Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

June 30, 2011 For the quarterly period ended June 30, 2011

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission file number 001-33740

Cypress Sharpridge Investments, Inc.

(Exact name of registrant as specified in its charter)

| Maryland | 20-4072657 | |

| (State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) | |

| 437 Madison Avenue, 33rd Floor New York, New York |

10022 | |

| (Address of principal executive offices) | (Zip Code) | |

(212) 612-3210

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. Check one:

| Large accelerated filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

| Class |

Outstanding at July 21, 2011 | |

| Common Stock ($0.01 par value) |

82,591,404 |

Table of Contents

| Page | ||||||

| PART I. |

Financial Information | |||||

| Item 1. |

Financial Statements | 1 | ||||

| Item 2. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations | 23 | ||||

| Item 3. |

Quantitative and Qualitative Disclosures about Market Risk | 38 | ||||

| Item 4. |

Controls and Procedures | 42 | ||||

| PART II. |

Other Information | |||||

| Item 1. |

Legal Proceedings | 42 | ||||

| Item 1A. |

Risk Factors | 42 | ||||

| Item 2. |

Unregistered Sales of Equity Securities and Use of Proceeds | 42 | ||||

| Item 3. |

Defaults Upon Senior Securities | 42 | ||||

| Item 4. |

(Removed and Reserved). | 42 | ||||

| Item 5. |

Other Information | 42 | ||||

| Item 6. |

Exhibits | 42 | ||||

| SIGNATURES | 43 | |||||

Table of Contents

| Item 1. | Financial Statements |

CYPRESS SHARPRIDGE INVESTMENTS, INC.

CONDENSED STATEMENTS OF ASSETS AND LIABILITIES (UNAUDITED)

| (In thousands, except per share numbers) | June 30, 2011 | December 31, 2010* | ||||||

| ASSETS: |

||||||||

| Investments in securities, at fair value (including pledged assets of $8,039,662 and $3,671,582, respectively) |

$ | 8,859,410 | $ | 6,331,048 | ||||

| Interest rate swap contracts, at fair value |

— | 9,113 | ||||||

| Interest rate cap, at fair value |

20,429 | 30,984 | ||||||

| Cash and cash equivalents |

1,092 | 1,510 | ||||||

| Receivable for securities sold |

400,849 | — | ||||||

| Interest receivable |

27,902 | 16,183 | ||||||

| Other assets |

829 | 429 | ||||||

| Total assets |

9,310,511 | 6,389,267 | ||||||

| LIABILITIES: |

||||||||

| Repurchase agreements |

7,548,091 | 3,443,843 | ||||||

| Interest rate swap contracts, at fair value |

49,151 | 9,757 | ||||||

| Payable for securities purchased |

626,476 | 2,234,401 | ||||||

| Distribution payable |

49,550 | — | ||||||

| Accrued interest payable (including accrued interest on repurchase agreements of $2,181 and $1,084, respectively) |

15,674 | 9,412 | ||||||

| Related party management fee payable |

1,125 | 800 | ||||||

| Accrued expenses and other liabilities |

635 | 715 | ||||||

| Total liabilities |

8,290,702 | 5,698,928 | ||||||

| Contingencies (note 8) |

||||||||

| NET ASSETS |

$ | 1,019,809 | $ | 690,339 | ||||

| Net assets consist of: |

||||||||

| Common Stock, $0.01 par value, 500,000 shares authorized (82,584 and 59,551 shares issued and outstanding, respectively) |

$ | 826 | $ | 596 | ||||

| Additional paid in capital |

1,015,816 | 739,005 | ||||||

| Retained earnings (Accumulated deficit) |

3,167 | (49,262 | ) | |||||

| NET ASSETS |

$ | 1,019,809 | $ | 690,339 | ||||

| NET ASSET VALUE PER SHARE |

$ | 12.35 | $ | 11.59 | ||||

| * | Derived from audited financial statements. |

See notes to financial statements.

1

Table of Contents

CYPRESS SHARPRIDGE INVESTMENTS, INC.

CONDENSED SCHEDULES OF INVESTMENTS

JUNE 30, 2011 (UNAUDITED)

INVESTMENTS IN SECURITIES—UNITED STATES OF AMERICA

| (In thousands) | Face Amount | Fair Value | ||||||

| Investments in Securities - 868.7%(d) |

||||||||

| Mortgage Pass-Through Agency RMBS - 866.3%(d) |

||||||||

| Fannie Mae Pools - 780.3%(d) |

||||||||

| 2.997%, due 10/1/2040(a)(b) |

$ | 52,842 | $ | 54,476 | ||||

| 3.002%, due 1/1/2041(a)(b) |

47,020 | 48,606 | ||||||

| 3.035%, due 12/1/2040(a)(b) |

181,531 | 187,809 | ||||||

| 3.100%, due 8/1/2041(b) |

35,000 | 35,984 | ||||||

| 3.100%, due 8/1/2041(b) |

15,000 | 15,422 | ||||||

| 3.205%, due 6/1/2041(a)(b) |

198,484 | 205,975 | ||||||

| 3.209%, due 11/1/2040(a)(b) |

45,228 | 46,956 | ||||||

| 3.217%, due 12/1/2040(a)(b) |

84,716 | 87,993 | ||||||

| 3.219%, due 7/1/2040(a)(b) |

45,161 | 47,018 | ||||||

| 3.241%, due 3/1/2041(a)(b) |

19,241 | 19,766 | ||||||

| 3.249%, due 4/1/2041(a)(b) |

74,024 | 76,924 | ||||||

| 3.250%, due 8/1/2041(b) |

40,000 | 41,356 | ||||||

| 3.250%, due 11/1/2040(a)(b) |

48,766 | 50,272 | ||||||

| 3.257%, due 6/1/2041(a)(b) |

59,832 | 62,186 | ||||||

| 3.264%, due 5/1/2041(a)(b) |

49,687 | 51,630 | ||||||

| 3.280%, due 8/1/2041(b) |

50,000 | 51,758 | ||||||

| 3.281%, due 6/1/2041(a)(b) |

133,944 | 139,159 | ||||||

| 3.289%, due 4/1/2041(a)(b) |

60,618 | 63,016 | ||||||

| 3.290%, due 8/1/2041(b) |

13,000 | 13,280 | ||||||

| 3.308%, due 8/1/2040(a)(b) |

43,163 | 44,823 | ||||||

| 3.326%, due 9/1/2040(a)(b) |

43,493 | 45,270 | ||||||

| 3.330%, due 8/1/2041(b) |

35,000 | 35,788 | ||||||

| 3.349%, due 9/1/2040(a)(b) |

48,385 | 50,410 | ||||||

| 3.370%, due 5/1/2041(a)(b) |

24,443 | 25,377 | ||||||

| 3.398%, due 4/1/2041(a)(b) |

49,270 | 50,993 | ||||||

| 3.402%, due 4/1/2041(a)(b) |

59,552 | 61,700 | ||||||

| 3.410%, due 8/1/2041(b) |

9,000 | 9,225 | ||||||

| 3.415%, due 6/1/2041(a)(b) |

123,557 | 127,894 | ||||||

| 3.420%, due 8/1/2041(b) |

10,000 | 10,238 | ||||||

| 3.465%, due 11/1/2040(a)(b) |

23,962 | 24,919 | ||||||

| 3.500%, due 1/1/2026(a) |

173,403 | 176,827 | ||||||

| 3.500%, due 1/1/2026(a) |

146,115 | 149,045 | ||||||

| 3.500%, due 12/1/2025(a) |

96,910 | 98,824 | ||||||

| 3.500%, due 12/1/2025(a) |

96,629 | 98,537 | ||||||

| 3.500%, due 2/1/2026(a) |

97,964 | 99,929 | ||||||

| 3.500%, due 2/1/2026(a) |

145,666 | 148,587 | ||||||

| 3.500%, due 2/1/2026(a) |

242,272 | 247,132 | ||||||

| 3.500%, due 3/1/2026(a) |

97,932 | 99,896 | ||||||

| 3.500%, due 3/1/2026(a) |

54,356 | 55,446 | ||||||

| 3.500%, due 3/1/2026(a) |

93,392 | 95,266 | ||||||

| 3.500%, due 4/1/2026(a) |

49,945 | 50,946 | ||||||

| 3.500%, due 5/1/2026(a) |

99,057 | 101,044 | ||||||

| 3.556%, due 7/1/2040(a)(b) |

17,514 | 18,266 | ||||||

| 3.568%, due 7/1/2040(a)(b) |

19,615 | 20,448 | ||||||

See notes to financial statements.

2

Table of Contents

CYPRESS SHARPRIDGE INVESTMENTS, INC.

CONDENSED SCHEDULES OF INVESTMENTS – Continued

JUNE 30, 2011 (UNAUDITED)

