Attached files

| file | filename |

|---|---|

| EX-23.1 - EX-23.1 - CURO Group Holdings Corp. | d579650dex231.htm |

| EX-5.1 - EX-5.1 - CURO Group Holdings Corp. | d579650dex51.htm |

| EX-4.3 - EX-4.3 - CURO Group Holdings Corp. | d579650dex43.htm |

| EX-1.1 - EX-1.1 - CURO Group Holdings Corp. | d579650dex11.htm |

Table of Contents

As filed with the Securities and Exchange Commission on May 14, 2018.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

CURO GROUP HOLDINGS CORP.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

6199 (Primary Standard Industrial Classification Code Number) |

90-0934597 (I.R.S. Employer Identification Number) |

3527 North Ridge Road

Wichita, Kansas 67205

(316) 425-1410

(Address, including Zip Code, and Telephone Number, including Area Code, of registrant’s principal executive offices)

Vin Thomas

Chief Legal Officer

3527 North Ridge Road

Wichita, Kansas 67205

(316) 425-1410

(Name, Address, including Zip Code, and Telephone Number, including Area Code, of Agent for Service)

Copies to:

| Thomas Mark David Cosgrove Willkie Farr & Gallagher LLP 787 Seventh Avenue New York, NY 10019 (212) 728-8000 |

F. Holt Goddard Jonathan Michels White & Case LLP 1221 Avenue of the Americas New York, NY 10020 (212) 819-8200 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date hereof.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ☐ | Accelerated filer ☐ | Non-accelerated filer ☒ (Do not check if a smaller reporting company) |

Smaller reporting company ☐ | Emerging growth company ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period with any new or revised accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

CALCULATION OF REGISTRATION FEE

|

| ||||||||

| Title of Each Class of Securities to Be Registered |

Amount to be Registered(1) |

Proposed Maximum Offering Price Per Share(2) |

Proposed Maximum Aggregate Offering Price(2) |

Amount of Registration Fee | ||||

| Common Stock, $0.001 par value per share |

5,750,000 | $24.17 | $138,977,500 | $17,302.70 | ||||

|

| ||||||||

|

| ||||||||

| (1) | Includes an additional 750,000 shares that the underwriters have the option to purchase. |

| (2) | Estimated solely for the purpose of calculating the amount of the registration fee pursuant to Rule 457(c) under the Securities Act of 1933, as amended. The proposed maximum offering price per share and proposed maximum aggregate offering price are based on the average high and low prices of the Registrant’s common stock on May 9, 2018 as reported on the New York Stock Exchange. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until a registration statement filed with the Securities and Exchange Commission is declared effective. This preliminary prospectus is not an offer to sell these securities, and we are not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED MAY 14, 2018

5,000,000 Shares

CURO Group Holdings Corp.

Common Stock

The selling stockholders identified in this prospectus are offering 5,000,000 shares of our common stock as described in this prospectus. We will not receive any proceeds from the sale of shares offered by the selling stockholders.

Our common stock is traded on the New York Stock Exchange under the symbol “CURO.” The last reported sale price of our common stock on May 11, 2018 was $24.30 per share.

Certain of the selling stockholders have granted the underwriters a 30-day option to purchase up to 750,000 additional shares of our common stock from them at the public offering price, less the underwriting discounts and commissions.

We are an “emerging growth company” as the term is used in the Jumpstart Our Business Startups Act of 2012 and, as such, have elected to comply with certain reduced public company reporting requirements. See “Summary—Implications of Being an Emerging Growth Company.”

Investing in our common stock involves risks. See “Risk Factors” on page 16.

| Price to Public |

Underwriting Discounts and Commissions |

Proceeds to the Selling Expenses)(1) | ||||

| Per Share |

$ | $ | $ | |||

| Total |

$ | $ | $ |

| (1) | See “Underwriting” for information relating to underwriting compensation, including certain expenses of the underwriters to be reimbursed by us. |

Neither the Securities and Exchange Commission, any state securities commission nor any other regulatory body has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares on or about , 2018.

| Credit Suisse | Jefferies | Stephens Inc. | ||

| William Blair | ||||

| Janney Montgomery Scott | ||||

The date of this prospectus is , 2018.

Table of Contents

You should rely only on the information contained in this document or to which we have referred you. Neither we, the selling stockholders nor the underwriters have authorized anyone to provide you with information that is different. This document may only be used where it is legal to sell these securities under applicable law. The information in this document may only be accurate on the date of this document regardless of the time of delivery of this prospectus or of any sale of shares of our common stock by the selling stockholders, and the information in any free writing prospectus that we may provide you in connection with this offering is accurate only as of the date of that free writing prospectus. Our business, financial condition, results of operations and future growth prospects may have changed since those dates. This prospectus is not an offer to sell or the solicitation of an offer to buy shares of our common stock in any circumstances under which such offer or solicitation is unlawful.

i

Table of Contents

This prospectus contains forward-looking statements that are subject to a number of risks and uncertainties, many of which are beyond our control. See “Risk Factors” and “Special Note Regarding Forward-Looking Statements.”

We do not intend our use or display of other companies’ tradenames, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other company. Each trademark, tradename or service mark of any other company appearing in this prospectus is the property of its respective holder.

We or one of our subsidiaries own or have applied for ownership of the marks “CURO,” “CURO Financial Technologies Corp.,” “Speedy Cash®,” “RC Rapid CashSM,” “OPT+SM,” “Rapid Cash,” “Avio Credit,” “LendDirect” and “Wage Day Advance.” All other trademarks, service marks and tradenames appearing in this prospectus are the property of their respective owners.

In this prospectus, when we refer to

| • | “CURO,” we are referring to CURO Group Holdings Corp. and its subsidiaries, including CURO Financial Technologies Corp.; |

| • | “CFTC,” we are referring to CURO Financial Technologies Corp.; |

| • | the “FFL Holders,” we are referring to Friedman Fleischer & Lowe Capital Partners II, L.P., FFL Executive Partners II, L.P. and FFL Parallel Fund II, L.P.; and |

| • | the “Founder Holders,” we are referring to Doug Rippel, Chad Faulkner and Mike McKnight and certain of their family trusts and affiliated entities. |

Unless otherwise specified herein or the context otherwise requires, all references to “$,” “U.S.$,” “USD” or “dollars” in this prospectus refer to U.S. dollars, all references to “C$” refer to Canadian dollars, and all references to “£,” “pound sterling” or “GBP” refer to British pounds sterling. The C$ and GBP are the functional currency of our Canadian and U.K. operations, respectively.

For investors outside the United States: neither we nor any of the underwriters have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. You are required to inform yourselves about and to observe any restrictions relating to this offering and the distribution of this prospectus outside of the United States.

Industry and Market Data

This prospectus and the information incorporated by reference include statistical data, market data and other industry data and forecasts, which we obtained from market research, publicly available information and independent industry publications and reports, including those by the Pew Research Center, CFI Group and FactorTrust. We have supplemented these data and forecasts where necessary with information from publicly available sources and our own internal estimates. We use these sources and estimates and believe them to be reliable, but they involve a number of assumptions and limitations.

