Attached files

| file | filename |

|---|---|

| 8-K - 8-K - CYS Investments, Inc. | d820737d8k.htm |

Kevin

Grant Chief Executive Officer

Investment Outlook

Banking and Financial Services Conference

November 13, 2014

EXHIBIT 99.1 |

Forward-Looking Statements

This presentation contains forward-looking statements, within the meaning of Section 27A

of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange

Act of 1934, as amended, that are based on management’s beliefs and assumptions, current

expectations, estimates and projections. Such statements, including information relating to

the Company’s expectations for distributions, availability and cost of financing,

scalability of management, market conditions, monetary policy, return on equity, the yield curve, the

economy, interest expense, affordability of housing, movements in interest rates,

governmental actions, the performance of the Company’s target assets, the impact

of current Federal Reserve voters on certain policies of the Federal Reserve, the policy views of central banks, and

the size of the mortgage market are not considered historical facts and are considered

forward-looking information under the federal securities

laws.

This

information

may

contain

words

such

as

“believes,”

“plans,”

“expects,”

“intends,”

“estimates”

or

similar

expressions.

This information is not a guarantee of the Company’s future performance and is subject

to risks, uncertainties and other important factors that could cause the

Company’s actual performance or achievements to differ materially from those expressed or implied by this forward-

looking information and include, without limitation, changes in the market value and yield of

our assets, changes in interest rates and the yield

curve,

net

interest

margin,

return

on

equity,

availability

and

terms

of

financing

and

hedging,

the

likelihood

that

proposed

legislation

is

made

law

and

the

anticipated

impact

thereof,

actions

by

the

U.S.

government

or

any

agency

thereof,

including

the

Federal

Reserve,

and

the

effects of such actions and various other risks and uncertainties related to our business and

the economy, some of which are described in our

filings

with

the

SEC.

Given

these

uncertainties,

you

should

not

rely

on

forward-looking

information.

The

Company

undertakes

no

obligations to update any forward-looking information, whether as a result of new

information, future events or otherwise. 2 |

CYS Overview

Focus on Cost

Efficiency

Target Assets

Agency Residential Mortgage Backed Securities

A Real Estate Investment Trust Formed in January 2006

Ample Financing

Sources

Financing lines with 45

lenders

Swap agreements with 18 counterparties

Dividend Policy

Self managed: highly scalable

Senior

Management

Kevin Grant, CEO, President, Chairman

Frances Spark, CFO

Company intends to distribute all or substantially all of its REIT

taxable income

3 |

Agency MBS Market

Continues To See Strong Demand 15 Year: Hedged vs. Unhedged

15 Year Fixed Hedged with Swaps: April 2009 –

November 2014

15

Year

Hedged

(i)

15

Year

Unhedged

(ii)

Borrow Short

Invest Long

November 7, 2014

4

Source: Bloomberg.

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

Note: Spreads calculated as: (i) 15 year CC Index = 50% 4 year swap, and (ii) 15

year Current Coupon Index |

Agency MBS Market

Continues To See Strong Demand 30 Year: Hedged vs. Unhedged

Source: Bloomberg

30 Year Fixed Hedged with Swaps: April 2009 –

November 2014

Borrow Short

Invest Long

30 Year Hedged

30 Year Unhedged

November 7, 2014

5

0.75

1.25

1.75

2.25

2.75

3.25

3.75

4.25

4.75

5.25

Note: Spread calculated as: (i) 30 year CC Index - 90% 5 year swap

|

•

Volatility in the Cap/Floor

Markets Hit a Low in July 2013

30 Yr MBS -

15 Yr MBS Spread

7 Yr Cap/Floor Implied Vol

November 2012 –

November 2014

April 2012 –

November 2014

•

30 Year MBS Have Cheapened

Meaningfully Relative to 15 Year

MBS

5 Year Swap vs. Fed Funds

January 2005 –

November 2014

Yield Curve

Creates positive carry

Very low cost of financing

Good ROE

Hedge flexibility very important

Fed still fighting deflation

End of QE Poses New Risks and New Opportunities

6

Source: Bloomberg

November 7, 2014

November 7, 2014

November 7, 2014

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

30.0

35.0

40.0

45.0

50.0

55.0

60.0

65.0

70.0

75.0 |

Global Ten Year

Yields: Is U.S. Growth Out of Sync with Rest of World?

