Attached files

| file | filename |

|---|---|

| EX-99.1 - EXHIBIT 99.1 - BRIGGS & STRATTON CORP | brhc10016746_ex99-1.htm |

| 8-K - 8-K - BRIGGS & STRATTON CORP | brhc10016746_8k.htm |

Exhibit 99.2

|

THIS DISCLOSURE STATEMENT IS BEING SUBMITTED FOR APPROVAL BUT HAS NOT YET BEEN APPROVED BY THE BANKRUPTCY COURT. THIS IS NOT A SOLICITATION

OF ACCEPTANCE OR REJECTION OF THE PLAN. ACCEPTANCES OR REJECTIONS MAY NOT BE SOLICITED UNTIL A DISCLOSURE STATEMENT HAS BEEN APPROVED BY THE BANKRUPTCY COURT. THE INFORMATION IN THIS DISCLOSURE STATEMENT IS SUBJECT TO CHANGE. THIS

DISCLOSURE STATEMENT IS NOT AN OFFER TO SELL ANY SECURITIES AND IS NOT SOLICITING AN OFFER TO BUY ANY SECURITIES.

|

EASTERN DISTRICT OF MISSOURI

SOUTHEASTERN DIVISION

|

§

|

Chapter 11

|

|

|

In re:

|

§

|

|

|

§

|

Case No. 20-43597-399

|

|

|

BRIGGS & STRATTON

|

§

|

|

|

CORPORATION, et al.,

|

§

|

(Jointly Administered)

|

|

§

|

||

|

Debtors.

|

§

|

AMENDED DISCLOSURE STATEMENT FOR JOINT CHAPTER 11 PLAN OF

BRIGGS & STRATTON CORPORATION AND ITS AFFILIATED DEBTORS

BRIGGS & STRATTON CORPORATION AND ITS AFFILIATED DEBTORS

|

WEIL, GOTSHAL & MANGES LLP

Ronit J. Berkovich (admitted pro hac vice)

Debora A. Hoehne (admitted pro hac vice)

Martha E. Martir (admitted pro hac vice)

767 Fifth Avenue

New York, New York 10153

Telephone: (212) 310-8000

Facsimile: (212) 310-8007

|

CARMODY MACDONALD P.C.

Robert E. Eggmann, #37374MO

Christopher J. Lawhorn, #45713MO

Thomas H. Riske, #61838MO

120 S. Central Avenue, Suite 1800

St. Louis, Missouri 63105

Telephone: (314) 854-8600

Facsimile: (314) 854-8660

|

|

Attorneys for Debtors

|

|

|

and Debtors in Possession

|

| Dated: |

November 6, 2020

|

|

St. Louis, Missouri

|

|

A SOLICITATION OF VOTES IS BEING CONDUCTED TO OBTAIN SUFFICIENT ACCEPTANCES

OF THE JOINT CHAPTER 11 PLAN OF BRIGGS & STRATTON CORPORATION AND ITS AFFILIATED DEBTORS (AS MAY BE AMENDED, MODIFIED, OR SUPPLEMENTED FROM TIME TO TIME,

THE “PLAN”). A COPY OF THE PLAN IS ANNEXED HERETO AS EXHIBIT A.

YOU ARE ADVISED TO REVIEW AND CONSIDER THIS DISCLOSURE STATEMENT AND THE PLAN CAREFULLY, INCLUDING THE INJUNCTION, RELEASE, AND EXCULPATION

PROVISIONS, AS YOUR RIGHTS MAY BE AFFECTED.

THE RECORD DATE FOR DETERMINING WHICH HOLDERS OF CLAIMS MAY VOTE ON THE PLAN IS NOVEMBER 9, 2020 (THE “VOTING RECORD DATE”).

THE VOTING DEADLINE TO ACCEPT OR REJECT THE PLAN IS 5:00 P.M., PREVAILING CENTRAL TIME, DECEMBER 11, 2020 (THE “VOTING DEADLINE”), UNLESS EXTENDED BY THE DEBTORS.

IF YOU FILE AN OBJECTION TO THE PLAN IN ACCORDANCE WITH THE PROCEDURES SET FORTH HEREIN, A HEARING WILL BE HELD IN PERSON AND

TELEPHONICALLY, ON DECEMBER 18, 2020 AT 9:00 A.M. (CENTRAL TIME) AT WHICH YOU WILL BE RQUIRED TO

APPEAR.

|

|

RECOMMENDATION BY THE DEBTORS

AND THE OFFICIAL COMMITTEE OF UNSECURED CREDITORS

The Board of Directors of Briggs & Stratton Corporation and the board of directors, managers, or

members, as applicable, of each of its affiliated Debtors have unanimously approved the transactions contemplated by the Plan (as defined herein) and recommend that all creditors whose votes are being solicited submit ballots to accept the

Plan.

The Official Committee of Unsecured Creditors also recommends that all creditors whose votes are

being solicited submit ballots to accept the Plan.

|

THE INFORMATION CONTAINED IN THIS DISCLOSURE STATEMENT IS INCLUDED HEREIN FOR THE PURPOSES OF SOLICITING SUFFICIENT ACCEPTANCES OF THE JOINT CHAPTER

11 PLAN OF BRIGGS & STRATTON CORPORATION AND ITS AFFILIATED DEBTORS. NO SOLICITATION OF VOTES TO ACCEPT OR REJECT THE PLAN MAY BE MADE EXCEPT PURSUANT TO SECTION 1125 OF THE BANKRUPTCY CODE.

HOLDERS OF CLAIMS OR INTERESTS SHOULD NOT CONSTRUE THE CONTENTS OF THIS DISCLOSURE

STATEMENT AS PROVIDING ANY LEGAL, BUSINESS, FINANCIAL, OR TAX ADVICE AND SHOULD CONSULT WITH THEIR OWN ADVISORS BEFORE VOTING ON THE PLAN. HOLDERS OF CLAIMS OR INTERESTS ARE ADVISED AND ENCOURAGED TO READ BOTH THE DISCLOSURE STATEMENT AND THE

PLAN IN THEIR ENTIRETY. IN PARTICULAR, ALL HOLDERS OF CLAIMS OR INTERESTS SHOULD CAREFULLY READ AND CONSIDER FULLY THE RISK FACTORS SET FORTH IN SECTION IX OF THIS DISCLOSURE STATEMENT. THE PLAN SUMMARIES AND STATEMENTS MADE IN THIS DISCLOSURE

STATEMENT ARE QUALIFIED IN THEIR ENTIRETY BY REFERENCE TO THE PLAN AND THE EXHIBITS ANNEXED TO THE PLAN, THE PLAN SUPPLEMENT, AND THIS DISCLOSURE STATEMENT. IN THE EVENT OF ANY CONFLICTS BETWEEN THE DESCRIPTIONS SET FORTH IN THIS DISCLOSURE

STATEMENT AND THE TERMS OF THE PLAN, THE TERMS OF THE PLAN SHALL GOVERN.

THE DISCLOSURE STATEMENT HAS BEEN PREPARED IN ACCORDANCE WITH SECTION 1125 OF THE BANKRUPTCY CODE AND BANKRUPTCY RULE 3016(B) AND NOT NECESSARILY IN

ACCORDANCE WITH OTHER NON-BANKRUPTCY LAW.

CERTAIN STATEMENTS CONTAINED IN THIS DISCLOSURE STATEMENT, INCLUDING STATEMENTS

INCORPORATED BY REFERENCE, PROJECTED CREDITOR RECOVERIES, PROJECTED FINANCIAL INFORMATION, AND OTHER FORWARD-LOOKING STATEMENTS, ARE BASED ON ESTIMATES AND

ASSUMPTIONS. CERTAIN OF THESE FORWARD-LOOKING STATEMENTS CAN BE IDENTIFIED BY THE USE OF WORDS SUCH AS “BELIEVES,” “EXPECTS,” “PROJECTS,” “INTENDS,” “PLANS,” “ESTIMATES,” “ASSUMES,” “MAY,” “SHOULD,” “WILL,” “SEEKS,” “ANTICIPATES,” “OPPORTUNITY,”

“PRO FORMA,” “PROJECTIONS,” OR OTHER SIMILAR EXPRESSIONS. THERE CAN BE NO ASSURANCE THAT SUCH STATEMENTS WILL BE REFLECTIVE OF ACTUAL OUTCOMES. FORWARD-LOOKING STATEMENTS ARE PROVIDED IN THIS DISCLOSURE STATEMENT PURSUANT TO THE SAFE HARBOR

ESTABLISHED UNDER THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995 AND SHOULD BE EVALUATED IN THE CONTEXT OF THE ESTIMATES, ASSUMPTIONS, UNCERTAINTIES, AND RISKS DESCRIBED HEREIN. READERS ARE CAUTIONED THAT ANY FORWARD-LOOKING STATEMENTS

CONTAINED HEREIN ARE BASED ON ASSUMPTIONS THAT ARE BELIEVED TO BE REASONABLE, BUT ARE SUBJECT TO A WIDE RANGE OF RISKS, INCLUDING THOSE IDENTIFIED IN SECTION IX OF THIS DISCLOSURE STATEMENT.

