Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended July 3, 2010

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 0-11559

KEY TRONIC CORPORATION

(Exact name of registrant as specified in its charter)

| Washington | 91-0849125 | |

| (State or other jurisdiction of Incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| N. 4424 Sullivan Road, Spokane Valley, Washington |

99216 | |

| (Address of principal executive offices) | (Zip Code) | |

(509) 928-8000

(Registrant’s telephone number, including area code)

N/A

(Former name, former address and former fiscal year, if changed since last report)

Securities Registered Pursuant to Section 12(b) of the Act: None

| Title of each class |

Name of each exchange on which registered | |

| Common stock, no par value | The NASDAQ Stock Market LLC |

Securities Registered Pursuant to Section 12(g) of the Act: None

Table of Contents

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulations S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

(Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | x | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

State the aggregate market value of the voting and non-voting common equity held by non affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter.

As of December 26, 2009, the aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was $34.9 million based on the closing price as reported on the NASDAQ.

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date: 10,326,855 shares of common stock were outstanding as of September 2, 2010.

Documents Incorporated by Reference:

The following documents are incorporated by reference to the extent specified herein:

| Document Description |

Part of Form 10-K | |

| Proxy Statement dated September 17, 2010 | Part III |

Table of Contents

KEY TRONIC CORPORATION

2010 FORM 10-K

FORWARD-LOOKING STATEMENTS

References in this report to “the Company”, “Key Tronic”, “we”, “our”, or “us” mean Key Tronic Corporation together with its subsidiaries, except where the context otherwise requires.

This Annual Report on Form 10-K contains forward-looking statements in addition to historical information. Forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from those reflected in the forward-looking statements. Risks and uncertainties that might cause such differences include, but are not limited to those outlined in “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Risks and Uncertainties that May Affect Future Results.” Readers are cautioned not to place undue reliance on forward-looking statements, which reflect management’s opinions only as of the date hereof. The Company undertakes no obligation to update forward-looking statements to reflect developments or information obtained after the date hereof and disclaims any obligation to do so. Readers should carefully review the

3

Table of Contents

risk factors described in periodic reports the Company files from time to time with the Securities and Exchange Commission, including Quarterly Reports on Form 10-Q and Current Reports on Form 8-K.

| Item 1. | BUSINESS |

Background

Key Tronic Corporation (dba: KeyTronicEMS Co.), was organized in 1969 as a Washington corporation that locally manufactured computer keyboards. The ability to design, build and deliver a quality product led to a reputation in the industry, allowing us to be a leading independent manufacturer of keyboards for computers in the United States. Our fully integrated design, tooling, and automated manufacturing capabilities enabled us to rapidly respond to customers’ needs for keyboards in production quantities worldwide. We supported our sales growth through the development and purchase of international manufacturing facilities. As the computer keyboard market matured with increasing competition from other international providers, we determined that our business could no longer solely rely on keyboard sales. After assessing market conditions and our strengths and capabilities, we shifted focus from keyboard manufacturing to contract manufacturing for a wide range of products. This strategy was based on our core strengths of innovative design and engineering expertise in electronics, mechanical engineering, and precision plastics combined with high-quality, low cost production, and assembly on an international basis. These strengths have made our company a strong competitor in the electronic manufacturing services (EMS) market.

Our Industry and Strategy

The expansion of the EMS industry during the last decade allowed us to continue to expand our customer base and the industries that we serve. The recent challenging global macroeconomic environment has had a negative impact on previously held customer programs. However, we successfully confronted the challenging global macroeconomic environment by reducing our costs while winning new customer programs, which allowed us to increase our profitability and strengthen our balance sheet during the global economic downturn. The increase in new programs represents a growing portion of our revenue and a promising foundation for our future. In keeping with our long-term strategic objectives, we have been successfully building a more diversified customer portfolio and a less concentrated revenue base, spanning a wider range of industries. We currently offer our customers the following services: integrated electronic and mechanical engineering, precision plastic molding, assembly, component selection, sourcing and procurement, worldwide logistics, and new product testing and production all at competitive pricing due to our global footprint.

We believe that we are well positioned in the EMS industry to continue the expansion of our customer base and achieve long term growth. Our core strengths continue to support our growth and our customers’ needs. We continue to focus on controlling operating expenses and leveraging the synergistic capabilities of our world-class facilities in the United States, Mexico, and China. This international production capability provides our customers with the benefits of improved supply-chain management, reduced inventory, lower labor costs, lower transportation costs, and reduced product fulfillment time. Given our competitive advantages and the growing need for some potential customers to move forward with their outsourcing strategies, we are strongly positioned to win new business in coming periods and grow our revenue and profits.

The EMS industry is intensely competitive. Although our customer base is growing we still have less than 1% of the potential global market and our revenue can fluctuate significantly due to reliance on a concentrated base of customers. We are planning for new customer growth in the coming quarters by securing new programs, increasing our worldwide manufacturing capacity, and continuing to improve our manufacturing and procurement processes. Ongoing challenges that we face include the following: Continuing to win programs from new and existing customers, balancing production capacity and key personnel in support of new customer programs, improving operating efficiencies, controlling costs while

4

Table of Contents

developing competitive pricing strategies, successfully transitioning new program wins to full production and successfully addressing industry-wide shortages in the global supply chain.

Customers and Marketing

We provide a mix of manufacturing services for outsourced Original Equipment Manufacturing (OEM) products. We provide the following EMS services: Product design, surface mount technologies (SMT) and pin through hole capability for printed circuit board assembly, tool making, precision plastic molding, liquid injection molding, automated tape winding, prototype design and full product builds.

Sales of the majority of our products have historically not been seasonal in nature, but may be seasonal in the future if there are changes in the types of products manufactured. Sales can, however, fluctuate significantly between quarters from changes in customers and customer demand due to our concentrated customer base.

For the fiscal years ended July 3, 2010, June 27, 2009, and June 28, 2008, the five largest customers in each year accounted for 57%, 52%, and 68% of total sales, respectively. The following customers represented 10% or more of total net sales over the last three fiscal years: KAZ Inc. (18%, less than 10%, less than 10%) International Game Technology, Inc. (12%, 13%, 18%), and Lexmark International, Inc. (less than 10%, 14%, 15%). It is anticipated that our new customer program wins will dilute our concentration of revenue in the future.

Although keyboard manufacturing is still included in our product offerings, we do not expect annual keyboard sales to be a material component of our business. We realized revenues of approximately $4.5 million, $4.2 million, and $5.8 million in fiscal years 2010, 2009, and 2008, respectively, from the sale of keyboards. In order to accommodate the demand for standard keyboard layouts, we maintain a purchase-from-stock program. The more popular standard layouts are built and stocked for immediate availability. Although we are recognized as a reputable contract manufacturer we still market our products and services primarily through our direct sales department aided by strategically located field sales people and distributors. Although we maintain relationships with several independent sales organizations to assist in marketing our EMS product lines, commissions earned and paid are not material to the consolidated financial statements.

Manufacturing

We have continually made investments in developing and expanding a capital equipment base to achieve vertical integration and efficiencies in our manufacturing processes. We have invested significant capital into SMT for volume manufacturing of complex printed circuit board assemblies. We also design and develop tooling for injection molding and manufacture the majority of plastic parts used in the products we manufacture. Additionally, we have equipment to maintain a controlled clean environment for manufacturing processes that require a high level of precise control.

We use a variety of manual and automated assembly processes in our facilities, depending upon product complexity and degree of customization. Some examples of automated processes include component insertion, SMT, flexible robotic assembly, automated storage tape winding, computerized vision system quality inspection, automated switch and key top installation, and automated functional testing.

