Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - Shepherd's Finance, LLC | Financial_Report.xls |

| EX-31.2 - CERTIFICATION - Shepherd's Finance, LLC | shepherds-ex3102.htm |

| EX-32.1 - CERTIFICATION - Shepherd's Finance, LLC | shepherds_ex3201.htm |

| EX-10.16 - SUBORDINATION OF MORTGAGE - Shepherd's Finance, LLC | shepherds_10k-ex1016.htm |

| EX-31.1 - CERTIFICATION - Shepherd's Finance, LLC | shepherds-ex3101.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

x Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the Fiscal Year Ended December 31, 2013

or

o Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the Transition Period From ________ to ________

Commission File Number 333-181360

SHEPHERD’S FINANCE, LLC

(Exact name of registrant as specified on its charter)

| Delaware | 36-4608739 |

| (State or other jurisdiction of | (I.R.S. Employer |

| Incorporation or organization) | Identification No.) |

12627 San Jose Blvd., Suite 203, Jacksonville, FL 32223

(Address of principal executive offices)

302-752-2688

(Registrant’s telephone number including area code)

____________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of the Form 10-K or any amendment of this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, accelerated filer, or non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | o | Accelerated filer | o |

| Non-accelerated filer | o | Smaller reporting company | x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes p No x

DOCUMENTS INCORPORATED BY REFERENCE:

None.

FORM 10-K

SHEPHERD’S FINANCE, LLC

TABLE OF CONTENTS

| Page | |

| Cautionary Note Regarding Forward-Looking Statements | 3 |

| PART I. | |

| Item 1. Business | 4 |

| Item 1A. Risk Factors | 14 |

| Item 1B. Unresolved Staff Comments | 23 |

| Item 2. Properties | 23 |

| Item 3. Legal Proceedings | 23 |

| Item 4. Mine Safety Disclosures | 23 |

| PART II. | |

| Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 23 |

| Item 6. Selected Financial Data | 23 |

| Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations | 24 |

| Item 7A. Quantitative and Qualitative Disclosures About Market Risk | 40 |

| Item 8. Financial Statements and Supplementary Data | 40 |

| Item 9. Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | 40 |

| Item 9A. Controls and Procedures | 40 |

| Item 9B. Other Information | 40 |

| PART III. | |

| Item 10. Directors, Executive Officers and Corporate Governance | 40 |

| Item 11. Executive Compensation | 41 |

| Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 43 |

| Item 13. Certain Relationships and Related Transactions, and Director Independence | 43 |

| Item 14. Principal Accounting Fees and Services | 44 |

| PART IV. | |

| Item 15. Exhibits, Financial Statement Schedules | 45 |

| SIGNATURES | 48 |

| 2 |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements contained in this Form 10-K of Shepherd’s Finance, LLC, other than historical facts, may be considered forward-looking statements within the meaning of the federal securities laws. Words such as “may,” “will,” “expect,” “anticipate,” “believe,” “estimate,” “continue,” “predict,” or other similar words identify forward-looking statements. Forward-looking statements appear in a number of places in this report, including without limitation, “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and include statements regarding our intent, belief or current expectation about, among other things, trends affecting the markets in which we operate, our business, financial condition and growth strategies. Although we believe that the expectations reflected in these forward-looking statements are based on reasonable assumptions, forward-looking statements are not guarantees of future performance and involve risks and uncertainties. Actual results may differ materially from those predicted in the forward-looking statements as a result of various factors, including but not limited to those set forth in “Item 1A. Risk Factors.” If any of the events described in “Risk Factors” occur, they could have an adverse effect on our business, financial condition, and results of operations.

When considering forward-looking statements, our risk factors, as well as the other cautionary statements in this report and in our Form S-1 Registration Statement should be kept in mind. Do not place undue reliance on any forward-looking statement. We are not obligated to update forward-looking statements.

| 3 |

PART I

ITEM 1. BUSINESS

Overview

We were organized in the Commonwealth of Pennsylvania in 2007 under the name 84 RE Partners, LLC and changed our name to Shepherd’s Finance, LLC on December 2, 2011. We converted to a Delaware limited liability company on March 29, 2012. Our business is focused on commercial lending to participants in the residential construction and development industry. We believe this market is underserved because of the lack of traditional lenders currently participating in the market. We are located in Jacksonville, Florida. Our operations are governed pursuant to our operating agreement.

From 2007 through the majority of 2011, we were the lessor in three commercial real estate leases with an affiliate, 84 Lumber Company. Beginning in late 2011, we began commercial lending to residential homebuilders. Our current loan portfolio is described more fully in this section under the sub heading “Our Loan Portfolio Secured by Real Estate.” We have a limited operating history as a finance company. We currently have one paid employee, our Vice President of Operations. Our only executive officer is our Chief Executive Officer, Daniel M. Wallach. Our Board of Managers is comprised of Mr. Wallach and two independent Managers–Bill Myrick and Kenneth R. Summers. Our officers are responsible for our day-to-day operations, while the Board of Managers is responsible for overseeing our business.

The commercial loans we extend are secured by mortgages on the underlying real estate. We extend and service commercial loans to small-to-medium sized homebuilders for the purchase of lots and/or the construction of homes thereon. We also extend and service loans for the purchase of undeveloped land and the development of that land into residential building lots. In addition, we may, depending on our cash position and the opportunities available to us, do none, any or all of the following: purchase defaulted unsecured debt from suppliers to homebuilders at a discount (and then secure that debt with real estate or other collateral), purchase defaulted secured debt from financial institutions at a discount, and purchase real estate in which we will operate our business.

Our Chief Executive Officer, Daniel M. Wallach, has been in the housing industry since 1985. He was the CFO of a multi-billion dollar supplier of building materials to home builders for 11 years. He also was responsible for that company’s lending business for 20 years. During those years, he was responsible for the creation and implementation of many secured lending programs to builders. Some of these were performed fully by that company, and some were performed in partnership with banks. In general, the creation of all loans, and the resolution of defaulted loans, was his responsibility, whether the loans were company loans or loans in partnership with banks. Through these programs, he was responsible for the creation of $2 billion in loans which generated interest spread of $50 million, after deducting for loan losses. Through the years, he managed the development of systems for reducing and managing the risks and losses on defaulted loans. Mr. Wallach also was responsible for that company’s unsecured debt to builders, which reached over $300 million at its peak. He also gained experience in securing defaulted unsecured debt.

To fund our business, we currently have four potential sources of capital: senior secured borrowings; our Notes offering, in which we are offering to the public up to $700 million of Fixed Rate Subordinated Notes pursuant to a Form S-1 Registration Statement (SEC File No. 333-181360); other unsecured borrowings; and equity capital. We began to advertise in March 2013 and have received $1,739,000 in Notes proceeds as of December 31, 2013. We anticipate continuing our sales efforts in 2014, focusing on the efforts that have proven fruitful.

