Attached files

| file | filename |

|---|---|

| EX-31.2 - CERTIFICATION OF CHIEF FINANCIAL OFFICER PURSUANT TO RULE 13A-14(A) - Fifth Street Asset Management Inc. | fsam-ex312_2016093010xq.htm |

| EX-32.2 - CERTIFICATION OF CHIEF FINANCIAL OFFICER PURSUANT TO SECTION 906 - Fifth Street Asset Management Inc. | fsam-ex322_2016093010xq.htm |

| EX-32.1 - CERTIFICATION OF CHIEF EXECUTIVE OFFICER PURSUANT TO SECTION 906 - Fifth Street Asset Management Inc. | fsam-ex321_2016093010xq.htm |

| EX-31.1 - CERTIFICATION OF CHIEF EXECUTIVE OFFICER PURSUANT TO RULE 13A-14(A) - Fifth Street Asset Management Inc. | fsam-ex311_2016093010xq.htm |

| EX-10.3 - ALEXANDER FRANK - AMENDMENT TO EMPLOYMENT AGREEMENT - Fifth Street Asset Management Inc. | fsam-ex103_2016093010xq.htm |

| EX-10.2 - IVELIN DIMITROV - AMENDMENT TO EMPLOYMENT AGREEMENT - Fifth Street Asset Management Inc. | fsam-ex102_2016093010xq.htm |

| EX-10.1 - BERNARD BERMAN - AMENDMENT TO EMPLOYMENT AGREEMENT - Fifth Street Asset Management Inc. | fsam-ex101_2016093010xq.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

Form 10-Q

(Mark One)

þ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) | ||

OF THE SECURITIES EXCHANGE ACT OF 1934 | |||

For the quarterly period ended September 30, 2016

OR

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) | ||

OF THE SECURITIES EXCHANGE ACT OF 1934 | |||

COMMISSION FILE NUMBER: 001-36701

Fifth Street Asset Management Inc.

(EXACT NAME OF REGISTRANT AS SPECIFIED IN ITS CHARTER)

DELAWARE | 46-5610118 | |

(State or jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

777 West Putnam Avenue, 3rd Floor Greenwich, CT | 06830 | |

(Address of principal executive office) | (Zip Code) | |

REGISTRANT'S TELEPHONE NUMBER, INCLUDING AREA CODE:

(203) 681-3600

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter periods as the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES þ NO ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES þ NO ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer o | Accelerated filer o | Non-accelerated filer þ | Smaller reporting company o | |||

(Do not check if a smaller reporting company) | ||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act) YES ¨ NO þ

The number of shares of the registrant's Class A common stock, par value $0.01 per share, outstanding as of November 18, 2016 was 6,602,374. The number of shares of the registrant's Class B common stock, par value $0.01 per share, outstanding as of November 18, 2016 was 42,856,854.

TABLE OF CONTENTS

Item 1. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

Item 1. | ||

Item 1A. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

Item 5. | ||

Item 6. | ||

FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q may contain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the "Securities Act"), and Section 21E of the Securities Exchange Act of 1934 as amended, (the "Exchange Act"), that reflect our current views with respect to, among other things, future events and financial performance. You can identify these forward-looking statements by the use of forward-looking words such as "outlook," "believes," "expects," "potential," "continues," "may," "will," "should," "seeks," "approximately," "predicts," "intends," "plans," "estimates," "anticipates" or the negative version of those words or other comparable words. The forward-looking statements are based on our beliefs, assumptions and expectations of our future performance, taking into account all information currently available to us. Such forward-looking statements are subject to various risks and uncertainties and assumptions relating to our operations, financial results, financial condition, business prospects, growth strategy and liquidity. We believe these factors include, but are not limited to, those described under "Risk Factors" in this Quarterly Report on Form 10-Q and in "Item 1A Risk Factors" in our Annual Report on Form 10-K for the year ended December 31, 2015, as such factors may be updated from time to time in our periodic filings with the Securities and Exchange Commission (the "SEC"), which are accessible on the SEC's website at www.sec.gov. If one or more of these or other risks or uncertainties materialize, or if our underlying assumptions prove to be incorrect, our actual results may vary materially from those indicated in these forward-looking statements. New risks and uncertainties arise over time, and it is not possible for us to predict those events or how they may affect us. Therefore, you should not place undue reliance on these forward-looking statements. Any forward-looking statement speaks only as of the date on which it is made. We do not undertake any obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise, except as required by law.

Unless the context otherwise requires, references to "we," "us," "our" and "the Company" are intended to mean the business and operations of Fifth Street Asset Management Inc. and its consolidated subsidiaries since the consummation of our initial public offering on November 4, 2014. When used in the historical context (i.e., prior to November 4, 2014), these terms are intended to mean the business and operations of Fifth Street Management Group.

When used in this Quarterly Report on Form 10-Q, unless the context otherwise requires:

• | "Adjusted Net Income" represents income before income tax benefit (provision) as adjusted for (i) certain compensation-related charges, (ii) unrealized gains (losses) on beneficial interests in CLOs, MMKT Notes and derivative liabilities, (iii) certain litigation costs and related recoveries (iv) the excess of cash dividends received from our investments in FSC and FSFR over the related income recognized under the equity method of accounting and (v) other non-recurring items; |

• | "AUM" refers to assets under management of the Fifth Street Funds and material control investments of these funds, and represents the sum of the net asset value of such funds and investments, the drawn debt and unfunded debt and equity commitments at the fund or investment-level (including amounts subject to restrictions) and uncalled committed debt and equity capital (including commitments to funds that have yet to commence their investment periods); |

• | "base management fees" refer to fees we earn for advisory services provided to our funds, which are generally based on a fixed percentage of fair value of assets, total commitments, invested capital, net asset value, total assets or principal amount of the investment portfolios managed by us; |

• | "catch-up" refers to a provision for a manager or adviser of a fund to receive the majority or all of the profits of such fund until the agreed upon profit allocation is reached; |

• | "CLO" refers to a collateralized loan obligation; |

• | “CLO I” refers to Fifth Street Senior Loan Fund I, LLC, a CLO in our senior loan fund strategy managed by CLO Management; |

• | "CLO II" refers to Fifth Street SLF II, Ltd. (formerly Fifth Street Senior Loan Fund II, LLC, prior to securitization), a CLO in our senior loan fund strategy managed by CLO Management; |

• | "CLO Management" refers to Fifth Street CLO Management LLC, the collateral manager for CLO I and CLO II; |

• | "fee-earning AUM" refers to the AUM on which we directly or indirectly earn management fees, and represents the sum of the net asset value of the Fifth Street Funds and their material control investments, and the drawn debt and unfunded debt and equity commitments at the fund or investment-level (including amounts subject to restrictions); |

• | "Fifth Street BDCs" and "our BDCs" refer to FSC and FSFR together; |

• | "Fifth Street Funds" and "our funds" refer to the Fifth Street BDCs and the other funds advised or managed by Fifth Street Management or CLO Management; |

• | "Fifth Street Management" refers to Fifth Street Management LLC and, unless the context otherwise requires, its subsidiaries; |

• | "Fifth Street Management Group" and the "Predecessor" refers to Fifth Street Management LLC, FSC, Inc., FSC CT, Inc., FSC Midwest, Inc., Fifth Street Capital West, Inc. (and their wholly-owned subsidiaries) and certain combined funds; |

i

• | "FSC" refers to Fifth Street Finance Corp., a publicly-traded business development company managed by Fifth Street Management; |

• | "FSFR" refers to Fifth Street Senior Floating Rate Corp., a publicly-traded business development company managed by Fifth Street Management; |

• | "FSOF" refers to "Fifth Street Opportunities Fund, L.P.", a hedge fund managed by Fifth Street Management; |

• | "Holdings Limited Partners" refers to active, limited partners in Fifth Street Holdings (other than us), which include, among other persons, the Principals; |

• | "hurdle rate" or "hurdle" refers to a specified minimum rate of return that a fund must exceed in order for the investment adviser or manager of such a fund to receive Part I Fees and/or performance fees; |

• | "management fees" refer to base management fees and Part I Fees; |

• | "MMKT" refers to MMKT Exchange LLC, a financial technology company in which FSM owns 80% of the common membership interests; |

• | "Part I Fees" refer to fees paid to us by our BDCs that are based on a fixed percentage of pre-incentive fee net investment income, which are calculated and paid quarterly, and subject to certain specified performance hurdles. Part I Fees are classified as management fees as they are predictable and are recurring in nature, are not subject to repayment (or clawback) and are generally cash-settled each quarter; |

• | "Part II Fees" refer to fees paid to us by our BDCs that are based on net capital gains, which are paid annually; |

• | "performance fees" refer to fees we earn based on the performance of a fund, which are generally based on certain specific hurdle rates as defined in the fund's investment management or partnership agreements, may be either an incentive fee or carried interest, are paid annually and also include Part II Fees; |

• | "permanent capital" refers to capital of funds that do not have redemption provisions or a requirement to return capital to investors upon exiting the investments made with such capital, except as required by applicable law, which funds currently consist of FSC and FSFR; such funds may be required to distribute all or a portion of capital gains and investment income or elect to distribute capital; |

• | "Principals" refers to Leonard M. Tannenbaum and Bernard D. Berman and, where applicable, any entities controlled directly or indirectly by them; |

• | "SLF I" refers to Fifth Street Senior Loan Fund I, LLC, a fund in our senior loan fund strategy, previously managed by Fifth Street Management prior to CLO I securitization; |

