Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - CURO Group Holdings Corp. | q32018ex-322cfo906cert.htm |

| EX-32.1 - EXHIBIT 32.1 - CURO Group Holdings Corp. | q32018ex-321ceo906cert.htm |

| EX-31.2 - EXHIBIT 31.2 - CURO Group Holdings Corp. | q32018ex-312cfo302cert.htm |

| EX-31.1 - EXHIBIT 31.1 - CURO Group Holdings Corp. | q32018ex-311ceo302cert.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended September 30, 2018

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _________to__________

Commission File Number 1-38315

CURO GROUP HOLDINGS CORP.

(Exact name of registrant as specified in its charter)

Delaware | 90-0934597 | |

(State or other jurisdiction Of incorporation or organization) | (I.R.S. Employer Identification No.) | |

3527 North Ridge Road, Wichita, KS | 67205 | |

(Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (316) 425-1410

Former name, former address and former fiscal year, if changed since last report: No Changes

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | Accelerated filer | ☐ | |

Non-accelerated filer | ☒ | |||

Smaller reporting company | ☐ | Emerging growth company | ☐ | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

At October 31, 2018 there were 45,992,983 shares of the registrant’s Common Stock, $0.001 par value per share, outstanding.

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

FORM 10-Q

THIRD QUARTER ENDED SEPTEMBER 30, 2018

INDEX

Page | |||||||

Item 1. | Financial Statements (unaudited) | ||||||

September 30, 2018 and December 31, 2017 | |||||||

Three and nine months ended September 30, 2018 and 2017 | |||||||

Three and nine months ended September 30, 2018 and 2017 | |||||||

Nine months ended September 30, 2018 and 2017 | |||||||

Item 2. | |||||||

Item 3. | |||||||

Item 4. | |||||||

Item 1. | |||||||

Item 1A. | |||||||

Item 2. | |||||||

Item 3. | |||||||

Item 4. | |||||||

Item 5. | |||||||

Item 6. | |||||||

2

PART I. FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

(in thousands, except share data)

September 30, 2018 | December 31, 2017 | ||||||

(Unaudited) | |||||||

ASSETS | |||||||

Cash | $ | 153,361 | $ | 162,374 | |||

Restricted cash (includes restricted cash of consolidated VIEs of $19,107 and $6,871 as of September 30, 2018 and December 31, 2017, respectively) | 24,236 | 12,117 | |||||

Gross loans receivable (includes loans of consolidated VIEs of $353,384 and $213,846 as of September 30, 2018 and December 31, 2017, respectively) | 567,675 | 432,837 | |||||

Less: allowance for loan losses (includes allowance for losses of consolidated VIEs of $49,951 and $46,140 as of September 30, 2018 and December 31, 2017, respectively) | (76,068 | ) | (69,568 | ) | |||

Loans receivable, net | 491,607 | 363,269 | |||||

Deferred income taxes | — | 772 | |||||

Income taxes receivable | 16,363 | 3,455 | |||||

Prepaid expenses and other | 40,109 | 42,512 | |||||

Property and equipment, net | 79,790 | 87,086 | |||||

Goodwill | 143,966 | 145,607 | |||||

Other intangibles, net of accumulated amortization of $43,250 and $41,156 as of September 30, 2018 and December 31, 2017, respectively) | 33,208 | 32,769 | |||||

Other | 13,090 | 9,770 | |||||

Total Assets | $ | 995,730 | $ | 859,731 | |||

LIABILITIES AND STOCKHOLDERS' EQUITY | |||||||

Accounts payable and accrued liabilities | $ | 52,853 | $ | 55,792 | |||

Deferred revenue | 9,667 | 11,984 | |||||

Income taxes payable | 338 | 4,120 | |||||

Accrued interest (includes accrued interest of consolidated VIEs of $1,603 and $1,266 as of September 30, 2018 and December 31, 2017, respectively) | 7,391 | 25,467 | |||||

Credit services organization guarantee liability | 13,243 | 17,795 | |||||

Deferred rent | 11,288 | 11,577 | |||||

Long-term debt (includes long-term debt and issuance costs of consolidated VIEs of $169,666 and $7,710 as of September 30, 2018 and $124,590 and $4,188 as of December 31, 2017, respectively) | 868,201 | 706,225 | |||||

Subordinated stockholder debt | 2,319 | 2,381 | |||||

Other long-term liabilities | 6,949 | 5,768 | |||||

Deferred tax liabilities | 13,617 | 11,486 | |||||

Total Liabilities | 985,866 | 852,595 | |||||

Commitments and contingencies | |||||||

Stockholders' Equity | |||||||

Preferred stock - $0.001 par value, 25,000,000 shares authorized; no shares were issued at either period end | — | — | |||||

Class A common stock - $0.001 par value; 225,000,000 shares authorized; 45,992,983 and 44,561,419 issued and outstanding as of September 30, 2018 and December 31, 2017, respectively) | 9 | 8 | |||||

Paid-in capital | 64,148 | 46,079 | |||||

(Accumulated deficit) retained earnings | (3,767 | ) | 3,988 | ||||

Accumulated other comprehensive loss | (50,526 | ) | (42,939 | ) | |||

Total Stockholders' Equity | 9,864 | 7,136 | |||||

Total Liabilities and Stockholders' Equity | $ | 995,730 | $ | 859,731 | |||

See accompanying Notes to Condensed Consolidated Financial Statements.

3

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF (LOSS) INCOME

(in thousands, except per share data)

(unaudited)

Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Revenue | $ | 283,004 | $ | 255,119 | $ | 793,745 | $ | 696,643 | |||||||

Provision for losses | 134,523 | 99,341 | 307,540 | 226,523 | |||||||||||

Net revenue | 148,481 | 155,778 | 486,205 | 470,120 | |||||||||||

Cost of providing services | |||||||||||||||

Salaries and benefits | 26,515 | 26,821 | 80,341 | 79,554 | |||||||||||

Occupancy | 13,522 | 13,815 | 40,269 | 41,421 | |||||||||||

Office | 7,742 | 5,715 | 20,799 | 15,519 | |||||||||||

Other costs of providing services | 12,604 | 12,991 | 39,731 | 40,954 | |||||||||||

Advertising | 24,114 | 16,270 | 51,424 | 35,599 | |||||||||||

Total cost of providing services | 84,497 | 75,612 | 232,564 | 213,047 | |||||||||||

Gross margin | 63,984 | 80,166 | 253,641 | 257,073 | |||||||||||

Operating expense | |||||||||||||||

Corporate, district and other | 35,185 | 34,247 | 114,294 | 103,797 | |||||||||||

Interest expense | 23,396 | 18,844 | 66,210 | 60,694 | |||||||||||

Loss on extinguishment of debt | 69,200 | — | 80,883 | 12,458 | |||||||||||

Restructuring costs | — | 7,393 | — | 7,393 | |||||||||||

Total operating expense | 127,781 | 60,484 | 261,387 | 184,342 | |||||||||||

Net (loss) income before income taxes | (63,797 | ) | 19,682 | (7,746 | ) | 72,731 | |||||||||

(Benefit) provision for income taxes | (16,775 | ) | 9,920 | 9 | 29,988 | ||||||||||

Net (loss) income | $ | (47,022 | ) | $ | 9,762 | $ | (7,755 | ) | $ | 42,743 | |||||

Weighted average common shares outstanding: | |||||||||||||||

Basic | 45,853 | 37,908 | 45,674 | 37,908 | |||||||||||

Diluted | 48,352 | 38,914 | 48,061 | 38,959 | |||||||||||

Net income per common share: | |||||||||||||||

Basic earnings per share | $ | (1.03 | ) | $ | 0.26 | $ | (0.17 | ) | $ | 1.13 | |||||

Diluted earnings per share: | $ | (0.97 | ) | $ | 0.25 | $ | (0.16 | ) | $ | 1.10 | |||||

See accompanying Notes to Condensed Consolidated Financial Statements.

4

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

(in thousands)

(unaudited)

Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Net (loss) income | $ | (47,022 | ) | $ | 9,762 | $ | (7,755 | ) | $ | 42,743 | |||||

Other comprehensive income (loss): | |||||||||||||||

Cash flow hedges, net of $0 tax in all periods | (187 | ) | — | (572 | ) | 333 | |||||||||

Foreign currency translation adjustment, net of $0 tax in all periods | 2,648 | 8,397 | (7,015 | ) | 18,148 | ||||||||||

Other comprehensive income (loss) | 2,461 | 8,397 | (7,587 | ) | 18,481 | ||||||||||

Comprehensive (loss) income | $ | (44,561 | ) | $ | 18,159 | $ | (15,342 | ) | $ | 61,224 | |||||

See accompanying Notes to Condensed Consolidated Financial Statements.

