Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended: December 31, 2010

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 000-51288

CNL LIFESTYLE PROPERTIES, INC.

(Exact name of registrant as specified in its charter)

| Maryland | 20-0183627 | |

| (State of other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| 450 South Orange Avenue Orlando, Florida |

32801 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (407) 650-1000

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of exchange on which registered | |

| None |

Not applicable |

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $0.01 par value per share

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (229.05 of this Chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ |

Accelerated filer ¨ | |

| Non-accelerated filer x |

Smaller reporting company ¨ | |

| (Do not check if a smaller reporting company) |

||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

While there is no established market for the registrant’s shares of common stock, the registrant has an ongoing primary offering of its shares of common stock pursuant to a registration statement on Form S-11. In each of its primary offerings, the registrant sold shares of its common stock for $10.00 per share, with discounts available for certain categories of purchasers. The number of shares held by non-affiliates as of June 30, 2010 (the last business day of the registrant’s most recently completed second fiscal quarter) was approximately 262,971,959.

As of March 10, 2011, there were 293,530,034 shares of the registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Registrant incorporates by reference portions of the CNL Lifestyle Properties, Inc. Definitive Proxy Statement for the 2011 Annual Meeting of Stockholders (Items 10, 11, 12, 13 and 14 of Part III) to be filed no later than April 30, 2011.

Table of Contents

Table of Contents

STATEMENT REGARDING FORWARD LOOKING INFORMATION

The following information contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These statements generally are characterized by the use of terms such as “may,” “will,” “should,” “plan,” “anticipate,” “estimate,” “intend,” “predict,” “believe” and “expect” or the negative of these terms or other comparable terminology. Although we believe that the expectations reflected in such forward-looking statements are based upon reasonable assumptions, our actual results could differ materially from those set forth in the forward-looking statements. Some factors that might cause such a difference include the following: continued or worsening economic environment, the lack of available debt for us and our tenants, including our inability to refinance existing debt, the general decline in value of real estate, conditions affecting the CNL brand name, increased direct competition, changes in government regulations or accounting rules, changes in local and national real estate conditions, our ability to obtain additional lines of credit or long-term financing on satisfactory terms, changes in interest rates, availability of proceeds from our offering of shares, availability of capital to expand and enhance our properties, our tenants’ inability to increase revenues or manage rising costs, our ability to identify suitable investments, our ability to close on identified investments, our ability to locate suitable tenants and operators for our properties and borrowers for our loans, tenant or borrower defaults under their respective leases or loans, tenant or borrower bankruptcies and inaccuracies of our accounting estimates. Given these uncertainties, we caution you not to place undue reliance on such statements. We undertake no obligation to publicly release the results of any revisions to these forward-looking statements that may be made to reflect future events or circumstances or to reflect the occurrence of unanticipated events.

| Item 1. | Business |

GENERAL

CNL Lifestyle Properties, Inc. is a Maryland corporation organized on August 11, 2003. We operate as a real estate investment trust, or REIT. The terms “us,” “we,” “our,” “our company” and “CNL Lifestyle Properties” include CNL Lifestyle Properties, Inc. and each of our subsidiaries. We have retained CNL Lifestyle Company, LLC, (the “Advisor”), as our Advisor to provide management, acquisition, disposition, advisory and administrative services. Our offices are located at 450 South Orange Avenue within the CNL Center at City Commons in Orlando, Florida 32801.

Our principal investment objectives include investing in a diversified portfolio of real estate with a goal to preserve, protect and enhance the long-term value of those assets. We primarily invest in lifestyle properties in the United States that we believe have the potential for long-term growth and income generation. Our investment thesis is supported by demographic trends which we believe affect consumer demand for the various lifestyle asset classes that are the focus of our investment strategy. We define lifestyle properties as those properties that reflect or are impacted by the social, consumption and entertainment values and choices of our society. We primarily lease our properties on a long-term, triple-net or gross basis (generally five to 20 years, plus multiple renewal options) to tenants or operators that we consider to be significant industry leaders. To a lesser extent, we also make and acquire loans (including mortgage, mezzanine and other loans), enter into joint ventures related to interests in real estate and engage third-party operators to manage certain properties on our behalf as permitted under applicable tax regulations.

Following our investment policies of acquiring carefully selected and well-located lifestyle and other income producing properties, we believe we have built a unique portfolio of assets with established long-term operating histories, and have created balanced diversification within the portfolio by region, operator and asset class. We will continue to focus on select acquisitions of income producing properties that we believe will enhance the portfolio and provide long-term value to our stockholders, while also concentrating on the management and oversight of our existing portfolio. We have also maintained a strong balance sheet and cash position with a low leverage ratio.

1

Table of Contents

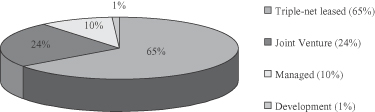

While we have primarily acquired wholly owned properties subject to long-term triple-net leases, we also make investments in properties through joint ventures, and to a lesser extent, engaged third-party operators to manage certain properties on our behalf. The following represents our types of property investments by number of total properties as of March 10, 2011:

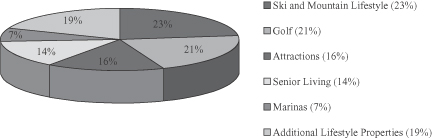

Asset classes and portfolio diversification. As of March 10, 2011, we had a portfolio of 150 lifestyle properties which when aggregated by initial purchase price was diversified as follows: approximately 23% in ski and mountain lifestyle, 21% in golf facilities, 14% in senior living, 16% in attractions, 7% in marinas and 19% in additional lifestyle properties. These assets consist of 22 ski and mountain lifestyle properties, 53 golf facilities, 29 senior living facilities, 21 attractions, 17 marinas and eight additional lifestyle properties. Thirty-seven of these 150 properties are owned through unconsolidated entities. Many of our properties feature characteristics that are common to more than one asset class, such as a ski resort with a golf facility. Our asset classifications are based on the primary property usage. The pie chart below shows our asset class diversification as of March 10, 2011, by initial purchase price.

2

Table of Contents

Our real estate investment portfolio is geographically diversified with properties in 32 states and two Canadian provinces. The map below shows our current property allocations across geographic regions as of March 10, 2011.

Our tenants and operators. We generally attempt to lease our properties to tenants and operators that we consider to be significant industry leaders. However, we do not believe the success of our properties is based solely on the performance or abilities of our tenant operators. In some cases, we consider the assets we have acquired to be unique, iconic or nonreplicable which by their nature have an intrinsic value. In addition, in the event a tenant is in default and vacates a property, under special provisions in the tax laws we are able to engage a third-party manager to operate the property on our behalf for a period of time until we re-lease it to a new tenant. During this period, the property remains open and we receive any net earnings from the property’s operations, although these amounts may be less than the rents that were contractually due under the prior leases. Any taxable income from these properties will be subject to income tax until we re-lease these properties to new tenants.

