Attached files

| file | filename |

|---|---|

| 8-K - FORM 8K - CNL LIFESTYLE PROPERTIES INC | d778803d8k.htm |

| EX-99.1 - PRESS RELEASE - CNL LIFESTYLE PROPERTIES INC | d778803dex991.htm |

CNL

Lifestyle Properties, Inc. CNL Lifestyle Properties, Inc.

Owning

Owning

America’s

America’s

Lifestyle

Lifestyle

®

®

Third Quarter 2014 Update

Third Quarter 2014 Update

November 14, 2014

November 14, 2014

Exhibit 99.2 |

2

Forward Looking Statements

Certain statements in this document may constitute forward-looking statements within the meaning

of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”) and

of Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). CNL Lifestyle Properties, Inc. (herein

also referred to as the “Company”) intends that all such forward-looking statements be

covered by the safe-harbor provisions for forward-looking statements of Section 27A of

the Securities Act and Section 21E of the Exchange Act, as applicable.

All statements, other than statements that relate solely to historical facts, including, among others,

statements regarding the Company’s future financial position, business strategy, projected

levels of growth, projected costs and projected financing needs, are forward-looking statements. Those statements

include statements regarding the intent, belief or current expectations of the management team, as

well as the assumptions on which such statements are based, and generally are identified by the

use of words such as “may,” “will,” “seeks,” “anticipates,” “believes,” “estimates,” “expects,” “plans,” “intends,”

“should,” “continues,” “pro forma” or similar expressions.

Forward-looking statements are not guarantees of future performance and actual results may differ

materially from those contemplated by such forward-looking statements due to a variety of risks,

uncertainties and other factors, including but not limited to, the factors detailed in our

Annual Report on Form 10-K for the year ended December 31, 2013, and other documents filed from time to time with the Securities

and Exchange Commission.

Many of these factors are beyond the Company’s ability to control or predict. Such factors

include, but are not limited to: changes in general economic conditions in the U.S. or globally

(including financial market fluctuations); risks associated with our investment strategy; risks associated with the real estate

markets in which the Company invests; risks of doing business internationally and global expansion,

including unfamiliarity with new markets and currency risks; risks associated with the use of

debt to finance the Company’s business activities, including refinancing and interest rate risk and the Company’s failure

to comply with its debt covenants; the Company’s failure to obtain, renew or extend necessary

financing or to access the debt or equity markets; competition for properties and/or tenants in

the markets in which the Company engages in business; the impact of current and future environmental, zoning and other

governmental regulations affecting the Company’s properties; the Company’s ability to make

necessary improvements to properties on a timely or cost- efficient basis; risks related to

development projects or acquired property value-add conversions, if applicable (including construction delays, cost overruns,

the Company’s inability to obtain necessary permits and/or public opposition to these

activities); defaults on or non-renewal of leases by tenants; failure to lease properties

at all or on favorable terms; unknown liabilities in connection with acquired properties or liabilities caused by property managers or operators;

the Company’s failure to successfully manage growth or integrate acquired properties and

operations; material adverse actions or omissions by any joint venture partners; increases in

operating costs and other expense items and costs, uninsured losses or losses in excess of the Company’s insurance coverage;

the impact of outstanding or potential litigation; risks associated with the Company’s tax

structuring; the Company’s failure to qualify and maintain its status as a real estate

investment trust and the Company’s ability to protect its intellectual property and the value of its brand. Management believes these forward-

looking statements are reasonable; however, such statements are necessarily dependent on assumptions,

data or methods that may be incorrect or imprecise and the Company may not be able to realize

them. Investors are cautioned not to place undue reliance on any forward-looking statements which are based

on current expectations. All written and oral forward-looking statements attributable to the

Company or persons acting on its behalf are qualified in their entirety by these cautionary

statements. Further, forward-looking statements speak only as of the date they are made and the Company undertakes no

obligation to update or revise forward-looking statements to reflect changed assumptions, the

occurrence of unanticipated events or changes to future operating results over time unless

otherwise required by law.

