Attached files

| file | filename |

|---|---|

| EX-21.1 - EXHIBIT 21.1 - Tri-Tech Holding, Inc. | dex211.htm |

| EX-99.2 - EXHIBIT 99.2 - Tri-Tech Holding, Inc. | dex992.htm |

| EX-23.1 - EXHIBIT 23.1 - Tri-Tech Holding, Inc. | dex231.htm |

Table of Contents

As filed with the Securities and Exchange Commission on January 8, 2010

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Tri-Tech Holding Inc.

(Exact Name of Registrant as Specified in its Charter)

| Cayman Islands | 8711 | Not Applicable | ||

| (State or Other Jurisdiction of Incorporation or Organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

| 5D, Tower A, 2 Building Business Center Jinyuan Shidai No. 2 East Road Landianchang, Haidian District Beijing, People’s Republic of China 100097 |

Phil Fan 6501 Chaucer Road Willowbrook, IL 60527 | |

| (+86-10) 8887 3946 | (630) 468-2361 | |

| (Address, including zip code, and telephone number, including area code, of principal executive offices) |

(Name, address, including zip code, and telephone number, including area code, of agent for service) |

Copies to:

| Bradley A. Haneberg, Esq. Anthony W. Basch, Esq. Zachary B. Ring, Esq. Kaufman & Canoles, P.C. Three James Center, 1051 East Cary Street 12th Floor Richmond, Virginia 23219 (804) 771-5700 – telephone (804) 771-5777 – facsimile |

Louis A. Bevilacqua, Esq. Joseph R. Tiano, Jr., Esq. Jing Zhang, Esq. Pillsbury Winthrop Shaw Pittman LLP 2300 N Street, N.W. Washington, DC 20037 (202) 663-8000 – telephone (202) 663-8007 – facsimile |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | x | |||

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price |

Amount of Registration Fee(1) | ||

| Ordinary Shares (2) |

$34,500,000 | $2,459.85 | ||

| Underwriter’s Warrants and Underlying Ordinary Shares(3) |

$3,750,000 | $267.38 | ||

| Total |

$38,250,000 | $2,727.23(4) | ||

| (1) | The registration fee for securities is based on an estimate of the Maximum Aggregate Offering Price of the securities, and such estimate is solely for the purpose of calculating the registration fee pursuant to Rule 457(o). |

| (2) | In accordance with Rule 416(a), the Registrant is also registering an indeterminate number of additional ordinary shares that shall be issuable pursuant to Rule 416 to prevent dilution resulting from share splits, share dividends or similar transactions. Includes shares that the underwriters have the option to purchase to cover over-allotments, if any. |

| (3) | We have agreed to issue warrants to our underwriters (the “Underwriter’s Warrants”) for nominal consideration. The exercise price of the Underwriter’s Warrants is equal to 125% of the price of the ordinary shares offered hereby. The resale of the Underwriter’s Warrants is registered hereunder. The Underwriter’s Warrants are exercisable within five years after the effective date of this registration statement. The ordinary shares underlying the Underwriter’s Warrants are deemed to have the same issuance date as the warrants and are being registered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, as amended. |

| (4) | Paid herewith. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to such Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JANUARY 8, 2010

TRI-TECH HOLDING INC.

Ordinary Shares

We are offering ordinary shares. Our ordinary shares are quoted on the Nasdaq Capital Market under the symbol “TRIT.” On January 7, 2010, the last reported market price of our ordinary shares was $23.11 per ordinary share. We intend to use the net proceeds from this offering for working capital, to pursue mergers and acquisitions if we locate favorable opportunities, new product development, and sales and marketing.

Investing in these ordinary shares involves significant risks. See “Risk Factors” beginning on page 8 of this prospectus.

| Per Ordinary Share | Total | |||||

| Underwriting public offering price |

$ | $ | ||||

| Underwriting discount |

$ | $ | ||||

| Proceeds to us, before expenses |

$ | $ | ||||

Our underwriters have an option exercisable within 45 days from the date of this prospectus to purchase up to additional ordinary shares from us at the public offering price, less the underwriting discount solely to cover over-allotments. The ordinary shares issuable upon exercise of the underwriter’s over-allotment option have been registered under the registration statement of which this prospectus forms a part.

The underwriters are offering these ordinary shares as set forth under “Underwriting.” The underwriters expect to deliver the ordinary shares against payment in U.S. dollars in New York, New York on , 2010.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of theses securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

Sole Bookrunning Manager

Newbridge Securities Corporation

Prospectus dated , 2010

Table of Contents

| 1 | ||

| 8 | ||

| 22 | ||

| 23 | ||

| 27 | ||

| 28 | ||

| 28 | ||

| 29 | ||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

30 | |

| 48 | ||

| 62 | ||

| 68 | ||

| 72 | ||

| 74 | ||

| 75 | ||

| 79 | ||

| 81 | ||

| 84 | ||

| 85 | ||

| 90 | ||

| 91 | ||

| 91 | ||

| 91 |

You should rely only on the information contained in this prospectus. Neither we nor the underwriters have authorized any other person to provide you with different information. This prospectus is not an offer to sell, nor is it seeking an offer to buy, these securities in any state where the offer or sale is not permitted. The information in this prospectus is accurate only as of the date on the front cover, but the information may have changed since that date.

Table of Contents

Except where the context otherwise requires and for purposes of this prospectus only:

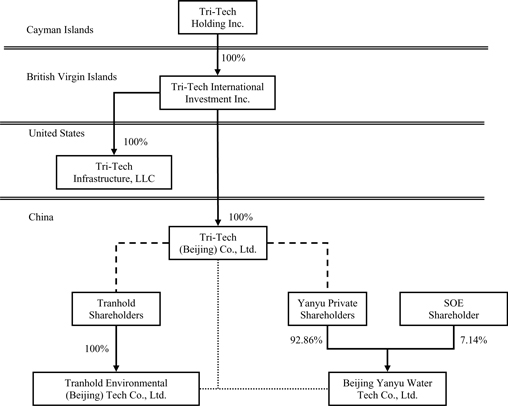

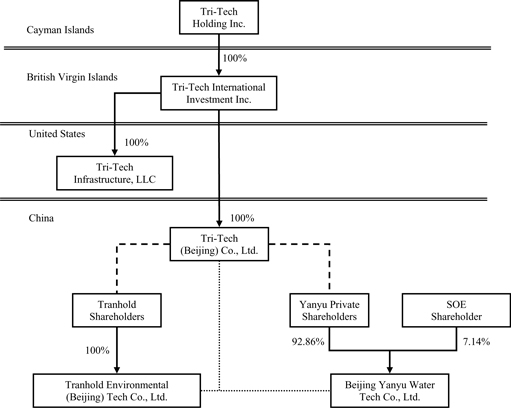

| • | the terms “we,” “us,” “our company,” “our” and “Tri-Tech” refer to Tri-Tech Holding Inc. (“TRIT” when referring solely to our Cayman Islands listing company); our wholly-owned subsidiary, Tri-Tech International Investment Inc., a British Virgin Islands company (“TTII”); our wholly-owned subsidiary, Tri-Tech Infrastructure, LLC, a Delaware limited liability company (“TIS”); TTII’s wholly-owned operating subsidiary, Tri-Tech (Beijing) Co., Ltd., a Chinese limited liability company (“TTB”); and our affiliated entities, Tranhold Environmental (Beijing) Tech Co., Ltd., a Chinese limited liability company (“Tranhold”) and Beijing Yanyu Water Tech Co., Ltd., a Chinese limited liability company (“Yanyu”), both of which TTB controls by virtue of contractual arrangements. |

| • | “SOE Shareholder” refers to Beijing Yan Yu Communications Telemetry United New Technology Development Department, a Chinese State Owned Entity which owns 7.14% of Yanyu; |

| • | “shares” and “ordinary shares” refer to our ordinary shares, $0.001 par value per share; |

| • | “China” and “PRC” refer to the People’s Republic of China, and for the purpose of this prospectus only, excluding Taiwan, Hong Kong and Macau; and |

| • | all references to “RMB,” “Renminbi” and “¥” are to the legal currency of China and all references to “USD,” “U.S. dollars,” “dollars,” and “$” are to the legal currency of the United States. |

This prospectus contains translations of certain RMB amounts into U.S. dollar amounts at a specified rate solely for the convenience of the reader unless otherwise noted, all translations made in this prospectus are based upon a rate of RMB 6.8290 to US$1.00, which was the exchange rate on September 30, 2009.

