Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - CASCADE MICROTECH INC | d644463d8k.htm |

Cascade Microtech

December 2013

Michael Burger, President & CEO

Jeff Killian, Vice President & CFO

Exhibit 99.1 |

Safe

Harbor and Non-GAAP Measures 2

This

presentation

includes

“forward-looking”

statements

within

the

meaning

of

the

Private

Securities

Litigation

Reform

Act

of

1995.

All

statements

other

than

statements

of

historical

fact

made

in

this

presentation

are

forward-looking

including,

among

others,

statements

regarding:

anticipated

growth

of

Cascade

Microtech

(the

“Company”);

market

opportunities;

new

products;

results

of

recent

acquisitions;

and

the

Company’s

target

model.

All

such

statements

are

only

predictions

and

are

based

on

current

expectations,

estimates

and

projections

about

the

Company’s

business

based

in

part

on

assumptions

made

by

management.

In

evaluating

these

statements,

you

should

specifically

consider

various

factors,

including:

changes

in

demand

for

the

Company’s

products;

trends

in

semiconductor

R&D

spending;

the

potential

failure

of

expected

market

opportunities

to

materialize;

potential

delays

in

product

introductions

or

market

acceptance;

potential

loss

of

customers;

general

challenges

in

integrating

acquired

businesses;

and

other

risks

discussed

from

time

to

time

in

the

Company’s

Securities

and

Exchange

Commission

filings

and

reports,

including

the

Company’s

Annual

Report

on

Form

10-K.

Such

forward-looking

statements

speak

only

as

of

the

date

on

which

they

are

made

and

the

Company

does

not undertake

any

obligation

to

update

any

forward-looking

statement

to

reflect

events

or

circumstances

after

the

date

of

this

presentation.

Please

refer

to

the

Appendix

for

a

description

and

reconciliation

of

Non-GAAP

financial

measures

used

in this

presentation:

EBITDAS

and

adjusted

EBITDAS. |

Cascade Microtech at a Glance

3

Cascade Microtech, Inc. (NASDAQ: CSCD) is a

worldwide leader in precision mechanical,

electrical measurements which aid in the test of

integrated circuits (ICs), optical devices and

other small structures

Founded in 1983

Headquartered in Beaverton, OR

>400 employees worldwide

Dominant market share in our target markets

–

Focused on research and engineering

communities within the semiconductor

market

–

The majority of all new processes and

device types are characterized using

Cascade Microtech products

Last twelve months (LTM) Revenue of $116M

with 6% year on year growth

LTM Adjusted EBITDAS of $14M with 16% year

on year growth

Engineering Test

Systems

Production Test

Systems

Engineering Probes

Production Probe

Cards

Note: Revenue and adjusted EBITDAS do not include the impact of ATT Systems;

includes RTP from Aug 1, 2013. (1) Adjusted EBITDAS is a non-GAAP

measure, please refer to the Appendix for a reconciliation of this non-GAAP measure.

We operate our business in two segments:

Probes and Systems

(1) |

New

product introductions and recent acquisitions drive segment SAM expansion

Strong revenue growth, expanding margins and cash flows with no debt

Diversified blue-chip customers across major capex spenders

Global service and support infrastructure aligned to customer locations

Critical enabler of next generation process technologies

Investment Highlights

4

Management team with a track record of execution and innovation

Product

portfolio

well-suited

to

solve

customers’

most

complex

test

challenges |

Cascade team capable of leveraging deep industry and operations expertise to drive

