Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - hhgregg, Inc. | Financial_Report.xls |

| EX-31.1 - CERTIFICATION OF THE CHIEF EXECUTIVE OFFICER - hhgregg, Inc. | d340850dex311.htm |

| EX-31.2 - CERTIFICATION OF THE CHIEF FINANCIAL OFFICER - hhgregg, Inc. | d340850dex312.htm |

| EX-32.2 - CERTIFICATION OF THE CHIEF FINANCIAL OFFICER - hhgregg, Inc. | d340850dex322.htm |

| EX-32.1 - CERTIFICATION OF THE CHIEF EXECUTIVE OFFICER - hhgregg, Inc. | d340850dex321.htm |

| EX-10.32 - EMPLOYMENT AGREEMENT, DATED FEBRUARY 15, 2012 - hhgregg, Inc. | d340850dex1032.htm |

| EX-10.31 - EMPLOYMENT AGREEMENT, DATED SEPTEMBER 13, 2011 - hhgregg, Inc. | d340850dex1031.htm |

| EX-23.1 - CONSENT OF KPMG LLP, INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM - hhgregg, Inc. | d340850dex231.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended March 31, 2012

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 001-33600

hhgregg, Inc.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 20-8819207 | |

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

| 4151 East 96th Street Indianapolis, IN | 46240 | |

| (Address of Principal Executive Offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (317) 848-8710

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Common Stock, par value $.0001 per share |

New York Stock Exchange |

Securities registered pursuant to section 12(g) of the Act:

None

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ¨ Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). x Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.(Check one):

| Large accelerated filer ¨ |

Accelerated filer x | |||

| Non-accelerated filer ¨ |

(Do not check if a smaller reporting company) | Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ¨ Yes x No

The aggregate market value of the voting and non-voting common stock held by non-affiliates of the registrant as of the last day of the second fiscal quarter ended September 30, 2011 was approximately $164,408,780 based on the closing stock price of $9.75 per share on that day. (For purposes of this calculation all of the registrant’s directors and executive officers are deemed affiliates of the registrant.)

The number of shares of hhgregg, Inc.’s common stock outstanding as of May 11, 2012 was 36,356,216.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s definitive Proxy Statement (to be filed pursuant to Regulation 14A within 120 days after the Registrant’s fiscal year-end of March 31, 2012) for the regular meeting of stockholders to be held on July 31, 2012, are incorporated by reference into Part III of this Annual Report on Form 10-K.

Table of Contents

| 5 | ||||||

| ITEM 1. |

5 | |||||

| ITEM 1A. |

13 | |||||

| ITEM 1B. |

21 | |||||

| ITEM 2. |

21 | |||||

| ITEM 3. |

23 | |||||

| ITEM 4. |

23 | |||||

| 24 | ||||||

| ITEM 5. |

24 | |||||

| ITEM 6. |

26 | |||||

| ITEM 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

28 | ||||

| ITEM 7A. |

42 | |||||

| ITEM 8. |

43 | |||||

| ITEM 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

68 | ||||

| ITEM 9A. |

68 | |||||

| ITEM 9B. |

68 | |||||

| 69 | ||||||

| ITEM 10. |

69 | |||||

| ITEM 11. |

69 | |||||

| ITEM 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

69 | ||||

| ITEM 13. |

Certain Relationships and Related Transactions, and Director Independence |

69 | ||||

| ITEM 14. |

69 | |||||

| 70 | ||||||

| ITEM 15. |

70 | |||||

2

Table of Contents

Cautionary Note Regarding Forward-Looking Statements

Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended (“Exchange Act”), provide a “safe harbor” for forward-looking statements to encourage companies to provide prospective information about their companies. Some of the statements in this document and any documents incorporated by reference constitute “forward-looking statements” within the meaning of Section 21E of the Exchange Act. These statements relate to future events or our future financial performance and involve known and unknown risks, uncertainties and other factors that may cause our businesses or our industries’ actual results, levels of activity, performance or achievements to be materially different from those expressed or implied by any forward-looking statements. Such statements include, in particular, statements about our plans, strategies, prospects, changes, outlook and trends in our business and the markets in which we operate under the heading “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “could,” “would,” “should,” “expect,” “plan,” “anticipate,” “intend,” “tends,” “believe,” “estimate,” “predict,” “potential” or “continue” or the negative of those terms or other comparable terminology. These statements are only predictions. Actual events or results may differ materially because of market conditions in our industries or other factors. All of the forward-looking statements are qualified in their entirety by reference to the factors discussed under “Management’s Discussion and Analysis of Financial Condition and Results of Operations” herein. The forward-looking statements are made as of the date of this document or the date of the documents incorporated by reference in this document, as the case may be, and we assume no obligation to update the forward-looking statements or to update the reasons why actual results could differ from those projected in the forward-looking statements. Some of the key factors that could cause actual results to differ from our expectations are:

| • | the effect of general and regional economic and employment conditions on our net sales; |

| • | the impact of average selling prices on net sales; |

| • | competition in existing, adjacent and new metropolitan markets; |

| • | competition from internet retailers; |

| • | ability to modify our product mix based on changes in consumer trends and preferences; |

| • | our ability to effectively manage and monitor our operations, costs and service quality; |

| • | our reliance on a small number of suppliers; |

| • | rapid inflation or deflation in core product prices; |

| • | the failure of manufacturers to introduce new products and technologies; |

| • | customer acceptance of new technology; |

| • | our dependence on our key management personnel; |

| • | our ability to attract and retain qualified sales personnel; |

| • | our ability to negotiate with our suppliers to provide product on a timely basis at competitive prices; |

| • | the identification and acquisition of suitable sites for our stores and the negotiation of acceptable leases for those sites; |

| • | fluctuation in seasonal demand; |

| • | our ability to maintain our rate of growth and penetrate new geographic areas; |

| • | our ability to obtain additional financing and maintain our credit facilities; |

| • | our ability to maintain and upgrade our information technology systems; |

| • | the effect of a disruption at our regional distribution centers; |

3

Table of Contents

| • | changes in cost for print and television advertising; and |

| • | changes in trade regulation, currency fluctuations and prevailing interest rates. |

Other factors that could cause actual results to differ from those implied by the forward-looking statements in this Annual Report on Form 10-K are more fully described in the “Risk Factors” section and elsewhere herein. Given these risks and uncertainties, you are cautioned not to place undue reliance on these forward-looking statements. The forward-looking statements included herein are made only as of the date hereof. We do not undertake and specifically decline any obligation to update any of these statements or to publicly announce the results of any revisions to these statements to reflect future events or developments.

4

Table of Contents

| ITEM 1. | Business. |

Our Company

Unless the context otherwise requires, the use of the terms “we”, “us”, “our”, “hhgregg” and the “Company” in this Annual Report on Form 10-K refers to hhgregg, Inc. and our subsidiaries. Our fiscal year ends on March 31.

We are a specialty retailer of home appliances, televisions, computers, consumer electronics, mattresses and related services operating under the name hhgregg™. As of March 31, 2012, we operated 208 stores in Alabama, Delaware, Florida, Georgia, Illinois, Indiana, Kentucky, Maryland, Mississippi, New Jersey, North Carolina, Ohio, Pennsylvania, South Carolina, Tennessee and Virginia. We differentiate ourselves from our competitors by providing our customers with a consultative and educational purchase experience. We also distinguish ourselves by offering next-day delivery on many of our products. Our superior customer purchase experience has enabled us to successfully compete against the other leading video and appliance retailers over the course of our 57-year history.