GDBR10

(1.185)

USGG10YR

0.338

GCAN10YR

(0.232)

GJGB10

(0.520)

Government Ten Year Yields

UK, US, Canada, Germany, Japan

August 2011 –

November 2014

Source: Bloomberg, November 7, 2014

7

GBTPGR10

(0.031)

0.00

0.50

1.00

1.50

2.00

2.50

3.00 |

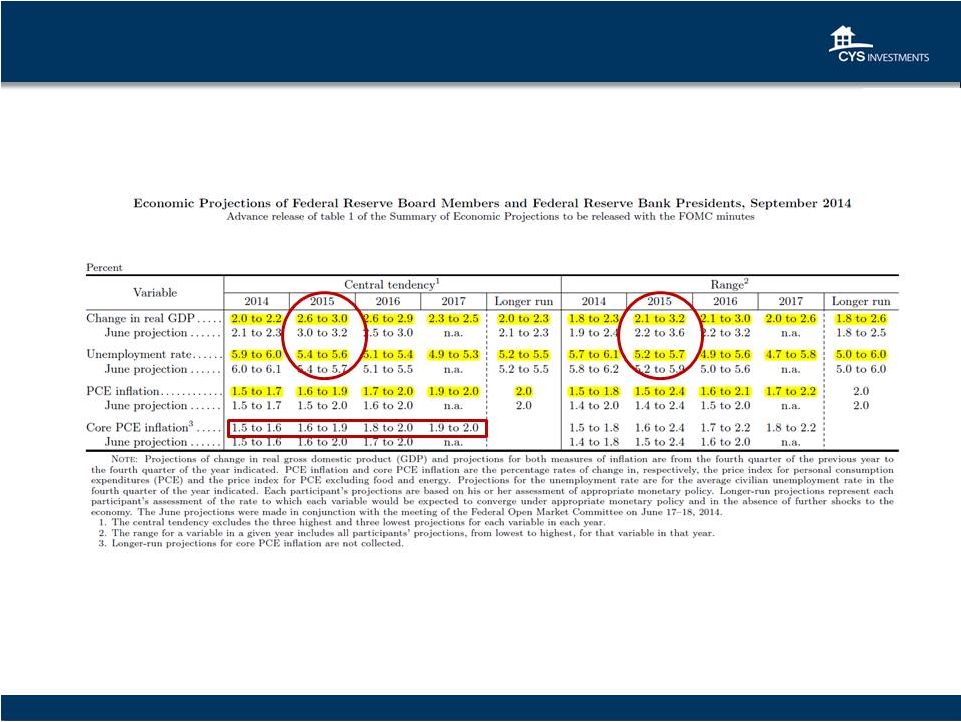

Actual Economic

Performance: Sluggish vs. Fed Projections

8

Source: Board of Governors of the Federal Reserve, September 17, 2014

|

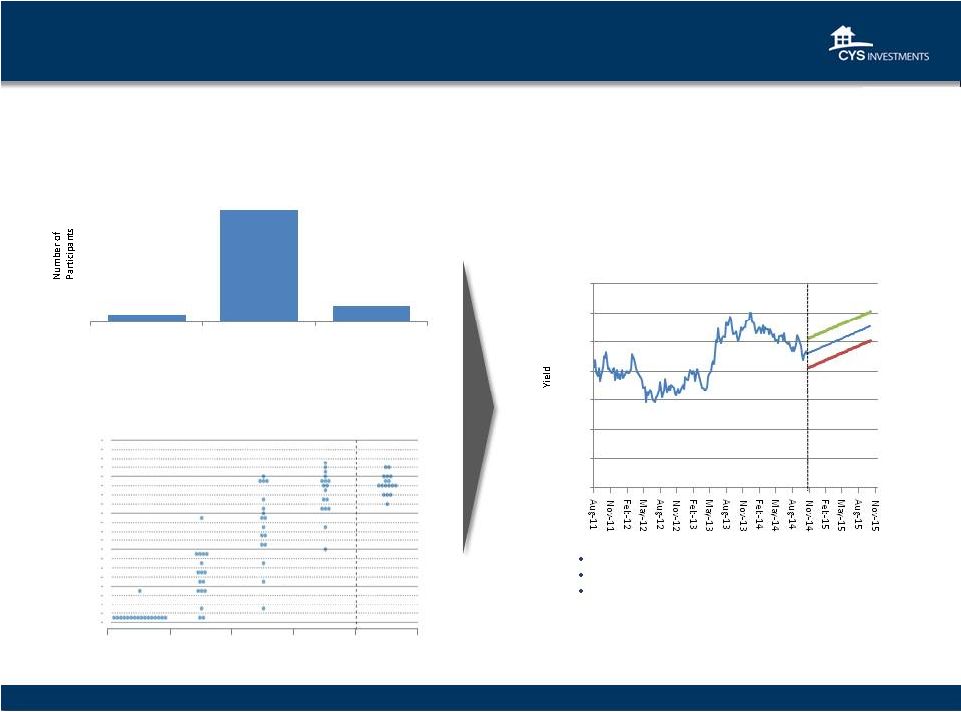

Appropriate

Timing of Policy Firming

•

Creates Significant Headwinds for the Economy

•

Housing Will Struggle

•

Corporate Interest Expense will rise

Overview of FOMC Participants Assessments of

Appropriate Monetary Policy

Can the Economy Withstand the

Implied Path of 10 Year UST?

Transition to a Normalized Yield Curve:

Will the Fed Push Out –

or Pull In -

Forward Rate Guidance?

9

Ten Year Treasury

August 2011 -

November 2014

and Implied Projection

+25

-25

%

%

2014

2015

2016

2017

1.0

2.0

3.0

4.0

5.0

0.0

1.5

2.5

3.5

4.5

0.5

Appropriate Pace

of Policy Firming

Target Fed Funds Rate at Year End

Longer Run

Source: Federal Reserve September 2014 Forecast, Bloomberg, CYS

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1

14

2

2014

2015

2016 |

2014-16 Fed

Voters: New Perspectives, Changing Outlooks

Powell

Dallas:

Fisher

Minneapolis:

Kocherlakota

Philadelphia:

Plosser

Hawkish

Dovish

Neutral

Yellen

Raskin’s Successor

Board of

