Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - Fifth Street Asset Management Inc. | fsam-ex322_2017093010xq.htm |

| EX-32.1 - EXHIBIT 32.1 - Fifth Street Asset Management Inc. | fsam-ex321_2017093010xq.htm |

| EX-31.2 - EXHIBIT 31.2 - Fifth Street Asset Management Inc. | fsam-ex312_2017093010xq.htm |

| EX-31.1 - EXHIBIT 31.1 - Fifth Street Asset Management Inc. | fsam-ex311_2017093010xq.htm |

| EX-10.11 - EXHIBIT 10.11 - Fifth Street Asset Management Inc. | fsam-ex1011_2017093010xq.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

Form 10-Q

(Mark One)

þ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) | ||

OF THE SECURITIES EXCHANGE ACT OF 1934 | |||

For the quarterly period ended September 30, 2017

OR

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) | ||

OF THE SECURITIES EXCHANGE ACT OF 1934 | |||

COMMISSION FILE NUMBER: 001-36701

Fifth Street Asset Management Inc.

(EXACT NAME OF REGISTRANT AS SPECIFIED IN ITS CHARTER)

DELAWARE | 46-5610118 | |

(State or jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

777 West Putnam Avenue, 3rd Floor Greenwich, CT | 06830 | |

(Address of principal executive office) | (Zip Code) | |

REGISTRANT'S TELEPHONE NUMBER, INCLUDING AREA CODE:

(203) 681-3600

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter periods as the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES þ NO ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES þ NO ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer o | Accelerated filer o | Non-accelerated filer o | Smaller reporting company þ | |||

(Do not check if a smaller reporting company) | ||||||

Emerging growth company þ | ||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act þ | ||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act) YES ¨ NO þ

The number of shares of the registrant's Class A common stock, par value $0.01 per share, outstanding as of November 14, 2017 was 20,332,868. The number of shares of the registrant's Class B common stock, par value $0.01 per share, outstanding as of November 14, 2017 was 30,715,668.

TABLE OF CONTENTS

Item 1. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

Item 1. | ||

Item 1A. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

Item 5. | ||

Item 6. | ||

FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q may contain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the "Securities Act"), and Section 21E of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), that reflect our current views with respect to, among other things, future events and financial performance. Words such as "outlook," "believes," "expects," "potential," "continues," "may," "will," "should," "seeks," "approximately," "predicts," "intends," "plans," "estimates," "anticipates" or the negative version of those words or other comparable words indicate forward-looking statements, although not all forward-looking statements include these words. The forward-looking statements in this Quarterly Report on Form 10-Q are subject to various risks and uncertainties and assumptions relating to our operations, financial results, financial condition, business prospects and liquidity. Our actual results may vary materially from those indicated in these forward-looking statements, including as a result of the factors described under "Risk Factors" in this Quarterly Report on Form 10-Q and in "Item 1A. Risk Factors" in our Annual Report on Form 10-K for the year ended December 31, 2016, as such factors may be updated from time to time in our periodic filings with the Securities and Exchange Commission (the "SEC"), which are accessible on the SEC's website at www.sec.gov. Other factors that could cause actual results to differ materially include: risks associated with our proposed dissolution and liquidation, changes in the economy, financial markets and political environment; risks associated with possible disruption in the economy generally due to terrorism or natural disasters; the timing of release of amounts subject to escrow pursuant to the Asset Purchase Agreement, dated as of July 13, 2017 by and among Fifth Street Management LLC, Oaktree Capital Management, L.P., and, for certain limited purposes, Fifth Street Asset Management Inc. and Fifth Street Holdings L.P., and the carrying value of certain assets and liabilities after the closing of the transaction with Oaktree Capital Management, L.P.; future changes in laws or regulations (including the interpretation of these laws and regulations by regulatory authorities); our ability to pay dividends to our stockholders; and other considerations that may be disclosed from time to time in our publicly disseminated documents and filings. New risks and uncertainties arise over time, and it is not possible for us to predict those events or how they may affect us. Therefore, you should not place undue reliance on these forward-looking statements. Any forward-looking statement speaks only as of the date on which it is made. Although we do not undertake any obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise, except as required by law you are advised to consult any additional disclosures that we may make directly to you or through reports that we in the future may file with the SEC, including annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K.

Unless the context otherwise requires, references to "we," "us," "our" and "the Company" are intended to refer to the business and operations of Fifth Street Asset Management Inc. and its consolidated subsidiaries.

When used in this Quarterly Report on Form 10-Q, unless the context otherwise requires:

• | "base management fees" refer to fees we earn for advisory services provided to our funds, which are generally based on a fixed percentage of fair value of assets, total commitments, invested capital, net asset value, total assets or principal amount of the investment portfolios managed by us; |

• | "catch-up" refers to a provision for a manager or adviser of a fund to receive the majority or all of the profits of such fund until the agreed upon profit allocation is reached; |

• | "CLO" refers to a collateralized loan obligation; |

• | “CLO I” refers to Fifth Street Senior Loan Fund I, LLC, a CLO in our senior loan fund strategy managed by CLO Management prior to its sale to NewStar Financial Inc. ("NewStar Financial"); |

• | "CLO II" refers to Fifth Street SLF II, Ltd. (formerly Fifth Street Senior Loan Fund II, LLC, prior to securitization), a CLO in our senior loan fund strategy managed by CLO Management prior to its sale to NewStar Financial; |

• | "CLO Management" refers to Fifth Street CLO Management LLC, the collateral manager for CLO I and CLO II prior to its sale to NewStar Financial; |

• | "Fifth Street BDCs" and "our BDCs" refer to FSC and FSFR together; |

• | "Fifth Street Funds" and "our funds" refer to the Fifth Street BDCs and the other funds advised or managed by Fifth Street Management or CLO Management prior to its sale to NewStar; |

• | "Fifth Street Holdings" refers to Fifth Street Holdings L.P. |

• | "Fifth Street Management" or "FSM" refers to Fifth Street Management LLC and, unless the context otherwise requires, its subsidiaries; |

• | "FSC" refers to the publicly-traded business development company managed by Fifth Street Management and named Fifth Street Finance Corp. as of September 30, 2017; |

• | "FSFR" refers to the publicly-traded business development company managed by Fifth Street Management and named Fifth Street Senior Floating Rate Corp. as of September 30, 2017; |

i

• | "FSOF" refers to Fifth Street Opportunities Fund, L.P., a private fund managed by Fifth Street Management prior to its wind down; |

• | "Holdings Limited Partners" refers to active, limited partners in Fifth Street Holdings (other than the Company), which include, among other persons, the Principals; |

• | "hurdle rate" or "hurdle" refers to a specified minimum rate of return that a fund must exceed in order for the investment adviser or manager of such a fund to receive Part I Fees and/or performance fees; |

• | "management fees" refer to base management fees and Part I Fees; |

• | "MMKT" refers to MMKT Exchange LLC, a financial technology company in which FSM owned 80% of the common membership interests prior to dissolution and “MMKT Notes” refers to the convertible promissory notes issued by MMKT to the Company and additional investors that were cancelled and settled pursuant to an agreement among MMKT and its noteholders entered into on August 8, 2016; |

• | "Part I Fees" refer to fees paid to us by our BDCs that are based on a fixed percentage of pre-incentive fee net investment income (subject, in the case of FSC, to certain limitations based on cumulative net increase in net assets resulting from operations), which are calculated and paid quarterly, and subject to certain specified performance hurdles. Part I Fees are classified as management fees as they are generally predictable and are recurring in nature, are not subject to repayment (or clawback) and are generally cash-settled each quarter; |

• | "Part II Fees" refer to fees paid to us by our BDCs that are based on net capital gains, which are paid annually; |

• | "performance fees" refer to fees we earn based on the performance of a fund, which are generally based on certain specific hurdle rates as defined in the fund's investment management or partnership agreements, may be either an incentive fee or carried interest, are paid annually and also include Part II Fees; |

• | "permanent capital" refers to capital of funds that do not have redemption provisions or a requirement to return capital to investors upon exiting the investments made with such capital, except as required by applicable law, which funds currently consisted of FSC and FSFR as of September 30, 2017; such funds may be required to distribute all or a portion of capital gains and investment income or elect to distribute capital; |

• | "Principals" refers to Leonard M. Tannenbaum and Bernard D. Berman and, where applicable, any entities controlled directly or indirectly by them; |

• | "SMA" means a separately managed account; and |

• | "TRA recipients" refers to the Principals and Ivelin M. Dimitrov. |

Amounts and percentages throughout this Quarterly Report on Form 10-Q may reflect rounding adjustments and consequently totals may not appear to sum.

ii

PART I - FINANCIAL INFORMATION

Item 1. Consolidated Financial Statements

Fifth Street Asset Management Inc.