Our leases and ventures. As part of our net lease investment strategy, we either acquire properties directly or purchase interests in entities that own the properties. Once we acquire the properties, we either lease them back to the original seller or to a third-party operator. These leases are usually structured as triple-net leases which means our tenants are generally responsible for repairs, maintenance, property taxes, ground lease or permit expenses (where applicable), utilities and insurance for the properties that they lease. The weighted-average lease rate of our consolidated properties subject to long-term triple-net leases as of December 31, 2010 was approximately 8.8%. This rate is based on the weighted-average annualized straight-lined base rent due under our leases.

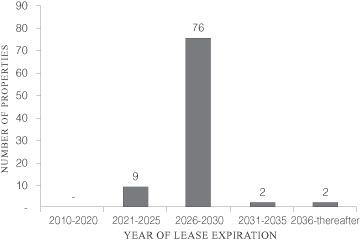

Our leases are generally long-term in nature (generally five to 20 years with multiple renewal options). We have no near-term lease expirations (other than at our one multi-family residential property, which generally

3

Table of Contents

enters into one-year leases with its tenants) with the first long-term lease expiring in December 2021, excluding available renewal periods. As of March 10, 2011, the average lease expiration of our portfolio (excluding our multi-family residential property and our unconsolidated properties) was approximately 17 years with the following breakdown:

We typically structure our leases to provide for the payment of a minimum annual base rent with periodic increases in base rent over the lease term. In addition, our leases provide for the payment of percentage rent normally based on a percentage of gross revenues generated at the property over certain thresholds. Within the provisions of our leases, we also generally require the payment of capital improvement reserve rent. Capital improvement reserves are paid by the tenant and are generally based on a percentage of gross revenue of the property and are set aside by us for capital improvements, replacements and other capital expenditures at the property. These amounts are and will remain our property during and after the term of the lease and help maintain the integrity of our assets.

To a lesser extent, when beneficial to our investment structure, certain properties may be leased to wholly-owned tenants that are taxable REIT subsidiaries or that are owned through taxable REIT subsidiaries (referred to as “TRS” entities). Under this structure, we engage third-party managers to conduct day-to-day operations. Under the TRS leasing structure, our results of operations will include the operating results of the underlying properties as opposed to rental income from operating leases that is recorded for properties leased to third-party tenants.

We have entered into joint ventures in which our partners subordinate their returns to our minimum return. This structure provides us with some protection against the risk of downturns in performance but may allow our partners to obtain a higher rate of return on their investment than we receive if the underlying performance of the properties exceeds certain thresholds. As of March 10, 2011, we had a total of 37 properties owned through three unconsolidated joint ventures.

Our managed properties. In certain circumstances, and subject to applicable tax regulations, we may engage third-party operators to manage properties on our behalf. For example, when beneficial to our investment structure, we may engage third-party operators to manage hotels and senior living properties under the TRS leasing structure. In addition, in the case of a tenant default and lease termination, we may engage a third-party manager to operate the property on our behalf for a period of time until we can re-lease the property. This allows us time to stabilize the property, if necessary, and enter into a new lease when market conditions are potentially more favorable. During this managed period, we recognize all the underlying property operating revenues and expenses in our consolidated financial statements and may be subject to more direct operating risk. As of March 10, 2011, we had 23 managed properties including four hotels, two golf courses, 16 attractions and one multi-family residential property.

4

Table of Contents

Our loans. As part of our overall investment and lending strategy, we have made and may continue to make or acquire loans (including mortgage, mezzanine or other loans) with respect to any of the asset classes in which we invest. We generally make loans to the owners of properties to enable them to acquire land, buildings, or both, or to develop property or as part of a larger acquisition. In exchange, the owner generally grants us a first lien or collateralized interest in a participating mortgage collateralized by the property or by interests in the entity that owns the property. Our loans generally require fixed interest payments. We expect that the interest rate and terms for long-term mortgage loans (generally, 10 to 20 years) will be similar to the rate of return on our long-term net leases. Mezzanine loans and other financings for which we have a secondary-lien or collateralized interest will generally have shorter terms (one to two years) and higher interest rates than our net leases and long-term mortgage loans. With respect to the loans that we make, we generally seek loans with collateral values resulting in a loan-to-value ratio of not more than 85%.

Our common stock offerings. As of December 31, 2010, we had raised approximately $3.0 billion (301.2 million shares) through our public offerings. During the period January 1, 2011 through March 10, 2011, we raised an additional $88.3 million (8.8 million shares). We have and will continue to use the net proceeds from our offerings to make select investments. We do not intend to commence another public offering of our shares following the completion of our current public offering on April 9, 2011. However, we intend to continue offering shares through our reinvestment plan. In making this decision, the board of directors considered a number of factors, including the Company’s size and diversification of our portfolio, our relatively low leverage and strong cash position, as well as the current stage of our lifecycle.

Seasonality. Many of the asset classes in which we invest are seasonal in nature and experience seasonal fluctuations in their business due to geographic location, climate and weather patterns. As a result, the businesses experience seasonal variations in revenues that may require our operators to supplement operating cash from their properties in order to be able to make scheduled rent payments to us. We have structured the leases for certain tenants such that rents are paid on a seasonal schedule with most, if not all, of the rent being paid during the tenant’s seasonally busy operating period.

As part of our diversification strategy, we have considered the varying and complimentary seasonality of our asset classes and portfolio mix. For example, the peak operating season of our ski and mountain lifestyle assets is staggered against the peak seasons in our attractions and golf portfolios to balance and mitigate the risks associated with seasonality. Generally seasonality does not significantly affect our recognition of rental income from operating leases due to straight-line revenue recognition in accordance with Generally Accepted Accounting Principles (“GAAP”). However, seasonality does impact the timing of when base rent payments are made by our tenants, which impacts our operating cash flows and the amount of rental revenue we recognize in connection with capital improvement reserve revenue and percentage rents paid by our tenants, which is recognized in the period in which it is earned and is generally based on a percentage of tenant revenues. In addition, seasonality directly impacts properties where we engage third-party operators to manage on our behalf and where we record property operating revenues and expenses rather than straight-line rents from operating leases. These properties will likely generate net operating losses during their non-peak months while generating most, if not all, of their operating income during their peak operating season. Our consolidated operating results and cash flows will fluctuate quarter to quarter depending on the number and types of properties being managed by third-party operators and the seasonal results of those properties.

Competition. As a REIT, we have historically experienced competition from other REITs (both traded and non-traded), real estate partnerships, mutual funds, institutional investors, specialty finance companies, opportunity funds, healthcare providers, and other investors, including, but not limited to, banks and insurance companies, many of which generally have had greater financial resources than we do for the purposes of leasing and financing properties within our targeted asset classes. These competitors often also have a lower cost of capital and are subject to less regulation. The level of competition impacts both our ability to raise capital, find real estate investments and locate suitable tenants. We may also face competition from other funds in which affiliates of our Advisor participate or advise.