5

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(in thousands and unaudited)

Nine Months Ended September 30, | |||||||

2018 | 2017 | ||||||

Cash flows from operating activities | |||||||

Net (loss) income | $ | (7,755 | ) | $ | 42,743 | ||

Adjustments to reconcile net income to net cash (used in) provided by operating activities: | |||||||

Depreciation and amortization | 14,006 | 14,120 | |||||

Provision for loan losses | 307,540 | 226,523 | |||||

Restructuring costs | — | 1,495 | |||||

Amortization of debt issuance costs | 3,411 | 2,637 | |||||

Amortization of bond (premium)/discount | (488 | ) | 809 | ||||

Deferred income tax benefit | 3,005 | (811 | ) | ||||

Loss on disposal of property and equipment | 691 | 403 | |||||

Loss on extinguishment of debt | 80,883 | 12,458 | |||||

Increase in cash surrender value of life insurance | (2,458 | ) | (1,045 | ) | |||

Share-based compensation expense | 6,112 | 311 | |||||

Changes in operating assets and liabilities: | |||||||

Loans receivable | (444,350 | ) | (295,127 | ) | |||

Accounts payable and accrued liabilities | (3,643 | ) | 11,055 | ||||

Income taxes payable | 326 | 11,387 | |||||

Income taxes receivable | (12,908 | ) | 4,590 | ||||

Other liabilities | (16,973 | ) | (2,136 | ) | |||

Net cash (used in) provided by operating activities | (72,601 | ) | 29,412 | ||||

Cash flows from investing activities | |||||||

Purchase of property, equipment and software | (8,200 | ) | (7,917 | ) | |||

Cash paid for Cognical Holdings preferred shares | (958 | ) | (4,975 | ) | |||

Changes in restricted cash | (12,284 | ) | (3,360 | ) | |||

Net cash used in investing activities | (21,442 | ) | (16,252 | ) | |||

Cash flows from financing activities | |||||||

Net proceeds from issuance of common stock | 11,549 | — | |||||

Proceeds from exercise of stock options | 408 | — | |||||

Proceeds from Non-Recourse U.S. SPV facility | 17,000 | 52,130 | |||||

Payments on Non-Recourse U.S. SPV facility | (61,590 | ) | (27,258 | ) | |||

Proceeds from Non-Recourse Canada SPV facility | 89,949 | — | |||||

Proceeds from issuance of 12.00% Senior Secured Notes | — | 461,329 | |||||

Payments on 10.75% Senior Secured Notes | — | (414,882 | ) | ||||

Payments on 12.00% Senior Secured Notes | (605,000 | ) | — | ||||

Proceeds from 8.25% Senior Secured Notes | 690,000 | — | |||||

Payments on 12.00% Senior Cash Pay Notes | — | (125,000 | ) | ||||

Debt issuance costs paid | (17,517 | ) | (14,222 | ) | |||

Proceeds from credit facilities | 65,169 | 33,028 | |||||

Payments on credit facilities | (36,169 | ) | (33,028 | ) | |||

Payments of call premiums from early debt extinguishments | (63,350 | ) | (11,152 | ) | |||

Dividends paid to CURO Group Holdings Corp. | — | (166,583 | ) | ||||

Dividends received from CURO Group Holdings Corp. | — | 166,583 | |||||

Dividends paid to stockholders | — | (36,500 | ) | ||||

Net cash provided by (used in) financing activities | 90,449 | (115,555 | ) | ||||

Effect of exchange rate changes on cash | (5,419 | ) | 4,415 | ||||

Net decrease in cash | (9,013 | ) | (97,980 | ) | |||

Cash at beginning of period | 162,374 | 193,525 | |||||

Cash at end of period | $ | 153,361 | $ | 95,545 | |||

6

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

NOTE 1 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES AND NATURE OF OPERATIONS

Basis of Presentation

The terms “CURO," "we,” “our,” “us,” and the “Company,” refer to CURO Group Holdings Corp. and its directly and indirectly owned subsidiaries as a combined entity, except where otherwise stated. The term "CFTC" refers to CURO Financial Technologies Corp., our wholly-owned subsidiary, and its directly and indirectly owned subsidiaries as a consolidated entity, except where otherwise stated.

We have prepared the accompanying unaudited Condensed Consolidated Financial Statements in accordance with accounting principles generally accepted in the United States of America (“US GAAP”), and with the accounting policies described in our 2017 Annual Report on Form 10-K. Certain information and note disclosures normally included in our annual financial statements prepared in accordance with US GAAP have been condensed or omitted, although we believe that the disclosures are adequate to enable a reasonable understanding of the information presented.

The unaudited Condensed Consolidated Financial Statements and the accompanying notes reflect all adjustments, which are, in the opinion of management, necessary to present fairly our results of operations, financial position and cash flows for the periods presented. The adjustments consist solely of normal recurring adjustments. You should read the Condensed Consolidated Financial Statements in conjunction with the Consolidated Financial Statements and related Notes included in our 2017 Annual Report on Form 10-K. Interim results of operations are not necessarily indicative of results that may be expected for future interim periods or for the year ending December 31, 2018.

We completed our initial public offering ("IPO") in December 2017. Prior to our IPO, we effected a 36-for-1 split of our common stock. We have retroactively adjusted all share and per share data for all periods presented to reflect the stock split as if the stock split had occurred at the beginning of the earliest period presented.

After our IPO, we initially qualified as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 (the "JOBS Act"). As an emerging growth company, we elected to take advantage of specified reduced reporting and other requirements that are otherwise generally required of public companies. In August 2018, we completed the issuance of $690.0 million of 8.25% Senior Secured Notes due 2025 ("2025 Notes"). See Note 5 - Long-Term Debt for further discussion of this issuance. This sale, along with the issuance of $605.0 million of 12.00% Senior Secured Notes due 2022 ("2022 Notes") during 2017 exceeded one of the required thresholds to retain emerging growth company status. Specifically, an emerging growth company loses this status on the date on which it has, during the previous three-year period, issued more than $1 billion in non-convertible debt, provided that none of certain other disqualifying conditions have been triggered. As a result of this change of status, we can no longer take advantage of the specified reduced reporting requirements and need to adopt certain recently issued accounting pronouncements for which we were previously allowed to defer. The impact to our accounting policy adoption practices are further described in Note 1. Additionally, the status change will require us to provide an auditor attestation of internal control over financial reporting under Sarbanes-Oxley Act Section 404(b).

Principles of Consolidation

The Condensed Consolidated Financial Statements include the accounts of CURO and its wholly-owned subsidiaries. We have eliminated intercompany transactions and balances in consolidation.

Use of Estimates

The preparation of Condensed Consolidated Financial Statements in conformity with US GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements. Estimates also affect the reported amounts of revenues and expenses during the periods reported. Some of the significant estimates that we have made in the accompanying Condensed Consolidated Financial Statements include allowances for loan losses, certain assumptions related to goodwill and intangibles, accruals related to self-insurance, Credit Services Organization ("CSO") guarantee liability and estimated tax liabilities. Actual results may differ from those estimates.

Nature of Operations

We are a growth-oriented, technology-enabled, highly-diversified consumer finance company serving a wide range of underbanked consumers in the United States ("U.S."), Canada, and the United Kingdom ("U.K.").

7

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

Recently Adopted Accounting Pronouncements

In May 2017, the Financial Accounting Standards Board ("FASB") issued ASU 2017-09, Compensation - Stock Compensation (Topic 718): Scope of Modification Accounting ("ASU 2017-09"). Under modification accounting, an entity is required to re-value its equity awards each time there is a modification to the terms of the awards. The provisions in ASU 2017-09 provide guidance about which changes to the terms or conditions of a share-based payment award require an entity to account for the effects of a modification, unless certain conditions are met. The amendments in this update were effective for all entities for annual periods, and interim periods therein, beginning after December 15, 2017. ASU 2017-09 was effective for all entities for annual periods, and interim periods therein, as of January 1, 2018. The adoption of this amendment did not have a material impact on our Consolidated Financial Statements.

In January 2017, FASB issued ASU 2017-01, Business Combinations (Topic 805): Clarifying the Definition of a Business ("ASU 2017-01"). ASU 2017-01 narrows the definition of a business and provides a framework that gives an entity a basis for making reasonable judgments about whether a transaction involves an asset or a business and provides a screen to determine when a set (an integrated set of assets and activities) is not a business. The screen requires a determination that when substantially all of the fair value of the gross assets acquired is concentrated in a single identifiable asset or a group of similar identifiable assets, the set is not a business. If the screen is not met, ASU 2017-01 (i) requires that to be considered a business, a set must include, at a minimum, an input and a substantive process that together significantly contribute to the ability to create output and (ii) removes the evaluation of whether a market participant could replace missing elements. The amendments provide a framework to assist entities in evaluating whether both an input and a substantive process are present. ASU 2017-01 is effective prospectively for public companies for annual periods beginning after December 15, 2017, including interim periods therein. With our loss of emerging growth company status, we adopted this guidance during the current quarter. The adoption of ASU 2017-01 did not have a material impact on our Consolidated Financial Statements.

In November 2016, FASB issued ASU 2016-18, Statement of Cash Flows (Topic 230): Restricted Cash ("ASU 2016-18"). ASU 2016-18 requires that a statement of cash flows explain the change during the period in the total of cash, cash equivalents and amounts generally described as restricted cash or restricted cash equivalents. As a result, amounts generally described as restricted cash and restricted cash equivalents should be included with cash and cash equivalents when reconciling the beginning-of-period and end-of-period total amounts shown on the statement of cash flows. The adoption should be applied using a retrospective transition method to each period presented. ASU 2016-18 is effective for public companies for fiscal years beginning after December 15, 2017 and interim periods therein. With our loss of emerging growth company status, we adopted this guidance during the current quarter. The adoption of ASU 2016-18 did not have a material impact on the presentation of our statement of cash flows in our Consolidated Financial Statements.

