Attached files

| file | filename |

|---|---|

| EX-32.2 - EX-32.2 - NCS Multistage Holdings, Inc. | ncsm-20201231xex32_2.htm |

| EX-32.1 - EX-32.1 - NCS Multistage Holdings, Inc. | ncsm-20201231xex32_1.htm |

| EX-31.2 - EX-31.2 - NCS Multistage Holdings, Inc. | ncsm-20201231xex31_2.htm |

| EX-31.1 - EX-31.1 - NCS Multistage Holdings, Inc. | ncsm-20201231xex31_1.htm |

| EX-23.1 - EX-23.1 - NCS Multistage Holdings, Inc. | ncsm-20201231xex23_1.htm |

| EX-21.1 - EX-21.1 - NCS Multistage Holdings, Inc. | ncsm-20201231xex21_1.htm |

| EX-10.30 - EX-10.30 - NCS Multistage Holdings, Inc. | ncsm-20201231xex10_30.htm |

| EX-10.29 - EX-10.29 - NCS Multistage Holdings, Inc. | ncsm-20201231xex10_29.htm |

| EX-4.1 - EX-4.1 - NCS Multistage Holdings, Inc. | ncsm-20201231xex4_1.htm |

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☑ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2020

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ______ to ______

Commission file number: 001-38071

NCS Multistage Holdings, Inc.

(Exact name of registrant as specified in its charter)

|

|

|

|

|

|

|

|

Delaware |

|

46-1527455 |

|

|

|

(State or other jurisdiction of incorporation or organization) |

|

(IRS Employer Identification number) |

|

|

|

|

|

|

|

|

|

19350 State Highway 249, Suite 600 |

|

|

|

|

|

Houston, Texas |

|

77070 |

|

|

|

(Address of principal executive offices) |

|

(Zip Code) |

|

Registrant’s telephone number, including area code: (281) 453-2222

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

|

|

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

|

Common Stock, $0.01 par value |

NCSM |

NASDAQ Capital Market |

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☑

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

|

|

|

|

|

|

|

|

Large accelerated filer |

☐ |

Accelerated filer |

☐ |

|

|

|

Non-accelerated filer |

☑ |

Smaller reporting company |

☑ |

|

|

|

|

|

Emerging growth company |

☑ |

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☑

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C.7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☑

As of June 30, 2020, the aggregate market value of the common stock of the registrant held by non-affiliates of the registrant was approximately $7.6 million (based on the closing sale price of the registrant’s common stock on that date).

As of March 4, 2021, there were 2,360,007 shares of common stock outstanding.

Portions of the definitive proxy statement for the registrant’s 2021 Annual Meeting of Stockholders are incorporated by reference in Part III of this Form 10-K. Such proxy statement will be filed with the Securities and Exchange Commission not later than 120 days after December 31, 2020.

|

|

|

|

|

|

|

Page |

|

Item 1. |

8 | |

|

Item 1A. |

15 | |

|

Item 1B. |

35 | |

|

Item 2. |

35 | |

|

Item 3. |

35 | |

|

Item 4. |

35 | |

|

Item 5. |

36 | |

|

Item 6. |

37 | |

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

40 |

|

Item 7A. |

58 | |

|

Item 8. |

60 | |

|

Item 9. |

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

93 |

|

Item 9A. |

93 | |

|

Item 9B. |

93 | |

|

Item 10. |

94 | |

|

Item 11. |

94 | |

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

94 |

|

Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

94 |

|

Item 14. |

94 | |

|

Item 15. |

95 | |

|

Item 16. |

97 | |

| 98 | ||

2

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (this “Form 10-K”) includes certain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements can be identified by words such as “anticipates,” “intends,” “plans,” “seeks,” “believes,” “estimates,” “expects” and similar references to future periods, or by the inclusion of forecasts or projections. Examples of forward-looking statements include, but are not limited to, statements we make regarding the outlook for our future business and financial performance, including the effects of the Coronavirus disease 2019 (“COVID-19”) pandemic thereon, such as those contained in Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Forward-looking statements are based on our current expectations and assumptions regarding our business, the economy and other future conditions. Because forward-looking statements relate to the future, by their nature, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict. As a result, our actual results may differ materially from those contemplated by the forward-looking statements. Important factors that could cause our actual results to differ materially from those in the forward-looking statements include regional, national or global political, economic, business, competitive, market and regulatory conditions and the following:

|

· |

the risks and uncertainties relating to public health crises, including the COVID-19 pandemic and its continuing impact on market conditions and our business, financial condition, results of operations, cash flows and stock price; |

|

· |

declines in the level of oil and natural gas exploration and production (“E&P”) activity within Canada and the United States; |

|

· |

oil and natural gas price fluctuations; |

|

· |

the financial health of our customers including their ability to pay for products or services provided; |

|

· |

inability to successfully implement our strategy of increasing sales of products and services into the United States; |

|

· |

significant competition for our products and services that results in pricing pressures, reduced sales, or reduced market share; |

|

· |

loss of significant customers; |

|

· |

our inability to successfully develop and implement new technologies, products and services; |

|

· |

our inability to protect and maintain critical intellectual property assets; |

|

· |

losses and liabilities from uninsured or underinsured business activities; |

|

· |

our failure to identify and consummate potential acquisitions; |

|

· |

our inability to integrate or realize the expected benefits from acquisitions; |

|

· |

currency exchange rate fluctuations; |

|

· |

impact of severe weather conditions; |

|

· |

risks resulting from the operations of a joint venture arrangement; |

|

· |

restrictions on the availability of our customers to obtain water essential to the drilling and hydraulic fracturing processes; |

|

· |

changes in legislation or regulation governing the oil and natural gas industry, including restrictions on emissions of greenhouse gases (“GHGs”); |

|

· |

our inability to meet regulatory requirements for use of certain chemicals by our tracer diagnostics business; |

|

· |

change in trade policy, including the impact of additional tariffs; |

|

· |

our inability to accurately predict customer demand, which may result in us holding excess or obsolete inventory; |

|

· |

failure to comply with or changes to federal, state and local and non-U.S. laws and other regulations, including anti-corruption and environmental regulations, the Coronavirus Aid, Relief, and Economic Security Act (the “CARES Act”) and the U.S. Tax Cuts and Jobs Act of 2017 (the “2017 Tax Act”); |

|

· |

loss of our information and computer systems; |

|

· |

system interruptions or failures, including complications with our enterprise resource planning system (“ERP”), cyber security breaches, identity theft or other disruptions that could compromise our information; |

|

· |

impairment in the carrying value of long-lived assets and goodwill; |

|

· |

our failure to establish and maintain effective internal control over financial reporting; |

3

|

· |

our success in attracting and retaining qualified employees and key personnel; |

|

· |

risks and uncertainties relating to cost reduction efforts or savings we may realize from such cost reduction efforts; |

|

· |

the reduction in our Senior Secured Credit Facility borrowing base or our inability to comply with the covenants in our debt agreements; and |

|

· |

our inability to obtain sufficient liquidity on reasonable terms, or at all. |

See Item 1A. “Risk Factors” and Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations” of this Form 10-K for a further description of these and other factors that could cause actual results to differ materially from those in the forward-looking statements. For the reasons described above, we caution you against relying on any forward-looking statements, which should also be read in conjunction with the other cautionary statements that are included elsewhere in this Form 10-K. Any forward-looking statement made by us in this Form 10-K speaks only as of the date on which we make it. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

