Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended June 30, 2014.

Or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission File Number 000-51171

EPIRUS BIOPHARMACEUTICALS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 04-3514457 | |

| (State or other jurisdiction of Incorporation or organization) |

(IRS Employer Identification Number) |

| 699 Boylston Street Eleventh Floor Boston, MA |

02116 | |

| (Address of Principal Executive Offices) | (Zip Code) |

(617) 600-4313

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | ¨ | Smaller reporting company | x | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

Number of shares of the registrant’s Common Stock, $0.001 par value per share, outstanding as of August 11, 2014: 12,926,593 shares

Table of Contents

EPIRUS BIOPHARMACEUTICALS, INC.

QUARTERLY REPORT ON

FORM 10-Q

INDEX

| PART I FINANCIAL INFORMATION | ||||||

| Item 1. |

2 | |||||

| Item 2. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

14 | ||||

| Item 3. |

22 | |||||

| Item 4. |

22 | |||||

| PART II OTHER INFORMATION | ||||||

| Item 1. |

24 | |||||

| Item 1A. |

24 | |||||

| Item 5. |

43 | |||||

| Item 6. |

63 | |||||

i

Table of Contents

FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q includes statements with respect to EPIRUS Biopharmaceuticals, Inc. and its subsidiaries (“Epirus,” “we,” “our,” “us” or the “Company”), which constitute “forward-looking statements” within the meaning of the safe harbor provisions of the United States Private Securities Litigation Reform Act of 1995. Words such as “believe,” “anticipate,” “expect,” “estimate,” “intend,” “plan,” “project,” “will be,” “will continue,” “will result,” “seek,” “could,” “may,” “might,” or any variations of such words or other words with similar meanings are intended to identify such forward-looking statements. Forward-looking statements in this Quarterly Report on Form 10-Q include, without limitation, statements regarding our future expectations; statements concerning product candidate development (including clinical and preclinical development), manufacturing and commercialization plans and timelines and related regulatory matters; any projections of financing needs, revenue, expenses, earnings or losses from operations, or other financial items; statements of the plans, strategies and objectives of management for future operations; any statements regarding safety and efficacy of product candidates; statements regarding our plans for partnerships, collaborations or other strategic transactions; any statements of expectation or belief; and any statements regarding other matters that involve known and unknown risks, uncertainties and other factors that may cause actual results, levels of activity, performance or achievements to differ materially from results expressed in or implied by this Quarterly Report on Form 10-Q.

The risks, uncertainties and assumptions referred to above include risks that are described in Part II, Item 1A of this Quarterly Report on Form 10-Q in the section entitled “Risk Factors”. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this Quarterly Report on Form 10-Q. We specifically disclaim any obligation to update these forward-looking statements in the future, except as required by law.

MERGER WITH OLD EPIRUS

On July 15, 2014, EPIRUS Biopharmaceuticals, Inc., formerly known as Zalicus Inc., a Delaware corporation (“Epirus,” “we,” “our,” “us” or the “Company”) consummated the Merger, as defined and described below, with the former entity EPIRUS Biopharmaceuticals, Inc., a Delaware corporation and private company (“Old Epirus”). Except as described in Note 13, “Subsequent Event,” the accompanying unaudited condensed consolidated financial statements do not give effect to the Merger. The historical financial statements have been labeled Zalicus Inc. for the purposes of this filing, which was the entity name in effect for the historical periods presented.

PRESENTATION FOR REVERSE STOCK SPLITS

On September 18, 2013, our board of directors unanimously approved a 1-for-6 reverse stock split of our common stock, which we effected on October 3, 2013. On July 15, 2014, our board of directors unanimously approved a 1-for-10 reverse stock split of our common stock, which we effected on July 16, 2014. All share and per share amounts of common stock, options and warrants in this Quarterly Report on Form 10-Q, including those amounts included in the accompanying condensed consolidated financial statements, have been restated for all periods to give retroactive effect to both the October 3, 2013 reverse stock split and the July 16, 2014 reverse stock split.

1

Table of Contents

Item 1. Condensed Consolidated Financial Statements—Unaudited

Zalicus Inc.

Condensed Consolidated Balance Sheets

(in thousands, except per share data)

(Unaudited)

| June 30, 2014 | December 31, 2013 |

|||||||

| Assets |

||||||||

| Current assets: |

||||||||

| Cash and cash equivalents |

$ | 14,396 | $ | 17,958 | ||||

| Restricted cash |

50 | 50 | ||||||

| Accounts receivable |

119 | 2,511 | ||||||

| Prepaid expenses and other current assets |

309 | 223 | ||||||

|

|

|

|

|

|||||

| Total current assets |

14,874 | 20,742 | ||||||

| Property and equipment, net |

— | 2,363 | ||||||

| Intangible asset, net |

— | 7,200 | ||||||

| Restricted cash and other assets |

1,800 | 1,801 | ||||||

|

|

|

|

|

|||||

| Total assets |

$ | 16,674 | $ | 32,106 | ||||

|

|

|

|

|

|||||

| Liabilities and stockholders’ equity |

||||||||

| Current liabilities: |

||||||||

| Accounts payable |

$ | 387 | $ | 2,237 | ||||

| Accrued expenses and other current liabilities |

1,543 | 3,339 | ||||||

| Deferred revenue |

— | 2,392 | ||||||

| Current portion of term loan payable |

— | 6,640 | ||||||

| Current portion of lease incentive obligation |

— | 284 | ||||||

|

|

|

|

|

|||||

| Total current liabilities |

1,930 | 14,892 | ||||||

| Term loan payable, net of current portion |

— | 2,132 | ||||||

| Deferred rent, net of current portion |

— | 309 | ||||||

| Lease incentive obligation, net of current portion |

— | 591 | ||||||

| Other liability |

430 | — | ||||||

| Stockholders’ equity: |

||||||||

| Preferred stock, $0.001 par value; 5,000 shares authorized; no shares issued and outstanding |

— | — | ||||||

| Common stock, $0.001 par value; 200,000 shares authorized; 2,611 and 2,609 shares issued and outstanding at June 30, 2014 and December 31, 2013, respectively |

3 | 3 | ||||||

| Additional paid-in capital |

394,400 | 393,819 | ||||||

| Accumulated deficit |

(380,089 | ) | (379,640 | ) | ||||

|

|

|

|

|

|||||

| Stockholders’ equity |

14,314 | 14,182 | ||||||

|

|

|

|

|

|||||

| Total liabilities and stockholders’ equity |

$ | 16,674 | $ | 32,106 | ||||

|

|

|

|

|

|||||

The accompanying notes are an integral part of the condensed consolidated financial statements.

2

Table of Contents

Zalicus Inc.

Condensed Consolidated Statements of Operations and Comprehensive Loss

(in thousands, except share and per share amounts)

(Unaudited)

| Three months ended June 30, | Six months ended June 30, | |||||||||||||||

| 2014 | 2013 | 2014 | 2013 | |||||||||||||

| Revenue: |

||||||||||||||||

| Royalties |

$ | — | $ | 1,713 | $ | — | $ | 3,145 | ||||||||

| cHTS services and other collaborations |

1,132 | 2,178 | 2,735 | 4,420 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total revenue |

1,132 | 3,891 | 2,735 | 7,565 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating expenses: |

||||||||||||||||

| Research and development |

2,143 | 9,845 | 5,224 | 16,924 | ||||||||||||

| General and administrative |

2,987 | 2,059 | 4,997 | 4,101 | ||||||||||||

| Amortization of intangible |

— | 2,180 | — | 4,361 | ||||||||||||

| Loss on exit of facility |

1,407 | — | 1,407 | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total operating expenses |

6,537 | 14,084 | 11,628 | 25,386 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Loss from operations |

(5,405 | ) | (10,193 | ) | (8,893 | ) | (17,821 | ) | ||||||||

| Interest income |

1 | 14 | 3 | 37 | ||||||||||||

| Interest expense |

— | (393 | ) | (86 | ) | (833 | ) | |||||||||

| Gain on divestiture of cHTS business |

8,645 | — | 8,645 | — | ||||||||||||

| Loss on early extinguishment of debt |

— | — | (217 | ) | — | |||||||||||

| Other income |

100 | 10 | 99 | 8 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total other income (expense), net |

