Attached files

| file | filename |

|---|---|

| EX-10.36 - EX-10.36 - EPIRUS Biopharmaceuticals, Inc. | eprs-20151231ex103676696.htm |

| EX-10.8 - EX-10.8 - EPIRUS Biopharmaceuticals, Inc. | eprs-20151231ex108496d9b.htm |

| EX-21.1 - EX-21.1 - EPIRUS Biopharmaceuticals, Inc. | eprs-20151231ex2115fefc7.htm |

| EX-31.1 - EX-31.1 - EPIRUS Biopharmaceuticals, Inc. | eprs-20151231ex3114f7fef.htm |

| EX-10.9 - EX-10.9 - EPIRUS Biopharmaceuticals, Inc. | eprs-20151231ex10939864a.htm |

| EX-10.16 - EX-10.16 - EPIRUS Biopharmaceuticals, Inc. | eprs-20151231ex1016101f8.htm |

| EX-10.25 - EX-10.25 - EPIRUS Biopharmaceuticals, Inc. | eprs-20151231ex1025d29f7.htm |

| EX-32.1 - EX-32.1 - EPIRUS Biopharmaceuticals, Inc. | eprs-20151231ex321f2a4aa.htm |

| EX-31.2 - EX-31.2 - EPIRUS Biopharmaceuticals, Inc. | eprs-20151231ex3120ca05e.htm |

| EX-23.1 - EX-23.1 - EPIRUS Biopharmaceuticals, Inc. | eprs-20151231ex231daab4b.htm |

| EX-10.10 - EX-10.10 - EPIRUS Biopharmaceuticals, Inc. | eprs-20151231ex10109e63d.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

☒ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2015

◻TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File No. 000-51171

EPIRUS BIOPHARMACEUTICALS, INC.

(Exact name of registrant as specified in its charter)

|

Delaware |

|

04-3514457 |

|

(State or other jurisdiction of Incorporation or organization) |

|

(IRS Employer Identification Number) |

|

|

|

|

|

699 Boylston Street Eighth Floor Boston, MA 02116 |

|

02116 |

|

(Address of Principal Executive Offices) |

|

(Zip Code) |

(617) 600-3497

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Exchange Act:

|

Common Stock, $0.001 par value per share |

|

The NASDAQ Stock Market LLC |

|

(Title of each class) |

|

(Name of each exchange on which registered) |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ◻ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ◻ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ◻

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ◻

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer |

◻ |

|

|

Accelerated filer |

☒ |

|

|

|

|

|

|

|

|

Non-accelerated filer |

◻ |

(Do not check if a smaller reporting company) |

|

Smaller reporting company |

◻ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Securities Exchange Act of 1934). Yes ◻ No ☒

As of June 30, 2015, the last business day of the registrant’s last completed second fiscal quarter, the aggregate market value of the Common Stock held by non-affiliates of the registrant was approximately $97,043,791 based on the closing price of the registrant’s Common Stock, as reported by the NASDAQ Capital Market, on such date. Shares of Common Stock held by each executive officer and director and certain affiliate stockholders known by the registrant to own 5% or more of the outstanding stock based on public filings and other information known to the registrant have been excluded since such persons may be deemed affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

The number of shares of the registrant’s Common Stock, par value $0.001 per share, outstanding as of March 25, 2016 was 26,184,349.

The exhibit index as required by Item 601(a) of Regulation S-K is included in Item 15 of Part IV of this report.

DOCUMENTS INCORPORATED BY REFERENCE

Specified portions of the registrant’s proxy statement with respect to the registrant’s 2016 Annual Meeting of Stockholders, which is to be filed pursuant to Regulation 14A within 120 days after the end of the registrant’s fiscal year ended December 31, 2015, are incorporated by reference into Part III of this Form 10-K.

EPIRUS Biopharmaceuticals, Inc.

Form 10‑K

Explanatory Note

The registrant qualified as a smaller reporting company for the fiscal year ended December 31, 2015. Because the registrant's public float exceeded $75.0 million on the last business day of the registrant’s last completed second fiscal quarter, the registrant will qualify and report as an accelerated filer in 2016, starting with its quarterly report on Form 10-Q for the quarter ending March 31, 2016. Pursuant to the rules of the Securities and Exchange Commission, the registrant is relying upon the smaller reporting company scaled disclosure rules for portions of this annual report on Form 10-K.

1

CAUTIONARY NOTE REGARDING FORWARD‑LOOKING STATEMENTS

Various statements throughout this report are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements may appear throughout this report. Words such as “believe,” “anticipate,” “expect,” “estimate,” “intend,” “plan,” “project,” “will be,” “will continue,” “will result,” “seek,” “could,” “may,” “might,” or the negative of these terms and similar expressions or words, identify forward-looking statements. Forward-looking statements are based upon current expectations that involve risks, changes in circumstances, assumptions and uncertainties. Important factors that could cause actual results to differ materially from those reflected in our forward-looking statements include, among others:

|

· |

our inability to obtain regulatory approval for, or successfully commercialize, our leading product candidate, BOW015, or our other product candidates, BOW050, BOW070, BOW080, BOW090 and BOW100; |

our inability to access sufficient capital resources to fund our operations as a going concern beyond the second quarter of 2016;

our inability to secure and maintain relationships with collaborators and single-source contract manufacturers;

our history of operating losses and inability to ever become profitable;

our limited history of complying with public company reporting requirements;

our limited sales and marketing infrastructure;

uncertainty and volatility in the price of our common stock;

our inability to develop, implement and maintain appropriate internal controls;

our inability to remediate the material weaknesses in our internal control over financial reporting;

uncertainty as to our employees’, independent contractors’ and other collaborators’ compliance with regulatory standards and requirements and insider trading rules;

uncertainty as to the relationship between the benefits of our product candidates and the risks of their side‑effect profiles;

our inability to effectively compete with the reference biologic products for our biosimilar product candidates and from other pharmaceuticals approved for the same indication as the reference biologic products;

our inability to complete our in-house cell line and process development activities;

dependence on the efforts of third-parties to conduct and oversee our clinical trials for our product candidates, to manufacture nonclinical and clinical supplies of our product candidates, to store critical components of our product candidates, and to commercialize our product candidates;

uncertainty relating to U.S. regulatory and legal landscapes and a fragmented payer market;

2

the extent of government regulations;

uncertainty of clinical trial results;

a loss of any of our key management personnel;

our inability to develop or commercialize our product candidates due to intellectual property rights held by third parties and our inability to protect the confidentiality of our trade secrets; and

the cost and effects of potential litigation.

All written and verbal forward‑looking statements attributable to us or any person acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. We caution investors not to rely too heavily on the forward‑looking statements we make or that are made on our behalf. We undertake no obligation, and specifically decline any obligation, to update or revise publicly any forward‑looking statements, whether as a result of new information, future events or otherwise.

We encourage you to read Management’s Discussion and Analysis of our Financial Condition and Results of Operations and our consolidated financial statements contained in this annual report on Form 10‑K. We also encourage you to read Item 1A of Part I of this annual report on Form 10‑K, entitled “Risk Factors,” which contains a more complete discussion of the risks and uncertainties associated with our business. In addition to the risks described above and in Item 1A of this report, other unknown or unpredictable factors also could affect our results. Therefore, the information in this report should be read together with other reports and documents that we file with the Securities and Exchange Commission (“SEC”) from time to time, including on Form 10‑Q and Form 8‑K, which may supplement, modify, supersede or update those risk factors. As a result of these factors, we cannot assure you that the forward‑looking statements in this report will prove to be accurate. Furthermore, if our forward‑looking statements prove to be inaccurate, the inaccuracy may be material. In light of the significant uncertainties in these forward‑looking statements, you should not regard these statements as a representation or warranty by us or any other person that we will achieve our objectives and plans in any specified time frame, or at all.

Explanatory Note

On July 15, 2014, EPIRUS Biopharmaceuticals, Inc., a Delaware corporation and private company, or Private Epirus, completed its merger with EB Sub, Inc., a wholly-owned subsidiary of Zalicus Inc., a Delaware corporation, or Zalicus, or the Merger. As part of the Merger, Zalicus was renamed EPIRUS Biopharmaceuticals, Inc., or Public Epirus, and Private Epirus was renamed EB Sub, Inc., or EB Sub.