4

RISK FACTORS SUMMARY

You should carefully consider the information set forth below in Item 1A. “Risk Factors” before deciding whether to invest in our securities. Below is a summary of principal risks associated with an investment in our securities.

|

· |

Our business, financial condition, results of operations, cash flows and stock price have been negatively impacted and may in the future be materially adversely affected by the COVID-19 pandemic. |

|

· |

Our business depends on the levels of expenditures by companies in the oil and natural gas industry and particularly on the level of E&P activity within Canada and the United States. |

|

· |

The cyclicality of the oil and natural gas industry may cause our results of operations to fluctuate. |

|

· |

Low commodity price environments can negatively impact oil and natural gas E&P companies and, in some cases, impair their ability to timely pay for products or services provided or can result in their insolvency or bankruptcy, any of which exposes us to credit risk of our oil and natural gas E&P customers. |

|

· |

We may not be able to successfully implement our strategy of increasing sales of our products and services for use in basins located in the United States. |

|

· |

Competition within our industry may adversely affect our ability to market our services. |

|

· |

A single customer constituted 10% of our revenue for the year ended December 31, 2020 and 8% of our revenue for the years ended December 31, 2019 and 2018. The loss of that customer or any other of our significant customers, or their failure to pay the amounts they owe us, could cause our revenue to decline substantially. |

|

· |

Our success depends on our ability to develop and implement new technologies, products and services. |

|

· |

Advancements in drilling and well completion technologies could have a material adverse effect on our business, financial condition, results of operations and cash flows. |

|

· |

Our competitors may infringe upon, misappropriate, violate or challenge the validity or enforceability of our intellectual property and we may not be able to adequately protect or enforce our intellectual property rights in the future. We may be adversely affected by disputes regarding intellectual property rights. |

|

· |

Our products are used in operations that are subject to potential hazards inherent in the oil and natural gas industry, including claims for personal injury and property damage, and, as a result, we are exposed to potential liabilities that may affect our financial condition and reputation. |

|

· |

Losses and liabilities from operating activities could have a material adverse effect on our financial condition and operations. |

|

· |

The growth of our business through acquisitions or strategic partnerships exposes us to various risks, including identifying suitable opportunities and integrating businesses, assets and personnel. |

|

· |

A significant amount of our revenue generated is denominated in the Canadian dollar and could be negatively impacted by currency fluctuations. |

|

· |

We conduct a portion of our operations through the Repeat Precision, LLC (“Repeat Precision”) joint venture, which subjects us to additional risks that could adversely affect the success of these operations and the ability of Repeat Precision to make cash distributions to us, which could adversely impact our financial position and results of operations. |

|

· |

Our operations may be limited or disrupted in certain parts of the continental United States, Canada and Norway during severe weather conditions, which could have a material adverse effect on our business, financial condition and results of operations. |

|

· |

Hydraulic fracturing is substantially dependent on the availability of water. Restrictions on the ability of our customers to obtain water may have a material adverse effect on our business, financial condition and results of operations. |

|

· |

The adoption of climate change legislation or regulations restricting emissions of GHGs, and associated litigation, could result in increased compliance or operating costs, limit the areas in which our customers may conduct exploration and production activities, and reduce demand for oil and natural gas. |

|

· |

Federal and state legislative and regulatory initiatives relating to hydraulic fracturing could result in increased costs and additional operating restrictions or delays on our customers which could in turn decrease the demand for our products and services. |

|

· |

Restrictions on drilling activities intended to protect certain species of wildlife may adversely affect the ability of our customers to conduct drilling activities in some of the areas where we operate. |

5

|

· |

We may not be able to meet applicable regulatory requirements for our use of certain chemicals by our tracer diagnostics business, and, even if requirements are met, complying on an ongoing basis with the numerous regulatory requirements will be time-consuming and costly. |

|

· |

Our operations and our customers’ operations are subject to a variety of governmental laws and regulations that may increase our costs, limit the demand for our products and services or restrict our operations. |

|

· |

Changes in trade policies, including the imposition of tariffs, could negatively impact our business, financial condition and results of operations. |

|

· |

If we are unable to accurately predict customer demand or if customers cancel their orders on short notice, we may hold excess or obsolete inventory, which would reduce gross margins. Conversely, insufficient inventory would result in lost revenue opportunities and potentially a loss in market share and damaged customer relationships. |

|

· |

We could be subject to additional income tax liabilities. |

|

· |

Loss of our information and computer systems could adversely affect our business. |

|

· |

We are subject to cyber security risks. A cyber incident could occur and result in information theft, data corruption, operational disruption and/or financial loss. |

|

· |

Complications with our ERP system could adversely impact our business and operations. |

|

· |

Impairment in the carrying value of long-lived assets and goodwill could negatively affect our operating results. |

|

· |

Our business operations in countries outside of the United States are subject to a number of U.S. federal laws and regulations, including restrictions imposed by the Foreign Corrupt Practices Act as well as trade sanctions administered by the Office of Foreign Assets Control and the Commerce Department. |

|

· |

Our success may depend on the continued service and availability of key personnel. |

|

· |

We may be unable to attract and retain skilled and technically knowledgeable employees, which could adversely affect our business. |

|

· |

We are subject to the risk of supplier concentration. |

|

· |

We may not be able to satisfy technical requirements, testing requirements, code requirements or other specifications under contracts and contract tenders. |

|

· |

Our outstanding indebtedness could adversely affect our financial condition and our ability to operate our business, and we may not be able to generate sufficient cash flows to meet our debt service obligations. |

|

· |

Restrictive covenants in the agreement governing our Senior Secured Credit Facility may restrict our ability to pursue our business strategies. |

|

· |

We are controlled by the funds controlled by Advent International Corporation (“Advent”), whose interests may differ from those of our public stockholders. |

|

· |

Future sales of our common stock, or the perception in the public markets that these sales may occur, could cause the market price for our common stock to decline. |

|

· |

Anti-takeover protections in our amended and restated certificate of incorporation, our amended and restated bylaws or our contractual obligations may discourage or prevent a takeover of our company, even if an acquisition would be beneficial to our stockholders. |

|

· |

We are an “emerging growth company” and “smaller reporting company” and may elect to comply with reduced reporting requirements applicable to emerging growth companies, which could make our common stock less attractive to investors. |

|

· |

We may identify material weaknesses or otherwise fail to maintain an effective system of internal controls, which may result in material misstatements of our financial statements or cause to us to fail to meet our reporting obligations or fail to prevent fraud; which would harm our business and could negatively impact the price of our common stock. |

We own or have the rights to use various trademarks, service marks and trade names referred to in this Form 10-K, including, among others, AirLock, MultiCycle, OST, Innovus, Terrus, Qumulus, Mongoose, PurpleSeal Express, Repeat Precision, NCS Multistage and NCS and their respective logos. Solely for convenience, we refer to trademarks, service marks and trade names in this Form 10-K without the TM, SM and ® symbols. Such references are not intended to indicate, in any way, that we will not assert, to the fullest extent permitted by law, our rights to our trademarks, service marks and trade names. Third party trademarks, service marks or trade names appearing in this Form 10-K are the property of their respective owners.