In August 2016, FASB issued ASU 2016-15, Statement of Cash Flows (Topic 230): Classification of Certain Cash Receipts and Cash Payments (a consensus of the Emerging Issues Task Force) (“ASU 2016-15”). The amendments in ASU 2016-15 provide guidance on eight specific cash flow issues, including debt prepayment or debt extinguishment costs, contingent consideration payments made after a business combination, distributions received from equity method investees and beneficial interests in securitization transactions. ASU 2016-15 was effective for public companies for fiscal years beginning after December 15, 2017 and interim periods therein. With our loss of emerging growth company status, we adopted this guidance during the current quarter. The adoption of ASU 2016-15 did not have a material impact on our Consolidated Statement of Cash Flows as we have historically presented debt prepayment and extinguishment costs as outflows from financing activities and we had no other material cash flows impacted by the guidance.

In January 2016, FASB issued ASU No. 2016-01, Financial Instruments-Overall (Subtopic 825-10): Recognition and Measurement of Financial Assets and Financial Liabilities (“ASU 2016-01”) which requires (i) equity investments (except those accounted for under the equity method of accounting, or those that result in consolidation of the investee) to be measured at fair value with changes in fair value recognized in net income, (ii) public entities to use the exit price notion when measuring the fair value of financial instruments for disclosure purposes and (iii) separate presentation of financial assets and financial liabilities by measurement category and form of financial asset (i.e., securities or loans and receivables). ASU 2016-01 eliminates the requirement to disclose the method(s) and significant assumptions used to estimate the fair value that is required to be disclosed for financial instruments measured at amortized cost. ASU 2016-01 is currently effective for public companies. With our loss of emerging growth company status during 2018, we adopted this guidance during the current quarter. The adoption of ASU 2016-01 did not have a material impact on our Consolidated Financial Statements.

In November 2015, FASB issued ASU No. 2015-17, Income Taxes (Topic 740): Balance Sheet Classification of Deferred Taxes (“ASU 2015-17”). ASU 2015-07 eliminates the requirement for organizations to present deferred tax liabilities and assets as current and noncurrent in a classified balance sheet. Instead, organizations will be required to classify all deferred tax assets and liabilities as noncurrent. ASU 2015-17 is currently effective for public companies. With our loss of emerging growth company

8

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

status during 2018, we adopted this guidance during the current quarter. The adoption of ASU 2015-17 did not have a material impact on our Consolidated Financial Statements.

In May 2014, FASB issued ASU No. 2014-09, Revenue from Contracts with Customers (Topic 606) (“ASU 2014-09”), which amended the existing accounting standards for revenue recognition. ASU 2014-09 establishes principles for recognizing revenue upon the transfer of promised goods or services to customers in an amount that reflects the expected consideration received in exchange for those goods or services. In addition to ASU 2014-09, the FASB issued the following ASUs updating the topic:

• | In December 2016, ASU No. 2016-20, Technical Corrections and Improvements to Topic 606, Revenue from Contracts with Customers |

• | In May 2016, ASU No. 2016-12 , Revenue from Contracts with Customers (Topic 606): Narrow-Scope Improvements and Practical Expedients |

• | In April 2016, ASU No. 2016-10, Revenue from Contracts with Customers (Topic 606): Identifying Performance Obligations and Licensing |

• | In March 2016, ASU No. 2016-08, Revenue from Contracts with Customers (Topic 606): Principal versus Agent Considerations (Reporting Revenue Gross versus Net). |

• | In August 2015, ASU No. 2015-14, Revenue from Contracts with Customers (Topic 606): Deferral of the Effective Date |

We adopted the provisions of Topic 606 during the quarter, which supersedes the revenue recognition requirements in ASC 605, Revenue Recognition (Topic 605). Topic 606 requires entities to recognize revenue when control of the promised goods or services is transferred to customers at an amount that reflects the consideration to which the entity expects to be entitled to in exchange for those goods or services. Most of our revenue is generated from interest or through servicing of financial contracts, both of which are excluded from the scope of ASU 2014-09. As a result, the standard did not have a material impact on our Condensed Financial Statements and we have made no adjustments to retained earnings or prior comparative periods.

Recently Issued Accounting Pronouncements Not Yet Adopted

In August 2018, FASB issued ASU No. 2018-13, Disclosure Framework - Changes to the Disclosure Requirements for Fair Value Measurement (“ASU 2018-13”), which amends ASC 820, Fair Value Measurement. ASU 2018-13 modifies the disclosure requirements for fair value measurements by removing, modifying, or adding certain disclosures. The provisions of ASU 2018-13 are effective for all entities for fiscal years beginning after December 15, 2019, and interim periods therein. Early adoption is permitted. An entity is permitted to early adopt any removed or modified disclosures upon issuance of ASU 2018-13 and delay adoption of the additional disclosures until their effective date. The removed and modified disclosures will be adopted on a retrospective basis and the new disclosures will be adopted on a prospective basis. We are currently assessing the impact adoption of ASU 2018-13 will have on our Consolidated Financial Statements.

In February 2018, FASB issued ASU 2018-02, Income Statement - Reporting Comprehensive Income (Topic 220): Reclassification of Certain Tax Effects from Accumulated Other Comprehensive income ("ASU 2018-02"). Current US GAAP requires deferred tax liabilities and assets to be adjusted for the effect of a change in tax laws or rates with the effect included in income from continuing operations in the period the change is enacted, including items of other comprehensive income for which the related tax effects are presented in other comprehensive income (“stranded tax effects”). ASU 2018-02 allows, but does not require, companies to reclassify stranded tax effects caused by the Tax Cuts and Jobs Act of 2017 (the "2017 Tax Act") from accumulated other comprehensive income to retained earnings. Additionally, ASU 2018-02 requires new disclosures by all companies, whether they opt to do the reclassification or not. The provisions of ASU 2018-02 are effective for all entities for fiscal years beginning after December 15, 2018, and interim periods therein. Early adoption is permitted. Companies should apply the proposed amendments either in the period of adoption or retrospectively to each period (or periods) in which the effect of the change in the U.S. federal corporate income tax rate in the 2017 Tax Act is recognized. We are currently assessing the impact adoption of ASU 2018-02 will have on our Consolidated Financial Statements.

In January 2017, FASB issued ASU 2017-04, Intangibles - Goodwill and Other (Topic 350): Simplifying the Test for Goodwill Impairment ("ASU 2017-04"). ASU 2017-04 simplified the goodwill impairment test by eliminating Step 2 of the test which requires an entity to compute the implied fair value of goodwill. Instead, an entity should recognize an impairment charge for the amount by which the carrying amount exceeds the reporting unit's fair value, and is limited to the amount of total goodwill allocated to that reporting unit. Under ASU 2017-04, an entity still has the option to perform the qualitative assessment for a reporting unit to determine if the quantitative impairment test is necessary. The provisions of ASU 2017-04 are effective for a public entity's annual or interim goodwill impairment tests in fiscal years beginning after December 15, 2019. We are currently assessing the impact adoption of ASU 2017-04 will have on our Consolidated Financial Statements.

In June 2016, FASB issued ASU 2016-13, Financial Instruments - Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments” ("ASU 2016-13"). This ASU modifies the impairment model to utilize an expected loss methodology in

9

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

place of the currently used incurred loss methodology, which will result in the more timely recognition of losses. ASU 2016-13 will be effective for public companies for fiscal years beginning after December 15, 2019 and interim periods therein. We anticipate that ASU 2016-13 will impact our current process for measuring credit losses and are currently assessing the impact it will have on our Consolidated Financial Statements.

In February 2016, FASB issued its new lease accounting guidance in ASU No. 2016-02, Leases (Topic 842) (“ASU 2016-02”). ASU 2016-02 requires lessees to recognize the following for all leases (with the exception of short-term leases) at the commencement date: (i) a lease liability, which is a lessee’s obligation to make lease payments, measured on a discounted basis; and (ii) a right-of-use asset, which is an asset that represents the lessee’s right to use, or control the use of, a specified asset for the lease term. Under the new guidance, lessor accounting is largely unchanged and lessees will no longer be provided with a source of off-balance sheet financing. In 2018, FASB released an additional transition method to adopt this new ASU. It allows companies to recognize a cumulative-effect adjustment in the period of adoption and to not restate prior periods. We will elect this transition method and it will be effective for us beginning January 1, 2019, with early adoption permitted. We plan, and are on schedule, to adopt the standard effective January 1, 2019. We expect ASU 2016-02 will have a material impact on our balance sheet with recognition of right-of-use assets and lease liabilities for operating leases. However, we do not expect adoption will have a material impact on our income statement. We do not expect the new standard will have material impacts on our liquidity or on our debt-covenant compliance under our current agreements.