Consolidated Statements of Financial Condition

September 30, 2017 | December 31, 2016 | |||||||

Assets | (unaudited) | (unaudited) | ||||||

Cash and cash equivalents | $ | 5,742,975 | $ | 6,727,085 | ||||

Management fees receivable (includes Part I Fees of $815,491 and $4,837,944 as of September 30, 2017 and December 31, 2016, respectively) | 8,986,275 | 15,346,566 | ||||||

Performance fees receivable | — | 123,300 | ||||||

Insurance recovery receivable | — | 9,250,000 | ||||||

Escrow receivable related to sale of CLO Management | 2,600,000 | — | ||||||

Prepaid expenses (includes $418,300 and $620,794 related to income taxes as of September 30, 2017 and December 31, 2016, respectively) | 1,586,792 | 2,073,393 | ||||||

Investments in equity method investees | 59,697,562 | 66,176,884 | ||||||

Beneficial interests in CLOs at fair value: (cost December 31, 2016: $24,138,496) | — | 23,155,062 | ||||||

Due from affiliates | 2,459,308 | 3,405,921 | ||||||

Fixed assets, net | 378,802 | 5,344,332 | ||||||

Deferred tax assets | 57,113,514 | 42,415,143 | ||||||

Deferred financing costs | — | 1,426,103 | ||||||

Other assets | 3,072,622 | 3,355,072 | ||||||

Total assets | $ | 141,637,850 | $ | 178,798,861 | ||||

Liabilities and Equity (Deficit) | ||||||||

Liabilities | ||||||||

Accounts payable and accrued expenses | $ | 14,477,440 | $ | 5,260,511 | ||||

Accrued compensation and benefits | 11,167,520 | 12,516,497 | ||||||

Reserve for expenses reimbursable to affiliates | 3,732,920 | — | ||||||

Income taxes payable | 33,693 | 223,694 | ||||||

Loans payable | 2,000,000 | 14,972,565 | ||||||

Legal settlement payable | — | 9,250,000 | ||||||

Credit facility payable (net of $598,400 of deferred financing costs at September 30, 2017) | 91,551,600 | 102,000,000 | ||||||

Dividends payable | 744,768 | 1,961,863 | ||||||

Due to affiliates | 26,358 | 30,412 | ||||||

Deferred rent liability | 1,927,941 | 2,079,354 | ||||||

Payable to related parties pursuant to tax receivable agreements | 49,483,760 | 35,990,255 | ||||||

Total liabilities | 175,146,000 | 184,285,151 | ||||||

Commitments and contingencies | ||||||||

Equity (deficit) | ||||||||

Preferred stock, $0.01 par value; 5,000,000 shares authorized; none issued and outstanding as of September 30, 2017 and December 31, 2016 | — | — | ||||||

Class A common stock, $0.01 par value; 500,000,000 shares authorized; 15,649,686 and 6,602,374 shares issued and outstanding as of September 30, 2017 and December 31, 2016, respectively | 156,497 | 66,024 | ||||||

Class B common stock, $0.01 par value; 50,000,000 shares authorized; 34,285,484 and 42,856,854 shares issued and outstanding as September of 30, 2017 and December 31, 2016, respectively | 342,855 | 428,569 | ||||||

Additional paid-in capital | 6,499,818 | 6,354,291 | ||||||

Accumulated deficit | (11,161,721 | ) | (1,726,061 | ) | ||||

Total stockholders' equity (deficit), Fifth Street Asset Management Inc. | (4,162,551 | ) | 5,122,823 | |||||

Non-controlling interests | (29,345,599 | ) | (10,609,113 | ) | ||||

Total deficit | (33,508,150 | ) | (5,486,290 | ) | ||||

Total liabilities and equity (deficit) | $ | 141,637,850 | $ | 178,798,861 | ||||

Management fees receivable, performance fees receivable and investments are with related parties. See notes to consolidated financial statements.

1

Fifth Street Asset Management Inc.

Consolidated Statements of Operations

(unaudited)

For the Three Months Ended September 30, | For the Nine Months Ended September 30, | ||||||||||||||||

2017 | 2016 | 2017 | 2016 | ||||||||||||||

Revenues | |||||||||||||||||

Management fees | $ | — | $ | 730,507 | $ | 922,187 | $ | 2,162,419 | |||||||||

Performance fees | — | 38,661 | — | 124,836 | |||||||||||||

Other fees | 7,336 | 55,092 | 7,336 | 170,241 | |||||||||||||

Total revenues | 7,336 | 824,260 | 929,523 | 2,457,496 | |||||||||||||

Expenses | |||||||||||||||||

Compensation and benefits | 4,897,425 | 1,159,255 | 8,666,014 | 5,257,631 | |||||||||||||

General, administrative and other expenses | 2,465,138 | 2,943,495 | 8,829,906 | 9,366,081 | |||||||||||||

Depreciation and amortization | 342,476 | 349,475 | 977,655 | 3,925,519 | |||||||||||||

Total expenses | 7,705,039 | 4,452,225 | 18,473,575 | 18,549,231 | |||||||||||||

Other income (expense) | |||||||||||||||||

Interest income | 95,867 | 386,626 | 725,340 | 1,082,368 | |||||||||||||

Interest expense | (46,778 | ) | (140,457 | ) | (344,062 | ) | (525,985 | ) | |||||||||

Income (loss) from equity method investments | (6,656,075 | ) | 1,576,215 | (2,016,009 | ) | 3,554,541 | |||||||||||

Unrealized loss on MMKT Notes | — | (2,582,405 | ) | — | — | ||||||||||||

Realized gain on settlement of MMKT Notes | — | 2,592,751 | — | 2,592,751 | |||||||||||||

Unrealized gain on beneficial interests in CLOs | 654,915 | 537,600 | 983,434 | 169,373 | |||||||||||||

Gain on extinguishment of debt | — | — | — | 2,000,000 | |||||||||||||

Gain on sale of CLO Management | 5,583,112 | — | 4,642,815 | — | |||||||||||||

Adjustment of TRA liability | 12,608,166 | — | 12,515,818 | 7,525,901 | |||||||||||||

Loss on impairment of fixed assets | (4,252,700 | ) | — | (4,252,700 | ) | — | |||||||||||

Other income (expense), net | — | (75,728 | ) | — | (620,514 | ) | |||||||||||

Total other income (expense), net | 7,986,507 | 2,294,602 | 12,254,636 | 15,778,435 | |||||||||||||

Income (loss) from continuing operations before provision for income taxes | 288,804 | (1,333,363 | ) | (5,289,416 | ) | (313,300 | ) | ||||||||||

Provision for income taxes | 16,423,914 | 672,108 | 15,851,288 | 6,481,489 | |||||||||||||

Net loss from continuing operations | (16,135,110 | ) | (2,005,471 | ) | (21,140,704 | ) | (6,794,789 | ) | |||||||||

Net income (loss) from discontinued operations, net of tax | (11,578,691 | ) | 12,185,290 | (1,727,678 | ) | 10,051,045 | |||||||||||

Net income (loss) | (27,713,801 | ) | 10,179,819 | (22,868,382 | ) | 3,256,256 | |||||||||||

Net (income) loss attributable to non-controlling interests | 17,585,079 | (10,417,537 | ) | 13,432,722 | (3,878,297 | ) | |||||||||||

Net loss attributable to Fifth Street Asset Management Inc. | $ | (10,128,722 | ) | $ | (237,718 | ) | $ | (9,435,660 | ) | $ | (622,041 | ) | |||||

Basic and diluted income (loss) per share: | |||||||||||||||||

Loss from continuing operations | $ | (0.49 | ) | $ | (0.47 | ) | $ | (0.57 | ) | $ | (0.01 | ) | |||||

Income (loss) from discontinued operations | (0.16 | ) | 0.43 | (0.04 | ) | (0.10 | ) | ||||||||||

Net loss attributable to Fifth Street Asset Management Inc. | $ | (0.65 | ) | $ | (0.04 | ) | $ | (0.61 | ) | $ | (0.11 | ) | |||||

Weighted average shares of Class A common stock outstanding - basic and diluted | 15,649,686 | 5,908,407 | 15,498,388 | 5,847,139 | |||||||||||||

2

Fifth Street Asset Management Inc.