6

Available information

Our website address is www.ncsmultistage.com. Information that we furnish to or file with the Securities and Exchange Commission (the “SEC”), including our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements, and any amendments to, or exhibits included in, those reports or statements are available for download, free of charge, on our website as soon as reasonably practicable after such materials are filed with or furnished to the SEC. From time to time, we also post announcements, updates, events, investor information and presentations on our website at http://ir.ncsmultistage.com in addition to copies of all recent press releases as means of disclosing material non-public information and for complying with our disclosure obligations under Regulation FD. Reports and statements that we file with or furnish to the SEC, including related exhibits, are also available on the SEC’s website at www.sec.gov. The contents of the websites referred to above are not incorporated into this filing. References to the URLs for these websites are intended to be inactive textual references only.

7

NCS Multistage Holdings, Inc. (“NCS,” the “Company,” “we,” “our” or “us”) is a leading provider of highly engineered products and support services that facilitate the optimization of oil and natural gas well completions and field development strategies. We provide our products and services primarily to E&P companies for use in onshore wells, predominantly wells that have been drilled with horizontal laterals in unconventional oil and natural gas formations. Our products and services are utilized in oil and natural gas basins throughout North America and in selected international markets, including Argentina, China, Russia, the Middle East and the North Sea. Our extensive research and development efforts are influenced and driven by the needs of our customers, allowing us to introduce innovative and commercial solutions that improve customer efficiency and profitability. We provided our products and services to over 200 customers in 2020, including leading large independent oil and natural gas companies and major oil companies.

Our primary offering is our fracturing systems products and services, which enable efficient pinpoint stimulation: the process of individually stimulating each entry point into a formation targeted by an oil or natural gas well. We began providing pinpoint stimulation products and services in 2006 and our fracturing systems products and services are typically utilized in cemented wellbores and enable our customers to precisely place stimulation treatments in a more controlled and repeatable manner as compared with traditional completion techniques. Fracturing systems products and services include our casing-installed sliding sleeves and downhole frac isolation assembly. Customers typically purchase our casing-installed sliding sleeves, a consumable product that is cemented at intervals into the casing of the wellbore and can also utilize services associated with our downhole frac isolation assembly, where our personnel supervise the use of the downhole frac isolation assembly during completion operations. Our fracturing systems products and services are utilized in conjunction with third-party providers of pressure pumping, coiled tubing and other services.

We own a 50% controlling interest in Repeat Precision, which we consolidate. Repeat Precision markets composite frac plugs and related products directly to customers and provides high-quality machining services for NCS products.

We provide tracer diagnostics services for well completion and reservoir characterization that utilize downhole chemical and radioactive tracers. Our customers utilize these services to better characterize their assets and to optimize completion designs. Chemical and radioactive tracer studies may provide a cost-effective and reliable means to determine the production profile along a lateral, assess fluid and proppant communication between wells during completions and determine stage and cluster level efficiency of completion designs.

We sell products for well construction, including our AirLock casing buoyancy system, liner hanger systems and toe initiation sleeves. Our customers utilize these products to safely and efficiently install casing and production liners, facilitate cementing operations and initiate a flow path into the formation at the commencement of stimulation operations.

Our revenue for the years ended December 31, 2020, 2019 and 2018, was $107.0 million, $205.5 million and $227.0 million, respectively. Our net loss attributable to NCS Multistage Holdings, Inc. for the years ended December 31, 2020, 2019 and 2018, was $(57.6) million, $(32.8) million and $(190.3) million, respectively. Our total assets for the years ended 2020, 2019 and 2018, were $138.7 million, $202.6 million and $229.7 million, respectively. For additional financial information by geographic area, see “Note 18. Segment and Geographic Information” of our consolidated financial statements.

Our business strategy is to increase the adoption of our products and services in all geographies, continue to be an innovator of technology and create value for our stockholders. We intend to achieve these objectives by (i) pursuing disciplined organic growth through increasing market adoption of our products and services in the United States, Canada and in select international markets, (ii) developing and introducing innovative technologies that are aligned with customer needs, (iii) maintaining financial strength and flexibility and (iv) selectively pursuing complementary acquisitions and joint ventures.

Through implementing this strategy, including the investment in Repeat Precision and the acquisition of Spectrum Tracer Services, LLC (“Spectrum”) in 2017, we have diversified our revenue base. In 2020, approximately 50% of our revenue was derived from fracturing systems products and services, nearly 30% was derived from Repeat Precision and approximately 10% was derived from each of our well construction products and tracer diagnostics services. This represents a more balanced portfolio, serving a larger addressable market than in 2016, when over 90% of our revenue was derived from fracturing systems products and services, with the remainder from well construction products. In addition, this diversification of our revenue base has, in part, contributed to a reduction in the percentage of revenue derived from the Canadian market from 71% in 2016 to 45% in 2020.

8

Products and Services

We provide highly engineered products and support services that facilitate the optimization of oil and natural gas well completions and field development strategies. Our key products and services include:

|

· |

Fracturing Systems. Our fracturing systems products and services encompasses our technology developed to enable efficient pinpoint stimulation and re-stimulation strategies. Pinpoint stimulation is the process of individually stimulating each entry point into a formation targeted by an oil or natural gas well, a process that we believe improves on traditional completion techniques. Our pinpoint stimulation solutions and refined field processes are designed to enable efficient, controlled, verifiable and repeatable completions. |

Our fracturing systems products and services are comprised of our casing-installed sliding sleeves and our downhole frac isolation assemblies, which are deployed using coiled tubing. Our services include advising customers on optimizing completion designs and operating the downhole frac isolation assemblies.

