Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - CYS Investments, Inc. | d348301d8k.htm |

Exhibit

99.1 UBS Global Financial Services Conference

May 8, 2012

Investment Outlook

May 2012 |

Forward

Looking Statements This presentation contains forward-looking statements,

within the meaning of Section 27A of the Securities Act of 1933, as amended,

and Section 21E of the Securities Exchange Act of 1934, as amended, that are

based on management’s beliefs and assumptions, current expectations,

estimates and projections. Such statements, including information relating to the Company’s

expectations

for

future

distributions

and

market

conditions,

are

not

considered

historical

facts

and

are

considered

forward-looking

information

under

the

federal

securities

laws.

This

information

may

contain

words

such

as

“believes,”

“plans,”

“expects,”

“intends,”

“estimates”

or similar expressions.

This information is not a guarantee of the Company’s future performance and is

subject to risks, uncertainties and other important factors that could cause

the Company’s actual performance or achievements to differ materially from those expressed

or implied by this forward-looking information and include, without limitation,

changes in the Company’s distribution policy, changes in the

Company’s ability to pay distributions, changes in the market value and yield of our assets, changes in interest

rates and the yield curve, net interest margin, return on equity, availability and

terms of financing and hedging and various other risks

and

uncertainties

related

to

our

business

and

the

economy,

some

of

which

are

described

in

our

filings

with

the

SEC.

Given

these uncertainties, you should not rely on forward-looking information.

The Company undertakes no obligations to update any forward-looking

information, whether as a result of new information, future events or otherwise.

1 |

CYS:

Overview Agency Residential Mortgage Backed Securities

Currently

financing

lines

with

33

lenders

Swap agreements with 18 counterparties

Self managed: highly scalable

Kevin Grant, CEO, President, Chairman

Frances Spark, CFO

Pay dividends and achieve capital appreciation throughout changing interest

rate and credit cycles

Be the most efficient Agency REIT in the market

Company intends to distribute all or substantially all of its REIT taxable

income 2

A Real Estate Investment Trust formed in January 2006

Target Assets

Objective

Senior Management

Focus on Cost

Efficiency

Ample Financing

Sources

Dividend Policy |

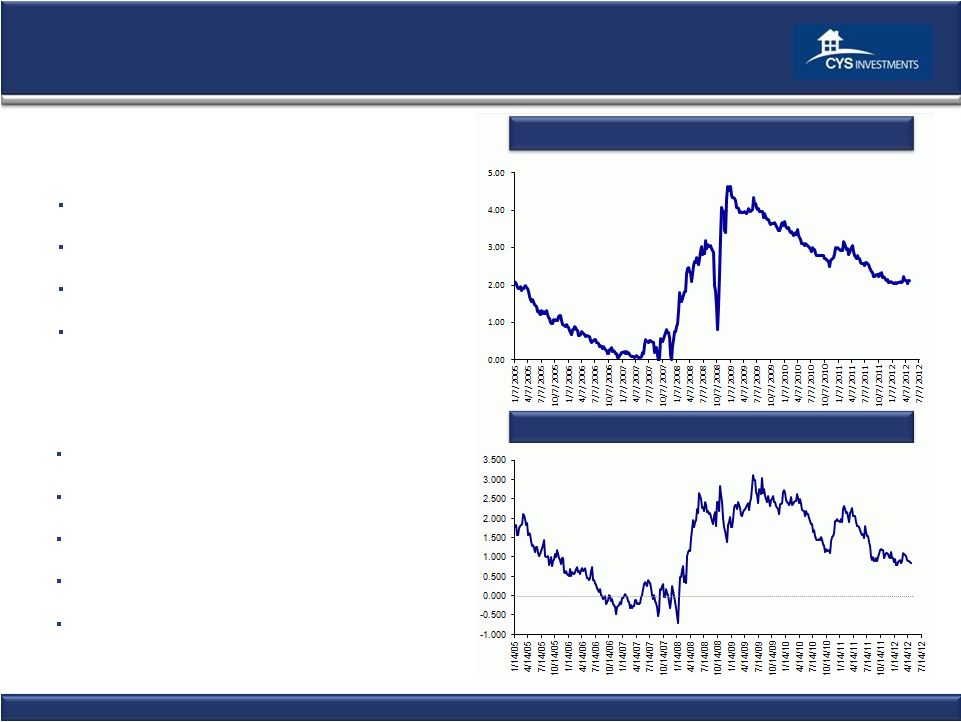

Attractive Environment Likely to Persist

Steep Curve

Creates significant positive carry

Very low cost of financing

Significant ROE

Hedge flexibility very important

Fed still fighting deflation

5 Year

Swap

vs.