Unless otherwise stated, we have translated balance sheet amounts with the exception of equity at December 31, 2008 at RMB 6.8346 to US$1.00 as compared to RMB 7.3046 to US$1.00 at December 31, 2007. We have stated equity accounts at their historical rate. The average translation rates applied to income statement accounts for the year ended December 31, 2008 and the year ended December 31, 2007 were RMB 6.9451 and RMB 7.6040, respectively. We make no representation that the RMB or U.S. dollar amounts referred to in this prospectus could have been or could be converted into U.S. dollars or RMB, as the case may be, at any particular rate or at all. On December 31, 2009, the exchange rate was $1.00 to RMB 6.8282. See “Risk Factors – Fluctuation of the Renminbi could materially affect our financial condition and results of operations” for discussions of the effects of fluctuating exchange rates on the value of our ordinary shares. Any discrepancies in any table between the amounts identified as total amounts and the sum of the amounts listed therein are due to rounding.

For the sake of clarity, this prospectus follows English naming convention of first name followed by last name, regardless of whether an individual’s name is Chinese or English. For example, the name of the chief executive officer of Tri-Tech would be presented as “Warren Zhao” (English) or “Wanzong Zhao” (Chinese), even though, in Chinese, his name would typically be presented as “Zhao Wanzong”.

We have relied on statistics provided by a variety of publicly-available sources regarding China’s expectations of growth and market potential in our industry, increased government spending and economic development. We did not sponsor, directly or indirectly, the publication of such materials. In particular:

| • | we have relied on The Tenth Five-year Plan for the Development of the Environmental Protection Industry prepared by China’s State Economic and Trade Commission for all statistics related to China’s environmental plans between 2000 and 2005; |

| • | we have relied on The National Eleventh Five-year Plan prepared by China’s Ministry of Environmental Protection for all statistics related to China’s environmental plans between 2005 and 2010; and |

| • | we have relied on 2007 and 2009 World Bank reports entitled, respectively, “Improving the Performance of China’s Urban Water Utilities” and “Addressing Water Scarcity in China” for statistics regarding China’s water shortages and its planned spending in environmental protection. |

i

Table of Contents

This summary highlights information that we present more fully in the rest of this prospectus. This summary does not contain all of the information you should consider before buying ordinary shares in this offering. This summary contains forward-looking statements that involve risks and uncertainties, such as statements about our plans, objectives, expectations, assumptions or future events. In some cases, you can identify forward-looking statements by terminology such as “anticipate,” “estimate,” “plan,” “project,” “continuing,” “ongoing,” “expect,” “we believe,” “we intend,” “may,” “should,” “could,” and similar expressions. These statements involve estimates, assumptions, known and unknown risks, uncertainties and other factors that could cause actual results to differ materially from any future results, performances or achievements expressed or implied by the forward-looking statements. You should read the entire prospectus carefully, including the “Risk Factors” section and the financial statements and the notes to those statements.

Our Company

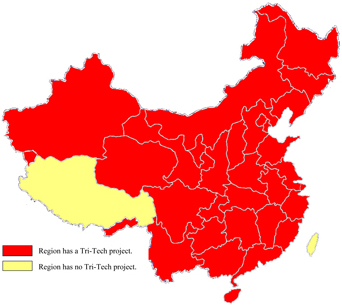

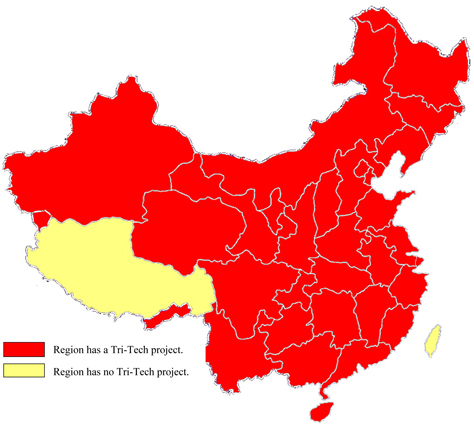

We are a leading provider of integrated solutions for China’s water environmental protection industry, including the water pollution remediation, software and engineering industries. We combine software and hardware to monitor and manage China’s natural and municipal water resources. We provide two lines of service: (i) Wastewater and Tail Gas Treatment and (ii) Water Resource Management. Our customers are mostly local and regional government bodies in China and since we began providing these services in 2002, we have implemented more than 200 projects in provinces, municipalities, autonomous regions and special administrative regions throughout China:

Through our Wastewater and Tail Gas Treatment segment, we design sewage treatment and odor control systems for municipal supplies. These systems, which coordinate technological solutions (software, management information systems, enterprise resource planning and local and wide area networking) with hardware (sensors, distributed control systems, programmable logic controllers, supervisory control and data acquisition systems and mechatronics), allow our clients to monitor and control numerous variables in the sewage treatment and odor control

1

Table of Contents

processes. Our goal in this regard is to be a total solution provider for our clients, allowing them to engage us to design processes and systems that work seamlessly to manage the process from the initial intake of raw sewage through the return of water to consumers for reuse.

Through our Water Resource Management segment, we assist the government in monitoring natural waterways. We provide systems that combine technological solutions (software, geological information systems, management information systems, enterprise resource planning and local, wireless and wide area networking) with hardware (sensors, supervisory control and data acquisition systems and mechatronics) to track water levels for drought and flood control, monitor groundwater quality and assist the government in planning its water resource use and management.

We recently received a $2 million modified Build-Transfer-Operate (“BTO”) contract for a wastewater treatment plant for the Dongli Economic Development Area in the Tianjin Municipality in Northern China. Under the modified BTO model, we will build the treatment plant and transfer ownership to the Dongli Economic Development Area once construction is completed. After we transfer ownership, the Dongli Economic Development Area will operate the plant; however, we will provide assistance and help them to operate the plant as necessary. We will not actually be operating the plant for the Dongli Economic Development Area, as would be the case under a more traditional BTO model. This is the first time we have used the modified BTO model and plan to use it in the future to help municipal clients with sewage discharge problems.

Using the modified BTO model, we finance the cost of a municipal project ourselves, then transfer ownership to the municipality after completion of construction. Under this model, we must have the capital to be able to finance significant portions of the projects ourselves before transferring ownership. As such, we need to have sufficient capital when bidding on modified BTO projects to be able to show the municipality that we have the capability to complete a certain project. We believe this offering will give us the necessary capital to pursue additional modified BTO projects in the future.

We are currently pursuing 100 river basin flood monitoring and forecasting systems in more than 100 counties with a market potential of $72.5 million. In addition, we are pursuing business in the industrial wastewater and process tail gas treatment market for the petrochemical industry. We are looking to increase sales in long-distance water transfer project with several urban water supply tasks for major cities including Beijing.