We design our stores to be visually appealing to our customers and to highlight our premium selection of consumer electronics and appliances. We utilize flat panel television display walls, appliance displays and digital product centers to showcase our broad selection of products with advanced features and functionality. We carry approximately 100 models of flat panel televisions and 350 models of appliances. Our new store prototypes typically range from 25,000 to 30,000 square feet and are located in power centers or freestanding locations in high traffic areas, as close as feasible to our major competitors. We drive store traffic and enhance our brand recognition through year-round television advertising, weekly newspaper inserts, direct mail, e-mail and web promotions.

Our sales can be categorized in the following manner:

| • | Video: We offer a broad selection of the latest video products, such as LED televisions and Blu-ray players. Representative brands include Coby, Curtis, Hisense, LG, Panasonic, Samsung, Sharp, Sony and Toshiba. For fiscal 2012, video products represented 43% of net sales. |

| • | Appliances: We offer a broad selection of major appliances, including the latest generation refrigerators, cooking ranges, dishwashers, freezers, washers and dryers, sold under a variety of leading brand names. Representative brands include Bosch, Frigidaire, GE, Haier, KitchenAid, LG, Maytag, Samsung and Whirlpool. For fiscal 2012, home appliances represented 37% of net sales. |

| • | Computing and mobile phones: We offer a broad selection of computer and mobile phone products, including notebook computers, tablets and mobile phones. Representative brands include Acer, Asus, Hewlett Packard, Samsung, Sony, Toshiba and Verizon. For fiscal 2012, computing and mobile phones represented 9% of net sales. |

| • | Other: We also sell audio products, furniture, mattresses and other select popular consumer electronics and accessories. Products such as home audio systems, cameras, personal navigation, gaming bundles, telephones and advanced cables generate and support store traffic and create cross-selling opportunities with our core products. Our suite of services is aimed at enhancing our customers’ superior purchase experience. For fiscal 2012, other products and services represented 11% of net sales. |

| • | Additionally, we sell a suite of services including third-party premium service plans (“PSPs”), third-party in-home service and repair of our products, next-day delivery and installation and in-home repair and maintenance. Services and PSP revenues are included as a component of net sales in the categories listed above. |

5

Table of Contents

We believe the following strengths contribute significantly to our success and position us for growth within our existing and new markets:

Superior customer purchase experience. We provide a superior purchase experience to our customers through our in-store experience, high level of customer service and delivery and installation capabilities, which we believe drives customer loyalty, referrals and repeat business. We are able to educate our customers on the features and benefits of the products we offer through our extensively trained, commissioned sales force. Approximately 95% of our sales associates are full-time employees, supporting our goal of hiring individuals who are career oriented and motivated. We believe that, when fully informed, customers frequently purchase higher-end, feature-rich products. Our ability to drive sales of more advanced video and appliance products has made us an important partner for our vendors to present their state-of-the-art offerings and enables us to be among the first to introduce new products and technologies in our stores. This further enhances our brand image and customer experience.

We offer next-day delivery for many of our products and also provide quality in-home installation services. These features significantly enhance our ability to sell large, more complex products. Our network of 17 regional and local distribution centers provides a local supply of inventory that supports our next-day delivery strategy. We conduct a significant number of customer surveys each year to ensure customer satisfaction and provide us with feedback to continue improving our superior customer purchase experience.

Balanced mix of premium video products and appliances. We offer an extensive selection of premium video products and appliances. Historically, our appliance business has provided us with financial stability and consistently strong cash flow while our video products are typically more seasonal in nature. Our cash flow tends to be more stable over the long term as a result of our balanced merchandise mix of video products and appliances. In addition, the combination of large screen televisions and appliances, each of which frequently requires home delivery and installation, provides us with efficiencies in home delivery and installation.

Proven ability to successfully penetrate new markets. We seek to expand our highly portable store concept into new markets where we believe there is significant underlying demand for our product mix and customer services, as well as an attractive demographic profile. We have successfully opened or acquired stores in 14 new metropolitan markets in the past five years, most recently in the Chicago, Illinois and Miami, Florida markets. We typically enter a market with a scaled presence to efficiently leverage our advertising spending, regional management and delivery and distribution infrastructure. Within a short time period, usually not exceeding 18 months, we grow our store count in the new market to optimize leverage of our fixed costs and our market share. In fiscal 2013, we plan to open 20 to 22 new stores, predominately in the markets of St. Louis, Missouri and Milwaukee, Wisconsin.

Strong store economics. We closely adhere to our prototype store format when opening new stores, which helps simplify our operations and ensures consistent execution. Our stores typically generate positive cash flow within three months of opening and provide a cash payback in less than three years. Strong store economics, combined with efficient inventory management, generate significant free cash flow to internally fund a portion of our growth. Stores opened during fiscal years 2009, 2010 and 2011 had strong first full year performance, including average net sales of $12.0 million, which contributed to our 4.4% operating income margin in fiscal 2012. During this same period, our new stores required average net capital expenditures of $0.7 million and average initial net-owned inventory investments of $1.0 million.

Multi-channel. We have enhanced our multi-channel capabilities to allow consumers to experience an integrated online and in-store purchase experience. Our multi-channel approach gives customers the ability to make a purchase in store, to buy online and pick up in store or to buy online and have the product shipped or delivered.

6

Table of Contents

Customer Purchase Experience

Our goal is to serve our customers in a manner that generates loyalty, referrals and repeat business. We focus on making every customer’s purchase experience a positive one and aim to be the primary destination for consumer electronics and home appliances in our markets. We employ multiple internal systems to ensure customer satisfaction in each of our markets, and we focus on offering a comprehensive suite of services such as delivery and home installation to our customers. We aim to offer the customer a convenient shopping experience by locating our stores in high traffic areas with a focus on visibility, access and parking availability.

Our philosophy for providing our customers with a superior purchase experience includes:

| • | employing a highly motivated, commissioned sales force and training them so they are able to educate our customers on the benefits of feature-rich, higher margin products; |

| • | offering a deep product assortment in core categories; |

| • | providing a warm and bright store ambiance that showcases our products well; |

| • | providing quick and efficient delivery for many of our products and quality in-home installation services; |

| • | offering extended-term financing through a third-party private label credit card to qualified customers; |

| • | offering convenient 40 minute call-ahead service for delivery; |

| • | soliciting customer feedback to allow us to monitor and improve individual employee performance; |

| • | conducting broad consumer and market research to ensure a top quality, competitively-priced offering; and |

| • | offering customer support through our central call center seven days per week. |

Private Label Credit Card. We offer customers financing through a private label credit card with a third-party financial institution. The third-party financial institution assumes the risk of collection from our customers and has no recourse against us for any uncollected amounts. Private label credit card sales accounted for 31%, 29% and 29% of our net sales in fiscal 2012, 2011 and 2010, respectively.