| Face Amount | Fair Value | |||||||

| 3.578%, due 8/1/2040(a)(b) |

$ | 45,707 | $ | 47,710 | ||||

| 3.600%, due 6/1/2041(a)(b) |

70,219 | 72,874 | ||||||

| 3.602%, due 10/1/2040(a)(b) |

56,629 | 59,153 | ||||||

| 3.602%, due 8/1/2040(a)(b) |

20,794 | 21,686 | ||||||

| 3.602%, due 8/1/2040(a)(b) |

45,514 | 47,507 | ||||||

| 3.640%, due 6/1/2041(b) |

70,838 | 73,295 | ||||||

| 3.654%, due 7/1/2040(a)(b) |

40,217 | 41,987 | ||||||

| 3.665%, due 6/1/2040(a)(b) |

17,680 | 18,481 | ||||||

| 3.668%, due 7/1/2040(a)(b) |

42,502 | 44,328 | ||||||

| 3.680%, due 8/1/2040(a)(b) |

45,168 | 47,210 | ||||||

| 3.699%, due 8/1/2040(a)(b) |

20,832 | 21,788 | ||||||

| 3.733%, due 5/1/2040(a)(b) |

39,846 | 41,759 | ||||||

| 3.737%, due 8/1/2040(a)(b) |

11,370 | 11,925 | ||||||

| 3.745%, due 9/1/2039(a)(b) |

26,663 | 27,956 | ||||||

| 3.818%, due 7/1/2040(a)(b) |

40,842 | 42,822 | ||||||

| 3.959%, due 10/1/2039(a)(b) |

34,140 | 35,878 | ||||||

| 3.976%, due 9/1/2039(a)(b) |

17,890 | 18,853 | ||||||

| 4.000%, due 1/1/2025(a) |

37,960 | 39,635 | ||||||

| 4.000%, due 1/1/2025(a) |

60,254 | 62,894 | ||||||

| 4.000%, due 1/1/2026(a) |

48,350 | 50,468 | ||||||

| 4.000%, due 1/1/2026(a) |

48,411 | 50,532 | ||||||

| 4.000%, due 10/1/2024(a) |

9,767 | 10,198 | ||||||

| 4.000%, due 10/1/2025(a) |

26,542 | 27,705 | ||||||

| 4.000%, due 10/1/2025(a) |

28,239 | 29,477 | ||||||

| 4.000%, due 10/1/2025(a) |

47,764 | 49,856 | ||||||

| 4.000%, due 10/1/2030(a) |

48,348 | 49,368 | ||||||

| 4.000%, due 10/1/2030(a) |

73,217 | 74,762 | ||||||

| 4.000%, due 10/1/2030(a) |

72,030 | 73,550 | ||||||

| 4.000%, due 10/1/2030(a) |

72,863 | 74,400 | ||||||

| 4.000%, due 11/1/2025(a) |

47,204 | 49,272 | ||||||

| 4.000%, due 11/1/2025(a) |

48,172 | 50,282 | ||||||

| 4.000%, due 11/1/2025(a) |

9,438 | 9,851 | ||||||

| 4.000%, due 12/1/2025(a) |

24,326 | 25,392 | ||||||

| 4.000%, due 12/1/2025(a) |

71,607 | 74,743 | ||||||

| 4.000%, due 12/1/2025(a) |

28,905 | 30,171 | ||||||

| 4.000%, due 12/1/2025(a) |

30,002 | 31,091 | ||||||

| 4.000%, due 12/1/2030(a) |

73,927 | 75,486 | ||||||

| 4.000%, due 2/1/2025(a) |

39,711 | 41,450 | ||||||

| 4.000%, due 2/1/2026(a) |

51,849 | 54,088 | ||||||

| 4.000%, due 2/1/2026(a) |

43,183 | 45,048 | ||||||

| 4.000%, due 2/1/2026(a) |

15,068 | 15,719 | ||||||

| 4.000%, due 2/1/2026(a) |

97,588 | 101,802 | ||||||

| 4.000%, due 3/1/2025(a) |

39,581 | 41,315 | ||||||

| 4.000%, due 3/1/2026(a) |

26,776 | 27,932 | ||||||

| 4.000%, due 3/1/2026(a) |

199,295 | 207,900 | ||||||

| 4.000%, due 3/1/2026(a) |

45,375 | 47,334 | ||||||

| 4.000%, due 3/1/2026(a) |

49,519 | 51,657 | ||||||

| 4.000%, due 4/1/2026(a) |

99,499 | 103,796 | ||||||

See notes to financial statements.

3

Table of Contents

CYPRESS SHARPRIDGE INVESTMENTS, INC.

CONDENSED SCHEDULES OF INVESTMENTS – Continued

JUNE 30, 2011 (UNAUDITED)

| Face Amount | Fair Value | |||||||

| 4.000%, due 4/1/2026(a) |

$ | 8,346 | $ | 8,706 | ||||

| 4.000%, due 4/1/2026(a) |

73,742 | 76,926 | ||||||

| 4.000%, due 4/1/2026(a) |

164,623 | 171,732 | ||||||

| 4.000%, due 4/1/2026(a) |

158,372 | 165,211 | ||||||

| 4.000%, due 5/1/2026(a) |

45,949 | 47,933 | ||||||

| 4.000%, due 5/1/2026(a) |

26,154 | 27,284 | ||||||

| 4.000%, due 5/1/2026 |

199,034 | 207,307 | ||||||

| 4.000%, due 6/1/2026(a) |

24,894 | 25,969 | ||||||

| 4.000%, due 7/1/2026 |

200,000 | 208,312 | ||||||

| 4.000%, due 9/1/2030(a) |

91,898 | 93,836 | ||||||

| 4.000%, due 9/1/2030(a) |

21,840 | 22,301 | ||||||

| 4.063%, due 6/1/2039(a)(b) |

16,724 | 17,679 | ||||||

| 4.500%, due 10/1/2024(a) |

30,857 | 32,788 | ||||||

| 4.500%, due 10/1/2024(a) |

33,217 | 35,295 | ||||||

| 4.500%, due 10/1/2024(a) |

27,760 | 29,497 | ||||||

| 4.500%, due 10/1/2030(a) |

48,817 | 51,052 | ||||||

| 4.500%, due 11/1/2024(a) |

41,908 | 44,529 | ||||||

| 4.500%, due 11/1/2030(a) |

49,505 | 51,771 | ||||||

| 4.500%, due 2/1/2026(a) |

54,320 | 57,718 | ||||||

| 4.500%, due 3/1/2024(a) |

13,525 | 14,371 | ||||||

| 4.500%, due 3/1/2025(a) |

46,168 | 49,027 | ||||||

| 4.500%, due 3/1/2026(a) |

71,395 | 75,906 | ||||||

| 4.500%, due 4/1/2025(a) |

30,604 | 32,499 | ||||||

| 4.500%, due 4/1/2030(a) |

27,828 | 29,101 | ||||||

| 4.500%, due 5/1/2023(a) |

22,784 | 24,223 | ||||||

| 4.500%, due 5/1/2030(a) |

46,127 | 48,238 | ||||||

| 4.500%, due 6/1/2024(a) |

16,394 | 17,420 | ||||||

| 4.500%, due 6/1/2025(a) |

29,954 | 31,809 | ||||||

| 4.500%, due 8/1/2024(a) |

13,244 | 14,072 | ||||||

| 4.500%, due 9/1/2024(a) |

19,283 | 20,489 | ||||||

| 5.000%, due 4/1/2041(a) |

244,429 | 260,128 | ||||||

| 5.000%, due 5/1/2041 |

243,845 | 259,506 | ||||||

| 5.000%, due 6/1/2041(a) |

100,000 | 106,341 | ||||||

| Total Fannie Mae Pools |

7,659,850 | 7,957,778 | ||||||

| Freddie Mac Pools - 70.8%(d) |

||||||||

| 3.059%, due 1/1/2041(a)(b) |

42,612 | 44,128 | ||||||

| 3.217%, due 12/1/2040(a)(b) |

47,438 | 49,372 | ||||||

| 3.247%, due 1/1/2041(a)(b) |

48,739 | 50,109 | ||||||

| 3.247%, due 2/1/2041(a)(b) |

40,908 | 42,035 | ||||||

| 3.259%, due 12/1/2040(a)(b) |

47,181 | 48,939 | ||||||

| 3.500%, due 4/1/2026(a) |

196,754 | 200,731 | ||||||

| 3.660%, due 6/1/2041(a)(b) |

50,419 | 52,558 | ||||||

| 4.000%, due 10/1/2025(a) |

66,713 | 69,583 | ||||||

| 4.500%, due 1/1/2025(a) |

30,259 | 32,095 | ||||||

| 4.500%, due 12/1/2024(a) |

13,469 | 14,286 | ||||||

| 4.500%, due 12/1/2024(a) |

13,246 | 14,050 | ||||||

| 4.500%, due 2/1/2025(a) |

40,351 | 42,774 | ||||||

| 4.500%, due 5/1/2025(a) |

17,892 | 18,967 | ||||||

See notes to financial statements.

4

Table of Contents

CYPRESS SHARPRIDGE INVESTMENTS, INC.

CONDENSED SCHEDULES OF INVESTMENTS – Continued

JUNE 30, 2011 (UNAUDITED)

