Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - Tri-Tech Holding, Inc. | v320488_ex32-2.htm |

| EX-32.1 - EXHIBIT 32.1 - Tri-Tech Holding, Inc. | v320488_ex32-1.htm |

| EX-31.1 - EXHIBIT 31.1 - Tri-Tech Holding, Inc. | v320488_ex31-1.htm |

| EX-31.2 - EXHIBIT 31.2 - Tri-Tech Holding, Inc. | v320488_ex31-2.htm |

U. S. SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-Q

| x | Quarterly report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the quarterly period ended June 30, 2012

| ¨ | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from ___________ to ___________.

Commission File Number 001-34427

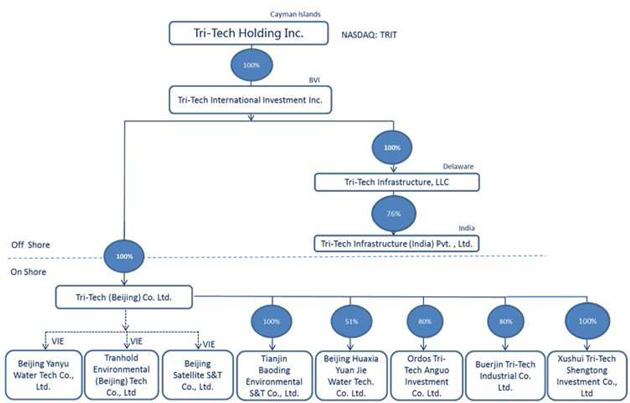

Tri-Tech Holding Inc.

(Exact name of registrant as specified in its charter)

| Cayman Islands | Not Applicable | |

| (State or other jurisdiction of | (I.R.S. employer | |

| incorporation or organization) | identification number) |

16th Floor of Tower B, Renji Plaza

101 Jingshun Road, Chaoyang District

Beijing 100102 China

(Address of principal executive offices and zip code)

+86 (10) 5732-3666

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company.

| Large accelerated filer | ¨ | Accelerated filer | ¨ | ||

| Non-accelerated filer (Do not check if a smaller reporting company) | ¨ | Smaller reporting company | x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

The Company is authorized to issue 30,000,000 ordinary shares, $0.001 par value per share. As of August 14, the Company has 8,218,406 ordinary shares outstanding, excluding 21,100 treasury shares.

TRI-TECH HOLDING INC.

FORM 10-Q

INDEX

| SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS | ii | ||

| PART I. | FINANCIAL INFORMATION | I-1 | |

| Item 1. | Financial Statements | I-1 | |

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | I-1 | |

| Item 3. | Quantitative and Qualitative Disclosures about Market Risk | I-20 | |

| Item 4. | Controls and Procedures | I-20 | |

| PART II. | OTHER INFORMATION | II-1 | |

| Item 1. | Legal Proceedings | II-1 | |

| Item 1A. | Risk Factors | II-1 | |

| Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds | II-1 | |

| Item 3. | Defaults Upon Senior Securities | II-1 | |

| Item 4. | Mine Safety Disclosures | II-1 | |

| Item 5. | Other Information | II-1 | |

| Item 6. | Exhibits | II-1 | |

| FINANCIAL STATEMENTS | F-1 | ||

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This document contains certain statements of a forward-looking nature. Such forward-looking statements, including but not limited to projected growth, trends and strategies, future operating and financial results, financial expectations and current business indicators are based upon current information and expectations and are subject to change based on factors beyond the control of the Company. Forward-looking statements typically are identified by the use of terms such as “look,” “may,” “should,” “might,” “believe,” “plan,” “expect,” “anticipate,” “estimate” and similar words, although some forward-looking statements are expressed differently. The accuracy of such statements may be impacted by a number of business risks and uncertainties that could cause actual results to differ materially from those projected or anticipated, including but not limited to the following:

| • | the timing of the development of future products; |

| • | projections of revenue, earnings, capital structure and other financial items; |

| • | statements of the Company’s plans and objectives; |

| • | statements regarding the capabilities of its business operations; |

| • | statements of expected future economic performance; |

| • | statements regarding competition in its market; and |

| • | assumptions underlying statements regarding the Company or its business. |

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. The Company undertakes no obligation to update this forward-looking information. Nonetheless, the Company reserves the right to make such updates from time to time by press release, periodic report or other method of public disclosure without the need for specific reference to this Report. No such update shall be deemed to indicate that other statements not addressed by such update remain correct or create an obligation to provide any other updates.

| ii |

PART I. FINANCIAL INFORMATION

| Item 1. | Financial Statements |

See the financial statements following the signature page of this report, which are incorporated herein by reference.

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

The following discussion contains, in addition to historical information, forward-looking statements that involve risks and uncertainties. The actual results could differ materially from those described herein.

Company Overview

Tri-Tech Holding Inc. (the “Company” or “we”) is a leading provider of integrated solutions, products and technologies to water resource management and environmental protection industries. The Company has successfully implemented projects in both Chinese and overseas markets such as India, the Middle East and North America.

The Company aims to provide tailored solutions to complex environmental challenges faced by both public and private sectors in China and beyond. Its clientele consists of a combination of government agencies, municipalities, and industrial entities located in China, India, the Middle East and North America. To maintain a leading position in its domestic market, the Company’s strategy is to reinforce customer recognition and to offer diversified proprietary products to exceed the expectations of its expanding client base. Internationally, the Company also continues to further its geographic reach in India, the Middle East and North America in the water and wastewater treatment industry. To implement the three engineering-procurement-construction contracts in India and to develop market further, the Company made a capital injection in the amount of Indian National Rupee (“INR”) 1,917,000 (or $35,273), in Tri-Tech Infrastructure (India) Pvt., Ltd (“TII”) on May 19, 2012. As a result of the capital injection, the Company increased its equity ownership in TII to 76% and became the controlling shareholder. The Company’s total investment in TII amounts to INR 2,217,000, or $55,886. The amount consists of two parts: the initial investment of INR 300,000 on October 19, 2011, which was adjusted to $20,613 due to TII’s earnings from the beginning of TII’s operation through May 19, 2012; and the investment of INR 1,917,000, or $35,273, on May 19, 2012.

The Company’s principal executive offices are located at the 16th Floor of Tower B, Renji Plaza, 101 Jingshun Road, Chaoyang District, Beijing 100102 China. The telephone number at this address is +86 (10) 5732-3666. Its ordinary shares are traded on the NASDAQ Capital Market under the symbol “TRIT.” The Company’s website, www.tri-tech.cn, provides a variety of information. Its annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K filed with the United States Securities and Exchange Commission (the “SEC”) are available, as soon as practicable after filing, under the investor relations tab on its website, or by a direct link to its filings on the SEC’s website.

Principal Products, Services and Their Markets

The Company operates in three segments: (i) Water, Wastewater Treatment and Municipal Infrastructure (“WWTM”), (ii) Water Resource Management System and Engineering Services (“WRME”), and (iii) Industrial Pollution Control and Safety (“IPCS”). Through its subsidiaries, variable interest entities (“VIE”) and joint venture partnership, the Company provides proprietary and third-party products, integrated systems and other services for the purposes of water resource monitoring, development, utilization and protection. The Company designs water works and customized facilities for reclaiming and reusing water and sewage treatment for China’s municipalities. These systems integrate process equipment, software, controls and instruments, information management systems, resource planning and local and distant networking hardware that includes sensors, control systems, programmable logic controllers, and supervisory control and data collection systems. The Company designs systems that track natural waterway levels for flood and drought control, monitor groundwater quality, manage water resources and irrigation systems. It also provides systems for volatile organic compound (“VOC”) abatement, odor control, water and wastewater treatment, water recycling facilities design, project engineering, procurement and construction for petroleum refineries, petrochemical and power plants as well as safe and clean production technologies for oil and gas field exploration and pipelines. With the acquisitions of J&Y International Inc. (“J&Y”) and Beijing Huaxia Yuanjie Water Technology Co., Ltd (“Yuanjie”), the Company expanded its product lines by adding thermal seawater desalination systems, zero liquid discharge (“ZLD”) systems, and secondary water supply systems targeting high-rise buildings.