Investment Objectives and Opportunity

Background and Strategy

Finance markets are highly fragmented, with numerous large, mid-size and small lenders and investment companies, such as banks, savings and loan associations, credit unions, insurance companies and institutional lenders, all competing for investment opportunities. Many of these market participants have experienced losses, as a result of the current credit environment, over the last seven years from this type of lending, and, as a result of credit losses and restrictive government oversight, are not participating in this market to the extent they had before the credit crisis (as evidenced by the general lack of availability of construction financing and the higher cost of financing for the few deals actually done). We believe that these lenders will be unable to satisfy the current demand for residential construction financing, creating attractive opportunities for niche lenders such as us for many years to come. Additionally, while we believe the current credit environment will be temporary, we believe the many participants in the finance markets will significantly alter their lending standards (including percentages loaned on collateral value, cash required up front from the builder, and the number of speculatively built homes allowed at any given time), which will also create attractive, long-term opportunities for us. Our goal is not to be a customer’s only source of commercial lending, but an extra, more user-friendly piece of their financing.

| 4 |

We create and service construction loans differently than most lenders have done in the past, in that we:

| · | Focus on long term lending relationships with customers, and only on this type of lending; |

| · | Are a specialist in this type of lending; |

| · | Intend to have a national footprint for lending without having the overhead of a national footprint of branches; |

| · | Generally use appraisers who are experts in the specific market (rather than simply using the cheapest or most readily available); |

| · | Will work out defaulted loans with the same person that created that loan, which will help both control the creation of bad loans, and the losses on bad loans; |

| · | Will pursue customers with defaulted loans faster and more aggressively than typical lenders; and |

| · | While pursuing those customers, will offer creative solutions to help them sell their home while in default (such as offering cash allowances for the purchase of furniture or appliances or paying extra up-front costs on behalf of the buyers in order to lower their mortgage interest rates and monthly payments). |

We believe that while creating speculative construction loans is a high risk venture, the reduction in competition, the differences in our lending versus typical bank lending (listed above); and our loss mitigation techniques (covered below) will all help this to continue to be a profitable business.

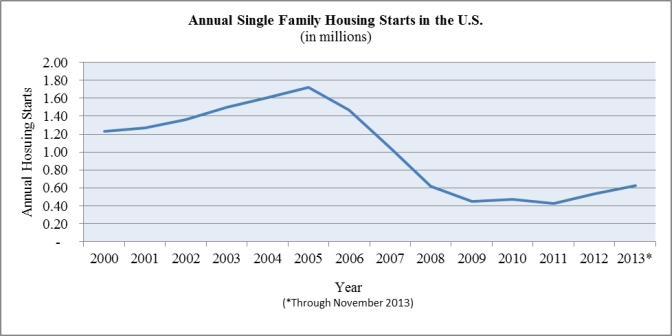

Over the past seven years, the housing market has been plagued by declining values and a lack of housing starts. More recently, values and starts have been rising. We believe that, despite the issues in the speculative construction industry that were a result of the declining values and a lack of housing starts, it is a good time for this type of lending because:

| · | Many traditional lenders to this market have exited or cut back, reducing competition and allowing large spreads (the difference between cost of funds and the rate we charge our borrowers). Better builders can be obtained as customers, with higher spreads; |

| · | The number of housing starts and the value of homes built are both low but improving. We believe that we were recently at the bottom of the housing cycle, and it is likely that housing starts and values will both increase over time. Increases in both of these items should have a positive effect on our performance; |

| · | There are fixed costs involved in running this kind of operation, such as payroll and the costs of being subject to public company reporting requirements. These require a fixed interest rate spread in dollars to cover these costs. Interest spread in 2013 of $439,000 was enough to cover these costs; and |

| · | We do various things to try to mitigate the risks inherent in this type of lending by: |

| · | Keeping the loan-to-value ratio, or LTV, between 60% and 75% on a portfolio basis, however, individual loans may, from time to time, have a greater LTV; |

| · | Generally using deposits from the builder on home construction loans to ensure the completion of the home. Lending losses on defaulted loans are usually a higher percentage when the home is not built, or is only partially built; |

| · | Having a higher yield than other forms of secured real estate lending; |

| · | Paying major subcontractors and suppliers directly, which reduces the frequency of liens on the property (liens generally hurt the net realized value of loss mitigation techniques); |

| · | Aggressively working with builders who are in default on their loan before and during foreclosure. This technique generally yields a reduced realized loss; and |

| · | Market grading. We review all lending markets, analyzing their historic housing start cycles. Then, the current position of housing starts is examined in each market. Markets are classified into volatile, average, or stable, and then graded based on that classification and our opinion of where the market is in its housing cycle. This grading is then used to determine the builder deposit amount, the LTV, and the yield. |

| 5 |

Additionally, most financial institutions are highly regulated. In exchange for that regulation, they offer FDIC insurance to their investors. We are not highly regulated, nor do we offer FDIC insurance to our investors. While we are subject to some regulation, such as anti-terrorism and commercial lending laws, currently, we are not subject to consumer lending rules or federal banking regulations. We believe this provides us with the opportunity to learn from the positive aspects of banking regulations while avoiding costly regulatory compliance.

Since we are not a tightly regulated company, we feel that we have a competitive edge that allows us to make prudent, business-minded decisions. While regulators are restricting investments by regulated financial institutions in commercial construction loans, our business plan emphasizes commercial construction lending as our main line of business. We believe this to be an opportunity as the regulatory environment and resulting contraction in commercial lending has resulted in this segment of the market having fewer lenders. We also believe the real estate market recently reached historically low levels, and feel, based on recent data relating to housing starts and home values, that the market has stabilized and is beginning to recover. Finally, while we have instituted many of the underwriting requirements and activities used by regulated financial institutions, we believe being unregulated provides us with more flexibility in our underwriting process and procedures.

Outside of differences in our lending policies, we believe the benefits to not being regulated include:

| · | our ability to better manage our outflow of funds because our Notes have a stated term. Banks must offer demand deposit accounts (checking accounts) and other accounts, which provide that funds can be withdrawn at any time; |

| · | avoiding FDIC insurance and other regulatory fees; |

| · | not being subject to the Community Reinvestment Act; and |

| · | eventually having less leverage than a bank. |

| Conversely, our lack of regulation introduces us to other risks which may harm us. For example: |

| · | we are not well diversified in our product risk; |

| · | we cannot benefit from government programs designed to protect regulated financial institutions; |

| · | we are not subject to periodic examinations by federal or state banking regulators; and |

| · | our cost of funds is higher. |

In addition, our Note holders will have greater risks than depositors in a regulated financial institution, since their investments will not be insured.

To help mitigate the risks associated with not being regulated, we:

| · | follow many of the same underwriting principals historically used by banks, including: |

| · | Collateralizing loans; |

| · | Using LTV’s to control risk; |

| · | Controlling the number of loans in one subdivision; |

| · | Underwriting appraisals; and |

| · | Conducting property inspections; |

| · | maintain loan files which will, generally, contain similar information as a bank loan file; |

| · | secure our loans with mortgages and other documents like banks do; and |

| · | monitor many of the same ratios bank regulators monitor. |

| 6 |

So, while we, in our opinion, improve on some policies and procedures historically used by banks, which we would not be able to do if we were regulated, we follow many of the policies and procedures set up by the various bank regulators. We believe this balanced approach helps us mitigate risk while providing us the opportunity to enter into what we believe to be an underserved market. One example of an improvement on a policy historically used by banks is appraiser selection. Many times banks use a random process to select an appraiser, or a process which uses a middle man. We generally select one of the most qualified appraisers in the specific portion of the market in which we are having the appraisal prepared. We believe this provides for a more consistent result. Another example is geographic diversity. Banks generally do not lend outside of their branch footprint. This does not give regional or local banks enough exposure to most of the United States, but gives them too much exposure in a smaller area. While we are currently heavily concentrated in one market, we are not constrained by policies that prevent better geographic diversity.

Our future loans will likely be marketed by lending representatives who work for us and are driven to maintain long-term customer relationships. As of December 31, 2013, we have retained only one employee in addition to our Chief Executive Officer. Hiring and retaining high quality lending representatives should not be difficult in the short-term banking environment, where construction loan officers will have a hard time finding and keeping employment with traditional lenders. In his previous experience, our Chief Executive Officer had a nationwide staff of 20 lenders working in the field. Compensation will be focused on the profitability of loans originated, not simply the volume of loans originated.

