Attached files

| file | filename |

|---|---|

| 8-K - CARROLLTON BANCORP FORM 8-K - BAY BANCORP, INC. | carrollton8k.htm |

Exhibit 99.1

Annual Shareholder Meeting

Investor Presentation

Investor Presentation

A Subsidiary of Carrollton Bancorp

August 28, 2013

2

This investor presentation contains forward-looking statements within the meaning of Section 21E of the

Securities Exchange Act of 1934 and the Private Securities Litigation Reform Act of 1995 concerning Carrollton

Bancorp’s plans, strategies, objectives, expectations, intentions, financial condition and results of operations.

These forward-looking statements reflect management’s current views and intentions and are subject to known

and unknown risks, uncertainties, assumptions and other factors that could cause the actual results to differ

materially from those contemplated by the statements. The significant risks and uncertainties related to

Carrollton Bancorp of which management is aware are discussed in detail in the periodic reports that Carrollton

Bancorp files with the Securities and Exchange Commission (the “SEC”), including in the “Risk Factors” section of

its Annual Report on Form 10-K for the year ended December 31, 2012 and its Quarterly Report on Form 10-Q

for the quarter ended June 30, 2013. Investors are urged to review Carrollton Bancorp’s periodic reports, which

are available at no charge through the SEC’s website at www.sec.gov and through Carrollton Bancorp’s website

at www.baybankmd.com on the “Investor Relations” page. Carrollton Bancorp assumes no obligation to update

any of these forward-looking statements to reflect a change in its views or events or circumstances that occur

after the date of this presentation.

Securities Exchange Act of 1934 and the Private Securities Litigation Reform Act of 1995 concerning Carrollton

Bancorp’s plans, strategies, objectives, expectations, intentions, financial condition and results of operations.

These forward-looking statements reflect management’s current views and intentions and are subject to known

and unknown risks, uncertainties, assumptions and other factors that could cause the actual results to differ

materially from those contemplated by the statements. The significant risks and uncertainties related to

Carrollton Bancorp of which management is aware are discussed in detail in the periodic reports that Carrollton

Bancorp files with the Securities and Exchange Commission (the “SEC”), including in the “Risk Factors” section of

its Annual Report on Form 10-K for the year ended December 31, 2012 and its Quarterly Report on Form 10-Q

for the quarter ended June 30, 2013. Investors are urged to review Carrollton Bancorp’s periodic reports, which

are available at no charge through the SEC’s website at www.sec.gov and through Carrollton Bancorp’s website

at www.baybankmd.com on the “Investor Relations” page. Carrollton Bancorp assumes no obligation to update

any of these forward-looking statements to reflect a change in its views or events or circumstances that occur

after the date of this presentation.

DISCLOSURE

§ Carrollton Bank was formed in 1903 and built a community bank franchise

serving the Baltimore market. Until April 19, 2013 when it merged into Bay

Bank, FSB, Carrollton Bank was a wholly-owned subsidiary of Carrollton

Bancorp.

serving the Baltimore market. Until April 19, 2013 when it merged into Bay

Bank, FSB, Carrollton Bank was a wholly-owned subsidiary of Carrollton

Bancorp.

§ Bay Bank, FSB was formed in 2010 as a subsidiary of Jefferson Bancorp Inc.

(JBI) by Financial Services Partners Fund I (FSPF) to purchase the assets and

liabilities of Bay National Bank from the FDIC in July 2010.

(JBI) by Financial Services Partners Fund I (FSPF) to purchase the assets and

liabilities of Bay National Bank from the FDIC in July 2010.

§ In 2012, JBI entered into a definitive agreement to acquire Carrollton Bancorp

through a reverse merger transaction. In the transaction, which closed on

April 19, 2013, JBI merged into Carrollton Bancorp, with Carrollton Bancorp as

the surviving holding company, and Carrollton Bank merged into Bay Bank,

FSB, with Bay Bank, FSB as the surviving bank.

through a reverse merger transaction. In the transaction, which closed on

April 19, 2013, JBI merged into Carrollton Bancorp, with Carrollton Bancorp as

the surviving holding company, and Carrollton Bank merged into Bay Bank,

FSB, with Bay Bank, FSB as the surviving bank.