• | "SLF II" refers to Fifth Street Senior Loan Fund II, LLC, a fund in our senior loan fund strategy, previously managed by Fifth Street Management prior to CLO II securitization; |

• | "SMA" means a separately managed account; and |

• | "TRA recipients" refers to the Principals and Ivelin M. Dimitrov. |

Many of the terms used in this Quarterly Report on Form 10-Q, including AUM, fee-earning AUM and Adjusted Net Income, may not be comparable to similarly titled measures used by other companies. In addition, our definitions of AUM and fee-earning AUM are not based on any definition of AUM or fee-earning AUM that is set forth in the agreements governing the investment funds that we manage and may differ from definitions of AUM set forth in other agreements to which we are a party from time to time, including the agreements governing our revolving credit facility. Please see "Management's Discussion and Analysis of Financial Condition and Results of Operations — Non-GAAP Financial Measures and Operating Metrics — Assets Under Management" and "— Fee-earning AUM" for more information on AUM and fee-earning AUM. Further, Adjusted Net Income is not a performance measure calculated in accordance with U.S. Generally Accepted Accounting Principles ("GAAP"). We use Adjusted Net Income as a measure of operating performance, not as a measure of liquidity. We believe that Adjusted Net Income provides investors with a meaningful indication of our core operating performance and Adjusted Net Income is evaluated regularly by our management as a decision tool for deployment of resources. We believe that reporting Adjusted Net Income is helpful in understanding our business and that investors should review the same supplemental non-GAAP financial measures that our management uses to analyze our performance. Adjusted Net Income has limitations as an analytical tool and should not be considered in isolation or as a substitute for analyzing our results prepared in accordance with GAAP. The use of Adjusted Net Income without consideration of related GAAP measures is not adequate due to the adjustments described above. See "Management's Discussion and Analysis of Financial Condition and Results of Operations — Non-GAAP Financial Measures and Operating Metrics — Adjusted Net Income."

Amounts and percentages throughout this Quarterly Report on Form 10-Q may reflect rounding adjustments and consequently totals may not appear to sum.

ii

PART I - FINANCIAL INFORMATION

Item 1. Consolidated Financial Statements

Fifth Street Asset Management Inc.

Consolidated Statements of Financial Condition

As of | ||||||||

September 30, 2016 | December 31, 2015 | |||||||

Assets | (unaudited) | (See Note 2) | ||||||

Cash and cash equivalents | $ | 4,137,833 | $ | 17,185,204 | ||||

Management fees receivable (includes Part I Fees of $7,867,962 and $(555,663) at September 30, 2016 and December 31, 2015, respectively) | 19,490,540 | 4,879,785 | ||||||

Performance fees receivable | 124,836 | 224,618 | ||||||

Insurance recovery receivable | 9,775,905 | — | ||||||

Prepaid expenses (includes $833,275 and $676,789 related to income taxes at September 30, 2016 and December 31, 2015, respectively) | 3,008,454 | 1,284,759 | ||||||

Investments in equity method investees | 59,060,165 | 32,388,943 | ||||||

Beneficial interests in CLOs at fair value: (cost September 30, 2016: $24,271,320; cost December 31, 2015: $24,617,568) | 23,360,754 | 23,537,629 | ||||||

Due from affiliates | 3,828,063 | 3,943,384 | ||||||

Fixed assets, net | 5,570,857 | 9,893,521 | ||||||

Deferred tax assets | 42,941,089 | 51,217,957 | ||||||

Deferred financing costs | 1,551,936 | 1,929,433 | ||||||

Other assets | 3,330,570 | 3,976,420 | ||||||

Total assets | $ | 176,181,002 | $ | 150,461,653 | ||||

Liabilities and Equity | ||||||||

Liabilities | ||||||||

Accounts payable and accrued expenses | $ | 7,411,469 | $ | 5,324,842 | ||||

Accrued compensation and benefits | 8,147,182 | 10,448,260 | ||||||

Income taxes payable | — | 28,559 | ||||||

Loans payable (including $0 and $4,738,026 at September 30, 2016 and December 31, 2015, respectively, of MMKT Notes at fair value) | 14,972,565 | 21,710,640 | ||||||

Legal settlement payable | 9,250,000 | — | ||||||

Credit facility payable | 92,000,000 | 65,000,000 | ||||||

Dividends payable | 1,884,686 | 1,748,062 | ||||||

Derivative liabilities at fair value | — | — | ||||||

Due to affiliates | 28,571 | 24,257 | ||||||

Deferred rent liability | 2,110,809 | 3,146,210 | ||||||

Payable to related parties pursuant to tax receivable agreements | 37,960,213 | 45,486,114 | ||||||

Total liabilities | 173,765,495 | 152,916,944 | ||||||

Commitments and contingencies | ||||||||

Equity (deficit) | ||||||||

Preferred stock, $0.01 par value; 5,000,000 shares authorized; none issued and outstanding as of September 30, 2016 and December 31, 2015 | — | — | ||||||

Class A common stock, $0.01 par value 500,000,000 shares authorized; 6,602,374 and 5,822,672 shares issued and 6,602,374 and 5,798,614 shares outstanding as of September 30, 2016 and December 31, 2015, respectively | 66,024 | 58,227 | ||||||

Class B common stock, $0.01 par value 50,000,000 shares authorized; 42,856,854 shares issued and outstanding as of September 30, 2016 and December 31, 2015 | 428,569 | 428,569 | ||||||

Additional paid-in capital | 2,132,621 | 2,661,253 | ||||||

Accumulated deficit | (817,027 | ) | (30,905 | ) | ||||

1,810,187 | 3,117,144 | |||||||

Less: Treasury stock, at cost: 24,058 shares as of December 31, 2015 | — | (180,064 | ) | |||||

Total stockholders' equity, Fifth Street Asset Management Inc. | 1,810,187 | 2,937,080 | ||||||

Non-controlling interests | 605,320 | (5,392,371 | ) | |||||

Total equity (deficit) | 2,415,507 | (2,455,291 | ) | |||||

Total liabilities and equity (deficit) | $ | 176,181,002 | $ | 150,461,653 | ||||

All management and performance fees are earned from affiliates of the Company. See notes to consolidated financial statements.

1

Fifth Street Asset Management Inc.

Consolidated Statements of Income

(unaudited)

For the Three Months Ended September 30, | For the Nine Months Ended September 30, | |||||||||||||||

2016 | 2015 | 2016 | 2015 | |||||||||||||

Revenues | (See Note 2) | (See Note 2) | ||||||||||||||

Management fees (includes Part I Fees of $7,867,962 and $9,166,813 and $21,890,239 and $26,766,547 for the three months and nine months ended September 30, 2016 and 2015, respectively) | $ | 19,670,420 | $ | 23,310,135 | $ | 58,049,388 | $ | 69,094,654 | ||||||||

Performance fees | 38,661 | 2,596 | 124,836 | 79,451 | ||||||||||||

Other fees | 2,748,115 | 2,176,510 | 6,482,213 | 5,672,077 | ||||||||||||

Total revenues | 22,457,196 | 25,489,241 | 64,656,437 | 74,846,182 | ||||||||||||

Expenses | ||||||||||||||||

Compensation and benefits | 9,536,656 | 10,258,766 | 27,183,281 | 28,791,731 | ||||||||||||

General, administrative and other expenses | 7,424,927 | 4,179,089 | 24,806,542 | 10,551,314 | ||||||||||||

Depreciation and amortization | 349,475 | 434,146 | 3,925,519 | 1,254,544 | ||||||||||||

Total expenses | 17,311,058 | 14,872,001 | 55,915,342 | 40,597,589 | ||||||||||||

Other income (expense) | ||||||||||||||||

Interest income | 386,626 | 110,525 | 1,082,368 | 293,665 | ||||||||||||

Interest expense | (1,149,549 | ) | (507,647 | ) | (3,344,996 | ) | (1,337,827 | ) | ||||||||

Income from equity method investments | 1,550,487 | 15,295 | 3,554,541 | 5,343 | ||||||||||||

Unrealized loss on MMKT Notes | (2,582,405 | ) | — | — | — | |||||||||||

Realized gain on settlement of MMKT Notes | 2,592,751 | — | 2,592,751 | — | ||||||||||||

Unrealized gain (loss) on beneficial interests in CLOs | 537,600 | (23,148 | ) | 169,373 | (590,546 | ) | ||||||||||

Gain on extinguishment of debt | — | — | 2,000,000 | — | ||||||||||||

Adjustment of TRA liability for tax rate change | — | — | 7,525,901 | — | ||||||||||||

Loss on legal settlement | — | — | (9,250,000 | ) | — | |||||||||||

Insurance recoveries | 50,905 | — | 12,297,636 | — | ||||||||||||

Unrealized gain on derivatives | 8,383,213 | — | — | — | ||||||||||||

Realized loss on derivatives | (3,078,357 | ) | — | (2,612,932 | ) | — | ||||||||||

Loss on investor settlement | — | — | (10,419,274 | ) | — | |||||||||||

Other income (expense), net | (50,000 | ) | — | (620,514 | ) | 122,000 | ||||||||||

Total other income (expense), net | 6,641,271 | (404,975 | ) | 2,974,854 | (1,507,365 | ) | ||||||||||

Income before provision for income taxes | 11,787,409 | 10,212,265 | 11,715,949 | 32,741,228 | ||||||||||||

Provision for income taxes | 1,607,590 | 982,110 | 8,459,693 | 3,490,115 | ||||||||||||

Net income | 10,179,819 | 9,230,155 | 3,256,256 | 29,251,113 | ||||||||||||

Net income attributable to non-controlling interests | (10,417,537 | ) | (8,079,583 | ) | (3,878,297 | ) | (25,696,758 | ) | ||||||||

Net income (loss) attributable to Fifth Street Asset Management Inc. | $ | (237,718 | ) | $ | 1,150,572 | $ | (622,041 | ) | $ | 3,554,355 | ||||||

Net income (loss) per share attributable to Fifth Street Asset Management Inc. Class A common stock - Basic | $ | (0.04 | ) | $ | 0.19 | $ | (0.11 | ) | $ | 0.60 | ||||||

Net income (loss) per share attributable to Fifth Street Asset Management Inc. Class A common stock - Diluted | $ | (0.04 | ) | $ | 0.19 | $ | (0.13 | ) | $ | 0.60 | ||||||

Weighted average shares of Class A common stock outstanding - Basic | 5,908,407 | 5,901,718 | 5,847,139 | 5,956,389 | ||||||||||||

Weighted average shares of Class A common stock outstanding - Diluted | 5,908,407 | 5,908,463 | 5,847,139 | 5,963,318 | ||||||||||||

All revenues are earned from affiliates of the Company. See notes to consolidated financial statements.

