Attached files

| file | filename |

|---|---|

| EX-21 - EXHIBIT 21 - ESCALADE INC | ex_21.htm |

| EX-23.2 - EXHIBIT 23.2 - ESCALADE INC | ex23_2.htm |

| EX-32.1 - EXHIBIT 32.1 - ESCALADE INC | ex32_1.htm |

| EX-23.1 - EXHIBIT 23.1 - ESCALADE INC | ex23_1.htm |

| EX-31.2 - EXHIBIT 31.2 - ESCALADE INC | ex31_2.htm |

| EX-31.1 - EXHIBIT 31.1 - ESCALADE INC | ex31_1.htm |

| EX-32.2 - EXHIBIT 32.2 - ESCALADE INC | ex32_2.htm |

| EX-10.23 - EXHIBIT 10.23 - ESCALADE INC | ex10_23.htm |

| EX-10.25 - EXHIBIT 10.25 - ESCALADE INC | ex10_25.htm |

| EX-10.24 - EXHIBIT 10.24 - ESCALADE INC | ex10_24.htm |

| EX-10.26 - EXHIBIT 10.26 - ESCALADE INC | ex10_26.htm |

United

States

Securities

and Exchange Commission

Washington,

D.C. 20549

Form

10-K

|

x

|

ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

|

|

For

the Fiscal Year Ended December 26, 2009

|

|

|

or

|

|

|

o

|

TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

|

For the

transition period from _____________ to _____________

Commission

File Number 0-6966

|

ESCALADE,

INCORPORATED

|

|

|

|

(Exact

name of registrant as specified in its

charter)

|

||

|

Indiana

|

13-2739290

|

|

|

(State

of incorporation)

|

(I.R.S.

EIN)

|

|

|

817

Maxwell Ave, Evansville, Indiana

|

47711

|

|

|

(Address

of Principal Executive Office)

|

(Zip

Code)

|

812-467-4449

(Registrant’s

Telephone Number)

Securities

registered pursuant to Section 12(b) of the Act

|

Common

Stock, No Par Value

|

The

NASDAQ Stock Market LLC

|

|

|

(Title

of Class)

|

(Name

of Exchange on Which Registered)

|

Securities

registered pursuant to section 12(g) of the Act: NONE

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in

Rule 405 of the Securities

Yes o No

x

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the Act

Yes o No

x

Indicate

by check mark whether the registrant (1) has filed all reports required to be

filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter period that the registrant was required

to file such reports), and (2) has been subject to such filing requirements for

the past 90 days.

Yes x No

o

Indicate

by check mark whether the registrant has submitted electronically and posted on

its corporate Web site, if any, every Interactive Data File required to be

submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding

12 months (or for such shorter period that the registrant was required to submit

and post such files).

Yes o No

o

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K is not contained herein, and will not be contained, to the best

of registrant’s knowledge, in definitive proxy or information statements

incorporated by reference in Part III of this Form 10-K or any amendment to this

Form 10-K. x

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, or a non-accelerated filer, or a smaller reporting company.

See the definitions of “Large accelerated filer,” “accelerated filer” and

“smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large

accelerated filer o

|

Accelerated

filer o

|

|||

|

Non-accelerated

filer o

|

Smaller

reporting company x

|

|||

|

(do

not check if a smaller reporting company)

|

|

Indicate

by checkmark whether the registrant is a shell company (as defined in Rule 12

b-2 of the Exchange Act).

Yes o No

x

Aggregate

market value of common stock held by nonaffiliates of the registrant as of July

11, 2009 based on the closing sale price as reported on the NASDAQ Global

Market: $8,091,686

The

number of shares of Registrant’s common stock (no par value) outstanding as of

February 11, 2010: 12,682,759

DOCUMENTS

INCORPORATED BY REFERENCE

Certain

portions of the registrant’s Proxy Statement relating to its annual meeting of

stockholders scheduled to be held on April 30, 2010 are incorporated by

reference into Part III of this Report.

Escalade,

Incorporated and Subsidiaries

Table

of Contents

|

Page

|

||||

|

3

|

||||

|

6

|

||||

|

13

|

||||

|

14

|

||||

|

14

|

||||

|

14

|

||||

|

15

|

||||

|

18

|

||||

|

18

|

||||

|

26

|

||||

|

27

|

||||

|

27

|

||||

|

27

|

||||

|

28

|

||||

|

29

|

||||

|

29

|

||||

|

29

|

||||

|

29

|

||||

|

30

|

||||

|

30

|

||||

2

General

Escalade,

Incorporated (“Escalade” or “Company”) operates in two business segments:

sporting goods and office products. Escalade and its predecessors have more than

80 years of manufacturing and selling experience in these two

industries.

The

following table presents the percentages contributed to Escalade’s net sales by

each of its business segments:

|

2009

|

2008

|

2007

|

||||||||||

|

Sporting

goods

|

66 | % | 66 | % | 70 | % | ||||||

|

Office

products

|

34 | % | 34 | % | 30 | % | ||||||

|

Total

net sales

|

100 | % | 100 | % | 100 | % | ||||||

For

additional segment information, see Note 14 – Operating Segment and Geographic

Information in the consolidated financial statements.

Sporting

Goods

Headquartered

in Evansville, Indiana, Escalade Sports manufactures and distributes widely

recognized brands in family game room and outdoor sporting goods products

through traditional department stores, mass merchandise retailers, and sporting

goods specific retailers. Escalade is the world’s largest producer of table

tennis tables. Some of the Company’s most recognized brands

include:

|

Product Segment

|

Brand Names

|

|

|

Table

Tennis

|

Ping-Pong®,

STIGA®

|

|

|

Pool

Tables and Accessories

|

Mizerak®,

Mosconi®

|

|

|

Basketball

Backboards and Goals

|

Goalrilla™,

Goaliath®, Silverback®

|

|

|

Game

Tables (Hockey and Soccer)

|

Harvard

Game®, RhinoPlay®, Atomic®

|

|

|

Archery

|

Trophy

Ridge®, Bear Archery®

|

|

|

Fitness

|

The

STEP®, USWeight™

|

|

|

Play

Systems

|

Woodplay®,

Oasis™

|

Sears

historically was one of Escalade Sports largest customers and accounted for 18%

of total consolidated revenues in 2007. In 2008, the Company was unable to

negotiate satisfactory terms for continued sales of table tennis and billiard

tables. Sales to Sears in 2008, declined to 6% of total consolidated revenues.

In 2009, the Company has one customer in the Sporting Goods group, Dick’s

Sporting Goods, which accounted for 14.7% of total consolidated

revenues.

Escalade

Sports manufactures in the U.S.A. and Mexico and imports product from China,

where the Company employs a number of contract manufacturers.

Certain

products produced by Escalade Sports are subject to regulation by the Consumer

Product Safety Commission. The Company believes it is in full compliance with

all applicable regulations.

Office

Products

Operating

as Martin Yale, the office products business has a worldwide presence with

manufacturing facilities in North America and Europe. Besides the sales offices

located at each manufacturing plant, Martin Yale has sales offices in the United

Kingdom, France, Spain, China, Italy, South Africa and Sweden.