Core Technologies and Solutions

ZLD Solution for Industrial Wastewater Treatment. The ZLD systems provide an optimal solution for wastewater treatment as no liquid pollutants are discharged into the environment and water is completely recycled. Solid by-products can be produced by treating wastewater with liquid evaporation concentration (mechanical vapor compression-horizontal spraying film evaporator) and crystallization (forced circulation crystallization system), which are key components of the ZLD solution. The Company can tailor ZLD solutions to its customers’ individual needs and requirements, and ensure reliability of technology and stability of system operation. Besides desalination, the technologies can also be used to treat high-concentration wastewater such as landfill leachate and high-salinity wastewater. The industries and companies served by the technologies include oil and gas exploration companies, petrochemical refineries and fertilizer plants, coal-fired and thermal power plants, pulp and paper mills, municipal water treatment facilities, and pharmaceutical and food-processing companies.

| I-1 |

Seawater Desalination Solution. There is a growing market for the business of seawater desalination due to fresh water resource shortage. The Company is capable of providing tailored seawater desalination solutions for different types of customers. These solutions include the thermal seawater desalination technology featuring low temperature multi-effect evaporation and multi-flash evaporation, typically for projects with easy access to low-cost heat source such as superheated vapor and hot liquid, and the membrane seawater desalination technology for projects with easy access to cheap electrical power. The Company also specializes in small skid-mounted seawater desalination units such as the mechanical vapor compression-spraying film evaporator.

VOC Treatment. In the industrial production process, some plants produce large volumes of volatile organic gases that are hazardous to the environment if discharged untreated. The Company’s thermal oxidation technology thoroughly treats these toxic, harmful and non-recyclable organic waste gases. The Company developed different thermal oxidation technologies such as regenerative thermal oxidizer, thermal oxidizer, regenerative catalytic oxidizer and catalytic oxidizer based on specific parameters for different waste gases.

Forward Osmosis Technology. The forward osmosis technology can turn muddy contaminated water into pure and potable water. It can also be used to treat industrial wastewater which contains toxic wastes that are not readily degradable. The Company’s products do not have the clogging or fouling problems seen in the reverse osmosis technology.

Flash Flood Disaster Warning Information Dissemination System. The disaster warning information dissemination platform is part of the flash flood monitoring and warning system. As the center of information distribution, it is the most important part of the integrated system. The platform timely and accurately transmits disaster warning information to areas threatened by flash flood through early warning programs and channels which receive instructions from county-level flood control offices, allowing recipients to take necessary precautionary measures to minimize casualties and property losses. The platform can be used to receive feedback from early warning stations to monitor the effectiveness of information dissemination.

Business Segments

The Company’s business segments are grouped according to the types of services provided and the types of clients served. The total sales and costs are divided into three segments accordingly. The Company assesses each segment’s performance based on net revenue and gross profit on contribution margin. More detailed descriptions of the three reportable operating segments follow:

Segment 1: Water, Wastewater Treatment and Municipal Infrastructure (“WWTM”)

WWTM focuses on municipal water supply and distribution, wastewater treatment and gray water recycling, through the procurement and construction of proprietary build-transfer-operation (“BTO”) processing equipment and processing control systems. The Company also provides municipal facilities engineering and operation management services for related infrastructure construction projects. This segment has historically provided the majority of its contract revenues. Representative projects in the China market include the expansion phase of the water treatment plant for the City of Ordos valued at approximately $20 million, which started in June 2011 and is expected to be completed by the end of 2012, and the recycled water quality upgrade project for Tianjin Airport Economic Zone with a total contract value of $1.46 million, which started in June 2011 and is expected to be operational by the end of 2012. Representative international projects include three Indian engineering-procurement-construction (“EPC”) contracts for sewage collection and treatment plants in three municipalities with a total contract value of $39 million, which started in November 2011 and are expected to be completed by the end of 2013.

Segment 2: Water Resource Management System and Engineering Service (“WRME”)

WRME involves projects relating to water resource management, flood control and forecasting, irrigation systems, and similar ventures through system integration of proprietary and third-party hardware and software products. For government agencies, the Company designs systems that track natural waterway levels for drought control, monitor groundwater quality, and generally manage water resources and irrigation systems. Representative projects include flash flood early warning and hydrologic monitoring projects for multiple counties in Heilongjiang, Fujian, Guizhou, Anhui and Shanxi provinces, with a total contract value of $7.02 million, which commenced in April of 2012 and are expected to be completed at different points in time from October to November, 2012.

| I-2 |

Segment 3: Industrial Pollution Control and Safety (“IPCS”)

IPCS focuses on industrial water, wastewater treatment and seawater desalination for industrial production and pollution control in the petroleum and power industries applying a variety of technologies such as ZLD, multi-effect evaporation, multi-flash evaporation, as well as emissions control. Projects in this segment include traditional EPC of equipment and modules, and the operation and maintenance of industrial wastewater treatment plants. For petroleum refineries, petrochemical factories and power plants, the Company provides systematic solutions for volatile organic compound abatement, odor control, water and wastewater treatment, and water recycling. The Company also provides safe and clean production technologies for oil and gas field exploration and pipeline transportation. Representative projects include the Dawangdian Industrial Park wastewater plant and pipeline project in Xushui County of Hebei Province, with a total contract value of $7.9 million, which is expected to be delivered by November 2012; the seawater desalination project for the utility plant of Qatar Petrochemical Co. Ltd. in Qatar, with a contract value of $8.3 million, which started in December 2011 and is expected to be delivered by November 2012; the Wuhan natural gas distribution network control system project, with a contract value of $1.5 million, which began in January 2012 and is expected to be completed by May 2013; and the water processing unit project for a steel plant in Mexico to be completed and delivered by early April 2013.

Revenues by Segment

In the three months ended June 30, 2012, our total revenues were $23.0 million, including $8.3 million from Segment 1, $8.4 million from Segment 2, and $6.3 million from Segment 3. The table below shows the performance of each business segment for the second quarter of 2012. Segment 1 contributed 36.3% of the total revenues; Segment 2 contributed 36.6%; and Segment 3 contributed the remaining 27.1%.

| Three Months Ended June 30, 2012 | ||||||||||||||||||||||||||||||||

| Segment 1: | % | Segment 2: | % | Segment 3: | % | Total: | % | |||||||||||||||||||||||||

| System Integration | $ | 8,354,428 | 100.0 | % | $ | 7,441,871 | 88.2 | % | $ | 5,945,471 | 95.1 | % | $ | 21,741,770 | 94.4 | % | ||||||||||||||||

| Hardware Products | $ | — | — | % | $ | 994,129 | 11.8 | % | $ | 304,635 | 4.9 | % | $ | 1,298,764 | 5.6 | % | ||||||||||||||||

| Software Products | $ | — | — | % | $ | — | — | % | $ | — | — | % | $ | — | — | % | ||||||||||||||||

| Total Revenues | $ | 8,354,428 | 36.3 | % | $ | 8,436,000 | 36.6 | % | $ | 6,250,106 | 27.1 | % | $ | 23,040,534 | 100 | % | ||||||||||||||||

The following table provides revenue percentage for each segment and category for the six months ended June 30, 2012. The total revenues increased by 11.9% comparing with the same period in 2011.

| Six Months Ended June 30, 2012 | ||||||||||||||||||||||||||||||||

| Segment 1: | % | Segment 2: | % | Segment 3: | % | Total: | % | |||||||||||||||||||||||||

| System Integration | $ | 16,761,401 | 100.0 | % | $ | 13,395,148 | 91.2 | % | $ | 10,117,883 | 93.6 | % | $ | 40,274,432 | 95.3 | % | ||||||||||||||||

| Hardware Products | $ | — | — | % | $ | 1,295,442 | 8.8 | % | $ | 691,972 | 6.4 | % | $ | 1,987,414 | 4.7 | % | ||||||||||||||||

| Software Products | $ | — | — | % | $ | — | — | % | $ | — | — | % | $ | — | — | % | ||||||||||||||||

| Total Revenues | $ | 16,761,401 | 39.7 | % | $ | 14,690,590 | 34.8 | % | $ | 10,809,855 | 25.5 | % | $ | 42,261,846 | 100 | % | ||||||||||||||||

Backlog and Pipeline for 2012

The Company’s backlog represents the amount of contract work remaining to be completed, that is, revenues from existing contracts and work in progress expected to be recorded in 2012 and onwards, based on the assumption that these projects will be completed on time according to the project schedules. As of June 30, 2012, the Company had a total backlog of $79.2 million, including $41.9 million in Segment 1, $12.2 million in Segment 2 and $25.1 million in Segment 3.

As of June 30, 2012, the Company expected potential projects in the pipeline with a total contract value of $152.2 million, of which approximately $89.7 million is in Segment 1, $23.1 million in Segment 2, and $39.4 million in Segment 3.

With a strong backlog, the Company anticipates that its revenues will reach a range between $103 million and $128 million, and its net income between $9.7 million and $12.1 million, in 2012.