While our business has initially been focused on transactions originating in the Pittsburgh area, we expect to expand into other geographic regions over time as we build or acquire market expertise that will allow us to successfully finance transactions in those areas. Our goal is to market our loans on a nationwide basis. We believe that this goal can only be achieved with sufficient funds from our Notes offering. Currently, our loan portfolio consists of loans made to a low number of customers, but, as we grow our loan assets, we intend to diversify our customer base.

Lines of Business

We seek to create a portfolio that includes some or all of the following investment characteristics: (i) provides current income; (ii) is well-secured by residential real estate; (iii) is short term in nature; and (iv) provides high interest spreads. While we primarily intend to provide commercial construction loans to homebuilders (for residential real estate), we may also purchase defaulted unsecured debt from suppliers to homebuilders at a discount (and then secure that debt with real estate or other collateral), purchase defaulted secured debt from financial institutions at a discount, and purchase real estate in which we will operate our business. Our investment policies may be amended or changed at any time by our Board of Managers.

Commercial Construction Loans to Homebuilders

We extend and service commercial loans to small-to-medium sized homebuilders for the purchase of lots and/or the construction of homes thereon. We also extend and service loans for the purchase of undeveloped land and the development of that land into residential building lots. Most of the loans will be for “spec homes” or “spec lots,” meaning they are built or developed speculatively (with no specific end-user home owner in mind). The loans are secured, and the collateral is the land, lots, and constructed items thereon, as well as additional collateral, as we deem appropriate. Generally, our loans are secured by a first priority mortgage lien; however, we may make loans secured by a second or other lower priority mortgage lien. The loans are demand loans, but the typical length of a home construction loan will range between six months and two years and is expected to average 10 months; the typical length of a development project ranges between three and six years. Larger developments are usually developed in phases.

In a typical home construction transaction, a homebuilder obtains a loan to purchase a lot and build a home on that lot. In some cases the builder has a contract with a customer to purchase the home upon its completion. In other cases, the home is built as a spec home, meaning there is no specific customer it is being built for, but the homebuilder believes it will sell before or shortly after completion, and that therefore building the home before it is under contract will increase the homebuilder’s sales and profitability. The builder may also believe that the construction of a spec home will increase the number of contract sales he will have in a given year, as it may be easier to sell contract homes when the customer can see the builder’s work in the spec home. In some cases, these speculatively built homes are constructed with the intention to keep them as a model for a period of time, to increase contract sales, and then be sold. These are called model homes. While we may lend to a homebuilder for any of these types of new construction homes, we believe that in the future we will generally be lending on spec homes.

In a typical development transaction, a homebuilder/developer purchases a specific parcel or parcels of land. Developers must secure financing in order to pay the purchase price for the land as well as to pay expenses incurred while developing the lots. This is the financing we provide. Once financing has been secured, the lot developers create individual lots. Developers secure permits allowing the property to be developed and then design and build roads and utility systems for water, sewer, gas and electricity to service the property. The individual lots are then sold before a home is built on them; paid off, built on and then sold; or built on, then sold and paid off (in these cases, we may subordinate our loan to the home construction loan). A portion of our current loan portfolio is made up of development loans and is more fully described in “Our Loan Portfolio Secured By Real Estate” in this section.

We fund the loans we originate using available cash resources that are generated primarily from borrowings, net operating cash flow and proceeds of the Notes.

There is a seasonal aspect to home construction, and this affects monthly cash flow. In general, since the home construction loans we create will last 10 months on average, and since we intend to be geographically diverse, we expect the seasonality impact to be somewhat mitigated.

| 7 |

Our real estate loans are or will be secured by one or more of the following:

| · | the parcels of land to be developed; |

| · | finished lots; |

| · | model homes and new single-family homes; |

| · | a pledge of some or all of the equity interests in the borrower entity or other parent entity that owns the borrower entity; |

| · | additional assets of the borrower, including parcels of undeveloped and developed real property; and |

| · | in certain cases, personal guarantees of the principals of the borrower entity. |

Our Chief Executive Officer is responsible for the oversight of all aspects of our commercial construction loan business, including:

| · | closing and recording of mortgage documents; |

| · | collecting principal and interest payments; |

| · | enforcing loan terms and other borrower’s requirements; |

| · | periodic review of each loan file; and |

| · | exercising our remedies in connection with defaulted or non-performing loans. |

Our customers are typically small-to-medium sized homebuilders that are currently building in the markets in which we lend to them. Generally, they benefit from doing business with us not just because they are able to sell additional homes (which we finance), but because, as they build additional homes, they are able to increase sales of homes that are built as contracted homes, where the eventual home owner supplies the loan. Builders generally have more success selling homes when a model or spec home is available for customers to see. We anticipate that most of our lending will be based on the following general policies:

| Customer Type | Small-to-Medium Size Homebuilders |

| Loan Type | Commercial |

| Loan Purpose | Construction of Homes or Development of Lots |

| Security | Homes, Lots, and/or Land |

| Priority | Generally, our loans will be secured by a first priority mortgage lien; however, we may make loans secured by a second or other lower priority mortgage lien. |

| Loan-to-Value Averages | 60-75% |

| Loan Amounts | Average home construction loan $200,000, development loans vary greatly |

| Term | Demand |

| Rate | Cost of Funds plus 2%, minimum rate of 7% |

| Origination Fee | 5% for home construction loans, development loans on a case by case basis |

| Title Insurance | Only on high risk loans |

| Hazard Insurance | Only on high risk loans |

| General Liability Insurance | Always |

| Credit | Builder should have significant building experience in the market, be building in the market currently, be able to make payments of interest, be able to make the required deposit, have acceptable personal credit, and have open lines of credit (unsecured) with suppliers reasonably within terms. We will generally not advertise to find customers, but will use our loan representatives. We believe this approach will allow us to focus our efforts on builders that meet our acceptable risk profile. |

| Third Party Guarantor | None |

| 8 |

We may change these policies at any time based on then-existing market conditions or otherwise, at the discretion of our Chief Executive Officer and Board of Managers.

Purchases and Securitization of Unsecured Debt from Suppliers to Homebuilders

Homebuilders generally buy their construction materials from building supply companies, which offer unsecured credit lines for these purchases. Sometimes the builder is unable to pay the principal on their line of credit when due, and in a small percentage of these cases, the builder owns unencumbered real estate. When this is the case, the building supply company may convert the unsecured line of credit to secured, using this real estate as security. In some of these situations, the building supply company is unwilling to complete this type of transaction, and is willing to take a payment of a percentage of the balance of the unsecured line as full payment. If we pay the building supply company a percentage of this debt, and then take the real estate as collateral for the whole amount of the original debt, management’s experience indicates we will be able to eventually collect from the builder, or from the sale of the property through foreclosure or otherwise, creating a profit for ourselves. We have not completed any of these transactions, but may choose to do so if the opportunity presents itself.

