Attached files

| file | filename |

|---|---|

| EX-3.2 - AMENDED AND RESTATED BYLAWS - Fifth Street Asset Management Inc. | ex32fsamrestatedbylaws.htm |

| EX-32.1 - CERTIFICATION OF CHIEF EXECUTIVE OFFICER PURSUANT TO SECTION 906 - Fifth Street Asset Management Inc. | fsam-ex321_2014093010q.htm |

| EX-32.2 - CERTIFICATION OF CHIEF FINANCIAL OFFICER PURSUANT TO SECTION 906 - Fifth Street Asset Management Inc. | fsam-ex322_2014093010xq.htm |

| EX-3.1 - AMENDED AND RESTATED CERTIFICATE OF INCORPORATION - Fifth Street Asset Management Inc. | ex31fsam-amendedandrestate.htm |

| EX-31.2 - CERTIFICATION OF CHIEF FINANCIAL OFFICER PURSUANT TO RULE 13A-14(A) - Fifth Street Asset Management Inc. | fsam-ex312_2014093010xq.htm |

| EX-31.1 - CERTIFICATION OF CHIEF EXECUTIVE OFFICER PURSUANT TO RULE 13A-14(A) - Fifth Street Asset Management Inc. | fsam-ex311_2014093010xq.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

Form 10-Q

(Mark One)

þ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) | ||

OF THE SECURITIES EXCHANGE ACT OF 1934 | |||

For the quarterly period ended September 30, 2014

OR

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) | ||

OF THE SECURITIES EXCHANGE ACT OF 1934 | |||

COMMISSION FILE NUMBER: 001-36701

Fifth Street Asset Management Inc.

(EXACT NAME OF REGISTRANT AS SPECIFIED IN ITS CHARTER)

DELAWARE | 46-5610118 | |

(State or jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

777 West Putnam Avenue, 3rd Floor Greenwich, CT | 06830 | |

(Address of principal executive office) | (Zip Code) | |

REGISTRANT'S TELEPHONE NUMBER, INCLUDING AREA CODE:

(203) 681-3600

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter periods as the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES ¨ NO þ

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES ¨ NO ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer o | Accelerated filer o | Non-accelerated filer þ | Smaller reporting company o | |||

(Do not check if a smaller reporting company) | ||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act) YES ¨ NO þ

The number of shares of the registrant's Class A common stock, par value $0.01 per share, outstanding as of December 10, 2014 was 6,000,033. The number of shares of the registrant's Class B common stock, par value $0.01 per share, outstanding as of December 10, 2014 was 42,856,854.

TABLE OF CONTENTS

Financial Statements | |||

Fifth Street Asset Management Inc.: | |||

Fifth Street Management Group: | |||

Notes to Combined Financial Statements (unaudited) | |||

Management's Discussion and Analysis of Financial Condition and Results of Operations | |||

Item 3. | Defaults Upon Senior Securities | ||

Item 4. | Mine Safety Disclosures | ||

Signatures | |||

FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q may contain forward-looking statements within the meaning of section 27A of the Securities Act of 1933, as amended (the "Securities Act"), and Section 21E of the Securities Exchange Act of 1934 as amended, (the "Exchange Act"), that reflect our current views with respect to, among other things, future events and financial performance. You can identify these forward-looking statements by the use of forward-looking words such as "outlook," "believes," "expects," "potential," "continues," "may," "will," "should," "seeks," "approximately," "predicts," "intends," "plans," "estimates," "anticipates" or the negative version of those words or other comparable words. The forward-looking statements are based on our beliefs, assumptions and expectations of our future performance, taking into account all information currently available to us. Such forward-looking statements are subject to various risks and uncertainties and assumptions relating to our operations, financial results, financial condition, business prospects, growth strategy and liquidity. We believe these factors include but are not limited to those described under "Risk Factors" in our prospectus dated October 29, 2014, filed with the Securities and Exchange Commission (the "SEC") in accordance with Rule 424(b) of the Securities Act of 1933 on October 30, 2014, which is accessible on the SEC's website at www.sec.gov. These factors should not be construed as exhaustive and should be read in conjunction with the risk factors and other cautionary statements that are included or incorporated by reference in this Quarterly Report on Form 10-Q and in the prospectus. If one or more of these or other risks or uncertainties materialize, or if our underlying assumptions prove to be incorrect, our actual results may vary materially from those indicated in these forward-looking statements. New risks and uncertainties arise over time, and it is not possible for us to predict those events or how they may affect us. Therefore, you should not place undue reliance on these forward-looking statements. Any forward-looking statement speaks only as of the date on which it is made. We do not undertake any obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise, except as required by law.

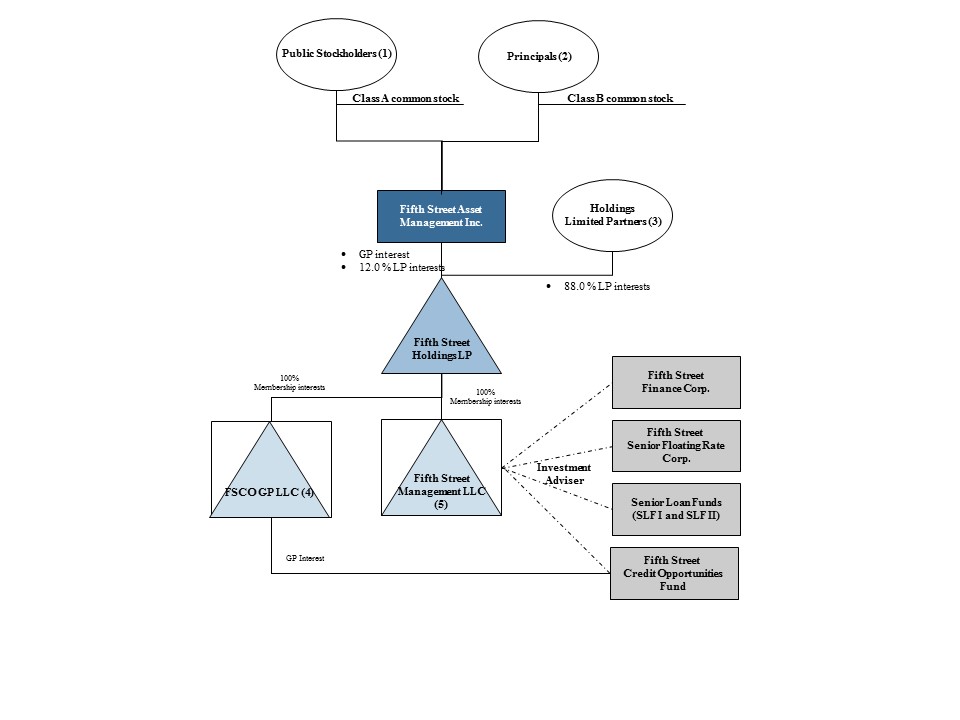

Fifth Street Asset Management Inc. "Fifth Street Asset Management" or "FSAM" was incorporated in Delaware on May 8, 2014 as a holding company with its primary asset expected to be a limited partnership interest in Fifth Street Holdings L.P. ("Fifth Street Holdings"). Prior to the consummation of our initial public offering ("IPO"), Fifth Street Asset Management Inc. had not commenced operations and had nominal assets and liabilities.

Pursuant to a reorganization (the "Reorganization") consummated in connection with our IPO, Fifth Street Asset Management Inc. became the general partner of Fifth Street Holdings, which became the sole managing member of Fifth Street Management LLC and FSCO GP LLC. As a holding company, Fifth Street Asset Management conducts all of its operations through Fifth Street Management LLC and FSCO GP LLC, wholly-owned subsidiaries of Fifth Street Holdings, including the provision of management services to Fifth Street Finance Corp., Fifth Street Senior Floating Rate Corp. and other affiliated private funds. Unless the context suggests otherwise, references in this Quarterly Report on Form 10-Q to (1) "Fifth Street," "we," "us" and "our" refer to our businesses, both before and after the consummation of our reorganization into a holding company structure and (2) our "Predecessor" refers to Fifth Street Management Group, our accounting predecessor, as well as the Combined Funds, in each case prior to the reorganization.