The sources of certain industry and market data contained in this prospectus are listed below.

| • | ACORN Canada, It’s Expensive to be Poor: How Canadian Banks are Failing Low Income Communities; May 2016. |

| • | Board of Governors of the Federal Reserve System, Report on the Economic Well-Being of U.S. Households in 2015; May 2016. |

| • | Center for Financial Services Innovation, or CFSI, 2016 Financially Underserved Market Size Study; November 2016. |

ii

Table of Contents

| • | CFI Group, Bank Satisfaction Barometer; 2016. |

| • | FactorTrust, The FactorTrust Underbanked Index; May 2017. |

| • | FICO, US Average FICO Score Hits 700: A Milestone for Consumers; July 2017. |

| • | Financial Credit Authority, High-cost credit; July 2017. |

| • | JPMorgan Chase & Co., Weathering Volatility: Big Data on the Financial Ups and Downs of U.S. Individuals; 2015. |

| • | L.E.K. Consulting, Consumer Specialist Lending—Newly Sustainable or Another Boom-and-Bust; Volume XVIII, Issue 10. |

| • | Pew Research Center, Smartphone Ownership and Internet Usage Continues to Climb in Emerging Economies; February 2016. |

| • | Pricewaterhouse Coopers LLP, or PWC, Banking the Under-Banked: The Growing Demand for Near Prime Credit; 2016. |

The industry in which we operate is subject to a high degree of uncertainty and risk due to a variety of factors, including those described in “Risk Factors” and elsewhere in this prospectus. These and other factors could cause our and the industry’s results to differ materially from those expressed in the estimates made by the independent parties and by us.

iii

Table of Contents

The following summary highlights information contained or incorporated by reference in this prospectus. You should read the following summary together with the more detailed information appearing or incorporated by reference in this prospectus, including our consolidated financial statements and related notes, before deciding whether to purchase shares of our common stock. The terms “we,” “our,” “us,” “CURO” and the “Company,” as used in this prospectus, refer to CURO Group Holdings Corp. and its consolidated subsidiaries, except where otherwise stated or where it is clear that the terms mean only CURO Group Holdings Corp. exclusive of its subsidiaries. Unless the context otherwise indicates or requires, the term “Curo Platform” and “platform,” as used in this prospectus, refer to our Company’s proprietary IT systems and operating platform.

Company Overview

We are a growth-oriented, technology-enabled, highly-diversified consumer finance company serving a wide range of underbanked consumers in the United States, Canada and the United Kingdom and are a market leader in our industry based on revenues. We believe that we have the only true omni-channel customer acquisition, onboarding and servicing platform that is integrated across store, online, mobile and contact center touchpoints. Our IT platform, which we refer to as the “Curo Platform,” seamlessly integrates loan underwriting, scoring, servicing, collections, regulatory compliance and reporting activities into a single, centralized system. We use advanced risk analytics powered by proprietary algorithms and over 15 years of loan performance data to efficiently and effectively score our customers’ loan applications. From 2010 through March 31, 2018, we extended over $15.1 billion in total credit across approximately 39.5 million total loans of which $1.2 billion in total credit was extended across approximately 3 million total loans from September 30, 2017 to March 31, 2018. Additionally, our revenue was $261.7 million and $963.6 million for the three months ended March 31, 2018 and the year ended December 31, 2017, respectively.

We operate in the United States under two principal brands, “Speedy Cash” and “Rapid Cash,” and launched our new brand “Avio Credit” in the United States in the second quarter of 2017. In the United Kingdom we operate online as “Wage Day Advance” and “Juo Loans” and, prior to their closure in the third quarter of 2017, our stores were branded “Speedy Cash.” In Canada, our stores are branded “Cash Money” and we offer “LendDirect” installment loans online and at certain stores. As of March 31, 2018, our store network consisted of 408 locations across 14 U.S. states and seven Canadian provinces and we offered our online services in 27 U.S. states, five Canadian provinces and the United Kingdom.

We offer a broad range of consumer finance products including Unsecured Installment Loans, Secured Installment Loans, Open-End Loans and Single-Pay Loans. We have tailored our products to fit our customers’ particular needs as they access and build credit. Our product suite allows us to serve a broader group of potential borrowers than most of our competitors. The flexibility of our products, particularly our installment and open-end products, allows us to continue serving customers as their credit needs evolve and mature. Our broad product suite creates a diversified revenue stream and our omni-channel platform seamlessly delivers our products across all contact points—we refer to it as “Call, Click or Come In.” We believe these complementary channels drive brand awareness, increase approval rates, lower our customer acquisition costs and improve customer satisfaction levels and customer retention.

We serve the large and growing market of individuals who have limited access to traditional sources of consumer credit and financial services. We define our addressable market as underbanked consumers in the United States, Canada and the United Kingdom. According to a study by CFSI, there are as many as 121 million Americans who are currently underserved by financial services companies. According to studies by ACORN Canada and PWC, the statistics in Canada and the United Kingdom are similar, with an estimated 15% of Canadian residents (approximately 5 million individuals) and an estimated 20% to 25% of United Kingdom residents (approximately 10 to 14 million individuals) classified as underbanked. Given our international

1

Table of Contents

footprint, this translates into an addressable target market of approximately 140 million individuals. We believe that with our scalable omni-channel platform and diverse product offerings, we are well positioned to gain market share as sub-scale players struggle to keep pace with the technological evolution taking place in the industry.

Our customers require essential financial services and value timely, transparent, affordable and convenient alternatives to banks, credit card companies and other traditional financial services companies. According to a recent study by FactorTrust, underbanked customers in the United States tend to have the following characteristics:

| • | average age of 39 for applicants and 41 for borrowers; |

| • | applicants are 47% male and 53% female; |

| • | 41% are homeowners; |

| • | 45% have a bachelor’s degree or higher; and |

| • | the top five employment segments are Retail, Food Service, Government, Banking/Finance and Business Services. |

In the United States, our customers generally earn between $25,000 and $75,000 annually. In Canada, our customers generally earn between C$25,000 and C$60,000 annually. In the United Kingdom, our customers generally earn between £18,000 and £31,000 annually. Our customers utilize the services provided by our industry for a variety of reasons, including that they often:

| • | have immediate need for cash between paychecks; |

| • | have been rejected for traditional banking services; |

| • | maintain sufficient account balances to make a bank account economically efficient; |

| • | prefer and trust the simplicity, transparency and convenience of our products; |

| • | need access to financial services outside of normal banking hours; and |

| • | reject complicated fee structures in bank products (e.g., credit cards and overdrafts). |

Products and Services

We provide Unsecured Installment Loans, Secured Installment Loans, Open-End Loans, Single-Pay Loans and a number of ancillary financial products including check cashing, proprietary reloadable prepaid debit cards (Opt+), credit protection insurance in the Canadian market, gold buying, retail installment sales and money transfer services. We have designed our products and customer journey to be consumer-friendly, accessible and easy to understand. Our platform and product suite enable us to provide several key benefits that appeal to our customers:

| • | transparent approval process; |

| • | flexible loan structure, providing greater ability to manage monthly payments; |

| • | simple, clearly communicated pricing structure; and |

| • | full account management online and via mobile devices. |

Our centralized underwriting platform and its proprietary algorithms are used for every aspect of underwriting and scoring of our loan products. The customer application, approval, origination and funding processes differ by state, country and channel. Our customers typically have an active phone number, open

2

Table of Contents

checking account, recurring income and a valid government-issued form of identification. For in-store loans, the customer presents required documentation, including a recent pay stub or support for underlying bank account activity for in-person verification. For online loans, application data is verified with third-party data vendors, our proprietary algorithms and/or tech-enabled account verification. Our proprietary, highly scalable scoring system employs a champion/challenger process whereby models compete to produce the most successful customer outcomes and profitable cohorts. Our algorithms use data relevancy and machine learning techniques to identify approximately 60 variables from a universe of approximately 11,600 that are the most predictive in terms of credit outcomes. The algorithms are continuously reviewed and refreshed and are focused on a number of factors related to disposable income, expense trends and cash flows, among other factors, for a given loan applicant. The predictability of our scoring models is driven by the combination of application data, purchased third-party data and our robust internal database of over 76 million records (as of March 31, 2018) associated with loan information. These variables are then combined in a series of algorithms to create a score that allows us to scale lending decisions.

