Attached files

| file | filename |

|---|---|

| EX-32 - EXHIBIT 32 - SusGlobal Energy Corp. | exhibit32.htm |

| EX-31.2 - EXHIBIT 31.2 - SusGlobal Energy Corp. | exhibit31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - SusGlobal Energy Corp. | exhibit31-1.htm |

| EX-10.29 - EXHIBIT 10.29 - SusGlobal Energy Corp. | exhibit10-29.htm |

| EX-10.28 - EXHIBIT 10.28 - SusGlobal Energy Corp. | exhibit10-28.htm |

| EX-10.27 - EXHIBIT 10.27 - SusGlobal Energy Corp. | exhibit10-27.htm |

| EX-4.6 - EXHIBIT 4.6 - SusGlobal Energy Corp. | exhibit4-6.htm |

| EX-4.4 - EXHIBIT 4.4 - SusGlobal Energy Corp. | exhibit4-4.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES AND EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2020

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES AND EXCHANGE ACT OF 1934

For the transition period from ______________to ______________

Commission file number: 000-56024

SUSGLOBAL ENERGY CORP.

(Exact name of registrant as specified in its charter)

|

Delaware |

38-4039116 |

|

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

|

|

|

|

200 Davenport Road |

|

|

Toronto, Ontario, Canada |

M5R1J2 |

|

(Address of principal executive offices) |

(Zip code) |

Registrant's telephone number, including area code:

(416) 223-8500

|

Securities registered pursuant to Section 12(b) of the Act: |

||||

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| N/A | N/A | N/A | ||

|

Securities registered pursuant to Section 12(g) of the Act: |

||||

|

Common Stock, par value $0.0001 per share |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined by Rule 405 of the Securities Act.

Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted every Interactive Data File required to be submitted pursuant to Rule 405 of Regulations S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes [X] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer [ ] |

Accelerated filer [ ] |

|

|

|

|

Non-accelerated filer [X] |

Smaller reporting company [X] |

|

|

|

|

Emerging growth company [X] |

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [X]

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yes [ ] No [X]

The aggregate market value of the 64,329,157 voting common stock held by non-affiliates of the registrant as of June 30, 2020 (the last business day of the registrant’s most recently completed second fiscal quarter) was $11,579,248 based on the closing price of $0.018 per share of the registrant’s common stock as quoted on the OTCQB marketplace on that date.

The number of shares of Common Stock, $0.0001 par value, of the registrant outstanding as of April 15, 2021 was 89,584,951.

DOCUMENTS INCORPORATED BY REFERENCE

None

TABLE OF CONTENTS

PART I

Item 1. Business.

OVERVIEW

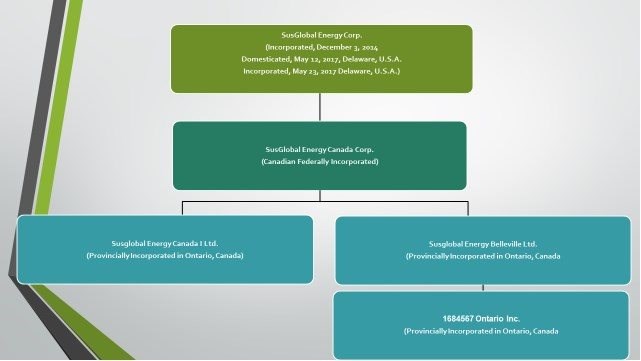

The following organization chart sets forth our wholly-owned subsidiaries:

General

On February 4, 2019, the Company registered its common stock, having a par value of $.0001 per share, pursuant to Section 12(g) of the Securities Exchange Act of 1934, as amended (the "Exchange Act") and is effective pursuant to General Instruction A.(d).

SusGlobal Energy Corp. ("SusGlobal") was formed by articles of amalgamation on December 3, 2014, in the Province of Ontario, Canada and its executive office is in Toronto, Ontario, Canada, at 200 Davenport Road. Our telephone number is 416-223-8500. Our website address is www.susglobalenergy.com. Our annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K are all available, free of charge, on our website as soon as practicable after we file the reports with the Securities and Exchange Commission (the "SEC"). SusGlobal Energy Corp., a company in the start-up stages and Commandcredit Corp. ("Commandcredit"), an inactive Canadian public company, amalgamated to continue business under the name of SusGlobal Energy Corp.

On May 23, 2017, SusGlobal filed an Application for Authorization to continue in another Jurisdiction with the Ministry of Government Services in Ontario and a certificate of corporate domestication and certificate of incorporation with the Secretary of State of the State of Delaware under which it changed its jurisdiction of incorporation from Ontario to the State of Delaware (the "Domestication"). In connection with the Domestication each of the currently issued and outstanding common shares were automatically converted on a one-for-one basis into common shares compliant with the laws of the state of Delaware (the "Shares"). As a result of the Domestication, pursuant to Section 388 of the General Corporation Law of the State of Delaware (the "DGCL"), SusGlobal continued its existence under the DGCL as a corporation incorporated in the State of Delaware. The business, assets and liabilities of SusGlobal and its subsidiaries on a consolidated basis, as well as its principal location and fiscal year, were the same immediately after the Domestication as they were immediately prior to the Domestication. SusGlobal filed a Registration Statement on Form S-4 to register the Shares and this registration statement was declared effective by the Securities and Exchange Commission on May, 23, 2017.

SusGlobal is a renewables company focused on acquiring, developing and monetizing a global portfolio of proprietary technologies in the waste to energy and regenerative products application.

When the terms "the Company," "we," "us" or "our" are used in this document, those terms refer to SusGlobal Energy Corp., and its wholly-owned subsidiaries, SusGlobal Energy Canada Corp., SusGlobal Energy Canada I Ltd., SusGlobal Energy Belleville Ltd., and 1684567 Ontario Inc.

On December 11, 2018, the Company began trading on the OTCQB venture market exchange, under the ticker symbol SNRG.

With the growing amount of organic wastes being produced by society as a whole, a solution for sustainable global management of these wastes must be achieved. SusGlobal through its proprietary technology and processes is equipped and confident to deliver this objective. Management believes renewable energy is the energy of the future. Sources of this type of energy are more evenly distributed over the earth's surface than finite energy sources, making it an attractive alternative to petroleum-based energy. Biomass, one of the renewable resources, is derived from organic material such as forestry, food, plant and animal residuals. SusGlobal can therefore help you turn what many consider waste into precious energy and regenerative products. The portfolio will be comprised of four distinct types of technologies: (a) Process Source Separated Organics ("SSO") in anaerobic digesters to divert from landfills and recover biogas. This biogas can be converted to gaseous fuel for industrial processes, electricity to the grid or cleaned for compressed renewable gas. (b) Increasing the capacity of existing infrastructure (anaerobic digesters) to allow processing of SSO to increase biogas yield. (c) Utilize recycled plastics to produce liquid fuels and (d) process SSO and digestate to produce an organic compost or a pathogen free organic liquid fertilizer. The convertibility of organic material into valuable end products such as biogas, liquid biofuels, organic fertilizers and compost shows the utility of renewables. These products can be converted into electricity, fuels and marketed to agricultural operations that are looking for an increase in crop yields, soil amendment and environmentally-sound practices. This practice also diverts these materials from landfills and reduces Greenhouse Gas Emissions ("GHG") that result from landfilling organic wastes. The Company can provide peace of mind that the full lifecycle of organic material is achieved, global benefits are realized and stewardship for total sustainability is upheld. It is management's objective to grow SusGlobal into a significant sustainable waste to energy and regenerative products provider, as Leaders in The Circular Economy®.

We believe the project and services offered can benefit both the public and private markets. The following includes some of our work managing organic waste streams: Anaerobic Digestion, Dry Digestion, Biogas Production, Wastewater Treatment, In-Vessel Composting, SSO Treatment, Biosolids Heat Treatment, Leachate Management and Composting.