Purchases of Defaulted Secured Debt from Financial Institutions

Many financial institutions made loans to homebuilders when lot and home values were higher than they are today. In many cases, these loans defaulted, and eventually these loans result in collateral foreclosure. After the foreclosure proceeding, the properties usually become the property of the financial institution, which then sells the property, generally at a loss. While the loan is in the foreclosure process, and after the process while the real estate is owned and for sale, the bank holds a nonperforming asset. Sometimes these nonperforming assets negatively impact the banks’ profitability and regulatory ratios. Some banks choose to cleanse their books of these items at a severe loss, allowing them to, while taking a loss, get back to their commercial lending business. There are opportunities to purchase some portfolios of defaulted loans, and/or real estate owned through foreclosure, at deep discounts compared to the actual value of the property. We have not completed any of these transactions, but may choose to do so if the opportunity presents itself.

Purchases of Real Estate

In limited circumstances, the commercial construction loans described above may result in us owning commercial real property as a result of a loan workout, foreclosure or similar circumstances. In addition, although making direct investments in commercial real property at this time will not be a significant focus of our investment strategy, we may make investments in commercial real property in which we operate. We intend to manage and dispose of any real property assets we acquire in the manner that our management determines is most advantageous to us. We have not completed any of these transactions, but may choose to do so if the opportunity presents itself.

Our Loan Portfolio Secured by Real Estate

Pennsylvania Loans

On December 30, 2011, pursuant to a credit agreement by and between us, Benjamin Marcus Homes, LLC (“BMH”), Investor’s Mark Acquisitions, LLC (“IMA”) and Mark L. Hoskins (“Hoskins”) (collectively, the “Hoskins Group”) (as amended, the “Credit Agreement”), we originated two new loan assets, one to BMH as borrower (the “BMH Loan”) and one to IMA as borrower (the “New IMA Loan”). Pursuant to the Credit Agreement and simultaneously with the origination of the BMH Loan and the New IMA Loan, we also assumed the position of lender on an existing loan to IMA (the “Existing IMA Loan”) and assumed the position of borrower on another existing loan in which IMA serves as the lender (the “SF Loan”). Throughout this report, we refer to the BMH Loan, the New IMA Loan, and the Existing IMA Loan collectively as the “Pennsylvania loans.” When we assumed the position of the lender on the Existing IMA Loan, we purchased a loan which was originated by the borrower’s former lender, and assumed that lender’s position in the loan and maintained the recorded collateral position in the loan. The borrower’s former lender and the seller of the BMH property are the same party, 84 FINANCIAL, L.P., an affiliate of 84 Lumber Company. The BMH Loan, the New IMA Loan and the Existing IMA Loan are all cross-defaulted and cross-collateralized with each other. Further, IMA and Hoskins serve as guarantors of the BMH Loan, and BMH and Hoskins serve as guarantors of the New IMA Loan and the Existing IMA Loan. As such, we are currently primarily reliant on a single developer and homebuilder for our revenues.

| 9 |

In April, July, September and December 2013, we entered into amendments to the BMH Loan. As a result of these amendments, BMH was allowed to borrow for the construction of homes on lots 204, 205, and 206 of the Hamlets subdivision and lot 5 in the Tuscany subdivision, both located in a suburb of Pittsburgh, Pennsylvania, and to borrow for the purchase of lot 5 of the Hamlets subdivision. We issued a letter of credit for $155,000 to a sewer authority relating to BMH Loan (the “Letter of Credit”), and we allowed a fully funded mortgage in the amount of $1,146,000 to be placed in superior position to our mortgage, with the $1,146,000 proceeds being used to reduce the balance of BMH’s outstanding loan with us. We chose to allow the $1,146,000 pay down of our loan with a superior mortgage because: (1) it should allow for the faster development of both the Hamlets and Tuscany subdivisions, decreasing the amount of risk time we will have; (2) it did not substantially alter the dollars we have at risk; and (3) it increased our return as a percentage of loan assets, as the Pennsylvania loans should be paid down quicker. The amount of the Letter of Credit is not included in our commitments to lend throughout the financial statements contained in this report, as any amount drawn would be included in the credit limit of BMH, and, as of December 31, 2013, BMH is under the credit limit by more than the amount of the Letter of Credit. The terms and conditions of the Pennsylvania loans are set forth in further detail below.

BMH Loan

The BMH Loan is a revolving demand loan in the original principal amount of up to $4,164,000, of which $3,568,000 was funded at closing. We collected a fee of $750,000 upon closing of the BMH Loan, which was funded from proceeds of the loan. Additionally, $450,000 of the loan proceeds was allocated to an interest escrow account (the “Interest Escrow”). Interest on the BMH Loan accrues annually at 2% plus the greater of (i) 5.0% or (ii) the weighted average price paid by us on or in connection with all of our borrowed funds (such weighted average price includes interest rates, loan fees, legal fees and any and all other costs paid by us on our borrowed funds, and, in the case of funds borrowed by us from our affiliates, the weighted average price paid by such affiliate on or in connection with such borrowed funds) (“COF”). Pursuant to the Credit Agreement, interest payments on the BMH Loan are funded from the Interest Escrow, with any shortfall funded by BMH. Payments of principal on the BMH Loan are due upon our demand and in accordance with the payment schedule and other terms and conditions set forth in the Credit Agreement. The Credit Agreement obligates BMH to make payoffs to us in varying amounts upon the sale or transfer of, or obtaining construction financing for, all or a portion of the property securing the BMH Loan. The BMH Loan may be prepaid in whole or in part at any time without penalty; provided, however, that prepayments will not relieve BMH of its obligation to continue to make payments on the BMH Loan as set forth in the Credit Agreement.

The BMH Loan is secured by a second priority mortgage in residential property consisting of one building lot and a parcel of land of approximately 34 acres which is currently partially under development, all located in the subdivision commonly known as the Hamlets of Springdale in Peters Township, Pennsylvania, a suburb of Pittsburgh, as well as the Interest Escrow. The seller of the property securing the BMH Loan retained a third mortgage in the amount of $400,000, with a balance of approximately $323,000 and $351,000 as of December 31, 2013 and 2012, respectively. The property securing the BMH Loan is subject to a mortgage in the amount of $1,146,000 which is held by United Bank and guaranteed by 84 FINANCIAL, L.P. The superior mortgage balance is subtracted from the appraised value of the land in the land valuation detail of the Pennsylvania loan financing receivables at December 31, 2013 in the table detailing the Pennsylvania loans below.

New IMA Loan

The New IMA Loan is a demand loan in the original principal amount of up to $2,225,000, of which $250,000 was funded at closing. We collected a fee of $250,000 upon closing of the New IMA Loan, which was funded from proceeds of the loan. Interest on the New IMA Loan accrues annually at 2.0% plus the greater of (i) 5.0% or (ii) the weighted average price paid by us on or in connection with all of our borrowed funds (such weighted average price includes interest rates, loan fees, legal fees and any and all other costs paid by us on our borrowed funds, and, in the case of funds borrowed by us from our affiliates, the weighted average price paid by such affiliate on or in connection with such borrowed funds). Pursuant to the Credit Agreement, interest payments on the New IMA Loan are funded from the Interest Escrow, with any shortfall funded by IMA. Payments of principal on the New IMA Loan are due upon our demand and in accordance with the payment schedule and other terms and conditions set forth in the Credit Agreement. The Credit Agreement obligates IMA to make payoffs to us in varying amounts upon the sale or transfer of, or obtaining construction financing for, all or a portion of the property securing the New IMA Loan. The New IMA Loan may be prepaid in whole or in part at any time without penalty; provided, however, that prepayments will not relieve IMA of its obligation to continue to make payments on the New IMA Loan as set forth in the Credit Agreement.