Governors

New York:

Dudley

Chicago:

Evans

Richmond:

Lacker

Atlanta:

Lockhart

San Francisco:

Williams

Fischer

Brainard

Tarullo

Cleveland:

Mester

Stein’s Successor

New York:

Dudley

10

New York:

Dudley

Cleveland:

Mester

Boston:

Rosengren

Kansas City:

George

St. Louis:

Bullard

2014

Voters

2015

Voters

2016

Voters

Source: federalreserve.gov, Barclays, Macroeconomic Advisers, LLC, Bank of America

Merrill Lynch, Bloomberg, Wall Street Journal, Indiana University, Marketwatch, Thomson Reuters, Federal Reserve Bank of Atlanta, Federal Reserve

Bank of Chicago, Federal Reserve Bank of Cleveland, Maryland Consumer Rights Coalition, Boston

Globe, Businessweek, Newsweek, Washington Post, CNBC. |

Central

Banks: Decidedly More Accommodative -

Focus on Global Deflation Risk

Draghi

EU

Hawkish

Dovish

Neutral

Xiaochuan

China

Xiaochuan

China

Tombini

Brazil

Tombini

Brazil

Australia

Stevens

Australia

Stevens

New Zealand

Wheeler

New Zealand

Wheeler

Kuroda

Japan

Canada

Poloz

Rajan

India

Kuroda

Japan

Carney

UK

Yellin

USA

11 |

GSE Reform

“Headway” Legislative

Level of

GSE

Credit Risk

Proposal

Government Involvement

Implication

Sharing

Status

Corker-Warner Bill

Limited: Only under

catastrophic scenarios where

losses on a pool of mortgages

exceeds 10%

Completely wound down over

5 years

10% first-loss piece is sold to

private entities

Corker-Warner under committee

discussion but not yet put to vote.