Operational Results Overview and Business Trends

General

China experienced slower growth during the second quarter of 2012. To soften the impact of the lowered growth rate, China has made adjustments in government sponsored investments in infrastructures, which decreased market demand for our products and services. The weakened demand, combined with the increasing costs of financing, labor and raw materials, presented unprecedented challenges to our sales. However, the Company was able to secure a moderate growth under the circumstances.

| I-3 |

To address the slowing growth rate without compromising its environmental initiatives, the Chinese government recently issued several key environment development programs in fields such as water conservancy, energy conservation, urban water supply, water treatment and seawater desalination. At a macro level, the government has pushed through specific policies to loosen monetary constrains, to reduce taxes and to increase investment on key projects to stabilize the economic growth.

To address the challenges, the Company focused on its profitability through enhancing its cost efficiencies. On the other hand, it emphasized strategic developments in markets where its core technologies have a competitive advantage against its competitors. In the meantime, the Company continued its efforts to develop its overseas market shares in water and waste water treatment sector to optimize the revenue growth of its portfolio.

In general, the Company expects the market demand of the overall industry to continue its stable growth in the next few quarters. The company anticipates a moderate growth through maximizing its income and minimizing its costs and expenses.

Segment 1: Water, Wastewater Treatment and Municipal Infrastructure

During the second quarter, revenue from our WWTM segment decreased by 50.2% compared to the same period last year. The decline was primarily due to the delay in execution of the expansion phase of Ordos Water Treatment Plant and three India Bihar Sewage System projects. In the second quarter, we nearly completed the civil construction and equipment procurement for the expansion phase of the Ordos project, when partial equipment has been delivered to the project site and the equipment installation has started. The India Bihar project made some progress in the second quarter, nearly completing the investigation of proposed sewerage pipe network and sewage treatment plants, soil testing, pipeline design and engineering of sewerage treatment plants. However, the overall project fell behind schedule. Currently, we are undergoing negotiation and inquiry of subcontracting and materials procurement. For the Tianjin Airport Economic Zone Wastewater Treatment Plant expansion project, we delivered part of the equipment such as pumps and conducted preparation work on project site. The Canada Jasper Lodge water treatment project was completed for a trial run. In addition, we made a recent breakthrough by winning a water quality testing equipment procurement contract for Water Quality Testing Center of Zhongwei City, Ningxia. The contract value totaled $1.78 million. We expect more success in marketing and bidding for water and wastewater treatment projects in the domestic and oversea markets and we expect our WWTM segment to continue its solid growth in the upcoming quarters.

![]()

Pic-1 Initial Phase of Ordos Drinking Water Plant

![]()

Pic-2 Initial Phase of Ordos Drinking Water Plant

| I-4 |

![]()

Pic-3 Canada Fairmont Jasper Lodge UF Water Treatment System

Segment 2: Water Resources Management Systems and Engineering Services

During the second quarter, sales from our WRME segment experienced a growth of 264.5%, compared to the same period last year. The significant increase was mainly attributable to the implementation of flash flood and small river hydrologic monitoring projects awarded in the second quarter and the execution of projects awarded in previous quarters. In the second quarter, the order backlog for the WRME segment continued to increase. We won $8.6 million flash flood and small river hydrologic monitoring contracts in six Chinese provinces, of which 70% are completed and part of the completed projects are in the stage of customer testing and acceptance. In mid-July, we were awarded $8.06 million contracts in flash flood and small river hydrologic monitoring projects in ten Chinese provinces and municipality.

In the upcoming quarters, we anticipate strong performance from our flash flood and hydrologic monitoring offerings as a result of the growing market demand. We are also focusing on the implementation of awarded projects out of the growing backlog. In addition, we will pursue opportunities in new business sectors such as information system upgrading for irrigation systems in China and overseas markets. In that regard, we recently won contracts worth $1.3 million for agricultural water conservation irrigation systems in Yelaman Township, Xinjiang.

Segment 3: Industrial Pollution Control and Safety

Our IPCS segment recorded a 459.2% increase of revenue during the second quarter of 2012 over the same period last year. The increase was mainly due to the implementation of the Dawangdian Industrial Park Wastewater Treatment project, the Qatar Seawater Desalination Unit project and the Mexico Steel Plant Wastewater Treatment project. Following the award of wastewater treatment plant construction project for the Dawangdian Industrial Park we were awarded a $5.5 million contract for wastewater pipeline network construction for the Dawangdian Industrial Park. Currently, we have completed the specific design of the Dawangdian project and have commenced the pipeline construction and equipment procurement. For the Qatar project, we have completed the majority of detailed engineering for the seawater desalination unit. For the water treatment project for the Mexico steel plant, we have submitted the engineering drawing to the customer for review and approval. For Wuhan Natural Gas High-Pressure Pipeline Co., we have completed the equipment procurement and system design for phases 1 and 2 of the automated control system project and started construction. For the South Yolotan-Osman project in Turkmenistan, we have completed the design for the security component and material orders for communication equipment. Next quarter, we will continue to expand our IPCS business in the China market, particularly in the thermal seawater desalination and zero liquid discharge technologies, which are our core strengths in industrial wastewater treatment. We anticipate sales from the segment to continue steady growth.

Strategies for Growth

Segment 1: Water, Wastewater Treatment and Municipal Infrastructure

For the WWTM segment, we will reinforce our leading position and continue to strengthen our core compatibility as an EPC contractor and BTO provider for municipal water treatment projects. Specifically, we will continue to develop water and wastewater treatment business in domestic market, focusing mainly on the construction and retrofit of municipal water and wastewater treatment facilities in small- to medium-sized cities in Central and West China. We will select projects with favorable payment terms and maintain tight controls over costs. Overseas, we will continue municipal project development in South Asia and North America to further diversify our customer base and optimize our revenue portfolio. In terms of our products, our main focus in the following quarters will be on research and development of membrane technology and products in municipal water and wastewater treatment field. To that end, we actively seek partnerships with leading European membrane products manufacturers and conduct research and development on the membrane treatment technology. Part of our research and development and manufacturing facilities in Baoding have started operation. Moreover, we will continue our domestic market development for forward osmosis membrane technology and explore the feasibility of applying forward osmosis membrane technology in industrial use. Lastly, we are looking at potential domestic acquisition opportunities emphasizing on proprietary membrane technologies. As a whole, we plan to further enhance our water and wastewater treatment technology by independent research and development, cooperative development, and mergers and acquisitions.

| I-5 |

Segment 2: Water Resources Management Systems and Engineering Services

For the WRME business segment, we will continue to expand our market share in flash flood and small river hydrologic monitoring. We will closely monitor market demands driven by the government policies and fund allocation. We have launched market survey and preparing several water resources management programs such as national water resources monitoring program and irrigation area information system program. We intend to capture a larger market share by partnering with international leading water conservancy information solution providers and importing competitive technologies from overseas. In addition, we are expanding the WRME business to the South Asian market. Starting in the second quarter of fiscal 2012, we have participated in several project biddings there.

Segment 3: Industrial Pollution Control and Safety

In the IPCS segment, we are refocusing on domestic market development. We conducted pilot testing of specialties industrial wastewater ZLD and thermal seawater desalination technologies and accelerated the commercialization of core technologies in the China market, prioritizing especially on the petrochemical industry. We believe higher effluent standards emphasizing on resource recovery and lower energy consumption present vast market opportunities. Moreover, we continue to explore the application of membrane technology in industrial wastewater treatment, through research and development and introduction of the technology to municipal governments. Overseas, we continue to undertake cutting-edge projects of industrial wastewater ZLD and thermal seawater desalination. Our competitive pricing structure, reliable operation and lower energy consumption enable us to compete effectively with international peers.

Funding for Continuous Growth

Funding is critical to maintaining our growth momentum, especially as we explore potential projects using the BTO business model. We are actively working with local Chinese banks to secure financial support. We renewed the credit line with Bank of Hangzhou totaling $12.7 million. In September 2011, we secured a credit line of $9.6 million from CITIC Bank. We also secured credit lines of $6.4 million and $2.4 million from ICBC Bank in February 2012 in June 2012, respectively, the latter of which was currently used to fund our payment to suppliers. Our total credit line from ICBC therefore amounted to 8.8 million. These credit lines provide us the liquidity to expand and grow our operations in a non-dilutive manner, to increase our financial flexibility and to optimize the efficiency of our capital structure. We also explore other project finance approaches to dovetail our BTO business model.

Competition

We operate in a highly competitive industry characterized by rapid technological development and evolving industrial standards. Given the stimulus initiatives in China, we expect the competition to intensify as more companies enter the market, notwithstanding relatively high barriers to entry in the need for technical expertise and funding.

