Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - HERITAGE FINANCIAL CORP /WA/ | d348198d8k.htm |

D.A. Davidson

D.A. Davidson

14

14

Financial Services Conference

Financial Services Conference

May 2012

May 2012

Brian L. Vance, President and CEO

Jeffrey J. Deuel, Executive Vice President and COO

Donald J. Hinson, Senior Vice President and CFO

Exhibit 99.1

th

th |

2

This presentation contains forward-looking statements that are subject to

risks and uncertainties, including, but not limited to: The credit and

concentration risks of lending activities Changes in general economic

conditions, either nationally or in our market areas Competitive market

pricing factors and interest rate risks Market interest rate

volatility Balance sheet (for example, loans) concentrations

Fluctuations in demand for loans and other financial services in our market

areas Changes in legislative or regulatory requirements or the results

of regulatory examinations The ability to recruit and retain key

management and staff Risks associated with our ability to implement our

expansion strategy and merger integration Stability of funding sources

and continued availability of borrowings Adverse changes in the

securities markets The inability of key third-party providers to

perform their obligations to us Changes in accounting policies and

practices and the use of estimates in determining fair value of certain of our

assets, which estimates may prove to be incorrect and result in significant

declines in valuation; and These and other risks as may be detailed from

time to time in our filings with the Securities and Exchange

Commission.

The Company cautions readers not to place undue reliance on any

forward-looking statements. Moreover, you should treat these

statements as speaking only as of the date they are made and based only on information then actually known to the

Company. The Company does not undertake and specifically disclaims any

obligation to revise any forward-looking statements to reflect the

occurrence of anticipated or unanticipated events or circumstances after

the date of such statements. These risks could cause our actual results

for 2012 and beyond to differ materially from those expressed in any forward-looking

