Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - HUMANIGEN, INC | ex32_2.htm |

| EX-32.1 - EXHIBIT 32.1 - HUMANIGEN, INC | ex32_1.htm |

| EX-31.2 - EXHIBIT 31.2 - HUMANIGEN, INC | ex31_2.htm |

| EX-31.1 - EXHIBIT 31.1 - HUMANIGEN, INC | ex31_1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

xQUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended June 30, 2020

OR

oTRANSITION REPORT UNDER SECTION 13 OF 15(d) OF THE EXCHANGE ACT OF 1934

From the transition period from to .

Commission File Number 001-35798

Humanigen, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 77-0557236 | |

| (State or other jurisdiction of | (IRS Employer | |

| incorporation) | Identification No.) |

533 Airport Boulevard, Suite 400 Burlingame, CA 94010

(Address of principal executive offices)

(Zip Code)

Registrant’s telephone number, including area code: (650) 243-3100

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on with registered |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

| Large accelerated filer o | Accelerated filer o | |

| Non-accelerated filer o |

Smaller reporting company x | |

| Emerging growth company o |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes x No o

As of August 13, 2020, there were 210,504,084 shares of common stock of the issuer outstanding.

HUMANIGEN, INC.

FORM 10-Q

| Item 1. | Financial Statements |

Humanigen, Inc.

Condensed Consolidated Balance Sheets

(in thousands, except share data)

(Unaudited)

| June 30, 2020 | December 31, 2019 | |||||||

| Assets | ||||||||

| Current assets: | ||||||||

| Cash and cash equivalents | $ | 41,729 | $ | 143 | ||||

| Prepaid expenses and other current assets | 770 | 309 | ||||||

| Total current assets | 42,499 | 452 | ||||||

| Restricted cash | 70 | 71 | ||||||

| Total assets | $ | 42,569 | $ | 523 | ||||

| Liabilities and stockholders’ deficit | ||||||||

| Current liabilities: | ||||||||

| Accounts payable | $ | 2,110 | $ | 5,046 | ||||

| Accrued expenses | 8,850 | 3,308 | ||||||

| Bridge Notes | - | 2,113 | ||||||

| Convertible notes - current | - | 2,033 | ||||||

| Notes payable to vendors | 8 | 1,094 | ||||||

| Total current liabilities | 10,968 | 13,594 | ||||||

| Convertible notes - non current | - | 1,247 | ||||||

| Total liabilities | 10,968 | 14,841 | ||||||

| Stockholders’ deficit: | ||||||||

| Common stock, $0.001 par value: 225,000,000 shares authorized at | ||||||||

June 30, 2020 and December 31, 2019; 209,874,577 and 114,034,451 shares issued and outstanding at June 30, 2020 and December 31, 2019, respectively | 210 | 114 | ||||||

| Additional paid-in capital | 342,775 | 270,463 | ||||||

| Accumulated deficit | (311,384 | ) | (284,895 | ) | ||||

| Total stockholders’ deficit | 31,601 | (14,318 | ) | |||||

| Total liabilities and stockholders’ deficit | $ | 42,569 | $ | 523 | ||||

See accompanying notes.

| 3 |

Humanigen, Inc.

Condensed Consolidated Statements of Operations

(in thousands, except share and per share data)

(Unaudited)

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||

| Operating expenses: | ||||||||||||||||

| Research and development | $ | 21,143 | $ | 1,234 | $ | 21,802 | $ | 1,593 | ||||||||

| General and administrative | 1,956 | 1,746 | 3,354 | 3,625 | ||||||||||||

| Total operating expenses | 23,099 | 2,980 | 25,156 | 5,218 | ||||||||||||

| Loss from operations | (23,099 | ) | (2,980 | ) | (25,156 | ) | (5,218 | ) | ||||||||

| Other expense: | ||||||||||||||||

| Interest expense | (923 | ) | (358 | ) | (1,333 | ) | (660 | ) | ||||||||

| Other income (expense), net | - | - | - | (1 | ) | |||||||||||

| Net loss | $ | (24,022 | ) | $ | (3,338 | ) | $ | (26,489 | ) | $ | (5,879 | ) | ||||

| Basic and diluted net loss per common share | $ | (0.16 | ) | $ | (0.03 | ) | $ | (0.20 | ) | $ | (0.05 | ) | ||||

| Weighted average common shares outstanding used to | ||||||||||||||||

| calculate basic and diluted net loss per common share | 153,419,159 | 111,110,926 | 132,691,688 | 110,560,662 | ||||||||||||

See accompanying notes.

| 4 |

Humanigen, Inc.

