Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - RAIT Financial Trust | d8k.htm |

RAIT

Financial Trust NAREIT REITWeek 2011

June 8, 2011

Exhibit 99.1

1 |

Forward Looking

Statements & Non-GAAP Financial Measures

This document and the related presentation may contain forward-looking statements within

the meaning of the Private Securities Litigation Reform Act of 1995. These

forward-looking statements include, but are not limited to, statements about RAIT Financial Trust’s (“RAIT”) plans, objectives, expectations and

intentions with respect to future operations, products and services and other statements that

are not historical facts. These forward-looking statements are based upon the

current beliefs and expectations of RAIT's management and are inherently subject to significant business, economic and competitive

uncertainties and contingencies, many of which are difficult to predict and generally not

within RAIT’s control. In addition, these forward-looking statements are

subject to assumptions with respect to future business strategies and decisions that are

subject to change. Actual results may differ materially from the anticipated results

discussed in these forward-looking statements. The following factors, among others, could cause actual results to differ materially from the

anticipated results or other expectations expressed in the forward- looking

statements: the risk factors discussed and identified in filings by RAIT with the Securities and Exchange Commission (“SEC”), including, without

limitation, RAIT’s most recent annual and quarterly reports filed with SEC.

You are cautioned not to place undue reliance on these forward-looking statements, which

speak only as of the date of this presentation. All subsequent written and oral

forward-looking statements attributable to RAIT or any person acting on its behalf are expressly qualified in their entirety by the cautionary statements

contained or referred to in this document and the related presentation. Except to the extent

required by applicable law or regulation, RAIT undertakes no obligation to update these

forward-looking statements to reflect events or circumstances after the date of this presentation or to reflect the occurrence of

unanticipated events.

The related presentation may contain non-U.S. generally accepted accounting principles

(“GAAP”) financial measures. A reconciliation of these non-GAAP

financial measures to the most directly comparable GAAP financial measure is included in

RAIT’s most recent annual and quarterly reports.