5

Table of Contents

In general, we perceive there to be a lower level of competition for the types of assets that we have acquired and intend to acquire in comparison to assets in core real estate sectors based on the number of willing buyers and the volume of transactions in their respective markets. Accordingly, we believe that being focused in specialty or lifestyle asset classes allows us to take advantage of unique opportunities. Some of our key competitive advantages are as follows:

| • | We acquire assets in niche sectors which historically trade at higher cap rates than other core commercial real estate sectors such as Apartment, Industrial, Office and Retail. |

| • | Some of our targeted assets classes, such as golf and ski, have experienced a net reduction in new supply, which has better equalized supply and demand. |

| • | Certain of our lifestyle properties have inherently high barriers to entry. For example, the process of obtaining permits to create a new ski resort or marina is highly regulated and significantly more difficult than obtaining permits for the construction of new office or retail space. Additionally, general geographic constraints, such as the availability of suitable waterfront property or mountain terrain, are an inherent barrier to entry in several of our asset classes. There are also high costs associated with building a new ski resort or regional gated attractions that may be prohibitive to potential market participants. |

| • | Our leasing arrangements generally require the payment of capital improvement reserve rent which is paid by the tenants and set aside by us to be reinvested into the properties. This arrangement allows us to maintain the integrity of our properties and mitigates deferred maintenance issues. |

| • | Unlike our competitors in many other commercial real estate sectors that generally receive no income in the event a tenant defaults or vacates a property, applicable tax laws allow us to engage a third-party manager to operate a property on our behalf for a period of time until we can re-lease it to a new tenant. During that period, we receive any net earnings from the underlying business operations, which may be less than rents collected under the previous leasing arrangement. However, our ability to continue to operate the property under such an arrangement helps to off-set taxes, insurance and other operating costs that would otherwise have to be absorbed by a landlord and allows the property some time to stabilize, if necessary, before entering into a new lease. |

Significant tenants and borrowers. As of December 31, 2010 and 2009 and for the three years ended through December 31, 2010, we had the following tenants that individually accounted for 10% or more of our aggregate total revenues or assets.

| Tenant |

Number & Type of Leased |

Percentage of Total Revenues |

Percentage of Total Assets |

|||||||||||||||||||

| 2010 | 2009 | 2008 | 2010 | 2009 | ||||||||||||||||||

| PARC Management, LLC (“PARC”)(1) |

— (1) | 11.0 | %(1) | 18.3 | % | 21.0 | % | — | (1) | 14.3 | % | |||||||||||

| Boyne USA, Inc. (“Boyne”) |

7 Ski & Mountain | 12.6 | % | 15.3 | % | 19.4 | % | 8.8 | % | 9.2 | % | |||||||||||

| Lifestyle Properties | ||||||||||||||||||||||

| Evergreen Alliance Golf Limited, L.P. (“EAGLE”) |

43 Golf Facilities | 12.1 | % | 14.3 | % | 20.6 | % | 14.6 | % | 15.4 | % | |||||||||||

| Booth Creek Ski Holding, Inc.(2) (“Booth”) |

1 Ski & Mountain | 1.8 | % | 8.3 | % | 12.2 | % | 1.2 | % | 6.3 | % | |||||||||||

| Lifestyle Property | ||||||||||||||||||||||

FOOTNOTES:

| (1) | As of December 31, 2010, we were in the process of transitioning all of our properties previously leased to PARC to new third-party managers. This process was completed in February 2011 and PARC is no longer a tenant of the Company. |

6

Table of Contents

| (2) | On October 25, 2010, Vail Resorts Inc. acquired 100% of the equity interest in the companies that operate Northstar-at-Tahoe Resort and The Village at Northstar from Booth Creek Resort Properties LLC and became our tenant under the existing leases on the properties. |

The significance of any given tenant or operator, and the related concentration of risk generally decrease as additional properties and operators are added to the portfolio. As shown above, there were only two tenants that individually accounted for 10% or more of our total revenues or assets as of December 31, 2010.

Tax status. We currently operate and have elected to be taxed as a REIT for federal income tax purposes beginning with the taxable year ended December 31, 2004. As a REIT, we generally will not be subject to federal income tax at the corporate level to the extent we distribute annually at least 90% of our taxable income to our stockholders and meet other compliance requirements. If we fail to qualify as a REIT in any taxable year, we will be subject to federal income tax on our taxable income at regular corporate rates and will not be permitted to qualify for treatment as a REIT for federal income tax purposes for four years following the year in which our qualification is lost.

Recent tax legislation. On October 18, 2010, the IRS published final regulations that require us to report the cost basis and gain or loss to a stockholder upon the sale or liquidation of “covered shares.” For purposes of the final regulations, all shares acquired by non-tax exempt stockholders on or after January 1, 2011 will be considered “covered shares” and will be subject to the new reporting requirement. In addition, beginning on January 1, 2012, all shares acquired by non-tax exempt stockholders through our Distribution Reinvestment Plan (DRP) will also be considered “covered shares.”

Upon the sale or liquidation of “covered shares,” a broker must report both the cost basis of the shares and the gain or loss recognized on the sale of those shares to the stockholder and to the IRS on Form 1099-B. In addition, effective January 1, 2011, S-corporations will no longer be exempt from Form 1099-B reporting and shares purchased by an S-corporation on or after January 1, 2012 will be “covered shares” under the final regulations. If we take an organizational action such as a stock split, merger, acquisition or return of capital distribution that affects the cost basis of “covered shares,” we will report to each stockholder and to the IRS a description of any such action and the quantitative effect of that action on the cost basis on an information return.

We have elected the first in, first out (FIFO) method as the default for calculating the cost basis and gain or loss upon the sale or liquidation of “covered shares”. A non-tax exempt stockholder may elect a different method of computation until the settlement date of the sold or liquidated shares. The election must be made in writing. Stockholders should consult with their tax advisors to determine the appropriate method of accounting for their investment.

Recently enacted legislation will require, after December 31, 2012, withholding at a rate of 30% on dividends in respect of, and gross proceeds from the sale of, shares of our stock held by or through certain foreign financial institutions (including investment funds), unless such institution enters into an agreement with the Secretary of the Treasury to report, on an annual basis, information with respect to shares in the institution held by certain U.S. persons and by certain non-U.S. entities that are wholly or partially owned by U.S. persons and to withhold on certain payments. Accordingly, the entity through which shares of stock is held will affect the determination of whether such withholding is required. Similarly, dividends in respect of, and gross proceeds from the sale of, shares of our stock held by an investor that is a non-financial non-U.S. entity will be subject to withholding at a rate of 30%, unless such entity either (i) certifies to us that such entity does not have any “substantial United States owners” or (ii) provides certain information regarding the entity’s “substantial United States owners,” which we will in turn provide to the Secretary of the Treasury. We will not pay any additional amounts to any stockholders in respect of any amounts withheld. Foreign persons are encouraged to consult with their tax advisors regarding the possible implications of the legislation on their investment in shares of our stock.