The Company can provide a full range of services for handling organic residuals in a period where innovation and sustainability are paramount. From start to finish we offer in-depth knowledge, a wealth of experience and cutting-edge technology for handling organic waste.

The primary focus of the services SusGlobal provides includes identifying idle or underutilized anaerobic digesters and integrating our technologies with capital investment to optimizing the operation of the existing digesters to reach their full capacity for processing SSO. Our processes not only divert significant organic waste from landfills, but also result in methane avoidance, with significant GHG reductions from waste disposal. The processes also produce renewable energy through the conversion of wastewater biosolids and organic wastes in the same equipment (co-digestion) and valuable end products such as biogas, electricity and organic fertilizer, both dry and liquid, considered Class AA organic fertilizer.

Currently, the primary customers are municipalities in both rural and urban centers throughout southern and central Ontario, Canada. Where necessary, to be in compliance with provincial and local environmental laws and regulations, SusGlobal submits applications to the respective authorities for approval prior to any necessary engineering being carried out.

Our Status as an Emerging Growth Company

We are an "emerging growth company," as defined in the Jumpstart Our Business Startups Act of 2012, and the JOBS Act. Certain specified reduced reporting and other regulatory requirements are available to public companies that are emerging growth companies.

These provisions include:

• an exemption from the auditor attestation requirement in the assessment of our internal controls over financial reporting required by Section 404 of the Sarbanes-Oxley Act of 2002;

• an exemption from the adoption of new or revised financial accounting standards until they would apply to private companies;

• an exemption from compliance with any new requirements adopted by the Public Company Accounting Oversight Board, or the PCAOB, requiring mandatory audit firm rotation or a supplement to the auditor's report in which the auditor would be required to provide additional information about our audit and our financial statements; and

• reduced disclosure of our executive compensation arrangements.

We have elected to opt out of the extended transition period for complying with new or revised accounting standards. This election is irrevocable.

We will continue to be an emerging growth company until the earliest of:

• the last day of our fiscal year in which we have total annual gross revenues of $1,070,000,000 (as such amount is indexed for inflation every five years by the SEC to reflect the change in the Consumer Price Index for All Urban Consumers published by the Bureau of Labor Statistics, setting the threshold to the nearest $1,000,000) or more;

• the last day of our fiscal year following the fifth anniversary of the date of our first sale of common equity securities pursuant to an effective registration statement under the Securities Act of 1933, as amended;

• the date on which we have, during the prior three-year period, issued more than $1,000,000,000 in non- convertible debt; or

• the date on which we are deemed to be a large accelerated filer under the rules of the Securities and Exchange Commission, or SEC, which means the market value of our common stock that is held by non-affiliates (or public float) exceeds $700 million as of the last day of our second fiscal quarter in our prior fiscal year.

We are also a "smaller reporting company," as defined under SEC Regulation S-K. As such, we also are exempt from the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act and also are subject to less extensive disclosure requirements regarding executive compensation in our periodic reports and proxy statements. We will continue to be deemed a smaller reporting company until (i) our public float exceeds $250 million on the last day of our second fiscal quarter in our prior fiscal year (if our annual revenues exceeded $100 million in such prior fiscal year); or (ii) our public float exceeds $700 million on the last day of our second fiscal quarter in our prior fiscal year (if our annual revenues were less than $100 million in such prior fiscal year).

RECENT BUSINESS DEVELOPMENTS

On April 8, 2021, the Company completed the purchase of its new truck and hauling trailer for a total purchase price of $171,483 (C$218,338), plus the applicable harmonized sales taxes. The Company paid deposits of $38,636 (C$49,193) on this purchase and financed the balance over a period of forty-eight months at a monthly principal and interest payment of $3,614 (C$4,601).

On March 4, 2021, the Company announced it has signed a Capital Market Advisory Agreement (the "Agreement") with Exchange Listing, LLC ("Exchange Listing") to provide advisory services with respect to the Company's initiative to list its shares of Common Stock on the Nasdaq Capital Market.

Exchange Listing provides companies with cost-effective and efficient direct access to one-stop solutions in the strategic planning and implementation of listing on senior exchanges such as NASDAQ or NYSE. Focusing on company-specific structuring to meet listing requirements, Exchange Listing serves as the primary point of contact with the exchange, investment bankers and lawyers throughout the listing process. With extensive experience in investment banking, securities law, corporate governance and business management, Exchange Listing and its strategic partners facilitate its clients' listing and capital markets objectives.

On February 10, 2021, the Company signed an Agreement of Purchase and Sale (the "APS") for certain assets for $3,534,300 (C$4,500,000), including a vendor take-back mortgage of $1,570,800 (C$2,000,000) at an annual interest rate of 2% maturing two years after closing. A deposit of $157,080 (C$200,000) was paid by the Company on February 10, 2021. The APS is expected to close on June 4, 2021, subject to successful completion of the due diligence process and the completion of the Phase II Environmental Site Assessment at a cost of $39,113 C$49,800), plus applicable harmonized sales taxes.

Purchase of Additional Lands

On November 12, 2020, the Company acquired additional lands described in the Company's Share Purchase Agreement (the "SPA") of 1684567 Ontario Inc. (“1684567”), in May of 2019. The additional lands include a 6.60-acre licensed gravel pit and a 0.20 acre right of way for a purchase price of $164,934 (C$210,000) plus the applicable harmonized sales tax. The Company is now the owner of a 49-acre land parcel at its Belleville, Ontario, Canada, organic waste processing and composting facility. The purchase was funded through an additional advance of $549,780 (C$700,000) on its 1st. mortgage. The funds received, $407,810 (C$519,238), were net of financing fees of $57,904 (C$73,725) and expenses including accrued interest, property taxes and other disbursements of $90,134 (C$114,762). The new first mortgage of $2,591,820 (C$3,300,000) was registered on November 12, 2020. The terms of the new 1st. mortgage are as noted under long-term debt, note 13(b) to the consolidated financial statements, including an interest rate at the higher of the Royal Bank of Canada's prime rate plus 7.55% (currently 10% per annum) and 10% per annum, and the principal amount is due December 1, 2021. Management used a portion of the additional advance to satisfy certain obligations with Pace Savings and Credit Union Limited ("PACE").

Business Acquisition

Effective May 24, 2019, the Company purchased all the issued and outstanding shares of 1684567. The transaction closed on May 28, 2019. The purchase consideration consisted of cash from working capital of $121,845 (C$163,836) and cash from a third-party mortgage obtained in the amount of $1,258,273 (C$1,691,910), net of financing fees of $84,894 (C$108,090)). The total purchase price includes the original offer of $1,314,304 (C$1,767,250) and reimbursement of vendor's expenses of $65,814 (C$88,496). The original first mortgage payable on this business acquisition had a principal amount of $1,413,720 (C$1,800,000). The terms of the first mortgage are as noted above. The first mortgage is secured by the shares held of 1684567, the land held having a total carrying value of $1,655,623 (C$2,108,000), a general assignment of rents, and a fire insurance policy. In addition, on December 19, 2019, the Company received an additional advance of $628,320 (C$800,000) from one of the same private lenders and additional private lenders. Financing fees on the additional, advance totaled $34,469 (C$43,887) on the same terms and conditions.

The principal asset of this acquired company was the land upon which the Company's organic composting facility is situated. The Company continues to operate the garbage collection operations that it acquired under this transaction.