The New IMA Loan is secured by a mortgage in residential property consisting of 18 lots located in the subdivision commonly known as the Tuscany Subdivision in Peters Township, Pennsylvania, a suburb of Pittsburgh. Construction of the improvements for the Tuscany Subdivision began in December 2012, with $561,000 remaining to be completed as of December 31, 2013. The property securing the New IMA Loan and the Existing IMA Loan is subject to a mortgage in the amount of $1,290,000, which is held by an unrelated third party. In connection with the closing of the New IMA Loan and the Existing IMA Loan, the holder of this mortgage entered into an agreement to amend, restate and further subordinate such mortgage. This subordination agreement also provides that, in the event of a foreclosure on and liquidation of the property securing the New IMA Loan and the Existing IMA Loan, we are entitled to receive liquidation proceeds up to $2,225,000 which excludes the collateral securing the BMH Loan, at which point the holder of this mortgage is entitled to receive liquidation proceeds up to the amount necessary to satisfy its outstanding mortgage, and we are then entitled to any remainder of the liquidation proceeds. The subordinated mortgage balance is subtracted from the appraised value of the finished lots in the lot valuation in the table detailing the Pennsylvania loans below.

| 10 |

Existing IMA Loan

The Existing IMA Loan is a demand loan in the original principal amount of $1,687,000, of which $1,687,000 was outstanding as of both December 31, 2013 and 2012. Interest on the Existing IMA Loan accrues annually at a rate of 7.0%. Pursuant to the Credit Agreement, interest payments on the Existing IMA Loan are funded from the Interest Escrow, with any shortfall funded by IMA. Payments of principal on the Existing IMA Loan are due upon the earlier of our demand or the satisfaction in full of the indebtedness related to the BMH Loan and the New IMA Loan. The Credit Agreement obligates IMA to make payoffs to us in varying amounts upon the sale or transfer of, or obtaining construction financing for, all or a portion of the property securing the Existing IMA Loan. The Existing IMA Loan may be prepaid in whole or in part at any time without penalty; provided, however, that prepayments will not relieve IMA of its obligation to continue to make payments on the Existing IMA Loan as set forth in the Credit Agreement.

The Existing IMA Loan is secured by a mortgage in the residential property that also secures the New IMA Loan.

SF Loan

The SF Loan, under which we are the borrower, is an unsecured loan in the original principal amount of $1,500,000, of which $1,500,000 was outstanding on both December 31, 2013 and 2012. Interest on the SF Loan accrues annually at a rate of 5.0%. Payments of interest only are due on a monthly basis, with the principal amount due on the date that the BMH Loan and the New IMA Loan are paid in full. We may prepay the SF Loan in part or in full at any time without penalty, subject to the terms and conditions set forth in the underlying promissory note. Pursuant to the Credit Agreement, payments on the SF Loan are used to fund the Interest Escrow. Further, pursuant to that certain Amended and Restated Commercial Pledge Agreement by and between us, IMA and BMH, IMA has pledged its interest in the SF Loan as collateral for IMA’s obligations under the New IMA Loan and the Existing IMA Loan. The SF Loan was created to both increase our net interest income, and to better secure the BMH Loan.

Interest Escrow

The Pennsylvania loans called for a funded Interest Escrow account which was funded with proceeds from the Pennsylvania loan. The initial funding on that Interest Escrow was $450,000. The balance as of December 31, 2013 and 2012 was $255,000 and $329,000, respectively. To the extent the balance is available in the Interest Escrow, interest due on certain loans is deducted from the Interest Escrow on the date due. The Interest Escrow is increased by 10% of lot payoffs on the same loans, and by interest on the SF Loan. All of these transactions are noncash to the extent that the total escrow amount does not need additional funding. The Interest Escrow is also used to contribute to the reduction of the $400,000 subordinated mortgage upon certain lot sales of the collateral of that loan.

Roll forward of interest escrow for the years ended December 31, 2013 and 2012:

| 2013 | 2012 | |||||||

| Beginning balance | $ | 329,000 | $ | 450,000 | ||||

| + SF Loan interest | 75,000 | 69,000 | ||||||

| + Additions from lot payoffs | 188,000 | 169,000 | ||||||

| - Interest and fees | (325,000 | ) | (341,000 | ) | ||||

| - Amount used to reduce $400,000 loan balance | (12,000 | ) | (18,000 | ) | ||||

| Ending balance | $ | 255,000 | $ | 329,000 | ||||

| 11 |

Initial Funding

On December 30, 2011 we purchased the Existing IMA Loan from the original lender with a cash payment of $186,000 and the assumption of that lender’s obligations under the SF Loan. We also loaned our borrower $2,368,000 in funded cash for its purchase of the land and lots securing the BMH Loan. Our borrower’s loan balances were increased by the $750,000 loan fee on the BMH Loan, the $250,000 loan fee on the New IMA Loan, and the $450,000 Interest Escrow, all of which were not funded with cash.

Whispering Pines Loan

Also in our loans receivable balance is another loan to the same customer in a different subdivision (Whispering Pines) with a balance net of loan fee and builder deposit of $116,000 and $0 as of December 31, 2013 and 2012, respectively. This loan has a builder deposit of 6% of the loan amount, a loan fee of 5% of the loan amount, and has an interest rate of our COF plus 2%. The collateral for the Whispering Pines Loan is a lot with a home under construction.

A detail of the financing receivables for the Pennsylvania loans at December 31, 2013 is as follows:

(All dollar [$] amounts shown in table and footnotes in thousands.)

| Item | Term | Interest Rate | Funded to borrower | Estimated collateral values | ||||||||

| BMH Loan | Demand(1) | COF +2% (7% Floor) | ||||||||||

| Land for phases 3, 4, and 5 | $ | – | $ | 1,041 | (4) | |||||||

| Lot 5 Hamlets | 142 | 180 | ||||||||||

| Interest Escrow | 450 | 255 | ||||||||||

| Loan Fee | 750 | – | ||||||||||

| Excess Paydown | (394 | ) | (5) | |||||||||

| Construction loan lot 118 Whispering Pines | 138 | 120 | ||||||||||

| Construction loan lot 5 Tuscany | 37 | – | ||||||||||

| Total BMH Loan | 1,123 | 1,596 | ||||||||||

| IMA Loans | ||||||||||||

| New IMA Loan (loan fee) | Demand(1) | COF +2% (7% Floor) | 250 | – | ||||||||

| New IMA Loan (advances) | Demand(1) | COF +2% (7% Floor) | 1,479 | – | ||||||||

| Existing IMA Loan | Demand(2) | 7% | 1,687 | 2,299 | (3) | |||||||

| Total IMA Loans | 3,416 | 2,299 | ||||||||||

| Unearned Loan Fee | (567 | ) | – | |||||||||

| SF Loan Payable | – | 1,500 | ||||||||||

| Total | $ | 3,972 | $ | 5,395 | ||||||||

_______________

(1) These are the stated terms; however, in practice, principal will be repaid upon the sale of each developed lot.

(2) These are the stated terms; however, in practice, principal will be repaid upon the sale of each developed lot after the BMH Loan and the New IMA Loan are satisfied.

(3) Estimated collateral value is equal to the appraised value of $4,140, net of estimated costs to finish the development of $561 and the second mortgage amount of $1,280.

(4) Estimated collateral value is equal to the raw ground appraised value of $1,910 plus improvements of $277, net of the outstanding first mortgage of $1,146.

(5) Excess Paydown is the amount of initial funding of the Interest Escrow and/or Loan Fee that have been repaid to date. These amounts are available to be reborrowed in the future.

| 12 |

New Jersey Loan

In August 2013, we entered into a line of credit agreement with a borrower for the construction of homes in New Jersey. The maximum credit line for this loan is $150,000, with $72,000 outstanding at December 31, 2013, net of the builder deposit and unearned loan fee. Each home built pursuant to this credit agreement will have a builder deposit of 6% of the available loan amount for that home and a loan fee of 5% of that available loan amount, with an interest rate of our cost of funds plus 2%.