When used in this Quarterly Report on Form 10-Q, unless the context otherwise requires:

• | "Adjusted Net Income" represents net income attributable to controlling interests in Fifth Street Management Group as adjusted for (i) one-time compensation-related charges, including the amortization of equity-based awards, (ii) non-recurring underwriting costs relating to public offerings of our funds, (iii) non-recurring professional fees incurred in connection with our initial public offering and (iv) other non-recurring items; |

• | "AUM" refers to assets under management of the Fifth Street Funds and material control investments of these funds, and represents the sum of the net asset value of such funds and investments, the drawn debt and unfunded debt and equity commitments at the fund or investment-level (including amounts subject to restrictions) and uncalled committed debt and equity capital (including commitments to funds that have yet to commence their investment periods); |

• | "base management fees" refer to fees we earn for advisory services provided to our funds, which are generally based on a fixed percentage of fair value of assets, total commitments, invested capital, net asset value, total assets or par value of the investment portfolios managed by us; |

• | "catch-up" refers to a provision for a manager or adviser of a fund to receive the majority or all of the profits of such fund until the agreed upon profit allocation is reached; |

• | "Combined Funds" refers to FSOF, SLF I and SLF II; |

• | "fee-earning AUM" refers to the AUM on which we directly or indirectly earn management fees, and represents the sum of the net asset value of the Fifth Street Funds and their material control investments, and the drawn debt and unfunded debt and equity commitments at the fund or investment-level (including amounts subject to restrictions); |

• | "Fifth Street BDCs" and "our BDCs" refer to FSC and FSFR together; |

i

• | "FSOF" refers to "Fifth Street Opportunities Fund, L.P." (formerly Fifth Street Credit Opportunities Fund, L.P.), a hedge fund managed by Fifth Street Management; |

• | "Fifth Street Management" refers to Fifth Street Management LLC and, unless the context otherwise requires, its subsidiaries; |

• | "Fifth Street Management Group" refers to Fifth Street Management LLC, FSC, Inc., FSC CT, Inc., FSC Midwest, Inc., Fifth Street Capital West, Inc. (and their wholly-owned subsidiaries) and the Combined Funds; |

• | "FSC" refers to Fifth Street Finance Corp., a publicly traded business development company managed by Fifth Street Management; |

• | "FSFR" refers to Fifth Street Senior Floating Rate Corp., a publicly traded business development company managed by Fifth Street Management; |

• | "hurdle rate" or "hurdle" refers to a specified minimum rate of return that a fund must exceed in order for the adviser or manager of such a fund to receive performance fees; |

• | "management fees" refer to base management fees and Part I Fees; |

• | "Fifth Street Funds" and "our funds" refer to the Fifth Street BDCs and the other funds advised or managed by Fifth Street Management; |

• | "Holdings Limited Partners" refers to active, limited partners in Fifth Street Holdings (other than us), which include, among other persons, the Principals; |

• | "Part I Fees" refer to fees paid to us by our BDCs that are based on a fixed percentage of pre-incentive fee net investment income, which are calculated and paid quarterly, and subject to certain specified performance hurdles. Part I Fees are classified as management fees as they are predictable and are recurring in nature, are not subject to repayment (or clawback) and are generally cash-settled each quarter; |

• | "Part II Fees" refer to fees paid to us by our BDCs that are based on net capital gains, which are paid annually; |

• | "performance fees" refer to fees we earn based on the performance of a fund, which are generally based on certain specific hurdle rates as defined in the fund's investment management or partnership agreements, may be either an incentive fee or carried interest, are paid annually and also include Part II Fees; |

• | "permanent capital" refers to capital of funds that do not have redemption provisions or a requirement to return capital to investors upon exiting the investments made with such capital, except as required by applicable law, which funds currently consist of FSC and FSFR; such funds may be required to distribute all or a portion of capital gains and investment income or elect to distribute capital; |

• | "Principals" refers to Leonard M. Tannenbaum and Bernard D. Berman and, where applicable, any entities controlled directly or indirectly by them; |

• | "SLF I" refers to Fifth Street Senior Loan Fund I Operating Entity, LLC, a fund in our senior loan fund strategy managed by Fifth Street Management; |

• | "SLF II" refers to Fifth Street Senior Loan Fund II Operating Entity, LLC, a fund in our senior loan fund strategy managed by Fifth Street Management; |

• | "Structured Equity" refers to the investment strategy of Fifth Street Mezzanine Partners II, L.P., a fund advised by an affiliate of Fifth Street Management; and |

• | "TRA recipients" refers to the Principals and Ivelin M. Dimitrov. |

Many of the terms used in this Quarterly Report on Form 10-Q, including AUM, fee-earning AUM and Adjusted Net Income, may not be comparable to similarly titled measures used by other companies. In addition, our definitions of AUM and fee-earning AUM are not based on any definition of AUM or fee-earning AUM that is set forth in the agreements governing the investment funds that we manage and may differ from definitions of AUM set forth in other agreements to which we are a party from time to time. Please see "Management's Discussion and Analysis of Financial Condition and Results of Operations — Non-GAAP Financial Measures and Operating Metrics — Assets Under Management" and "— Fee-earning AUM" for more information on AUM and fee-earning AUM. Further, Adjusted Net Income is not a performance measure calculated in accordance with U.S. Generally Accepted Accounting Principles ("GAAP"). We use Adjusted Net Income as a measure of operating performance, not as a measure of liquidity. We believe that Adjusted Net Income provides investors with a meaningful indication of our core operating performance and Adjusted Net Income is evaluated regularly by our management as a decision tool for deployment of resources. We believe that reporting Adjusted Net Income is helpful in understanding our business and that investors should review the same supplemental non-GAAP financial measures that our management uses to analyze our performance. Adjusted Net Income has limitations as an analytical tool and should not be considered in isolation or as a substitute for analyzing our results prepared in accordance with GAAP. The use of Adjusted Net Income without consideration of related GAAP measures is not adequate due to the adjustments described above. See "Management's Discussion and Analysis of Financial Condition and Results of Operations — Non-GAAP Financial Measures and Operating Metrics — Adjusted Net Income."

Amounts and percentages throughout this Quarterly Report on Form 10-Q may reflect rounding adjustments and consequently totals may not appear to sum.

ii

PART I - FINANCIAL INFORMATION

Item 1. Financial Statements

Fifth Street Asset Management Inc.

Statement of Financial Condition

As of September 30, 2014

(unaudited)

Assets | ||||

Cash | $ | 1,000 | ||

Total assets | $ | 1,000 | ||

Stockholder's equity | ||||

Common stock, par value – $0.01 per share; 5,000 shares authorized, 33 shares issued and outstanding | $ | 1 | ||

Additional paid-in capital | 999 | |||

Total stockholder's equity | $ | 1,000 | ||

See notes to Statement of Financial Condition.

1

Fifth Street Asset Management Inc.

Notes to Statement of Financial Condition

(unaudited)

Note 1. Organization

In anticipation of its initial public offering (the "IPO") that closed November 4, 2014, Fifth Street Asset Management Inc. (the "Company" or "FSAM") was incorporated in Delaware on May 8, 2014 as a holding company with its primary asset expected to be a limited partnership interest in Fifth Street Holdings L.P. ("Fifth Street Holdings"). Fifth Street Holdings was formed on June 27, 2014 by Leonard M. Tannenbaum and another member of Fifth Street Management LLC (the "Principals") as a Delaware limited partnership. Prior to the transactions described below, the Principals were the general partners and limited partners of Fifth Street Holdings. Fifth Street Holdings has a single class of limited partnership interests (the "Holdings LP Interests"). Immediately prior to the IPO:

• | The Principals contributed the general partnership interests of Fifth Street Holdings to FSAM in exchange for 100% of the Company's Class B common stock, par value $0.01 per share (the "Class B Common Stock"); |

• | The members of Fifth Street Management LLC contributed 100% of their membership interests of Fifth Street Management LLC to Fifth Street Holdings in exchange for Holdings LP Interests; and |

• | The members of FSCO GP LLC ("FSCO GP"), a Delaware limited liability company, formed on January 6, 2014 to serve as the general partner of Fifth Street Opportunities Fund, L.P. (‘‘FSOF,'' formerly Fifth Street Credit Opportunities Fund, L.P.) contributed 100% of their membership interests in FSCO GP to Fifth Street Holdings in exchange for Holdings LP Interests. |

As a result of the above transactions, FSAM became the general partner of Fifth Street Holdings, which was also organized to be a holding company for Fifth Street Management LLC and FSCO GP. As a holding company, FSAM conducts all of its operations through Fifth Street Management LLC and FSCO GP, wholly-owned subsidiaries of Fifth Street Holdings, including the provision of management services to Fifth Street Finance Corp., Fifth Street Senior Floating Rate Corp. and other affiliated private funds. Fifth Street Management Group is the Company's accounting predecessor prior to the IPO.