Condensed Consolidated Statements of Cash Flows

(in thousands)

(Unaudited)

| Six Months Ended | ||||||||

| June 30, | ||||||||

| 2020 | 2019 | |||||||

| Operating activities: | ||||||||

| Net loss | $ | (26,489 | ) | $ | (5,879 | ) | ||

| Adjustments to reconcile net loss to net cash used in operating activities: | ||||||||

| Stock based compensation expense | 622 | 1,426 | ||||||

| Issuance of common stock for payment of compensation | 48 | 90 | ||||||

| Issuance of common stock in exchange for services | 70 | 68 | ||||||

| Changes in operating assets and liabilities: | ||||||||

| Prepaid expenses and other assets | (461 | ) | 60 | |||||

| Accounts payable | (2,936 | ) | 717 | |||||

| Accrued expenses | 6,531 | 1,245 | ||||||

| Net cash used in operating activities | (22,615 | ) | (2,273 | ) | ||||

| Financing activities: | ||||||||

| Net proceeds from issuance of common stock | 67,069 | - | ||||||

| Proceeds from exercise of stock options | - | 325 | ||||||

| Net proceeds from issuance of convertible notes | 467 | 1,275 | ||||||

| Net proceeds from issuance of PPP loan | 83 | - | ||||||

| Net proceeds from issuance of bridge notes | 350 | 950 | ||||||

| Payments on PPP loan | (83 | ) | - | |||||

| Payments on bridge notes | (2,400 | ) | - | |||||

| Payments on convertible notes | (518 | ) | - | |||||

| Payments on notes payable to vendors | (768 | ) | - | |||||

| Net cash provided by financing activities | 64,200 | 2,550 | ||||||

| Net increase in cash, cash equivalents and restricted cash | 41,585 | 277 | ||||||

| Cash, cash equivalents and restricted cash, beginning of period | 214 | 885 | ||||||

| Cash, cash equivalents and restricted cash, end of period | $ | 41,799 | $ | 1,162 | ||||

| Supplemental cash flow disclosure: | ||||||||

| Cash paid for interest | $ | 668 | $ | 8 | ||||

| Supplemental disclosure of non-cash investing and financing activities: | ||||||||

| Conversion of notes payable and related accrued interest and fees to common stock | $ | 4,316 | $ | 981 | ||||

| Beneficial conversion feature of Convertible notes | $ | - | $ | 142 | ||||

| Issuance of stock options in lieu of cash compensation | $ | 165 | $ | 195 | ||||

| Issuance of warrants for services | $ | 118 | $ | - | ||||

See accompanying notes.

| 5 |

Humanigen, Inc.

Condensed Consolidated Statements of Stockholders’ Equity (Deficit)

(in thousands, except share data)

(Unaudited)

| Three and Six Months Ended June 30, 2020 | ||||||||||||||||||||

| Additional | Total | |||||||||||||||||||

| Common Stock | Paid-In | Accumulated | Stockholders’ | |||||||||||||||||

| Shares | Amount | Capital | Deficit | Equity | ||||||||||||||||

| Balances at January 1, 2020 | 114,034,451 | $ | 114 | $ | 270,463 | $ | (284,895 | ) | $ | (14,318 | ) | |||||||||

| Issuance of common stock | 200,000 | - | 65 | - | 65 | |||||||||||||||

| Issuance of common stock in exchange for services | 29,342 | - | 13 | - | 13 | |||||||||||||||

| Issuance of stock options for payment of compensation | - | - | 133 | - | 133 | |||||||||||||||

| Issuance of common stock for payment of compensation | 47,997 | - | 19 | - | 19 | |||||||||||||||

| Issuance of warrant for services | - | - | 1 | - | 1 | |||||||||||||||

| Stock-based compensation expense | - | - | 265 | - | 265 | |||||||||||||||

| Net loss | - | - | - | (2,467 | ) | (2,467 | ) | |||||||||||||

| Balances at March 31, 2020 | 114,311,790 | 114 | 270,959 | (287,362 | ) | (16,289 | ) | |||||||||||||

| Issuance of common stock for conversion of debt | 11,989,578 | 12 | 4,304 | - | 4,316 | |||||||||||||||

| Issuance of common stock, net of expenses | 82,528,718 | 83 | 66,921 | - | 67,004 | |||||||||||||||

| Issuance of common stock in exchange for services | 77,313 | - | 57 | - | 57 | |||||||||||||||

| Issuance of stock options for payment of compensation | - | - | 32 | - | 32 | |||||||||||||||

| Issuance of common stock for payment of compensation | 24,574 | - | 29 | - | 29 | |||||||||||||||

| Issuance of warrant for services | - | - | 117 | - | 117 | |||||||||||||||

| Issuance of common stock upon option exercise | 942,604 | 1 | (1 | ) | - | - | ||||||||||||||

| Stock-based compensation expense | - | - | 357 | - | 357 | |||||||||||||||

| Net loss | - | - | - | (24,022 | ) | (24,022 | ) | |||||||||||||

| Balances at June 30, 2020 | 209,874,577 | $ | 210 | $ | 342,775 | $ | (311,384 | ) | $ | 31,601 | ||||||||||

| Three and Six Months Ended June 30, 2019 | ||||||||||||||||||||

| Additional | Total | |||||||||||||||||||

| Common Stock | Paid-In | Accumulated | Stockholders’ | |||||||||||||||||

| Shares | Amount | Capital | Deficit | Deficit | ||||||||||||||||

| Balances at January 1, 2019 | 109,897,526 | $ | 110 | $ | 266,381 | $ | (274,601 | ) | $ | (8,110 | ) | |||||||||

| Issuance of common stock for payment of compensation | 93,358 | - | 90 | - | 90 | |||||||||||||||

| Issuance of stock options for payment of compensation | - | - | 195 | - | 195 | |||||||||||||||

| Issuance of common stock in exchange for services | 82,432 | - | 68 | 68 | ||||||||||||||||