THE DEBTORS ARE UNDER NO OBLIGATION TO (AND EXPRESSLY DISCLAIM ANY OBLIGATION TO) UPDATE OR ALTER ANY FORWARD-LOOKING STATEMENTS WHETHER AS A RESULT

OF NEW INFORMATION, FUTURE EVENTS, OR OTHERWISE, UNLESS INSTRUCTED TO DO SO BY THE BANKRUPTCY COURT (AS DEFINED BELOW).

NO INDEPENDENT AUDITOR OR ACCOUNTANT HAS REVIEWED OR APPROVED THE LIQUIDATION ANALYSIS ANNEXED HERETO AS EXHIBIT B.

THE STATEMENTS CONTAINED IN THIS DISCLOSURE STATEMENT ARE MADE AS OF THE DATE HEREOF UNLESS OTHERWISE SPECIFIED. THE TERMS OF THE PLAN GOVERN IN

THE EVENT OF ANY INCONSISTENCY WITH THE SUMMARIES IN THIS DISCLOSURE STATEMENT.

ALL EXHIBITS TO THE DISCLOSURE STATEMENT ARE INCORPORATED INTO, AND ARE A PART OF, THIS DISCLOSURE STATEMENT AS IF SET FORTH IN FULL HEREIN.

THE INFORMATION IN THIS DISCLOSURE STATEMENT IS BEING PROVIDED SOLELY FOR PURPOSES OF VOTING TO ACCEPT OR REJECT THE PLAN PURSUANT TO SECTION 1125

OF THE BANKRUPTCY CODE OR IN CONNECTION WITH CONFIRMATION OF THE PLAN. NOTHING IN THIS DISCLOSURE STATEMENT MAY BE USED BY ANY PARTY FOR ANY OTHER PURPOSE.

A HEARING TO CONSIDER CONFIRMATION OF THE PLAN WILL BE HELD BEFORE THE HONORABLE BARRY S. SCHERMER, UNITED STATES BANKRUPTCY JUDGE, AT THE UNITED

STATES BANKRUPTCY COURT FOR THE EASTERN DISTRICT OF MISSOURI, SOUTHEASTERN DIVISION, 111 S. 10TH ST, COURTROOM 5 NORTH, ST, LOUIS, MISSOURI 63102, ON DECEMBER 18, 2020 AT 9 A.M.

(CENTRAL TIME), OR AS SOON THEREAFTER AS COUNSEL MAY BE HEARD.

THE BANKRUPTCY COURT HAS DIRECTED THAT ANY OBJECTIONS TO CONFIRMATION OF THE PLAN BE SERVED AND FILED ON OR BEFORE DECEMBER 11, 2020 AT 4:00 P.M. (CENTRAL TIME).

PLEASE READ THIS DISCLOSURE STATEMENT, INCLUDING THE PLAN, IN ITS ENTIRETY. THE DISCLOSURE STATEMENT SUMMARIZES THE TERMS OF THE PLAN, BUT SUCH

SUMMARY IS QUALIFIED IN ITS ENTIRETY BY THE ACTUAL PROVISIONS OF THE PLAN. ACCORDINGLY, IF THERE ARE ANY INCONSISTENCIES BETWEEN THE PLAN AND THIS DISCLOSURE STATEMENT, THE TERMS OF THE PLAN SHALL CONTROL.

ii

TABLE OF CONTENTS

|

I. INTRODUCTION

|

1

|

||

|

II. OVERVIEW OF THE COMPANY’S OPERATIONS

|

17

|

||

|

A.

|

The Debtors’ Business

|

17

|

|

|

B.

|

Debtors’ Organizational Structure.

|

20

|

|

|

C.

|

Directors and Officers.

|

21

|

|

|

D.

|

Debtors’ Prepetition Capital Structure

|

22

|

|

|

III. CIRCUMSTANCES LEADING TO COMMENCEMENT OF THE CHAPTER 11 CASES

|

31

|

||

|

A.

|

Strategic and Cash Preservation Initiatives

|

31

|

|

|

B.

|

COVID-19

|

32

|

|

|

C.

|

Prepetition Marketing and Restructuring Efforts

|

32

|

|

|

IV. OVERVIEW OF THE CHAPTER 11 CASES

|

34

|

||

|

A.

|

Commencement of The Chapter 11 Cases and First-Day Motions

|

34

|

|

|

B.

|

DIP Financing and Cash Collateral

|

35

|

|

|

C.

|

Retiree Benefits

|

36

|

|

|

D.

|

Procedural Motions and Retention of Professionals

|

36

|

|

|

E.

|

Sale Transaction and Global Settlement

|

36

|

|

|

F.

|

Appointment of the Creditors’ Committee

|

40

|

|

|

G.

|

Bar Date

|

41 | |

|

H.

|

Statements and Schedules, and Rule 2015.3 Financial Reports

|

42

|

|

|

I.

|

Automatic Stay Motions

|

42

|

|

|

J.

|

Workers’ Compensation

|

43

|

|

|

K.

|

Plaintiff-Side Litigations

|

44

|

|

|

L.

|

Executory Contracts

|

44

|

|

|

M.

|

Remaining Assets

|

45

|

|

|

N.

|

Claims Against the Estates

|

46

|

|

|

O.

|

Asbestos and Products Liability Insurance

|

48

|

|

|

P.

|

The Plan and the Wind-Down Process

|

49

|

|

|

V. SUMMARY OF PLAN

|

50

|

||

|

A.

|

Administrative Expenses and Priority Claims

|

50

|

|

|

B.

|

Classification of Claims and Interests

|

52

|

|

|

C.

|

Treatment of Claims and Interests

|

53

|

|

|

D.

|

Means for Implementation

|

67

|

|

|

E.

|

Distributions

|

76

|

|

|

F.

|

Procedures for Disputed Claims

|

80

|

|

|

G.

|

Executory Contracts and Unexpired Leases

|

82

|

|

|

H.

|

Conditions Precedent to Confirmation of Plan and Effective Date

|

84

|

|

|

I.

|

Effect of Confirmation of Plan

|

85

|

|

|

J.

|

Retention of Jurisdiction

|

91

|

|

|

K.

|

Miscellaneous Provisions

|

92

|

|

|

VI. VALUE

|

96

|

||

|

VII. CERTAIN U.S. FEDERAL INCOME TAX CONSEQUENCES OF PLAN

|

96

|

||

|

A.

|

Consequences to Debtors

|

98

|

|

|

B.

|

Consequences to Holders of Certain Claims

|

99

|

|

|

C.

|

Tax Treatment of a Liquidating Trust and Holders of Beneficial Interests

|

102

|

|

|

D.

|

Withholding on Distributions and Information Reporting

|

104

|

|

|

VIII. CERTAIN RISK FACTORS TO BE CONSIDERED

|

104

|

||

|

A.

|

Certain Bankruptcy Law Considerations

|

105

|

|

|

B.

|

Additional Factors

|

106 | |

|

IX. VOTING PROCEDURES AND REQUIREMENTS

|

108

|

||

|

A.

|

Voting Deadline

|

108

|

|

|

B.

|

Voting Procedures

|

109

|

|

|

C.

|

Parties Entitled to Vote

|

109

|

|

|

X. CONFIRMATION OF PLAN

|

111

|

||

|

A.

|

Disclosure Statement Hearing and Confirmation Hearing

|

111 | |

|

B.

|

Objections to Confirmation and Final Approval of Disclosure Statement

|

112

|

|

|

C.

|

Requirements for Confirmation of Plan

|

113

|

|

|

(i)

|

Requirements of Section 1129(a) of Bankruptcy Code

|

113

|

|

|

(ii)

|

Additional Requirements for Non-Consensual Confirmation Under Section 1129(b) of the Bankruptcy Code

|

115

|

|

|

XI. ALTERNATIVES TO CONFIRMATION AND CONSUMMATION OF PLAN

|

117

|

||

|

A.

|

Alternative Plan

|

117

|

|

|

B.

|

Liquidation Under Chapter 7 or Applicable Non-Bankruptcy Law

|

117

|

|

|

XII. CONCLUSION AND RECOMMENDATION

|

118

|

||

4

|

EXHIBIT A:

|

Plan

|

|

EXHIBIT B:

|

Liquidation Analysis

|

|

EXHIBIT C:

|

Recovery Analysis

|

5

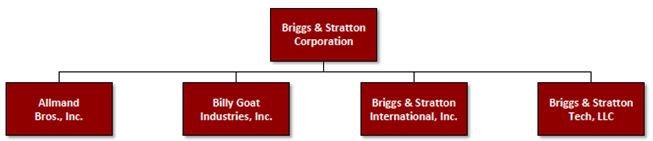

Briggs & Stratton Corporation (“BSC”), Billy Goat Industries, Inc. (“BGI” or “Billy Goat”), Allmand Bros., Inc. (“ABI” or “Allmand Bros.”), Briggs & Stratton International, Inc. (“BSI” or “B&S International), and Briggs & Stratton Tech, LLC (“BST” or “B&S Tech”) (collectively, the “Debtors” and together with their non-Debtor affiliates, “Briggs & Stratton” or the “Company”) commenced their chapter 11 cases (the “Chapter 11 Cases”) in the

United States Bankruptcy Court for the Eastern District of Missouri (the “Bankruptcy Court”) on July 20, 2020 (the “Petition Date”).