Consolidated Statement of Changes in Equity (Deficit)

For the Nine Months Ended September 30, 2017 and 2016

(unaudited)

Class A Common Stock | Class B Common Stock | Additional Paid-in Capital | Accumulated Deficit | Treasury Stock | Non-Controlling Interests | Total Equity (Deficit) | ||||||||||||||||||||||||||||

Shares | Amount | Shares | Amount | |||||||||||||||||||||||||||||||

Balance, December 31, 2015 | 5,822,672 | $ | 58,227 | 42,856,854 | $ | 428,569 | $ | 2,661,253 | $ | (30,905 | ) | $ | (180,064 | ) | $ | (5,392,371 | ) | $ | (2,455,291 | ) | ||||||||||||||

Cumulative effect of ASU 2016-09 adoption | — | — | — | — | 145,127 | (164,081 | ) | — | (160,023 | ) | (178,977 | ) | ||||||||||||||||||||||

Paid and accrued dividends - $0.30 per Class A common share | — | — | — | — | (1,824,330 | ) | — | — | — | (1,824,330 | ) | |||||||||||||||||||||||

Paid and accrued dividends on restricted stock units | — | — | — | — | (35,131 | ) | — | — | (264,359 | ) | (299,490 | ) | ||||||||||||||||||||||

Issuance of shares in connection with vesting of RSUs | 43,701 | 437 | — | — | — | — | — | — | 437 | |||||||||||||||||||||||||

Issuance of shares to settle derivative liability | 760,059 | 7,601 | — | — | 3,259,559 | — | — | — | 3,267,160 | |||||||||||||||||||||||||

Retirement of Class A common stock | (24,058 | ) | (241 | ) | — | — | (179,823 | ) | — | 180,064 | — | — | ||||||||||||||||||||||

Deemed capital contribution | — | — | — | — | 676,617 | — | — | 5,134,177 | 5,810,794 | |||||||||||||||||||||||||

Distributions to members | — | — | — | — | — | — | — | (11,373,105 | ) | (11,373,105 | ) | |||||||||||||||||||||||

Reallocation of equity for changes in ownership interest | — | — | — | — | (3,070,991 | ) | — | — | 3,070,991 | — | ||||||||||||||||||||||||

Amortization of equity-based compensation | — | — | — | — | 500,340 | — | — | 5,711,713 | 6,212,053 | |||||||||||||||||||||||||

Net income (loss) | — | — | — | — | — | (622,041 | ) | — | 3,878,297 | 3,256,256 | ||||||||||||||||||||||||

Balance, September 30, 2016 | 6,602,374 | $ | 66,024 | 42,856,854 | $ | 428,569 | $ | 2,132,621 | $ | (817,027 | ) | $ | — | $ | 605,320 | $ | 2,415,507 | |||||||||||||||||

Class A Common Stock | Class B Common Stock | Additional Paid-in Capital | Accumulated Deficit | Non-Controlling Interests | Total Deficit | |||||||||||||||||||||||||

Shares | Amount | Shares | Amount | |||||||||||||||||||||||||||

Balance, December 31, 2016 | 6,602,374 | $ | 66,024 | 42,856,854 | $ | 428,569 | $ | 6,354,291 | $ | (1,726,061 | ) | $ | (10,609,113 | ) | $ | (5,486,290 | ) | |||||||||||||

Dividends paid - $0.125 per Class A common share | — | — | — | — | (1,947,078 | ) | — | — | (1,947,078 | ) | ||||||||||||||||||||

Accrued dividends on restricted stock units | — | — | — | — | 40,701 | — | 92,746 | 133,447 | ||||||||||||||||||||||

Issuance of shares in connection with previously vested RSUs | 274,862 | 2,749 | — | — | (2,749 | ) | — | — | — | |||||||||||||||||||||

Issuance of Class A common stock and cancellation of Class B common stock in connection with exchange of Holdings LP Interests | 8,772,450 | 87,724 | (8,571,370 | ) | (85,714 | ) | (2,010 | ) | — | — | — | |||||||||||||||||||

Distributions to Holdings Limited Partners | — | — | — | — | — | — | (12,940,843 | ) | (12,940,843 | ) | ||||||||||||||||||||

Reallocation of equity for changes in ownership interest | — | — | — | — | (3,645,212 | ) | — | 3,645,212 | — | |||||||||||||||||||||

Amortization of equity-based compensation | — | — | — | — | 1,111,995 | — | 3,899,121 | 5,011,116 | ||||||||||||||||||||||

Net tax benefit in connection with TRA | — | — | — | — | 4,589,880 | — | — | 4,589,880 | ||||||||||||||||||||||

Net loss | — | — | — | — | — | (9,435,660 | ) | (13,432,722 | ) | (22,868,382 | ) | |||||||||||||||||||

Balance, September 30, 2017 | 15,649,686 | $ | 156,497 | 34,285,484 | $ | 342,855 | $ | 6,499,818 | $ | (11,161,721 | ) | $ | (29,345,599 | ) | $ | (33,508,150 | ) | |||||||||||||

See notes to consolidated financial statements.

3

Fifth Street Asset Management Inc.

Consolidated Statements of Cash Flows

(unaudited)

For the Nine Months Ended September 30, | |||||||||

2017 | 2016 | ||||||||

Cash flows from operating activities | |||||||||

Net loss | $ | (21,140,704 | ) | $ | (6,794,789 | ) | |||

Adjustments to reconcile net loss to net cash provided by (used in) operating activities: | |||||||||

Depreciation and amortization | 765,335 | 3,713,200 | |||||||

Amortization of fractional interests in aircrafts | 212,320 | 212,319 | |||||||

Realized gain on sale of CLO Management | (4,642,815 | ) | — | ||||||

Amortization of equity-based compensation | 1,740,859 | 1,858,102 | |||||||

Write-off of MMKT capitalized software costs | — | 624,512 | |||||||

Unrealized (gain) loss on beneficial interests in CLOs | (983,434 | ) | (169,373 | ) | |||||

Distributions of earnings from equity method investments | 1,017,458 | 3,059,289 | |||||||

Interest income accreted on beneficial interest in CLOs | (725,321 | ) | (1,082,342 | ) | |||||

Loss on impairment of fixed assets | 4,252,700 | — | |||||||

Interest expense on MMKT Notes | — | 92,119 | |||||||

Deferred taxes | 15,900,832 | 8,276,868 | |||||||

Deferred rent | (151,413 | ) | (1,035,401 | ) | |||||

Realized gain on MMKT Notes | — | (2,592,751 | ) | ||||||

Loss on lease abandonment | — | 1,240,928 | |||||||

Gain on extinguishment of debt | — | (2,000,000 | ) | ||||||

Adjustment of TRA liability | (12,515,818 | ) | (7,525,901 | ) | |||||

(Income) loss from equity method investments | 2,016,009 | (3,554,541 | ) | ||||||

Changes in operating assets and liabilities: | |||||||||

Management fees receivable | 536,506 | (55,947 | ) | ||||||

Performance fees receivable | — | 21,062 | |||||||

Escrow receivable related to sale of CLO Management | (2,600,000 | ) | — | ||||||

Prepaid expenses | 486,601 | (1,723,695 | ) | ||||||

Due from affiliates | 408,119 | (535,519 | ) | ||||||

Other assets | 70,130 | 433,531 | |||||||

Accounts payable and accrued expenses | 4,216,929 | 832,003 | |||||||

Accrued compensation and benefits | (1,348,977 | ) | (2,301,078 | ) | |||||

Income taxes payable | (190,001 | ) | (28,559 | ) | |||||

Due to affiliates | — | 4,314 | |||||||

Net cash provided by (used in) continuing operating activities | (12,674,685 | ) | (9,031,649 | ) | |||||

Net cash provided by discontinued operating activities | 17,834,248 | 14,043,368 | |||||||

Net cash provided by operating activities | 5,159,563 | 5,011,719 | |||||||

Cash flows from investing activities | |||||||||

Purchases of fixed assets | (52,505 | ) | (15,048 | ) | |||||

Purchases of equity method investments | — | (37,548,532 | ) | ||||||

Redemptions of equity method investments - FSOF | 666,563 | 6,000,000 | |||||||

Distributions from equity method investments - FSC and FSFR common stock | 2,902,592 | 842,801 | |||||||

Distributions received from beneficial interest in CLOs | — | 1,428,590 | |||||||

Proceeds from sale of CLO Management | 16,534,067 | — | |||||||

Net cash provided by (used in) investing activities | 20,050,717 | (29,292,189 | ) | ||||||

Cash flows from financing activities | |||||||||

Proceeds from borrowings under credit facility | — | 30,000,000 | |||||||

Repayments under credit facility | (9,850,000 | ) | (3,000,000 | ) | |||||

Deferred financing costs paid | (372,821 | ) | — | ||||||

Repayments of notes payable | — | (2,237,443 | ) | ||||||

Distributions to Holdings limited partners | (12,940,843 | ) | (11,373,105 | ) | |||||

Dividends to Class A shareholders | (3,030,726 | ) | (2,156,353 | ) | |||||

Net cash provided by (used in) financing activities | (26,194,390 | ) | 11,233,099 | ||||||

4

Fifth Street Asset Management Inc.