1

Month

LIBOR:

1/2005

–

5/1

Hybrid

Net

Interest

Margin:

1/2005

–

Source: Bloomberg

(1) May 4, 2012

Mortgage Yields Currently Attractive

Par-Priced

7/1

hybrid

rates

now

1.62%

(1)

30

Year

fixed

rates

now

2.97%

(1)

15

Year

fixed

rates

now

2.28%

(1)

Hedging rates historically low

May 4, 2012

May 4, 2012

3

5/2012

5/2012 |

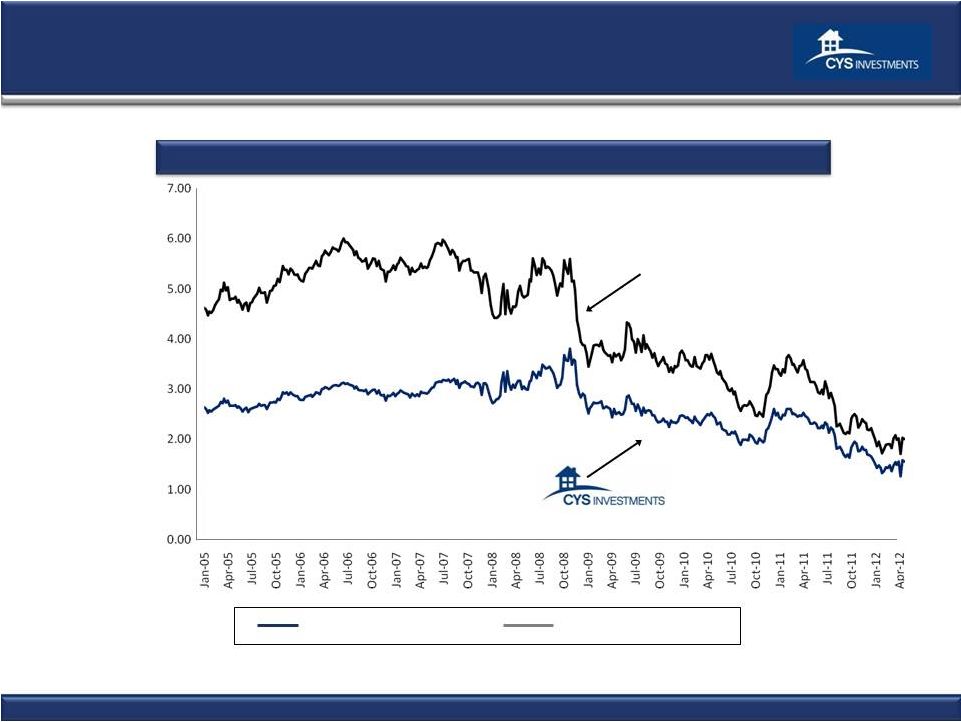

Attractive Investment Environment Remains

15 Year Hedged

(i)

15 Year Unhedged

(ii)

Borrow Short

Invest Long

May 4, 2012

15

Year

Fixed

Hedged

with

Swaps:

1/1/2005

–

5/4/2012

4

Source: Bloomberg.