SusGlobal Receives a Certificate of Registration for the Trademark EARTH’s JOURNEY® and the Trademark CARING FOR EARTH’S JOURNEY®

On November 24, 2020, the Company received a Certificate of Registration from the United States Patent and Trademark Office for the trademark EARTH’s JOURNEY® and trademark CARING FOR EARTH’S JOURNEY® (the “Marks”). The Marks were registered under Registration Number 6,197,171 and Registration Number 6,195,955 on November 10, 2020 on the Supplemental Register. The registrations will be in effect for an initial term of ten years, expiring November 10, 2030, with the option of renewing the registrations for successive ten-year terms. Now that the Marks are registered, it is permitted to use indicia of registration (e.g. ®, or phrases such as “Reg U.S. Pat. And T.M. Office”).

SusGlobal Receives Trademark Registration for LEADERS IN THE CIRCULAR ECONOMY®

After having filed on March 13, 2019, trademark applications in Canada and the United States, on July 16, 2020, the Company announced it had received a Certificate of Registration from the United States Patent and Trademark Office ("USPTO") for the trademark LEADERS IN THE CIRCULAR ECONOMY (the "Mark").

The Mark was registered under Registration Number 6,098,063 on July 7, 2020 on the Supplemental Register. The registration will be in effect for an initial term of ten years, expiring on July 7, 2030, with the option of renewing the registration for successive ten-year terms for the following class:

treatment and processing of organic waste; organic waste disposal services, namely, destruction and recycling of waste; organic waste management services, namely, converting waste into energy; recycling of organic waste; technical consulting in the field of waste management, namely, consulting in the field of waste treatment; recycling of plastic; recycling, namely, transform biosolids and organic waste into a pathogen free recognized organic fertilizer and compost and regenerative products, namely, biogas, electricity, liquid fertilizer, compost.

Now that the Mark is registered, The Company is permitted to use indicia of registration (e.g. ®, or phrases such as "Reg. U.S. Pat. and T.M. Office").

SusGlobal to Commence Integration of The Ydro Process(R) at Its Belleville Organic Waste Processing and Composting Facility

On May 27, 2020, the Company announced it has agreed to commence The Ydro Process® integration into the existing operations at the Organic Waste Processing and Composting Facility of its wholly owned subsidiary SusGlobal Energy Belleville Ltd. ("SusGlobal Belleville").

TradeWorks Environmental's Ydro Process® is integrated into the existing SusGlobal Belleville operations by applying the Ydro Series®

Microorganisms product once during the preparation stage of the batches in the appropriate Gore® system windrows.

The integration of the Ydro Process® is expected to:

Reduce:

• Odors generated from the composting processing, its products (compost), as well as its by-products (i.e. leachate).

• Energy requirements, and the electrical consumption for aeration-heating purposes.

Increase:

• Degradation/decomposition rate and efficiency of the composting process.

• Composting process and reduce the compost processing time.

• Composting performance and efficiency of the system.

• System's composting capacity and composting cycles (over its design limit).

• Compost quality, compost maturity, N:P:K & C:N ratio.

• Composting temperature (naturally, through the biological activity).

Energy Retrofit Program

On January 15, 2020, the Independent Electrical System Operator (the "IESO") pre-approved the Company's Save on Energy Retrofit Program Application (the "Program"). The total cost of the Program is estimated at $93,221 (C$118,692). On successful completion, the Company expects to receive a hydro grant from the IESO of approximately 50% of the total cost of the Program, or $46,991 (C$59,831). The Program is designed to realize a savings of approximately 50% in hydro costs annually, with an overall return on investment estimated at 125%.

New and Renewed Consulting Contracts

On December 17, 2020, the Company entered into an Executive Chairman Consulting Agreement (the "CEO's Consulting Agreement"), by and among the Company, Travellers International Inc. ("Travellers"), and the CEO, who is also a director, the Executive Chairman and President of the Company, effective January 1, 2021 (the "Effective Date"). The CEO's Consulting Agreement replaced the consulting agreement which expired on December 31, 2020.

Pursuant to the terms of the CEO's Consulting Agreement, for his services as the CEO, the compensation is at a rate of $23,562 (C$30,000) per month for twelve (12) months, beginning on the Effective Date, and at a rate of $31,416 (C$40,000) per month for twelve (12) months, beginning January 1, 2022. In addition, the Company agreed to grant the CEO 1,000,000 restricted shares of the Company's common stock, par value of $0.0001 per share (the "Common Stock") on the Effective Date, and 1,000,000 shares of Common Stock on January 1, 2022. The Company has also agreed to reimburse the CEO for certain out-of-pocket expenses incurred by the CEO.

The CEO's Consulting Agreement is for a term of twenty-four (24) months. Upon a Constructive Discharge (as defined in the CEO's Consulting Agreement) and subject to certain notification requirements and the Company's opportunity to cure the Constructive Discharge, the CEO will be entitled to a compensation of twelve (12) months' fees, as well as any bonus compensation owing.

On December 17, 2020, the Company entered into an Executive Consulting Agreement (the "CFO Consulting Agreement"), by and between the Company and the CFO of the Company, effective January 1, 2021. Pursuant to the terms of the CFO Consulting Agreement, the CFO is entitled to fees of $6,283 (C$8,000) per month for his services. In addition, the Company has also agreed to grant the CFO 50,000 restricted shares of the Company's Common Stock, par value of $0.0001 per share on the Effective Date. The Company has also agreed to reimburse the CFO for certain out-of-pocket expenses incurred by the CFO. The CFO's Consulting Agreement replaced the consulting agreement which expired on December 31, 2020.

The CFO's Consulting Agreement is for a term of twelve (12) months. Upon a Constructive Discharge (as defined in the CFO's Consulting Agreement) and subject to certain notification requirements and the Company's opportunity to cure the Constructive Discharge, the CFO will be entitled to a compensation of two (2) months' fees, as well as any bonus compensation owing.

Financings

(a) Securities Purchase Agreements

On April 1, 2021, the Company entered into a securities purchase agreement with an investor (the "April 2021 Investor"), in which the Company issued to the investor a 10% unsecured convertible promissory note (the “April 2021 Investor Note”) in the aggregate principal amount of $275,000, due September 30, 2021, convertible at any time after issuance at a per share price at $0.20. In addition, the April 2021 Investor received 200,000 common shares of the Company, on issuance of the April 2021 Investor Note. On April 5, 2021, the Company received $245,000, net of transaction related expenses of $30,000.

On March 31, 2021, the Company entered into a securities purchase agreement with an investor (the "March 2021 Investor"), in which the Company issued to the investor a 10% unsecured convertible promissory note (the “March 2021 Investor Note”) in the aggregate principal amount of $275,000, due September 30, 2021, convertible at any time after issuance at a per share price at $0.20. In addition, the March 2021 Investor received 200,000 common shares of the Company, on issuance of the March 2021 Investor Note. On March 31, 2021, the Company received $245,000, net of transaction related expenses of $30,000.

On October 18, 2019, the Company entered into a securities purchase agreement (the "October 2019 SPA") with one investor (the "October 2019 Investor") pursuant to which the Company issued to the October 2019 Investor one 12% unsecured convertible promissory note (the "October 2019 Investor Note") in the principal amount of $156,000. On this date, the Company received proceeds of $129,600, net of transaction related expenses of $26,400.

The maturity date of the October 2019 Investor note was October 18, 2020.

On July 19, 2019, the Company entered into a securities purchase agreement (the "July 2019 SPA") with one investor (the "July 2019 Investor") pursuant to which the Company issued to the July 2019 Investor one 12% unsecured convertible promissory note (the "July 2019 Investor Note") in the principal amount of $170,000. On this date, the Company received proceeds of $138,225, net of transaction related expenses of $31,775.

The maturity date of the July 2019 Investor Note was July 19, 2020.