8,746 | (369 | ) | 8,444 | (788 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income (loss) |

$ | 3,341 | $ | (10,562 | ) | $ | (449 | ) | $ | (18,609 | ) | |||||

|

|

|

|

|

|

|

|

|

|||||||||

| Earnings (loss) attributable to common stockholders—basic and diluted |

$ | 3,275 | $ | (10,562 | ) | $ | (449 | ) | $ | (18,609 | ) | |||||

|

|

|

|

|

|

|

|

|

|||||||||

| Earnings (loss) per share—basic and diluted |

$ | 1.25 | $ | (4.87 | ) | $ | (0.17 | ) | $ | (8.67 | ) | |||||

|

|

|

|

|

|

|

|

|

|||||||||

| Weighted average number of common shares used in earnings (loss) per share calculation—basic and diluted |

2,610,891 | 2,170,443 | 2,610,783 | 2,145,571 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Comprehensive income (loss) |

$ | 3,341 | $ | (10,567 | ) | $ | (449 | ) | $ | (18,620 | ) | |||||

|

|

|

|

|

|

|

|

|

|||||||||

The accompanying notes are an integral part of the condensed consolidated financial statements.

3

Table of Contents

Zalicus Inc.

Condensed Consolidated Statements of Cash Flow

(in thousands)

(Unaudited)

| Six Months ended June 30, | ||||||||

| 2014 | 2013 | |||||||

| Operating activities |

||||||||

| Net loss |

$ | (449 | ) | $ | (18,609 | ) | ||

| Adjustments to reconcile net loss to net cash used in operating activities: |

||||||||

| Depreciation and amortization |

377 | 5,037 | ||||||

| Gain on divestiture of cHTS business |

(8,645 | ) | — | |||||

| Loss on extinguishment of term loan |

67 | — | ||||||

| Loss on exit of facility |

1,407 | — | ||||||

| Noncash interest expense |

9 | 99 | ||||||

| Noncash rent expense |

(118 | ) | (142 | ) | ||||

| Stock-based compensation expense |

622 | 1,048 | ||||||

| Foreign exchange gain |

— | (6 | ) | |||||

| Decrease in deferred rent |

(62 | ) | (74 | ) | ||||

| Changes in assets and liabilities: |

||||||||

| Decrease in accounts receivable |

2,040 | 716 | ||||||

| Increase in prepaid expenses and other assets |

(276 | ) | (344 | ) | ||||

| Decrease in accounts payable |

(1,850 | ) | (1,832 | ) | ||||

| Decrease in accrued restructuring |

— | (34 | ) | |||||

| Decrease in accrued expenses and other long-term liabilities |

(2,176 | ) | 418 | |||||

| Decrease in deferred revenue |

(1,185 | ) | (1,696 | ) | ||||

|

|

|

|

|

|||||

| Net cash used in operating activities |

(10,239 | ) | (15,419 | ) | ||||

| Investing activities |

||||||||

| Proceeds from sale of intangible asset |

7,200 | — | ||||||

| Proceeds from sale of cHTS business, net of costs to sell |

8,366 | — | ||||||

| Purchases of property and equipment |

— | (157 | ) | |||||

| Purchases of short-term investments |

— | (17,493 | ) | |||||

| Sales and maturities of short-term investments |

— | 31,437 | ||||||

|

|

|

|

|

|||||

| Net cash provided by investing activities |

15,566 | 13,787 | ||||||

| Financing activities |

||||||||

| Repayment of term loan |

(8,848 | ) | (3,164 | ) | ||||

| Repurchases of common stock |

(41 | ) | — | |||||

| Proceeds from issuance of common stock, net of issuance cost |

— | 3,128 | ||||||

| Proceeds from exercise of stock options |

— | 7 | ||||||

|

|

|

|

|

|||||

| Net cash used in financing activities |

(8,889 | ) | (29 | ) | ||||

|

|

|

|

|

|||||

| Effect of exchange rate changes on cash and cash equivalents |

— | (6 | ) | |||||

|

|

|

|

|

|||||

| Net decrease in cash and cash equivalents |

(3,562 | ) | (1,667 | ) | ||||

| Cash and cash equivalents at beginning of the period |

17,958 | 4,531 | ||||||

|

|

|

|

|

|||||

| Cash and cash equivalents at end of the period |

$ | 14,396 | $ | 2,864 | ||||

|

|

|

|

|

|||||

| Cash paid for interest |

$ | 148 | $ | 728 | ||||

|

|

|

|

|

|||||

The accompanying notes are an integral part of the condensed consolidated financial statements.

4

Table of Contents

Zalicus Inc.

Notes to Condensed Consolidated Financial Statements

(all dollar amounts are in thousands, except share and per share amounts)

(Unaudited)

| 1. | Organization |

On July 15, 2014, EPIRUS Biopharmaceuticals, Inc., formerly known as Zalicus Inc., a Delaware corporation (“Epirus,” “we,” “our,” “us” or the “Company”) completed its merger with the former entity EPIRUS Biopharmaceuticals, Inc., a Delaware corporation and private company (“Old Epirus”), pursuant to the terms of that certain Agreement and Plan of Merger and Reorganization (as amended, the “Merger Agreement”), dated as of April 15, 2014, by and among the Company, Old Epirus and EB Sub, Inc. (“EB Sub”), formerly known as BRunning, Inc., a Delaware corporation and wholly-owned subsidiary of the Company (the “Merger”). The boards of directors of the Company and Old Epirus approved the Merger on April 15, 2014, and the stockholders of the Company and Old Epirus approved the Merger and related matters on July 15, 2014, including the change of the Company’s name from Zalicus Inc. to EPIRUS Biopharmaceuticals, Inc. Pursuant to the Merger Agreement, EB Sub merged with and into Old Epirus with Old Epirus being the surviving corporation of the Merger and thereby becoming a wholly-owned subsidiary of the Company. Except as described in Note 13, “Subsequent Event,” the accompanying unaudited condensed financial statements do not give effect to the Merger. The historical financial statements have been labeled Zalicus Inc. for the purposes of this filing, which was the entity name in effect for the historical periods presented.

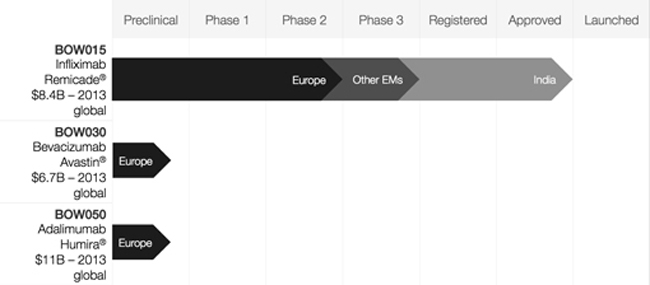

Prior to the Merger, the Company was a biopharmaceutical company developing drug candidates with a focus on the treatment of pain. Following the Merger, Epirus became a commercial-stage biotechnology company focused on improving patient access to important biopharmaceuticals by developing, manufacturing, and commercializing biosimilar therapeutics, or biosimilars, in targeted geographies worldwide. The Company has a principal place of business in Boston, Massachusetts. To date, the Company has devoted substantially all of its resources to the development of its drug discovery technologies and the research and development of its drug candidates, including conducting preclinical and clinical trials and seeking intellectual property protection for its technology and product candidates. The Company focuses on the development of biosimilar monoclonal antibodies (MAbs) for markets outside of North American and Japan. The Company’s lead product candidate is BOW015, a biosimilar version of Remicade (infliximab). Remicade, marketed by Johnson & Johnson, Merck Schering and Mitsubishi Tanabe for the treatment of various inflammatory diseases, achieved approximately $8.4 billion in global sales in 2013. In March 2014, the Company’s manufacturing partner, Reliance Life Sciences Pvt Ltd, or RLS, obtained manufacturing and marketing approval in India for BOW015 as a treatment for rheumatoid arthritis. The Company has reported positive bioequivalence and efficacy data in the clinical development program for BOW015, including a Phase 1 clinical trial in the United Kingdom and in an interim analysis for a Phase 3 clinical trial in India, in each case showing equivalence with Remicade. The Company’s pipeline of biosimilar product candidates also includes BOW050, a biosimilar version of Humira (adalimumab), which is marketed by AbbVie and used to treat inflammatory diseases, and BOW030, a biosimilar version of Avastin (bevacizumab), which is marketed by Genentech/Roche and used to treat a variety of cancers. Both BOW050 and BOW030 are in preclinical development. Collectively, Remicade, Humira and Avastin generated $26.2 billion in global sales in 2013 according to EvaluatePharma. The Company is advancing development and commercialization partnerships for its product candidates in Brazil, China and India, as well as in additional markets in Southeast Asia and North Africa. In August 2013, the Company transferred all of its intellectual property to its subsidiary, Epirus Switzerland GmbH, a Swiss corporation.