Note: Spreads calculated as: (i) 15 year CC

Index = 50% 4 year swap, and (ii) 15 year Current Coupon Index |

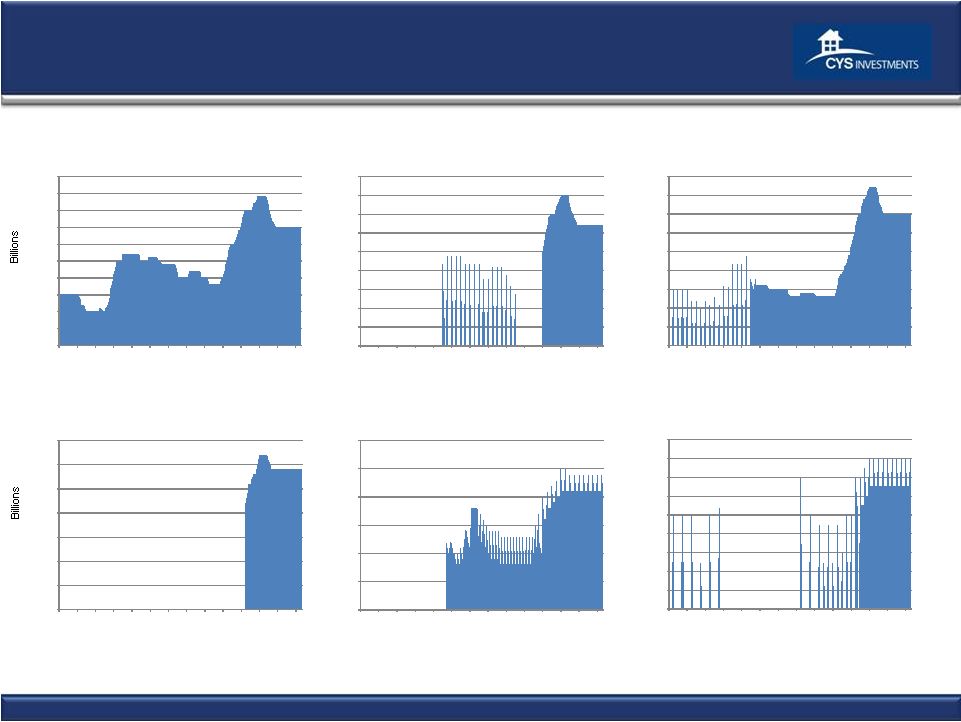

10 Year

Treasury Note Auctions 11/98 –

3/12

Treasury Auction Volume

2 Year Treasury Note Auctions

2/98 –

3/12

3 Year Treasury Note Auctions

10/98 –

3/12

Source: Bloomberg, US Treasury

5 Year Treasury Note Auctions

2/98 –

3/12

7 Year Treasury Note Auctions

2/00 –

3/12

30 Year Treasury Note Auctions

2/00–

3/12

0

5

10

15

20

25

30

35

40

45

50

Nov

'98

Nov

'99

Nov

'00

Nov

'01

Nov

'02

Nov

'03

Nov

'04

Nov

'05

Nov

'06

Nov

'07

Nov

'08

Nov

'09

Nov

'10

Nov

'11

0

5

10

15

20

25

30

35

40

45

Nov

'98

Nov

'99

Nov

'00

Nov

'01

Nov

'02

Nov

'03

Nov

'04

Nov

'05

Nov

'06

Nov

'07

Nov

'08

Nov

'09

Nov

'10

Nov

'11

0

5

10

15

20

25

30

35

40

45

Nov

'98

Nov

'99

Nov

'00

Nov

'01

Nov

'02

Nov

'03

Nov

'04

Nov

'05

Nov

'06

Nov

'07

Nov

'08

Nov

'09

Nov

'10

Nov

'11

0

5

10

15

20

25

30

35

Nov

'98

Nov

'99

Nov

'00

Nov

'01

Nov

'02

Nov

'03

Nov

'04

Nov

'05

Nov

'06

Nov

'07

Nov

'08

Nov

'09

Nov

'10

Nov

'11

0

5

10

15

20

25

30

Nov

'98

Nov

'99

Nov

'00

Nov

'01

Nov

'02

Nov

'03

Nov

'04

Nov

'05

Nov

'06

Nov

'07

Nov

'08

Nov

'09

Nov

'10

Nov

'11

0

2

4

6

8

10

12

14

16

18

Nov

'98

Nov

'99

Nov

'00

Nov

'01

Nov

'02

Nov

'03

Nov

'04

Nov

'05

Nov

'06

Nov

'07

Nov

'08

Nov

'09

Nov

'10

Nov

'11

5 |

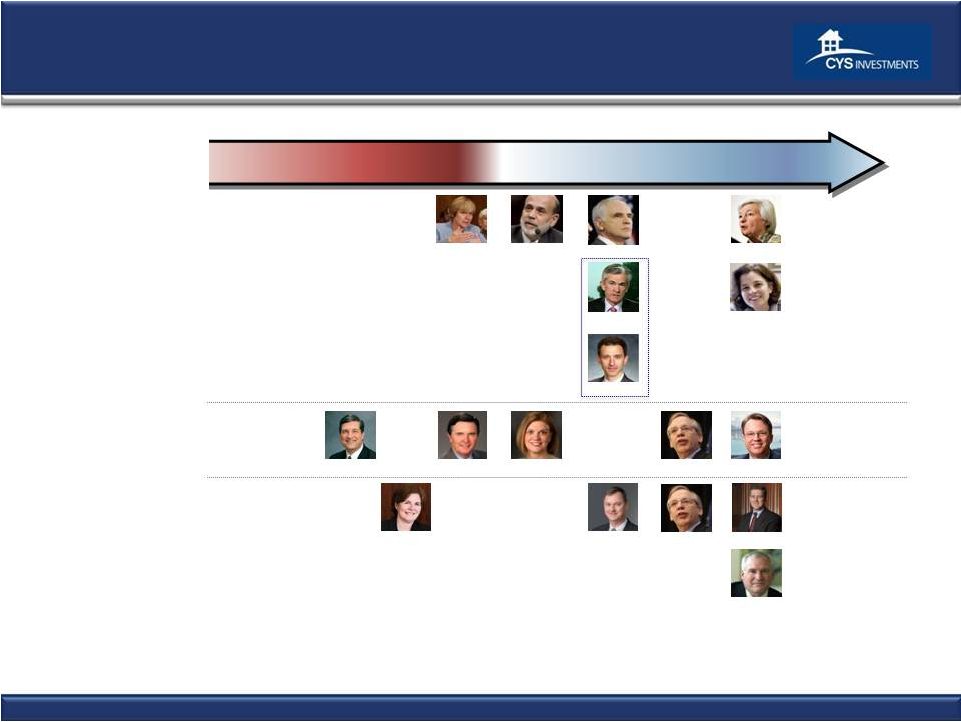

Hawkish

Dovish

Neutral

Lacker

Duke

Tarullo

Lockhart

Pianalto

Yellen

Raskin

Bernanke

Governors

2012 Voters

Fed Voters Moving To Be Even More Dovish in 2012

Williams

2013 Voters

Dudley

Evans

Rosengren

Bullard

Powell

Stein

Obama

Nominees

Sources: federalreserve.gov, Macroeconomic Advisers, LLC, Bank of America

Merrill Lynch, Bloomberg, Wall Street Journal, Indiana University, Marketwatch, Thomson Reuters, Federal Reserve Bank of Atlanta, Federal Reserve Bank of Chicago, Federal