NOTE 2 - VARIABLE INTEREST ENTITIES

At September 30, 2018, we held two credit facilities whereby we sell certain loan receivables to wholly-owned, bankruptcy-remote special purpose subsidiaries, which are considered variable interest entities ("VIEs"). We incur additional debt through the non-recourse facilities (See Note 5 - Long-Term Debt for further discussion) that is collateralized by these underlying loan receivables. We entered into the new Non-Recourse Canada SPV facility in August 2018. We extinguished the Non-Recourse U.S. SPV facility using the using the proceeds from the 8.25% Senior Secured Notes due September 1, 2025 ("8.25% Senior Secured Notes") in October 2018 (See Note 15 - Subsequent Events).

We have determined that we are the primary beneficiary of the VIEs and are required to consolidate them. We include the assets and liabilities related to the VIEs in our Consolidated Financial Statements and we account for them as secured borrowings. We parenthetically disclose on our Consolidated Balance Sheets the VIEs’ assets that can only be used to settle the VIEs' obligations and liabilities if the VIEs’ creditors have no recourse against our general credit.

The carrying amounts of the consolidated VIEs' assets and liabilities associated with our special purpose subsidiaries were as follows (September 30, 2018 includes balances for both the U.S. and Canada VIEs while the December 31, 2017 includes the U.S. VIE):

(in thousands) | September 30, 2018 | December 31, 2017 | |||||

Assets | |||||||

Restricted cash | $ | 19,107 | $ | 6,871 | |||

Loans receivable less allowance for loan losses | 303,433 | 167,706 | |||||

Total Assets | $ | 322,540 | $ | 174,577 | |||

Liabilities | |||||||

Accounts payable and accrued liabilities | $ | 1,360 | $ | 12 | |||

Deferred revenue | 149 | — | |||||

Accrued interest | 1,603 | 1,266 | |||||

Long-term debt | 161,956 | 120,402 | |||||

Total Liabilities | $ | 165,068 | $ | 121,680 | |||

10

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

NOTE 3 – LOANS RECEIVABLE AND REVENUE

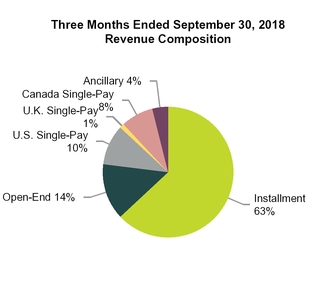

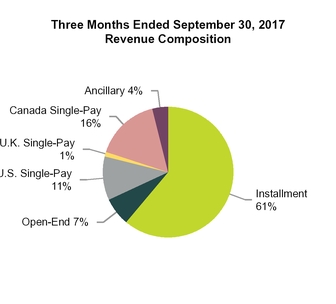

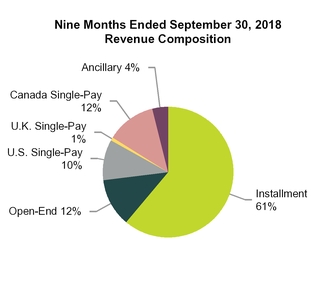

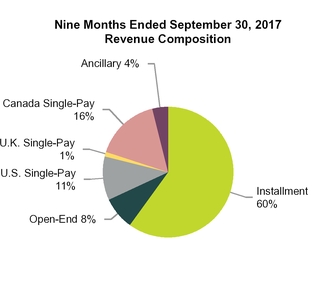

The following table summarizes revenue by product for the periods indicated:

Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

(in thousands) | 2018 | 2017 | 2018 | 2017 | |||||||||||

Unsecured Installment | $ | 148,591 | $ | 128,785 | $ | 405,010 | $ | 343,365 | |||||||

Secured Installment | 28,562 | 26,407 | 81,195 | 73,249 | |||||||||||

Open-End | 40,290 | 18,630 | 94,735 | 52,342 | |||||||||||

Single-Pay | 53,205 | 70,895 | 178,512 | 197,926 | |||||||||||

Ancillary | 12,356 | 10,402 | 34,293 | 29,761 | |||||||||||

Total revenue | $ | 283,004 | $ | 255,119 | $ | 793,745 | $ | 696,643 | |||||||

The following tables summarize Loans receivable by product and the related delinquent loans receivable at September 30, 2018:

September 30, 2018 | ||||||||||||||||

(in thousands) | Single-Pay | Unsecured Installment | Secured Installment | Open-End | Total | |||||||||||

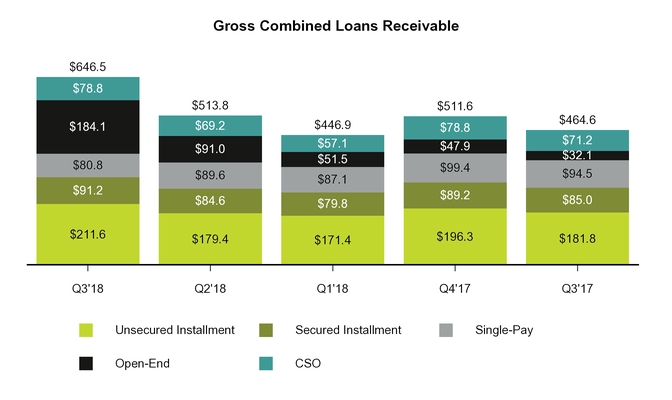

Current loans receivable | $ | 80,867 | $ | 156,947 | $ | 74,017 | $ | 184,067 | $ | 495,898 | ||||||

Delinquent loans receivable | — | 54,618 | 17,159 | — | 71,777 | |||||||||||

Total loans receivable | 80,867 | 211,565 | 91,176 | 184,067 | 567,675 | |||||||||||

Less: allowance for losses | (3,768 | ) | (43,066 | ) | (11,221 | ) | (18,013 | ) | (76,068 | ) | ||||||

Loans receivable, net | $ | 77,099 | $ | 168,499 | $ | 79,955 | $ | 166,054 | $ | 491,607 | ||||||

September 30, 2018 | ||||||||||

(in thousands) | Unsecured Installment | Secured Installment | Total | |||||||

Delinquent loans receivable | ||||||||||

0-30 days past due | $ | 21,374 | $ | 8,117 | $ | 29,491 | ||||

31-60 days past due | 16,542 | 4,395 | 20,937 | |||||||

61-90 days past due | 16,702 | 4,647 | 21,349 | |||||||

Total delinquent loans receivable | $ | 54,618 | $ | 17,159 | $ | 71,777 | ||||

The following tables summarize Loans receivable by product and the related delinquent loans receivable at December 31, 2017:

December 31, 2017 | ||||||||||||||||

(in thousands) | Single-Pay | Unsecured Installment | Secured Installment | Open-End | Total | |||||||||||

Current loans receivable | $ | 99,400 | $ | 151,343 | $ | 73,165 | $ | 47,949 | $ | 371,857 | ||||||

Delinquent loans receivable | — | 44,963 | 16,017 | — | 60,980 | |||||||||||

Total loans receivable | 99,400 | 196,306 | 89,182 | 47,949 | 432,837 | |||||||||||

Less: allowance for losses | (5,916 | ) | (43,754 | ) | (13,472 | ) | (6,426 | ) | (69,568 | ) | ||||||

Loans receivable, net | $ | 93,484 | $ | 152,552 | $ | 75,710 | $ | 41,523 | $ | 363,269 | ||||||

11

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

December 31, 2017 | ||||||||||

(in thousands) | Unsecured Installment | Secured Installment | Total | |||||||

Delinquent loans receivable | ||||||||||

0-30 days past due | $ | 18,358 | $ | 8,116 | $ | 26,474 | ||||

31-60 days past due | 12,836 | 3,628 | 16,464 | |||||||

61-90 days past due | 13,769 | 4,273 | 18,042 | |||||||

Total delinquent loans receivable | $ | 44,963 | $ | 16,017 | $ | 60,980 | ||||

The following tables summarize loans guaranteed by us under our CSO programs and the related delinquent receivables at September 30, 2018:

September 30, 2018 | ||||||||||

(in thousands) | Unsecured Installment | Secured Installment | Total | |||||||

Current loans receivable guaranteed by the Company | $ | 63,688 | $ | 2,425 | $ | 66,113 | ||||

Delinquent loans receivable guaranteed by the Company | 12,119 | 593 | 12,712 | |||||||

Total loans receivable guaranteed by the Company | 75,807 | 3,018 | 78,825 | |||||||

Less: CSO guarantee liability | (12,750 | ) | (493 | ) | (13,243 | ) | ||||

Loans receivable guaranteed by the Company, net | $ | 63,057 | $ | 2,525 | $ | 65,582 | ||||

September 30, 2018 | ||||||||||

(in thousands) | Unsecured Installment | Secured Installment | Total | |||||||

Delinquent loans receivable | ||||||||||

0-30 days past due | $ | 10,419 | $ | 462 | $ | 10,881 | ||||

31-60 days past due | 1,077 | 65 | 1,142 | |||||||

61-90 days past due | 623 | 66 | 689 | |||||||

Total delinquent loans receivable | $ | 12,119 | $ | 593 | $ | 12,712 | ||||

The following tables summarize loans guaranteed by us under our CSO programs and the related delinquent receivables at December 31, 2017:

December 31, 2017 | ||||||||||

(in thousands) | Unsecured Installment | Secured Installment | Total | |||||||

Current loans receivable guaranteed by the Company | $ | 62,676 | $ | 3,098 | $ | 65,774 | ||||

Delinquent loans receivable guaranteed by the Company | 12,480 | 537 | 13,017 | |||||||