3

Martin

Yale products include: data shredders, paper trimmers, paper folding machines,

paper drills, collators, bursting machines, letter openers, and other office

related products. Martin Yale brands include Martin Yale®, Premier®, Master®,

Master View®, Mead Hatcher™, Intimus®, and Paper Monster®.

Martin

Yale products are sold throughout office products retailers, wholesalers and

catalog distributors. No single Martin Yale customer accounted for more than 10%

of Office Product sales during 2009.

Marketing

and Product Development

In both

the sporting goods and office product business segments, Escalade has rigorously

developed strategic plans to enhance and promote product branding. The Company

constantly evaluates the quality-to-price paradigm of its customers, and then

designs and redesigns its products to achieve the best fit. Marketing efforts

are then initiated through its retail partners in the form of advertising and

other promotion allowances. In general, the Company does not directly advertise

to end-users.

In order

to meet customer needs, each operating segment conducts its own independent

research and development efforts to design new products and enhance already

existing products. On a consolidated basis, the Company incurred research and

development costs of approximately $2.0 million, $2.3 million and $2.3 million

in 2009, 2008 and 2007, respectively.

Competition

Escalade

is subject to competition with various manufacturers in each product line

produced or sold by Escalade. The Company is not aware of any other single

company that is engaged in both the same industries as Escalade or that produces

the same range of products as Escalade within such industries. Nonetheless,

competition exists for many Escalade products within both the sporting goods and

office product industries. Some competitors are larger and have substantially

greater resources than the Company. Escalade believes that its long-term success

depends on its ability to strengthen its relationship with existing customers,

attract new customers and develop new products that satisfy the quality and

price requirements of sporting goods and office product customers.

Licenses,

Trademarks and Brand Names

The

Company has an agreement and contract with Sweden Table Tennis AB for the

exclusive right and license to distribute and produce table tennis equipment

under the brand name STIGA® for the United States and Canada. The company also

owns several registered trademarks and brand names including but not limited to

Ping-Pong®, Bear Archery®, Goalrillaä, The Step®, and

Wood Play® which are used in the Sporting Goods business segment and Premier®

and Intimus® which are used in the Office Products business

segment.

Backlog

and Seasonality

Sales are

based primarily on standard purchase orders and in most cases orders are shipped

within the same month received. Unshipped orders at the end of the fiscal year

(backlog), were not material, and therefore not an indicator of future results.

Consumer demand for sporting goods has typically been seasonal and driven by

holiday season demand; however, increased diversity in product categories, such

as playground and basketball, has helped the Company achieve more evenly

distributed revenues. In 2009, 2008 and 2007, approximately 49%, 52% and 58%,

respectively, of sporting goods sales came in the second half of the year.

Demand for Office Products has not been seasonal and is not expected to be so in

the future.

4

Employees

The

number of employees at December 26, 2009 and December 27, 2008 for each business

segment were as follows:

|

2009

|

2008

|

|||||||

|

Sporting

Goods

|

||||||||

|

USA

|

259 | 277 | ||||||

|

Mexico

|

104 | 206 | ||||||

|

Asia

|

8 | 8 | ||||||

| 371 | 491 | |||||||

|

Office

Products

|

||||||||

|

USA

|

93 | 106 | ||||||

|

Europe

|

128 | 134 | ||||||

|

Asia

|

8 | 8 | ||||||

| 229 | 248 | |||||||

|

Total

|

600 | 739 | ||||||

The

I.U.E./C.W.A. (United Electrical Communication Workers of America, AFL-CIO)

represents hourly rated employees at the Escalade Sports’ Evansville, Indiana

distribution center. There are approximately 15 covered employees at December

26, 2009. A 3-year labor contract was negotiated and renewed in April 2009; the

new agreement expires on April 30, 2012. Management believes it has satisfactory

relations with its employees.

Sources

of Supplies

Raw

materials for Escalade’s various product lines consist of wood, steel, plastics,

fiberglass and packaging. Escalade relies upon suppliers in various countries

and upon various third party Asian manufacturers for certain of its game tables

and non-security paper shredders. The Company believes that these sources will

continue to provide adequate supplies as needed and that all other materials

needed for the Company’s various operations are available in adequate quantities

from a variety of domestic and foreign sources.

SEC

Reports

The

Company’s internet site (www.escaladeinc.com) makes available free of charge to

all interested parties the Company’s annual report on Form 10-K, quarterly

reports on Form 10-Q, and current reports on Form 8-K, and all amendments to

those reports, as well as all other reports and schedules filed electronically

with the Securities and Exchange Commission (the “Commission”), as soon as

reasonably practicable after such material is electronically filed with or

furnished to the Commission. Interested parties may also find reports, proxy and

information statements and other information on issuers that file electronically

with the Commission at the Commission’s internet site

(http://www.sec.gov).

5

Overall

sales in both sporting goods and office products declined in 2009 due mainly to

consumer uncertainty generated by the poor economy in the United States and

globally. Sales may further decline in 2010. Recovering or replacing these

declining or lost sales will be a significant challenge. The Company cannot

provide any assurance that it will be able to recover or replace all or any

portion of these declining or lost sales.

Sales

to Escalade Sports’ largest customer declined significantly in 2008 and in 2009

and sales to this customer continue to be reduced.

Sears

historically was one of Escalade Sports largest customers and accounted for 18%

of total consolidated revenues in 2007. In 2008, sales to Sears accounted for 6%

of total consolidated revenues, representing a decline of 12% from prior year.

Although Escalade Sports had been a preferred supplier of sporting goods

products to Sears for more than 30 years and had won numerous awards from Sears

for delivering outstanding products and services, the Company never had a

long-term supplier contract with Sears. In 2008, Escalade Sports was unable to

negotiate satisfactory terms for continued sales of table tennis and billiard

tables, which products represented approximately 50% of total sales to Sears in

2007. The Company stopped supplying those products to Sears in the second half

of 2008 and did not supply those products to Sears in 2009. Although the Company

has achieved placement with other large mass-retail customers that will

partially offset this lost business, it cannot provide any assurance that the

Company will be able to recover or replace all of these declining or lost sales

to Sears.

If

the Company would lose significant customers in the future, the Company may have

difficulty in replacing such lost revenues.

The

Company has several large customers and historically has derived substantial

revenues from those customers. The Company needs to continue to expand its

customer base to minimize the effects of the loss of any single customer in the

future. If sales to one or more significant customers would be lost or

materially reduced, there can be no assurance that the Company will be able to

replace such revenues, which losses could have a material adverse effect on the

Company’s business, financial condition, and results of operations.

Markets

are highly competitive and the Company may not continue to compete

successfully.

The

market for sporting goods and office products is highly fragmented and intensely

competitive. Escalade competes with a variety of regional, national and

international manufacturers for customers, employees, products, services and

other important aspects of the business. In sporting goods, the Company has

historically sold a large percentage of our sporting goods products to mass

merchandisers, and has increasingly attempted to expand sales to specialty

retailer and dealer markets. Similarly, the Company has traditionally sold

office products to office products retailers and specialty machine dealers. In

addition to competition for sales into those distribution channels, vendors also

must compete in sporting goods with large format sporting goods stores,

traditional sporting goods stores and chains, warehouse clubs, discount stores

and department stores, and in office products with office supply superstores,

computer and electronics superstores, contract stationers, and others. Some of

the current and potential competitors are larger than Escalade and have

substantially greater financial resources that may be devoted to sourcing,

promoting and selling their products, and may discount prices more heavily than

the Company can afford.