§ The post-merger Bay Bank, FSB, which remained a federal savings bank, has

approximately $470 million in assets. The common stock of its holding

company, Carrollton Bancorp, is listed on NASDAQ under the ticker symbol

“CRRB”.

approximately $470 million in assets. The common stock of its holding

company, Carrollton Bancorp, is listed on NASDAQ under the ticker symbol

“CRRB”.

HISTORY OF BAY BANK

Carrollton

Bank

Opens

Bank

Opens

Shelf

Charter

approved

for JBI

Charter

approved

for JBI

JBI Acquired

Bay National

Bank from

FDIC

Bay National

Bank from

FDIC

Bay Bank

Grows

Organically

Grows

Organically

The new

Bay Bank

Bay Bank

& CRRB

April 2013

July 2010 to

Present

Present

2010

July 2010

1903

THE PATH TO BAY BANK / CARROLLTON

BANCORP

BANCORP

5

DEAL METRICS OF MERGER

TRANSACTION VALUE

CONSIDERATION

IMPLIED PRICE / SHARE

CRRB TARP TREATMENT

CAPITAL RAISE

CLOSING

COST SAVINGS

$25.1 million ($14.1 million consideration to existing Carrollton Bancorp

shareholders and $11 million additional investment by FSPF prior to closing.

shareholders and $11 million additional investment by FSPF prior to closing.

42.5% of existing Carrollton Bancorp shareholders elected cash in exchange

for their stock, 57.5% retained their stock.

for their stock, 57.5% retained their stock.

§ Carrollton Bancorp issued approximately 7.87 million shares of common

stock to FSPF in exchange for its shares of JBI.

stock to FSPF in exchange for its shares of JBI.

§ Existing Carrollton shareholders had an option to either retain their

shares or exchange their shares for $6.20 per share in cash.

shares or exchange their shares for $6.20 per share in cash.

Repayment of $9.2 million of TARP CPP obligations prior to closing.

$11MM capital injection by FSPF into JBI prior to closing.

April 19, 2013

Transaction drives EPS growth with potential to achieve up to 20%

cumulative cost savings.

cumulative cost savings.

6

STRONG FINANCIAL SPONSOR

Financial Services Partners Fund I is managed by Hovde Private Equity Advisors, LLC.

Hovde differentiates itself as a proven community bank investing specialist and has a

track record of making control investments in community banks and thrifts since 1994.

7

Kevin Cashen, CEO and President - Baltimore native with over 29 years of experience in community

banking in Virginia and Maryland including Loyola Federal S&L, Signet Bank and Chevy Chase Bank.

banking in Virginia and Maryland including Loyola Federal S&L, Signet Bank and Chevy Chase Bank.

H. King Corbett, Chief Lending Officer - Baltimore native with over 35 years of banking experience

in the Baltimore market with banks including Maryland National Bank, Sovran Bank, First National Bank of

Maryland (now M&T Bank) and SunTrust Bank.

in the Baltimore market with banks including Maryland National Bank, Sovran Bank, First National Bank of

Maryland (now M&T Bank) and SunTrust Bank.

H. Les Patrick, Chief Credit Officer/Special Assets - Banker with over 35 years of experience

in the Baltimore/Washington markets. Joined the Bank from Bank of America. Worked with other banks

including National Bank of Washington, American Security Bank, Equitable Bank, Maryland National Bank and

Provident Bank.

in the Baltimore/Washington markets. Joined the Bank from Bank of America. Worked with other banks

including National Bank of Washington, American Security Bank, Equitable Bank, Maryland National Bank and

Provident Bank.

Gary M. Jewell, Senior Vice President of Electronic Banking - Leader at legacy Carrollton

Bank since July 1998 and had been Senior Vice President and Retail Delivery Group Manager. Prior to joining

the Bank, Director of Product Management and Point of Sale Services for the MOST EFT network.

Bank since July 1998 and had been Senior Vice President and Retail Delivery Group Manager. Prior to joining

the Bank, Director of Product Management and Point of Sale Services for the MOST EFT network.

David Borowy, Interim Chief Financial Officer - Experienced financial professional with prior roles

as CFO of legacy Bay National Bank and Calvert Street Capital Corporation. Mr. Borowy has previously served

as interim CFO, guiding the institution during its acquisition of Carrollton Bancorp.

as CFO of legacy Bay National Bank and Calvert Street Capital Corporation. Mr. Borowy has previously served

as interim CFO, guiding the institution during its acquisition of Carrollton Bancorp.