In this annual report, unless the context specifically indicates otherwise, “the Company,” “we,” “us,” “our,” and “Epirus,” refer to Public Epirus and its subsidiaries following the Merger, effective on July 15, 2014, and to Private Epirus and its subsidiaries prior to the Merger.

“EPIRUS Biopharmaceuticals”, “In Market, For Market”, “SCALE” and “Infimab” are registered trademarks of EPIRUS Biopharmaceuticals, Inc. Our logos and trademarks are the property of EPIRUS Biopharmaceuticals, Inc. All other brand names or trademarks appearing in this annual report are the property of their respective holders. Use or display by us of other parties' trademarks, trade dress, or products in this prospectus supplement is not intended to, and does not, imply a relationship with, or endorsements or sponsorship of, us by the trademark or trade dress owners.

3

Overview

We are a global biopharmaceutical company focused on building a pure-play, sustainable and profitable biosimilar business by improving patient access through cost-effective medicines. Our ability to deliver on this vision is anchored in our strong technical platform and pragmatic approach to development and commercialization.

Our business focuses on biosimilars, which are biologic drugs that are demonstrated to be “highly similar” to a previously approved biologic drug, known as a “reference product”. A biosimilar has to undergo extensive analytical characterization and prove similarity in efficacy and safety to the reference product in order to be approved by regulators.

Global healthcare systems continue to be challenged with expensive therapies. According to Express Scripts®, in the United States, the cost of a biologic drug accounted for approximately 40% of total drug spending in 2014. These cost pressures provide a large opportunity for biosimilars. Over the next decade, biologic drugs with approximately $90 billion worth of annual sales will lose patent protection, based on projected global sales estimates from EvaluatePharma®. Approximately half of the biosimilar market opportunity is outside the United States. We believe that biosimilars are likely to play a crucial role in reducing healthcare costs and improving patient access.

We are headquartered in Boston, Massachusetts, with laboratories and technical capabilities, including our proprietary CHOBC® cell line platform, in Utrecht, the Netherlands, and business operations, clinical and regulatory teams based in Zug, Switzerland.

As a biopharmaceutical company charting a course for long-term success, we are deeply committed to building a focused, sustainable and profitable pure-play biosimilar business. Specifically, we believe the path to achieving our goals has a foundation in the following five key strategies:

|

· |

build and utilize technical capabilities to optimize product characteristics and manage costs; |

|

· |

plan our pipeline to gain cost synergies from product development, through clinical development and to eventual commercialization; |

|

· |

focus on global markets where the regulatory, legal and commercial landscapes are more evolved while evaluating and preparing in the long term for potential United States market entry; |

|

· |

enter into partnership arrangements where we expect to retain substantial economics over time; and |

|

· |

implement an efficient global tax structure. |

Since our inception, we have maintained in-house technical capabilities supported by external vendor laboratories. In September 2015, we acquired our primary vendor laboratory, Bioceros Holding B.V., a Netherlands company, or Bioceros, to expand our biosimilar pipeline and to vertically integrate our product development capabilities. As a result of the acquisition, Bioceros has become our wholly-owned subsidiary, renamed Epirus Biopharmaceuticals (Netherlands) B.V.

Bioceros was focused on the development of monoclonal antibodies (mAbs). We acquired Bioceros’ proprietary CHOBC cell line platform, all related intellectual property rights, a fully equipped laboratory and bioreactor capabilities designed for the development of mAbs and protein therapeutics, with a focus on biosimilars, including capabilities for the production of three new biosimilar product candidates to add to our pipeline of biosimilar product candidates, as further described below. We believe that the addition of Bioceros staff and capabilities, combined with existing in-house expertise, provides us with a strong technical foundation to accelerate product development and optimize product quality. Specifically, we believe that our ability to rapidly and efficiently conduct and repeat experiments to optimize product quality and cell line titers and process yields will help us to reduce regulatory risk and manage long term cost of goods.

4

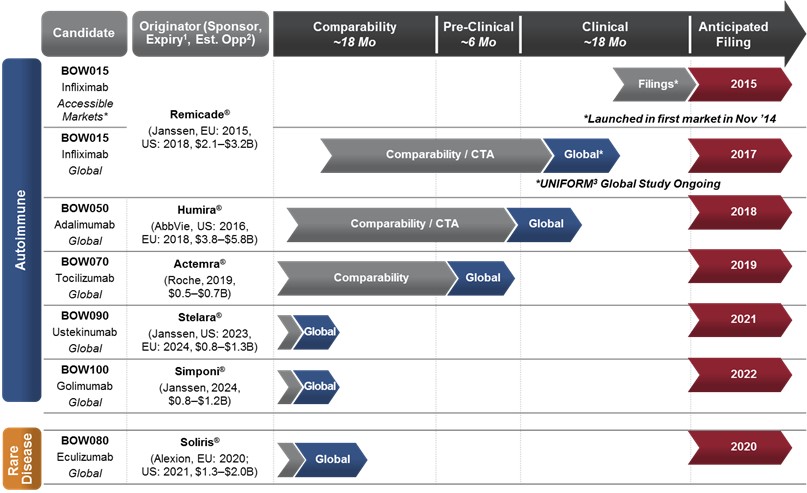

We currently have a robust and cohesive pipeline of five biosimilar product candidates in the autoimmune and inflammation areas, including BOW015, a biosimilar version of Remicade® (infliximab), BOW050, a biosimilar version of Humira® (adalimumab), BOW070, a biosimilar version of Actemra® (tocilizumab), BOW090, a biosimilar version of STELARA® (ustekinumab) and BOW100, a biosimilar version of SIMPONI® (golimumab).

We expect the standardization of our technology platform and the clustering of the therapeutic area will allow us to have a greater degree of focus, synergy and cost management across product development, manufacturing, clinical and commercialization. Additionally, we have expanded our therapeutic focus with a rare disease product candidate, BOW080, a biosimilar version of Soliris® (eculizumab). We believe there will be a significant unmet need for cost-effective therapies for rare diseases. Cumulatively, these six reference products generated approximately $29.2 billion in global innovator sales in 2014, according to EvaluatePharma. We estimate this to be a biosimilar market opportunity of more than $9 billion. Furthermore, there are over 20 other mAbs with near-term patent expiries clustered in five therapeutic areas, which we believe will provide mid- to long-term pipeline growth options for us, including expanding our rare disease business.

For our lead product candidate, BOW015, we have reported bioequivalence, efficacy and safety data from a previous Phase 1 study in healthy volunteers and a Phase 3 study in active rheumatoid arthritis patients, both of which demonstrated the equivalence of BOW015 to Remicade. Our Phase 3 study included an open label phase, where we demonstrated that patients can be safely initiated and effectively maintained on BOW015 for 58 weeks, and that patients can be safely switched from Remicade to BOW015 and effectively maintained out to 58 weeks. Using this regulatory package, in 2014, in collaboration with our commercialization partner Sun Pharmaceutical Industries Ltd., or Sun, we launched BOW015 as the first infliximab biosimilar in India, sold under the brand name InfimabTM. We have also filed for approval in additional Southeast Asian and Latin American countries.

To date, nearly 1,000 patients have been treated with BOW015. We expect this early experience to provide valuable in-market experience while we continue making BOW015 available to patients globally, to support filings in developed markets, and to build important commercial experience.

In November 2015, we completed manufacturing readiness for BOW015 to support the initiation of a global clinical program for BOW015. In February 2016, we initiated this global clinical program, which we expect to support regulatory filings in developed markets such as Europe and North America. The UNIFORM (Understanding BOW015 (infliximab-EPIRUS) and reference infliximab (Remicade®) in patients with active rheumatoid arthritis on stable doses of methotrexate) study is a 58-week, double-blind, one-to-one randomized, comparator-controlled multi-center global study to compare safety, efficacy and immunogenicity and demonstrate clinical equivalence of BOW015 with Remicade. We plan to enroll over 500 patients with active rheumatoid arthritis in the UNIFORM study, which will be conducted at sites in Europe, North America and Latin America. The primary endpoint at week 16 for the study will assess the proportion of patients that meet ACR20, which is a 20 percent or greater improvement in American College of Rheumatology assessment. We have been designing this clinical program in consultation with European regulatory bodies in order to obtain the data that may be necessary to support potential approval of BOW015 in developed markets.