| Face Amount | Fair Value | |||||||

| 4.500%, due 7/1/2024(a) |

$ | 40,349 | $ | 42,797 | ||||

| Total Freddie Mac Pools |

696,330 | 722,424 | ||||||

| Ginnie Mae Pools - 15.2%(d) |

||||||||

| 3.500%, due 7/20/2040(a)(b) |

81,077 | 84,934 | ||||||

| 3.500%, due 7/20/2040(a)(b) |

47,812 | 50,087 | ||||||

| 4.000%, due 1/20/2040(a)(b) |

19,009 | 20,046 | ||||||

| Total Ginnie Mae Pools |

147,898 | 155,067 | ||||||

| Total Mortgage Pass-Through Agency RMBS (cost - $8,705,534) |

8,504,078 | 8,835,269 | ||||||

| Collateralized Loan Obligation Securities - 2.4%(d) |

||||||||

| AMMC CLO V LTD(c) |

2,249 | 1,754 | ||||||

| AMMC CLO VII, LTD(c) |

3,900 | 3,237 | ||||||

| ARES VIR CLO, LTD(c)(e) |

3,775 | 2,190 | ||||||

| BALLYROCK CLO 2006-2, LTD(c) |

4,270 | 4,270 | ||||||

| CARLYLE HIGH YIELD PARTNERS VIII, LTD(c) |

3,000 | 2,220 | ||||||

| EATON VANCE CDO IX, LTD(c) |

2,500 | 2,375 | ||||||

| FLAGSHIP CLO V, LTD(c) |

3,750 | 3,000 | ||||||

| PHOENIX CLO II, LTD (formerly AVENUE CLO V)(c) |

2,000 | 1,620 | ||||||

| PRIMUS CLO I, LTD(c) |

2,500 | 1,875 | ||||||

| TRIMARAN CLO VII, LTD(c) |

2,000 | 1,600 | ||||||

| Total Collateralized Loan Obligation Securities (cost - $18,754) |

29,944 | 24,141 | ||||||

| Total Investments in Securities (cost - $8,724,288) |

$ | 8,534,022 | $ | 8,859,410 | ||||

| Notional Amount |

Fair Value | |||||||

| Interest Rate Cap Contracts - 2.0%(d) |

||||||||

| December 2014 Expiration, Cap Rate 2.0725% |

$ | 200,000 | $ | 2,636 | ||||

| October 2015 Expiration, Cap Rate 1.4275% |

300,000 | 10,347 | ||||||

| November 2015 Expiration, Cap Rate 1.3600% |

200,000 | 7,446 | ||||||

| Total Interest Rate Cap Contracts (Cost, $15,641) |

$ | 700,000 | $ | 20,429 | ||||

| Interest Rate Swap Contracts - 4.8%(d) |

||||||||

| May 2013 Expiration, Pay Rate 1.6000%, Receive Rate 3-Month LIBOR |

100,000 | (1,794 | ) | |||||

| June 2013 Expiration, Pay Rate 1.3775%, Receive Rate 3-Month LIBOR |

300,000 | (4,136 | ) | |||||

| July 2013 Expiration, Pay Rate 1.3650%, Receive Rate 3-Month LIBOR |

300,000 | (4,018 | ) | |||||

| December 2013 Expiration, Pay Rate 1.3088%, Receive Rate 3-Month LIBOR |

400,000 | (4,165 | ) | |||||

| December 2013 Expiration, Pay Rate 1.2640%, Receive Rate 3-Month LIBOR |

400,000 | (3,731 | ) | |||||

| December 2013 Expiration, Pay Rate 1.2813%, Receive Rate 3-Month LIBOR |

500,000 | (4,868 | ) | |||||

| December 2013 Expiration, Pay Rate 1.3225%, Receive Rate 3-Month LIBOR |

400,000 | (4,289 | ) | |||||

| April 2014 Expiration, Pay Rate 1.6700%, Receive Rate 3-Month LIBOR (f) |

250,000 | (1,707 | ) | |||||

| July 2014 Expiration, Pay Rate 1.7200%, Receive Rate 3-Month LIBOR |

100,000 | (1,771 | ) | |||||

| July 2014 Expiration, Pay Rate 1.7325%, Receive Rate 3-Month LIBOR |

250,000 | (4,439 | ) | |||||

| August 2014 Expiration, Pay Rate 1.3530%, Receive Rate 3-Month LIBOR |

200,000 | (1,033 | ) | |||||

| September 2014 Expiration, Pay Rate 1.3120%, Receive Rate 3-Month LIBOR |

500,000 | (1,322 | ) | |||||

| October 2014 Expiration, Pay Rate 1.1725%, Receive Rate 3-Month LIBOR |

240,000 | 574 | ||||||

| February 2015 Expiration, Pay Rate 2.1450%, Receive Rate 3-Month LIBOR |

500,000 | (13,031 | ) | |||||

| June 2016 Expiration, Pay Rate 1.9400%, Receive Rate 3-Month LIBOR |

300,000 | 579 | ||||||

| Total Interest Rate Swap Contracts (Cost, $0) |

$ | 4,740,000 | $ | (49,151 | ) | |||

See notes to financial statements.

5

Table of Contents

LEGEND

| (a) | Securities or a portion of the securities are pledged as collateral for repurchase agreements or interest rate swap contracts. |

| (b) | The coupon rate shown on floating or adjustable rate securities represents the rate at June 30, 2011. |

| (c) | Securities exempt from registration under Rule 144A of the Securities Act of 1933. These securities may only be resold in transactions exempt from registration, normally to qualified institutional buyers. At June 30, 2011, the fair value of these securities amounted to $24,141 or 2.4% of net assets. |

| (d) | Percentage of net assets. |

| (e) | Non-income producing security. |

| (f) | Interest rate swap contains a one-time option to cancel at $0. |

See notes to financial statements.

6

Table of Contents

CYPRESS SHARPRIDGE INVESTMENTS, INC.

CONDENSED SCHEDULES OF INVESTMENTS – Continued

DECEMBER 31, 2010 (UNAUDITED)*

INVESTMENTS IN SECURITIES—UNITED STATES OF AMERICA

| (In thousands) |

Face Amount | Fair Value | ||||||

| Investments in Securities - 917.1%(d) |

||||||||

| Mortgage Pass-Through Agency RMBS - 914.1%(d) |

||||||||

| Fannie Mae Pools - 802.1%(d) |

||||||||

| 3.000%, due 1/1/2041(a)(b) |

$ | 50,363 | $ | 51,416 | ||||

| 3.013%, due 10/1/2040(a)(b) |

59,284 | 60,418 | ||||||

| 3.042%, due 12/1/2040(b) |

194,331 | 199,189 | ||||||

| 3.210%, due 11/1/2040(a)(b) |

49,731 | 50,957 | ||||||

| 3.212%, due 12/1/2040(a)(b) |

100,076 | 103,078 | ||||||

| 3.233%, due 7/1/2040(a)(b) |

47,318 | 48,667 | ||||||

| 3.251%, due 11/1/2040(a)(b) |

49,712 | 50,762 | ||||||

| 3.309%, due 8/1/2040(a)(b) |

47,107 | 48,594 | ||||||

| 3.336%, due 9/1/2040(a)(b) |

48,525 | 49,858 | ||||||

| 3.340%, due 9/1/2040(a)(b) |

55,821 | 57,416 | ||||||

| 3.462%, due 11/1/2040(a)(b) |

24,735 | 25,193 | ||||||

| 3.500%, due 12/1/2025(a) |

100,441 | 101,367 | ||||||

| 3.500%, due 1/1/2026(a) |

179,924 | 181,582 | ||||||

| 3.500%, due 12/1/2025 |

4,139 | 4,177 | ||||||

| 3.500%, due 12/1/2025 |

16,274 | 16,424 | ||||||

| 3.500%, due 12/1/2025(a) |

99,910 | 100,831 | ||||||

| 3.500%, due 1/1/2026 |

150,000 | 151,031 | ||||||

| 3.500%, due 2/1/2026 |

550,000 | 552,234 | ||||||

| 3.500%, due 3/1/2026 |

150,000 | 150,094 | ||||||

| 3.500%, due 4/1/2026 |

400,000 | 399,031 | ||||||

| 3.506%, due 8/1/2040(a)(b) |

48,469 | 50,032 | ||||||

| 3.558%, due 7/1/2040(a)(b) |

22,367 | 22,890 | ||||||

| 3.571%, due 7/1/2040(a)(b) |

19,640 | 20,085 | ||||||

| 3.579%, due 8/1/2040(a)(b) |

49,287 | 50,415 | ||||||

| 3.605%, due 10/1/2040(a)(b) |

59,742 | 61,158 | ||||||

| 3.605%, due 8/1/2040(a)(b) |

21,609 | 22,104 | ||||||

| 3.615%, due 8/1/2040(a)(b) |

48,456 | 49,631 | ||||||

| 3.648%, due 6/1/2040(a)(b) |

19,497 | 20,224 | ||||||

| 3.664%, due 7/1/2040(a)(b) |

45,354 | 46,987 | ||||||

| 3.676%, due 7/1/2039(a)(b) |

6,108 | 6,364 | ||||||

| 3.679%, due 7/1/2040(a)(b) |

46,360 | 47,667 | ||||||

| 3.683%, due 8/1/2040(a)(b) |

47,674 | 48,944 | ||||||

| 3.688%, due 5/1/2040(a)(b) |

13,923 | 14,464 | ||||||

| 3.694%, due 8/1/2040(a)(b) |

23,798 | 24,437 | ||||||

| 3.755%, due 5/1/2040(a)(b) |

46,830 | 48,486 | ||||||

| 3.771%, due 8/1/2040(a)(b) |

14,108 | 14,524 | ||||||

| 3.776%, due 9/1/2039(a)(b) |

29,583 | 30,984 | ||||||

| 3.830%, due 7/1/2040(a)(b) |

46,251 | 47,773 | ||||||

| 3.974%, due 10/1/2039(a)(b) |

38,779 | 40,546 | ||||||

| 3.983%, due 9/1/2039(a)(b) |

18,868 | 19,789 | ||||||

| 4.000%, due 12/1/2025(a) |

25,104 | 25,951 | ||||||

| 4.000%, due 12/1/2030(a) |

75,493 | 76,497 | ||||||

| 4.000%, due 1/1/2026(a) |

50,369 | 52,069 | ||||||

| 4.000%, due 12/1/2025(a) |

75,088 | 77,623 | ||||||

See notes to financial statements.

7

Table of Contents

CYPRESS SHARPRIDGE INVESTMENTS, INC.