The Debtors submit this disclosure statement (as amended, modified, or supplemented from time to time, the “Disclosure Statement”) pursuant to section 1125 of title 11 of the United States Code (the “Bankruptcy Code”) in

connection with the solicitation of votes with respect to the Joint Chapter 11 Plan of Briggs & Stratton Corporation and its Affiliated Debtors, dated

October 9, 2020 (as amended, modified, or supplemented, the “Plan”).1 The Plan is annexed hereto as Exhibit A and is incorporated herein by reference.

The purpose of this Disclosure Statement, including the exhibits annexed hereto, is to provide information of a kind, and in sufficient detail, to enable creditors of

the Debtors that are entitled to vote on the Plan to make an informed decision on whether to vote to accept or reject the Plan. This Disclosure Statement contains summaries of the Plan, events that have occurred or will occur in the Chapter 11

Cases, certain documents related to the Plan, and instructions for voting on the Plan.

From the beginning, the Debtors announced that their goals in these Chapter 11 Cases were to maximize unsecured creditor recoveries by implementing a comprehensive

restructuring swiftly through a sale of substantially all of their assets and equity interests to the highest or best bidder through a court-approved sale process and minimizing administrative expenses by working cooperatively with creditors,

including the Creditors’ Committee.2 The Debtors are pleased to have accomplished these goals in a very short time frame, as they have successfully sold their assets, reached a global settlement with the Creditors’ Committee on the major

issues in these chapter 11 cases, and proposed this Plan, which provides a recovery to general unsecured creditors. The final steps of this process are confirming the Plan, consummating the Plan, and making distributions to creditors.

|

The Plan has been proposed in close consultation with the Creditors’ Committee, and the Creditors’ Committee urges all creditors to vote

to accept the Plan.

|

| A. |

Summary of the Sale Transaction and the Global Settlement

|

The Debtors commenced the Chapter 11 Cases with a stalking horse bid from the Purchaser (as defined herein), after a robust, months-long marketing process conducted by

the Debtors and their advisors in pursuit of the most beneficial solution for the Debtors and their creditors. Through the Stalking Horse Agreement (as defined herein), the Debtors secured a guaranteed purchase price of $550 million (subject to

adjustment) plus assumed liabilities for their business and through the bidding procedures developed by the Debtors and their advisors, the Debtors retained the right to seek and accept a higher or better bid allowing for potential increased

recovery for creditors. While the Debtors did not receive a higher or better bid, the Debtors still achieved a substantial purchase price for their assets, which the Debtors believe reflects the value of their estates and will allow creditors to

receive the largest possible recovery from the Debtors’ estates under the circumstances, which will allow the Debtors to pay unsecured creditors’ claims in part.

| 1 |

Capitalized terms used in this Disclosure Statement, but not defined herein, shall have the meanings ascribed to such terms in the Plan. To the extent any

inconsistencies exist between this Disclosure Statement and the Plan, the Plan shall govern.

|

| 2 |

The Creditors’ Committee was appointed on August 5, 2020, as discussed in Section (IV)(F) infra.

|

On September 15, 2020, the Bankruptcy Court entered an order3 authorizing the sale of the Debtors’ assets and equity interests to the Stalking Horse Bidder

(the “Sale Transaction”). The Sale Transaction closed on September 21, 2020, at which time the Purchaser paid the purchase price of $550 million to the

Debtors through a combination of cash, credit bid, and certain other deductions and adjustments, and the Purchaser assumed substantially all of the Debtors’ assets and assumed certain of the Debtors’ liabilities.

In the weeks leading to the hearing to approve the Sale Transaction (as defined herein), the Debtors entered into extensive negotiations with the Creditors’ Committee,

the Pension Benefit Guaranty Corporation (the “PBGC”) (the Debtors’ largest creditor), the DIP Agent and DIP Lenders (as defined below), and the Purchaser to

resolve the Creditors’ Committee’s and the PBGC’s potential objections to the Sale Transaction and to ensure the Debtors could move swiftly to consummate the Sale Transaction and the subsequent Plan with the support of the Creditors’ Committee and

the PBGC. The parties were able to reach a global settlement (the “Global Settlement”), by which the Creditors’ Committee and the PBGC consented to the Sale

Transaction to the extent it was consummated before September 27, 2020. Under the Global Settlement, the Debtors and the Creditors’ Committee agreed to work in good faith on a chapter 11 plan to facilitate and give effect to the Global Settlement.4

CONFIRMATION OF THE AMENDED PLAN WILL BIND ALL CREDITORS TO THE GLOBAL SETTLEMENT WHETHER OR NOT SUCH CREDITORS HAVE VOTED TO ACCEPT

THE AMENDED PLAN.

| B. |

The Plan

|

The Plan provides for the orderly distribution of each Debtor’s available cash, including (i) net cash proceeds received by the Debtors from the Sale Transaction

(including any proceeds to be received post-closing thereof) (the “Sale Transaction Proceeds”), and (ii) cash realized from the Debtors’ business and their

wind-down operations, including the sale of any remaining assets that were not included in the Sale Transaction (the “Wind-Down Proceeds”).

The Plan provides that the Sale Transaction Proceeds and Wind-Down Proceeds shall be used to fund (i) the ongoing wind-down costs of the Chapter 11 Cases, and (ii) the

Distributions to holders of Allowed Claims under the Plan. Specifically, the Plan provides that the Sale Transaction Proceeds and Wind-Down Proceeds shall be used, first, to (a) pay holders of Allowed (or reserve for holders of Disputed)

Administrative Expense Claims, Fee Claims, and DIP Claims; (b) to fund the wind-down process (pursuant to a wind-down budget); and (c) to satisfy any

Statutory Fees required to be paid in accordance with the Bankruptcy Code, the Bankruptcy Rules or any order of the Bankruptcy Court.

Following such payments, the Plan provides that the remaining Sale Transaction Proceeds and Wind-Down Proceeds (the “Net Cash Proceeds”) shall be allocated among the Debtors as follows:

| 3 |

Order (I) Authorizing the Sale of the Assets and Equity Interest to the Purchaser Free and Clear

of Liens, Claims, Interests, and Encumbrances; (II) Authorizing the Assumption and Assignment of Certain Executory Contracts and Unexpired Leases; and (III) Granting Related Relief (Docket No. 898) (the “Sale Order”).

|

| 4 |

The terms of the Global Settlement are set out in further detail in section (IV)(E)(d) infra.

|

2

| a) |

79.0% of the Net Cash Proceeds shall be allocated to BSC (the “Net Cash Proceeds (BSC)”);

|

| b) |

8.1% of the Net Cash Proceeds shall be allocated to BGI (the “Net Cash Proceeds (BGI)”);

|

| c) |

6.7% of the Net Cash Proceeds shall be allocated to ABI (the “Net Cash Proceeds (ABI)”);

|

| d) |

4.8% of the Net Cash Proceeds shall be allocated to BSI (the “Net Cash Proceeds (BSI)”);

and

|

| e) |

1.4% of the Net Cash Proceeds shall be allocated to BST (the “Net Cash Proceeds (BST)”).

|

The allocation above is based on an analysis by the Debtors’ financial advisor, Houlihan Lokey, in consultation with the Creditors’ Committee’s financial advisor. It

allocates the Net Cash Proceeds based on an equal weighting of revenue, assets, and adjusted EBITDA, subject to adjustments made based on bids received for the different entities, certain remaining assets, and other qualitative factors such as

intercompany relationships between the entities.

The Plan further provides that the Net Cash Proceeds allocable to each Debtor shall be distributed first to each Debtor’s priority and other secured claims and then

pro rata (proportionately) to holders of Allowed General Unsecured Claims against such Debtor, in each case after giving effect to the “PBGC Subordination,”

which refers to the agreement of the PBGC, pursuant to the Global Settlement, to subordinate to other general unsecured creditors the first $5 million of the recovery it would otherwise receive from the Plan.5 The Debtors do not expect

there to be a recovery for shareholders.

The Plan provides for the appointment of a Plan Administrator (the identity of which will be provided in the Plan Supplement (as defined below)) to oversee the Plan,

including to liquidate/monetize any remaining assets, to resolve disputed claims, and to make distributions to creditors under the Plan.