Our engineering expertise and automated manufacturing processes enable us to work closely with our customers during the design and prototype stages of production and to jointly increase productivity and reduce response time to the marketplace. We use computer-aided design techniques and software to assist in preparation of the tool design layout and component placement, to reduce tooling and production costs, improve component and product quality, and enhance turnaround time during product development.

We purchase materials and components for our products from many different suppliers, including both domestic and international sources. We develop close working relationships with our suppliers, many of whom have been supplying products to us for several years.

5

Table of Contents

Research, Development, and Engineering

Research, development, and engineering (RD&E) expenses consist principally of employee related costs, third party development costs, program materials costs, depreciation, and allocated information technology and facilities costs. Our RD&E expenses were $2.8 million, $2.3 million, and $2.7 million in fiscal years 2010, 2009, and 2008 respectively. In each of these years, we focused most of our RD&E efforts on current customer EMS programs. The increase in RD&E in fiscal year 2010 compared to fiscal year 2009 is primarily the result of higher incentive compensation and increased headcount. The decrease in RD&E in fiscal year 2009 compared to fiscal year 2008 is the result of cost reduction efforts and lower incentive and bonus expenses.

Competition

The market for the products and services we provide is highly competitive. There are numerous competitors in the EMS industry, many of which have substantially more resources and are more geographically diverse than we are. Some of our competitors have similar international production capabilities, large financial resources and some have substantially greater manufacturing, research and development, and marketing resources. There is also competition from the manufacturing operations of our current and potential customers, who are continually evaluating the merits of manufacturing their products internally versus the advantages of outsourcing. We believe that we can currently compete favorably to these factors primarily on the basis of our international footprint, responsiveness, creativity, vertical production capability, quality, and cost.

Trademarks and Patents

Our name and logo are federally registered trademarks, and we believe they are valuable assets of our business. During 2001, we began operating under the trade name “KeyTronicEMS Co.” to better identify our primary business concentration. We also own several keyboard patents; however, since our focus is EMS, management believes that these patents will not have a significant impact on future revenues.

Employees

We consider our employees to be our primary strength and we make considerable efforts to maintain a well-qualified workforce. Our employee benefits include bonus programs involving periodic payments to all employees based on meeting quarterly or fiscal year performance targets. We regularly provide transportation, medical services, and meals to all of our employees in foreign locations. We maintain a 401(k) plan for U.S. employees, which provides a discretionary matching company contribution of up to 4% of an employee’s salary. We provide group health, life, and disability insurance plans. We also maintain stock option plans and other long term incentive plans for certain employees and outside directors. As of July 3, 2010 we had 2,036 employees compared to 1,963 on June 27, 2009, and 2,502 on June 28, 2008. Since we can have significant fluctuations in product demand, we seek to maintain flexibility in our workforce by utilizing skilled temporary and short-term contract labor in our manufacturing facilities in addition to full-time employees. Our employees in Reynosa, Mexico, are represented by a local union. We have no history of any material interruption of production due to labor disputes. We anticipate that this particular subsidiary will cease its operations during fiscal year 2011. As a result, we will no longer retain employees in Reynosa, Mexico.

Backlog

On July 31, 2010 our order backlog was valued at approximately $56.9 million, compared to approximately $29.9 million on July 25, 2009, which reflects an increase in expected revenue during fiscal year 2011. Even though our order backlog is comprised of firm purchase orders, the amount of backlog is not necessarily indicative of future sales but can be indicative of trends in expected future sales revenue. Due to the relationships with our customers, we will occasionally allow orders to be canceled or rescheduled and as a result is not a meaningful indicator of future financial results. If there are canceled or rescheduled orders, we will attempt to negotiate fees to cover the costs we have incurred. Order backlog consists of

6

Table of Contents

purchase orders received for products expected to be shipped approximately within the next twelve months, although shipment dates are subject to change due to design modifications, customer forecast changes, or other customer requirements.

Foreign Markets

Information concerning net sales and long-lived assets (property, plant, and equipment) by geographic areas is set forth in footnote 12 of the consolidated financial statements of this Annual Report on Form 10-K, under the caption “Enterprise-Wide Disclosures”, and that information is incorporated herein.

Executive Officers of the Registrant

The table below sets forth the name, current age and current position of our executive officers and other significant employees as of July 3, 2010:

| Name |

Age | Positions Held | ||

| Executive Officers | ||||

| Craig D. Gates |

51 | President and Chief Executive Officer | ||

| Ronald F. Klawitter |

58 | Executive Vice President of Administration, Chief Financial Officer and Treasurer | ||

| Douglas G. Burkhardt |

52 | Executive Vice President of Worldwide Operations | ||

| Lawrence J. Bostwick |

58 | Vice President of Engineering and Quality | ||

| Phil Hochberg |

48 | Vice President of Business Development | ||

| Brett R. Larsen |

37 | Vice President of Finance, and Controller | ||

| Don Sinclair* |

57 | Vice President of Materials |

| * | Subsequent to July 3, 2010, Mr. Sinclair announced his resignation with the Company effective August 31, 2010. |

Executive Officers

CRAIG D. GATES – President and Chief Executive Officer

Mr. Gates, age 51, has been President and Chief Executive officer of the Company since April 2009. Previously he was Executive Vice President and General Manager from August 2002 to April 2009. He served as Executive Vice President of Marketing, Engineering and Sales from July 1997 to August 2002 and served as Vice President and General Manager of New Business Development from October 1995 to July 1997. He joined the Company as Vice President of Engineering in October of 1994. From 1982 he held various engineering and management positions within the Microswitch Division of Honeywell, Inc., in Freeport, Illinois, and from 1991 to October 1994 he served as Director of Operations, Electronics for Microswitch. Mr. Gates has a Bachelor of Science Degree in Mechanical Engineering and a Masters in Business Administration from the University of Illinois, Urbana.

RONALD F. KLAWITTER – Executive Vice President of Administration, Chief Financial Officer, and Treasurer

Mr. Klawitter, age 58, has been Executive Vice President of Administration, CFO, and Treasurer since July 1997. Previously he was Vice President of Finance, Secretary, and Treasurer of the Company from October 1995 to July 1997. He was Acting Secretary from November 1994 to October 1995 and Vice President of Finance and Treasurer from 1992 to October 1995. From 1987 to 1992, Mr. Klawitter was Vice President of Finance at Baker Hughes Tubular Service, a subsidiary of Baker Hughes, Inc. Mr. Klawitter has a BA degree from Wittenberg University and is a Certified Public Accountant.

7

Table of Contents

DOUGLAS G. BURKHARDT – Executive Vice President of Worldwide Operations

Mr. Burkhardt, age 52, has been Executive Vice President of Worldwide Operations of the company since July 22, 2010. Previously Mr. Burkhardt was Vice President of Worldwide Operations from July 2008 to July 2010 and Director of China Operations and Program Management from January 2006 to July 2008. Mr. Burkhardt also served as Director of Northwest and China Operations from November of 1998 to January of 2006. Mr. Burkhardt also served as Director of Customer Satisfaction from March 1997 to November 1998 and Director of Molding from September of 1995 to March of 1997. Prior to this, Mr. Burkhardt served in other various senior management positions within the company. Mr. Burkhardt has been with the company since May of 1989. Prior to joining Key Tronic, Mr. Burkhardt worked for House of Aluminum and Glass for 12 years where he was the plant manager.

LAWRENCE J. BOSTWICK – Vice President of Engineering and Quality

Mr. Bostwick, age 58, has been Vice President of Engineering and Quality since July 2008. Previously he was Director of Engineering and Quality from February 2007 to July 2008 and served as Corporate Director of Quality from February 2006 to February 2007. From 2003 to 2006 he was Director of Supply Chain Management and Quality for the Lancer Corporation and from 1998 to 2003 he was Vice President of Operations for Thermacore International. He is a graduate of the Westinghouse and General Electric – Engineering and Manufacturing Professional Development Programs. He is certified in both Quality and Industrial Engineering and is a Lean – Six Sigma Master Black Belt. Mr. Bostwick has a combined B.S. degree in Production and Operation and Industrial Engineering from Bowling Green State University and a Masters degree in Industrial Engineering and Business Administration from Syracuse University.