|

· |

Casing-installed sliding sleeves. Our Innovus casing-installed sliding sleeves are a consumable product, sold to our customers and cemented in place in a well’s casing. We produce two primary models of sliding sleeves: models which can be opened only once, and models which can be opened and closed multiple times throughout the life of a well giving our customers the benefit of additional completion options and the ability to better optimize a well’s production phase. We have recently introduced a new sliding sleeve model with a dual-barrel that can be converted during the production phase to regulate water injection in enhanced recovery applications. Our casing-installed sliding sleeves can be utilized in both cemented and open-hole wellbores, with no practical limitation on the number of stages that can be installed in a well, and feature an inner-diameter which is the same as the casing in the wellbore. During completion operations, the downhole frac isolation assembly is placed in the sleeve and the inner barrel of the sleeve is shifted down, exposing the frac ports to the formation, allowing the completion of that stage to begin. |

|

· |

Downhole frac isolation assembly. Our proprietary downhole frac isolation assembly is comprised of several subcomponents, including a resettable bridge plug for stage isolation, a sleeve locator to efficiently locate our sliding sleeves in the wellbore, an abrasive perforating sub that can perforate the casing where our sliding sleeves are not installed and gauge packages that can measure and record downhole data. The assembly, which is attached to a third-party’s coiled tubing reel, is primarily used to locate our sliding sleeves, to establish wellbore isolation and to shift our sliding sleeves open or closed. In addition, gauges within the downhole frac isolation assembly record downhole pressure and temperature data, which can be utilized to optimize the design of future completions. Further, because our downhole frac isolation assembly is deployed on coiled tubing, our customers have access to real-time downhole pressure measurements which can be used to adjust strategies during a well completion. We typically do not sell the assemblies and utilize them in our service to our customers. Our personnel operate the assemblies during completion operations in coordination with other on-site service providers. |

|

· |

Sand jet perforating. Our sand jet perforating technology uses a variation of the downhole frac isolation assembly utilized for shifting sleeves. Sand jet perforating is typically used with cemented wellbores. To cut access points into the formation, sand-laden fluid is pumped down the coiled tubing and through tungsten-carbide nozzles. The high-velocity slurry cuts through the casing and cement and into the formation. The tunnels created through this process serve as initiation points for stimulation. Stimulation treatments are pumped down the annulus between the coiled tubing and the casing. Although the sand jet perforating process requires more time per stage than using sliding sleeves, it provides a practical option for pinpoint stimulation in wells that are already cased, as in the case of drilled, but uncompleted wells. |

|

· |

SpotFrac system. Our SpotFrac system provides a means to straddle and mechanically isolate producing zones for targeted refracturing applications. The system includes a sand jet perforating assembly, enabling additional stages to be added if desired, and can perforate, isolate and stimulate multiple stages in a single trip. |

|

· |

Accelus sleeves. Our Accelus sliding sleeves can be cemented in place or utilized in open-hole wells. The sleeves are activated by pumping a ball from the surface that lands on seats in the sleeves, providing pinpoint stimulation. In some instances, the Accelus sleeves will be utilized together with our coiled-tubing deployed technology in a hybrid application to increase the number of stages that can be run in extended-reach applications, with the Accelus sleeves installed at the toe of such wells. |

|

· |

Repeat Precision. We own a 50% interest in Repeat Precision. Repeat Precision markets its high-performance Purple Seal line of composite frac plugs and bridge plugs, RP single-use disposable setting tools, Purple Seal Express systems, which combine a Purple Seal Frac Plug with a single-use disposable setting tool, and related products. It sells these products directly to E&P customers as well as to other oilfield services companies that act as distributors. Repeat Precision also provides high-quality machining services for certain NCS products. |

9

|

· |

Tracer Diagnostics. We provide chemical and radioactive tracer diagnostics technologies used by E&P companies to assess completion performance, evaluate well production, and optimize field development strategies. Our fracture fluid identifier tracers, water-soluble tracers (“WSTs”), oil-soluble tracers (“OSTs”) and natural gas tracers enable efficient, cost-effective downhole diagnostics, providing E&P companies with critical data to better optimize reservoir development and production. |

|

· |

Well Construction. Our well construction products are designed to allow our customers to safely and efficiently install casing and production liners, facilitate cementing operations and initiate a flow path into the formation at the commencement of stimulation operations. Our well construction products include: |

|

· |

AirLock casing buoyancy system. Our AirLock casing buoyancy system facilitates landing casing strings in horizontal wells without altering a customer’s preferred casing and cementing operations. The AirLock system, which is installed with a well’s casing, allows the vertical casing section to be filled with fluid, while the lateral section remains air-filled and buoyant. The enhanced buoyancy significantly reduces sliding friction, while the enhanced weight of the vertical section provides the force needed to push the casing to the toe of the well, ensuring the casing reaches the desired depth and reducing casing running time and cost. Our AirLock system consists of two components that are made up in the casing string during run-in: a debris-trap and a seal collar. The debris-trap is installed in a casing connection just above the float shoe and the seal collar is installed at the bottom-most point of the vertical portion of the wellbore. The seal collar contains a breakable seal that locks air in the lower section of casing while the upper section is run and filled with fluid. After the casing is landed, surface pressure is increased to fragment the seal at a predetermined pressure, leaving an unrestricted casing bore, while seal fragments are collected by the debris-trap, facilitating cementing operations. |

|

· |

Liner hanger systems. Our proprietary liner hanger systems are specifically designed to perform in complex horizontal wells and are fully compatible with our fracturing systems products. The liner hanger is used to distribute the loads and weight of the liner to the supporting casing. |

|

· |

Toe initiation sleeves. Our toe initiation sleeves are designed to provide initial formation access for multistage completions. After shifting open the toe initiation sleeve, a customer can perform a casing integrity test, a pre-frac injection fall-off test, flush the wellbore to facilitate the pumping of completion tools to the toe of the well or execute the first fracturing stage for the well. |

Business History

We were incorporated in Delaware on November 28, 2012, under the name “Pioneer Super Holdings, Inc.” On December 13, 2016, we changed our name to “NCS Multistage Holdings, Inc.” On May 3, 2017, we completed the initial public offering (“IPO”) of our common stock.

Reverse Stock Split

On December 1, 2020, we implemented a reverse stock split of our shares of common stock in a ratio of 1-for-20, and no change in the par value of the common and preferred stock. In connection with the reverse stock split, we transferred our securities to the Nasdaq Capital Market effective December 24, 2020. Unless we indicated otherwise, all share and per share information in this Annual Report on Form 10-K (“Form 10-K”) reflects the reverse stock split. For additional information regarding the reverse stock split, see “Note 1. Organization and Basis of Presentation” and “Note 12. Stockholders’ Equity” of our consolidated financial statements.

Intellectual Property and Patent Protection

We have dedicated resources to the development and acquisition of new technology and products designed to optimize well completions and field development strategies, primarily for use in onshore wells drilled with horizontal laterals in unconventional formations. Our sales and earnings are influenced by our ability to successfully introduce new or improved products to the North American and international markets. Our fracturing systems, wellbore construction products, tracer and other equipment and services involve proprietary technologies, some of which are protected by patents.

We hold 40 U.S. utility patents and 43 related international utility patents. These relate to various products and services from each of our product lines, such as our Airlock casing buoyancy system, OSTs, casing installed sliding sleeves, frac isolation assemblies, and other equipment and methods utilized in the provision of our services. Our U.S. utility patents expire between 2030 and 2039. Our international utility patents expire between 2025 and 2036.

We also have a number of U.S. and international patent applications pending. Some of these patent applications cover equipment and methods which are currently in development. The applications are in various stages of the patent prosecution process and patents may not issue on such applications in any jurisdiction for some time, if they issue at all.

10

We believe that our patents have historically been important in enabling us to compete in the market to supply our customers with our products and services. We intend to enforce, and have in the past vigorously enforced, our intellectual property rights. We may from time to time in the future be involved in litigation to determine the enforceability, scope and validity of our patent rights. In addition to patent rights, we use a significant amount of trade secrets, or “know-how,” and other proprietary information and technology as well as intellectual property licensed from third parties.

