Attached files

| file | filename |

|---|---|

| EX-99.2 - ADDITIONAL FINANCIAL INFORMATION FOR Q3 2020 - KINGSTONE COMPANIES, INC. | kins_ex992.htm |

| 8-K - CURRENT REPORT - KINGSTONE COMPANIES, INC. | kins-20201231.htm |

Exhibit 99.1

FOR IMMEDIATE RELEASE

Kingstone

Announces 2020 Third Quarter Financial Results

Company to Host Conference Call on November 9, 2020 at 8:30 a.m.

ET

Kingston, NY —

November 6, 2020 – Kingstone Companies, Inc.

(Nasdaq: KINS) (the

“Company” or “Kingstone”), a Northeast

regional property and casualty insurance holding company, today

announced its financial results for the quarter ended September 30,

2020.

Financial and Operational Highlights

2020 Third Quarter

(All results are compared to prior year period unless otherwise

noted)

●

Catastrophes, primarily Tropical Storm Isaias,

added 31.5% to net loss ratio for the quarter; Net combined ratio

excluding the impact of catastrophes1

was 80.4%

●

Direct written premiums1

from personal lines grew by

6.4%; Direct written

premiums1

including commercial liability lines

in run off decreased by 0.6%

●

Net loss ratio excluding commercial lines in run

off and catastrophe losses1

of 42.1% compared to

53.5%

●

Net operating income (loss) exclusive of

catastrophe losses1

per diluted share of $0.54 compared to

$(.19)

●

Book value per share of $8.37 down $0.03 from Q2

after $0.64 per share impact from catastrophes 1

Quarterly Dividend of $0.04 per share

The Company announced that its Board of Directors declared a

quarterly dividend of $0.04 per share payable on December 15, 2020

to stockholders of record at the close of business on November 30,

2020.

____________________

1 These measures are not based on accounting principles

generally accepted in the United States (“GAAP”) and

are defined and reconciled to the most directly comparable GAAP

measures in Form 8-K Exhibit 99.2 “Additional Financial

Information for Q3 2020” (also available at

www.kingstonecompanies.com).

Management Commentary

Barry Goldstein, Kingstone’s Chief Executive Officer,

elaborated on the Company’s results:

“Our third quarter’s results demonstrate the progress

we’ve made and the resilience of our company. As we announced

on October 7th,

losses and loss adjustment expenses incurred attributable to

Tropical Storm Isaias were sizeable and the most since Superstorm

Sandy in 2012. It led to a full catastrophe retention ($8.125

million pre-tax) being absorbed by Kingstone in the third quarter.

Isaias drove our quarterly combined ratio to a very poor 111.9%.

Peel back the onion just one layer and you’ll find that, by

itself, Isaias’ loss and loss adjustment expense added 29.5

points to the combined ratio.

Apart from catastrophes, we posted an excellent combined ratio of

80.4%. Increased rates are being rolled on and earned in. Our exit

from commercial liability lines is complete; our final policy ran

off at the end of September. No longer will these highly volatile

lines adversely impact our company. Our focus on profitability is

yielding the anticipated results.

Meryl Golden, Kingstone’s Chief Operating Officer,

continued:

“Relative to Isaias, I am happy to report that almost 90% of

these claims are now closed and feel really good about the efforts

of our claims organization in achieving this outcome.

“We are pleased with our x-catastrophe results this quarter

and the improvement we are seeing over the prior year. We are also

in a good place from a reserving perspective. The reserve

strengthening we took last year was appropriate, with our reserves

being solidly in the middle of our outside actuary’s mid-year

review, which was recently completed. The runoff of commercial

liability claims continues to be favorable, and we recorded our

fourth straight quarter of stable prior year loss

development.

I am also happy to share that Kingstone 2.0, our effort to

modernize the Company, continues to progress well. In Q3 we

implemented our new claims system and filed our new Homeowners

program in NY. In Q4, we will file our new Condo/Tenant and

Dwelling Fire programs in NY, introduce a new interface for our

Select Producers and start the conversion to our new policy

management system. We have been able to make these investments

without an increase in expenses, after adjusting for the Quota

Share. We are excited to see the impact on Company performance of

these initiatives.”