Leveraging early commercial experience and our robust global clinical program, we expect to file for approval of BOW015 in developed markets, such as Europe and North America, in 2017. For the remainder of our pipeline, we expect that our filings will be global and harmonized.

We believe that the biosimilar market in the United States will likely be attractive over the long term. Currently there are near term challenges in the United States, including an evolving but uncertain regulatory framework and legal situation, a complex commercial environment, a fragmented payor market and a market which focuses on switching patients off existing reference drugs.

We believe that the most attractive market opportunity for biosimilars in the near term is outside of the United States. Many global markets outside the United States have more defined regulatory environments, limited legal encumbrance, commercial precedence and payors seeking lower cost biologics. For each of the markets outside of the United States, which collectively represent approximately 50% of the global opportunity for biosimilars, we intend to

5

take specific approaches to build profitable partnerships and, to date, we have grown the global distribution coverage of BOW015 in over 70 countries.

For European markets and select additional territories, in July 2015, we entered into an agreement with Swiss Pharma International AG, an affiliate of Pharmaceutical Works Polpharma S.A., or, together with Swiss Pharma International AG, Polpharma, for the development and commercialization of BOW015, BOW050 and BOW070 in certain designated territories. The designated territories include the European Union (with the exception of Austria, Belgium, Denmark, Finland, Luxembourg, the Netherlands and Sweden, which are reserved for us, along with Switzerland and Norway), together with certain countries in the Middle East, Turkey, Russia, and other countries comprising the Commonwealth of Independent States, or CIS.

In local production markets, such as China, where local authorities mandate or strongly encourage local production as a condition for regulatory and/or commercial acceptance, we intend to collaborate with local partners to enable in-country production of our products. We have entered into agreements with Livzon Mabpharm Inc., or Livzon, for the global development and commercialization of certain antibodies or related biological compounds, including BOW015 and BOW070, for China and associated markets.

In India, the current market and near-term markets, such as Latin America, in which our current BOW015 data package is expected to be sufficient for approval, we intend to pursue near-term product launches. This would enable us to gain valuable in-market patient exposure and commercial experience while we continue to work on making BOW015 available globally. This early commercial experience will strengthen our regulatory filings for Europe, the United States and additional global markets. In collaboration with our commercialization partner Sun, we launched BOW015 in India in November 2014, under the brand name Infimab. We expect to utilize our existing regulatory data package to gain regulatory approval for BOW015 in additional countries. In May 2015, we also entered into a development and future distribution agreement with mAbxience S.A., or Mabxience, a company organized and existing under the laws of Uruguay and a wholly owned subsidiary of CHEMO Group, for BOW015 in Latin American markets, including Argentina, Chile, Ecuador, Paraguay, Uruguay and Venezuela.

Finally, in the United States, we intend to retain rights and evaluate market conditions prior to determining a commercial plan commensurate with our objectives to create value. We are currently evaluating development and commercial options including partnerships, hybrid profit sharing approaches and potentially building or acquiring commercial infrastructure.

The combination of a global sales approach and a focus on deals which would allow us to retain substantial economic value is supported by our Swiss-based tax structure, which we believe will allow us to efficiently manage future cash for operations outside the United States.

Our long-term ability to deliver these important medicines to patients worldwide can only be achieved through a disciplined approach. Our experienced management team plans to address the diverse regulatory, legal and commercial landscape by gaining near-term market access, creating a strong technical platform with opportunities for sustainable pipeline growth, and finding tax-optimized partnership deals that maximize future value to provide us with a path forward to build a sustainable and profitable biosimilar business.

Going Concern

We believe that our existing cash and cash equivalents will be sufficient to fund our operations into the second quarter of 2016. As of December 31, 2015, our total unrestricted cash and cash equivalents was $31.5 million. We will need to raise additional capital in the near term to fund our operating requirements and continue as a going concern. If we cannot raise the money that we need in order to continue to operate our business, we will be forced to delay, scale back or eliminate some or all of our proposed operations. If any of these were to occur, there is a substantial risk that our business would fail.

This need to raise additional capital in the near term coupled with our recurring losses from operations and our stockholders’ deficit raise substantial doubt about our ability to continue as a going concern. As a result, our independent

6

registered public accounting firm included an explanatory paragraph in its report on our consolidated financial statements for the year ended December 31, 2015, which appear elsewhere in this annual report, with respect to this uncertainty. This uncertainty may adversely affect our ability to raise additional capital.

Products

Our product pipeline contains six products at different stages of development. The most advanced of these is BOW015 (infliximab), which has received marketing and manufacturing approval in India, and for which we have reported favorable Phase 1 and Phase 3 clinical data. Our other pipeline products, BOW050 (adalimumab), a proposed biosimilar to Humira, BOW070 (tocilizumab), a proposed biosimilar to Actemra, BOW080 (eculizumab), a proposed biosimilar to Soliris, BOW090 (ustekinumab), a proposed biosimilar to STELARA and BOW100 (golimumab), a proposed biosimilar to SIMPONI, are in preclinical development.

1. Ark Patent Intelligence and other public databases 2. Assumes 40% price discount, 40-60% biosimilar. 3. UNIFORM Study – Understanding BOW015 ( infliximab-EPIRUS) and reference infliximab (Remicade®) in patients with active rheumatoid arthritis on stable doses of methotrexate.

*BOW015 launched in its first market in collaboration with Sun under the trade name Infimab™ in India; additional near-term filings targeted for select accessible markets; Remicade is a registered trademark of Johnson and Johnson; Humira is a registered trademark of AbbVie; Actemra is a registered trademark of Chugai Seiyaku Kabushiki Kaisha Corp., a member of the Roche Group; Stelara is owned and marketed by Centocor Ortho Biotech Inc, a wholly owned subsidiary of Johnson & Johnson; Simponi is marketed by Janssen Biotech Inc; Soliris is a registered trademark of Alexion Pharmaceuticals, Inc.

BOW015 (Infliximab)

Our lead product candidate is BOW015 (infliximab, reference biologic Remicade), a monoclonal antibody against tumor necrosis factor alpha (TNF-α). It is intended for the treatment of inflammatory diseases including rheumatoid arthritis, Crohn's Disease, ankylosing spondylitis, psoriatic arthritis and psoriasis. According to EvaluatePharma, Remicade, a prescription product marketed globally by Johnson & Johnson, Merck Schering and Mitsubishi Tanabe, generated approximately $8.8 billion in global innovator sales in 2014. We have conducted extensive bioanalytical and physicochemical comparisons of BOW015 to Remicade and have data from a Phase 1 study in the

7

United Kingdom and a Phase 3 double blind comparator study in India demonstrating bioequivalence, safety, quality and efficacy of BOW015.

On September 23, 2014, we announced positive long-term data (58 week) from an efficacy and safety trial comparing BOW015 to Remicade. The study consisted of a 16 week, double blinded, head to head comparison with Remicade for safety and efficacy followed by an open label phase where Remicade responders were switched to BOW015 and all patients were followed for the duration of the study. The study met its primary endpoint of ACR20 response, the American College of Rheumatology criteria for clinical improvement in patients with rheumatoid arthritis, indicating a 20% improvement across a series of diagnostic parameters. These patients were then followed out to week 58 in an open label phase of the trial, with BOW015 patients remaining on BOW015 and Remicade responders being switched to BOW015 for the remainder of the 58 weeks. Furthermore, these data suggest that patients can safely be started and durably maintained on BOW015 and that patients can safely be switched from Remicade to BOW015.

Using this regulatory package, we filed for and received approval in India in September 2014, and have also filed for approval in additional Southeast Asian and Latin American countries. In collaboration with our commercialization partner Sun, we launched BOW015 in India in November 2014. BOW015 is sold under the brand name Infimab and is the first infliximab biosimilar approved in India. To date, nearly 1,000 patients have been treated with BOW015.

The early commercial experience in India and near-term anticipated experience in select Southeast Asian and Latin American countries, will provide valuable in-market experience while we continue making BOW015 available to patients globally. This experience will support filings in developed markets, such as the United States and Europe, and will build important commercial experience.