Total loans receivable guaranteed by the Company | 75,156 | 3,635 | 78,791 | |||||||

Less: CSO guarantee liability | (17,073 | ) | (722 | ) | (17,795 | ) | ||||

Loans receivable guaranteed by the Company, net | $ | 58,083 | $ | 2,913 | $ | 60,996 | ||||

12

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

December 31, 2017 | ||||||||||

(in thousands) | Unsecured Installment | Secured Installment | Total | |||||||

Delinquent loans receivable | ||||||||||

0-30 days past due | $ | 10,477 | $ | 459 | $ | 10,936 | ||||

31-60 days past due | 1,364 | 41 | 1,405 | |||||||

61-90 days past due | 639 | 37 | 676 | |||||||

Total delinquent loans receivable | $ | 12,480 | $ | 537 | $ | 13,017 | ||||

The following table summarizes activity in the allowance for loan losses during the three months ended September 30, 2018:

Three Months Ended September 30, 2018 | ||||||||||||||||||

(in thousands) | Single-Pay | Unsecured Installment | Secured Installment | Open-End | Other | Total | ||||||||||||

Balance, beginning of period | $ | 4,372 | $ | 35,279 | $ | 10,386 | $ | 9,717 | $ | — | $ | 59,754 | ||||||

Charge-offs | (43,427 | ) | (37,151 | ) | (11,188 | ) | (32,770 | ) | (3,207 | ) | (127,743 | ) | ||||||

Recoveries | 29,500 | 5,748 | 2,325 | 9,191 | 2,646 | 49,410 | ||||||||||||

Net charge-offs | (13,927 | ) | (31,403 | ) | (8,863 | ) | (23,579 | ) | (561 | ) | (78,333 | ) | ||||||

Provision for losses | 13,511 | 39,025 | 9,698 | 31,686 | 561 | 94,481 | ||||||||||||

Effect of foreign currency translation | (188 | ) | 165 | — | 189 | — | 166 | |||||||||||

Balance, end of period | $ | 3,768 | $ | 43,066 | $ | 11,221 | $ | 18,013 | $ | — | $ | 76,068 | ||||||

Allowance for loan losses as a percentage of gross loan receivables | 4.7 | % | 20.4 | % | 12.3 | % | 9.8 | % | N/A | 13.4 | % | |||||||

The following table summarizes activity in the CSO guarantee liability during the three months ended September 30, 2018:

Three Months Ended September 30, 2018 | |||||||||

(in thousands) | Unsecured Installment | Secured Installment | Total | ||||||

Balance, beginning of period | $ | 11,193 | $ | 426 | $ | 11,619 | |||

Charge-offs | (44,896 | ) | (1,087 | ) | (45,983 | ) | |||

Recoveries | 6,901 | 665 | 7,566 | ||||||

Net charge-offs | (37,995 | ) | (422 | ) | (38,417 | ) | |||

Provision for losses | 39,552 | 490 | 40,042 | ||||||

Balance, end of period | $ | 12,750 | $ | 493 | $ | 13,243 | |||

The following table summarizes activity in the allowance for loan losses and the CSO guarantee liability, in total, during the three months ended September 30, 2018:

Three Months Ended September 30, 2018 | ||||||||||||||||||

(in thousands) | Single-Pay | Unsecured Installment | Secured Installment | Open-End | Other | Total | ||||||||||||

Balance, beginning of period | $ | 4,372 | $ | 46,472 | $ | 10,812 | $ | 9,717 | $ | — | $ | 71,373 | ||||||

Charge-offs | (43,427 | ) | (82,047 | ) | (12,275 | ) | (32,770 | ) | (3,207 | ) | (173,726 | ) | ||||||

Recoveries | 29,500 | 12,649 | 2,990 | 9,191 | 2,646 | 56,976 | ||||||||||||

Net charge-offs | (13,927 | ) | (69,398 | ) | (9,285 | ) | (23,579 | ) | (561 | ) | (116,750 | ) | ||||||

Provision for losses | 13,511 | 78,577 | 10,188 | 31,686 | 561 | 134,523 | ||||||||||||

Effect of foreign currency translation | (188 | ) | 165 | (1 | ) | 189 | — | 165 | ||||||||||

Balance, end of period | $ | 3,768 | $ | 55,816 | $ | 11,714 | $ | 18,013 | $ | — | $ | 89,311 | ||||||

13

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

The following table summarizes activity in the allowance for loan losses during the three months ended September 30, 2017:

Three Months Ended September 30, 2017 | ||||||||||||||||||

(in thousands) | Single-Pay | Unsecured Installment | Secured Installment | Open-End | Other | Total | ||||||||||||

Balance, beginning of period | $ | 5,313 | $ | 41,406 | $ | 19,196 | $ | 4,523 | $ | — | $ | 70,438 | ||||||

Charge-offs | (51,709 | ) | (29,058 | ) | (8,985 | ) | (10,437 | ) | (1,446 | ) | (101,635 | ) | ||||||

Recoveries | 31,194 | 3,169 | 1,911 | 4,446 | 921 | 41,641 | ||||||||||||

Net charge-offs | (20,515 | ) | (25,889 | ) | (7,074 | ) | (5,991 | ) | (525 | ) | (59,994 | ) | ||||||

Provision for losses | 20,632 | 31,110 | 1,989 | 6,348 | 525 | 60,604 | ||||||||||||

Effect of foreign currency translation | (88 | ) | 311 | — | — | — | 223 | |||||||||||

Balance, end of period | $ | 5,342 | $ | 46,938 | $ | 14,111 | $ | 4,880 | $ | — | $ | 71,271 | ||||||

Allowance for loan losses as a percentage of gross loan receivables | 5.7 | % | 25.8 | % | 16.6 | % | 15.2 | % | N/A | 18.1 | % | |||||||

The following table summarizes activity in the CSO guarantee liability during the three months ended September 30, 2017:

Three Months Ended September 30, 2017 | ||||||||||||

(in thousands) | Single-Pay | Unsecured Installment | Secured Installment | Total | ||||||||

Balance, beginning of period | $ | — | $ | 14,748 | $ | 834 | $ | 15,582 | ||||

Charge-offs | (235 | ) | (43,124 | ) | (1,487 | ) | (44,846 | ) | ||||

Recoveries | 233 | 6,326 | 858 | 7,417 | ||||||||

Net charge-offs | (2 | ) | (36,798 | ) | (629 | ) | (37,429 | ) | ||||

Provision for losses | 2 | 38,106 | 629 | 38,737 | ||||||||

Balance, end of period | $ | — | $ | 16,056 | $ | 834 | $ | 16,890 | ||||

The following table summarizes activity in the allowance for loan losses and the CSO guarantee liability, in total, during the three months ended September 30, 2017:

Three Months Ended September 30, 2017 | ||||||||||||||||||

(in thousands) | Single-Pay | Unsecured Installment | Secured Installment | Open-End | Other | Total | ||||||||||||

Balance, beginning of period | $ | 5,313 | $ | 56,154 | $ | 20,030 | $ | 4,523 | $ | — | $ | 86,020 | ||||||

Charge-offs | (51,944 | ) | (72,182 | ) | (10,472 | ) | (10,437 | ) | (1,446 | ) | (146,481 | ) | ||||||

Recoveries | 31,427 | 9,495 | 2,769 | 4,446 | 921 | 49,058 | ||||||||||||

Net charge-offs | (20,517 | ) | (62,687 | ) | (7,703 | ) | (5,991 | ) | (525 | ) | (97,423 | ) | ||||||

Provision for losses | 20,634 | 69,216 | 2,618 | 6,348 | 525 | 99,341 | ||||||||||||

Effect of foreign currency translation | (88 | ) | 311 | — | — | — | 223 | |||||||||||

Balance, end of period | $ | 5,342 | $ | 62,994 | $ | 14,945 | $ | 4,880 | $ | — | $ | 88,161 | ||||||

14

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

The following table summarizes activity in the allowance for loan losses during the nine months ended September 30, 2018:

Nine Months Ended September 30, 2018 | ||||||||||||||||||

(in thousands) | Single-Pay | Unsecured Installment | Secured Installment | Open-End | Other | Total | ||||||||||||

Balance, beginning of period | $ | 5,916 | $ | 43,754 | $ | 13,472 | $ | 6,426 | $ | — | $ | 69,568 | ||||||

Charge-offs | (135,951 | ) | (112,630 | ) | (33,755 | ) | (76,926 | ) | (4,475 | ) | (363,737 | ) | ||||||

Recoveries | 94,783 | 18,083 | 7,487 | 30,451 | 2,733 | 153,537 | ||||||||||||

Net charge-offs | (41,168 | ) | (94,547 | ) | (26,268 | ) | (46,475 | ) | (1,742 | ) | (210,200 | ) | ||||||

Provision for losses | 39,340 | 93,936 | 24,017 | 57,962 | 1,742 | 216,997 | ||||||||||||

Effect of foreign currency translation | (320 | ) | (77 | ) | — | 100 | — | (297 | ) | |||||||||

Balance, end of period | $ | 3,768 | $ | 43,066 | $ | 11,221 | $ | 18,013 | $ | — | $ | 76,068 | ||||||