CONDENSED SCHEDULES OF INVESTMENTS – Continued

DECEMBER 31, 2010 (UNAUDITED)*

| Face Amount | Fair Value | |||||||

| 4.000%, due 12/1/2025 |

$ | 30,566 | $ | 31,598 | ||||

| 4.000%, due 1/1/2026 |

50,444 | 51,510 | ||||||

| 4.000%, due 12/1/2025 |

31,096 | 31,859 | ||||||

| 4.000%, due 12/1/2024(a) |

22,837 | 23,554 | ||||||

| 4.000%, due 10/1/2024(a) |

11,035 | 11,382 | ||||||

| 4.000%, due 1/1/2025(a) |

41,384 | 42,683 | ||||||

| 4.000%, due 1/1/2025(a) |

65,069 | 67,265 | ||||||

| 4.000%, due 2/1/2025(a) |

43,086 | 44,540 | ||||||

| 4.000%, due 3/1/2025(a) |

43,404 | 44,869 | ||||||

| 4.000%, due 9/1/2030(a) |

96,940 | 98,229 | ||||||

| 4.000%, due 9/1/2030(a) |

23,974 | 24,293 | ||||||

| 4.000%, due 10/1/2025(a) |

27,531 | 28,460 | ||||||

| 4.000%, due 10/1/2030(a) |

49,695 | 50,356 | ||||||

| 4.000%, due 10/1/2030(a) |

74,994 | 75,992 | ||||||

| 4.000%, due 10/1/2030(a) |

74,413 | 75,402 | ||||||

| 4.000%, due 10/1/2025(a) |

29,823 | 30,830 | ||||||

| 4.000%, due 10/1/2030(a) |

74,750 | 75,744 | ||||||

| 4.000%, due 10/1/2025(a) |

49,680 | 51,356 | ||||||

| 4.000%, due 11/1/2025(a) |

49,461 | 51,130 | ||||||

| 4.000%, due 11/1/2025(a) |

50,118 | 51,810 | ||||||

| 4.000%, due 11/1/2025(a) |

9,941 | 10,277 | ||||||

| 4.000%, due 2/1/2026 |

100,000 | 102,734 | ||||||

| 4.063%, due 6/1/2039(a)(b) |

19,102 | 20,082 | ||||||

| 4.096%, due 9/1/2039(a)(b) |

24,491 | 25,701 | ||||||

| 4.500%, due 5/1/2024(a) |

12,186 | 12,856 | ||||||

| 4.500%, due 6/1/2024(a) |

20,005 | 20,980 | ||||||

| 4.500%, due 5/1/2024(a) |

13,063 | 13,700 | ||||||

| 4.500%, due 6/1/2024(a) |

17,943 | 18,817 | ||||||

| 4.500%, due 9/1/2024(a) |

21,594 | 22,647 | ||||||

| 4.500%, due 9/1/2024(a) |

21,095 | 22,123 | ||||||

| 4.500%, due 10/1/2024(a) |

36,292 | 38,062 | ||||||

| 4.500%, due 9/1/2024(a) |

1,937 | 2,031 | ||||||

| 4.500%, due 11/1/2024(a) |

11,631 | 12,198 | ||||||

| 4.500%, due 10/1/2024(a) |

38,299 | 40,166 | ||||||

| 4.500%, due 11/1/2024(a) |

49,978 | 52,415 | ||||||

| 4.500%, due 10/1/2024(a) |

29,910 | 31,368 | ||||||

| 4.500%, due 4/1/2030(a) |

28,916 | 29,998 | ||||||

| 4.500%, due 5/1/2030(a) |

48,182 | 49,984 | ||||||

| 4.500%, due 6/1/2025(a) |

33,361 | 35,050 | ||||||

| 4.500%, due 10/1/2030(a) |

49,664 | 51,522 | ||||||

| 4.500%, due 11/1/2030(a) |

50,338 | 52,221 | ||||||

| 4.500%, due 2/1/2026 |

300,000 | 314,109 | ||||||

| 5.500%, due 9/1/2023(a) |

32,265 | 34,714 | ||||||

| 5.500%, due 2/1/2041 |

200,000 | 213,594 | ||||||

| 6.000%, due 5/1/2037(a) |

8,749 | 9,401 | ||||||

| 6.000%, due 4/1/2038(a) |

14,299 | 15,555 | ||||||

| Total Fannie Mae Pools |

5,403,989 | 5,537,130 | ||||||

See notes to financial statements.

8

Table of Contents

CYPRESS SHARPRIDGE INVESTMENTS, INC.

CONDENSED SCHEDULES OF INVESTMENTS – Continued

DECEMBER 31, 2010 (UNAUDITED)*

| Face Amount | Fair Value | |||||||

| Freddie Mac Pools - 88.6%(d) |

||||||||

| 3.052%, due 1/1/2041(a)(b) |

$ | 45,411 | $ | 46,424 | ||||

| 3.200%, due 12/1/2040(a)(b) |

50,012 | 51,281 | ||||||

| 3.247%, due 12/1/2040(b) |

49,646 | 50,980 | ||||||

| 3.500%, due 3/1/2026 |

200,000 | 199,938 | ||||||

| 4.000%, due 10/1/2025(a) |

73,474 | 75,689 | ||||||

| 4.500%, due 7/1/2024(a) |

48,351 | 50,527 | ||||||

| 4.500%, due 2/1/2025(a) |

43,717 | 45,739 | ||||||

| 4.500%, due 12/1/2024(a) |

15,509 | 16,207 | ||||||

| 4.500%, due 12/1/2024(a) |

15,096 | 15,775 | ||||||

| 4.500%, due 1/1/2025(a) |

33,201 | 34,696 | ||||||

| 4.500%, due 5/1/2025(a) |

18,565 | 19,423 | ||||||

| 5.500%, due 9/1/2023(a) |

4,998 | 5,360 | ||||||

| Total Freddie Mac Pools |

597,980 | 612,039 | ||||||

| Ginnie Mae Pools - 23.4%(d) |

||||||||

| 3.500%, due 7/20/2040(a)(b) |

84,444 | 87,841 | ||||||

| 3.500%, due 7/20/2040(a)(b) |

49,868 | 51,874 | ||||||

| 4.000%, due 1/20/2040(a)(b) |

20,627 | 21,686 | ||||||

| Total Ginnie Mae Pools |

154,939 | 161,401 | ||||||

| Total Mortgage Pass-Through Agency RMBS (cost - $6,308,441) |

6,156,908 | 6,310,570 | ||||||

| Collateralized Loan Obligation Securities - 3.0%(d) |

||||||||

| AMMC CLO V LTD(c) |

2,249 | 1,349 | ||||||

| AMMC CLO VII, LTD(c) |

3,900 | 2,578 | ||||||

| ARES VIR CLO, LTD(c)(e) |

3,775 | 1,623 | ||||||

| BALLYROCK CLO 2006-2, LTD(c) |

4,270 | 3,843 | ||||||

| CARLYLE HIGH YIELD PARTNERS VIII, LTD(c) |

3,000 | 2,250 | ||||||

| EATON VANCE CDO IX, LTD(c) |

2,500 | 1,915 | ||||||

| FLAGSHIP CLO V, LTD(c) |

3,750 | 2,363 | ||||||

| PHOENIX CLO II, LTD (formerly AVENUE CLO V)(c)(e) |

2,000 | 1,127 | ||||||

| PRIMUS CLO I, LTD(c) |

2,500 | 1,750 | ||||||

| TRIMARAN CLO VII, LTD(c) |

2,000 | 1,680 | ||||||

| Total Collateralized Loan Obligation Securities (cost - $21,183) |

29,944 | 20,478 | ||||||

| Total Investments in Securities (cost - $6,329,624) |

$ | 6,186,852 | $ | 6,331,048 | ||||

| Interest Rate Cap Contracts - 4.5%(d) | Notional Amount |

Fair Value | ||||||

| December 2014 Expiration, Cap Rate 2.073% |

$ | 200,000 | $ | 4,752 | ||||

| October 2015 Expiration, Cap Rate 1.428% |

300,000 | 15,340 | ||||||

| November 2015 Expiration, Cap Rate 1.360% |

200,000 | 10,892 | ||||||

| Total Interest Rate Cap Contracts (Cost, $17,560) |

$ | 700,000 | $ | 30,984 | ||||

| Interest Rate Swap Contracts - (0.1)%(d) |

||||||||

| May 2013 Expiration, Pay Rate 1.600%, Receive Rate 3-Month LIBOR |

$ | 100,000 | $ | (1,496 | ) | |||

| June 2013 Expiration, Pay Rate 1.378%, Receive Rate 3-Month LIBOR |

300,000 | (2,718 | ) | |||||

| July 2013 Expiration, Pay Rate 1.365%, Receive Rate 3-Month LIBOR |

300,000 | (2,484 | ) | |||||

See notes to financial statements.

9

Table of Contents

CYPRESS SHARPRIDGE INVESTMENTS, INC.

CONDENSED SCHEDULES OF INVESTMENTS – Continued

DECEMBER 31, 2010 (UNAUDITED)*

| Notional Amount |

Fair Value | |||||||

| December 2013 Expiration, Pay Rate 1.3088%, Receive Rate 3-Month LIBOR |

$ | 400,000 | $ | (776 | ) | |||

| December 2013 Expiration, Pay Rate 1.2813%, Receive Rate 3-Month LIBOR |

500,000 | (539 | ) | |||||

| December 2013 Expiration, Pay Rate 1.2640%, Receive Rate 3-Month LIBOR |

400,000 | (255 | ) | |||||

| December 2013 Expiration, Pay Rate 1.3225%, Receive Rate 3-Month LIBOR |

400,000 | (904 | ) | |||||

| July 2014 Expiration, Pay Rate 1.7200%, Receive Rate 3-Month LIBOR |

100,000 | (733 | ) | |||||

| July 2014 Expiration, Pay Rate 1.7325%, Receive Rate 3-Month LIBOR |

250,000 | (1,787 | ) | |||||

| August 2014 Expiration, Pay Rate 1.353%, Receive Rate 3-Month LIBOR |

200,000 | 1,529 | ||||||

| September 2014 Expiration, Pay Rate 1.312%, Receive Rate 3-Month LIBOR |

500,000 | 5,460 | ||||||

| October 2014 Expiration, Pay Rate 1.1725%, Receive Rate 3-Month LIBOR |

240,000 | 4,059 | ||||||

| Total Interest Rate Swap Contracts (Cost, $0) |

$ | 3,690,000 | $ | (644 | ) | |||

LEGEND

| * | Derived from audited financial statements. |

| (a) | Securities or a portion of the securities are pledged as collateral for repurchase agreements or interest rate swap contracts. |

| (b) | The coupon rate shown on floating or adjustable rate securities represents the rate at December 31, 2010. |

| (c) | Securities exempt from registration under Rule 144A of the Securities Act of 1933. These securities may only be resold in transactions exempt from registration, normally to qualified institutional buyers. At December 31, 2010, the fair value of these securities amounted to $20,478 or 3.0% of net assets. |

| (d) | Percentage of net assets. |

| (e) | Non-income producing security. |

See notes to financial statements.

10

Table of Contents

CYPRESS SHARPRIDGE INVESTMENTS, INC.