Consolidated Statements of Cash Flows

(unaudited)

Net decrease in cash | (984,110 | ) | (13,047,371 | ) | |||||

Cash, beginning of period | 6,727,085 | 17,185,204 | |||||||

Cash, end of period | $ | 5,742,975 | $ | 4,137,833 | |||||

Supplemental disclosures of cash flow information: | |||||||||

Cash paid during the period for interest | $ | 3,789,461 | $ | 2,857,564 | |||||

Cash paid during the period for income taxes | $ | 190,001 | $ | 251,236 | |||||

Non-cash investing activities: | |||||||||

Non-cash contribution to FSOF | $ | 123,300 | $ | 78,720 | |||||

Non-cash distribution from FSOF | $ | 123,300 | $ | 78,720 | |||||

Non-cash financing activities: | |||||||||

Accrued dividends | $ | 744,768 | $ | 1,126,478 | |||||

Deemed capital contribution | $ | — | $ | 5,810,794 | |||||

Issuance of shares to settle derivative liability | $ | — | $ | 3,267,160 | |||||

Assumed liabilities in connection with sale of CLO Management | $ | 12,972,565 | $ | — | |||||

Increase in deferred tax assets as a result of exchange of Holdings LP Interests | $ | 30,599,203 | $ | — | |||||

Increase in amounts payable to related parties pursuant to tax receivable agreement | $ | 26,009,323 | $ | — | |||||

All revenues are earned from affiliates of the Company. All gains (losses) from investments are from related parties. See notes to consolidated financial statements.

5

Fifth Street Asset Management Inc.

Notes to Consolidated Financial Statements

(Unaudited)

Note 1. Organization

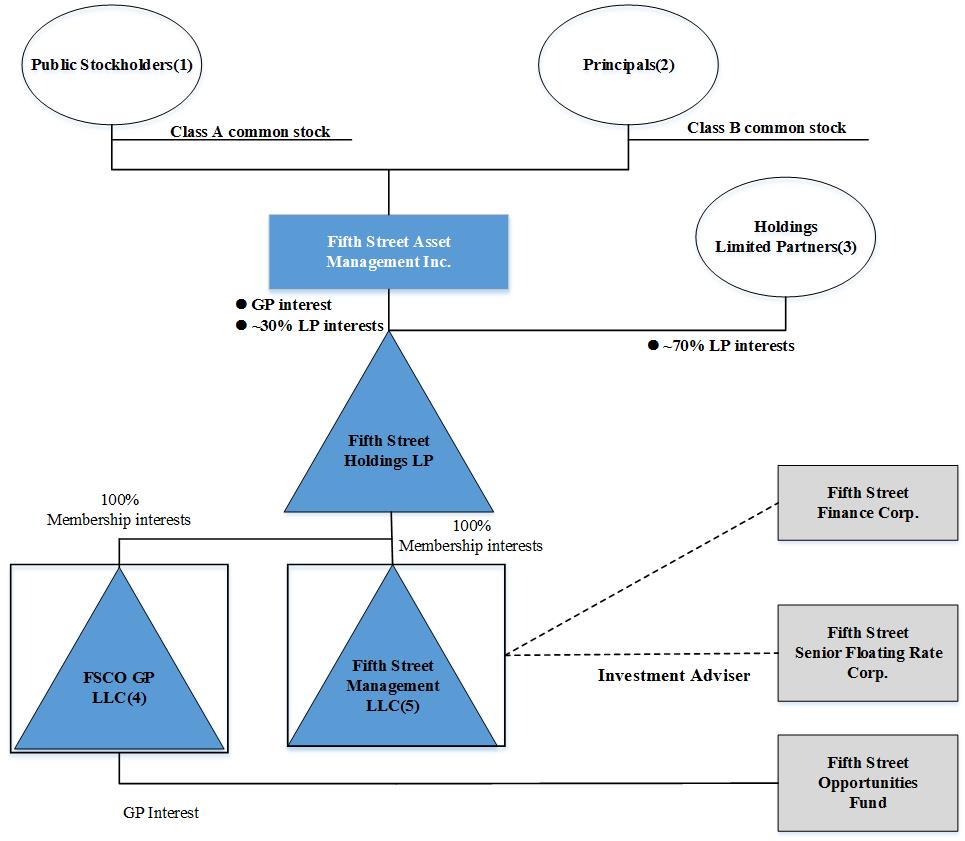

Prior to the closing of the asset sale to Oaktree Capital Management, L.P. (“Oaktree”) on October 17, 2017, Fifth Street Asset Management Inc. ("FSAM"), together with its consolidated subsidiaries (collectively, the "Company"), was an alternative asset management firm headquartered in Greenwich, CT that provided asset management services to its investment funds (referred to as the "Fifth Street Funds" or the "funds"), which, as of September 30, 2017, consisted of Fifth Street Finance Corp. (formed on January 2, 2008, "FSC") and Fifth Street Senior Floating Rate Corp. (formed on May 22, 2013, "FSFR"), both publicly-traded business development companies regulated under the Investment Company Act of 1940, as amended (together, the "BDCs"). As of September 30, 2017, the Company conducted all of its operations through Fifth Street Management LLC ("FSM") and its consolidated subsidiaries.

As of September 30, 2017, the Company's had three primary sources of revenues: management fees, performance fees and other fees. These revenues were derived from the Company's agreements with the funds it managed as of September 30, 2017, primarily the BDCs. For the three and nine months ended September 30, 2017 and 2016 presented in the Consolidated Statements of Operations, revenues from continuing operations consisted of management fees and other fees earned from CLO I, CLO II and FSOF, which were driven by the amount of the average principal balance of investments during the period, with respect to the CLOs, or net asset value, with respect to FSOF. As of September 30, 2017, the Company conducted substantially all of its operations through one reportable segment that provided asset management services to the Fifth Street Funds. The Company generated all of its revenues in the United States.

On July 13, 2017 we sold 100% of the limited liability company interests of CLO Management, a wholly-owned subsidiary of Fifth Street Holdings and the collateral manager for funds within our senior loan strategy, for an aggregate purchase price of $29.0 million less borrowings outstanding at CLO Management, subject to post-closing adjustments for working capital and transaction expenses, which resulted in an aggregate net purchase price of $15.3 million.

In September 2017, the Company completed the wind down of Fifth Street Opportunities Fund, L.P., a private fund managed by Fifth Street Management (“FSOF”, formerly Fifth Street Credit Opportunities Fund, L.P.), and returned invested capital to investors. In connection with the wind down, the investment management agreement with FSOF was terminated.

As of September 30, 2017, the Company determined the closing of the asset sale to Oaktree was probable to occur. As the asset sale is a strategic shift and will have a major effect on the Company's operations and financial results, all activities related to the management and administration of the BDCs (the "BDC Investment Advisory Business") are reflected as discontinued operations for all periods presented. As a result, the Company evaluated the carrying value of certain assets and liabilities, including but not limited to, prepaid expenses, fixed assets, deferred tax assets, accounts payable and accrued expenses, deferred rent liability and payables to related parties, which include the carrying value of the TRA liability and lease termination payments in connection with vacating the lease of our corporate headquarters. As a result of the Company's plan of liquidation approved by its Board of Directors on October 23, 2017, the Company expects future periods will be presented under the liquidation basis of accounting, and accordingly, there may be additional adjustments to the carrying value of assets and liabilities to reflect net realizable value.

The Oaktree transaction closed on October 17, 2017. See Note 2 - Discontinued Operations and Note 15 - Subsequent Events.

Oaktree Transaction

As previously disclosed, on July 13, 2017, FSM, Oaktree Capital Management, L.P. (“Oaktree”), FSAM (solely for the purposes set forth therein) and Fifth Street Holdings (solely for the purposes set forth therein) entered into an Asset Purchase Agreement (the “Asset Purchase Agreement”).

On September 7, 2017, in connection with the transactions contemplated by the Asset Purchase Agreement, the stockholders of each of FSC and FSFR approved the entry of FSC and FSFR, as applicable, into new investment agreements with Oaktree. On October 17, 2017 (the “Closing”), Oaktree entered into new investment advisory agreements with each of FSC and FSFR and FSM’s investment advisory agreements with each of FSC and FSFR were terminated.

At the Closing and upon the terms and subject to the conditions set forth in the Asset Purchase Agreement, FSM sold, conveyed, assigned and transferred to Oaktree and Oaktree purchased, acquired and accepted from FSM all of FSM’s right, title and interest in specified business records with respect to FSM’s existing investment advisory agreements with each of FSC and FSFR for a purchase price of $320 million in cash. Oaktree acquired intellectual property used exclusively in these business records, and any goodwill associated with the investment advisory business conducted by FSM pursuant to these investment advisory agreements. At the Closing and in accordance with the Asset Purchase Agreement, the outstanding balance of the Company's credit facility in the amount of $92,150,000 was paid off.

6

Fifth Street Asset Management Inc.

Notes to Consolidated Financial Statements

(Unaudited)

From and after the Closing, FSM and Fifth Street Holdings have agreed to indemnify Oaktree, its affiliates and its and their respective representatives (the “Buyer Indemnified Parties”) from liability or losses resulting from (i) buyer specified losses, (ii) the breach of any covenant of FSM, FSAM or Fifth Street Holdings in connection with the Asset Purchase Agreement and (iii) any excluded liability under the Asset Purchase Agreement, subject to a cap of $32 million and with sole recourse to a $32 million purchase price escrow. Oaktree may seek indemnification for attorneys’ fees and consequential damages within this cap up to an amount of $22 million. The Buyer Indemnified Parties’ right to such indemnification survives through December 20, 2019, after which time remaining amounts in the escrow account will be released to FSM.