If

the Company is unable to predict or react to changes in consumer demand, it may

lose customers and sales may decline.

Success

depends in part on the ability to anticipate and respond in a timely manner to

changing consumer demand and preferences regarding sporting goods and office

products. Products must appeal to a broad range of consumers whose preferences

cannot be predicted with certainty and are subject to change. The Company often

makes commitments to manufacture products months in advance of the proposed

delivery to customers. If Escalade misjudges the market for products, sales may

decline significantly. The Company may have to take significant inventory

markdowns on unpopular products that are overproduced and/or miss opportunities

for other products that may rise in popularity, both of which could have a

negative impact on profitability. A major shift in consumer demand away from

sporting goods or office products could also have a material adverse effect on

business, results of operations and financial condition.

6

Quarterly

operating results are subject to fluctuation.

Operating

results have fluctuated from quarter to quarter in the past, and the Company

expects that they will continue to do so in the future. Earnings may not recover

to historical levels and may fall short of either a prior fiscal period or

market expectations. Factors that could cause these quarterly fluctuations

include the following: international, national and local general economic and

market conditions; the size and growth of the overall sporting goods and office

products markets; intense competition among manufacturers, marketers,

distributors and sellers of products; demographic changes; changes in consumer

preferences; popularity of particular designs, categories of products and

sports; seasonal demand for products; the size, timing and mix of purchases of

products; fluctuations and difficulty in forecasting operating results; ability

to sustain, manage or forecast growth and inventories; new product development

and introduction; ability to secure and protect trademarks, patents and other

intellectual property; performance and reliability of products; customer

service; the loss of significant customers or suppliers; dependence on

distributors; business disruptions; increased costs of freight and

transportation to meet delivery deadlines; changes in business strategy or

development plans; general risks associated with doing business outside the

United States, including, without limitation: exchange rates, import duties,

tariffs, quotas and political and economic instability; changes in government

regulations; any liability and other claims asserted against the Company;

ability to attract and retain qualified personnel; and other factors referenced

or incorporated by reference in this Form 10-K and any other filings with the

Securities and Exchange Commission.

The

Company’s Senior Secured Revolving Credit Facility matures May 31, 2010 and the

Company may be unable to renew or replace this financing.

The

Company has significantly reduced the carrying value of its Credit Facilities

from $46.5 million as of year-end 2008 to $27.6 million as of year-end 2009 and

is and has been in compliance with all debt covenants under its Senior Secured

Revolving Credit Facility which was signed April 2009. The Company has begun

preliminary discussions regarding renewal of its Senior Secured Revolving Credit

Facility and anticipates finalizing a renewal or replacement credit agreement by

May 31, 2010, although there can be no assurances that such agreement will be

entered into or, if completed, that it will be executed by the loan maturity

date.

Operating

results may be impacted by changes in the economy that impact business and

consumer spending.

In

general, sales depend on discretionary spending by consumers. A deterioration of

current economic conditions such as that experienced in both the United States

and the global economy in 2008 and 2009 adversely impacted sales in 2009 and a

continuing economic downturn could result in further declines in revenues and

impair growth in 2010. Severely negative economic conditions could greatly

impair the ability and willingness of consumers to buy products. Operating

results are directly impacted by the health of the North American, European and

Asian economies. Business and financial performance may be adversely affected by

current and future economic conditions, including unemployment levels, energy

costs, interest rates, recession, inflation, the impact of natural disasters and

terrorist activities, and other matters that influence business and consumer

spending.

If

the national and global financial crisis intensifies, potential disruptions in

the credit markets may adversely affect business, including the availability and

cost of short-term funds for liquidity requirements and ability to meet

long-term commitments, which could adversely affect results of operations, cash

flows and financial condition.

If

internal funds are not available from operations we may be required to rely on

the banking credit and equity markets to meet financial commitments and

short-term liquidity needs. Even if the Company is able to successfully renew

the credit facility as discussed above, disruptions in the capital and credit

markets, as experienced during 2008 and 2009, could adversely affect its ability

to borrow pursuant to the Credit Agreement with Chase or to borrow from other

financial institutions. Access to funds under the Credit Agreement or pursuant

to arrangements with other financial institutions is dependent on Chase’s or

other financial institutions’ ability to meet funding commitments. Financial

institutions, including Chase, may not be able to meet their funding commitments

if they experience shortages of capital and liquidity or if they experience high

volumes of borrowing requests from other borrowers within a short period of

time.

7

Longer

term disruptions in the capital and credit markets as a result of uncertainty,

changing or increased regulation, reduced alternatives or failures of

significant financial institutions could adversely affect access to the

liquidity needed for business. Any disruption could require the Company to take

measures to conserve cash until the markets stabilize or until alternative

credit arrangements or other funding for our business needs can be arranged.

Such measures could include deferring capital expenditures and reducing or

eliminating future share repurchases, dividend payments or other discretionary

uses of cash.

Current

financial conditions in the United States and globally may have significant

effects on customers and suppliers that would result in material adverse effects

on business, operating results and stock price.

Current

financial conditions in the United States and globally and the concern that the

worldwide economy may enter into a prolonged recessionary period may materially

adversely affect customers’ access to capital or willingness to spend capital on

products and/or their levels of cash liquidity with which to pay for products

that they will order or have already ordered from the Company. In addition,

current financial conditions may materially adversely affect suppliers’ access

to capital and liquidity with which to maintain their inventories, production

levels and/or product quality, could cause them to raise prices, lower

production levels or result in their ceasing operations. Continuing adverse

economic conditions in our markets would also likely negatively impact business,

which could result in: (1) reduced demand for products; (2) increased price

competition for products; (3) increased risk of excess or obsolete inventories;

(4) increased risk of collectability of cash from customers; (5) increased risk

in potential reserves for doubtful accounts and write-offs of accounts

receivable; (6) reduced revenues and (7) higher operating costs as a percentage

of revenues.

All of

the foregoing potential consequences of current financial conditions are

difficult to forecast and mitigate. As a consequence, operating results for a

particular period are difficult to predict, and, therefore, prior results are

not necessarily indicative of future results to be expected in future periods.

Any of the foregoing effects could have a material adverse effect on business,

results of operations and financial condition and could adversely affect stock

price.

Negative

economic conditions could prevent us from accurately forecasting demand for our

products which could adversely affect our operating results or market

share.

The

current negative economic conditions and market instability in the United States

and globally makes it increasingly difficult for the Company, customers and

suppliers to accurately forecast future product demand trends, which could cause

the Company to produce excess products that can increase inventory carrying

costs and result in obsolete inventory. Alternatively, this forecasting

difficulty could cause a shortage of products, or materials used in products,

that could result in an inability to satisfy demand for products and a loss of

market share.

The

Company may pursue strategic acquisitions, which could have an adverse impact on

our business.