| 2. | Basis of Presentation |

The accompanying unaudited condensed consolidated financial statements present the historical results and financial position of the Company prior to the Merger and have been prepared in accordance with accounting principles generally accepted in the United States (“GAAP”) for interim financial reporting and as required by Regulation S-X, Rule 10-01. Accordingly, they do not include all of the information and footnotes required by GAAP for complete financial statements. In the opinion of management, all adjustments (including those which are normal and recurring) considered necessary for a fair presentation of the interim financial information have been included. When preparing financial statements in conformity with GAAP, the Company must make estimates and

5

Table of Contents

assumptions that affect the reported amounts of assets, liabilities, revenues, expenses and related disclosures at the date of the financial statements. Actual results could differ from those estimates. Additionally, operating results for the three and six months ended June 30, 2014 reflect the results of operations of the Company prior to the Merger and are therefore not indicative of the results that may be expected for any other interim period or for the fiscal year ending December 31, 2014. For further information, refer to the consolidated financial statements and footnotes included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2013 as filed with the Securities and Exchange Commission (“SEC”) on March 14, 2014.

Reverse Stock Splits

On October 3, 2013, the Company effected a 1-for-6 reverse stock split of its outstanding common stock. On July 16, 2014, the Company effected a 1-for-10 reverse stock split of its outstanding common stock. The accompanying consolidated financial statements and notes to the consolidated financial statements give retroactive effect to both the October 3, 2013 reverse stock split and the July 16, 2014 reverse stock split for all periods presented. The shares of common stock retained a par value of $0.001 per share. Accordingly, stockholders’ equity reflects the reverse stock split by reclassifying from common stock to additional paid-in capital an amount equal to the par value of the decreased shares resulting from both of the reverse stock splits.

| 3. | Significant Accounting Policies |

In the six months ended June 30, 2014, there were no changes to the Company’s significant accounting policies identified in the Company’s most recent Annual Report on Form 10-K for the fiscal year ended December 31, 2013. In connection with the Merger, the Company will adopt the significant accounting policies of Old Epirus, which are included in Old Epirus’ consolidated financial statements for the year ended December 31, 2013 and Old Epirus’ interim condensed consolidated financial statements for the three months ended March 31, 2014, both of which are included in the Company’s joint proxy statement/prospectus on Form S-4/A filed with the SEC on June 4, 2014.

Recent Accounting Pronouncements

Revenue Recognition

In May 2014, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) No. 2014-09, Revenue from Contracts with Customers, which amends the guidance for accounting for revenue from contracts with customers. This ASU supersedes the revenue recognition requirements in Accounting Standards Codification Topic 605, Revenue Recognition, and creates a new Topic 606, Revenue from Contracts with Customers. This guidance is effective for fiscal years beginning after December 15, 2016, with early adoption not permitted. Two adoption methods are permitted: retrospectively to all prior reporting periods presented, with certain practical expedients permitted; or retrospectively with the cumulative effect of initially adopting the ASU recognized at the date of initial application. The Company has not yet determined which adoption method it will utilize or the effect that the adoption of this guidance will have on its consolidated financial statements.

Discontinued Operations and Disposals

In April 2014, the FASB issued ASU No. 2014-8, Reporting Discontinued Operations and Disclosures of Disposals of Components of an Entity (“ASU 2014-8”). ASU 2014-8 changes the criteria for determining which disposals can be presented as discontinued operations and modifies related disclosure requirements. Under the new guidance, a discontinued operation is defined as a disposal of a component or group of components that is disposed of or is classified as held for sale and represents a strategic shift that has a major effect on an entity’s operations and financial results. This accounting guidance applies prospectively to new disposals and new classifications of disposal groups as held for sale. The guidance is effective for fiscal years beginning after December 15, 2014.

6

Table of Contents

Development Stage Entity

In June 2014, the FASB issued ASU No. 2014-10, Development Stage Entities (Topic 915): Elimination of Certain Financial Reporting Requirements, Including an Amendment to Variable Interest Entities Guidance in Topic 810, Consolidation (“ASU 2014-10”). ASU 2014-10 removes all incremental financial reporting requirements from GAAP for development stage entities, including the removal of Topic 915 from the FASB Accounting Standards Codification (“ASC”). In addition, the update adds an example disclosure in Risks and Uncertainties, ASC Topic 275, to illustrate one way that an entity that has not begun planned principal operations could provide information about the risks and uncertainties related to the company’s current activities and removes an exception provided to development stage entities in Consolidations, ASC Topic 810, for determining whether an entity is a variable interest entity—which may change the consolidation analysis, consolidation decision, and disclosure requirements for a company that has an interest in a company in the development stage. ASU 2014-10 is effective for fiscal years beginning after December 15, 2014 with the revised consolidation standards effective for fiscal years beginning after December 15, 2016. Early adoption is permitted. The Company expects to early adopt the guidance and eliminate the presentation and disclosure requirements of ASC Topic 915 during the three months ending September 30, 2014.

| 4. | Divestiture of Combination High Throughput Screening Platform |

On June 2, 2014, the Company completed the sale of its combination High Throughput Screening platform (the “cHTS Business”) and certain assets and liabilities related to the cHTS Business to Horizon Discovery Limited, an English limited company, and Horizon Discovery Inc., a Delaware corporation (together, the “Horizon Discovery Group”), pursuant to the Asset Purchase Agreement (the “Purchase Agreement”), dated as of May 14, 2014, with the Horizon Discovery Group (such transaction, the “Horizon Sale”). Under the terms of the Purchase Agreement, at the closing of the transaction, the Company received cash proceeds of $8,544 from the Horizon Discovery Group, including $544 as a closing adjustment for net working capital.

In connection with the Horizon Sale, the Company sublet its Cambridge, Massachusetts facility to Horizon Discovery Inc. (the “Sublease”). Pursuant to the Sublease, Horizon Discovery Inc. will pay to the Company approximately $92 per month through May 2016 and approximately $134 per month from June 2016 through January 2017, when the Company’s original lease for its Cambridge facility and the Sublease terminate. The Company’s obligations under its original lease remain and the Company will continue its payments to the Cambridge facility landlord of approximately $134 per month through January 2017. The Company ceased use of the facility on June 2, 2014. In connection with the Company’s exit of the facility and the execution of the Sublease, during the three and six months ended June 30, 2014, the Company recognized a net loss of $1,407 in the condensed consolidated statement of operations and other comprehensive loss, which is comprised of the fair value of the Company’s payments under the original lease, net of amounts to be received under the Sublease and net of the amortization of deferred rent and lease incentive obligation, and the acceleration of depreciation of the Company’s leasehold improvements (Note 5). As of June 30, 2014, the Company had liabilities related to the exit of the facility totaling $919. Because of the continuing cash flows under the Sublease, the historical results of operations of the cHTS Business do not meet the current criteria to be classified as discontinued operations.

As of May 31, 2014, the net carrying value of the assets and liabilities of the cHTS Business sold was approximately $(279) and consisted primarily of unbilled accounts receivable, prepaid expenses, property and equipment and deferred revenue. During the three and six months ended June 30, 2014, the Company recognized a gain on the sale of the cHTS Business of $8,645, net of $178 of costs to sell, in the condensed consolidated statement of operations and comprehensive loss.