FSM and Fifth Street Holdings have also agreed to indemnify each of FSC and its subsidiaries and FSFR and its subsidiaries against (i) all costs and out-of-pocket expenses incurred by the BDCs and their subsidiaries in connection with existing examinations and investigations by the SEC and (ii) related fees, fines, monetary penalties, deductibles and disgorgements ordered by the SEC to be paid by the BDCs, net of any disgorgements paid by FSM to the BDCs and insurance recoveries received by the BDCs (“BDC Net Losses”). The primary source of recourse of SEC investigation-related costs and expenses is a $10 million purchase price escrow. Any SEC investigation-related costs and expenses in excess of $10 million and any BDC Net Losses may also be satisfied against the $35 million of shares of FSC common stock and $10 million of shares of FSFR common stock owned by Fifth Street Holdings and pledged pursuant to certain pledge agreements to be entered into at Closing by Fifth Street Holdings to secure any such indemnification obligations of FSM and Fifth Street Holdings relating to BDC Net Losses and certain SEC investigation-related legal costs and expenses. Oaktree’s right to such indemnification survives through the date that is 45 days after all SEC investigations have been settled or it is confirmed by the SEC that the BDCs are not under investigation (subject to extension for any pending claims against directors and officers of the BDCs where such directors remain entitled to indemnification coverage from the BDCs), after which time remaining amounts in the escrow will be released to FSM and the stock pledges will terminate.

From and after the Closing, Oaktree will indemnify FSM, FSAM, Fifth Street Holdings and their respective affiliates and representatives (collectively, the “Seller Indemnified Parties”) from liability or losses arising out of or resulting from (i) any losses in connection with the costs and expenses incurred by the Seller Indemnified Parties in defending against claims arising after the Closing that relate to the investment advisory business acquired by Oaktree and (ii) the breach of any representation, warranty and covenant of Oaktree that is to be performed prior to the Closing.

Each of FSM and Oaktree shared expenses associated with the BDCs’ preparation and filing of proxy materials in connection with the special meetings of their stockholders together with FSAM’s proxy solicitation expenses and filing fees under the Hart-Scott-Rodino Antitrust Improvement Act of 1976, as amended. FSM paid $321,043 of costs relating to the preparation and filing of proxy materials prior to Closing.

On July 13, 2017, concurrently with the execution of the Asset Purchase Agreement, FSM entered into a letter agreement with Oaktree pursuant to which FSM agreed to reimburse up to $5 million of Oaktree’s transaction expenses incurred in connection with the negotiation, execution and delivery of the Asset Purchase Agreement and the performance by Oaktree of its obligations thereunder at the Closing. At the Closing, FSM reimbursed Oaktree the full amount pursuant to this letter agreement, which amount was accrued as of September 30, 2017 and included in discontinued operations.

Concurrently with the execution of the Asset Purchase Agreement, FSAM and Oaktree entered into a Noncompetition and Nonsolicitation Agreement, dated as of July 13, 2017, pursuant to which, through October 17, 2020, FSAM agreed to specified restrictions on its ability to invest in debt or debt-like preferred equity where the investment opportunity being offered to all offerees exceeds $5 million (subject to certain exceptions). Such restrictions apply through October 17, 2027 with respect to investments in business development companies managed by Oaktree or any of its affiliates. FSAM also agreed to restrictions on its ability to solicit for employment any full-time employees of Oaktree or advisors or consultants, who are engaged for a substantial portion of their time by Oaktree, through October 17, 2020.

The Company recorded $7,743,199 and $15,085,039 in expenses during the three and nine months ended September 30, 2017 relating to the Oaktree transaction, all of which are included in discontinued operations.

7

Fifth Street Asset Management Inc.

Notes to Consolidated Financial Statements

(Unaudited)

Reorganization

In anticipation of its initial public offering (the "IPO") that closed November 4, 2014, FSAM was incorporated in Delaware on May 8, 2014 as a holding company with its primary asset expected to be a limited partnership interest in Fifth Street Holdings. Fifth Street Holdings was formed on June 27, 2014 by Leonard M. Tannenbaum and Bernard D. Berman (the "Principals") as a Delaware limited partnership. Prior to the transactions described below, the Principals were the general partners and limited partners of Fifth Street Holdings. Fifth Street Holdings has a single class of limited partnership interests (the "Holdings LP Interests"). Immediately prior to the IPO:

• | The Principals contributed their general partnership interests in Fifth Street Holdings to FSAM in exchange for 100% of FSAM's Class B common stock; |

• | The members of FSM contributed 100% of their membership interests in FSM to Fifth Street Holdings in exchange for Holdings LP Interests; and |

• | The members of FSCO GP, a Delaware limited liability company, formed on January 6, 2014 to serve as the general partner of FSOF, contributed 100% of their membership interests in FSCO GP to Fifth Street Holdings in exchange for Holdings LP Interests. |

These collective actions are referred to herein as the "Reorganization."

Initial Public Offering

On November 4, 2014, FSAM issued 6,000,000 shares of Class A common stock in the IPO at a price of $17.00 per common share. The proceeds totaled $95.9 million, net of underwriting commissions of $6.1 million. The proceeds were used to purchase a 12.0% limited partnership interest in Fifth Street Holdings.

Immediately following the Reorganization and the closing of the IPO on November 4, 2014:

• | The Principals held 42,856,854 shares of FSAM Class B common stock and 42,856,854 Holdings LP Interests. |

• | FSAM held 6,000,000 Holdings LP Interests and the former members of FSM and FSCO GP, including the Principals, held 44,000,000 Holdings LP Interests. |

• | The Principals, through their holdings of FSAM Class B common stock in the aggregate, had approximately 97.3% of the voting power of FSAM's common stock. |

Upon the completion of the Reorganization and the IPO, FSAM also became the general partner of Fifth Street Holdings. Fifth Street Holdings and its wholly-owned subsidiaries (including FSM, CLO Management and FSCO GP) are consolidated by FSAM in the consolidated financial statements. The portion of net income attributable to the limited partners of Fifth Street Holdings, excluding FSAM, is recorded as "Net (income) loss attributable to non-controlling interests" on the Consolidated Statements of Operations.

Exchange Agreement

In connection with the Reorganization, FSAM entered into an exchange agreement with the limited partners of Fifth Street Holdings that granted each limited partner of Fifth Street Holdings, and certain permitted transferees, the right, beginning two years after the closing of the IPO and subject to vesting and minimum retained ownership requirements, on a quarterly basis, to exchange such person's Holdings LP Interests for shares of Class A common stock of FSAM, on a one-for-one basis, subject to customary conversion rate adjustments for splits, unit distributions and reclassifications (collectively referred to as the "Exchange Agreement"). As a result, each limited partner of Fifth Street Holdings, over time, has the ability to convert his or her illiquid ownership interests in Fifth Street Holdings into Class A common stock of FSAM, which can more readily be sold in the public markets.

On January 4, 2017, pursuant to the terms of the Exchange Agreement, a director of the Company and certain other Holdings Limited Partners exchanged an aggregate of 8,772,450 Holdings LP Interests of Fifth Street Holdings for shares of the Company’s Class A common stock on a one-for-one basis and, in the case of the Principals, submitted to the Company 8,571,370 shares of the Company’s Class B common stock for cancellation. The acquisition of additional Holdings LP Interests are treated as reorganizations of entities under common control as required by the Financial Accounting Standards Board (the "FASB") Accounting Standards Codification ("ASC") Topic 805. See Note 15 - Subsequent Events for a description of certain subsequent exchanges.

As of September 30, 2017 and December 31, 2016, FSAM held approximately 30.8% and 13.0% of Fifth Street Holdings, respectively. FSAM’s percentage ownership in Fifth Street Holdings will continue to change as Holdings LP Interests are exchanged for Class A common stock of FSAM or when FSAM otherwise issues or repurchases FSAM common stock.

8

Fifth Street Asset Management Inc.

Notes to Consolidated Financial Statements

(Unaudited)

FSAM's purchase of Holdings LP Interests concurrent with its IPO and the subsequent and future exchanges by holders of Holdings LP Interests for shares of FSAM's Class A common stock pursuant to the Exchange Agreement are expected to result in increases in its share of the tax basis of the tangible and intangible assets of Fifth Street Holdings, which will increase the tax depreciation and amortization deductions that otherwise would not have been available to FSAM. These increases in tax basis and tax depreciation and amortization deductions are expected to reduce the amount of cash taxes that FSAM would otherwise be required to pay in the future. As of September 30, 2017, FSAM was party to a tax receivable agreement ("TRA") with certain limited partners of Fifth Street Holdings (the "TRA Recipients") that requires FSAM to pay the TRA Recipients 85% of the amount of cash savings, if any, in U.S. federal, state, local and foreign income tax that FSAM actually realizes (or, under certain circumstances, is deemed to realize) as a result of the increases in tax basis in connection with exchanges by the TRA Recipients described above and certain other tax benefits attributable to payments under the tax receivable agreement.