| Exercise of stock options | 75,000 | - | 50 | - | 50 | |||||||||||||||

| Stock-based compensation expense | - | - | 697 | - | 697 | |||||||||||||||

| Net loss | - | - | - | (2,541 | ) | (2,541 | ) | |||||||||||||

| Balances at March 31, 2019 | 110,148,316 | 110 | 267,481 | (277,142 | ) | (9,551 | ) | |||||||||||||

| Convertible note beneficial conversion feature | - | - | 143 | 143 | ||||||||||||||||

| Conversion of advance notes | 2,179,622 | 2 | 979 | - | 981 | |||||||||||||||

| Exercise of common stock options | 413,625 | 1 | 274 | - | 275 | |||||||||||||||

| Stock-based compensation expense | - | - | 729 | - | 729 | |||||||||||||||

| Net loss | - | - | - | (3,338 | ) | (3,338 | ) | |||||||||||||

| Balances at June 30, 2019 | 112,741,563 | $ | 113 | $ | 269,606 | $ | (280,480 | ) | $ | (10,761 | ) | |||||||||

See accompanying notes.

| 6 |

Humanigen, Inc.

Notes to Condensed Consolidated Financial Statements

(Unaudited)

1. Nature of Operations

Description of the Business

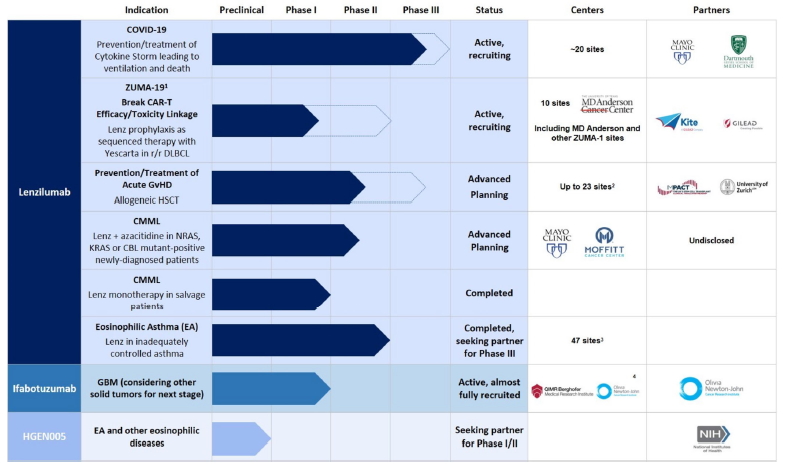

The Company was incorporated on March 15, 2000 in California and reincorporated as a Delaware corporation in September 2001 under the name KaloBios Pharmaceuticals, Inc. Effective August 7, 2017, the Company changed its legal name to Humanigen, Inc. During February 2018, the Company completed the restructuring transactions announced in December 2017 and continued its transformation into a clinical-stage biopharmaceutical company by further developing its clinical stage immuno-oncology and immunology portfolio of monoclonal antibodies. The Company is currently focused on developing its novel human granulocyte-macrophage colony-stimulating factor (“GM-CSF”) neutralization and gene-knockout platforms and its portfolio of antibodies based on its proprietary Humaneered® monoclonal antibody technology and has initiated research in next-generation cell and gene therapies.

The Company’s lead product candidate is lenzilumab, a proprietary Humaneered monoclonal antibody (a biologic) that has been demonstrated to neutralize a naturally occurring inflammatory factor (GM-CSF). GM-CSF is a cytokine which acts directly on myeloid cells to cause expansion, activation, and to initiate and promote the production of other cytokines and chemokines, including IL-6, TNFa, IL-1, MCP-1, MIP-1a, and IP-10 as part of the body’s immune response. GM-CSF is thought of as a communication conduit between the innate and adaptive immune systems. Once initiated, the inflammatory cascade in certain cases may quickly evolve into a self-perpetuating “cytokine storm” as the production of cytokines and chemokines increases expansion and trafficking of myeloid cells. This, in turn, leads to abnormally high levels of inflammatory cytokines, endothelial activation, vascular permeability, disseminated intravascular coagulation, and neurologic inflammation. This cytokine storm is frequently referred to as cytokine release syndrome, or CRS. The neutralization of GM-CSF has been shown to prevent and potentially treat cytokine storm and reduce levels of inflammatory myeloid cells. Reduction of these factors demonstrates that GM-CSF is a critical upstream and early regulator of many inflammatory cytokines known to be important in the pathophysiology of CRS (Sterner RM et al. Blood 2019. 133(7): 697–709).

During 2019 and throughout the early portion of the first quarter of 2020, the Company continued to pursue its anti-GM-CSF programs to prevent or reduce the serious and potentially life-threatening side effects associated with chimeric antigen receptor T-cell (“CAR-T”) therapy and to prevent or treat graft-versus-host disease (“GvHD”) in patients undergoing allogeneic hematopoietic stem cell transplantation (“HSCT”). In collaboration with Kite Pharmaceuticals, Inc., a Gilead company (“Kite or the “Kite Collaboration”), the Company seeks to study the effect of lenzilumab on the safety of Yescarta®, axicabtagene ciloleucel (“Yescarta”), Kite’s FDA-approved CAR-T therapy. A clinical trial, ZUMA-19, is underway to measure the effect of lenzilumab in reducing CRS and neurotoxicity (NT), with a secondary endpoint of increased efficacy of Yescarta. The first patient was dosed with lenzilumab in ZUMA-19 on June 29, 2020.