In connection with the reorganization, FSAM entered into an exchange agreement (the "Exchange Agreement") with the Fifth Street Holdings Limited Partners that granted each Fifth Street Holdings Limited Partner and certain permitted transferees the right, beginning two years after the closing of the IPO and subject to vesting and minimum retained ownership requirements, on a quarterly basis, to exchange such person's Holdings LP Interests for shares of Class A common stock of FSAM, par value $0.01 per share (the "Class A Common Stock") on a one-for-one basis, subject to customary conversion rate adjustments for splits, unit distributions and reclassifications. As a result, each Fifth Street Holdings Limited Partner, over time, has the ability to convert his or her illiquid ownership interests in Fifth Street Holdings into Class A Common Stock that can more readily be sold in the public markets.

On November 4, 2014, FSAM issued 6,000,000 shares of Class A Common Stock in the IPO at a price of $17.00 per common share. The net proceeds totaled $95.9 million after deducting underwriting commissions of $6.1 million and before offering costs of approximately $3.7 million that were borne by the Company. The net proceeds were used to purchase a 12.0% limited partnership interest of Fifth Street Holdings from its limited partners. For reporting periods subsequent to its IPO, FSAM will consolidate the financial results of Fifth Street Holdings, its consolidated subsidiaries and certain private investment funds for all periods presented. The Company's Statement of Financial Condition as of September 30, 2014 does not reflect the effect of the reorganization, the IPO and the related transactions; which all occurred subsequent to the reporting date.

Our purchase of Holdings LP Interests concurrent with our IPO, and the subsequent and future exchanges by holders of Holdings LP Interests for shares of our Class A common stock pursuant to the Exchange Agreement is expected to result in increases in our share of the tax basis of the tangible and intangible assets of Fifth Street Holdings, which will increase the tax depreciation and amortization deductions that otherwise would not have been available to us. These increases in tax basis and tax depreciation and amortization deductions are expected to reduce the amount of cash taxes that we would otherwise be required to pay in the future. We have entered into a tax receivable agreement with the TRA Recipients that requires us to pay them 85% of the amount of cash savings, if any, in U.S. federal, state, local and foreign income tax that we actually realize (or, under certain circumstances, are deemed to realize) as a result of the increases in tax basis in connection with exchanges by the TRA Recipients described above and certain other tax benefits attributable to payments under the tax receivable agreement.

Immediately following the reorganization transactions described above and the closing of the IPO on November 4, 2014:

• | the Principals held 42,856,854 shares of Class B Common Stock and 42,856,854 Holdings LP Interests, the Holdings Limited Partners, including the Principals, held 44,000,000 Holdings LP Interests and FSAM held 6,000,000 Holdings LP Interests; and |

• | through their holdings of Class B Common Stock, the Principals, in the aggregate, had approximately 97.3% of the voting power of FSAM's common stock. |

2

Fifth Street Asset Management Inc.

Notes to Statement of Financial Condition

(unaudited)

As of September 30, 2014, the reorganization and IPO transactions described above had not yet occurred and the Company did not have an ownership interest in Fifth Street Holdings, and thus, did not commence its business operations through Fifth Street Management and FSCO GP. As a result the Company's Statement of Financial Condition does not reflect the operations of our current business. For reporting periods subsequent to the IPO, FSAM will consolidate the financial results of Fifth Street Holdings, its consolidated subsidiaries and certain private investment funds.

Note 2. Summary of Significant Accounting Policies

Basis of Accounting — The Statement of Financial Condition has been prepared in accordance with accounting principles generally accepted in the United States of America. Separate statements of operations, changes in stockholder's equity and cash flows have not been presented in the financial statements because there has been no activity that would impact those statements other than the reorganization transactions and reverse stock split.

Basis of Presentation — The unaudited Statement of Financial Condition and related notes have been prepared in accordance with accounting principles generally accepted in the United States of America ("GAAP") as set forth in the Financial Accounting Standards Board's ("FASB") Accounting Standards Codification ("ASC") and Rule 10-01 of Regulation S-X. Accordingly, certain information and footnote disclosures normally included in the financial statements prepared under GAAP have been condensed or omitted. In the opinion of management, all adjustments considered necessary for a fair statement of the Company's unaudited interim financial statement has been included and is of a normal and recurring nature.

Note 3. Stockholder's Equity

As of September 30, 2014, the Company was authorized to issue 5,000 shares of common stock, par value $0.01 per share. In exchange for $1,000, the Company has issued 100 shares of common stock, all of which were held by Leonard M. Tannenbaum, as of September 30, 2014.

Note 4. Subsequent Events

The Company has evaluated subsequent events through the date of issuance of the Statement of Financial Condition and has determined the following event requires disclosure, in addition to the reorganization and the IPO transactions discussed above:

On October 13, 2014, the Company effectuated a one-for-three reverse stock split and amended its certificate of incorporation to allow for the issuance of 500,000,000 shares of Class A common stock, 50,000,000 shares of Class B common stock and 5,000,000 shares of preferred stock, all with a par value of $0.01 per share.

3

Fifth Street Management Group

(Predecessor to Fifth Street Asset Management Inc.)

Combined Statements of Financial Condition

As of | ||||||||

September 30, 2014 | December 31, 2013 | |||||||

(unaudited) | ||||||||

Assets | ||||||||

Cash and cash equivalents | $ | 344,499 | $ | 4,015,728 | ||||

Management fees receivable (includes Part I Fees of $10,244,392 and $9,054,422 at September 30, 2014 and December 31, 2013, respectively) | 23,091,676 | 21,409,763 | ||||||

Performance fees receivable | 54,826 | — | ||||||

Prepaid expenses | 400,970 | 142,033 | ||||||

Due from affiliates | 1,955,882 | 3,848,491 | ||||||

Fixed assets, net | 10,307,333 | 1,436,681 | ||||||

Other assets | 6,274,707 | 2,652,975 | ||||||

Assets of Combined Funds: | ||||||||

Cash and cash equivalents | 35,139,719 | — | ||||||

Investments at fair value | 376,072,358 | — | ||||||

Derivative assets at fair value | 155,240 | — | ||||||

Interest and dividends receivable | 626,772 | — | ||||||

Unsettled trades receivable | 36,392,084 | — | ||||||

Collateral receivable | 4,570,487 | — | ||||||

Deferred financing costs | 2,540,792 | — | ||||||

Total assets | $ | 497,927,345 | $ | 33,505,671 | ||||

Liabilities and Equity | ||||||||

Liabilities | ||||||||

Accounts payable and accrued expenses | $ | 5,323,209 | $ | 1,198,205 | ||||

Accrued compensation and benefits | 7,422,583 | 538,035 | ||||||

Due to former member | 1,379,214 | 2,093,437 | ||||||

Loan payable | 4,000,000 | 4,000,000 | ||||||

Due to affiliates | 143,130 | 2,671,334 | ||||||

Deferred rent liability | 3,220,032 | 1,980,146 | ||||||

Liabilities of Combined Funds: | ||||||||

Accounts payable and accrued expenses | 474,345 | — | ||||||

Payments in advance from portfolio companies | 4,826,501 | — | ||||||

Securities sold short at fair value | 3,138,808 | — | ||||||

Unsettled trades payable | 110,464,323 | — | ||||||

Interest payable | 1,421,607 | — | ||||||

Notes payable | 213,488,434 | — | ||||||

Total liabilities | 355,302,186 | 12,481,157 | ||||||

Commitments and contingencies | ||||||||

Redeemable non-controlling interests in Combined Fund | 50,248,636 | — | ||||||

Non-controlling interests in Combined Funds | 67,222,460 | — | ||||||

Members' equity | 25,154,063 | 21,024,514 | ||||||

Total equity | 92,376,523 | 21,024,514 | ||||||

Total liabilities, redeemable non-controlling interests and equity | $ | 497,927,345 | $ | 33,505,671 | ||||

All management and performance fees are earned from affiliates of the Company. See notes to combined financial statements.