Product Service and Support. We currently outsource product service and repair of our products sold with and without extended warranties. The majority of extended warranties we sell to our customers are third-party PSPs. The PSPs typically extend three to five years beyond the manufacturer’s warranty and cover all service and repair-related maintenance. We closely monitor the performance of our third-party vendor to ensure the quality and timeliness of their repair services. We offer customer support via our central customer service call center. Our service center is open seven days a week and provides customers with a toll-free resource to ask product and other support-related questions. We complete the customer purchase experience by offering a full array of in-store and in-home product services, including PC optimization and home theater and appliance installation to ensure the customer is able to fully enjoy their purchase.

Merchandising and Purchasing

Merchandise. We focus on offering extensive product and brand selections. We offer a broad selection of leading brands at everyday competitive prices and provide a balance of digital and home theater products and appliances. Our premium products help drive margins and profitability while our lower-margin products help drive customer traffic. Our balanced mix of premium video products and appliances historically has provided us with a more stable and less-seasonal cash flow.

7

Table of Contents

Product Categories. We sell a wide variety of premium video products, including digital televisions and home theater systems, appliances, audio products, notebook computers, mattresses and related services. The table below lists selected products and representative brands for our core merchandise categories:

| Category |

Products |

Selected Brands | ||

| Video |

Flat panel televisions and Blu-Ray and DVD players | Coby, Curtis, Hisense, LG, Panasonic, Samsung, Sharp, Sony and Toshiba | ||

| Appliances |

Washers and dryers, refrigerators, cooking ranges, dishwashers, freezers, and air conditioners | Bosch, Frigidaire, GE, Haier, KitchenAid, LG, Maytag, Samsung and Whirlpool | ||

| Computing and mobile phones |

Computers, mobile phones and tablets | Acer, Asus, Hewlett Packard, Samsung, Sony, Toshiba and Verizon | ||

| Other |

Digital camcorders, digital cameras, gaming bundles, home theater receivers, mattresses, MP3 players, personal navigation, speaker systems and telephones | Canon, Nikon, Samsung, Serta and Sony | ||

Vendor Relationships. Our top 10 and 20 suppliers accounted for over 77.2% and 89.9%, respectively, of merchandise purchased by us during fiscal 2012. Our key suppliers include Frigidaire, GE, HP, LG, Panasonic, Samsung, Sharp, Sony, Toshiba and Whirlpool.

Our purchasing strategy varies by vendor and product line. We do not have long-term contracts with any of our major suppliers. Inventory purchases are managed through the placement of purchase orders with our vendors. Our ability to sell a broad selection of products has made us an important partner to our vendors for showcasing their higher-margin product offerings and introducing new products and technologies to consumers. In an effort to support our strategy, vendors offer us various incentives including volume discounts, trade financing, co-op advertising, purchase discounts and allowances, promotional items and inventory on a consignment basis.

Personnel and Training

Commissioned Sales Associates. We seek to hire individuals who are career-oriented and motivated by a commission-based environment. Approximately 95% of our sales associates are full-time employees. Our sales associates are compensated based on both sales and product profitability. New sales associates are required to complete 80 hours of initial in-house training focused on product knowledge and functionality, customer service and general store operations. Sales associates also participate in on-going training for an average of ten hours per month to stay current with new product offerings and customer service initiatives. This on-going training includes quarterly meetings with vendors to learn about upcoming product releases.

Manager-In-Training (MIT) Program. We operate a professional development program that provides managers with a variety of tools and training to assist them in leading their associates and meeting their performance objectives. Manager candidates undergo comprehensive training in store operations, sales, management and communication skills so that they can eventually manage their own stores and have the opportunity to become regional managers. Candidates first participate in our MIT program, which develops each manager’s managerial and supervisory skills. After completion of our training programs, manager candidates work as assistant managers. Managers earn an opportunity to operate higher-volume stores as they demonstrate greater proficiency in their management skills.

8

Table of Contents

Our store and regional managers are essential to our store expansion strategy. We use experienced store and regional managers from our existing markets to open new markets. Our MIT program provides a pipeline of future store and regional managers. This program enables us to staff our management positions in new stores from a pool of experienced managers and backfill the openings created in existing stores with well-developed, internal promotions.

Distribution and Warehousing

Our distribution and warehousing functions are designed to optimize inventory availability and turnover, increase delivery efficiency, and minimize product handling. Our distribution and warehousing system at March 31, 2012 consisted of five regional distribution centers, or RDCs, and 12 local distribution centers, or LDCs. RDCs receive products directly from manufacturers and stock merchandise for local customer delivery as well as store and LDC replenishment. LDCs receive inventory daily from their respective RDCs or directly from manufacturers for home delivery. Merchandise is generally not transferred between stores. Our RDCs and LDCs operate seven days a week. All of our distribution facilities are leased.

The following table sets forth certain information relating to our RDCs and LDCs as of March 31, 2012:

| Facility |

Opening Date | Area Served | Size (sq. ft) | |||||

| RDC: |

||||||||

| Atlanta, Georgia |

January 2003 | Southeast | 273,200 | |||||

| Brandywine, Maryland |

March 2010 | Mid-Atlantic | 393,440 | |||||

| Aurora, Illinois |

July 2011 | Great Lakes | 247,360 | |||||

| Indianapolis, Indiana |

June 1986 | Midwest | 319,458 | |||||

| Davenport, Florida |

April 2008 | Florida | 282,126 | |||||

| LDC: |

||||||||

| Birmingham, Alabama |

April 2007 | Birmingham | 65,000 | |||||

| Charlotte, North Carolina |

April 2005 | Charlotte | 99,688 | |||||

| Cincinnati, Ohio |

March 1999 | Cincinnati | 100,800 | |||||

| Cleveland, Ohio |

September 2001 | Cleveland | 100,800 | |||||

| Columbus, Ohio |

August 1999 | Columbus | 89,643 | |||||

| Jacksonville, Florida |

March 2008 | Jacksonville | 71,760 | |||||

| Louisville, Kentucky |

August 2002 | Louisville | 61,000 | |||||

| Pembroke Park, Florida |

May 2011 | Miami | 66,095 | |||||

| Nashville, Tennessee |

October 2006 | Nashville | 100,000 | |||||

| Philadelphia, Pennsylvania |

April 2010 | Philadelphia | 86,304 | |||||

| Pittsburgh, Pennsylvania |

September 2011 | Pittsburgh | 20,465 | |||||

| Raleigh, North Carolina |

August 2007 | Raleigh | 108,000 | |||||

Typically, large appliances, large-screen televisions, home theater products and mattresses are delivered to a customer’s home. The majority of our customers purchasing these products also use our delivery or installation service. Our stores carry a limited inventory of these larger items to accommodate customers who prefer to transport merchandise themselves. Smaller-sized items such as Blu-Ray players, digital cameras, notebook computers, small appliances, tablets and televisions less than 50 inches are adequately stocked in-store to meet customer demand.

Our delivery is outsourced in all of our markets. Our outsourcing partners assign certain contractors to us and those contractors deliver products exclusively for us, generally carry our logo on their vehicles and wear hhgregg uniforms. This allows us to maintain our brand identity and high customer service levels following the purchase of our products. We remain the customer’s primary point of contact throughout the delivery and installation process regardless of whether or not the service is outsourced, thereby ensuring that we maintain

9

Table of Contents

control over the quality of the service provided. We also closely monitor our delivery partners to assess our customers’ satisfaction with their services. We are not subject to any long-term agreements with any of our delivery partners.