2

Fifth Street Asset Management Inc.

Consolidated Statement of Changes in Equity

For the Nine Months Ended September 30, 2016

(unaudited)

Class A Common Stock | Class B Common Stock | Additional Paid-in Capital | Accumulated Deficit | Treasury Stock | Non-Controlling Interests | Total Equity (Deficit) | |||||||||||||||||||||||||||||

Shares | Amount | Shares | Amount | ||||||||||||||||||||||||||||||||

Balance, December 31, 2015 (See Note 2) | 5,822,672 | $ | 58,227 | 42,856,854 | $ | 428,569 | $ | 2,661,253 | $ | (30,905 | ) | $ | (180,064 | ) | $ | (5,392,371 | ) | $ | (2,455,291 | ) | |||||||||||||||

Cumulative effect of ASU 2016-09 adoption | — | — | — | — | 145,127 | (164,081 | ) | — | (160,023 | ) | (178,977 | ) | |||||||||||||||||||||||

Paid and accrued dividends - $0.30 per Class A common share | — | — | — | — | (1,824,330 | ) | — | — | — | (1,824,330 | ) | ||||||||||||||||||||||||

Paid and accrued dividends on restricted stock units | — | — | — | — | (35,131 | ) | — | — | (264,359 | ) | (299,490 | ) | |||||||||||||||||||||||

Issuance of shares in connection with vesting of RSUs | 43,701 | 437 | — | — | — | — | — | — | 437 | ||||||||||||||||||||||||||

Issuance of shares to settle derivative liability | 760,059 | 7,601 | — | — | 3,259,559 | — | — | — | 3,267,160 | ||||||||||||||||||||||||||

Retirement of Class A common stock | (24,058 | ) | (241 | ) | (179,823 | ) | 180,064 | — | |||||||||||||||||||||||||||

Deemed capital contribution | — | — | — | — | 676,617 | — | — | 5,134,177 | 5,810,794 | ||||||||||||||||||||||||||

Distributions to members | — | — | — | — | — | — | — | (11,373,105 | ) | (11,373,105 | ) | ||||||||||||||||||||||||

Reallocation of equity for changes in ownership interest | — | — | — | — | (3,070,991 | ) | — | — | 3,070,991 | — | |||||||||||||||||||||||||

Amortization of equity-based compensation | — | — | — | — | 500,340 | — | — | 5,711,713 | 6,212,053 | ||||||||||||||||||||||||||

Net income | — | — | — | — | — | (622,041 | ) | — | 3,878,297 | 3,256,256 | |||||||||||||||||||||||||

Balance, September 30, 2016 | 6,602,374 | $ | 66,024 | 42,856,854 | $ | 428,569 | $ | 2,132,621 | $ | (817,027 | ) | $ | — | $ | 605,320 | $ | 2,415,507 | ||||||||||||||||||

See notes to consolidated financial statements.

3

Fifth Street Asset Management Inc.

Consolidated Statements of Cash Flows

(unaudited)

For the Nine Months Ended September 30, | ||||||||

2016 | 2015 | |||||||

Cash flows from operating activities | (See Note 2) | |||||||

Net income | $ | 3,256,256 | $ | 29,251,113 | ||||

Adjustments to reconcile net income to net cash provided by operating activities: | ||||||||

Depreciation and amortization | 3,713,200 | 1,042,224 | ||||||

Amortization of fractional interests in aircrafts | 212,319 | 212,320 | ||||||

Amortization of deferred financing costs | 377,497 | 377,498 | ||||||

Amortization of equity-based compensation | 6,216,367 | 4,480,918 | ||||||

Write-off of capitalized software costs | 624,512 | — | ||||||

Unrealized gain on beneficial interests in CLOs | (169,373 | ) | 590,546 | |||||

Distributions of earnings from equity method investments | 3,059,289 | — | ||||||

Interest income accreted on beneficial interest in CLOs | (1,082,342 | ) | (231,231 | ) | ||||

Interest expense on MMKT Notes | 92,119 | — | ||||||

Deferred taxes | 8,276,868 | 3,224,207 | ||||||

Deferred rent | (1,035,401 | ) | (73,570 | ) | ||||

Realized gain on settlement of MMKT Notes | (2,592,751 | ) | — | |||||

Loss on investor settlement | 10,419,274 | — | ||||||

Loss on lease abandonment | 1,240,928 | — | ||||||

Gain on extinguishment of debt | (2,000,000 | ) | — | |||||

Adjustment of TRA liability for tax rate change | (7,525,901 | ) | — | |||||

Realized loss on derivatives | 3,267,160 | — | ||||||

Income from equity method investments | (3,554,541 | ) | (5,343 | ) | ||||

Changes in operating assets and liabilities: | ||||||||

Management fees receivable | (14,610,755 | ) | 4,795,110 | |||||

Performance fees receivable | 21,062 | 27,184 | ||||||

Insurance recovery receivable | (9,775,905 | ) | — | |||||

Prepaid expenses | (1,723,695 | ) | 221,566 | |||||

Due from affiliates | 115,321 | 1,670,438 | ||||||

Other assets | 433,531 | (81,541 | ) | |||||

Accounts payable and accrued expenses | 832,003 | (1,061,858 | ) | |||||

Accrued compensation and benefits | (2,301,078 | ) | (649,123 | ) | ||||

Income taxes payable | (28,559 | ) | (361,052 | ) | ||||

Legal settlement payable | 9,250,000 | — | ||||||

Due to Principal | — | (16,863 | ) | |||||

Due to affiliates | 4,314 | (59,316 | ) | |||||

Net cash provided by operating activities | 5,011,719 | 43,353,227 | ||||||

Cash flows from investing activities | ||||||||

Purchases of fixed assets | (15,048 | ) | (874,060 | ) | ||||

Purchases of equity method investments | (37,548,532 | ) | (8,879,679 | ) | ||||

Redemptions of equity method investments | 6,000,000 | 1,200,000 | ||||||

Distributions from equity method investments | 842,801 | — | ||||||

Distributions received from beneficial interest in CLO | 1,428,590 | 225,282 | ||||||

Purchases of beneficial interest in CLO | — | (21,523,005 | ) | |||||

Net cash used in investing activities | (29,292,189 | ) | (29,851,462 | ) | ||||

Cash flows from financing activities | ||||||||

Proceeds from loan payable | — | 21,620,819 | ||||||

Proceeds from borrowings under credit facility | 30,000,000 | 48,000,000 | ||||||

Repayments under credit facility | (3,000,000 | ) | (25,000,000 | ) | ||||

Repayments of notes payable | (2,237,443 | ) | (9,046,929 | ) | ||||

Capital contributions from non-controlling interests | — | 20,000 | ||||||

Distributions to members | (11,373,105 | ) | (41,639,038 | ) | ||||

Repurchases of Class A common stock | — | (1,849,140 | ) | |||||

Dividends to Class A shareholders | (2,156,353 | ) | (2,807,562 | ) | ||||

Net cash provided by (used in) financing activities | 11,233,099 | (10,701,850 | ) | |||||

Net increase (decrease) in cash and cash equivalents | (13,047,371 | ) | 2,799,915 | |||||

Cash and cash equivalents, beginning of period | 17,185,204 | 3,238,008 | ||||||

Cash and cash equivalents, end of period | $ | 4,137,833 | $ | 6,037,923 | ||||

4

Fifth Street Asset Management Inc.

Consolidated Statements of Cash Flows

(unaudited)

Supplemental disclosures of cash flow information: | ||||||||

Cash paid during the period for interest | $ | 2,857,564 | $ | 887,425 | ||||

Cash paid during the period for income taxes | $ | 251,236 | $ | 1,064,200 | ||||

Non-cash investing activities: | ||||||||

Non-cash contribution to FSOF | $ | 78,720 | $ | 106,635 | ||||

Non-cash distribution from FSOF | $ | 78,720 | $ | 106,635 | ||||

Non-cash financing activities: | ||||||||

Accrued dividends | $ | 1,126,478 | $ | 1,608,759 | ||||

Deemed capital contribution | $ | 5,810,794 | $ | — | ||||

Issuance of shares to settle derivative liability | $ | 3,267,160 | $ | — | ||||

All management and performance fees are earned from affiliates of the Company. See notes to consolidated financial statements.

5

Fifth Street Asset Management Inc.