Reserve Bank of Cleveland, Maryland Consumer Rights Coalition, Boston Globe,

Businessweek, Newsweek, Washington Post, CNBC. Dudley

George

6 |

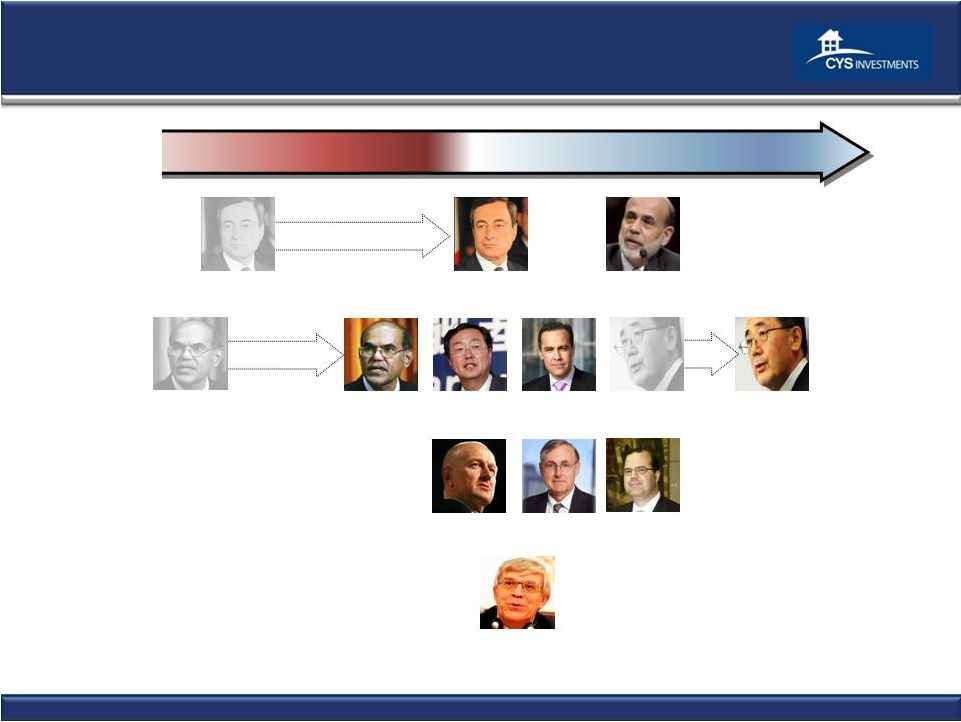

The Brief

Hawkish Interlude Appears Over Xiaochuan

China

Bernanke

Shirakawa

Japan

Canada

Carney

Australia

Stevens

New Zealand

Bollard

Draghi

EU

Tombini

Brazil

Subbarao

India

Global Accommodation Has Reluctantly Restarted

Hawkish

Dovish

Neutral

Draghi

EU

Ignatiev

Russia

Shirakawa

Japan

Subbarao

India

USA

7 |

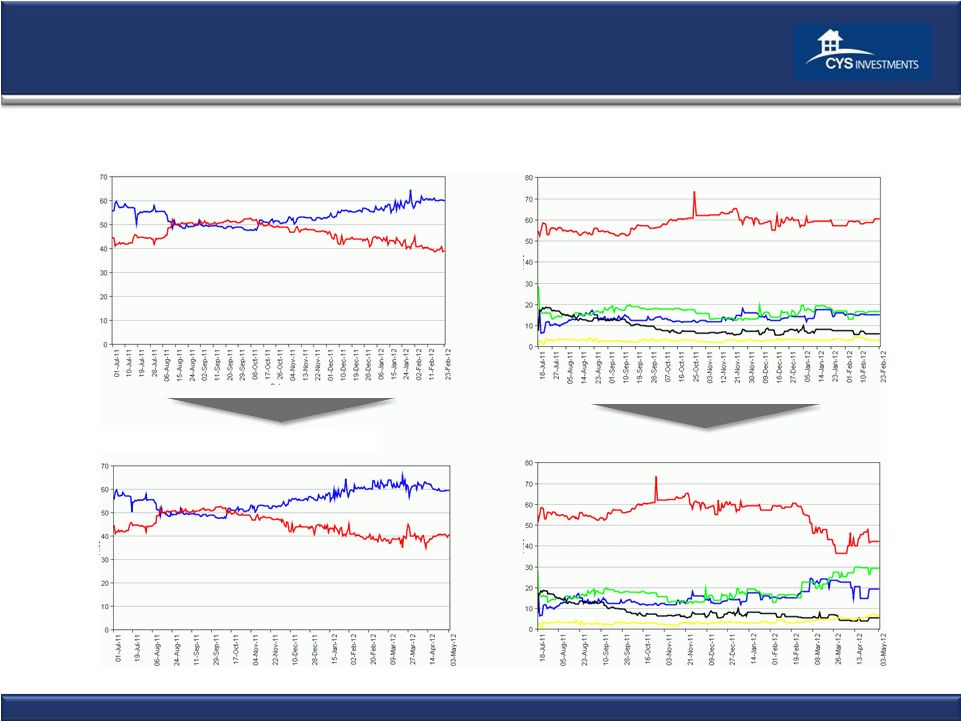

The Iowa

Electronic Futures Market: Obama Re-elected and a Republican Congress

Democrat

Republican

Republican House/

Republican Senate

Republican House/

Democrat Senate

Democrat House/

Democrat Senate

Democrat House/

Republican Senate

Source: The Iowa Electronic Markets

2012

US