The Company did not recognize a provision for income taxes for the three or six months ended June 30, 2014. No provision for income taxes is expected for such period because the Company has sufficient net operating loss carryforwards to offset the Company’s expected taxable income for the period prior to its merger with Old Epirus.

| 5. | Property and Equipment |

Property and equipment consist of the following:

| June 30, 2014 |

December 31, 2013 |

|||||||

| Leasehold improvements |

$ | 5,596 | $ | 5,596 | ||||

| Laboratory equipment |

— | 5,949 | ||||||

| Computer equipment |

— | 843 | ||||||

| Construction in progress |

— | 39 | ||||||

7

Table of Contents

| June 30, 2014 |

December 31, 2013 |

|||||||

| Capitalized software |

— | 815 | ||||||

| Furniture and fixtures |

— | 497 | ||||||

|

|

|

|

|

|||||

| 5,596 | 13,739 | |||||||

| Less: accumulated depreciation |

(5,596 | ) | (11,376 | ) | ||||

|

|

|

|

|

|||||

| $ | — | $ | 2,363 | |||||

|

|

|

|

|

|||||

All of the Company’s laboratory equipment, computer equipment, construction in progress, capitalized software and furniture and fixtures was sold to Horizon Discovery Group in connection with the Horizon Sale. Leasehold improvements were not part of the net assets sold to the Horizon Discovery Group. The net carrying value of the property and equipment sold was $384.

Depreciation expense, including amortization of assets recorded under capital leases, for the six months ended June 30, 2014 was $1,979, $1,602 of which was related to the acceleration of depreciation of the Company’s leasehold improvements and was recorded as a component of loss on exit of facility in the condensed consolidated statement of operations and other comprehensive loss. Upon execution of the Purchase Agreement, the Company reevaluated the useful life of leasehold improvements and determined the remaining useful life to be the remaining period prior to the execution of the Sublease, or the period from May 15, 2014 through June 2, 2014.

| 6. | Licensing of Sodium Channel Pain Modulator Program and Assignment of Prednisporin Patents |

Licensing of Sodium Channel Pain Modulator Program

On June 18, 2014, the Company licensed its sodium channel modulator program, including intellectual property and related pipeline assets, to AnaBios Corporation. Under the terms of the agreement, the Company will be eligible to receive up to $17,200 in clinical and regulatory milestone payments and royalties up to 12% of net sales on any future products resulting from this license. The Company did not receive any upfront cash or assets in the licensing transaction.

Assignment of Prednisporin Patents

On June 30, 2014, the Company and Fovea Pharmaceuticals, a wholly-owned subsidiary of Sanofi, entered into an agreement pursuant to which the parties mutually agreed to terminate that Second Amended and Restated License Agreement, dated July 22, 2009, between the parties (the “2009 Agreement”). Under the 2009 Agreement, the Company granted Fovea an exclusive worldwide license to certain drug combinations to treat allergic and inflammatory diseases of the front of the eye. Fovea had advanced one such combination, Prednisporin (FOV1101), through Phase 2b clinical development for allergic conjunctivitis and was seeking to continue the development of Prednisporin (FOV1101) through a sublicense. The Company was eligible to receive up to an additional $39,000 from Fovea upon achievement of certain clinical and regulatory milestones for Prednisporin (FOV1101) and each other product candidate subject to the 2009 Agreement. Following this termination, the Company assigned certain of its patents which had previously been licensed under the 2009 Agreement to a third party controlled by certain former owners of Fovea. This third party may exploit these patent rights independently or in conjunction with another third party. In consideration of such patents, the Company received $100, plus $15 to reimburse the Company’s legal costs associated with the transaction. During the three months ended June 30, 2014, the Company recognized other income of approximately $100 in the condensed consolidated statement of operations and comprehensive income.

| 7. | Intangible Asset |

The intangible asset relates to rights to receive milestone payments and royalties from Mallinckrodt Inc. for the commercial rights to Exalgo that were acquired as part of the merger with Neuromed Pharmaceuticals Ltd., or Neuromed. The intangible asset was initially recorded on December 21, 2009 at a value of $45,943 with an ongoing useful life of five years, representing the remaining patent life of Exalgo.

8

Table of Contents

On January 31, 2014, the Company’s subsidiary Zalicus Pharmaceuticals Ltd., or Zalicus Canada, and Mallinckrodt Medical Imaging – Ireland, an affiliate of Mallinckrodt plc, entered into a Royalty Purchase Agreement (the “Royalty Purchase Agreement”) relating to the asset purchase agreement, dated as of June 11, 2009, between the Company and Mallinckrodt Inc. (collectively with Mallinckrodt Medical Imaging – Ireland and Mallinckrodt plc, “Mallinckrodt”), as amended (the “Asset Purchase Agreement”). Under the terms of the Royalty Purchase Agreement, in exchange for the payment of $7,200 from Mallinckrodt to the Company on January 31, 2014, the Company terminated any further rights it has to the payment of royalties on net sales of Exalgo by Mallinckrodt for any period subsequent to December 31, 2013.

As of December 31, 2013, the Company concluded that facts and circumstances existed which indicated that the carrying value of the intangible asset exceeded its estimated fair value. The Company determined the estimated fair value of the intangible asset as of December 31, 2013 based on the $7,200 in proceeds from the Royalty Purchase Agreement. As a result, during the year ended December 31, 2013, the Company recorded an impairment charge of $1,732 in the consolidated statements of operations and comprehensive loss.

The Company recorded the sale of the intangible asset for proceeds of $7,200, with no gain or loss, in the six months ended June 30, 2014.

| 8. | Accrued Expenses |

Accrued expenses consisted of the following:

| June 30, 2014 | December 31, 2013 | |||||||

| Accrued clinical trial costs |

$ | 103 | $ | 803 | ||||

| Accrued payroll and related benefits |

28 | 656 | ||||||

| Accrued professional fees and merger costs |

719 | 290 | ||||||

| Accrued current portion of sublease liability |

489 | — | ||||||

| Accrued research collaboration expense |

— | 1,015 | ||||||

| Accrued other expenses |

204 | 575 | ||||||

|

|

|

|

|

|||||

| $ | 1,543 | $ | 3,339 | |||||

|

|

|

|

|

|||||

| 9. | Term Loan Payable |

On January 31, 2014, the Company prepaid its outstanding indebtedness of $8,647 to Oxford Finance Corporation (the “Lender”) under the loan and security agreement (the “Loan and Security Agreement”). The proceeds from the Royalty Purchase Agreement of $7,200, along with the royalty payment of approximately $2,006 from Mallinckrodt for royalties earned on net sales of Exalgo for the quarter ended December 31, 2013, were sufficient to prepay the remaining balance of $8,647, including accrued interest and a final payment fee of $300, under the Loan and Security Agreement. As a result, the Loan and Security Agreement was terminated effective January 31, 2014, and the Lender has released all security interests in the Company’s tangible and intangible property. In the six months ended June 30, 2014, the Company recorded a loss on extinguishment of $217 in the condensed consolidated statement of operations and comprehensive loss.

| 10. | Earnings (Loss) Per Share |

Earnings (loss) per common share is calculated using the two-class method, which is an earnings allocation formula that determines earnings (loss) per share for the holders of the Company’s common shares and participating securities. The Company’s restricted stock units (“RSUs”) contain participation rights in any dividend paid by the Company and are deemed to be participating securities. Earnings available to common stockholders and participating RSUs is allocated as if all of the earnings for the period had been distributed. The participating securities do not include a contractual obligation to share in losses of the Company and are not included in the calculation of net loss per share in the periods that have a net loss.

Diluted earnings per share is computed using the more dilutive of (a) the two-class method or (b) the treasury stock method. The Company allocates earnings to common stockholders and holders of RSUs based on

9

Table of Contents

dividend rights and ownership interests. The weighted-average number of common shares included in the computation of diluted earnings (loss) gives effect to all potentially dilutive common stock equivalents. The Company’s potentially dilutive shares, which include outstanding stock options, unvested RSUs and warrants, are only included in the calculation of diluted net loss per share when their effect is dilutive.