Importantly, the Plan is not premised upon the substantive consolidation of the Debtors or their assets or liabilities. The Plan is being proposed as a joint plan of

the Debtors for administrative purposes only and treats the Claims against each Debtor separately. Accordingly, if the Bankruptcy Court does not confirm the Plan with respect to one or more Debtors, it may still, subject to the consent of the

applicable Debtors, confirm the Plan with respect to any other Debtor that satisfies the confirmation requirements of section 1129 of the Bankruptcy Code.6

| C. |

Confirmation Timeline

|

The Debtors seek to move forward expeditiously with the solicitation of votes and a hearing on confirmation of the Plan in an effort to minimize the continuing accrual

of administrative expenses. Accordingly, subject to the Bankruptcy Court’s approval, the Debtors are proceeding on the following timeline with respect to the Disclosure Statement and the Plan:

| 5 |

Under Section 1.79 of the Plan, PBGC Subordination means, pursuant to the Global Settlement,

that the first $5 million that the PBGC would otherwise recover on account of the PBGC General Unsecured Claims hereunder shall be subordinated to the recovery of all other Allowed General Unsecured Claims in manner that ensures that the

benefit of the PBGC Subordination is allocated to classes 4(a), 4(b), and 4(c) proportionately in accordance with the relative Net Cash Proceeds allocated to each of those classes, with the PBGC General Unsecured Claim not recovering in any

class until the PBGC Subordination is fully effectuated.

|

| 6 |

The Debtors reserve the right to argue that the Plan may be confirmed as long as there is one impaired accepting class of creditors in the joint plan. See In re Transwest Resort Properties Inc., 881 F.3d 724 (9th Cir. 2018).

|

3

|

Deadline to Object to the Disclosure Statement

|

November 2, 2020 at 5:00 p.m. (CT)

|

|

Disclosure Statement Hearing

|

November 9, 2020 at 10:00 a.m. (CT)

|

|

Voting Record Date

|

November 9, 2020

|

|

Plan Supplement Filing

|

Seven (7) calendar days prior to the Plan Objection Deadline

(anticipated to be December 4, 2020)

|

|

Deadline to Object to Confirmation of Plan

|

December 11, 2020 at 5:00 p.m. (CT)

|

|

Voting Deadline

|

December 11, 2020 at 5:00 p.m. (CT)

|

|

Deadline to File (i) Reply to Plan Objection(s) and (ii) Brief in Support of Plan Confirmation

|

December 16, 2020 at 5:00 p.m. (CT)

|

|

Plan Confirmation Hearing

|

December 18, 2020 at 9:00 a.m. (CT)

|

| D. |

Summary of Plan Classification and Treatment of Claims

|

|

THE DEBTORS AND CREDITORS’ COMMITTEE SUPPORT CONFIRMATION OF THE PLAN AND URGE ALL HOLDERS OF CLAIMS ENTITLED TO VOTE ON THE PLAN TO VOTE TO

ACCEPT THE PLAN. THE DEBTORS BELIEVE THAT THE PLAN PROVIDES THE HIGHEST AND BEST POSSIBLE RECOVERY FOR ALL STAKEHOLDERS.

|

WHO IS ENTITLED TO VOTE: Under the Bankruptcy Code, only holders of claims or

interests in “impaired” Classes are entitled to vote on the Plan (unless, for reasons discussed in more detail below, such holders are deemed to reject the Plan pursuant to section 1126(g) of the Bankruptcy Code). Under section 1124 of the

Bankruptcy Code, a class of claims or interests is deemed to be “impaired” unless (i) the Plan leaves unaltered the legal, equitable, and contractual rights to which such claim or interest entitles the holder thereof or (ii) notwithstanding any

legal right to an accelerated payment of such claim or interest, the Plan, among other things, cures all existing defaults (other than defaults resulting from the occurrence of events of bankruptcy) and reinstates the maturity of such claim or

interest as it existed before the default.

HOLDERS OF CLAIMS IN CLASS 4(A) (GENERAL UNSECURED CLAIMS AGAINST BSC), CLASS 4(B) (GENERAL UNSECURED CLAIMS AGAINST BGI), 4(C) (GENERAL UNSECURED

CLAIMS AGAINST ABI), CLASS 4(D) (GENERAL UNSECURED CLAIMS AGAINST BSI), AND CLASS 4(E) (GENERAL UNSECURED CLAIMS AGAINST BST) ARE THE ONLY CLASSES BEING SOLICITED UNDER, AND THE ONLY CLASSES ENTITLED TO VOTE ON, THE PLAN.

4

THE PLAN INCLUDES CERTAIN RELEASES SET FORTH IN SECTION 10.6 OF THE PLAN. THE PLAN PROVIDES THAT HOLDERS OF CLAIMS IN CLASS 4(A) (GENERAL UNSECURED

CLAIMS AGAINST BSC), CLASS 4(B) (GENERAL UNSECURED CLAIMS AGAINST BGI), 4(C) (GENERAL UNSECURED CLAIMS AGAINST ABI), CLASS 4(D) (GENERAL UNSECURED CLAIMS AGAINST BSI), AND CLASS 4(E) (GENERAL UNSECURED CLAIMS AGAINST BST)WHO (I) VOTE TO ACCEPT THE

PLAN, (II) ABSTAIN FROM VOTING ON THE PLAN, OR (III) WHO VOTE TO REJECT THE PLAN BUT, IN EITHER OF CASES (II) AND (III), DO NOT OPT OUT OF GRANTING THE RELEASES SET FORTH IN SECTION 10.6 OF THE PLAN, SHALL BE DEEMED TO GRANT SUCH RELEASES.

The following table summarizes (i) the treatment of Claims and Interests that are classified under the Plan, (ii) which Classes are impaired by the Plan, (iii) which

Classes are entitled to vote on the Plan, and (iv) the estimated recoveries for holders of Claims and Interests under the Plan. The table is qualified in its entirety by reference to the full text of the Plan. For a more detailed summary of the

terms and provisions of the Plan, see Article V—Summary of Plan below. The Plan constitutes a separate plan for each Debtor. Each class of Claims and Interests only addresses claims against, or interests in, a particular Debtor. A discussion of

the amount of Claims in each Class is set forth in Article V.B hereof.

Note that the “Approximate Recovery Under the Plan” is only an estimate. As the General Bar Date only occurred on October 7, 2020 (and the Governmental Bar Date will

not occur until January 19, 2021), the Debtors have only begun the process of reconciling Claims. The actual recovery under the Plan will depend, among other things, on the Allowed amount of General Unsecured Claims in each Class.

|

Class

|

Claim or

Equity Interest

|

Treatment

|

Impaired or

Unimpaired

|

Entitled to

Vote on

the Plan

|

Approximate

Recovery

Under Plan7

|

|

1(a)

|

Priority Tax Claims

against BSC

|

Except to the extent that a holder of an Allowed Priority Tax Claim against BSC agrees to less favorable treatment,

each holder of an Allowed Priority Tax Claim against BSC shall receive, in full and final satisfaction of such Allowed Priority Tax Claim against BSC, at the sole option of the Debtors or the Plan Administrator, as applicable, (a) Cash

(from the Net Cash Proceeds (BSC)) in an amount equal to such Allowed Priority Tax Claim against BSC on, or as soon thereafter as is reasonably practicable, the later of (i) the Effective Date, to the extent such Claim is an Allowed

Priority Tax Claim against BSC on the Effective Date; (ii) the first Business Day after the date that is forty-five (45) calendar days after the date such Priority Tax Claim becomes an Allowed Priority Tax Claim against BSC; and (iii) the

date such Allowed Priority Tax Claim against BSC is due and payable in the ordinary course as such obligation becomes due; or (b) equal annual Cash payments (from the Net Cash Proceeds (BSC)) in an aggregate amount equal to the amount of

such Allowed Priority Tax Claim against BSC, together with interest at the applicable rate under section 511 of the Bankruptcy Code, over a period not exceeding five (5) years from and after the Petition Date; provided, that the Debtors reserve the right to prepay all or a portion of any such amounts at any time under this option without penalty or premium.

|

Unimpaired

|

No (Presumed to accept)

|

100%

|

|

7

|

The recovery percentages listed herein for Classes 4(a)-4(e) take into account the PBGC subordination and reflect

recoveries to General Unsecured Creditors other than the PBGC. In addition, please note that the recovery percentages for such Classes are estimates only and as the General Bar Date occurred on October 7, 2020 and certain other bar

dates have not yet occurred, as discussed in Section IV(G), the Debtors have only begun to reconcile claims. The high end of the range is based on the Debtors’ estimate of known liquidated claims with the low end of the range being

calculated using a placeholder estimate of unknown and unliquidated claims.

|

5

|

Class

|

Claim or

Equity Interest

|

Treatment

|

Impaired or

Unimpaired

|

Entitled to

Vote on

the Plan

|

Approximate

Recovery

Under Plan7

|

|

1(b)

|

Priority Tax Claims

against BGI

|

Except to the extent that a holder of an Allowed Priority Tax Claim against BGI agrees to less favorable treatment,

each holder of an Allowed Priority Tax Claim against BGI shall receive, in full and final satisfaction of such Allowed Priority Tax Claim against BGI, at the sole option of the Debtors or the Plan Administrator, as applicable, (a) Cash

(from the Net Cash Proceeds (BGI)) in an amount equal to such Allowed Priority Tax Claim against BGI on, or as soon thereafter as is reasonably practicable, the later of (i) the Effective Date, to the extent such Claim is an Allowed