We compete primarily on the basis of customer recognition, industry reputation, product innovation and a competitive pricing structure. Through mergers and acquisitions, we are able to offer advanced technologies at an attractive price when competing with domestic and international rivals. Due to our nationwide distribution and customer service network and knowledge of the local market, we enjoy an advantage in China over international competitors who typically appoint only one distributor in the Chinese market responsible for selling and servicing their products. In addition, we provide a more comprehensive set of products than most of our international or local competitors. If competition in the industry intensifies, we may see these advantages decrease or disappear. In order to maintain and enhance our competitive advantage, we must continue to focus on competitive pricing, technological innovation, market trends, as well as improvement in proprietary products.

Although we believe our competitive strengths provide us with advantages over many of our competitors, some of our international rivals have better brand recognition, longer operating histories, longer or more established relationships with their customers, stronger research and development capabilities and greater marketing budgets and other resources. Most of our international competitors are substantially larger and have greater access to capital than we do. Some of our domestic competitors have stronger customer bases, better access to government resources and stronger industry-based background. In areas such as the ZLD solution and seawater desalination, we anticipate fierce competition from multi-national competitors.

| I-6 |

Principal Suppliers

Our suppliers vary from project to project. Often, they are specifically appointed by the clients. Most of the materials or equipment we purchase are not unique and are easily available in the market. The prices for those purchases, although increasing, are relatively consistent and predictable. A specific supplier might constitute a significant percentage of our total purchases at a certain time for a large contract. The dependence on a specific supplier usually ends when the project is completed. We do not rely on any single supplier in the long term.

As planned, we have deployed ERP modules to centralize our supply chain management for some of our subsidiaries. In addition, we are furthering the deployment of the ERP modules to integrate all subsidiaries.

Customers and Marketing/Distribution Methods

We operate on a project basis, and this particular nature does not usually allow us to create a long-term relationship with our customers. We negotiate with various government agencies, municipalities, industrial enterprises and/or their general contractors in order to secure and undertake our various contracts. Our major customers usually account for a certain percentage of our total sales. Our top five customers collectively represented approximately 56.3% and 86.7% of our total revenue for the three months ended June 30, 2012 and 2011, respectively. Although we are dependent on our large clients to a certain degree, unlike other commercial businesses, collectability of accounts receivables are relatively secure because our client base consists primarily of government agencies or large state-owned enterprises.

Patents and Proprietary Rights

As of June 30, 2012, we owned 11 product patents and 39 software copyrights.

Government Regulation and Approval

As described in greater detail above in the discussion of our business segments, government policies and initiatives in the various industries we serve have a considerable impact on our potential for growth in domestic market. We generally undertake projects for government entities and enterprises, and must complete the projects in accordance with the terms of the contracts in which we enter with those entities.

Employees

As of June 30, 2012, we had a total headcount of 446, of which 233 (52%) were in technical support and project management, 97 (22%) in sales, 13 (3%) in research and development, 44 (10%) in finance, and the remaining 59 (13%) in general and administrative functions. The increase of our headcount was mainly in the project management department, which grew by 69 during the second quarter. In the general and administrative department, headcount decreased by 27. In the sales department, headcount increased by 11. In the research and development department, headcount was the same as that on March 31, 2012. Total headcount increased by 56 from that on March 31, 2012. Our teams are very stable compared to our peers.

Research and Development

We focus our research and development efforts on improving our development efficiency and the quality of our products and services. Some of our technical support team regularly participate in research and development programs. There are five major on-going software research and development projects and one hardware research and development project. These projects are expected to be completed in 2012.

As our research and development base, Tianjin Baoding Environmental Technology Co., Ltd. (“Baoding”) focuses on technology development, software development, pilot testing, manufacturing and pre-installation/pre-assembly of our proprietary products. The Baoding research, development and production facility construction officially started in June 2011. Part I of phase one of the construction is for odor control system manufacturing and automatic control box assembly workshops, which has been completed. The main construction of Part II of phase one has been completed in August 2012, and is expected to be in use by the end of 2012. Phase two and phase three are scheduled to be completed by the end of 2013.

Properties

Our primary office location is the 15th and 16th Floor of Tower B, Renji Plaza, 101 Jingshun Road, Chaoyang District, Beijing. The rental space for the two floors is 908 square meters for the 15th floor and 986 square meters for the 16th floor. The lease contract for this location is from September 1, 2010 to August 31, 2013. We also have a 1,300 square meter rental office in Tianjin, located at 4th Floor, Kaide A Complex, 7 Rongyuan Road, Huayuan Property Management Zone, Tianjin, with a rental term that runs until December 2014. In April 2012, we rented a 1,1398 square meter office in Beijing to relocate our subsidiary Yanyu, located at 10th Floor of Tower B, Baoneng Center, Futong East Road, Chaoyang District, Beijing, with a rental term that runs until March 2015. In addition, we have three other rental office locations in various areas of Beijing, for which the lease contracts are to expire at different points in time during the third quarter.

| I-7 |

Baoding, one of the Company’s subsidiaries, is located at West Tianbao Road, Baodi Economic Development Zone in Tianjin. The subsidiary occupies an area of 158,954 square meters and has a 50-year land use right starting on January 18, 2011.

Results of Operations

Overview for the Three and Six Months Ended June 30, 2012 and 2011

Our operating revenues are primarily derived from system design and integration, hardware product design and manufacturing and sales. Our second quarter results reflected stable growth. Highlights of our financial results during the three months ended June 30, 2012 include:

| · | Total revenues increased to $23,040,534 in the second quarter of 2012, an increase of $2,838,647, or 14.1%, from $20,201,887 in the same period of 2011. This increase is primarily attributable to the following factors: |

| o | Systems integration revenue increased from $19,883,553 in the second quarter of 2011 to $21,741,770 in the same period in 2012, an increase of $1,858,217, or 9.3%. |

| o | Hardware products revenue totaled $1,298,764 in the second quarter of 2012, an increase of $980,430, or 308.0%, from $318,334 in the second quarter of 2011. |

| · | Total cost of revenues increased by $2,318,799 from $14,897,669 in the second quarter of 2011 to $17,216,468 in the second quarter of 2012, a 15.6% increase. This increase is attributable to the increase in system integration cost by $1,986,382 and the increase in hardware product cost by $332,417. |

| · | Total operating expenses were $4,194,927 for the second quarter of 2012, or 18.2% of total revenues, compared with $2,381,341, or 11.8%, of total revenues, in the same period of 2011. This represents an increase of $1,813,586, or 76.2%. |

| · | Operating income decreased to $1,629,139 in the second quarter of 2012, by 44.3%, from $2,922,877 in the second quarter of 2011, representing 7.1% and 14.5% of total revenues in the second quarter of 2012 and 2011, respectively. |

| · | Net income attributable to TRIT decreased to $1,370,887, or by 22.2%, for the second quarter of 2012, from $1,761,688 for the second quarter of 2011. |

The following are the operating results for the three months ended June 30, 2012 and 2011:

| Three Months Ended June 30, 2012 ($) | % of Sales | Three Months Ended June 30, 2011 ($) | % of Sales | Change ($) | Change (%) | |||||||||||||||||||

| Revenue | 23,040,534 | 100.0 | % | 20,201,887 | 100.0 | % | 2,838,647 | 14.1 | % | |||||||||||||||

| Cost of Revenues | 17,216,468 | 74.7 | % | 14,897,669 | 73.7 | % | 2,318,799 | 15.6 | % | |||||||||||||||

| Selling and Marketing Expenses | 935,853 | 4.1 | % | 472,150 | 2.3 | % | 463,703 | 98.2 | % | |||||||||||||||

| General and Administrative Expenses | 3,247,546 | 14.1 | % | 1,882,432 | 9.3 | % | 1,365,114 | 72.5 | % | |||||||||||||||

| Research and Development | 11,528 | 0.1 | % | 26,759 | 0.1 | % | (15,231 | ) | (56.9 | )% | ||||||||||||||

| Total Operating Expenses | 4,194,927 | 18.2 | % | 2,381,341 | 11.8 | % | 1,813,586 | 76.2 | % | |||||||||||||||

| Operating Income | 1,629,139 | 7.1 | % | 2,922,877 | 14.5 | % | (1,293,738 | ) | (44.3 | )% | ||||||||||||||

| Other Expenses | (34,350 | ) | (0.1 | )% | (93,067 | ) | (0.5 | )% | 58,717 | (63.1 | )% | |||||||||||||

| Income before Provision for Income Taxes | 1,594,789 | 6.9 | % | 2,829,810 | 14.0 | % | (1,235,021 | ) | (43.6 | )% | ||||||||||||||

| Provision for Income Taxes | 287,062 | 1.2 | % | 439,423 | 2.2 | % | (152,361 | ) | (34.7 | )% | ||||||||||||||

| Net Income | 1,307,727 | 5.7 | % | 2,390,387 | 11.8 | % | (1,082,660 | ) | (45.3 | )% | ||||||||||||||

| Less: Net (Loss) Income Attributable to Noncontrolling Interests | (63,160 | ) | (0.3 | )% | 628,699 | 3.1 | % | (691,859 | ) | (110.0 | )% | |||||||||||||

| Net Income Attributable to TRIT | 1,370,887 | 5.9 | % | 1,761,688 | 8.7 | % | (390,801 | ) | (22.2 | )% | ||||||||||||||

