Attached files

| file | filename |

|---|---|

| EX-31.1 - SECTION 302 CEO CERTIFICATION - KEY TRONIC CORP | q42017exhibit311.htm |

| EX-32.2 - SECTION 906 CFO CERTIFICATION - KEY TRONIC CORP | q42017exhibit322.htm |

| EX-32.1 - SECTION 906 CEO CERTIFICATION - KEY TRONIC CORP | q42017exhibit321.htm |

| EX-31.2 - SECTION 302 CFO CERTIFICATION - KEY TRONIC CORP | q42017exhibit312.htm |

| EX-23.1 - CONSENT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM - KEY TRONIC CORP | q42017exhibit231.htm |

| EX-21 - SUBSIDIARIES OF REGISTRANT - KEY TRONIC CORP | q42017exhibit21.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

____________________________________________________________

FORM 10-K

____________________________________________________________

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED JULY 1, 2017

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE PERIOD FROM TO

Commission File Number 0-11559

____________________________________________________________

KEY TRONIC CORPORATION

(Exact name of registrant as specified in its charter)

____________________________________________________________

Washington | 91-0849125 | |

(State or other jurisdiction of Incorporation or organization) | (I.R.S. Employer Identification No.) | |

N. 4424 Sullivan Road, Spokane Valley, Washington | 99216 | |

(Address of principal executive offices) | (Zip Code) | |

(509) 928-8000

(Registrant’s telephone number, including area code)

N/A

(Former name, former address and former fiscal year, if changed since last report)

____________________________________________________________

Securities Registered Pursuant to Section 12(b) of the Act: None

Title of each class | Name of each exchange on which registered | |

Common stock, no par value | The NASDAQ Stock Market LLC | |

Securities Registered Pursuant to Section 12(g) of the Act: None

____________________________________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulations S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

(Check one):

Large accelerated filer | ¨ | Accelerated filer | x | |||

Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Emerging growth company | ¨ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

State the aggregate market value of the voting and non-voting common equity held by non affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter.

As of December 31, 2016, the aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was $79.8 million based on the closing price as reported on the NASDAQ.

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date: 10,759,680 shares of common stock were outstanding as of September 6, 2017.

____________________________________________________________

Documents Incorporated by Reference:

Certain information is incorporated into Part III of this report by reference to the Proxy Statement for the registrant's 2017 annual meeting of stockholders to be filed with the Securities and Exchange Commission pursuant to Regulation 14A not later than 120 days after the end of the fiscal year covered by this Form 10-K.

KEY TRONIC CORPORATION

2017 FORM 10-K

TABLE OF CONTENTS

Page No. | ||

PART I | ||

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

PART II | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | 31-56 | |

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

PART III | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

PART IV | ||

Item 15. | ||

3

FORWARD-LOOKING STATEMENTS

References in this report to “the Company,” “Key Tronic,” “KeyTronicEMS,” “we,” “our,” or “us” mean Key Tronic Corporation together with its subsidiaries, except where the context otherwise requires.

This Annual Report on Form 10-K contains forward-looking statements in addition to historical information. Forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from those reflected in the forward-looking statements. Risks and uncertainties that might cause such differences include, but are not limited to those outlined in “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Risks and Uncertainties that May Affect Future Results.” Readers are cautioned not to place undue reliance on forward-looking statements, which reflect management’s opinions only as of the date hereof. The Company undertakes no obligation to update forward-looking statements to reflect developments or information obtained after the date hereof and disclaims any obligation to do so. Readers should carefully review the risk factors described in periodic reports the Company files from time to time with the Securities and Exchange Commission, including Quarterly Reports on Form 10-Q and Current Reports on Form 8-K.

PART I

Item 1. | BUSINESS |

Background

Key Tronic Corporation (dba: KeyTronicEMS Co.) was organized in 1969, as a Washington corporation that locally manufactured computer keyboards. The ability to design, build and deliver a quality product led us to become a leading independent manufacturer of keyboards for computers in the United States. Our fully integrated design, tooling, and automated manufacturing capabilities enabled us to rapidly respond to customers’ needs for keyboards in production quantities worldwide. We supported our sales growth through the development and purchase of international manufacturing facilities. As the computer keyboard market matured with increasing competition from other international providers, we determined that our business could no longer solely rely on keyboard sales.

After assessing market conditions and our strengths and capabilities, we shifted our focus from keyboard manufacturing to contract manufacturing for a wide range of products. Our unique strategic attributes are based on our core strengths of innovative design and engineering expertise in electronics, mechanical engineering, sheet metal fabrication and stamping, and precision plastics combined with high-quality, low cost production, and assembly on an international basis while providing exceptional customer service. These strengths have made our company a strong competitor in the electronic manufacturing services (EMS) market.

Acquisition

On September 3, 2014, we completed the acquisition of all of the outstanding shares of CDR Manufacturing, Inc. (dba Ayrshire Electronics), which added five locations (four in North America and one in Mexico). This acquisition expanded our printed circuit board assembly capacity, total revenue, and added to and diversified our customer base with the addition of many new multi-national companies. Subsequent to the acquisition, the Reynosa, Mexico operations were transferred to the Company’s existing Juarez, Mexico facilities. During the second quarter of fiscal year 2017, we closed the Harrodsburg, Kentucky facility in order to improve operating efficiencies. The remaining programs from the Kentucky facility have been transferred to other Key Tronic facilities.

Our Industry and Strategy

The expansion of the EMS industry and our acquisitions have allowed us to continue to expand our customer base and the industries that we serve. The increase in new programs represents a growing portion of our revenue and a promising foundation for our future. In keeping with our long-term strategic objectives, we have been successfully building a more diversified customer portfolio, spanning a wider range of industries. We currently offer our customers the following services: integrated electronic and mechanical engineering, precision plastic molding, sheet metal fabrication, printed circuit board (PCB) and complete product assembly, component selection, sourcing and procurement, worldwide logistics, and new product testing and production all at competitive pricing due to our global footprint. We differentiate ourselves from others our size and larger in the EMS industry by providing vertical integration, a flexible and responsive approach to our customer’s changing supply demand, and complete design engineering support.

4

We believe that we are well positioned in the EMS industry to continue the expansion of our customer base and achieve long term growth. Our unique blend of multinational facilities, vertical integration, centralized management, and core strengths continue to support our growth and our customers’ needs. We continue to focus on controlling operating expenses and leveraging the synergistic capabilities of our world-class facilities in the United States, Mexico, and China. This international production capability provides our customers with the benefits of improved supply-chain management, reduced inventory, lower labor costs, lower transportation costs, and reduced product fulfillment time. Given our competitive advantages and the growing pressure for new potential customers to move forward with their outsourcing strategies, we are strongly positioned to win new business in coming periods and grow our revenue and profits.

The EMS industry is intensely competitive. Although our customer base is growing, we still have less than 1% of the potential global market and our revenue can fluctuate significantly due to reliance on a concentrated base of customers. We are planning for new customer growth in the coming quarters by securing new programs with new and existing customers, increasing our worldwide manufacturing capacity, leveraging further our design engineering capabilities and continuing to improve our manufacturing and procurement processes. Ongoing challenges that we face include but are not limited to the following: Continuing to win programs from new and existing customers, balancing capital employed, production capacity and key personnel in support of new customer programs, improving operating efficiencies, controlling costs while developing competitive pricing strategies, and successfully transitioning new program wins to full production.

Customers and Marketing

We provide a mix of manufacturing services for outsourced Original Equipment Manufacturing (OEM) products. We provide the following EMS services: Product design, surface mount technologies (SMT) and pin through hole capability for printed circuit board assembly, tool making, precision plastic molding, sheet metal fabrication, liquid injection molding, complex assembly, automated tape winding, prototype design and full product assembly.