RAIT’s SEC filings are available on RAIT’s website at www.raitft.com. 2 |

About RAIT

Diversified full service commercial real estate company with $3.8 billion

assets under management

Lender -

Commercial Real Estate Loans

Multi-family, office, retail

Origination platform for bridge, mezzanine and CMBS Loans

Long-dated, match funded liabilities

Owner –

Commercial real estate properties

Primarily multi-family & office

Captive property management

Operate as a REIT

IPO –

1998 : approximately 400 employees nationwide

Experienced management team that has invested through multiple cycles

Quarterly common dividend of $0.06 per share, split-adjusted,

representing an approximate 4% dividend yield

1:3 reverse-split effective June 30, 2011

3 |

Experienced

Management Team Officer

Position

Years of

Experience

Comments

Scott F. Schaeffer

Chairman of the Board, CEO

and President

26

Chairman of the Board since December 2010

CEO of RAIT since February 2009

President since September 2000

Jack E. Salmon

CFO and Treasurer

34

CFO and Treasurer of RAIT since December 2006

Joined RAIT in 2006

Raphael Licht

COO and Secretary

18

COO of RAIT since February 2009

Chief Legal Officer and Chief Administrative Officer from

December 2006 to February 2009

Joined RAIT in 2006

Ken Frappier

Executive Vice President –

Portfolio and Risk

Management

37

Executive Vice President of RAIT since February 2008

Chief Credit Officer of RAIT from December 2006 to February

2008

Senior Vice President of Portfolio and Risk Management of RAIT

from April 2002 to December 2006

Jim Sebra

Senior Vice President

and CAO

14

SVP and CAO since May 2007

Joined RAIT in 2006

Andres Viroslav

Vice President, Director of

Corporate Communications

16

Vice President of RAIT since 2002

Joined RAIT in September 2001

4 |

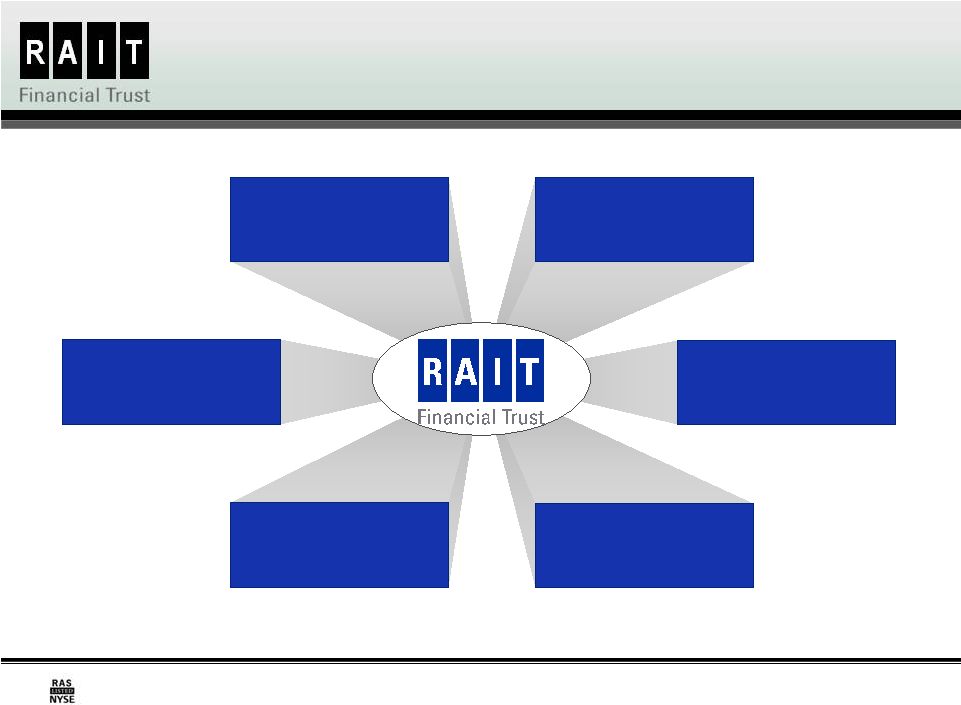

Diversified

Platform Assets Under

Management

$0.9 billion of

CRE properties

Manage $1.8B

of U.S. real

estate debt

S&P Rated

Loan Servicer

and Special

Servicer

Midland Enterprise

System

Cash

Management

/

Treasury

Functions

(SOX

Environment)

Broker Dealer

& Advisory

Services

CMBS

Origination and

Securitization

Advise Institutional

Investors on RE

Assets:

Origination, valuation,

management,

servicing,

acquisition, disposition

& reporting

$1.1B

of

CRE

loans

Asset &

Property

Management

Jupiter

Communities, LLC

CRP Commercial

Services

Investor Reporting

Leasing Capabilities

Monthly Credit

Analysis

Property-Level

Accounting

Non-Traded

REIT Sponsor

& Advisor

Independence

Realty Trust, Inc.

Captive Dealer

Manager

Generate fee

income

5 |

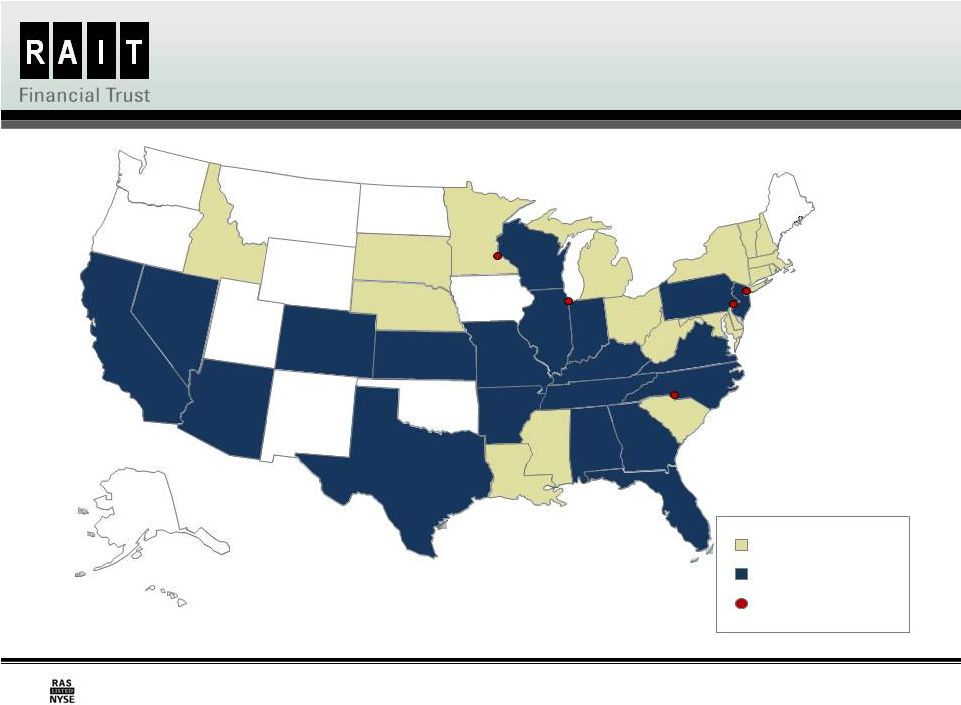

Where We Are:

National Reach 6

LEGEND

RAIT

CRE

Loans

RAIT

Commercial Services

Offices

AK

CA

OR

WA

MT

ID

NV

AZ

UT

WY

ND

SD

NE

KS

OK

NM

TX

CO

MN

IA

MO

AR

LA

IL

IN

WI

MI

PA

OH

NJ

DE

KY

TN

MS

AL

GA

FL

NC

SC

VA

WV

MD

RI

NY

ME

MA

VT

NH

CT

CRE

Loans owned

and/or managed by Jupiter

Communities and/or CRP |

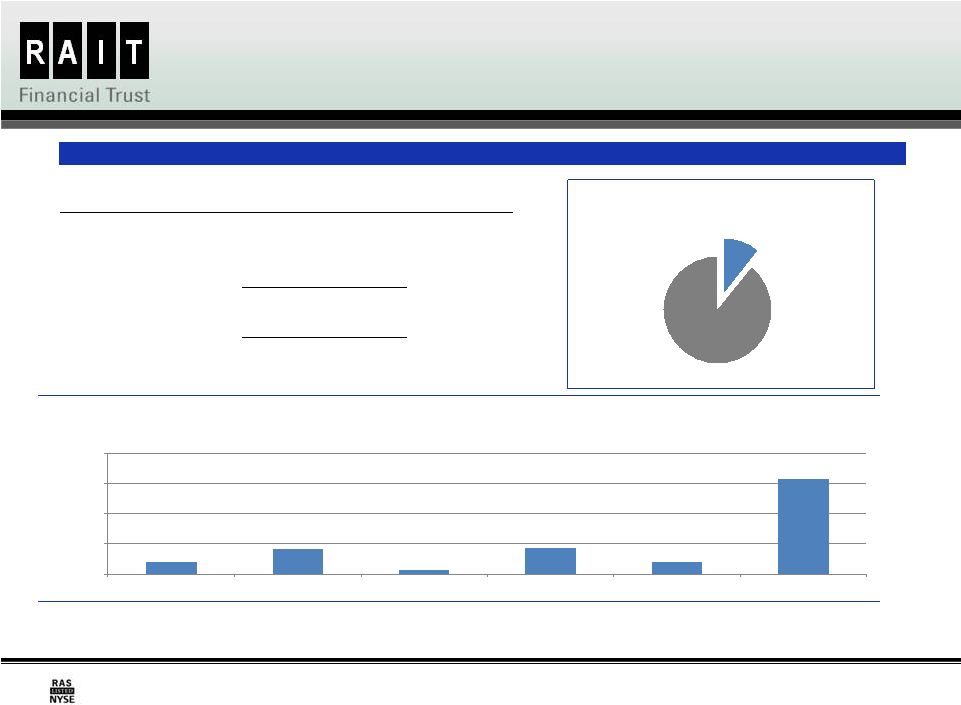

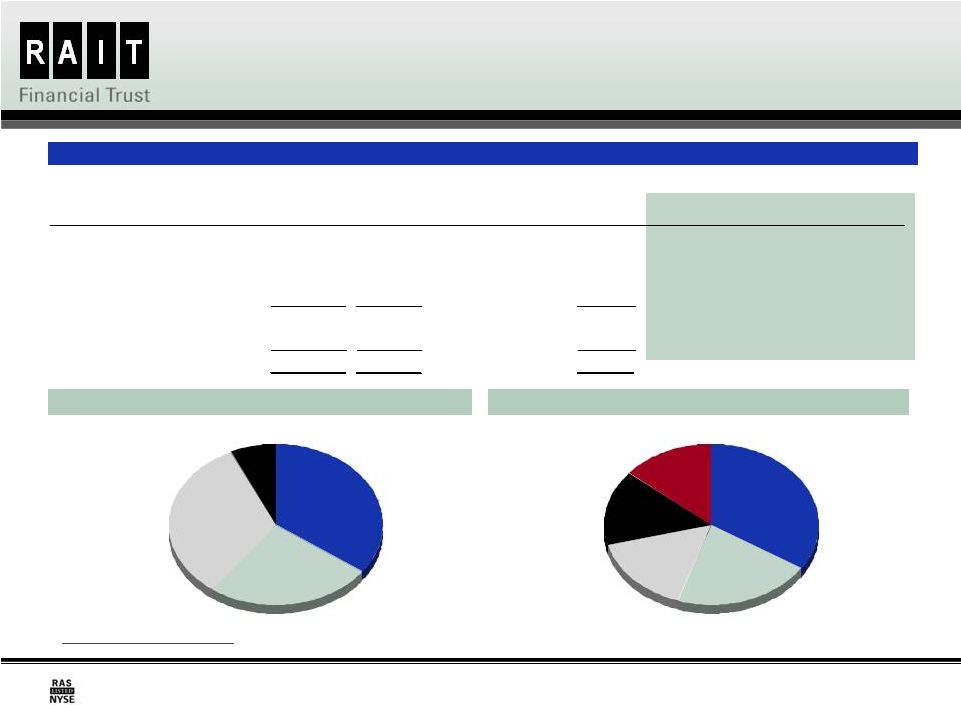

Recourse Debt

Summary – 6/3/2011

RAIT’s recourse indebtedness represents a manageable 10% of total

indebtedness $20,040

$40,913

$7,245

$43,000

$19,381

$158,771

$-

$50,000

$100,000

$150,000

$200,000

2011

2012 (3)

2013

2014

2015

Thereafter

Recourse Debt Maturities

(in 000's)

Recourse

10%

Non-

recourse

90%

Debt Breakdown

Description

Unpaid Principal

Balance

Weighted-

Average

Interst Rate

Contractual Maturity

Recourse Indebtedness:

7.0% convertible senior notes (1)

115,000

$

7.0%

Apr. 2031

6.875% convertible senior notes (2)

40,913

6.9%

Apr. 2027

Secured credit facilities

20,040

4.5%

Dec. 2011

Senior secured notes

43,000

12.5%

Apr. 2014

First mortgage on real estate owned

7,245

5.0%

Sept. 2013

Toal senior recourse indebtedness

226,198

$

7.7%

TRUPS

38,052

5.2%

Oct. 2015 to Mar. 2035

TRUPS

25,100

7.7%

Apr. 2037

Total junior recourse indebtedness

63,152

$

6.2%

($ in 000s)

7

(1) Our 7.0% convertible senior notes are redeemable, at par at the option of the holder, in April 2016,

April 2021, and April 2026. (2) Our 6.875% convertible senior notes are redeemable, at par at the option of the holder, in April

2012, April 2017, and April 2022. (3) Assumes full exercise of our 6.875% convertible senior notes redemption right in April 2012.

|

Recent

Performance Positioned

for

Growth

Improving

Cash Flow

Improved

Asset