Performance highlights for the six months ended June 30, 2012 include:

| · | Total revenues increased to $42,261,846 from $37,755,098, an increase of $4,506,748, or 11.9%. |

| · | Cost of revenues increased to $31,220,280 in the six-month period in 2012 from $27,440,700 for the same period last year, an increase of $3,779,580, or 13.8%. |

| I-8 |

| · | Total operating expenses increased to $7,956,150 in the first six months of 2012 from $4,802,293 in the same period 2011, an increase of $3,153,857, or 65.7%. The most significant contributor to this increase is general and administrative expenses, which increased by $2,151,680, or 54.5%, from the six-month period in 2011. |

| · | Operating income for the six months ended June 30, 2012 was $3,085,416, or 7.3%, of the total revenues, compared to $5,512,105 for the same period last year, representing a decrease of $2,426,689, or 44.0%. |

| · | Net income attributable to TRIT was $2,809,012, or 6.6% of total revenues, a decrease of $651,657, or 18.8%, from $3,460,669 for the same period last year. |

The following are the operating results for the six months ended June 30, 2012 and 2011:

| Six Months Ended June 30, 2012 ($) | % of Sales | Six Months Ended June 30, 2011 ($) | % of Sales | Change ($) | Change (%) | |||||||||||||||||||

| Revenue | 42,261,846 | 100.0 | % | 37,755,098 | 100.0 | % | 4,506,748 | 11.9 | % | |||||||||||||||

| Cost of Revenues | 31,220,280 | 73.9 | % | 27,440,700 | 72.7 | % | 3,779,580 | 13.8 | % | |||||||||||||||

| Selling and Marketing Expenses | 1,774,846 | 4.2 | % | 786,323 | 2.1 | % | 988,523 | 125.7 | % | |||||||||||||||

| General and Administrative Expenses | 6,100,906 | 14.4 | % | 3,949,226 | 10.5 | % | 2,151,680 | 54.5 | % | |||||||||||||||

| Research and Development | 80,398 | 0.2 | % | 66,744 | 0.2 | % | 13,654 | 20.5 | % | |||||||||||||||

| Total Operating Expenses | 7,956,150 | 18.8 | % | 4,802,293 | 12.7 | % | 3,153,857 | 65.7 | % | |||||||||||||||

| Operating Income | 3,085,416 | 7.3 | % | 5,512,105 | 14.6 | % | (2,426,689 | ) | (44.0 | )% | ||||||||||||||

| Other Income (expenses) | 256,555 | 0.6 | % | (97,134 | ) | (0.3 | )% | 353,689 | (364.1 | )% | ||||||||||||||

| Income before Provision for Income Taxes | 3,341,971 | 7.9 | % | 5,414,971 | 14.3 | % | (2,073,000 | ) | (38.3 | )% | ||||||||||||||

| Provision for Income Taxes | 601,555 | 1.4 | % | 845,059 | 2.2 | % | (243,504 | ) | (28.8 | )% | ||||||||||||||

| Net Income before Allocation to Noncontrolling Interests | 2,740,416 | 6.5 | % | 4,569,912 | 12.1 | % | (1,829,496 | ) | (40.0 | )% | ||||||||||||||

| Less: Net (Loss) Income Attributable to Noncontrolling Interests | (68,596 | ) | (0.2 | )% | 1,109,243 | 2.9 | % | (1,177,839 | ) | (106.2 | )% | |||||||||||||

| Net Income Attributable to TRIT | 2,809,012 | 6.6 | % | 3,460,669 | 9.2 | % | (651,657 | ) | (18.8 | )% | ||||||||||||||

Revenues

Our revenues are subject to value added tax (“VAT”), business tax, urban maintenance and construction tax and additional education surcharges. Among the above taxes, VAT has been deducted from the calculation of revenues.

Our total revenues for the second quarter of 2012 were $23,040,534, an increase of $2,838,647, or 14.1%, compared with the same period last year. This increase is primarily attributable to an increase in the system integration category, from $19,883,553 in the second quarter of 2011 to $21,741,770 in the same period for 2012, or an increase of 9.3%. Revenue from Segment 1 constituted 36.3% of total revenues. Revenue from Segment 2 totaled $8,436,000, or 36.6% of total revenues. Revenue from Segment 3 totaled $6,250,106, constituting 27.1% of total revenues for the second quarter, mostly in the system integration category.

For the six months ended June 30, 2012, total revenues reached $42,261,846, of which 39.7%, or $16,761,401, was from Segment 1, 34.8%, or $14,690,590, was from Segment 2, and 25.5%, or $10,809,855, was from Segment 3. The system integration category constituted 95.3% of the total revenue, or $40,274,432. Hardware product sales revenue totaled $ 1,987,414, constituting the remaining 4.7%.

Cost of Revenues

Cost of revenues is based on total actual costs incurred plus estimated costs to completion applied to the percentage of completion as measured at different stages. It includes material costs, equipment costs, transportation costs, processing costs, packaging costs, quality inspection and control, outsourced construction service fees and other costs that directly relate to the execution of the services and delivery of projects. Cost of revenues also includes freight charges, purchasing and receiving costs and inspection costs when they are incurred.

Total cost of revenues was $17,216,468 for the second quarter of 2012, an increase of $2,318,799, or 15.6%, from $14,897,669 in the second quarter of 2011. The system integration category, which was the largest contributor to the revenue increase, was also the largest contributor to the increase in cost of revenues, totaling $16,608,958. The increase in cost of revenues in the system integration category was $1,986,382, or 13.6%, from $14,622,576 in the second quarter of 2011 to $16,608,958 in the second quarter of 2012. The increase is mainly a result of the increase in total revenues.

| I-9 |

Total cost of revenues for the six months ended June 30, 2012 was $31,220,280, an increase of $3,779,580, or 13.8%, compared to $27,440,700 for the same period in 2011. The cost for system integration category, totaling $30,193,175, had an increase of $3,919,850, or 14.9%, from $26,273,325 in the same period 2011, while the total hardware products cost decreased from $1,167,375 in the same period last year to $1,027,105.

Our gross margin decreased from 26.3% in the second quarter of 2011 to 25.3% in the second quarter of 2012. The most important reason for this decrease is the lower gross margin of the Indian project at 20%, which constituted 17.3% of our total revenues for this quarter. We accepted the project despite its lower gross margin as a first step to opening the India market.

The gross margin for the six months ended June 30, 2012 and 2011 was 26.1% and 27.3%, respectively.

Our strategy is to carefully choose higher-margin projects. In the next two to three years, we will continue to look for ways to minimize the negative impact on our gross margin through optimizing product and system design, leveraging bargaining power in procurement, and exploring supply chain financing and local equipment sourcing.

Selling and Marketing Expenses

Selling and marketing expenses consist primarily of compensation, marketing, travel and business entertainment expenses. In the second quarter of 2012, total selling and marketing expenses increased by $463,703, or 98.2%, from $472,150 in the second quarter of 2011 to $935,853 in the same period of 2012. This was a result of an increase in compensation-related expenses of $217,226, or 121.3%, from $179,065 in the second quarter of 2011 to $396,291 in the same period of 2012, an increase in other selling expenses of $120,742, or 95.5%, from $126,430 in the second quarter of 2011 to $247,172 in the same period of 2012, an increase in travel expenses of $112,856, or 162.4%, from $69,501 in the second quarter of 2011 to $182,357 in the same period of 2012, and an increase in entertainment expenses of $12,879, or 13.3%, from $97,154 in the second quarter of 2011 to $110,033 in the same period of 2012.