Geography and Channel Mix

For the three months ended March 31, 2018 and the years ended December 31, 2017, 2016 and 2015, approximately 78%, 77%, 73% and 71%, respectively, of our consolidated revenues were generated from services provided within the United States and approximately 18%, 19%, 23% and 23%, respectively, of our consolidated revenues were generated from services provided within Canada. For the three months ended March 31, 2018 and each of the years ended December 31, 2017 and 2016, approximately 61%, 60% and 61% of our long-lived assets were located within the United States, respectively and approximately 38%, 38% and 36% of our long-lived assets were located within Canada. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations” incorporated by reference in this prospectus for additional information on our geographic segments.

Stores: As of March 31, 2018, we had 408 stores in 14 U.S. states and seven provinces in Canada, which included the following:

| • | 213 United States locations: Texas (90), California (36), Nevada (18), Arizona (13), Tennessee (11), Kansas (10), Illinois (8), Alabama (7), Missouri (5), Louisiana (5), Colorado (3), Oregon (3), Washington (2) and Mississippi (2); and |

| • | 195 Canadian locations: Ontario (126), Alberta (27), British Columbia (26), Saskatchewan (6), Nova Scotia (5), Manitoba (4) and New Brunswick (1). |

Online: As of March 31, 2018, we lend online in 27 states in the United States, five provinces in Canada and in England, Wales, Scotland and Northern Ireland in the United Kingdom.

3

Table of Contents

Overview of Loan Products

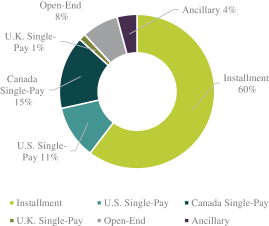

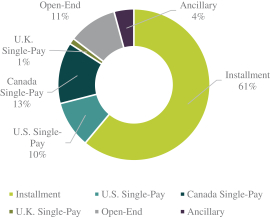

The following charts reflect the revenue contribution, including CSO fees, of the products and services that we currently offer in the regions in which we operate:

| Year Ended December 31, 2017 $963.6 million |

Three Months Ended March 31, 2018 $261.8 million | |

|

| |

For the three months ended March 31, 2018 and the years ended December 31, 2017, 2016 and 2015, the revenue generated through our online channel was 43%, 38%, 33% and 30%, respectively, of consolidated revenue.

For the three months ended March 31, 2018, approximately 51% of loan revenue for our U.S. operations was generated in-store, while the remaining 49% was generated online. For the three months ended March 31, 2018, approximately 93% of our loan revenue for our Canada operations was generated in-store, while the remaining 7% was generated online.

Below is an outline of the primary products we offered as of March 31, 2018.

| Installment Unsecured | Installment Secured | Open-End | Single-Pay | |||||

| Channel |

Online and in-store: 14 U.S. States, Canada and the U.K.(1) |

Online and in-store: 7 U.S. States |

Online: KS, TN, ID, UT, RI, VA, DE and Canada; In-store: KS, TN and Canada |

Online and in-store: 12 U.S. States, Canada and the U.K.(1) | ||||

| Approximate Average Loan Size(2) |

$604 | $1,222 | $702 | $348 | ||||

| Duration |

Up to 60 months | Up to 42 months | Revolving / open-ended | Up to 62 days | ||||

| Pricing |

14.1% average monthly interest rate(3) |

11.3% average monthly interest rate(3) |

Daily interest rates ranging from 0.13% to 0.99% |

Fees ranging from $13 to $25 per $100 borrowed | ||||

| (1) | Online only in the United Kingdom. |

| (2) | Includes CSO loans. |

| (3) | Weighted average of the contractual interest rates for the portfolio as of March 31, 2018. Excludes CSO fees. |

4

Table of Contents

Unsecured Installment Loans

Unsecured Installment Loans are fixed-term, fully-amortizing loans with a fixed payment amount due each period during the term of the loan. Loans are originated and owned by us or third-party lenders pursuant to credit services organization and credit access business statutes, which we refer to as our CSO programs. For CSO programs, we arrange and guarantee the loans. Payments are due bi-weekly or monthly to match the customer’s pay cycle. Customers may prepay without penalty or fees. Unsecured Installment Loan terms are governed by enabling state legislation in the United States, provincial and federal legislation and national regulations in Canada and national regulation in the United Kingdom. Unsecured Installment Loans comprised 50.8%, 49.8%, 39.9% and 38.7% of our consolidated revenue during the three months ended March 31, 2018 and the years ended December 31, 2017, 2016 and 2015, respectively. We believe that the flexible terms and lower payments associated with Installment Loans significantly expand our addressable market by allowing us to serve a broader range of customers with a variety of credit needs.

Secured Installment Loans

Secured Installment Loans are similar to Unsecured Installment Loans but are also secured by a vehicle title. These loans are originated and owned by us or by third-party lenders through our CSO programs. For these loans the customer provides clear title or security interest in the vehicle as collateral. The customer receives the benefit of immediate cash but retains possession of the vehicle while the loan is outstanding. The loan requires periodic payments of principal and interest with a fixed payment amount due each period during the term of the loan. Payments are due bi-weekly or monthly to match the customer’s pay cycle. Customers may prepay without penalty or fees. Secured Installment Loan terms are governed by enabling state legislation in the United States. Secured Installment Loans comprised 10.3%, 10.5%, 9.8% and 10.6% of our consolidated revenue during the three months ended March 31, 2018 and the years ended December 31, 2017, 2016 and 2015, respectively.

Open-End Loans

Open-End Loans are a line of credit for the customer without a specified maturity date. Customers may draw against their line of credit, repay with minimum, partial or full payment and redraw as needed. We report and earn interest on the outstanding loan balances drawn by the customer against their approved credit limit. Customers may prepay without penalty or fees. Typically, customers do not draw the full amount of their credit limit. Loan terms are governed by enabling state legislation in the United States. Unsecured Open-End Loans comprised 9.5%, 6.7%, 7.0% and 5.2% of our consolidated revenue during the three months ended March 31, 2018 and the years ended December 31, 2017, 2016 and 2015, respectively. Secured Open-End Loans are offered as part of our product mix in states with enabling legislation and accounted for approximately 0.9%, 0.9%, 1.0% and 1.2% of our consolidated revenue during the three months ended March 31, 2018 and the years ended December 31, 2017, 2016 and 2015, respectively.

Single-Pay Loans

Single-Pay Loans are generally unsecured short-term, small-denomination loans whereby a customer receives cash in exchange for a post-dated personal check or a pre-authorized debit from the customer’s bank account. We agree to defer deposit of the check or debiting of the customer’s bank account until the loan due date, which typically falls on the customer’s next pay date. Single-Pay Loans are governed by enabling state legislation in the United States, provincial and federal legislation in Canada and national regulation in the United Kingdom. Single-Pay Loans comprised 24.3%, 27.9%, 37.8% and 39.6% of our consolidated revenue during the three months ended March 31, 2018 and the years ended December 31, 2017, 2016 and 2015, respectively. Single Pay Loans originated in the U.S. comprised 10%, 11%, 14% and 14% of our consolidated revenue during the three months ended March 31, 2018 and the years ended December 31, 2017, 2016 and 2015, respectively.

5

Table of Contents

Ancillary Products

We also provide a number of ancillary financial products including check cashing, proprietary reloadable prepaid debit cards (Opt+), credit protection insurance in the Canadian market, gold buying, retail installment sales and money transfer services. We had approximately 115,000 active Opt+ cards as of March 31, 2018, which includes any card with a positive balance or transaction in the past 90 days. Opt+ customers have loaded nearly $1.8 billion to their cards since we started offering this product in 2011.

