”) (NYSE: RAS), is a diversified full service

commercial real estate company organized as an internally-managed REIT with

$3.6 billion of assets under management

Scalable commercial real estate platform with over 350 employees

Seasoned commercial real estate Lender

Origination platform for bridge, mezzanine and CMBS Loans

Owner –

commercial real estate properties (primarily multi-family properties)

Sophisticated asset management

Captive property management for multi-family and office properties

Non-traded REIT sponsor

Increased quarterly common dividend 33% in the first quarter to $0.08 per

common share

No unsecured, recourse debt maturities until October 2015 |

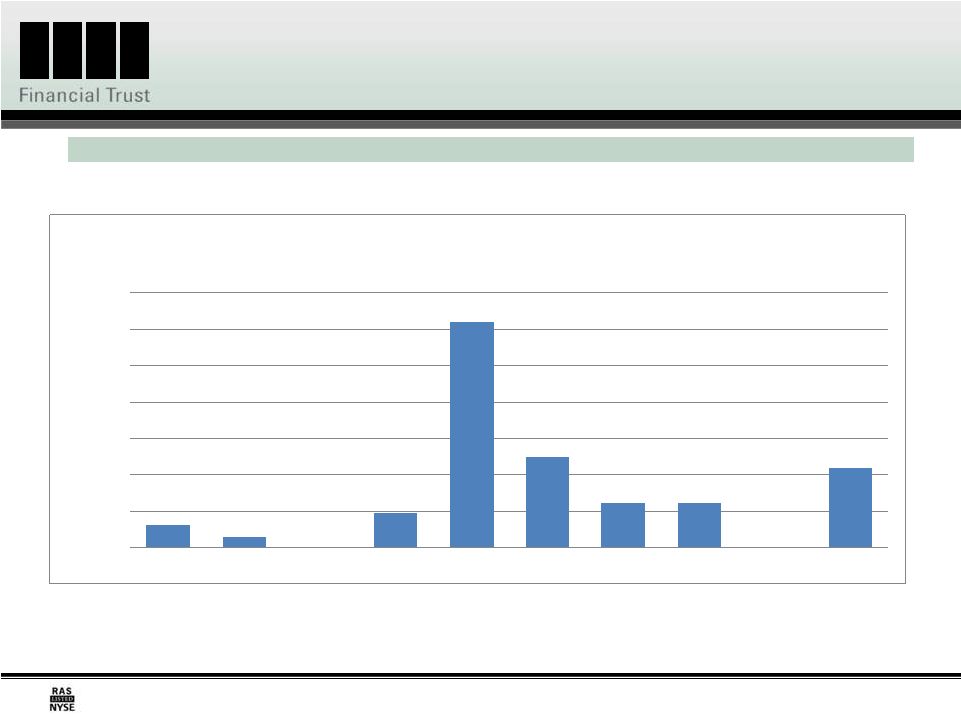

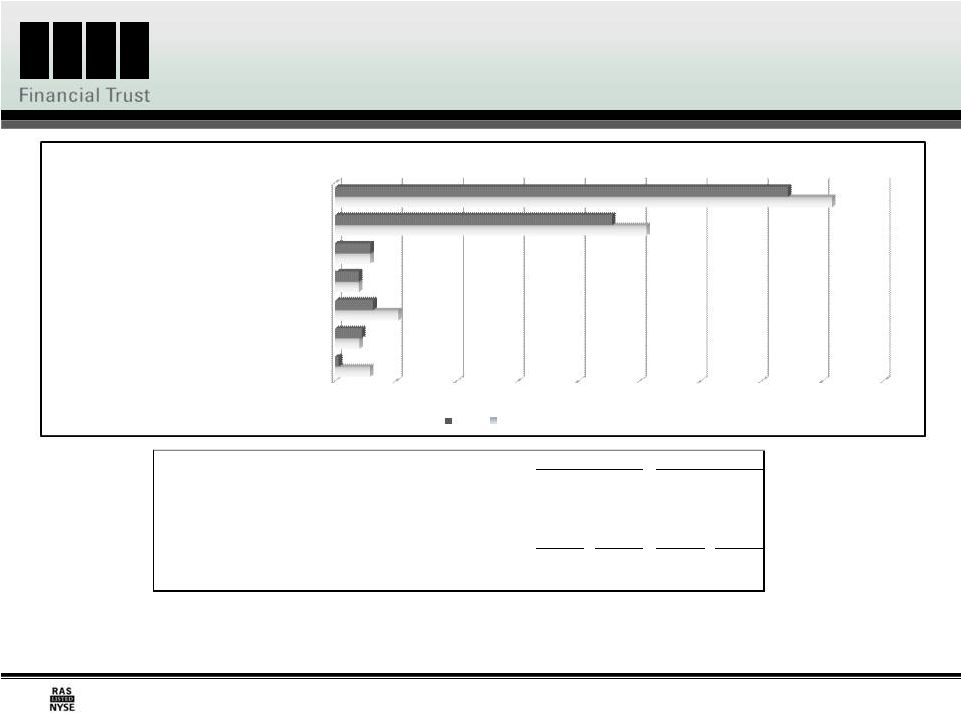

Recourse Debt

Summary As of June 30, 2012 ($ in 000s)

4

R

A

I

T

(1)

Assumes full exercise of holders’ 7.0% convertible senior notes redemption right in April

2016.

(2)

Includes senior secured notes issued by us with an aggregate principal amount equal to $100,000 with a

weighted average coupon of 7.0%, which are eliminated in consolidation $12,633

$6,187

$-

$19,381

$124,033

$50,000

$25,000

$25,000

$-

$43,771

$-

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

2012

2013

2014

2015

2016 (1)

2017 (2)

2018 (2)

2019 (2)

2020

Thereafter

Recourse Debt Maturities and Redemption Dates

(in 000s)

No unsecured, recourse debt maturities until October 2015

|

5

R

A

I

T

Synergistic Business Lines

Commercial real estate lending

$1.1 billion in loans

Originate, underwrite, close CMBS and transitional CRE loans

Directly owned commercial real estate

$994 million portfolio: $595 million multi-family, $271 million office, $81 million

retail and $47 million land

Asset and property management

Scalable non-traded REIT platform

Full service property management capabilities

CDOs –

earning management fees |

6

R

A

I

T

Commercial Real Estate Lending

Commercial real estate lending

$1.1 billion of CRE loans at June 30, 2012

Capitalize

on

existing,

scalable

platform

and

internal

expertise

to

originate

bridge,

mezzanine and CMBS loans of $5 million to $30 million on multi-family, office, retail

and light industrial properties

Growing pipelines

Spread expansion opportunities

Fee income opportunities –

originating, managing and servicing |

7

R

A

I

T

Commercial Real Estate Lending: CMBS

CMBS

loans:

warehouse

providers

Barclays

$150

million

Citibank

$100

million

CMBS

pipeline

at

approximately

$450

million

at

June

30,

2012

$231

million

of

availability

at

June

30,

2012

Originated

$37

million

of

CMBS

loans

through

June

30,

2012

Securitized

$25

million

of

CMBS

loans

through

July

15,

2012

Expect

to

fund

and

securitize

CMBS

loans

quarterly |

8

R

A

I

T

Commercial Real Estate Lending: Bridge &

Mezzanine Lending

Bridge & mezzanine lending

$233 million in transitional loan originations through June 30, 2012

General

terms

–

transitional

properties

Bridge

loans

–

floating

rate,

fees,

approximately

7%

coupons

Mezzanine loans -

floating rate, fees, approximately 12%+ coupons

Funding

Senior participations: Developing bank participation program

$44 million in un-restricted cash available at June 30, 2012

|

R

A

I

T

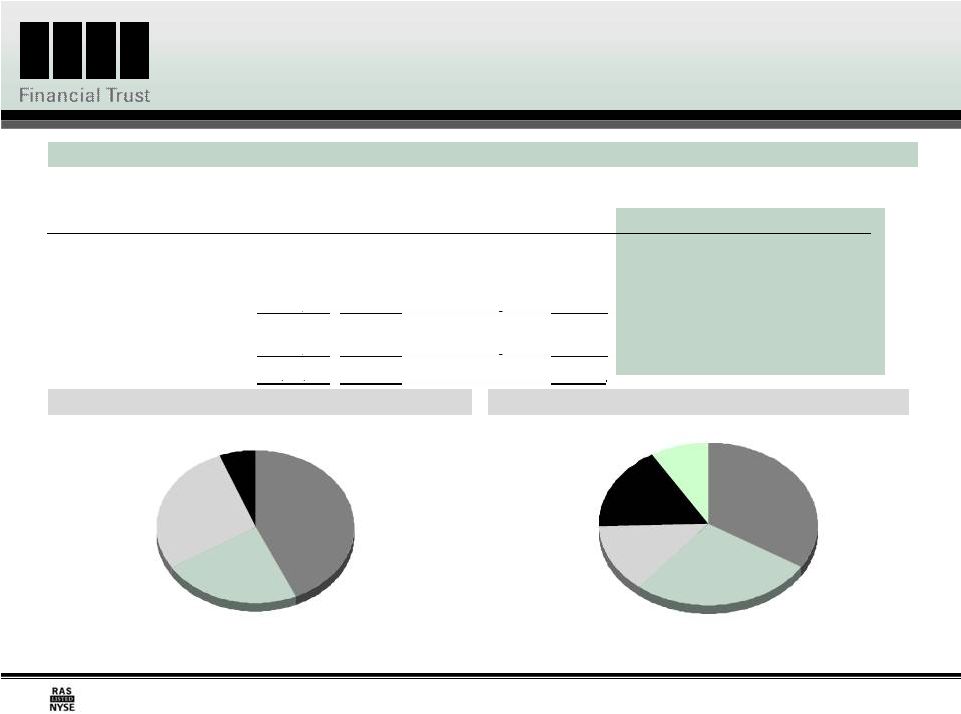

CRE Loan Portfolio Statistics

By Property Type

(1)

(1) Based on book value at 6/30/2012.

By Geographic Region

(1)

Improved credit performance of the loan portfolio

As of June 30, 2012 unless otherwise Indicated ($ in 000s)

Mid Atlantic

27%

Southeast

14%

Northeast

9%

Central

33%

West

17%

Multi-family

23%

Retail

28%

Other

6%

Office

43%

9

Book Value

Weighted-

Average

Coupon

Range of Maturities

Number

of Loans

Key Statistics

Q2

2012

Q2

2011

Commercial Real Estate (CRE) Loans

Non-accrual loans

$73,592

$94,117

Commercial mortgages

$692,406

6.3%

Aug.

2012

to Jul. 2022

49

% change

(22%)

Mezzanine loans

280,651

9.5%

Aug.

2012

to Nov. 2038

87

Reserve for losses

35,426

49,906

Preferred equity interests

65,669

9.6%

Mar. 2014

to Aug. 2025

23

% change

(29%)

Total CRE Loans

$1,038,726

7.3%

159

Provision for losses

500

950

Other loans

53,684

4.5%

Aug.