Customers

Our customer base primarily consists of oil and natural gas producers in North America and certain international markets as well as oilfield service companies. For the years ended December 31, 2020, 2019 and 2018, we had over 200, 325 and 310 customers, respectively. Our top five customers accounted for approximately 31%, 22% and 24% of our revenue for the years ended December 31, 2020, 2019 and 2018, respectively. Crescent Point Energy (“Crescent Point”) accounted for 10% of our revenue during the year ended December 31, 2020. No other customer accounted for more than 10% of our revenue during 2020. No customer represented more than 10% of our revenue for the years ended December 31, 2019 and 2018. Although we believe we have a broad customer base and wide geographic coverage of operations, the loss of one or more of our significant customers could have a material adverse effect on our results of operations. For additional information relating to risks regarding the loss of any of our significant customers, see Item 1A. “Risk Factors.”

Our sales and marketing activities are performed through a technically-trained direct sales force. We recognize the importance of a technical marketing program in demonstrating the advantages of new technologies that offer benefits relative to established industry methodologies. Our technical sales force advises customers on the benefits of pinpoint stimulation, Innovus sliding sleeves, well construction products and tracer diagnostics services.

In the U.S. and Canada, sales of our fracturing systems products and services, liner hangers and tracer diagnostics services are made directly to E&P companies. Our customers also hire coiled tubing companies and pressure pumping services companies that work alongside us during the completion of a well. We provide our AirLock casing buoyancy system, liner hanger products and toe initiation sleeves directly to E&P companies as well as to oilfield services companies that act as distributors for those products. Although we do not typically maintain supply or service contracts with our customers, a significant portion of our sales represents recurring business. Repeat Precision, which maintains a sales force separate from NCS in the U.S., sells its products directly to E&P companies as well as to oilfield services companies that act as distributors.

International sales are made through local NCS entities or to our local operating partners on a free on board or free carrier basis with a point of sale in the United States. Some of the locations in which we have operating partners or sales representatives include China and the Middle East. Our operating partners and representatives do not have authority to contractually bind our company, but market our products in their respective territories as part of their product or service offering.

We provide extensive support services and have developed proprietary methodologies for assessing and reporting the information that is collected on our downhole gauges and through tracer diagnostics evaluations.

In addition to the technical marketing effort, we occasionally engage in field trials to demonstrate the economic benefits of our products and services.

Seasonality

A substantial portion of our business is subject to quarterly variability. In Canada, we typically experience higher activity levels in the first quarter of each year, as our customers take advantage of the winter freeze to gain access to remote drilling and production areas. In the past, our revenue in Canada has declined during the second quarter due to warming weather conditions that result in thawing, softer ground, difficulty accessing drill sites and road bans that curtail drilling and completion activity. Access to well sites typically improves throughout the third and fourth quarters in Canada, leading to activity levels that are higher than in the second quarter, but lower than activity in the first quarter. Our business can also be impacted by a reduction in customer activity during the winter holidays in late December and early January. In recent years, many customers in the U.S. exhausted their capital budgets prior to the end of the year, leading to reductions in drilling and completion activity during the fourth quarter.

Suppliers and Raw Materials

We acquire component parts and raw materials from suppliers, including machine shops. The prices we pay for our raw materials may be affected by, among other things, energy, steel and other commodity prices, tariffs and duties on imported materials

11

and foreign currency exchange rates. Most of the raw materials we use in our operations, such as steel in various forms, electronic components, chemicals and elastomers are available from many sources.

We generally try to purchase our raw materials from multiple suppliers, so we are not dependent on any one supplier. We will generally utilize multiple machine shops for the manufacturing of our component parts so that we are not dependent on any one machine shop. To decrease fixed costs, in connection with a more challenging commodity price environment, we have reduced our internal manufacturing capacity and relied more heavily on certain machine shops. Our suppliers are also active in multiple regions which allows us to react to changes in foreign currency exchange rates and tariffs and duties. For example, we have made changes to the suppliers of certain raw materials based on tariff rates. In addition, sourcing certain product categories from Repeat Precision allows us to reduce our costs.

While we experienced modest disruptions to our supply chain as a result of the COVID-19 pandemic, including delays in importation of certain chemical products from China and temporary work-from-home orders that reduced the capacity at the Repeat Precision machine shop operations in Mexico, such disruptions were temporary in nature, the impacted products are available through alternative sources of supply and we maintained sufficient inventory on hand to meet customer demand. We have also experienced delays in access to certain materials and products utilized in our research and development activities, which has led, and may continue to lead to delays in new product introductions. See Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for more information.

Operating Risks and Insurance

We currently carry a variety of insurance for our operations. Although we believe we currently maintain insurance coverage adequate for the risks involved, there is a risk our insurance may not be sufficient to cover any particular loss or that our insurance may not cover all losses.

The markets in which we operate are highly competitive. To be successful, we must provide services and products that meet the specific needs of E&P companies at competitive prices. We compete in all areas of our operations with a number of companies, some of which have financial and other resources greater than or comparable to ours.

We believe that we compete not only against other providers of pinpoint stimulation equipment and services, but also with companies that support the other primary means of hydraulically fracturing a horizontal well, including plug and perf and ball drop completions. We also compete with other suppliers of well construction products, tracer diagnostics services, and composite frac plugs.

Our major competitors for our completion products and services include Baker Hughes Company (“Baker Hughes”), Core Laboratories N.V., DMC Global Inc., Forum Energy Technologies, Inc., Halliburton Company, Innovex Downhole Solutions, Nine Energy Service, Inc., NOV Inc., Oil States International, Inc., Packers Plus Energy Services, Schlumberger Limited, Schoeller-Bleckmann Oilfield Equipment AG and Weatherford International public limited company as well as a number of smaller or regional competitors.

We believe that the most significant factors influencing a customer’s decision to utilize our equipment and services are technology, service quality, safety track record and price. While we must be competitive in our pricing, we believe our customers select our products and services based on the technical attributes of our products and equipment, the level of technical and operational service we provide before, during and after the job, and the know-how derived from our extensive operational track record.

Government Regulations

We are subject to stringent and complex federal, state, provincial and local laws and regulations governing the discharge of materials into the environment or otherwise relating to protection of worker health, safety and the environment. Compliance with these laws and regulations may require the acquisition of permits to conduct regulated activities, capital expenditures to prevent, limit or address emissions and discharges, and stringent practices to handle, recycle and dispose of certain wastes and materials. Failure to comply with these laws and regulations may result in the assessment of administrative, civil and criminal penalties, the imposition of remedial or corrective obligations, and the issuance of injunctive relief.

We believe that we are in substantial compliance with applicable environmental, health and safety laws and regulations. Further, we do not anticipate that compliance with existing environmental, health and safety laws and regulations will have a material effect on our consolidated financial statements. However, laws and regulations protecting the environment generally have become more stringent in recent years and are expected to continue to do so. It is possible, that substantial costs for compliance with applicable environmental, health and safety laws and regulations may be incurred in the future. Moreover, it is possible that other developments,

12

such as the adoption of stricter environmental laws, regulations, and enforcement policies, could result in additional costs or liabilities that we cannot currently quantify.