4

Fifth Street Management Group

(Predecessor to Fifth Street Asset Management Inc.)

Combined Statements of Income

(unaudited)

For the Three Months Ended September 30, | For the Nine Months Ended September 30, | |||||||||||||||

2014 | 2013 | 2014 | 2013 | |||||||||||||

Revenues | ||||||||||||||||

Management fees (includes Part I Fees of $10,244,392 and $7,174,961 and $27,983,472 and $21,518,635 for the three and nine months ended September 30, 2014 and 2013, respectively) | $ | 23,091,676 | $ | 16,891,382 | $ | 68,144,517 | $ | 47,049,812 | ||||||||

Performance fees (includes Part II fees of $54,826 for the three and nine months ended September 30, 2014) | 139,049 | — | 139,049 | — | ||||||||||||

Other fees | 2,187,933 | 753,768 | 4,205,987 | 3,188,954 | ||||||||||||

Total revenues | 25,418,658 | 17,645,150 | 72,489,553 | 50,238,766 | ||||||||||||

Expenses | ||||||||||||||||

Compensation and benefits | 6,529,830 | 6,377,780 | 25,711,012 | 16,077,114 | ||||||||||||

Fund offering and start-up expenses | 909,681 | 5,570,735 | 1,200,434 | 5,663,002 | ||||||||||||

Expenses of Combined Funds | 256,273 | — | 298,530 | — | ||||||||||||

General, administrative and other expenses | 3,432,949 | 1,226,437 | 7,491,543 | 3,575,267 | ||||||||||||

Depreciation and amortization | 408,541 | 51,664 | 641,449 | 153,592 | ||||||||||||

Total expenses | 11,537,274 | 13,226,616 | 35,342,968 | 25,468,975 | ||||||||||||

Other income (expense) | ||||||||||||||||

Interest and other income (expense), net | 42,685 | 2,648 | 68,735 | 11,378 | ||||||||||||

Interest and other income of Combined Funds | 3,325,341 | — | 5,045,949 | — | ||||||||||||

Interest expense of Combined Funds | (1,591,675 | ) | — | (2,578,659 | ) | — | ||||||||||

Net realized gain on investments of Combined Funds | 686,671 | — | 1,402,501 | — | ||||||||||||

Net change in unrealized appreciation (depreciation) on investments of Combined Funds | 974,134 | — | 2,061,861 | — | ||||||||||||

Net realized gain on derivatives of Combined Funds | 63,089 | 63,089 | ||||||||||||||

Net change in unrealized appreciation on derivatives of Combined Funds | 155,240 | — | 155,240 | — | ||||||||||||

Total other income, net | 3,655,485 | 2,648 | 6,218,716 | 11,378 | ||||||||||||

Net income | 17,536,869 | 4,421,182 | 43,365,301 | 24,781,169 | ||||||||||||

Net income attributable to redeemable non-controlling interests in Combined Fund | (1,072,218 | ) | — | (2,336,539 | ) | — | ||||||||||

Net income attributable to non-controlling interests in Combined Funds | (1,909,540 | ) | — | (2,924,678 | ) | — | ||||||||||

Net income attributable to controlling interests in Fifth Street Management Group | $ | 14,555,111 | $ | 4,421,182 | $ | 38,104,084 | $ | 24,781,169 | ||||||||

All revenues are earned from affiliates of the Company. See notes to combined financial statements.

5

Fifth Street Management Group

(Predecessor to Fifth Street Asset Management Inc.)

Combined Statement of Changes in Equity and Redeemable Non-Controlling Interests in Combined Fund

For the Nine Months Ended September 30, 2014

(unaudited)

Members' Equity | Non-Controlling Interests in Combined Funds | Total Equity | Redeemable Non-Controlling Interests in Combined Fund | |||||||||||||

Balance, December 31, 2013 | $ | 21,024,514 | $ | — | $ | 21,024,514 | $ | — | ||||||||

Capital contributions from members | 2,967,749 | — | 2,967,749 | — | ||||||||||||

Amortization of equity-based compensation | 1,487,646 | — | 1,487,646 | — | ||||||||||||

Reclassification of distributions to former member | 800,381 | — | 800,381 | — | ||||||||||||

Purchase of former member interests | 2,327,548 | 2,327,548 | ||||||||||||||

Capital contributions to Fifth Street Opportunities Fund, L.P. | — | — | — | 47,912,097 | ||||||||||||

Capital contributions to Fifth Street Senior Loan Fund I Operating Entity, LLC | — | 33,857,927 | 33,857,927 | — | ||||||||||||

Capital contributions to Fifth Street Senior Loan Fund II Operating Entity, LLC | — | 30,500,000 | 30,500,000 | — | ||||||||||||

Distributions | (41,557,859 | ) | (60,145 | ) | (41,618,004 | ) | — | |||||||||

Net income | 38,104,084 | 2,924,678 | 41,028,762 | 2,336,539 | ||||||||||||

Balance, September 30, 2014 | $ | 25,154,063 | $ | 67,222,460 | $ | 92,376,523 | $ | 50,248,636 | ||||||||

See notes to combined financial statements.

6

Fifth Street Management Group

(Predecessor to Fifth Street Asset Management Inc.)

Combined Statements of Cash Flows

(unaudited)

For the Nine Months Ended September 30, | ||||||||

2014 | 2013 | |||||||

Cash flows from operating activities | ||||||||

Net income | $ | 43,365,301 | $ | 24,781,169 | ||||

Adjustments to reconcile net income to net cash provided by (used in) operating activities: | ||||||||

Depreciation and amortization | 641,449 | 153,592 | ||||||

Amortization of equity-based compensation | 3,815,194 | 1,254,961 | ||||||

Reclassification of distributions to former member | 800,381 | — | ||||||

Fair value adjustment – due to former member | 180,863 | (250,772 | ) | |||||

Deferred rent | 1,239,886 | 19,597 | ||||||

Attributable to Combined Funds: | ||||||||

Net realized gain on investments of Combined Funds | (1,402,501 | ) | — | |||||

Net change in unrealized appreciation on investments of Combined Funds | (2,061,861 | ) | — | |||||

Net realized gain on derivatives of Combined Funds | (63,089 | ) | — | |||||

Net change in unrealized appreciation on derivatives of Combined Funds | (155,240 | ) | — | |||||

Accretion of original issue discount on investments of Combined Funds | (160,000 | ) | — | |||||

Changes in operating assets and liabilities: | ||||||||

Management fees receivable | (1,681,913 | ) | (14,082,955 | ) | ||||

Performance fees receivable | (54,826 | ) | — | |||||

Prepaid expenses | (258,937 | ) | 58,374 | |||||

Due from affiliates | 1,892,609 | (271,200 | ) | |||||

Other assets | (272,462 | ) | (14,819 | ) | ||||

Accounts payable and accrued expenses | 724,613 | (91,054 | ) | |||||

Accrued compensation and benefits | 6,884,548 | 6,322,544 | ||||||

Due to former member | (895,086 | ) | (647,286 | ) | ||||

Due to affiliates | (2,528,204 | ) | 346,333 | |||||

Attributable to Combined Funds: | ||||||||

Purchases of investments of Combined Funds | (428,151,956 | ) | — | |||||

Proceeds from sales of investments of Combined Funds | 129,587,772 | — | ||||||

Purchases and covers of short positions | (14,935,684 | ) | — | |||||

Proceeds from sales of investments sold short | 18,326,008 | — | ||||||

Receivable from counterparty | (4,570,487 | ) | — | |||||

Change in other assets of Combined Funds | (626,772 | ) | — | |||||

Change in other liabilities of Combined Funds | 6,722,453 | — | ||||||

Net cash provided by (used in) operating activities | (243,637,941 | ) | 17,578,484 | |||||

Cash flows from investing activities | ||||||||

Purchases of fixed assets | (9,460,980 | ) | (216,799 | ) | ||||

Net cash used in investing activities | (9,460,980 | ) | (216,799 | ) | ||||

Cash flows from financing activities | ||||||||

Distributions to members | (38,590,110 | ) | (27,885,614 | ) | ||||

Attributable to Combined Funds: | ||||||||

Capital contributions from redeemable non-controlling interests | 47,912,097 | — | ||||||