TALENTED MANAGEMENT TEAM

8

EXPERIENCED BOARD OF DIRECTORS

11

JUNE 30, 2013 LOAN & DEPOSIT COMPOSITION

|

Loan Portfolio

|

($000s)

|

Rate

|

%

|

|

Gross Loans

|

$374,920

|

6.41%

|

100.0%

|

|

Deposit Composition

|

($000s)

|

Rate

|

%

|

|

|

|||

|

|

|||

|

|

|||

|

|

|||

|

|

|||

|

Total Deposits

|

410,859

|

0.41%

|

100.00%

|

14

MARKET OVERVIEW

As of June 30, 2012 (Source: SNL Financial)

15

IN MARYLAND, SMALL BUSINESSES COMPRISE 97.6% OF ALL EMPLOYERS

AND EMPLOY 52.1% OF THE PRIVATE SECTOR WORKFORCE:

§Of the 109,087 employer firms, 106,441 have fewer than 500 employees

§These firms employ more than 1.1 million workers (1,105,231)

§These firms have an annual payroll of approximately $45.7 billion,

47% of the total payroll of employer firms in the state

47% of the total payroll of employer firms in the state

SMALL BUSINESSES DOMINANT MARYLAND MARKET

Source: Department of Business & Economic Development

16

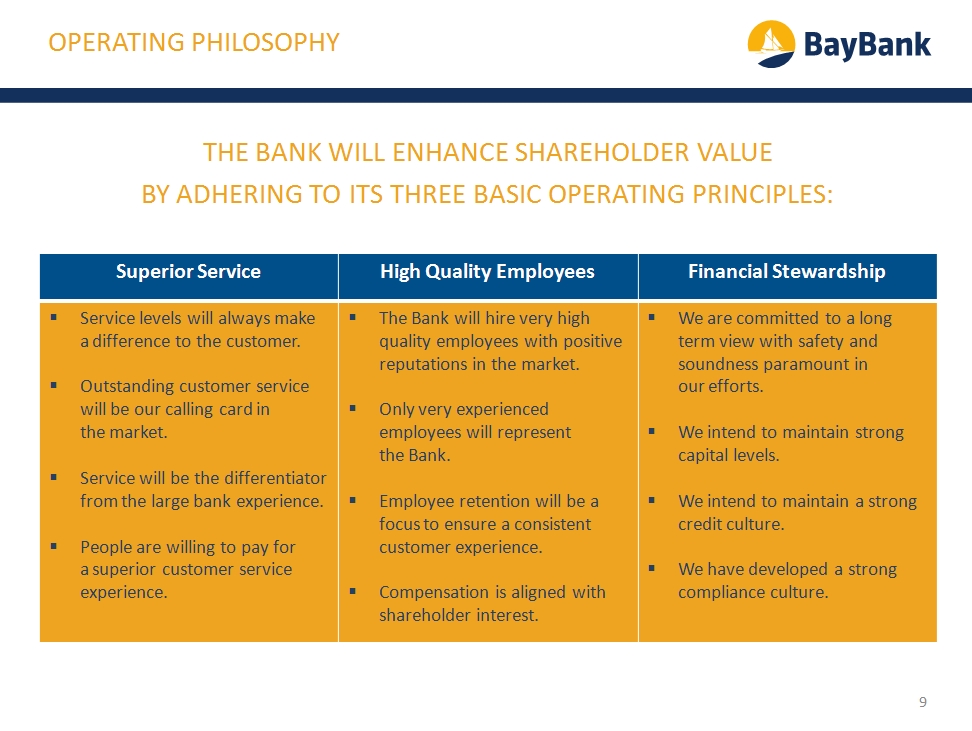

§ Exceptional new management team and board of directors from both companies.

§ Vibrant, high-growth primary market in greater Baltimore-Washington corridor.

§ Balanced community banking business model with strong credit and fee-based products.

§ Enhanced scale attributes, improved profitability and increased legal lending limit.

§ Strong balance sheet with 10% tier one capital and moderate classified assets-to capital.

§ Positioned to grow organically and via acquisition to become a $1-3 billion in assets.

SUMMARY

INVESTOR CONTACT:

Kevin B. Cashen

President & CEO

410.427.3707

kcashen@baybankmd.com

www.baybankmd.com