Advertising and Promotion

We utilize ongoing advertising and weekly promotions to increase our brand awareness and to drive online and in-store traffic. We aggressively promote our products and services through the use of a balanced media mix, which includes preprinted newspaper inserts, television, direct mail, e-mail communications, radio, digital advertising, social media, web promotions, outdoor billboards and event sponsorship. We currently outsource creative and media placement to advertising agencies, but handle newspaper insert and direct mail design and placement internally.

We enter new major markets with a comprehensive brand awareness campaign for a three-week period leading up to our grand opening. During the week of grand opening, we utilize a combination of television, radio, direct mail, social media and special newspaper insert offers to drive traffic to our stores.

Our website, www.hhgregg.com, features our full line of products and services and provides useful information to consumers on the features and benefits of our products, services, store locations and hours of operation. We offer both online shopping with delivery, as well as an in-store pickup option to increase customer traffic. We also utilize the internet as an important customer information resource to drive in-store purchases of our merchandise and services.

Management Information Systems

Over the past five years, we have been systematically updating and upgrading our management information systems in a multi-phase process to improve the efficiency of our store operations and enhance critical corporate and business planning functions. During this time period, we

| • | installed a new enterprise data warehouse to better integrate operating and merchandising information in a relational data base environment, |

| • | implemented a demand management and forecasting tool to add more robust analytical capabilities to our inventory management process, |

| • | opened an off-site data center to enhance our disaster recovery capabilities, and |

| • | converted our financial reporting and accounting systems to a retail industry standard application to support our anticipated future growth. |

Our management information systems include a wide-area network linking our stores and distribution centers to our corporate offices. This provides real-time polling of sales, scheduled deliveries and inventory levels at the store and distribution center level. In our distribution centers, we use radio frequency networks to assist in receiving, stock put-away, stock movement, order filling, cycle counting and inventory management.

Competition

The consumer electronics and appliance industry is highly competitive and concentrated among a group of major retailers. Our stores compete against other consumer electronics retailers, specialty home office retailers, mass merchants, home improvement superstores and internet-based businesses. Our stores also compete against independent dealers, regional chain discount stores, wholesale clubs and other specialty single- and multi-unit retail stores. Mass merchants continue to increase their offerings of consumer electronics products, primarily those that are less complex to sell, deliver and install. Additionally, internet retailers continue to gain market share in smaller size consumer electronics products.

10

Table of Contents

We compete against national retailers including Best Buy, Home Depot, Lowe’s, Sears and Wal-Mart in the vast majority of our markets. We also compete against regional retailers, such as BrandsMart and Fry’s, in several of our markets. We continue to perform well in digital televisions and major appliances in the majority of our markets. This performance is achieved despite the presence, or entrance, of each of these leading competitors in our markets.

The consumer electronics and appliance industry competes on product selection, price and customer service. We differentiate ourselves through our emphasis on an extensive product offering, customer service and satisfaction while matching our competitors on price. We believe that our highly trained commissioned sales force, broad product and brand offerings and customer support services allow us to compete effectively in our markets for the following reasons:

| • | Our commissioned sales force is motivated to attend to customer needs quickly and is knowledgeable about the products we carry. The majority of our key competitors pay their sales force on an hourly basis. Because our sales staff is commissioned and highly trained in product knowledge, we believe our sales force is driven to more quickly and efficiently assist our customers in making their purchase decisions. We believe that when fully informed, customers purchase higher-end, feature-rich products due to an appreciation of the performance of those products. |

| • | By combining this knowledgeable sales force with a broad selection of key brands and products with complex, premium features, we differentiate ourselves from our competitors. |

| • | We promote our products both in our stores and through advertising. We also highlight our service offerings, such as next-day delivery and 40 minute call-ahead delivery. These services are key to our customer base which appreciates better product information, high-end products and more flexible delivery. |

Environmental Matters

We are not aware of any federal, state or local provisions which have been enacted or adopted regulating the discharge of materials into the environment, or otherwise relating to the protection of the environment, that have materially affected, or are likely to materially affect, our net earnings or competitive position, or have resulted or are expected to result in material capital expenditures. During fiscal 2012, we had no capital expenditures for environmental control facilities and no such expenditures are anticipated in the foreseeable future.

Seasonality

We experience seasonal fluctuations in our net sales and operating results due in part to seasonal shopping patterns. For example, in fiscal 2012 and 2011, we generated 33.2% and 30.0%, respectively, of our net sales in the fiscal quarter ended December 31, which includes the holiday selling season. We also incur significant additional costs and expenses during the fiscal quarter ended December 31 due to increased staffing levels and higher purchase volumes.

Trade Names and Trademarks

We have registered, acquired the registration of, or claim ownership of the following trade names and trademarks for use in our business: hhgregg™, HHGREGG.COM®, H.H. Gregg Appliances Electronics Computers®, HHGREEN® , GIVING YOU THE POWER TO GO GREEN®, HHG®, Fine Lines®, hhgregg Fine Lines™, Fine Points™ and Price and Advice Guaranteed™.

Employees

As of March 31, 2012, we employed approximately 6,700 employees, of whom approximately 85% were full-time. We have no collective bargaining agreements covering any of our employees and have never experienced any material labor disruption. We consider our employee relations to be good.

11

Table of Contents

Available Information

We are subject to the reporting requirements of the Exchange Act and its rules and regulations. The Exchange Act requires us to file reports, proxy statements and other information with the U.S. Securities and Exchange Commission (SEC). Copies of these reports, proxy statements and other information can be read and copied at:

SEC Public Reference Room

100 F Street N.E.

Washington, D.C. 20549

Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330.

The SEC maintains a Web site that contains reports, proxy statements and other information regarding issuers that file electronically with the SEC. These materials may be obtained electronically by accessing the SEC’s Web site at http://www.sec.gov.

We make available, free of charge on our Web site, our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act, as soon as reasonably practicable after we electronically file these documents with, or furnish them to, the SEC. These documents are posted on our Web site at www.hhgregg.com — select the “Investor Relations” link and then the “Financials and SEC Filings” link.

We also make available, free of charge on our Web site, the charters of the Audit Committee, Compensation Committee, Executive Committee and Nominating and Corporate Governance Committee, as well as the Code of Business Conduct and Ethics, Whistleblower Policy, Related Party Policy and the Corporate Governance Guidelines. These documents are posted on our Web site at www.hhgregg.com — select the “Investor Relations” link and then the “Corporate Governance” link.

Copies of any of the above-referenced documents will also be made available, free of charge, upon written request to:

hhgregg, Inc.

Vice President of Finance

4151 E 96th Street

Indianapolis, IN 46240

12

Table of Contents

| ITEM 1A. | Risk Factors |

Described below are certain risks that our management believes are applicable to our business and the industry in which we operate. You should carefully consider each of the following risks and all of the information set forth in this Annual Report on Form 10-K.