statements by, or on behalf of, us, and could negatively affect the

Company’s operating and stock price performance. Forward Looking

Statement |

•

Company Information

•

Financial Performance

•

Corporate Strategies

3

Overview |

Company Information

Company Information

4 |

Our Market Area

5

Financial Data as of March 31, 2012

Total assets: $1.21 billion

Total assets: $167.8 million

Branches: 27

Branches: 6 |

Company Overview

•

Providing financial services for the region since 1927

•

Commercial bank with strong ties to the communities

we serve

•

A full range of services for businesses and consumers

•

Positioned for future growth in the Seattle/Bellevue

and Vancouver/Portland markets

•

Focused on our mission of customer satisfaction,

employee empowerment, and shareholder value

6 |

Award Recognition

7

•

Top Places to Work

•

Washington Best Workplaces

•

The 100 Best Companies to Work For

Business Examiner –

2012 -

Large Company & Appreciation Awards and

2009 Large Company & Equity Award

Puget Sound Business Journal –

Gold Award 2011, Bronze Award 2010 and

Silver Award 2009

The

Seattle

Business

Magazine –

2nd

Midsized

Companies

for

2010 |

Award Recognition

8

Publically

Traded

Pacific

Northwest

Companies

-

Debt

Free

for

2009

Washington State Financial Services Champion of the Year

Seattle District of the US Small Business Administration for 2010 and

2009 Best Bank in the South Sound

The Olympian -

Heritage Bank for years 2011, 2010 & 2008

Best of the Northwest

The Seattle Times -

Top 20 Companies of the Decade for 2009

Business Excellence Award

The

Greater

Yakima

Chamber

of

Commerce

-

Central

Valley

Bank

in

2009

Business of the Year Award

The

Greater

Yakima

Chamber

of

Commerce

-

Central

Valley

Bank

in

2010 |

Financial Performance

Financial Performance

9 |

Balance Sheet Growth

10

75%

80%

85%

90%

95%

100%

105%

$

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

2007

2008

2009

2010

2011

Q1 2012

Loans

Deposits

Total Assets

% Loans to Deposits |

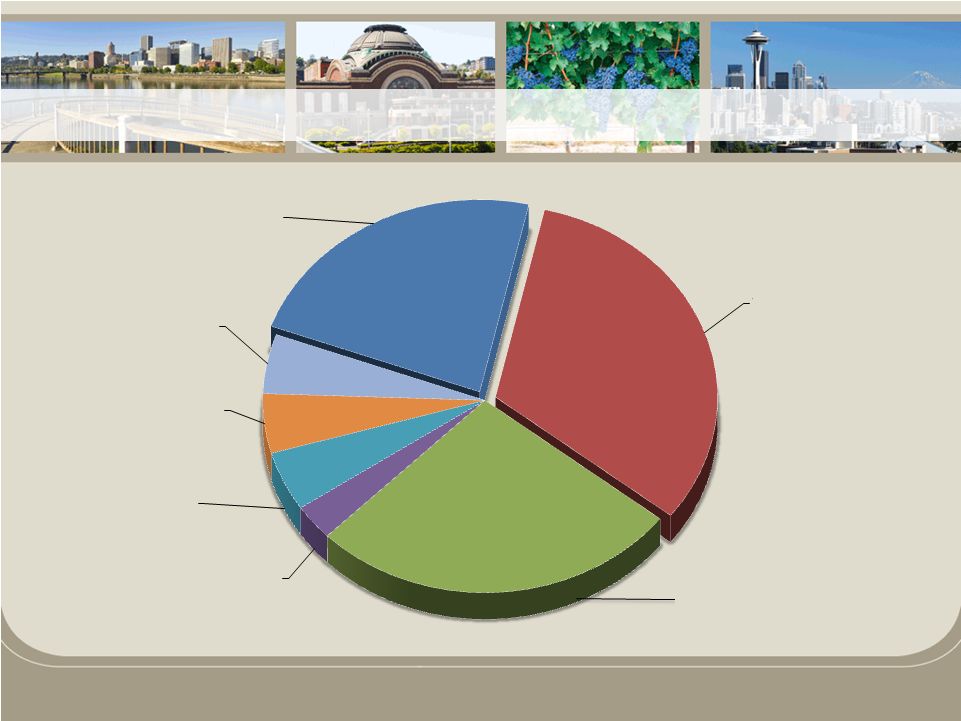

Diversified Loan Portfolio

11

Financial data as of March 31, 2012

CRE Owner

Occupied

23%

Consumer

5%

Residential

Real Estate

5%

Commercial

Construction

5%

Residential

Construction

3%

CRE Non-Owner

Occupied

27%

Commercial &

Industrial

32% |

Credit Quality

12

* HFWA ratios relate to originated loan portfolios only. Regional Peer data not

available for Q1’12 Regional

Peer

Group

(12):

Ticker

Symbols

–

BANR,

CACB,

COLB,

FFNW,

HOME,

NRIM,

PCBK,

PRWT,

RVSB,

TSBK,

WBCO,

WCBO

Source: SNL Financial

0%

3%

6%

9%

Q1'10

Q2'10

Q3'10

Q4'10

Q1'11

Q2'11

Q3'11

Q4'11

Q1'12

HFWA

Regional Peers

NPAs/Assets (%)

0%

40%

80%

120%

160%

Q1'10

Q2'10

Q3'10

Q4'10

Q1'11

Q2'11

Q3'11

Q4'11

Q1'12

Reserves/NPLs (%)

HFWA

Regional Peers |

Attractive Deposit Base

13

Financial data as of March 31, 2012

Non-Maturity

Deposits

/

Total

Deposits

CDs

27.6%

Non-

Interest

Demand

20.6%

Interest

Checking

(NOW)