The coronavirus pandemic, which is due to the SARS-CoV-2 virus and leads to the condition referred to as COVID-19, is frequently characterized in the later and sometimes fatal stages by severe and critical, progressive viral pneumonia that can progress to acute respiratory distress syndrome (“ARDS”), respiratory failure and death. Publications have indicated that ARDS in this setting is caused by the body’s autoimmune response to CRS. Published data point to GM-CSF being a key triggering cytokine, with elevated levels especially in those patients who transition to the Intensive Care Unit (“ICU”).

In response to this published data indicating that GM-CSF inhibition may play a role in treating patients with COVID-19, the Company is developing lenzilumab in patients with COVID-19 in a Phase III study. Given the severity of the pandemic and the lack of approved therapies for COVID-19, the Company believes that this single Phase III study may be suitable for registration and depending on the results of this study may file for approval with the FDA. The Company has commenced enrollment in a multicenter randomized, placebo-controlled, double-blind clinical trial to assess whether lenzilumab can reduce the time to recovery in hospitalized subjects with severe or critical COVID-19 pneumonia. The first patient was dosed with lenzilumab on May 5, 2020.

Lenzilumab was granted emergency single use Investigational New Drug Application (IND) authorization from the FDA (often referred to as compassionate use) to treat patients with COVID-19. On June 15, 2020, the Company announced that Mayo Clinic published (www.medrxiv.org/content/10.1101/2020.06.08.20125369v1) data derived from the compassionate use of lenzilumab in treatment of 12 patients hospitalized in the Mayo Clinic system. Under applicable FDA rules, a patient cannot receive a compassionate use drug unless FDA has issued an individual patient emergency IND authorization, which the Mayo Clinic requested from FDA prior to each individual patient dosing of lenzilumab. Accordingly, there was no randomized control group in the Mayo Clinic program. The Company did not pre-select patients to receive lenzilumab through the compassionate use program and did not deny any requests for compassionate use. Mayo Clinic clinicians solely determined the patients for which they would request emergency IND authorization from the FDA.

| 7 |

See Management’s Discussion and Analysis of Financial Condition and Results of Operations in Item 2 of this Quarterly Report on Form 10-Q for additional information regarding the business.

Liquidity and Going Concern

The Condensed Consolidated Financial Statements for the three and six months ended June 30, 2020 were prepared on the basis of a going concern, which contemplates that the Company will be able to realize assets and discharge liabilities in the normal course of business. However, the Company has incurred net losses since its inception and has negative operating cash flows. These conditions raise substantial doubt about the Company’s ability to continue as a going concern. The financial statements do not include any adjustments that might be necessary if the Company is unable to continue as a going concern.

As described in more detail in Note 7, on June 1, 2020, the Company entered into a securities purchase agreement with certain accredited investors to complete a private placement of our common stock (the “Private Placement”). At the closing, the Company issued and sold 82,528,718 shares of its common stock at a purchase price of $0.87 per share, for aggregate gross proceeds of approximately $71.8 million. The Company used a portion of the proceeds to retire certain indebtedness, as further described in Note 4 - Debt. The Company expects to use the remaining proceeds from the Private Placement to fund its Phase III study of lenzilumab in COVID-19, its collaboration with Kite, initiate manufacturing activities in anticipation of potential receipt of an Emergency Use Authorization (“EUA”) from FDA and subsequent commercialization, and other development programs, as well as for working capital and other general corporate purposes.

As of June 30, 2020, the Company had cash and cash equivalents of $41.8 million. Considering the Company’s current cash resources and its current and expected levels of operating expenses, management expects to need additional capital to fund the Company’s planned operations for the next twelve months. Management may seek to raise such additional capital through equity offerings, debt financings, and/or payments under new or existing licensing or collaboration agreements. While management believes this plan to raise additional funds will alleviate the conditions that raise substantial doubt, these plans are not entirely within its control and cannot be assessed as being probable of occurring. If sufficient funds are not available on acceptable terms when needed, the Company could be required to significantly reduce its operating expenses and delay, reduce the scope of, or eliminate one or more of its development programs. If any of these events occur, the Company’s ability to achieve the development and commercialization goals would be adversely affected.

Basis of Presentation

The accompanying interim unaudited Condensed Consolidated Financial Statements have been prepared in accordance with U.S. generally accepted accounting principles (“U.S. GAAP”) for interim financial information and on a basis consistent with the annual consolidated financial statements and include all adjustments necessary for the presentation of the Company’s condensed consolidated financial position, results of operations and cash flows for the periods presented. The Condensed Consolidated Financial Statements include the accounts of the Company and its wholly owned subsidiaries. These financial statements have been prepared on a basis that assumes that the Company will continue as a going concern, which contemplates the realization of assets and the satisfaction of liabilities and commitments in the normal course of business. The December 31, 2019 Condensed Consolidated Balance Sheet was derived from the audited financial statements but does not include all disclosures required by U.S. GAAP. These interim financial results are not necessarily indicative of the results to be expected for the year ending December 31, 2020, or for any other future annual or interim period. The accompanying unaudited Condensed Consolidated Financial Statements should be read in conjunction with the audited consolidated financial statements and the related notes thereto included in the Company’s 2019 Form 10-K.