On March 30, 2010, the President signed into law the Health Care and Education Reconciliation Act of 2010, which requires U.S. stockholders who meet certain requirements and are individuals, estates or certain

7

Table of Contents

trusts to pay an additional tax on, among other things, dividends on and capital gains from the sale or other disposition of stock for taxable years beginning after December 31, 2012. U.S. stockholders should consult their tax advisors regarding the effect, if any, of this legislation on their ownership and disposition of shares of our stock.

FINANCIAL INFORMATION ABOUT INDUSTRY SEGMENTS

Our current business consists of investing in, owning and leasing lifestyle properties primarily in the United States. We evaluate all of our lifestyle properties as a single industry segment and review performance on a property-by-property basis. Accordingly, we do not report segment information.

FINANCIAL INFORMATION ABOUT GEOGRAPHIC AREAS

We have one consolidated property located in British Columbia, Canada, Cypress Mountain, that generated total rental income of approximately $6.3 million for both of the years ended December 31, 2010 and 2009 and $6.7 million for the year ended December 31, 2008. We also own interests in two properties located in Canada through unconsolidated entities that generated a combined equity in earnings of approximately $0.1 million during the year ended December 31, 2010 and a combined equity in losses of approximately $0.3 million and $0.2 million during the years ended December 31, 2009 and 2008, respectively. The remainder of our rental income was generated from properties or investments located in the United States.

ADVISORY SERVICES

We have engaged CNL Lifestyle Company, LLC as our Advisor. Under the terms of the advisory agreement, our Advisor is responsible for our day-to-day operations, administers our bookkeeping and accounting functions, serves as our consultant in connection with policy decisions to be made by our board of directors, manages our properties, loans, and other permitted investments and renders other services as the board of directors deems appropriate. In exchange for these services, our Advisor is entitled to receive certain fees from us. First, for supervision and day-to-day management of the properties and the mortgage loans, our Advisor receives an asset management fee, which is payable monthly, in an amount equal to 0.08334% per month based on the total real estate asset value of a property as defined in the advisory agreement (exclusive of acquisition fees and acquisition expenses), the outstanding principal amounts of any loans made by us and the amount invested in any other permitted investments as of the end of the preceding month. Second, for the selection, purchase, financing, development, construction or renovation of real properties and services related to the incurrence of debt, our Advisor receives an acquisition fee equal to 3% of the gross proceeds from our common stock offerings and loan proceeds from debt, lines of credit and other permanent financing that we use to acquire properties or to make or acquire loans and other permitted investments.

In addition, we reimburse our Advisor for all of the costs it incurs in connection with the administrative services it provides to us. However, in accordance with the advisory agreement, our Advisor is required to reimburse us for the amount by which the total operating expenses (as described in the advisory agreement) incurred by us in any four consecutive fiscal quarters (the “Expense Year”) exceed the greater of 2% of average invested assets or 25% of net income (the “Expense Cap”). For the Expense Years ended December 31, 2010, 2009 and 2008, operating expenses did not exceed the Expense Cap.

The current advisory agreement continues until March 22, 2011, and was extended by unanimous consent of our board of directors through April 9, 2011, at which time we will engage CNL Lifestyle Advisor Corporation (the “New Advisor”) as our advisor and enter into an advisory agreement with substantially similar terms and services as those provided under our current advisory agreement. The current directors and officers of the Advisor will be elected and appointed as the directors and officers of the New Advisor and will have similar responsibilities and roles with the New Advisor as they currently hold with the Advisor except as otherwise noted in Item 9B. of this filing. In addition, the New Advisor will continue to engage and contract with other affiliates of our current advisor to cause those affiliates to provide services and personnel to perform duties on behalf of the Company.

8

Table of Contents

LEGAL AND REGULATORY CONSIDERATIONS

General. Our properties are subject to various laws, ordinances and regulations, including regulations relating to common areas. We believe that each of our properties as of December 31, 2010 has the necessary permits and approvals to operate its business.

Americans with Disabilities Act. Our U.S. properties must comply with Title III of the Americans with Disabilities Act of 1990, or the ADA, to the extent that such properties are “public accommodations” as defined by the ADA. The ADA may require removal of structural barriers to access by persons with disabilities in certain public areas of our properties where such removal is readily achievable. We believe that our properties are in substantial compliance with the ADA and that we will not be required to make substantial capital expenditures to address the requirements of the ADA. However, noncompliance with the ADA could result in imposition of fines or an award of damages to private litigants. The obligation to make readily achievable accommodations is an ongoing one, and we will continue to assess our properties and to make alterations as appropriate in this respect.

Environmental, Health, and Safety Matters. We are subject to many federal, state, and local environmental, health, and safety laws. The applicability of specific environmental, health, and, safety laws to each of our individual properties is dependent upon a number of property-specific factors, including: the current and former uses of the property; any impacts to the property from other properties; the type and amount of any emissions or discharges from or releases at the property; the building materials used at the property, including any asbestos-containing materials; and, among other factors, the type and amount of any hazardous substances or wastes used, stored, or generated at the property.

Under various laws relating to protection of the environment, current and former owners and operators of real property may be liable for any contamination resulting from the presence or release of hazardous or toxic substances at the property. Current and former owners and operators may also be held liable to the government or to third parties for property damage and for investigation and remediation costs related to contamination, regardless of whether the owners and operators were responsible for or even knew of the contamination, and the liability may be joint and several. The government may be entitled to a lien on a contaminated property. Certain environmental laws, as well as the common law, may subject us to liability for damages or injuries suffered by third parties as a result of environmental contamination or releases originating at our properties, including releases of asbestos, and the liabilities associated with our properties could exceed the values of the respective properties. Some of our properties were previously used for industrial purposes, and those properties may contain some degree of contamination. Environmental impacts or contamination at our properties may prevent us from selling or leasing the properties or using them as collateral. Environmental laws may regulate the use of our properties or the types of operations which can be conducted at our properties, and these regulations may necessitate corrective or other expenditures.

Some of our properties may contain asbestos-containing building materials. Asbestos-containing building materials are subject to management and maintenance requirements under environmental laws, and owners and operators may be subject to penalty for noncompliance. Environmental laws may allow suits by third parties for recovery from owners and operators for personal injury related to exposure to asbestos-containing building materials.

Prior to the purchase of our properties, we generally engaged independent environmental consultants to perform Phase I environmental assessments, which normally do not involve soil, groundwater or other invasive sampling. When Phase I environmental assessment results indicated the need to do so, we conducted Phase II assessments, which do involve invasive sampling. These assessments have not revealed any materially adverse environmental conditions which impact or have impacted our properties other than conditions which have been remediated or are currently undergoing remediation. There can be no assurance, however, that new environmental liabilities have not developed since the assessments were performed, that the assessment failed to reveal material adverse environmental conditions, liabilities, or compliance concerns, or that future developments, including changes in laws or regulations, will not impose environmental costs or liabilities upon

9

Table of Contents

us. If we become subject to material environmental liabilities, these liabilities could adversely effect us, our business and assets, the results of our operations, and our ability to meet our obligations.