If any of the events described below occur, our business, financial condition, results of operations, liquidity or access to the capital markets could be materially adversely affected. The following risks could cause our actual results to differ materially from our historical experience and from results predicted by forward-looking statements made by us or on our behalf related to conditions or events we anticipate may occur in the future. All forward-looking statements made by us or on our behalf are qualified by the risks below.

Our business is dependent on the general economic conditions in our markets.

In general, our sales depend on discretionary spending by our customers. General economic factors and other conditions that may affect our business, include periods of slow economic growth or recession, volatility and/or lack of liquidity from time to time in U.S. and world financial markets and the consequent reduced availability and/or higher cost of borrowing to hhgregg and its customers, slower rates of growth in real disposable personal income, sustained high rates of unemployment, high consumer debt levels, increasing fuel and energy costs, inflation or deflation of commodity prices, natural disasters, acts of terrorism and developments in the war against terrorism. General economic conditions and discretionary spending are beyond our control and are affected by, among other things:

| • | consumer confidence in the economy; |

| • | unemployment trends; |

| • | consumer debt levels; |

| • | consumer credit availability; |

| • | the housing and home improvement markets; |

| • | gasoline and fuel prices; |

| • | interest rates and inflation; |

| • | slower rates of growth in real disposable personal income; |

| • | natural disasters; |

| • | national and international security concerns; |

| • | tax rates and tax policy; and |

| • | other matters that influence consumer confidence and spending. |

Increasing volatility in financial markets may cause some of the above factors to change with an even greater degree of frequency and magnitude. The above factors could result in slowdown in the economy or an uncertain economic outlook, which could have a material adverse effect on our business and results of operations.

Other conditions that may impact our results of operations include disruptions in the availability of content such as sporting events or other televised content. Such disruptions may influence the demand for hardware that our customers purchase to access such content, which would have an adverse effect on our results of operations.

We have many competitors, direct and indirect. If we fail to execute our merchandising, marketing and distribution strategies effectively, those competitors could take sales and market share from us.

The retail market for consumer electronics and major home appliances is intensely competitive. We currently compete against a diverse group of national retailers, including Best Buy, Home Depot, Lowe’s, Sears,

13

Table of Contents

Wal-Mart, internet retailers, regional or independent specialty retail stores and mass merchandisers that sell many of the same or similar consumer electronics and major home appliances that we do. There are few barriers to entry and as a result new competitors may enter our existing or new markets at any time.

We may not be able to compete successfully against existing and future competitors. Some of our competitors have financial resources that are substantially greater than ours and may be able to purchase inventory at lower prices. Our competitors may respond more quickly to new or emerging technologies and may have greater resources to devote to discounts, promotions and sales of products and services. They may also have financial resources that enable them to weather economic downturns better than us. As it relates to internet retailers, we will need to ensure we have an effective multi-channel strategy.

Our existing competitors or new entrants into our industry may use a number of different strategies to compete against us, including:

| • | lower pricing; |

| • | more aggressive advertising and marketing; |

| • | enhanced product and service offerings; |

| • | extension of credit to customers on terms more favorable than we make available; |

| • | innovative store formats; |

| • | improved retail sales methods; |

| • | online product offerings; |

| • | not charging sales tax at the time of sale on internet purchases; and |

| • | expansion into markets where we currently operate. |

Competition could cause us to lose market share, net sales and customers, which could negatively impact our comparable store sales, increase expenditures or reduce prices or margins, any of which could have a material adverse effect on our business and results of operations.

Our ability to maintain and increase both net sales and product margins depends to a large extent on the periodic introduction and availability of new products and technologies.

We believe that the introduction and continued growth in consumer acceptance of new products will have a significant impact on our ability to increase net sales and maintain product margins. Our products are subject to significant technological changes, and we are dependent on our suppliers to continually invest in research and development to ensure we have new products and technologies in our stores. Innovative, heavily-featured products are typically introduced at relatively high price points. In response to continuing pressure from consumers and our competitors, price points may be reduced more quickly and to a greater degree, as compared to our prior practice in order to drive consumption. As a result, unit sales must increase at a greater rate than average selling prices decline in order to maintain or grow comparable store sales. If new product introductions do not drive enough sales volume at higher price points, prices will have to be reduced in order to sell existing inventory, which may negatively impact our ability to maintain our historical comparable store sales levels. If there were no new technologies or features in our products, we would see a material adverse impact to our revenues and product margins.

A disruption in our relationships with, or in the operations of, any of our key suppliers could cause our net sales and profitability to decline.

The success of our business and our growth strategy depends to a significant degree on our relationships with our suppliers. Our largest suppliers include Frigidaire, GE, Hewlett Packard, LG, Panasonic, Samsung,

14

Table of Contents

Sharp, Sony, Toshiba and Whirlpool. We do not have long-term supply agreements or exclusive arrangements with our major suppliers. We typically order our inventory through the issuance of individual purchase orders to vendors. We have no contractual assurance of the continued supply of merchandise in the amount and assortment we currently offer our customers and we may be subject to rationing by suppliers. In addition, we rely heavily on a relatively small number of suppliers. Our top 10 and 20 suppliers represented 77.2% and 89.9%, respectively, of our purchases in fiscal 2012. The loss of any one or more of our key suppliers or our failure to establish and maintain relationships with these and other suppliers could materially adversely affect our supply and assortment of products, as we may not be able to find suitable replacements to supply products at competitive prices.

Our suppliers also supply us with marketing funds and volume rebates. If our suppliers fail to continue these incentives, it could have a material adverse effect on our sales and results of operations.

The ongoing global crisis may also adversely affect our suppliers’ access to capital and liquidity with which to maintain their inventory, production levels and product quality and to operate their businesses, all of which could adversely affect our supply chain. It may cause suppliers to reduce their offerings of customer incentives and vendor allowances, cooperative marketing expenditures and product promotions. It may also cause them to change their pricing policies, which could impact demand for their products. The ongoing crisis and market instability make it difficult for us and our suppliers to accurately forecast future product demand trends, which could cause us to carry too much or too little merchandise in various product categories.

Disruptions in our supply chain and other factors affecting the distribution of our merchandise could adversely impact our business.

Any disruption in the operation of our distribution centers could result in our inability to meet our customers’ delivery requirements, higher costs, inability to stock our stores, or longer lead time associated with distributing merchandise. Any such disruption within our supply chain network, including damage or destruction to one of our five regional distribution centers, could result in decreased net sales, increased costs and reduced profits.

If we fail to anticipate changes in consumer preferences, our net sales and profitability may decline.

Our products must appeal to a broad range of consumers whose preferences cannot be predicted with certainty and are subject to change. Our ability to maintain and increase net sales depends to a large extent on the periodic introduction and availability of new products and technologies. Our success depends upon our ability to anticipate and respond in a timely manner to trends in consumer preferences relating to major household appliances and consumer electronics such as high efficiency appliances and high definition televisions. These products are subject to significant technological changes and pricing limitations and are subject to the actions and cooperation of third parties, such as movie distributors and television and radio broadcasters, all of which could affect the success of these and other new consumer electronics technologies. It is possible that new products will never achieve widespread consumer acceptance. Our margins are enhanced due to our ability to sell more feature-rich products with higher margins early in the product life cycle, thus a lack of new products in the market would impair our ability to maintain gross margins as a percentage of sales. Significant deviations from the anticipated consumer preferences for the products we sell could result in lost sales and lower margins due to the need to mark down excess inventory. If we are unable to effectively introduce and sell new products to our customers, our business and results of operations could be adversely affected.