Notes to Consolidated Financial Statements

Note 1. Organization

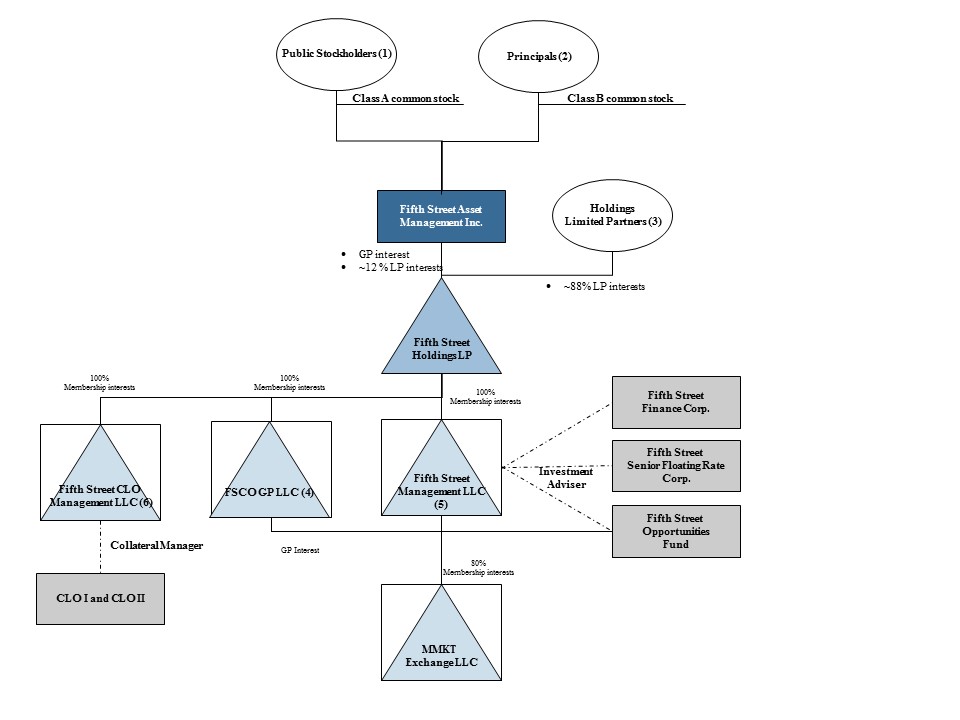

Fifth Street Asset Management Inc. ("FSAM"), together with its consolidated subsidiaries (collectively, the "Company"), is an alternative asset management firm headquartered in Greenwich, CT that provides asset management services to its investment funds (referred to as the "Fifth Street Funds" or the "funds"), which, to date, consist primarily of Fifth Street Finance Corp. (formed on January 2, 2008, "FSC") and Fifth Street Senior Floating Rate Corp. (formed on May 22, 2013, "FSFR"), both publicly-traded business development companies regulated under the Investment Company Act of 1940 (together, the "BDCs"). The Company conducts all of its operations through its consolidated subsidiaries, Fifth Street Management LLC ("FSM"), Fifth Street CLO Management LLC ("CLO Management") and FSCO GP LLC ("FSCO GP").

The Company's primary sources of revenues are management fees, primarily from the BDCs, which are driven by the amount of the assets under management and quarterly investment performance of the Fifth Street Funds. The Company conducts substantially all of its operations through one reportable segment that provides asset management services to the Fifth Street Funds. The Company generates all of its revenues in the United States.

Reorganization

In anticipation of its initial public offering (the "IPO") that closed November 4, 2014, FSAM was incorporated in Delaware on May 8, 2014 as a holding company with its primary asset expected to be a limited partnership interest in Fifth Street Holdings L.P. ("Fifth Street Holdings"). Fifth Street Holdings was formed on June 27, 2014 by Leonard M. Tannenbaum and Bernard D. Berman (the "Principals") as a Delaware limited partnership. Prior to the transactions described below, the Principals were the general partners and limited partners of Fifth Street Holdings. Fifth Street Holdings has a single class of limited partnership interests (the "Holdings LP Interests"). Immediately prior to the IPO:

• | The Principals contributed their general partnership interests in Fifth Street Holdings to FSAM in exchange for 100% of FSAM's Class B common stock; |

• | The members of FSM contributed 100% of their membership interests in FSM to Fifth Street Holdings in exchange for Holdings LP Interests; and |

• | The members of FSCO GP, a Delaware limited liability company, formed on January 6, 2014 to serve as the general partner of Fifth Street Opportunities Fund, L.P. (''FSOF,'' formerly Fifth Street Credit Opportunities Fund, L.P.) contributed 100% of their membership interests in FSCO GP to Fifth Street Holdings in exchange for Holdings LP Interests. |

These collective actions are referred to herein as the "Reorganization."

Initial Public Offering

On November 4, 2014, FSAM issued 6,000,000 shares of Class A common stock in the IPO at a price of $17.00 per common share. The proceeds totaled $95.9 million, net of underwriting commissions of $6.1 million. The proceeds were used to purchase a 12.0% limited partnership interest in Fifth Street Holdings.

Immediately following the Reorganization and the closing of the IPO on November 4, 2014:

• | The Principals held 42,856,854 shares of FSAM Class B common stock and 42,856,854 Holdings LP Interests. |

• | FSAM held 6,000,000 Holdings LP Interests and the former members of FSM and FSCO GP, including the Principals, held 44,000,000 Holdings LP Interests. |

• | The Principals, through their holdings of FSAM Class B common stock in the aggregate, had approximately 97.3% of the voting power of FSAM's common stock. |

Upon the completion of the Reorganization and the IPO, FSAM became the general partner of Fifth Street Holdings and acquired a 12.0% limited partnership interest in Fifth Street Holdings. Fifth Street Holdings and its wholly-owned subsidiaries (including FSM, CLO Management and FSCO GP) are consolidated by FSAM in the consolidated financial statements. The portion of net income attributable to the limited partners of Fifth Street Holdings, excluding FSAM, is recorded as "Net income attributable to non-controlling interests" on the Consolidated Statements of Income.

6

Fifth Street Asset Management Inc.

Notes to Consolidated Financial Statements

Exchange Agreement

In connection with the Reorganization, FSAM entered into an exchange agreement with the limited partners of Fifth Street Holdings that granted each limited partner of Fifth Street Holdings, and certain permitted transferees, the right, beginning two years after the closing of the IPO and subject to vesting and minimum retained ownership requirements, on a quarterly basis, to exchange such person's Holdings LP Interests for shares of Class A common stock of FSAM, on a one-for-one basis, subject to customary conversion rate adjustments for splits, unit distributions and reclassifications (collectively referred to as the "Exchange Agreement"). As a result, each limited partner of Fifth Street Holdings, over time, has the ability to convert his or her illiquid ownership interests in Fifth Street Holdings into Class A common stock of FSAM, which can more readily be sold in the public markets. As of September 30, 2016 and December 31, 2015, FSAM held approximately 13.0% and 11.6% of Fifth Street Holdings, respectively. FSAM’s percentage ownership in Fifth Street Holdings will continue to change as Holdings LP Interests are exchanged for Class A common stock of FSAM or when FSAM otherwise issues or repurchases FSAM common stock.

FSAM's purchase of Holdings LP Interests concurrent with its IPO, and the subsequent and future exchanges by holders of Holdings LP Interests for shares of FSAM's Class A common stock pursuant to the Exchange Agreement are expected to result in increases in its share of the tax basis of the tangible and intangible assets of Fifth Street Holdings, which will increase the tax depreciation and amortization deductions that otherwise would not have been available to FSAM. These increases in tax basis and tax depreciation and amortization deductions are expected to reduce the amount of cash taxes that FSAM would otherwise be required to pay in the future. FSAM entered into a tax receivable agreement ("TRA") with certain limited partners of Fifth Street Holdings (the "TRA Recipients") that requires FSAM to pay the TRA Recipients 85% of the amount of cash savings, if any, in U.S. federal, state, local and foreign income tax that FSAM actually realizes (or, under certain circumstances, is deemed to realize) as a result of the increases in tax basis in connection with exchanges by the TRA Recipients described above and certain other tax benefits attributable to payments under the tax receivable agreement.

RiverNorth Settlement

On February 18, 2016, the Company entered into a purchase and settlement agreement ("PSA") with RiverNorth Capital Management, LLC ("RiverNorth") pursuant to which RiverNorth would withdraw its competing FSC proxy solicitation. In connection with the execution and delivery of the PSA, on March 24, 2016, the Company purchased 4,078,304 shares of common stock of FSC for $25.0 million of cash at a purchase price of $6.13 per share, net of certain dividends payable to the Company pursuant to the PSA. Pursuant to a letter agreement with the Company, Leonard M. Tannenbaum purchased 5,142,296 shares of common stock of FSC at a net purchase price of $6.13 per share. During the three months ended March 31, 2016, the Company recorded a loss of $10,419,274 on the purchase which represented the premium paid by the Company and Mr. Tannenbaum in excess of the FSC closing share price on the date of the transaction. The premium paid by Mr. Tannenbaum was included as a loss in the consolidated financial statements since the Company directly benefited from this payment.

In addition, the Company issued RiverNorth a warrant to purchase 3,086,420 shares of FSAM's Class A common stock that, upon exercise, the Company was obligated to pay RiverNorth an amount equal to the lesser of: (i) $5 million and (ii) the spread value of the warrant based on a $3.24 strike price. The warrant was exercised by RiverNorth on June 23, 2016. Refer to Note 3 for further information.