Financial Highlights Table

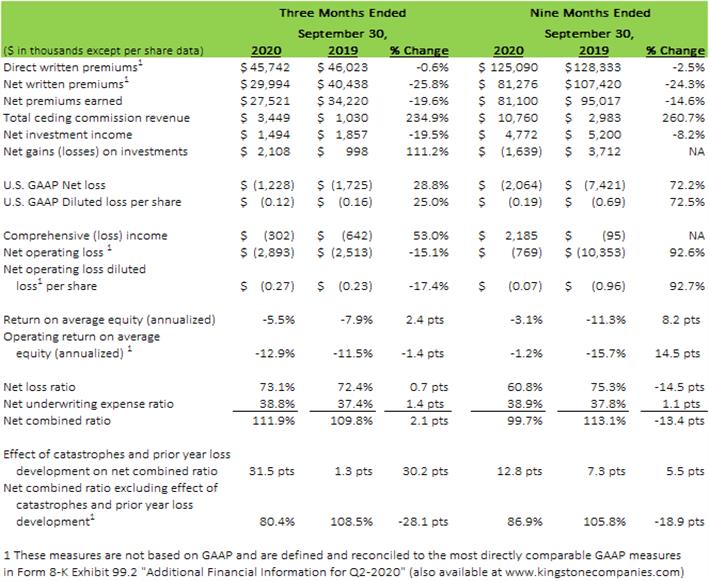

2020 Third Quarter Financial Review

Net Loss:

There was a net loss of $1.2 million during the three-month period

ended September 30, 2020, compared to net loss of $1.7 million in

the prior year period. The decrease in net loss in the latest

three-month period can be attributed to the increase in ceding

commissions due to the inception of a 25% personal lines quota

share on December 15, 2019 and the dramatic positive swing in

financial markets that have been reversing the unrealized losses

from the first quarter resulting from the impact of the Covid-19

pandemic, offset by the decrease in net premiums earned due to the

inception of 25% personal lines quota share. The net loss ratio for

the latest three-month period increased by 0.7 points compared to

the prior three month period, as described in the ‘Net Loss

Ratio and Underlying Net Loss Ratio Excluding Commercial

Lines’ section below.

Earnings (Loss) per share (“EPS”):

Kingstone reported a loss of $0.12 per diluted share for the three

months ended September 30, 2020, compared to loss of $0.16 per

diluted share for the three months ended September 30, 2019. EPS

for the three-month periods ended September 30, 2020 and 2019 was

based on 10.67 million and 10.78 million weighted average diluted

shares outstanding, respectively.

Direct

Written Premiums1,

Net Written Premiums1

and Net

Premiums Earned (See Definitions and Non-GAAP Measures

below):

Direct written premiums1

for the third quarter of 2020 were

$45.7 million, a decrease of $0.3 million, or 0.6%, from $46.0

million in the prior year period. The increase in premiums from

personal lines was offset by a $2.0 million decrease in premiums

from our commercial lines business as result of our decision in

July 2019 to no longer underwrite this line of business, and a

decrease in premiums from livery physical damage due to a decline

in business from the Covid-19 pandemic. Direct written premiums

from our personal lines business for the third quarter of 2020 were

$43.6 million, an increase of $2.6 million, or 6.4%, from $41.0

million in the prior year period.

We refer to our New York business as “Core”

1

and the business in other states as

“Expansion” 1.

Expansion direct written premiums 1

for the third quarter of 2020 were

$9.2 million, an increase of $1.8 million from the $7.4 million

written in the prior year period.

Net written premiums1

decreased 25.8% to $30.0 million

during the three-month period ended September 30, 2020 from $40.4

million in the prior year period. The decrease in the third quarter

was attributable to the

inception of a 25% personal lines quota share on December 15, 2019

and the decrease in commercial lines premiums which are not subject

to a quota share treaty.

Net premiums earned for the quarter ended September 30, 2020

decreased 19.6% to $27.5 million, compared to $34.2 million for the

quarter ended September 30, 2019. The decrease was attributable to

the inception of a 25% personal lines quota share on December 15,

2019 and the decrease in commercial lines premiums which are not

subject to a quota share treaty. The 10% personal lines quota share

was in run-off for the quarter ended September 30,

2019.

Net Loss Ratio and Underlying Net Loss Ratio Excluding Commercial

Lines1:

For the quarter ended September 30, 2020 (“Three Months

2020”), the net loss ratio increased 0.7 points, from 72.4%

for the quarter ended September 30, 2019 (“Three Months

2019”) to 73.1% in Three Months 2020. The net loss ratio

increased due to the impact of catastrophe events, primarily

related to Tropical Storm Isaias on August 4, 2020. Partially

offsetting the increased catastrophe losses, there was a large

reduction in the impact of prior year loss development compared the

same period in the prior year.

The impact of catastrophe losses was significant in Three Months

2020 when compared to Three Months 2019. In the Three Months 2020,

Tropical Storm Isaias resulted in over 1,700 reported claims and

direct losses exceeded our catastrophe reinsurance retention of $10

million. After quota share reinsurance, the net impact of Isaias is

$8.125 million, or a 29.5 point impact on the quarterly loss ratio.

There were several smaller catastrophe events during the quarter,

and in total the impact of catastrophe events on the loss ratio was

31.5 points for the quarter. This compares to a 1.3 point impact

from catastrophe events in Three Months 2019, or an increase in the

impact from catastrophe events of 30.2 points compared to the prior

period.