The

Company has grown in part over the years, through acquisitions of complementary

companies or businesses, which have been part of the strategic plan and may

continue to pursue acquisitions in the future from time to time. Acquisitions

may result in difficulties in assimilating acquired companies, and may result in

the diversion of capital and management’s attention from other business issues

and opportunities. The Company may not be able to successfully integrate

operations that it acquires, including their personnel, financial systems,

distribution, and operating procedures. If the Company fails to successfully

integrate acquisitions, business could suffer. In addition, the integration of

any acquired business, and their financial results, may adversely affect

operating results. Escalade will consider acquisitions in the future, but we

currently do not have any agreements with respect to any such

acquisitions.

8

Growth

may strain resources, which could adversely affect business and financial

performance.

Both the

sporting goods and office products businesses have grown over the past several

years through strategic acquisitions. Growth places additional demands on

management and operational systems. If the Company is not successful in

continuing to support operational and financial systems, expanding the

management team and increasing and effectively managing customers and suppliers,

growth may result in operational inefficiencies and ineffective management of

the business, which could adversely affect the business and financial

performance.

Ability

to expand business will be dependent upon the availability of adequate

capital.

The rate

of expansion will also depend on the availability of adequate capital, which in

turn will depend in large part on cash flow generated by the business and the

availability of equity and debt capital. Escalade can make no assurances that it

will be able to obtain equity or debt capital on acceptable terms or at all,

especially considering the current disruptions in the credit

markets.

Failure

to improve operational efficiency and reduce administrative costs could have a

material adverse effect on liquidity, financial position and results of

operations.

The

Company’s ability to improve profit margins is largely dependent on the success

of on-going initiatives to streamline infrastructure, improve operational

efficiency and reduction of administrative costs at every level of the Company.

Failure to continue to implement these initiatives successfully, or the failure

of such initiatives to result in improved profitability, could have a material

adverse effect on liquidity, financial position and results of

operations.

Business

may be adversely affected by the actions of and risks associated with

third-party suppliers.

The raw

materials that the Company purchases for manufacturing operations and many of

the products that it sells are sourced from a wide variety of third-party

suppliers. The Company cannot control the supply, design, function or cost of

many of the products that are offered for sale and are dependent on the

availability and pricing of key materials and products. Disruptions in the

availability of raw materials used in production of these products may adversely

affect sales and result in customer dissatisfaction. In addition, global

sourcing of many of the products sold is an important factor in our financial

performance. The ability to find qualified suppliers and to access products in a

timely and efficient manner is a significant challenge, especially with respect

to goods sourced outside the United States. Political instability, the financial

instability of suppliers, merchandise quality issues, trade restrictions,

tariffs, currency exchange rates, transport capacity and costs, inflation and

other factors relating to foreign trade are beyond the Company’s

control.

Historically,

instability in the political and economic environments of the countries in which

the Company or its suppliers obtain products and raw materials has not had a

material adverse effect on operations. However, the Company cannot predict the

effect that future changes in economic or political conditions in such foreign

countries may have on operations. In the event of disruptions or delays in

supply due to economic or political conditions in foreign countries, such

disruptions or delays could adversely affect results of operations unless and

until alternative supply arrangements could be made. In addition, products and

materials purchased from alternative sources may be of lesser quality or more

expensive than the products and materials currently purchased

abroad.

Deterioration

in relationships with suppliers or in the financial condition of suppliers could

adversely affect liquidity, financial position and results of

operations.

Access to

materials, parts and supplies is dependent upon close relationships with

suppliers and the ability to purchase products from the principal suppliers on

competitive terms. The Company does not enter into long-term supply contracts

with these suppliers, and has no current plans to do so in the future. These

suppliers are not required to sell to the Company and are free to change the

prices and other terms. Any deterioration or change in the relationships with,

or in the financial condition of our significant suppliers, could have an

adverse impact on the ability to procure materials and parts necessary to

produce products for sale and distribution. If any of the significant suppliers

terminated or significantly curtailed its relationship with the Company or

ceased operations, the Company would be forced to expand relationships with

other suppliers, seek out new relationships with new suppliers or risk a loss in

market share due to diminished product offerings and availability. Any change in

one or more of these suppliers’ willingness or ability to continue to supply the

Company with their products could have an adverse impact on liquidity, financial

position and results of operations.

9

Escalade

may be subject to product liability claims and the Company’s insurance may not

be sufficient to cover damages related to those claims.

The

Company may be subject to lawsuits resulting from injuries associated with the

use of sporting goods equipment and office products that it sells. The Company

may incur losses relating to these claims or the defense of these claims. There

is a risk that claims or liabilities will exceed our insurance coverage. In

addition, the Company may be unable to retain adequate liability insurance in

the future. In addition, the Company is subject to regulation by the Consumer

Product Safety Commission and similar state regulatory agencies. If the Company

fails to comply with government and industry safety standards, it may be subject

to claims, lawsuits, fines and adverse publicity that could have a material

adverse effect on our business, results of operations and financial

condition.

Intellectual

property rights are valuable, and any inability to protect them could reduce the

value of products.

The

Company obtains patents, trademarks and copyrights for intellectual property,

which represent important assets to the Company. If the Company fails to

adequately protect intellectual property through patents, trademarks and

copyrights, our intellectual property rights may be misappropriated by others,

invalidated or challenged, and our competitors could duplicate the Company’s

products or may otherwise limit any competitive design or manufacturing

advantages. The Company believes that success is likely to depend upon continued

innovation, technical expertise, marketing skills and customer support and

services rather than on legal protection of intellectual property rights.

However, the Company intends to aggressively assert its intellectual property

rights when necessary.

The

Company is subject to risks associated with laws and regulations related to

health, safety and environmental protection.

Products,

and the production and distribution of products, are subject to a variety of

laws and regulations relating to health, safety and environmental protection.

Laws and regulations relating to health, safety and environmental protection

have been passed in several jurisdictions in which the Company operates in the

United States and abroad. Although the Company does not anticipate any material

adverse effects based on the nature of operations and the thrust of such laws,

there is no assurance such existing laws or future laws will not have a material

adverse effect on business, results of operations and financial

condition.

International

operations expose the Company to the unique risks inherent in foreign

operations.

The

Company has operations in Mexico, Europe and Asia.. Foreign operations encounter

risks similar to those faced by U.S. operations, as well as risks inherent in

foreign operations, such as local customs and regulatory constraints, control

over product quality and content, foreign trade policies, competitive

conditions, foreign currency fluctuations and unstable political and economic

conditions. The 2003 acquisition of Schleicher & Company, International AG

in Germany and the Company’s business relationships in Asia have increased our

exposure to these foreign operating risks, which could have an adverse impact on

international income and worldwide profitability.

The

Company could be adversely affected by changes in currency exchange rates and/or

the value of the United States dollar.

The

Company is exposed to risks related to the effects of changes in foreign

currency exchange rates and the value of the United States dollar. Changes in

currency exchange rates and the value of the United States dollar can have a

significant impact on earnings from international operations. While the Company

carefully watches fluctuations in currency exchange rates, these types of

changes can have material adverse effects on business, results of operations and

financial condition.

10

Failure

to improve and maintain the quality of internal controls over financial

reporting could materially and adversely affect the ability to provide timely

and accurate financial information, which could harm the Company’s reputation

and share price.

Management

is responsible for establishing and maintaining adequate internal controls over

financial reporting for the Company to provide reasonable assurance regarding

the reliability of financial reporting and the preparation of financial

statements in accordance with generally accepted accounting principles.