Our total revenues increased 80.5% from $4.7 million in 2007 to $8.4 million in 2008. Our net income increased 29.7% from $1.3 million in 2007 to 1.7 million in 2008. Our total revenues increased 96.4% from $5.6 million for the nine months ended September 30, 2008 to $10.9 million in the same period in 2009, and our net income grew 97.4% from $1.3 million in the nine months ended September 30, 2008 to $2.5 million in the same period in 2009.

Industry and Market Background

The Chinese government began to focus upon technology and science shortly after the formation of the PRC. From 1949 to 1977, the Chinese government directly controlled all research, development and engineering activities through its State Development Planning Commission and State Science and Technology Commission. In the 1980s, China began to implement market-oriented economic reforms designed to improve the Chinese science and technology industry, among other priorities. During this period, China further reduced the central government’s control over the operation of research oriented businesses. In the 1990s, Chinese policymakers again attempted to enhance the development of high technology businesses by experimenting with additional reduction of governmental control while also providing new forms of ownership for these businesses. In addition, in 1992, the Chinese government liberalized market access by adopting policies that favored foreign investment in high technology businesses. By the end of the 1990s, the Chinese government had further abandoned its control over many high technology businesses and adopted a progressive tax structure designed to further encourage the financial development of these businesses. These policies positively impacted the development of Chinese software and engineering businesses.

As a result of China’s high population density and rapid industrialization, China’s environmental infrastructure is under great stress. China has a smaller water supply than the United States but approximately five times as many people. China faces water scarcity, frequent floods in the south and east and droughts in the north and west, serious water pollution and heavy strains on the environment. Water usage in China quintupled from 1949 to

2

Table of Contents

2007. In short, China struggles to procure, clean and provide enough potable water for a growing population. In addition, due to comparatively inefficient water use, Chinese industries may use three to ten times more water than comparable industries in the west, exacerbating China’s need for water resource management.

As a result of this increased demand for resources, the Chinese government has increased its financial investment in environmental protection legislation and increased environmental standards. Between 1995 and 2000, China invested approximately $47.4 billion in environmental protection. From 2000 through 2005, the investment grew to approximately $92.1 billion. From 2005 through 2010, China’s environmental investment is expected to be approximately $184.2 billion. This growth represents a cumulative annual growth rate of approximately 14.5%. Of the estimated $184.2 billion to be spent on environmental protection, approximately $39.5 billion is expected to be used for water resource management, urban water management, wastewater treatment, sewage reuse and water treatment.

In November 2008, the Chinese government announced a stimulus package worth approximately $585 billion designed to respond to the current global economic crisis. The first two allocations of the stimulus package allocated approximately 10% of the $33 billion to environmental projects in China. While it is unclear at this point how much of the stimulus package will be allocated to or ultimately spent in our industry, the stimulus package may cause our industry to grow significantly. Conversely, any failure to spend allocated funds or to continue to allocate such funds to our industry could materially harm our industry in general and our company in particular.

We believe China’s increased focus on environmental protection and conserving and improving its water resources provides an opportunity to our company, as our business designs sewage treatment and odor control systems and provides systems to monitor and manage China’s water resources.

Our Competitive Strengths

We believe the following strengths differentiate us from our competitors in our market in China:

| • | We are a customized integration solution provider that provides integrated solutions from feasibility studies through implementation. |

| • | Our business centers on Chinese governmental bodies, including the Ministry of Water Resources, local and provincial government bodies, and we have strong customer recognition and industry reputation among those governmental bodies, evidenced by project recognition and awards from the Ministry of Water Resources, Ministry of Environmental Protection and Ministry of Construction. |

| • | We have proven solution and service development capability and monitoring and management systems expertise, including a broad and growing portfolio of software and service, such as application software platforms, utility tools, engineering and consulting. |

| • | We have proven management with a successful track record. Our top executives have over 100 years of combined experience. |

| • | We have a broad client base stretching across China with over 250 projects successfully implemented in 29 provinces and municipalities. |

| • | We have industry leading proprietary technology: we have obtained seven software copyrights and two patents for our technology in China. |

| • | Our business possesses high barriers to entry such as high levels of talent and a technical and capital intensive business model. |

Our Strategies

We provide integrated software and hardware solutions for China’s water environmental protection industry. Our goal is to become the leading provider of such solutions in our market in China. We intend to achieve this goal by implementing the following strategies:

| • | We intend to leverage our expertise in China’s water environmental protection industry to apply our solutions to other industries, including power generation, chemical and metallurgical industries; |

3

Table of Contents

| • | We intend to broaden product offerings by extending product lines to upstream and downstream business segments; |

| • | We intend to reinforce and improve market position by strengthening research and development capacities; |

| • | We intend to build alliances with research institutions and international manufacturers to enrich product offerings; |

| • | We seek to be an early entrant into new markets and projects in order to build a strong reputation among the local and central governments to which we will provide services; |

| • | We intend to continue to employ the modified BTO model for projects; and |

| • | We intend to explore possible overseas business opportunities and seek out candidates for merger and acquisition opportunities. |

Our Challenges and Risks

We believe our primary challenges are:

| • | We currently have a single industry focus, and our area of focus is substantially affected by changes in government priorities and spending; |

| • | There are uncertainties in our development, introduction and marketing of new solutions and services; |

| • | We must actively recruit, train and retain skilled technical and sales personnel; |

| • | We face significant competition from existing competitors and new market entrants; |

| • | Execution of our growth strategy is complex; and |

| • | We rely principally on dividends paid by our PRC operating subsidiary, TTB, and our PRC affiliates, Yanyu and Tranhold, to fund cash and financing requirements, and there are PRC laws restricting the ability of these entities from paying dividends or making other distributions to us. |

In addition, we face risks and uncertainties that may materially affect our business, financial condition, results of operations and prospects. Thus, you should consider the risks discussed in “Risk Factors” and elsewhere in this prospectus before investing in our ordinary shares.

Our Corporate Structure

Overview

We are a holding company incorporated in the Cayman Islands that owns all of the outstanding capital stock of TTII, our wholly-owned subsidiary organized in the British Virgin Islands. TTII, in turn, owns all of the outstanding capital stock of TTB, its operating subsidiary based in Beijing, China. TTB has entered into control agreements with all of the owners of Tranhold and 92.86% of the owners of Yanyu, which agreements allow TTB to control Tranhold and Yanyu. Through our ownership of TTII and TTB and TTB’s agreements with Tranhold and Yanyu, we can substantially influence Yanyu’s and Tranhold’s daily operations and financial affairs, appoint their senior executives and approve all matters requiring shareholder approval. As a result, we are considered the primary beneficiary of Yanyu and Tranhold and consolidate their results, assets and liabilities in our financial statements. For a description of these contractual agreements, see “Our Corporate Structure – Contractual Arrangements with Yanyu, Tranhold and Their Respective Shareholders.” We recently formed TIS, our wholly-owned subsidiary in the U.S. to develop opportunities in the United States. As of this date of this prospectus, we have not conducted any business through TIS.