In November 2015, we completed manufacturing readiness for BOW015 to support the initiation of a global clinical program for BOW015. In February 2016, we initiated this global clinical program, which will support regulatory filings in established markets such as Europe and North America. The UNIFORM Study is a 58-week, double-blind, one-to-one randomized, comparator-controlled multi-center global study to compare safety, efficacy and immunogenicity and demonstrate clinical equivalence of BOW015 with Remicade. We plan to enroll over 500 patients with active rheumatoid arthritis in the UNIFORM study, which will be conducted at sites in Europe, North America and Latin America. The primary endpoint at week 16 for the study will assess the proportion of patients that meet ACR20. We have been designing this clinical program in consultation with European regulatory bodies in order to obtain the data that may be necessary to support potential approval of BOW015 in developed markets. We expect to file for approval of BOW015 in developed markets, including Europe and North America, in 2017.

We have agreements with Polpharma for the development and commercialization of BOW015 in certain developed markets, with Livzon for the development and commercialization of BOW015 in certain local production markets, and with Sun and Mabxience for the development and commercialization of BOW015 in certain accessible markets. In total, over 70 countries have global distribution coverage for BOW015.

BOW050 (Adalimumab)

We are currently developing and evaluating commercialization opportunities for BOW050 as a proposed biosimilar to Humira in a range of target markets, including our collaboration with Polpharma for the development and commercialization of BOW050, among our other product candidates, in the territories designated under the Polpharma agreement. Humira (marketed by AbbVie) is an inhibitor of TNF-α used to treat inflammatory diseases, including rheumatoid arthritis and certain other forms of adult and pediatric arthritis, ankylosing spondylitis, inflammatory bowel disease, and chronic psoriasis and psoriasis. According to EvaluatePharma, Humira generated approximately $12.9 billion in global innovator sales in 2014. Physiochemical characterization of BOW050 is ongoing and the product may enter clinical trials in late 2016, providing a path to an anticipated global filing in 2018.

8

BOW070 (Tocilizumab)

We are in the comparability phase of development of BOW070, a proposed biosimilar version of Actemra (marketed by Genentech/Roche). Actemra is an immunosuppressive drug for the treatment of rheumatoid arthritis, polyarticular arthritis and systemic juvenile idiopathic arthritis. According to EvaluatePharma, Actemra generated approximately $1.3 billion in global innovator sales in 2014. We are targeting a global filing for BOW070 in 2019.

We have agreements with Polpharma for the development and commercialization of BOW070 in certain developed markets and with Livzon for the development and commercialization of BOW070 in certain local production markets.

BOW080 (Eculizumab)

We are in the comparability phase of development of BOW080, a proposed biosimilar version of Soliris (marketed by Alexion Pharmaceuticals, Inc.). Soliris is currently indicated to treat ultra-rare blood disorders, including paroxysmal nocturnal hemoglobinuria (PNH) and atypical hemolytic uremic syndrome (aHUS). According to EvaluatePharma, Soliris generated approximately $2.2 billion in global innovator sales in 2014. We are targeting a global filing for BOW080 in 2020.

BOW090 (Ustekinumab)

We are in the comparability phase of development of BOW090, a proposed biosimilar version of STELARA (marketed by Janssen Pharmaceuticals, Inc.). STELARA is an immunosuppressant drug for the treatment of plaque psoriasis and psoriatic arthritis. According to EvaluatePharma, STELARA generated approximately $2.1 billion in global innovator sales in 2014. We are targeting a global filing for BOW090 in 2021.

BOW100 (Golimumab)

We are in the comparability phase of development of BOW100, a proposed biosimilar version of SIMPONI (marketed by Janssen Pharmaceuticals, Inc.). SIMPONI is an inhibitor of TNF-α used to treat inflammatory diseases, including rheumatoid arthritis, ankylosing spondylitis, ulcerative colitis, and psoriatic arthritis. According to EvaluatePharma, SIMPONI generated approximately $1.9 billion in global innovator sales in 2014. We are targeting a global filing for BOW100 in 2022.

Management

Our senior management team and our board of directors have worked for prominent biotechnology and pharmaceutical companies including Amgen, Biogen Idec, Pfizer, Quintiles, Wyeth (acquired by Pfizer), Genzyme (acquired by Sanofi), Shire, Cephalon, Millennium, Takeda, BioAssets (acquired by Cephalon), Cubist Pharmaceuticals (acquired by Merck), Invida (acquired by Menarini), Therion Biologics and ToleRx. Our president and chief executive officer, Amit Munshi, was a co‑founder, and the chief business officer at Kythera Biopharmaceuticals (acquired by Allergan Plc), which underwent a successful initial public offering on NASDAQ in 2013. Mr. Munshi has more than 25 years of pharmaceutical and biotechnology experience in both the United States and internationally, including general management, product development, licensing and business development.

Strategy

We believe that successfully building a pure-play biosimilar business requires a clear path toward sustainability and profitability. We have cultivated a therapeutically focused product portfolio and are diligently aware of profitability and sustainability. In order to reach our objectives, we have chosen to focus on markets that meet three important criteria: (1) clear, precedent‑driven regulatory pathway; (2) minimal exposure to potential patent encumbrances; and (3) a commercially viable path. We believe that the most attractive market opportunity for biosimilars in the near term is outside of the United States. Europe and the markets in the Middle East, Latin America and Asia have defined regulatory environments, limited legal encumbrance, commercial precedence and payors seeking lower cost biologics. For each of

9

the markets outside of the United States, which collectively represent approximately 50% of the global opportunity for biosimilars, we intend to take specific approaches to build profitable partnerships.

We believe the market in the United States is large and attractive over the long term, however, in the near term, challenges include an evolving but uncertain regulatory framework and legal situation, a complex commercial environment with a need to focus on switching patients off existing reference drugs, and a fragmented payor market.

Our key priorities in executing on our strategy include:

|

· |

In Europe, we intend to commercialize our products using a licensing or distribution model in conjunction with direct sales. These markets are expected to be the financial anchor of our business in the near- to mid-term. Europe has an existing regulatory approval pathway and a patent environment we believe offers a clear path forward for our pipeline. From a commercial perspective, the European market for biosimilars is strengthened by the desire of governments to reduce overall healthcare expenditure. Through a combination of substitution rules, regional tenders and political pressure to introduce biosimilars, Europe represents a commercially tractable market. For European markets, in July 2015, we entered into an agreement with Swiss Pharma International AG, an affiliate of Pharmaceutical Works Polpharma S.A., for the development and commercialization of BOW015, BOW050 and BOW070 in certain designated territories. The designated territories include the European Union (with the exception of Austria, Belgium, Denmark, Finland, Luxembourg, the Netherlands and Sweden, which are reserved for us, along with Switzerland and Norway), together with certain countries in the Middle East, Turkey, Russia, and other countries comprising the Commonwealth of Independent States, or CIS. |

|

· |

In local production markets, such as China, we intend to collaborate with local partners to enable in‑country production of our products. In local production markets, local authorities mandate or strongly encourage local production, and additional clinical work above and beyond that submitted for Indian regulatory approval will likely be necessary to secure approval for BOW015. In these markets, several biologics have already seen their key patents expire. Furthermore, we expect to establish local commercialization partnerships in these, often tender driven, markets. Any necessary additional local studies would likely be supported by our current or future local partners. For instance, in China, we have entered into an Exclusive License and Collaboration Agreement and a New Collaboration Compound Supplement to the Collaboration Agreement with Livzon for the global development and commercialization of certain antibodies or related biological compounds, including BOW015 and BOW070. Finally, where appropriate, we will leverage our proprietary SCALE manufacturing technology (as described further below) to generate In Market, For MarketTM manufacturing solutions in these markets. |

|

· |

In near-term markets, such as India and Latin America, in which our current regulatory data are expected to be sufficient for approval, we intend to pursue product launches. These markets are likely to reference and accept as the basis for approval the Indian BOW015 regulatory package and the current data set and also allow importation of BOW015 manufactured outside of such markets. These markets often present no innovator patent protection. We expect that this will enable us to gain in-market patient exposure needed to support eventual filings in developed markets and allow us to build important commercial and commercial support services with and for our partners. Under the terms of our existing license agreement, Sun is responsible for the commercialization of BOW015 in India and selected Southeast Asian and North African countries. In collaboration with Sun, we launched BOW015 in India in November 2014. BOW015 is sold under the brand name Infimab and is the first infliximab biosimilar approved in India. We have also filed for approval in additional Southeast Asian and Latin American countries. In May 2015, we also entered into a development and future distribution agreement with mAbxience S.A., a company organized and existing under the laws of Uruguay and a wholly owned subsidiary of CHEMO Group, for BOW015 in Latin American markets, including Argentina, Chile, Ecuador, Paraguay, Uruguay and Venezuela. |

|

· |

Finally, in the United States, we intend to evaluate our commercial plan commensurate with our objectives to create value. As the regulatory and legal environments in the United States become clearer, |

10

we anticipate seeking a commercial partner or alternative commercial model for BOW015, which may include contracting directly with payors or other third‑party entities. We are currently evaluating development and commercial options including partnerships, hybrid profit sharing approaches and potentially building or acquiring commercial infrastructure. |

Our strategy for commercial success relies on tailored approaches to address the diversity of our target global markets. Additionally, we intend to leverage our development and commercial experience with BOW015 to both advance our pipeline and our overall direct sales infrastructure.