The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the amounts and disclosures reported in the Condensed Consolidated Financial Statements and accompanying notes. Actual results could differ materially from those estimates. The Company believes judgment is involved in determining the valuation of the fair value-based measurement of stock-based compensation and warrant valuations. The Company evaluates its estimates and assumptions as facts and circumstances dictate. As future events and their effects cannot be determined with precision, actual results could differ from these estimates and assumptions, and those differences could be material to the Condensed Consolidated Financial Statements.

| 8 |

Certain prior year amounts have been reclassified to conform to the current year presentation. Such reclassifications had no effect on prior years’ Net loss or Stockholders’ equity (deficit).

2. Summary of Significant Accounting Policies

There have been no material changes in the Company’s significant accounting policies since those previously disclosed in the 2019 Form 10-K.

Derivative Financial Instruments

The Company has equity conversion features within its 2020 Convertible Redeemable Notes that qualify as embedded derivatives under the guidance of FASB ASC Topic 815, Derivatives and Hedging. As part of that guidance, an analysis is performed on each embedded derivative to determine whether it should be bifurcated from the host instrument and recorded separately within the Consolidated Balance Sheet at its fair value. Changes in fair value are recorded in other income (expense) within the Consolidated Statement of Operations. Refer to Note 4 - Debt and Note 5 – Derivative Instruments for further discussion of the Company’s embedded derivatives.

3. Potentially Dilutive Securities

The Company’s potentially dilutive securities, which include stock options, restricted stock units and warrants, have been excluded from the computation of diluted net loss per common share as the effect of including those securities would be to reduce the net loss per common share and be antidilutive. Therefore, the denominator used to calculate both basic and diluted net loss per common share is the same in each period presented.

The following outstanding potentially dilutive securities have been excluded from the computations of diluted net loss per common share:

| As of June 30, | ||||||||

| 2020 | 2019 | |||||||

| Options to purchase common stock | 16,516,695 | 15,139,374 | ||||||

| Warrants to purchase common stock | 541,193 | 331,193 | ||||||

| 17,057,888 | 15,470,567 | |||||||

4. Debt

Notes Payable to Vendors

On June 30, 2016, the Company issued promissory notes in an aggregate principal amount of approximately $1.2 million to certain claimants in accordance with the Company’s Plan of Reorganization (the “Plan”) filed with the United States Bankruptcy Court for the District of Delaware (the “Bankruptcy Court”) (Case No. 15-12628 (LSS) (the “Bankruptcy Case”) which became effective June 30, 2016, at which time the Company emerged from its Chapter 11 bankruptcy proceedings. The notes were unsecured, accrued interest at 10% per annum and became due and payable in full, including principal and accrued interest on June 30, 2019. In July and August, 2019, following the receipt of proceeds from the 2019 Bridge Notes, the Company used approximately $0.5 million of the proceeds to retire a portion of these notes, including accrued interest. After giving effect to these payments, the aggregate principal amount and accrued but unpaid interest on these notes approximated $1.1 million as of December 31, 2019 and the Company had accrued $0.3 million in interest expense. In June and July 2020, the Company used the proceeds from the Private Placement (as defined below) to repay the remaining outstanding principal including accrued and unpaid interest on these notes and the notes were extinguished. As of June 30, 2020, one note for $8.0 thousand, including principal and accrued but unpaid interest was still outstanding; this note was repaid in July 2020.

Advance Notes

In June, July and August, 2018 the Company received an aggregate of $0.9 million of proceeds from advances made to the Company (the “Advance Notes”) by four different lenders including Dr. Cameron Durrant, the Company’s Chairman and Chief Executive Officer; Cheval Holdings, Ltd. (“Cheval”), an affiliate of Black Horse Capital, L.P. (“BHC”), the Company’s controlling stockholder at the time; and Ronald Barliant, a director of the Company. The Advance Notes accrued interest at a rate of 7% per year, compounded annually.

| 9 |

In accordance with their terms, on May 30, 2019, in connection with the Company’s announcement of the Collaboration Agreement with Kite, the lenders converted the amounts due under the Advance Notes into the Company’s common stock at the conversion price of $0.45 per share. The Company issued a total of 2,179,622 shares of common stock in connection with the conversion.

2018 Convertible Notes

Commencing September 19, 2018, the Company delivered a series of convertible promissory notes (the “2018 Notes”) evidencing an aggregate of $2.5 million of loans made to the Company by six different lenders, including an affiliate of BHC, the Company’s controlling stockholder at the time. The 2018 Notes accrued interest at a rate of 7% per annum and, in general, were set to mature twenty-four months from the date the 2018 Notes were signed. The Company used the proceeds from the 2018 Notes for working capital.

The 2018 Notes were convertible into equity securities of the Company in three different scenarios, including if the Company sold its equity securities on or before the date of repayment of the 2018 Notes in any financing transaction that resulted in gross proceeds to the Company of less than $10 million (a “Non-Qualified Financing”). In connection with a Non-Qualified Financing, the noteholders were able to convert their remaining 2018 Notes into either (i) such equity securities as the noteholder would acquire if the principal and accrued but unpaid interest thereon (the “Conversion Amount”) were invested directly in the financing on the same terms and conditions as given to the financing investors in the Non-Qualified Financing, or (ii) common stock at a conversion price equal to $0.45 per share (subject to ratable adjustment for any stock split, stock dividend, stock combination or other recapitalization occurring subsequent to the date of the Notes).