2014 Outlook

In 2014, we anticipate using proceeds from the Notes and other sources to generate additional loans, mostly spec home construction loans, and increasing our customer and geographic diversity.

Competition

Historically, our industry has been highly competitive. We compete for opportunities with numerous public and private investment vehicles, including financial institutions, specialty finance companies, mortgage banks, pension funds, opportunity funds, hedge funds, REITs and other institutional investors, as well as individuals. Many competitors are significantly larger than us, have well established operating histories and may have greater access to capital, resources and other advantages over us. These competitors may be willing to accept lower returns on their investments or to modify underwriting standards and, as a result, our origination volume and profit margins could be adversely affected.

We believe that this is a good time to extend commercial loans to builders in the residential real estate market because, currently, this market appears underserved, home values are low, and many of our competitors have sustained losses due to declines in home values and, therefore, are reluctant to lend in this space at this time. We expect our loans to be different than other lenders in the markets in which we are active. Typically the differences are:

| · | our loans may have a higher fee; |

| · | our loans may include an interest free period (whereas other lenders typically charge interest); and |

| · | some of our loans may have lower costs as a result of not requiring title or hazard insurance. |

Regulatory Matters

Financial Regulation

Our operations are not subject to the stringent regulatory requirements imposed upon the operations of commercial banks, savings banks, and thrift institutions, and are not subject to periodic compliance examinations by federal or state banking regulators.

Further, our Notes are not certificates of deposit or similar obligations or guaranteed by any depository institution and are not insured by the FDIC or any governmental or private insurance fund, or any other entity.

The Investment Company Act of 1940

An investment company is defined under the Investment Company Act of 1940, as amended (the “Investment Company Act”), to include any issuer engaged primarily in the business of investing, reinvesting, or trading in securities. Absent an exemption, investment companies are required to register as such with the SEC and to comply with various governance and operational requirements. If we were considered an “investment company” within the meaning of the Investment Company Act, we would be subject to numerous requirements and restrictions relating to our structure and operation. If we were required to register as an investment company under the Investment Company Act and to comply with these requirements and restrictions, we may have to make significant changes in our proposed structure and operations to comply with exemption from registration, which could adversely affect our business. Such changes may include, for example, limiting the range of assets in which we may invest. We intend to conduct our operations so as to fit within an exemption from registration under the Investment Company Act for purchasing or otherwise acquiring mortgages and other liens on and interest in real estate. In order to satisfy the requirements of such exemption, we may need to restrict the scope of our operations.

| 13 |

Environmental Compliance

We do not believe that compliance with federal, state, or local laws relating to the protection of the environment will have a material effect on our business in the foreseeable future. However, loans we extend or purchase are secured by real property. In the course of our business, we may own or foreclose and take title to real estate that could be subject to environmental liabilities with respect to these properties. We (or our loan customers) may be held liable to a governmental entity or to third parties for property damage, personal injury, investigation and clean-up costs incurred by these parties in connection with environmental contamination or may be required to investigate or clean up hazardous or toxic substances or chemical release at a property. The costs associated with the investigation or remediation activities could be substantial. In addition, if we become the owner of or discover that we were formerly the owner of a contaminated site, we may be subject to common law claims by third parties based on damages and costs resulting from environmental contamination emanating from the property. To date, we have not incurred any significant costs related to environmental compliance and we do not anticipate incurring any significant costs for environmental compliance in the future. Generally, when we are lending on property which is being developed into single family building lots, an environmental assessment is done by the builder for the various governmental agencies. When we lend for new construction on newly developed lots, the lots have generally been reviewed while they were being developed. We also perform our own physical inspection of the lot, which includes assessing potential environmental issues. Before we take possession of a property through foreclosure, we again assess the property for possible environmental concerns, which, if deemed to be a significant risk compared to the value of the property, could cause us to forego foreclosure on the property and to seek other avenues for collection.

ITEM 1A. RISK FACTORS

Below are risks and uncertainties that could adversely affect our operations that we believe are material to investors. Other risks and uncertainties may exist that we do not consider material based on the information currently available to us at this time.

Risks Related to Our Structure

Payment on the Notes is subordinate to the payment of our outstanding present and future senior debt, if any. Since there is no limit on the amount of senior debt we may incur, our present and future senior debt may make it difficult to repay the Notes.

As of December 31, 2013, we had $0 of senior debt outstanding, with availability on our senior debt lines of credit of $1,500,000. The Notes are subordinate and junior in priority to any and all of our senior debt and equal to any and all non-senior debt, including other Notes. There are no restrictions in the indenture regarding the amount of senior debt or other indebtedness that we may incur. Upon the maturity of our senior debt, by lapse of time, acceleration or otherwise, the holders of our senior debt have first right to receive payment, in full, prior to any payments being made to our Note holders or to other non-senior debt. Therefore, upon such maturity of our senior debt our Note holders would only be repaid in full if the senior debt is satisfied first and, following satisfaction of the senior debt, if there is an amount sufficient to fully satisfy all amounts owed under the Notes and any other non-senior debt.

If we are unable to raise substantial funds, we will be limited in our ability to diversify the loans we make, and our ability to repay the Notes that have been sold will be dependent on the performance of the specific loans we make.

We are conducting this offering of Notes ourselves without any underwriter or placement agent. We have no experience in conducting a notes offering or any other securities offering. Although we intend to sell up to the maximum offering amount of the Notes, there is no minimum amount of proceeds that must be received from the sale of the Notes in order to accept proceeds from Notes actually sold. As a result, the amount of proceeds we raise in this offering may be substantially less than the amount we would need to achieve a broadly diversified portfolio of loans. If we are unable to raise a substantial amount of funds, we will make fewer loans, resulting in less diversification in terms of the number of loans we make, the borrowers on such loans, and the geographic regions in which our collateral is located. In such event, the likelihood of our profitability being affected by the performance of any one of our loans will increase. Our ability to repay the Notes will be subject to greater risk to the extent that we lack a diversified portfolio of loans.

If we are unable to meet our Note maturity and redemption obligations, and we are unable to obtain additional financing or other sources of capital, we may be forced to sell off our operating assets or we might be forced to cease our operations, and our Note holders could lose some or all of their investments.

Our Notes have maturities ranging from one year to four years. In addition, holders of our Notes may request redemption upon death. We intend to pay our Note maturity and redemption obligations using our normal cash sources, such as collections on our loans to customers, as well as proceeds from the sale of the Notes. We may experience periods in which our Note maturity and redemption obligations are high. Since our loans are generally repaid when our borrower sells a real estate asset, our operations and other sources of funds may not provide sufficient available cash flow to meet our continued Note maturity and redemption obligations. Therefore, we will be substantially reliant upon the net offering proceeds we receive from the sale of the Notes to pay these obligations. If we are unable to repay or redeem the principal amount of the Notes when due, and we are unable to obtain additional financing or other sources of capital, we may be forced to sell off our operating assets or we might be forced to cease our operations, and our Note holders could lose some or all of their investments.

| 14 |

Management has broad discretion over the use of proceeds from this offering, and it is possible that the funds will not be used effectively to generate enough cash for payment of principal and interest on the Notes.