Insurance. We maintain, or cause operators to maintain, insurance including, but not limited to, liability, fire, wind, earthquake, and business income coverage on all of our properties that are not being leased on a triple-net basis under various policies. We select policy specifications and insured limits which we believe to be appropriate given the relative risk of loss, the cost of the coverage and industry practice and, in the opinion of our company’s management, our properties that are not being leased on a triple-net basis are currently adequately insured. We do not carry insurance for generally uninsured losses such as loss from war or nuclear reaction. Certain of our properties are located in areas known to be seismically active. See “Risk Factors—Risks Related to Our Business and Operations—Potential losses may not be covered by insurance.”

EMPLOYEES

Reference is made to Item 10. “Directors, Executive Officers and Corporate Governance” in our Definitive Proxy Statement for a listing of our executive officers. We have no employees. Our executive officers are compensated through our advisor and/or its affiliates.

AVAILABLE INFORMATION

We make available free of charge on our Internet website, www.cnllifestylereit.com, our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and, if applicable, amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, as soon as reasonably practicable after we electronically file such material with, or furnish it to, the U.S. Securities and Exchange Commission (the “Commission”). The public may read and copy any materials that we file with the Commission at the Commission’s Public Reference Room at Room 1580, 100 F Street, N.E., Washington, D.C. 20549 and may obtain information on the Public Reference Room by calling the Commission at 1-800-SEC-0330. The Commission maintains an internet site that contains reports, proxy and information statements, and other information that we file electronically with the Commission (http://www.sec.gov).

10

Table of Contents

| Item 1A. | Risk Factors |

Real Estate and Other Investment Risks

The economic environment and general market conditions in recent years have affected certain of the lifestyle properties in which we invest. A continuation of such conditions could adversely affect our financial condition and results of operations. The recent economic and market conditions have affected the value and operating performance of certain of our properties which resulted in tenant defaults, losses on lease terminations, loan loss provisions and impairments charges. Continued or worsening global economic conditions including unemployment rates, the effects of unrest in the Middle East and rising oil prices, inflationary risks and rising costs, and a lack of consumer confidence with decreased consumer spending could result in additional losses to us and have a negative impact on our results of operations and our ability to pay distributions to our stockholders.

The economic environment has affected certain of our tenants’ ability to make rental payments to us in accordance with their lease agreement. Some of our tenants have experienced difficulties or have been unable to obtain working capital lines of credit or renew their existing lines of credit due to current state of economy and the capital markets which impacted their ability to pay the full amount of rent due under their leases. As a result, we restructured the leases for certain tenants such that the rents are paid on a seasonal schedule with most, if not all, of the rent being paid during the tenants’ seasonally busy period. In other cases, we restructured the lease terms to allow for rent deferrals or reductions for a period of time to provide temporary relief that then become payable in later periods of the lease term. In addition, we have refunded security deposits which must be replaced up to specified amounts and have provided lease allowances. The rent deferrals granted, the security deposits refunded and lease allowances paid directly reduced our cash flows from operating activities. Other restructures, such as the reductions in lease rates and the future amortization of lease allowances against rental income have reduced and will continue to reduce our net operating results and cash flows in current and future periods.

Our operating results will experience seasonal fluctuations on properties in which we have engaged third-party managers to operate the properties on our behalf. In certain circumstances, we have engaged third-party managers to operate the properties on our behalf as a result of tenant defaults or utilizing the TRS leasing structure. In these situations, we recognize the properties’ operating revenues and expenses in our consolidated financial statements and may be subject to more direct operating risk. In addition, certain of our managed properties are seasonal in nature due to geographic location, climate and weather patterns. These properties will likely generate net operating losses during their non-peak months while generating most, if not all, of their operating income during their peak operating season. Our consolidated operating results will fluctuate quarter to quarter depending on the number and types of properties being managed by third-party operators and the seasonal results of those properties.

We will be exposed to various operational risks, liabilities and claims with respect to the properties that we engage third-party managers to operate on our behalf which may adversely affect our operating results. With respect to the properties that are managed by third-party operators, we are exposed to various operational risk, liabilities and claims in addition to those generally applicable to ownership of real property. These risks include the operator’s inability to manage the properties and fulfill its obligations, increases in labor costs and services, cost of energy, insurance, operating supplies and litigation costs relating to accidents or injuries at the properties. Although we maintain reasonable levels of insurance, we cannot be certain the insurance will adequately cover all litigation costs relating to accidents or inquires. Any one or a combination of these factors, together with other market and conditions beyond our control, could result in operating deficiencies at our managed properties which could have a material effect on our operating results.

Because our revenues are highly dependent on lease payments from our properties and interest payments from loans that we make, defaults by our tenants or borrowers would reduce our cash available for the repayment of our outstanding debt and for distributions. Our ability to repay any outstanding debt and make distributions to stockholders will depend upon the ability of our tenants and borrowers to make payments to us,

11

Table of Contents

and their ability to make these payments will depend primarily on their ability to generate sufficient revenues in excess of operating expenses from businesses conducted on our properties. For example, the ability of our tenants to make their scheduled payments to us will depend upon their ability to generate sufficient operating income at the property they operate. A tenant’s failure or delay in making scheduled rent payments to us or a borrower’s failure to make debt service payments to us may result from the tenant or borrower realizing reduced revenues at the properties it operates.

Discretionary consumer spending may affect the profitability of certain properties we acquire. The financial performance of certain properties in which we have invested and may invest in the future depends in part on a number of factors relating to or affecting discretionary consumer spending for the types of services provided by businesses operated on these properties. Unfavorable local, regional, or national economic developments or uncertainties regarding future economic prospects have reduced consumer spending in the markets where we own properties and, when combined with the lack of available debt, have adversely affected certain of our tenants’ businesses. As a result, certain of our tenants have experienced declines in operating results, and a number of our tenants have modified the terms of certain of their leases with us. Any continuation of such events that leads to lower spending on lifestyle activities could impact our tenants’ ability to pay rent and thereby have a negative impact on our results of operations.

The inability to increase or maintain lease rates at our properties might affect the level of distributions to stockholders. Given the nature of certain properties we have acquired or may acquire, the relative stagnation of base lease rates in certain sectors might not allow for substantial increases in rental revenue to us that could allow us to maintain or increase levels of distributions to stockholders.

Seasonal revenue variations in certain asset classes will require the operators of those asset classes to manage cash flow properly over time so as to meet their non-seasonal scheduled rent payments to us. Certain of the properties in which we invest or may invest are generally seasonal in nature due to geographic location, climate and weather patterns. For example, revenue and profits at ski resorts and their related properties are substantially lower and historically result in losses during the summer months due to the closure of ski operations, while many attractions properties are closed during the winter months and produce the majority of their revenues and profits during summer months. As a result of the seasonal nature of certain business operations that may be conducted on properties we acquire, these businesses will experience seasonal variations in revenues that may require our operators to supplement revenue at their properties in order to be able to make scheduled rent payments to us or require us to, in certain cases, adjust their lease payments so that we collect more rent during their seasonally busy time.