The Company also entered into a swap agreement with RiverNorth whereas on each settlement date, if the settlement date share price of FSC common stock was less than $6.25, the Company was obligated to pay RiverNorth an amount equal to the excess of $6.25 over the settlement date share price multiplied by the 3,878,542 notional shares of common stock underlying the swap. Alternatively, if the settlement date share price of FSC common stock was greater than $6.25, RiverNorth was obligated to pay the Company for the excess of the settlement date share price over $6.25 in cash. The settlement dates ranged from October 2016 to January 2017. The Company was also entitled to a portion of dividends on FSC shares underlying the total return swap which were earned by RiverNorth prior to the settlement date. On September 7, 2016, the Company settled the swap agreement with RiverNorth (see Note 3).

Ironsides Settlement

On September 30, 2016, the Company entered into a purchase and settlement agreement with Ironsides Partners LLC, Ironsides Partners Special Situations Master Fund II L.P. and Ironsides P Fund L.P. (collectively, "Ironsides"). In connection with the agreement, the Company agreed to purchase 1,942,533 shares of FSFR’s common stock for a per-share purchase price of $9.00 from Ironsides. The transaction is expected to settle on November 30, 2016. As of September 30, 2016, the total consideration of $17,482,797 represents a premium to the FSFR stock price in an amount of $854,715 based on a share price of $8.56 on that date.

7

Fifth Street Asset Management Inc.

Notes to Consolidated Financial Statements

In connection with the execution and delivery of the purchase and settlement agreement with Ironsides, the Company and Leonard M. Tannenbaum, Chairman and Chief Executive Officer of the Company, have entered into a letter agreement, or the Letter Agreement, that provides that the Company will purchase the maximum number of shares of FSFR’s common stock that the Company determines, in its sole discretion, it can purchase with immediately available funds and that will not violate any of the terms or conditions of any contractual arrangements or regulations to which the Company is a party to or its property or assets are subject to. Any additional shares that the Company is obligated to purchase pursuant to the purchase and sale agreement will be purchased by Mr. Tannenbaum. The Letter Agreement also provides for mutual indemnification of the parties in connection with their obligations under the purchase and sale agreement and the Letter Agreement. The Company did not record this transaction as of September 30, 2016 as it cannot reasonably estimate the allocation between the Company and Mr. Tannenbaum.

MMKT Exchange LLC

On December 22, 2014, FSM entered into a limited liability company agreement, as majority member, with Leonard Tannenbaum’s brother, as minority member, for the purpose of forming MMKT Exchange LLC (previously IMME LLC), a Delaware limited liability company ("MMKT"). MMKT was a financial technology company that sought to bring increased liquidity and transparency to middle market loans. FSM made a capital contribution of $80,000 for an 80% membership interest in MMKT. In addition, MMKT issued $5,900,000 of MMKT Notes (as defined in note 15), of which $1,300,000 was held by the FSM. MMKT is consolidated in the Company’s consolidated financial statements and any intercompany balances between MMKT and FSM are eliminated.

As of March 31, 2016, MMKT reevaluated alternatives for the business and determined it was appropriate to scale back its operations. As a result, during the three months ended March 31, 2016, the MMKT Notes were written down to reflect the estimated net tangible assets of the business at loan expiration, which resulted in a an unrealized gain of $2,582,405. Additionally, previously capitalized software costs of $624,512 were written off as it was determined it was no longer probable that the software being developed would be placed into service.

During the three months ended June 30, 2016, MMKT determined that it would cease further development of its technology and market its intellectual property for sale and distribute all available cash to its convertible noteholders as soon as practicable. On August 8, 2016, MMKT entered into an agreement with its noteholders to settle and cancel the MMKT Notes in exchange for consideration of $2,833,050, of which $634,460 was paid to FSM. As a result of the cancellation, the Company realized a gain of $2,592,751 during the three months September 30, 2016. In connection with the settlement and cancellation of the MMKT notes, FSM incurred an expense of $100,000 that was paid to third-party noteholders in exchange for a release of claims against FSM and MMKT, which is included in Other income (expense) in the Consolidated Statements of Income.

On August 12, 2016, MMKT sold the rights to its platform, including all intellectual property, in exchange for $50,000 and distributed the proceeds to its noteholders, including $11,197 which was distributed to FSM. The Company recognized a gain of $50,000 related to this sale within Other income (expense) in the Consolidated Statements of Income. As of September 30, 2016, MMKT is in the process of winding up its business operations and dissolving MMKT Exchange LLC. Upon the final liquidation, the noteholders are entitled to a distribution equal to cash remaining after the settlement of all liabilities (see Note 8).

Note 2. Significant Accounting Policies

Revision of Previously Issued Financial Statements for Correction of Immaterial Errors

During the three months ended September 30, 2016, the Company identified an error related to the accounting treatment of its investments in common shares of the BDCs. In September 2015, the Company began purchasing common shares in the BDCs and treated such shares as available-for-sale securities under Accounting Standards Codification (“ASC”) 320. In 2016, the Company made substantial additional purchases of the BDC common shares. As a result, the Company revisited its accounting method for the shares held. The Company determined that it does exert significant influence over the BDCs and accordingly, its investments in the BDCs should have been accounted for as equity method investments under ASC 323 since inception. As of June 30, 2016, the cumulative error was an understatement of income from equity method investments of $1.7 million, an overstatement of other income of $2.5 million (resulting in a net decrease to income before provision for income taxes of $0.8 million), and an understatement of other comprehensive income of $6.5 million. The Company assessed the materiality of these errors on its prior quarterly and annual financial statements, assessing materiality both quantitatively and qualitatively, in accordance with the SEC’s Staff Accounting Bulletin (“SAB”) No. 99 and SAB No. 108 and concluded that the errors were not material to any of its previously issued financial statements. However, in order to correctly present the shares as an equity method investment in the appropriate period, management revised previously issued financial statements (the

8

Fifth Street Asset Management Inc.

Notes to Consolidated Financial Statements

"Revision"). The Company also corrected immaterial out-of-period adjustments that had been previously reported. These prior period adjustments will be reflected in future quarterly and annual filings for the respective period.

Set forth below is a summary of the amounts and financial statement line items impacted by these revisions for the periods presented in this Form 10-Q and previous filings.

Three Months Ended June 30, 2016 | ||||||||||||

Consolidated Statement of Income: | As previously reported | Adjustments | As revised | |||||||||

Income from equity method investments | $ | — | $ | 1,110,217 | $ | 1,110,217 | ||||||

Other income (expense), net | 1,571,903 | (1,546,728 | ) | 25,175 | ||||||||

Total other income, net | 10,608,494 | (436,511 | ) | 10,171,983 | ||||||||

Income before provision for income taxes | 11,643,558 | (436,511 | ) | 11,207,047 | ||||||||

Provision for income taxes | 7,237,303 | (122,427 | ) | 7,114,876 | ||||||||

Net income | 4,406,255 | (314,084 | ) | 4,092,171 | ||||||||

Net income attributable to non-controlling interests | (3,629,933 | ) | 385,308 | (3,244,625 | ) | |||||||

Net income attributable to Fifth Street Asset Management Inc. | $ | 776,322 | $ | 71,224 | $ | 847,546 | ||||||

Net income per share attributable to Fifth Street Asset Management Inc. - Basic | $ | 0.13 | $ | 0.02 | $ | 0.15 | ||||||

Net income per share attributable to Fifth Street Asset Management Inc. - Diluted | $ | 0.07 | $ | — | $ | 0.07 | ||||||

Six Months Ended June 30, 2016 | ||||||||||||

Consolidated Statement of Income: | As previously reported | Adjustments | As revised | |||||||||

Income from equity method investments | $ | — | $ | 1,978,326 | $ | 1,978,326 | ||||||

Other income (expense), net | 1,783,490 | (2,328,275 | ) | (544,785 | ) | |||||||

Total other expense, net | (3,316,468 | ) | (349,949 | ) | (3,666,417 | ) | ||||||

Income (loss) before provision for income taxes | 278,488 | (349,949 | ) | (71,461 | ) | |||||||

Provision for income taxes | 6,971,891 | (119,788 | ) | 6,852,103 | ||||||||

Net loss | (6,693,403 | ) | (230,161 | ) | (6,923,564 | ) | ||||||

Net loss attributable to non-controlling interests | 6,230,340 | 308,826 | 6,539,166 | |||||||||

Net loss attributable to Fifth Street Asset Management Inc. | $ | (463,063 | ) | $ | 78,665 | $ | (384,398 | ) | ||||

Net loss per share attributable to Fifth Street Asset Management Inc. - Basic | $ | (0.08 | ) | $ | 0.01 | $ | (0.07 | ) | ||||

Net loss per share attributable to Fifth Street Asset Management Inc. - Diluted | $ | (0.10 | ) | $ | — | $ | (0.10 | ) | ||||

9

Fifth Street Asset Management Inc.