2012

to Oct. 2016

3

% change

(47%)

Total investments in loans

$1,092,410

7.2%

162 |

10

R

A

I

T

Directly Owned Commercial Real Estate

Directly owned real estate portfolio

$994 million of CRE properties at June 30, 2012

Strategy to maximize value over time through increasing occupancy and higher

rental rates

Increasing rental income from June 30, 2011 through June 30, 2012

Increasing average effective rent, average occupancy and net operating income

from June 30, 2011 to June 30, 2012

Assets acquired below borrower’s cost upon loan conversions

Portfolio is internally managed by seasoned property management professionals

|

11

R

A

I

T

Directly Owned Commercial Real Estate

Portfolio Statistics

Net Real Estate Operating Income

Average Effective Rent

(a)

Improved Occupancy and Net Operating Income

As of June 30, 2012 unless otherwise Indicated ($ in 000s)

Investments

in Real

Estate

Quantity

Number of

Properties

Average Physical Occupancy

6/30/2012

6/30/2011

Multi-family real estate properties

$594,928

8,014 units

33

91.2%

88.6%

Office real estate properties

270,724

2,015,524 sq. ft.

11

71.0%

68.8%

Retail real estate properties

81,454

1,422,298 sq. ft.

4

70.0%

62.0%

Parcels of land

47,059

19.9 acres

10

–

–

Total

$994,165

58

85.2%

83.1%

Q2 2012

Q2 2011

Rental income

$25,540

$22,138

Real estate operating expenses

(13,487)

(13,791)

Net Real Estate Operating Income

$12,053

$8,347

Number of owned properties

58

48

Average Occupancy

85.2%

83.1%

Property Type

Q2 2012

Q2 2011

% Variance

Multi-family

(b)

$695

$673

3%

Office

(c)

19.07

18.39

4%

Retail

(c)

12.44

6.69

(d)

86%

(d)

(a)

Based on properties owned as of June 30, 2012.

(b)

Average effective rent is rent per unit per month.

(c)

Average effective rent is rent per square foot per year.

(d)

Retail rental rate of $6.69 per square foot for Q2 2011 was lower than contractual rates due to certain

one-time leasing adjustments. Without these one-time items, the Q2 2011 retail rental

rate would have been approximately $8.53 per square foot. This translates into a 46% increase in

rental rates on our retail portfolio from Q2 2011 through Q2 2012

|

12

R

A

I

T

Scalable non-traded REIT platform

Independence Realty Trust, Inc. (“IRT”) & Independence Mortgage Trust, Inc.

(“IMT”)

Raise capital through retail Broker/Dealer & financial advisor networks

IRT

–

multi-family equity REIT

RAIT

equity

investment

of

$51

million

pari

passu

with

returns

to

IRT

equity

investors

RAIT contributed seven properties to IRT with an aggregate purchase price of $133.3

million Monthly dividend –

6% current run rate based on $10 initial offering price

Target maximum equity raise: $1.1 billion

IMT

–

structured finance REIT: formed in October 2011 and is currently in

registration with the SEC

We expect IMT to acquire and manage a portfolio of commercial real estate loans, CMBS and

other commercial real estate-related securities

Target maximum equity raise: $1.7 billion

Any disclosure relating to IRT or IMT is neither an offer nor a solicitation to purchase

securities issued by IRT and IMT Fee Income: Asset and Property Management

|

13

R

A

I

T

Fee Income: Asset and Property Management

Asset management

Management fees

CDOs

$1.9 billion of commercial real estate loans

$1.7 billion of U.S. real estate debt securities

S & P and Morningstar rated loan servicer and special servicer

Property management

Property management fees

Jupiter Communities

Multi-family focused

47 properties and 10,290 units

CRP Commercial Services

Office focused

3 million square feet

As of June 30, 2012 |

14

R

A

I

T

2012 Opportunities for Growth

Focus on growth through:

Utilizing RAIT’s core commercial real estate platform to generate appropriate

risk-adjusted returns by originating, underwriting and managing commercial real

estate loans

Focus on CMBS and transitional loans (bridge and mezzanine loans)

Continuing to effectively manage RAIT’s portfolio of owned real estate to deliver

increasing rental and occupancy rates while managing operating costs

Leveraging RAIT’s capabilities through non-traded REIT platform to grow fee

income and assets under management

Opportunistically investing in discounted RAIT liabilities including CDO debt and

convertible debt |

15

R

A

I

T

2012-2013 Projected Cash Received from

Investments

(1)