26.3%

Money Market

15.3%

Savings

10.2%

Total

Deposits

0.46%

72.4%

Cost

of

Interest

Bearing

Deposits

0.57%

Cost

of

Deposits

$1.1

billion |

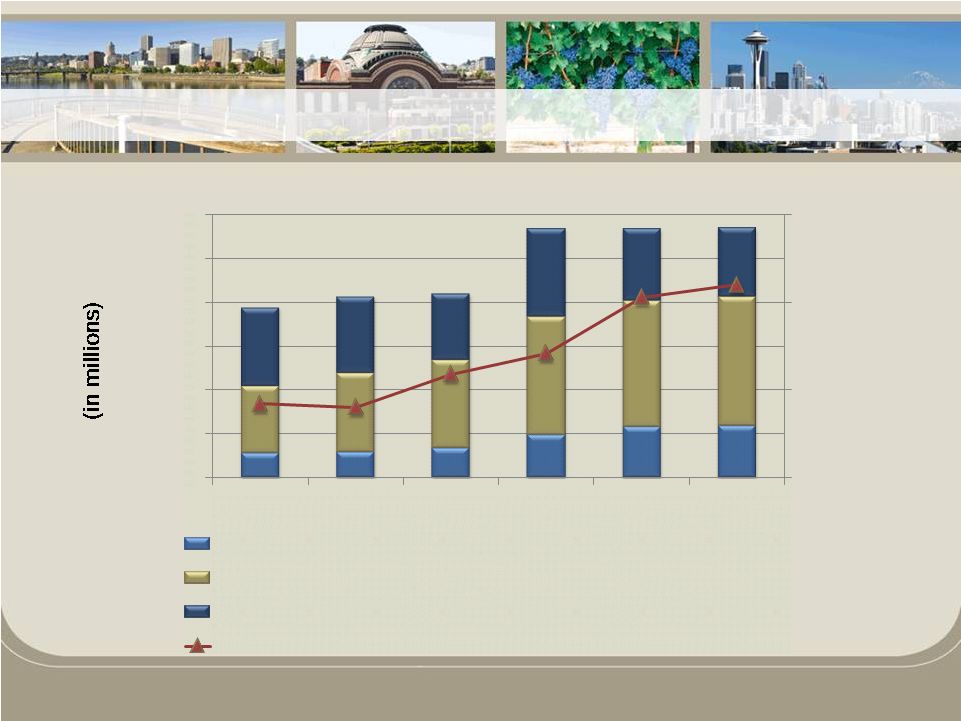

Core Deposit Growth

14

10%

15%

20%

25%

$-

$200

$400

$600

$800

$1,000

$1,200

2007

2008

2009

2010

2011

Q1 2012

Non-Interest Demand Deposits

NOW/Savings/MMA

Certificate of Deposit

% of Non-Interest Demand Deposits to Total Deposits

|

Equity Growth

15

$85.0

$113.1

$158.5

$202.3

$202.5

5%

10%

15%

$-

$20

$40

$60

$80

$100

$120

$140

$160

$180

$200

$220

2007

2008

2009

2010

2011

Q1 2012

Total Equity

Tangible Common Equity/Tangible Assets

$205.7 |

Earnings

Net Income

Quarterly Net Income

16

$10.7

$6.4

$0.6

$13.4

$6.5

$-

$2

$4

$6

$8

$10

$12

$14

$16

2007

2008

2009

2010

2011

$0.8

$1.7

$1.8

$2.2

$4.2

$-

$1.0

$2.0

$3.0

$4.0

$5.0

Q1'11

Q2'11

Q3'11

Q4'11

Q1'12 |

Net Interest Margin

Annual NIM

Quarterly NIM

17

Adjusted

Net

Interest

Margin

removes

the

effects

of

“incremental

accretion

income”

from

net

interest

income

in

the

net

interest

margin

calculation.

“Incremental

accretion

income”

represents

the

amount

of

income

recorded

on

the

acquired

loans

above

the

contractual

stated

interest

rate of the individual loan notes.