Priority Tax Claim against BGI on the Effective Date; (ii) the first Business Day after the date that is forty-five (45) calendar days after the date such Priority Tax Claim becomes an Allowed Priority Tax Claim against BGI; and (iii) the

date such Allowed Priority Tax Claim against BGI is due and payable in the ordinary course as such obligation becomes due; or (b) equal annual Cash (from the Net Cash Proceeds (BGI)) payments in an aggregate amount equal to the amount of

such Allowed Priority Tax Claim against BGI, together with interest at the applicable rate under section 511 of the Bankruptcy Code, over a period not exceeding five (5) years from and after the Petition Date; provided, that the Debtors reserve the right to prepay all or a portion of any such amounts at any time under this option without penalty or premium.

|

Unimpaired

|

No (Presumed to accept)

|

100%

|

|

1(c)

|

Priority Tax Claims

against ABI

|

Except to the extent that a holder of an Allowed Priority Tax Claim against ABI agrees to less favorable treatment,

each holder of an Allowed Priority Tax Claim against ABI shall receive, in full and final satisfaction of such Allowed Priority Tax Claim against ABI, at the sole option of the Debtors or the Plan Administrator, as applicable, (a) Cash

(from the Net Cash Proceeds (ABI)) in an amount equal to such Allowed Priority Tax Claim against ABI on, or as soon thereafter as is reasonably practicable, the later of (i) the Effective Date, to the extent such Claim is an Allowed

Priority Tax Claim against ABI on the Effective Date; (ii) the first Business Day after the date that is forty-five (45) calendar days after the date such Priority Tax Claim becomes an Allowed Priority Tax Claim against ABI; and (iii) the

date such Allowed Priority Tax Claim against ABI is due and payable in the ordinary course as such obligation becomes due; or (b) equal annual Cash payments (from the Net Cash Proceeds (ABI)) in an aggregate amount equal to the amount of

such Allowed Priority Tax Claim against ABI, together with interest at the applicable rate under section 511 of the Bankruptcy Code, over a period not exceeding five (5) years from and after the Petition Date; provided, that the Debtors reserve the right to prepay all or a portion of any such amounts at any time under this option without penalty or premium.

|

Unimpaired

|

No (Presumed to accept)

|

100%

|

6

|

Class

|

Claim or

Equity Interest

|

Treatment

|

Impaired or

Unimpaired

|

Entitled to

Vote on

the Plan

|

Approximate

Recovery

Under Plan7

|

|

1(d)

|

Priority Tax Claims

against BSI

|

Except to the extent that a holder of an Allowed Priority Tax Claim against BSI agrees to less favorable treatment,

each holder of an Allowed Priority Tax Claim against BSI shall receive, in full and final satisfaction of such Allowed Priority Tax Claim against BSI, at the sole option of the Debtors or the Plan Administrator, as applicable, (a) Cash

(from the Net Cash Proceeds (BSI)) in an amount equal to such Allowed Priority Tax Claim against BSI on, or as soon thereafter as is reasonably practicable, the later of (i) the Effective Date, to the extent such Claim is an Allowed

Priority Tax Claim against BSI on the Effective Date; (ii) the first Business Day after the date that is forty-five (45) calendar days after the date such Priority Tax Claim becomes an Allowed Priority Tax Claim against BSI; and (iii) the

date such Allowed Priority Tax Claim against BSI is due and payable in the ordinary course as such obligation becomes due; or (b) equal annual Cash payments (from the Net Cash Proceeds (BSI)) in an aggregate amount equal to the amount of

such Allowed Priority Tax Claim against BSI, together with interest at the applicable rate under section 511 of the Bankruptcy Code, over a period not exceeding five (5) years from and after the Petition Date; provided, that the Debtors reserve the right to prepay all or a portion of any such amounts at any time under this option without penalty or premium.

|

Unimpaired

|

No (Presumed to accept)

|

100%

|

|

1(e)

|

Priority Tax Claims

against BST

|

Except to the extent that a holder of an Allowed Priority Tax Claim against BST agrees to less favorable treatment,

each holder of an Allowed Priority Tax Claim against BST shall receive, in full and final satisfaction of such Allowed Priority Tax Claim against BST, at the sole option of the Debtors or the Plan Administrator, as applicable, (a) Cash

(from the Net Cash Proceeds (BST)) in an amount equal to such Allowed Priority Tax Claim against BST on, or as soon thereafter as is reasonably practicable, the later of (i) the Effective Date, to the extent such Claim is an Allowed

Priority Tax Claim against BST on the Effective Date; (ii) the first Business Day after the date that is forty-five (45) calendar days after the date such Priority Tax Claim becomes an Allowed Priority Tax Claim against BST; and (iii) the

date such Allowed Priority Tax Claim against BST is due and payable in the ordinary course as such obligation becomes due; or (b) equal annual Cash payments (from the Net Cash Proceeds (BST)) in an aggregate amount equal to the amount of

such Allowed Priority Tax Claim against BST, together with interest at the applicable rate under section 511 of the Bankruptcy Code, over a period not exceeding five (5) years from and after the Petition Date; provided, that the Debtors reserve the right to prepay all or a portion of any such amounts at any time under this option without penalty or premium.

|

Unimpaired

|

No (Presumed to accept)

|

100%

|

7

|

Class

|

Claim or

Equity Interest

|

Treatment

|

Impaired or

Unimpaired

|

Entitled to

Vote on

the Plan

|

Approximate

Recovery

Under Plan7

|

|

2(a)

|

Priority Non-Tax

Claims against BSC

|

Except to the extent that a holder of an Allowed Priority Non-Tax Claim against BSC agrees to less favorable

treatment, on or as soon as practicable after the Effective Date, each holder thereof shall be paid in full in Cash (from the Net Cash Proceeds (BSC)) or otherwise receive treatment consistent with the provisions of section 1129(a)(9) of

the Bankruptcy Code.

|

Unimpaired

|

No (Presumed to accept)

|

100%

|

|

2(b)

|

Priority Non-Tax

Claims against BGI

|

Except to the extent that a holder of an Allowed Priority Non-Tax Claim against BGI agrees to less favorable

treatment, on or as soon as practicable after the Effective Date, each holder thereof shall be paid in full in Cash (from the Net Cash Proceeds (BGI)) or otherwise receive treatment consistent with the provisions of section 1129(a)(9) of

the Bankruptcy Code.

|

Unimpaired

|

No (Presumed to accept)

|

100%

|

|

2(c)

|

Priority Non-Tax

Claims against ABI

|

Except to the extent that a holder of an Allowed Priority Non-Tax Claim against ABI agrees to less favorable

treatment, on or as soon as practicable after the Effective Date, each holder thereof shall be paid in full in Cash (from the Net Cash Proceeds (ABI)) or otherwise receive treatment consistent with the provisions of section 1129(a)(9) of

the Bankruptcy Code.

|

Unimpaired

|

No (Presumed to accept)

|

100%

|

|

2(d)

|

Priority Non-Tax

Claims against BSI

|

Except to the extent that a holder of an Allowed Priority Non-Tax Claim against BSI agrees to less favorable

treatment, on or as soon as practicable after the Effective Date, each holder thereof shall be paid in full in Cash (from the Net Cash Proceeds (BSI)) or otherwise receive treatment consistent with the provisions of section 1129(a)(9) of

the Bankruptcy Code.

|

Unimpaired

|

No (Presumed to accept)

|

100%

|

|

2(e)

|

Priority Non-Tax

Claims against BST

|

Except to the extent that a holder of an Allowed Priority Non-Tax Claim against BST agrees to less favorable

treatment, on or as soon as practicable after the Effective Date, each holder thereof shall be paid in full in Cash (from the Net Cash Proceeds (BST)) or otherwise receive treatment consistent with the provisions of section 1129(a)(9) of

the Bankruptcy Code.

|

Unimpaired

|

No (Presumed to accept)

|

100%

|

8

|

Class

|

Claim or

Equity Interest

|

Treatment

|

Impaired or

Unimpaired

|

Entitled to

Vote on

the Plan

|

Approximate

Recovery

Under Plan7

|

|

3(a)

|

Other Secured Claims

against BSC

|

(i) Except to the extent that a holder of an Allowed Other Secured Claim against BSC agrees to different treatment, on

the later of the Effective Date and the date that is thirty (30) days after the date such Other Secured Claim against BSC becomes an Allowed Claim, or as soon thereafter as is reasonably practicable, each holder of an Allowed Other Secured

Claim against BSC will receive, on account of such Allowed Claim, at the sole option of the Debtors or the Plan Administrator, as applicable: (a) Cash (from the Net Cash Proceeds (BSC)) in an amount equal to the Allowed amount of such

Claim; (b) such other treatment sufficient to render such holder’s Allowed Other Secured Claim against BSC Unimpaired; or (c) return of the applicable collateral in satisfaction of the Allowed amount of such Other Secured Claim against BSC.