CSO Programs

Through our CSO programs, we act as a credit services organization/credit access business on behalf of customers in accordance with applicable state laws. We currently offer loans through CSO programs in stores and online in the state of Texas and online in the state of Ohio. In Texas we offer Unsecured Installment Loans and Secured Installment Loans with a maximum term of 180 days. In Ohio we offer an Unsecured Installment Loan product with a maximum term of 18 months. As a CSO we earn revenue by charging the customer a fee, or the CSO fee, for arranging an unrelated third party to make a loan to that customer.

During the three months ended March 31, 2018 and the years ended December 31, 2017 and 2016, approximately 51.8%, 53.6% and 53.2%, respectively, of Unsecured Installment Loans, and 45%, 53.6% and 62.5%, respectively, of Secured Installment Loans originated under CSO programs were paid off prior to the original maturity date.

The majority of revenue generated through our CSO programs was for Unsecured Installment Loans, which comprised 97.2% and 96.4% of total CSO revenue for the three months ended March 31, 2018 and the year ended December 31, 2017, respectively.

Total revenue generated through our CSO programs comprised 26.3% and 26.6% of our consolidated revenue during the three months ended March 31, 2018 and the year ended December 31, 2017, respectively.

Industry Overview

We operate in a segment of the financial services industry that provides lending products to underbanked consumers in need of convenient and flexible access to credit and other financial products. In the United States alone, according to a study by the Center for Financial Services Innovation, or CFSI, these underserved consumers in our target market spent an estimated $126.5 billion on fees and interest related to credit products similar to those we offer.

We believe our target consumers have a need for tailored financing products to cover essential expenses. According to a study by the Federal Reserve, 44% of American adults could not cover an emergency expense costing $400 or would cover it by selling an asset or borrowing money. Additionally, a study conducted by JP Morgan Chase & Co., which analyzed the transaction information of 2.5 million of its account holders, found that 41% of those sampled experienced month-to-month income swings of more than 30%.

We compete against a wide variety of consumer finance providers including online and branch-based consumer lenders, credit card companies, pawn shops, rent-to-own and other financial institutions that offer similar financial services. A study by CFSI has estimated that spending on credit products offered by our industry exhibited a 10.0% CAGR from 2010 to 2015. This growth has been accompanied by shrinking access to credit for our customer base as evidenced by an estimated $142 billion reduction in the availability of non-prime consumer credit from the 2008 to 2009 credit crisis to 2015 (based on analysis of master pool trust data of securitizations for major credit card issuers).

6

Table of Contents

In addition to the beneficial secular trends broadly impacting the consumer finance landscape, we believe we are well positioned to grow our market share as a result of several changes we have observed related to consumer preferences within alternative financial services. Specifically, we believe that a combination of evolving consumer preferences, increasing use of mobile devices and overall adoption rates for technology are driving significant change in our industry.

| • | Shifting preference towards installment loans—We believe from our experience in offering installment loan products since 2008 that single-pay loans are becoming less popular or less suitable for a growing portion of our customers. Customers generally have shown a preference for our Installment Loan products, which typically have longer terms, lower periodic payments and a lower relative cost. Offering more flexible terms and lower payments also significantly expands our addressable market by broadening our products’ appeal to a larger proportion of consumers in the market. |

| • | Increasing adoption of online channels—Our experience is that customers prefer service across multiple channels or touch points. Approximately 63% of respondents in a recent study by CFI Group said they conducted more than half of their banking activities electronically. That same group of respondents reported an overall level of satisfaction that met or exceeded the average. Our full year 2017 and first quarter 2018 online revenue of $367.2 million and $113.5 million represented 38% and 43%, respectively, of our total revenues for such periods. |

| • | Increasing adoption of mobile apps and devices—With the proliferation of pay-as-you-go and other smartphone plans, many of our underbanked customers have moved directly to mobile devices for loan origination and servicing. According to a 2016 study by the Pew Research Center involving the United States, the United Kingdom and Canada, smartphone penetration is 72%, 68% and 67%, respectively. Additionally, 43% of respondents to a study by CFI Group said they conduct transactions using a mobile banking app. Five years ago, less than 30% of our U.S. customers reached us via a mobile device. In the first quarter of 2018, that percentage was over 80%. |

Our Strengths

We believe the following competitive strengths differentiate us and serve as barriers for others seeking to enter our market.

| • | Unique omni-channel platform / site-to-store capability—We believe we have the only fully-integrated store, online, mobile and contact center platform to support omni-channel customer engagement. We offer a seamless “Call, Click or Come In” capability for customers to apply for loans, receive loan proceeds, make loan payments and otherwise manage their accounts in store, online or over the phone. Customers can utilize any of our three channels at any time and in any combination to obtain a loan, make a payment or manage their account. In addition, we have our “Site-to-Store” capability in which online customers that do not qualify for a loan online are referred to a store to complete a loan transaction with one of our associates. Our “Site-to-Store” program resulted in approximately 38,000 loans in the three months ended March 31, 2018. These aspects of our platform enable us to source a larger number of customers, serve a broader range of customers and continue serving these customers for longer periods of time. |

| • | Industry leading product and geographic diversification—In addition to channel diversification, we have increased our diversification by product and geography allowing us to serve a broader range of customers with a flexible product offering. As part of this effort, we have also developed and launched new brands and will continue to develop new brands with differentiated marketing messages. These initiatives have helped diversify our revenue streams, enabling us to appeal to a wider array of borrowers. |

| • | Leading analytics and information technology drives strong credit risk management—We have developed a bespoke, proprietary IT platform, referred to as the Curo Platform, which is a unified, |

7

Table of Contents

| centralized platform that seamlessly integrates activities related to customer acquisition, underwriting, scoring, servicing, collections, compliance and reporting. Our IT platform is underpinned by over 15 years of continually updated customer data comprising over 76 million loan records (as of March 31, 2018) used to formulate our robust, proprietary underwriting algorithms. This platform then automatically applies multi-algorithmic analysis to a customer’s loan application to produce a “Curo Score,” which drives our underwriting decision. Globally, as of March 31, 2018 we have approximately 176 employees who write code and manage our networks and infrastructure for our IT platform. This fully-integrated IT platform enables us to make real-time, data-driven changes to our acquisition and risk models, which yield significant benefits in terms of customer acquisition costs and credit performance. |

| • | Multi-faceted marketing strategy drives low customer acquisition costs—Our marketing strategy includes a combination of strategic direct mail, television advertisements and online and mobile-based digital campaigns, as well as strategic partnerships and other commonly used modes of marketing communications. Our global Marketing, Risk and Credit Analytics team, consisting of approximately 83 professionals as of March 31, 2018, uses our integrated IT platform to cross reference marketing spend, new customer account data and granular credit metrics to optimize our marketing budget across these channels in real time to produce higher quality new loans. Besides these diversified marketing programs, our stores play a critical role in creating brand awareness and driving new customer acquisition. From January 2015 through the end of March 2018, we acquired nearly 2.2 million new customers in North America. |

| • | Focus on customer experience—We focus on customer service and experience and have designed our stores, website and mobile application interfaces to appeal to our customers’ needs. We continue to augment our web and mobile app interfaces to enhance our “Call, Click or Come In” strategy, with a focus on adding functionality across all our channels. Our stores are branded with distinctive and recognizable signage, conveniently located and typically open seven days a week. Furthermore, we have highly experienced managers in our stores, which we believe is a critical component to driving customer retention, lowering acquisition costs and driving store-level margins. For example as of March 31, 2018, the average tenure for our U.S. store managers is almost eight years, for district managers is over 11 years, and for regional directors it is nearly 13 years. |