Our real estate assets may be subject to impairment charges. We periodically evaluate the recoverability of the carrying value of our real estate assets for impairment indicators. Factors considered in evaluating impairment of our existing real estate assets held for investment include significant declines in property operating profits, recurring property operating losses and other significant adverse changes in general market conditions. Generally, a real estate asset held for investment is not considered impaired if the undiscounted, estimated future cash flows of the asset over its estimated holding period are in excess of the asset’s net book value at the balance sheet date. Investments in unconsolidated entities are not considered impaired if the estimated fair value of the investment exceeds the carrying value of the investment and the decline is considered to be other than temporary. Management makes assumptions and estimates when considering impairments and actual results could vary materially from these assumptions and estimates.

We do not have control over market and business conditions that may affect our success. The following external factors, as well as other factors beyond our control, may reduce the value of properties that we acquire, the ability of tenants to pay rent on a timely basis, or at all, the amount of the rent to be paid and the ability of borrowers to make loan payments on time, or at all:

| • | changes in general or local economic or market conditions; |

12

Table of Contents

| • | the pricing and availability of debt, operating lines of credit or working capital; |

| • | increased costs of energy, insurance or products; |

| • | increased costs and shortages of labor; |

| • | increased competition; |

| • | quality of management; |

| • | failure by a tenant to meet its obligations under a lease; |

| • | bankruptcy of a tenant or borrower; |

| • | the ability of an operator to fulfill its obligations; |

| • | limited alternative uses for properties; |

| • | changing consumer habits; |

| • | condemnation or uninsured losses; |

| • | changing demographics; and |

| • | changing government regulations. |

Further, the results of operations for a property in any one period may not be indicative of results in future periods, and the long-term performance of such property generally may not be comparable to, and cash flows may not be as predictable as, other properties owned by third parties in the same or similar industry. If tenants are unable to make lease payments or borrowers are unable to make loan payments as a result of any of these factors, cash available for distributions to our stockholders may be reduced.

Our exposure to typical real estate investment risks could reduce our income. Our properties, loans and other permitted investments will be subject to the risks typically associated with investments in real estate. Such risks include the possibility that our properties will generate rent and capital appreciation, if any, at rates lower than we anticipated or will yield returns lower than those available through other investments or that the value of our properties will decline. Further, there are other risks by virtue of the fact that our ability to vary our portfolio in response to changes in economic and other conditions will be limited because of the general illiquidity of real estate investments. Income from our properties may be adversely affected by many factors including, but not limited to, an increase in the local supply of properties similar to our properties, a decrease in the number of people interested in participating in activities related to the businesses conducted on the properties that we acquire, adverse weather conditions, changes in government regulation, international, national or local economic deterioration, increases in energy costs and other expenses affecting travel, factors which may affect travel patterns and reduce the number of travelers and tourists, increases in operating costs due to inflation and other factors that may not be offset by increased revenue, and changes in consumer tastes.

If one or more of our tenants file for bankruptcy protection, we may be precluded from collecting all sums due. If one or more of our tenants, or the guarantor of a tenant’s lease, commences, or has commenced against it, any proceeding under any provision of the U.S. federal bankruptcy code, as amended, or any other legal or equitable proceeding under any bankruptcy, insolvency, rehabilitation, receivership or debtor’s relief statute or law (“Bankruptcy Proceeding”), we may be unable to collect sums due under our lease(s) with that tenant. Any or all of the tenants, or a guarantor of a tenant’s lease obligations, could be subject to a Bankruptcy Proceeding. A Bankruptcy Proceeding may bar our efforts to collect pre-bankruptcy debts from those entities or their properties unless we are able to obtain an enabling order from the bankruptcy court. If a lease is rejected by a tenant in bankruptcy, we would only have a general unsecured claim against the tenant, and may not be entitled to any further payments under the lease. We believe that our security deposits in the form of letters of credit would be protected from bankruptcy in most jurisdictions. However, a tenant’s or lease guarantor’s Bankruptcy Proceeding could hinder or delay efforts to collect past due balances under relevant leases or guarantees and

13

Table of Contents

could ultimately preclude collection of these sums. Such an event could cause a decrease or cessation of rental payments which would reduce our cash flow and the amount available for distribution to our stockholders. In the event of a Bankruptcy Proceeding, we cannot assure you that the tenant or its trustee will assume our lease. If a given lease, or guaranty of a lease, is not assumed, our cash flow and the amounts available for distribution to our stockholders may be adversely affected.

Multiple property leases or loans with individual tenants or borrowers increase our risks in the event that such tenants or borrowers become financially impaired. The value of our properties will depend principally upon the value of the leases entered into for properties that we acquire. Defaults by a tenant or borrower may continue for some time before we determine that it is in our best interest to terminate the lease or foreclose on the property of the borrower. Tenants may lease more than one property, and borrowers may enter into more than one loan. As a result, a default by, or the financial failure of, a tenant or borrower could cause more than one property to become vacant or be in default or more than one lease or loan to become non-performing. Defaults or vacancies can reduce and have reduced our cash receipts and funds available for distribution and could decrease the resale value of affected properties until they can be re-leased.

It may be difficult for us to exit a joint venture after an impasse. In our joint ventures, there will be a potential risk of impasse in some business decisions because our approval and the approval of each co-venturer may be required for some decisions. In any joint venture, we may have the right to buy the other co-venturer’s interest or to sell our own interest on specified terms and conditions in the event of an impasse regarding a sale. In the event of an impasse, it is possible that neither party will have the funds necessary to complete a buy-out. In addition, we may experience difficulty in locating a third-party purchaser for our joint venture interest and in obtaining a favorable sale price for the interest. As a result, it is possible that we may not be able to exit the relationship if an impasse develops.

The current U.S. housing market may adversely affect our operators’ and tenants’ ability to increase or maintain occupancy levels at, and rental income from, our senior living facilities which may impact the amount of distributions and earnings we received from our unconsolidated venture that owns senior living facilities. Our tenants and operators in our senior living facilities may experience relatively flat or declining occupancy levels in the near-term due to falling home prices, declining incomes, stagnant home sales and other economic factors. Seniors may choose to postpone their plans to move into senior living facilities rather than sell their homes at a loss, or for a profit below their expectations. Moreover, tightening lending standards have made it more difficult for potential buyers to obtain mortgage financing, all of which have contributed to the declining home sales. Any future rise in interest rates may compound or prolong this problem. In addition, the senior living segment may continue to experience a decline in occupancy associated with private pay residents choosing to move out of the facilities to be cared for at home by relatives due to the weak economy. A material decline in occupancy levels and revenues may make it more difficult for them to meet scheduled rent payments to us, which could adversely affect our financial condition.