Management cannot be certain that weaknesses and deficiencies in internal

controls will not arise or be identified or that the Company will be able to

correct and maintain adequate controls over financial processes and reporting in

the future. Any failure to maintain adequate controls or to adequately implement

required new or improved controls could harm operating results or cause failure

to meet reporting obligations in a timely and accurate manner. Ineffective

internal controls over financial reporting could also cause investors to lose

confidence in reported financial information, which could adversely affect the

trading price of the Company’s common stock.

Disclosure

controls and procedures are designed to provide reasonable assurance of

achieving their objectives. However, management, including the Chief Executive

Officer and Chief Financial Officer, does not expect that disclosure controls

and procedures will prevent all errors and all fraud. A control system, no

matter how well conceived and operated, can provide only reasonable, not

absolute, assurance that the objectives of the control system are met. Further,

the design of a control system must reflect the fact that there are resource

constraints, and the benefits of controls must be considered relative to their

costs. Because of inherent limitations in all control systems, no evaluation of

controls can provide absolute assurance that all control issues and instances of

fraud, if any, have been detected.

Failure

to effectively implement the global integrated information system (“SURGE”)

could cause incorrect information or delays in getting information which could

adversely affect the performance of the Company.

The

Company began an integrated information systems evaluation process in the fourth

quarter of 2007 which resulted in the selection of Oracle as its vendor. In

2008, the Company spent $6.6 million establishing the foundation and network for

a system wide-roll out. The project experienced some delays and the system went

live in the North American Office Products and one business entity within

Sporting Goods in the beginning of 2009. In 2009, the Company has spent

additional $0.8 million dollars. The Company is currently re-evaluating the

global integrated information system to compare costs to fully implement and

maintain this system with purchase and implementation costs and on-going

maintenance fees of other integrated information systems. Should the Company

decide to abandon the Oracle system, the remaining book value of the Oracle

system of approximately $5.9 million ($3.9 million, net of tax) would be

expensed over the estimated remaining economic life of the system. A decision

regarding full implementation options has not been made. There can be no

assurance the Company will have the necessary funds (estimated to be in excess

of $2.0 million) or the staff to fully avail itself of the control features

inherent in the system design. Without such utility, the Company management is

faced with cumbersome and time consuming efforts to manually consolidate its

financial information. Such inefficiencies and delays could cause sales and

profit to decline and/or could affect relationships with key customers and/or

suppliers.

The

preparation of financial statements requires the use of estimates that may vary

from actual results.

The

preparation of consolidated financial statements in conformity with accounting

principles generally accepted in the United States and the other countries in

which the Company does business requires management to make significant

estimates that may affect financial statements. Due to the inherent nature of

making estimates, actual results may vary substantially from such estimates,

which could materially adversely affect our business, financial condition, and

results of operations. For more information on our critical accounting

estimates, please see the Critical Accounting Estimates section on page 23 of

this Form 10-K.

11

Changes

in accounting standards could impact reported earnings and financial

condition.

The

accounting standard setters, including the Financial Accounting Standards Board,

the International Accounting Standards Board, the Securities & Exchange

Commission and the Public Company Accounting Oversight Board, periodically

change the financial accounting and reporting standards that govern the

preparation of our consolidated financial statements. These changes can be hard

to predict and apply and can materially affect how the Company records and

reports its financial condition and results of operations. In some cases, the

Company could be required to apply a new or revised standard retrospectively,

which may result in the restatement of prior period financial

statements.

Effective

tax rate may fluctuate.

We are a

multi-national, multi-channel provider of sporting goods and office products. As

a result, the Company’s effective tax rate is derived from a combination of

applicable tax rates in the various countries, states and other jurisdictions in

which the Company operates. The effective tax rate may be lower or higher than

our tax rates have been in the past due to numerous factors, including the

sources of income, any agreement with taxing authorities in various

jurisdictions, the tax filing positions taken in various jurisdictions and

changes in the political environment in the jurisdictions in which the Company

operates. We base estimates of an effective tax rate at any given point in time

upon a calculated mix of the tax rates applicable to the Company and to

estimates of the amount of business likely to be done in any given jurisdiction.

The loss of one or more agreements with taxing jurisdictions, a change in the

mix of business from year to year and from country to country, changes in rules

related to accounting for income taxes, changes in tax laws and any of the

multiple jurisdictions in which the Company operates, or adverse outcomes from

tax audits that the Company may be subject to in any of the jurisdictions in

which the Company operates, could result in an unfavorable change in the

effective tax rate which could have an adverse effect on business and results of

our operations.

The

market price of our common stock is likely to be highly volatile as the stock

market in general can be highly volatile.

The

public trading of our common stock is based on many factors, which could cause

fluctuation in the Company’s stock price. These factors may include, among other

things:

|

●

|

General

economic and market conditions;

|

|

|

●

|

Actual

or anticipated variations in quarterly operating

results;

|

|

|

●

|

Lack

of research coverage by securities analysts;

|

|

|

●

|

If

securities analysts provide coverage, our inability to meet or exceed

securities analysts’ estimates or expectations;

|

|

|

●

|

Conditions

or trends in our industries;

|

|

|

●

|

Changes

in the market valuations of other companies in our

industries;

|

|

|

●

|

Announcements

by us or our competitors of significant acquisitions, strategic

partnerships, divestitures, joint ventures or other strategic

initiatives;

|

|

|

●

|

Capital

commitments;

|

|

|

●

|

Additional

or departures of key personnel;

|

|

|

●

|

Sales

and repurchases of our common stock; and

|

|

|

●

|

The

ability to maintain listing of the Company’s common stock on the NASDAQ

Global Market.

|

Many of

these factors are beyond the Company’s control. These factors may cause the

market price of the Company’s common stock to decline, regardless of operating

performance.

12

Information

security may be compromised.

Through

sales and marketing activities, the Company collects and stores certain

information that customers provide to purchase products or services or otherwise

communicate and interact with the Company. Despite instituted safeguards for the

protection of such information, we cannot be certain that all of the systems are

entirely free from vulnerability to attack. Computer hackers may attempt to

penetrate the network security and, if successful, misappropriate confidential

customer or business information. In addition, an employee, a contractor or

other third party with whom we do business may attempt to circumvent the

Company’s security measures in order to obtain such information or inadvertently

cause a breach involving such information. Loss of customer or business

information could disrupt operations, damage the Company’s reputation, and

expose the Company to claims from customers, financial institutions, payment

card associations and other persons, any of which could have an adverse effect

on business, financial condition and results of operations. In addition,

compliance with tougher privacy and information security laws and standards may

result in significant expense due to increased investment in technology and the

development of new operational processes.

Terrorist

attacks or acts of war may seriously harm business.

Among the

chief uncertainties facing the nation and the world and, as a result, the

business, is the instability and conflict in the Middle East. Obviously, no one

can predict with certainty what the overall economic impact will be as a result

of these circumstances. Terrorist attacks may cause damage or disruption to the

Company, employees, facilities and customers, which could significantly impact

net sales, costs and expenses and financial condition. The potential for future

terrorist attacks, the national and international responses to terrorist

attacks, and other acts of war and hostility may cause greater uncertainty and

cause business to suffer in ways the Company currently cannot

predict.

These

risks are not exhaustive.