The Company’s sales of shares pursuant to the ELOC Purchase Agreement with Lincoln Park Capital Fund, LLC (“LPC”) constituted a Non-Qualified Financing. Commencing on April 2, 2020, the holders of the 2018 Notes notified the Company of their exercise of their conversion rights under the 2018 Notes. See “2019 Convertible Notes” for additional information regarding the conversion of 2018 Notes by the holders.

As of December 31, 2019, the Company had accrued $0.2 million in interest related to these promissory notes. Interest expense recorded during the three and six months ended June 30, 2020 was approximately $564 thousand and $817 thousand, respectively.

2019 Convertible Notes

Commencing on April 23, 2019, the Company delivered a series of convertible promissory notes (the “2019 Notes” and together with the 2018 Notes, the “Convertible Notes”) evidencing an aggregate of $1.3 million of loans made to the Company. The 2019 Notes accrued interest at a rate of 7.5% per annum and, in general, were set to mature twenty-four months from the date the 2019 Notes were signed. The Company used the proceeds from the 2019 Notes for working capital.

The 2019 Notes were convertible into equity securities of the Company in four different scenarios, including if the Company sold its equity securities on or before the date of repayment of the 2019 Notes in any financing transaction that resulted in gross proceeds to the Company of less than $10 million (a “Non-Qualified Financing”). In connection with a Non-Qualified Financing, the noteholders were able to convert their remaining 2019 Notes into either (i) such equity securities as the noteholder would acquire if the Conversion Amount were invested directly in the financing on the same terms and conditions as given to the financing investors in the Non-Qualified Financing, or (ii) common stock at a conversion price equal to $1.25 per share (subject to ratable adjustment for any stock split, stock dividend, stock combination or other recapitalization occurring subsequent to the date of the 2019 Notes).

The Company’s sales of shares pursuant to the ELOC Purchase Agreement with LPC constituted a Non-Qualified Financing. Commencing on April 2, 2020, holders of the Convertible Notes, including Cheval, an affiliate of BHC, the Company’s controlling stockholder at the time, notified the Company of their exercise of their conversion rights under the Convertible Notes. Pursuant to the exemption from registration afforded by Section 3(a)(9) under the Securities Act, the Company issued an aggregate of 11,989,578 shares of its common stock upon the conversion of $4.3 million in aggregate principal and interest on the Convertible Notes that were converted, which obligations were retired. Of these, the Company issued 1,583,333 shares to Cheval. Dr. Dale Chappell, who was serving as the Company’s ex-officio chief scientific officer at the time and currently serves as its Chief Scientific Officer, controls BHC and reports beneficial ownership of all shares held by it and its affiliates, including Cheval. After giving effect to the shares issued upon such conversions, no convertible notes issued in 2018 or 2019 were outstanding as of June 30, 2020.

| 10 |

As of December 31, 2019, the Company had accrued $0.1 million in interest related to the 2019 Notes. Interest expense related to the 2019 Notes, recorded during the three and six months ended June 30, 2020, was approximately $178 thousand and $219 thousand, respectively.

The Advance Notes, the 2018 Notes and the 2019 Notes had an optional voluntary conversion feature in which the holder could convert the notes in the Company’s common stock at maturity at a conversion rate of $0.45 per share for the Advance Notes and the 2018 Notes and at a conversion rate of $1.25 for the 2019 Notes. The intrinsic value of this beneficial conversion feature was $1.8 million upon the issuance of the Advance Notes, the 2018 Notes and the 2019 Notes and was recorded as additional paid-in capital and as a debt discount which is accreted to interest expense over the term of the Advance Notes and Notes. Interest expense includes debt discount amortization of $558 thousand and $785 thousand for the three and six months ended June 30, 2020, respectively.

The Company evaluated the embedded features within the Advance Notes, the 2018 Notes and the 2019 Notes to determine if the embedded features are required to be bifurcated and recognized as derivative instruments. The Company determined that the Advance Notes, the 2018 Notes and the 2019 Notes contain contingent beneficial conversion features (“CBCF”) that allow or require the holder to convert the Advance Notes, the 2018 Notes and the 2019 Notes, as applicable, to Company common stock at a conversion rate of $0.45 per share for the Advance Notes and the 2018 Notes and $1.25 for the 2019 Notes, but did not contain embedded features requiring bifurcation and recognition as derivative instruments. Upon the occurrence of a CBCF that results in conversion of the Advance Notes, the 2018 Notes or the 2019 Notes to Company common stock, the remaining unamortized discount will be charged to interest expense. Upon conversion of the Advance Notes on May 30, 2019, the remaining unamortized discount was charged to interest expense. Upon the conversion of the Convertible Notes in April 2020, the remaining related unamortized discount was charged to interest expense.

2020 Convertible Redeemable Notes

On March 13, 2020 and March 19, 2020 (the “Issuance Dates”), the Company delivered two convertible redeemable promissory notes (the “2020 Notes”) evidencing loans with an aggregate principal amount of $518,333 made to the Company.