CONDENSED STATEMENTS OF OPERATIONS (UNAUDITED)

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

| (In thousands, except per share numbers) | 2011 | 2010 | 2011 | 2010 | ||||||||||||

| INVESTMENT INCOME - Interest income |

$ | 65,720 | $ | 17,265 | $ | 106,700 | $ | 34,202 | ||||||||

| EXPENSES: |

||||||||||||||||

| Interest |

4,470 | 1,081 | 7,574 | 2,067 | ||||||||||||

| Management fees |

3,311 | 1,152 | 6,151 | 2,228 | ||||||||||||

| Related party management compensation |

589 | 315 | 1,134 | 645 | ||||||||||||

| General, administrative and other |

965 | 619 | 1,999 | 1,445 | ||||||||||||

| Total expenses |

9,335 | 3,167 | 16,858 | 6,385 | ||||||||||||

| Net investment income |

56,385 | 14,098 | 89,842 | 27,817 | ||||||||||||

| GAINS AND (LOSSES) FROM INVESTMENTS: |

||||||||||||||||

| Net realized gain (loss) on investments |

9,438 | (2,168 | ) | 15,346 | (9,420 | ) | ||||||||||

| Net unrealized appreciation (depreciation) on investments |

119,787 | 34,535 | 133,698 | 48,252 | ||||||||||||

| Net gain (loss) from investments |

129,225 | 32,367 | 149,044 | 38,832 | ||||||||||||

| GAINS AND (LOSSES) FROM SWAP AND CAP CONTRACTS: |

||||||||||||||||

| Net swap and cap interest income (expense) |

(14,875 | ) | (3,138 | ) | (26,733 | ) | (6,432 | ) | ||||||||

| Net gain (loss) on termination of swap contracts |

(3,493 | ) | (17,205 | ) | (3,492 | ) | (17,205 | ) | ||||||||

| Net unrealized appreciation (depreciation) on swap and cap contracts |

(67,820 | ) | 1,483 | (57,142 | ) | (5,263 | ) | |||||||||

| Net gain (loss) from swap and cap contracts |

(86,188 | ) | (18,860 | ) | (87,367 | ) | (28,900 | ) | ||||||||

| NET INCOME |

$ | 99,422 | $ | 27,605 | $ | 151,519 | $ | 37,749 | ||||||||

| NET INCOME PER COMMON SHARE BASIC & DILUTED |

||||||||||||||||

| Basic |

$ | 1.20 | $ | 1.47 | $ | 1.97 | $ | 2.01 | ||||||||

| Diluted |

$ | 1.20 | $ | 1.46 | $ | 1.97 | $ | 2.01 | ||||||||

See notes to financial statements.

11

Table of Contents

CYPRESS SHARPRIDGE INVESTMENTS, INC.

CONDENSED STATEMENTS OF CHANGES IN NET ASSETS (UNAUDITED)

| (In thousands) | Three Months Ended June 30, 2011 |

Six Months Ended June 30, 2011 |

||||||

| Net income: |

||||||||

| Net investment income |

$ | 56,385 | $ | 89,842 | ||||

| Net realized gain (loss) on investment securities |

9,438 | 15,346 | ||||||

| Net unrealized appreciation (depreciation) on investments |

119,787 | 133,698 | ||||||

| Net gain (loss) on swap and cap contracts |

(86,188 | ) | (87,367 | ) | ||||

| Net income |

99,422 | 151,519 | ||||||

| Capital transactions: |

||||||||

| Net proceeds from issuance of common shares |

86 | 275,907 | ||||||

| Distributions to shareholders |

(49,554 | ) | (99,090 | ) | ||||

| Amortization of related party compensation |

589 | 1,134 | ||||||

| Increase (decrease) in net assets from capital transactions |

(48,879 | ) | 177,951 | |||||

| Total increase in net assets |

50,543 | 329,470 | ||||||

| Net assets: |

||||||||

| Beginning of period |

969,266 | 690,339 | ||||||

| End of period |

$ | 1,019,809 | $ | 1,019,809 | ||||

See notes to financial statements.

12

Table of Contents

CYPRESS SHARPRIDGE INVESTMENTS, INC.

CONDENSED STATEMENTS OF CASH FLOWS (UNAUDITED)

| Six Months Ended June 30, | ||||||||

| (In thousands) | 2011 | 2010 | ||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: |

||||||||

| Net income |

$ | 151,519 | $ | 37,749 | ||||

| Adjustments to reconcile net income to net cash used in operating activities: |

||||||||

| Purchase of investment securities |

(3,690,210 | ) | (864,685 | ) | ||||

| Proceeds from disposition of investment securities |

881,033 | 192,690 | ||||||

| Principal repayments of investment securities |

415,367 | 263,185 | ||||||

| Amortization of related party compensation |

1,134 | 645 | ||||||

| Amortization of premiums on investment securities |

14,493 | 3,404 | ||||||

| Amortization of premiums on interest rate cap contracts |

1,919 | — | ||||||

| Net realized (gain) loss on investment securities |

(15,346 | ) | 9,420 | |||||

| Net unrealized (appreciation) depreciation on swap and cap contracts |

57,142 | 5,263 | ||||||

| Net unrealized (appreciation) depreciation on investments |

(133,698 | ) | (48,252 | ) | ||||

| Change in assets and liabilities: |

||||||||

| Receivable for securities sold |

(400,849 | ) | 600 | |||||

| Interest receivable |

(11,719 | ) | 266 | |||||

| Other assets |

(400 | ) | (726 | ) | ||||

| Payable for securities purchased and terminated swap contract |

(1,607,925 | ) | 356,622 | |||||

| Accrued interest payable |

6,262 | (1,615 | ) | |||||

| Related party management fee payable |

325 | 59 | ||||||

| Accrued expenses and other liabilities |

(80 | ) | (35 | ) | ||||

| Net cash used in operating activities |

(4,331,033 | ) | (45,410 | ) | ||||

| CASH FLOWS FROM FINANCING ACTIVITIES: |

||||||||

| Proceeds from repurchase agreements |

19,346,529 | 7,624,130 | ||||||

| Repayments of repurchase agreements |

(15,242,281 | ) | (7,549,238 | ) | ||||

| Net proceeds from issuance of common shares |

275,907 | 129,891 | ||||||

| Distributions paid |

(49,540 | ) | (20,638 | ) | ||||

| Net cash provided by financing activities |

4,330,615 | 184,145 | ||||||

| Net increase (decrease) in cash and cash equivalents |

(418 | ) | 138,735 | |||||

| CASH AND CASH EQUIVALENTS - Beginning of period |

1,510 | 1,890 | ||||||

| CASH AND CASH EQUIVALENTS - End of period |

$ | 1,092 | $ | 140,625 | ||||

| SUPPLEMENTAL DISCLOSURES OF CASH FLOW INFORMATION: |

||||||||

| Interest paid |

$ | 29,316 | $ | 10,606 | ||||

| SUPPLEMENTAL DISCLOSURES OF NONCASH FLOW INFORMATION: |

||||||||

| Distributions declared, not yet paid |

$ | 49,550 | $ | 11,261 | ||||

See notes to financial statements.

13

Table of Contents

CYPRESS SHARPRIDGE INVESTMENTS, INC.

CONDENSED NOTES TO FINANCIAL STATEMENTS (UNAUDITED)

1. ORGANIZATION

Cypress Sharpridge Investments, Inc. (the “Company”) was formed as a Maryland corporation on January 3, 2006, and commenced operations on February 10, 2006. The Company is externally managed and advised by Cypress Sharpridge Advisors LLC (the “Manager”), a Delaware limited liability company, pursuant to a management agreement (the “Management Agreement”). The Manager is a joint venture between Cypress CSI Advisors LLC, a sponsor of private equity funds and leveraged buyouts of U.S. companies in the industrial, consumer, media and financial sectors, and Sharpridge Capital Management, L.P., a fixed income asset management company. Certain individuals associated with Cypress CSI Advisors LLC and Sharpridge Capital Management, L.P. serve on the Company’s board of directors and the Manager’s investment committee.

The Company has elected to be taxed and intends to continue to qualify as a real estate investment trust (“REIT”) and is required to comply with the provisions of the Internal Revenue Code of 1986, as amended (the “Code”), with respect thereto. The Company’s strategy had been to invest a majority of its capital in residential mortgage-backed securities that are issued and guaranteed by a federally chartered corporation (“Agency RMBS”), such as the Federal National Mortgage Association (“Fannie Mae”) or the Federal Home Loan Mortgage Corporation (“Freddie Mac”), or an agency of the U.S. government such as the Government National Mortgage Association (“Ginnie Mae”), and subordinated tranches of asset-backed securities, including collateralized debt or loan obligations (“CLOs”). In March 2008, the board of directors amended the investment guidelines, pursuant to which the Company was mandated to invest exclusively in Agency RMBS. In March 2010, the board of directors further amended the investment guidelines so that the Company may also invest in collateralized mortgage obligations issued by Fannie Mae, Freddie Mac or Ginnie Mae. The Company’s common stock trades on the New York Stock Exchange under the symbol “CYS”.

2. SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation

The accompanying interim unaudited condensed financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America (“GAAP”) and the instructions to Form 10-Q and Article 10, Rule 10-01 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by GAAP for complete financial statements. In the opinion of management, all adjustments (consisting of normal recurring accruals) considered necessary for a fair presentation have been included. The interim unaudited condensed financial statements should be read in conjunction with the Company’s audited financial statements as of and for the year ended December 31, 2010, included in the annual report on Form 10-K. The results for interim periods are not necessarily indicative of the results to be expected for the fiscal year.

The Company adopted Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) 946, Clarification of the Scope of Audit and Accounting Guide Investment Companies (“ASC 946”), prior to its deferral in February 2008. Under ASC 946, the Company uses financial reporting for investment companies.

Segment Reporting

The Company operates as a single segment reporting to the Chief Executive Officer, who manages the entire investment portfolio.

Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the amounts reported in the financial statements and accompanying notes. Actual results could differ from those management estimates.

Cash and Cash Equivalents

Cash and cash equivalents include cash on hand, cash held in banks and highly liquid investments with original maturities of three months or less. Interest income earned on cash and cash equivalents is recorded in interest income.

Interest Rate Swap and Cap Contracts

The Company utilizes interest rate swaps and caps to hedge the interest rate risk associated with the financing of its portfolio. Specifically, the Company seeks to hedge the exposure to potential interest rate mismatches between the interest earned on investments and the borrowing costs caused by fluctuations in short term interest rates. In a simple interest rate swap, one investor pays a floating rate of interest on a notional principal amount and receives a fixed rate of interest on the same notional principal amount for a specified period of time. Alternatively, an investor may pay a fixed rate and receive a floating rate. In a simple interest rate cap, one investor pays a premium for a notional principal amount based on a capped interest rate (the “cap rate”). If the floating

14

Table of Contents

interest rate (the “floating rate”) exceeds the cap rate, the investor receives a payment from the cap counterparty equal to the difference between the floating rate and the cap rate on the same notional principal amount for a specified period of time. Alternatively, an investor may receive a premium and pay the difference in cap rate and floating rate. Interest rate swaps and caps are asset/liability management tools.