Our growth strategy depends in part on our ability to open and profitably operate new stores in existing and new geographic markets. If we fail to successfully manage the challenges our planned growth poses, fail to maintain our financial and internal controls and systems or encounter unexpected difficulties during our expansion, our net sales and profitability could be materially adversely affected.

New stores that we open may not be profitable or may take longer than anticipated to open or to reach desired levels of profitability. Furthermore, the addition of new stores in existing markets may adversely affect

15

Table of Contents

the performance of nearby stores. Collectively, these circumstances could lower our profit, operating income and profit margins. There are a number of factors that could affect our ability to open or acquire, as well as operate new stores at profitable levels consistent with our existing stores, including:

| • | the inability to identify and acquire suitable store sites and to negotiate acceptable leases for these sites; |

| • | competition in existing, adjacent and new markets; |

| • | the failure to open enough stores in new markets to achieve a sufficient market presence to compete successfully; |

| • | the unfamiliarity with local real estate markets and demographics in adjacent and new markets; |

| • | difficulties associated with the hiring, training and retention of additional sales personnel and store managers; |

| • | the inability to obtain government approvals, licenses and permits in a timely manner; |

| • | the failure to adequately supervise construction and manage development costs; |

| • | the inability to secure adequate landlord financing; |

| • | difficulties or delay in obtaining construction materials and labor; and |

| • | problems or delays in pre-opening store promotion and related publicity. |

In addition, our growth plans will require management to expend significant time, effort and resources to ensure the continuing adequacy of our financial and other internal controls, operating procedures, information systems, product purchasing, inventory management, warehousing and distribution systems and employee training programs. We may not be able to effectively manage these increased demands or respond on a timely basis to the changing demands that our planned expansion will impose on our management, financial and other internal controls and information systems. If we fail to successfully manage the challenges our planned growth poses, fail to improve these systems and controls or encounter unexpected difficulties during our expansion, our net sales and profitability could be materially adversely affected.

Lack of available retail store sites on terms acceptable to us, rising real estate prices and other costs and risks relating to new store openings could severely limit our growth opportunities. Our strategy includes opening stores in new and existing markets. We must successfully choose store sites, execute favorable real estate transactions on terms that are acceptable to us, hire competent personnel and effectively open and operate these new stores. Our plans to increase our number of retail stores will depend in part on the availability of existing retail stores or store sites. A lack of available financing on terms acceptable to real estate developers or a tightening credit market may adversely affect the number or quality of retail sites available to us. We cannot assure you that stores or sites will be available to us, or that they will be available on terms acceptable to us. If additional retail store sites are unavailable on acceptable terms, we may not be able to carry out a significant part of our growth strategy. Rising real estate costs and acquisition, construction and development costs could also inhibit our ability to grow. If we fail to locate desirable sites, obtain lease rights to these sites on terms acceptable to us, hire adequate personnel and open and effectively operate these new stores, our financial performance could be adversely affected. In addition, our expansion in new and existing markets may present competitive, distribution, merchandising and regulatory challenges that differ from our current challenges, including competition among our stores, diminished novelty of our store design and concept, added strain on our distribution centers, additional information to be processed by our management information systems and diversion of management attention from operations, such as the control of inventory levels in our stores. We also cannot guarantee that we will be able to obtain and distribute adequate product supplies to our stores or maintain adequate warehousing and distribution capability at acceptable costs. New stores also may have lower than anticipated sales volumes relative to previously opened stores during their comparable years of operation, and sales volumes at new stores may not be sufficient to achieve store-level profitability or profitability comparable to that of existing stores. New stores in new markets, where we are less familiar with the target customer and less well-known, may face different or additional risks and increased costs compared to stores operated in existing

16

Table of Contents

markets or new stores in existing markets. For example, expansion into new markets could bring us into direct competition with retailers with whom we have no past experience as direct competitors. We also may not be able to advertise cost-effectively in new or smaller markets in which we have less store density, which could slow sales growth at such stores. To the extent that we are not able to meet these various challenges, our sales could decrease, our operating costs could increase and our profitability could be impacted.

If we fail to hire, train and retain qualified managers, sales associates and other employees we could lose sales to our competitors.

A key element of our competitive strategy is to provide product expertise to our customers through our extensively trained, commissioned sales associates which, we believe, results in more of our customers purchasing higher-margin, feature-rich products. If we are unable to attract and retain qualified personnel as needed in the future, including qualified sales personnel and candidates for our MIT program, our level of customer service may decline, which may decrease our net sales and profitability. Our ability to control labor costs, which may impact our ability to hire and retain qualified personnel, is subject to numerous external factors, including prevailing wage rates, the impact of legislation or regulations governing healthcare benefits or labor relations, such as the Employee Free Choice Act, and health and other insurance costs. Additionally, the National Labor Relations Board could significantly impact the nature of labor relations in the U.S. and how union elections and contract negotiations are conducted. If our labor and/or benefit costs increase, we may not be able to hire or maintain qualified personnel to the extent necessary to execute our competitive strategy, which could adversely affect our results of operations.

If we do not maintain the security of customer, associate, or company information, we could damage our reputation, incur substantial additional costs and become subject to litigation.

Any significant compromise or breach of customer, associate or company data security could significantly damage our reputation and result in additional costs, lost sales, fines and lawsuits. The regulatory environment related to information security and privacy is increasingly rigorous, with new and constantly changing requirements applicable to our business, and compliance with those requirements could result in additional costs. There is no guarantee that the procedures that we have implemented to protect against unauthorized access to secured data are adequate to safeguard against all data security breaches. If any such compromise or breach were to occur, it could adversely affect our results of operations.

Regulatory developments in the United States could impact our private-label credit card financing offers and have a material adverse impact on our net sales and profitability.

We offer private-label credit cards through a third-party financial institution that manages and directly extends credit to our customers. Cardholders who choose the private-label card can receive low- or no-interest promotional financing on qualifying purchases. If a customer utilizes a deferred interest financing offer and fails to comply with the terms of the offer, all deferred interest becomes due and payable to the third-party financial institution. Private label credit card sales accounted for 31%, 29% and 29% of our net sales in fiscal 2012, 2011 and 2010, respectively. Recently enacted legislative and regulatory changes that focus on a variety of credit related matters have had no material adverse impact on our operations to date. However, if future legislative or regulatory restrictions or prohibitions arise that affect our ability to offer promotional financing and we are unable to adjust our operations in a timely manner, our revenue and profitability may be materially adversely affected.

If our third-party delivery services are unable to meet our promised delivery schedule, our net sales may decline due to a decline in customer satisfaction.

We offer next-day delivery on many of the products we sell. Our deliveries are outsourced to third-party delivery services. Our third-party delivery services are subject to risks that are beyond our control. If our

17

Table of Contents

products are not delivered to our customers on time, our customers may cancel their orders or we may lose business from these customers in the future. As a result, our net sales and profitability may decline.