|

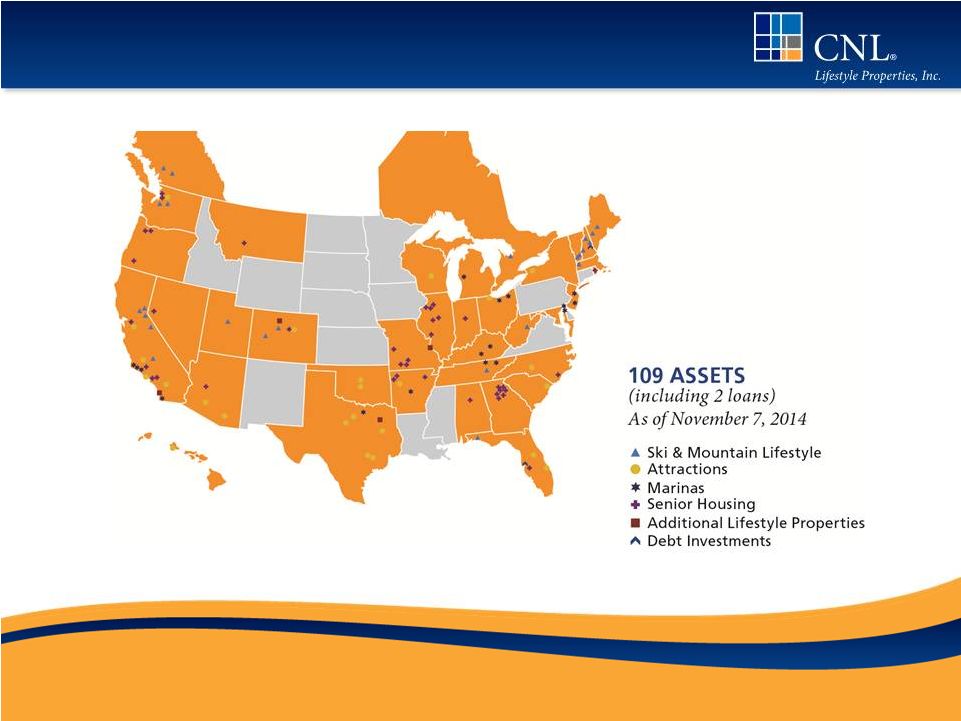

CNL

Lifestyle Properties, Inc. Portfolio of 107 lifestyle-oriented

properties and two loans as of

November 7, 2014

Diversified by asset type,

geography and operator

Iconic assets and industry-

leading operators

Summary REIT Information

GAAP Total Assets

$2.5 billion

Property Focus

Demographically Driven / Lifestyle-Oriented

Geographic

Diversification

34 states and 2 Canadian provinces

Established Assets

Conservative Capital Structure

Leasing and Preferred Return Structures

Diversified Portfolio

Exit Strategy

The Board of Directors is evaluating various

strategic alternatives to provide liquidity to

shareholders on or before December 31, 2015

Ski & Mountain

Attractions

Senior Housing

Marinas

Additional

•

24 properties

•

24 properties

•

38 properties

•

17 properties

•

4 properties

CNL Lifestyle Properties, Inc.

3 |

Recent Highlights

On September 30

th

, 46 of our 48 golf properties were sold and we received net

sales proceeds after closing costs totaling approximately $197 million -

after

retiring existing golf debt, the proceeds were primarily used to

retire other debt

Jefferies LLC, a leading global investment banking and advisory firm, is currently

assisting in the evaluation of various strategic alternatives to

provide liquidity to

shareholders

Acquired five senior housing communities in Q3 2014 totaling $101 million

Invested over $8 million of owner capital into various portfolio

assets, including

the Splashtown expansion

Year to date through September 30, 2014, our “same-store”

attraction properties

experienced an 8.3% increase in revenue and a 16.0% increase in EBITDA

Received $83 million in proceeds from the repayment of two notes

receivable

that matured in September and used proceeds to retire debt

4 |

Geographic Diversification

5 |

The portfolio is broadly diversified across asset classes to

mitigate against seasonality and volatility

Sector Diversification

As of November 7, 2014

By Initial Purchase Price

6

30%

25%

26%

7%

12% |

Sector Performance

7

Ski & Mountain

24 properties

Attractions

24 properties

Additional Lifestyle

4 properties

Senior Housing

38 properties

Marinas

17 properties

107 properties as of November 7, 2014

Source: CNL Lifestyle Properties, Inc. September 30, 2014, Form 10-Q

Past performance is not indicative of future returns.

-

Favorable weather

conditions drove

summer operations

(mountain biking and

aerial adventures) and

strong group and

conference business in

Q3 offset by higher

employee healthcare

costs.

-

Higher revenue and

EBITDA due to capital

improvements and

initiatives to drive

attendance. As a result,

the sector experienced

higher visitation, higher

season pass sales, and

higher in-park spending.