Capital contributions from non-controlling interests | 64,357,927 | — | ||||||

Distributions to non-controlling interests | (60,145 | ) | — | |||||

Issuance of notes payable by Combined Funds | 213,488,434 | — | ||||||

Deferred financing costs | (2,540,792 | ) | — | |||||

Net cash provided by (used in) financing activities | 284,567,411 | (27,885,614 | ) | |||||

Net increase (decrease) in cash and cash equivalents | 31,468,490 | (10,523,929 | ) | |||||

Cash and cash equivalents, beginning of period | 4,015,728 | 16,156,777 | ||||||

Cash and cash equivalents, end of period (including Combined Funds) | 35,484,218 | 5,632,848 | ||||||

Less: Cash and cash equivalents of the Combined Funds | 35,139,719 | — | ||||||

Cash and cash equivalents of the Company, end of period | $ | 344,499 | $ | 5,632,848 | ||||

Supplemental disclosures of cash flow information | ||||||||

Cash paid during the period for interest | $ | 74,795 | $ | — | ||||

Cash paid during the period for interest - Combined Funds | $ | 915,921 | $ | — | ||||

Non-cash investing activities: | ||||||||

Fixed asset purchases included in accounts payable | $ | 51,121 | $ | — | ||||

Non-cash financing activities: | ||||||||

Non-cash capital contribution by member | $ | 2,967,749 | $ | 5,680,001 | ||||

Non-cash distribution to member | $ | (2,967,749 | ) | $ | (5,680,001 | ) | ||

7

Fifth Street Management Group

(Predecessor to Fifth Street Asset Management Inc.)

Notes to Combined Financial Statements

For the Nine Months Ended September 30, 2014

(unaudited)

Note 1. Organization and Basis of Presentation

Organization

Fifth Street Management Group (the "Company") is an alternative asset management firm headquartered in Greenwich, CT that provides asset management services to its investment funds, primarily consisting of Fifth Street Finance Corp. (formed on January 2, 2008, "FSC") and Fifth Street Senior Floating Rate Corp. (formed on May 22, 2013, "FSFR"), both publicly traded business development companies regulated under the Investment Company Act of 1940 (together, the "BDCs").

The investment advisory business of the Fifth Street Management Group is presently conducted through the following affiliated entities:

• | Fifth Street Management LLC ("FSM"), a limited liability company organized under the laws of the State of Delaware on March 8, 2007 under its original name of FSC Management LLC to provide asset management services. The Company conducts substantially all of its asset management services through FSM, including those provided to the BDCs. |

• | FSC CT, Inc. ("FSC CT"), a Connecticut corporation, formed on March 28, 2012 to provide administrative services related primarily to the Company's activities in Connecticut and, effective January 1, 2014, to provide administrative services to the BDCs and FSM. |

• | FSC, Inc., a New York corporation, formed on January 3, 2007 to provide administrative services to the BDCs and FSM through December 31, 2013. |

• | Fifth Street Capital LLC, a limited liability company organized under the laws of the State of New York on July 14, 2004 for the purpose of providing administrative and investment advisory services to Fifth Street Mezzanine Partners II, L.P. ("Fund II", an uncombined affiliate) and other entities which may be formed from time to time. Fifth Street Capital LLC is a wholly-owned subsidiary of FSC, Inc. |

• | FS Transportation LLC ("FS Transportation") is a limited liability company organized under the laws of the State of Connecticut on March 2, 2010 and provides transportation services to the Company's officers and employees. FS Transportation is a wholly-owned subsidiary of FSC, Inc. |

• | FSC Midwest, Inc., an Illinois corporation, formed on March 28, 2012 to provide administrative services related primarily to the Company's activities in the midwestern United States. |

• | Fifth Street Capital West, Inc., a California corporation, formed on December 26, 2006 to provide administrative services related primarily to the Company's activities in the western United States. |

In addition to the above entities, subsequent to December 31, 2013, the Company has included the following entities in the Combined Financial Statements:

• | FSCO GP LLC ("FSCO GP"), a Delaware limited liability company, formed on January 6, 2014 to serve as the general partner of Fifth Street Opportunities Fund, L.P. ("FSOF," formerly Fifth Street Credit Opportunities Fund, L.P.), which primarily invests in yield-oriented corporate credit assets and equities; and |

• | Fifth Street EIV, LLC ("Fifth Street EIV"), a Delaware limited liability company formed on February 7, 2014 to hold FSM's equity interest in Fifth Street Senior Loan Fund I Operating Entity, LLC ("SLF I"), which primarily invests in senior secured loans to middle-market companies. |

• | Fifth Street EIV II, LLC ("Fifth Street EIV II"), a Delaware limited liability company formed on July 10, 2014 to hold FSM employees' equity interests in Fifth Street Senior Loan Fund II Operating Entity, LLC ("SLF II"), which primarily invests in senior secured loans to middle-market companies. |

FSOF, SLF I and SLF II are collectively referred to as the "Combined Funds." See Note 2 for further information on the consolidation of these funds.

The Company's primary sources of revenues are management fees, primarily from the BDCs, which are driven by the amount of the assets under management and quarterly investment performance of the funds it manages.

The Company conducts substantially all of its operations through one reportable segment which provides asset management services to its alternative investment vehicles. The Company generates all of its revenues in the United States.

8

Fifth Street Management Group

(Predecessor to Fifth Street Asset Management Inc.)

Notes to Combined Financial Statements

For the Nine Months Ended September 30, 2014

(unaudited)

Basis of Presentation

The unaudited interim combined financial statements and related notes have been prepared in accordance with accounting principles generally accepted in the United States of America ("GAAP") as set forth in the Financial Accounting Standards Board's ("FASB") Accounting Standards Codification ("ASC") and Rule 10-01 of Regulation S-X. Accordingly, certain information and footnote disclosures normally included in the combined financial statements prepared under GAAP have been condensed or omitted. In the opinion of management, all adjustments considered necessary for a fair statement of the Company's unaudited interim combined financial statements have been included and are of a normal and recurring nature. The operating results presented for the interim periods are not necessarily indicative of the results that may be expected for any other interim period or for the entire year. These combined financial statements should be read in conjunction with the Company's audited combined financial statements as of and for the years ended December 31, 2013 and 2012 and notes thereto included in Fifth Street Asset Management Inc.'s final prospectus dated October 29, 2014 filed with the Securities and Exchange Commission ("SEC") in accordance with Rule 424(b) of the Securities Act of 1933 on October 30, 2014. The December 31, 2013 Combined Statement of Financial Condition data was derived from the audited combined financial statements at that date. All significant intercompany transactions and balances have been eliminated in combination.

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions affecting amounts reported in the combined financial statements and accompanying notes. The most significant of these estimates are related to (i) fair value measurements of the assets and liabilities of the Combined Funds; (ii) the valuation of equity-based compensation, and (iii) estimating the fair value of the amount due to a former member. These estimates are based on the information that is currently available to the Company and on various other assumptions that the Company believes to be reasonable under the circumstances. Actual results could differ materially from those estimates under different assumptions and conditions.

The Company has not presented earnings per share amounts in the Combined Statements of Income as they would not be meaningful based on the Company’s ownership structure as of the date of these combined financial statements. Additionally, the subsequent reorganization (as discussed in Note 12) has significantly changed the ownership of the Company, and therefore, has not been presented retroactively.

The combined financial statements include the accounts of the above affiliated entities, all of which are either wholly or substantially owned and/or under the voting control of the managing member, Leonard M. Tannenbaum (collectively, the "Fifth Street Management Group") and do not reflect the effect of the reorganization, the initial public offering and related transactions which occurred after September 30, 2014 (see Note 12).

The "members" refer to the managing member, seven other existing equity members and five other existing non-equity members.