results Cascade Microtech’s Seasoned Leadership

5

Michael Burger

President & CEO

Appointed President and CEO in 2010

Member of Board of Directors

CEO experience: Merix

Steven Harris

Executive Vice President

Appointed EVP in June 2009

Former Vice President of Research & Development at Electro Scientific

Industries Served in a variety of product development and engineering

positions at Tektronix Ellen Raim

Vice President, HR

Joined Cascade Microtech as Vice President of Human Resources

in

2010

Served as Vice President of Human Resources at Electro Scientific Industries

Former Director of World Wide Talent Acquisition at Intel

Steve Mahon

Vice President,

Operations

Joined Cascade Microtech as Vice President of Operations in 2010

Served as director of process engineering at TriQuint Semiconductor

Former fabrication manager of Electronic Designs

Debbora Ahlgren

Vice President, Marketing

Joined Cascade Microtech as Vice President of Marketing in 2012

Served as Vice President of Marketing at the CBA Group

Former Senior Vice President of Sales and Marketing for OptimalTest

Appointed CFO in 2010

Joined Cascade Microtech as Director of Finance in 2008

Held various position at TriQuint Semiconductor including treasurer, corporate

controller Jeff Killian

Vice President & CFO

Robert Selley

Vice President, Sales &

Service

Joined Cascade Microtech as Vice President of Sales and Service in 2013

Led the internationals sales organizations at both Apcon and ONPATH Technologies

Served as Director of Sales Operations at Electro Scientific Industries

|

What

is Wafer Probing? 6

On-wafer testing is a growing

requirement

–

Identifies and characterizes

performance on the wafer

–

Enables significantly

improved yield

–

More cost effective than

packaged test

Advanced packaging

accelerates trend

–

Cascade Microtech enables

new developments at the

wafer level

Customer Wafer

Cascade Systems

Cascade Probes

Contacting a

Customer Circuit

Wafer probing refers to the functional

testing of semiconductor devices while

they are still in wafer form |

A

Strong History of Innovation 2010

First multi-contact

probe for small pads

Acquires Test Division

of SUSS MicroTec

2000

1990

HP invests in

MicroChamber™

environment

First RF-capable GHz probe

card Infinity Probe®

introduced

1980

First 18 GHz µw probe

1995

First double-sided probe

system HF chucks for up

to 200 GHz

Alessi acquired for FA

1/f noise measurement system

First HP device

characterization system

DC/RF parametric probe card

New 300 mm on-wafer prober

1985

First submicron probe

holder

2005

300 mm ‘vertical probe’

system

First WLR system for 300 mm

BlueRay high-speed production

prober

ProbeShield®

technology

Acquires Aetrium’s Reliability

Test Business

Acquires ATT Test Systems

2013

7 |

Consumer Trends Fuel Growth Opportunities

Wireless Devices

•

High-frequency RF

•

Shrinking geometries

•

Lower voltages

•

Power

Higher data rates

More data

Consumer Devices

•

Faster digital interfaces

•

Video

•

IC packaging innovation

Integration of functions

Shrinking

geometries

Green Power Devices

•

Higher voltages

•

Higher current

•

Reliability

•

LED

Lower cost of test

Computing Devices

•

Faster buses

•

Shrinking geometries

•

Device integration

•

Power

Measurement

diversification

Accelerating the Need for Cascade Microtech’s Products

8 |

22

nm Cascade Microtech Growth Funnel

Production (FAB)

90

nm

65 nm

32/45

nm

28 nm

1 Silicon

Process nodes

Technology integration & materials

Device designs

Wafer diameter

450 mm

20 nm

14 nm

5 nm

HKMG

FinFET

RF-CMOS

Growth funnel driven by

-

New process nodes

-

New technology integrations and materials

-

New device structures and device designs

-

New wafer geometries

9

Advanced packages

Microbump

TSV

st |

Products Cover Entire Semiconductor Lifecycle

Production (FAB)

Assembly & Test

1

Silicon

Virtual design

Support pre-production and validation activities

Engineering Products

Support application or production flow

Production Products

10

Engineering Probes

Engineering Probe Stations

Reliability Test Products

Production Probe Cards

Production Probers

(HBLED & High Power)