Sales of the majority of our products have not historically been seasonal in nature, but may be seasonal in the future if there are changes in the types of products manufactured. Sales can, however, fluctuate significantly between quarters from changes in customers and customer demand due to the concentration of sales generated by our largest customers.

For the fiscal years 2017, 2016 and 2015, the five largest customers in each year accounted for 42%, 41% and 42% of combined total net sales, respectively. We continue to diversify our customer base by adding additional programs and customers. We expect net sales to our five largest customers as a percentage of total net sales to approximate current levels going forward.

The following table represents all customers that represented 10% or more of total net sales during the last three fiscal years:

Percentage of Net Sales by Fiscal Year | |||||

2017 | 2016 | 2015 | |||

Customer A | 18% | 18% | 17% | ||

There can be no assurance that the Company’s principal customers will continue to purchase products from the Company at current levels. Moreover, the Company typically does not enter into long-term volume purchase contracts with its customers, and the Company’s customers have certain rights to extend or delay the shipment of their orders. The loss of one or more of the Company’s major customers, or the reduction, delay or cancellation of orders from such customers, could materially and adversely affect the Company’s business, operating results and financial condition.

We market our products and services primarily through our direct sales department which is comprised of strategically located field sales people and distributors. We also maintain relationships with several independent sales organizations to assist in marketing our EMS product lines.

Manufacturing

We have continually made investments in developing and expanding a capital equipment base to achieve vertical integration and efficiencies in our manufacturing processes. We have invested significant capital into SMT for volume manufacturing of complex printed circuit board assemblies and in our metal shop providing precision metal stamping, fabricating, and finishing. We also design and develop tooling for injection molding and sheet metal fabrication and manufacture the majority of plastic and sheet metal parts used in the products we manufacture. Additionally, we have equipment to maintain a controlled clean environment for manufacturing processes that require a high level of precise control.

We use a variety of manual and automated assembly processes in our facilities, depending upon product complexity and degree of customization. Some examples of automated processes include component insertion, SMT, selective soldering, flexible robotic assembly, automated storage tape winding, computerized vision system quality inspection, laser turrets, automated switch and key top installation, and automated functional testing.

5

Our engineering expertise and automated manufacturing processes enable us to work closely with our customers during the design and prototype stages of production and to jointly increase productivity and reduce response time to the marketplace. We use computer-aided design techniques and software to assist in preparation of the tool design layout and component placement, to reduce tooling and production costs, improve component and product quality, and enhance turnaround time during product development.

We purchase materials and components for our products from many different suppliers, including both domestic and international sources. We develop close working relationships with our suppliers, many of whom have been supplying products to us for several years.

Research, Development, and Engineering

As part of our long-term strategy, we are committed to supporting our customers by providing research, development, and engineering services. We have recently seen an increase in the success of providing design support on existing and potential customers in differentiating ourselves. These services allow us to facilitate in optimizing new product designs, and the production processes of our customers' programs.

Research, development, and engineering (RD&E) expenses consist principally of employee related costs, third party development costs, program materials costs, depreciation, and allocated information technology and facilities costs.

Competition

The market for the products and services we provide is highly competitive. There are numerous competitors in the EMS industry, many of which have substantially more resources and are more geographically diverse than we are. Some of our competitors have similar international production capabilities, large financial resources and some have substantially greater manufacturing, research and development, and marketing resources. There is also competition from the manufacturing operations of our current and potential customers, who are continually evaluating the merits of manufacturing their products internally versus the advantages of outsourcing. We believe that we can currently compete favorably in these areas primarily on the basis of our international footprint, responsiveness, creativity, vertical production capability, quality, and cost.

Trademarks

Our name and logo are federally registered trademarks, and we believe they are valuable assets of our business. We operate under the trade name “KeyTronicEMS” to better identify our primary business concentration in contract manufacturing in the EMS industry.

Employees

We consider our employees to be our primary strength and we make considerable efforts to maintain a well-qualified workforce. Our employee benefits include bonus programs involving periodic payments to all employees based on meeting quarterly or fiscal year performance targets. We regularly provide transportation, medical services, and meals to all of our employees in foreign locations. The Company also has defined contribution plans available to U.S. employees who have attained age 21 and provide group health, life, and disability insurance plans. We also maintain share based compensation plans and other long term incentive plans for certain employees and outside directors.

As of July 1, 2017 we had 5,038 full-time employees compared to 4,947 on July 2, 2016, and 4,866 on June 27, 2015. Since we can have significant fluctuations in product demand, we seek to maintain flexibility in our workforce by utilizing skilled temporary and short-term contract labor in our manufacturing facilities in addition to full-time employees.

Backlog

On July 29, 2017 our order backlog was valued at approximately $126.9 million, compared to approximately $122.2 million on July 30, 2016. The amount of backlog is not necessarily indicative of future sales but can be indicative of trends in expected future sales revenue. Due to the relationships with our customers, we will occasionally allow orders to be canceled or rescheduled and as a result it is not a meaningful indicator of future financial results. If there are canceled or rescheduled orders, we typically negotiate fees to cover the costs we have incurred. Order backlog consists of purchase orders received for products expected to be shipped approximately within the next twelve months, although shipment dates are subject to change due to design modifications, customer forecast changes, or other customer requirements.

Foreign Markets

Information concerning net sales and long-lived assets (property, plant, and equipment) by geographic areas is set forth in Note 12, “Enterprise-Wide Disclosures” of the consolidated financial statements of this Annual Report on Form 10-K and that information is incorporated herein.

6

Executive Officers of the Registrant

The table below sets forth the name, current age and current position of our executive officers and other significant employees:

Name | Age | Positions Held |

Executive Officers | ||

Craig D. Gates | 58 | President and Chief Executive Officer |

Brett R. Larsen | 44 | Executive Vice President of Administration, Chief Financial Officer, and Treasurer |

Douglas G. Burkhardt | 59 | Executive Vice President of Worldwide Operations |

Philip S. Hochberg | 55 | Executive Vice President of Business Development |

Lawrence J. Bostwick | 65 | Vice President of Regulatory Affairs |

David H. Knaggs | 36 | Vice President of Quality |

Frank Crispigna III | 56 | Vice President of Materials |

Duane D. Mackleit | 49 | Vice President of Program Management |

Chad T. Orebaugh | 46 | Vice President of Engineering |

Executive Officers

CRAIG D. GATES – President and Chief Executive Officer

Mr. Gates, age 58, has been President and Chief Executive officer of the Company since April 2009. Previously, he was Executive Vice President and General Manager from August 2002 to April 2009. He served as Executive Vice President of Marketing, Engineering and Sales from July 1997 to August 2002 and served as Vice President and General Manager of New Business Development from October 1995 to July 1997. He joined the Company as Vice President of Engineering in October of 1994. From 1982 to 1991 he held various engineering and management positions within the Microswitch Division of Honeywell, Inc., in Freeport, Illinois, and from 1991 to October 1994 he served as Director of Operations, Electronics for Microswitch. Mr. Gates has a Bachelor of Science Degree in Mechanical Engineering and a Masters in Business Administration from the University of Illinois, Urbana.

BRETT R. LARSEN – Executive Vice President of Administration, Chief Financial Officer, and Treasurer

Mr. Larsen, age 44, has served as Executive Vice President of Administration, Chief Financial Officer, and Treasurer since July 2015. Previously, he was Vice President of Finance and Controller from February 2010 to July 2015. He was Chief Financial Officer of FLSmidth Spokane, Inc. from December 2008 to February 2010. From October 2005 through November 2008, Mr. Larsen served as Controller of Key Tronic Corporation. From May 2004 to October 2005, Mr. Larsen served as Manager of Financial Reporting of Key Tronic Corporation. From 2002 to May 2004, Mr. Larsen was an audit manager for the public accounting firm BDO USA, LLP. He also held various auditing and supervisory positions with Grant Thornton LLP from 1997 to 2002. Mr. Larsen has a Bachelor of Science degree in Accounting and a Masters degree in Accounting from Brigham Young University and is a Certified Public Accountant.