The selling and marketing expenses for the six months ended June 30, 2012 totaled $1,774,846, an increase of $988,523, or 125.7%, from $786,323 for the same period last year. This increase was mainly due to headcount increase in sales and rapid geographic expansion. Compensation-related costs increased from $294,890 for the six-month period ended June 30, 2011 to $708,791 for the same period this year, an increase of $413,901, or 140.4%. Travel expenses increased from $135,772 for the six-month period ended June 30, 2011 to $239,260 for the same period this year, an increase of $103,488, or 76.2%. Other selling expenses increased from $207,909 for the six-month period ended June 30, 2011 to $608,550 for the same period this year, an increase of $400,641, or 192.7%. Consisting mainly of employee benefits, business promotion, office expenses, vehicle maintenance and bidding expenses, the significant increase in other selling and marketing expenses came mainly from business promotion and bidding expenses. Entertainment expenses increased by $70,494, or 47.7%, from $147,751 in the first half of 2011 to $218,245 for the same period of 2012.

Selling and marketing expenses for the three months and six months ended June 30, 2012 took up approximately 4.1% and 4.2% of total revenues, respectively. We anticipate its continued increase during the second half of the year.

General and Administrative Expenses

General and administrative expenses consist primarily of compensation costs, rental expenses, professional fees, and other overhead expenses. General and administrative expenses increased by $1,365,114, or 72.5%, from $1,882,432 in the second quarter of 2011 to $3,247,546 in the second quarter of 2012. Of this increase, $188,085 was for officers’ salaries, which increased from $180,415 in the second quarter of 2011 to $368,500 in the second quarter of 2012. Salaries for mid-level management, technical support team, and other office staff increased by $159,148, or 33.2%, from $479,400 in the second quarter of 2011 to $638,548 in the second quarter of 2012. Of other human resource expenses, endowment and social insurance increased by 14.3% and 159.2%, respectively, to $62,497 and $124,668, in the second quarter of 2012. Rent increased by $103,480, or 58.7%, from $176,326 in the second quarter of 2011 to $279,806 in the second quarter of 2012 due to office relocation. Professional fees increased by $150,688, or 90.2%, from $167,151 to $317,839, which was mainly for consulting and legal services. Amortization of intangible assets and software increased by $89,125, from $124,811 in the second quarter of 2011 to $213,936 in the same period of 2012. This increase was due to the purchase of certain software and intangible assets in our acquired subsidiaries and the amortization of land use rights. Depreciation expense increased by $23,891, or 40.4%, from $59,204 in the second quarter of 2011 to $83,095 in the second quarter of 2012. Other general and administrative expenses increased by $566,331, or 95.6%, from $592,326 to $1,158,657 in the second quarter of 2012, including mainly office expenses, utilities, travel, communication, other services and option expense.

| I-10 |

In the first six months of 2012, we strengthened our administrative support, including human resources and finance functions. Many highly qualified professionals joined us to support the revenue growth. Total general and administrative expenses for the six months ended June 30, 2012 was $6,100,906, an increase of $2,151,680, or 54.5%, from $3,949,226 for the same period last year. Of this increase, $590,431 was for compensation-related costs. Of other human resource expenses, endowment and social insurance increased by 42.0% and 102.9% respectively, to $44,842 and $131,885, in the first six months of 2012. Rent increased by $167,704, or 46.6%, from $359,613 in the first six months of 2011 to $527,317 in the same period of 2012. Professional fee increased by $220,565, or 62.8%, from $351,037 in the first six month of 2011 to $571,602 for the same period of 2012, mainly due to consulting services exploring new business opportunities. Amortization and depreciation increased by $158,048 and $38,674, or 58.6% and 33.4%, respectively. Other general and administrative overhead increased by $799,530 for the first six months of 2012, or 63.5%, compared to the same period last year.

General and administrative expenses for the three months and six months ended June 30, 2012 took up approximately 14.1% and 14.4% of total revenues. We anticipate it to continue its increase but at a lower speed in the future.

Provision for Income Tax

We provide for deferred income taxes using the asset and liability method. Under this method, we recognize deferred income taxes for tax credits, net operating losses available for carry-forwards and significant temporary differences. We classify deferred tax assets and liabilities as current or non-current based upon the classification of the related asset or liability in the financial statements or the expected timing of their reversal if they do not relate to a specific asset or liability. We provide a valuation allowance to reduce the amount of deferred tax assets if it is considered more likely than not that some portion or all of the deferred tax assets will not be realized.

Our operations are subject to income and transaction taxes of China since most of our business activities take place there. Significant estimates and judgments are required in determining our provision for income taxes. Some of these estimates are based on interpretations of existing tax laws or regulations, as well as predictions related to future changes in these laws and regulations. The ultimate amount of tax liability may be uncertain as a result. We do not anticipate any events which could change these uncertainties.

We, including our subsidiaries and VIEs, are subject to income taxes on an entity level for income arising in or derived from the tax jurisdictions in which each entity is domiciled. According to the New Enterprise Income Tax Law in China, the unified enterprise income tax (“EIT”) rate is 25%. However, five of our subsidiaries are eligible for certain favorable tax policies for being high-tech companies.

| EIT | ||||||||

| Three Months Ended June 30, | ||||||||

| 2012 | 2011 | |||||||

| % | % | |||||||

| TTB | 15 | 7.5 | ||||||

| BSST | 15 | 15 | ||||||

| Yanyu | 15 | 15 | ||||||

| Tranhold | 25 | 25 | ||||||

| TTA | 25 | 25 | ||||||

| Baoding | 15 | 15 | ||||||

| Yuanjie | 15 | — | ||||||

| Buerjin | 25 | — | ||||||

| Xushui | 25 | — | ||||||

| Consolidated Effective EIT | 18 | 16 | ||||||

The favorable income tax treatment for TTB at 7.5% expired at the end of 2011. Thereafter, the EIT rate became 15%, since TTB continues to qualify as a high-tech company. The provision for income tax for the second quarter of 2012 was $287,062.

We have not recorded tax provision for U.S. tax purposes as they have no assessable profits arising in or derived from the United States and we intend to permanently reinvest accumulated earnings in the PRC operations.

Net Income before Income Taxes

In the quarter ended June 30, 2012, our net income before provision for income taxes was $1,594,789, a decrease of $1,235,021, or 43.6%, compared to $2,829,810 in the same period in 2011. Our provision for income taxes decreased by $152,361, from $439,423 in the second quarter of 2011 to $287,062 in the same period of 2012. In the second quarter of 2012, net income attributable to shareholders of TRIT was $1,370,887, a decrease of $390,801, or 22.2%, from $1,761,688 for the same period of 2011.

| I-11 |

For the six months ended June 30, 2012, our net income before provision for income taxes decreased by 38.3%, or $2,073,000, from $5,414,971 for the same period last year to $3,341,971. The provision for income taxes decreased by $243,504, or 28.8%, from $845,059 to $601,555. The net income attributable to the shareholders of TRIT was $2,809,012, a decrease of $651,657, or 18.8%, from $3,460,669 for the same period in 2011. The net income decreased because revenues did not increase whereas expenses grew quickly to meet increasing business demands. Moreover, we granted options in the second quarter which led to option expense of $0.35 million.

Liquidity and Capital Resources

As highlighted in the consolidated statements of cash flows, our liquidity and available capital resources are impacted by four key components: (i) cash and cash equivalents, (ii) operating activities, (iii) financing activities, and (iv) investing activities.

Consolidated cash flows for the six months ended June 30, 2012 and 2011 were as follow:

| Six Months Ended June 30, | ||||||||||||

| 2012 ($) | 2011($) | Change($) | ||||||||||

| Net Cash (Used in) Operating Activities | (8,297,972 | ) | (10,385,697 | ) | 2,087,725 | |||||||

| Net Cash Provided by (Used in) Investing Activities | 106,389 | (2,914,949 | ) | 3,021,338 | ||||||||

| Net Cash Provided by Financing Activities | 5,409,603 | 2,524,703 | 2,884,900 | |||||||||

| Effects of Exchange Rate Changes on Cash and Cash Equivalents | 408,797 | 499,908 | (91,111 | ) | ||||||||

| Net Decrease in Cash and Cash Equivalents | (2,373,183 | ) | (10,276,035 | ) | 7,902,852 | |||||||

| Cash and Cash Equivalents, Beginning of Period | 11,935,746 | 23,394,995 | (11,459,249 | ) | ||||||||

| Cash and Cash Equivalents, End of Period | 9,562,563 | 13,118,960 | (3,556,397 | ) | ||||||||

Cash and Cash Equivalents

As of June 30, 2012, our cash and cash equivalents amounted to $9,562,563. The restricted cash as of June 30, 2012 and December 31, 2011 amounted to $4,278,156 and $4,629,878, respectively, which are not included in the total amount of cash and cash equivalents. The restricted cash consisted of deposits as collaterals for the issuance of letters of credit. Our subsidiaries that own these deposits do not have material cash obligations to any third parties. Therefore, the restriction does not impact our liquidity.