Other

sections of this Form 10-K may include additional factors which could adversely

impact business and financial performance. Moreover, the Company operates in a

very competitive and rapidly changing environment. New risk factors emerge from

time to time and it is not possible for management to predict all risk factors,

nor can the Company assess the impact of all factors on business or the extent

to which any factor, or combination of factors, may cause actual results to

differ materially from those contained in any forward-looking statements. Given

these risks and uncertainties, investors should not place undue reliance on

forward-looking statements as a prediction of actual results.

None.

13

At

December 26, 2009, the Company operated from the following

locations:

|

Location

|

Square

Footage

|

Owned

or Leased

|

Use

|

||||

|

Sporting Goods

|

|||||||

|

Evansville,

Indiana, USA

|

359,000 |

Owned

|

Distribution;

sales and marketing; administration

|

||||

|

Olney,

Illinois, USA

|

108,500 |

Leased

|

Manufacturing

and distribution

|

||||

|

Gainesville,

Florida, USA

|

154,200 |

Owned

|

Manufacturing

and distribution

|

||||

|

Rosarito,

Mexico

|

66,500 |

Owned

|

Manufacturing

and distribution

|

||||

|

Rosarito,

Mexico

|

108,200 |

Leased

|

Manufacturing

|

||||

|

Reynosa,

Mexico

|

126,800 |

Owned

|

Idle

|

||||

|

Raleigh,

N. Carolina, USA

|

69,800 |

Leased

|

Manufacturing

and distribution

|

||||

|

Jacksonville,

Florida, USA

|

18,000 |

Leased

|

Sales

and marketing

|

||||

|

Shanghai,

China

|

650 |

Leased

|

Sales

and sourcing

|

||||

|

Office Products

|

|||||||

|

Wabash,

Indiana, USA

|

141,000 |

Owned

|

Manufacturing

and distribution; sales and marketing; administration

|

||||

|

Sanford,

N. Carolina, USA

|

2,100 |

Leased

|

Sales

and marketing

|

||||

|

Markdorf,

Germany

|

70,300 |

Owned

|

Manufacturing

and distribution; sales and marketing; administration

|

||||

|

Paris,

France

|

1,335 |

Leased

|

Distribution;

sales and marketing

|

||||

|

Crawley,

UK

|

8,300 |

Leased

|

Sales

and marketing

|

||||

|

Barcelona,

Spain

|

8,600 |

Leased

|

Distribution;

sales and marketing

|

||||

|

Johannesburg,

South Africa

|

4,800 |

Leased

|

Distribution;

sales and marketing

|

||||

|

Sollentuna,

Sweden

|

1,400 |

Leased

|

Sales

office

|

||||

|

Beijing,

China

|

1,400 |

Leased

|

Sales

office

|

||||

At the

end of 2009, the Company has one idle facility. The Company completed the

consolidation of the Mexican production facilities into the Rosarito, Mexico

location in February 2009. The Reynosa facility is on the market to be sold;

however, it has been classified as held for use in the Company’s financial

statements. The Company believes that its facilities are in satisfactory and

suitable condition for their respective operations. The Company also believes

that it is in compliance with all applicable environmental regulations and is

not subject to any proceeding by any federal, state or local authorities

regarding such matters. The Company provides regular maintenance and service on

its plants and machinery as required.

The

Company is involved in litigation arising in the normal course of its business,

but the Company does not believe that the disposition or ultimate resolution of

such claims or lawsuits will have a material adverse affect on the business or

financial condition of the Company.

The

Company is not aware of any probable or levied penalties against the Company

relating to the American Jobs Creation Act.

14

The

Company’s common stock is traded under the symbol “ESCA” on the NASDAQ Global

Market. The following table sets forth, for the calendar periods indicated, the

high and low sales prices of the Common Stock as reported by the NASDAQ Global

Market:

|

Prices

|

High

|

Low

|

||||||

|

2009

|

||||||||

|

Fourth

quarter ended December 26, 2009

|

$ | 3.07 | $ | 1.96 | ||||

|

Third

quarter ended October 3, 2009

|

3.44 | 0.72 | ||||||

|

Second

quarter ended July 11, 2009

|

1.48 | 0.43 | ||||||

|

First

quarter ended March 21, 2009

|

1.15 | 0.30 | ||||||

|

2008

|

||||||||

|

Fourth

quarter ended December 27, 2008

|

$ | 2.54 | $ | 0.48 | ||||

|

Third

quarter ended October 4, 2008

|

5.40 | 2.51 | ||||||

|

Second

quarter ended July 12, 2008

|

9.14 | 4.80 | ||||||

|

First

quarter ended March 22, 2008

|

9.39 | 8.00 | ||||||

|

2007

|

||||||||

|

Fourth

quarter ended December 29, 2007

|

$ | 9.90 | $ | 8.78 | ||||

|

Third

quarter ended October 6, 2007

|

9.95 | 8.06 | ||||||

|

Second

quarter ended July 14, 2007

|

10.01 | 8.85 | ||||||

|

First

quarter ended March 24, 2007

|

10.78 | 8.98 | ||||||

The

closing market price on February 11, 2010 was $2.70 per share.

Depending

on profitability and cash flows from operations, the Board of Directors issues

annual dividends. Based on the Company’s 2008 and 2009 performance, the Board

did not declare a dividend in 2009 and does not expect to declare a dividend in

2010. Dividends issued/declared during 2008 and 2007 are as

follows:

|

Record

Date

|

Payment

Date

|

Amount

per Common Share

|

||||

|

March

9, 2007

|

March

16, 2007

|

$ | 0.22 | |||

|

March

14, 2008

|

March

21, 2008

|

$ | 0.25 | |||

There

were approximately 198 holders of record of the Company’s Common Stock at

February 11, 2010. The approximate number of stockholders, including those held

by depository companies for certain beneficial owners, was 937.

15

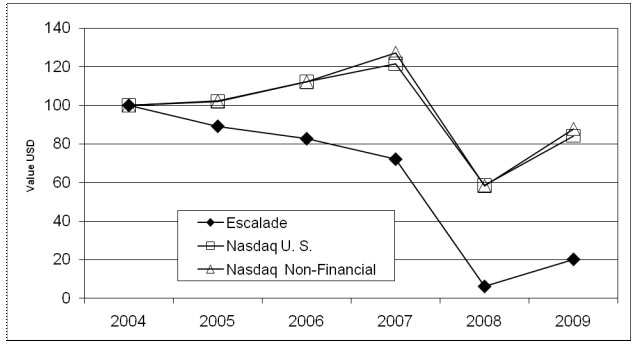

SHAREHOLDER

RETURN PERFORMANCE GRAPH

Set forth

below is a line graph comparing the yearly percentage change in the cumulative

total shareholder return on the Company’s common stock with that of the

cumulative total return on the NASDAQ US Stock Market Index and the NASDAQ

Non-Financial Stocks Index for the five year period ended December 26, 2009. The

following information is based on an investment of $100, on January 1, 2004, in

the Company’s common stock, the NASDAQ US Stock Market Index and the NASDAQ

Non-Financial Stocks Index, with dividends reinvested.