Because our hhgregg stores are generally concentrated in the eastern half of the United States, we are subject to regional risks.

During fiscal 2012, we operated stores in Alabama, Delaware, Florida, Georgia, Illinois, Indiana, Kentucky, Maryland, Mississippi, New Jersey, North Carolina, Ohio, Pennsylvania, South Carolina, Tennessee and Virginia. We therefore have exposure to these local economies as well as weather conditions and natural disasters occurring in these markets. If these markets individually or collectively suffer an economic downturn or other adverse event, there could be an adverse impact on our comparable store sales, net sales and profitability and our ability to implement our planned expansion program. Several of our larger competitors operate stores nationwide and thus are not as vulnerable as we are to these risks. In addition, our net sales depend on discretionary consumer spending, which may decrease on a regional basis due to a number of factors beyond our control, including unfavorable economic conditions, increases in consumer debt levels, unemployment or inflation, or other factors that adversely affect consumer confidence.

Any failure of our information technology infrastructure or management information systems, could cause a disruption in our business and our results of operations could be materially adversely impacted.

Our ability to operate our business from day to day largely depends on the efficient operation of our information technology infrastructure and management information systems. We use our management information systems to conduct our operations and for critical corporate and business planning functions, including store operations, sales management, merchandising, marketing, supply chain and inventory management, financial reporting and accounting, delivery and other customer services and various administrative functions. Any failure that is not covered by our disaster recovery plan could cause an interruption in our operations and adversely affect our results of operations.

We are subject to certain statutory, regulatory and legal developments which could have a material adverse impact on our business.

Our statutory, regulatory and legal environment exposes us to complex compliance and litigation risks that could materially adversely affect our operations and financial results. The most significant compliance and litigation risks we face are:

| • | The difficulty of complying with sometimes conflicting statutes and regulations in local, state and national jurisdictions; |

| • | The impact of proposed, new or changing statues and regulations, including, but not limited to, financial reform, environmental, labor reform, health care reform, corporate governance matters and/or other as yet unknown legislation that could affect how we operate and execute our strategies as well as alter our expense structure; |

| • | The impact of changes in tax laws (or interpretations thereof by courts and taxing authorities) and accounting standards; |

| • | The impact of litigation trends, including class action lawsuits involving consumers and stockholders, and labor and employment matters; and |

| • | Changes in trade regulations, currency fluctuations, economic or political instability, natural disasters, public health emergencies and other factors beyond our control may increase the cost of items we purchase or create shortages of these items, which in turn could have a material adverse effect on our cost of goods, or may force us to increase prices, thereby adversely impacting net sales and profitability. |

18

Table of Contents

Adapting to regulatory changes and defending against lawsuits and other proceedings may involve significant expense and divert management’s attention and resources from other matters which could adversely affect our results of operations.

We have significant future capital needs that we may be unable to fund and this failure could curtail our projected growth.

Our expansion plans will require substantial capital, including funds for capital expenditures, pre-opening costs, working capital requirements and initial operating losses related to new store openings. We also require additional capital for remodeling and renovating our existing stores and continuous management information systems updates. Net capital expenditures during fiscal 2012 were $81.4 million. If the cash provided by operating activities, available borrowings under our revolving credit facility and proceeds from sale and leaseback transactions are not sufficient to fund our operations, store expansion and renovation activities and infrastructure and information technology investment, we may be required to seek additional capital. If we are not able to obtain such additional financing on favorable terms, we may need to curtail our expansion plans and defer some or all of the upgrade of our management information systems.

Our quarterly results fluctuate due to seasonal demand for our products and if we miscalculate this demand our net sales and profitability could decline.

We experience seasonal fluctuations in our net sales and operating results due in part to seasonal shopping patterns. For example, in fiscal 2012 and 2011, we generated 33.2% and 30.0%, respectively, of our net sales in the fiscal quarter ended December 31, which includes the holiday selling season. We also incur significant additional costs and expenses during this fiscal quarter due to increased staffing levels and higher purchase volumes. If we miscalculate the demand for our products generally or for our product mix during the fiscal quarter ending December 31, our net sales could decline, resulting in excess inventory, which could tie up our working capital and revolving credit facility, as well as lower our profit margin as a result of product markdowns. A shortfall in expected net sales, combined with significant additional expenses during the fiscal quarter ended December 31, could cause a significant decline in our operating results.

If we are unable to retain key management, we could have difficulty implementing our business strategy, which may result in reduced net sales, operating margins and profitability.

We are dependent on the skills, experience and continued service of our senior management. We have employment agreements with these key officers which include secrecy, non-competition and other customary provisions. If members of senior management cease to be active in the management of our business or decide to join a competitor or otherwise compete directly or indirectly with us, our business and operations could be harmed, and we could have difficulty in implementing our strategy, which may result in reduced net sales, operating margins and profitability.

Our executive officers, directors and stockholders affiliated with our directors own a large percentage of our voting common stock and could limit the influence of our other stockholders on corporate decisions.

Our executive officers, directors, current holders of more than 5% of our outstanding common stock and their respective affiliates beneficially own, in the aggregate, approximately 50.0% of our outstanding common stock. Should some of these stockholders act together, they would be able to control all matters requiring approval by our stockholders, including mergers, sales of assets, the election of directors or other significant corporate transactions. The interests of these stockholders may not always coincide with our corporate interests or the interests of our other stockholders, and they may act in a manner with which our other stockholders may not agree or that may not be in the best interests of our other stockholders.

19

Table of Contents

We may be subject to periodic litigation and other regulatory proceedings. These proceedings may be affected by changes in laws and government regulations or changes in the enforcement thereof.

We are involved in a number of legal proceedings that arise from time to time in the ordinary course of business. Litigation is inherently unpredictable, and the outcome of some of these proceedings and other contingencies could require us to take or refrain from taking action which, in either case, could adversely affect our operations or reduce our net income. Additionally, defending against these lawsuits and proceedings may involve significant expense and diversion of management’s attention and resources from other matters.

We have anti-takeover defense provisions in our certificate of incorporation and bylaws that may deter potential acquirers and depress the price of our common stock.

Our certificate of incorporation and bylaws contain provisions that could have the effect of making it more difficult for a third party to acquire, or of discouraging a third party from attempting to acquire, control of us. These provisions:

| • | authorize our board of directors to issue “blank check” preferred stock and determine the powers, preferences and privileges of those shares without prior stockholder approval; |

| • | limit the calling of special meetings of stockholders; and |

| • | impose a requirement that an affirmative vote of the holders of 66 2/3% of the outstanding shares of common stock is required to amend certain provisions of the certificate of incorporation and bylaws. |

Under these various provisions in our certificate of incorporation, bylaws, a takeover attempt or third-party acquisition of us, including a takeover attempt that may result in a premium over the market price for shares of our common stock, could be delayed, deterred or prevented. In addition, these provisions may prevent the market price of our common stock from increasing in response to actual or rumored takeover attempts and may also prevent changes in our management. As a result, these anti-takeover and change of control provisions may limit the price investors are willing to pay in the future for shares of our common stock.