Performance

8

Reduced

Leverage &

Operating

Costs

Reduced debt to equity ratio to 2.1x from a peak of

7.4x in June 2009

Reduced recourse debt by $105 million in 2010 &

$45.9 million in 2011

Debt reduction has resulted in significant cash savings

CRE securitizations remain fully cash-flowing and

performance test coverage ratios continue to improve

Declared regular quarterly common dividend of $0.06

per share, split-adjusted, effective in July 2011

Increasing occupancy and rental rates in all property

types

Increased 2010 net operating income from owned real

estate year-over-year |

9

2011 Strategic Initiatives:

CRE Lending

Commercial Real Estate Lending

Capitalize

on

existing,

scalable

platform

and

internal

expertise

to

originate Bridge and CMBS loans of $5 million to $30 million on stable

multi-family, office, retail and light industrial properties

Growing pipeline; repayment flows increasing

Lending capacity within CRE securitizations

Spread expansion opportunities

Fee

income

opportunities

–

originating,

securitizing,

managing

Sourcing

capital

for

future

growth

–

lines

of

credit,

JV,

warehouse,

debt

&

other sources |

10

2011 Strategic Initiatives:

Direct Real Estate

Directly Owned Real Estate Portfolio

Maximize value over time through increasing occupancy and higher

rental rates

Assets acquired below borrower’s cost

Asset value creation opportunity

Increasing rental income

Invested approximately $20.8 million in capital expenditures to reposition

the portfolio

Jupiter

Communities

–

internal

multi-family

property

manager

CRP

Commercial

Services

–

internal

office

property

manager |

11

2011 Strategic Initiatives:

Non-Traded REITs

New Non-Traded REIT Platform Leverages RAIT’s Real Estate

Expertise

Independence

Realty

Trust,

Inc.