Events which adversely affect the ability of seniors to afford our daily resident fees could cause the occupancy rates, resident fee revenues and results of operations of our senior living facilities to decline. Costs to seniors associated with certain types of the senior living properties generally are not reimbursable under government reimbursement programs such as Medicaid and Medicare. Substantially all of the resident fee revenues generated by our facilities will be derived from private payment sources consisting of income or assets of residents or their family members. Only seniors with income or assets meeting or exceeding certain standards can typically afford to pay our daily resident and service fees and, in some cases, entrance fees. Economic downturns such as the one recently experienced in the United States, reductions or declining growth of government entitlement programs, such as social security benefits, or stock market volatility could adversely affect the ability of seniors to afford the fees for our senior living facilities. If our tenants or managers are unable to attract and retain seniors with sufficient income, assets or other resources required to pay the fees associated with assisted and independent living services, the occupancy rates, resident fee revenues and results of operations for these facilities could decline, which, in turn, could have a material adverse effect on our business.

14

Table of Contents

We may be unable to identify and complete acquisitions on favorable terms or at all. We continually evaluate the market of available properties and may acquire additional lifestyle properties when opportunities exist. Our ability to acquire properties on favorable terms may be subject to the following significant risks:

| • | we may be unable to acquire a desired property because of competition from other real estate investors with significant capital, including both publicly traded REITs and institutional investment funds; |

| • | even if we are able to acquire a desired property, competition from other potential acquirors may significantly increase the purchase price or result in other less favorable terms; |

| • | even if we enter into agreements for the acquisition of desired lifestyle properties, these agreements are typically subject to customary conditions to closing, including completion of due diligence investigations to our satisfaction; |

| • | we may be unable to finance acquisitions on favorable terms or at all; and |

| • | we may acquire properties subject to liabilities and without any recourse, or with only limited recourse, with respect to unknown liabilities such as liabilities for clean-up of undisclosed environmental contamination, claims by tenants, vendors or other persons dealing with the former owners of the properties and claims for indemnification by general partners, directors, officers and others indemnified by the former owners of the properties. |

If we cannot complete property acquisitions on favorable terms, our financial condition, results of operations, cash flow, cash available for distribution and ability to satisfy our debt service obligations could be materially adversely affected.

The real estate industry is capital intensive and we are subject to risks associated with ongoing needs for renovation and capital improvements to our properties as well as financing for such expenditures. In order for us to remain competitive, our properties will have an ongoing need for renovations and other capital improvements, including replacements, from time to time, of furniture, fixtures and equipment. These capital improvements may give rise to the following risks:

| • | construction cost overruns and delays; |

| • | a possible shortage of available cash to fund capital improvements and the related possibility that financing for these capital improvements may not be available to us on satisfactory terms; and |

| • | disruptions in the operation of the properties while capital improvements are underway. |

We will not control the management of our properties. In order to maintain our status as a REIT for federal income tax purposes, we may not operate certain types of properties we acquire or participate in the decisions affecting their daily operations. Our success, therefore, will depend on our ability to select qualified and creditworthy tenants and managers who can effectively manage and operate the properties. Our tenants will be responsible for maintenance and other day-to-day management of the properties and, because our revenues will largely be derived from rents, our financial condition will be dependent on the ability of third-party tenants and/or operators to operate the properties successfully. We will attempt to enter into leasing agreements with tenants having substantial prior experience in the operation of the type of property being rented, however, there can be no assurance that we will be able to make such arrangements. Additionally, if we elect to treat property we acquire as a result of a borrower’s default on a loan or a tenant’s default on a lease as “foreclosure property” for federal income tax purposes, we will be required to operate that property through an independent contractor over whom we will not have control. If our tenants or third-party operators are unable to operate the properties successfully or if we select unqualified managers, then such tenants and operators might not be able to pay our rent, or generate sufficient property-level operating income for us, which could adversely affect our financial condition.

Joint venture partners may have different interests than we have, which may negatively impact our control over our ventures. Investments in joint ventures involve the risk that our co-venturer may have economic or

15

Table of Contents

business interests or goals which, at a particular time, are inconsistent with our interests or goals, that the co-venturer may be in a position to take action contrary to our instructions, requests, policies or objectives, or that the co-venturer may experience financial difficulties and be unable to fund its share of required capital contributions. Among other things, actions by a co-venturer might subject assets owned by the joint venture to liabilities in excess of those contemplated by the terms of the joint venture agreement or to other adverse consequences. This risk is also present when we make investments in securities of other entities. If we do not have full control over a joint venture, the value of our investment will be affected to some extent by a third party that may have different goals and capabilities than ours. As a result, joint ownership of investments and investments in other entities may adversely affect our returns on investments and, therefore, cash available for distributions to our stockholders may be reduced.

Adverse weather conditions may damage certain properties we acquire and/or reduce our operators’ ability to make scheduled rent payments to us. Weather conditions may influence revenues at certain types of properties we acquire. These adverse weather conditions include heavy snowfall (or lack thereof), hurricanes, tropical storms, high winds, heat waves, frosts, drought (or reduced rainfall levels), excessive rain, avalanches, mudslides and floods. Adverse weather could reduce the number of people participating in activities at properties we acquire and have acquired. Certain properties may be susceptible to damage from weather conditions such as hurricanes, which may cause damage (including, but not limited to property damage and loss of revenue) that is not generally insurable at commercially reasonable rates. Further, the physical condition of properties we acquire must be satisfactory to attract visitation. In addition to severe or generally inclement weather, other factors, including, but not limited to plant disease and insect infestation, as well as the quality and quantity of water, could adversely affect the conditions at properties we own and acquire or develop. Most properties have some insurance coverage that will offset such losses and fund needed repairs.

Potential losses may not be covered by insurance. We maintain, or cause our operators to maintain, insurance including, but not limited to, liability, fire, wind, earthquake and business income coverage on all of our properties that are not being leased on a triple-net basis under various insurance policies. We select policy specifications and insured limits which we believe to be appropriate and adequate given the relative risk of loss, the cost of the coverage and industry practice. We do not carry insurance for generally uninsured losses such as loss from riots, terrorist threats, war or nuclear reaction. Most of our policies, like those covering losses due to floods, are insured subject to limitations involving large deductibles or co-payments and policy limits which may not be sufficient to cover losses. While we carry earthquake insurance on our properties that are not being leased on a triple-net basis, the amount of our earthquake insurance coverage may not be sufficient to fully cover losses from earthquakes. In addition, we may discontinue earthquake or other insurance on some or all of our properties in the future if the cost of premiums for any of these policies exceeds, in our judgment, the value of the coverage relative to the risk of loss.

Our operating results may be negatively affected by potential development and construction delays and resultant increased costs and risks. We may invest in properties upon which we will develop and construct improvements. We will be subject to risks relating to uncertainties associated with re-zoning for development and environmental concerns of governmental entities and/or community groups, and our ability to control construction costs or to build in conformity with plans, specifications and timetables. Our performance also may be affected or delayed by conditions beyond our control. Moreover, delays in completion of construction also could give tenants the right to terminate preconstruction leases for space at a newly developed project. Furthermore, we must rely upon projections of rental income, expenses and estimates of the fair market value of property upon completion of construction before agreeing to a property’s purchase price. If our projections are inaccurate, we may pay too much for a property and our return on our investment could suffer.