-

Both occupancy and

Revenue per Occupied

Unit were up over the last

year. Average occupancy

for the entire portfolio was

91.9% for the quarter

ended September 30,

2014, exceeding the

industry average of

90.5%. Higher average

resident rates offset by

higher resident care

expenses and R&M.

-

Revenue and EBITDA were

down slightly in Q3

compared to the prior year

due to property transitions

from leased to managed

structures. We expect

improved operating results in

the future after the initial

transition year.

-

Steady performance at

Dallas Market Center.

Refinancing existing debt

in October.

-

Includes two remaining

golf courses which we

expect to sell by the end

of 2014. |

Same-Store Property Performance

8

Note: Includes results for comparable consolidated leased and managed properties

owned for the entirety of 2014 and 2013. Source: CNL Lifestyle

Properties, Inc. September 30, 2014, Form 10-Q # of

Properties

Revenue

EBITDA

TTM Rent

Coverage

Ski and Mountain Lifestyle

17

6.2%

-11.2%

1.35x

Attractions

21

8.4%

10.0%

2.25x

Senior Housing

20

2.3%

-8.6%

1.17x

Marinas

17

-1.9%

-10.8%

n/a

Total

75

6.7%

6.5%

1.45x

# of

Properties

Revenue

EBITDA

Ski and Mountain Lifestyle

17

-2.2%

-6.7%

Attractions

21

8.3%

16.0%

Senior Housing

20

3.0%

-5.6%

Marinas

17

-4.3%

-17.4%

Total

75

1.8%

0.6%

Three Months Ended September 30, 2014, Compared to Same Period 2013

Nine Months Ended September 30, 2014, Compared to Same Period 2013

Ski and mountain lifestyle - favorable weather conditions for summer operations which include

mountain biking and aerial adventures, as well as strong group and conference business at

various resorts but was offset with higher health care costs when compared to 2013.

Sector down YTD due to warm winter temperatures and drought conditions at our California

properties. Attractions - increase in both revenue and EBITDA due to capital improvements made and

manager’s efforts to promote and drive attendance which resulted in an increase in season

pass sales and in-park spending. Year over year increase in visitation – 10.3%.

Senior housing - revenue increased due to higher average resident rates but was offset by higher

resident care expenses, repairs and maintenance expenses and other operating costs.

Marinas - transitioned from leased to managed structures during Q4 2013 and Q2 2014 resulting in

the incurrence of management fees reducing the operating margin on the properties. |

Full

Year Financial Summary (in Millions) 9

Source: CNL Lifestyle Properties, Inc. 2013 Form 10-K and September 30, 2014,

Form 10-Q The Company believes that its presentation of historical

non-GAAP financial measures provides useful supplementary information to and facilitates additional analysis by investors. These historical

non-GAAP financial measures are in addition to, not a substitute for, or

superior to, measures of financial performance prepared in accordance with U.S. Generally Accepted Accounting Principles.

See reconciliation to GAAP net income (loss) contained in the Appendix.

Past performance is not indicative of future returns.

Trailing 12 month 2014 FFO, MFFO and Adjusted EBITDA were

higher primarily due to:

An increase in rents from properties acquired after Q3 2013 and

increases in “same-store”

rents and NOI from managed properties

Reduced asset management fees due to the sale of 42 senior

housing properties held in three unconsolidated joint ventures and a

reduction in fees charged by our Advisor, effective April 1, 2014, as

well as a reduction in bad debt expense

Partially offset by an increase in interest expense from additional

borrowings, a loan loss provision and a reduction in income

contribution from the sale of 42 senior housing properties held in

three unconsolidated joint ventures

Adjusted EBITDA

FFO

MFFO |

Credit Metrics

(1) Calculated as adjusted EBITDA divided by interest

expense (2) Net debt is total debt less cash

(3) Debt includes line of credit

10

Source: CNL Lifestyle Properties, Inc. 2013 Form 10-K and September 30, 2014,

Form 10-Q The Company believes that its presentation of historical

non-GAAP financial measures provides useful supplementary information to and facilitates additional analysis by investors. These historical

non-GAAP financial measures are in addition to, not a substitute for, or

superior to, measures of financial performance prepared in accordance with U.S. Generally Accepted Accounting Principles.

See reconciliation to GAAP net income (loss) contained in the Appendix.

Past performance is not indicative of future returns.