(“IRT”)

-

Non-Traded

REIT

Acquisition

-

acquired on January 20, 2011

RAIT will serve as external manager & advisor

Target asset class: multi-family

Fee stream

»

.75 bps on average invested assets

»

1% 3

rd

party financing coordination fee

»

4% of revenue property management fee (Jupiter Communities)

»

Expense reimbursement

»

Back-end promote structure

RAIT equity investment pari passu with returns to IRT equity investors

Target maximum equity raise: $1 billion

Expect registration statement to be effective in Q2 2011

Raise capital through retail Broker/Dealer & financial advisor networks

65% maximum aggregate leverage

Any disclosure relating to IRT is neither an offer nor a solicitation to purchase

securities issued by IRT |

12

Experienced

Management Team

Diversified Real Estate

Platform

Creating Shareholder

Value is Key to our

Success

Access to Capital for

Growth

Cash Distributions

Growth & Income

Focus

Cornerstones for Success–Why Invest ? |

13

Appendix |

14

Key Statistics –

3/31/2011

March 31,

2011

December

31, 2010

September

30, 2010

June 30,

2010

March 31,

2010

Financial Statistics:

Assets under management

$3,822,534

$3,837,526

$3,901,342

$4,014,556

$9,911,824

Debt to equity ratio

2.1x

2.3x

2.6x

2.7x

2.8x

Total revenue

$58,279

$59,057

$58,899

$60,370

$66,244

Recourse debt maturing in one year

$20,040

$41,489

$7,919

$9,919

$10,905

Earnings per share – diluted

$0.05

$0.29

$0.16

$0.27

$0.41

Commercial Real Estate (“CRE”) Loan

Portfolio:

CRE loans-- unpaid principal

$1,149,169

$1,173,141

$1,216,875

$1,288,466

$1,305,816

Non-accrual loans -- unpaid principal

$121,054

$122,306

$143,212

$131,377

$132,978

Non-accrual loans as a % of reported

loans

10.5%

10.4%

11.8%

10.2%

10.2%

Reserve for losses

$58,809

$61,731

$73,029

$70,699

$68,850

Reserves as a % of non-accrual loans

48.6%

50.5%

51.0%

53.8%

51.8%

Provision for losses

$1,950

$2,500

$10,813

$7,644

$17,350

CRE Property Portfolio:

Reported investments in real estate

$867,726

$841,488

$823,881

$803,548

$795,952

Number of properties owned

48

47

47

47

46

Multifamily units owned

8,311

8,311

8,231

7,893

7,893

Office square feet owned

1,786,908

1,632,978

1,634,997

1,732,626

1,550,401

Retail square feet owned

1,116,063

1,116,112

1,069,588

1,069,588

1,069,652

Average occupancy data:

Multifamily

88.0%

85.5%

84.6%

83.5%

78.0%

Office

70.7%

67.8%

52.5%

55.5%

54.2%

Retail

56.3%

58.8%

57.7%

58.7%

60.1%

Total

82.4%

79.2%

74.8%

74.4%

70.8%

(Not split-adjusted; dollars in thousands, except share and per share

amounts) |

15

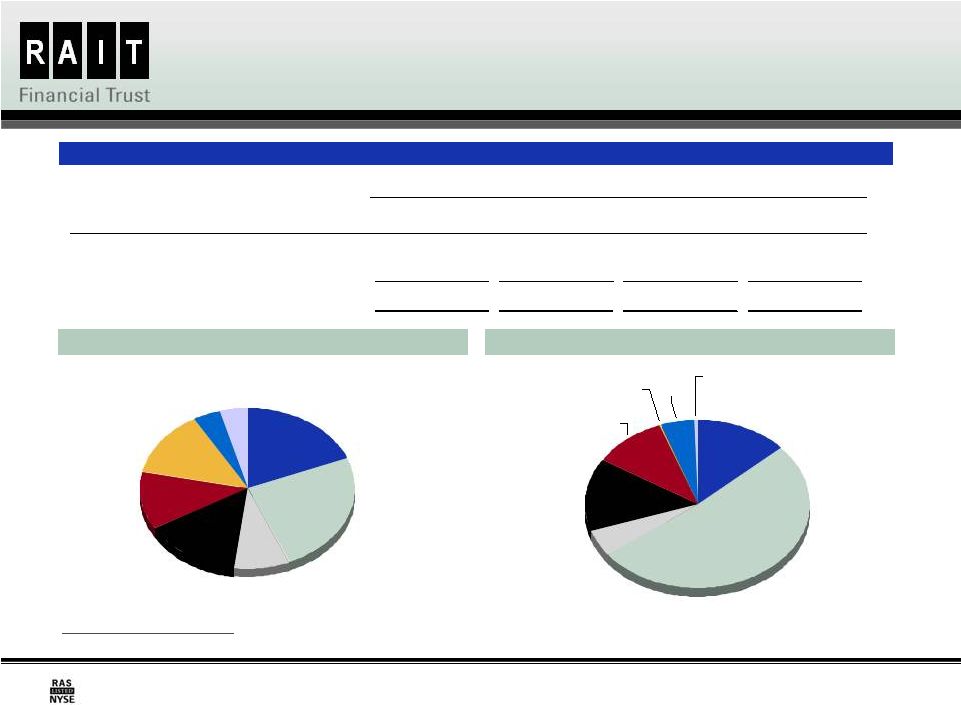

Commercial Real Estate Portfolio:

Loan Portfolio Statistics –

3/31/2011

By Property Type

(1)

(1) Based on book value.

By Geographic Region

(1)

Book Value

Weighted-

Average

Coupon

Range of Maturities

Number

of Loans

Key Statistics

Q1 2011

Q4 2010

Commercial Real Estate (CRE) Loans

Non-accrual loans

$121,054

$122,306

Commercial mortgages

$688,527

6.7%

May 2011 to Dec. 2020

42

% change

(1%)

Mezzanine loans

352,809

9.2%

May 2011 to Nov. 2038

103

Reserve for losses

58,809

61,731

Preferred equity interests

89,616

10.1%

Nov. 2011 to Aug. 2025

23

% change

(5%)

Total CRE Loans

$1,130,952

7.8%

168

Provision for losses

1,950

2,500

Other loans

61,321

6.7%

May 2011 to Oct. 2016

5

% change

(22%)

Total investments in loans

$1,192,273

7.7%

173

($ in 000s)

Improved credit performance of the loan portfolio

Mid Atlantic

21%

Southeast

16%

Northeast

14%

West

15%

Central

34%

Retail

25%

Office

33%

Other

7%

Multi-family

35% |

16

Commercial Real Estate Portfolio:

Owned Real Estate Statistics –

3/31/2011

Net Real Estate Operating Income

Occupancy Rates by Property Type

Average Physical Occupancy

Investments

in Real

Estate

Quantity

Number of

Properties

3/31/211

12/31/2010

Q1 2011

Q4 2010

Multi-family real estate properties

$570,849

8,311 units

33

88%

86%

$673

$681

Office real estate properties

226,800

1,786,908 sq. ft.

10

71%

68%

17.88

18.00

Retail real estate properties

47,869

1,116,063 sq. ft.

2

56%

59%

9.71

9.40

Parcels of land

22,208

7.3 acres

3

–

–

–

–

Total

$867,726

48

82%

79%

($ in 000s)

(1) Investments in real estate include $48.9 million of assets held for sale

as of March 31, 2011. (2) Based on operating performance for the

respective quarters. (3) Average effective rent is rent per unit per

month. (4) Average effective rent is rent per square foot per

year. Improved occupancy and net operating income

Q1 2011

Q4 2010

Rental income

$21,290

$20,170

Real estate operating expenses

(12,617)

(13,404)

Net Real Estate Operating Income

$8,673

$6,766

Number of owned properties

48

47

Occupancy

82%

79%

78%

84%

85%

86%

88%

54%

56%

53%

68%

71%

60%

59%

58%

59%

56%

71%

74%

75%

79%

82%

40%

50%

60%

70%

80%

90%

100%

Q12010

Q22010

Q32010

Q42010

Q12011

Multi-family

Office

Retail

Total

(1)(3)

(4)

(4)

(2)

Average Effective Rent

(1) |

17

Balance Sheet –

3/31/2011

(Not split-adjusted; dollars in thousands, except share and per share

amounts) As of

March 31,

2011

As of

December 31,

2010

Assets

Investments in mortgages and loans, at amortized cost:

Commercial

mortgages,

mezzanine

loans,

other

loans

and

preferred

equity

interests

$ 1,190,576

$

1,219,110

Allowance for losses

(66,769)

(69,691)

Total investments in mortgages and loans

1,123,807

1,149,419

Investments in real estate

867,726

841,488

Investments in securities and security-related receivables, at fair value

718,937

705,451

Cash and cash equivalents

39,463

27,230

Restricted cash

179,308

176,723

Accrued interest receivable

Other assets

Deferred financing costs, net of accumulated amortization of $10,559 and

$9,943, respectively

Intangible assets, net of accumulated amortization of $1,917 and

$1,777, respectively

Total assets

Liabilities and Equity

Indebtedness:

Recourse indebtedness

Non-recourse indebtedness

Total indebtedness

Accrued interest payable

Accounts payable and accrued expenses

Derivative liabilities

Deferred

taxes,

borrowers’

escrows

and

other

liabilities

Total liabilities

Equity:

Shareholders’

equity:

Preferred shares, $0.01 par value per share, 25,000,000 shares authorized;

7.75% Series A cumulative redeemable preferred shares, liquidation preference

$25.00 per share, 2,760,000 shares issued and outstanding

8.375% Series B cumulative redeemable preferred shares, liquidation preference

$25.00 per share, 2,258,300 shares issued and outstanding

8.875% Series C cumulative redeemable preferred shares, liquidation preference

$25.00 per share, 1,600,000 shares issued and outstanding

Common shares, $0.01 par value per share, 200,000,000 shares authorized,

114,083,141 and 105,900,570 issued and outstanding

Additional paid in capital

Accumulated other comprehensive income (loss)

Retained earnings (deficit)

Total

shareholders’

equity

Noncontrolling interests

Total equity

Total liabilities and equity

$ 3,029,363

2,993,432

$

37,764

37,138

6,346

32,840

22,963

19,954

3,049

3,189

$ 3,029,363

$

2,993,432

$ 277, 891

$

293,357

1,552,726

1,544,820

1,830,617

1,838,177

20,444

19,925

25,495

25,089

164,127

184,878

20,852

6,833

2,061,535

2,074,902

28

23

16

1,141

1,060

1,721,730

1,691,681

(114,514)

(127,602)

(644,562)

(647,110)

963,862

918,096

3,966

434

967,828

918,530

28

23

16 |

18

Consolidated Statements of Operations

(Not split-adjusted; dollars in thousands, except share and per share

amounts) For the Three-Month

Periods Ended

March 31

20

11

2010

Revenue:

Interest income

$ 33,558

$ 41,330

Rental income

21,290

16,075

Fee and other income

3,431

8,839

Total revenue

58,279

66,244

Expenses:

Interest expense

23,367

25,470

Real estate operating expense

12,617

10,522

Compensation expense

6,544

8,052

General and administrative expense

4,968

4,890

Provision for loan losses

1,950

17,350

Depreciation and amortization

7,119

6,223

Total expenses

56,565

72,467

Operating income

1,714

(6,223)

Interest and other income (expense)

83

82

Gains (losses) on sale of assets

1,415

3,924

Gains (losses) on extinguishment of debt

(537)

19,810

Change in fair value of financial instruments

5,611

16,437

Income (loss) before taxes and discontinued operations

8,286

34,030

Income tax benefit (provision)

54

(47)

Income (loss) from continuing operations

8,340

Income (loss) from discontinued operations

791

470

Net income (losss)

9,131

34,453

(Income) loss allocated to preferred shares

(3,414)

(3,406)

(Income)

loss

allocated

to

noncontrolling

interests

50

235

Net income (loss) allocable to common shares

$

$ 31,282

Earnings (loss) per share—Basic:

Continuing operations

$ 0.04

$ 0.41

Discontinued operations

0.01

0.01

Total earnings (loss) per share—Basic

$ 0.05

$ 0.42

Weighted-average shares outstanding—Basic

74,952,313

Earnings (loss) per share—Diluted:

Continuing operations

$ 0.04

$ 0.40

Discontinued operations

0.01

0.01

Total earnings (loss) per share—Diluted

$ 0.05

$ 0.41

Weighted-average shares outstanding—Diluted

110,904,359

75,512,999

5,767

109,856,729

33,983 |

19

Adjusted Funds From Operations

(Not split-adjusted; dollars in thousands, except share and per share

amounts) For the Three-Months Periods

Ended March 31

2011

2010

Funds From Operations (“FFO”) (1):

Net income (loss) allocable to common

shares.................................. $ 5,767

$

31,282

Adjustments:

Depreciation

expense...............................................................