Presidential

Election

Winner-Takes-All

Market

2012 Congressional Control Winner-Takes-All Market

As of February 29

As of February 29

As of May 3

As of May 3

Republican House/

Democrat Senate

Democrat House/

Democrat Senate

Democrat House/

Republican Senate

Republican House/

Republican Senate

Democrat

Republican

8 |

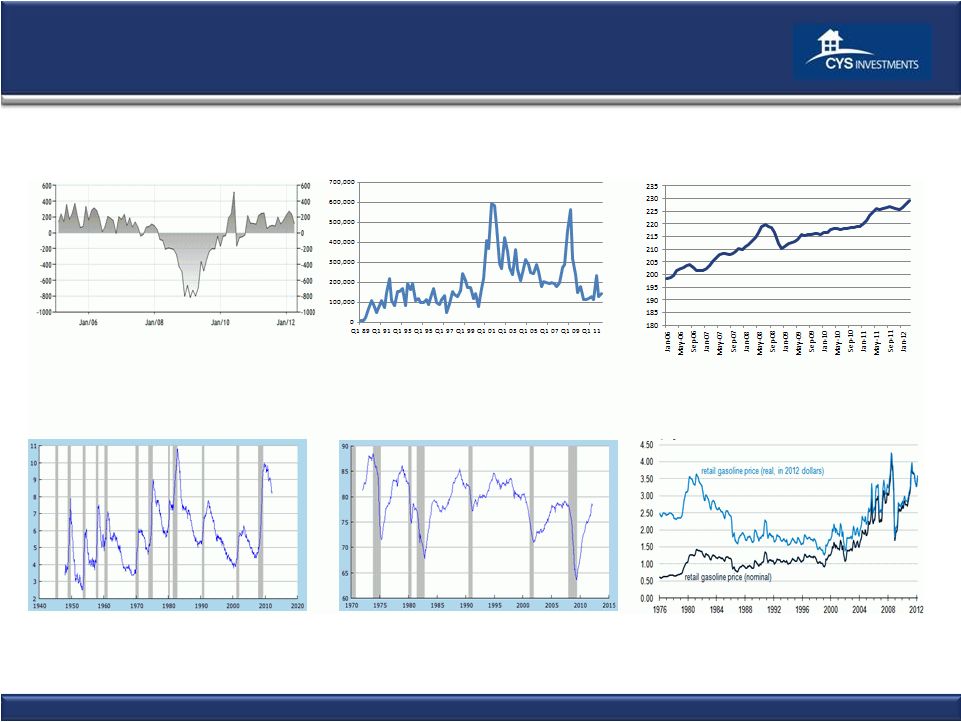

Source: S&P, Fiserv, and Macromarkets LLC / Haver Analytics, BLS, Challenger,

Gray & Christmas, US Dept. of Energy, NYMEX U.S. Retail Gasoline Price, Regular

Grade 1976 –

Present

Capacity Utilization: Manufacturing

1972 –

Present

%

Civilian Unemployment Rate

1947 -

present

%

Economic Recovery Below Normal Pace

CPI-U All Items, Core

2006 –

Present

% Change -

Year to Year

Total Nonfarm Private Payroll Employment

2005-present

000’s

Challenger, Gray & Christmas, Inc.