(ii) Except as otherwise specifically provided in the Plan, upon the payment in full in Cash of an Other Secured Claim

against BSC, any Lien securing an Other Secured Claim against BSC that is paid in full, in Cash, shall be deemed released, and the holder of such Other Secured Claim against BSC shall be authorized and directed to release any collateral or

other property of the Debtors (including any Cash collateral) held by such holder and to take such actions as may be requested by the Plan Administrator, to evidence the release of such Lien, including the execution, delivery and filing or

recording of such releases as may be requested by the Plan Administrator.

|

Unimpaired

|

No (Presumed to accept)

|

100%

|

|

3(b)

|

Other Secured Claims

against BGI

|

(i) Except to the extent that a holder of an Allowed Other Secured Claim against BGI agrees to different treatment, on

the later of the Effective Date and the date that is thirty (30) days after the date such Other Secured Claim against BGI becomes an Allowed Claim, or as soon thereafter as is reasonably practicable, each holder of an Allowed Other Secured

Claim against BGI will receive, on account of such Allowed Claim, at the sole option of the Debtors or the Plan Administrator, as applicable: (a) Cash (from the Net Cash Proceeds (BGI)) in an amount equal to the Allowed amount of such

Claim; (b) such other treatment sufficient to render such holder’s Allowed Other Secured Claim against BGI Unimpaired; or (c) return of the applicable collateral in satisfaction of the Allowed amount of such Other Secured Claim against BGI.

(ii) Except as otherwise specifically provided in the Plan, upon the payment in full in Cash of an Other Secured Claim

against BGI, any Lien securing an Other Secured Claim against BGI that is paid in full, in Cash, shall be deemed released, and the holder of such Other Secured Claim against BGI shall be authorized and directed to release any collateral or

other property of the Debtors (including any Cash collateral) held by such holder and to take such actions as may be requested by the Plan Administrator, to evidence the release of such Lien, including the execution, delivery and filing or

recording of such releases as may be requested by the Plan Administrator.

|

Unimpaired

|

No (Presumed to accept)

|

100%

|

9

|

Class

|

Claim or

Equity Interest

|

Treatment

|

Impaired or

Unimpaired

|

Entitled to

Vote on

the Plan

|

Approximate

Recovery

Under Plan7

|

|

3(c)

|

Other Secured Claims

against ABI

|

(i) Except to the extent that a holder of an Allowed Other Secured Claim against ABI agrees to different treatment, on

the later of the Effective Date and the date that is thirty (30) days after the date such Other Secured Claim against ABI becomes an Allowed Claim, or as soon thereafter as is reasonably practicable, each holder of an Allowed Other Secured

Claim against ABI will receive, on account of such Allowed Claim, at the sole option of the Debtors or the Plan Administrator, as applicable: (a) Cash (from the Net Cash Proceeds (ABI)) in an amount equal to the Allowed amount of such

Claim; (b) such other treatment sufficient to render such holder’s Allowed Other Secured Claim against ABI Unimpaired; or (c) return of the applicable collateral in satisfaction of the Allowed amount of such Other Secured Claim against ABI.

(ii) Except as otherwise specifically provided in the Plan, upon the payment in full in Cash of an Other Secured Claim

against ABI, any Lien securing an Other Secured Claim against ABI that is paid in full, in Cash, shall be deemed released, and the holder of such Other Secured Claim against ABI shall be authorized and directed to release any collateral or

other property of the Debtors (including any Cash collateral) held by such holder and to take such actions as may be requested by the Plan Administrator, to evidence the release of such Lien, including the execution, delivery and filing or

recording of such releases as may be requested by the Plan Administrator.

|

Unimpaired

|

No (Presumed to accept)

|

100%

|

|

3(d)

|

Other Secured Claims

against BSI

|

(i) Except to the extent that a holder of an Allowed Other Secured Claim against BSI agrees to different treatment, on

the later of the Effective Date and the date that is thirty (30) days after the date such Other Secured Claim against BSI becomes an Allowed Claim, or as soon thereafter as is reasonably practicable, each holder of an Allowed Other Secured

Claim against BSI will receive, on account of such Allowed Claim, at the sole option of the Debtors or the Plan Administrator, as applicable: (a) Cash (from the Net Cash Proceeds (BSI)) in an amount equal to the Allowed amount of such

Claim; (b) such other treatment sufficient to render such holder’s Allowed Other Secured Claim against BSI Unimpaired; or (c) return of the applicable collateral in satisfaction of the Allowed amount of such Other Secured Claim against BSI.

(ii) Except as otherwise specifically provided the Plan, upon the payment in full in Cash of an Other Secured Claim

against BSI, any Lien securing an Other Secured Claim against BSI that is paid in full, in Cash, shall be deemed released, and the holder of such Other Secured Claim against BSI shall be authorized and directed to release any collateral or

other property of the Debtors (including any Cash collateral) held by such holder and to take such actions as may be requested by the Plan Administrator, to evidence the release of such Lien, including the execution, delivery and filing or

recording of such releases as may be requested by the Plan Administrator.

|

Unimpaired

|

No (Presumed to accept)

|

100%

|

10

|

Class

|

Claim or

Equity Interest

|

Treatment

|

Impaired or

Unimpaired

|

Entitled to

Vote on

the Plan

|

Approximate

Recovery

Under Plan7

|

|

3(e)

|

Other Secured Claims

against BST

|

(i) Except to the extent that a holder of an Allowed Other Secured Claim against BST agrees to different treatment, on

the later of the Effective Date and the date that is thirty (30) days after the date such Other Secured Claim against BST becomes an Allowed Claim, or as soon thereafter as is reasonably practicable, each holder of an Allowed Other Secured

Claim against BST will receive, on account of such Allowed Claim, at the sole option of the Debtors or the Plan Administrator, as applicable: (a) Cash (from the Net Cash Proceeds (BST)) in an amount equal to the Allowed amount of such

Claim; (b) such other treatment sufficient to render such holder’s Allowed Other Secured Claim against BST Unimpaired; or (c) return of the applicable collateral in satisfaction of the Allowed amount of such Other Secured Claim against BST.

(ii) Except as otherwise specifically provided in the Plan, upon the payment in full in Cash of an Other Secured Claim

against BST, any Lien securing an Other Secured Claim against BST that is paid in full, in Cash, shall be deemed released, and the holder of such Other Secured Claim against BST shall be authorized and directed to release any collateral or

other property of the Debtors (including any Cash collateral) held by such holder and to take such actions as may be requested by the Plan Administrator, to evidence the release of such Lien, including the execution, delivery and filing or

recording of such releases as may be requested by the Plan Administrator.

|

Unimpaired

|

No (Presumed to accept)

|

100%

|

11

|

Class

|

Claim or

Equity Interest

|

Treatment

|

Impaired or

Unimpaired

|

Entitled to

Vote on

the Plan

|

Approximate

Recovery

Under Plan7

|

|

4(a)

|

General Unsecured

Claims against BSC

|

Except to the extent that a holder of an Allowed General Unsecured Claim against BSC agrees to less favorable

treatment of such Claim, in full and final satisfaction, compromise, and settlement of and in exchange for such Allowed General Unsecured Claim against BSC, each holder thereof shall receive its Pro Rata share of the Net Cash Proceeds (BSC)

after the Priority Tax Claims against BSC, Priority Non-Tax Claims against BSC and the Other Secured Claims against BSC are satisfied (or reserved for) in full in accordance with the Plan, until all Allowed General Unsecured Claims against

BSC are satisfied in full in Cash; provided, however, for purposes of determining the Pro Rata share under the Plan, the PBGC Subordination shall be enforced; provided, further, that: (A) if any portion of a General Unsecured Claim against BSC is an Insured Claim, such portion of such General Unsecured Claim shall be processed in accordance with section 7.9 of the Plan and the

holder of such Insured Claim shall not be paid from the Net Cash Proceeds (BSC), and (B) the portion of a General Unsecured Claim against BSC that is not an Insured Claim shall receive its Pro Rata share of the Net Cash Proceeds (BSC), as

provided herein, solely to the extent that such uninsured portion of such General Unsecured Claim against BSC is an Allowed General Unsecured Claim.

|

Impaired

|

Yes

|

6 - 8%8

|

|

4(b)

|

General Unsecured

Claims against BGI

|

Except to the extent that a holder of an Allowed General Unsecured Claim against BGI agrees to less favorable

treatment of such Claim, in full and final satisfaction, compromise, and settlement of and in exchange for such Allowed General Unsecured Claim against BGI, each holder thereof shall receive its Pro Rata share of the Net Cash Proceeds (BGI)

after the Priority Tax Claims against BGI, Priority Non-Tax Claims against BGI and the Other Secured Claims against BGI are satisfied (or reserved for) in full in accordance with the Plan, until all Allowed General Unsecured Claims against

BGI are satisfied in full in Cash; provided, however, for purposes of determining the Pro Rata share under the Plan, the PBGC Subordination shall be enforced; provided, further, that: (A) if any portion of a General Unsecured Claim against BGI is an Insured Claim, such portion of such General Unsecured Claim shall be processed in accordance with section 7.9 of the Plan and the

holder of such Insured Claim shall not be paid from the Net Cash Proceeds (BGI), and (B) the portion of a General Unsecured Claim against BGI that is not an Insured Claim shall receive its Pro Rata share of the Net Cash Proceeds (BGI), as

provided herein, solely to the extent that such uninsured portion of such General Unsecured Claim against BGI is an Allowed General Unsecured Claim.

|

Impaired

|

Yes

|

1 - 2%9

|

|

8

|

The estimated recovery for general unsecured claims depends on the amount of allowed priority claims and allowed general

unsecured claims, which, based on the results of the claims reconciliation process, may ultimately be materially different from the estimates in the Recovery Analysis. See footnote three of the Recovery Analysis, annexed hereto as Exhibit C. The Debtors believe that certain

priority claims and general unsecured claims should be reclassified and/or disallowed as part of the claims reconciliation process. However, the Debtors cannot assure that such claims will ultimately be reclassified and/or disallowed.