Notes to Consolidated Financial Statements

Three Months Ended June 30, 2016 | ||||||||||||

Consolidated Statement of Comprehensive Income: | As previously reported | Adjustments | As revised | |||||||||

Net income | $ | 4,406,255 | $ | (314,084 | ) | $ | 4,092,171 | |||||

Adjustment for change in fair value of available-for-sale securities | (1,423,276 | ) | 1,423,276 | — | ||||||||

Tax effect of adjustment for change in fair value of available-for-sale securities | 20,304 | (20,304 | ) | — | ||||||||

Total comprehensive income | 3,003,283 | 1,088,888 | 4,092,171 | |||||||||

Less: Comprehensive income attributable to non-controlling interests | (2,374,581 | ) | (870,044 | ) | (3,244,625 | ) | ||||||

Comprehensive income attributable to Fifth Street Asset Management Inc. | $ | 628,702 | $ | 218,844 | $ | 847,546 | ||||||

Six Months Ended June 30, 2016 | ||||||||||||

Consolidated Statement of Comprehensive Income: | As previously reported | Adjustments | As revised | |||||||||

Net loss | $ | (6,693,403 | ) | $ | (230,161 | ) | $ | (6,923,564 | ) | |||

Adjustment for change in fair value of available-for-sale securities | (7,119,228 | ) | 7,119,228 | — | ||||||||

Tax effect of adjustment for change in fair value of available-for-sale securities | 284,010 | (284,010 | ) | — | ||||||||

Total comprehensive loss | (13,528,621 | ) | 6,605,057 | (6,923,564 | ) | |||||||

Less: Comprehensive loss attributable to non-controlling interests | 12,518,400 | (5,979,234 | ) | 6,539,166 | ||||||||

Comprehensive loss attributable to Fifth Street Asset Management Inc. | $ | (1,010,221 | ) | $ | 625,823 | $ | (384,398 | ) | ||||

Six Months Ended June 30, 2016 | ||||||||||||

Consolidated Statement of Cash Flows: | As previously reported | Adjustments | As revised | |||||||||

Cash flows from operating activities | ||||||||||||

Net loss | $ | (6,693,403 | ) | $ | (230,161 | ) | $ | (6,923,564 | ) | |||

Distributions of earnings from equity method investments | — | 1,700,636 | 1,700,636 | |||||||||

Deferred taxes | 6,990,955 | (119,788 | ) | 6,871,167 | ||||||||

Income from equity method investments | (25,728 | ) | (1,978,326 | ) | (2,004,054 | ) | ||||||

Net cash used in operating activities | (5,487,912 | ) | (627,639 | ) | (6,115,551 | ) | ||||||

Cash flows from investing activities | ||||||||||||

Purchases of equity method investments | — | (26,925,757 | ) | $ | (26,925,757 | ) | ||||||

Purchases of available-for-sale securities | (26,925,757 | ) | 26,925,757 | $ | — | |||||||

Distributions from equity method investments | — | 627,639 | 627,639 | |||||||||

Net cash used in investing activities | (19,577,470 | ) | 627,639 | (18,949,831 | ) | |||||||

Net decrease in cash and cash equivalents | (8,568,646 | ) | — | (8,568,646 | ) | |||||||

Cash and cash equivalents, beginning of period | 17,185,204 | — | 17,185,204 | |||||||||

Cash and cash equivalents, end of period | $ | 8,616,558 | $ | — | $ | 8,616,558 | ||||||

10

Fifth Street Asset Management Inc.

Notes to Consolidated Financial Statements

Three Months Ended March 31, 2016 | ||||||||||||

Consolidated Statement of Income: | As previously reported | Adjustments | As revised | |||||||||

Income from equity method investments | $ | — | $ | 868,109 | $ | 868,109 | ||||||

Other income (expense), net | 211,587 | (781,547 | ) | (569,960 | ) | |||||||

Total other expense, net | (13,924,962 | ) | 86,562 | (13,838,400 | ) | |||||||

Loss before income tax benefit | (11,365,070 | ) | 86,562 | (11,278,508 | ) | |||||||

Income tax benefit | (265,412 | ) | 2,639 | (262,773 | ) | |||||||

Net loss | (11,099,658 | ) | 83,923 | (11,015,735 | ) | |||||||

Net loss attributable to non-controlling interests | 9,860,273 | (76,483 | ) | 9,783,790 | ||||||||

Net loss attributable to Fifth Street Asset Management Inc. | $ | (1,239,385 | ) | $ | 7,440 | $ | (1,231,945 | ) | ||||

Net loss per share attributable to Fifth Street Asset Management Inc. - Basic | $ | (0.21 | ) | $ | — | $ | (0.21 | ) | ||||

Net loss per share attributable to Fifth Street Asset Management Inc. - Diluted | $ | (0.24 | ) | $ | — | $ | (0.24 | ) | ||||

Three Months Ended March 31, 2016 | ||||||||||||

Consolidated Statement of Comprehensive Income: | As previously reported | Adjustments | As revised | |||||||||

Net loss | $ | (11,099,658 | ) | $ | 83,923 | $ | (11,015,735 | ) | ||||

Adjustment for change in fair value of available-for-sale securities | (5,695,952 | ) | 5,695,952 | — | ||||||||

Tax effect of adjustment for change in fair value of available-for-sale securities | 263,706 | (263,706 | ) | — | ||||||||

Total comprehensive loss | (16,531,904 | ) | 5,516,169 | (11,015,735 | ) | |||||||

Less: Comprehensive loss attributable to non-controlling interests | 14,892,981 | (5,109,191 | ) | 9,783,790 | ||||||||

Comprehensive loss attributable to Fifth Street Asset Management Inc. | $ | (1,638,923 | ) | $ | 406,978 | $ | (1,231,945 | ) | ||||

Three Months Ended March 31, 2016 | ||||||||||||

Consolidated Statement of Cash Flows: | As previously reported | Adjustments | As revised | |||||||||

Cash flows from operating activities | ||||||||||||

Net loss | $ | (11,099,658 | ) | $ | 83,923 | $ | (11,015,735 | ) | ||||

Distributions of earnings from equity method investments | — | 600,549 | 600,549 | |||||||||

Deferred taxes | (246,396 | ) | 2,639 | (243,757 | ) | |||||||

Income from equity method investments | (552 | ) | (868,109 | ) | (868,661 | ) | ||||||

Net cash used in operating activities | (15,033,201 | ) | (180,998 | ) | (15,214,199 | ) | ||||||

Purchases of equity method investments | — | (26,925,757 | ) | (26,925,757 | ) | |||||||

Purchases of available-for-sale securities | (26,925,757 | ) | 26,925,757 | — | ||||||||

Distributions from equity method investments | — | 180,998 | 180,998 | |||||||||

Net cash used in investing activities | (20,752,835 | ) | 180,998 | (20,571,837 | ) | |||||||

Net decrease in cash and cash equivalents | (11,775,890 | ) | — | (11,775,890 | ) | |||||||

Cash and cash equivalents, beginning of period | 17,185,204 | — | 17,185,204 | |||||||||

Cash and cash equivalents, end of period | $ | 5,409,314 | $ | — | $ | 5,409,314 | ||||||

11

Fifth Street Asset Management Inc.

Notes to Consolidated Financial Statements

December 31, 2015 | ||||||||||||

Consolidated Statement of Financial Condition: | As previously reported | Adjustments | As revised | |||||||||

Investments in equity method investees | $ | 6,427,272 | $ | 25,961,671 | $ | 32,388,943 | ||||||

Investments in available-for-sale securities at fair value | 26,771,258 | (26,771,258 | ) | — | ||||||||

Deferred tax assets | 51,180,237 | 37,720 | 51,217,957 | |||||||||

Total assets | $ | 151,233,520 | $ | (771,867 | ) | $ | 150,461,653 | |||||

Accumulated other comprehensive income | 27,276 | (27,276 | ) | — | ||||||||

Retained earnings | — | (30,905 | ) | (30,905 | ) | |||||||

Total stockholders' equity, Fifth Street Asset Management Inc. | 2,995,261 | (58,181 | ) | 2,937,080 | ||||||||

Non-controlling interests | (4,678,685 | ) | (713,686 | ) | (5,392,371 | ) | ||||||

Total equity (deficit) | (1,683,424 | ) | (771,867 | ) | (2,455,291 | ) | ||||||

Total liabilities and equity | $ | 151,233,520 | $ | (771,867 | ) | $ | 150,461,653 | |||||

Year Ended December 31, 2015 | ||||||||||||

Consolidated Statement of Income: | As previously reported | Adjustments | As revised | |||||||||

Income (loss) from equity method investments | $ | 20,630 | $ | (269,940 | ) | $ | (249,310 | ) | ||||

Other income, net | 279,405 | (157,405 | ) | 122,000 | ||||||||

Total other expense, net | (2,519,624 | ) | (427,345 | ) | (2,946,969 | ) | ||||||

Income before provision for income taxes | 39,029,901 | (427,345 | ) | 38,602,556 | ||||||||

Provision for income taxes | 5,065,420 | (19,717 | ) | 5,045,703 | ||||||||

Net income | 33,964,481 | (407,628 | ) | 33,556,853 | ||||||||

Net income attributable to non-controlling interests | (31,556,455 | ) | 376,723 | (31,179,732 | ) | |||||||

Net income attributable to Fifth Street Asset Management Inc. | $ | 2,408,026 | $ | (30,905 | ) | $ | 2,377,121 | |||||

Net income per share attributable to Fifth Street Asset Management Inc. - Basic and Diluted | $ | 0.41 | $ | (0.01 | ) | $ | 0.40 | |||||

Year Ended December 31, 2015 | ||||||||||||

Consolidated Statement of Comprehensive Income: | As previously reported | Adjustments | As revised | |||||||||

Net income | $ | 33,964,481 | $ | (407,628 | ) | $ | 33,556,853 | |||||

Adjustment for change in fair value of available-for-sale securities | 382,242 | (382,242 | ) | — | ||||||||

Tax effect of adjustment for change in fair value of available-for-sale securities | (18,003 | ) | 18,003 | — | ||||||||

Total comprehensive income | 34,328,720 | (771,867 | ) | 33,556,853 | ||||||||

Less: Comprehensive income attributable to non-controlling interests | (31,893,418 | ) | 713,686 | (31,179,732 | ) | |||||||

Comprehensive income attributable to Fifth Street Asset Management Inc. | $ | 2,435,302 | $ | (58,181 | ) | $ | 2,377,121 | |||||

12

Fifth Street Asset Management Inc.