PHIL HOCHBERG – Vice President of Business Development

Mr. Hochberg, age 48, has been Vice President of Business Development since October 2009. Previously he was Director of Business Development and Program Management from July 2008 to October 2009. Mr. Hochberg served as Director of Business Development from October 2004 to July 2008 and as Director of EMS Sales and Marketing from July 2000 to October 2004. Prior to joining Key Tronic, Mr. Hochberg worked for Quinton Instrument Company as their Director of Marketing and Product Management from 1992 to 2000. From 1988 to 1992, he was employed by SpaceLabs Medical as their Business Development Marketing Manager. Mr. Hochberg has an MBA from the University of British Columbia, a BA Psychology, with a minor in Business from Washington University in St. Louis.

BRETT R. LARSEN – Vice President of Finance, and Controller

Mr. Larsen, age 37, has served as Vice President of Finance and Controller since February 2010. He was Chief Financial Officer of FLSmidth Spokane, Inc. from December 2008 to February 22, 2010. From October 2005 through November 2008, Mr. Larsen served as Controller of Key Tronic Corporation. From May 2004 to October 2005, Mr. Larsen served as Manager of Financial Reporting of Key Tronic Corporation. From 2002 to May 2004, Mr. Larsen was an audit manager for the public accounting firm BDO Seidman, LLP. He also held various auditing and supervisory positions with Grant Thornton LLP from 1997 to 2002. Mr. Larsen has a Bachelor of Science degree in Accounting and a Masters degree in Accounting from Brigham Young University and is a Certified Public Accountant.

DON SINCLAIR – Vice President of Material

Mr. Sinclair, age 57, has served as the Vice President of Materials since January 2010. Prior to joining Key Tronic, Mr. Sinclair was employed by Advanced Input Systems Division of Esterline Corporation, where he held various positions such as: Director of Materials, Managing Director – Offshore Operations, and Vice President of Business Development from 1998 to 2009. Prior to 1998, Mr. Sinclair held management positions at companies including Intermec Technologies, Honeywell and Westinghouse. Mr. Sinclair has a Bachelor of Science Degree in Business from Washington State University.

8

Table of Contents

Available Information

Our principal executive offices are located at N. 4424 Sullivan Road, Spokane Valley, Washington 99216, and our telephone number is (509) 928-8000. Our website is located at http://www.keytronicems.com where filings of our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q or current reports on Form 8-K are available after they have been filed with the Securities and Exchange Commission. The information presented on our website currently and in the future is not considered to be part of this document or any document incorporated by reference in this document.

| Item 1A. | RISK FACTORS |

There are risks and uncertainties that could affect our business. These risks and uncertainties include but are not limited to, the risk factors described below, in Item 7A: “Quantitative and Qualitative Disclosures about Market Risk” and elsewhere in this Form 10-K.

RISKS AND UNCERTAINTIES THAT COULD AFFECT FUTURE RESULTS

The following risks and uncertainties could affect our actual results and could cause results to differ materially from past results or those contemplated by our forward-looking statements. When used herein, the words “expects”, “believes”, “anticipates” and similar expressions are intended to identify forward-looking statements.

Potential Fluctuations in Quarterly Results

Our quarterly operating results have varied in the past and may vary in the future due to a variety of factors, including adverse changes in the U.S. and global macroeconomic environment, volatility in overall demand for our customers’ products, success of customers’ programs, timing of new programs, new product introductions or technological advances by us, our customers and our competitors, and changes in pricing policies by us, our customers, our suppliers, and our competitors. Our customer base is diverse in the markets they serve, however, decreases in demand, particularly from customers that supply the banking, consumer products, and gambling industries, could affect future quarterly results. Additionally, our customers could be impacted by the illiquidity of the credit markets which could directly impact our operating results.

Component procurement, production schedules, personnel and other resource requirements are based on estimates of customer requirements. Occasionally, our customers may request accelerated production that can stress resources and reduce operating margins. In addition, because many of our operating expenses are relatively fixed, a reduction in customer demand can harm our gross profit and operating results. The products which we manufacture for our customers have relatively short product lifecycles. Therefore, our business, operating results and financial condition are dependent in significant way on our ability to obtain orders from new customers and new product programs from existing customers.

Operating results can also fluctuate if changes are made to significant estimates and assumptions. Significant estimates and assumptions include the allowance for doubtful receivables, provision for obsolete and non-saleable inventory, the valuation allowance on deferred tax assets, impairment of long-lived assets, long-term incentive compensation accrual, and the provision for warranty costs.

Economic Conditions

Recently there have been adverse conditions and uncertainty in the global economy as the result of unstable global financial and credit markets, inflation, and recession. These unfavorable economic conditions and the weakness of the credit market could affect the demand for our customers’ products. The current global macroeconomic environment may affect some of our customers that could reduce orders and change forecasts which could adversely affect our sales in future periods. Additionally, the financial strength of our customers and suppliers and their ability to obtain and rely on credit financing may affect their ability to fulfill their obligations to us and have an adverse affect on our financial results.

9

Table of Contents

Credit Markets

The current illiquidity and financial instability in the credit markets could adversely impact lenders and potentially limit the ability of our suppliers and customers to borrow. This may affect their ability to fulfill their obligations to us and have an adverse effect on our financial results.

Dependence on Suppliers

We are dependent on many suppliers, including sole source suppliers, to provide key components and raw materials used in manufacturing customers’ products. Over the past few quarters we have seen supply shortages in certain electronic components. This has resulted in longer lead times and the inability to meet our customers request for flexible production and we have missed or extended shipment dates. If demand for these components continues to outpace supply capacity these delays could further affect future operations. Delays in deliveries from suppliers or the inability to obtain sufficient quantities of components and raw materials could cause delays or reductions in shipment of products to our customers which could adversely affect our operating results and damage customer relationships.

Concentration of Credit Risk

Cash and cash equivalents are exposed to concentrations of credit risk. We place our cash with high credit quality institutions. At times, such balances may be in excess of the federal depository insurance limit or may be on deposit at institutions which are not covered by insurance. If such institutions were to become insolvent during which time it held our cash and cash equivalents in excess of the insurance limit, it could be necessary to obtain other credit financing to operate our facilities.

Competition

The EMS industry is intensely competitive. Competitors may offer customers lower prices on certain high volume programs. This could result in price reductions, reduced margins and loss of market share, all of which would materially and adversely affect our business, operating results, and financial condition. If we were unable to provide comparable or better manufacturing services at a lower cost than our competitors, it could cause sales to decline. In addition, competitors can copy our non-proprietary designs after we have invested in development of products for customers, thereby enabling such competitors to offer lower prices on such products due to savings in development costs.

Concentration of Major Customers

At present, our customer base is highly concentrated and could become more or less concentrated. Our largest EMS customer accounted for 18% of net sales in fiscal year 2010. This same customer accounted for 6% of sales in 2009 and 0% in 2008. For the fiscal years ended 2010, 2009, and 2008, the five largest customers accounted for 57%, 52%, and 68% of total sales, respectively. There can be no assurance that our principal customers will continue to purchase products from us at current levels. Moreover, we typically do not enter into long-term volume purchase contracts with our customers, and our customers have certain rights to extend or delay the shipment of their orders. We, however, require that our customers contractually agree to buy back inventory purchased within specified lead times to build their products if not used.