Europe

Europe has an established regulatory framework for biosimilars, and the European Medicines Agency (EMA) has approved Celltrion's infliximab program under the trade names Inflectra/Remsima®. The initial launch of Inflectra/Remsima and the approval of over 20 biosimilars over the last decade suggest that the legal landscape in Europe is conducive to the introduction of biosimilars. In general, the European patent landscape provides for far fewer patent extensions for manufacturing, method of use, or processes, as compared to the patent landscape in the United States. Finally, the European market for biosimilars is strengthened by the desire of governments to reduce overall healthcare expenditure. Through a combination of substitution rules, regional tenders and political pressure to introduce biosimilars, Europe represents a commercially attractive market.

Our operating strategy across Europe and other select territories is to enter into profit-sharing collaborations in order to retain maximum value. In July 2015, we entered into a Collaboration Agreement with Polpharma, for the development and commercialization in certain designated territories of our product candidates, BOW015, BOW050 and BOW070. The designated territories include the European Union (with the exception of Austria, Belgium, Denmark, Finland, Luxembourg, the Netherlands and Sweden, which are reserved for us), together with certain countries in the Middle East, Turkey, Russia, and other countries comprising the Commonwealth of Independent States, or CIS. We will also retain exclusive rights for the three products in North America and other markets outside of the designated territories, including Switzerland and Norway. Polpharma is a leading generics player based in Poland, operating across Europe, the Caucasus and Central Asia, with manufacturing subsidiaries in Russia and Kazakhstan. Polpharma is among the top 20 generic drug manufacturers in the world with annual sales of approximately $1 billion. Polpharma’s portfolio includes about 600 products with another 200 in pipeline.

Local production markets, including China

In local production markets, such as China, governments either mandate or have a strong preference for local manufacture and supply of pharmaceutical products and have implemented frameworks and/or established various incentives for such local production. These incentives may include facilitating access to funding, acceleration of the regulatory review process, improved or preferential access to government tenders and direct or indirect trade barriers on imported products. In these markets, there is a clear regulatory and patent landscape. Also, the commercial opportunity is substantial, tractable and protectable. In most of these markets, the transference of product manufacturing is rewarded by government incentives, access to tenders, and ability to restrict competition from imported products.

In China, the central and provincial governments encourage local production of biopharmaceuticals. In September 2014, we entered into an Exclusive License and Collaboration Agreement (the “Livzon Collaboration Agreement”) with Livzon for the global development and commercialization of certain antibodies or related biological compounds, including BOW015. In September 2015, we entered into a New Collaboration Compound Supplement with Livzon to add BOW070 as a compound to be governed by the Livzon Collaboration Agreement. Livzon is a fully integrated pharmaceutical company based in Guangdong Province, China, with over 5,000 employees, multiple production facilities across China, and approximately $730 million in revenue from over 200 marketed products across a range of therapeutic areas. Livzon is focused on monoclonal antibody development and production, leveraging single use disposable systems that we expect will be compatible with the optimized processes we are currently developing with our partners for BOW015 and BOW070.

11

Near-term markets, including India and Latin America

In India, our current market and near-term markets, including Southeast Asia and Latin America, regulatory frameworks are clear and patent environments allow for freedom to operate. From a commercial perspective, innovator drugs have had limited market penetration in these markets due, in part, to the relatively high cost of these branded products. Further, as evidenced by several products already launched, biosimilars may actually be able to significantly expand the accessible patient populations in these markets. The commercial focus in these markets is market development and expansion. As further discussed below, in March 2014, our manufacturing partner, Reliance Life Sciences Pvt Ltd, or RLS, obtained manufacturing and marketing approval on our behalf in India for BOW015 as a treatment for rheumatoid arthritis. In September 2014, again with RLS, we received final manufacturing clearance from the Drug Controller General of India, or DCGI.

In January 2014, we entered into an agreement with our commercialization partner, Sun, to commercialize BOW015 in India and other selected Southeast Asian and North African markets, pending marketing authorization in those jurisdictions. These markets, including India, do not require that BOW015 be manufactured within the applicable country. In collaboration with Sun, we launched BOW015 in India in November 2014. BOW015 is sold under the brand name Infimab and is the first infliximab biosimilar approved in India. To date, nearly 1,000 patients have been treated with BOW015. We will be responsible for any additional development activities required by Indian regulatory authorities. Sun is responsible for all marketing and commercialization activities with respect to BOW015 in India, as well as any costs associated with development, regulatory filings and marketing and commercialization in the additional countries covered by the agreement. Under the terms of the agreement, we will supply Sun with commercial products, and Sun will be required to make payments to us upon achievement of certain development and sales milestones for BOW015, as well as to pay us a royalty on net sales of BOW015 in all territories covered by the agreement.

In addition to India and the other countries covered by our agreement with Sun, we believe that our existing regulatory dossier for BOW015 will be sufficient to achieve regulatory approval in a range of South and Central American countries. In late 2015, we also filed for approval in additional Southeast Asian and Latin American countries. We expect to grant rights to commercialize BOW015 in these countries, pending receipt of marketing authorization, through a licensing structure similar to the approach taken in India.

In May 2015, we entered into an Exclusive License Agreement (the “Mabxience License Agreement”) with Mabxience for the development, manufacturing and commercialization of BOW015. Under the Mabxience License Agreement, we granted to Mabxience an exclusive, royalty-bearing, non-transferable, sublicenseable license to develop, manufacture, commercialize and distribute BOW015 in the Mabxience territory. The Mabxience territory consists of Argentina, Chile, Ecuador, Paraguay, Uruguay and Venezuela. Pursuant to the Mabxience License Agreement, Mabxience will be solely responsible, at its expense, for all aspects of commercialization of licensed product in the Mabxience territory. Mabxience is a global fully integrated biopharmaceutical company specialized in research, development and manufacturing of biosimilars for the treatment and/or prevention of several diseases in diverse therapeutic areas. Mabxience is acting worldwide, creating a broad and balanced presence in all major pharmaceutical markets to address global opportunities and customers’ needs, with full-line research and manufacturing capabilities and highly qualified professionals worldwide. Mabxience is a wholly-owned subsidiary of CHEMO Group, a well-established Spanish-based global healthcare corporation.

United States

Given the still nascent and uncertain biosimilar market in the United States, our strategy remains focused on evaluating partnerships or an alternative commercial model, which may include contracting directly with payers or other third-party entities. While the recently completed FDA advisory committee hearing to weigh the approvability of Celltrion’s Remsima for commercial sale in the United States resulted in very encouraging regulatory signals in the United States, the need for greater legal and commercial clarity remain as important considerations in our partnership discussions and decisions.

12

Industry Overview

Biosimilars Definition

Biosimilars are highly similar versions of approved biological drug products, referred to as reference or innovator products. Because a biosimilar product may reference existing information regarding the structure, safety, and efficacy of a previously approved reference product, a biosimilar product application emphasizes analytical characterization to demonstrate similarity between the proposed biosimilar and the reference product. In addition, preclinical and clinical studies may be required to support an application for approval. Biosimilars are often characterized as fitting within one of two categories: first generation, less complex biologics; and second generation, more complex biologics, including fusion proteins and monoclonal antibodies, or mAbs.