On May 23, 2019, the Company entered into a securities purchase agreement (the "May 2019 SPA") with one investor (the "May 2019 Investor") pursuant to which the Company issued to the May 2019 Investor one 12% unsecured convertible promissory note (the "May 2019 Investor Note") in the principal amount of $250,000. On this date, the Company received proceeds of $204,250, net of transaction related expenses of $45,750.

The maturity date of the May 2019 Investor note was May 23, 2020.

As a result of the unsecured convertible notes not having been repaid by their respective due dates, these defaults resulted in the principal balance of each of the May 2019, July 2019, and October 2019 Investor Notes increasing by 10% and the interest rate on each of those notes increasing from 12% to 24% annually.

On January 20, 2021, the October 2019 Investor, the July 2019 Investor and the May 2019 Investor, accepted in full 2,100,000 common shares of the Company representing payment in full of all obligations due and owing under their unsecured convertible promissory notes.

On March 7 and March 8, 2019, the Company entered into two securities purchase agreements (the "March 2019 SPAs") with two investors (the "March 2019 Investors") pursuant to which the Company issued to each March 2019 Investor two 12% unsecured convertible promissory notes comprised of the first notes (the "First Notes") being in the amount of $275,000 each, and the remaining notes in the amount of $275,000 each (the "Back-End Notes," and, together with the First Notes, the "March 2019 Investor Notes") in the aggregate principal amount of $1,100,000, with such principal and the interest thereon convertible into Common Stock at the March 2019 Investors' option. Each First Note contains a $25,000 Original Issue Discount such that the issue price of each First Note was $250,000. The proceeds on the issuance of the First Notes were received from the March 2019 Investors upon the signing of the March 2019 SPAs. The proceeds on the issuance of the Back-End Notes were initially received by the issuance of two offsetting $250,000 secured notes to the Company by the March 2019 Investors (the "Buyer Notes"), provided that prior to conversion of the Back-End Notes, the March 2019 Investors must have paid back the Back-End Notes in cash.

Although the March 2019 SPAs are dated March 7, 2019 and March 8, 2019 (each, a "March 2019 Effective Date"), they became effective upon the receipt in cash of the issue price by the March 2019 Investors. On March 11, 2019, the Company received cash of $456,000, net of transaction-related expenses, for the First Notes from the March 2019 Investors.

Since the unsecured convertible promissory noted were not repaid by their due dates, these defaults resulted in the outstanding balance (principal plus accrued interest) increasing by 10% and the interest rate on the 2019 March Investor Notes increasing from 12% to 24% annually.

During the year ended December 31, 2020, the March 2019 Investors converted a total of $91,802 (2019-$75,000) of their March 2019 Investor Notes.

In addition, on December 24, 2020, one of the two March 2019 Investors accepted a payment of $165,000 representing payment in full of all obligations due and owing under their March 2019 Investor Note. This resulted in a gain on forgiveness of debt of $119,983, including accrued interest of $68,085, disclosed under other income (loss) in the consolidated statements of operations and comprehensive loss.

On January 19, 2021, the remaining March 2019 Investor and the Company reached an agreement for payment in full of all obligations due and owing under its convertible promissory notes by payments totaling $550,000, $50,000 on January 20, 2021, $200,000 on or before March 1, 2021 which was converted to 1,075,124 shares on March 11, 2021 and $300,000 on or before March 31, 2021. The payment due on or before March 31, 2021 was extended to April 29, 2021.

On January 28, 2019, the Company entered into securities purchase agreements (the "January 2019 SPAs") with three investors (the "January 2019 Investors") pursuant to which the Company issued to the January 2019 Investors 12% unsecured convertible promissory notes (the "January 2019 Investor Notes") in the aggregate principal amount of $337,500, with such principal and the interest thereon convertible into shares of the Company's common stock (the "Common Stock") at the January 2019 Investors' option. Although the January 2019 SPAs are dated January 28, 2019 (the "January 2019 Effective Date"), they became effective upon the receipt in cash of the issue price by the January 2019 Investors.

The amounts of $102,500, $100,000, and $100,000, totaling $302,500, represented the proceeds to the Company, net of transaction-related expenses, for the January 2019 Notes from the January 2019 Investors and were received in cash from February 1 through February 4, 2019.

The maturity date of each of the January 2019 Investor Notes is January 28, 2020 (the "January 2019 Maturity Dates"). The Notes bear interest at a rate of twelve percent (12%) per annum (the "January 2019 Interest Rate"), which interest shall be paid by the Company to the January 2019 Investors in Common Stock at any time the January 2019 Investors send a notice of conversion to the Company. The January 2019 Investors are entitled to, at their option, convert all or any amount of the principal face amount and any accrued but unpaid interest of the January 2019 Notes into Common Stock, at any time, at a conversion price for each share of Common Stock equal to 65% multiplied by the lowest trading price (as defined in the January 2019 Notes) of the Common Stock as reported on the National Quotations Bureau OTC Marketplace exchange upon which the Company's shares are traded during the twenty (20) consecutive Trading Day period immediately preceding (i) the January 2019 Effective Date; or (ii) the conversion date.

The Company has reserved a minimum of eight (8) times the number of its authorized and unissued Common Stock (the "January 2019 Reserved Amounts"), free from pre-emptive rights, to provide for the issuance of Common Stock upon the full conversion of the January 2019 Notes. Upon full conversion of the January 2019 Investor Notes, any shares remaining in such reserve shall be cancelled. The Company increases the January 2019 Reserved Amount in accordance with the Company's obligations under the January 2019 Investor Notes.

Since the unsecured convertible promissory notes were not repaid by their maturity dates these defaults resulted in the outstanding balance (principal plus accrued interest) of each of the January 2019 Investor Notes to increase by 50% and increased by a further $15,000 (together the "Default Amounts") along with the interest rate increasing from 12% to 24% annually. The January 2019 Investors had the option to require the Company to immediately issue, in lieu of the Default Amount, the number of shares of common stock of the Company equal to the Default Amount divided by the conversion price then in effect.

During the year ended December 31, 2020, the January 2019 Investors converted a total of $61,925 (2019-$158,618) of their January 2019 Investor Notes. On December 16 and 21 of 2020, the two remaining January 2019 Investors, agreed to accept payments totaling $98,000 from the Company representing payment in full of all obligations due and owing under the January 2019 Investor Notes. This resulted in a gain on forgiveness of debt of $200,151, including accrued interest of $77,753 disclosed under other income (loss) in the consolidated statements of operations and comprehensive loss.

On issuance, the convertible promissory notes described above, were able to be prepaid until 180 days from their applicable effective date with the following penalties: (i) if any of the convertible promissory notes are prepaid within sixty (60) days following their applicable effective date, then the prepayment premium shall be 125% of the face amount plus any accrued interest; (ii) if any of the convertible promissory notes are prepaid during the period beginning on the date which is sixty-one (61) days following their applicable effective date, and ending on the date which is ninety (90) days following their applicable effective date, then the prepayment premium shall be 135% of the face amount plus any accrued interest; (iii) if any of the convertible promissory notes are prepaid during the period beginning on the date which is ninety-one (91) days following their applicable effective date, and ending on the date which is one hundred eighty (180) days following their applicable effective date, then the prepayment premium shall be 145% of the face amount plus any accrued interest. Such prepayment redemptions must be closed and funded within three days of giving notice of prepayment or the right to prepay shall be forfeited.

Pursuant to the terms of the security purchase agreements for the convertible promissory notes described above, for so long as the noted investors own any shares of Common Stock issued upon the conversion of the applicable investor notes, the Company has covenanted to secure and maintain the listing of such shares of Common Stock. The Company is also subject to certain customary negative covenants under the investor notes and the security purchase agreements, including but not limited to the requirement to maintain its corporate existence and assets, require registration of or stockholder approval for the investor notes or the Common Stock upon the conversion of the applicable investor notes.