st

Thermal

Systems |

Outstanding Customers in All Major Sectors

11

Fabless

Government/Institute Research

Integrated Device Manufacturer

University Research

Subcons

Foundry

The Who’s Who of the semiconductor industry with minimal concentration

|

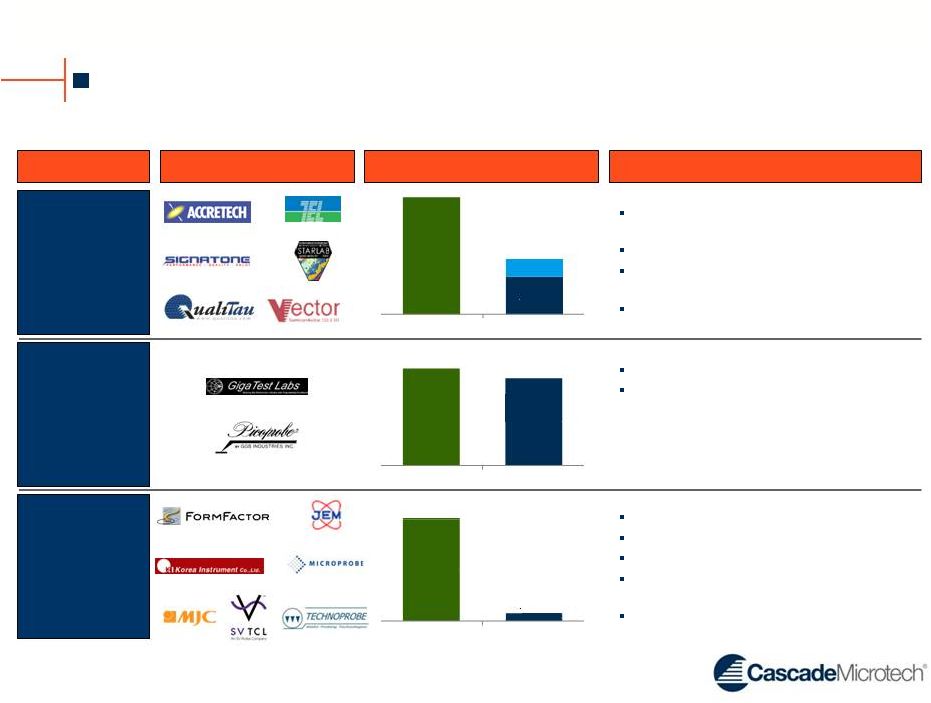

12

Market

Industry Participants

Market Share

Comments

Systems

Engineering

Probes

Production

Probe Cards

Focused primarily on engineering

applications

Accretech and TEL not competitors

Production platforms aimed at HB-LED

and Power markets

Significant long term opportunity in 450mm

Relatively small, but stable market

Addresses nearly all of the market and has

50% share today

Large, highly-fragmented market

Do not compete in memory

CSCD focuses only on advanced test

Strong position in RF with leading global

semiconductor vendors

Large opportunity in SoC

Significant Market Opportunities

Growth &

acquisitions

$654M

$210M

$100M

$310M

TAM

SAM

$39M

$35M

TAM

SAM

$1.2B

$59M

TAM

SAM |

CM300 300mm lab probe station

–

Scalable configurations with enhancement roadmap

–

Semi-

or fully-

automated

–

New Velox™

test automation software

–

Announced January, 2013; Units shipped to customers

APS200TESLA fab prober (Power)

–

Advanced power IC testing with safety and anti-arcing technology

–

Addressing an emerging $20 billion IC market; $60 million SAM

–

3”-, 4”-, 6”-

and 8”-

wafer capable, production prober

–

Capable of withstanding up to 10.5 kV and 400 Amps

–

Announced in Q2 2012; First shipments in Q3 2013

SMART150 lab probe station

–

Protect extensive installed base of manual probe stations

–

Address

customer

pain

points

with

focused

applications

(mmW,

RF,

others)

–

Flexibility and scalability through upgradeable configurations

–

Announced in Q3 2012; Now shipping in volume

13

New Products, Expanding Markets

New products are aligned with market/customer requirements and expand

Cascade’s SAM |

Acquisitions:

Aetrium’s RTP Products & ATT Systems

Closing Date

Purchase Price

LTM Revenue

LTM EBITDA

Valuation Multiple

Year Founded

Headquarters

Aetrium’s Reliability Test Products

ATT Test Systems

10/1/13

7/31/13

2001

First Product released in 1998

Munich, Germany

North St. Paul, MN

$2.4M in cash

Additional $1.0M upon achievement of

certain milestones

$10.3M

(2)

$3.3M

(1)

$0.6M

(1)

1.0x LTM Revenue

6.0x LTM EBITDA

$26.9 M

$11.2M in cash at close

$1.0M deferred cash payment

1.6M shares of CSCD Stock

~2.6x LTM Revenue

~6.2x LTM EBITDA

$4.4M

(2)

(1)

Based on Aetrium 8-K filed July 31, 2013. EBITDA based on GAAP operating

income. (2)