DOUGLAS G. BURKHARDT – Executive Vice President of Worldwide Operations

Mr. Burkhardt, age 59, has been Executive Vice President of Worldwide Operations of the Company since July 2010. Previously Mr. Burkhardt was Vice President of Worldwide Operations from July 2008 to July 2010 and Director of China Operations and Program Management from January 2006 to July 2008. Mr. Burkhardt also served as Director of Northwest and China Operations from November of 1998 to January of 2006. Mr. Burkhardt also served as Director of Customer Satisfaction from March 1997 to November 1998 and Director of Molding from September of 1995 to March of 1997. Prior to this, Mr. Burkhardt served in other various senior management positions within the Company. Mr. Burkhardt has been with the Company since May of 1989. Prior to joining Key Tronic, Mr. Burkhardt worked for House of Aluminum and Glass for 12 years where he was the plant manager.

PHILIP S. HOCHBERG – Executive Vice President of Business Development

Mr. Hochberg, age 55, has been Executive Vice President of Business Development since July 2012. Prior to this, Mr. Hochberg served as Vice President of Business Development from October 2009 through June 2012. He was Director of Business Development and Program Management from July 2008 to October 2009. Mr. Hochberg served as Director of Business Development from October 2004 to July 2008 and as Director of EMS Sales and Marketing from July 2000 to October 2004. Prior to joining Key Tronic, Mr. Hochberg worked for Quinton Instrument Company as their Director of Marketing and Product Management from 1992 to 2000. From 1988 to 1992, he was employed by SpaceLabs Medical as their Business Development Marketing Manager. Mr. Hochberg has an MBA from the University of British Columbia, a BA in Psychology, with a minor in Business from Washington University in St. Louis.

7

LAWRENCE J. BOSTWICK – Vice President of Regulatory Affairs

Mr. Bostwick, age 65, has been Vice President of Engineering and Quality since July 2008. Previously he was Director of Engineering and Quality from February 2007 to July 2008 and served as Corporate Director of Quality from February 2006 to February 2007. From 2003 to 2006 he was Director of Supply Chain Management and Quality for the Lancer Corporation and from 1998 to 2003 he was Vice President of Operations for Thermacore International. He is a graduate of the Westinghouse and General Electric – Engineering and Manufacturing Professional Development Programs. He is certified in both Quality and Industrial Engineering and is a Lean – Six Sigma Master Black Belt. Mr. Bostwick has a combined B.S. degree in Production and Operation and Industrial Engineering from Bowling Green State University and a Masters degree in Industrial Engineering and Business Administration from Syracuse University.

DAVID H. KNAGGS – Vice President of Quality

Mr. Knaggs, age 36, has been Vice President of Quality of the company since October 2016. Before joining KeyTronicEMS, Mr. Knaggs worked at Telect, Inc. from 2008 to 2016 as their Director of Engineering. Prior to that, he worked at Isothermal Systems Research as Lead Systems Engineer from 2003 to 2008. He has a Bachelor of Science degree in Mechanical Engineering with a minor in mathematics from the University of Washington.

FRANK CRISPIGNA III – Vice President of Materials

Mr. Crispigna, age 56, has been Vice President of Materials of the company since October 2011. Prior to this, Mr. Crispigna held a variety of Materials and Supply Chain positions at Plexus Corporation since 1997, most recently serving as the Director – Supply Chain Solutions from 2005 - 2011. He has a Masters degree in Business Administration, and a Bachelor of Business Administration Degree in Marketing from the University of Wisconsin – Oshkosh. Mr. Crispigna also is a C.P.M., and received his certification in Supply Chain Leadership from the University of Wisconsin.

DUANE D. MACKLEIT – Vice President of Program Management

Mr. Mackleit, age 49, has been Vice President of Program Management of the company since July 2012. He served as Director of Program Management from July 2008 through June 2012. From May 2006 to July 2008 he served as Principal Program Manager. Prior to that, he served as Program Manager from March 2002 to May 2006 and Associate Program Manager from August 2000 to March 2002. Mr. Mackleit has also held several other positions with Key Tronic Corporation. Mr. Mackleit has an AA in Business from Spokane Falls Community College and a BA in Business/Marketing from Eastern Washington University. He also holds a MBA from Gonzaga University.

CHAD T. OREBAUGH – Vice President of Engineering

Mr. Orebaugh, age 46, has been Vice President of Engineering since April 2017. Prior to this, Mr. Orebaugh served as Director of Engineering since May 2013. From April 2010 to May 2013, he served as Manager of Engineering. From January 2000 to April 2010 he served as Lead Mechanical Engineer. Prior to that, he served as Mechanical Engineer from October 1998 to January 2000 and Associate Mechanical Engineer since October 1997. Mr. Orebaugh holds a BA in Mechanical Engineering from Gonzaga University.

Available Information

Our principal executive offices are located at 4424 North Sullivan Road, Spokane Valley, Washington 99216, and our telephone number is (509) 928-8000. Our website is located at http://www.keytronic.com where filings of our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q or current reports on Form 8-K are available after they have been filed with the Securities and Exchange Commission. The information presented on our website currently and in the future is not considered to be part of this document or any document incorporated by reference in this document.

8

Item 1A. | RISK FACTORS |

There are risks and uncertainties that could affect our business. These risks and uncertainties include but are not limited to, the risk factors described below, in Item 7A: “Quantitative and Qualitative Disclosures about Market Risk” and elsewhere in this Form 10-K.

RISKS AND UNCERTAINTIES THAT MAY AFFECT FUTURE RESULTS

The following risks and uncertainties could affect our actual results and could cause results to differ materially from past results or those contemplated by our forward-looking statements. When used herein, the words “expects,” “believes,” “anticipates” and other similar expressions are intended to identify forward-looking statements.

We may experience fluctuations in quarterly results of operations.

Our quarterly operating results have varied in the past and may vary in the future due to a variety of factors, including adverse changes in the U.S. and global macroeconomic environment, volatility in overall demand for our customers’ products, success of customers’ programs, timing of new programs, new product introductions or technological advances by us, our customers and our competitors, and changes in pricing policies by us, our customers, our suppliers, and our competitors. Our customer base is diverse in the markets they serve, however, decreases in demand, particularly from customers in certain industries could affect future quarterly results. Additionally, our customers could be adversely impacted by illiquidity in the credit markets which could directly impact our operating results.

Component procurement, production schedules, personnel and other resource requirements are based on estimates of customer requirements. Occasionally, our customers may request accelerated production that can stress resources and reduce operating margins. Conversely, our customers may abruptly lower or cancel production which may lead to a sudden, unexpected increase in inventory or accounts receivable for which we may not be reimbursed even when under contract with customers. In addition, because many of our operating expenses are relatively fixed, a reduction in customer demand can harm our gross profit and operating results. The products which we manufacture for our customers have relatively short product lifecycles. Therefore, our business, operating results and financial condition are dependent in a significant way on our ability to obtain orders from new customers and new product programs from existing customers.

Operating results can also fluctuate if changes are made to significant estimates and assumptions. Significant estimates and assumptions include the allowance for doubtful receivables, provision for obsolete and non-saleable inventory, stock-based compensation, the valuation allowance on deferred tax assets, valuation of goodwill, impairment of long-lived assets, long-term incentive compensation accrual, the provision for warranty costs, the impact of hedging activities and purchase price allocation.