20

Table of Contents

| ITEM 1B. | Unresolved Staff Comments. |

None.

| ITEM 2. | Properties. |

Stores and Store Operations

Operations. Our store operations are organized into 27 geographic regions. Each region is supervised by a regional manager who monitors store operations and meets regularly with store managers to discuss merchandising, new product introductions, sales promotions, customer feedback and store operating performance. A store is typically overseen by a general manager, two sales managers and a staff averaging 20 salespeople and 10 additional support staff. Our stores are open seven days and six nights a week.

Locations. As of March 31, 2012, we leased all of our stores and distribution centers, which are located in Alabama, Delaware, Florida, Georgia, Illinois, Indiana, Kentucky, Maryland, Mississippi, New Jersey, North Carolina, Ohio, Pennsylvania, South Carolina, Tennessee and Virginia. Our stores average approximately 33,000 square feet. We also lease our corporate headquarters which is located in Indianapolis, Indiana. Our corporate headquarters includes a store, corporate training center, regional distribution and warehousing facility, and corporate call center. Our distribution and warehousing system consists of five regional distribution centers, or RDCs, and twelve local distribution centers, or LDCs. For a description of our RDCs and LDCs, see “Item 1. Business-Distribution and Warehousing.”

The following table sets forth our store locations:

| State |

Stores Opened at March 31, 2011 |

Store Openings |

Store Closures |

Stores Opened at March 31, 2012 |

||||||||||||

| Alabama |

5 | 1 | — | 6 | ||||||||||||

| Delaware |

3 | — | — | 3 | ||||||||||||

| Florida |

23 | 11 | — | 34 | ||||||||||||

| Georgia |

15 | — | — | 15 | ||||||||||||

| Illinois |

— | 15 | — | 15 | ||||||||||||

| Indiana |

17 | 1 | — | 18 | ||||||||||||

| Kentucky |

6 | — | — | 6 | ||||||||||||

| Maryland |

11 | — | — | 11 | ||||||||||||

| Mississippi |

1 | — | — | 1 | ||||||||||||

| New Jersey |

3 | — | — | 3 | ||||||||||||

| North Carolina |

17 | — | — | 17 | ||||||||||||

| Ohio |

26 | 2 | — | 28 | ||||||||||||

| Pennsylvania |

14 | 4 | — | 18 | ||||||||||||

| South Carolina |

6 | 1 | — | 7 | ||||||||||||

| Tennessee |

11 | — | — | 11 | ||||||||||||

| Virginia |

15 | — | — | 15 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| 173 | 35 | — | 208 | |||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

Market and Site Selection. We target markets that meet our demographic and competitive criteria, including areas that demonstrate above average economic growth and household incomes, and home ownership rates. Our target markets typically include most or all of our major competitors. When considering new sites, we analyze total store and market potential and advertising and occupancy costs for a market, as well as proximity to distribution facilities. Within our markets, we open or acquire our stores in power centers or freestanding locations in high traffic areas, usually near our major competitors. Primary site evaluation criteria include total sales volume potential, co-tenancies, traffic patterns, visibility, access, parking availability and occupancy costs.

21

Table of Contents

We initially open multiple stores in a new market and add stores to the market over time to increase market share and improve the leverage of our fixed costs. We plan to continue to open or acquire stores in new and existing markets.

Store Development. In the past five years, we have successfully entered 14 new metropolitan markets, most recently in Chicago, Illinois and Miami, Florida. Historically, we have been able to locate and open stores profitably in a wide variety of trade areas by negotiating lease terms that we believe are favorable. Approximately 12 to 18 months are required for site approval, lease negotiation, property build out, the hiring and training of associates and the stocking of inventory before the opening of a store. This timeframe can be reduced to six to nine months when no new property build-out is required. In fiscal 2013, we plan to open 20 to 22 new stores, predominately in the markets of St. Louis, Missouri and Milwaukee, Wisconsin.

We generally lease new stores through build-to-suit arrangements, whereby a landlord develops a building shell for long-term rental to us. This strategy significantly reduces our capital outlay for new store construction by limiting our capital outlay to furniture, fixtures and equipment. Additionally, we occasionally execute a sale and leaseback on stores not developed through a build-to-suit program. Through this sale and leaseback process, in which the land, building and/or leasehold improvements are sold to a third party and leased back to us on a single tenant basis, much of the construction cost associated with a new store can be deferred and recognized over a long-term rental period, which is generally 10 to 15 years.

22

Table of Contents

| ITEM 3. | Legal Proceedings. |

We are engaged in various legal proceedings in the ordinary course of business and have certain unresolved claims pending. Although we diligently defend against these claims, we may enter into discussions regarding settlement of these and other lawsuits and may enter into settlement agreements, if we believe settlement is in the best interests of our company and our stockholders. The ultimate liability, if any, for the aggregate amounts claimed cannot be determined at this time. However, management believes, based on the examination of these matters and experiences to date, that the ultimate liability, if any, in excess of amounts already provided for in the consolidated financial statements is not likely to have a material effect on our consolidated financial position, results of operations or cash flows.

| ITEM 4. | Mine Safety Disclosures. |

Not applicable.

23

Table of Contents

| ITEM 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. |

Our common stock is traded on the New York Stock Exchange under the ticker symbol HGG. The table below sets forth the high and low sales prices of our common stock as reported on the New York Stock Exchange — Composite Index during the periods indicated.

| Stock Price | ||||||||

| High | Low | |||||||

| Fiscal 2012 |

||||||||

| Fourth Quarter |

$ | 13.81 | $ | 10.03 | ||||

| Third Quarter |

16.45 | 9.48 | ||||||

| Second Quarter |

13.64 | 9.75 | ||||||

| First Quarter |

15.47 | 12.02 | ||||||

| Fiscal 2011 |

||||||||

| Fourth Quarter |

$ | 21.97 | $ | 13.16 | ||||

| Third Quarter |

26.03 | 20.95 | ||||||

| Second Quarter |

25.00 | 18.90 | ||||||

| First Quarter |

30.22 | 23.32 | ||||||

We did not pay cash dividends on our common stock during the last two fiscal years and do not expect to pay cash dividends in the near future. In addition, the terms of our credit facilities place restrictions on our ability to pay dividends and otherwise transfer assets to our stockholders. See “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations-Liquidity and Capital Resources”. As of April 30, 2012, there were 76 holders of record of our common stock (which does not include the number of individual beneficial owners whose shares were held on their behalf by brokerage firms in street name).

24

Table of Contents

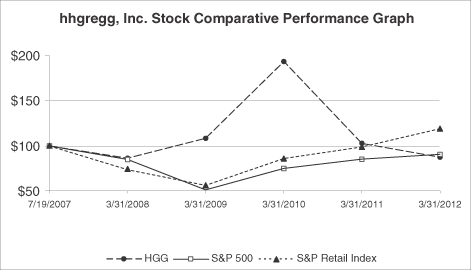

hhgregg Stock Comparative Performance Graph

The information contained in this hhgregg Stock Comparative Performance Graph section shall not be deemed to be “soliciting material” or “filed” or incorporated by reference in future filings with the SEC, or subject to the liabilities of Section 18 of the Exchange Act, except to the extent that we specifically incorporate it by reference into a document filed under the Securities Act of 1933 or the Exchange Act.