In connection with the transactions contemplated by the Asset Purchase Agreement, on July 13, 2017, FSAM, Fifth Street Holdings, the TRA Recipients, the Tannenbaum Trust, the Bernard D. Berman 2012 Trust and FSC CT II, Inc. entered into a Waiver and Termination of Tax Receivable Agreement (“TRA Waiver”) pursuant to which the TRA Recipients agreed (i) to irrevocably waive any and all rights to receive tax benefit payments payable at any time under the TRA, including any tax benefit payments that would result from the consummation of the transactions contemplated by the Asset Purchase Agreement other than certain payments accrued for the fiscal year ended December 31, 2016 that have not been paid and (ii) to release FSAM and Fifth Street Holdings from their respective obligations under the TRA. Effective as of October 17, 2017, the TRA automatically terminated without any further action required by any party to the TRA Waiver, and all rights and obligations of the parties thereto were immediately extinguished.

RiverNorth Settlement

On February 18, 2016, the Company entered into a purchase and settlement agreement ("PSA") with RiverNorth Capital Management, LLC ("RiverNorth") pursuant to which RiverNorth would withdraw its competing FSC proxy solicitation. In connection with the execution and delivery of the PSA, on March 24, 2016, the Company purchased 4,078,304 shares of common stock of FSC for $25.0 million of cash at a purchase price of $6.13 per share, net of certain dividends payable to the Company pursuant to the PSA, resulting in a loss of $4,608,480, which represents the premium paid by the Company in excess of the FSC closing share price on the date of the transaction. Pursuant to a letter agreement with the Company, Leonard M. Tannenbaum purchased 5,142,296 shares of common stock of FSC from RiverNorth at a net purchase price of $6.13 per share, resulting in a loss of $5,810,794 which represents the premium paid by Mr. Tannenbaum in excess of the FSC closing share price on the date of the transaction. Such amount was recorded as a loss in the Consolidated Statement of Operations and as a deemed contribution/distribution in the Consolidated Statement of Changes in Stockholder's Equity (Deficit) since Mr. Tannenbaum holds a controlling interest in FSAM and the Company directly benefited from this payment. The total premium paid by the Company and Mr. Tannenbaum in the amount of $10,419,274 was recorded as a loss during the three months ended March 31, 2016 and is included in discontinued operations.

In addition, the Company issued RiverNorth a warrant to purchase 3,086,420 shares of FSAM's Class A common stock that, upon exercise, the Company was obligated to pay RiverNorth an amount equal to the lesser of: (i) $5 million and (ii) the spread value of the warrant based on a $3.24 strike price. The warrant was exercised by RiverNorth on June 23, 2016. Refer to Note 4 for further information.

The Company also entered into a swap agreement with RiverNorth whereas on each settlement date, if the settlement date share price of FSC common stock was less than $6.25, the Company was obligated to pay RiverNorth an amount equal to the excess of $6.25 over the settlement date share price multiplied by the 3,878,542 notional shares of common stock underlying the swap. Alternatively, if the settlement date share price of FSC common stock was greater than $6.25, RiverNorth was obligated to pay the Company for the excess of the settlement date share price over $6.25 in cash. The Company was also entitled to a portion of dividends on FSC shares underlying the total return swap which were earned by RiverNorth prior to the settlement date. On September 7, 2016, the Company settled the swap agreement with RiverNorth. Refer to Note 4 for further information.

Ironsides Settlement

On September 30, 2016, the Company entered into a PSA with Ironsides Partners LLC, Ironsides Partners Special Situations Master Fund II L.P. and Ironsides P Fund L.P. (collectively, "Ironsides"). Upon execution of the PSA, Ironsides agreed that it would not, and would not permit any of its controlled Affiliates or Associates (as defined in the PSA) to, during a standstill period: (1) nominate or recommend for nomination any person for election as a director at any annual or special meeting of stockholders of FSAM, FSC and FSFR (the "Fifth Street Parties"), directly or indirectly, (2) submit any proposal for consideration at, or bring any other business before, any annual or special meeting of any of the Fifth Street Parties'

9

Fifth Street Asset Management Inc.

Notes to Consolidated Financial Statements

(Unaudited)

stockholders, directly or indirectly, or (3) initiate, encourage or participate in any “withhold” or similar campaign with respect to any annual or special meeting of any of the Fifth Street Parties' stockholders, directly or indirectly. During the standstill period, Ironsides shall not publicly or privately encourage or support any other stockholder to take any of the actions described above. On November 30, 2016, in connection with the execution and delivery of the PSA, the Company purchased 1,295,767 shares of common stock of FSFR for a per-share purchase price of $9.00. Pursuant to a letter agreement with the Company, Mr. Tannenbaum purchased 646,863 shares of common stock of FSFR from Ironsides for a per-share purchase price of $9.00. These purchases were not made at a premium to the market price of the FSFR shares on the date of purchase.

Sale of CLO Management

On July 1, 2017, Fifth Street Holdings entered into a purchase agreement (the “CLO Purchase Agreement”) with NewStar Financial Inc. ("NewStar Financial"). At the closing of the transactions contemplated thereby, on July 20, 2017, NewStar Financial acquired 100% of the limited liability company interests of Fifth Street CLO Management LLC ("CLO Management"), a wholly-owned subsidiary of Fifth Street Holdings L.P. (Fifth Street Holdings) and the collateral manager for CLO I and CLO II, each a collateralized loan obligation in the Company’s senior loan fund strategy, for an aggregate purchase price of $29.0 million less borrowings outstanding at CLO Management of $13.0 million, subject to post-closing adjustments for working capital and transactions expenses, which resulted in an aggregate net purchase price of $15.3 million. The Company recorded a gain on the sale of CLO Management in the amount of $4.6 million.

Note 2. Discontinued Operations

The following condensed financial information reflects the BDC Investment Advisory business for the three and nine months ended September 30, 2017 and 2016.

For the Three Months Ended September 30, | For the Nine Months Ended September 30, | |||||||||||||||

2017 | 2016 | 2017 | 2016 | |||||||||||||

Revenues | ||||||||||||||||

Management fees (includes Part I Fees of $815,491 and $8,895,485; $7,867,963 and $21,890,239 for the three and nine months ended September 30, 2017 and 2016, respectively) | $ | 8,986,275 | $ | 18,939,913 | $ | 35,701,216 | $ | 55,886,969 | ||||||||

Other fees | 1,850,622 | 2,693,023 | 5,737,910 | 6,311,972 | ||||||||||||

Total revenues | 10,836,897 | 21,632,936 | 41,439,126 | 62,198,941 | ||||||||||||

Expenses | ||||||||||||||||

Compensation and benefits | 8,294,404 | 8,377,401 | 16,657,939 | 21,925,650 | ||||||||||||

General, administrative and other expenses | 9,853,160 | 4,481,432 | 22,110,535 | 15,440,461 | ||||||||||||

Total expenses | 18,147,564 | 12,858,833 | 38,768,474 | 37,366,111 | ||||||||||||

Other income (expense) | ||||||||||||||||

Interest expense | (1,963,561 | ) | (1,009,092 | ) | (4,947,890 | ) | (2,819,011 | ) | ||||||||

Reserve for expenses reimbursable to affiliates | (3,732,920 | ) | — | (3,732,920 | ) | — | ||||||||||

Loss on legal settlement | — | — | — | (9,250,000 | ) | |||||||||||

Insurance recoveries | — | 50,905 | 4,332,024 | 12,297,636 | ||||||||||||

Loss on investor settlement | — | — | — | (10,419,274 | ) | |||||||||||

Unrealized gain on derivatives | — | 8,383,213 | — | — | ||||||||||||

Realized loss on derivatives | — | (3,078,357 | ) | — | (2,612,932 | ) | ||||||||||

Total other income (expense), net | (5,696,481 | ) | 4,346,669 | (4,348,786 | ) | (12,803,581 | ) | |||||||||

Income (loss) before provision (benefit) for income taxes | (13,007,148 | ) | 13,120,772 | (1,678,134 | ) | 12,029,249 | ||||||||||

Provision (benefit) for income taxes | (1,428,457 | ) | 935,482 | 49,544 | 1,978,204 | |||||||||||

Income (loss) from discontinued operations, net of tax | $ | (11,578,691 | ) | $ | 12,185,290 | $ | (1,727,678 | ) | $ | 10,051,045 | ||||||

10

Fifth Street Asset Management Inc.