As such, the recovery for Class 4(a) could be as low as 6% if certain filed and unreconciled priority claims and general unsecured claims asserted against the Debtors are ultimately allowed as part of the claims reconciliation process.

|

Additionally, this range is not inclusive of unliquidated tort claims. Forty-four (44) claims related to unliquidated tort claims were filed against the Debtors, of which thirty-nine (39) claims are related to asbestos-related litigations and may be reduced by applicable insurance coverage, as discussed in more detail in section IV(O) infra. The Debtors do not currently have an estimate for such tort claims, and the recovery amount for general unsecured creditors may be lower depending on the ultimate value of the unliquidated tort claims. If the unliquidated tort claims are ultimately allowed and not paid by available insurance, recovery for general unsecured creditors could be even lower.

|

9

|

The estimated recovery for general unsecured claims depends on the amount of allowed priority claims and allowed general

unsecured claims, which, based on the results of the claims reconciliation process, may ultimately be materially different from the estimates in the Recovery Analysis. See footnote three of the Recovery Analysis, annexed hereto as Exhibit C. The Debtors believe that certain

priority claims and general unsecured claims should be reclassified and/or disallowed as part of the claims reconciliation process. However, the Debtors cannot assure that such claims will ultimately be reclassified and/or disallowed.

As such, the recovery for Class 4(b) could be as low as 1% if certain filed and unreconciled priority claims and general unsecured claims asserted against the Debtors are ultimately allowed as part of the claims reconciliation process.

|

12

|

Class

|

Claim or

Equity Interest

|

Treatment

|

Impaired or

Unimpaired

|

Entitled to

Vote on

the Plan

|

Approximate

Recovery

Under Plan7

|

|

4(c)

|

General Unsecured

Claims against ABI

|

Except to the extent that a holder of an Allowed General Unsecured Claim against ABI agrees to less favorable

treatment of such Claim, in full and final satisfaction, compromise, and settlement of and in exchange for such Allowed General Unsecured Claim against ABI, each holder thereof shall receive its Pro Rata share of the Net Cash Proceeds (ABI)

after the Priority Tax Claims against ABI, Priority Non-Tax Claims against ABI and the Other Secured Claims against ABI are satisfied (or reserved for) in full in accordance with the Plan, until all Allowed General Unsecured Claims against

ABI are satisfied in full in Cash; provided, however, for purposes of determining the Pro Rata share under the Plan, the PBGC Subordination shall be enforced; provided, further, that: (A) if any portion of a General Unsecured Claim against ABI is an Insured Claim, such portion of such General Unsecured Claim shall be processed in accordance with section 7.9 of the Plan and the

holder of such Insured Claim shall not be paid from the Net Cash Proceeds (ABI), and (B) the portion of a General Unsecured Claim against ABI that is not an Insured Claim shall receive its Pro Rata share of the Net Cash Proceeds (ABI), as

provided herein, solely to the extent that such uninsured portion of such General Unsecured Claim against ABI is an Allowed General Unsecured Claim.

|

Impaired

|

Yes

|

1 - 2%10

|

|

4(d)

|

General Unsecured

Claims against BSI

|

Except to the extent that a holder of an Allowed General Unsecured Claim against BSI agrees to less favorable

treatment of such Claim, in full and final satisfaction, compromise, and settlement of and in exchange for such Allowed General Unsecured Claim against BSI, each holder thereof shall receive its Pro Rata share of the Net Cash Proceeds (BSI)

after the Priority Tax Claims against BSI, Priority Non-Tax Claims against BSI and the Other Secured Claims against BSI are satisfied (or reserved for) in full in accordance with the Plan, until all Allowed General Unsecured Claims against

BSI are satisfied in full in Cash; provided, however, for purposes of determining the Pro Rata share under the Plan, the PBGC Subordination shall be enforced; provided, further, that: (A) if any portion of a General Unsecured Claim against BSI is an Insured Claim, such portion of such General Unsecured Claim shall be processed in accordance with section 7.9 of the Plan and the

holder of such Insured Claim shall not be paid from the Net Cash Proceeds (BSI), and (B) the portion of a General Unsecured Claim against BSI that is not an Insured Claim shall receive its Pro Rata share of the Net Cash Proceeds (BSI), as

provided herein, solely to the extent that such uninsured portion of such General Unsecured Claim against BSI is an Allowed General Unsecured Claim.

|

Impaired

|

Yes

|

N/A11

|

|

10

|

The estimated recovery for general unsecured claims depends on the amount of allowed priority claims and allowed general

unsecured claims, which, based on the results of the claims reconciliation process, may ultimately be materially different from the estimates in the Recovery Analysis. See footnote three of the Recovery Analysis, annexed hereto as Exhibit C. The Debtors believe that certain

priority claims and general unsecured claims should be reclassified and/or disallowed as part of the claims reconciliation process. However, the Debtors cannot assure that such claims will ultimately be reclassified and/or disallowed.

As such, the recovery for Class 4(c) could be as low as 1% if certain filed and unreconciled priority claims and general unsecured claims asserted against the Debtors are ultimately allowed as part of the claims reconciliation process.

|

|

11

|

The Debtors believe that the PBGC is the only creditor in this class.

|

13

|

Class

|

Claim or

Equity Interest

|

Treatment

|

Impaired or

Unimpaired

|

Entitled to

Vote on

the Plan

|

Approximate

Recovery

Under Plan7

|

|

4(e)

|

General Unsecured

Claims against BST

|

Except to the extent that a holder of an Allowed General Unsecured Claim against BST agrees to less favorable

treatment of such Claim, in full and final satisfaction, compromise, and settlement of and in exchange for such Allowed General Unsecured Claim against BST, each holder thereof shall receive its Pro Rata share of the Net Cash Proceeds (BST)

after the Priority Tax Claims against BST, Priority Non-Tax Claims against BST and the Other Secured Claims against BST are satisfied (or reserved for) in full in accordance with the Plan, until all Allowed General Unsecured Claims against

BST are satisfied in full in Cash; provided, however, for purposes of determining the Pro Rata share under the Plan, the PBGC Subordination shall be enforced; provided, further, . that: (A) if any portion of a General Unsecured Claim against BST is an Insured Claim, such portion of such

General Unsecured Claim shall be processed in accordance with section 7.9 of the Plan and the holder of such Insured Claim shall not be paid from the Net Cash Proceeds (BST), and (B) the portion of a General Unsecured Claim against BST that

is not an Insured Claim shall receive its Pro Rata share of the Net Cash Proceeds (BST), as provided herein, solely to the extent that such uninsured portion of such General Unsecured Claim against BST is an Allowed General Unsecured Claim.

|

Impaired

|

Yes

|

0.1%12

|

|

5(a)

|

Subordinated Securities

Claims against BSC

|

On the Effective Date, all Subordinated Securities Claims against BSC shall be deemed cancelled without further action

by or order of the Bankruptcy Court, and shall be of no further force and effect, whether surrendered for cancellation or otherwise. Holders of Subordinated Securities Claims against BSC shall not receive or retain any property under the

Plan on account of such Subordinated Securities Claims against BSC; provided, however, that in the event that all other Allowed Claims against BSC have been satisfied in full in accordance with the Bankruptcy Code and the Plan, each holder

of a Subordinated Securities Claim against BSC may receive its Pro Rata Share of any remaining assets in BSC.

|

Impaired

|

No (Deemed to reject)

|

0%

|

|

12

|

The Debtors believe that the PBGC is the only creditor in this class.

|

14

|

Class

|

Claim or

Equity Interest

|

Treatment

|

Impaired or

Unimpaired

|

Entitled to

Vote on

the Plan

|

Approximate

Recovery

Under Plan7

|

|

5(b)

|

Subordinated

Securities Claims

against BGI

|

On the Effective Date, all Subordinated Securities Claims against BGI shall be deemed cancelled without further action

by or order of the Bankruptcy Court, and shall be of no further force and effect, whether surrendered for cancellation or otherwise. Holders of Subordinated Securities Claims against BGI shall not receive or retain any property under the

Plan on account of such Subordinated Securities Claims against BGI; provided, however, that in the event that all other Allowed Claims against BGI have been satisfied in full in accordance with the Bankruptcy Code and the Plan, each holder

of a Subordinated Securities Claim against BGI may receive its Pro Rata Share of any remaining assets in BGI.

|

Impaired

|

No (Deemed to reject)

|

0%

|

|

5(c)

|

Subordinated

Securities Claims

against ABI

|

On the Effective Date, all Subordinated Securities Claims against ABI shall be deemed cancelled without further action

by or order of the Bankruptcy Court, and shall be of no further force and effect, whether surrendered for cancellation or otherwise. Holders of Subordinated Securities Claims against ABI shall not receive or retain any property under the