| • | Strong compliance culture with centralized collections operations—We seek to consistently engage in proactive and constructive dialogue with regulators in each of our jurisdictions and have made significant investments in best-practice automated tools for monitoring, training and compliance management. As of March 31, 2018, our compliance group consisted of 27 individuals based in all of the countries in which we operate and our compliance management systems are integrated into our proprietary IT platform. Additionally, our in-house centralized collections strategy, supported by our proprietary back-end customer database and analytics team, drives an effective, compliant and highly-scalable model. |

| • | Demonstrated access to capital markets and diversified funding sources—We have raised nearly $1.2 billion of debt financing in six separate offerings since 2008, most recently in October 2017. See “Part II, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Recent Developments” in our Annual Report on Form 10-K for the year ended December 31, 2017, as amended, incorporated by reference in this prospectus. We also closed a $150 million nonrecourse installment loan financing facility in 2016 and have routinely accessed banks and other lenders for revolving credit capacity. Additionally, our initial public offering in December of 2017 raised over $80 million of net proceeds. We believe this is a significant differentiator from our peers who may have trouble accessing capital markets to fund their business models if credit markets tighten. For more information, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources” incorporated by reference in this prospectus. |

| • | Experienced and innovative management team and sponsor—Our senior leadership team is among the most experienced in the industry with over a century of collective experience and an average tenure at |

8

Table of Contents

| CURO of approximately seven years. We also have deep bench strength across key functional areas including accounting, compliance, IT and legal. Our equity sponsor, FFL Partners, LLC, or FFL Partners, has been our partner since 2008 and has contributed significant resources to helping define our growth strategy. |

| • | History of growth and profitability—Throughout our operating history we have maintained strong profitability and growth. Between 2010 and 2017, we grew revenue, Adjusted EBITDA, net income and Adjusted Net Income at a CAGR of 24.8%, 25.0%, 13.8% and 19.8%, respectively. At the same time, we have grown our product offerings to better serve our growing and expanding customer base. |

Growth Strategy

| • | Leverage our capabilities to continue growing installment and open-end products—Installment and open-end products accounted for 72% and 68% of our consolidated revenue for the three months ended March 31, 2018 and year ending December 31, 2017, respectively, up from 19% in 2010, and we believe that our customers greatly prefer these products. We anticipate that these products will continue to account for a greater share of our revenue and provide us a competitive advantage versus other consumer lenders with narrower product focus. We believe that our ability to continue to be successful in developing and managing new products is based upon our capabilities in three key areas. |

| • | Underwriting: Installment and open-end products generally have lower yields than single-pay products, which necessitates more stringent credit criteria supported by more sophisticated credit analytics. Our industry-leading analytics platform combines data from over 76 million records (as of March 31, 2018) associated with loan information from third-party reporting agencies. |

| • | Collections and Customer Service: Installment and open-end products have longer terms than single-pay loans, in some cases up to 48 months. These longer terms drive the need for a more comprehensive collection and default servicing strategy that emphasizes curing a default and putting the customer back on a track to repay the loan. We utilize a centralized collection model that prevents our branch management personnel from ever having to contact customers to resolve a delinquency. We have also invested in building new contact centers in all of the countries in which we operate, each of which utilize sophisticated dialer technologies to help us contact our customers in a scalable, efficient manner. |

| • | Funding: The shift to larger balance installment loans with extended terms and open-end loans with revolving terms requires more substantial and more diversified funding sources. Given our deep and successful track record in accessing diverse sources of capital, we believe that we are well-positioned to support future new product transition. |

| • | Serve additional types of borrowers—In addition to growing our existing suite of installment and open-end lending products, we are focused on expanding the total number of customers that we are able to serve through product, geographic and channel expansion. This includes expansion of our online channel, particularly in the United Kingdom, as well as continued targeted additions to our physical store footprint. We also continue to introduce additional products to address our customers’ preference for longer term products that allow for greater flexibility in managing their monthly payments. |

| • | In the second quarter of 2017, we launched Avio Credit, a new online product branded in the United States targeting individuals in the 600-675 FICO band. This product is structured as an Unsecured Installment Loan with varying principal amounts and loan terms up to 48 months. As of April 2017, 10% of U.S. consumers had FICO scores between 600 and 649. A further 13.2% of U.S. consumers had FICO scores between 650 and 699, a portion of whom would fall into the credit profile targeted by our Avio Credit product. |

9

Table of Contents

| • | We expect to expand our LendDirect brand in Canada to include additional provinces and increase acquisition efforts in existing markets. We opened three LendDirect stores in Canada during the fourth quarter of 2017, two during the first quarter of 2018 and plan to open additional locations later in 2018. Seven million Canadians have a FICO score below 700. We estimate that the consumer credit opportunity for this customer segment exceeds C$165 billion. We believe these customers represent a highly-fragmented market with low penetration. |

| • | In the United Kingdom, we launched online longer-term loans in November 2017 with our Juo Loans brand. According to a study by the Financial Conduct Authority, the U.K. guarantor market in 2016 comprised £300 million in loans outstanding and had annual originations of approximately £200 million. A report by L.E.K. Consulting found that this market experienced double digit percentage growth from 2008 to 2017. We believe the U.K. guarantor market is currently dominated by one lender but otherwise largely made up of smaller participants with growth challenges. |

| • | Continue to bolster our core business through enhancement of our proprietary risk scoring models—We continuously refine and update our credit models to drive additional improvements in our performance metrics. By regularly updating our credit underwriting algorithms we can continue to expand the value of each of our customer relationships through improved credit performance. By combining these underwriting improvements with data driven marketing spend, we believe our optimization efforts will produce margin expansion and earnings growth. |

| • | Expand credit for our borrowers—Through extensive testing and our proprietary underwriting, we have successfully increased credit limits for customers, enabling us to offer “the right loan to the right customer.” The favorable take rates and successful credit performance have improved overall vintage and portfolio performance. For the first three months of 2018, our average loan amount for Unsecured and Secured Installment Loans was $604 and $1,222, respectively, compared to $596 and $1,326, respectively, in the same period in 2017. |

| • | Continue to improve the customer journey and experience—We have projects in our development pipeline to enhance our “Call, Click or Come In” customer experience and execution, ranging from redesign of web and app interfaces to enhanced service features to payments optimization. |

| • | Enhance our network of strategic partnerships—Our strategic partnership network generates applicants that we then close through our diverse array of marketing channels. By further leveraging these existing networks and expanding the reach of our partnership platform to include new relationships, we can increase the number of overall leads we receive. On April 30, 2018, we announced a partnership with a bank partner to offer consumers in the U.S. a flexible and innovative line of credit product. |

Corporate and Other Information

The CURO business was founded in 1997 in Riverside, California. We set out to offer a variety of convenient, easily accessible financial and loan services and over our 20 years of operations, expanded across the United States, Canada and the United Kingdom. CURO Financial Technologies Corp., or CFTC (then known as Speedy Cash Holdings Corp.), was incorporated in Delaware on July 16, 2008. On September 10, 2008, our founders sold or otherwise contributed all of the outstanding equity of the various operating entities that comprised the CURO business to a wholly-owned subsidiary of CFTC in connection with an investment in CFTC by Friedman Fleischer & Lowe Capital Partners II, L.P. and its affiliated funds, or FFL Partners. CURO Group Holdings Corp. (then known as Speedy Group Holdings Corp.) was incorporated in Delaware on February 7, 2013 as the parent company of CFTC. On May 11, 2016, we changed the name of Speedy Group Holdings Corp. to CURO Group Holdings Corp. We similarly changed the names of some of its subsidiaries.