During the term of the interest rate swap or cap, the Company makes or receives periodic payments and unrealized gains or losses are recorded as a result of marking the swap and cap to their fair value. When the swap or cap is terminated, the Company records a realized gain or loss equal to the difference between the proceeds from (or cost of) the closing transaction and the Company’s cost basis in the contract, if any. The periodic payments, amortization of premiums on cap contracts and any realized or unrealized gains or losses are reported under gains and losses from swap and cap contracts in the statement of operations. Swaps involve a risk that interest rates will move contrary to the Company’s expectations, thereby increasing its payment obligation.

Because the Company uses financial reporting for investment companies, its investments, including its interest rate swap and cap contracts, are carried at fair value with changes in fair value included in earnings. Consequently, there is no impact to designating interest rate swaps and caps as cash flow or fair value hedges under GAAP.

The Company is exposed to credit loss in the event of nonperformance by the counterparty to the swap or cap, limited to the amount of collateral posted that exceeds the fair value of the contract. However, as of June 30, 2011 and December 31, 2010 the Company did not anticipate nonperformance by any counterparty. Should interest rates move unexpectedly, the Company may not achieve the anticipated benefits of the interest rate swap or cap and may realize a loss.

Investment Valuation

Valuation of the Company’s investments is determined by the Manager. Investments are valued using third-party pricing services and dealer quotes. The third-party pricing services use pricing models that incorporate such factors as coupons, primary and secondary mortgage rates, prepayment speeds, spread to the Treasury curves and interest rate swap curves, convexity, duration, periodic and life caps and credit enhancement. The dealer quotes incorporate common market pricing methods, including a spread measurement to the Treasury curves or interest rate swap curve as well as underlying characteristics of the particular security including coupon, periodic and life caps, rate reset period, issuer, additional credit support and expected life of the security. The Manager reviews all prices used to ensure that current market conditions are represented. This review includes comparisons of similar market transactions, alternative third-party pricing services and dealer quotes, or comparisons to a pricing model. The resulting unrealized gains and losses are reflected in the statement of operations.

Agency RMBS

The Company’s investments in Agency RMBS consist of whole-pool pass-through certificates backed by fixed rate, monthly reset adjustable-rate loans (“ARMs”) and hybrid ARMs, the principal and interest of which are guaranteed by Fannie Mae, Freddie Mac or Ginnie Mae. Hybrid ARMs have interest rates that have an initial fixed period (typically three, five, seven or ten years) and thereafter reset at regular intervals in a manner similar to ARMs.

Forward Settling Transactions

The Company may engage in forward settling transactions. The Company records forward settling transactions on the trade date and maintains security positions such that sufficient liquid assets will be available to make payment on the settlement date for the securities purchased. Securities purchased on a forward settling basis are carried at fair value and begin earning interest on the settlement date. Losses may occur on these transactions due to changes in market conditions or the failure of counterparties to perform under the contract. The Company may transact in To-Be-Announced Securities (“TBAs”). As with other forward settling transactions, a seller agrees to issue TBAs at a future date. However, the seller does not specify the particular securities to be delivered. Instead, the Company agrees to accept any security that meets specified terms such as issuer, interest rate and terms of underlying mortgages. The Company records TBAs on the trade date utilizing information associated with the specified terms of the transaction as opposed to the specific mortgages. TBAs are carried at fair value and begin earning interest on the settlement date. Losses may occur due to the fact that the actual underlying mortgages received may be less favorable than those anticipated by the Company. As of June 30, 2011 and December 31, 2010, the Company had pledged Agency RMBS with a fair value of $3.4 million and $10.1 million, respectively, on its open forward settling and TBA transactions.

Collateralized Debt or Loan Obligations

The Company has investments in collateralized debt obligations and collateralized loan obligations (collectively “CLOs”), which are securities backed by pools of variously rated loans or bonds. Underwriters of CLOs package a large and diversified pool of loans or bonds, including high risk, high yield bonds, which is then separated into “tiers.” Typically, the top tier represents the last tier to take losses and therefore the lowest risk and pays the lower interest rate; a middle tier would take losses prior to the top tier and therefore has more risk than the top tier so it pays a higher rate than the top tier; the bottom tier takes losses first and therefore represents the highest risk and, instead of receiving a fixed interest rate, may receive the residual interest payments from the pool.

15

Table of Contents

Repurchase Agreements

Repurchase agreements are borrowings that are collateralized by the Company’s Agency RMBS and are carried at their amortized cost, which approximates their fair value due to their short term nature, generally 30-90 days. The Company’s repurchase agreement counterparties are large institutional dealers in fixed income securities. Collateral is valued daily and counterparties may require additional collateral when appropriate. At June 30, 2011 and December 31, 2010, Agency RMBS owned with a fair value of approximately $7,927.1 million and $3,657.2 million, respectively, have been pledged as collateral for repurchase agreements for which the counterparty has the right to sell or repledge.

Investment Transactions and Income

The Company records its transactions in securities on a trade date basis. Realized gains and losses on securities transactions are recorded on an identified cost basis. Interest income and expense are recorded on the accrual basis. Interest income on Agency RMBS is accrued based on outstanding principal amount of the securities and their contractual terms. Interest on CLOs is accrued at a rate determined based on estimated future cash flows and adjusted prospectively as future cash flow amounts are recast. For CLOs placed on nonaccrual status or when the Company cannot reliably estimate cash flows, the cost recovery method is used. Amortization of premium and accretion of discount are recorded using the yield to maturity method, and are included in interest income in the statement of operations.

Share-Based Compensation

The Company accounts for share-based compensation issued to its non-management directors and executive officers and certain officers and employees of its Manager and its sub-advisors and other individuals who provide services to the Company, as designated by its Manager (“Manager Designees”), using the fair value based methodology prescribed by ASC 718, Share-Based Payment (“ASC 718”). Compensation cost related to restricted common stock and common stock options issued to the Manager Designees is initially measured at estimated fair value at the grant date, and is remeasured on subsequent dates to the extent the awards are unvested. Compensation cost related to non-management directors is measured at its estimated fair value at the grant date and amortized and expensed over the vesting period. The Company has elected to use the straight line method pursuant to ASC 718 to amortize compensation expense for the restricted common stock and common stock options granted to the Manager Designees.

Income Taxes

The Company has elected to be taxed as a REIT and intends to continue to comply with provisions of the Code with respect thereto. As a REIT, the Company generally will not be subject to federal or state income tax. To maintain its qualification as a REIT, the Company must distribute at least 90% of its REIT taxable income to its stockholders and meet certain other tests relating to assets and income.

Earnings Per Share (“EPS”)

Basic EPS is computed using the two class method by dividing net income (loss) after adjusting for the impact of unvested stock awards deemed to be participating securities, by the weighted average number of common shares outstanding calculated excluding unvested stock awards. Diluted EPS is computed by dividing net income (loss), after adjusting for the impact of unvested stock awards deemed to be participating securities, by the weighted average number of common shares outstanding calculated excluding unvested stock awards, giving effect to common stock options and warrants, if they are not anti-dilutive. See note 3 for EPS computations.

Recent Accounting Pronouncements

The FASB has recently issued or discussed a number of proposed standards on such topics as financial statement presentation, revenue recognition, financial instruments, hedging, contingencies and fair value. Some of the proposed changes are potentially significant and could have a material impact on the Company’s reporting. The Company has not yet fully evaluated the potential impact of these proposals but will make such an evaluation as the standards are finalized.

16

Table of Contents

3. EARNINGS PER SHARE

Components of the computation of basic and diluted EPS were as follows (in thousands, except per share numbers):

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

| 2011 | 2010 | 2011 | 2010 | |||||||||||||

| Net income |

$ | 99,422 | $ | 27,605 | $ | 151,519 | $ | 37,749 | ||||||||

| Less dividends paid: |

||||||||||||||||

| Common shares |

(49,087 | ) | (10,929 | ) | (98,155 | ) | (20,943 | ) | ||||||||

| Unvested shares |

(467 | ) | (335 | ) | (935 | ) | (640 | ) | ||||||||

| Undistributed earnings |

49,868 | 16,341 | 52,429 | 16,166 | ||||||||||||

| Basic weighted average shares outstanding: |

||||||||||||||||

| Common shares |

81,798 | 18,328 | 75,976 | 18,267 | ||||||||||||

| Basic earnings per common share: |

||||||||||||||||

| Distributed earnings |

$ | 0.60 | $ | 0.60 | $ | 1.29 | $ | 1.15 | ||||||||

| Undistributed earnings |

0.60 | 0.87 | 0.68 | 0.86 | ||||||||||||

| Basic earnings per common share |

$ | 1.20 | $ | 1.47 | $ | 1.97 | $ | 2.01 | ||||||||

| Diluted weighted average shares outstanding: |

||||||||||||||||

| Common shares |

81,798 | 18,328 | 75,976 | 18,267 | ||||||||||||

| Net effect of dilutive warrants(1) |

1 | 12 | 1 | 13 | ||||||||||||

| 81,799 | 18,340 | 75,977 | 18,280 | |||||||||||||

| Diluted earnings per common share: |

||||||||||||||||

| Distributed earnings |

$ | 0.60 | $ | 0.60 | $ | 1.29 | $ | 1.15 | ||||||||

| Undistributed earnings |

0.60 | 0.86 | 0.68 | 0.86 | ||||||||||||

| Diluted earnings per common share |

$ | 1.20 | $ | 1.46 | $ | 1.97 | $ | 2.01 | ||||||||

| (1) | The impact of equity instruments is not included in the computation of EPS for periods in which their inclusion would be anti-dilutive. For the three and six months ended June 30, 2011 and 2010, the Company had an aggregate of 131,088 stock options outstanding with a weighted average exercise price of $30.00 that were not included in the calculation of EPS for the three and six months ended June 30, 2011 and 2010, as their inclusion would have been anti-dilutive. These equity instruments may have a dilutive impact on future EPS. |

4. INVESTMENTS IN SECURITIES AND INTEREST RATE SWAP AND CAP CONTRACTS

The Company’s valuation techniques are based on observable and unobservable inputs. Observable inputs reflect readily obtainable data from independent sources, while unobservable inputs reflect the Company’s market assumptions. ASC 820 classifies these inputs into the following hierarchy:

Level 1 Inputs—Quoted prices for identical instruments in active markets.