4

Table of Contents

Our current corporate structure is as follows:

|

Equity interest | |

|

|

Contractual arrangements including Proxy Agreement, Equity Interest Pledge Agreement, Equity Interest Purchase Agreement, Management Fee Payment Agreement and Operating Agreement. For a description of these agreements, see “Corporate Structure—Contractual Arrangements with Yanyu, Tranhold and Their Respective Shareholders.” | |

|

|

Contractual arrangements including Proxy Agreement, Equity Interest Pledge Agreement, Equity Interest Purchase Agreement, Exclusive Technical and Consulting Service Agreement, Management Fee Payment Agreement and Operating Agreement. For a description of these agreements, see “Corporate Structure—Contractual Arrangements with Yanyu, Tranhold and Their Respective Shareholders.” | |

5

Table of Contents

Corporate Information

Our principal executive offices are located at 5D, Tower A, 2 Building Business Center Jinyuan Shidai, No. 2 East Road Landianchang, Haidian District, Beijing, PRC 100097. Our telephone number is (+86-10) 8887 3946. Fax (+86-10) 8886 3726. Our website address is www.tri-tech.cn. Information contained on the website is not a part of this prospectus.

The Offering

| Shares Offered: | ordinary shares | |

| Offering Price per Share | $ per share | |

| Shares Outstanding Prior to Completion of Offering: | 5,255,000 ordinary shares | |

| Shares to be Outstanding after Offering: | ordinary shares | |

| NASDAQ Capital Market Symbol: | “TRIT” (CUSIP No. G9103F 106) | |

| Transfer Agent: | Computershare Trust Company, N.A. 250 Royall Street, Canton, Massachusetts 02021 | |

| Risk Factors: | Investing in these securities involves a high degree of risk. As an investor, you should be able to bear a complete loss of your investment. You should carefully consider the information set forth in the “Risk Factors” section of this prospectus before deciding to invest in our ordinary shares. | |

| Option to Purchase Additional Ordinary Shares: | We have granted to the underwriters an option exercisable within 45 days from the date of this prospectus, to purchase up to an additional ordinary shares solely to cover over-allotments. | |

| Timing and Settlement for Ordinary Shares: | We expect to deliver the ordinary shares registered hereunder against payment on , 2010. | |

| Use of Proceeds: | Our net proceeds from this offering are expected to be approximately $ . Net proceeds will be used to fund new projects, pursue acquisitions if we locate favorable opportunities and general corporate purposes. | |

Underwriter’s Warrants

In connection with this offering, we will, for a nominal amount, sell to our underwriters warrants to purchase up to ten percent (10%) of the shares sold in this offering, excluding any over-allotment (“Underwriter’s Warrants”). These warrants are exercisable for a period of five years from the date of issuance at a price equal to 125% of the price of the shares in this offering. During the term of the warrants, the holders thereof will be given the opportunity to profit from a rise in the market price of our ordinary shares, with a resulting dilution in the interest of our other shareholders. The term on which we could obtain additional capital during the life of these warrants may be adversely affected because the holders of these warrants might be expected to exercise them when we are able to obtain any needed additional capital in a new offering of securities at a price greater than the exercise price of the warrants. If the underwriter exercises all of its warrants, we would have % more shares outstanding after the warrant exercise than at the conclusion of the offering, assuming no other issuances. See “Underwriting.”

6

Table of Contents

Summary Financial Information

In the table below, we provide you with summary financial data of our company. This information is derived from our consolidated financial statements included elsewhere in this prospectus. Historical results are not necessarily indicative of the results that may be expected for any future period. When you read this historical selected financial data, it is important that you read it along with the historical statements and notes and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included elsewhere in this prospectus.

| For the Fiscal Year ended December 31, |

For the nine months ended September 30, (Unaudited) | |||||||||||

| 2008 | 2007 | 2009 | 2008 | |||||||||

| Total Sales |

$ | 8,449,958 | $ | 4,682,023 | $ | 10,905,169 | $ | 5,551,366 | ||||

| Income from Operations |

1,796,572 | 1,221,035 | 2,923,162 | 1,275,551 | ||||||||

| Other Income (Expense) |

110,512 | 88,262 | 65,301 | 78,108 | ||||||||

| Net Income attributable to TRIT |

1,696,153 | 1,307,929 | 2,525,545 | 1,279,658 | ||||||||

| Other Comprehensive Income attributable to TRIT |

251,182 | 80,058 | 66,409 | 295,861 | ||||||||

| Comprehensive Income attributable to TRIT |

1,947,335 | 1,387,987 | 2,591,954 | 1,575,519 | ||||||||

| Basic Earnings per Share (based on 3,679,542, 3,555,000, 3,555,000 and 1,777,500 TRIT shares outstanding, on September 30, 2009 and 2008, December 31, 2008 and 2007, respectively)(1) |

0.48 | 0.74 | 0.69 | 0.36 | ||||||||

| Diluted Earnings per Share (based on 3,689,604, 3,555,000, 3,555,000 and 1,777,500 TRIT shares outstanding, on September 30, 2009 and 2008, December 31, 2008 and 2007, respectively)(1) |

0.48 | 0.74 | 0.68 | 0.36 | ||||||||

| Pro forma Basic Earnings per Share (based on 3,339,542 TRIT shares outstanding on September 30, 2009 and 3,215,000 TRIT shares outstanding on September 30, 2008 and December 31, 2008)(2) |

0.53 | N/A | 0.76 | 0.40 | ||||||||

| Pro forma Diluted Earnings per Share (based on 3,349,604 TRIT shares outstanding on September 30, 2009 and 3,215,000 TRIT shares outstanding on September 30, 2008 and December 31, 2008)(2) |

0.53 | N/A | 0.75 | 0.40 | ||||||||

| December 31, | September 30, (Unaudited) | ||||||||

| 2008 | 2007 | 2009 | |||||||

| Total Assets |

$ | 8,774,224 | $ | 6,802,274 | $ | 23,308,203 | |||

| Total Current Liabilities |

2,824,536 | 2,817,131 | 4,743,980 | ||||||

| Noncontrolling Interests |

137,519 | 120,308 | 150,676 | ||||||

| TRIT Shareholders’ Equity |

5,812,169 | 3,864,835 | 18,344,478 | ||||||

| Total Liabilities and Shareholders’ Equity |

8,774,224 | 6,802,274 | 23,308,203 | ||||||

| (1) | We have presented earnings per share in TRIT after giving retroactive effect to the 71.1-for-1 share split of our ordinary shares that was completed May 22, 2009. |

| (2) | We have presented these pro forma earnings per share after (a) giving retroactive effect to the 71.1-for-1 share split of our ordinary shares that was completed May 22, 2009 and (b) assuming the redemption of the 340,000 shares placed into escrow as described in the section entitled “Related Party Transactions - Founders’ Shares Subject to Redemption.” Pro forma EPS for the nine months ended September 30, 2008, calculated on the foregoing assumptions and based on 3,215,000 TRIT shares, is $0.40. No pro forma numbers have been provided for the year ended December 31, 2007. |

7

Table of Contents

Investment in our securities involves a high degree of risk. You should carefully consider the risks described below together with all of the other information included in this prospectus before making an investment decision. The risks and uncertainties described below are not the only ones we face, but represent the material risks to our business. If any of the following risks actually occurs, our business, financial condition or results of operations could suffer. In that case, you may lose all or part of your investment. You should not invest in this offering unless you can afford to lose your entire investment.

Risks Related to Our Business

We operate in a very competitive industry and may not be able to maintain our revenues and profitability.

Our competitors include both domestic companies and international companies. Some of these competitors have significantly greater financial and marketing resources and name recognition than we have. As the Chinese government continues to allocate funds from the stimulus package to be spent in our industry, more domestic and international competitors may enter the market. We believe that while the Chinese market for our services is subject to intense competition, the number of large competitors is relatively limited, and, as such, while we effectively compete in our market, our competitors occupy a substantial competitive position. If the Chinese government continues to emphasize spending on environmental protection and continues to allocate funds to the water protection industry, the number of our competitors will likely increase and there can be no assurance that we will be able to effectively compete in our industry.