While we do not anticipate that compliance with existing environmental, health and safety laws and regulations will have a material adverse effect on our operations, we and/or our customers are subject to a wide range of such laws and regulations, which could materially and adversely affect their businesses and indirectly, through reduced demand for our products and services, have a material adverse effect on our business, financial condition and results of operations, including with respect to the following:

|

· |

Air Emissions. The Federal Clean Air Act (the “CAA”) and comparable state laws regulate emissions of various air pollutants through air emissions permitting programs and the imposition of other emission control requirements. In addition, the Environmental Protection Agency (“EPA”) has developed, and continues to develop, stringent regulations governing emissions of toxic air pollutants at specified sources. Non-compliance with air permits or other requirements of the CAA and associated state laws and regulations can result in the imposition of administrative, civil and criminal penalties, as well as the issuance of orders or injunctions limiting or prohibiting non-compliant operations. |

|

· |

Water Discharges. The Federal Clean Water Act (the “CWA”), and analogous state laws impose restrictions and strict controls with respect to the discharge of pollutants, including spills and leaks of oil and other substances, into state waters or waters of the United States. The discharge of pollutants into regulated waters is prohibited, except in accordance with the terms of a permit issued by the EPA or an analogous state agency. Federal and state regulatory agencies can impose administrative, civil and criminal penalties as well as other enforcement mechanisms for non-compliance with discharge permits or other requirements of the CWA and analogous state laws and regulations. |

|

· |

Climate Change. Governmental and public concern over the threat of climate change arising from GHG emissions is giving rise to an increased likelihood of regulatory actions to address climate change in the United States and abroad. As a result, our customers are or may become subject to statutes or regulations aiming to reduce emissions of GHGs. In December 2009, the EPA determined that emissions of carbon dioxide, methane and other GHGs present an endangerment to public health and the environment because emissions of such gases are, according to the EPA, contributing to warming of the earth’s atmosphere and other climatic changes. Based on these findings, the EPA has begun adopting and implementing regulations to restrict emissions of GHGs under existing provisions of the CAA. For example, in June 2016, the EPA published final rules under the CAA that establish new and more stringent emission control standards for methane and volatile organic compounds (“VOCs”) released from new and modified oil and natural gas development and production operations. These rules could have an adverse effect on our customers and result in an indirect material adverse effect on our business. However, in September 2020, the EPA finalized amendments that relax certain aspects of the methane and VOC emissions limitations, including rescinding the methane and VOC standards for the transmission and storage segment of the oil and natural gas industry, rescinding emissions limits for methane from all segments of the industry and revising standards for VOC emissions in the production and processing segments of the industry. The 2016 rules as well as the September 2020 amendments are the subject of litigation and, as a result, the future implementation of these rules remains uncertain. Regardless of the pending litigation, the EPA under the current administration may reconsider the September 2020 final rule, which could result in more stringent rulemaking. |

Various U.S. states or groups of states have adopted or considered adopting legislation, regulations or other governmental actions focused on reducing GHG emissions, including cap and trade programs, carbon taxes, reporting and tracking initiatives and renewable portfolio standards. At the international level, the United Nations-sponsored Paris Agreement is a non-binding agreement for nations to limit their GHG emissions through individually-determined reduction goals. Although the United States withdrew from the Paris Agreement in November 2020, the President issued an executive order recommitting the United States to the Paris Agreement on January 20, 2021. Although it is not possible at this time to predict how any legal requirements imposed following the implementation of the Paris Agreement or otherwise that may be adopted or issued to address GHG emissions would impact our business or that of our customers, any such future laws, regulations or legal requirements imposing reporting or permitting obligations on, or limiting emissions of GHGs from, oil and natural gas exploration activities could require our customers to incur costs to reduce emissions of GHGs associated with their operations. In addition, substantial limitations on GHG emissions could adversely affect demand for the oil and natural gas our customers produce.

|

· |

Non-Hazardous and Hazardous Wastes. The Resource Conservation and Recovery Act (“RCRA”) and comparable state laws control the management and disposal of hazardous and non-hazardous waste. These laws and regulations govern the generation, storage, treatment, transfer and disposal of wastes that our customers generate. Drilling fluids, produced waters, and most of the other wastes associated with the exploration, development, and production of oil or natural gas, if properly handled, are currently exempt from regulation as hazardous waste under RCRA and, instead, are regulated under RCRA’s less stringent non-hazardous waste provisions, state laws or other federal laws. It is possible, however, that certain oil and natural gas drilling and production wastes now classified as non-hazardous could be classified as hazardous wastes in the future. A loss of the RCRA exclusion for drilling fluids, produced waters and related wastes could result in an increase in our customers’ costs to manage and dispose of generated wastes and a corresponding decrease in their drilling operations, which developments could have a material adverse effect on our business. |

13

|

· |

Contamination. The Comprehensive Environmental Response, Compensation, and Liability Act, and comparable state laws, impose joint and several liability, without regard to fault or legality of conduct, on classes of persons who are considered to be responsible for the release of a hazardous substance into the environment. These persons include the owner or operator of the site where the release occurred, and anyone who disposed or arranged for the disposal of a hazardous substance released at the site. In addition, it is not uncommon for neighboring landowners and other third-parties to file claims for personal injury and property damage allegedly caused by hazardous substances released into the environment. |

|

· |

Occupational Health and Safety. We are subject to a number of federal and state laws and regulations, including the federal Occupational Safety and Health Act and comparable state statutes, establishing requirements to protect the health and safety of workers. Substantial fines and penalties can be imposed and orders or injunctions limiting or prohibiting certain operations may be issued in connection with any failure to comply with laws and regulations relating to worker health and safety. |

|

· |

Radioactive Materials. Part of our business involves the use of radioactive tracers, typically consisting of three standard isotopes (Iridium 192, Scandium 46 and Antimony 124), to help determine the existence of fractures within a well formation. The use of these materials requires us to obtain and comply with radioactive materials licenses issued by the U.S. Nuclear Regulatory Commission (“NRC”) or its counterparts in the states where we perform these services if they are among the states to which the NRC has delegated its regulatory authority pursuant to the Atomic Energy Act (so-called “Agreement States”). Under the terms of these licenses, we are required to train designated personnel, maintain records, submit periodic reports, ensure the safety and reliability of related equipment and storage facilities, conduct radiation safety monitoring, and ensure the proper disposal of materials and equipment at the end of their useful lives. In the event we fail to adequately comply with these requirements, we could be subject to enforcement action, which could include fines, injunctive relief, or the revocation of our licenses. |

In addition, the oil and natural gas industry is extensively regulated by numerous federal, state and local authorities, including with respect to permitting for the drilling of wells, drilling bonds and reporting concerning operations. Legislation and regulation affecting the oil and natural gas industry is frequently under review for amendment or expansion, which can increase the regulatory burden. Failure to comply with laws and regulations can result in substantial fines and penalties. In addition, the effect of these regulations may be to limit or increase the cost of oil and natural gas E&P companies, which could have a material adverse effect on our customers and indirectly materially and adversely affect our business. Although changes to the regulatory burden on the oil and natural gas industry could affect the demand for our services, we would not expect to be affected any differently or to any greater or lesser extent than other companies in the industry with similar operations.