Prior year development was slightly favorable in Three Months 2020,

with a 0.4 point favorable impact to the overall loss ratio. This

was the fourth consecutive quarter of stable prior year loss

development. The favorable loss development for Three Months 2020

compares to 14.7 points of unfavorable impact in Three Months 2019.

Prior year loss development in Three Months 2019 was driven by the

completion of reserve adjustments for commercial lines business,

which is now in runoff. As of the end of Three Months 2020, there

are were 189 open commercial lines claims, down from 205 claims

that were open at June 30, 2020. The impact of prior year

development was 15.1 points more favorable in Three Months 2020

compared to the prior year period.

The underlying loss ratio (loss ratio excluding the impact of

catastrophes and prior year development) 1

was 42.0% for Three Months 2020, a

decrease of 14.4 points from the 56.4% underlying loss ratio

recorded for Three Months 2019. The improvement was primarily

due to reduced claim severity in personal lines, driven by a much

lower impact from large fire claims in Three Months 2020 compared

to the prior period. Claim frequency in the livery physical damage

line also continued to show significant improvement over the prior

year period. The impact of commercial lines on the overall loss

ratio continues to decline due to a smaller open claims inventory

and a smaller proportion of net earned premium attributable to

commercial lines. Excluding commercial lines, the underlying loss

ratio improved 8.9 points, from 51.4% for Three Months 2019 to

42.5% for Three Months 2020.

Net Other Underwriting Expense Ratio:

For the quarter ended September 30, 2020, the net underwriting

expense ratio was 38.8% as compared to 37.4% in the prior year

period, an increase of 1.4 percentage points. The 1.4 percentage

point increase in the net underwriting expense ratio is

attributable to the effect that the 25% personal lines quota share

treaty and the elimination of the commercial lines business had on

decreasing net premiums earned.

____________________

1 These measures are not based on GAAP and are defined and

reconciled to the most directly comparable GAAP measures in Form

8-K Exhibit 99.2 “Additional Financial Information for Q3

2020” (also available at www.kingstonecompanies.com).

Balance Sheet / Investment Portfolio

Kingstone’s cash and investment holdings were $220.7 million

at September 30, 2020 compared to $221.6 million at September 30,

2019. The Company’s investment holdings are comprised

primarily of investment grade corporate, mortgage-backed and

municipal securities, with fixed income investments representing

approximately 83.5% of total investments at September 30, 2020 and

86.8% at September 30, 2019. The Company’s effective duration

on its fixed-income portfolio is 4.7 years.

Net investment income decreased 19.5% to $1.49 million for the

third quarter of 2020 from $1.86 million in the prior year

period.

Accumulated Other Comprehensive Income (AOCI)

As of September 30, 2020, AOCI was $9.02 million compared to $4.44

million at September 30, 2019.

Book Value

The Company’s book value per share at September 30, 2020 was

$8.37, an increase of 4.1% compared to $8.04 at September 30,

2019.

FOR ADDITIONAL INFORMATION PLEASE VISIT OUR WEBSITE AT

WWW.KINGSTONECOMPANIES.COM.

Conference Call Details

Management will discuss the Company’s operations and

financial results in a conference call on Monday, November 9, 2020,

at 8:30 a.m. ET.

The dial-in numbers are:

(877) 407-3105 (U.S.)

(201) 493-6794 (International)

Accompanying Webcast

The

call will be simultaneously webcast over the Internet via the

Kingstone website or by clicking on the conference call link:

Third

Quarter 2020 Earnings Conference Call

The

webcast will be archived and accessible for approximately 30

days.

Definitions and Non-GAAP Measures

Direct written premiums represent the total premiums charged on policies

issued by the Company during the respective fiscal period.

Net

premiums written are direct

written premiums less premiums ceded to reinsurers. Net premiums

earned, the GAAP measure most comparable to direct written premiums

and net premiums written, are net premiums written that are

pro-rata earned during the fiscal period presented. All of the

Company’s policies are written for a twelve-month period.

Management uses direct written premiums and net premiums written,

along with other measures, to gauge the Company’s performance

and evaluate results.

Core direct written premiums - represents the total premiums charged on

policies issued by the Company during the respective fiscal period

from its business located in New York.

Expansion direct written premiums - represents the total premiums charged on

policies issued by the Company during the respective fiscal period

from its business located in other states (i.e., outside New

York).

Net operating income (loss) - is net income (loss)

exclusive of realized investment gains (losses), net of tax. Net

income (loss) is the GAAP measure most closely comparable to net

operating income (loss).

Management

uses net operating income (loss) along with other measures to gauge

the Company’s performance and evaluate results, which can be

skewed when including realized investment gains (losses), and may

vary significantly between periods. Net operating income (loss) is

provided as supplemental information, not as a substitute for net

income (loss) and does not reflect the Company’s overall

profitability.