6,570

6,003

(Gains) Losses on sale of real

estate........................................ (266)

Funds from

operations........................................................................

$ 12,337

$ 37,019

Funds from Operations per

share.......................................................

$ 0.11

$ 0.49

Weighted-average

shares -

diluted

110,904,359

75,512,999

Adjusted Funds From Operations (“AFFO”) (1):

Funds from

Operations........................................................................

$ 12,337

$

37,019

Adjustments:

Change in fair value of financial instruments..............................

(5,611)

(16,437)

(Gains) Losses on debt extinguishment......................................

537

(19,810)

Capital expenditures, net of direct

financing................................ (362)

(158)

Straight-line rental

adjustments.................................................. (919)

(26)

Amortization of deferred items and intangible assets..................

673

(1)

Share-based

compensation.........................................................

259

1,671

Adjusted Funds from

Operations..........................................................

$ 6,914

$ 2,258

Adjusted Funds from Operations per

share...........................................

$ 0.06

$ 0.03

Weighted-average

shares

-

diluted

110,904,359

75,512,999

-

(1) We believe that funds from operations, or FFO, and adjusted funds from operations, or AFFO,

each of which are non-GAAP measures, are additional appropriate measures of the operating performance of a REIT and us in particular. We compute FFO in accordance with the standards

established by the National Association of Real Estate Investment Trusts, or NAREIT, as net income or

loss allocated to common shares (computed in accordance with GAAP), excluding real estate-related depreciation and amortization expense, gains or losses on sales of real estate and the

cumulative effect of changes in accounting principles. AFFO is a computation made by analysts and

investors to measure a real estate company's cash flow generated by operations. We calculate AFFO by adding to or subtracting from FFO: change in fair value of financial instruments; gains

or losses on debt extinguishment; capital expenditures, net of any direct financing associated with

those capital expenditures; straight-line rental effects; amortization of various deferred items and intangible assets; and share-based compensation. Our calculation of AFFO differs from the

methodology used for calculating AFFO by certain other REITs and, accordingly, our AFFO may not be

comparable to AFFO reported by other REITs. Our management utilizes FFO and AFFO as measures of our operating performance, and believes they are also useful to investors, because

they facilitate an understanding of our operating performance after adjustment for certain non-cash

items, such as real estate depreciation, share-based compensation and various other items required by GAAP that may not necessarily be indicative of current operating performance and that

may not accurately compare our operating performance between periods. Furthermore, although FFO, AFFO

and other supplemental performance measures are defined in various ways throughout the REIT industry, we also believe that FFO and AFFO may provide us and our investors with

an additional useful measure to compare our financial performance to certain other REITs.

Neither FFO nor AFFO is equivalent to net income or cash generated from operating activities determined in accordance with U.S. GAAP. Furthermore, FFO and AFFO do not represent amounts

available for management's discretionary use because of needed capital replacement or expansion, debt

service obligations or other commitments or uncertainties. Neither FFO nor AFFO should be considered as an alternative to net income as an indicator of our operating performance or as

an alternative to cash flow from operating activities as a measure of our liquidity.

References to “we”, “us”, and “our” refer to RAIT Financial Trust and its subsidiaries.

|

20

Investment in Debt Securities Issued by Real

Estate Companies –

3/31/2011

TruPS and Subordinated Debentures by Industry Sector

(1)

(1) Based on estimated fair value.

(2) S&P Ratings as of March 31, 2011.

Other Securities by Ratings Distribution

(1)(2)

As of March 31, 2011

Investment Description

Estimated Fair

Value

Amortized Cost

Weighted-Average

Coupon

Weighted Average

Years to Maturity

TruPS and Subordinated Debentures

$546,081

$801,700

5.2%

21.9

Other securities

172,856

312,560

4.9%

27.3

Total

$718,937

$1,114,260

5.2%

23.4

($ in 000s)

RAIT earns senior management fees from the legacy Taberna portfolio

Office

25%

Residential

Mortgage

8%

Specialty

Finance

15%

Retail

13%

Hospitality

4%

Homebuilders

12%

Storage

4%

Commercial

Mortgage

19%

BBB

51%

BB

5%

B

14%

AAA

5%

D

0%

CCC

11%

AA

1%

A

13% |