Either may become the front runner

from the Senate side but both will

likely have private capital in the

first loss place with several

mechanisms for risk sharing

Senate Banking Committee voted

in favor of the bill 13-9 on May 15.

Insufficient support to allow the

bill to be brought to the Senate

floor for debate/vote.

Johnson -

Crapo Bill

Based on Corker-Warner,

limited: only on scenarios

where losses on a pool of

mortgages exceeds a 10%

private loss position.

GSE’s wound down over 5 year

period, replaced by FMIC.

Similar to Corker-Warner, 10%

first-loss piece is sold to private

entities.

PATH Act

Very limited: dissolves the

GSEs completely and reduces

the scope of the FHA/VA

guarantee

Placed into receivership and

completely liquidated with

Initially, a 10% risk-sharing

program on new GSE and FHA

business, although private

market securitization is intended

eventually to replace GSEs

No news. In early 2013, the Path Act

seemed to be the clear front-runner

on the House side. The final housing

finance reform, if it happens, could

be a compromise between the PATH

Act and whatever comes out of the

Senate

Delaney-Carney-Himes

Limited: Ginnie Mae is

required to provide an explicit

government guarantee once

the 5% risk slice is eroded

when one of the private

monoline insurers defaults

GSEs will be slowly wound

down and eventually converted

into private reinsurers with

limited capacities to take on

mortgage credit risk

5% first-loss piece on each new

Ginnie Mae securitization, as

well as a 10% pro-rata risk slice

on the top 95% of each Ginnie

Mae securitization

Source: Barclays, CYS

12 |

Economic

Recovery Below Normal Pace U.S. Regular Conventional Gas Price

$ per gal

Updated: 2014-11-03

Capacity Utilization: Manufacturing

Updated: 2014-10-16

Civilian Unemployment Rate

Updated: 2014-11-07

CPI-U All Items

Updated: 2014-10-22

Total Nonfarm Private Payroll Employment

Updated: 2014-11-05

Total Unemployed + All Marginally Attached + Total

Employed Part Time for Economic Reasons

Updated: 2014-11-07

Source: Federal Reserve Bank of St. Louis

13 |

Housing Finance

Has Not Rebounded Source: St Louis Fed, www.census.gov

14

New Homes

Existing Homes

Homeownership Rate

Seasonally Adjusted Homeownership Rate

Recession

1995 1997

1999 2001 2003 2005 2007

2009 2011 2013 2014

70

69

68

67

66

65

64

63

Share of Government Guaranteed Mortgages

New and Existing Homes Months of Supply

Home Ownership Rate

January 1999 – present

1990 – 2013

January 1985 - present (%)

|

Mortgage Market

Shrinkage Likely to Continue 15

3.0%

3.5%

4.0%

Single Family

Mortgage Origination Volume

2000-2015E

2000

2005

2010

2012

2013

Est.

2014

Fcst.

2015

Fcst.

1,000

2,000

3,000

4,000

Mortgage Debt Outstanding

2007-2014

Mortgage Debt Outstanding

Growth Rate

Source: http://www.federalreserve.gov/econresdata/releases/mortoutstand/current.htm

9,000

9,500

10,000

10,500

11,000

11,500

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Refinance Originations

1.9T

1.1T

1.3T

Residential Mortgage Debt Decline Driven By:

1.

Home prices now reset lower

2.

Delevering Consumers/Homeowners

3.

Psychology of lower leverage

4.

Low volume of new and existing home sales

5.

All-cash home purchase transactions, and higher downpayments

6.

Scheduled principal payments

7.

High percentage of cash-in refi’s versus cash-out refi’s.

8.