We supply equipment and services to customers in the oil and natural gas industry conducting hydraulic fracturing operations. Although we do not directly engage in hydraulic fracturing activities, our customers purchase our products and services for use in their hydraulic fracturing activities. Hydraulic fracturing is typically regulated by state oil and natural gas commissions and similar agencies. Some states have adopted, and other states are considering adopting, regulations that could impose new or more stringent permitting, disclosure or well construction requirements on hydraulic fracturing operations. States could also elect to prohibit high volume hydraulic fracturing altogether, following the approach taken by the State of New York in 2015. Aside from state laws, local land use restrictions may restrict drilling in general or hydraulic fracturing in particular. Municipalities may adopt local ordinances attempting to prohibit hydraulic fracturing altogether or, at a minimum, allow such fracturing processes within their jurisdictions to proceed but regulating the time, place and manner of those processes. In addition, the federal government can limit hydraulic fracturing activities on federal lands through permitting. On January 27, 2021, the current administration issued an executive order directing the Secretary of the Interior to pause on entering into new oil and natural gas leases on public lands or offshore waters to the extent possible. This moratorium is subject to litigation, which remains pending. In addition, the current administration cancelled the construction permit for the Keystone XL oil pipeline, which would have transported Canadian oil to the Gulf Coast. We do not currently expect that the recent executive order regarding leases on public land or the cancellation of the Keystone XL oil pipeline will have a material impact on our business in the short term. Various studies have also been conducted or are currently underway by the EPA, and other federal agencies concerning the potential environmental impacts of hydraulic fracturing activities. State and federal regulatory agencies have recently focused on a possible connection between the operation of injection wells used for oil and natural gas waste disposal and seismic activity. Similar concerns have been raised that hydraulic fracturing may also contribute to seismic activity. At the same time, certain environmental groups have suggested that additional laws may be needed to more closely and uniformly limit or otherwise regulate the hydraulic fracturing process, and legislation has been proposed by some members of Congress to provide for such regulation.

The current administration’s moratorium on entering into new oil and natural gas leases on public lands and efforts to decrease or eliminate fossil fuel subsidies as well as the adoption of new laws or regulations at the federal or state levels prohibiting, limiting or otherwise regulating the hydraulic fracturing process could make it more difficult, or even impossible, to complete oil and natural gas wells, increase our customers’ costs of compliance and doing business, and otherwise adversely affect the hydraulic fracturing services they perform, which could negatively impact demand for our products and services. In addition, heightened political, regulatory, and public scrutiny of hydraulic fracturing practices could expose us or our customers to increased legal and regulatory

14

proceedings, which could be time-consuming, costly, or result in substantial legal liability or significant reputational harm. We could be directly affected by adverse litigation involving us, or indirectly affected if the cost of compliance limits the ability of our customers to operate. Such costs and scrutiny could directly or indirectly, through reduced demand for our products and services, have a material adverse effect on our business, financial condition and results of operations.

As of December 31, 2020, we had 210 employees of which 191 are full-time employees. As of such date, 119 of our employees were based in the United States, 84 were based in Canada and seven were based outside of North America. Our international operations, with the exception of our Argentinean operations, are currently serviced by employees from the United States and Canada. In addition, our consolidated joint venture, Repeat Precision, has 218 employees, 20 of which are based in the U.S. and 198 of which are based in Mexico. We are not a party to any collective bargaining agreements, and we consider our relations with our employees to be good.

Described below are certain risks that we believe apply to our business and the industry in which we operate. You should carefully consider each of the following risk factors in conjunction with other information provided in this Form 10-K and in our other public disclosures. The risks described below highlight potential events, trends or other circumstances that could adversely affect our business, financial condition, results of operations, cash flows, liquidity or access to sources of financing, and consequently, the market value of our common stock. Additional risks and uncertainties not currently known to us or that we currently deem immaterial may also materially adversely affect our business, financial condition and results of operations. All forward-looking statements made by us or on our behalf are qualified by the risks described below.

Risks Related to Our Business and the Oil and Natural Gas Industry

Our business, financial condition, results of operations, cash flows and stock price have been negatively impacted and may in the future be materially adversely affected by the COVID-19 pandemic.

Our business, financial condition, results of operations, cash flows and stock price have been negatively impacted and may in the future be materially adversely affected by the decline in market conditions primarily related to COVID-19 which has spread from China to many other countries including the United States. In March 2020, the World Health Organization characterized COVID-19 as a pandemic, and the President of the United States declared the COVID-19 pandemic a national emergency. The pandemic has resulted in governments around the world implementing increasingly stringent measures to help control the spread of the virus, including quarantines, “shelter in place” and “stay at home” orders, travel restrictions, business curtailments, school closures, and other measures.

The demand for crude oil has been materially reduced as a result of such measures taken by governments around the world, which has resulted in excess supply of crude oil and a rapid and material reduction in crude oil prices. As a result, E&P companies responded by significantly reducing their capital expenditure for 2020, resulting in significant reductions in drilling and completion activity, which led to a decrease in demand by our customers for our products and services for the year. In 2021, E&P companies have announced planned capital expenditure budgets that target maintaining production at levels consistent with late 2020, resulting in modest year-over year reductions in capital spending. For as long as we remain in a low commodity price environment, we would generally expect our customers and potential customers to continue to operate at these lower levels of drilling, completion and other production activities or, if conditions worsen, they may further reduce their capital expenditures. These lower capital expenditure levels have resulted in and will continue to result in a reduction in spending on our products and services and impact the prices we are able to charge our customers. Furthermore, if any of our significant customers decides not to continue to use our products and services, or if any of our key suppliers experiences a significant disruption that limits our ability to manufacture and sell certain of our products, as a result of the COVID-19 pandemic, our revenue would decline, which could have a material adverse effect on our business, financial condition and results of operations.

Although we believe our cash on hand, cash flows from operations and potential borrowings under our Senior Secured Credit Facility (defined below) will be sufficient to fund our capital expenditures and liquidity requirements for the next twelve months, we cannot guarantee that this will be the case, particularly if the decline in market conditions primarily related to the COVID-19 pandemic on the demand for crude oil, customer spending and the resulting demand for our products and services continues for an extended period of time or worsens. These negative impacts of the COVID-19 pandemic have had and are likely to continue to have a material negative impact on our financial performance, which could result in a breach of the covenants and a default under the Amended Credit Agreement (defined below). In the event of a default, the lenders may elect to declare all outstanding borrowings under the facility immediately due and payable. In addition, the total amount available to be drawn under our Senior Secured Credit Facility is substantially lower than the commitments due to borrowing limits imposed by our borrowing base that is calculated based on eligible receivables, which does not include receivables at Repeat Precision, and the amount available may decline if our business

15

continues to be materially adversely impacted by the decline in market conditions primarily related to the COVID-19 pandemic. In the event of a reduction in liquidity as a result of a default under the Amended Credit Agreement or the reduction of our borrowing capacity as result of business conditions, we may not be able to obtain liquidity from additional indebtedness, the capital markets or otherwise on reasonable terms, or at all, and our business may not generate sufficient cash flow from operations to fund our debt obligations or capital requirements.