Allowance for loan losses as a percentage of gross loan receivables | 4.7 | % | 20.4 | % | 12.3 | % | 9.8 | % | N/A | 13.4 | % | |||||||

The following table summarizes activity in the CSO guarantee liability during the nine months ended September 30, 2018:

Nine Months Ended September 30, 2018 | |||||||||

(in thousands) | Unsecured Installment | Secured Installment | Total | ||||||

Balance, beginning of period | $ | 17,073 | $ | 722 | $ | 17,795 | |||

Charge-offs | (119,632 | ) | (3,299 | ) | (122,931 | ) | |||

Recoveries | 25,227 | 2,610 | 27,837 | ||||||

Net charge-offs | (94,405 | ) | (689 | ) | (95,094 | ) | |||

Provision for losses | 90,082 | 461 | 90,543 | ||||||

Balance, end of period | $ | 12,750 | $ | 493 | $ | 13,243 | |||

The following table summarizes activity in the allowance for loan losses and the CSO guarantee liability, in total, during the nine months ended September 30, 2018:

Nine Months Ended September 30, 2018 | ||||||||||||||||||

(in thousands) | Single-Pay | Unsecured Installment | Secured Installment | Open-End | Other | Total | ||||||||||||

Balance, beginning of period | $ | 5,916 | $ | 60,827 | $ | 14,194 | $ | 6,426 | $ | — | $ | 87,363 | ||||||

Charge-offs | (135,951 | ) | (232,262 | ) | (37,054 | ) | (76,926 | ) | (4,475 | ) | (486,668 | ) | ||||||

Recoveries | 94,783 | 43,310 | 10,097 | 30,451 | 2,733 | 181,374 | ||||||||||||

Net charge-offs | (41,168 | ) | (188,952 | ) | (26,957 | ) | (46,475 | ) | (1,742 | ) | (305,294 | ) | ||||||

Provision for losses | 39,340 | 184,018 | 24,478 | 57,962 | 1,742 | 307,540 | ||||||||||||

Effect of foreign currency translation | (320 | ) | (77 | ) | (1 | ) | 100 | — | (298 | ) | ||||||||

Balance, end of period | $ | 3,768 | $ | 55,816 | $ | 11,714 | $ | 18,013 | $ | — | $ | 89,311 | ||||||

15

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

The following table summarizes activity in the allowance for loan losses during the nine months ended September 30, 2017:

Nine Months Ended September 30, 2017 | ||||||||||||||||||

(in thousands) | Single-Pay | Unsecured Installment | Secured Installment | Open-End | Other | Total | ||||||||||||

Balance, beginning of period | $ | 5,501 | $ | 17,775 | $ | 10,737 | $ | 5,179 | $ | — | $ | 39,192 | ||||||

Charge-offs | (140,614 | ) | (53,632 | ) | (15,926 | ) | (28,113 | ) | (3,846 | ) | (242,131 | ) | ||||||

Recoveries | 94,535 | 13,803 | 6,726 | 13,903 | 2,450 | 131,417 | ||||||||||||

Net charge-offs | (46,079 | ) | (39,829 | ) | (9,200 | ) | (14,210 | ) | (1,396 | ) | (110,714 | ) | ||||||

Provision for losses | 45,810 | 68,264 | 12,574 | 13,911 | 1,396 | 141,955 | ||||||||||||

Effect of foreign currency translation | 110 | 728 | — | — | — | 838 | ||||||||||||

Balance, end of period | $ | 5,342 | $ | 46,938 | $ | 14,111 | $ | 4,880 | $ | — | $ | 71,271 | ||||||

Allowance for loan losses as a percentage of gross loan receivables | 5.7 | % | 25.8 | % | 16.6 | % | 15.2 | % | N/A | 18.1 | % | |||||||

The following table summarizes activity in the CSO guarantee liability during the nine months ended September 30, 2017:

Nine Months Ended September 30, 2017 | ||||||||||||

(in thousands) | Single-Pay | Unsecured Installment | Secured Installment | Total | ||||||||

Balance, beginning of period | $ | 274 | $ | 15,630 | $ | 1,148 | $ | 17,052 | ||||

Charge-offs | (2,121 | ) | (104,246 | ) | (6,790 | ) | (113,157 | ) | ||||

Recoveries | 1,335 | 23,051 | 4,041 | 28,427 | ||||||||

Net charge-offs | (786 | ) | (81,195 | ) | (2,749 | ) | (84,730 | ) | ||||

Provision for losses | 512 | 81,621 | 2,435 | 84,568 | ||||||||

Balance, end of period | $ | — | $ | 16,056 | $ | 834 | $ | 16,890 | ||||

The following table summarizes activity in the allowance for loan losses and the CSO guarantee liability, in total, during the nine months ended September 30, 2017:

Nine Months Ended September 30, 2017 | ||||||||||||||||||

(in thousands) | Single-Pay | Unsecured Installment | Secured Installment | Open-End | Other | Total | ||||||||||||

Balance, beginning of period | $ | 5,775 | $ | 33,405 | $ | 11,885 | $ | 5,179 | $ | — | $ | 56,244 | ||||||

Charge-offs | (142,735 | ) | (157,878 | ) | (22,716 | ) | (28,113 | ) | (3,846 | ) | (355,288 | ) | ||||||

Recoveries | 95,870 | 36,854 | 10,767 | 13,903 | 2,450 | 159,844 | ||||||||||||

Net charge-offs | (46,865 | ) | (121,024 | ) | (11,949 | ) | (14,210 | ) | (1,396 | ) | (195,444 | ) | ||||||

Provision for losses | 46,322 | 149,885 | 15,009 | 13,911 | 1,396 | 226,523 | ||||||||||||

Effect of foreign currency translation | 110 | 728 | — | — | — | 838 | ||||||||||||

Balance, end of period | $ | 5,342 | $ | 62,994 | $ | 14,945 | $ | 4,880 | $ | — | $ | 88,161 | ||||||

NOTE 4 – CREDIT SERVICES ORGANIZATION

The CSO fee receivable amounts under our CSO programs were $13.7 million and $14.5 million at September 30, 2018 and December 31, 2017, respectively. As noted, we bear the risk of loss through our guarantee to purchase any defaulted customer loans from the lenders. The terms of these loans range from three to 18 months. As of September 30, 2018 and December 31, 2017, the maximum amount payable under all such guarantees was $65.9 million and $65.2 million, respectively. Our guarantee liability was $13.2 million and $17.8 million at September 30, 2018 and December 31, 2017, respectively.

We have placed $17.0 million and $17.9 million in collateral accounts for the lenders at September 30, 2018 and December 31, 2017, respectively, which is reflected in "Prepaid expenses and other" in the Condensed Consolidated Balance Sheets. The balances required to be maintained in these collateral accounts vary based upon lender but are typically based on a percentage

16

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

of the outstanding loan balances held by the lender. The percentage of outstanding loan balances required for collateral is negotiated between us and each such lender.

NOTE 5 – LONG-TERM DEBT

Long-term debt consisted of the following:

(in thousands) | September 30, 2018 | December 31, 2017 | ||||||

8.25% Senior Secured Notes (due 2025) | $ | 677,245 | $ | — | ||||

12.00% Senior Secured Notes (due 2022) | — | 585,823 | ||||||

Non-Recourse U.S. SPV Facility | 76,614 | 120,402 | ||||||

Non-Recourse Canada SPV Facility | 85,342 | — | ||||||

Senior Revolver | 29,000 | — | ||||||

Cash Money Revolving Credit Facility | — | — | ||||||

Long-term debt | $ | 868,201 | $ | 706,225 | ||||

Senior Secured Notes

In February and November 2017, CFTC issued $470.0 million and $135.0 million, respectively, of 12.00% Senior Secured Notes due March 1, 2022 ("12.00% Senior Secured Notes"). The February issuance refinanced similar notes that were nearing maturity, and the extinguishment of the existing notes resulted in a pretax loss of $12.5 million during the nine months ended September 30, 2017. In connection with these 12.00% Senior Secured Notes, we capitalized financing costs of approximately $18.3 million, the balance of which is included in the Condensed Consolidated Balance Sheets as a component of Long-term debt and is being amortized over the term of the 12.00% Senior Secured Notes and included as a component of interest expense.

On February 5, 2018, CFTC issued a notice of redemption for $77.5 million of its 12.00% Senior Secured Notes using a portion of the cash proceeds from our IPO as required by the underlying indenture (the transaction whereby the 12.00% Senior Secured Notes were partially redeemed, the “Redemption”). The Redemption occurred on March 7, 2018 at a price equal to 112.00% of the principal amount of the 12.00% Senior Secured Notes redeemed, plus accrued and unpaid interest paid thereon, to the date of Redemption. The Redemption price and the amortization of a corresponding portion of the capitalized financing costs resulted in a loss on Redemption of $11.7 million. Following the Redemption, $527.5 million of the original outstanding principal amount of the 12.00% Senior Secured Notes remain outstanding. CFTC conducted the Redemption pursuant to the Indenture governing the 12.00% Senior Secured Notes (the “Indenture”), dated as of February 15, 2017, by and among CFTC, the guarantors party thereto and TMI Trust Company, as trustee and collateral agent.