Notes to Consolidated Financial Statements

Year Ended December 31, 2015 | ||||||||||||

Consolidated Statement of Cash Flows: | As previously reported | Adjustments | As revised | |||||||||

Cash flows from operating activities | ||||||||||||

Net income | $ | 33,964,481 | $ | (407,628 | ) | $ | 33,556,853 | |||||

Deferred taxes | 5,178,675 | (19,717 | ) | 5,158,958 | ||||||||

(Income) loss from equity method investments | (83,405 | ) | 269,940 | 186,535 | ||||||||

Net cash provided by operating activities | 67,480,808 | (157,405 | ) | 67,323,403 | ||||||||

Cash flows from investing activities | ||||||||||||

Purchases of equity method investments | (7,500,000 | ) | (26,389,016 | ) | (33,889,016 | ) | ||||||

Purchases of available-for-sale securities | (26,389,016 | ) | 26,389,016 | — | ||||||||

Distributions from equity method investments | 225,282 | 157,405 | 382,687 | |||||||||

Net cash used in investing activities | (53,833,253 | ) | 157,405 | (53,675,848 | ) | |||||||

Net increase in cash and cash equivalents | 13,947,196 | — | 13,947,196 | |||||||||

Cash and cash equivalents, beginning of period | 3,238,008 | — | 3,238,008 | |||||||||

Cash and cash equivalents, end of period | $ | 17,185,204 | $ | — | $ | 17,185,204 | ||||||

Three Months Ended September 30, 2015 | ||||||||||||

Consolidated Statement of Income: | As previously reported | Adjustments (1) | As revised | |||||||||

Management fees | $ | 23,609,474 | $ | (299,339 | ) | $ | 23,310,135 | |||||

Other fees | 1,347,133 | 829,377 | 2,176,510 | |||||||||

Total revenues | 24,959,203 | 530,038 | 25,489,241 | |||||||||

General, administrative and other expenses | 3,349,712 | 829,377 | 4,179,089 | |||||||||

Total expenses | 14,042,624 | 829,377 | 14,872,001 | |||||||||

Income from equity method investments | 12,492 | 2,803 | 15,295 | |||||||||

Total other expense, net | (407,778 | ) | 2,803 | (404,975 | ) | |||||||

Income before provision for income taxes | 10,508,801 | (296,536 | ) | 10,212,265 | ||||||||

Provision for income taxes | 995,506 | (13,396 | ) | 982,110 | ||||||||

Net income | 9,513,295 | (283,140 | ) | 9,230,155 | ||||||||

Net income attributable to non-controlling interests | (8,341,728 | ) | 262,145 | (8,079,583 | ) | |||||||

Net income attributable to Fifth Street Asset Management Inc. | $ | 1,171,567 | $ | (20,995 | ) | $ | 1,150,572 | |||||

Net income per share attributable to Fifth Street Asset Management Inc. - Basic and Diluted | $ | 0.20 | $ | (0.01 | ) | $ | 0.19 | |||||

13

Fifth Street Asset Management Inc.

Notes to Consolidated Financial Statements

Nine Months Ended September 30, 2015 | ||||||||||||

Consolidated Statement of Income: | As previously reported | Adjustments (1) | As revised | |||||||||

Management fees | $ | 70,417,077 | $ | (1,322,423 | ) | $ | 69,094,654 | |||||

Other fees | 3,668,878 | 2,003,199 | 5,672,077 | |||||||||

Total revenues | 74,165,406 | 680,776 | 74,846,182 | |||||||||

General, administrative and other expenses | 8,548,115 | 2,003,199 | 10,551,314 | |||||||||

Total expenses | 38,594,390 | 2,003,199 | 40,597,589 | |||||||||

Income from equity method investments | 2,540 | 2,803 | 5,343 | |||||||||

Total other expense, net | (1,510,168 | ) | 2,803 | (1,507,365 | ) | |||||||

Income before provision for income taxes | 34,060,848 | (1,319,620 | ) | 32,741,228 | ||||||||

Provision for income taxes | 3,551,329 | (61,214 | ) | 3,490,115 | ||||||||

Net income | 30,509,519 | (1,258,406 | ) | 29,251,113 | ||||||||

Net income attributable to non-controlling interests | (26,859,217 | ) | 1,162,459 | (25,696,758 | ) | |||||||

Net income attributable to Fifth Street Asset Management Inc. | $ | 3,650,302 | $ | (95,947 | ) | $ | 3,554,355 | |||||

Net income per share attributable to Fifth Street Asset Management Inc. - Basic and Diluted | $ | 0.61 | $ | (0.01 | ) | $ | 0.60 | |||||

Three Months Ended September 30, 2015 | ||||||||||||

Consolidated Statement of Comprehensive Income: | As previously reported | Adjustments (1) | As revised | |||||||||

Net income | $ | 9,513,295 | $ | (283,140 | ) | $ | 9,230,155 | |||||

Adjustment for change in fair value of available-for-sale securities | 538,494 | (538,494 | ) | — | ||||||||

Tax effect of adjustment for change in fair value of available-for-sale securities | (25,410 | ) | 25,410 | — | ||||||||

Total comprehensive income | 10,026,379 | (796,224 | ) | 9,230,155 | ||||||||

Less: Comprehensive income attributable to non-controlling interests | (8,549,626 | ) | 470,043 | (8,079,583 | ) | |||||||

Comprehensive income attributable to Fifth Street Asset Management Inc. | $ | 1,476,753 | $ | (326,181 | ) | $ | 1,150,572 | |||||

Nine Months Ended September 30, 2015 | ||||||||||||

Consolidated Statement of Comprehensive Income: | As previously reported | Adjustments (1) | As revised | |||||||||

Net income | $ | 30,509,519 | $ | (1,258,406 | ) | $ | 29,251,113 | |||||

Adjustment for change in fair value of available-for-sale securities | (28,904 | ) | 28,904 | — | ||||||||

Tax effect of adjustment for change in fair value of available-for-sale securities | 1,370 | (1,370 | ) | — | ||||||||

Total comprehensive income | 30,481,985 | (1,230,872 | ) | 29,251,113 | ||||||||

Less: Comprehensive income attributable to non-controlling interests | (26,709,534 | ) | 1,012,776 | (25,696,758 | ) | |||||||

Comprehensive income attributable to Fifth Street Asset Management Inc. | $ | 3,772,451 | $ | (218,096 | ) | $ | 3,554,355 | |||||

14

Fifth Street Asset Management Inc.

Notes to Consolidated Financial Statements

Nine Months Ended September 30, 2015 | ||||||||||||||||

Consolidated Statement of Cash Flows: | As previously reported | Deconsolidation of Fund (2) | Adjustment (1) | As revised | ||||||||||||

Cash flows from operating activities | ||||||||||||||||

Net income | $ | 30,509,519 | $ | — | $ | (1,258,406 | ) | $ | 29,251,113 | |||||||

Deferred taxes | 3,224,078 | — | 129 | 3,224,207 | ||||||||||||

Income from equity method investments | (2,540 | ) | — | (2,803 | ) | (5,343 | ) | |||||||||

Management fees receivable | 3,472,687 | — | 1,322,423 | 4,795,110 | ||||||||||||

Prepaid Expenses | 282,909 | — | (61,343 | ) | 221,566 | |||||||||||

Purchases of investment of Consolidated Fund | (304,435,163 | ) | 304,435,163 | — | — | |||||||||||

Change in other assets of Consolidated Fund | (3,277,652 | ) | 3,277,652 | — | — | |||||||||||

Net cash provided by (used in) operating activities | (264,359,588 | ) | 307,712,815 | — | 43,353,227 | |||||||||||

Purchases of equity method investments | (7,500,000 | ) | — | (1,379,679 | ) | (8,879,679 | ) | |||||||||

Purchases of available-for-sale securities | (1,379,679 | ) | — | 1,379,679 | — | |||||||||||

Purchases of beneficial interest in CLO | (612,889 | ) | (20,910,116 | ) | — | (21,523,005 | ) | |||||||||

Net cash used in investing activities | (8,941,346 | ) | (20,910,116 | ) | — | (29,851,462 | ) | |||||||||

Issuance on notes payable by Consolidated Fund | 364,066,775 | (364,066,775 | ) | — | — | |||||||||||

Deferred financing costs | (2,744,980 | ) | 2,744,980 | — | — | |||||||||||

Net cash provided by (used in) investing activities | 350,619,945 | (361,321,795 | ) | — | (10,701,850 | ) | ||||||||||

Net increase in cash and cash equivalents | 77,319,011 | (74,519,096 | ) | — | 2,799,915 | |||||||||||

Cash and cash equivalents, beginning of period | 3,238,008 | — | — | 3,238,008 | ||||||||||||

Cash and cash equivalents, end of period (including Consolidated Fund) | 80,557,019 | (74,519,096 | ) | — | 6,037,923 | |||||||||||

Less: Cash and cash equivalents of the Consolidated Fund | 74,519,096 | (74,519,096 | ) | — | — | |||||||||||

Cash and cash equivalents, end of period | $ | 6,037,923 | $ | — | $ | — | $ | 6,037,923 | ||||||||

(1) Amounts include previous revisions in the December 31, 2015 Form 10-K relating to Part I Fees and the gross presentation of certain reimbursements from the BDCs.

(2) Amounts represent deconsolidation of a CLO as previously disclosed in the December 31, 2015 Form 10-K.