This income stems from the discount established at the time these loan

portfolios were acquired and modified as a result of quarterly cash flow

re-estimations. 4.0%

4.5%

5.0%

5.5%

6.0%

2007

2008

2009

2010

2011

Net

Interest

Margin

Adjusted

Net

Interest

Margin

4.0%

4.5%

5.0%

5.5%

6.0%

Q1'11

Q2'11

Q3'11

Q4'11

Q1'12

Net

Interest

Margin

Adjusted

Net

Interest

Margin |

Operating Expenses

18

60%

65%

70%

75%

$-

$2

$4

$6

$8

$10

$12

$14

$16

Q1 2011

Q2 2011

Q3 2011

Q4 2011

Q1 2012

Salaries & Benefits

Occupancy

Other

Efficiency Ratio |

Corporate Strategies

Corporate Strategies

19 |

Growth Initiatives

•

Organic Growth

–

Lender recruitment

–

Strategic branching

–

Develop Southwest Washington

–

Launch Wealth Management initiative

•

Targeted Acquisitions

–

Enhance Pacific Northwest footprint

20 |

Growth Initiatives

•

Lender Recruitment

–

During 2011 we hired 7 new Lenders and a

Market Executive

•

3 lenders in King County (Seattle/Bellevue/Kent)

•

2 lenders in Pierce County (Tacoma)

•

1 lender in Thurston County (Olympia)

•

1 lender in Portland, OR

•

1 Market Executive for Vancouver, WA / OR

–

Continue to recruit Lenders

21 |

Growth Initiatives

•

Originated Loan Growth

–

Increased $35 million, or 4.4%, in Q4 2011

–

Increased

net

loans

$20.2

million,

or

2.0%,

in

2011

–

Increased originated loans $95.9 million, or 12.9%,

in 2011

–

Originated loan growth was flat in Q1 2012

22 |

Growth Initiatives

•

Core deposits

–

Non-maturity deposits (total deposits less CDs)

•

Increased $73.1 million, or 10.0%, during 2011

•

Non-maturity deposits increased to 71.0% of total

deposits

•

Demand deposits increased $36.4 million, or 18.7%,

during 2011

•

Demand deposits increased to 20.4% of total deposits,

as of 12/31/11

•

Trends continue in 2012

23 |

Growth Initiatives

•

Deposits at acquired branches reporting

steady growth since acquisition

–

Former Cowlitz Bank branches (acquired in

July 2010) increased deposits by 19.5%

during 2011

24 |

Growth Initiatives

25

•

Wealth Management

–

Trust services added in Cowlitz Bank transaction

–

Wealth Management leader joined team in 2011

–

Goal to align existing Trust and Brokerage Services with

new Investment Management Services to create

integrated Wealth Management platform

–

Serve the clients on both sides of their balance sheet

with responsive credit products as well as

comprehensive asset management services

–

Relatively low capital requirements, fee income from

organic growth, and growth through acquisitions |

Leverage Capital

•

FDIC Acquisitions

–

Successfully completed two FDIC acquisitions

–

Continue to consider future FDIC assisted

transactions

–

Expect very few closures in WA/OR in 2012

•

Bank Mergers and Acquisitions

–

Actively seeking M&A opportunities

26 |

Capital Management Strategies

Cash Dividends

Stock Repurchases

Announced 5% repurchase program in Q3 2011

Since inception, repurchased 210,205 shares (27%

of repurchase program at an average price of $11.68)

27

2011

2012

Q2

Q3

Q4

Q1

Q2

Quarterly

Dividend

$0.03

$0.05

$0.05

$0.06

$0.08

Special

Dividend

-

-

$0.25

-

- |

Conclusion

Conclusion

28 |

Core Strategies

29

Maintain

Disciplined

Approach

Continue

Growth

Initiatives

Leverage

Capital

Manage Core

Business |

Investment Value

•

Strong financial performance trends

•

Well-positioned to take advantage of the right

opportunities

•

Continuing focus on building long-term

franchise value

•

Disciplined approach to acquisitions

•

Experienced management team supported by

a strong Board of Directors

30 |

Thank You

Thank You

Questions?

Questions?

Heritage Financial Corporation

Heritage Financial Corporation |