The 2020 Notes accrued interest at a rate of 7.0% per annum and were set to mature on March 13, 2021 and March 19, 2021, respectively. The 2020 Notes contained an original issue discount of $33,000 and $18,833, respectively. The Company used the proceeds from the 2020 Notes for working capital.

The notes could be redeemed by the Company at any time before the 270th day following issuance, at a redemption price equal to the principal and accrued but unpaid interest on the notes to the date of redemption, plus a premium that increases on day 61 and day 121 from the issuance date. Accordingly, the notes were repaid in June 2020 with proceeds from the Private Placement, and the notes were extinguished.

The Company evaluated the embedded features within the 2020 Notes and determined that the embedded features are required to be bifurcated and recognized as stand-alone derivative instruments. The variable-share settlement features within the 2020 Notes qualify as redemption features and meet the net settlement criterion for qualification as a stand-alone derivative. In determining the fair value of the bifurcated derivative, the Company evaluated the likelihood of conversion of the 2020 Notes to Company stock. As the Company believed it would have adequate funding prior to the six month anniversary of the 2020 Notes, the first conversion option for the holders of the 2020 Notes, and it had the intent to either begin making amortizing payments or to pay off the 2020 Notes in their entirety prior to that date, the fair value was determined to be $0. The original issue discount was accreted to Interest expense and the remaining balance was charged to Interest expense upon payoff.

Interest expense related to the 2020 Notes, recorded during the three and six months ended June 30, 2020, was approximately $161 thousand and $165 thousand, respectively.

Interest expense includes the original issue discount amortization of approximately $50 thousand and $52 thousand for the three and six months ended June 30, 2020, respectively.

| 11 |

Bridge Notes

On June 28, 2019, the Company issued three short-term, secured bridge notes (the “June Bridge Notes”) evidencing an aggregate of $1.7 million of loans made to the Company by three parties: Cheval , an affiliate of BHC, the Company’s controlling stockholder at the time, lent $750,000; Nomis Bay LTD, the Company’s second largest stockholder, lent $750,000; and Dr. Cameron Durrant, the Company’s Chief Executive Officer and Chairman of the Board of Directors (the “Board”), lent $200,000. The proceeds from the June Bridge Notes were used to satisfy a portion of the unsecured obligations incurred in connection with the Company’s emergence from bankruptcy in 2016 and for working capital and general corporate purposes. Of the $1.7 million in proceeds received, $950,000 was received on June 28, 2019 and was recorded as Advance notes in the Condensed Consolidated Balance Sheet as of June 30, 2019. The remaining proceeds of $750,000 were received July 1, 2019 and recorded accordingly.

The June Bridge Notes accrued interest at a rate of 7.0% per annum and after giving effect to multiple extensions, were set to mature on December 31, 2020. The June Bridge Notes could become due and payable at such earlier time as the Company raised more than $3,000,000 in a bona fide financing transaction or upon a change in control. Accordingly, the June Bridge Notes were repaid in June 2020 with proceeds from the Private Placement, and the June Bridge Notes were extinguished.

On November 12, 2019, the Company issued two short-term, secured bridge notes (the “November Bridge Notes” and together with the June Bridge Notes, the “2019 Bridge Notes”) evidencing an aggregate of $350,000 of loans made to the Company by two parties: Cheval, an affiliate of BHC, our controlling stockholder at the time, lent $250,000; and Dr. Cameron Durrant, our Chief Executive Officer and Chairman of our Board, lent $100,000. The proceeds from the November Bridge Notes were used for working capital and general corporate purposes.

The November Bridge Notes ranked on par with the June Bridge Notes, and possessed other terms and conditions substantially consistent with those notes. The November Bridge Notes accrued interest at a rate of 7.0% per annum and after giving effect to multiple extensions, were set to mature on December 31, 2020. The November Bridge Notes could become due and payable at such earlier time as the Company raised more than $3,000,000 in a bona fide financing transaction or upon a change in control. Accordingly, the November Bridge Notes were repaid in June 2020 with proceeds from the Private Placement.

In April 2020, the Company issued two short-term, secured bridge notes (the “April Bridge Notes” and together with the June Bridge Notes and the November Bridge Notes, the “Bridge Notes”) evidencing an aggregate of $350,000 of loans made to the Company: Cheval, an affiliate of BHC, the Company’s controlling stockholder at the time, loaned $100,000, and Nomis Bay, the Company’s second largest stockholder, loaned $250,000. The proceeds from the April Bridge Notes were used for working capital and general corporate purposes.

The April Bridge Notes ranked on par with the June Bridge Notes and the November Bridge Notes, and possessed other terms and conditions substantially consistent with them. The notes accrued interest at a rate of 7.0% per annum and were set to mature on December 31, 2020. The April Bridge Notes could become due and payable at such earlier time as the Company raised more than $10,000,000 in a bona fide financing transaction or upon a change in control. Accordingly, these April Bridge Notes were repaid in June 2020 with proceeds from the Private Placement, and these bridge notes were extinguished.

The Bridge Notes were secured by a lien on substantially all of the Company’s assets, which liens have been released.

Interest expense related to the Bridge Notes, recorded during the three and six months ended June 30, 2020, was approximately $30 thousand and $66 thousand, respectively.