Note 2. Significant Accounting Policies

Principles of Consolidation

The combined financial statements include the accounts of the Company and entities in which it, directly or indirectly, is determined to have a controlling financial interest under the following set of guidelines:

• | Variable Interest Entities ("VIEs") — The Company determines whether, if by design, an entity has equity investors who lack the characteristics of a controlling financial interest or does not have sufficient equity at risk to finance its expected activities without additional subordinated financial support from other parties. If an entity has either of these characteristics, it is considered a VIE and must be consolidated by its primary beneficiary. An enterprise is determined to be the primary beneficiary if it holds a controlling financial interest. A controlling financial interest is defined as (a) the power to direct the activities of a VIE that most significantly impact the entity's economic performance and (b) the obligation to absorb losses of the entity or the right to receive benefits from the entity that could potentially be significant to the VIE. The consolidation guidance requires an analysis to determine (a) whether an entity in which the Company holds a variable interest is a VIE and (b) whether the Company's involvement, through holding interests directly or indirectly in the entity or contractually through other variable interests (for example, management and performance related fees), would give it a controlling financial interest. Performance of that analysis requires the exercise of judgment. Certain VIEs qualify for the deferral under ASU 2010-10, Amendments to Statement 167 for Certain Investment Funds, if the following criteria are met: |

a. | The entity has all of the attributes of an investment company as defined in the American Institute of Certified Public Accountants Accounting and Auditing Guide, Investment Companies ("Investment Company Guide"), |

9

Fifth Street Management Group

(Predecessor to Fifth Street Asset Management Inc.)

Notes to Combined Financial Statements

For the Nine Months Ended September 30, 2014

(unaudited)

or does not have all the attributes of an investment company but it is an entity for which it is acceptable based on industry practice to apply measurement principles that are consistent with the Investment Company Guide,

b. | The reporting entity does not have explicit or implicit obligations to fund any losses of the entity that could potentially be significant to the entity, and |

c. | The entity is not a securitization or asset-backed financing entity or an entity that was formerly considered a qualifying special purpose entity. |

Where the VIEs have qualified for the deferral of the current consolidation guidance, the analysis is based on previous consolidation guidance. This guidance requires an analysis to determine (a) whether an entity in which the Company holds a variable interest is a variable interest entity and (b) whether the Company's involvement, through holding interests directly or indirectly in the entity or contractually through other variable interests (for example, management and performance related fees), would be expected to absorb a majority of the variability of the entity.

Under both guidelines, the Company determines whether it is the primary beneficiary of a VIE at the time it becomes involved with a variable interest entity and reconsiders that conclusion continually. In evaluating whether the Company is the primary beneficiary, the Company evaluates its economic interests in the entity held either directly by the Company and its affiliates or indirectly through employees. The consolidation analysis can generally be performed qualitatively; however, if it is not readily apparent that the Company is not the primary beneficiary, a quantitative analysis may also be performed. Investments and redemptions (either by the Company, affiliates of the Company or third parties) or amendments to the governing documents of the respective investment funds could affect an entity's status as a VIE or the determination of the primary beneficiary. At each reporting date, the Company assesses whether it is the primary beneficiary and will consolidate or deconsolidate accordingly.

The Company has not consolidated any entities into the combined financial statements under the VIE model as it does not have an interest in any VIE.

• | Voting Interest Entities — For entities that are not VIEs, the Company consolidates those entities in which it has an equity investment of greater than 50% and has control over significant operating, financial and investing decisions of the entity. Additionally, the Company consolidates entities in which the Company is a substantive, controlling general partner and the limited partners have no substantive rights to participate in the ongoing governance and operating activities. |

The Company has determined that FSOF should be consolidated by FSCO GP as the limited partners of FSOF do not have substantive kick-out or participating rights. The Company has included the results of FSCO GP in its combined financial statements as it is under common control of the managing member.

The Company has determined that SLF I should be consolidated by FSM (the manager of SLF I and a combined entity) as the investors of SLF I do not have substantive kick-out or participating rights.

The Company has determined that SLF II should be consolidated by FSM (the manager of SLF II and a combined entity) as the investors of SLF II do not have substantive kick-out or participating rights.

Including the results of the Combined Funds significantly increases the reported amounts of the assets, liabilities, revenues, expenses and cash flows of the Company; however, the Combined Funds results included herein have no direct effect on the net income attributable to controlling interests or on total controlling equity. Instead, economic ownership interests of the investors in the Combined Funds are reflected as redeemable non-controlling interests with respect to FSOF and non-controlling interests with respect to SLF I and SLF II, in the accompanying combined financial statements.

Concentration of Credit Risk and Other Risks and Uncertainties

Financial instruments which potentially subject the Company to concentrations of credit risk consist primarily of cash and cash equivalents. The Company maintains its cash and cash equivalents with high-credit quality financial institutions.

For the nine months ended September 30, 2014 and 2013, 100% of revenues and receivables were earned or derived from advisory or administrative services provided to the BDCs and other affiliated entities.

The Company is dependent on the managing member for all key decisions and its continued business operations. If for any reason the services of our managing member were to become unavailable, there could be a material adverse effect on the Company's operations, liquidity and profitability.

10

Fifth Street Management Group

(Predecessor to Fifth Street Asset Management Inc.)

Notes to Combined Financial Statements

For the Nine Months Ended September 30, 2014

(unaudited)

Fair Values of Financial Instruments

The carrying amounts of cash and cash equivalents, management and performance fees receivable from affiliates, prepaid expenses, due from/to affiliates, accounts payable and accrued expenses and accrued compensation and benefits approximate fair value due to the immediate or short-term maturity of these financial instruments. The fair value of the amount due to a former member was determined using the present value of the expected future payments. The fair value of the loan payable is determined using current applicable rates for similar instruments as of the date of the Combined Statement of Financial Condition and approximates the carrying value of such debt.

Cash and Cash Equivalents

Cash equivalents include short-term, highly liquid investments that are readily convertible to known amounts of cash and have original maturities of three months or less. The Company and its Combined Funds place its cash and cash equivalents with U.S. financial institutions and, at times, amounts may exceed federally insured limits. The Company and its Combined Funds monitor the credit standing of these financial institutions.

Cash and cash equivalents held at the Combined Funds, which includes amounts held by prime brokers, represent cash that, although not legally restricted, is not available to support the liquidity needs of the Company, as the use of such amounts is limited to the investment activities of the Combined Funds.

Fixed Assets

Fixed assets consist of furniture, fixtures and equipment (including automobiles, computer hardware and software) and leasehold improvements, and are recorded at cost, less accumulated depreciation and amortization. Depreciation of furniture, fixtures and equipment is computed using the straight-line method over the estimated useful lives of the respective assets (three to eight years). Amortization of improvements to leased properties is computed using the straight-line method based upon the initial term of the applicable lease or the estimated useful life of the improvements, whichever is shorter, and ranges from five to 10 years. Routine expenditures for repairs and maintenance are charged to expense when incurred. Major betterments and improvements are capitalized. Upon retirement or disposition of fixed assets, the cost and related accumulated depreciation are removed from the accounts and any resulting gain or loss is recognized in the Combined Statements of Income. The Company evaluates fixed assets for impairment whenever events or changes in circumstances indicate that an asset's carrying value may not be fully recovered. During the three months ended September 30, 2014, the Company wrote-off leasehold improvements in connection with the lease terminations discussed in Note 9. No other impairments were deemed necessary for the nine months ended September 30, 2014 and 2013.

Deferred Rent

The Company recognizes rent expense on a straight-line basis over the expected lease term. Within the provisions of certain leases, there are free rent periods and escalations in payments over the base lease term. The effects of these items have been reflected in rent expense on a straight-line basis over the expected lease term. Landlord contributions and tenant allowances are included in the straight-line calculations and are being deferred over the lease term and are reflected as a reduction in rent expense.

Redeemable Non-controlling Interests

The Company consolidates a credit-focused hedge fund (FSOF) that it manages, wherein investors are able to redeem their interests, in cash or in kind or both, after an initial lock-up period of one year, without penalty. Amounts relating to these fund investors' interests in FSOF are presented as redeemable non-controlling interests in the Combined Statements of Financial Condition. Allocations of profits and losses to these interests are reflected within net income attributable to redeemable non-controlling interests in the Combined Statements of Income. The allocation of net income or loss to redeemable non-controlling interests in the Combined Fund is based on the relative ownership interests of the limited partners after the consideration of contractual arrangements that govern allocations of income or loss. These interests are adjusted for general partner allocations and by subscriptions and redemptions in funds that occur during the period.

Non-controlling Interests

In addition to the members' interests in the Fifth Street Management Group, the Company also consolidates senior loan funds (SLF I and SLF II) in which non-controlling interests are present. Amounts relating to the fund's investors' interests in SLF I and SLF II are presented as non-controlling interests in the Combined Statements of Financial Condition. Allocations of profits and losses to these interests are reflected within net income attributable to non-controlling interests in the Combined Statements of Income. Investors in this fund presented within non-controlling interests are not able to redeem their interests until the fund liquidates or is otherwise wound-up.