Job Cut Announcement Report

1/2007 –

3/2012, by Quarter

9 |

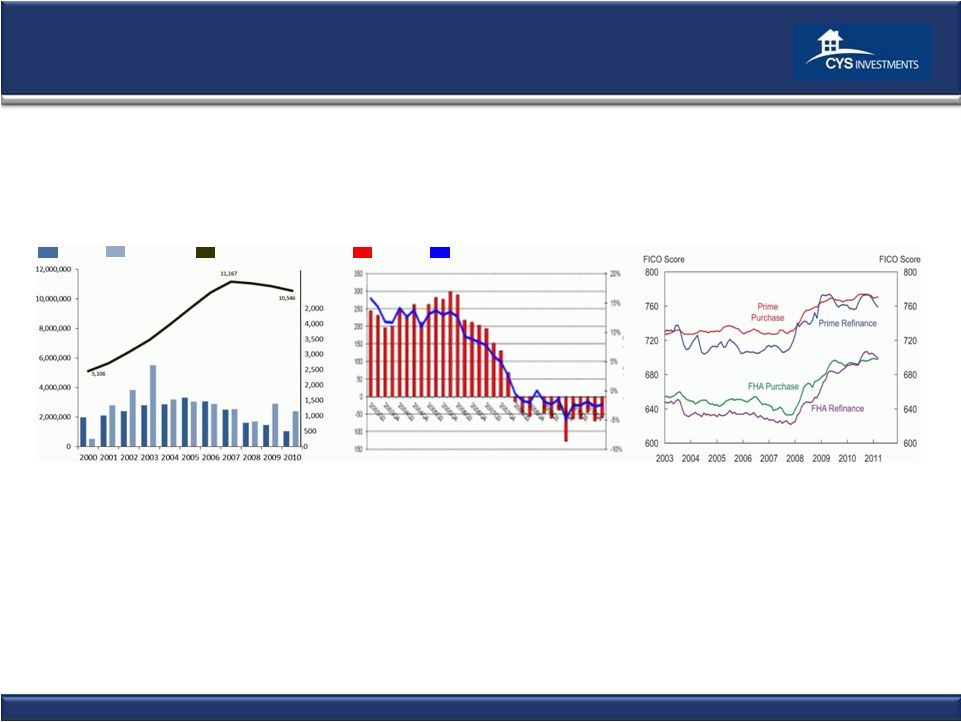

Mortgage

Market Shrinkage Likely to Continue Residential Mortgage Debt Decline Driven By:

1.

Declining home prices

2.

Delevering Consumers/Homeowners

3.

Psychology of lower leverage

4.

Low volume of new and existing home sales

5.

All-cash home purchase transactions, and higher downpayments

6.

Scheduled principal payments

7.

High percentage of cash-in refis versus cash-out refis.

Quarterly Growth in

Residential Mortgage Debt

Q2 2003 –

Q4 2010

Growth

Net Issuance

Home Mortgage Originations

2000 -

2010

In billions

Refinance

Purchase

Home Mortgage Debt

Outstanding

2000 -

2010

In millions

Total Home Mortgage Debt

Median Credit Score at

Mortgage Origination

2003-2012

Source: BLS, LPS Applied Analytics, Financial Stability Oversight Council 2011 Annual