The convertible promissory notes described above contained certain representations, warranties, covenants and events of default including if the Company is delinquent in its periodic report filings with the Securities and Exchange Commission which would increase the amount of the principal and interest rates under the convertible promissory notes in the event of such defaults. In the event of a default, at the option of the applicable investor and in their sole discretion, the applicable investor may consider any of their convertible promissory notes immediately due and payable.

For the year ended December 31, 2020, the Company recorded interest and Default Amounts of $562,562 (2019-$142,963). As at December 31, 2020, $316,048 (2019-$142,963) of accrued interest is included in accrued liabilities in the consolidated balance sheets. In addition, during the year ended December 31, 2020, $15,277 (2019-$15,162) of accrued interest was converted.

(b) PACE

On March 31, 2020, PACE and the Company reached an agreement with respect to the repayment of the outstanding balances owing to PACE ((i), (ii) and (iii), below). One of the credit facilities, in the amount of $34,391 (C$48,788), was repaid in full on April 3, 2020, and the remaining credit facilities and the corporate term loan are now due on or before July 30, 2021. On April 3, 2020, the Company provided PACE with funds, held in trust on March 31, 2020, to bring the remaining credit facilities and the corporate term loan current. In addition, the letter of credit the Company has with PACE in favor of the Ministry of the Environment, Conservation and Parks (the "MECP"), was renewed to September 30, 2020 and will remain in effect to September 30, 2021, unless terminated by PACE. On April 3, 2020, the shares previously pledged as security to PACE, were released and are currently held as security for the personal guarantee from the CEO and charge against the Haute leased premises. This obligations to PACE are considered to be in default as a result of defaults on the unsecured convertible promissory notes.

On November 12, 2020, PACE and the Company reached a new agreement to repay the remaining credit facilities and corporate term loan on or before January 29, 2021. As part of the agreement, the Company will bring all the amounts owing to PACE current, and prepay to January 2021, the regular monthly principal and interest payments.

On November 13, 2020, the agreed amounts were paid to PACE.

On February 18, 2021, PACE and the Company reached a new agreement extending the repayment of the remaining credit facilities and corporate term loan to on or before July 30, 2021.

Details of each of the remaining credit facilities and corporate term loan are as follows:

| (i) | The credit facility bears interest at the PACE base rate of 7.00% plus 1.25% per annum, currently 8.25%, is payable in monthly blended installments of principal and interest of $6,883 (C$8,764) and matures on September 2, 2022. The first and only advance on this credit facility received on February 2, 2017, in the amount of $1,256,640 (C$1,600,000), is secured by a business loan general security agreement, a $1,256,640 (C$1,600,000) personal guarantee from the CEO and a charge against the Haute leased premises. Also pledged as security are the shares of the wholly-owned subsidiaries, and a limited recourse guarantee against each of these parties. As noted above, the pledged shares were delivered by PACE and are currently held as security for the personal guarantee from the CEO and charge against the Haute leased premises. The credit facility is fully open for prepayment at any time without notice or bonus. |

| (ii) | The credit facility advanced on June 15, 2017, in the amount of $471,240 (C$600,000), bears interest at the PACE base of 7.00% plus 1.25% per annum, currently 8.25%, is payable in monthly blended installments of principal and interest of $3,849 (C$4,901), and matures on September 2, 2022. The credit facility is secured by a variable rate business loan agreement on the same terms, conditions and security as noted above. |

| (iii) | The corporate term loan advanced on September 13, 2017, in the amount of $2,924,945 (C$3,724,147), bears interest at the PACE base rate of 7.00% plus 1.25% per annum, currently 8.25%, is payable in monthly blended installments of principal and interest of $23,335 (C$29,711), and matures September 13, 2022. The corporate term loan is secured by a business loan general security agreement representing a floating charge over the assets and undertakings of the Company, a first priority charge under a registered debenture and a lien registered under the Personal Property Security Act in the amount of $3,142,368 (C$4,000,978) against the assets including inventory, accounts receivable and equipment. The corporate term loan also included an assignment of existing contracts included in the APA. |

For the year ended December 31, 2020, $302,758 (C$405,788) (2019-$313,182; C$415,525) in interest was incurred on the PACE long-term debt. As at December 31, 2020 $18,319 (C$23,325) (2019-$124,926; C$162,263) in accrued interest is included in accrued liabilities in the consolidated balance sheets.

(c) First Mortgage

As described above, under Purchase of Additional Lands and Business Acquisition, the Company obtained a 1st. mortgage provided by private lenders to finance the acquisition of the shares of 1684567 and to provide funds for additional financing needs, received in three tranches totaling $2,591,820 (C$3,300,000) (2019-$2,001,740; C$2,600,000). The 1st mortgage is repayable interest only on a monthly basis at an annual rate of the higher of the Royal Bank of Canada's prime rate plus 6.05% per annum (currently 8.50%) and 10% per annum with a maturity date of December 1, 2021. The mortgage payable is secured by the shares held of 1684567, a first mortgage on the land described in note 10, long-lived assets, in the consolidated balance sheets with a carrying value of $1,655,623 (C$2,108,000), a general assignment of rents, and a fire insurance policy. Financing fees on the mortgage totaled $177,266 (C$225,702). As at December 31, 2020, $36,215 (C$46,110) (2019-$8,138; C$10,570) of accrued interest is included in accrued liabilities in the consolidated balance sheets. In addition, as at December 31, 2020, there is $50,253 (C$63,984) (2019-$67,464; C$87,627) of unamortized finance fees included in long-term debt in the consolidated balance sheets.

For the year ended December 31, 2020, $214,853 (C$287,968) (2019-$83,662; C$111,002) in interest was incurred on the mortgage payable and included in the consolidated statements of operations and comprehensive loss.

(d) Canada Emergency Business Account (the "CEBA")

As a result of the COVID-19 virus, the Government of Canada launched the CEBA, a program to ensure that small businesses have access to the capital they need to see them through the current challenges and better position them to quickly return to providing services to their communities and creating employment. The program is administered by Canadian chartered banks and credit unions.

On April 27, 2020, the Company received a total of $62,832 (C$80,000) and on December 17, 2020 a further $15,708 (C$20,000) under this program, from its Canadian chartered bank.

Under the initial term date of the loans, which is detailed in the CEBA term loan agreements, the amounts are due on December 31, 2022 and are interest-free. If the loans are not repaid by December 31, 2022, the Company can make payments, interest only, on a monthly basis at an annual rate of 5% per annum, under the extended term date, beginning January 31, 2023, maturing December 31, 2025. In addition, if 75% of the loans are repaid by the initial term, December 31, 2022, the Company's Canadian chartered bank will forgive the balance. The CEBA term loan agreements contain a number of positive and negative covenants, for which the Company is not in full compliance.

(e) Financings Related to Obligations Under Capital Lease

The Company has three obligations under capital lease relating to machinery and equipment at their waste management and organic composting facility.

|

(i) |

The lease agreement for certain equipment for the Company's organic waste processing and composting facility at a cost of $225,135 (C$286,650), is payable in monthly blended installments of principal and interest of $4,587 (C$5,840), plus applicable harmonized sales taxes and an option to purchase the equipment for a final payment of $22,462 (C$28,600), plus applicable harmonized sales taxes on October 31, 2021. The lease agreement bears interest at the rate of 5.982% annually, compounded monthly, due September 30, 2021. |

|

|

|

|

(ii) |

The lease agreement for certain equipment for the Company's organic composting facility at a cost of $194,347 (C$247,450), is payable in monthly blended installments of principal and interest of $4,020 (C$5,118), plus applicable harmonized sales taxes for a period of forty-six months plus the first two monthly blended installments of $7,854 (C$10,000) plus applicable harmonized sales taxes and an option to purchase the equipment for a final payment of $ 19,384 (C$24,680) plus applicable harmonized sales taxes on February 27, 2022. The leasing agreement bears interest at the rate of 6.15% annually, compounded monthly, due January 27, 2022. |

|

(iii) |

The lease agreement for certain equipment for the Company's organic waste processing and composting facility at a cost of $306,031 (C$389,650), is payable in monthly blended installments of principal and interest of $5,382 (C$6,852), plus applicable harmonized sales taxes for a period of fifty-nine months plus an initial deposit of $15,276 (C$19,450) plus applicable harmonized sales taxes and an option to purchase the equipment for a final payment of a nominal amount of $79 (C$100) plus applicable harmonized sales taxes on February 27, 2025. The leasing agreement bears interest at the rate of 3.59% annually, compounded monthly, due January 27, 2025. |

During the year ended December 31, 2020, $18,090 (C$24,246) (2019-$16,021; C$21,257) in interest was charged.