11

Fifth Street Management Group

(Predecessor to Fifth Street Asset Management Inc.)

Notes to Combined Financial Statements

For the Nine Months Ended September 30, 2014

(unaudited)

Non-controlling interest holders in SLF I and SLF II owned approximately 72.8% of the Company's combined total equity as of September 30, 2014.

Revenue Recognition

The Company has two principal sources of revenues: management fees and performance fees. These revenues are derived from the Company's agreements with the funds it manages, primarily the BDCs. The advisory agreements, on which revenues are based, are generally renewable on an annual basis by the general partner or the board of directors of the respective funds.

Management Fees

Management fees are generally based on a defined percentage of fair value of assets, total commitments, invested capital, net asset value ("NAV"), net investment income, total assets or par value of the investment portfolios managed by the Company. All management fees are earned from affiliated funds of the Company. The contractual terms of management fees vary by fund structure and investment strategy and range from 0.40% to 2.00% for base management fees, which are asset or capital-based.

Management fees from affiliates also include quarterly incentive fees on the net investment income from the BDCs ("Part I Fees"). Part I Fees are generally equal to 20.0% of the BDCs net investment income (before Part I Fees and performance fees payable based on capital gains), subject to fixed "hurdle rates" as defined in the respective investment advisory agreement. No fees are recognized until the BDCs net investment income exceeds the respective hurdle rate, with a "catch-up" provision that serves to ensure the Company receives 20% of the BDCs net investment income from the first dollar earned. Such fees are classified as management fees as they are paid quarterly, predictable and recurring in nature, not subject to repayment (or clawback) and cash settled each quarter. Management fees from affiliates are recognized as revenue in the period advisory services are rendered, subject to the Company's assessment of collectability.

Performance Fees

Performance fees are earned from the funds managed by the Company based on the performance of the respective funds. The contractual terms of performance fees vary by fund structure and investment strategy and are generally 15.0% to 20.0%.

The Company has elected to adopt Method 2 of ASC 605-20, Revenue Recognition ("ASC 605") for revenue based on a formula. Under this method, the Company records revenue when it is entitled to performance-based fees, subject to certain hurdles or benchmarks. The performance fees for any period are based upon an assumed liquidation of the fund's net assets on the reporting date, and distribution of the net proceeds in accordance with the fund's income allocation provisions. The performance fees may be subject to reversal to the extent that the performance fees recorded exceed the amount due to the general partner or investment manager based on a fund's cumulative investment returns.

Performance fees related to the BDCs ("Part II Fees") are calculated and payable in arrears as of the end of each fiscal year of the BDCs and equal 20% of the BDCs realized capital gains, if any, on a cumulative basis since inception, computed net of all realized capital losses and unrealized capital depreciation on a cumulative basis, less the aggregate amount of any previously paid capital gain incentive fees.

Other Fees

The Company also provides administrative services to the BDCs that are reported within Revenues — Other fees. These fees are recognized as revenue in the period administrative services are rendered. These fees generally represent the portion of compensation, overhead and other expenses incurred by the Company directly attributable to the funds, but may also be based on a fund's asset value. The Company selects the vendors, incurs the expenses, and is the primary obligor under the related arrangements. The Company is considered the principal under these arrangements and is required to record the expense and related reimbursement revenue on a gross basis. Other fees are recognized in the periods during which the related expenses are incurred and the reimbursements are contractually earned.

Compensation and Benefits

Compensation generally includes salaries, bonuses and equity-based compensation charges. Bonuses are accrued over the service period to which they relate. All payments made to the Company's managing member since inception and all payments made to equity members since December 1, 2012 (see Note 11) related to their granted or purchased interests are accounted for as distributions on the equity held by such members.

Equity-Based Compensation

Compensation expense related to the issuance of equity-based awards is measured at fair value of the award on the grant date, in excess of any amounts paid for the interest, and is recognized on a straight-line basis over the requisite service period, with a corresponding increase in members' equity. Equity-based compensation expense is adjusted, as necessary, for actual

12

Fifth Street Management Group

(Predecessor to Fifth Street Asset Management Inc.)

Notes to Combined Financial Statements

For the Nine Months Ended September 30, 2014

(unaudited)

forfeitures so as to reflect expenses only for the portion of the award that ultimately vests. Equity-based compensation expense is presented within compensation and benefits in the Combined Statements of Income. Cash settled equity-based awards are classified as liabilities and are re-measured at the end of each reporting period using the intrinsic-value method (that is, current settlement value), as permitted for non-public companies under ASC 718.

Part I Fee-Sharing Arrangements

The Company also has fee-sharing arrangements whereby certain employees or members are entitled to a share of Part I Fees. These fees are typically paid to the Company and are then paid to the participant on a quarterly basis. To the extent that the payments to the employees or non-equity members are probable and reasonably estimable, the Company accrues these payments as compensation expense.

Reimbursable Expenses

In the normal course of business, the Company pays certain expenses on behalf of the BDCs, primarily for professional travel and other costs associated with particular portfolio company holdings of the BDCs, for which it is reimbursed. Such expenses are not an obligation of the Company and are recorded as due from affiliates at the time of disbursement (see Note 10).

Fund Offering and Start-up Expenses

In certain instances, the Company may bear offering costs related to capital raising activities of the BDCs, including underwriting commissions, which are expensed as incurred. In addition, the Company expenses all costs associated with starting a new investment fund. Included in the Statement of Income for the nine months ended September 30, 2014, is approximately $822,000 of expenses associated with a follow-on equity offering of FSC. Included in the Statement of Income for the nine months ended September 30, 2013 is approximately $5,659,000 of expenses associated with the initial public offering of FSFR.

Income Taxes

Substantially all of the Company's earnings flow through to owners of the Company without being subject to entity level income taxes. Accordingly, no provision for income taxes has been recorded in the combined financial statements.

The Company has no unrecognized tax benefits at September 30, 2014 and December 31, 2013. The Company's Federal and state income tax returns prior to fiscal year 2010 are closed and management continually evaluates expiring statutes of limitations, audits, proposed settlements, changes in tax law and new authoritative rulings.

The Company recognizes interest and penalties associated with tax matters such as franchise tax liabilities, if applicable, as general and administrative and other expenses.

Market and Other Risk Factors

Due to the nature of the Combined Funds' investment strategy, the Company is subject to market and other risk factors, including, but not limited to the following:

Market Risk

The market price of investments may significantly fluctuate during the period of investment. Investments may decline in value due to factors affecting securities markets generally or particular industries represented in the securities markets. The value of an investment may decline due to general market conditions which are not specifically related to such investment, such as real or perceived adverse economic conditions, changes in the general outlook for corporate earnings, changes in interest or currency rates or adverse investor sentiment generally. They may also decline due to factors that affect a particular industry or industries, such as labor shortages or increased production costs and competitive conditions within an industry.

FSOF may sell securities short which allows it to profit from declines in market prices to the extent such decline exceeds the transaction costs and any costs of borrowing. A short sale involves the sale of a security that is not owned in the expectation of purchasing the same security at a later date at a lower price. To make delivery to the buyer, FSOF must borrow the security, and is obligated to pay the lender of the security any dividend or interest payable on the security until it returns the security to the lender. This is accomplished by a later purchase of the security by FSOF. A short sale, which is generally collateralized by the underlying security, involves the risk that the market price of the security will increase as any appreciation in the price of the borrowed assets would result in a loss, which is theoretically unlimited in amount. In addition, the party from whom the security was borrowed to effect the short sale may demand the return of the security before FSOF had planned. In this situation, FSOF may be forced to cover the short position in the market at a higher price than its short sale.

13

Fifth Street Management Group

(Predecessor to Fifth Street Asset Management Inc.)

Notes to Combined Financial Statements

For the Nine Months Ended September 30, 2014

(unaudited)

Limited Liquidity of Investments

The Combined Funds intend to invest in investments that may not be readily marketable. Illiquid investments may trade at a discount from comparable, more liquid investments, and at times there may be no market at all for such investments. Subordinate investments may be less marketable, or in some instances illiquid, because of the absence of registration under federal securities laws, contractual restrictions on transfer, the small size of the market and the small size of the issue (relative to issues of comparable interests). As a result, the Combined Funds may encounter difficulty in selling its investments or may, if required to liquidate investments to satisfy redemption requests of its investors or debt service obligations, be compelled to sell such investments at less than fair value.