On August 13, 2018, CGHC issued $690.0 million of 8.25% Senior Secured Notes due September 1, 2025 ("8.25% Senior Secured Notes"). The proceeds from issuance of the 8.25% Senior Secured Notes were used to extinguish the February and November 2017 12.00% Senior Secured Notes due March 1, 2022 and resulted in a pretax loss of $69.2 million during the three months ended September 30, 2018. In connection with the 8.25% Senior Secured Notes, we capitalized financing costs of approximately $12.9 million, the balance of which is included in the Condensed Consolidated Balance Sheet as a component of Long-term debt and is being amortized over the term of the 8.25% Senior Secured Notes and included as a component of interest expense.

As of September 30, 2018, CGHC was in full compliance with the covenants and other provisions of the 8.25% Senior Secured Notes.

Non-Recourse U.S. SPV Facility

In November 2016, CURO Receivables Finance I, LLC, a Delaware limited liability company (the “SPV Borrower”) and our wholly-owned subsidiary, entered into a five-year revolving credit facility that provides an $80.0 million term loan and $70.0 million revolving borrowing capacity that can expand over time (“Non-Recourse U.S. SPV Facility”). The loans bear interest at an annual rate of up to 12.00% plus the greater of (i) 1.0% per annum and (ii) the three-month LIBOR. The SPV Borrower also pays a 0.50% per annum commitment fee on the unused portion of the commitments. During the quarter, we paid $3.9 million of interest. As of September 30, 2018, the SPV Borrower was in full compliance with the covenants and other provisions of the Non-Recourse U.S. SPV Facility. During the three months ended September 30, 2018, a portion of the proceeds from the 8.25% Senior Secured Notes were used to extinguish the revolver's balance of $42.4 million. In October 2018, we extinguished the remaining term loan balance of $80.0 million. We made the final termination payment of $2.7 million on October 26, 2018, resulting in a loss on the extinguishment of debt of $9.7 million in October 2018. See Note 15, "Subsequent Events" for additional details on the October extinguishment.

17

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

Non-Recourse Canada SPV Facility

On August 2, 2018, CURO Canada Receivables Limited Partnership, a newly created, bankruptcy-remote special purpose vehicle (the "Canada SPV Borrower") and our wholly-owned subsidiary, entered into a four-year revolving credit facility that provides for C$175.0 million of initial borrowing capacity and the ability to expand such capacity up to C$250.0 million ("Non-Recourse Canada SPV Facility"). The loans bear interest at an annual rate of 6.75% plus the three-month CDOR. The Canada SPV Borrower also pays a 0.50% per annum commitment fee on the unused portion of the commitments. During the quarter, we paid $0.4 million of interest cost. This facility matures in 2022. As of September 30, 2018, the Canada SPV Borrower was in full compliance with the covenants and other provisions of the Non-Recourse Canada SPV Facility.

Senior Revolver

In September 2017, CFTC and CURO Intermediate Holdings Corp., our wholly-owned subsidiary, entered into a $25.0 million Senior Secured Revolving Loan Facility (the “Senior Revolver”). The terms of the Senior Revolver generally conform to the related provisions in the Indenture dated February 15, 2017 for our 12.00% Senior Secured Notes and complements our other financing sources, while providing seasonal short-term liquidity. In February 2018, the Senior Revolver capacity was increased to $29.0 million as permitted by the Indenture to the 12.00% Senior Secured Notes based upon consolidated tangible assets. The Senior Revolver is now syndicated with participation by a second bank.

There is $29.0 million maximum availability under the Senior Revolver, including up to $5.0 million of standby letters of credit, for a one-year term, renewable for successive terms following annual review. As of September 30, 2018, CFTC and CURO Intermediate Holdings Corp. were in full compliance with the covenants and other provisions of the Senior Revolver. The Senior Revolver was fully drawn as of September 30, 2018.

Cash Money Revolving Credit Facility

Cash Money Cheque Cashing, Inc., one of our Canadian subsidiaries, maintains a C$7.3 million revolving credit facility with Royal Bank of Canada (the "Cash Money Revolving Credit Facility"), which provides short-term liquidity required to meet the working capital needs of our Canadian operations. Aggregate draws under this facility are limited to the lesser of: (i) the borrowing base, which is defined as a percentage of cash, deposits in transit and accounts receivable, and (ii) C$7.3 million. As of December 31, 2017, the borrowing capacity under our revolving credit facility was reduced by C$0.3 million in stand-by-letters of credit.

The Cash Money Revolving Credit Facility is collateralized by substantially all of Cash Money’s assets and contains various covenants that include, among other things, that the aggregate borrowings outstanding under the facility not exceed the borrowing base, restrictions on the encumbrance of assets and the creation of indebtedness. Borrowings under the Cash Money Revolving Credit Facility bear interest (per annum) at the prime rate of a Canadian chartered bank plus 1.95%. The Cash Money Revolving Credit Facility was undrawn at September 30, 2018 and December 31, 2017.

In July 2018 the Cash Money Revolving Credit Facility capacity was increased from C$7.3 million to C$10.0 million.

NOTE 6 – SHARE-BASED COMPENSATION

On November 8, 2017, our stockholders approved a new equity plan (“2017 Incentive Plan”). The 2017 Incentive Plan provides for the issuance of up to 5.0 million shares, subject to certain adjustment provisions, for the granting of stock options, restricted stock awards, restricted stock units (“RSUs”), stock appreciation rights, performance awards and other awards that may be settled in or based upon our common stock. Awards may be granted to certain of our officers, employees, consultants and directors. The 2017 Incentive Plan provides that shares of common stock subject to awards granted become available for issuance if such awards expire, terminate, are canceled for any reason or are forfeited by the recipient.

RSUs are typically valued at the date of grant based on the value of our common stock and are expensed using the straight-line method over the service period. Grants of RSUs do not confer full stockholder rights such as voting rights and cash dividends, but provide for additional dividend equivalent RSU awards in lieu of cash dividends. Unvested shares of RSUs may be forfeited upon termination of employment depending on the circumstances of the termination, or failure to achieve the required performance condition, if applicable.

A summary of the status of RSUs as of September 30, 2018 and changes during the nine months ended September 30, 2018 is presented in the following table:

18

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

Units | Weighted Average Grant Date Fair Value | |||||

December 31, 2017 | 1,516,241 | $ | 14.00 | |||

Granted | 90,372 | 17.46 | ||||

Vested | (49,994 | ) | 14.20 | |||

Forfeited | — | — | ||||

September 30, 2018 | 1,556,619 | $ | 14.19 | |||

Share-based compensation expense during the three months ended September 30, 2018 and 2017, which includes compensation costs from stock options and RSUs, was $2.1 million and $0.5 million, respectively, and during the nine months ended September 30, 2018 and 2017 was $6.1 million and $1.8 million, respectively, and is included in the Condensed Consolidated Statements of Income as a component of "Corporate, district and other" expense. The increased expense during the nine months ended September 30, 2018 is primarily due to grants of RSUs in December 2017, as further disclosed in our 2017 Annual Report on Form 10-K.

As of September 30, 2018, there was $16.5 million of unrecognized compensation cost related to share-based awards, which we will recognize over a weighted-average period of 2.2 years.

NOTE 7 – INCOME TAXES

Our effective tax rate was 26.3% and 50.4% during the three months ended September 30, 2018 and 2017, respectively. Our effective tax rate was (0.1)% and 41.2% during the nine months ended September 30, 2018 and 2017, respectively.

On December 22, 2017, the 2017 Tax Act became law, which enacted various changes to the U.S. corporate tax law. Some of the most significant provisions affecting us include a reduced U.S. corporate income tax rate from 35% to 21% effective in 2018, a one-time “deemed repatriation” tax on unremitted earnings accumulated in non-U.S. jurisdictions and reported on the 2017 corporate income tax return, and a 2018 and forward minimum tax on global intangible low-taxed income ("GILTI"). At 2017 year-end, we recorded an estimated provisional deemed repatriation tax of $8.1 million. Subsequently, the IRS issued additional guidance regarding the calculation of the deemed repatriation tax and we recorded an additional accrual of $1.2 million during the period ended March 31, 2018. Through September 30, 2018, we have estimated zero GILTI tax for 2018. Previously, through June, 2018, we had estimated $1.1 million of GILTI tax annually and recorded approximately $0.6 million in the first quarter of 2018. Changes in estimates of foreign sourced income resulted in the reversal of the previously recorded $0.6 million during the three months ended September 30, 2018.

During the three months ended September 30, 2018 we recorded a tax benefit of $3.3 million for the fair market value impact of a 2010 plan that we modified in 2017 creating a taxable event. Additionally, we have not recorded a tax benefit for losses in the U.K. or in certain subsidiaries in Canada.

As of September 30, 2018, we estimated and provided $9.3 million for cumulative undistributed non-U.S. earnings as part of the 2017 repatriation tax provision and the 2018 GILTI tax in the 2017 Tax Act. We intend to reinvest our foreign earnings indefinitely in our non-U.S. operations and therefore have not provided for any non-U.S. withholding tax that would be assessed on dividend distributions. If the earnings of $172.9 million were distributed to the U.S., we would be subject to estimated Canadian withholding taxes of approximately $8.6 million. In the event the earnings were distributed to the U.S., we would adjust our income tax provision for the period and would determine the amount of foreign tax credit that would be available.