We expect to use the proceeds from this offering for purposes detailed in our prospectus under the “Questions and Answers” and “Use of Proceeds” sections. Because no specific allocation of the proceeds is required in the indenture, our management will have broad discretion in determining how the proceeds of the offering will be used.

We are controlled by Daniel M. Wallach, as, currently, he is our only executive officer and beneficially owns all of our outstanding membership interests.

Daniel M. Wallach, our Chief Executive Officer (who is also on our Board of Managers), constructively or beneficially owns all of the equity interests in our Company. As our only executive officer, Mr. Wallach is responsible for all aspects of our day-to-day operations. Though the approval of the independent Managers is required for all affiliate transactions, Mr. Wallach will, nonetheless, be able to exercise significant control over our affairs as the independent Managers may be removed by a vote of holders of 80% of our outstanding voting membership interests.

If we lose or are unable to hire or retain key personnel, we may be delayed or unable to implement our business plan, which would adversely affect our ability to repay the Notes.

Our success depends to a significant degree upon the contributions of Daniel M. Wallach, our Chief Executive Officer and Manager. We do not have an employment agreement with Mr. Wallach and cannot guarantee that he will remain affiliated with us. If he were to cease his affiliation with us, our operating results would suffer. We believe that our future success depends, in part, upon our ability to hire and retain additional personnel. We cannot assure our Note holders that we will be successful in attracting and retaining such personnel, which could hinder our ability to implement our business plan.

Our Note holders will not have the opportunity to evaluate our investments before they are made.

We intend to use the net offering proceeds in accordance with the “Use of Proceeds” section of our prospectus, including investment in secured real estate loans for the acquisition and development of parcels of real property as single-family residential lots and/or the construction of single-family homes. Since we have not identified any investments that we will make with the net proceeds of this offering, we are generally unable to provide our Note holders with information to evaluate the potential investments we may make with the net offering proceeds before purchasing the Notes. Our Note holders must rely on our management to evaluate our investment opportunities, and we are subject to the risk that our management may not be able to achieve our objectives, may make unwise decisions or may make decisions that are not in our best interest.

There is no sinking fund to ensure repayment of the Notes at maturity, so our Note holders are totally reliant upon our ability to generate adequate cash flows.

We do not contribute funds to a separate account, commonly known as a sinking fund, to repay the Notes upon maturity. Because funds are not set aside periodically for the repayment of the Notes over their respective terms, our Note holders must rely on our consolidated cash flows from operations, investing and financing activities and other sources of financing for repayment, such as funds from the sale of the Notes, loan repayments, and other borrowings. To the extent cash flows from operations and other sources are not sufficient to repay the Notes our Note holders may lose all or part of their investments.

If we default in our Note payment obligations, the indenture agreement provides that the trustee could accelerate all payments due under the Notes, which would further negatively affect our financial position.

Our obligations with respect to the Notes are governed by the terms of indenture agreement with U.S. Bank, as trustee. Under the indentures, in addition to other possible events of default, if we fail to make a payment of principal or interest under any Note and this failure is not cured within 30 days, we will be deemed in default. Upon such a default, the trustee or holders of 25% in principal of the outstanding Notes could declare all principal and accrued interest immediately due and payable. If our total assets do not cover these payment obligations, we would most likely be unable to make all payments under the Notes when due, and we might be forced to cease our operations.

The portion of our business plan utilizing a note offering for a source of funds for commercial lending purposes is new to us. This may decrease the likelihood that we will be successful and able to pay principal and interest on the Notes.

We have no experience with managing a notes offering as a source of funds for our business activities. This decreases the likelihood that the results from our new business plan will be similar to or better than the results we obtained under our prior business plan. If we are not successful, our ability to pay principal and interest on the Notes may be adversely affected.

| 15 |

We are an “emerging growth company” under the federal securities laws and are subject to reduced public company reporting requirements.

In April 2012, President Obama signed into law the Jumpstart Our Business Startups Act, or the JOBS Act. We are an “emerging growth company,” as defined in the JOBS Act, and are eligible to take advantage of certain exemptions from, or reduced disclosure obligations relating to, various reporting requirements that are normally applicable to public companies.

We will remain an “emerging growth company” until the earliest of (1) the last day of the first fiscal year in which we have total annual gross revenues of $1 billion or more, (2) the last day of the fiscal year following the fifth anniversary of the date of the first sale of our common equity securities pursuant to an effective registration statement, (3) the date on which we become a “large accelerated filer” as defined in Rule 12b-2 under the Exchange Act (which would occur if the market value of our common equity held by non-affiliates exceeds $700 million, measured as of the last business day of our most recently completed second fiscal quarter, and we have been publicly reporting for at least 12 months) or (4) the date on which we have issued more than $1 billion in non-convertible debt during the preceding three-year period. Under the JOBS Act, emerging growth companies are not required to (1) provide an auditor’s attestation report on management’s assessment of the effectiveness of internal control over financial reporting, pursuant to Section 404 of the Sarbanes-Oxley Act, (2) comply with new requirements adopted by the Public Company Accounting Oversight Board, or the PCAOB, which require mandatory audit firm rotation or a supplement to the auditor’s report in which the auditor must provide additional information about the audit and the issuer’s financial statements, (3) comply with new audit rules adopted by the PCAOB after April 5, 2012 (unless the SEC determines otherwise), (4) provide certain disclosures relating to executive compensation generally required for larger public companies or (5) hold shareholder advisory votes on executive compensation.

Additionally, the JOBS Act provides that an “emerging growth company” may take advantage of an extended transition period for complying with new or revised accounting standards that have different effective dates for public and private companies. This means an “emerging growth company” can delay adopting certain accounting standards until such standards are otherwise applicable to private companies. We intend to take advantage of such extended transition period. Since we will not be required to comply with new or revised accounting standards on the relevant dates on which adoption of such standards is required for other public companies, our financial statements may not be comparable to the financial statements of companies that comply with public company effective dates. If we were to subsequently elect to instead comply with these public company effective dates, such election would be irrevocable pursuant to Section 107 of the JOBS Act.

Risks Related to Our Business

Currently, we are reliant on a single developer and homebuilder, the Hoskins Group, for most of our revenues and a portion of our financing.

As of December 31, 2013, 98% of our outstanding loan balance consisted of loans made to Benjamin Marcus Homes, LLC and Investor’s Mark Acquisitions, LLC, both of which are owned by Mark Hoskins (collectively all three parties referred to herein as the “Hoskins Group”). We also have an unsecured loan payable to Investor’s Mark Acquisitions, LLC. Therefore, currently, we are substantially reliant upon a single developer and homebuilder for all of our revenues and a portion of our financing. Any event of bankruptcy, insolvency or general downturn in the business of this developer and homebuilder will have a substantial adverse financial impact on our business and our ability to pay back our Note holders’ investments in the Notes in the long term.

We have a limited operating history and limited experience operating as a company, so we may not be able to successfully operate our business or generate sufficient revenue.

We were organized in May 2007 and, in the past, we were the lessor in three commercial real estate leases with an affiliate, 84 Lumber Company. At the time of the initial leases, our Chief Executive Officer, Daniel M. Wallach, was the Chief Financial Officer of 84 Lumber Company. Mr. Wallach’s employment with 84 Lumber Company ended in April 2011, and the leased properties were sold to 84 Lumber Company affiliates in May and September 2011, thereby terminating the leases. In December 2011, we made our first real estate loan of the type described in our “Business” section. Therefore, we have a limited operating history and limited experience operating as a company from which to evaluate our business or our likelihood of future success in operating our business, generating revenues, or achieving profitability. We cannot assure our Note holders that we will be able to operate our business successfully or implement our operating policies and strategies described in the business section.