The loss of one or more of our major customers, or the reduction, delay or cancellation of orders from such customers, due to economic conditions or other forces, could materially and adversely affect our business, operating results and financial condition. Specifically, some of our major customers provide products to the banking and gambling industries which have been adversely affected by the unfavorable economic environment. The contraction in demand from our customers in these industries could continue to impact our customer orders and continue to have a negative impact on our operations over the next several fiscal quarters. Additionally, if one or more of our customers were to become insolvent or otherwise unable to pay for the manufacturing services provided by us, our operating results and financial condition would be adversely affected.

Foreign Manufacturing Operations

Most of the products manufactured by us are produced at our facilities located in Mexico and China. These international operations may be subject to a number of risks, including:

10

Table of Contents

| • | difficulties in staffing and managing foreign operations; |

| • | political and economic instability (including acts of terrorism, civil unrest, forms of violence and outbreaks of war), which could impact our ability to ship and/or receive product; |

| • | unexpected changes in regulatory requirements and laws; |

| • | longer customer payment cycles and difficulty collecting accounts receivable; |

| • | export duties, import controls and trade barriers (including quotas); |

| • | governmental restrictions on the transfer of funds; |

| • | burdens of complying with a wide variety of foreign laws and labor practices; |

| • | fluctuations in currency exchange rates, which could affect component costs, local payroll, utility and other expenses; and |

| • | inability to utilize net operating losses incurred by our foreign operations to reduce our U.S. income taxes; |

| • | our foreign locations may be impacted by hurricanes, earthquakes, water shortages, tsunamis, floods, typhoons, fires, extreme weather conditions and other natural or manmade disasters. |

Our operations in certain foreign locations receive favorable income tax treatment in the form of tax credits or other incentives. In the event that such tax holidays or other incentives are not extended, are repealed, or we no longer qualify for such programs, our taxes may increase, which would reduce our net income.

Additionally, certain foreign jurisdictions restrict the amount of cash that can be transferred to the U.S or impose taxes and penalties on such transfers of cash. To the extent we have excess cash in foreign locations that could be used in, or is needed by, our operations in the United States, we may incur significant penalties and/or taxes to repatriate these funds.

Dependence on Key Personnel

Our future success depends in large part on the continued service of our key technical, marketing and management personnel and on our ability to continue to attract and retain qualified employees. There can be no assurance that we will be successful in attracting and retaining such personnel. The loss of key employees could have a material adverse effect on our business, operating results and financial condition.

Technological Change and New Product Risk

The markets for our customers’ products is characterized by rapidly changing technology, evolving industry standards, frequent new product introductions and relatively short product life cycles. The introduction of products embodying new technologies or the emergence of new industry standards can render existing products obsolete or unmarketable. Our success will depend upon our customers’ ability to enhance existing products and to develop and introduce, on a timely and cost-effective basis, new products that keep pace with technological developments and emerging industry standards and address evolving and increasingly sophisticated customer requirements. Failure of our customers to do so could substantially harm our customers’ competitive positions. There can be no assurance that our customers will be successful in identifying, developing and marketing products that respond to technological change, emerging industry standards or evolving customer requirements.

Interest Rate Risk

We are exposed to interest rate risk under our revolving credit facility with interest rates based on various levels of margin added to published prime rate and LIBOR rates depending on the calculation of a certain financial covenant.

Compliance with Current and Future Environmental Regulation

We are subject to a variety of domestic and foreign environmental regulations relating to the use, storage, and disposal of materials used in our manufacturing processes. If we fail to comply with any present or future regulations, we could be subject to future liabilities or the suspension of current manufacturing operations. In addition, such regulations could restrict our ability to expand our operations or could require us to acquire costly equipment, substitute materials, or incur other significant expenses to comply with government regulations.

11

Table of Contents

Foreign Currency Fluctuations

A significant portion of our operations are in foreign locations. As a result, transactions occur in currencies other than the U.S. dollar. Exchange rate fluctuations among other currencies used by us could directly or indirectly affect our financial results. Future currency fluctuations are dependent upon a number of factors and cannot be easily predicted. We currently use Mexican peso forward contracts to hedge foreign currency fluctuations for a portion of our Mexican peso denominated expenses. However, unexpected expenses could occur from future fluctuations in exchange rates.

Dilution and Stock Price Volatility

Holders of the common stock will suffer immediate dilution to the extent outstanding options to purchase the common stock are exercised. Our stock price may be subject to wide fluctuations and possible rapid increases or declines over a short time period. These fluctuations may be due to factors specific to us such as variations in quarterly operating results or changes in earnings estimates, or to factors relating to the EMS industry or to the securities markets in general, which, in recent years, have experienced significant price fluctuations. These fluctuations often have been unrelated to the operating performance of the specific companies whose stocks are traded.

Disclosure and Internal Controls

Management does not expect that our disclosure controls and internal controls and procedures will prevent all errors or fraud. A control system is designed to give reasonable, but not absolute, assurance that the objectives of the control system are met. In addition, any control system reflects resource constraints and the benefits of controls must be considered relative to their costs. Inherent limitations of a control system may include: judgments in decision making may be faulty, breakdowns can occur simply because of error or mistake and controls can be circumvented by collusion or management override. Due to the inherent limitations in a cost-effective control system, misstatements due to error or fraud may occur and may not be detected.

| Item 1B. | UNRESOLVED STAFF COMMENTS |

None

| Item 2. | PROPERTIES |

We have manufacturing and sales operations located in the United States, Mexico, and China. The table below lists the locations and square footage of our operating facilities:

| Location |

Approx. Sq. Ft. |

Type of Interest (Leased/Owned) |

Description of Use | |||

| Spokane Valley, Washington (1) | 61,000 | Leased | Sales, research, administration and manufacturing | |||

| Spokane Valley, Washington | 36,000 | Leased | Manufacturing | |||

| El Paso, Texas | 80,000 | Leased | Shipping and warehouse | |||

| Total USA |

177,000 | |||||

| Juarez, Mexico | 174,000 | Owned | Manufacturing | |||

| Juarez, Mexico | 60,000 | Owned | Manufacturing and warehouse | |||

| Juarez, Mexico | 66,000 | Owned | Manufacturing and warehouse | |||

| Juarez, Mexico(2) | 115,000 | Owned | Manufacturing and warehouse | |||

| Juarez, Mexico(3) | 72,000 | Leased | Manufacturing and warehouse | |||

| Reynosa, Mexico(4) | 140,000 | Leased | Manufacturing | |||

| Reynosa, Mexico(4) | 100,000 | Leased | Warehouse | |||

12

Table of Contents

| Total Mexico |

727,000 | |||||

| Shanghai, China (5) |

83,000 | Leased | Manufacturing | |||

| Total China |

83,000 | |||||

| Grand Total |

987,000 | |||||

| (1) | On June 15, 2010, the company amended its lease with Royal Hills Associates (RHA) to extend the lease for an additional ten years, which we continue to occupy as our headquarters (see Note 3 to Consolidated Financial Statements) |

| (2) | During fiscal year 2010, we purchased a 115, 000 square foot manufacturing facility in Juarez, Mexico for additional assembly space. In addition, as part of the purchase transaction we obtained an option to purchase an additional adjacent manufacturing facility. |

| (3) | In fiscal year 2009, we leased a new facility in Juarez, Mexico for more storage capacity and additional assembly space. |

| ( 4 ) | These facilities are used exclusively to manufacture products for one EMS customer. We anticipate that this particular subsidiary will cease its operations during fiscal year 2011. |

| ( 5 ) | In fiscal year 2010, we increased our leased space in China to 83,000 sq. ft. to accommodate an additional SMT line and for additional assembly space. Subsequent to fiscal year 2010, we entered into an agreement to lease an additional 36,000 square feet of manufacturing space. |