Operating return on average common equity - is net operating

income (loss) divided by average common equity. Return on average

common equity is the GAAP measure most closely comparable to

operating return on average common equity.

Management

uses net operating income (loss) and operating return on average

common equity, along with other measures, to gauge the

Company’s performance and evaluate results, which can be

skewed when including realized investment gains (losses), which may

vary significantly between periods. Net operating income (loss) and

operating return on average common equity are provided as

supplemental information, are not a substitute for net income

(loss) or return on average common equity and do not reflect the

Company’s overall profitability or return on average common

equity.

Underlying net loss ratio - is a non-GAAP ratio, which is computed

as the difference between GAAP net loss ratio and the effect of

catastrophes and prior year loss development on the net loss

ratio.

Underlying net loss ratio excluding Commercial Lines

- is a non-GAAP ratio, which

is computed as the difference between GAAP net loss ratio and the

loss ratio that relates to commercial lines, catastrophes, and

prior year loss development.

Net loss ratio excluding commercial lines - is a non-GAAP ratio, which is computed

as the difference between GAAP net loss ratio and the loss ratio

that relates to commercial lines.

Net loss ratio excluding commercial lines in run-off and

catastrophes - is a

non-GAAP ratio, which is computed as the difference between GAAP

net loss ratio and the loss ratio that relates to commercial lines

in run-off and catastrophes.

Net combined ratio excluding effect of catastrophes and prior year

loss development - is a non-GAAP ratio, which is computed as

the difference between GAAP net combined ratio and the effect of

catastrophes and prior year loss development on the net combined

ratio.

Net combined ratio excluding effect of catastrophes - is a

non-GAAP ratio, which is computed as the difference between GAAP

net combined ratio and the effect of catastrophes on the net

combined ratio.

We

believe that these ratios are useful to investors and they are used

by management to reveal the trends in our business that may be

obscured by catastrophe losses and prior year loss development, as

well as the loss ratio that relates to commercial lines which is in

run off. Catastrophe losses cause our loss ratios to vary

significantly between periods as a result of their incidence of

occurrence and magnitude, and can have a significant impact on the

net loss ratio and net combined ratio. Prior year loss development

can cause our loss ratio to vary significantly between periods and

separating this information allows us to better compare the results

for the current accident period over time. Due to our decision in

July 2019 to no longer underwrite commercial lines, excluding the

loss ratio related to such line of business allows us to compare

our loss ratio with regard to our ongoing lines of business. We

believe these measures are useful for investors to evaluate these

components separately and in the aggregate when reviewing our

underwriting performance. We also provide them to facilitate a

comparison to our outlook on the underlying net loss ratio

excluding commercial lines and net combined ratio excluding the

effect of catastrophes and prior year loss development. The most

directly comparable GAAP measures are the net loss ratio and net

combined ratio. The underlying net loss ratio excluding commercial

lines, net loss ratio excluding commercial lines and net combined

ratio excluding the effect of catastrophes and prior year loss

development should not be considered a substitute for the net loss

ratio and net combined ratio and do not reflect the Company’s

net loss ratio and net combined ratio.

Book value per share exclusive of catastrophes – is a

non-GAAP ratio which is computed as the difference between GAAP

book value per share and the effect of catastrophes on book value

per share.

___________________________________________________________________________________________________

About Kingstone Companies, Inc.

Kingstone

is a northeast regional property and casualty insurance holding

company whose principal operating subsidiary is Kingstone Insurance

Company (“KICO”). KICO is a New York domiciled carrier

writing business through retail and wholesale agents and brokers.

KICO offers primarily personal lines insurance products in New

York, New Jersey, Rhode Island, Massachusetts, and Connecticut.

Kingstone is also licensed in Pennsylvania, New Hampshire and

Maine.

Forward-Looking Statements

Statements

in this press release may contain “forward-looking

statements” within the meaning of the Private Securities

Litigation Reform Act of 1995. All statements, other than

statements of historical facts, may be forward-looking statements.

These statements are based on management’s current

expectations and are subject to uncertainty and changes in

circumstances. These statements involve risks and uncertainties

that could cause actual results to differ materially from those

included in forward-looking statements due to a variety of factors.

For more details on factors that could affect expectations, see

Part I, Item 1A of our Annual Report on Form 10-K for the year

ended December 31, 2019 under “Factors That May Affect Future

Results and Financial Condition” and Part II, Item 1A of our

Quarterly Report on Form 10-Q for the period ended September 30,

2020, to be filed with the Securities and Exchange Commission.

Kingstone undertakes no obligation to publicly update or revise any

forward-looking statements, whether as a result of new information,

future events or otherwise, except as required by law.

CONTACT:

Kingstone Companies, Inc.

Amanda

M. Goldstein

Investor

Relations Director

(516)

960-1319