QM Rules Restrictive

Home Purchase Originations |

Economics of

Forward Purchase Source: Bloomberg, November 7, 2014

16 |

1

As of 9/30/14

2

Annualized dividend yield is calculated using the stock price at the quarter end.

$14.5B Agency RMBS and U.S. Treasuries Portfolio

CYS Common Stock Dividends

September

2009

-

September

2014

CYS

Agency

RMBS

and

U.S.

Treasury

Portfolio

1

Portfolio Composition and Dividends

17

20 Year

Fixed Rate:

1%

30 Year

Fixed Rate: 36%

Agency

Hybrid

ARMs: 13%

U.S.

Treasuries:

4%

15 Year

Fixed Rate: 46%

Dividend

Special Dividend

Annualized

Dividend

Yield

(2)

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

$0.70

$0.80

$0.90

$1.00

Note: the December 2012 dividend was composed of $0.40 quarterly cash dividend, and $0.52

special cash dividend.

|

Portfolio

Characteristics 18

Face Value

Fair Value

Weighted Average

Asset Type

(in thousands)

Cost/Face

Fair Value/Face

Yield

(1)

Coupon

CPR

(2)

15 Year Fixed Rate

$

6,422,985

$

6,670,579

$

102.89

$

103.85

2.20

%

3.17

%

8.5%

20 Year Fixed Rate

71,568

78,005

102.98

108.99

1.34

%

4.50

%

15.4%

30 Year Fixed Rate

4,987,788

5,267,793

105.13

105.61

2.97

%

4.02

%

5.9%

Hybrid ARMs

(3)

1,857,254

1,901,530

103.48

102.38

1.94

%

2.57

%

15.5%

U.S. Treasury Securities

560,000

556,150

99.33

99.31

1.77

%

1.63

%

NA

Total

$

13,899,595

$

14,474,057

$

103.63

$

104.13

2.42

%

3.34

%

9.2%

CYS Agency RMBS and U.S. Treasury Portfolio Characteristics*

*

As of 9/30/14

(1)

This is a forward yield and is calculated based on the cost basis of the security at

September 30, 2014.

(2)

CPR is a method of expressing the prepayment rate for a mortgage pool that assumes that a

constant fraction of the remaining principal is prepaid each month or year.

Specifically, the constant prepayment rate is an annualized version of the prior three month prepayment

rate for those bonds held at September 30, 2014. Securities with no prepayment history are

excluded from this calculation.

(3)

The weighted average months to reset of our Hybrid ARM portfolio was 59.8 at September30,

2014. Months to reset is the number of months remaining before the fixed rate on a

Hybrid ARM becomes a variable rate. At the end of the fixed period, the variable rate will be

determined by the margin and the pre-specified caps of the Hybrid ARM and will reset

annually. |

(1)

Drop Income is a component of our net realized and unrealized gain (loss) on investments on

our consolidated statements of operations, and is therefore excluded from Core

Earnings. (2)

Core Earnings is defined as net income (loss) available to common shares excluding net

realized gain (loss) on investments, net unrealized gain (loss) on investments, net

realized gain (loss) on termination of swap and cap contracts and net unrealized gain (loss) on swap and cap

contracts.

Financial Information

19

Income Statement Data

(In thousands, except per share numbers)

Sept. 30, 2014

June 30, 2014

Total interest income

77,132

71,978

Total interest expense

33,446

27,039

Net interest income

43,686

44,939

Other income (loss):

Net realized gain (loss) on investments

40,470

33,118

Net unrealized gain (loss) on investments

(112,085)

157,479

Net realized gain (loss) on termination of swap and cap contracts

(6,004)

Net unrealized gain (loss) on swap and cap contracts

58,909

(65,181)

Other income

50

50

Total other income (loss)

(12,656)

119,462

Total expenses

6,045

6,020

Net income (loss)

24,985

$

158,381

$

Dividends on preferred stock

(5,203)

(5,203)

Net income (loss) available to common shares

19,782

$

153,178

$

Net income (loss) per common share basic & diluted

0.12

$

0.95

$

Drop income per common share (diluted)