The geographic diversity of these locations allows us to offer services near certain of our customers and major electronics markets with the additional benefit of reduced labor costs. We consider the productive capacity of our current facilities sufficient to carry on our current business. In addition, in Juarez, Mexico one of our buildings includes adjacent vacant land that could be developed into additional manufacturing and warehouse space and we have a purchase option on another facility. All of our facilities are ISO certified to ISO 9001:2008 standards, ISO-14001 environmental standards, and ISO-13485:2003 medical devices standards. The Spokane, Washington facilities are additionally registered to AS9100B, ITAR and ISO/TS 16949. Our China facilities are also registered to AS9100B and ISO/TS.

| Item 3. | LEGAL PROCEEDINGS |

We are a party to certain lawsuits or claims in the ordinary course of business. We do not believe that these proceedings, individually or in the aggregate, will have a material adverse effect on our financial position, results of operations or cash flow.

| Item 4. | RESERVED |

| Item 5: | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED SHAREHOLDER MATTERS, AND ISSUER PURCHASES OF EQUITY SECURITIES |

Market Information

Our common stock is traded on the NASDAQ Global Market, formerly the NASDAQ National Market System under the symbol “KTCC”. Quarterly high and low closing sales prices for our common stock for fiscal years 2010 and 2009 were as follows:

13

Table of Contents

| 2010 | 2009 | |||||||||||

| High | Low | High | Low | |||||||||

| First Quarter |

$ | 2.40 | $ | 1.60 | $ | 3.84 | $ | 2.47 | ||||

| Second Quarter |

3.60 | 2.26 | 2.56 | 0.97 | ||||||||

| Third Quarter |

6.02 | 3.69 | 1.22 | 0.86 | ||||||||

| Fourth Quarter |

6.61 | 4.88 | 1.94 | 0.91 | ||||||||

High and low stock prices are based on the daily closing price reported by the NASDAQ Stock Market. These quotations represent prices between dealers without adjustment for markups, markdowns, and commissions, and may not represent actual transactions.

Holders and Dividends

As of July 3, 2010, we had 804 shareholders of common stock on record. As a result of our credit agreement with Wells Fargo, N.A. we are restricted from declaring or paying dividends in cash and stock. We have not paid a cash dividend and do not anticipate payment of dividends in the foreseeable future.

Equity Compensation Plan Information

Information concerning securities authorized for issuance under our equity compensation plans is set forth in Part III, Item 12 of this Annual Report, under the caption “Securities Authorized for Issuance under Equity Compensation Plans”, and that information is incorporated herein by reference.

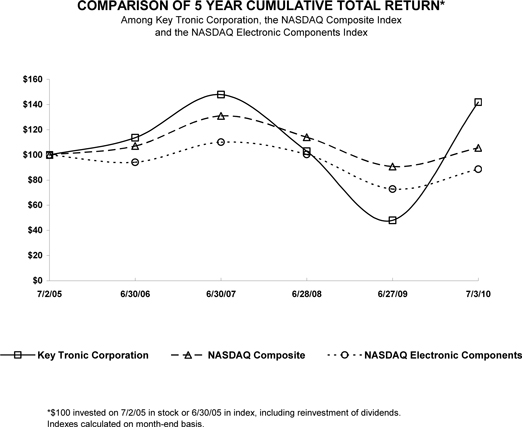

Performance Graph

Set forth below is a line graph comparing the cumulative total shareholder return on our common stock with the cumulative total return of the NASDAQ Stock Market (U.S. & Foreign) Index and the NASDAQ Electronic Components Index in fiscal 2010.

14

Table of Contents

| 7/2/05 | 6/30/06 | 6/30/07 | 6/28/08 | 6/27/09 | 7/3/10 | |||||||

| Key Tronic Corporation |

100.00 | 113.66 | 147.97 | 102.91 | 47.97 | 141.86 | ||||||

| NASDAQ Composite |

100.00 | 107.08 | 130.99 | 114.02 | 90.79 | 105.54 | ||||||

| NASDAQ Electronic Components |

100.00 | 94.09 | 110.15 | 100.35 | 72.87 | 88.63 |

| Item 6: | SELECTED FINANCIAL DATA |

The following selected data is derived from our audited consolidated financial statements and should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” the consolidated financial statements and related notes, and other information included in this report.

15

Table of Contents

Financial Highlights

(In thousands, except for Supplemental Data and Book Value per Share)

| Fiscal Years | ||||||||||||||||||||

| July 3, 2010 |

June 27, 2009 |

June 28, 2008 |

June 30, 2007 |

July 1, 2006 |

||||||||||||||||

| Consolidated Statements of Operations Data: |

||||||||||||||||||||

| Net sales |

$ | 199,620 | $ | 184,924 | $ | 204,122 | $ | 201,712 | $ | 187,699 | ||||||||||

| Gross profit |

19,250 | 13,180 | 16,820 | 17,670 | 17,304 | |||||||||||||||

| Gross margin percentage |

9.6 | % | 7.1 | % | 8.2 | % | 8.8 | % | 9.2 | % | ||||||||||

| Operating income |

7,388 | 1,783 | 6,834 | 6,810 | 5,861 | |||||||||||||||

| Operating margin percentage |

3.7 | % | 1.0 | % | 3.3 | % | 3.4 | % | 3.1 | % | ||||||||||

| Net income |

8,690 | 1,063 | 5,584 | 5,230 | 9,753 | |||||||||||||||

| Earnings per share – diluted |

0.85 | 0.11 | 0.54 | 0.51 | 0.97 | |||||||||||||||

| Consolidated Cash Flow Data: |

||||||||||||||||||||

| Cash flows provided by (used in) operations |

3,697 | 10,038 | (718 | ) | (1,857 | ) | (34 | ) | ||||||||||||

| Capital expenditures |

3,378 | 1,891 | 1,180 | 3,137 | 1,638 | |||||||||||||||

| Consolidated Balance Sheet Data: |

||||||||||||||||||||

| Net working capital (1) |

44,708 | 37,444 | 45,695 | 41,222 | 31,703 | |||||||||||||||

| Total assets |

101,642 | 77,755 | 98,344 | 89,388 | 88,695 | |||||||||||||||

| Long-term liabilities |

4,236 | 3,030 | 13,241 | 14,719 | 11,665 | |||||||||||||||

| Shareholders’ equity |

59,417 | 51,114 | 49,081 | 43,244 | 37,548 | |||||||||||||||

| Book value per share (2) |

5.79 | 5.08 | 4.90 | 4.36 | 3.85 | |||||||||||||||

| Supplemental Data: |

||||||||||||||||||||

| Number of shares outstanding at year-end |

10,264,390 | 10,065,974 | 10,024,308 | 9,921,045 | 9,750,413 | |||||||||||||||

| Number of employees at year-end |

2,036 | 1,963 | 2,502 | 2,227 | 2,840 | |||||||||||||||

| Approximate square footage of operational facilities |

987,000 | 849,000 | 777,000 | 784,000 | 723,000 | |||||||||||||||

| (1) | Net working capital is defined as total current assets less total current liabilities. Net working capital measures the portion of current assets that are financed by long term funds and is an indicator of short term financial management. |

| (2) | Book value per share is defined as total shareholders’ equity divided by the number of shares outstanding at the end of the fiscal year. |

16

Table of Contents

| Item 7: | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

Overview

KeyTronicEMS is a leader in electronic manufacturing services and solutions to original equipment manufacturers of a broad range of products. We provide engineering services, worldwide procurement and distribution, materials management, world-class manufacturing and assembly services, in-house testing, and unparalleled customer service. Our international production capability provides our customers with benefits of improved supply-chain management, reduced inventories, lower transportation costs, and reduced product fulfillment time. We continue to make investments in all of our operating facilities to give us the production capacity and logistical advantages to continue to win new business. The following information should be read in conjunction with the consolidated financial statements included herein and with Item 1A, Risk Factors.