We are considered a critical infrastructure industry, as defined by the U.S. Department of Homeland Security. Although we have continued to operate our facilities to date consistent with federal guidelines and state and local orders, the COVID-19 pandemic and any preventive or protective actions taken by governmental authorities may have a material adverse effect on our operations, supply chain, customers and transportation networks, including business shutdowns or disruptions. To date, we have experienced delays in importation of certain chemical products from China, and temporary work-from-home orders have reduced operating capacity at the Repeat Precision machine shop operations in Mexico. We have also experienced delays in access to certain materials and products utilized in our research and development activities, which has led, and may continue to lead to delays in new product introductions. Work-from-home orders and other restrictions have also led to delays in planned work in Argentina and China.

On March 31 and April 1, 2020, we also implemented, as of such date, a workforce reduction resulting in termination of over 80 employees, temporary furloughs for certain employees and lower compensation levels for executives and employees not participating in furloughs and on May 4, 2020 and in July 2020, we implemented, as of such date, additional workforce reductions resulting in the termination of approximately 50 employees per each reduction in response to the current difficult market conditions primarily related to the COVID-19 pandemic, the recent fall in demand for, and the price of, crude oil and reductions in customer capital spending plans. The reductions result in the loss of longer-term employees, institutional knowledge and expertise and the reallocation and combination of certain roles and responsibilities across the organization. These reductions, or others which may be caused by, but not limited to, the temporary inability of our workforce to work due to illness, quarantine, or government action, may negatively impact our operations.

The increase in certain of our employees working remotely has amplified certain information technology risks to our business and increased the demand on our information technology resources and systems, including increased phishing and other cyber security attacks as cybercriminals attempt to exploit uncertainty surrounding the COVID-19 pandemic and an increase in the number of points of potential attack, including laptops and mobile devices, to be secured. Any failure to effectively manage these risks, including to identify and appropriately respond to any cyberattacks, may adversely affect our business.

The extent to which the COVID-19 pandemic may continue to adversely impact our business depends on future developments, which are highly uncertain and unpredictable, depending upon the severity and duration of the pandemic and the effectiveness of actions taken globally to contain or mitigate its effects. Any resulting financial impact cannot be estimated reasonably at this time, but may materially adversely affect our business, financial condition, results of operations and cash flows. Even after the COVID-19 pandemic has subsided, we may experience materially adverse impacts to our business due to any resulting economic recession or depression. To the extent the COVID-19 pandemic adversely affects our business, financial results and results of operations, it may also have the effect of heightening many of the other risks described below.

Our business depends on the levels of expenditures by companies in the oil and natural gas industry and particularly on the level of E&P activity within Canada and the United States.

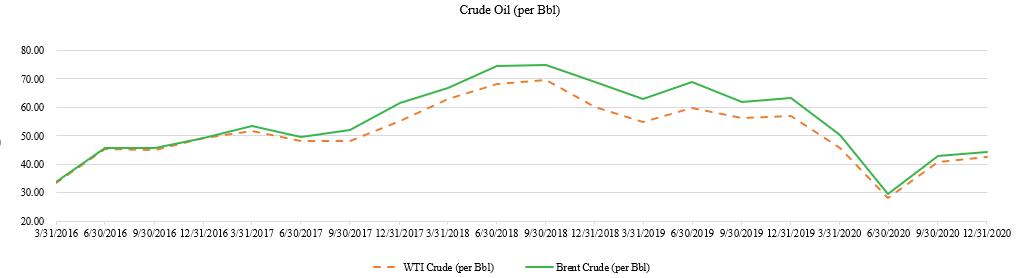

Demand for our products and services depends substantially on the level of expenditures by companies in the oil and natural gas industry. These expenditures are generally dependent on our customers’ views of future oil and natural gas prices and are sensitive to our customers’ views of future economic growth and the resulting impact on demand for oil and natural gas. Declines, as well as anticipated declines, in oil and natural gas prices could result in project modifications, delays or cancellations, general business disruptions, and delays in payment of, or nonpayment of, amounts that are owed to us. For example, the COVID-19 pandemic in 2020 materially reduced the demand for crude oil and natural gas as a result of measures taken by governments around the world to mitigate the spread of the disease, which lead to a decline in commodity prices. The low commodity price environment resulted in a reduction in the drilling, completion and other production activities of most of our customers and a reduction in their spending on our products and services. The reduction in demand from our customers reduced the prices we were able to charge our customers for our products and services. Although oil pricing has improved since mid-2020, oil and natural gas prices remain volatile, and prolonged reductions in oil and natural gas prices have had and may continue to have a material adverse effect on our business, financial condition and results of operations. In addition, more stable or higher commodity prices do not necessarily translate to a higher level of expenditures by companies in the oil and natural gas industry. For example, in recent years, investors in E&P companies have been prioritizing free cash flow and return of capital to shareholders over production growth, leading to lower expenditures. In addition, E&P companies require significant capital to drill and complete wells and it is becoming increasingly difficult to access capital. These trends may continue, even if commodity prices were to increase.

16

Many factors over which we have no control affect the supply of and demand for, and our customers’ willingness to explore, develop and produce oil and natural gas, and therefore, influence demand levels and prices for our products and services, including:

|

· |

the domestic and foreign supply of and demand for oil and natural gas; |

|

· |

the level of prices, and expectations about future prices, of oil and natural gas; |

|

· |

the level of global oil and natural gas E&P; |

|

· |

the cost of exploring for, developing, producing and delivering oil and natural gas; |

|

· |

the expected decline rates of current production; |

|

· |

the price and quantity of foreign imports; |

|

· |

political and economic conditions in oil producing countries, including the Middle East, Africa, South America and Russia; |

|

· |

the ability of members of the Organization of Petroleum Exporting Countries (“OPEC”) to agree to and maintain oil price and production controls; |

|

· |

regional or global health epidemics; |

|

· |

speculative trading in crude oil and natural gas derivative contracts; |

|

· |

the level of consumer product demand; |

|

· |

the discovery rates of new oil and natural gas reserves; |

|

· |

contractions in the credit market; |

|

· |

the strength or weakness of the United States Dollar (“USD”); |

|

· |

available pipeline and other transportation capacity; |

|

· |

the levels of oil and natural gas storage; |

|

· |

weather conditions and other natural disasters; |

|

· |

political instability in oil and natural gas producing countries; |

|

· |

domestic and foreign tax policy; |

|

· |

domestic and foreign governmental approvals and regulatory requirements and conditions; |

|

· |

the continued threat of terrorism and the impact of military and other action, including military action in the Middle East; |

|

· |

technical advances affecting energy demand, generation and consumption; |

|

· |