Our directors, including the Founder Holders, executive officers and the FFL Holders, collectively own approximately 75% of our common stock as of March 23, 2018. Following the completion of this offering,

10

Table of Contents

our directors, including the Founder Holders, executive officers and the FFL Holders will beneficially own approximately 64% of our outstanding common stock. For additional information on the beneficial ownership of our common stock prior to and immediately after the completion of this offering, see “Selling Stockholders.”

Our principal business office is located at 3527 North Ridge Road, Wichita, Kansas 67205. Our website address is www.curo.com. We do not incorporate the information contained on, or accessible through, our corporate website into this prospectus, and you should not consider it to be part of this prospectus.

Initial Public Offering

We completed our initial public offering of 6,666,667 shares of common stock on December 11, 2017, at a price of $14.00 per share, which provided net proceeds to us of $81.1 million. On December 7, 2017, our stock began trading on the New York Stock Exchange, or the NYSE, under the symbol “CURO.” In connection with the closing, the underwriters had a 30-day option to purchase up to an additional 1,000,000 shares at the initial public offering price, less the underwriting discount, which they exercised on January 5, 2018. The exercise of this option provided additional net proceeds to us of $13.0 million.

On March 7, 2018, we used a portion of the net proceeds from our initial public offering to redeem $77.5 million of our 12.00% Senior Secured Notes due 2022 and to pay related fees, expenses, premiums and accrued interest. For additional information, see Note 25—Subsequent Events to the consolidated audited financials in our Annual Report on Form 10-K for the year ended December 31, 2017, as amended, which is incorporated by reference herein.

In connection with our initial public offering, we, our executive officers and directors and stockholders agreed with the underwriters of that offering not to dispose of or hedge any of the shares of our common stock or securities convertible into or exchangeable for shares of our common stock from December 6, 2017, the date of the prospectus for our initial public offering, continuing through the date that is 180 days after the date of that prospectus. In connection with this offering, Credit Suisse Securities (USA) LLC and Jefferies LLC have agreed to waive this lock-up restriction with respect to the selling stockholders, which include certain of our officers and directors. This waiver relates only to the sale of shares in this offering and becomes effective at the time of pricing of this offering.

Implications of Being an Emerging Growth Company

As a company with less than $1.07 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act.

An emerging growth company may take advantage of specified reduced reporting and other requirements that are otherwise generally applicable to public companies. As an emerging growth company:

| • | we are not required to engage an auditor to report on the effectiveness of our internal control over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act of 2002, or Sarbanes-Oxley Act; |

| • | we are not required to comply with any requirement that may be adopted by the Public Company Accounting Oversight Board, or PCAOB, regarding a supplement to the auditor’s report providing additional information about the audit and the financial statements (i.e., an auditor discussion and analysis); |

| • | we are not required to submit certain executive compensation matters to stockholder advisory votes, such as “say-on-pay,” “say-on-frequency” and “say-on-golden parachutes”; |

11

Table of Contents

| • | we are not required to disclose certain executive compensation-related items, such as the correlation between executive compensation and performance and comparisons of the Chief Executive Officer’s compensation to median employee compensation, or to include a compensation committee report, provided we comply with the scaled compensation disclosure rules applicable to smaller reporting companies; and |

| • | we may take advantage of an extended transition period for complying with new or revised accounting standards, allowing us to delay the adoption of some accounting standards until those standards would otherwise apply to private companies. |

We have elected to take advantage of these reduced reporting and other requirements available to us as an emerging growth company. As a result of these elections, the information that we provide or incorporate by reference in this prospectus may be different from the information you may receive from other public companies. In addition, it is possible that certain investors will find our common stock less attractive as a result of our elections, which may result in a less active trading market for our shares and more volatility in our stock price.

We may take advantage of these provisions until we are no longer an emerging growth company. We could remain an emerging growth company until the last day of the fifth fiscal year following the completion of our initial public offering, which occurred on December 11, 2017, or until the earliest of the following: (i) the last day of the first fiscal year in which our total annual gross revenues are at least $1.07 billion; (ii) the date that we become a “large accelerated filer,” as defined in Rule 12b-2 under the Securities Exchange Act of 1934, as amended, or the Exchange Act, which would occur as of the end of the fiscal year in which, among other things, the market value of our voting and non-voting common equity securities held by non-affiliates is at least $700 million as of the last business day of our most recently completed second fiscal quarter; or (iii) the date on which we have issued more than $1 billion in nonconvertible debt securities during the preceding three-year period.

12

Table of Contents

The Offering

| Common stock offered by the selling stockholders |

5,000,000 shares. |

| Option to purchase additional shares |

The underwriters have a 30-day option to purchase up to an additional 750,000 shares of our common stock from certain of the selling stockholders. |

| Common stock outstanding immediately before and after completion of this offering |

45,561,419 shares. |

| Use of proceeds |

We will not receive any proceeds from the sale of common stock by the selling stockholders named in this prospectus. |

| Dividend policy |

See “Dividend Policy” for a discussion of our policy on paying dividends. |

| NYSE listing symbol |

“CURO.” |

| Risk factors |

Investing in our common stock involves substantial risks. You should carefully read and consider the information set forth under the heading “Risk Factors” and all other information set forth and incorporated by reference in this prospectus before deciding to invest in our common stock. |

The number of shares of our common stock to be outstanding after this offering is based on 45,561,419 shares outstanding as of March 23, 2018 and excludes:

| • | 1,946,256 shares of our common stock issuable upon the exercise of options outstanding as of March 23, 2018 at a weighted average price of $3.02 per share; |

| • | 1,549,098 shares of our common stock underlying restricted stock unit awards granted under the CURO Group Holdings Corp. 2017 Incentive Plan, or the 2017 Incentive Plan, as of March 23, 2018; |

| • | 3,450,902 shares of our common stock reserved for future issuance pursuant to our 2017 Incentive Plan as of March 23, 2018; |

| • | 2,500,000 shares of our common stock reserved for future issuance pursuant to our CURO Group Holdings Corp. Employee Stock Purchase Plan, or the Employee Stock Purchase Plan, as of March 23, 2018; and |

| • | the shares issued upon exercise of stock options by certain of the selling stockholders as further described under “Selling Stockholders” in this prospectus. |

Unless we specifically state otherwise, all information in this prospectus assumes:

| • | no exercise of outstanding stock options since March 23, 2018; |

| • | that the public offering price of our shares of common stock will be $24.30 per share, the last reported sale price of our common stock on the NYSE on May 11, 2018; and |

| • | no exercise by the underwriters of their option to purchase additional shares of common stock from certain of the selling stockholders. |

13

Table of Contents

Summary Consolidated Financial and Other Data

Set forth below is our summary consolidated financial and other data as of and for the periods indicated. We have derived the summary consolidated financial and other data as of and for the years ended December 31, 2017, 2016 and 2015 from our audited consolidated financial statements and the accompanying notes thereto incorporated by reference in this prospectus. We have derived the summary consolidated financial and other data as of and for the three month periods ended March 31, 2018 and 2017 from our unaudited consolidated financial statements incorporated by reference in this prospectus and that, in our opinion, include all adjustments, consisting of normal, recurring adjustments, necessary for the fair presentation of such information. Our historical results for any prior period are not necessarily indicative of results we may expect or achieve in any future period. Our results for any interim period are not necessarily indicative of results we may achieve during a full year.