In addition, as the Chinese government increase spending in the water protection industry, our competitors may devote more resources to introducing new water protection systems. If these new systems are more attractive to customers than the systems we currently provide or are able to develop, we may be unable to attract new customers and may lose market share. We believe that competition may become more intense as more integrated automation service providers, including Chinese/foreign joint ventures, are qualified to conduct business. We believe it is likely that competitors will devote significant resources to competing more effectively in our market as the Chinese government continues to emphasize spending in the environmental protection and specifically water protection industry. We cannot assure you that we will be able to compete successfully against any new or existing competitors, or against any new water protection systems our competitors may implement. All of these competitive factors could have a material adverse effect on our revenues and profitability.

We are dependent on continued regulatory enforcement.

While we increasingly pursue economically driven markets, our business is materially dependent on the continued enforcement by the government of various environmental regulations. In a period of relaxed environmental standards or enforcement, local and regional governments may be less willing to allocate funds to consulting services designed to prevent or correct environmental problems.

We are dependent on the state of the PRC’s economy as all of our business is conducted in the PRC.

Currently, all of our business operations are conducted in the PRC, and all of our customers are also located in the PRC. Accordingly, any significant slowdown in the PRC economy may cause our customers to reduce expenditures or delay the building of new facilities or projects. This may in turn lead to a decline in the demand for our products and services. That would have a material adverse effect on our business, financial condition and results of operations.

We are dependent on China’s continued emphasis on environmental protection initiatives and spending.

In the Eleventh Five Year Plan and in the approximately $585 billion stimulus package announced in November 2008, the Chinese government has allocated significant funds to environmental protection in general and to our industry, water environmental protection, in particular. To the extent new or existing domestic and foreign companies believe that China will continue to invest in our industry, it is likely that they will devote resources to competing more effectively in our market and, as a result, we will face increased competition. If the Chinese government fails to allocate or spend funds in the future in our industry, such change in priorities could materially harm our company, particularly if we face increased competition.

8

Table of Contents

We may not be able to secure new customers.

Our business is project-based, and many of our major customers are non-recurring customers. For example, once we design and complete a water treatment facility for a local government client, that client is unlikely to need another water treatment facility until the existing facility becomes obsolete or insufficient for the local needs. If we fail to secure projects from new customers, our revenues will decline and our business, prospects, financial condition and results of operations could be materially and adversely affected. Because our primary customers are local government entities in China, the process of adding new customers is time-consuming and subject to political pressures that may not be present in other industries or countries.

Our business is capital intensive and our growth strategy may require additional capital which may not be available on favorable terms or at all.

We may require additional cash resources due to changed business conditions, implementation of our growth strategy or potential investments or acquisitions we may pursue. To meet our capital needs, we may sell additional equity or debt securities or obtain additional credit facilities. The sale of additional equity securities could result in dilution of your holdings. The incurrence of indebtedness would result in increased debt service obligations and could require us to agree to operating and financial covenants that would restrict our operations. Financing may not be available in amounts or on terms acceptable to us, if at all. Any failure by us to raise additional funds on terms favorable to us, or at all, could limit our ability to expand our business operations and could harm our overall business prospects.

Our revenues are highly dependent on several large customers that vary from year to year.

While we provide our services to a variety of customers, our revenues are typically dependent on several large projects each year. For instance, a customer in our Wastewater and Tail Gas Treatment segment accounted for 17% of our revenues in 2008. Another customer in our Water Resource Management segment, accounted for 12% of our revenues in 2008 and 15% in 2007. In 2007, two other customers in our Wastewater and Tail Gas Treatment segment accounted for 30% and 12% of our revenues, respectively. While we do not expect our revenues to be dependent on these particular customers in the future, we do expect our revenues to be dependent upon several large projects each year. Disruption, delay, or loss of any such project could materially harm our operations.

Our business could be affected by cost overruns, project delays and/or incorrect estimation of project costs.

As our business is project-based, it is important that we manage our projects efficiently in terms of time, procurement of materials and allocation of resources. If our initial cost estimates are incorrect or delays occur in a project resulting in cost overruns, the profitability of that project will be adversely affected. Currently, we offer some of our customers a warranty period of up to 12 months after the completion of projects, during which we are obliged to provide free rectification work against any manufacturing defects. Cost overruns due to additional rectification work and delays in completion of projects would adversely affect our profitability. We may also face potential liability from legal suits brought against us by our customers for causing loss due to any delay in completing a project. Mismanagement of or mistakes made during our projects would adversely affect our profitability as well as our reputation among our customers. We may also face potential liability from legal suits brought against us by our customers who have suffered loss due to such mismanagement or mistakes. This would also adversely affect our profitability and financial position.

Our customers may make claims against us and/or terminate our services in whole or in part prematurely should we fail to implement projects which fully satisfy their requirements and expectations.

Failure to implement projects which fully satisfy the requirements and expectations of our customers or defective system structure or products as a result of design or workmanship or due to acts of nature may lead to claims against us and/or termination of our services in whole or in part prematurely. This may arise from a variety of factors including unsatisfactory design or implementation, staff turnover, human errors or misinterpretation of and failure to adhere to regulations and procedures. This may adversely affect our profits and reputation.

We rely on subcontractors for our projects.

As we may from time to time subcontract some parts of our projects to subcontractors, such as engineering, assembly and integration works, we face the risk of unreliability of work performed by our subcontractors. Should

9

Table of Contents

our subcontractors default on their contractual obligations and work specifications, our ability to deliver the end product or service to our customers in accordance with quality and/or timing specifications may, in turn, be compromised. Furthermore, if we are unable to secure competitive rates from our subcontractors, our financial performance may be adversely affected.

We are subject to risks associated with technological changes.

We may not be able to protect our processes, technologies and systems against claims by other parties. Although we have two registered patents and seven software copyrights in respect of the processes, technologies and systems we use frequently in our systems, we have not purchased or applied for any patents other than these as we are of the view that it may not be cost-effective to do so. For such other processes, technologies and systems for which we have not applied for or purchased or been licensed to use patents or copyrights, we may have no legal recourse to protecting our rights in the event that they are replicated by other parties. If our competitors are able to replicate our processes, technologies and systems at lower costs, we may lose our competitive edge and our profitability will be adversely affected.

We may face claims for infringement of third-party intellectual property rights.

Although we develop our software products, each is based upon middleware developed by third parties, including Microsoft, Oracle and Intouch. We integrate this technology, licensed by ourselves or our customers from third parties, in our software products. If we or our customers, as applicable, are unable to continue to license any of this third party software, or if the third party licensors do not adequately maintain or update their products, we would face delays in the releases of our software until equivalent technology can be identified, licensed or developed, and integrated into our software products. These delays, if they occur, could harm our business, operating results and financial condition.

There has been a substantial amount of litigation in the software and Internet industries regarding intellectual property rights. It is possible that in the future third parties may claim that our current or potential future software solutions infringe their intellectual property. We expect that software product developers will increasingly be subject to infringement claims as the number of products and competitors in our industry segment grows and the functionality of products in different industry segments overlap. In addition, we may find it necessary to initiate claims or litigation against third parties for infringement of our proprietary rights or to protect our trade secrets. Although we may disclaim certain intellectual property representations to our customers, these disclaimers may not be sufficient to fully protect us against such claims. Any claims, with or without merit, could be time consuming, result in costly litigation, cause product shipment delays or require us to enter into royalty or license agreements. Royalty or licensing agreements, if required, may not be available on terms acceptable to us or at all, which could have a material adverse effect on our business, operating results and financial condition.

Failure to adequately protect our intellectual property rights may undermine our competitive position, and litigation to protect our intellectual property rights may be costly.