Basic and diluted earnings (loss) per common share are calculated as follows:

| Three months ended June 30, | Six months ended June 30, | |||||||||||||||

| 2014 | 2013 | 2014 | 2013 | |||||||||||||

| Numerator: |

||||||||||||||||

| Net income (loss) |

$ | 3,341 | $ | (10,562 | ) | $ | (449 | ) | $ | (18,609 | ) | |||||

| Earnings attributable to participating restricted stock units |

(66 | ) | — | — | — | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Earnings (loss) attributable to common stockholders - basic and diluted |

$ | 3,275 | $ | (10,562 | ) | $ | (449 | ) | $ | (18,609 | ) | |||||

|

|

|

|

|

|

|

|

|

|||||||||

| Denominator: |

||||||||||||||||

| Weighted-average number of common shares used in earnings per share - basic and diluted |

2,610,891 | 2,170,443 | 2,610,783 | 2,145,571 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Earnings (loss) per share - basic and diluted |

$ | 1.25 | $ | (4.87 | ) | $ | (0.17 | ) | $ | (8.67 | ) | |||||

|

|

|

|

|

|

|

|

|

|||||||||

The following potentially dilutive securities outstanding, prior to the use of the treasury stock method, have been excluded from the computation of diluted weighted-average shares outstanding for the three and six months ended June 30, 2014 and 2013, as they would be anti-dilutive.

| Three months ended June 30, | Six months ended June 30, | |||||||||||||||

| 2014 | 2013 | 2014 | 2013 | |||||||||||||

| Options outstanding |

157,203 | 179,116 | 157,203 | 179,116 | ||||||||||||

| Unvested restricted stock units |

— | 7,292 | 52,778 | 7,292 | ||||||||||||

| Warrants outstanding |

6,860 | 6,860 | 6,860 | 6,860 | ||||||||||||

| 11. | Stock-Based Compensation |

The Company recognized, for the three and six months ended June 30, 2014 and 2013, stock-based compensation expense of approximately $316 and $621, and $517 and $1,048, respectively, in connection with its stock-based payment awards.

Stock Options

A summary of the status of the Company’s stock option plans at June 30, 2014 and changes during the six months then ended is presented in the table and narrative below:

| Options | Weighted Average Exercise Price |

Weighted Average Remaining Contractual Term (In Years) |

Aggregate Intrinsic Value |

|||||||||||||

| Outstanding at December 31, 2013 |

168,133 | $ | 76.30 | |||||||||||||

| Granted |

25,000 | 14.70 | ||||||||||||||

| Exercised |

— | — | ||||||||||||||

| Cancelled |

(35,930 | ) | 68.79 | |||||||||||||

|

|

|

|

|

|||||||||||||

| Outstanding at June 30, 2014 |

157,203 | $ | 68.22 | 6.57 | $ | — | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Vested or expected to vest at June 30, 2014 |

132,699 | $ | 72.68 | 6.21 | $ | — | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Exercisable at June 30, 2014 |

87,283 | $ | 90.46 | 5.07 | $ | — | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

10

Table of Contents

The aggregate intrinsic value in the table above represents the value (the difference between the Company’s closing common stock price on the last trading day of the six months ended June 30, 2014 and the exercise price of the options, multiplied by the number of in-the-money options) that would have been received by the option holders had all option holders exercised their options on June 30, 2014. As of June 30, 2014, there was $1,139 of total unrecognized stock-based compensation expense related to stock options granted under the plans. The expense is expected to be recognized over a weighted-average period of 1.94 years. In connection with the Merger (described in Notes 1 and 13) and as a result of the termination of certain employees subsequent to the Merger, 43,699 unvested options vested on July 15, 2014.

The table above includes 22,584 stock options issued on January 3, 2013 with performance-based vesting criteria. The fair value of the options granted was determined using the Black-Scholes pricing model. In November 2013, the Company concluded the vesting criteria would not be achieved with respect to these outstanding performance-based options, as confirmed by the Compensation Committee of the Board of Directors, such that the options expired on July 1, 2014. Accordingly, for the six months ended June 30, 2014, the Company did not recognize any expense related to these stock options.

In connection with the Horizon Sale, Horizon Discovery Group offered employment to certain employees of the Company, all of whom accepted. Upon accepting employment with Horizon Discovery Group and terminating employment with the Company, in accordance with the Company’s stock option plan, the employees’ non-vested stock options were forfeited and the employees will have a certain period of time to exercise vested options before the options expire.

During the three and six months ended June 30, 2014 and 2013, respectively, the weighted-average assumptions used in the Black-Scholes pricing model for new grants were as follows:

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

| 2014 | 2013 | 2014 | 2013 | |||||||||||||

| Volatility factor |

N/A | 106.69 | % | 122.60 | % | 106.47 | % | |||||||||

| Risk-free interest rate |

N/A | 1.69 | % | 2.02 | % | 1.03 | % | |||||||||

| Dividend yield |

N/A | — | — | — | ||||||||||||

| Expected term (in years) |

N/A | 6.0 | 6.0 | 6.0 | ||||||||||||

Restricted Stock Units

A summary of the status of non-vested RSUs as of June 30, 2014 and changes during the six months then ended is as follows:

| Restricted Stock Units |

Weighted- Average Grant Date Fair Value |

Weighted Average Remaining Contractual Term (in Years) |

Aggregate Intrinsic Value |

|||||||||||||

| Nonvested at December 31, 2013 |

7,292 | $ | 50.50 | |||||||||||||

| Granted |

50,000 | 14.70 | ||||||||||||||

| Vested |

(4,514 | ) | 53.40 | |||||||||||||

| Cancelled |

— | — | ||||||||||||||

|

|

|

|

|

|||||||||||||

| Nonvested at June 30, 2014 |

52,778 | $ | 16.30 | 0.04 | $ | 644 | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

As of June 30, 2014, there was $691 of total unrecognized stock-based compensation expense related to non-vested RSUs. The expense is expected to be recognized over a weighted-average period of 0.04 years.

During February 2014, the Company issued 50,000 RSUs to certain employees, which vest with respect to one third (1/3) of the RSUs on the first anniversary of the grant date and an additional one third (1/3) on each

11

Table of Contents

anniversary thereafter until the third anniversary of the grant date. In the event of a change of control, as defined in the agreements governing the awards, 50% of the unvested portion of the RSUs shall immediately vest. In the event of the employee’s termination of employment within 12 months following a change of control without cause or for good reason, each as defined in the agreements governing the awards, any then unvested RSUs shall immediately vest. On July 15, 2014, after completion of the Merger, the employees holding these RSUs were terminated and all of the Company’s unvested RSUs immediately vested.

| 12. | Legal Proceedings |

From time to time, the Company is involved in legal proceedings and claims of various types and accounts for these legal proceedings in accordance with ASC Topic 450, “Contingencies.” The Company records a liability in its consolidated financial statements for these matters when a loss is considered probable and the amount of loss can be reasonably estimated. The Company reviews these estimates each accounting period as additional information is known and adjusts the loss provision when appropriate. If the loss is not probable or cannot be reasonably estimated, a liability is not recorded in its consolidated financial statements.

Between April 28, 2014 and May 2, 2014, three putative class action lawsuits were filed by purported stockholders of the Company in the Business Litigation Session of the Massachusetts Superior Court, Suffolk County, against the Company, EB Sub, the members of the Company’s board of directors and Old Epirus. These actions are: Paul Patrick Laky v. Zalicus Inc., et al., Civ. A. No. 14-1380; Michael Ma v. Zalicus Inc., et al ., Civ. A. No. 14-1381; Diane Harrypersaud v. Zalicus Inc., et al., Civ. A. No. 14-1455 (collectively, the “Massachusetts Actions”). On May 21, 2014, plaintiffs Michael Ma and Diane Harrypersaud filed a consolidated amended complaint. The Massachusetts Actions allege that the Company’s board of directors breached its fiduciary duties, and that Old Epirus, the Company and EB Sub aided and abetted the purported breaches, in connection with the proposed Merger. The Massachusetts Actions seek relief including, among other things, to enjoin defendants from proceeding with the Merger, to enjoin defendants from consummating the Merger unless additional procedures are implemented and rescind the Merger if consummated (or to award rescissionary damages), an award of compensatory damages, and an award of all costs of the Massachusetts Actions, including reasonable attorneys’ fees and experts’ fees.