Report 10 |

11

11

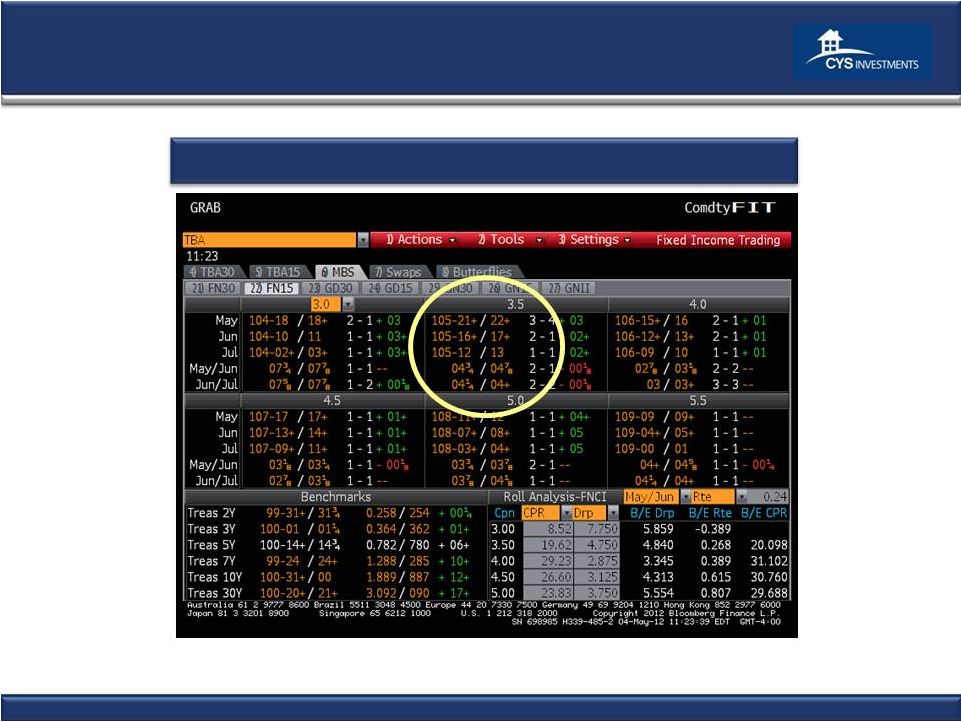

Economics of Forward Purchase

Example:

15

yr.

3½%

drop

=

~4

3/4

/32

pt.

per

month

1

Source: Bloomberg 05/04/12

1

4

3/4

/32 represents a discount to the purchase price of the security of approximately $0.30 per month from

trade date to settlement date. |

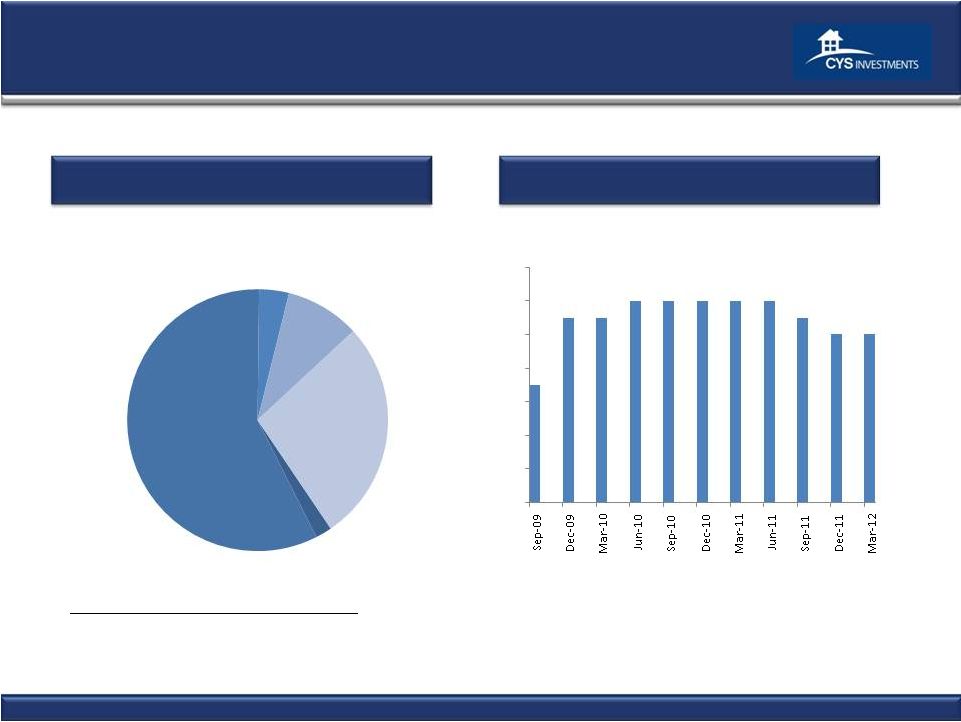

Portfolio Composition and Results

CYS Agency RMBS Portfolio

1

As of 3/31/12

15 Year Fixed

Total Agency RMBS: $13,307.4 million

30 Year

Fixed Rate,

9%

Hybrid ARMs,

27%

Rate, 58%

10 Year Fixed

Rate, 2%

20 Year Fixed

Rate, 4%

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.35

0.55

0.55

0.60

0.60

0.60

0.60

0.60

0.55

0.50

0.50

12

1

CYS Dividends: 9/09 –

4/12 |

Portfolio Characteristics

* As of 3/31/11

13

CYS Agency RMBS Portfolio Characteristics*

(1)

MTR, or “Months to Reset,” is the number of months remaining before the fixed rate on a

hybrid ARM becomes a variable rate. At the end of the fixed period, the variable rate

will be determined by the margin and the pre-specified caps of the ARM. After the fixed period, the interest rates on

100% of our hybrid ARMs reset annually. (2) CPR, or

“Constant Prepayment Rate,” is a method of expressing the prepayment rate for a mortgage pool that assumes that a constant fraction of

the remaining principal is prepaid each month or year. Specifically, the CPR is an annualized version

of the prior three month prepayment rate. Securities with no prepayment history are

excluded from this calculation.