We rely on a combination of patent, copyrights, trade secret laws and confidentially provisions in contracts with our customers and our employers to protect our intellectual property rights. We believe that the protection of our intellectual property will become increasingly important to our business. Implementation and enforcement of intellectual property-related laws in China has historically been lacking due primarily to ambiguities in PRC intellectual property law. Accordingly, protection of intellectual property and proprietary rights in China may not be as effective as in the United States or other countries. We will continue to rely on a combination of patents, trade secrets, trademarks, copyrights and confidentiality contractual arrangements to provide protection in this regard, but this protection may be inadequate. For example, our pending or future patent applications may not be approved or, if allowed, they may not be of sufficient strength or scope. As a result, third parties may use the technologies and proprietary processes that we have developed and compete with us, which could negatively affect any competitive advantage we enjoy, dilute our brand and harm our operating results.

In addition, policing the unauthorized use of our proprietary technology can be difficult and expensive. Litigation may be necessary to enforce our intellectual property rights and given the relative unpredictability of China’s legal system and potential difficulties enforcing a court judgment in China, there is no guarantee litigation would result in an outcome favorable to us. Furthermore, any such litigation may be costly and may divert management attention away from our core business. An adverse determination in any lawsuit involving our intellectual property is likely to jeopardize our business prospects and reputation. We have no insurance coverage

10

Table of Contents

against litigation costs so we would be forced to bear all litigation costs if we cannot recover them from other parties. All of the foregoing factors could harm our business and financial condition.

The registered capital of our PRC subsidiaries and affiliates may, in some cases, limit the size of the projects we bid for.

We tender for projects in the normal course of business. There are instances where our potential customers require tendering companies to have a minimum registered share capital equivalent to the worth of the project. Therefore, the size of the projects that we are able to successfully tender for may sometimes be dependent on the registered capital of TTB, Tranhold and Yanyu. Although some customers may take into account other factors like our trading status and our track record, we are unable to assure you that we would be able to secure projects which are valued at more than our registered capital. Consequently, our revenue, business and financial results may be adversely and materially affected. In particular, the registered capital of Yanyu, Tranhold and TTB are ¥10,000,000, ¥50,000,000 and $6,150,000, respectively.

Introduction of new laws or changes to existing laws by the PRC government may adversely affect our business.

The PRC legal system is a codified legal system made up of written laws, regulations, circulars, administrative directives and internal guidelines. Unlike common law jurisdictions like the U.S., decided cases (which may be taken as reference) do not form part of the legal structure of the PRC and thus have no binding effect. Furthermore, in line with its transformation from a centrally planned economy to a more free market-oriented economy, the PRC government is still in the process of developing a comprehensive set of laws and regulations. As the legal system in the PRC is still evolving, laws and regulations or the interpretation of the same may be subject to further changes. For example, the PRC government may impose restrictions on the amount of tariff that may be payable by municipal governments to waste water treatment service providers like us. Also, more stringent environmental regulations may also affect our ability to comply with, or our costs to comply with, such regulations. Such changes, if implemented, may adversely affect our business or financial results.

We are heavily dependent upon the services of experienced personnel and executive officers who possess skills that are valuable in our industry, and we may have to actively compete for their services.

We are heavily dependent upon our ability to attract, retain and motivate skilled personnel to serve our clients. Many of our personnel possess skills that would be valuable to all companies engaged in our industry. Consequently, we expect that we will have to actively compete for these employees. Some of our competitors may be able to pay our employees more than we are able to pay to retain them. Our ability to profitably operate is substantially dependent upon our ability to locate, hire, train and retain our personnel. Although we have not experienced difficulty locating, hiring, training or retaining our employees to date, there can be no assurance that we will be able to retain our current personnel, or that we will be able to attract and assimilate other personnel in the future. If we are unable to effectively obtain and maintain skilled personnel, the development and quality of our services could be materially impaired. See “Our Business—Employees.”

In particular, our performance is substantially dependent on the performance of our executive officers and key employees. Specifically, the services of:

| • | Mr. Warren Zhao, Chairman of the Board and Chief Executive Officer; |

| • | Mr. Peter Dong, Chief Financial Officer; and |

| • | Mr. Phil Fan, President |

would be difficult to replace. We do not have in place “key person” life insurance policies on any of our employees. The loss of the services of any of our executive officers or other key employees could substantially impair our ability to successfully development new systems and develop new programs and enhancements. See “Our Business—Employees” and “Management.”

We do not intend to pay dividends in the foreseeable future.

We have not previously paid any cash dividends, and we do not anticipate paying any dividends on our ordinary shares. As our business is largely project-related, we have a relatively high capital requirement. In addition, as we intend to remain in a growth mode, we intend to reinvest any profits in the foreseeable future to grow the business. Although we achieved net profitability beginning in 2006, we cannot assure you that our operations will

11

Table of Contents

continue to result in sufficient revenues to enable us to operate at profitable levels or to generate positive cash flows. Furthermore, there is no assurance our Board of Directors will declare dividends even if we are profitable. Dividend policy is subject to the discretion of our Board of Directors and will depend on, among other things, our earnings, financial condition, capital requirements and other factors. If we determine to pay dividends on any of our ordinary shares in the future, we will be dependent, in large part, on receipt of funds from Yanyu and Tranhold. See “Dividend Policy.”

Foreign Operational Risks

TTB’s contractual arrangements with Tranhold and Yanyu may not be as effective in providing control over Tranhold and Yanyu as direct ownership.

We conduct substantially all of our operations, and generate substantially all of our revenues, through contractual arrangements with Tranhold and Yanyu that provide us, through our ownership of TTII and its ownership of TTB, with effective control over Tranhold and Yanyu. We depend on Tranhold and Yanyu to hold and maintain contracts with our customers. Tranhold and Yanyu also own substantially all of our intellectual property, facilities and other assets relating to the operation of our business, and employ the personnel for substantially all of our business. Neither our company nor TTB has any ownership interest in Tranhold and Yanyu. Although we have been advised by Beijing Kang Da Law Firm, our PRC legal counsel, that each contract under TTB’s contractual arrangements with Tranhold and Yanyu is valid, binding and enforceable under current PRC laws and regulations, these contractual arrangements may not be as effective in providing us with control over Tranhold and Yanyu as direct ownership of Tranhold and Yanyu would be. In addition, Tranhold and Yanyu may breach the contractual arrangements. For example, Tranhold may decide not to make contractual payments to TTB, and consequently to our company, in accordance with the existing contractual arrangements. In the event of any such breach, we would have to rely on legal remedies under PRC law. These remedies may not always be effective, particularly in light of uncertainties in the PRC legal system.

The term of our contractual agreements with the VIEs is longer than the terms of operation for Yanyu, Tranhold and TTB.

The term of all contractual agreements with our VIEs is for 25 years, beginning on November 28, 2008. However, the operating terms of Yanyu, Tranhold and TTB are due to expire earlier. Specifically, the terms of operation for Yanyu, Tranhold and TTB will expire March 28, 2022, June 5, 2033 and February 5, 2026, respectively. While we believe the terms of operation for Yanyu, Tranhold and TTB will be renewed before their respective dates of expiration, it is possible that the operating terms may expire before the termination of the contractual agreements with the VIEs. If this happens, Yanyu, Tranhold or TTB may not be able to fulfill its obligations under the VIE contractual agreements.

We are subject to foreign exchange risks.