(1)

Constitutes forward-looking information. Actual full year 2012-2013 projected

cash received from investments and each individual line item presented herein, could vary significantly

from the projections presented. The above projections assume: Investment portfolios

remain static with June 30, 2012 balances and generate cash at historical levels; RAIT does not

raise additional capital; RAIT continues to receive its securitization collateral management

fees and generates property management fees and loan origination fees from third parties at

historical levels; RAIT’s sponsored non-traded REITs experience significant growth in

their investment portfolios by the end of the period covered and the identified cash uses remain at

historical levels.

($'s in millions, except per share amounts)

Projected cash received from investments

(1)

140

$

-

150

$

157

$

-

$169

Less: CDO and property level interest costs

(51)

(50)

Less: Corporate interest and preferred dividends

(33)

(33)

Less: General and administrative costs

(32)

-

(35)

(32)

-

(35)

Projected net cash received from investments

(1)

$24

-

$31

$41

-

$51

Per Share

0.48

$

-

0.63

$

0.84

$

-

1.05

$

2012

2013

$-

$10

$20

$30

$40

$50

$60

$70

$80

$90

CRE loan interest received

Owned real estate cash received

CDO management fees received

CMBS loan sales

Loan origination fees received

($'s in Millions)

2012

2013

Non-traded REITs -- asset management fees

Property management fees - 3rd party

|

16

R

A

I

T

Adjusted Book Value

(1)

Amount

Per Share (2)

Total shareholders' equity, as

reported………………………………………………………………………………..

841,612

$

16.87

$

Liquidation value of preferred stock

(3)……………………………………………………………………………….

(167,025)

(3.35)

RAIT book

value…………………………………………………………………………………………………………………….

674,587

13.52

Adjustments:

Taberna securitizations net

effect…………………………………………………………………………………..

(547,257)

(10.97)

CRE CDO derivative

liabilities…………………………………………………………………………………………..

79,816

1.60

Accumulated depreciation and

amortization…………………………………………………………………..

99,333

1.99

Valuation of recurring collateral and property management

fees………………...………………..

20,970

0.42

Total

adjustments…………………………………………………………………………………………………………………..

(347,138)

(6.96)

Adjusted book

value…………………………………………………………………………………………………….

327,449

$

6.56

$

As of June 30, 2012

(1)

Management views adjusted book value as a useful and appropriate supplement to

shareholders’ equity and book value per share. The measure serves as an

additional measure of our value because it facilitates evaluation of us without the effects of various items that we are required to

record in accordance with GAAP but which have limited economic impact on our business.

Those adjustments primarily reflect the effect of consolidated securitizations where

we do not currently receive cash flows on our retained interests, accumulated depreciation and amortization,

the valuation of long-term derivative instruments and a valuation of our recurring

collateral and property management fees. Adjusted book value is a non-GAAP

financial measurement, and does not purport to be an alternative to reported shareholders’ equity, determined in accordance with

GAAP, as a measure of book value. Adjusted book value should be reviewed in connection with

shareholders’ equity as set forth in our consolidated balance sheets, to help

analyze our value to investors. Adjusted book value may be defined in various ways throughout the REIT

industry. Investors should consider these differences when comparing our adjusted book

value to that of other REITs.

(2)

Based on 49,905,866 common shares outstanding as of June 30, 2012.

(3)

Based on 2,787,931 Series A preferred shares, 2,271,620 Series B preferred shares, and

1,621,430 Series C preferred shares outstanding as of June 30, 2012, all of which have

a liquidation preference of $25.00 per share. |

17

R

A

I

T

RAIT Highlights

Experienced management team

Integrated platform with synergistic business lines

Pipeline of investment opportunities

Improving cash flow

Provided common dividend guidance of at least $0.08 per quarter for 2012

|