(f) Other

On February 10, 2021, the Company raised $157,260 (C$200,000), in a private placement on the issuance of 630,480 common shares of the Company.

During the year December 31, 2020, Travellers loaned the company $433,147 (C$551,499) and converted a portion of the unpaid balance, $348,010 (C$443,099) of these loans and accrued interest of $6,399 (C$8,171), into 3,184,992 common shares of the Company. The Travellers loans were unsecured and bore interest at the rate of 12% per annum.

Subsequent to December 31, 2020 and up to the date of this filing, Travellers loaned the Company a further $204,922 (C$260,914) and converted these loans into 715,847 common shares of the Company.

In addition, on February 25, 2021, Travellers converted a total of $81,167 (C$101,700) of fees owing into 289,881 common shares of the Company.

During the year ended December 31, 2019, the Company repaid $172,350 (C$223,860) of outstanding loans to Travellers, including interest of $18,370 (C$23,860).

As at the date of this filing, there is a balance of $18,064 (C$23,000) in advances owing to the CEO.

During the year ended December 31, 2020 $nil (C$nil) (2019-$3,717; C$4,932) of interest was charged on the Director Loans. The Director Loans, which bore interest at 12% per annum and which were loaned to the Company on April 18,2018, were repaid in full on July 19, 2019 with accrued interest.

Treatment of Organic Waste and Septage

On February 28, 2019, the Company announced that it had received the project completion report titled: Development Optimization and Validation of an Innovative Integrated Anaerobic Thermophilic Digester Treatment of Organic Waste and Septage. The report was written by a research team at Fleming College's Centre for Advancement of Water and Wastewater Technologies, located in Lindsay, Ontario, Canada. The collaborative project was supported by the Advancing Water Technologies Program (the "AWT Program") of Southern Ontario Water Consortium. The project focused on the development of a new and innovative technology for handling and processing organic residuals. This new technology utilizes the anaerobic mesophilic digestion process coupled with thermophilic digestion to maximize biogas yields and produce organic fertilizer through optimal operations.

Asset Purchase

On September 15, 2017, the Company entered into an asset purchase agreement (the "APA) with Astoria Organic Matters Ltd., and Astoria Organic Matters Canada LP ("Astoria"), pursuant to which the Company purchased certain assets of Astoria from the court appointed receiver of Astoria, BDO Canada Limited (the "Receiver"). The purchase price for the composting buildings, Gore cover system, driveway and paving, office trailer, certain machinery and equipment, computer equipment, computer software and intangible assets (the "Assets") consisted of cash of $3,005,300 (C$4,100,000), funded by PACE and 529,970 restricted common shares of the Company, determined to be valued at $529,970 (C$700,000) based on private placement pricing at the time. In addition, legal costs of $21,442 (C$29,253) in connection with acquiring the Assets are included in the cost of the organic composting facility. In addition, the Company purchased certain accounts receivable which it was required to collect, totaling $127,650 (C$174,147) and a deposit with a local municipality in the amount of $36,650 (C$50,000).

On May 9, 2017, the company signed a memorandum of agreement with Kentech (the "Kentech Agreement"), a corporation existing under the laws of the province of Ontario, Canada ("Kentech"). The Kentech Agreement provides the Company the right to acquire and the right to use the equipment and innovative processes of Kentech in relation to the production of liquid fertilizer from organic waste material. The Kentech Agreement is for a period of five years, commencing on the date of the Kentech Agreement. The Kentech Agreement may be terminated by either party upon providing six months' notice.

On December 7, 2016, the Company was awarded funding for the AWT Program, a program for business led collaborations in the water sector. The AWT Program is administered by the Southern Ontario Water Consortium to assist small and medium sized businesses in the Province of Ontario, Canada, leverage world-class research facilities and academic expertise to develop and demonstrate water technologies for successful introduction to market. In addition, the AWT Program is designed to enhance the Ontario water cluster and continue to build Ontario's reputation for water excellence around the world. The Company's academic partner is the CAWT at Fleming College in Lindsay, Ontario, Canada. The original AWT Program budget was for $586,400 ($800,000 CAD), of which the Company contributes 50% in cash and in-kind contributions and CAWT contributes 50%. CAWT revised its budget for the second and third years of the AWT Program. As a result, the cash commitments for 2017 and 2018, the second and third years of the AWT Program were cancelled.

The Company had already completed and provided its commitment for the first year of the AWT Program which ended March 31, 2017, consisting of professional fees of $7,217 ($9,432 CAD) and a contribution to the capital requirements of the AWT Program, totaling $71,017 ($94,000 CAD), for equipment to be used in the AWT Program and to be retained by CAWT.

Operations

The Company owns the Environmental Compliance Approvals (the "ECAs") issued by the MECP from the Province of Ontario, in place to accept up to 70,000 metric tonnes of waste annually from the provinces of Ontario, Quebec and from New York state, and to operate a waste transfer station with the capacity to process up to an additional 50,000 metric tonnes of waste annually. Once built, the location of the waste transfer station will be alongside the organic waste processing and composting facility which is currently operating in Belleville, Ontario, Canada.

Waste Transfer Station- Access to the waste transfer station is critical to haulers who collect waste in areas not in close proximity to disposal facilities where such disposal continues to be permitted. Tipping fees charged to third parties at waste transfer stations are usually based on the type and volume or weight of the waste deposited at the waste transfer station, the distance to the disposal site, market rates for disposal costs and other general market factors.

Organic Composting Facility- As noted above, the Company's organic waste processing and composting facility, located in Belleville, Ontario Canada, has ECAs in place to accept up to 70,000 metric tonnes of waste annually and is currently in operation. Certain assets of the organic waste processing and composting facility, including the ECAs for the waste transfer station (not yet built), were acquired by the Company on September 15, 2017, from the Receiver for Astoria, under the APA. The Company charges tipping fees for the waste accepted at the organic waste composting facility based on arrangements in place with the customers and the type of waste accepted. Typical waste accepted includes, leaf and yard, biosolids, food, liquid, paper sludge and source separated organics. During year ended December 31, 2020, tipping fees ranged from $22 (C$30) to $119 (C$159) per metric tonne (2019-$19 (C$25) to $100 (C$130 per metric tonne).

Competition

Seasonal Trends

Our operating revenues tend to be somewhat higher in summer months, primarily due to waste volumes resulting from higher construction and demolition waste volumes and the availability of leaf and yard waste along with contracts involving the grinding of leaf and yard waste. In addition, revenue from the sale of organic compost would be higher beginning in late spring and tapering off in the fall.

Employees

As of December 31, 2020, the Company had eight full-time employees and two independent contractors. Of the eight full time employees, two were employed in management and administrative positions, and the balance in operations. The two independent contractors provide services in management positions. None of our employees are covered by collective bargaining agreements.