If we set aside insufficient reserves for capital expenditures, we may be required to defer necessary property improvements. If we do not have enough reserves for capital expenditures to supply needed funds for capital improvements throughout the life of the investment in a property, and there is insufficient cash available from our operations, we may be required to defer necessary improvements to the property that may cause the property to suffer from a greater risk of obsolescence, a decline in value and/or a greater risk of decreased cash flow as a

16

Table of Contents

result of attracting fewer potential tenants to the property and adversely affecting our tenants’ businesses. If we lack sufficient capital to make necessary capital improvements, then we may not be able to maintain projected rental rates for certain properties, and our results of operations and ability to pay distributions to our stockholders may be negatively impacted.

We may be required to defer property expansion during the foreclosure period after tenant’s default. In cases where a tenant has defaulted and we have foreclosed on the leases and engaged a third-party manager to operate the property for a period of time, we are prohibited by tax regulations from conducting any new construction during the foreclosure period to expand these properties. The inability to continue to expand certain of our properties may reduce the competitiveness of the properties and result in declining revenues and operating income. This may impact properties’ value and the level of distributions we can pay.

Our failure or the failure of the tenants and managers of our facilities to comply with licensing and certification requirements, the requirements of governmental programs, fraud and abuse regulations or new legislative developments may materially adversely affect the operations of our senior living properties. The operations of our senior living properties are subject to numerous federal, state and local laws and regulations that are subject to frequent and substantial changes resulting from legislation, adoption of rules and regulations, and administrative and judicial interpretations of existing laws. The ultimate timing or effect of any changes in these laws and regulations cannot be predicted. Failure to obtain licensure or loss or suspension of licensure or certification may prevent a facility from operating or result in a suspension of certain revenue sources until all licensure or certification issues have been resolved. Facilities may also be affected by changes in accreditation standards or procedures of accrediting agencies that are recognized by governments in the certification process. State laws may require compliance with extensive standards governing operations and agencies administering those laws regularly inspect such facilities and investigate complaints. Failure to comply with all regulatory requirements could result in the loss of the ability to provide or bill and receive payment for health care services at our senior living facilities. Additionally, transfers of operations of certain senior living facilities are subject to regulatory approvals not required for transfers of other types of commercial operations and real estate. We may have no direct control over the tenant’s or manager’s ability to meet regulatory requirements and failure to comply with these laws, regulations and requirements may materially adversely affect the operations of these properties.

Cost control and other health care reform measures may reduce reimbursement revenue available to certain of our senior living properties. The health care industry is facing various challenges, including increased government and private payor pressure on health care providers to control costs and the vertical and horizontal consolidation of health care providers. The pressure to control health care costs has intensified in recent years as a result of the national health care reform debate and has continued as Congress attempts to slow the rate of growth of federal health care expenditures as part of its effort to balance the federal budget. Similar debates are ongoing at the state level in many states. These trends are likely to lead to reduced or slower growth in reimbursement for services provided at some of our senior living properties and could therefore result in reduced profitability of such properties, adversely affecting our income or results from investments in such properties.

Each year, legislative proposals are introduced or proposed in Congress and in some state legislatures that would effect major changes in the health care system, nationally or at the state level. We cannot predict whether any proposals will be adopted or, if adopted, what effect, if any, these proposals would have on those of our senior living facilities offering health care services and, thus, our business. Health care, including the long-term care and assisted living sectors, remains a dynamic, evolving industry. On March 23, 2010, the Patient Protection and Affordable Care Act of 2010 was enacted and on March 30, 2010, the Health Care and Education Reconciliation Act was enacted, which in part modified the Patient Protection and Affordable Care Act. Together, the two Acts serve as the primary vehicle for comprehensive health care reform in the United States. The two Acts are intended to reduce the number of individuals in the United States without health insurance and effect significant other changes to the ways in which health care is organized, delivered and reimbursed. The legislation will become effective in a phased approach, beginning in 2010 and concluding in 2018. At this time,

17

Table of Contents

the effects of the legislation and its impact on our business are not yet known. Our business could be materially and adversely affected by the two Acts and further governmental initiatives undertaken pursuant to the two Acts.

We may incur significant costs complying with the Americans with Disabilities Act and similar laws. Under the Americans with Disabilities Act of 1990, or the ADA, all public accommodations must meet federal requirements related to access and use by disabled persons. We have not conducted an audit or investigation of all of our properties to determine our compliance with the ADA. If one or more of our properties does not comply with the ADA, then we would be required to incur additional costs to bring the property into compliance. Additional federal, state and local laws also may require modifications to our properties, or restrict our ability to renovate our properties. We cannot predict the ultimate cost of compliance with the ADA or other legislation. If we incur substantial costs to comply with the ADA and any other similar legislation, our financial condition, results of operations, cash flow, cash available for distribution and ability to satisfy our debt service obligations could be materially adversely affected.

Lending Related Risks

Our loans may be affected by unfavorable real estate market conditions. When we make loans, we are at risk of default on those loans caused by many conditions beyond our control, including local and other economic conditions affecting real estate values and interest rate levels. We do not know whether the values of the properties collateralizing mortgage loans will remain at the levels existing on the dates of origination of the loans. If the values of the underlying properties drop or in some instances fail to rise, our risk will increase and the value of our interests may decrease.

Foreclosures create additional ownership risks that could adversely impact our returns on mortgage investments. When we acquire property by foreclosure following defaults under our mortgage, bridge or mezzanine loans, we have the economic and liability risks as the owner of such property. This additional liability could adversely impact our returns on mortgage investments.

Our loans will be subject to interest rate fluctuations. If we invest in fixed-rate, long-term loans and interest rates rise, the loans will yield a return lower than then-current market rates. If interest rates decrease, we will be adversely affected to the extent that loans are prepaid, because we will not be able to make new loans at the previously higher interest rate.

Lack of principal amortization of loans increases the risk of borrower default at maturity and delays in liquidating defaulted loans could reduce our investment returns and our cash available for distributions. Certain of the loans that we have made do not require the amortization of principal during their term. As a result, a substantial amount of, or the entire principal balance of such loans, will be due in one balloon payment at their maturity. Failure to amortize the principal balance of loans may increase the risk of a default during the term, and at maturity of loans. In addition, certain of our loans have or may have a portion of the interest accrued and payable upon maturity. We may not receive any of that accrued interest if our borrower defaults. A default under loans could have a material adverse effect on our ability to pay distributions to stockholders. Further, if there are defaults under our loans, we may not be able to repossess and sell the underlying properties or other security quickly. The resulting time delay could reduce the value of our investment in the defaulted loans. An action to foreclose on a mortgaged property securing a loan is regulated by state statutes and rules and is subject to many of the delays and expenses of other lawsuits if the defendant raises defenses or counterclaims. In the event of default by a mortgagor, these restrictions, among other things, may impede our ability to foreclose on or sell the mortgaged property or to obtain proceeds sufficient to repay all amounts due on our loan. Any failure or delay by a borrower in making scheduled payments to us may adversely affect our ability to make distributions to stockholders.