Plan on account of such Subordinated Securities Claims against ABI; provided, however, that in the event that all other Allowed Claims against ABI have been satisfied in full in accordance with the Bankruptcy Code and the Plan, each holder

of a Subordinated Securities Claim against ABI may receive its Pro Rata Share of any remaining assets in ABI.

|

Impaired

|

No (Deemed to reject)

|

0%

|

|

5(d)

|

Subordinated

Securities Claims

against BSI

|

On the Effective Date, all Subordinated Securities Claims against BSI shall be deemed cancelled without further action

by or order of the Bankruptcy Court, and shall be of no further force and effect, whether surrendered for cancellation or otherwise. Holders of Subordinated Securities Claims against BSI shall not receive or retain any property under the

Plan on account of such Subordinated Securities Claims against BSI; provided, however, that in the event that all other Allowed Claims against BSI have been satisfied in full in accordance with the Bankruptcy Code and the Plan, each holder

of a Subordinated Securities Claim against BSI may receive its Pro Rata Share of any remaining assets in BSI.

|

Impaired

|

No (Deemed to reject)

|

0%

|

|

5(e)

|

Subordinated

Securities Claims

against BST

|

On the Effective Date, all Subordinated Securities Claims against BST shall be deemed cancelled without further action

by or order of the Bankruptcy Court, and shall be of no further force and effect, whether surrendered for cancellation or otherwise. Holders of Subordinated Securities Claims against BST shall not receive or retain any property under the

Plan on account of such Subordinated Securities Claims against BST; provided, however, that in the event that all other Allowed Claims against BST have been satisfied in full in accordance with the Bankruptcy Code and the Plan, each holder

of a Subordinated Securities Claim against BST may receive its Pro Rata Share of any remaining assets in BST.

|

Impaired

|

No (Deemed to reject)

|

0%

|

15

|

Class

|

Claim or

Equity Interest

|

Treatment

|

Impaired or

Unimpaired

|

Entitled to

Vote on

the Plan

|

Approximate

Recovery

Under Plan7

|

|

6(a)

|

Intercompany

Interests in BGI

|

All Intercompany Interests in BGI shall be cancelled if

and when BGI is dissolved in accordance with Section 5.4(f) of the Plan. Each holder of an Intercompany Interest in BGI shall neither receive nor retain any property of the estate or direct interest in property of the estate of

BGI on account of such Intercompany Interests thereafter; provided, however, that in the event that all Allowed Claims against BGI have been satisfied in full in accordance with the Bankruptcy Code and the Plan, each holder of an

Intercompany Interest in BGI may receive its Pro Rata Share of any remaining assets in BGI.

|

Impaired

|

No (Deemed to reject)

|

0%

|

|

6(b)

|

Intercompany

Interests in ABI

|

All Intercompany Interests in ABI shall be cancelled if and when ABI is dissolved in accordance with Section 5.4(f) of the Plan. Each holder of an Intercompany Interest in ABI shall neither receive nor retain any property of the estate or direct interest in property of the estate of ABI

on account of such Intercompany Interests thereafter; provided, however, that in the event that all Allowed Claims against BGI have been satisfied in full in accordance with the Bankruptcy Code and the Plan, each holder of an

Intercompany Interest in ABI may receive its Pro Rata Share of any remaining assets in ABI.

|

Impaired

|

No (Deemed to reject)

|

0%

|

|

6(c)

|

Intercompany

Interests in BSI

|

All Intercompany Interests in BSI shall be cancelled if

and when BSI is dissolved in accordance with Section 5.4(f) of the Plan. Each holder of an Intercompany Interest in BSI shall neither receive nor retain any property of the estate or direct interest in property of the estate of

BSI on account of such Intercompany Interests thereafter; provided, however, that in the event that all Allowed Claims against BSI have been satisfied in full in accordance with the Bankruptcy Code and the Plan, each holder of an

Intercompany Interest in BSI may receive its Pro Rata Share of any remaining assets in BSI.

|

Impaired

|

No (Deemed to reject)

|

0%

|

|

6(d)

|

Intercompany

Interests in BST

|

All Intercompany Interests in BST shall be cancelled if and when BST is dissolved in accordance with Section 5.4(f) of the Plan. Each holder of an Intercompany Interest in BST shall neither receive nor retain any property of the estate or direct interest in property of the estate

of BST on account of such Intercompany Interests thereafter; provided, however, that in the event that all Allowed Claims against BST have been satisfied in full in accordance with the Bankruptcy Code and the Plan, each holder of an

Intercompany Interest in BST may receive its Pro Rata Share of any remaining assets in BST.

|

Impaired

|

No (Deemed to reject)

|

0%

|

16

|

Class

|

Claim or

Equity Interest

|

Treatment

|

Impaired or

Unimpaired

|

Entitled to

Vote on

the Plan

|

Approximate

Recovery

Under Plan7

|

|

7(a)

|

Equity Interests in

BSC

|

On the Effective Date, (i) all Equity Interests in BSC shall be cancelled and one share of BSC common stock (the

“Single Share”) shall be issued to the Plan Administrator to hold in trust as custodian for the benefit of the former holders of Equity Interests in BSC consistent with their former relative priority and economic entitlements and the Single

Share shall be recorded on the books and records maintained by the Plan Administrator without any necessity for any other or further actions to be taken by or on behalf of BSC; (ii) each former holder of Equity Interests in BSC (through

their interest in the Single Share, as applicable) shall neither receive nor retain any property of the Estate or direct interest in property of the Estate on account of such Equity Interests in BSC; provided, that in the event that all

Allowed Claims have been satisfied in full in accordance with the Bankruptcy Code and the Plan, each former holder of an Equity Interest in BSC may receive its share of any remaining assets of BSC consistent with such holder’s rights of

payment and former relative priority and economic entitlements existing immediately prior to the Petition Date; (iii) unless otherwise determined by the Plan Administrator, on the date that BSC’s Chapter 11 Case is closed in accordance with

Section 5.16 of the Plan, the Single Share issued on the Effective Date shall be deemed cancelled and of no further force and effect without any necessity for any other or further actions to be taken by or on behalf of BSC, provided that

such cancellation does not adversely impact the Debtors’ Estates; and (iv) the continuing rights of the former holders of Equity Interests in BSC (including through their interest in Single Share or otherwise) shall be nontransferable

except (A) by operation of law or (B) for administrative transfers where the ultimate beneficiary has not changed, subject to the Plan Administrator’s consent.

|

Impaired

|

No (Deemed to reject)

|

0%

|

II.

|

|

A.

|

The Debtors’ Business

|

| a) |

History and Formation

|

Briggs & Stratton began in 1908 as an informal partnership between inventor Stephen F. Briggs and investor Harold M. Stratton that eventually developed into Briggs

& Stratton as it is known today. The partnership first ventured into the automobile manufacturing business. From there, Briggs & Stratton progressed to manufacturing automobile parts. In 1910, Briggs & Stratton incorporated, and due

to the growing demand for automobiles, starter switches became the early mainstay of the Company’s business. Between 1920 and 1960, Briggs & Stratton provided power for innumerable applications, including agricultural and military

applications. In 1953, Briggs & Stratton revolutionized the first lightweight aluminum engine.

17

As a result of the rapid growth of suburbs, the lawn and garden market grew, and mowers, powered by Briggs & Stratton engines, became an integral part of suburban

life. A period of product innovations followed, including Easy-Spin® starting, lo-tone mufflers, and an automatic choke. Upon the entry of moderately priced premium Japanese engines to the market, and faced with demand by mass retailers for lower

prices, the Company was faced with a critical challenge. Briggs & Stratton responded to this challenge by reorganizing into product-focused divisions, expanding product lines to include the industrial/commercial and Vanguard® engine lines, and

expanding its presence in lucrative foreign markets.

Briggs & Stratton later entered the end-products business. In 2001, Briggs & Stratton purchased Generac Portable Products Systems, which produced pressure

washers, generators, pumps, and other home products. In 2004, the Company acquired Simplicity Manufacturing, a leading designer and marketer of a broad range of premium outdoor power equipment used in both consumer and commercial lawn and garden

applications. This acquisition included the Snapper, Snapper-Pro, Giant-Vac, and Ferris brands.

Briggs & Stratton expanded into the global markets beginning with Asian markets in 2005 when it opened a manufacturing facility in Chongqing, China. In 2006,

Briggs & Stratton started production in its first European plant in Ostrava, Czech Republic. Globally, the Company’s engines can be found on diverse applications such as milking machines in Mexico, sugar cane crushers in Puerto Rico, fishing

boats in Vietnam, rice harvesters in the Philippines, and cocoa pod grinders in Indonesia, to name a few.

| b) |

Prepetition Business Operations

|

The Company conducted its operations in two reportable segments: engines (the “Engines

Segment”) and products (the “Products Segment”). The Engines Segment sold engines and battery packs worldwide, primarily to original equipment

manufacturers (“OEMs”) of lawn and garden equipment and other gasoline engine powered equipment. The Products Segment designed, manufactured, and marketed a