Between May 1, 2014, and May 16, 2014, three putative class action lawsuits were filed by purported stockholders of the Company in the Court of Chancery of the State of Delaware against the Company, EB Sub, the members of the Company’s board of directors and Old Epirus. These actions are: Harvey Stein v. Zalicus, Inc. et al., Case No. 9602; Tuan Do v. Zalicus, Inc. et al., Case No. 9636; and Sy Simcha Mendlowitz and Bennet Mattingly v. Zalicus, Inc., et al., Case No. 9664 (collectively, the “Delaware Actions”). On May 23, 2014, plaintiff Harvey Stein filed a verified amended complaint, and on May 27, 2014, plaintiff Tuan Do filed a verified amended complaint. The Delaware Actions allege that the Company’s board of directors breached its fiduciary duties, and that Old Epirus and EB Sub aided and abetted the purported breaches, in connection with the proposed Merger. The Delaware Actions seek relief including, among other things, to preliminarily and permanently enjoin the proposed Merger, to enjoin consummation of the proposed Merger and rescind the Merger if consummated (or to award rescissionary damages), an award of compensatory damages, and an award of all costs of the Delaware Actions, including reasonable attorneys’ fees and experts’ fees.

On June 6, 2014, plaintiffs’ counsel in the Delaware Actions filed a motion seeking to schedule a preliminary injunction hearing in advance of the stockholder vote on the proposed Merger, and seeking expedited discovery in advance of that hearing. Old Epirus, the Company, and the individual defendants opposed the motion. After a hearing, on June 13, 2014, the Delaware Court of Chancery denied plaintiffs’ motion.

The defendants deny the allegations in the Massachusetts and Delaware Actions, believe the actions are meritless, and intend to vigorously defend the actions. At each reporting period, the Company evaluates whether or not a potential loss amount or a potential range of loss is probable and reasonably estimable. In light of the early stages of the Massachusetts Actions and Delaware Actions, an estimate of the amount or range of reasonably possible loss in connection with these matters cannot be made.

12

Table of Contents

| 13. | Subsequent Event |

Merger

As described in Note 1, “Organization,” on July 15, 2014, the Company completed the Merger with Old Epirus. Pursuant to the Merger and after giving effect to the 1-for-10 reverse stock split that occurred on July 16, 2014 (the “2014 Reverse Split”), each share of capital stock of Old Epirus was exchanged for 0.13259 shares of common stock, par value $0.001 per share (the “Common Stock”) of the Company. Outstanding options and warrants of Old Epirus were exchanged at the same ratio. Upon the consummation of the Merger and after giving effect to the 2014 Reverse Split, equityholders of Old Epirus were issued an aggregate of 10,288,180 shares of Common Stock plus 1,174,038 shares of Common Stock which could be issued in the future upon exercise of stock options and warrants. Immediately following the consummation of the Merger and after giving effect to the 2014 Reverse Split, the Company had approximately 12,926,593 shares of Common Stock issued and outstanding.

The Merger will be accounted for as a “reverse merger” under the acquisition method of accounting for business combinations with Old Epirus treated as the accounting acquirer. Old Epirus was determined to be the accounting acquirer based upon the terms of the merger and other factors, such as relative voting rights and the composition of the combined company’s board of directors and senior management. All of the assets and liabilities of the Company will be recorded at their respective fair values as of the acquisition date and consolidated with those of Old Epirus. Transaction costs will be expensed as incurred.

Given the timing of the closing of the Merger, the purchase accounting is incomplete at this time. As such, it is not practicable for the Company to disclose the allocation of purchase price to assets acquired and liabilities assumed and pro forma revenues and earnings of the combined entity. The fair value of the consideration transferred in the Merger will be measured using the closing trading price of Common Stock on July 15, 2014, the closing date of the Merger. This information will be included in the Company’s Quarterly Report on Form 10-Q for the fiscal quarter ended September 30, 2014 to be filed with SEC.

13

Table of Contents

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

You should read the following discussion and analysis of our financial condition and results of operations in conjunction with our financial statements and their notes appearing elsewhere in this quarterly report. The following discussion contains forward-looking statements that involve risks and uncertainties. Our actual results and the timing of certain events could differ materially from those anticipated in these forward-looking statements as a result of certain factors, including those discussed below and elsewhere in this quarterly report.

In the following discussion the terms “Epirus,” “we,” “our,” “us” or the “Company” refer to EPIRUS Biopharmaceuticals, Inc., formerly known as Zalicus Inc., a Delaware corporation.

Overview

Recent Developments

Merger with Old Epirus

On July 15, 2014, we completed our merger with the former entity EPIRUS Biopharmaceuticals, Inc., a Delaware corporation and private company (“Old Epirus”), pursuant to the terms of that certain Agreement and Plan of Merger and Reorganization (as amended, the “Merger Agreement”), dated as of April 15, 2014, by and among us, Old Epirus and EB Sub, Inc. (“EB Sub”), formerly known as BRunning, Inc., a Delaware corporation and wholly-owned subsidiary of the Company (the “Merger”). Our board of directors and the board of directors of Old Epirus approved the Merger on April 15, 2014, and our stockholders and the stockholders of Old Epirus approved the Merger and related matters on July 15, 2014, including the change of our company name from Zalicus Inc. to EPIRUS Biopharmaceuticals, Inc. Pursuant to the Merger Agreement, EB Sub merged with and into Old Epirus with Old Epirus being the surviving corporation of the Merger and thereby becoming our wholly-owned subsidiary.

Pursuant to the terms of the Merger Agreement, at the effective time of the Merger (the “Effective Time”), each outstanding share of Old Epirus capital stock was converted into the right to receive approximately 0.13259 shares of our common stock (the “Exchange Ratio”). In addition, at the Effective Time: (i) we assumed all outstanding options to purchase shares of Old Epirus common stock, which options converted into options to purchase shares of our common stock, in each case appropriately adjusted based on the Exchange Ratio; and (ii) we assumed all outstanding warrants to purchase shares of the capital stock of Old Epirus, which were converted into warrants to purchase shares of our common stock, in each case appropriately adjusted based on the Exchange Ratio. As of the Effective Time, former stockholders of Old Epirus held approximately 81% of the combined company, calculated on a fully-diluted basis, and former stockholders of the Company held approximately 19% of the combined company, calculated on a fully-diluted basis. No fractional shares of common stock were issued in connection with the Merger. Instead, Old Epirus stockholders received cash in lieu of any fractional shares of our common stock that they would otherwise have been entitled to receive in connection with the Merger.

In connection with the completion of the Merger, on July 15, 2014, we filed a Certificate of Amendment to our Sixth Amended and Restated Certificate of Incorporation, effecting on July 16, 2014, a one-for-ten reverse stock split of our issued and outstanding common stock (the “Reverse Stock Split”). As a result of the Reverse Stock Split, each ten shares of our common stock issued and outstanding immediately prior to the Reverse Stock Split were automatically combined into and became one share of common stock. No fractional shares were issued as a result of the Reverse Stock Split and any stockholder who otherwise would have been entitled to receive fractional shares is entitled to receive cash in an amount, without interest, determined by multiplying such fraction of a share by $11.80, the closing price of a share of Company common stock on the Nasdaq Stock Market on July 15, 2014, after giving effect to the Reverse Stock Split. Also, as a result of the Reverse Stock Split, the per share exercise price of, and the number of shares of common stock underlying, our stock options, warrants and other derivative securities outstanding immediately prior to the Reverse Stock Split were automatically proportionally adjusted based on the one-for-ten split ratio in accordance with the terms of such options, warrants or other derivative securities, as the case may be.

After giving effect to the Reverse Stock Split and the Merger, we have approximately 12.9 million shares of common stock outstanding. The Reverse Stock Split did not alter the par value of our common stock or modify any voting rights or other terms of the common stock.

14

Table of Contents

Also in connection with the completion of the Merger, we changed our name from “Zalicus Inc.” to “EPIRUS Biopharmaceuticals, Inc.” and our stock began trading on the Nasdaq Stock Market under the symbol “EPRS” on July 16, 2014.