Annualized using the unaudited 11 months ending October 1, 2013

14

Business

Description

Offers package-

and wafer-level reliability

solutions for wafer process technologies

A leading manufacturer of advanced thermal

systems used in testing of semiconductor wafers

Strategic Rationale

Expands wafer-level reliability (WLR) test

capabilities

Enables Cascade to offer complete WLR solution

Leverage Cascade’s sales channel and global

support organization to drive additional revenue

Accelerates development of next-generation

system products with thermal capabilities

Current installed base of 1,500+ systems

Lowers product cost through vertical integration

of high-cost components |

Global Support Infrastructure Aligned with Customer Centers

15

•

Coverage of all major engineering & production areas worldwide

•

Over 1,700 active customers

•

Nearly 8,000 probe stations installed worldwide

•

Cascade Microtech Certified Pre-owned business launched in 2012

Headquarters

Beaverton, OR

Manufacturing,

Customer Operations

North St Paul, Minnesota

Reliability Test Products

Munich, Germany

ATT Systems &

Customer Operations

Dresden, Germany

Manufacturing

Japan

Customer Operations

Shanghai

Customer Operations

Taiwan

Customer Operations

Singapore

Customer Operations |

Key

Financials |

Financial Highlights

Strong Growth

Complementary acquisitions expected to accelerate growth; achieved 30% revenue

CAGR from 2009 to 2012

Improving Margins

Success model goals of 50% gross margins and 20% EBITDAS;

Generated

45%

gross

margins

and

12%

Adjusted

EBITDAS

margins

over

LTM

(9/30/13)

Commitment to

Investing in R&D

Continued investment in R&D further builds upon technology leadership

position Stable Revenue

with Consistent

Profitability

Revenue has been much less cyclical than broader semi cap equipment industry

Positive earnings for last 8 consecutive quarters

Strong Balance

Sheet

Strong cash position with no debt

17

Newly introduced products expected to contribute to long-term growth

Minimal CapEx requirements

(1)

(1)

(1)

EBITDAS and Adjusted EBITDAS are non-GAAP measures, please refer to the Appendix for a

reconciliation of these non-GAAP measures.

|

Track Record of Revenue Growth and Profitability

18

Revenue

Adjusted EBITDAS

2010:

Strong recovery with market

improvement and M&A

2011:

Growth outpaced the market and

totaled 13%

2012:

Consistently strong performance

quarter over quarter

2013:

Record Q3 and LTM revenue

EPS

(1)

(2)

Note: Graphs do not include the impact of ATT Systems.

Note: LTM Revenue represents the revenue for the 4 consecutive quarters ending 9/30/2013

(1)

Adjusted EBITDAS is a non-GAAP measure, please refer to the Appendix for a reconciliation of this

non-GAAP measure (2)

Earnings per share (EPS) shown is diluted EPS from continuing operations

|

Strong Balance Sheet

19

$21 million in cash

and investments

Debt free

$10 million revolving

credit facility

(1)

Pro forma (PF) based on 8K/A filed December 2013 Note: 3/31/10 is

first quarter after Suss Microtech acquisition cost of $15.6M in cash and 0.7M shares of

Cascade Microtech stock

Assets

3/31/2010

12/31/2011

12/31/2012

9/30/2013

PF

(1)

Cash and Investments

$23

$15

$23

$32

$21

Accounts Receivable

13

24

21

18

19

Inventory

22

24

24

23

26

Prepaid and other current

5

5

4

3

4

Total Current

$63

$68

$72

$76

$70

Fixed Assets

12

9

8

7

7

Goodwill & purchased Intangibles

5

3

3

4

30

Other Assets

3

3

2

2

2

Total Assets

$83

$83

$85

$89

$109

Liabilities

Accounts Payable

$5

$6

$6

$6

$6

Accrued Liabilities

6

8

7

6

7

Other Current Liabilities

1

6

3

1

1

Total Current Liabilities

$12

$20

$16

$13

$14

Other Long-Term Liabilities

4

4

3

3

8

Total Liabilities

$16

$24

$19

$16

$22

Shareholders' Equity

Equity

67

59

66

73

87

Total Liabilities and Equity

$83

$83

$85

$89

$109 |

Attractive Margin Structure

20

2010

2011

2012

Q1

2013

Q2

2013

Q3

2013

Revenue

100%

100%

100%

100%

100%

100%

Gross

Margin

38%

40%

44%

42%

47%

48%

Adjusted

EBITDAS(1)