Notes to Consolidated Financial Statements

(Unaudited)

Note 3. Significant Accounting Policies

Basis of Presentation

The consolidated financial statements of the Company have been prepared in accordance with accounting principles generally accepted in the United States of America ("GAAP") and pursuant to the rules and regulations of the Securities and Exchange Commission (the "SEC") and the requirements for reporting on Form 10-Q and Regulation S-X. In the opinion of management, all adjustments of a normal recurring nature considered necessary for the fair presentation of the consolidated financial statements have been made. All significant intercompany transactions and balances have been eliminated in consolidation. For the periods presented herein, total comprehensive income (loss) is equivalent to net income (loss), and accordingly, no statements of comprehensive income (loss) are presented.

Principles of Consolidation

The consolidated financial statements include the accounts of the Company and entities in which it, directly or indirectly, is determined to have a controlling financial interest under ASC Topic 810, as amended by ASU No. 2015-02. Under the variable interest model, the Company determines whether, if by design, an entity has equity investors who lack substantive participating or kick-out rights. If equity investors do not have such rights, the entity is considered a variable interest entity ("VIE") and must be consolidated by its primary beneficiary. An enterprise is determined to be the primary beneficiary if it holds a controlling financial interest. A controlling financial interest is defined as (a) the power to direct the activities of a VIE that most significantly impact the entity's economic performance and (b) the obligation to absorb losses of the entity or the right to receive benefits from the entity that could potentially be significant to the VIE. The consolidation guidance requires an analysis to determine (a) whether an entity in which the Company holds a variable interest is a VIE and (b) whether the Company's involvement, through holding interests directly or indirectly in the entity, would give it a controlling financial interest. Performance of that analysis requires the exercise of judgment.

Under the consolidation guidance, the Company determines whether it is the primary beneficiary of a VIE at the time it becomes involved with a variable interest entity and reconsiders that conclusion continually. In evaluating whether the Company is the primary beneficiary, the Company evaluates its economic interests in the entity held either directly or indirectly by the Company. The consolidation analysis can generally be performed qualitatively; however, if it is not readily apparent that the Company is not the primary beneficiary, a quantitative analysis may also be performed. Investments and redemptions (either by the Company, affiliates of the Company or third parties) or amendments to the governing documents of the respective investment funds could affect an entity's status as a VIE or the determination of the primary beneficiary. At each reporting date, the Company assesses whether it is the primary beneficiary and will consolidate or deconsolidate accordingly.

For equity investments where the Company does not control the investee, and where it is not the primary beneficiary of a VIE, but can exert significant influence over the financial and operating policies of the investee, the Company follows the equity method of accounting. The evaluation of whether the Company exerts control or significant influence over the financial and operational policies of its investees requires significant judgment based on the facts and circumstances surrounding each individual investment. Factors considered in these evaluations may include the type of investment, the legal structure of the investee, the terms and structure of the investment agreement, including investor voting or other rights, the terms of the Company's investment advisory agreement or other agreements with the investee, any influence the Company may have on the governing board of the investee, the legal rights of other investors in the entity pursuant to the fund’s operating documents and the relationship between the Company and other investors in the entity.

Consolidated Variable Interest Entities

Fifth Street Holdings

FSAM is the sole general partner of Fifth Street Holdings and, as such, it operates and controls all of the business and affairs of Fifth Street Holdings and its wholly-owned subsidiaries. Under ASC 810, Fifth Street Holdings meets the definition of a VIE because the limited partners do not hold substantive kick-out or participating rights. Since FSAM has the obligation to absorb expected losses and the right to receive benefits that could be significant to Fifth Street Holdings and is the sole general partner, FSAM is considered to be the primary beneficiary of Fifth Street Holdings. The assets of Fifth Street Holdings can be used to settle the obligations of FSAM based on the discretion of FSAM in its capacity as the general partner of Fifth Street Holdings.

As a result, the Company consolidates the financial results of Fifth Street Holdings and its wholly-owned subsidiaries and records the economic interests in Fifth Street Holdings held by the limited partners other than FSAM as "Non-controlling interests" on the Consolidated Statements of Financial Condition and "Net (income) loss attributable to non-controlling interests" on the Consolidated Statements of Operations.

11

Fifth Street Asset Management Inc.

Notes to Consolidated Financial Statements

(Unaudited)

Voting Interest Entities

Entities that are not VIEs are generally evaluated under the voting interest model. The Company consolidates voting interest entities that it controls through a majority voting interest or through other means.

Unconsolidated Variable Interest Entities

Prior to the sale of CLO Management and the wind down of FSOF, the Company's interests in these VIEs were not consolidated because the Company was not deemed the primary beneficiary. The Company's interest in such entities generally is in the form of direct interests and fixed fee arrangements. As of September 30, 2017, there are no unconsolidated variable interest entities.

CLOs

In February 2015, the Company closed a securitization of the senior secured loans warehoused in Fifth Street Senior Loan Fund I, LLC ("CLO I"). In September 2015, Fifth Street Senior Loan II, LLC merged into Fifth Street SLF II Ltd. ("CLO II"), and the Company closed a securitization of the senior secured loans previously warehoused in Fifth Street Senior Loan Fund II, LLC. CLO Management, a wholly owned-consolidated subsidiary of Fifth Street Holdings, is the collateral manager of CLO I and CLO II (collectively referred to as the "CLOs"), and as such, it operates and controls all of the business and affairs of the CLOs. Under ASC 810, the CLOs meet the definition of a VIE because the total equity at risk is not sufficient to finance their activities.

Prior to the sale of CLO Management, the Company determined that it did not have an obligation to absorb expected losses that could be significant to the CLOs. Therefore, the Company was not considered to be the primary beneficiary of the CLOs and, accordingly, did not consolidate their financial results.

Use of Estimates

The preparation of consolidated financial statements in conformity with GAAP requires management to make estimates and assumptions affecting amounts reported in the consolidated financial statements and accompanying notes. As of September 30, 2017, the most significant of these estimates are related to: (i) the valuation of equity-based compensation, (ii) the estimate of future taxable income, which impacts the carrying amount of the Company’s deferred income tax assets, (iii) the determination of net tax benefits in connection with the Company's tax receivable agreements, (iv) the valuation of the Company's investments, (v) the measurement of asset and liabilities associated with exit and disposal activities related to the abandonment of office space, (vi) the calculation of interest income accreted on beneficial interests in CLOs, (vii) the accretion of the residual excess of the Company's share of FSC and FSFR's net assets over its cost basis and (viii) the measurement of impairment of fixed assets. These estimates are based on the information that is currently available to the Company and on various other assumptions that the Company believes to be reasonable under the circumstances. Actual results could differ materially from those estimates under different assumptions and conditions.

Concentration of Credit Risk and Other Risks and Uncertainties

Financial instruments which potentially subject the Company to concentrations of credit risk consist primarily of cash and cash equivalents. The Company maintains its cash and cash equivalents with high-credit quality financial institutions.

For the nine months ended September 30, 2017 and 2016, substantially all revenues and receivables were earned or derived from advisory or administrative services provided to the BDCs and other affiliated entities. See Note 2.

Fair Value Measurements

The carrying amounts of cash, management fees receivable, performance fees receivable, prepaid expenses, insurance recovery receivable, due from/to affiliates, accounts payable and accrued expenses, accrued compensation and benefits, income taxes payable, legal settlement payable and dividends payable approximate fair value due to the immediate or short-term maturity of these financial instruments.

Cash and Cash Equivalents

Cash equivalents include short-term, highly liquid investments that are readily convertible to known amounts of cash and have original maturities of three months or less. The Company places its cash and cash equivalents with U.S. financial institutions and, at times, amounts may exceed federally insured limits. The Company monitors the credit standing of these financial institutions.

12

Fifth Street Asset Management Inc.

Notes to Consolidated Financial Statements

(Unaudited)

Equity Method Investments

Investments over which the Company exercises significant influence, but which do not meet the requirements for consolidation, are accounted for using the equity method of accounting, whereby the Company records its share of the underlying income or losses of equity method investees. The Company did not elect the fair value option on its equity method investments.

Investments in equity method investees consists of the Company's general partner interests in FSOF (prior to wind down) and investments in FSC and FSFR common stock. The Company exercises significant influence with respect to FSOF and the BDCs as a result of its management contracts with them, and specifically with respect to the BDCs, its inclusion of its employees on the board of directors.

Beneficial Interest in CLOs

Beneficial interests in CLOs meet the definition of a debt security under ASC Topic 325-40, Beneficial Interest in Securitized Financial Assets. Income from the beneficial interest in CLOs is recorded using the effective interest method based upon an estimation of an effective yield to maturity utilizing assumed cash flows. The Company monitors the expected residual payments, and effective yield is determined and updated periodically, as needed. Any distributions received from the beneficial interests in CLOs in excess of the calculated income using the effective yield are treated as a reduction of the cost.

The Company earned interest income of $95,865 and $725,321, respectively, from beneficial interests in CLOs, for the three and nine months ended September 30, 2017 and $386,617 and $1,082,342, respectively, for the three and nine months ended September 30, 2016.