(3) Weighted average months to reset of our hybrid ARM

portfolio.

Par Value

Fair Value

Asset Type

Cost/Par

Fair

Value/Par

MTR

(1)

Coupon

CPR

(2)

10 Year Fixed Rate

$256,373

$269,227

$103.88

$105.01

N/A

3.50%

13.8%

15 Year Fixed Rate

7,306,193

7,666,261

103.05

104.93

N/A

3.54%

14.8%

20 Year Fixed Rate

460,938

489,662

102.36

106.23

N/A

4.16%

21.8%

30 Year Fixed Rate

1,132,244

1,225,193

106.90

108.21

N/A

5.09%

26.5%

Hybrid ARMs

3,493,632

3,657,100

102.54

104.68

65.9

3.19%

20.1%

Total/Weighted Average

$ 12,649,380

$13,307,443

$103.24

$ 105.20

65.9

(3)

3.61%

17.3%

Weighted Average

(in thousands) |

History

of Transparent and Consistent Financial Reporting

CYS uses Financial Reporting for Investment Companies

CYS

financial

reporting

-

Best

in

Class

Schedule of investments

NAVs have reflected mark-to-market accounting since inception

No OCI account on balance sheet

Realized and unrealized losses taken through income statement

Losses expensed in period incurred

14 |

15

Historical Financials

3/31/2012

12/31/2011

Income Statement Data (in 000's)

Investment Income – Interest Income

$65,369

$61,631

Total expenses

11,972

10,510

Net Investment Income

53,397

51,121

Net gain (loss) from investments

33,150

(8,587)

Net gain (loss) from swap and cap contracts

(17,429)

1,559

Net Income

$69,118

$44,093

Net Income Per Common Share (diluted)

$0.66

$0.53

Distributions per Common Share

$0.50

$0.50

Non-GAAP Measure (in 000's)

Core Earnings

(1)

$41,891

$37,836

Non-GAAP Reconciliation (in 000's)

NET INCOME

$69,118

$44,093

Net (gain) loss from investments

(33,150)

8,587

Net (gain) loss on termination of swap contracts

--

1,411

Net unrealized (appreciation) depreciation on swap

and cap contracts

5,923

(16,255)

Core Earnings

$41,891

$37,836

Key Portfolio Statistics*

Average yield on Agency RMBS

(2)

2.78%

2.81%

Average cost of funds and hedge

(3)

0.90%

1.01%

Interest rate spread net of hedge

(4)

1.88%

1.80%

Operating expense ratio

(5)

1.46%

1.53%

Leverage ratio (at period end)

(6)

7.7:1

7.7:1

Balance Sheet Data (in 000's)

3/31/2012

12/31/2011

Cash and Cash Equivalents

$10,643

$11,508

Total Assets

$13,555,905

$9,518,057

Repurchase Agreements

$8,234,669

$7,880,814

Net assets

$1,525,792

$1,077,458

Net assets per common share

$13.14

$13.02

Three Months Ended

As of

(1) Core Earnings is defined as net income (loss) excluding net gain (loss) on investments, net

realized gain (loss) on termination of swap contracts and unrealized appreciation (depreciation) on swap and cap contracts.

(2) Our average yield on Agency RMBS for the period was calculated by dividing our interest income

from Agency RMBS by our average Agency RMBS.

(3) Our average cost of funds and hedge for the period was calculated by dividing our total interest

expense, including our net swap and cap interest income (expense), by our average repurchase agreements.

(4) Our interest rate spread net of hedge for the period was calculated by subtracting our average

cost of funds and hedge from our average yield on Agency RMBS.

(5) Our operating expense ratio is calculated by dividing operating expenses by average net

assets.

(6) Our leverage ratio was calculated by dividing (i) the Company’s repurchase agreements balance

plus payable for securities purchased minus receivable for securities sold by (ii) net assets.

* All percentages are annualized.

|

Financial Highlights

Steep yield curve and attractive spreads in target assets

Tailwinds likely to continue

Fed Transparency very helpful

Investment Company accounting provides transparency

16 |

UBS

Global Financial Services Conference May 8, 2012

Investment Outlook

May 2012 |