Our mission is to provide our customers with superior manufacturing and engineering services at the lowest total cost for the highest quality products, and create long-term mutually beneficial business relationships.

Executive Summary

Our sales of $199.6 million in fiscal year 2010 increased by 8.0% as compared to sales of $184.9 million in fiscal year 2009. This increase in sales was primarily driven by new customer programs for both longstanding and new customers, partially offset by a continuance of an unfavorable macroeconomic environment and industry-wide shortages in the global supply chain. Sales for the first quarter of fiscal year 2011 are expected to be within the range of $58 million to $61 million. Results will depend on actual levels of customers’ orders and the timing of the start up of production of new product programs. We believe that we are well positioned in the EMS industry to win new business in coming periods and profitably grow our revenue as the economy recovers.

The concentration of our largest customers increased during fiscal year 2010 with the top five customers’ sales increasing to 57% of total sales in 2010 from 52% in 2009, and 68% in 2008. Our current customer relationships involve a variety of products, including consumer electronics, electronic storage devices, plastics, household products, gaming devices, specialty printers, telecommunications, industrial equipment, and computer accessories. The total number of our customers continued to increase during fiscal year 2010. These new customers have programs that represent small annual sales while others have multi-million-dollar potential.

Gross profit as a percent of sales was 9.6% in fiscal year 2010 compared to 7.1% for the prior fiscal year. The increase in gross profit as a percentage of net sales was primarily due to higher sales, increased leverage of fixed costs, a decrease in manufacturing facility costs due to favorable foreign exchange changes, a decrease in headcount of overhead employees and severance costs incurred in fiscal year 2009 that did not recur in fiscal year 2010.

Operating income as a percentage of sales for fiscal year 2010 was 3.7% compared to 1.0% for fiscal year 2009. The increase in operating income as a percentage of sales was due to an improved gross margin, combined with our continued success in controlling operating expenses and improving efficiencies during fiscal year 2010.

Net income for fiscal year 2010 was $8.7 million or $0.85 per diluted share, up from $1.1 million or $0.11 per diluted share for fiscal year 2009. The increase in net income for fiscal year 2010 as compared to fiscal year 2009 was primarily due to an approximate 2.5% improvement in our gross margin. Also, our fiscal year 2010 results include an income tax benefit of $1.4 million, resulting in part from the release of our valuation allowance on deferred tax assets related to our domestic net operating loss carryforwards that occurred in the third quarter of fiscal 2010.

17

Table of Contents

We maintain a strong balance sheet with a current ratio of 2.18 and a long-term debt to equity ratio of .03. Total cash provided by operating activities as defined on our cash flow statement was $3.7 million during fiscal year 2010. We maintain sufficient liquidity for our expected future operations and had $1.6 million in borrowings on our revolving line of credit with Wells Fargo, N.A. of which $18.4 million remained available at July 3, 2010. We believe cash flow generated from operations, our borrowing capacity, and equipment lease financing should provide adequate capital for planned growth over the long term.

Results of Operations

The following table sets forth for the periods indicated certain items of the consolidated statements of income expressed as a percentage of net sales. The financial information and discussion below should be read in conjunction with the consolidated financial statements and notes contained in this Annual Report.

| Years Ended | |||||||||

| July 3, 2010 | June 27, 2009 | June 28, 2008 | |||||||

| Net sales |

100.0 | % | 100.0 | % | 100.0 | % | |||

| Cost of sales |

90.4 | 92.9 | 91.8 | ||||||

| Gross profit |

9.6 | 7.1 | 8.2 | ||||||

| Operating expenses (income) |

|||||||||

| Research, development and engineering |

1.4 | 1.2 | 1.3 | ||||||

| Selling, general and administrative |

4.5 | 4.5 | 4.0 | ||||||

| Goodwill impairment |

— | 0.4 | — | ||||||

| Gain on sale of real estate held for sale |

— | — | (0.4 | ) | |||||

| Total operating expenses |

5.9 | 6.1 | 4.9 | ||||||

| Operating income |

3.7 | 1.0 | 3.3 | ||||||

| Interest expense |

— | 0.3 | 0.5 | ||||||

| Income before income taxes |

3.7 | 0.7 | 2.8 | ||||||

| Income tax provision (benefit) |

(0.7 | ) | 0.1 | 0.1 | |||||

| Net income |

4.4 | % | 0.6 | % | 2.7 | % | |||

Net Sales

Net sales were $199.6 million, $184.9 million, and $204.1 million in fiscal years 2010, 2009, and 2008, respectively.

Net sales increased $14.7 million during fiscal year 2010 as compared with fiscal year 2009. This increase in sales was primarily driven by new customer programs for both longstanding and new customers, partially offset by a continuance of an unfavorable macroeconomic environment and industry-wide shortages in the global supply chain. The $19.2 million decrease in net sales during fiscal year 2009 reflects the expected lower demand from established customers due to the unfavorable global macroeconomic environment. We anticipate that several more new customer programs will enter production in fiscal year 2011 and begin contributing to revenue.

The table below shows the revenue by industry sectors as a percentage of revenue for the following fiscal years:

18

Table of Contents

| Years Ended | |||||||||

| July 3, 2010 | June 27, 2009 | June 28, 2008 | |||||||

| Commercial Printer |

9 | % | 15 | % | 16 | % | |||

| Communication |

5 | % | 10 | % | 9 | % | |||

| Computer and Peripheral |

15 | % | 17 | % | 8 | % | |||

| Consumer |

32 | % | 19 | % | 9 | % | |||

| Gaming |

13 | % | 13 | % | 19 | % | |||

| Industrial |

4 | % | 4 | % | 3 | % | |||

| Transaction Printer |

22 | % | 22 | % | 36 | % | |||

| Total |

100 | % | 100 | % | 100 | % | |||

We provide services to customers in a number of industries and produce a variety of products for our customers in each industry. As we continue to diversify our customer base and win new customers we may continue to see a change in the industry concentrations of our revenue.

Sales to foreign locations represented 17.9%, 11.3%, and 5.6% of our total net sales in fiscal years 2010, 2009, and 2008, respectively.

Cost of Sales

Total cost of sales as a percentage of net sales was 90.4%, 92.9%, and 91.8% in fiscal years 2010, 2009, and 2008, respectively.

Total cost of materials as a percentage of net sales was approximately 68.6%, 69.2%, and 66.9% in fiscal years 2010, 2009, and 2008, respectively. The change from year-to-year is directly related to changes in product mix.

Production and support costs as a percentage of net sales were 21.8%, 23.7%, and 24.9% in fiscal years 2010, 2009, and 2008, respectively. The decrease in fiscal year 2010 as compared to fiscal year 2009 is related to higher fixed cost absorption due to a $14.7 million increase in net sales, while production and support costs decreased $0.3 million due to favorable foreign exchange rates and a reduction of manufacturing facility payroll. These savings were partially offset by an increase in the provision for obsolete inventory. The decrease in fiscal year 2009 as compared to fiscal year 2008 was due to a $6.9 million decrease in production and support costs related to headcount reductions, favorable foreign exchange rates and cost saving initiatives. This was partially offset by a $19.2 million decrease in net sales.

We provide for obsolete and non-saleable inventories based on specific identification of inventory against current demand and recent usage. The amounts charged to expense for these inventories were approximately $2.2 million, $0.3 million, and $0.2 million in fiscal years 2010, 2009, and 2008, respectively. The increased provision in fiscal year 2010 was primarily due to no longer manufacturing for certain customers that were no longer viable.