NOTE 8 – FINANCIAL INSTRUMENTS

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants. We are required to use valuation techniques that are consistent with the market approach, income approach and/or cost approach. Inputs to valuation techniques refer to the assumptions that market participants would use in pricing the asset or liability based on market data obtained from independent sources, or unobservable, meaning those that reflect our own estimate about the assumptions market participants would use in pricing the asset or liability based on the best information available in the circumstances. Accounting standards establish a three-level fair value hierarchy based upon the assumptions (inputs) used to price assets or liabilities. The hierarchy requires us to maximize the use of observable inputs and minimize the use of unobservable inputs.

The three levels of inputs used to measure fair value are listed below.

19

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

Level 1 – Inputs are quoted prices in active markets for identical assets or liabilities.

Level 2 – Inputs include quoted market prices for similar assets or liabilities in active markets, quoted prices for identical or similar assets or liabilities in markets that are not active, inputs other than quoted prices that are observable for the asset or liability and inputs that are derived principally from or corroborated by observable market data by correlation or other means (market corroborated inputs).

Level 3 – Unobservable inputs reflecting our own judgments about the assumptions market participants would use in pricing the asset or liability since limited market data exists. We develop these inputs based on the best information available, including our own data.

Financial Assets and Liabilities Not Measured at Fair Value

The table below presents the carrying amounts and estimated fair values of assets and liabilities that were not recorded at fair value on the Condensed Consolidated Balance Sheets at September 30, 2018.

Estimated Fair Value | |||||||||||||||

(dollars in thousands) | Carrying Value September 30, 2018 | Level 1 | Level 2 | Level 3 | September 30, 2018 | ||||||||||

Financial assets: | |||||||||||||||

Cash | $ | 153,361 | $ | 153,361 | $ | — | $ | — | $ | 153,361 | |||||

Restricted cash | 24,236 | 24,236 | — | — | 24,236 | ||||||||||

Loans receivable, net | 491,607 | — | — | 491,607 | 491,607 | ||||||||||

Investment in Cognical | 6,600 | — | — | 6,600 | 6,600 | ||||||||||

Financial liabilities: | |||||||||||||||

Credit services organization guarantee liability | $ | 13,243 | $ | — | $ | — | $ | 13,243 | $ | 13,243 | |||||

2018 Senior Secured Notes | 677,245 | — | — | 651,848 | 651,848 | ||||||||||

Non-Recourse U.S. SPV facility | 76,614 | — | — | 80,000 | 80,000 | ||||||||||

Non-Recourse Canada SPV facility | 85,342 | — | — | 89,666 | 89,666 | ||||||||||

The table below presents the carrying amounts and estimated fair values of assets and liabilities that were not recorded at fair value on the Condensed Consolidated Balance Sheets at December 31, 2017.

Estimated Fair Value | |||||||||||||||

(dollars in thousands) | Carrying Value December 31, 2017 | Level 1 | Level 2 | Level 3 | December 31, 2017 | ||||||||||

Financial assets: | |||||||||||||||

Cash | $ | 162,374 | $ | 162,374 | $ | — | $ | — | $ | 162,374 | |||||

Restricted cash | 12,117 | 12,117 | — | — | 12,117 | ||||||||||

Loans receivable, net | 363,269 | — | — | 363,269 | 363,269 | ||||||||||

Investment in Cognical | 5,600 | — | — | 5,600 | 5,600 | ||||||||||

Financial liabilities: | |||||||||||||||

Credit services organization guarantee liability | $ | 17,795 | $ | — | $ | — | $ | 17,795 | $ | 17,795 | |||||

2017 Senior Secured notes | 585,823 | — | — | 663,475 | 663,475 | ||||||||||

Non-Recourse U.S. SPV facility | 120,402 | — | — | 124,590 | 124,590 | ||||||||||

Loans receivable are carried on the Condensed Consolidated Balance Sheets net of the allowance for estimated loan losses, which we calculate primarily based upon models that back-test subsequent collections history for each type of loan product. The unobservable inputs used to calculate the carrying value include additional quantitative factors, such as current default trends and changes to the portfolio mix are also considered in evaluating the accuracy of the models, as well as additional qualitative factors such as the impact of new loan products, changes to underwriting criteria or lending policies, new store development or entrance into new markets, changes in jurisdictional regulations or laws, recent credit trends and general economic conditions. Loans have terms ranging up to 60 months. The carrying value of loans receivable approximates the fair value.

20

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

In connection with our CSO programs, we guarantee consumer loan payment obligations to unrelated third-party lenders for loans that we arrange for consumers on the third-party lenders’ behalf. We are required to purchase from the lender defaulted loans we have guaranteed. The estimated fair value of the guarantee liability related to CSO loans we have guaranteed was $13.2 million and $17.8 million as of September 30, 2018 and December 31, 2017, respectively. We record the initial measurement of this guarantee liability at fair value using Level 3 inputs with subsequent measurement of the liability measured as a contingent loss. The unobservable inputs used to calculate fair value include the nature of the loan products, the creditworthiness of the borrowers in the customer base, our historical loan default history for similar loans, industry loan default history, historical collection rates on similar products, current default trends, past-due account roll rates, changes to underwriting criteria or lending policies, new store development or entrance into new markets, changes in jurisdictional regulations or laws, recent credit trends and general economic conditions.

The fair value of our Senior Secured Notes was based on broker quotations. The fair value of the Non-Recourse U.S. SPV facility was based on the cash needed for final settlement.

Derivative Financial Instrument

We seek to minimize risks from foreign currency rate fluctuations on anticipated transactions in the ordinary course of business through the use of cash flow hedges. During the nine months ended September 30, 2018, we entered into a series of cash flow hedges in which the hedging instruments were forwards to purchase £10.4 million. These contracts will complete in the three months ending December 31, 2018.

We performed an assessment that determined all critical terms of the hedging instrument and the hedged transaction match and, as such, have qualitatively concluded that changes in the hedge instrument’s intrinsic value will completely offset the change in the expected cash flows based on changes in the spot rate. Since the effectiveness of this hedge is assessed based on changes in the hedge instrument’s intrinsic value, the change in the time value of the contract would be excluded from the assessment of hedge effectiveness. We recorded changes in the hedge instrument’s intrinsic value, to the extent that they were effective as a hedge, in "Other comprehensive income." As of September 30, 2018 we have recorded an unrealized loss of $0.6 million in "Other comprehensive income" associated with this hedge.

Foreign Currency Forward Contract

On June 29, 2018, we entered into a forward contract that is not designated to receive hedge accounting treatment. The purpose of this forward contract is to reduce income statement volatility resulting from our foreign currency denominated assets and liabilities in Canada and to protect the cash required to settle those items. The forward contract is recorded at fair value on the balance sheet with changes in the fair value being recorded in the income statement. As of September 30, 2018, the forward contract did not have a fair value and did not impact the Condensed Consolidated Financial Statements.

Purchase of Cognical Holdings Inc. Preferred Shares

During the three months ended March 31, 2018, we purchased 560,872 additional preferred shares of Cognical Holdings, Inc. ("Cognical") for $1.0 million. As a result of this transaction, along with share purchases during 2017, we currently own 10.4% of the equity of Cognical. We record these purchases in "Other assets" on our Consolidated Balance Sheets. No additional interest in Cognical was acquired through September 30, 2018.

NOTE 9 – STOCKHOLDERS' EQUITY

In connection with our IPO in December 2017, the underwriters had a 30-day option to purchase up to an additional 1.0 million shares at the initial public offering price, less the underwriting discount to over-allotments, if any. The underwriters exercised this option and purchased 1.0 million shares on January 5, 2018. The exercise of this option provided additional proceeds to us of $13.1 million.

21

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

NOTE 10 – EARNINGS PER SHARE

The following presents the computation of basic earnings per share (in thousands, except per share amounts):

Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Basic: (1) | |||||||||||||||

Net income | $ | (47,022 | ) | $ | 9,762 | $ | (7,755 | ) | $ | 42,743 | |||||

Weight average common shares | 45,853 | 37,908 | 45,674 | 37,908 | |||||||||||

Basic earnings per share | $ | (1.03 | ) | $ | 0.26 | $ | (0.17 | ) | $ | 1.13 | |||||

(1) We have adjusted the share and per share information to reflect the 36-to-1 split of our common stock, which occurred In November 2017. | |||||||||||||||

The following computation reconciles the differences between the basic and diluted earnings per share presentations (in thousands, except per share amounts):

Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Diluted: (1) | |||||||||||||||

Net income | $ | (47,022 | ) | $ | 9,762 | $ | (7,755 | ) | $ | 42,743 | |||||

Weighted average common shares - basic | 45,853 | 37,908 | 45,674 | 37,908 | |||||||||||

Dilutive effect of stock options and restricted stock units | 2,499 | 1,006 | 2,387 | 1,051 | |||||||||||

Weighted average common shares - diluted | 48,352 | 38,914 | 48,061 | 38,959 | |||||||||||

Diluted earnings per share | $ | (0.97 | ) | $ | 0.25 | $ | (0.16 | ) | $ | 1.10 | |||||

(1) We have adjusted the share and per share information to reflect the 36-to-1 split of our common stock, which occurred in November 2017. | |||||||||||||||