Consolidated

Leverage Including Share

Year

Leverage

of Unconsolidated Entities

2011

32.0%

43.3%

2012

38.7%

45.3%

2013

44.6%

48.1%

Sept 2014

44.5%

47.8%

Interest Coverage (1)

Net Debt / Adjusted EBITDA (2)

Year

Coverage

2011

5.5x

2012

6.3x

2013

6.1x

Sep-14

4.2x

Year

Coverage

2011

2.4x

2012

2.5x

2013

2.6x

TTM Sept 2014

2.6x

Debt / GAAP Total Assets (3) |

Key

Credit Information 11

Weighted average interest rate is 5.65% (5.91% without JV debt)

71% fixed rate debt, 2% hedged and 27% variable rate debt

Note:

Chart

as

of

September

30,

2014.

2014

maturities

are

expected

to

be

refinanced

or

retired

with

proceeds

from

asset

sales.

DMC

JV

was refinanced in Q4 with a one year short term loan.

|

Contact Information

12

For more information about

CNL Lifestyle Properties, please contact

CNL Client Services at 866-650-0650. |

Appendix

13

Appendix |

Reconciliation of FFO and MFFO to Net Income

(Loss)

14

Source: CNL Lifestyle Properties, Inc. September 30, 2014, Form 10-Q

The Company believes that its presentation of historical non-GAAP financial

measures provides useful supplementary information to and facilitates additional analysis by investors. These historical

non-GAAP financial measures are in addition to, not a substitute for, or

superior to, measures of financial performance prepared in accordance with U.S. Generally Accepted Accounting Principles.

2014

2013

2014

2013

Net income (loss)

30,623

$

78,293

$

1,765

$

(211)

$

Adjustments:

Depreciation and amortization:

Continuing operations

33,622

30,731

96,691

88,588

Discontinued operations

-

7,618

4,891

22,577

Impairment of real estate assets:

Continuing operations

-

2,740

-

45,191

Discontinued operations

-

-

4,464

-

Gain on sale of unconsolidated entities:

-

-

Continuing operations

-

(55,394)

-

(55,394)

Gain on sale of real estate investment:

Discontinued operations

(3,953)

(2)

(3,883)

(2,085)

Net effect of FFO adjustment from unconsolidated entities:

Continuing operations

3,819

1,484

12,208

11,820

Total funds from operations

64,111

65,470

116,136

110,486

Acquisition fees and expenses:

Continuing operations

509

1,009

2,513

1,922

Straight-line adjustments for leases and notes receivable:

Continuing operations

4,617

(1,633)

(1,547)

(2,675)

Discontinued operations

-

(291)

-

(827)

Loss from extinguishment of debt:

Continuing operations

1,682

-

2,282

-

Discontinued operations

8,293

-

8,028

-

Contingent purchase price consideration adjustment

Continuing operations

(665)

-

(665)

-

Amortization of above/below market intangible assets and liabilities

Continuing operations

89

(1)

113

(3)

Discontinued operations

-

350

359

1,033

Loan loss provision:

Continuing operations

750

-

3,270

-

Accretion of discounts/amortization of premiums:

Continuing operations

44

3

50

9

MFFO adjustments from unconsolidated entities:

Straight-line adjustment for leases and notes receivable:

Continuing operations

113

(29)

175

(175)

Amortization of above/below market intangible assets and

liabilities: Continuing operations

(41)

47

(116)

39

Modified funds from operations

79,502

$

64,925

$

130,598

$

109,809

$

Weighted average number of shares of common stock

325,707

319,507

324,194

317,960

outstanding (basic and diluted)

FFO per share (basic and diluted)

0.20

$

0.20

$

0.36

$

0.35

$

MFFO per share (basic and diluted)

0.24

$

0.20

$

0.40

$

0.35

$

Quarter Ended

September 30,

Nine Months Ended

September 30,

Past performance is not indicative of future returns.

1. This amount represents our share of the FFO or MFFO adjustments allowable under the NAREIT

or IPA definitions, respectively, multiplied by the percentage of income or loss recognized

under the HLBV method. 2. In evaluating

investments in real estate, management differentiates the costs to acquire the investment from

the operations derived from the investment. By adding back acquisition fees and expense

relating to business combinations, management believes MFFO provides useful supplemental

information of its operating performance and will also allow comparability between real estate

entities regardless of their level of acquisition activities. Acquisition fees and expenses

include payments to our advisor or third parties. Acquisition fees and expenses relating to business

combinations under GAAP are considered operating expenses and as expenses included in the

determination of net income (loss) and income (loss) from continuing operations, both of which