We are exposed to general economic conditions, which could have a material adverse impact on our business, operating results and financial condition.

Adverse economic conditions and uncertainty in the global economy such as unstable global financial and credit markets, inflation, and recession can negatively impact our business. Unfavorable economic conditions could affect the demand for our customers’ products by triggering a reduction in orders as well as a decline in forecasts which could adversely affect our sales in future periods. Additionally, the financial strength of our customers and suppliers and their ability to obtain and rely on credit financing may affect their ability to fulfill their obligations to us and have an adverse effect on our financial results.

The majority of our sales come from a small number of customers and a decline in sales to any of these customers could adversely affect our business.

At present, our customer base is concentrated and could become more or less concentrated. There can be no assurance that our principal customers will continue to purchase products from us at current levels. Moreover, we typically do not enter into long-term volume purchase contracts with our customers, and our customers have certain rights to extend or delay the shipment of their orders. We, however, typically require that our customers contractually agree to buy back inventory purchased within specified lead times to build their products if not used.

The loss of one or more of our major customers, or the reduction, delay or cancellation of orders from such customers, due to economic conditions or other forces, could materially and adversely affect our business, operating results and financial condition. The contraction in demand from certain industries could impact our customer orders and have a negative impact on our operations over the foreseeable future. Additionally, if one or more of our customers were to become insolvent or otherwise unable to pay for the manufacturing services provided by us, our operating results and financial condition would be adversely affected.

9

We depend on a limited number of suppliers for certain components that are critical to our manufacturing processes. A shortage of these components or an increase in their price could interrupt our operations and result in a significant change in our results of operations.

We are dependent on many suppliers, including sole source suppliers, to provide key components and raw materials used in manufacturing customers’ products. We have seen supply shortages in certain electronic components. In addition, our suppliers' facilities may also experience earthquakes, tsunamis and other natural disasters which may cause a shortage of components. This can result in longer lead times and the inability to meet our customers request for flexible production and extended shipment dates. If demand for components outpaces supply, capacity delays could affect future operations. Delays in deliveries from suppliers or the inability to obtain sufficient quantities of components and raw materials could cause delays or reductions in shipment of products to our customers which could adversely affect our operating results and damage customer relationships.

We operate in a highly competitive industry; if we are not able to compete effectively in the EMS industry, our business could be adversely affected.

Competitors may offer customers lower prices on certain high volume programs. This could result in price reductions, reduced margins and loss of market share, all of which would materially and adversely affect our business, operating results, and financial condition. If we were unable to provide comparable or better manufacturing services at a lower cost than our competitors, it could cause sales to decline. In addition, competitors can copy our non-proprietary designs and processes after we have invested in development of products for customers, thereby enabling such competitors to offer lower prices on such products due to savings in development costs.

Cash and cash equivalents are exposed to concentrations of credit risk.

We place our cash with high credit quality institutions. At times, such balances may be in excess of the federal depository insurance limit or may be on deposit at institutions which are not covered by insurance. If such institutions were to become insolvent during which time it held our cash and cash equivalents in excess of the insurance limit, it could be necessary to obtain other credit financing to operate our facilities.

Our ability to secure and maintain sufficient credit arrangements is key to our continued operations.

There is no assurance that we will be able to retain or renew our credit agreements in the future. In the event the business grows rapidly or there is uncertainty in the macroeconomic climate, additional financing resources could be necessary in the current or future fiscal years. There is no assurance that we will be able to obtain equity or debt financing at acceptable terms, or at all in the future. In addition, we have restrictive covenants with our financial institution which could impact how we manage our business. If we cannot meet our financial covenants, our borrowings could become immediately payable which could have a material adverse impact on our financial statements. For a summary of our banking arrangements, see Note 4 Long-Term Debt of the “Notes to Consolidated Financial Statements.”

Our operations may be subject to certain risks.

We manufacture product in facilities located in Mexico, China and the United States. These operations may be subject to a number of risks, including:

• | difficulties in staffing, turnover and managing onshore and offshore operations; |

• | political and economic instability (including acts of terrorism, pandemics, civil unrest, forms of violence and outbreaks of war), which could impact our ability to ship, manufacture, and/or receive product; |

• | unexpected changes in regulatory requirements and laws; |

• | longer customer payment cycles and difficulty collecting accounts receivable; |

• | export duties, import controls and trade barriers (including quotas); |

• | governmental restrictions on the transfer of funds; |

• | burdens of complying with a wide variety of foreign laws and labor practices; |

• | our locations may be impacted by hurricanes, tornadoes, earthquakes, water shortages, tsunamis, floods, typhoons, fires, extreme weather conditions and other natural or man-made disasters. |

Our operations in certain foreign locations receive favorable income tax treatment in the form of tax credits or other incentives. In the event that such tax incentives are not extended, are repealed, or we no longer qualify for such programs, our taxes may increase, which would reduce our net income.

10

Additionally, certain foreign jurisdictions restrict the amount of cash that can be transferred to the U.S or impose taxes and penalties on such transfers of cash. To the extent we have excess cash in foreign locations that could be used in, or is needed by, our operations in the United States, we may incur significant penalties and/or taxes to repatriate these funds.

Fluctuations in foreign currency exchange rates could increase our operating costs.

We have manufacturing operations located in Mexico and China. A significant portion of our operations are denominated in the Mexican peso and the Chinese currency, the renminbi ("RMB"). Currency exchange rates fluctuate daily as a result of a number of factors, including changes in a country's political and economic policies. Volatility in the currencies of our entities and the United States dollar could seriously harm our business, operating results and financial condition. The primary impact of currency exchange fluctuations is on the cash, receivables, payables and expenses of our operating entities. As part of our hedging strategy, we currently use Mexican peso forward contracts to hedge foreign currency fluctuations for a portion of our Mexican peso denominated expenses. We currently do not hedge expenses denominated in RMB. Unexpected losses could occur from increases in the value of these currencies relative to the United States dollar.

Our success will continue to depend to a significant extent on our key personnel.

Our future success depends in large part on the continued service of our key technical, marketing and management personnel and on our ability to continue to attract and retain qualified production employees. There can be no assurance that we will be successful in attracting and retaining such personnel, particularly in our manufacturing locales that may be experiencing high demand for similar key personnel. The loss of key employees could have a material adverse effect on our business, operating results and financial condition.

If we are unable to maintain our technological and manufacturing process expertise, our business could be adversely affected.

The markets for our customers’ products is characterized by rapidly changing technology, evolving industry standards, frequent new product introductions and short product life cycles. The introduction of products embodying new technologies or the emergence of new industry standards can render existing products obsolete or unmarketable. Our success will depend upon our customers’ ability to enhance existing products and to develop and introduce, on a timely and cost-effective basis, new products that keep pace with technological developments and emerging industry standards and address evolving and increasingly sophisticated customer requirements. Failure of our customers to do so could substantially harm our customers’ competitive positions. There can be no assurance that our customers will be successful in identifying, developing and marketing products that respond to technological change, emerging industry standards or evolving customer requirements.

Start-up costs and inefficiencies related to new or transferred programs can adversely affect our operating results and such costs may not be recoverable if such new programs or transferred programs are canceled or don’t meet expected sales volumes.

Start-up costs, the management of labor and equipment resources in connection with the establishment of new programs and new customer relationships, and the need to obtain required resources in advance can adversely affect our gross margins and operating results. These factors are particularly evident in the ramping stages of new programs. These factors also affect our ability to efficiently use labor and equipment. We are currently managing a number of new programs. Consequently, our exposure to these factors has increased. In addition, if any of these new programs or new customer relationships were terminated, our operating results could be harmed, particularly in the short term. We may not be able to recoup these start-up costs or replace anticipated new program revenues.