Financial Assurance and Insurance Obligations

Financial Assurance

Municipal and governmental waste service contracts generally require contracting parties to demonstrate financial responsibility for their obligations under the contract. Financial assurance is also a requirement for (i) obtaining or retaining disposal site or waste transfer station operating permits; and (ii) estimated post-closure and environmental remedial obligations at our operations. We have established financial assurance using letters of credit and/or deposits with the municipalities. The type of assurance used is based on several factors, most importantly: the jurisdiction, contractual requirements, market factors and availability of credit capacity.

A letter of credit in favor of the MECP is supported by our credit facility with PACE. As at December 31, 2020 and the date of filing, the MECP has not drawn on the letter of credit. The letter of credit with the MECP is renewable annually, and is in force until September 30, 2021, unless terminated by PACE.

Insurance

We carry a broad range of insurance coverages, including general liability, automobile liability, workers' compensation, real and personal property, directors' and officers' liability, environmental and pollution legal liability and other coverages we believe are customary to the industry. Our exposure to loss for insurance claims is generally limited to the per-incident deductible under the related insurance policy. We do not expect the impact of any known casualty, property, environmental or other contingency to have a material impact on our financial condition, results of operations or cash flows. For the year ended December 31, 2020, we have self-insured certain buildings and equipment.

Regulation

Our business is subject to extensive and evolving federal, provincial and local environmental, health, safety and transportation laws and regulations. These laws and regulations are administered by the MECP, Environment Canada, and various other federal, provincial and local environmental, zoning, transportation, land use, health and safety agencies in Canada. Many of these agencies regularly examine our operations to monitor compliance with these laws and regulations and have the power to enforce compliance, obtain injunctions or impose civil or criminal penalties in case of non-compliance. On November 5, 2020, the MECP conducted two audits for two of our ECAs. The MECPs comments were received late December 2020. The audits resulted in the Company taking corrective action regarding sampling, testing and the removal of exceeding waste from the site during 2021. The Company has completed some of the corrective action and responded to the MECP and will continue with the remaining corrective action through 2021. The Company has accrued actual and estimated costs totaling $354,125 (C$450,885) in connection with the corrective action. In addition, the Company has accrued for deferred assets relating to machinery it anticipates purchasing in 2021, in the amount of $215,953 (C$274,959).

Because the primary mission of our business is to manage solid and liquid waste hauled to our organic waste processing and composting facility in an environmentally sound manner, our capital expenditures are related, either directly or indirectly, to environmental protection measures, including compliance with federal, provincial and local rules. There are costs associated with siting, design, permitting, operations, monitoring, site maintenance, corrective actions, financial assurance, and facility closure and post-closure obligations. With acquisition, development or expansion of a waste management or waste transfer station, we must often spend considerable time, effort and money to obtain or maintain required permits and approvals. There are no assurances that we will be able to obtain or maintain required governmental approvals. Once obtained, operating permits are subject to renewal, modification, suspension or revocation by the issuing agency. Compliance with current regulations and future requirements could require us to make significant capital and operating expenditures. However, most of these expenditures are made in the normal course of business and do not place us at any competitive disadvantage.

The primary Provincial statutes affecting our business are summarized below:

Provincial and Local Regulations

Various provincial and local regulations affect our operations. The Province of Ontario has its own laws and regulations governing solid waste disposal, water and air pollution, and, in most cases, releases and cleanup of hazardous substances and liabilities for such matters. The Province of Ontario has also adopted regulations governing the design, operation, maintenance and closure of waste transfer stations. Some regions, municipalities and other local governments in Ontario have adopted similar laws and regulations. Our facilities and operations are likely to be subject to these types of requirements.

Our operations are affected by the increasing preference for alternatives to landfill disposal. Many regional and local governments in Ontario mandate recycling and waste reduction at the source and prohibit the disposal of certain types of waste, such as yard waste, food waste and electronics at landfills. The number of regional and local governments in Ontario with recycling requirements and disposal bans continues to grow, while the logistics and economics of recycling the items remain challenging. In addition, Ontario has imposed timelines for the ban of organics from landfills in the province in an effort to totally divert these wastes from landfills. This will provide opportunities for the expansion of facilities like ours. This had already occurred in the province of Quebec and in the United States of America (the "USA"), where various states have enacted, or are considering enacting, laws that restrict the disposal within the state of solid waste generated outside the state. While laws that overtly discriminate against out-of-state waste have been found to be unconstitutional, some laws that are less overtly discriminatory have been upheld in court. From time to time, the United States Congress has considered legislation authorizing states to adopt regulations, restrictions, or taxes on the importation of out-of-state or out-of-jurisdiction waste. Additionally, several state and local governments have enacted "flow control" regulations, which attempt to require that all waste generated within the state or local jurisdiction be deposited at specific sites. In 1994, the U.S. Supreme Court ruled that a flow control ordinance that gave preference to a local facility that was privately owned was unconstitutional, but in 2007, the Court ruled that an ordinance directing waste to a facility owned by the local government was constitutional. The United States Congress' adoption of legislation allowing restrictions on interstate transportation of out-of-state or out-of-jurisdiction waste or certain types of flow control, or courts' interpretations of interstate waste and flow control legislation, could adversely affect our solid and hazardous waste management services.

Federal, Provincial and Local Climate Change Initiatives

In light of regulatory and business developments related to concerns about climate change, we have identified a strategic business opportunity to provide our public and private sector customers with sustainable solutions to reduce their Greenhouse Gas ("GHG") emissions. As part of our on-going marketing evaluations, we assess customer demand for and opportunities to develop waste services offering verifiable carbon reductions, such as waste reduction, increased recycling, and conversion of biogas and discarded materials into electricity and fuel. We use carbon life cycle tools in evaluating potential new services and in establishing the value proposition that makes us attractive as an environmental service provider. We are active in support of public policies that encourage development and use of lower carbon energy and waste services that lower users' carbon footprints. We understand the importance of broad stakeholder engagement in these endeavors, and actively seek opportunities for public policy discussion on more sustainable materials management practices. In addition, we work with stakeholders at the federal and provincial level in support of legislation that encourages production and use of renewable, low-carbon fuels and electricity. Despite the past U.S. withdrawal from the Paris Climate Accords, we have seen no reduction in customer demand for services aligned with their GHG reduction goals and strategies. Ontario is part of the WCI led by the state of California and, if anything, California has doubled down on their GHG reduction goals. The states of Oregon and Washington are also considering joining the WCI that currently includes, amongst other states and provinces, California, Ontario and Quebec as members.

We continue to assess the physical risks to company operations from the effects of severe weather events and use risk mitigation planning to increase our resiliency in the face of such events. We are investing in infrastructure to withstand more severe storm events, which may afford us a competitive advantage and reinforce our reputation as a reliable service provider through continued service in the aftermath of such events.

Item 1A. Risk Factors.

In an effort to keep our stockholders and the public informed about our business, we may make "forward-looking statements." Forward-looking statements usually relate to future events and anticipated revenues, earnings, cash flows or other aspects of our operations or operating results. Forward-looking statements are often identified by the words, "will," "may," "should," "continue," "anticipate," "believe," "expect," "plan," "forecast," "project," "estimate," "intend" and words of a similar nature and generally include statements containing:

• projections about accounting and finances;

• plans and objectives for the future;

• projections or estimates about assumptions relating to our performance; or

• our opinions, views or beliefs about the effects of current or future events, circumstances or performance.

You should view these statements with caution. These statements are not guarantees of future performance, circumstances or events. They are based on facts and circumstances known to us as of the date the statements are made. All aspects of our business are subject to uncertainties, risks and other influences, many of which we do not control. Any of these factors, either alone or taken together, could have a material adverse effect on us and could change whether any forward-looking statement ultimately turns out to be true. Additionally, we assume no obligation to update any forward-looking statement as a result of future events, circumstances or developments. The following discussion should be read together with the Consolidated Financial Statements and the notes thereto. Outlined below are some of the risks that we believe could affect our business and financial statements for 2020 and beyond and that could cause actual results to be materially different from those that may be set forth in forward-looking statements made by the Company.