Level 2 Inputs—Quoted prices for similar instruments in active markets; quoted prices for identical or similar instruments in markets that are not active; and model-derived valuations whose inputs are observable or whose significant value drivers are observable.

Level 3 Inputs—Instruments with primarily unobservable value drivers.

The following tables provide a summary of the Company’s assets and liabilities that are measured at fair value on a recurring basis as of June 30, 2011 and December 31, 2010:

June 30, 2011

| Fair Value Measurements Using | ||||||||||||||||

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| (in thousands) | ||||||||||||||||

| Assets |

||||||||||||||||

| Agency RMBS |

$ | — | $ | 8,835,269 | $ | — | $ | 8,835,269 | ||||||||

| CLOs |

— | — | 24,141 | 24,141 | ||||||||||||

| Interest rate cap contracts |

— | 20,429 | — | 20,429 | ||||||||||||

| Total |

$ | — | $ | 8,855,698 | $ | 24,141 | $ | 8,879,839 | ||||||||

| Liabilities |

||||||||||||||||

| Interest rate swap contracts(a) |

$ | — | $ | (49,151 | ) | $ | — | $ | (49,151 | ) | ||||||

17

Table of Contents

December 31, 2010

| Fair Value Measurements Using | ||||||||||||||||

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| (in thousands) | ||||||||||||||||

| Assets |

||||||||||||||||

| Agency RMBS |

$ | — | $ | 6,310,570 | $ | — | $ | 6,310,570 | ||||||||

| CLOs |

— | — | 20,478 | 20,478 | ||||||||||||

| Interest rate cap contracts |

— | 30,984 | — | 30,984 | ||||||||||||

| Interest rate swap contracts(a) |

— | 9,113 | — | 9,113 | ||||||||||||

| Total |

$ | — | $ | 6,350,667 | $ | 20,478 | $ | 6,371,145 | ||||||||

| Liabilities |

||||||||||||||||

| Interest rate swap contracts(a) |

$ | — | $ | 9,757 | $ | — | $ | 9,757 | ||||||||

| (a) | Subject to master netting arrangements |

The table below presents a reconciliation of changes in assets classified as Level 3 in the Company’s financial statements for the three and six months ended June 30, 2011. There were no changes in the three and six months ended June 30, 2010. A discussion of the method of fair valuing these assets is included above in “Investment Valuation.” Net unrealized appreciation (depreciation) on the assets is included in net unrealized appreciation (depreciation) on investments in the statement of operations.

Fair Value Reconciliation, Level 3

(in thousands)

| Three Months

Ended June 30, 2011 |

Six Months

Ended June 30, 2011 |

|||||||

| CLOs |

||||||||

| Beginning balance Level 3 assets |

$ | 23,947 | $ | 20,478 | ||||

| Change in net unrealized appreciation (depreciation) |

1,515 | 6,092 | ||||||

| Cash payments recorded as a reduction of cost basis |

(1,321 | ) | (2,429 | ) | ||||

| Transfers into Level 3 |

— | — | ||||||

| Ending balance Level 3 assets |

$ | 24,141 | $ | 24,141 | ||||

The Agency RMBS portfolio consisted of Agency RMBS as follows:

June 30, 2011

| Par Value | Fair Value | Weighted Average | ||||||||||||||||||||||||||

| Asset Type |

(in thousands) | Cost/Par | Fair Value/Par |

MTR(1) | Coupon | CPR(2) | ||||||||||||||||||||||

| 15 Year Fixed Rate |

$ | 4,439,585 | $ | 4,605,393 | $ | 102.33 | $ | 103.73 | N/A | 3.89 | % | 5.5 | % | |||||||||||||||

| 20 Year Fixed Rate |

626,399 | 643,866 | 102.35 | 102.79 | N/A | 4.14 | % | 2.5 | % | |||||||||||||||||||

| 30 Year Fixed Rate |

588,274 | 625,974 | 103.33 | 106.41 | N/A | 5.00 | % | N/A | (3) | |||||||||||||||||||

| Hybrid ARMs |

2,849,820 | 2,960,036 | 102.24 | 103.87 | 63.1 | 3.37 | % | 12.8 | % | |||||||||||||||||||

| Total/Weighted Average |

$ | 8,504,078 | $ | 8,835,269 | $ | 102.37 | $ | 103.89 | 63.1 | (4) | 3.81 | % | 7.3 | % | ||||||||||||||

December 31, 2010

| Par Value | Fair Value | Weighted Average | ||||||||||||||||||||||||||

| Asset Type |

(in thousands) | Cost/Par | Fair Value/Par |

MTR(1) | Coupon | CPR(2) | ||||||||||||||||||||||

| 15 Year Fixed Rate |

$ | 3,549,194 | $ | 3,622,862 | $ | 102.16 | $ | 102.08 | N/A | 3.87 | % | 23.1 | % | |||||||||||||||

| 20 Year Fixed Rate |

647,360 | 660,237 | 102.38 | 101.99 | N/A | 4.14 | % | 6.9 | % | |||||||||||||||||||

| 30 Year Fixed Rate |

223,047 | 238,549 | 105.60 | 106.95 | N/A | 5.55 | % | 28.2 | % | |||||||||||||||||||

| Hybrid ARMs |

1,737,307 | 1,788,922 | 102.70 | 102.97 | 63.2 | 3.43 | % | 18.4 | % | |||||||||||||||||||

| Total/Weighted Average |

$ | 6,156,908 | $ | 6,310,570 | $ | 102.46 | $ | 102.50 | 63.2 | (4) | 3.83 | % | 18.9 | % | ||||||||||||||

18

Table of Contents

| (1) | “Months to Reset” is the number of months remaining before the fixed rate on a hybrid ARM becomes a variable rate. At the end of the fixed period, the variable rate will be determined by the margin and the pre-specified caps of the ARM. After the fixed period, 100% of the hybrid ARMS in the portfolio reset annually. |

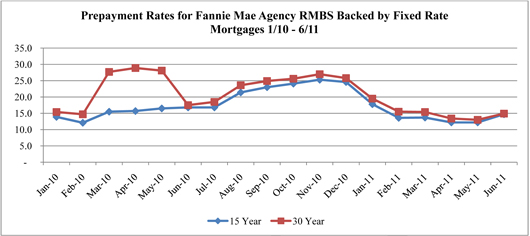

| (2) | CPR, or “Constant Prepayment Rate,” is a method of expressing the prepayment rate for a mortgage pool that assumes that a constant fraction of the remaining principal is prepaid each month or year. Specifically, the constant prepayment rate is an annualized version of the prior three month prepayment rate for those Agency RMBS held at June 30, 2011. Securities with no prepayment history are excluded from this calculation. |

| (3) | The Agency RMBS backed by 30 year mortgages in the portfolio are newly issued securities, and therefore, did not have three months of CPR history as of June 30, 2011. |

| (4) | Weighted average months to reset of our Hybrid ARM portfolio. |

As of June 30, 2011 and December 31, 2010, the Company’s Agency RMBS were purchased at a net premium to their par value due to the average interest rates on these investments being higher than prevailing market rates. As of June 30, 2011 and December 31, 2010, approximately $201.9 million and $152.7 million, respectively, of unamortized premium was included in the cost basis of the securities.

Actual maturities of Agency RMBS are generally shorter than stated contractual maturities (which range up to 30 years), as they are affected by the contractual lives of the underlying mortgages, periodic payments and prepayments of principal. As of June 30, 2011 and December 31, 2010, the average final contractual maturity of the Company’s Agency RMBS portfolio is in year 2032 and 2031, respectively. Based on current estimates, the Agency RMBS will have a weighted average expected life of less than five years. Interest income on Agency RMBS for the three and six months ended June 30, 2011 was $64.7 million, and $104.7 million, respectively, and $16.5 million and $32.9 million for the three and six months ended June 30, 2010, respectively.

In order to mitigate its interest rate exposure, the Company enters into interest rate swap and cap contracts. Below is a summary of the Company’s interest rate swap and cap contracts transacted during the three and six months ended June 30, 2011 and 2010 (in thousands).

| Three & Six Months Ended June 30, 2011 |

Three & Six Months Ended June 30, 2010 |

|||||||||||||

| Trade Date |

Transaction |

Notional | Trade Date |

Transaction |

Notional | |||||||||

| February 2011 |

Opened | $ | 500,000 | April 2010 | Terminated | $ | (400,000 | ) | ||||||

| March 2011 |

Opened | 250,000 | April 2010 | Opened | 400,000 | |||||||||

| May 2011 |

Terminated | (300,000 | ) | May 2010 | Terminated | (640,000 | ) | |||||||

| May 2011 |

Opened | 300,000 | May 2010 | Opened | 740,000 | |||||||||

| June 2011 |

Opened | 300,000 | June 2010 | Terminated | (100,000 | ) | ||||||||

| Net Increase |

$ | 1,050,000 | June 2010 | Opened | 400,000 | |||||||||

| Net Increase | $ | 400,000 | ||||||||||||

19

Table of Contents

As of June 30, 2011 and December 31, 2010, the Company had net pledged Agency RMBS and U.S Treasury securities with a fair value of $109.1 million and $4.3 million, respectively, as collateral on interest rate swap and cap contracts. Below is a summary of our interest rate swap and cap contracts open as of June 30, 2011 and December 31, 2010 and for the three and six months ended June 30, 2011 and 2010 (dollars in thousands):

| Derivatives not designated as hedging instruments under ASC 815(a) | ||||||||||

| Interest Rate Swaps |

Notional Amount | Fair Value | Statement of Assets and Liabilities Location | |||||||

| June 30, 2011 |

$ | 0 | $ | 0 | Assets | |||||

| June 30, 2011 |

4,740,000 | (49,151 | ) | Liabilities | ||||||

| December 31, 2010 |

2,140,000 | 9,113 | Assets | |||||||

| December 31, 2010 |

1,550,000 | (9,757 | ) | Liabilities | ||||||

| Interest Rate Caps |

Notional Amount | Fair Value | Statement of Assets and Liabilities Location | |||||||

| June 30, 2011 |

$ | 700,000 | $ | 20,429 | Assets | |||||

| December 31, 2010 |

700,000 | 30,984 | Assets | |||||||

| Amount of Gain or (Loss) Recognized in Income on Derivative |

||||||||||||||||||

| Derivatives not designated as hedging |

Location of Gain or (Loss) Recognized in |

Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

| 2011 | 2010 | 2011 | 2010 | |||||||||||||||

| Interest rate swap and cap contracts |

Net gain (loss) from interest rate swap and cap contracts | $ | (86,188 | ) | $ | (18,860 | ) | $ | (87,367 | ) | $ | (28,900 | ) | |||||

| (a) | See note 2 for additional information on the Company’s purpose for entering into interest rate swaps and caps and the decision not to designate them as hedging instruments. |

Credit Risk

At June 30, 2011 and December 31, 2010, the Company continued to minimize its exposure to credit losses on its mortgage assets by purchasing Agency RMBS. The payment of principal and interest on Agency RMBS is guaranteed by Freddie Mac, Fannie Mae or Ginnie Mae. In September 2008, both Freddie Mac and Fannie Mae were placed in the conservatorship of the United States government. While it is hoped that the conservatorship will help stabilize Freddie Mac’s and Fannie Mae’s losses and overall financial position, there can be no assurance that it will succeed or that, if necessary, Freddie Mac or Fannie Mae will be able to satisfy their guarantees of Agency RMBS.