The following information is only a summary and may not be complete. Accordingly, you should read this summary consolidated financial data in conjunction with the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our audited and unaudited consolidated financial statements and the notes thereto in our Annual Report on Form 10-K for the year ended December 31, 2017, as amended, and our Quarterly Report on Form 10-Q for the quarterly period ended March 31, 2018 incorporated by reference in this prospectus.

| (in thousands, except per share data) |

Three Months Ended March 31, (unaudited) |

Year Ended December 31, |

||||||||||||||||||

| 2018 | 2017 | 2017 | 2016 | 2015 | ||||||||||||||||

| Consolidated Statements of Income Data: |

||||||||||||||||||||

| Revenue |

$ | 261,758 | $ | 224,580 | $ | 963,633 | $ | 828,596 | $ | 813,131 | ||||||||||

| Provision for losses |

81,031 | 61,736 | 326,226 | 258,289 | 281,210 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net revenue |

180,727 | 162,844 | 637,407 | 570,307 | 531,921 | |||||||||||||||

| Cost of providing services |

||||||||||||||||||||

| Salaries and benefits |

26,918 | 26,433 | 105,196 | 104,541 | 107,059 | |||||||||||||||

| Occupancy |

13,427 | 14,095 | 54,612 | 54,509 | 53,288 | |||||||||||||||

| Office |

6,981 | 4,868 | 21,402 | 20,463 | 19,929 | |||||||||||||||

| Other costs of providing services |

14,400 | 14,855 | 54,902 | 53,617 | 47,380 | |||||||||||||||

| Advertising |

9,756 | 7,688 | 52,058 | 43,921 | 65,664 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total cost of providing services |

71,482 | 67,939 | 288,170 | 277,051 | 293,320 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Gross margin |

109,245 | 94,905 | 349,237 | 293,256 | 238,601 | |||||||||||||||

| Operating (income) expense |

||||||||||||||||||||

| Corporate, district and other |

40,454 | 32,993 | 154,973 | 124,274 | 130,534 | |||||||||||||||

| Interest expense |

22,349 | 23,366 | 82,684 | 64,334 | 65,020 | |||||||||||||||

| Loss (gain) on extinguishment of debt |

11,683 | 12,458 | 12,458 | (6,991 | ) | — | ||||||||||||||

| Restructuring |

— | — | 7,393 | 3,618 | 4,291 | |||||||||||||||

| Goodwill and intangible asset impairment charges |

— | — | — | — | 2,882 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total operating expense |

74,486 | 68,817 | 257,508 | 185,235 | 202,727 | |||||||||||||||

| Net income before taxes |

34,759 | 26,088 | 91,729 | 108,021 | 35,874 | |||||||||||||||

| Provision for income tax expense |

11,467 | 9,450 | 42,576 | 42,577 | 18,105 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income |

$ | 23,292 | $ | 16,638 | $ | 49,153 | $ | 65,444 | $ | 17,769 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Basic earnings per share |

$ | 0.51 | $ | 0.44 | $ | 1.28 | $ | 1.73 | $ | 0.47 | ||||||||||

| Diluted earnings per share |

$ | 0.49 | $ | 0.43 | $ | 1.25 | $ | 1.69 | $ | 0.46 | ||||||||||

14

Table of Contents

| (in thousands, except per share data) |

Three Months Ended March 31, (unaudited) |

Year Ended December 31, |

||||||||||||||||||

| 2018 | 2017 | 2017 | 2016 | 2015 | ||||||||||||||||

| Non-GAAP Statement of Operations Data and Other Operating Data (unaudited): |

||||||||||||||||||||

| Adjusted Net Income(1) |

$ | 35,601 | $ | 26,477 | $ | 79,074 | $ | 66,411 | $ | 24,656 | ||||||||||

| EBITDA(2) |

$ | 61,769 | $ | 54,108 | $ | 193,250 | $ | 191,260 | $ | 120,006 | ||||||||||

| Adjusted EBITDA(3) |

$ | 75,215 | $ | 68,632 | $ | 232,215 | $ | 189,361 | $ | 130,876 | ||||||||||

| Adjusted EBITDA Margin(4) |

28.7 | % | 30.6 | % | 24.1 | % | 22.9 | % | 16.1 | % | ||||||||||

| Gross Margin Percentage(5) |

41.7 | % | 42.3 | % | 36.2 | % | 35.4 | % | 29.3 | % | ||||||||||

| Number of stores (at period end) |

408 | 419 | 407 | 420 | 420 | |||||||||||||||

| Selected Balance Sheet Data (at period end): |

||||||||||||||||||||

| Cash |

$ | 130,739 | $ | 145,803 | $ | 162,374 | $ | 193,525 | $ | 100,561 | ||||||||||

| Gross loans receivable |

$ | 389,838 | $ | 304,842 | $ | 432,837 | $ | 286,196 | $ | 252,180 | ||||||||||

| Less: allowance for loan losses |

(60,886 | ) | (71,601 | ) | (69,568 | ) | (39,192 | ) | (32,948 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Loans receivable, net |

$ | 328,952 | $ | 233,241 | $ | 363,269 | $ | 247,004 | $ | 219,232 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total assets |

$ | 785,381 | $ | 715,819 | $ | 859,731 | $ | 780,798 | $ | 666,017 | ||||||||||

| Total liabilities (including debt) |

$ | 742,832 | $ | 655,452 | $ | 852,595 | $ | 739,943 | $ | 685,399 | ||||||||||

| Total stockholders’ equity (deficit) |

$ | 42,549 | $ | 60,367 | $ | 7,136 | $ | 40,855 | $ | (19,382 | ) | |||||||||

| (1) | We define Adjusted Net Income as net income plus or minus certain non-cash or other adjusting items. We provide Adjusted Net Income in this prospectus because our management finds it useful in evaluating the performance and underlying operations of our business. We provide a detailed description of Adjusted Net Income and how we use it, including a reconciliation of Net Income to Adjusted Net Income in “Selected Consolidated Financial Data—Supplemental Non-GAAP Financial Information” in this prospectus. |

| (2) | We define EBITDA as earnings before interest, income taxes, depreciation and amortization. We provide EBITDA in this prospectus because our management finds it useful in evaluating the performance and underlying operations of our business. We provide a detailed description of EBITDA and how we use it, along with a reconciliation of EBITDA to Net income, in “Selected Consolidated Financial Data—Supplemental Non-GAAP Financial Information” in this prospectus. |

| (3) | We define Adjusted EBITDA as earnings before interest, income taxes, depreciation and amortization, plus or minus certain non-cash or other adjusting items. We provide Adjusted EBITDA in this prospectus because our management finds it useful in evaluating the performance and underlying operations of our business. We provide a detailed description of Adjusted EBITDA and how we use it, along with a reconciliation of Adjusted EBITDA to Net Income, in “Selected Consolidated Financial Data—Supplemental Non-GAAP Financial Information” in this prospectus. |

| (4) | Calculated as Adjusted EBITDA as a percentage of revenue. |

| (5) | Calculated as Gross Margin as a percentage of revenue. |

15

Table of Contents

Investing in our common stock involves a high degree of risk. You should carefully consider the following risks and all of the other information contained or incorporated by reference in this prospectus, including our consolidated financial statements and related notes, before investing in our common stock. While we believe that the risks and uncertainties described below are the material risks currently facing us, additional risks that we do not yet know of or that we currently think are immaterial may also arise and materially affect our business. If any of the following risks materialize, our business, financial condition and results of operations could be materially and adversely affected. In that case, the trading price of our common stock could decline, and you may lose some or all of your investment. This prospectus also contains forward-looking statements and estimates that involve risks and uncertainties. Our actual results could differ materially from those anticipated in the forward-looking statements as a result of specific factors, including the risks and uncertainties described below.