We provide warranties on certain products we sell and estimate warranty costs based on historical experience and anticipated product returns. The amounts charged to expense are determined based on an estimate of warranty exposure. The net warranty expense (recovery) was approximately $45,000, $(93,000), and $196,000 in fiscal years 2010, 2009, and 2008, respectively. Warranty expense for fiscal year 2010 is related to workmanship claims on keyboards and EMS products. The recovery in fiscal year 2009 was related to the release of a warranty claim for a specific product that was identified in fiscal year 2008. Warranty expense for fiscal year 2008 was primarily related to workmanship claims on a specific EMS product.

Gross Profit

Gross profit as a percentage of net sales was 9.6%, 7.1%, and 8.2% in fiscal years 2010, 2009, and 2008, respectively.

The 2.5 percentage point increase in gross profit as a percentage of net sales from fiscal year 2009 to 2010 was primarily the result of a $14.7 million increase in net sales, while production and support cost

19

Table of Contents

decreased by $0.3 million due to favorable foreign exchange changes, a decrease in headcount of overhead employees and severance costs incurred in fiscal year 2009 that did not recur in fiscal year 2010. This was partially offset by a $8.9 million increase in material costs. The 1.1 percentage point decrease in gross profit as a percentage of net sales from fiscal year 2008 to 2009 was the result of lower fixed cost absorption due to net sales decreasing $19.2 million. Additionally we incurred charges of approximately $1.3 million for severance charges related to cost reduction efforts during fiscal year 2009.

We took early pay discounts to suppliers that totaled approximately $364,000, $142,000, and $51,000 in fiscal years 2010, 2009, and 2008, respectively. Early pay discounts will fluctuate based on our liquidity and changes in the discounts and terms offered by our suppliers.

Changes in gross profit margins reflect the impact of a number of factors that can vary from period to period, including product mix, start-up costs and efficiencies associated with new programs, product life cycles, sales volumes, capacity utilization of our resources, management of inventories, component pricing and shortages, end market demand for customers’ products, fluctuations in and timing of customer orders, and competition within the EMS industry. These and other factors can cause variations in operating results. There can be no assurance that gross margins will not decrease in future periods.

Research, Development and Engineering

Research, development and engineering expenses (RD&E) consists principally of employee related costs, third party development costs, program materials, depreciation and allocated information technology and facilities costs. Total RD&E was $2.8 million, $2.3 million, and $2.7 million in fiscal years 2010, 2009, and 2008, respectively. As a percentage of net sales, RD&E was 1.4%, 1.2% and 1.3% in fiscal years 2010, 2009 and 2008, respectively.

The increase in RD&E expenses in fiscal year 2010 compared to fiscal year 2009 is primarily the result of higher incentive compensation expense and increased headcount. The decrease in RD&E expenses in fiscal year 2009 compared to fiscal year 2008 is the result of reduced headcount and lower incentive and bonus expenses.

Selling, General and Administrative

Selling, general and administrative expenses (SG&A) consist principally of salaries and benefits, advertising and marketing programs, sales commissions, travel expenses, provision for doubtful accounts, facilities costs, and professional services. Total SG&A expenses were $9.1 million, $8.4 million, and $8.3 million in fiscal years 2010, 2009, and 2008, respectively. As a percentage of net sales SG&A was 4.5%, 4.5%, and 4.0% in fiscal years 2010, 2009, and 2008, respectively. Approximately half of our SG&A expenses relates to salary costs of our employees.

The $0.7 million increase in SG&A expenses in fiscal year 2010 as compared to fiscal year 2009 is primarily due to a $1.6 million increase in incentive compensation expense. This was partially offset by an approximate $0.3 million decrease in salaries in addition to an approximate $0.6 million decrease in expense related to the write off of a receivable in the prior year. The increase in SG&A expenses in fiscal year 2009 compared to fiscal year 2008 is mainly attributable to foreign exchange losses on Mexican peso denominated financial assets and the addition of a sales representative which were partially offset by cost reduction efforts. Additionally, in fiscal year 2009 there was a charge of $0.6 million to provide for doubtful collection of receivables, of which $0.5 million was related to the write off of a foreign receivable.

Goodwill Impairment

We recorded an impairment charge of $765,000 during fiscal year 2009. We did not record an impairment charge during fiscal year 2010. As of July 3, 2010 and June 27, 2009, there was no goodwill recorded in the Company’s Consolidated Balance Sheet.

Interest Expense

We had net interest expense of $0.1 million, $0.6 million and $1.0 million in fiscal years 2010, 2009, and 2008, respectively. Interest expense decreased in fiscal year 2010 when compared to fiscal years 2009 and 2008 as the average balance of the revolving line of credit was lower along with a decrease in variable

20

Table of Contents

interest rates. We do not currently use derivatives to hedge interest rate risk. We often utilize short-term fixed LIBOR rates on portions of our revolving line of credit to limit the affect of interest rate volatilities.

Income Tax Provision

We had an income tax benefit of $1.4 million during fiscal year 2010 as compared to $130,000 and $261,000 tax expense in fiscal years 2009, and 2008, respectively. The income tax benefit of fiscal year 2010 is primarily related the release of the valuation allowance on our deferred tax assets related to domestic tax net operating loss carryforwards (NOLs) and foreign tax credits, partially offset by the recognition of domestic deferred tax liabilities for an unremitted portion of foreign and the change of applicable tax regimes in Mexico.

Due to increased profitability, revenue growth, and new customer programs, we have determined that a valuation allowance against our domestic NOLs is not longer required. We anticipate that we will fully utilize our domestic NOLs prior to their expiration. In addition, we reviewed our requirements for liquidity domestically to fund our revenue growth and to look for potential future acquisitions. We have changed our previous assessments of being indefinitely reinvested and now anticipate repatriating a portion of our unremitted foreign earnings. The associated taxes and potential foreign tax credits are included in the income tax benefit that was realized during fiscal year 2010. The tax provision in fiscal years 2009 and 2008 is primarily related to income taxes in China and Mexico. For further information on taxes please review footnote 7 of the “Notes to Consolidated Financial Statements”.

International Subsidiaries

We offer customers a complete global manufacturing solution. Our facilities provide our customers the opportunity to have their products manufactured in the facility that best serves specific cost, product manufacturing, and distribution needs. The locations of active foreign subsidiaries are as follows:

| • | Key Tronic Juarez, SA de CV owns an SMT, assembly and molding facility, and three assembly and storage facilities in Juarez, Mexico. This subsidiary is primarily used to support our U.S. operations. |

| • | Key Tronic Reynosa, SA de CV leases manufacturing and warehouse facilities in Reynosa, Mexico. This subsidiary is used exclusively to manufacture products for one EMS customer. We anticipate that this particular subsidiary will cease its operations during fiscal year 2011, as its one EMS customer will no longer be needing manufacturing services. |

| • | Key Tronic Computer Peripherals (Shanghai) Co., Ltd. leases a facility with SMT and assembly capabilities in Shanghai, China, which began operations in 1999. Its primary function is to provide EMS services for export; however, it is also currently manufacturing certain electronic keyboards. |

Foreign sales (based on shipping instructions) from our worldwide operations, including domestic exports, were $35.7 million, $20.9 million, and $11.4 million in fiscal years 2010, 2009, and 2008, respectively. Products and manufacturing services provided by our subsidiary operations are sold to customers directly by the parent company. Key Tronic Computer Peripherals (Shanghai) Co., Ltd., our subsidiary in Shanghai, China, had only minimal sales to customers in China during the past three fiscal years.

Capital Resources and Liquidity

Cash flows provided by operating activities were $3.7 million in fiscal year 2010 as compared to $10.0 million provided by operating activities in fiscal year 2009 and $(0.7) million used in fiscal year 2008.