Operating Activities

Net cash used in operating activities was $8,297,972 for the six months ended June 30, 2012, compared with $10,385,697 in the same period 2011. The decrease of $2,087,725 in operating cash outflow was mainly attributable to our rapid growth and aggressive expansion in new markets in forms of accounts receivables and unbilled receivables. Net accounts receivable increased from $19.9 million on December 31, 2011 to $23.0 million on June 30, 2012, an increase of $3.1 million. Unbilled receivables increased from $7.3 million on December 31, 2011 to $21.0 million on June 30, 2012, an increase of $13.7 million. Prepayments to suppliers and subcontractors increased from $4.9 million on December 31, 2011 to $8.7 million on June 30, 2012, an increase of $3.7 million. Deposits on projects decreased from $1.2 million on December 31, 2011 to $1.1 million on June 30, 2012, a decrease of $0.1 million.

| June 30, 2012 ($) (unaudited) | December 31, 2011 ($) | Change ($) | Change (%) | |||||||||||||

| Cash | 9,562,563 | 11,935,746 | (2,373,183 | ) | (19.9 | ) | ||||||||||

| Restricted cash | 1,723,780 | 2,087,920 | (364,140 | ) | (17.4 | ) | ||||||||||

| Accounts and notes receivable | 23,899,980 | 20,507,146 | 3,392,834 | 16.5 | ||||||||||||

| Allowance for doubtful accounts | (859,405 | ) | (619,062 | ) | (240,343 | ) | 38.8 | |||||||||

| Accounts and notes receivable, net | 23,040,575 | 19,888,084 | 3,152,491 | 15.9 | ||||||||||||

| Unbilled revenue | 21,011,695 | 7,254,830 | 13,756,865 | 189.6 | ||||||||||||

| Prepayments to suppliers and subcontractors | 8,654,805 | 4,908,697 | 3,746,108 | 76.3 | ||||||||||||

| Deposits on projects | 1,053,579 | 1,212,691 | (159,112 | ) | (13.1 | ) | ||||||||||

Investing Activities

Net cash provided by investing activities was $106,389 during the six months ended June 30, 2012, an increase of $3,021,338 from net cash used in investing activities of $2,914,949 in the same period of 2011. This increase was mainly due to the collection of restricted cash and collection of loans to third-party companies.

| I-12 |

Financing Activities

The cash provided by financing activities was $5,409,603 in the six months ended June 30, 2012, compared to $2,524,703 in the same period of 2011. The increase was due to increased bank borrowings.

Effect of Exchange Rate Changes on Cash and Cash Equivalents

Net cash gain due to currency exchange was $408,797 in the six months ended June 30, 2012, a decrease of $91,111 compared to that of $499,908 in the same period of 2011.

Restricted Net Assets

Our ability to pay dividends is primarily dependent on receiving distributions of funds from our subsidiaries, VIEs and other affiliates entities, which is restricted by certain regulatory requirements. Relevant Chinese statutory laws and regulations permit payments of dividends by our Chinese affiliates only out of their retained earnings, if any, as determined in accordance with PRC accounting standards and regulations. In addition, our PRC affiliates are required to set aside at least 10% of their after-tax profit after deducting any accumulated deficit based on PRC accounting standards each year to our general reserves until the accumulated amount of such reserves reach 50% of our registered capital. These reserves are not distributable as cash dividends. Our off-shore subsidiaries, TIS and Tri-Tech International Investment, Inc. (“TTII”), do not have material cash obligations to third parties. Therefore, the dividend restriction does not impact our liquidity. There is no significant difference between accumulated profit calculated pursuant to PRC accounting standards and that pursuant to U.S. GAAP. As of June 30, 2012 and December 31, 2011, restricted retained earnings were $1,866,994 for both, and restricted net assets were $4,446,696 and $4,553,729, respectively. Unrestricted retained earnings as of June 30, 2012 and December 31, 2011 were $22,491,398 and $19,682,386, respectively, which were the amounts available for distribution in the form of dividends or for reinvestment.

Working Capital and Cash Flow Management

As of June 30, 2012, our working capital was $8,920,490, with current assets totaling $75,746,975 and current liabilities totaling $66,826,485. Of the current assets, cash and cash equivalents was $9,562,563.

However, we may require additional cash to undertake larger projects or to complete strategic acquisitions in the future. In the event our current capital is insufficient to fund these and other business plans, we may take the following actions to meet such working capital needs:

| · | We may look into the possibility of optimizing our funding structure by obtaining short- and/or long-term debt through commercial loans. We are actively exploring opportunities with major Chinese banks, such as ICBC Bank, CITIC Bank, Hangzhou Bank and CMBC Bank we expect to acquire additional lines of credit and tap into other financing channels to take on more projects in the future. Other financing instruments into which we are currently looking include supply chain financing, project financing, trust fund financing, commercial loan and capital leasing. |

| · | We may improve our collection of accounts receivable. Most of our clients are central, provincial and local governments. We believe that our clients are in good financial conditions. Therefore, we expect good collectability from relatively high accounts receivables. The accounts receivable collection should catch up with our rapid growth in the near future. Given the high interest rate on unpaid contract price for long-term projects, it is possible that some clients may choose to pay before interests start to accrue. |

Segment Information

We have three reportable operating segments. The segments are grouped according to the types of goods and services provided and the types of clients that use such goods and services. Total sales and costs are divided among these three segments. We assess each segment’s performance based on net revenue and gross profit on contribution margin.

Segment 1: Water, Wastewater Treatment and Municipal Infrastructure

The following are the operating results for the three months ended June 30, 2012 and 2011 for Segment 1:

| I-13 |

Three months ended June 30,

| 2012 ($) | 2011($) | Change ($) | Change (%) | ||||||||

| Revenues | 8,354,428 | 16,769,633 | (8,415,205 | ) | (50.2 | )% | |||||

| Cost of Revenues | 6,327,955 | 12,589,753 | (6,261,798 | ) | (49.7 | )% | |||||

| Operating Expenses: | |||||||||||

| Selling and Marketing Expenses | 222,521 | 143,878 | 78,643 | 54.7 | % | ||||||

| General and Administrative Expenses | 1,389,852 | 1,196,760 | 193,092 | 16.1 | % | ||||||

| Research and Development | 6,167 | 7,936 | (1,769 | ) | (22.3 | )% | |||||

| Total Operating Expenses | 1,618,540 | 1,348,574 | 269,966 | 20.0 | % | ||||||

| Other Income (Expenses) | 100,754 | (34,363 | ) | 135,117 | (393.2 | )% | |||||

| Income before Provision for Income Taxes | 508,687 | 2,796,943 | (2,288,256 | ) | (81.8 | )% |

Revenues for Segment 1 were $8,354,428 for the three months ended June 30, 2012, a decrease of $8,415,205, or 50.2%, from $16,769,633 in the same period of 2011. This decrease was mainly attributable to the Ordos drinking water plant project, on which we recognized revenue of $16 million in the second quarter of 2011 and $1.9 million in the second quarter of 2012. Although we recognized revenue of $3.98 million on the Indian project in the second quarter of 2012, the revenue increase from the Indian project did not entirely offset the revenue decrease from Ordos. Revenue from segment 1 is expected to increase next quarter.

Cost of revenues for Segment 1 was $6,327,955 in the second quarter of 2012, a decrease of $6,261,798, or 49.7%, from that of $12,589,753 in the second quarter of 2011. As the Company recognizes revenue following the percentage-of-completion method, measured by different stages of completion, the decrease in cost of revenues was mainly due to the recognized completion stages of our projects during the periods.

Total operating expenses in Segment 1 were $1,618,540, an increase of $269,966, or 20.0%, compared with $1,348,574 in the second quarter of 2011. The selling and marketing expenses increased from $143,878 in the second quarter of 2011 to $222,521 in the same period of 2012, an increase of $78,643, or 54.7%. The increase was mainly due to the increase in headcount and travel expenses. The general and administrative expenses for the second quarter of 2012 were $1,389,852, an increase of $193,092, or 16.1%, compared with $1,196,760 for the same period in 2011. The increase was caused by increases in salaries, rent and professional service expenses.