Basis of Presentation

The unaudited consolidated financial statements of the Company have been prepared in accordance with accounting principles generally accepted in the United States of America ("GAAP") and pursuant to the rules and regulations of the Securities and Exchange Commission (the "SEC") and the requirements for reporting on Form 10-Q and Regulation S-X. In the opinion of management, all adjustments of a normal recurring nature considered necessary for the fair presentation of the consolidated financial statements have been made. All significant intercompany transactions and balances have been eliminated in consolidation.

15

Fifth Street Asset Management Inc.

Notes to Consolidated Financial Statements

Principles of Consolidation

The consolidated financial statements include the accounts of the Company and entities in which it, directly or indirectly, is determined to have a controlling financial interest under ASC 810, as amended by ASU No. 2015-02. Under the variable interest model, the Company determines whether, if by design, an entity has equity investors who lack substantive participating or kick-out rights. If equity investors do not have such rights, the entity is considered a variable interest entity ("VIE") and must be consolidated by its primary beneficiary. An enterprise is determined to be the primary beneficiary if it holds a controlling financial interest. A controlling financial interest is defined as (a) the power to direct the activities of a VIE that most significantly impact the entity's economic performance and (b) the obligation to absorb losses of the entity or the right to receive benefits from the entity that could potentially be significant to the VIE. The consolidation guidance requires an analysis to determine (a) whether an entity in which the Company holds a variable interest is a VIE and (b) whether the Company's involvement, through holding interests directly or indirectly in the entity, would give it a controlling financial interest. Performance of that analysis requires the exercise of judgment.

Under the consolidation guidance, the Company determines whether it is the primary beneficiary of a VIE at the time it becomes involved with a variable interest entity and reconsiders that conclusion continually. In evaluating whether the Company is the primary beneficiary, the Company evaluates its economic interests in the entity held either directly or indirectly by the Company. The consolidation analysis can generally be performed qualitatively; however, if it is not readily apparent that the Company is not the primary beneficiary, a quantitative analysis may also be performed. Investments and redemptions (either by the Company, affiliates of the Company or third parties) or amendments to the governing documents of the respective investment funds could affect an entity's status as a VIE or the determination of the primary beneficiary. At each reporting date, the Company assesses whether it is the primary beneficiary and will consolidate or deconsolidate accordingly.

For equity investments where the Company does not control the investee, and where it is not the primary beneficiary of a VIE, but can exert significant influence over the financial and operating policies of the investee, the Company follows the equity method of accounting. The evaluation of whether the Company exerts control or significant influence over the financial and operational policies of its investees requires significant judgment based on the facts and circumstances surrounding each individual investment. Factors considered in these evaluations may include the type of investment, the legal structure of the investee, the terms and structure of the investment agreement, including investor voting or other rights, the terms of the Company's investment advisory agreement or other agreements with the investee, any influence the Company may have on the governing board of the investee, the legal rights of other investors in the entity pursuant to the fund’s operating documents and the relationship between the Company and other investors in the entity.

Consolidated Variable Interest Entities

Fifth Street Holdings

FSAM is the sole general partner of Fifth Street Holdings and, as such, it operates and controls all of the business and affairs of Fifth Street Holdings and its wholly-owned subsidiaries, FSM, CLO Management and FSCO GP. Under ASC 810, Fifth Street Holdings meets the definition of a VIE because the limited partners do not hold substantive kick-out or participating rights. Since FSAM has the obligation to absorb expected losses and the right to receive benefits that could be significant to Fifth Street Holdings and is the sole general partner, FSAM is considered to be the primary beneficiary of Fifth Street Holdings. The assets of Fifth Street Holdings can be used to settle the obligations of FSAM based on the discretion of FSAM in its capacity as the general partner of Fifth Street Holdings.

As a result, the Company consolidates the financial results of Fifth Street Holdings and its wholly-owned subsidiaries and records the economic interests in Fifth Street Holdings held by the limited partners other than FSAM as "Non-controlling interests" on the Consolidated Statements of Financial Condition and "Net income attributable to non-controlling interests" on the Consolidated Statements of Income.

Voting Interest Entities

Entities that are not VIEs are generally evaluated under the voting interest model. The Company consolidates voting interest entities that it controls through a majority voting interest or through other means.

16

Fifth Street Asset Management Inc.

Notes to Consolidated Financial Statements

Unconsolidated Variable Interest Entities

The Company holds interests in certain VIEs that are not consolidated because the Company is not deemed the primary beneficiary. The Company's interest in such entities generally is in the form of direct interests and fixed fee arrangements. The maximum exposure to loss represents the potential loss of assets by the Company relating to these non-consolidated entities. The Company's interests in these non-consolidated VIEs and their respective maximum exposure to loss relating to non-consolidated VIEs as of September 30, 2016 is $24,584,966, which represents the fair value of beneficial interests as well as management fees receivable at such date.

CLOs

In February 2015, the Company closed a securitization of the senior secured loans warehoused in Fifth Street Senior Loan Fund I, LLC ("CLO I"). In September 2015, Fifth Street Senior Loan II, LLC merged into Fifth Street SLF II Ltd. ("CLO II"), and the Company closed a securitization of the senior secured loans previously warehoused in Fifth Street Senior Loan Fund II, LLC. Fifth Street CLO Management LLC ("CLO Management"), a wholly owned-consolidated subsidiary of Fifth Street Holdings, is the collateral manager of CLO I and CLO II (collectively referred to as the "CLOs"), and as such, it operates and controls all of the business and affairs of the CLOs. Under ASC 810, the CLOs meet the definition of a VIE because the total equity at risk is not sufficient to finance it activities.

The Company determined that it did not have an obligation to absorb expected losses that could be significant to CLO I and CLO II. Therefore, the Company is not considered to be the primary beneficiary of the CLOs, and accordingly, does not consolidate their financial results. As of September 30, 2016, investments held by the Company in the senior secured and subordinated notes of the CLOs are included within "Beneficial interests in CLOs at fair value" on the Consolidated Statements of Financial Condition.

Use of Estimates

The preparation of consolidated financial statements in conformity with GAAP requires management to make estimates and assumptions affecting amounts reported in the consolidated financial statements and accompanying notes. The most significant of these estimates are related to: (i) the valuation of equity-based compensation, (ii) the estimate of future taxable income, which impacts the carrying amount of the Company’s deferred income tax assets, (iii) the determination of net tax benefits in connection with the Company's tax receivable agreements, (iv) the valuation of the Company's investments, (v) the valuation of derivative liabilities and (vi) the measurement of asset and liabilities associated with exit and disposal activities related to the abandonment of office space. These estimates are based on the information that is currently available to the Company and on various other assumptions that the Company believes to be reasonable under the circumstances. Actual results could differ materially from those estimates under different assumptions and conditions.

Concentration of Credit Risk and Other Risks and Uncertainties

Financial instruments which potentially subject the Company to concentrations of credit risk consist primarily of cash and cash equivalents.

For the nine months ended September 30, 2016 and 2015, substantially all revenues and receivables were earned or derived from advisory or administrative services provided to the BDCs and other affiliated entities.

The Company is dependent on its chief executive officer, Leonard M. Tannenbaum, who holds over 90% of the combined voting power of the Company through his ownership of shares of common stock. If for any reason the services of the Company's chief executive officer were to become unavailable, there could be a material adverse effect on the Company's operations, liquidity and profitability.

Fair Value Measurements

The carrying amounts of cash and cash equivalents, management and performance fees receivable from affiliates, prepaid expenses, insurance recovery receivable, due from/to affiliates, accounts payable and accrued expenses, accrued compensation and benefits, income taxes payable, legal settlement payable and dividend payable approximate fair value due to the immediate or short-term maturity of these financial instruments.

Cash and Cash Equivalents

Cash equivalents include short-term, highly liquid investments that are readily convertible to known amounts of cash and have original maturities of three months or less. The Company places its cash and cash equivalents with U.S. financial institutions and, at times, amounts may exceed federally insured limits. The Company monitors the credit standing of these financial institutions.

17

Fifth Street Asset Management Inc.

Notes to Consolidated Financial Statements

Equity Method Investments

Investments over which the Company exercises significant influence, but which do not meet the requirements for consolidation, are accounted for using the equity method of accounting, whereby the Company records its share of the underlying income or losses of equity method investees. The Company did not elect the fair value option on its equity method investments.

Investments in equity method investees consists of the Company's general partner interests in an unconsolidated fund and investments in FSC and FSFR common stock. The Company exercises significant influence with respect to the fund and BDCs as a result of its management contracts with the affiliated fund and BDCs, and specifically with respect to the BDCs, its board of director representation.

Beneficial Interest in CLOs

Beneficial interests in CLOs meet the definition of a debt security under ASC 325-40, Beneficial Interest in Securitized Financial Assets. Income from the beneficial interest in CLOs is recorded using the effective interest method based upon an estimation of an effective yield to maturity utilizing assumed cash flows. The Company monitors the expected residual payments, and effective yield is determined and updated periodically, as needed. Any distributions received from the beneficial interests in CLOs in excess of the calculated income using the effective yield are treated as a reduction of the cost.

The Company earned interest income of $386,617 and $1,082,342, respectively, from beneficial interests in CLOs, for the three and nine months ended September 30, 2016 and $95,396 and $231,231, respectively, for the three and nine months ended September 30, 2015.

Fair Value Option

The Company has elected the fair value option, upon initial recognition, for all beneficial interests in CLOs, which had a cost of $24,271,320 as of September 30, 2016. There were $537,600 and $169,373 of unrealized gains, respectively, recorded on beneficial interests in CLOs for the three and nine months ended September 30, 2016. There was $23,148 and $590,546 of unrealized losses, respectively, recorded on beneficial interests in CLOs for the three and nine months ended September 30, 2015.