COMPARISON

OF FIVE YEAR CUMULATIVE TOTAL RETURN

|

2004

|

2005

|

2006

|

2007

|

2008

|

2009

|

|||||||||||||

|

Escalade

Common Stock

|

100 | 89 | 83 | 72 | 6 | 20 | ||||||||||||

|

NASDAQ

US Stock Index

|

100 | 102 | 112 | 122 | 59 | 84 | ||||||||||||

|

NASDAQ

Non-Financial Stock Index

|

100 | 102 | 112 | 127 | 58 | 88 | ||||||||||||

The above

performance graph does not constitute soliciting material and should not be

deemed filed or incorporated by reference into any other Company filing under

the Securities Act of 1933 or the Securities Exchange Act of 1934, except to the

extent the Company specifically incorporates the performance graph by reference

therein.

16

ISSUER

PURCHASES OF EQUITY SECURITIES

|

Period

|

(a)

Total Number of Shares (or Units) Purchased

|

(b) Average Price Paid per Share (or Unit) | (c) Total Number of Shares (or Units) Purchased as Part of Publicly Announced Plans or Programs |

(d)

Maximum Number (or Approximate Dollar Value) of Shares (or Units) that May

Yet Be Purchased Under the Plans or Programs

|

||||||||||||

|

Shares

purchases prior to 10/03/2009 under the current repurchase

program.

|

982,916 | $ | 8.84 | 982,916 | $ | 2,273,939 | ||||||||||

|

Fourth

quarter purchases:

|

||||||||||||||||

|

10/04/2009

– 10/31/2009

|

None

|

None

|

None

|

No

Change

|

||||||||||||

|

11/01/2009

– 11/28/2009

|

None

|

None

|

None

|

No

Change

|

||||||||||||

|

11/29/2009

– 12/26/2009

|

None

|

None

|

None

|

No

Change

|

||||||||||||

|

Total

share purchases under the current program

|

982,916 | $ | 8.84 | 982,916 | $ | 2,273,939 | ||||||||||

The

Company has one stock repurchase program which was established in February 2003

by the Board of Directors and which initially authorized management to expend up

to $3,000,000 to repurchase shares on the open market as well as in private

negotiated transactions. In each of February 2005 and 2006, August 2007 and

February 2008 the Board of Directors increased the remaining balance on this

plan to its original level of $3,000,000. The repurchase plan has no termination

date and there have been no share repurchases that were not part of a publicly

announced program.

17

(In

thousands, except per share data)

|

At

and For Years Ended

|

December

26, 2009

|

December

27, 2008

|

December

29, 2007

|

December

30, 2006

|

December

31, 2005

|

|||||||||||||||

|

Income

Statement Data

|

||||||||||||||||||||

|

Net

sales

|

||||||||||||||||||||

|

Sporting

goods

|

$ | 76,807 | $ | 98,039 | $ | 129,788 | $ | 136,733 | $ | 120,996 | ||||||||||

|

Office

products

|

39,192 | 50,647 | 55,788 | 54,732 | 62,319 | |||||||||||||||

|

Total

net sales

|

115,999 | 148,686 | 185,576 | 191,465 | 183,315 | |||||||||||||||

|

Net

income (loss)

|

1,657 | (7,496 | ) | 9,255 | 8,495 | 12,916 | ||||||||||||||

|

Weighted-average

shares

|

12,632 | 12,684 | 12,901 | 13,012 | 13,055 | |||||||||||||||

|

Per

Share Data

|

||||||||||||||||||||

|

Basic

earnings (loss) per share

|

$ | 0.13 | $ | (0.59 | ) | $ | 0.72 | $ | 0.65 | $ | 0.99 | |||||||||

|

Cash

dividends

|

$ | — | $ | 0.25 | $ | 0.22 | $ | 0.20 | $ | 0.15 | ||||||||||

|

Balance

Sheet Data

|

||||||||||||||||||||

|

Working

capital

|

9,688 | 4,842 | 31,442 | 33,125 | 42,350 | |||||||||||||||

|

Total

assets

|

127,238 | 147,701 | 152,016 | 150,715 | 124,860 | |||||||||||||||

|

Short-term

bank debt

|

27,644 | 46,525 | 13,033 | 10,336 | 1,066 | |||||||||||||||

|

Long-term

bank debt

|

— | — | 19,135 | 22,609 | 18,487 | |||||||||||||||

|

Total

stockholders’ equity

|

82,764 | 78,790 | 91,742 | 85,715 | 76,623 | |||||||||||||||

Fiscal

year 2009 was positively impacted by significant cost reductions and

consolidation of certain manufacturing and distributions

facilities.

Fiscal

year 2008 was negatively impacted by loss of sales to Sears, a major sporting

goods retailer, impairment of certain long-lived assets and a general economic

downturn.

Fiscal

year 2007 was positively impacted by the sale of rights to license potential

future intellectual property.

Fiscal

year 2006 was adversely impacted by the completion of a plan to rationalize

certain products in the Office Products business.

Fiscal

year 2005 the rationalization of certain products lowered sales in the Office

Products business.

The

following section should be read in conjunction with Item 1: Business; Item 1A:

Risk Factors; Item 6: Selected Financial Data; and Item 8: Financial Statements

and Supplementary Data.

Forward-Looking

Statements

This

report contains forward-looking statements relating to present or future trends

or factors that are subject to risks and uncertainties. These risks include, but

are not limited to, the impact of competitive products and pricing, product

demand and market acceptance, new product development, the continuation and

development of key customer and supplier relationships, Escalade’s ability to

control costs, general economic conditions, fluctuation in operating results,

changes in the securities market, Escalade’s ability to obtain financing and to

maintain compliance with the terms of such financing and other risks detailed

from time to time in Escalade’s filings with the Securities and Exchange

Commission. Escalade’s future financial performance could differ materially from

the expectations of management contained herein. Escalade undertakes no

obligation to release revisions to these forward-looking statements after the

date of this report.

18

Overview

Escalade,

Incorporated (“Escalade” or “Company”) manufactures and distributes products for

two industries: Sporting Goods and Office Products. Within these industries the

Company has successfully built a market presence in niche markets. This strategy

is heavily dependent on expanding the customer base, barriers to entry, brand

recognition and excellent customer service. A key strategic advantage is the

Company’s established relationships with major customers that allow the Company

to bring new products to the market in a cost effective manner while maintaining

a diversified product line and wide customer base. In addition to strategic

customer relations, the Company has substantial manufacturing and import

experience that enable it to be a low cost supplier.