Customers may change production timing and demand schedules which makes it difficult for us to schedule production and capital expenditures and to maximize the efficiency of our manufacturing capacity.

Changes in demand for customer products reduce our ability to accurately estimate the future requirements of our customers. This makes it difficult to schedule production and maximize utilization of our manufacturing capacity. We must determine the levels of business that we will seek and accept from customers, set production schedules, commit to procuring inventory, and allocate personnel and resources, based on our estimates of our customers' requirements. Customers can require sudden increases and decreases in production which can put added stress on resources and reduce margins. Sudden decreases in production can lead to excess inventory on hand which may or may not be reimbursed by our customers even when under contract.

Continued growth could further lead to capacity constraints. We may need to transfer production to other facilities, acquire new facilities, or outsource production which could negatively impact gross margin.

11

An adverse change in the interest rates for our borrowings could adversely affect our financial condition.

We are exposed to interest rate risk under our revolving line of credit and term loan. We currently hedge a portion of our term loan with an interest rate swap. We have not historically hedged the interest rate on our credit facility; therefore, unless we do so, significant changes in interest rates could adversely affect our results of operations. Refer to the discussion in note 4, "Long-Term Debt" to the consolidated financial statements for further details of our debt obligations. We are also exposed to interest rate risk on our factoring activities.

Compliance or the failure to comply with current and future environmental laws or regulations could cause us significant expense.

We are subject to a variety of domestic and foreign environmental regulations relating to the use, storage, and disposal of materials used in our manufacturing processes. If we fail to comply with any present or future regulations, we could be subject to future liabilities or the suspension of current manufacturing operations. In addition, such regulations could restrict our ability to expand our operations or could require us to acquire costly equipment, substitute materials, or incur other significant expenses to comply with government regulations.

Our stock price is volatile.

Holders of the common stock will suffer immediate dilution to the extent outstanding equity awards are exercised to purchase common stock. Our stock price may be subject to wide fluctuations and possible rapid increases or declines over a short time period. These fluctuations may be due to factors specific to us such as our stock's thinly traded nature, variations in quarterly operating results or changes in earnings estimates, or to factors relating to the EMS industry or to the securities markets in general, which, in recent years, have experienced significant price fluctuations. These fluctuations often have been unrelated to the operating performance of the specific companies whose stocks are traded.

Due to inherent limitations, there can be no assurance that our system of disclosure and internal controls and procedures will be successful in preventing all errors, theft and fraud, or in informing management of all material information in a timely manner.

Management does not expect that our disclosure controls and internal controls and procedures will prevent all errors or fraud. A control system is designed to give reasonable, but not absolute, assurance that the objectives of the control system are met. In addition, any control system reflects resource constraints and the benefits of controls must be considered relative to their costs. Inherent limitations of a control system may include: judgments in decision making may be faulty, breakdowns can occur simply because of error or mistake and controls can be circumvented by collusion or management override. Due to the inherent limitations in a cost-effective control system, misstatements due to error or fraud may occur and may not be detected.

If we do not manage our growth effectively, our profitability could decline.

Our business is experiencing growth which can place considerable additional demands upon our management team and our operational, financial and management information systems. Our ability to manage growth effectively requires us to continue to implement and improve these systems; avoid cost overruns; maintain customer, supplier and other favorable business relationships during possible transition periods; continue to develop the management skills of our managers and supervisors; and continue to train, motivate and manage our employees. Our failure to effectively manage growth could have a material adverse effect on our results of operations.

12

If our manufacturing processes and services do not comply with applicable statutory and regulatory requirements, or if we manufacture products containing design or manufacturing defects, demand for our services may decline and we may be subject to liability claims.

We manufacture and design products to our customers’ specifications, and, in some cases, our manufacturing processes and facilities may need to comply with applicable statutory and regulatory requirements. For example, medical devices that we manufacture or design, as well as the facilities and manufacturing processes that we use to produce them, are regulated by the Food and Drug Administration and non-U.S. counterparts of this agency. In addition, our customers’ products and the manufacturing processes that we use to produce them often are highly complex. As a result, products that we manufacture may at times contain manufacturing or design defects, and our manufacturing processes may be subject to errors or not be in compliance with applicable statutory and regulatory requirements. Defects in the products we manufacture or design, whether caused by a design, manufacturing or component failure or error, or deficiencies in our manufacturing processes, may result in delayed shipments to customers or reduced or canceled customer orders. If these defects or deficiencies are significant, our business reputation may also be damaged. The failure of the products that we manufacture or our manufacturing processes and facilities to comply with applicable statutory and regulatory requirements may subject us to legal fines or penalties and, in some cases, require us to shut down or incur considerable expense to correct a manufacturing process or facility. Our customers are required to indemnify us against liability associated with designing products to meet their specifications. However, if our customers are responsible for the defects, they may not, or may not have resources to, assume responsibility for any costs or liabilities arising from these defects, which could expose us to additional liability claims.

Energy price increases may negatively impact our results of operations.

Certain components that we use in our manufacturing process are petroleum-based. In addition, we, along with our suppliers and customers, rely on various energy sources in our transportation activities. While significant uncertainty currently exists about the future levels of energy prices, a significant increase is possible. Increased energy prices could cause an increase to our raw material costs and transportation costs. In addition, increased transportation costs of certain of our suppliers and customers could be passed along to us. We may not be able to increase our product prices enough to offset these increased costs. In addition, any increase in our product prices may reduce our future customer orders and profitability.

Disruptions to our information systems, including security breaches, losses of data or outages, could adversely affect our operations.

We rely on information technology networks and systems to process, transmit and store electronic information. In particular, we depend on our information technology infrastructure for a variety of functions, including worldwide financial reporting, inventory management, procurement, invoicing and email communications. Any of these systems may be susceptible to outages due to fire, floods, power loss, telecommunications failures, terrorist attacks and similar events. Despite the implementation of network security measures, our systems and those of third parties on which we rely may also be vulnerable to computer viruses, break-ins and similar disruptions. If we or our vendors are unable to prevent such outages and breaches, our operations could be disrupted.

We are involved in various legal proceedings.

In the past, we have been notified of claims relating to various matters including contractual matters, intellectual property rights or other issues arising in the ordinary course of business. In the event of such a claim, we may be required to spend a significant amount of money to defend or otherwise address the claim. The Company is currently involved in an arbitration claim with a former customer to collect a significant payment for excess inventory purchased to an existing manufacturing agreement in place at the time. Any litigation or dispute resolution, even where a claim is without merit, could result in substantial costs and diversion of resources. Accordingly, the resolution or adjudication of such disputes, even those encountered in the ordinary course of business, could have a material adverse effect on our business, consolidated financial conditions and results of operations.

Our levels of insurance coverage may not be sufficient for potential damages, claims or losses.

We have various forms of business and liability insurance which we believe are appropriate based on the needs of companies in our industry. As a result, not all of our potential business risks or potential losses would be covered by our insurance policies. If we sustain a significant claim or loss which is not covered by insurance, our net income could be negatively impacted.

13

Changes in securities laws and regulations will increase our costs and risk of noncompliance.