are performance measures under GAAP. All paid and accrued acquisition fees and expenses will

have negative effects on returns to investors, the potential for future distributions, and cash

flows generated by us, unless earnings from operations or net sales proceeds from the

disposition of properties are generated to cover the purchase price of the property. 3. Under GAAP, rental

receipts are allocated to periods using various methodologies. This may result in income

recognition that is significantly different than underlying contract terms. By adjusting for

these items (to reflect such payments from a GAAP accrual basis to a cash basis of disclosing

the rent and lease payments), MFFO provides useful supplemental information on the realized

economic impact of lease terms and debt investments, providing insight on the contractual cash

flows of such lease terms and debt investments, and aligns results with management’s analysis of

operating performance. 4. Loss from early

extinguishment of debt includes swap breakage fees, write-off of unamortized loan costs and

reclassification of loss on termination of cash flow hedges from other comprehensive income

(loss) into interest expense.

5. We recorded a loan loss provision on one of our mortgages and other notes receivable as a

result of uncertainty related to the collectability of the note receivable. 6. Management believes

that the elimination of the contingent purchase price consideration adjustment, which

represents the Yield Guarantee, included in interest and other income (expense) for GAAP

purposes is appropriate because the adjustment is a non-recurring, non-cash adjustment

that is not reflective of our ongoing operating performance and aligns results with management’s

analysis of operating performance. (1)

(2)

(3)

(4)

(6)

(5)

(1)

(3) |

Reconciliation of Adjusted EBITDA to Net

Income (Loss)

15

Source: CNL Lifestyle Properties, Inc. September 30, 2014, Form 10-Q

The Company believes that its presentation of historical non-GAAP financial

measures provides useful supplementary information to and facilitates additional analysis by investors. These historical non-GAAP

financial measures are in addition to, not a substitute for, or superior to,

measures of financial performance prepared in accordance with U.S. Generally Accepted Accounting Principles.

Past performance is not indicative of future returns.

2014

2013

2014

2013

Net income (loss)

30,623

$

78,293

$

1,765

$

(211)

$

(Income) loss from discontinued operations

1,380

4,036

(1,188)

8,275

Interest and other income

(775)

13

(866)

(504)

Bargain purchase gain on acquisition of real estate

(4)

-

(2,653)

-

(2,653)

Interest expense and loan cost amortization

18,556

15,852

57,322

48,513

Equity in earnings of unconsolidated entities

(1)

(3,176)

(4,147)

(6,949)

(9,183)

Gain on sale of unconsolidated entities

(3)

-

(55,394)

-

(55,394)

Depreciation and amortization

33,622

30,731

96,691

88,587

Impairment provision

-

2,740

-

45,191

Loss from extinguishment of debt

1,620

-

1,816

-

Loan loss provision

750

-

3,270

-

Recovery on lease terminations

-

-

(741)

-

Straight-line adjustments for leases and notes receivables

(2)

4,617

(1,924)

(1,547)

(3,502)

Cash distributions from unconsolidated entities

(1)

3,321

3,177

9,896

23,290

Adjusted EBITDA

90,538

$

70,724

$

159,469

$

142,409

$

Quarter Ended

September 30,

Nine Months Ended

September 30,

1. Investments in our unconsolidated joint ventures are accounted for under the HLBV method of

accounting. Under this method, we recognize income or loss based on the change in liquidating proceeds we

would receive from a hypothetical liquidation of our investments based on depreciated book value. We

adjust EBITDA for equity in earnings (loss) of our unconsolidated entities because we believe this is not

reflective of the joint ventures’ operating performance or cash flows available for distributions

to us. We believe cash distributions from our unconsolidated entities, exclusive of any financing transactions, are

reflective of their operating performance and its impact to us and have been added back to adjusted

EBITDA above. For the quarter and nine months ended September 30, 2013, cash distributions from

unconsolidated entities excludes approximately $5.3 million in return of capital.

2. We believe that adjusting for straight-line adjustments for leased properties and

mortgages and other notes receivable is appropriate because they are non-cash adjustments and reflect the actual cash

receipts received by us from our tenants and borrowers.

3. In July 2013, we completed the sale of our interests in 42 senior housing properties held

through three unconsolidated joint ventures. See “Distributions from Unconsolidated Entities” above for additional

information.

4. In connection with an acquisition of an attraction property, we recorded a bargain purchase

gain as a result of the fair value of the net assets acquired exceeding the consideration transferred as discussed

above.. |