The current U.S. debt ceiling and budget deficit concerns have increased the possibility of the credit-rating agencies downgrading the U.S.’s credit rating for the first time in history. Because Fannie Mae and Freddie Mac are in conservatorship of the U.S. Government, if the U.S.’s credit rating was downgraded it would likely impact the credit risk associated with Agency RMBS and, therefore, decrease the value of the Agency RMBS in the Company’s portfolio. In addition, a downgrade of the U.S.’s credit rating would create broader financial turmoil and uncertainty, which would weigh heavily on the global banking system.

The Company’s CLOs do not have the backing of Fannie Mae, Freddie Mac or Ginnie Mae. Payment of principal and interest is dependent on the performance of the underlying loans, which are subject to borrower default and possible losses.

5. BORROWINGS

The Company leverages its Agency RMBS portfolio through the use of repurchase agreements. Each of the borrowing vehicles used by the Company bears interest at floating rates based on a spread above or below the London InterBank Offered Rate (“LIBOR”). The fair value of borrowings under repurchase agreements approximates their carrying amount due to the short-term nature of these financial instruments.

Certain information with respect to the Company’s borrowings is summarized in the following tables. Each of the borrowings listed is contractually due in one year or less (dollars in thousands).

| June 30, 2011 |

||||

| Outstanding borrowings |

$ | 7,548,091 | ||

| Interest accrued thereon |

$ | 2,181 | ||

| Weighted average borrowing rate |

0.25% | |||

| Weighted average remaining maturity (in days) |

37.6 | |||

| Fair value of the collateral(1) |

$ | 7,927,098 | ||

| December 31, 2010 |

||||

| Outstanding borrowings |

$ | 3,443,843 | ||

| Interest accrued thereon |

$ | 1,084 | ||

| Weighted average borrowing rate |

0.32% | |||

| Weighted average remaining maturity (in days) |

39.3 | |||

| Fair value of the collateral(1) |

$ | 3,657,185 | ||

| (1) | Collateral for borrowings consists of Agency RMBS. |

20

Table of Contents

At June 30, 2011 and December 31, 2010, the Company did not have any repurchase agreements where the amount at risk exceeded 10% of net assets.

6. SHARE CAPITAL

The Company authorized 500,000,000 shares of common stock having par value of $0.01 per share. As of June 30, 2011 and December 31, 2010, the Company had issued and outstanding 82,584,330 and 59,550,836 shares of common stock. The Company issued 23,033,494 and 40,794,324 shares of common stock during the six months ended June 30, 2011 and year ended December 31, 2010, respectively.

Below is a description of the warrants outstanding at December 31, 2010. There were no warrants outstanding at June 30, 2011.

| Expiration |

Additional shares of common stock |

Exercise Price | ||||||

| April 30, 2011 |

15,200 | $ | 11.00 | |||||

The Company also authorized 50,000,000 shares of preferred stock having a par value of $0.01 per share. As of June 30, 2011 and December 31, 2010, no such shares were issued or outstanding.

On February 15, 2011, the Company closed a public offering of 23,000,000 shares of its common stock at a public offering price of $12.35 per share for total net proceeds of approximately $275.8 million, after the underwriting discount and commissions and expenses.

The Company sponsors a dividend reinvestment and direct stock purchase plan through which stockholders may purchase additional shares of common stock by reinvesting some or all of the cash dividends received on shares of common stock. This plan became effective on June 22, 2010. Stockholders may also make optional cash purchases of shares of common stock subject to certain limitations detailed in the plan prospectus. From June 22, 2010 to December 31, 2010 the Company issued 607,902 shares under the plan raising approximately $8.0 million of net proceeds. For the six months ended June 30, 2011 the Company issued 6,957 shares under the plan raising approximately $87,452 of net proceeds. As of June 30, 2011 and December 31, 2010, there were approximately 9.4 million shares available for issuance under this plan.

On June 7, 2011 the Company entered into a sales agreement with JMP Securities LLC to, from time to time, publicly offer and sell up to 15,000,000 shares of the Company’s common stock in at-the-market transactions and/or privately negotiated transactions. As of June 30, 2011 the Company had not sold any common stock under the sales agreement. As of June 30, 2011, 15,000,000 shares of common stock remained available for issuance to be sold under the sales agreement.

7. MANAGEMENT AGREEMENT AND RELATED PARTY TRANSACTIONS

The Manager manages the Company’s day-to-day operations, subject to the direction and oversight of the Company’s board of directors. The Management Agreement was executed on February 10, 2006. The initial term of the Management Agreement expired on December 31, 2008, and it has been automatically renewed each year for a one-year term. The current term will expire on December 31, 2011. Going forward, the Management Agreement will be automatically renewed for a one-year term each anniversary date thereafter unless notice of non-renewal is given to the Company by the Manager. The Company’s independent directors review the Manager’s performance annually, and the Management Agreement may be terminated upon the affirmative vote of at least two-thirds of our independent directors, or by a vote of the holders of a majority of the outstanding shares of our common stock. In the event the Management Agreement is terminated as described above, the Company shall pay to the Manager a termination fee in accordance with the provisions of the Management Agreement. In the event the Company elects to internalize its management, the Management Agreement shall terminate without payment of any termination fee to the Manager.

The Management Agreement provides, among other things, that the Company pays to the Manager, in exchange for managing the day-to-day operations of the Company, certain fees and reimbursements, consisting of a base management fee and reimbursement for out-of-pocket and certain other costs incurred by the Manager and on behalf of the Company. The base management fee, which is paid monthly, was equal to 1/12 of (A) 1.50% of the first $250,000,000 of Net Assets (as defined in the Management Agreement), (B) 1.25% of such Net Assets that are greater than $250,000,000 and less than or equal to $500,000,000, and (C) 1.00% of such Net

21

Table of Contents

Assets that are greater than $500,000,000. The Company is also required to reimburse the Manager for its pro-rata portion of rent, utilities, legal and investment services, market information systems and research publications and materials. In addition, the Company recognized share-based compensation expense related to common stock options and restricted common stock granted to the Company’s executive officers and Manager Designees, which is included in related party management compensation on the statement of operations.

For the three and six months ended June 30, 2011 and 2010, the Company incurred the following in base management fees and expense reimbursement (in thousands):

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

| 2011 | 2010 | 2011 | 2010 | |||||||||||||

| Base Management Fees |

$ | 3,041 | $ | 987 | $ | 5,730 | $ | 1,924 | ||||||||

| Expense Reimbursement |

270 | 165 | 421 | 304 | ||||||||||||

| Total |

$ | 3,311 | $ | 1,152 | $ | 6,151 | $ | 2,228 | ||||||||

8. CONTINGENCIES

The Company enters into certain contracts that contain a variety of indemnifications, principally with the Manager and brokers. The maximum potential amount of future payment the Company could be required to make under these indemnification provisions is unknown. The Company has not incurred any costs to defend lawsuits or settle claims related to these indemnification agreements. As a result, the estimated fair value of these agreements is minimal. Accordingly, the Company has no liabilities recorded for these agreements as of June 30, 2011 and December 31, 2010.

9. FINANCIAL HIGHLIGHTS

In accordance with financial reporting requirements applicable to investment companies, the Company has included below certain financial highlight information for the three and six months ended June 30, 2011 and 2010:

| Per Share | ||||||||||||||||

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

| 2011 | 2010 | 2011 | 2010 | |||||||||||||

| Net asset value, beginning of period |

$ | 11.74 | $ | 13.03 | $ | 11.59 | $ | 13.02 | ||||||||

| Net income: |

||||||||||||||||

| Net investment income |

0.68 | (a) | 0.75 | (a) | 1.17 | (a) | 1.48 | (a) | ||||||||

| Net gain (loss) from investments and swap and cap contracts |

0.52 | (a) | 0.72 | (a) | 0.80 | (a) | 0.53 | (a) | ||||||||

| Net income |

1.20 | 1.47 | 1.97 | 2.01 | ||||||||||||

| Capital transactions: |

||||||||||||||||

| Distributions to shareholders |

(0.60 | ) | (0.60 | ) | (1.20 | ) | (1.15 | ) | ||||||||

| Issuance of common shares and amortization of related party management compensation |

0.01 | (a) | (0.75 | )(a) | (0.01 | )(a) | (0.73 | )(a) | ||||||||

| Net decrease in net asset value from capital transactions |

(0.59 | ) | (1.35 | ) | (1.21 | ) | (1.88 | ) | ||||||||

| Net asset value, end of period |

$ | 12.35 | $ | 13.15 | $ | 12.35 | $ | 13.15 | ||||||||

| Total return (%) |

10.31 | %(b) | 5.53 | %(b) | 16.91 | %(b) | 9.83 | %(b) | ||||||||

| Ratios to Average Net Assets |

||||||||||||||||

| Expenses before interest expense |

1.92 | %(c) | 3.21 | %(c) | 2.02 | %(c) | 3.39 | %(c) | ||||||||

| Total expenses |