Both first and second generation biosimilars are significantly more complex and difficult to characterize, manufacture and develop than small molecule generics. For example, the first generation biological drug, Epogen (epoetin alfa) has a molecular weight that is 25x greater than that of small molecule drug Lipitor (atorvastatin calcium). The second generation mAb biologics—e.g., Remicade (infliximab) and Humira (adalimumab)—are, in turn, nearly 5x larger than the first generation biologicals. MAb biosimilars are complex to manufacture in part because they require the use of living organisms to produce them, and this introduces challenges in manufacturing and production on a commercial scale. Glycosylation (complex carbohydrate branches that are added by the cellular machinery) and other forms of molecular modification are hallmarks of proteins produced in living cells, in particular mammalian cells. Compared to first generation biologics, mAbs are not only larger but also have greater structural complexity, including complex glycosylation patterns which may be critical for the function and activity of the molecule. MAb biosimilars therefore must be rigorously and accurately characterized to establish their biosimilarity to reference biologics in terms of glycosylation patterns, or glycoforms, and other important molecular modifications. Biosimilars—both first and second generation—also require significantly more clinical testing and regulatory review than small molecule generics, as described in more detail below.

The manufacturing, clinical and regulatory complexity and challenges of developing “second generation” biosimilars create barriers to market entry. As such, these “second generation” biosimilars can usually be sold at relatively higher prices, and with better margins, than small molecule generics and first generation biosimilars.

Regulatory Aspects of Biosimilars

Similar to other follow‑on product opportunities, product development proceeds differently with biosimilars than with innovative biologic candidates. This is a result of abbreviated development requirements for the approval of biosimilars as compared with innovative biologic products. Because the structure/function and target characteristics of the reference biologic are already known, a biosimilar product application emphasizes analytical characterization to demonstrate similarity between the biosimilar and the reference biological product, which regulators have already determined to be safe and effective.

Early Reduction of Risk in Drug Development

In the development of novel pharmaceuticals and biologic products, the question of whether or not a product will ever reach the point of being commercially viable remains largely unanswered. As such, the innovator company assumes significant risk through the completion of Phase 3 trials, in which the drug or biologic therapeutic is administered to a sufficient number of subjects to make a definitive determination of a drug’s safety and efficacy. Comprehensive Phase 3 trials are conducted for novel biologics at significant cost and exposure for the innovator company. In contrast, a large proportion of de‑ risking occurs much earlier in the development process of biosimilars through analytic testing. As the antibody, its target, and its mechanism of action have already been validated clinically by the reference product sponsor, and the dose, regimen, and indications are already known, early testing provides greater insight into the future regulatory success for biosimilars. Preclinical and early clinical studies required to demonstrate

13

comparability to the originator drug’s pharmacokinetic/pharmacodynamic (PK/PD), safety, and potency profile may provide early indications of a product’s eventual regulatory outcome.

The regulatory standards applicable to establish such biosimilarity vary by jurisdiction. Over the last 10 years, many jurisdictions globally have established formal regulatory regimes for review and approval of biosimilar products, but these regimes are at differing stages of development, with limited harmonization among jurisdictions.

Technical Complexity of Biosimilars

Historically, biologics have not yielded readily to the development of generic versions. Because biologics are structurally far larger and more complex than small molecule drugs, their manufacturing processes and requirements are correspondingly more complex as well. Biologics are produced through a technologically challenging five‑step process:

|

· |

Scientists isolate and identify the genetic code of the protein they want to produce. |

|

· |

This genetic code is inserted into living cells (bacteria, yeast, or cultured mammalian cells). Once inside the cell, the genetic code instructs the cell to produce the protein, or biotech medicine, which will later be used to treat a specific disease. Mammalian cells are the most complex of the various cell lines and generate complexities in protein structure through various biochemical modifications. |

|

· |

These genetically modified cells (known as cell lines) are carefully selected and cultured over time in bioreactor tanks, surrounded by nutrients designed to encourage protein production. The specific conditions for production determine important physical attributes of the protein—such as glycosylation (complex carbohydrate branches that are added by the cellular machinery)—for its function. The structure and function of the final product is therefore highly sensitive to the specific conditions under which it is generated. |

|

· |

The protein is then isolated from the cells and the nutrients through a sequence of purification processes. |

|

· |

Finally, the isolated protein is packaged, typically after a number of steps to ensure sterility and stability, into sterile vials or syringes for use by doctors and patients. |

Because the structure and function of a biologic, such as a monoclonal antibody, are directly linked to its production process in living systems, companies that intend to develop a biosimilar must go through all five steps above, from isolation and identification of the target protein and creation of a proprietary cell line, to final packaging of the drug product. Furthermore, companies must go to great lengths to characterize their molecules relative to the reference biologic. They must also prove to regulators that the proposed biosimilar is highly similar to the original in terms of safety and efficacy through a combination of laboratory and clinical studies. In summary, biosimilars must be shown to be comparable to their reference biologics in terms of structure, purity, safety and efficacy.

Importantly, just as there is variation among individual human beings at the biochemical level, there is also natural variation among biologic molecules created by cell systems, because they are derived directly from living systems. Even originator biologics are characterized by inherent structural and functional variability. This leads to a range of profiles and performance for the innovator molecules, themselves, even among batches produced at the same facility. As a result, “identical” copies of biologics such as antibodies are not the objective for biosimilars. Instead, biosimilars must fall within a range of values across important structural and functional parameters compared to those of the reference drug.

Barriers to Entry

The high technical and performance standards that every biosimilar must achieve to gain regulatory approval provide two advantages to biosimilar developers and manufacturers, such as our company. First, such standards create a significant barrier to entry in the form of both regulatory and clinical hurdles that a company must overcome to bring biosimilar products to market, thus increasing the complexity and related costs for potential competitors. Second, these

14

high standards are expensive to achieve, thus the limited number of producers who can meet these standards can then command pricing for biosimilar products that, while lower than the pricing for the reference product, is still high enough to generate meaningful revenues and profits.

Competition

Based on our market analysis, we may be subject to competition for BOW015 in various jurisdictions from the following groups:

(1)Johnson & Johnson developed the reference product for BOW015, Remicade, along with its partners Merck Schering and Mitsubishi Tanabe, which are responsible for sales outside the United States. Remicade is one of the longest established biologics, supported by extensive safety and efficacy data and widespread use in multiple indications. We expect that Remicade’s market share will gradually erode over time with the advent of biosimilars; however, Johnson & Johnson will seek to defend its market share against biosimilar entry, which may include reduction in prices and other incentives.

(2)Celltrion (Korea) and Hospira, Inc. (acquired by Pfizer) co-commercializes a biosimilar infliximab product in European and other global markets. Celltrion markets its product under the name Remsima® and Hospira under the name Inflectra®. Remsima and Inflectra were approved by the EMA in 2013 with all approved indications as Remicade and represent the first biosimilar infliximab to be launched in major markets. Celltrion’s Biologics License Application in the United States is currently under FDA review with a decision expected in the first half of 2016. It is likely that Celltrion, if approved, will launch Remsima in the United States upon expiration of the patent protection on Remicade in 2018.

(3)We are aware that other companies, including Samsung Bioepis, Pfizer and Amgen, are in pre-clinical and clinical stages of development and may become competitors for BOW015 in various markets over time. In March 2015, Samsung Bioepis submitted a Marketing Authorization Application to the EMA for its biosimilar infliximab. A decision from the EMA has yet to be announced. Samsung Bioepis and Biogen Idec also recently entered into a joint venture to develop, manufacture and market biosimilars. For the other companies, there is limited data available and we cannot currently predict if and when the potential competitors will launch in our target markets.

Based on our market analysis, we may be subject to competition for BOW050 in various jurisdictions from the following groups:

(1)AbbVie developed the reference product for BOW050, Humira. Humira is supported by extensive safety and efficacy data and widespread use in multiple indications. We expect that Humira’s market share will gradually erode over time with the advent of biosimilars; however, AbbVie will seek to defend its market share against biosimilar entry, which may include reduction in prices and other incentives.