Our dominant transactional currency is the Chinese RMB, including the cost of materials which are imported by our suppliers. With costs mainly denominated in RMB, our transactional foreign exchange exposure for the past few years has been insignificant. However, as our suppliers take into account the fluctuations in foreign exchange rates when they price the imported materials which we procure from them, such fluctuations in foreign exchange rates may result in changes in the purchase price of imported materials. Any future significant fluctuations in foreign exchange rates may have a material impact on our financial performance in the event that we are unable to transfer the increased costs to our customers.

Since our operations and significant assets are located in the PRC, shareholders may find it difficult to enforce a U.S. judgment against the assets of our company, our directors and executive officers.

Our operations and significant assets are located in the PRC. In addition, most of our executive officers and directors are non-residents of the U.S., and substantially all the assets of such persons are located outside the U.S. As a result, it could be difficult for investors to effect service of process in the U.S., or to enforce a judgment obtained in the U.S. against us or any of these persons. See “Enforceability of Civil Liabilities.”

12

Table of Contents

We may become a passive foreign investment company, which could result in adverse U.S. tax consequences to U.S. investors.

Based upon the nature of our business activities, we may be classified as a passive foreign investment company (“PFIC”), by the U.S. Internal Revenue Service (“IRS”), for U.S. federal income tax purposes. Such characterization could result in adverse U.S. tax consequences to you if you are a U.S. investor. For example, if we are a PFIC, a U.S. investor will become subject to burdensome reporting requirements. The determination of whether or not we are a PFIC is made on an annual basis and will depend on the composition of our income and assets from time to time. Specifically, we will be classified as a PFIC for U.S. tax purposes if either:

| • | 75% or more of our gross income in a taxable year is passive income; or |

| • | the average percentage of our assets by value in a taxable year which produce or are held for the production of passive income (which includes cash) is at least 50%. |

The calculation of the value of our assets is based, in part, on the then market value of our ordinary shares, which is subject to change. In addition, the composition of our income and assets will be affected by how, and how quickly, we spend the cash we raise in this offering. We are not a PFIC as of the date of this prospectus, but we cannot assure you that we will not be a PFIC for any taxable year. See “Taxation – United States Federal Income Taxation—Passive Foreign Investment Company.”

Adverse changes in economic and political policies of the PRC government could have a material adverse effect on the overall economic growth of China, which could adversely affect our business.

Substantially all of our business operations are conducted in China. Accordingly, our results of operations, financial condition and prospects are subject to a significant degree to economic, political and legal developments in China. China’s economy differs from the economies of most developed countries in many respects, including with respect to the amount of government involvement, level of development, growth rate, control of foreign exchange and allocation of resources.

Since the adoption of the “open door policy” in 1978 and the “socialist market economy” in 1993, the PRC government has been reforming and is expected to continue to reform its economic and political systems. Any changes in the political and economic policy of the PRC government may lead to changes in the laws and regulations or the interpretation of the same, as well as changes in the foreign exchange regulations, taxation and import and export restrictions, which may in turn adversely affect our financial performance. While the current policy of the PRC government seems to be one of imposing economic reform policies to encourage foreign investments and greater economic decentralization, there is no assurance that such a policy will continue to prevail in the future.

While the PRC economy has experienced significant growth in the past 30 years, growth has been uneven across different regions and among various economic sectors of China. The PRC government has implemented various measures to encourage economic development and guide the allocation of resources. Some of these measures benefit the overall PRC economy, but may also have a negative effect on us. For example, our financial condition and results of operations may be adversely affected by government control over capital investments or changes in tax regulations that are applicable to us. Since early 2004, the PRC government has implemented certain measures to control the pace of economic growth. Such measures may cause a decrease in the level of economic activity in China, which in turn could adversely affect our results of operations and financial condition.

Failure to comply with the U.S. Foreign Corrupt Practices Act and Chinese anti-corruption laws could subject us to penalties and other adverse consequences.

We are required to comply with the China’s anti-corruption laws and the United States Foreign Corrupt Practices Act, which generally prohibits U.S. companies from engaging in bribery or other prohibited payments to foreign officials for the purpose of obtaining or retaining business. In addition, we are required to maintain records that accurately and fairly represent our transactions and have an adequate system of internal accounting controls. Foreign companies, including some of our competitors, are not subject to these prohibitions. Corruption, extortion, bribery, pay-offs, theft and other fraudulent practices occur from time-to-time in mainland China. If our competitors engage in these practices, they may receive preferential treatment from personnel of some companies, giving our competitors an advantage in securing business or from government officials who might give them priority in obtaining new licenses, which would put us at a disadvantage. Although we inform our personnel that such

13

Table of Contents

practices are illegal, we cannot assure you that our employees or other agents will not engage in such conduct for which we might be held responsible. If our employees or other agents are found to have engaged in such practices, we could suffer severe penalties and other consequences that may have a material adverse effect on our business, financial condition and results of operations. In addition, our brand and reputation, our sales activities or the price of our ordinary shares could be adversely affected if we become the target of any negative publicity as a result of actions taken by our employees or other agents.

We are subject to foreign exchange controls in the PRC.

Our PRC subsidiary and affiliates are subject to PRC rules and regulations on currency conversion. In the PRC, the State Administration for Foreign Exchange (“SAFE”) regulates the conversion of the RMB into foreign currencies. Currently, foreign investment enterprises (“FIEs”) are required to apply to SAFE for “Foreign Exchange Registration Certificate for FIEs”. TTB is a FIE. With such registration certifications (which need to be renewed annually), FIEs are allowed to open foreign currency accounts including the “recurrent account” and the “capital account”. Currently, conversion within the scope of the “recurrent account” can be effected without requiring the approval of SAFE. However, conversion of currency in the “capital account” (e.g. for capital items such as direct investments, loans, securities, etc.) still requires the approval of SAFE.

The PRC government imposes controls on the convertibility of the Renminbi into foreign currencies and, in certain cases, the remittance of currency out of China. We receive nearly all of our revenues in Renminbi. Under our current corporate structure, our income is derived from payments from TTB. Shortages in the availability of foreign currency may restrict the ability of TTB to remit sufficient foreign currency to pay dividends or other payments to us, or otherwise satisfy their foreign currency denominated obligations. Under existing PRC foreign exchange regulations, payments of current account items, including profit distributions, interest payments and expenditures from trade-related transactions, can be made in foreign currencies without prior approval from the PRC SAFE by complying with certain procedural requirements. However, approval from appropriate government authorities is required where Renminbi is to be converted into foreign currency and remitted out of China to pay capital expenses such as the repayment of bank loans denominated in foreign currencies. The PRC government may also at its discretion restrict access in the future to foreign currencies for current account transactions. If the foreign exchange control system prevents us from obtaining sufficient foreign currency to satisfy our currency demands, we may not be able to pay dividends in foreign currencies to our shareholders. This risk is particularly important where, as in this offering, we need governmental approval to bring offering proceeds into the PRC. See “Our Business – Regulations on Foreign Exchange.”

The value of the Renminbi against the U.S. dollar and other currencies may fluctuate and is affected by, among other things, changes in political and economic conditions. On July 21, 2005, the PRC government changed its decade-old policy of pegging the value of the Renminbi to the U.S. dollar. Under the new policy, the Renminbi is permitted to fluctuate within a narrow and managed band against a basket of certain foreign currencies. This change in policy has resulted in an appreciation of the Renminbi against the U.S. dollar. While the international reaction to the Renminbi revaluation has generally been positive, there remains significant international pressure on the PRC government to adopt an even more flexible currency policy, which could result in a further and more significant appreciation of the Renminbi against the U.S. dollar. Any significant revaluation of Renminbi may materially and adversely affect our cash flows, revenues, earnings and financial position, and the value of, and any dividends payable on, our ordinary shares in U.S. dollars. For example, an appreciation of Renminbi against the U.S. dollar would make any new Renminbi denominated investments or expenditures more costly to us, to the extent that we need to convert U.S. dollars into Renminbi for such purposes. See “Exchange Rate Information.”