We are required to file as an accelerated filer. As such, we are subject to additional requirements contained in the Sarbanes-Oxley Act of 2002 (the Sarbanes-Oxley Act) and more recently the Dodd-Frank Act. The Sarbanes-Oxley and Dodd-Frank Acts required or will require changes in some of our corporate governance, securities disclosure and compliance practices. In response to the requirements of the Sarbanes-Oxley and Dodd-Frank Acts, the SEC and NASDAQ promulgated new rules and additional rulemaking is expected in the future. Compliance with these new rules and future rules has increased and may increase further our legal, financial and accounting costs as well as a potential risk of noncompliance. Absent significant changes in related rules, which we cannot assure, we anticipate some level of increased costs related to these new regulations to continue indefinitely. We also expect these developments to make it more difficult and more expensive to obtain director and officer liability insurance, and we may be forced to accept reduced coverage or incur substantially higher costs to obtain coverage. Likewise, these developments may make it more difficult for us to attract and retain qualified members of our Board of Directors or qualified management personnel. Further, the costs associated with the compliance with and implementation of procedures under these and future laws and related rules could have a material impact on our results of operations. In addition, the costs associated with noncompliance with additional securities laws and regulations could also impact our business.

We may encounter complications with acquisitions, which could potentially harm our business.

Any current or future acquisitions may require additional equity financing, which could be dilutive to our existing shareholders, or additional debt financing, which could potentially affect our credit ratings. Any downgrades in our credit ratings associated with an acquisition could adversely affect our ability to borrow by resulting in more restrictive borrowing terms. To integrate acquired businesses, we must implement our management information systems, operating systems and internal controls, and assimilate and manage the personnel of the acquired operations. The integration of acquired businesses may be further complicated by difficulties managing operations in geographically dispersed locations. The integration of acquired businesses may not be successful and could result in disruption by diverting management’s attention from the core business. In addition, the integration of acquired businesses may require that we incur significant restructuring charges or other increases in our expenses and working capital requirements, which reduce our return on invested capital.

Acquisitions may involve numerous other risks and challenges including but not limited to: potential loss of key employees and customers of the acquired companies; the potential for deficiencies in internal controls at acquired companies; lack of experience operating in the geographic market or industry sector of the acquired business; constraints on available liquidity, and exposure to unanticipated liabilities of acquired companies. These and other factors could harm our ability to achieve anticipated levels of profitability at acquired operations or realize other anticipated benefits of an acquisition, and could adversely affect our consolidated business and operating results.

Our goodwill and identifiable intangible assets could become impaired, which could reduce the value of our assets and reduce net income in the year in which the write-off occurs.

Goodwill represents the excess of the cost of an acquisition over the fair value of the net assets acquired. The Company also ascribes value to certain identifiable intangible assets, which consists of customer relationships, non-compete agreements, and favorable leases, as a result of the acquisitions of Sabre and Ayrshire. The Company may incur impairment charges on goodwill or identifiable intangible assets if it determines that the fair values of goodwill or identifiable intangible assets are less than their current carrying values. The Company evaluates, on a regular basis, whether events or circumstances have occurred that indicate all, or a portion, of the carrying amount of goodwill may no longer be recoverable, in which case an impairment charge to earnings would become necessary.

Refer to Notes 1 and 15 to the consolidated financial statements and critical accounting policies and estimates' in management’s discussion and analysis of financial condition and results of operations for further discussion regarding the impairment testing of goodwill and identifiable intangible assets.

A decline in general economic conditions or global equity valuations could impact the judgments and assumptions about the fair value of the Company’s businesses and the Company could be required to record impairment charges on its goodwill or other identifiable intangible assets in the future, which could impact the Company’s consolidated balance sheet, as well as the Company’s consolidated statement of operations. If the Company was required to recognize an impairment charge in the future, the charge would not impact the Company's consolidated cash flows, current liquidity, capital resources, and covenants under its existing credit facilities.

14

Changes in financial accounting standards may affect our reported financial condition or results of operations as well increase costs related to implementation of new standards and modifications to internal controls.

Our consolidated financial statements are prepared in conformity with accounting standards generally accepted in the United States, or U.S. GAAP. These principles are subject to amendments made primarily by the Financial Accounting Standards Board (FASB) and the Securities and Exchange Commission (SEC). A change in those policies can have a significant effect on our reported results and may affect our reporting of transactions which are completed before a change is announced. For example, significant changes to revenue recognition rules will be effective for us in fiscal 2019 and we may incur significant costs to implement this new rule. Changes to accounting rules or challenges to our interpretation or application of the rules by regulators may have a material adverse effect on our reported financial results or on the way we conduct business. In addition, the continued convergence of U.S. GAAP and International Financial Reporting Standards ("IFRS") creates uncertainty as to the financial accounting policies and practices we will need to adopt in the future.

Item 1B. | UNRESOLVED STAFF COMMENTS |

None

Item 2. | PROPERTIES AS OF DATE OF FILING |

We have manufacturing and sales operations located in the United States, Mexico, and China. The table below lists the locations and square footage of our operating facilities:

Location | Approx. Sq. Ft. | Type of Interest (Leased/Owned) | Description of Use | ||||

Corinth, Mississippi | 350,000 | Leased | Manufacturing and warehouse | ||||

El Paso, Texas | 80,000 | Leased | Shipping and warehouse | ||||

Fayetteville, Arkansas | 175,000 | Leased | Manufacturing and warehouse | ||||

Harrodsburg, Kentucky (1) | 22,000 | Owned | Manufacturing and warehouse | ||||

Louisville, Kentucky | 2,000 | Leased | Administration | ||||

Oakdale, Minnesota | 60,000 | Leased | Manufacturing and warehouse | ||||

Spokane Valley, Washington | 95,000 | Leased | Sales, research, administration and manufacturing | ||||

Spokane Valley, Washington | 36,000 | Leased | Manufacturing | ||||

Total USA | 820,000 | ||||||

Juarez, Mexico | 193,000 | Leased | Warehouse | ||||

Juarez, Mexico | 174,000 | Owned | Manufacturing | ||||

Juarez, Mexico | 115,000 | Owned | Manufacturing and warehouse | ||||

Juarez, Mexico | 103,000 | Owned | Manufacturing and warehouse | ||||

Juarez, Mexico | 72,000 | Leased | Manufacturing | ||||

Juarez, Mexico | 66,000 | Owned | Manufacturing and warehouse | ||||

Juarez, Mexico | 60,000 | Owned | Manufacturing and warehouse | ||||

Total Mexico | 783,000 | ||||||

Shanghai, China | 121,000 | Leased | Manufacturing and warehouse | ||||

Shanghai, China | 36,000 | Leased | Manufacturing | ||||

Total China | 157,000 | ||||||

Grand Total | 1,760,000 | ||||||

(1) | During fiscal year 2017, we closed the Harrodsburg, Kentucky location and transferred customer programs to other facilities in the USA. The facility is currently listed for sale. Additionally, the property is not yet actively marketed and sale of the building in less than one year is not probable at this time. As such, the property is appropriately being reported in Property, Plant, and Equipment. |

The geographic diversity of these locations allows us to offer services near certain of our customers and major electronics markets with the additional benefit of reduced labor costs. We consider the productive capacity of our current facilities sufficient to carry on our current business. In addition, in Juarez, Mexico one of our buildings includes adjacent vacant land that could be developed into additional manufacturing and warehouse space.

15

All of our facilities are ISO certified to ISO 9001:2008 standard and to Customs Trade Partnership against Terrorism (CTPAT). In addition, the Juarez, Mexico; Shanghai, China and Spokane, Washington facilities are registered/certified to ISO/TS 16949 automotive standard, AS 9100C aviation, space and defense standard, ISO 13485 medical devices, ISO 14001 environmental standard, ANSI/ESD S20.20-2007 Electrostatic Discharge Control Program, OHSAS 18001 Occupational Health and Safety standard, and SA8000 / ISO 2600 social accountability standard. Oakdale, Minnesota is additionally registered to ISO-13485:2003 medical devices standard, AS9100C aviation, space and defense standard, and NADCAP certified. The Spokane, Washington and Juarez, Mexico facilities are additionally registered to ISO/IEC 80079-34 explosive atmospheres. Additionally, Juarez, Mexico is registered by the NSF for water products. The Oakdale, Minnesota; Corinth, Mississippi; Fayetteville, Arkansas and Spokane, Washington facilities are all registered by the U.S. State Department for International Traffic in Arms Regulations (ITAR).