Risks Relating to the Regulation of Our Industry

The CFPB promulgated new rules applicable to our loans that could have a material adverse effect on our business and results of operations.

The CFPB adopted a new rule applicable to payday vehicle title and certain high-cost installment loans in November 2017, which we refer to as the CFPB Rule, with most provisions becoming effective 21 months after this CFPB Rule is published in the Federal Register (August 2019).

This CFPB Rule establishes ability-to-repay, or ATR, requirements for “covered short-term loans,” such as our single-payment loans, and for “covered longer-term balloon-payment loans,” such as our revolving lines of credit, as currently structured. It establishes “penalty fee prevention” provisions that will apply to all of our loans, including our covered short-term loans, covered longer-term balloon-payment loans and our installment loans, which are “covered longer-term loans” under the CFPB Rule.

Covered short-term loans are consumer loans with a term of 45 days or less. Covered longer-term balloon payment loans include consumer loans with a term of more than 45 days where (i) the loan is payable in a single payment, (ii) any payment is more than twice any other payment, or (iii) the loan is a multiple advance loan that may not fully amortize by a specified date and the final payment could be more than twice the amount of other minimum payments. Covered longer-term loans are consumer loans with a term of more than 45 days where (i) the total cost of credit exceeds an annual rate of 36%, and (ii) the lender obtains a form of “leveraged payment mechanism” giving the lender a right to initiate transfers from the consumer’s account. Post-dated checks, authorizations to initiate ACH payments and authorizations to initiate prepaid or debit card payments are all leveraged payment mechanisms under the CFPB Rule. While there are certain coverage exceptions (for example, an exception for typical pawn loans), they do not apply to our loans.

The ATR provisions of the CFPB Rule apply to covered short-term loans and covered longer-term balloon-payment loans but not to covered longer-term loans. Under these provisions, to make a covered short-term loan or a covered longer-term balloon-payment loan, a lender has two options.

| • | A “full payment test,” under which the lender must make a reasonable determination of the consumer’s ability to repay the loan in full and cover major financial obligations and living expenses over the term of the loan and the succeeding 30 days. Under this test, the lender must take account of the consumer’s basic living expenses and obtain and generally verify evidence of the consumer’s income and major financial obligations. |

| • | A “principal-payoff option,” under which the lender may make up to three sequential loans, without engaging in an ATR analysis. The first of these so-called Section 1041.6 Loans in any sequence of Section 1041.6 Loans without a 30-day cooling off period between them is limited to $500, the second is limited to two-thirds of the first and the third is limited to one-third of the first. A lender may not use this |

16

Table of Contents

| option if (1) the consumer had in the past 30 days an outstanding covered short-term loan or an outstanding longer-term balloon-payment loan that is not a Section 1041.6 Loan, or (2) the new Section 1041.6 Loan would result in the consumer having more than six covered short-term loans (including Section 1041.6 Loans) during a consecutive 12-month period or being in debt for more than 90 days on such loans during a consecutive 12-month period. For Section 1041.6 Loans, the lender cannot take vehicle security or structure the loan as open-end credit. |

We believe that conducting a comprehensive ATR analysis will be costly and that many of our short-term borrowers will not be able to pass a full payment test. Accordingly, we expect that the full payment test option will have little if any utility for us. The option to make Section 1041.6 Loans using the principal-payoff option may be more viable but the restrictions on these loans under the CFPB Rule will significantly reduce the permitted borrowings by individual consumers. Accordingly, ATR provisions may have an adverse impact on individual customers’ ability to borrow and our business.

The CFPB Rule’s penalty fee prevention provisions, which will apply to all covered loans, may have a greater impact on our operations than the ATR provisions of the CFPB Rule. Under these provisions, if two consecutive attempts to collect money from a particular account of the borrower are unsuccessful due to insufficient funds, the lender cannot make any further attempts to collect from such account unless and until it provides notice of the unsuccessful attempts to the borrower and obtains from the borrower a new and specific authorization for additional payment transfers. Obtaining such authorization will be costly and in many cases not possible.

Additionally, the penalty fee prevention provisions will require the lender generally to give the consumer at least three business days’ advance notice before attempting to collect payment by accessing a consumer’s checking, savings, or prepaid account. These requirements will necessitate revisions to our payment, customer notification, and compliance systems and create delays in initiating automated collection attempts where payments we initiate are initially unsuccessful.

In short, if and when the CFPB Rule goes into effect, the penalty fee prevention provisions will require substantial modifications in our current practices. These modifications would increase costs and reduce revenues. Accordingly, this aspect of the CFPB Rule could have a substantial adverse impact on our results of operations. However, as of the date hereof, these provisions will not become effective before August 2019, and the CFPB Rule remains subject to potential override by disapproval under the Congressional Review Act. Moreover, the current acting or successor director could suspend, delay, modify or withdraw the CFPB Rule. Further, we expect that important elements of the CFPB Rule will be subject to legal attack, including application of the penalty fee provisions to card payments (where issuing banks do not charge penalty fees on declined transactions). Thus, it is impossible to predict whether and when the CFPB Rule (and the penalty fee provisions) will go into effect and, if so, whether and how it (and they) might be modified. While we will make every effort to be in compliance with the new CFPB Rule by August 2019, we make no assurances that we will be fully compliant by the time the rule becomes effective.

In January 2018, the CFPB announced that it intends to engage in a rulemaking process to reconsider the CFPB Rule pursuant to the Administrative Procedure Act (APA). On April 9, 2018, the Community Financial Services Association of America (CFSA) and the Consumer Service Alliance of Texas filed a lawsuit against the CFPB in the U.S. District Court for the Western District of Texas, Austin Division, seeking to invalidate the CFPB Rule. The lawsuit alleges that the rule violates the APA because it exceeds the Bureau’s statutory authority and is arbitrary, capricious, and unsupported by substantial evidence. The lawsuit also argues that the CFPB’s structure is unconstitutional under the Constitution’s separation of powers because the agency’s powers are concentrated in a single, unchecked director who is improperly insulated from both presidential supervision and congressional appropriation, and hence unaccountable to the American people.

17

Table of Contents

Our industry is strictly regulated everywhere we operate, and these regulations could have an adverse effect on our business and results of operations.

We are subject to substantial regulation everywhere we operate. In the United States and Canada, our business is subject to a variety of statutes and regulations enacted by government entities at the federal, state or provincial, and municipal levels. In the United Kingdom, we are subject to statutes and regulations enacted by the U.K. government, as well as directly applicable European Union legislation. These regulations affect our business in many ways, and include regulations relating to:

| • | the amount we may charge in interest rates and fees; |

| • | the terms of our loans (such as maximum and minimum durations), repayment requirements and limitations, number and frequency of loans, maximum loan amounts, renewals and extensions, required repayment plans and reporting and use of state-wide databases; |

| • | underwriting requirements; |

| • | collection and servicing activity, including initiation of payments from consumer accounts; |

| • | the establishment and operation of credit services organizations or credit access businesses, which we refer to as CSOs and CABs in this prospectus; |

| • | licensing, reporting and document retention; |

| • | unfair, deceptive and abusive acts and practices; |

| • | non-discrimination requirements; |

| • | disclosures, notices, advertising and marketing; |

| • | loans to members of the military and their dependents; |

| • | requirements governing electronic payments, transactions, signatures and disclosures; |

| • | check cashing; |

| • | money transmission; |

| • | currency and suspicious activity recording and reporting; |

| • | privacy and use of personally identifiable information and consumer data, including credit reports; |

| • | anti-money laundering and counter-terrorist financing requirements, including currency and suspicious transaction recording and reporting; |

| • | posting of fees and charges; and |