(1)

0.11

$

0.12

$

Core Earnings per common share (diluted)

(2)

0.20

$

0.21

$

Distributions per common share

0.30

$

0.32

$

Non-GAAP Measure/Reconciliation (in 000's)

NET INCOME (LOSS) AVAILABLE TO COMMON SHARES

$19,782

$153,178

Net realized (gain) loss on investments

(40,470)

(33,118)

Net unrealized (gain) loss on investments

112,085

(157,479)

Net realized (gain) loss on termination of swap and cap contracts

-

6,004

Net unrealized (gain) loss on swap and cap contracts

(58,909)

65,181

Core Earnings

$32,488

$33,766

Three Months Ended |

Financial

Information 20

1)

The average settled Debt Securities is calculated by averaging the month end cost basis of

settled Debt Securities during the period.

2)

The average total Debt Securities is calculated by averaging the month end cost basis of total

Debt Securities during the period.

3)

The average repurchase agreements are calculated by averaging the month end repurchase

agreements balance during the period. 4)

The average Debt Securities liabilities are calculated by adding the average month end

repurchase agreements balance plus average unsettled Debt Securities during the period.

5)

The average stockholders' equity is calculated by averaging the month end stockholders' equity

during the period. 6)

The average common shares outstanding are calculated by averaging the daily common shares

outstanding during the period.

7)

The leverage ratio is calculated by dividing (i) the Company's repurchase agreements balance

plus payable for securities purchased minus receivable for securities sold by (ii) stockholders' equity.

8)

The average yield on Debt Securities for the period is calculated by dividing total interest

income by average settled Debt Securities. 9)

The average yield on total Debt Securities including Drop Income for the period is calculated

by dividing total interest income plus Drop Income by average total Debt Securities.

10)

The average cost of funds for the period is calculated by dividing repurchase agreement

interest expense by average amount of repurchase agreements outsending for the period.

11)

The average cost of funds and hedge for the period is calculated by dividing interest expense

by average repurchase agreements.

12)

The adjusted average cost of funds and hedge for the period is calculated by dividing interest

expense by average Debt Securities liabilities. 13)

The interest rate spread net of hedge for the period is calculated by subtracting average cost

of funds and hedge from average yield on settled Debt Securities.

14)

The interest rate spread net of hedge including Drop Income for the period is calculated by

subtracting adjusted average cost of funds and hedge from average yield on total Debt Securities

including Drop Income.

15)

The operating expense ratio for the period is calculated by dividing operating expenses by

average stockholders' equity. The table above includes calculations of the Company’s Agency RMBS and U.S.

Treasury Securities portfolio (“Debt Securities”) * All

percentages are annualized. (In thousands, except per share numbers)

Three Months Ended

Key Balance Sheet Metrics

Sept. 30, 2014

June 30, 2014

Average settled Debt Securities

(1)

$ 11,837,201

$ 11,599,873

Average total Debt Securities

(2)

$ 14,138,849

$ 13,711,749

Average repurchase agreements

(3)

$ 10,189,360

$ 9,981,049

Average Debt Securities liabilities

(4)

$ 12,491,008

$ 12,092,925

Average stockholders' equity

(5)

$ 1,937,700

$ 1,916,575

Average common shares outstanding

(6)

Leverage ratio (at period end)

(7)

6.63:1

6.35:1

Key Performance Metrics* (in %)

Average yield on settled Debt Securities

(8)

2.61

2.48

Average yield on total Debt Securities including drop income

(9)

2.67

2.67

Average cost of funds

(10)

0.30

0.30

Average cost of funds and hedge

(11)

1.31

1.08

Adjusted average cost of funds and hedge

(12)

1.07

0.89

Interest rate spread net of hedge

(13)

1.30

1.40

Interest rate spread net of hedge including drop income

(14)

1.60

1.78

Operating expense ratio

(15)

1.25

1.26 |

Kevin

Grant Chief Executive Officer

Investment Outlook

Banking and Financial Services Conference

November 13, 2014 |