Upon completion of the Merger, Frank Haydu, Sally W. Crawford, Michael Kauffman and W. James O’Shea resigned from our board of directors of the Company (the “Board”), J. Kevin Buchi, Geoffrey Duyk, Daotian Fu, Julie McHugh, Amit Munshi and Scott Rocklage were appointed as members of the Board and Mark H.N. Corrigan and William Hunter resigned from the Board and were re-appointed as a Class III director and Class II director, respectively. Also upon completion of the Merger, Mark H.N. Corrigan and Justin Renz were removed as the Company’s Chief Executive Officer and Chief Financial Officer, respectively, and Amit Munshi and Tom Shea were appointed President and Chief Executive Officer and Chief Financial Officer and Treasurer of the Company, respectively.

Business After the Merger

We are a commercial-stage biotechnology company focused on improving patient access to important biopharmaceuticals by developing, manufacturing, and commercializing biosimilar therapeutics, or biosimilars, in targeted geographies worldwide. Our lead product candidate is BOW015, a biosimilar version of Remicade (infliximab). Remicade, marketed by Johnson & Johnson, Merck Schering and Mitsubishi Tanabe for the treatment of various inflammatory diseases, achieved approximately $8.4 billion in global sales in 2013. In March 2014, our manufacturing partner, Reliance Life Sciences Pvt Ltd, or RLS, obtained manufacturing and marketing approval in India for BOW015 as a treatment for rheumatoid arthritis. We have reported positive bioequivalence and efficacy data in the clinical development program for BOW015, including a Phase 1 clinical trial in the United Kingdom and a Phase 3 clinical trial in India, in each case showing equivalence with Remicade. We anticipate announcing the final 54 week safety data from the completed Phase 3 study in the third quarter of 2014. We also expect to initiate additional clinical work to support European approval in the first half of 2015 and have been designing this clinical program in consultation with European regulatory bodies. Our pipeline of biosimilar product candidates also includes BOW050, a biosimilar version of Humira (adalimumab), which is marketed by AbbVie and used to treat inflammatory diseases, and BOW030, a biosimilar version of Avastin (bevacizumab), which is marketed by Genentech/Roche and used to treat a variety of cancers. Both BOW050 and BOW030 are in preclinical development. Collectively, Remicade, Humira and Avastin generated $26.2 billion in global sales in 2013 according to EvaluatePharma. We are advancing development and commercialization partnerships for our product candidates in China and India, as well as in additional markets in Southeast Asia and North Africa and pursuing opportunities for developments and commercial partnerships in Brazil.

Biosimilars are highly similar versions of already approved biological drug products, referred to as reference products. We are currently focused on developing biosimilars to therapeutic monoclonal antibodies, or MAbs. We seek to take advantage of a convergence of four trends shaping the global market for MAb biosimilars. First, the market for MAbs is large and growing, and comprises many of the top-selling therapeutics in the world. According to EvaluatePharma, sales of MAbs accounted for $61.8 billion globally in 2013 and grew at a compound annual growth rate of 14% from 2010 through 2013. We seek to develop and commercialize biosimilars to address the global market, outside North America and Japan, at a cost that is expected to be less than that incurred by the innovators of the respective reference products. Second, sixteen MAbs, representing $43.3 billion of global sales in 2013, are expected to lose patent protection globally by 2020, creating an opportunity for companies focusing on biosimilars to the referenced MAbs. Third, defined but diverse commercial and regulatory frameworks exist globally for the introduction of biosimilars, including MAb biosimilars. Fourth, MAbs are often very expensive. In many countries outside the United States, public and private payors are seeking to lower the cost of biologics and improve patient access to these important medications. This favors biosimilar versions of biologics that are priced at a discount to the branded reference products.

Our product candidates are enabled by our proprietary, fully-integrated manufacturing platform, SCALE™, which enables turn-key, locally-based manufacturing of biosimilars for direct supply into global markets. We intend to leverage the SCALE platform to manufacture biosimilars locally in countries that require local production. We believe that our SCALE platform provides us with a competitive advantage by giving us the ability to accelerate access to our biosimilar candidates in many emerging markets.

15

Table of Contents

Our strategy for commercial success relies on tailored approaches to address the diversity of target global markets. We will direct our initial commercial efforts at markets in which we can leverage either our existing regulatory package, in the case of BOW015, or an initial regulatory package for which approval has been granted in one or more countries. In a second category of markets, in which additional clinical work may be necessary to secure approval, and where local authorities encourage local production, we intend to collaborate with local partners to enable in-country production of our products using our SCALE manufacturing platform. Finally, in other international markets, such as Europe, which require a separate regulatory approval or may reference a European product approval package, we intend to commercialize our products using a licensing or distribution model in conjunction with direct sales. We believe that the combination of early launch in emerging markets and a subsequent launch in Europe is the optimal ramp for building a high-growth global biosimilars business. We currently have an agreement to commercialize BOW015 in India with our partner Ranbaxy Laboratories, or Ranbaxy. As our commercialization strategy evolves, we may, subject to the terms of our agreement with Ranbaxy, engage additional partners and/or choose to sell directly into the Indian market. We anticipate commercializing BOW015 in India by early 2015. Additionally, with Ranbaxy and/or other potential partners, we intend to file for regulatory approval in additional markets where our current data are deemed sufficient for approval. We expect to commence a Phase 3 trial for BOW015 in Europe in the first half of 2015. If this trial is successful, we intend to pursue regulatory approval for BOW015 in Europe. To date, we have not yet commercialized BOW015 in any of our target markets, and therefore we have not yet received revenues from the sale of BOW015.

For more information regarding our business following the Merger, please see Part II, Item 5 of this Quarterly Report on Form 10-Q.

Business Prior to the Merger

Prior to the Merger, we were a biopharmaceutical company that discovered and developed novel treatments for patients suffering from pain. We had a portfolio of proprietary product candidates targeting pain and had entered into multiple revenue-generating collaborations with large pharmaceutical companies relating to other products, product candidates and drug discovery technologies. We also applied our expertise in the discovery and development of selective ion channel modulators and our combination high throughput screening technology, or cHTS to discover new product candidates for our portfolio or for our collaborators in the areas of pain and oncology.

Prior to the Merger, our most advanced product candidate was Z944, a novel, oral, state-dependent, selective T-type calcium channel modulator we sought to develop for the treatment of pain indications. T-type calcium channels have been recognized as key targets for therapeutic intervention in a broad range of cell functions and have been implicated in pain signaling. During 2013, we completed a Phase 1b clinical trial utilizing Laser-Evoked-Potentials, or LEP, to provide both objective and subjective assessments of the activity of Z944 in induced pain states. On November 1, 2013, we announced positive results from this Phase 1b clinical trial. Based on these results, prior to the Merger, we were planning to evaluate multiple modified-release formulations of Z944 in a Phase 1 pharmacokinetic and safety study in the first half of 2014, with the goal of advancing a modified-release formulation of Z944 toward Phase 2 clinical development in an appropriate pain indication by late 2014. We are currently evaluating post-Merger plans for further development of Z944.

Until June 2014, we had also been performing discovery research and preclinical development activities on our proprietary selective ion channel modulators targeting the Nav1.7 sodium channel for the treatment of pain. This discovery research and preclinical development was conducted as part of a research collaboration with Hydra Biosciences, Inc., or Hydra, a recognized leader in novel ion channel discovery and development. This collaboration expired in February 2014 in accordance with its terms. On June 18, 2014, we licensed our sodium channel modulator program, including intellectual property and related pipeline assets, to AnaBios Corporation. Under the terms of the agreement we will be eligible to receive up to $17.2 million in clinical and regulatory milestone payments and royalties up to 12% of net sales on any future products resulting from this license.