Fair Value Option

Prior to the sale of CLO Management, the Company had elected the fair value option, upon initial recognition, for all beneficial interests in CLOs. There were $654,915 and $983,434 of unrealized gains, respectively, recorded on beneficial interests in CLOs for the three and nine months ended September 30, 2017. There were $537,600 and 169,373 of unrealized gains, respectively, recorded on beneficial interests in CLOs for the three and nine months ended September 30, 2016.

The fair value option permits the irrevocable election of fair value on an instrument-by-instrument basis at initial recognition of an asset or liability or upon an event that gives rise to a new basis of accounting for that instrument. The Company believes that by electing the fair value option for these financial instruments, it provides consistent measurement with its peers in the asset management industry. Changes in the fair value of these assets and liabilities and related interest income/expense are recorded within "Other income (expense)" in the Consolidated Statements of Operations. Refer to Note 5 for a description of valuation methodologies for the beneficial interests in CLOs.

Derivative Instruments

Derivative instruments include warrant and swap contracts issued in connection with the RiverNorth settlement. The derivative instruments are not designated as hedging instruments and are carried at fair value. Changes in fair value are recorded within "Unrealized gain (loss) on derivatives" and upon settlement of a derivative instrument, the Company records a "Realized gain (loss) on derivatives" in the Consolidated Statements of Operations, both of which are included within discontinued operations.

See Note 4 for quantitative disclosures regarding derivative instruments.

Fixed Assets

Fixed assets consist of furniture, fixtures and equipment (including automobiles, computer hardware and purchased software), software developed for internal use and leasehold improvements, and are recorded at cost, less accumulated depreciation and amortization. Depreciation of furniture, fixtures and equipment is computed using the straight-line method over the estimated useful lives of the respective assets (three to eight years). Software developed for internal use, which is amortized over three years, consists of costs incurred during the application development stage of software developed for the Company's proprietary use and includes costs of Company personnel who are directly associated with the development. Amortization of improvements to leased properties is computed using the straight-line method based upon the initial term of the applicable lease or the estimated useful life of the improvements, whichever is shorter, and ranges from five to 10 years. Routine expenditures for repairs and maintenance are charged to expense when incurred. Major betterments and improvements are capitalized. Upon retirement or disposition of fixed assets, the cost and related accumulated depreciation are removed from the accounts and any resulting gain or loss is recognized in the Consolidated Statements of Operations. The Company evaluates fixed assets for impairment whenever events or changes in circumstances indicate that an asset's carrying value may not be fully recovered.

13

Fifth Street Asset Management Inc.

Notes to Consolidated Financial Statements

(Unaudited)

Deferred Financing Costs

Deferred financing costs, which consist of fees and expenses paid in connection with the closing of Fifth Street Holdings' credit facility, are capitalized at the time of payment. Deferred financing costs are amortized using the straight line method over the term of the credit facility and are included in interest expense on the Consolidated Statements of Operations. In connection with an amendment to the Company's credit facility on June 30, 2017 (See Note 9), the Company wrote off $208,000 of deferred financing costs and reclassified the remaining balance to credit facility payable on the Consolidated Statement of Financial Condition. During the three months ended September 30, 2017, the Company reduced the amortization period for deferred financing costs from the contractual maturity date to the closing date of the Oaktree transaction, as the Asset Purchase Agreement required the repayment of the Company's credit facility. This resulted in $948,859 of total amortization of deferred financing costs during the three months ended September 30, 2017, which is included in discontinued operations.

Deferred Rent

The Company recognizes rent expense on a straight-line basis over the expected lease term. Within the provisions of certain leases, there are free rent periods and escalations in payments over the base lease term. The effects of these items have been reflected in rent expense on a straight-line basis over the expected lease term. Landlord contributions and tenant allowances are included in the straight-line calculations and are being deferred over the lease term and are reflected as a reduction in rent expense.

Revenue Recognition

As of September 30, 2017, the Company had three principal sources of revenues: management fees, performance fees and other fees. These revenues were derived from the Company's agreements with the funds it manages, primarily the BDCs. The investment advisory agreements on which revenues are based were generally renewable on an annual basis by the general partner or the board of directors of the respective funds.

Management Fees

Management fees were generally based on a defined percentage of fair value of assets, total commitments, invested capital, net asset value, net investment income, total assets or principal amount of the investment portfolios managed by the Company. All management fees are earned from affiliated funds of the Company. The contractual terms of management fees varied by fund structure and investment strategy and range from 0.40% to 1.75% for base management fees, which are asset or capital-based.

Management fees from affiliates also included quarterly incentive fees on the net investment income from the BDCs ("Part I Fees"). Part I Fees were generally equal to 20.0% of the BDCs' net investment income (before Part I Fees and performance fees payable based on capital gains), subject to fixed "hurdle rates" or preferred returns, as defined in the applicable investment advisory agreement. No fees were recognized until the BDCs' net investment income exceeds the applicable hurdle rate, with a "catch-up" provision that serves to ensure the Company receives 20.0% of the BDCs' net investment income from the first dollar earned. Such fees were classified as management fees as they are paid quarterly, predictable and recurring in nature, not subject to repayment (or clawback) and cash settled each quarter. Management fees from affiliates were recognized as revenue in the period investment advisory services are rendered, subject to the Company's assessment of collectability. On March 20, 2017, Fifth Street Management entered into a new investment advisory agreement with FSC, which, effective as of January 1, 2017, (i) decreased the quarterly preferred return to 1.75% on the income portion of the incentive fee and (ii) implemented a total return requirement that may decrease the incentive fee payable to Fifth Street Management by 25% per quarter to the extent that FSC’s cumulative incentive fees over a lookback period of up to 12 quarters exceed 20.0% of FSC's cumulative net increase in net assets resulting from operations.

Performance Fees

Performance fees were earned from the funds managed by the Company based on the performance of the respective funds. The contractual terms of performance fees varied by fund structure and investment strategy and were generally 15.0% to 20.0% of investment performance.

The Company has elected to adopt Method 2 of ASC Topic 605-20, Revenue Recognition for Revenue Based on a Formula. Under this method, the Company recognizes revenue based on the respective fund's performance during the period, subject to certain hurdles or benchmarks. The performance fees for any period are based upon an assumed liquidation of the fund's net assets on the reporting date, and distribution of the net proceeds in accordance with the fund's income allocation provisions. The performance fees may be subject to reversal to the extent that the performance fees recorded exceed the amount due to the general partner or investment manager based on a fund's cumulative investment returns.

14

Fifth Street Asset Management Inc.

Notes to Consolidated Financial Statements

(Unaudited)

Performance fees related to the BDCs ("Part II Fees") were calculated and payable in arrears as of the end of each fiscal year of the BDCs and equal 20.0% of the BDCs' realized capital gains, if any, on a cumulative basis since inception, computed net of all realized capital losses and unrealized capital depreciation on a cumulative basis, less the aggregate amount of any previously paid Part II fees.

Other Fees

The Company also provides administrative services to the Fifth Street Funds. These fees are reported within Revenues - Other fees in the Consolidated Statements of Operations. These fees generally represent reimbursable compensation, overhead and other expenses incurred by the Company on behalf of the funds. The Company is considered the principal under these arrangements and is required to record the expense and related reimbursement revenue on a gross basis.

Compensation and Benefits

Compensation generally includes salaries, bonuses, severance and equity-based compensation charges. Bonuses are accrued over the service period to which they relate.

Retention Bonus Agreements

The Company has entered into retention bonus agreements in the amount of $2,652,000 with certain key employees. Included in compensation expense for the three and nine months ended September 30, 2017 is $131,760 ($55,287 of which is included in discontinued operations) and $930,640 ($674,942 of which is included in discontinued operations) of amortization related to these agreements, respectively and $479,564 ($448,406 of which is included in discontinued operations) and $862,753 ($798,807 of which is included in discontinued operations), respectively, for the three and nine months ended September 30, 2016. There were no retention bonuses forfeited during the nine months ended September 30, 2017.

Severance Agreements

The Company has entered into various severance and change in control agreements with certain key employees, which provide for the payment of severance and other benefits to each participant in the event of a termination without cause or for good reason, and in certain cases, the payment of a cash bonus upon the occurrence of a change in control event. The amounts of such payments and benefits vary by employee. The Company records expenses related to such severance and change in control agreements by employee if, and when, a termination or change in control event occurs. Included in compensation expense for the three and nine months ended September 30, 2017 is $5,022,569 ($4,751,890 of which is included in discontinued operations) and $6,474,976 ($6,204,297 of which is included in discontinued operations), respectively, related to these severance arrangements. Included in compensation expense for the three and nine months ended September 30, 2016 is $1,247,644 (all of which is included in discontinued operations) and $1,949,198 ($1,615,677 of which is included in discontinued operations), respectively, related to these severance arrangements.

Equity-Based Compensation

The Company accounts for stock-based compensation in accordance with ASC Topic 718, Compensation – Stock Compensation. Under the fair value recognition provision of this guidance, share-based compensation cost is measured at the grant date based on the fair value of the award and is recognized as expense over the requisite service period.