Counterparty Risk

Some of the markets in which the Combined Funds may effect transactions are "over-the-counter" or "interdealer" markets. The participants in such markets are typically not subject to credit evaluation and regulatory oversight, unlike members of exchange-based markets. This exposes the Combined Funds to the risk that a counterparty will not settle a transaction in accordance with its terms and conditions because of a dispute over the terms of the applicable contract (whether or not such dispute is bona fide) or because of a credit or liquidity problem, causing the Combined Funds to suffer loss. Such "counterparty risk" is accentuated for contracts with longer maturities where events may intervene to prevent settlement, or where the Combined Funds have concentrated its transactions with a single or small group of counterparties.

Credit Risk

There are no restrictions on the credit quality of the investments the Combined Funds intend to make. Investments may be deemed by nationally recognized rating agencies to have substantial vulnerability to default in payment of interest and/or principal. Some investments may have low-quality ratings or be unrated. Lower rated and unrated investments have major risk exposure to adverse conditions and are considered to be predominantly speculative. Generally, such investments offer a higher return potential than higher rated investments, but involve greater volatility of price and greater risk of loss of income and principal.

In general, the ratings of nationally recognized rating organizations represent the opinions of agencies as to the quality of the securities they rate. Such ratings, however, are relative and subjective; they are not absolute standards of quality and do not evaluate the market value risk of the relevant securities. It is also possible that a rating agency might not change its rating of a particular issue on a timely basis to reflect subsequent events. The Combined Funds may use these ratings as initial criteria for the selection of portfolio assets but are not required to utilize them.

Interest Rate Risk

Fluctuations in interest rates expose the Company to interest rate risk on certain assets and liabilities of the Combined Funds. These changes may affect the fair value, interest income and interest expense related to certain floating rate assets and liabilities that are indexed to market interest rates.

Accounting Policies of Combined Funds

The Combined Funds, in which the Company has only minor ownership interests, are included in the Company's combined financial statements. The majority ownership interests in these funds are held by the investors in the funds, and these interests are reflected within redeemable non-controlling interests and non-controlling interests in the Combined Statements of Financial Condition. Management fees from the Combined Funds are eliminated in consolidation; however, the controlling interest is increased by the amount of the eliminated management fees.

The Combined Funds are considered investment companies for GAAP purposes. Pursuant to specialized accounting guidance for investment companies and the retention of that guidance in the Company's combined financial statements, the investments held by the Combined Funds are reflected in the combined financial statements at their estimated fair values.

Investments and Derivative Instruments at Fair Value

Investments at fair value include the Combined Funds' investments in securities, investment companies and other investments, including derivative instruments. Securities transactions are recorded on a trade-date basis. Realized gains and losses on sales of investments are determined on a specific identification basis and are included within net realized gains of Combined Funds in the Combined Statements of Income. Premiums and discounts are amortized and accreted, respectively, to income of the Combined Funds in the Combined Statements of Income.

The fair value of investments and derivative instruments held by the Combined Funds is based on observable market prices when available. Such values are generally based on the last reported sales price as of the reporting date. In the absence of

14

Fifth Street Management Group

(Predecessor to Fifth Street Asset Management Inc.)

Notes to Combined Financial Statements

For the Nine Months Ended September 30, 2014

(unaudited)

readily ascertainable market values, the determination of the fair value of investments held by the Combined Funds may require significant judgment or estimation (see Note 3). Actual results could differ materially from these estimates under different assumptions and conditions.

Deferred Financing Costs

Deferred financing costs consist of fees and expenses paid in connection with the closing or amending of the SLF I and SLF II credit facilities and are capitalized at the time of payment. Deferred financing costs are amortized using the straight line method over the terms of the respective credit facilities and are included in interest expense of the Combined Funds in the Company's Combined Statement of Income.

Securities Sold Short at Fair Value

Securities sold short reflect commitments to deliver specified amounts of securities and thereby create a liability to purchase these securities at a future date. Such amounts are reflected as a liability at the fair value of such securities on September 30, 2014. Subsequent market fluctuations may require FSOF to acquire these securities at prices which differ from the fair value reflected in the Combined Statement of Financial Condition, and such difference could be material.

Interest and Other Income of the Combined Funds

Income of the Combined Funds consists of interest income, dividend income and other miscellaneous items. Interest income is recorded on an accrual basis. The Combined Funds may place debt obligations, including bank debt and other participation interests, on non-accrual status and, when necessary, reduce current interest income by charging off any interest receivable when collection of all or a portion of such accrued interest has become doubtful. As of and for the nine months ended September 30, 2014, no investments were put on non-accrual status. Dividend income is recorded on the ex-dividend date, net of withholding taxes, if applicable.

Expenses of the Combined Funds

Expenses of the Combined Funds consist of other miscellaneous expenses and are recorded on an accrual basis.

Interest Expense of Combined Funds

Interest expense of Combined Funds consists of interest (including unused fees and deferred financing costs) incurred on indebtedness under the SLF I and SLF II credit facilities. Interest expense is recorded on an accrual basis and payable quarterly.

Recent Accounting Pronouncements

In June 2013, the FASB issued ASU 2013-08, Financial Services — Investment Companies ("ASU 2013-08"). ASU 2013-08 provides clarifying guidance to determine if an entity qualifies as an investment company. ASU 2013-08 also requires an investment company to measure non-controlling interests in other investment companies at fair value. The following disclosures are required by ASU 2013-08: (i) whether an entity is an investment company and is applying the accounting and reporting guidance for investment companies; (ii) information about changes, if any, in an entity's status as an investment company; and (iii) information about financial support provided or contractually required to be provided by an investment company to any of its investees. The requirements of ASU 2013-08 were adopted by the Company beginning in the first quarter of 2014. There are no changes to the current requirements relating to the retention of specialized accounting in the financial statements of a non-investment company parent. These updates did not have a material impact on the Company's financial condition or results of operations.

In May 2014, the FASB issued ASU No. 2014-09 ("ASU 2014-09"), Revenue from Contracts with Customers, which requires an entity to recognize the amount of revenue to which it expects to be entitled for the transfer of promised goods or services to customers. ASU 2014-09 will replace most existing revenue recognition guidance in GAAP when it becomes effective. The new standard will be effective for the Company on January 1, 2017. Early application is not permitted. The standard permits the use of either the retrospective or cumulative effect transition method. The Company is evaluating the effect that ASU 2014-09 will have on its combined financial statements and related disclosures. The Company has not yet selected a transition method nor has it determined the effect of this standard on its combined financial statements and its ongoing financial reporting.

In June 2014, the FASB issued ASU No. 2014-12, Accounting for Share-Based Payments When the Terms of an Award Provide That a Performance Target Could Be Achieved after the requisite service period, which clarifies the recognition of stock-based compensation over the required service period, if it is probable that the performance condition will be achieved. This guidance will be effective for fiscal years, and interim periods within those years, beginning after December 15, 2015 and

15

Fifth Street Management Group

(Predecessor to Fifth Street Asset Management Inc.)

Notes to Combined Financial Statements

For the Nine Months Ended September 30, 2014

(unaudited)

should be applied prospectively. The Company is currently evaluating the effect that this guidance will have on its combined financial statements and its ongoing financial reporting.

In August 2014, the FASB issued ASU No. 2014-13, Measuring the Financial Assets and Financial Liabilities of a Consolidated Collateralized Financing Entity ("CFE"). This new guidance requires reporting entities to use the more observable of the fair value of the financial assets or the financial liabilities to measure the financial assets and the financial liabilities of a CFE when a CFE is initially consolidated. It permits entities to make an accounting policy election to apply this same measurement approach after initial consolidation or to apply other GAAP to account for the consolidated CFE's financial assets and financial liabilities. It also prohibits all entities from electing to use the fair value option in ASC 825 to measure either the financial assets or financial liabilities of a consolidated CFE that is within the scope of this issue. This guidance is effective for fiscal years beginning after December 15, 2015, and interim periods therein. Early adoption is permitted using a modified retrospective transition approach as described in the pronouncement. The Company is currently evaluating the effect that this guidance will have on its combined financial statements and its ongoing financial reporting.