The $6.3 million decrease in cash provided by operating activities in fiscal year 2010 as compared with fiscal year 2009 was primarily due to an increase in trade receivables and inventory, partially offset by an increase in accounts payable. Trade receivables increased by $10.1 million as a result of the increase in sales that occurred during the fourth quarter of fiscal year 2010. The $7.5 million increase in inventory was attributable to new customer programs and increasing lead times on certain components which led to some scheduled shipments not being shipped by the end of the fiscal year. We purchase inventory based on customer forecasts and orders and expected lead times, and when those forecasts cannot be met or changes are made to lead times, inventory can increase. The $10.5 million increase in accounts payable was primarily driven by the increase in inventory and extending payment terms during fiscal year 2010.

21

Table of Contents

Accounts payable fluctuates with changes in inventory levels, volume of purchases, and negotiated supplier terms.

The $10.7 million increase in cash provided by operating activities in fiscal year 2009 as compared to fiscal year 2008 was primarily due to a decrease in trade receivables and inventory. Trade receivables and inventory decreased by $10.5 million and $5.3 million, respectively, during fiscal year 2009, partially offset by a $10.8 million decrease in accounts payable. These decreases are the result of lower sales in the fourth quarter of fiscal year 2009 as compared to fiscal year 2008 and a concerted effort to reduce our inventory and align it with our current level of business.

Cash used in investing activities includes capital expenditures and proceeds from the sale of property and equipment. Capital expenditures were $3.4 million, $1.9 million, and $1.2 million in fiscal years 2010, 2009, and 2008, respectively. Our capital expenditures are primarily for purchases of manufacturing assets to support our operations in Spokane Valley, Washington, Mexico and China. The increase in capital expenditures for fiscal year 2010 as compared to fiscal year 2009 was primarily related to the purchase of a manufacturing facility and to a lesser extent the increased investment in manufacturing equipment to support the requirements of our growing customer base and sales. Capital expenditures increased for fiscal year 2009 as compared to fiscal year 2008 as we invested in manufacturing equipment to support the requirements of new customers.

Our primary financing activity in fiscal years 2010, 2009, and 2008 was borrowing and repayment under our revolving line of our credit facility. Our credit agreement with Wells Fargo Bank N.A. provides a revolving line of credit facility of up to $20 million, subject to availability. The agreement specifies that the proceeds of the revolving line of credit be used primarily for working capital and general corporate purposes of the Company and its subsidiaries. The outstanding balance under the credit facility was $1.6 million as of July 3, 2010. We had availability to borrow an additional $18.4 million under the Wells Fargo line of credit and we were in compliance with our loan covenants.

Our cash requirements are affected by the level of current operations and new EMS programs. We believe that projected cash from operations, funds available under the revolving credit facility and leasing capabilities will be sufficient to meet our working and fixed capital requirements for the foreseeable future.

Contractual Obligations and Commitments

In the normal course of business, we enter into contracts which obligate us to make payments in the future.

The table below sets forth our significant future obligations by fiscal year:

Payments Due by Fiscal Year (in thousands)

| Total | 2011 | 2012 | 2013 | 2014 | 2015 | Thereafter | |||||||||||||||

| Wells Fargo Bank N.A. revolving loan (1) |

$ | 1,554 | $ | 1,554 | $ | — | $ | — | $ | — | $ | — | $ | — | |||||||

| Operating leases (2) |

9,831 | 2,819 | 1,251 | 772 | 763 | 762 | 3,464 | ||||||||||||||

| Short-term note (3) |

671 | 671 | |||||||||||||||||||

| Purchase orders (4) |

|||||||||||||||||||||

| (1) | The terms of the Wells Fargo Bank N.A. revolving loan are discussed in the consolidated financial statements at Note 4, “Long-Term Debt”. As of July 3, 2010 we were in compliance with our loan covenants. Breaching these covenants could have resulted in a material impact on our operations or financial condition. |

| (2) | We maintain vertically integrated manufacturing operations in Mexico and Shanghai, China. Such operations are heavily dependent upon technically superior manufacturing equipment including molding machines in various tonnages, SMT lines, clean rooms, and automated insertion, and test equipment for the various products we are capable of producing. In addition, |

22

Table of Contents

| we lease some of our administrative and manufacturing facilities. A complete discussion of properties can be found in Part 1, Item 2 at “Properties”. Leases have proven to be an acceptable method for us to acquire new or replacement equipment and to maintain facilities with a minimum impact on our short term cash flows for operations. Amounts presented above include interest and principal, if applicable. |

| (3) | See Note 3 to Consolidated Financial Statements for additional discussion related to building and land purchase during the fourth quarter of fiscal year 2010. |

| (4) | As of July 3, 2010, we had open purchase order commitments for materials and other supplies of approximately $86.5 million. Included in the open purchase orders are various blanket orders for annual requirements. Actual needs under these blanket purchase orders fluctuate with our manufacturing levels. In addition, we have contracts with our customers that minimize our exposure to losses for material purchased within lead-times necessary to meet customer forecasts. Purchase orders generally can be cancelled without penalty within specified ranges that are determined in negotiations with our suppliers. These agreements depend in part on the type of materials purchased as well as the circumstances surrounding any requested cancellations. |

In addition to the cash requirements presented above, we have various other accruals which are not included in the table above. We owe our suppliers approximately $24.1 million for accounts payable and shipments in transit at the end of the fiscal year. We generally pay our suppliers in a range from 30 to 120 days depending on terms offered. These payments are financed by operating cash flows and our revolving line of credit.

We believe that cash flows generated from operations, leasing facilities, and funds available under the revolving credit facility will satisfy cash requirements for a period in excess of 12 months and into the foreseeable future.

Critical Accounting Policies and Estimates

Preparation of our consolidated financial statements requires management to make estimates and assumptions that affect the reported amount of assets, liabilities, revenues and expenses. Note 1 to our consolidated financial statements describes the significant accounting policies used in the preparation of our consolidated financial statements. Management believes the most complex and sensitive judgments, because of their significance to our consolidated financial statements, result primarily from the need to make estimates about effects of matters that are inherently uncertain. The most significant areas involving management judgments are described below. Actual results in these areas could differ from management’s estimates.

Inactive, Obsolete, and Surplus Inventory Reserve

We reserve for inventories that we deem inactive, obsolete or surplus. This reserve is calculated based upon the demand for the products that we produce. Demand is determined by expected sales or customer forecasts. If expected sales do not materialize, then we would have inventory in excess of our reserves and would have to charge the excess against future earnings. In the case where we have purchased material based upon a customer’s forecast, we are usually covered by lead-time assurance agreements with each customer. These contracts state that the financial liability for material purchased within agreed upon lead-time and based upon the customer’s forecasts, lies with the customer. If we purchase material outside the lead-time assurance agreement and the customer’s forecasts do not materialize or if we have no lead-time assurance agreement for a specific program, we would have the financial liability and may have to charge inactive, obsolete or surplus inventory against earnings.

Allowance for Doubtful Accounts

We value our accounts receivable net of an allowance for doubtful accounts of $111,000 at July 3, 2010 and June 27, 2009. This allowance is based on estimates of the portion of accounts receivable that may not be collected in the future. The estimates used are based primarily on specific identification of potentially uncollectible accounts. Such accounts are identified using publicly available information in

23

Table of Contents

conjunction with evaluations of current payment activity. However, if any of our customers were to develop unexpected and immediate financial problems that would prevent payment of open invoices, we could incur additional and possibly material expenses that would negatively impact earnings.

Accrued Warranty

An accrual is made for expected warranty costs, with the related expense recognized in cost of goods sold. We review the adequacy of this accrual quarterly based on historical analysis and anticipated product returns and rework costs. As we have made the transition from manufacturing primarily keyboards to primarily EMS products, our exposure to warranty claims has declined significantly. Our warranty period for keyboards is generally longer than that for EMS products. We only warrant materials and workmanship on EMS products, and we do not warrant design defects for EMS customers.

Income Taxes