Item 3. | LEGAL PROCEEDINGS |

We are a party to certain lawsuits or claims in the ordinary course of business. We do not believe that these proceedings, individually or in the aggregate, will have a material adverse effect on our financial position, results of operations or cash flow. Refer to Commitment and Contingencies footnote for further details on litigation in the fiscal year.

Item 4. | MINE SAFETY DISCLOSURES |

Not Applicable

PART II

Item 5: | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED SHAREHOLDER MATTERS, AND ISSUER PURCHASES OF EQUITY SECURITIES |

Market Information

Our common stock is traded on the NASDAQ Global Market, formerly the NASDAQ National Market System under the symbol “KTCC.” Quarterly high and low sales prices for our common stock for fiscal years 2017 and 2016 were as follows:

2017 | 2016 | ||||||||||||||

High | Low | High | Low | ||||||||||||

First Quarter | $ | 8.28 | $ | 7.23 | $ | 11.15 | $ | 9.75 | |||||||

Second Quarter | 8.18 | 7.08 | 10.39 | 7.50 | |||||||||||

Third Quarter | 8.20 | 7.08 | 8.47 | 6.09 | |||||||||||

Fourth Quarter | 8.00 | 6.69 | 8.97 | 6.99 | |||||||||||

High and low stock prices are based on the daily sales prices reported by the NASDAQ Stock Market. These quotations represent prices between dealers without adjustment for markups, markdowns, and commissions, and may not represent actual transactions.

Holders and Dividends

As of July 1, 2017, we had 688 shareholders of common stock on record. As a result of our credit agreement with Wells Fargo Bank, N.A. we are restricted from declaring or paying dividends in cash or stock without the Bank’s prior written consent. We have not paid a cash dividend and do not anticipate payment of dividends in the foreseeable future.

Equity Compensation Plan Information

Information concerning securities authorized for issuance under our equity compensation plans is set forth in Part III, Item 12 of this Annual Report, under the caption “Securities Authorized for Issuance under Equity Compensation Plans”, and that information is incorporated herein by reference.

16

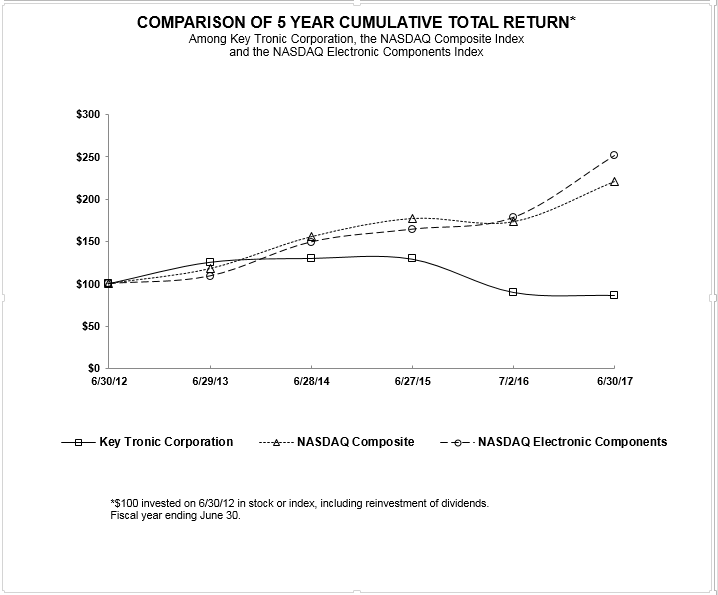

Performance Graph

Set forth below is a line graph comparing the cumulative total shareholder return on our common stock with the cumulative total return of the NASDAQ Stock Market (U.S. & Foreign) Index and the NASDAQ Electronic Components Index in fiscal 2017.

6/30/2012 | 6/29/2013 | 6/28/2014 | 6/27/2015 | 7/2/2016 | 7/1/2017 | ||||||||||||

Key Tronic Corporation | 100.00 | 125.61 | 130.22 | 129.37 | 89.68 | 86.04 | |||||||||||

NASDAQ Composite | 100.00 | 117.69 | 155.50 | 177.19 | 173.36 | 221.11 | |||||||||||

NASDAQ Electronic Components | 100.00 | 108.97 | 149.17 | 164.19 | 178.10 | 251.18 | |||||||||||

17

Item 6: | SELECTED FINANCIAL DATA |

The following selected data is derived from our audited consolidated financial statements and should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” the consolidated financial statements and related notes, and other information included in this report.

Financial Highlights

(In thousands, except for Supplemental Data and Per Share Amounts)

Fiscal Year Ended | |||||||||||||||||||

July 1, 2017 | July 2, 2016 | June 27, 2015 (3) | June 28, 2014(3) | June 29, 2013 | |||||||||||||||

Consolidated Statements of Operations Data: | |||||||||||||||||||

Net sales | $ | 467,797 | $ | 484,965 | $ | 433,997 | $ | 305,394 | $ | 361,033 | |||||||||

Gross profit | 38,300 | 38,825 | 33,305 | 26,854 | 34,512 | ||||||||||||||

Gross margin percentage | 8.2 | % | 8.0 | % | 7.7 | % | 8.8 | % | 9.6 | % | |||||||||

Operating income | 9,544 | 10,416 | 6,653 | 9,304 | 18,126 | ||||||||||||||

Operating margin percentage | 2.0 | % | 2.1 | % | 1.5 | % | 3.0 | % | 5.0 | % | |||||||||

Net income | 5,617 | 6,533 | 4,304 | 7,613 | 12,583 | ||||||||||||||

Earnings per share – diluted | 0.51 | 0.58 | 0.38 | 0.67 | 1.12 | ||||||||||||||

Consolidated Cash Flow Data: | |||||||||||||||||||

Cash flows provided by operations | 9,425 | 4,580 | 7,667 | 1,458 | 29,282 | ||||||||||||||

Capital expenditures | 9,307 | 13,277 | 8,808 | 7,763 | 3,470 | ||||||||||||||

Consolidated Balance Sheet Data: | |||||||||||||||||||

Net working capital (1) | 100,440 | 97,349 | 98,318 | 71,049 | 73,827 | ||||||||||||||

Total assets | 232,840 | 235,924 | 230,794 | 156,660 | 135,130 | ||||||||||||||

Long-term liabilities | 38,520 | 46,232 | 43,237 | 848 | 3,030 | ||||||||||||||

Shareholders’ equity | 116,567 | 105,582 | 100,768 | 103,645 | 94,160 | ||||||||||||||

Book value per share (2) | $ | 10.83 | $ | 9.84 | $ | 9.42 | $ | 9.83 | $ | 8.97 | |||||||||

Supplemental Data: | |||||||||||||||||||

Number of shares outstanding at year-end | 10,759,680 | 10,725,349 | 10,706,136 | 10,546,750 | 10,502,188 | ||||||||||||||

Number of employees at year-end | 5,038 | 4,947 | 4,866 | 3,343 | 2,584 | ||||||||||||||

Approximate square footage of operational facilities | 1,760,000 | 1,828,000 | 1,892,000 | 1,139,000 | 1,011,000 | ||||||||||||||

(1) | Net working capital is defined as total current assets less total current liabilities. Net working capital measures the portion of current assets that are financed by long term funds and is an indicator of short term financial management. |

(2) | Book value per share is defined as total shareholders’ equity divided by the number of shares outstanding at the end of the fiscal year. |

(3) | Reflects the acquisition of Ayrshire on September 3, 2014 in fiscal year 2015 and Sabre on July 1, 2013 in fiscal year 2014. |

18

Item 7: | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

Overview

KeyTronicEMS is a leader in electronic manufacturing services and solutions to original equipment manufacturers of a broad range of products. We provide engineering services, worldwide procurement and distribution, materials management, world-class manufacturing and assembly services, in-house testing, and unparalleled customer service. Our international production capability provides our customers with benefits of improved supply-chain management, reduced inventories, lower transportation costs, and reduced product fulfillment time. We continue to make investments in all of our operating facilities to give us the production capacity, capabilities and logistical advantages to continue to win new business. The following information should be read in conjunction with the consolidated financial statements included herein and with Item 1A, Risk Factors included as part of this filing.