3%

7%

12%

9%

14%

13%

Target

Success

Model

100%

50%

20%

Poised to leverage growth driven by new products and market expansion

Supply chain efficiencies

Channel leverage

(1) Adjusted EBITDAS is a non-GAAP measure, please refer to the Appendix for a

reconciliation of this non-GAAP measure. |

Investment Highlights

21

Critical enabler of next generation process technologies

Critical enabler of next generation process technologies

Strong revenue growth and cash flows with expanding margins

Strong revenue growth and cash flows with expanding margins

Management team with a track record of execution and innovation

Management team with a track record of execution and innovation

Diversified blue-chip customers across major capex spenders

New product introductions and recent acquisitions drive segment SAM expansion

Global service and support infrastructure aligned to customer locations

Product

portfolio

well-suited

to

solve

customers’

most

complex

test

challenges |

Appendix |

Appendix: Reconciliations of GAAP to

Non-GAAP Financial Measures

In this presentation we use the following Non-GAAP financial measures, which

we define in this

Appendix

and

reconcile

to

GAAP

financial

measures

:

EBITDAS

and Adjusted

EBITDAS.

Definitions:

–

EBITDAS

is defined as operating income from continuing operations before depreciation and

amortization and stock-based compensation. EBITDAS should not be

construed as a substitute for net income or net cash provided by (used in)

operating activities (all as determined in accordance with GAAP) for the

purpose of analyzing the Company’s operating performance, financial position and

cash flows, as EBITDAS is not defined by GAAP. However, the Company regards

EBITDAS as a complement to net income and other GAAP financial performance

measures, including an indirect measure of operating cash flow.

–

Adjusted

EBITDAS

is

defined

as

operating

income

from

continuing

operations

before

depreciation

and amortization and stock-based compensation and certain other items

(adjustments) such as restructuring, facility move and project costs, and

acquisition related expenses that the Company believes are not

representative of its ongoing operating performance. Adjusted EBITDAS should not

be

construed

as

a

substitute

for

net

income

or

net

cash

provided

by

(used in) operating activities (all

as determined in accordance with GAAP) for the purpose of analyzing the

Company’s operating performance, financial position and cash flows, as

adjusted EBITDAS is not defined by GAAP. However,

the

Company

regards

adjusted

EBITDAS

as

a

complement

to

net income and other GAAP

financial

performance

measures,

including

an

indirect

measure

of

operating cash flow.

23 |

Reconciliation of Pro Forma to GAAP

24

Twelve Months Ended

December 31,

2013 Quarterly Data

Nine Months Ended

September 30,

Twelve Months Ended

September 30,

2010

2011

2012

Q1 2013

Q2 2013

Q3 2013

2012

2013

2012

2013

Revenue

92,597

104,610

112,962

27,471

30,307

28,197

82,594

85,975

109,892

116,343

Reconciliation to EBITDAS

Income (Loss) from Operations

(8,108)

(4,190)

7,557

1,041

2,517

1,571

5,273

5,129

6,388

7,413

Depreciation and Amortization

4,374

4,559

4,629

1,200

1,176

1,146

3,407

3,522

4,505

4,744

Stock Based Comp

1,836

1,853

1,459

334

538

343

1,136

1,215

1,528

1,538

EBITDAS

(1,898)

2,222

13,645

2,575

4,231

3,060

9,816

9,866

12,421

13,695

EBITDAS %

-2.0%

2.1%

12.1%

9.4%

14.0%

10.9%

11.9%

11.5%

11.3%

11.8%

Reconciliation to Adjusted EBITDAS

EBITDAS

(1,898)

2,222

13,645

2,575

4,231

3,060

9,816

9,866

12,421

13,695

Restructuring

2,684

3,418

-

-

112

-

-

112

3

112

Acquisition and Acquisition Related

2,056

-

-

-

-

627

-

627

-

627

Facility Consolidation and Other

23

1,174

-

-

-

-

-

-

41

-

Adjusted EBITDAS

2,865

6,814

13,645

2,575

4,343

3,687

9,816

10,605

12,465

14,434

Adjusted EBITDAS %

3.1%

6.5%

12.1%

9.4%

14.3%

13.1%

11.9%

12.3%

11.3%

12.4% |