Until November 2013, we had also been advancing the development of Z160, a novel, oral N-type calcium channel modulator we were seeking to develop for the treatment of chronic pain. In December 2012 and August 2012, we initiated Phase 2 clinical trials of Z160 for the treatment of neuropathic pain, including, post-herpetic neuralgia, or PHN, a painful neuropathic condition resulting from an outbreak of the herpes zoster virus, otherwise known as shingles, and lumbosacral radiculopathy, or LSR, a common neuropathic back pain condition resulting

16

Table of Contents

from the compression or irritation of the nerves exiting the lumbar region of the spine, respectively. Patient enrollment completed for both studies in September 2013. Results from both Phase 2 trials of Z160 were released on November 11, 2013 and Z160 did not meet the primary endpoint in either of these Phase 2 trials. Based on the results of these trials, we have terminated further development of Z160.

On June 2, 2014, the Company sold its cHTS platform (the “cHTS Business”) and certain assets and liabilities related to the cHTS Business to Horizon Discovery Limited, an English private limited company, and Horizon Discovery Inc., a privately held Delaware corporation (together, the “Horizon Discovery Group”), pursuant to the Asset Purchase Agreement (the “Purchase Agreement”), dated as of May 14, 2014, with the Horizon Discovery Group (such transaction, the “Horizon Sale”). Under the terms of the Purchase Agreement, at the closing of the transaction, we received cash proceeds of $8.5 million from the Horizon Discovery Group, including $0.5 million as a closing adjustment for net working capital.

In connection with the Horizon Sale, we sublet our Cambridge, Massachusetts facility to Horizon Discovery Inc. (the “Sublease”). Pursuant to the Sublease, Horizon Discovery Inc. will pay to us approximately $92,000 per month through May 2016 and approximately $134,000 per month from June 2016 through January 2017, when our original lease for our Cambridge facility and the Sublease terminate. Our obligations under the original lease remain and we will continue our payments to the Cambridge facility landlord of approximately $134,000 per month through January 2017. We ceased use of the facility on June 2, 2014. In connection with our exit of the facility and the execution of the Sublease, during the three and six months ended June 30, 2014, we recognized a net loss of $1.4 million in the condensed consolidated statement of operations and other comprehensive loss, which is comprised of the fair value of our remaining payments under the original lease, net of amounts to be received under the Sublease and net of the amortization of deferred rent and lease incentive obligation, and an acceleration of depreciation of our leasehold improvements. As of June 30, 2014, we had liabilities related to the exit of the facility totaling $0.9 million. Because of the continuing cash flows under the Sublease, the historical results of operations of the cHTS Business do not meet the current criteria to be classified as discontinued operations.

The United States commercial rights to Exalgo® were acquired by Mallinckrodt Inc., or Mallinckrodt, then a subsidiary of Covidien plc (“Covidien”) from Neuromed Pharmaceuticals Inc., which became a wholly-owned subsidiary of Zalicus pursuant to a merger completed in December 2009, in June 2009 pursuant to an asset purchase agreement to sell all of the tangible and intangible assets associated with Exalgo, including the rights to develop and commercialize the product candidate in the United States. Exalgo is an extended release formulation of hydromorphone, an opioid analgesic that has been used in an immediate release formulation to treat pain for many years, and is intended for use in the management of moderate to severe pain in opioid tolerant patients requiring continuous, around-the-clock opioid analgesia for an extended period of time. Under the asset purchase agreement, Mallinckrodt is responsible for all commercialization activities for Exalgo in the United States, including marketing and sales, and for all post-approval regulatory activities. We received a $40.0 million milestone payment following FDA approval of Exalgo in March 2010, and received tiered royalties on net sales of Exalgo by Mallinckrodt following its commercial launch in April 2010. We recognized $16.0 million in revenue related to these royalties through December 31, 2013.

On January 31, 2014, we and Mallinckrodt Medical Imaging—Ireland entered into a royalty purchase agreement relating to the asset purchase agreement (“Royalty Purchase Agreement”). Under the terms of the Royalty Purchase Agreement, in exchange for the payment of $7.2 million from Mallinckrodt to the Company on January 31, 2014, we terminated any further rights we had to the payment of royalties on net sales of Exalgo by Mallinckrodt for any period subsequent to December 31, 2013. As a result, we recorded an impairment charge of $1.7 million related to the Exalgo intangible asset in the year ended December 31, 2013.

On June 30, 2014, we and Fovea Pharmaceuticals (“Fovea”), a wholly-owned subsidiary of Sanofi, entered into an agreement pursuant to which we and Fovea mutually agreed to terminate the Second Amended and Restated License Agreement, dated July 22, 2009, between the parties. Following this termination, we assigned certain of our patents which had previously been licensed under the agreement to a third party controlled by certain former owners of Fovea. This third party may exploit these patent rights independently or in conjunction with another third party. In consideration of such patents, we received $100,000 plus $15,000 to reimburse our legal costs associated with the transaction. During the three months ended June 30, 2014, we recognized other income of approximately $0.1 million in the condensed consolidated statement of operations and comprehensive income.

17

Table of Contents

As of June 30, 2014, we had an accumulated deficit of $380.1 million. We had a net loss of $0.4 million and $18.6 million for the six months ended June 30, 2014 and 2013, respectively.

Our management currently uses consolidated financial information in determining how to allocate resources and assess performance. We have determined that we conduct operations in one business segment. For each of the six months ended June 30, 2014 and 2013, all of our revenues were from customers located in the United States.

Critical Accounting Policies

We believe that several accounting policies are important to understanding our historical and future performance. We refer to these policies as “critical” because these specific areas generally require us to make judgments and estimates about matters that are uncertain at the time we make the estimate, and different estimates—which also would have been reasonable—could have been used, which would have resulted in different financial results.

The critical accounting policies we identified in our most recent Annual Report on Form 10-K for the fiscal year ended December 31, 2013 related to intangible assets, revenue recognition, stock-based compensation, accrued expenses and income taxes. There were no changes to our critical accounting policies in the six months ended June 30, 2014. It is important that the discussion of our operating results that follows be read in conjunction with the critical accounting policies disclosed in our Annual Report on Form 10-K, as filed with the SEC on March 14, 2014.

In connection with the Merger, we will adopt the critical accounting policies of Old Epirus, which are included in Old Epirus’ “Epirus Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in the Company’s joint proxy statement/prospectus on Form S-4/A filed with the SEC on June 4, 2014.

Results of Operations

The following discussion of the Company’s results of operations refers to the Company’s results of operations prior to the Merger, and are not indicative of the Company’s prospective results of operations following the Merger.

Comparison of the Three Months ended June 30, 2014 and June 30, 2013

Revenue. For the three months ended June 30, 2014, we recorded $1.1 million of revenue from cHTS services and other collaborations. For the three months ended June 30, 2013, we recorded $3.9 million of revenue from Exalgo royalties and cHTS services and other collaborations, which comprised royalty revenue from Mallinckrodt on net sales of Exalgo of $1.7 million and revenue from our cHTS services and other collaborations of $2.2 million. The decrease in revenue for the three months ended June 30, 2014 was primarily due to a $1.7 million decrease in revenue from Exalgo royalties as a result of the January 2014 Royalty Purchase Agreement entered into with an affiliate of Mallinckrodt, pursuant to which we terminated any further rights we had to the payment of royalties on net sales of Exalgo, and a $1.1 million decrease in revenue from our cHTS services and other collaborations as a result of Horizon Sale. Due to our sale of the cHTS Business and our rights to Exalgo royalties, we do not expect to earn future revenues related to the cHTS Business or Exalgo royalties.

Research and Development Expense. Research and development expense for the three months ended June 30, 2014 was $2.1 million compared to $9.8 million for the three months ended June 30, 2013. The $7.7 million decrease was due primarily to a $5.8 million decrease in expenses related to the clinical development of Z160, a $0.9 million decrease in ion channel discovery costs, a $0.4 million decrease in Z944 and other clinical program costs, and a $0.3 million decrease in cHTS services and other collaboration discovery costs. The $5.8 million decrease in expenses related to Z160 is due to termination of all development activities related to Z160 in the fourth quarter of 2013.

18

Table of Contents

As a result of the Merger, we expect the costs related to the development of our product candidates targeting the treatment of pain indications, including Z944 and Z160, will decrease significantly while we focus our resources on the development of our biosimilar product candidates and evaluate post-Merger plans for future development of Z944.