Any investment in our securities involves a high degree of risk, including the risks described below. Our business, financial condition and results of operations could suffer as a result of these risks, and the trading price of our shares could decline, perhaps significantly, and you could lose all or part of your investment. The risks discussed below also include forward-looking statements and our actual results may differ substantially from those discussed in these forward-looking statements. See the section entitled "Information Regarding Forward-Looking Statements."

The COVID-19 Outbreak May Adversely Affect Our Business Operations and Financial Condition

In December 2019, an outbreak of a novel strain of coronavirus ("COVID-19") was reported. On March 11, 2020, the World Health Organization characterized COVID-19 as a pandemic. Developments in this area continue daily at the local, provincial and national levels. The Company has taking steps, consistent with directions from local, provincial and federal authorities, to mitigate known risks with the health and safety of its employees and customers as its first priority. The outbreak of COVID-19was declared a national emergency. Many provinces and municipalities in Canada, announced aggressive actions to reduce the spread of COVID-19, including limiting non-essential gatherings of people, ceasing all non-essential travel, ordering certain businesses and government agencies to cease non-essential operations at physical locations and issuing "social or physical distancing" orders, which direct individuals to remain at their places of residence (subject to limited exceptions). COVID-19 poses the risk that we or our employees, contractors, customers, government and third-party payors and others may be prevented from conducting business activities for an indefinite period of time, including due to spread of the disease within these groups or due to shutdowns that have been and may continue to be requested or mandated by governmental authorities.

The Company has acted on the aggressive emergency measures set in place by the provincial government and federal authorities, keeping in mind, firstly, the immediate health and safety of our employees and customers. Employees in the head office, located in Toronto, Ontario, Canada had been working remotely for some time or alternating their office time, ensuring there is no more than one employee present, ensuring they are social distancing and wearing protective face covering within the office and elsewhere outside the office, as per the measures set in place by provincial and local authorities. Employees at the site in Belleville, Ontario, Canada, have also been following the same procedures. The Company has prohibited face to face meetings and all meetings are now and for some time, being held by teleconference.

The Company is fortunate that its operations have not been forced to close as we're considered an essential service. In the early stages of COVID-19, the receipt of organic waste has increased, the likely impact of the requirement for the public to stay in their residences, unless they themselves are employed in an essential business or service. A broad, sustained outbreak of COVID-19 will negatively impact our results and financial condition for the following reasons: (i) a large percentage of our customers are municipalities and their limited operations have resulted in a delay in the collection of outstanding receivables in the early months of COVID-19, impacting our cash flows, including the use of cash (ii) members of the board, management or employee team, some of whom are particularly at-risk for the severe symptoms of COVID-19, or of our small number of other employees, may become ill or have family members who are ill and are absent as a result, or they may elect not to come to work due to the illness affecting others in our office or facility (iii) the outbreak may materially impact our operations for a sustained period of time due to the current travel bans and restrictions, quarantines, social or physical distancing orders and shutdowns.

The occurrence of any of the these noted events and potentially others, could have a material adverse effect on our business, financial condition and results of operations. The COVID-19 outbreak and mitigation measures have had and may continue to have an adverse impact on global economic conditions which could have an adverse effect on our business and financial condition. The extent to which the COVID-19 outbreak impacts our results will depend on future developments that are highly uncertain and cannot be predicted, including new information that may emerge concerning the severity of COVID-19 and the actions to contain its impact.

To date, there has been no material impact on the Company's workforce, operations, financial performance, liquidity, or supply chain as a result of COVID-19. However, the ultimate duration and severity of COVID-19 or its effects on the economy, the capital and credit markets, or the Company's workforce, customers, and suppliers, as well as governmental and regulatory responses, are uncertain.

Risks Related to Our Business and Industry

We may experience claims that our products infringe the intellectual property rights of others, which may cause us to incur unexpected costs or prevent us from selling our products.

We seek to improve our business processes and develop new products and applications. Many of our competitors have a substantial amount of intellectual property that we must continually monitor to avoid infringement. We cannot guarantee that we will not experience claims that our processes and products infringe issued patents (whether present or future) or other intellectual property rights belonging to others. If we are sued for infringement and lose, we could be required to pay substantial damages or be enjoined from using or selling the infringing products or technology. Further, intellectual property litigation is expensive and time-consuming, regardless of the merits of any claim, and could divert our management's attention from operating our business.

Our relationship with our employees could deteriorate, and certain key employees could leave the Company, which could adversely affect our business and our results of operations.

Our business involves complex operations and therefore demands a management team and employee workforce that is knowledgeable and expert in many areas necessary for our operations. We rely on our ability to attract and retain skilled employees, including our specialized research and development and sales and service personnel, to maintain our efficient production. The departure of a significant number of our highly skilled employees or of one or more employees who hold key management positions could have an adverse impact on our operations, including as a result of customers choosing to follow a regional manager to one of our competitors.

We face intense competition, and our failure to compete successfully may have an adverse effect on our net sales, gross profit and financial condition.

Our industry is highly competitive. Many of our competitors may have greater financial, technical and marketing resources than we do and may be able to devote greater resources to promoting and selling certain products, and our competitors may therefore have greater financial, technical and marketing resources available to them than we do.

If we do not compete successfully by developing and deploying new cost-effective products, processes and technologies on a timely basis and by adapting to changes in our industry and the global economy, our net sales, gross profit and financial condition could be adversely affected.

Failure to comply with the Foreign Corrupt Practices Act, or FCPA, and other similar anti-corruption laws, could subject us to penalties and damage our reputation.

We are subject to the FCPA, which generally prohibits U.S. companies and their intermediaries from making corrupt payments to foreign officials for the purpose of obtaining or keeping business or otherwise obtaining favorable treatment and requires companies to maintain certain policies and procedures. Certain of the jurisdictions in which we conduct business may be at a heightened risk for corruption, extortion, bribery, pay-offs, theft and other fraudulent practices. Under the FCPA, U.S. companies may be held liable for actions taken by their strategic or local partners or representatives. If we, or our intermediaries, fail to comply with the requirements of the FCPA, or similar laws of other countries, governmental authorities in the United States or elsewhere, as applicable, could seek to impose civil and/or criminal penalties, which could damage our reputation and have a material adverse effect on our business, financial condition and results of operations.

We are not insured against all potential risks.

To the extent available, we maintain insurance coverage that we believe is customary in our industry. Such insurance does not, however, provide coverage for all liabilities, including certain hazards incidental to our business, and we cannot assure you that our insurance coverage will be adequate to cover claims that may arise or that we will be able to maintain adequate insurance at rates we consider reasonable.

We may not be able to consummate future acquisitions or successfully integrate acquisitions into our business, which could result in unanticipated expenses and losses.

Part of our strategy is to grow through acquisitions. Consummating acquisitions of related businesses, or our failure to integrate such businesses successfully into our existing businesses, could result in unanticipated expenses and losses. Furthermore, we may not be able to realize any of the anticipated benefits from the acquisitions.

In connection with potential future acquisitions, the process of integrating acquired operations into our existing operations may result in unforeseen operating difficulties and may require significant financial resources that would otherwise be available for the ongoing development or expansion of existing operations. Some of the risks associated with acquisitions include:

• unexpected losses of key employees or customers of the acquired company;

• conforming the acquired company's standards, processes, procedures and controls with our operations;

• coordinating new product and process development;

• hiring additional management and other critical personnel;

• negotiating with labor unions; and

• increasing the scope, geographic diversity and complexity of our operations.