We have two lines of credit from affiliates which allow us to incur a significant amount of secured debt. These lines are collateralized by a lien against all of our assets. We expect to incur a significant amount of additional debt in the future, including issuance of the Notes, which will subject us to increased risk of loss.

As of December 31, 2013, we had $0 of secured debt outstanding, with availability on our senior debt lines of credit of $1,500,000. These lines are from affiliates. The affiliate loans are collateralized by a lien against all of our assets. In addition, we expect to incur a significant amount of additional debt in the future, including issuance of the Notes, borrowing under credit facilities and other arrangements. The Notes will be subordinated in right of payment to all secured debt, including the affiliate loans. Therefore, in the event of a default on the secured debt, affiliates of our Company, including Mr. Wallach, have the right to receive payment ahead of our Note holders. Accordingly, our business is subject to increased risk of a total loss of our Note holders’ investments if we are unable to repay all of our secured debt, including the affiliate loans.

| 16 |

Our operations are not subject to the stringent banking regulatory requirements designed to protect investors, so repayment of our Note holders’ investments is completely dependent upon our successful operation of our business.

Our operations are not subject to the stringent regulatory requirements imposed upon the operations of commercial banks, savings banks, and thrift institutions, and are not subject to periodic compliance examinations by federal or state banking regulators. For example, we will not be well diversified in our product risk, and we cannot benefit from government programs designed to protect regulated financial institutions. Therefore, an investment in our Notes does not have the regulatory protections that the holder of a demand account or a certificate of deposit at a bank does. The return on and of Notes purchased by a Note holder is completely dependent upon our successful operations of our business. To the extent that we do not successfully operate our business, our ability to pay interest and principal on the Notes will be impaired.

Most of our assets will be commercial construction loans to homebuilders and/or developers which are a higher than average credit risk, and therefore could expose us to higher rates of loan defaults, which could impact our ability to repay amounts owed to our Note holders.

Our primary business is extending commercial construction loans to homebuilders, along with some loans for land development. These loans are considered higher risk because the ability to repay depends on the homebuilder’s ability to sell a newly built home. These homes typically are not sold by the homebuilder prior to commencement of construction. Therefore, we may have a higher risk of loan default among our customers than other commercial lending companies. If we suffer increased loan defaults, in any given period, our operations could be materially adversely affected and we may have difficulty making our principal and interest payments on the Notes.

We depend on the availability of significant sources of credit to meet our liquidity needs and our failure to maintain these sources of credit could materially and adversely affect our liquidity in the future.

We plan to maintain a line of credit with a financial institution in the future, so that we may draw funds when necessary to meet our obligation to redeem maturing Notes, pay interest on the Notes, meet our commitments to lend money to our customers, and for other general corporate purposes. We do not have a financial institution line of credit at this time. If we fail to obtain such a line of credit or maintain one, we will be more dependent on the proceeds from the Notes for our continued liquidity. If the sale of the Notes is significantly reduced or delayed for any reason and we fail to obtain or renew a line of credit, or we default on our line of credit, our ability to meet our obligations, including our Note obligations, could be materially adversely affected, and we may not have enough cash to pay back our Note holders’ investments. Also, the failure to maintain an active line of credit (and therefore using cash for liquidity instead of a borrowing line), even though we have liquidity from the Notes, will reduce our earnings, because we will be paying interest on the Notes, while we are holding cash instead of reducing our borrowings.

If the proceeds from the issuance of the Notes exceed the cash flow needed to fund the desirable business opportunities that are identified, we may not be able to invest all of the funds in a manner that generates sufficient income to pay the interest and principal on the Notes.

Our ability to pay interest on our debt, including the Notes, pay our expenses, and cover loan losses is dependent upon interest and fee income we receive from loans extended to our customers. If we are not able to lend to a sufficient number of customers at high enough interest rates, we may not have enough interest and fee income to meet our obligations, which could impair our ability to pay interest and principal to our Note holders. If money brought in from new Notes and from repayments of loans from our customers exceeds our short term obligations such as expenses, Note interest and redemptions, and line of credit principal and interest, then it is likely to be held as cash, which will have a lower return than the interest rate we are paying on the Notes. This will lower earnings and may cause losses which could impair our ability to repay the principal and interest on the Notes.

The collateral securing our mortgage loans may not be sufficient to pay back the principal amount in the event of a default by the borrowers.

In the event of default, our mortgage loan investments are generally dependent entirely on the loan collateral to recover our investment. Our loan collateral consists primarily of a mortgage on the underlying property. In the event of a default, we may not be able to recover the premises promptly and the proceeds we receive upon sale of the property may be adversely affected by risks generally related to interests in real property, including changes in general or local economic conditions and/or specific industry segments, declines in real estate values, increases in interest rates, real estate tax rates and other operating expenses including energy costs, changes in governmental rules, regulations and fiscal policies, including environmental legislation, acts of God, and other factors which are beyond our or our borrowers’ control. Current market conditions may reduce the proceeds we are able to receive in the event of a foreclosure on our collateral. Our remedies with respect to the loan collateral may not provide us with a recovery adequate to recover our investment.

| 17 |

Currently, we are substantially reliant on the local homebuilding industry in the Pittsburgh, Pennsylvania market.

Our loan investments are currently not diversified geographically. As of December 31, 2013, 98% of our outstanding loan balances are concentrated in the Pittsburgh, Pennsylvania market. We believe that home values are the predominant factor which impacts the amount of money we may lose on loans which default. Even during the recent recession, home prices in the Pittsburgh market have steadily risen. It is still possible that the Pittsburgh housing market could become subject to the same negative conditions that have affected home values nationally. Because of our reliance on the Pittsburgh housing market, any adverse conditions affecting the local housing market in this area will have a magnified adverse effect on our loan portfolio and adversely affect our ability to pay back our Note holders’ investments in the Notes. Adverse conditions affecting the local housing market could include, but are not limited to, declines in new housing starts, declines in new home prices, declines in new home sales, increases in the supply of available building lots or built homes available for sale, increases in unemployment, and unfavorable demographic changes.

Our business is not industry-diversified and the homebuilding industry has undergone a significant downturn. Further deterioration in industry or economic conditions could further decrease demand and pricing for new homes and residential home lots. A decline in housing values similar to the recent national downturn in the real estate market would have a negative impact on our business. Smaller value declines will also have a negative impact on our business. These factors may decrease the likelihood we will be able to generate enough cash to repay the Notes.

Developers and homebuilders to whom we may make loans will use the proceeds of our loans to develop raw land into residential home lots and construct homes. The developers obtain the money to repay our development loans by selling the residential home lots to homebuilders or individuals who will build single-family residences on the lots, or by obtaining replacement financing from other lenders. A developer’s ability to repay our loans is based primarily on the amount of money generated by the developer’s sale of its inventory of single-family residential lots. Homebuilders obtain the money to repay our loans by selling the homes they construct or by obtaining replacement financing from other lenders, and thus, the homebuilders’ ability to repay our loans is based primarily on the amount of money generated by the sale of such homes.

The homebuilding industry is cyclical and is significantly affected by changes in industry conditions, as well as in general and local economic conditions, such as:

| · | employment level and job growth; |

| · | demographic trends, including population increases and decreases and household formation; |

| · | availability of financing for homebuyers; |

| · | interest rates; |

| · | affordability of homes; |

| · | consumer confidence; |

| · | levels of new and existing homes for sale, including foreclosed homes and homes held by investors and speculators; and |

| · | housing demand generally. |