Other income was $100,754 in the second quarter of 2012, a $135,117 increase compared to other expense of $34,363 in the same period of 2011. The increase was mainly due to unrecognized financing income in the second quarter of 2012.

Income before provision for income taxes was $508,687 in the quarter ended June 30, 2012, a decrease of $2,288,256, or 81.8%, from that of $2,796,943 in the same period of 2011.

The following are the operating results for the six months ended June 30, 2012 and 2011 for Segment 1:

Six months ended June 30,

| 2012 ($) | 2011($) | Change ($) | Change (%) | ||||||||

| Revenues | 16,761,401 | 29,674,019 | (12,912,618 | ) | (43.5 | )% | |||||

| Cost of Revenues | 12,252,219 | 22,211,750 | (9,959,531 | ) | (44.8 | )% | |||||

| Operating Expenses: | |||||||||||

| Selling and Marketing Expenses | 448,147 | 252,935 | 195,212 | 77.2 | % | ||||||

| General and Administrative Expenses | 2,920,267 | 1,937,901 | 982,366 | 50.7 | % | ||||||

| Research and Development | 11,918 | 7,936 | 3,982 | 50.2 | % | ||||||

| Total Operating Expenses | 3,380,332 | 2,198,772 | 1,181,560 | 53.7 | % | ||||||

| Other Income (Expenses) | 448,169 | (40,016 | ) | 488,185 | (1,220.0 | )% | |||||

| Income before Provision for Income Taxes | 1,577,019 | 5,223,481 | (3,646,462 | ) | (69.8 | )% |

In Segment 1, revenues were $16,761,401 for the six months ended June 30, 2012, a decrease of $12,912,618, or 43.5%, from $29,674,019 in the same period of 2011. The decrease was attributable to the declining revenue from the Ordos project as it approached the end, which decrease other projects did not offset.

Cost of revenues for Segment 1 was $12,252,219 for the six months ended June 30, 2012, a decrease of $9,959,531, or 44.8%, from that of $22,211,750 in the same period of 2011. The six-month gross margin for Segment 1 was 26.9%, compared to 25.1% for the same period of 2011, due to the higher gross margin of newly acquired projects by Yuanjie.

Total operating expenses in Segment 1 were $3,380,332, an increase of $1,181,560, or 53.7%, compared with $2,198,772 in the same period of 2011. The selling and marketing expenses increased by $195,212, or 77.2%, from $252,935 for the six months ended June 30, 2011 to $448,147 in the same period of 2012. The general and administrative expenses for the six months ended June 30, 2012 were $2,920,267, an increase of $982,366, or 50.7%, compared with $1,937,901 for the same period in 2011. This growth was mainly caused by the expansion of geographic reach of our business.

| I-14 |

Other expenses were $448,169 for the six months ended June 30, 2012, a $488,185 increase compared to that of $(40,016) in the same period of 2011.

Income before provision for income taxes was $1,577,019 for the six months ended June 30, 2012, a decrease of $3,646,462, or 69.8%, from that of $5,223,481 in the same period in 2011.

Segment 2: Water Resource Management System and Engineering Services

The following are the operating results for the three months ended June 30, 2012 and 2011 for Segment 2:

Three months ended June 30,

| 2012 ($) | 2011($) | Change ($) | Change (%) | ||||||||

| Revenues | 8,436,000 | 2,314,470 | 6,121,530 | 264.5 | % | ||||||

| Cost of Revenues | 6,089,299 | 1,576,744 | 4,512,555 | 286.2 | % | ||||||

| Operating Expenses: | |||||||||||

| Selling and Marketing Expenses | 457,484 | 215,005 | 242,479 | 112.8 | % | ||||||

| General and Administrative Expenses | 908,000 | 247,098 | 660,902 | 267.5 | % | ||||||

| Research and Development | 5,361 | 8,263 | (2,902 | ) | (35.1 | )% | |||||

| Total Operating Expenses | 1,370,845 | 470,366 | 900,479 | 191.4 | % | ||||||

| Other Expenses | 21,326 | 30,230 | (8,904 | ) | (29.5 | )% | |||||

| Income before Provision for Income Taxes | 954,530 | 237,130 | 717,400 | 302.5 | % |

In Segment 2, revenues were $8,436,000 for the three months ended June 30, 2012, an increase of $6,121,530, or 264.5%, from $2,314,470 in the same period of 2011. Revenues in this segment increased significantly because Yanyu had previously won many contracts in 2011 and 2012, the revenue stream from which is starting to be recognized in the second quarter of 2012.

Cost of revenues in Segment 2 was $6,089,299 in the quarter ended June 30, 2012, an increase of $4,512,555, or 286.2%, from $1,576,744 in the same period of 2011. This increase was mainly due to the increase of projects.

Total operating expenses in Segment 2 were $1,370,845 for the quarter ended June 30, 2012, an increase of $900,479, or 191.4%, compared with $470,366 in the second quarter of 2011. The selling and marketing expenses increased from $215,005 in the second quarter of 2011 to $457,484 in the second quarter of 2012, an increase of $242,479, or 112.8%. The increase was mainly due to increases in headcount and travel expenses. The general and administrative expenses for the second quarter of 2012 were $908,000, an increase of $660,902, or 267.5%, compared with $247,098 for the same period in 2011. The increase was mainly caused by the rents for the new office and increased professional and consulting fees.

Other expenses were $21,326 in the quarter ended June 30, 2012, a decrease of $8,904 from $30,230 in the same period of 2011. The decrease was mainly due to interest expense.

Income before provision for income taxes was $954,530 in the quarter ended June 30, 2012, an increase of $717,400 from $237,130 in the same period of 2011.

The following are the operating results for the six months ended June 30, 2012 and 2011 for Segment 2:

Six months ended June 30,

| 2012 ($) | 2011($) | Change ($) | Change (%) | ||||||

| Revenues | 14,690,590 | 3,955,529 | 10,735,061 | 271.4 | % | ||||

| Cost of Revenues | 10,610,453 | 2,445,352 | 8,165,101 | 333.9 | % | ||||

| Operating Expenses: | |||||||||

| Selling and Marketing Expenses | 883,774 | 365,733 | 518,041 | 141.6 | % | ||||

| General and Administrative Expenses | 1,530,294 | 742,334 | 787,960 | 106.1 | % | ||||

| Research and Development | 68,480 | 48,248 | 20,232 | 41.9 | % | ||||

| Total Operating Expenses | 2,482,548 | 1,156,315 | 1,326,233 | 114.7 | % | ||||

| Other Expenses | 62,242 | 30,295 | 31,947 | 105.5 | % | ||||

| Income before Provision for Income Taxes | 1,535,347 | 323,567 | 1,211,780 | 374.5 | % |

Segment 2 revenues were $14,690,590 for the six months ended June 30, 2012, an increase of $10,735,061, or 271.4%, compared with $3,955,529 in the same period of 2011. The increase was mainly attributable to Yanyu’s business expansion.

| I-15 |

Cost of revenues in Segment 2 was $10,610,453 for the six months ended June 30, 2012, an increase of $8,165,101, or 333.9%, from $2,445,352 in the same period of 2011. The six-month gross margin for this segment was 27.8%, compared to 38.2% for the same period of 2011. The decline was mainly due to newly acquired projects by Yanyu with lower gross margins. We expect the decline to reverse in the following quarters.

Total operating expenses in Segment 2 were $2,482,548, an increase of $1,326,233, or 114.7%, compared with $1,156,315 in the six months of 2011. The selling and marketing expenses increased from $365,733 for the six months ended June 30, 2011 to $883,774 in the same period of 2012, an increase of $518,041, or 141.6%. The increase was mainly due to increases in employees, travel expenses and other contractual service fees. As the result of Yanyu’s business expansion, the Company’s general and administrative expenses for the six months ended June 30, 2012 were $1,530,294, an increase of $787,960, or 106.1%, compared with $742,334 for the same period in 2011.

Other expenses were $62,242 for the six months ended June 30, 2012, a decrease of $31,947, compared with other expenses of $30,295 in the same period of 2011. The decrease was primarily due to the scrap of inventory and interest expenses on credit lines.

Income before provision for income taxes was $1,535,347 for the six months ended June 30, 2012, an increase of $1,211,780, or 374.5%, compared with $323,567 in the same period of 2011.

Segment 3: Industrial Pollution Control and Safety

The following are the operating results for the three months ended June 30, 2012 and 2011 for Segment 3:

Three months ended June 30,

| 2012 ($) | 2011($) | Change($) | Change (%) | ||||||||

| Revenues | 6,250,106 | 1,117,784 | 5,132,322 | 459.2 | % | ||||||