Our mission is to provide our customers with superior manufacturing and engineering services at the lowest total cost for the highest quality products, and create long-term mutually beneficial business relationships by employing our “Trust, Commitment, Results” philosophy.

Executive Summary

During fiscal 2017, our revenue and margins were impacted by declining demand from some longstanding customers, which was not yet offset by the continued ramp in revenue from our new programs. While the EMS business is very competitive, we continued to win new business during the year, including two new programs involving gaming and seismic monitoring devices awarded in the fourth quarter, bringing the total number of significant program wins to nine for the fiscal year.

Net sales of $467.8 million for fiscal year 2017 decreased by 3.5 percent as compared to net sales of $485.0 million in fiscal year 2016. The decrease in net sales was primarily driven by a decrease in net sales from the former longstanding customer and closure of our Harrodsburg, Kentucky facility which has been discussed in prior quarters, partially offset by an increase in new program wins.

Throughout fiscal 2017, we made significant investments in improving our customer support organization and expanding our SMT, sheet metal and plastic molding capabilities in preparation for future growth. Moving into fiscal 2018, we continue to see a strong pipeline of potential new business and our new programs continue to ramp. We believe we’re well positioned to see growth in revenue and increasing profitability in the second half of the year

For the first quarter of fiscal year 2018, the Company expects to report revenue in the range of $110 million to $115 million. Future results will depend on actual levels of customers’ orders, the timing of the start-up of production of new product programs and the potential impact of the geopolitical uncertainty. We believe that we are well positioned in the EMS industry to continue expansion of our customer base and continue long-term growth.

We continue to diversify our customer base by adding additional programs and customers. Our current customer relationships involve a variety of products, including consumer electronics, electronic storage devices, plastics, household products, gaming devices, specialty printers, telecommunications, industrial equipment, military supplies, computer accessories, medical, educational, irrigation, automotive, transportation management, robotics, RFID, power supply, off-road vehicle equipment, fitness equipment, HVAC controls, consumer products, home building products, material handling systems and lighting equipment.

Gross profit as a percent of net sales was 8.2 percent in fiscal year 2017 compared to 8.0 percent for the prior fiscal year. The increase in gross profit as a percentage of net sales was primarily related to a decrease in material related costs partially offset by an increase in certain overhead costs. The level of gross margin is impacted by product mix, timing of the startup of new programs, facility utilization, pricing within the electronics industry and material costs, which can fluctuate significantly from quarter to quarter and year to year.

Operating income as a percentage of net sales for fiscal year 2017 was 2.0 percent compared to 2.1 percent for fiscal year 2016. The decrease in operating income as a percentage of net sales was primarily due to an increase in selling, general and administrative expenses. This increase in SG&A expenses is primarily related to an increase in legal fees.

Net income for fiscal year 2017 was $5.6 million or $0.51 per diluted share, as compared to net income of $6.5 million or $0.58 per diluted share for fiscal year 2016. The decrease in net income for fiscal year 2017 as compared to fiscal year 2016 was primarily driven by the decrease in net revenue as described above.

19

We maintain a strong balance sheet with a current ratio of 2.3 and a debt to equity ratio of 0.37. Total cash provided by operating activities as defined on our cash flow statement was $9.4 million during fiscal year 2017. We maintain sufficient liquidity for our expected future operations. As of July 1, 2017, we had $18.3 million outstanding on our revolving line of credit with Wells Fargo Bank, N.A. As a result, $26.3 million remained available to borrow as of July 1, 2017. We believe cash flow from operations, our borrowing capacity, our accounts receivable sale program, and equipment financing should provide adequate capital for planned growth over the long term.

RESULTS OF OPERATIONS

Comparison of the Fiscal Year Ended July 1, 2017 with the Fiscal Year Ended July 2, 2016

The following table sets forth for the periods indicated certain items of the consolidated statements of income expressed as a percentage of net sales. The financial information and discussion below should be read in conjunction with the consolidated financial statements and notes contained in this Annual Report.

Fiscal Year Ended | |||||||||||||||||

July 1, 2017 | % of net sales | July 2, 2016 | % of net sales | $ change | % point change | ||||||||||||

Net sales | $ | 467,797 | 100.0% | $ | 484,965 | 100.0% | $ | (17,168 | ) | — | |||||||

Cost of sales | 429,497 | 91.8 | 446,140 | 92.0 | (16,643 | ) | (0.2) | ||||||||||

Gross profit | 38,300 | 8.2 | 38,825 | 8.0 | (525 | ) | 0.2 | ||||||||||

Operating expenses: | |||||||||||||||||

Research, development and engineering | 6,393 | 1.4 | 6,397 | 1.3 | (4 | ) | 0.1 | ||||||||||

Selling, general and administrative | 22,363 | 4.8 | 22,012 | 4.5 | 351 | 0.3 | |||||||||||

Total operating expenses | 28,756 | 6.2 | 28,409 | 5.8 | 347 | 0.4 | |||||||||||

Operating income | 9,544 | 2.0 | 10,416 | 2.1 | (872 | ) | (0.1) | ||||||||||

Interest expense, net | 2,288 | 0.4 | 2,265 | 0.5 | 23 | (0.1) | |||||||||||

Income before income taxes | 7,256 | 1.6 | 8,151 | 1.7 | (895 | ) | (0.1) | ||||||||||

Income tax provision | 1,639 | 0.4 | 1,618 | 0.3 | 21 | 0.1 | |||||||||||

Net income | $ | 5,617 | 1.2% | $ | 6,533 | 1.3% | $ | (916 | ) | (0.1) | |||||||

Effective income tax rate | 22.6 | % | 19.9 | % | |||||||||||||

Net Sales

The decrease in net sales of $17.2 million from prior year was primarily driven by a decrease in net sales from the former longstanding customer which has been discussed in prior quarters, partially offset by an increase in new program wins.

The following table shows the revenue by industry sectors as a percentage of revenue for fiscal years 2017 and 2016:

Fiscal Year Ended | |||

July 1, 2017 | July 2, 2016 | ||

Industrial | 40% | 39% | |

Consumer | 35 | 31 | |

Gaming | 9 | 7 | |

Communication | 8 | 13 | |

Printers | 5 | 6 | |

Computer and Peripheral | 2 | 1 | |

Transportation | 1 | 3 | |

Total | 100% | 100% | |

We provide services to customers in a number of industries and produce a variety of products for our customers in each industry. Key Tronic does not target any particular industry, but rather seeks to find programs that strategically fit our vertical manufacturing capabilities. As we continue to diversify our customer base and win new customers, we will continue to see a change in the industry concentrations of our revenue.

Sales to foreign locations represented 22.6 percent and 28.3 percent of our total net sales in fiscal years 2017 and 2016, respectively.

20

Cost of Sales