A

majority of the Company’s products are in markets that are currently

experiencing low growth rates. Where the Company enjoys a commanding market

position, such as table tennis tables in the Sporting Goods segment and paper

folding machines in the Office Products segment, revenue growth is expected to

be roughly equal to general growth/decline in the economy. However, in markets

that are fragmented and where the Company is not the dominant leader, such as

archery in the Sporting Goods segment and data security shredders in the Office

Products segment, the Company anticipates growth. To enhance internal growth,

the Company has a strategy of acquiring companies or product lines that

complement or expand the Company’s product lines. A key objective is the

acquisition of product lines with barriers to entry that the Company can take to

market through its established distribution channels or through new market

channels. Significant synergies are achieved through assimilation of acquired

product lines into the existing company structure. Management believes that key

indicators in measuring the success of this strategy are revenue growth,

earnings growth and the expansion of channels of distribution. The following

table sets forth the annual percentage change in revenues and net income (loss)

over the past three years:

|

2009

|

2008

|

2007

|

||||||||||

|

Net

revenue

|

||||||||||||

|

Sporting

Goods

|

-21.7 | % | -24.5 | % | -5.1 | % | ||||||

|

Office

Products

|

-22.6 | % | -9.2 | % | 1.9 | % | ||||||

|

Total

|

-22.0 | % | -19.9 | % | -3.1 | % | ||||||

|

Net

Income

|

122.1 | % | -181.0 | % | 9.0 | % | ||||||

Results

of Operations

The

following schedule sets forth certain consolidated statement of income data as a

percentage of net revenue for the periods indicated:

|

2009

|

2008

|

2007

|

||||||||||

|

Net

revenue

|

100.0 | % | 100.0 | % | 100.0 | % | ||||||

|

Cost

of products sold

|

70.9 | % | 75.4 | % | 70.8 | % | ||||||

|

Gross

margin

|

29.1 | % | 24.6 | % | 29.2 | % | ||||||

|

Selling,

administrative and general expenses

|

25.4 | % | 26.8 | % | 20.8 | % | ||||||

|

Impairment

of assets

|

0.0 | % | 1.8 | % | 0.0 | % | ||||||

|

Amortization

|

2.0 | % | 1.5 | % | 1.4 | % | ||||||

|

Operating

income (loss)

|

1.7 | % | -5.5 | % | 7.0 | % | ||||||

Consolidated

Revenue and Gross Margin

Continued

sales declines to mass market retail customers in the Sporting Goods business

resulted in an overall decline of 21.7% in consolidated net revenues for 2009

compared to 2008. Declines in the specialty retail and dealer channels were

similar to declines in the mass market retail customers. Revenues from the

Office Products business decreased 22.6% in 2009 compared to 2008. Approximately

1% of the decline is due to changes in foreign exchange rates. The remaining

decline is a result of general economic conditions and tightening of credit

availability which has slowed customer spending.

19

The

overall gross margin in 2009 increased in the Sporting Goods business in

comparison to 2008 due to a combination of factors. Gross margin percentage for

2009 was 22.9% compared to 14.6% for 2008. The Company initiated various cost

reduction measures in 2008 including the consolidation of the Company’s Mexican

operations into one facility. This consolidation was completed in February 2009

and resulted in a reduction of the unfavorable manufacturing variances

experienced in 2008. The overall gross margin in 2009 decreased in the Office

Products business in comparison to 2008 to 41.3% compared to 43.8% in 2008 as a

result of lower sales volume which generated under absorbed factory

variances.

Consolidated

Selling, General and Administrative Expenses

Consolidated

selling, general and administrative expenses (“SG&A”) were $29.5 million in

2009 compared to $39.9 million in 2008, a decrease of $10.4 million or 26%. In

2008 and 2009, the Company implemented many costs saving initiatives including

the reduction of staff by approximately 20%, the voluntary reduction of officer

and director salaries by 10% and other cost saving initiatives from which the

effect was realized in 2009.

Other

Income

Other

income increased in 2009 compared to 2008. In 2008, the Company realized a loss

on the sale of third-party equity securities and recognized impairment on

remaining securities which combined totaled approximately $1.4 million. In 2009,

the Company sold its remaining equity securities and recognized approximately

$0.4 million gain; a partial recovery of the previously recorded impairment.

Income from equity investments increased approximately $0.5 to $1.6 million in

2009 compared with 2008.

Provision

for Income Taxes

The

effective income tax rate in 2009 was lower relative to 2008 primarily due to a

reduced tax benefit in 2008 resulting from state net operating losses generated

in 2008 for which the Company does not expect to be able to utilize. . The

effective tax rate for 2009 was 36.4% compared to (26.4%) and 34.9% in 2008 and

2007 respectively. The Company expects its future effective tax rates to

approximate the effective tax rate achieved in 2009.

Sporting

Goods

Net

sales, operating income (loss), and net income (loss) for the Sporting Goods

business segment for the three years ended December 26, 2009 were as

follows:

|

In

Thousands

|

2009

|

2008

|

2007

|

|||||||||

|

Net

Revenue

|

$ | 76,807 | $ | 98,039 | $ | 129,788 | ||||||

|

Operating

income (loss)

|

4,610 | (6,250 | ) | 7,745 | ||||||||

|

Net

income (loss)

|

1,273 | (5,428 | ) | 5,341 | ||||||||

Net

revenue declined 21.7% in 2009 compared to 2008. Sales to the Company’s mass

market retail customers declined roughly 22% in 2009 compared to 2008 and

reflect the same two factors as in the previous year; a general slowdown in the

US economy which is adversely affecting mass retailers in general and a

continued industry wide decline in consumer demand for game tables. The Company

continues to aggressively pursue opportunities with its mass market retail

customers, but 2010 sales to this channel are expected to be comparable to 2009.

To improve this trend, the Company continues to pursue a strategy of expanding

certain product offerings and distribution through specialty retailers and

dealers. Sales to these channels now comprise 46% of total revenues compared to

45% and 38% for 2008 and 2007, respectively. Anticipated sales in the specialty

retail and distributor channels are expected to remain relatively stable in

2010. Consequently, the Company anticipates total 2010 sales for the Sporting

Goods segment to be comparable to 2009.

20

Sales in

2008 were lower than 2007 due primarily to a reduction in sales to the

Sears.

The gross

margin ratio in 2009 increased 56.9% compared to 2008 due to aggressive cost

reduction measures and facility consolidation. As a result, operating income as

a percentage of net revenue increased to 6.0% in 2009 compared to a loss of 6.4%

in 2008. Management anticipates operating income to slightly increase in 2010 as

2009 personnel reductions and facility consolidations are fully

realized.

Net

income for 2009 increased from 2008 due primarily to realization of cost cutting

measures and improved gross margins and the nonrecurring impact of the Company’s

long-lived asset impairment adjustments in 2008.

Office

Products

Net

sales, operating income, and net income for the Office Products business segment

for the three years ended December 26, 2009 were as follows:

|

In

Thousands

|

2009

|

2008

|

2007

|

|||||||||

|

Net

Sales

|

$ | 39,192 | $ | 50,647 | $ | 55,788 | ||||||

|

Operating

income

|

1,780 | 3,930 | 8,809 | |||||||||

|

Net

income

|

1,077 | 1,835 | 5,617 | |||||||||

Sales in

the Office Products business decreased 22.6% in 2009 compared to 2008 primarily

due to the worsening of the U.S. economy and economic problems in Southern

Europe and Russian countries. Management anticipates a return of revenues from

office product retailers as the economy stabilizes. The Company has widened its

product range and offered new product launches to improve its

opportunities.

Excluding

the effect of changing foreign exchange rates, 2008 sales were down 9.2% from

2007.

Profitability

in the Office Products segment decreased in 2009 as evidenced by the ratio of

operating income to net sales which decreased to 4.6% in 2009 compared with 7.8%

in 2008. The primary reasons for this decline in profitability are under

absorbed factory variances due to low sales and changes in product mix, an

increasingly competitive environment, and foreign exchange rate fluctuations.

Management anticipates operating income to increase in 2010 due to a broadening