Failure to comply with Chinese regulations regarding the registration requirements for employee stock ownership plans or share option plans may subject the PRC plan participants or us to fines and other legal or administrative sanctions.

In December 2006, the People’s Bank of China promulgated the Administrative Measures for Individual Foreign Exchange, which set forth the respective requirements for foreign exchange transactions by Chinese individuals under either the current account or the capital account. In January 2007, the SAFE issued the Implementation Rules of the Administrative Measures for Individual Foreign Exchange, which, among other things, specified approval requirements for certain capital account transactions such as a Chinese citizen’s participation in the employee stock ownership plans or stock option plans of an overseas publicly-listed company. On March 28, 2007, the SAFE promulgated the Processing Guidance on Foreign Exchange Administration for Domestic

14

Table of Contents

Individuals Participating in Employee Stock Holding Plans or Stock Option Plans of Overseas-Listed Companies. Under this rule, PRC citizens who are granted stock options by an overseas publicly-listed company are required, through a qualified PRC domestic agent or PRC subsidiary of such overseas publicly-listed company, to register with the SAFE and complete certain other procedures. We and our Chinese employees who receive stock option grants will be subject to this rule. Our board of directors has adopted the Tri-Tech Holding Inc. 2009 Stock Incentive Plan and as of the date of this prospectus we have issued options to purchase 525,500 ordinary shares to our key employees. We and the optionees intend to make the required registration, however failure or inability by our company or the Chinese optionees to comply with these regulations may subject these individuals to fines and other legal or administrative sanctions.

We do not have business interruption, litigation or natural disaster insurance.

The insurance industry in China is still at an early state of development. In particular PRC insurance companies offer limited business products. As a result, we do not have any business liability, disruption insurance or any other forms of insurance coverage for our operations in China. Any business interruption, litigation or natural disaster may result in our business incurring substantial costs and the diversion of resources.

We may have difficulty maintaining adequate management, legal and financial controls in the PRC.

The PRC historically has been deficient in Western style management and financial reporting concepts and practices, as well as in modern banking, and other control systems. We may have difficulty in hiring and retaining a sufficient number of qualified employees to work in the PRC. As a result of these factors, and especially given that we are a publicly listed company in the U.S. and subject to regulation as such, we may experience difficulty in maintaining management, legal and financial controls, collecting financial data and preparing financial statements, books of account and corporate records and instituting business practices that meet Western standards. We may have difficulty establishing adequate management, legal and financial controls in the PRC. Therefore, we may, in turn, experience difficulties in implementing and maintaining adequate internal controls as required under Section 404 of the Sarbanes-Oxley Act of 2002 and other applicable laws, rules and regulations. This may result in significant deficiencies or material weaknesses in our internal controls which could impact the reliability of our financial statements and prevent us from complying with SEC rules and regulations and the requirements of the Sarbanes-Oxley Act of 2002. Any such deficiencies, weaknesses or lack of compliance could have a materially adverse effect on our business.

Any recurrence of severe acute respiratory syndrome, or SARS, pandemic avian influenza or another widespread public health problem, could adversely affect the Chinese economy as a whole and adversely affect demand for our business.

A renewed outbreak of SARS, pandemic avian influenza or another widespread public health problem in China, where we earn substantially all of our revenues, could have a negative effect on our operations. Our operations may be affected by a number of health-related factors, including the following:

| • | quarantines or closures of some or our offices at which we provide services, which would severely disrupt our operations; |

| • | the sickness or death of our key officers and employees; and |

| • | a general slowdown in the Chinese economy. |

Any of the foregoing events or other unforeseen consequences of public health problems could adversely affect our markets or our ability to operate profitably.

TTB’s contractual arrangements with Tranhold and Yanyu may result in adverse tax consequences to us.

We could face material and adverse tax consequences if the PRC tax authorities determine that TTB’s contractual arrangements with Yanyu and Tranhold were not made on an arm’s length basis and adjust our income and expenses for PRC tax purposes in the form of a transfer pricing adjustment. A transfer pricing adjustment could result in a reduction, for PRC tax purposes, of adjustments recorded by Tranhold and Yanyu, which could adversely affect us by increasing Tranhold’s and Yanyu’s tax liability without reducing TTB’s tax liability, which could further result in late payment fees and other penalties to Tranhold and Yanyu for underpaid taxes.

15

Table of Contents

PRC laws and regulations governing our businesses and the validity of certain of our contractual arrangements are uncertain. If we are found to be in violation of such PRC laws and regulations, we could be subject to sanctions. In addition, changes in such PRC laws and regulations may materially and adversely affect our business.

There are substantial uncertainties regarding the interpretation and application of PRC laws and regulations, including, but not limited to, the laws and regulations governing our business, or the enforcement and performance of TTB’s contractual arrangements with Yanyu and Tranhold. TRIT, TTII and TTB are considered foreign persons or foreign invested enterprises under PRC law. As a result, TRIT, TTII and TTB are subject to PRC law limitations on foreign ownership of Chinese companies. These laws and regulations are relatively new and may be subject to change, and their official interpretation and enforcement may involve substantial uncertainty. The effectiveness of newly enacted laws, regulations or amendments may be delayed, resulting in detrimental reliance by foreign investors. New laws and regulations that affect existing and proposed future businesses may also be applied retroactively.

The PRC government has broad discretion in dealing with violations of laws and regulations, including levying fines, revoking business and other licenses and requiring actions necessary for compliance. In particular, licenses and permits issued or granted to us by relevant governmental bodies may be revoked at a later time by higher regulatory bodies. We cannot predict the effect of the interpretation of existing or new PRC laws or regulations on our businesses. We cannot assure you that our current ownership and operating structure would not be found in violation of any current or future PRC laws or regulations. As a result, we may be subject to sanctions, including fines, and could be required to restructure our operations or cease to provide certain services. In addition, any litigation in China may be protracted and result in substantial costs and diversion of resources and management attention. Any of these or similar actions could significantly disrupt our business operations or restrict us from conducting a substantial portion of our business operations, which could materially and adversely affect our business, financial condition and results of operations.

The shareholders of Tranhold and Yanyu have potential conflicts of interest with us, which may adversely affect our business.

Neither we nor TTB owns any portion of the equity interests of Yanyu or Tranhold. Instead, we rely on TTB’s contractual obligations to enforce our interest in receiving payments from Tranhold and Yanyu. Conflicts of interests may arise between Tranhold’s and Yanyu’s shareholders and our company if, for example, their interests in receiving dividends from Tranhold and Yanyu were to conflict with our interest requiring these companies to make contractually-obligated payments to TTB. As a result, we have required Tranhold and Yanyu and each of their respective shareholders (other than the SOE Shareholder) to execute irrevocable powers of attorney to appoint the individual designated by us to be his attorney-in-fact to vote on their behalf on all matters requiring shareholder approval by Tranhold and Yanyu, as applicable, and to require Tranhold’s and Yanyu’s compliance with the terms of its contractual obligations. We cannot assure you, however, that when conflicts of interest arise, these companies’ shareholders will act completely in our interests or that conflicts of interests will be resolved in our favor. In addition, these shareholders could violate their agreements with us by diverting business opportunities from us to others. If we cannot resolve any conflicts of interest between us and Tranhold’s and Yanyu’s respective shareholders, we would have to rely on legal proceedings, which could result in the disruption of our business.