(2)Currently Cadila Healthcare Ltd., is the only company that markets a biosimilar adalimumab under the brand name Exemptia™. Exemptia is only approved and available in India with the full label as Humira.

(3)We are aware that other companies, including Amgen, Samsung Bioepis, Pfizer, Boehringer Ingelheim, Sandoz, Momenta/Baxter, Coherus, Biocon/Mylan, and Therapeutics Proteins International are in pre-clinical and clinical stages of development and may become competitors for BOW050 in various markets over time. In November 2015, Amgen submitted a Biologics License Application to the FDA for its biosimilar adalimumab and subsequently submitted a Marketing Authorization Application to the EMA in December. Both applications are currently

15

pending regulatory review. For the other companies, there is limited data available and we cannot currently predict if and when the potential competitors will launch in our target markets.

Based on our market analysis, we may be subject to competition for our other biosimilar product candidates in the early stages of development, including BOW070, BOW080, BOW090 and BOW100. There is limited publicly available data on potential competitive molecules for these product candidates at this time.

Clinical Development of BOW015 (Infliximab)

We have conducted extensive bioanalytical and physicochemical comparisons of BOW015 to Remicade and have data from a Phase 1 study in the United Kingdom and a 189-patient Phase 3 double blind comparator study in India demonstrating bioequivalence, safety and efficacy of BOW015. The Phase 3 study in India met the primary endpoint of efficacy at an interim analysis conducted at 16 weeks and finished its open label phase with a 54-week end-point in the third quarter of 2014. In March 2014, BOW015 was granted manufacturing and marketing approval in India through our manufacturing partner RLS as a treatment for rheumatoid arthritis. Final manufacturing site authorization was received in July 2014. The approval was based on the 16-week, double blind safety and efficacy data comparing BOW015 against Remicade as the active comparator and reference product, in accordance with the required regulatory process in India. In November 2014, we launched BOW015, under the brand name Infimab, in India with Sun and intend to launch in additional territories thereafter by leveraging our existing regulatory data package.

In November 2015, we completed manufacturing readiness for BOW015 to support the initiation of a global clinical program for BOW015. In February 2016, we initiated this global clinical program, which will support regulatory filings in established markets such as Europe and the United States. The UNIFORM Study is a 58-week, double-blind, one-to-one randomized, comparator-controlled multi-center global study to compare safety, efficacy and immunogenicity and demonstrate clinical equivalence of BOW015 with Remicade. We plan to enroll over 500 patients with active rheumatoid arthritis in the UNIFORM study, which will be conducted at sites in Europe, North America and Latin America. The primary endpoint at week 16 for the study will assess the proportion of patients that meet ACR20. We have been designing this clinical program in consultation with European regulatory bodies in order to obtain the data that may be necessary to support potential approval of BOW015 in developed markets. We expect to file for approval of BOW015 in developed markets, including Europe and North America, in 2017.

Since BOW015 is a biosimilar molecule, its characterization requires comparative analysis to the reference product, Remicade. The BOW015 drug substance and drug product manufacturing processes have been designed in conjunction with our manufacturing partners to make the final BOW015 drug product comparable to that of Remicade, and with comparable safety and efficacy in accordance with regulatory requirements.

We have produced a data package to demonstrate biosimilarity of BOW015 to Remicade. Its comparability data set, developed under a comparability and characterization protocol, addresses the physicochemical, biochemical and biological properties of infliximab and has been designed to assess biosimilarity between the reference product and BOW015. Critical Quality Attributes, or CQAs, are physical, chemical, biological or microbiological properties or characteristics that should be within appropriate limits to ensure the desired product quality. The CQAs of infliximab have been identified based on the mechanism of action, clinical experience, impact/risk assessment of production processes and the assessed ranges of specific attribute data generated by analysis of multiple lots of Remicade. The CQAs are supported by Annex I of the Summary of Product Characteristics of the Remicade European Public Assessment Report. Full side-by-side characterization of BOW015 and Remicade, including all CQAs for infliximab, has been completed. The data set includes all known attributes that have the potential to impact safety, potency and efficacy.

The types of assays used to assess biosimilarity include the following:

|

· |

Physicochemical. These are assays that measure the physical and chemical structure of the molecule. |

|

· |

In vitro biochemical. These are assays that measure the interaction of the molecule with other molecules (e.g. target binding). |

16

|

· |

In vitro biological. These are assays that measure the interaction of the molecule with biological media (e.g. cellular or animal test systems). |

These three levels of characterization are complementary and correlations are drawn from the individual and aggregate findings. For example, glycosylation heterogeneity (a physicochemical attribute) has direct impact on FcᵞRIIIa binding (a biochemical attribute), which in turn drives ADCC (antigen-dependent cellular cytotoxicity) activity (a biological attribute). In this way, multiple data sets support and confirm each other and the biosimilarity of BOW015 to Remicade.

The assessment of CQAs demonstrated similarity between BOW015 and Remicade. Both BOW015 and Remicade are produced using similar manufacturing processes. Minor differences between BOW015 and Remicade in the non-critical quality attributes may be consequences of differing manufacturing technologies and have not demonstrated adverse impact on the biology and efficacy of BOW015 in either in vitro or clinical studies.

We have also conducted multiple preclinical studies on BOW015. These studies include:

|

· |

Single dose toxicity of BOW015 in Swiss albino mice |

|

· |

Single dose toxicity of BOW015 in Wistar rats |

|

· |

Repeat dose (4-week) study in Wistar rats |

|

· |

Repeat dose (4-week) study in New Zealand White Rabbits |

|

· |

Skin sensitization study of BOW015 in Dunkin Hartley Guinea Pigs (Maximization Test) |

We believe that BOW015 has yielded satisfactory results in each of the preclinical studies to support regulatory filings in each of the additional markets we are seeking to target. Infliximab binds selectively to human and chimpanzee tumor necrosis factor-alpha (TNF-α), and thus additional preclinical studies in non-relevant species were not required by Medicines and Healthcare Products Regulatory Agency (UK) prior to initiating Phase 1.

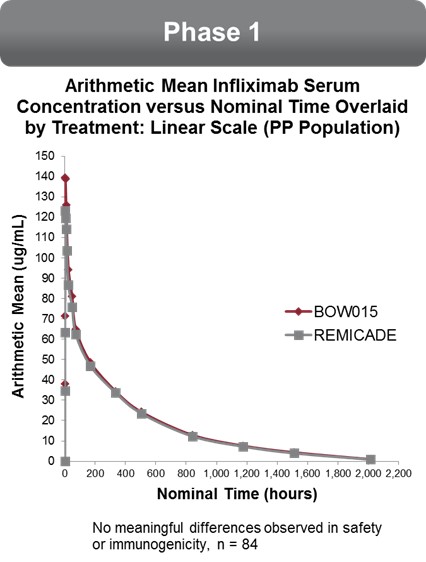

BOW015 Phase 1 Study

Our Phase 1 bioequivalence study was conducted in the United Kingdom in 2012 under the authority of the Medicines and Healthcare Products Regulatory Agency. The primary objective of the study was to compare the pharmacokinetics of infliximab administered by intravenous infusion. The secondary objectives of the study were to assess (i) the safety and tolerability and (ii) immunogenicity of BOW015 compared to Remicade. The study was conducted at a single clinical site and compared the safety and pharmacokinetic profile of BOW015 to Remicade after a single intravenous dose. The two drugs were considered to be similar if at various timepoints the concentrations of the drugs were comparable and were within the specific statistical parameters of 80%‑125%. The study design and criteria for success were based on standard bioequivalence requirements.

Eighty‑four healthy volunteers were randomized one‑to‑one and given either BOW015 or Remicade via intravenous infusion at a dose level of 5mg/kg with a 12‑week follow‑up period. The study was to detect bioequivalence at 90% confidence interval of BOW015 to Remicade. Out of the 84 subjects, 43 evaluable subjects received the test product BOW015 and 41 subjects received the reference product Remicade.

The profile of BOW015 and Remicade is shown in the graph below. The pre‑ defined pharmacokinetic values for the maximum height of the drug concentration as well as the pattern of elimination are similar. Thus, the study demonstrated similarity in PK profiles between BOW015 and the reference product Remicade. A single severe adverse

17

event was reported in one of the patients receiving Remicade. This was considered by the investigator as unlikely to be related to the experimental protocol.

No relevant differences in immunogenicity test results between the two treatment groups were observed, nor were any differences observed between the two groups in safety or tolerability.

BOW015 Phase 3 Study

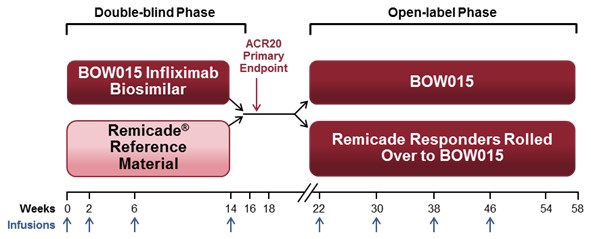

We conducted a randomized, double-blind, active comparator Phase 3 study in India of the efficacy and safety of BOW015 in patients with severe, active rheumatoid arthritis on stable doses of methotrexate. The study randomized subjects to the two treatment arms in a 2:1 allocation. Out of 189 total subjects, 127 were given BOW015 and 62 were given Remicade during the first 16 weeks of the study. The primary endpoint of the study was equivalence of both arms on the standardized American College of Rheumatology 20% improvement (ACR20) scoring system—a composite scoring system that includes objective laboratory measures as well as physician and patient assessments of well-being. Secondary endpoints included the ACR50 and ACR70 (50% and 70% improvement respectively) and the various components of the ACR20 scoring system. From week 22, BOW015 responders were administered BOW015 in an open-label phase for the study duration of 54 weeks, while Remicade responders were crossed over into the open label phase and switched to BOW015 for the study duration of 54 weeks. Non-responders immediately entered a three-month follow-up phase.

Both BOW015 and Remicade were administered at a dose of 3mg/kg given as an intravenous infusion at week 0, followed with similar doses at weeks 2, 6 and 14. Subjects were assessed at week 16 and responders were able to enter an open‑label phase. In the open‑label phase, subjects received BOW015 at a dose of 3mg/kg given as an intravenous

18

infusion at weeks 22, 30, 38 and 46 and were followed up at Weeks 54 and 58. Subjects who were non‑responders at week 16 entered a follow‑up phase for immunogenicity, PK and safety for an additional 3 months.

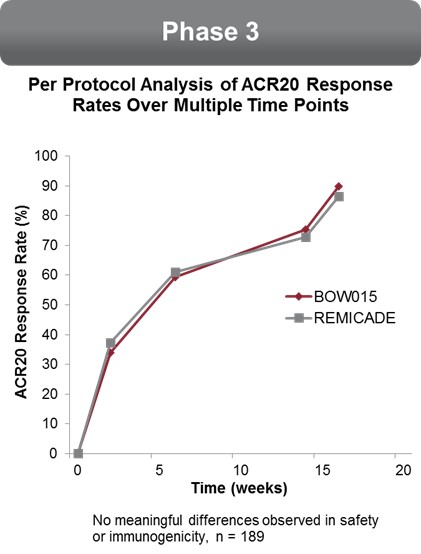

The 16‑week data showed that patients responded to BOW015 at a rate of 89.8% ACR20 compared to an 86.4% ACR20 response rate to Remicade. This outcome met its statistical endpoint within the pre-specified equivalence margin at a 95% confidence interval. The results met the 23% equivalence margin authorities required for approval by the Indian

19

regulatory authorities. There was no difference reported in safety or immunogenicity between the treatment groups. There was also no reported difference between the groups on the secondary endpoints.

We measured the patients’ responses on an ACR20 scoring system to BOW015 and Remicade at multiple time points. The data suggest that BOW015 and Remicade patients responded similarly at all time‑points up to the final 16 week efficacy endpoint.

Comparison of BOW015 and Remicade at multiple time points

In September 2014 we announced 58 week data, which demonstrated therapeutic equivalence to Remicade and confirmed the safety of switching from Remicade to BOW015. In the open‑label phase, patients who continued on BOW015 were compared to patients who received four doses of Remicade, followed by a switch to four doses of BOW015. Immune responses as well as overall safety and tolerability for BOW015 were comparable to the arm

20

switched from Remicade to BOW015 and were consistent with the expected profile of Remicade. Further, ACR20 responses were durably maintained to 54 weeks from the week 16 primary endpoint previously reported.

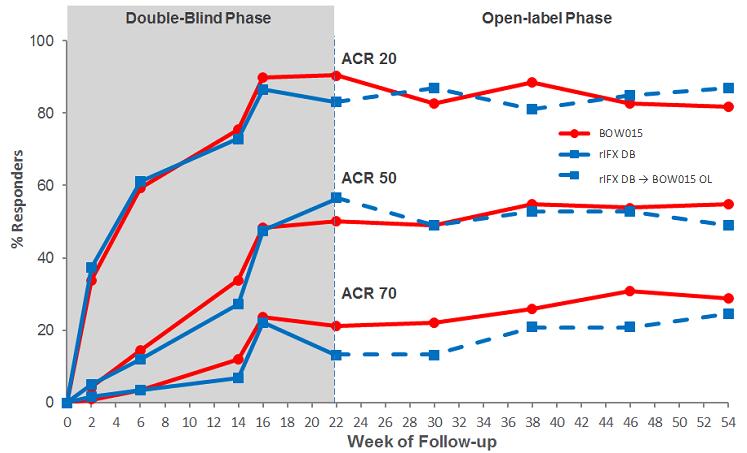

Equivalence in ACR20 Response Rates—Double Blind (DB) and Open Label (OL) Phase

License and Acquisition Agreements

Acquisition of Bioceros

On September 9, 2015, we entered into and closed a definitive Stock Purchase Agreement (the “Stock Purchase Agreement”) with Bioceros Holding B.V., a Netherlands company and our primary vendor for preclinical development work (“Bioceros”), the sellers identified therein (the “Sellers”) and Oscar Schoots and Carine van den Brink as the representatives of the Sellers. Under the Stock Purchase Agreement, we purchased all of the outstanding shares of the share capital of Bioceros (the “Share Transfer”), with the result that Bioceros has become our wholly-owned subsidiary following the Share Transfer. Bioceros is a leading provider of services related to the preclinical development of monoclonal antibodies and generation of good manufacturing practices (GMP)-ready protein producing cell lines. The assets acquired include Bioceros’ proprietary CHOBC® cell line platform, all related intellectual property rights, and a fully equipped laboratory together with Bioceros’ staff of scientists and bioreactor capabilities designed for the development of monoclonal antibodies and protein therapeutics, with a focus on biosimilars, including capabilities for the production of three new biosimilar product candidates to add to our pipeline of biosimilar product candidates, as further described above.

As a result of the Share Transfer, the Sellers will receive a total of $14.1 million in consideration, consisting of: (i) an initial cash payment of $3.4 million, (ii) a second cash payment of $1.7 million, to be paid on the first anniversary of the closing date, (iii) an initial issuance of shares of our common stock, $0.001 par value per share (the “Common Stock”) with a value of $4.0 million, calculated as set forth in the Stock Purchase Agreement and (iv) a second issuance of shares of Common Stock with a value of $5.0 million, calculated as set forth in the Stock Purchase Agreement, to be issued on the date that is six months after the closing date, subject to our setoff rights with regard to the second cash payment and the second installment of shares of Common Stock. In addition, the Sellers will receive, if any such

21

payment is due, a pro rata share of a net cash payout equal to the aggregate amount of Bioceros’ net cash at closing in excess of $1.2 million, calculated as set forth in the Stock Purchase Agreement.

In connection with the Stock Purchase Agreement, Bioceros granted to a newly-formed Netherlands company (“NewCo”), which is owned by the Sellers, a fully paid-up, non-exclusive, transferable (under limited, specified circumstances) license to Bioceros’ CHOBC® platform and future improvements thereto, for NewCo’s use in the development of monoclonal antibodies and proteins other than biosimilar monoclonal antibodies and Ig fusion proteins.

Prior to the Share Transfer, we were party to several license and master services agreements with Bioceros, for non-exclusive licenses under its rights in the cell line and associated intellectual property relating to molecules such as adalimumab and tocilizumab for certain designated territories.

Sun Pharmaceutical Industries Ltd.