5. Derivative Instruments

The Company had certain embedded equity conversion features within its 2020 Notes that require bifurcation and recognition as stand-alone derivatives. See Note 4 – Debt for additional information and discussion on the bifurcated derivatives.

| 12 |

6. Commitments and Contingencies

Contractual Obligations and Commitments

As of June 30, 2020, other than the retirement and conversion of certain debt described in Note 4 and the license agreements described in Note 8, there were no material changes to the Company’s contractual obligations from those set forth in the 2019 Form 10-K.

Guarantees and Indemnifications

The Company has certain agreements with service providers with which it does business that contain indemnification provisions pursuant to which the Company typically agrees to indemnify the party against certain types of third-party claims. The Company accrues for known indemnification issues when a loss is probable and can be reasonably estimated. The Company would also accrue for estimated incurred but unidentified indemnification issues based on historical activity. As the Company has not incurred any indemnification losses to date, there were no accruals for or expenses related to indemnification issues for any period presented.

7. Stockholders’ Equity

Lincoln Park Capital Purchase Agreement

On November 8, 2019, the Company entered into a purchase agreement (the “ELOC Purchase Agreement”) and a registration rights agreement with LPC, pursuant to which the Company had the right to sell to LPC up to $20,000,000 in shares of the Company’s common stock, $0.001 par value per share (the “Common Stock”), subject to certain limitations and conditions set forth in the ELOC Purchase Agreement.

Under the ELOC Purchase Agreement, the Company had the right, from time to time at its sole discretion and subject to certain conditions, to direct LPC to purchase up to 100,000 shares of Common Stock, with such amounts increasing based on certain threshold prices but not to exceed $750,000 in total proceeds on any purchase date. The purchase price of shares of Common Stock pursuant to the ELOC Purchase Agreement was based on the market prices of the Common Stock at the time of such purchases as set forth in the ELOC Purchase Agreement. Such sales of Common Stock by the Company, if any, could occur from time to time, at the Company’s option, over the 36-month period expiring in December 2022.

In connection with the signing of the ELOC Purchase Agreement on November 8, 2019, the Company issued 706,592 shares of its common stock to LPC. The issuance of the shares were recorded as debt issuance costs in Common stock and Additional paid-in capital with no net effect on Stockholders’ equity (deficit).

During the months of December 2019 and January 2020, the Company issued a total of 700,000 shares for aggregate proceeds of $0.3 million under the ELOC Purchase Agreement.

On June 2, 2020, following completion of the Private Placement described below, the Company notified LPC of its decision to terminate the ELOC Purchase Agreement. The termination of the ELOC Purchase Agreement became effective on June 3, 2020.

2020 Private Placement

On June 1, 2020, the Company entered into a securities purchase agreement (the “Purchase Agreement”) with certain accredited investors (the “Investors”) to complete a private placement of our common stock (the “Private Placement”). The closing of the Private Placement occurred on June 2, 2020 (the “Closing Date”). At the closing, the Company issued and sold 82,528,718 shares of its common stock (the “Shares”) at a purchase price of $0.87 per share, for aggregate gross proceeds of approximately $71.8 million. The Company used a portion of the proceeds to retire certain indebtedness, as further described in Note 4 - Debt. The Company expects to use the remaining proceeds from the Private Placement to fund its Phase III study of lenzilumab in COVID-19, to secure manufacturing capacity, to progress Chemistry, Manufacturing and Controls (“CMC”) work, to prepare for commercialization in the event of approval of lenzilumab for use in COVID-19 patients under an EUA or otherwise, its collaboration with Kite and other development programs and for working capital and other general corporate purposes. See Note 10 for information regarding two complaints filed against us in connection with the Private Placement.

| 13 |

On the Closing Date, the Company and the Investors also entered into a registration rights agreement (the “Registration Rights Agreement”) pursuant to which the Company agreed to prepare and file a registration statement (the “Resale Registration Statement”) for the resale of the Shares with the Securities and Exchange Commission (the “SEC”),.

Subject to certain limitations and an overall cap, the Company may be required to pay liquidated damages to the investors at a rate of 2% of the invested capital for each occurrence (and continuation for 30 consecutive days thereafter) of a breach by the Company of certain of its obligations under the Registration Rights Agreement.

The Purchase Agreement also requires that the Company use its commercially reasonable efforts to achieve a listing of the Common Stock on a national securities exchange, subject to certain limitations set forth in the Purchase Agreement. On July 6, 2020, the Company applied to have its common stock approved for listing on the Nasdaq Capital Market. The Company’s ability to obtain Nasdaq’s approval of the listing application will require the Company to satisfy a number of conditions, including the Company’s ability to meet certain listing criteria including a minimum stock price and total value of public float. Accordingly, the Company can make no assurances that the application for listing will be approved.

2012 Equity Incentive Plan

Under the Company’s 2012 Equity Incentive Plan, the Company may grant shares, stock units, stock appreciation rights, performance cash awards and/or options to employees, directors, consultants, and other service providers. For options, the per share exercise price may not be less than the fair market value of a Company common share on the date of grant. Awards generally vest and become exercisable over three to four years and expire 10 years from the date of grant. Options generally become exercisable as they vest following the date of grant.

On June 1, 2020, with a limited number of shares remaining available for grant, and with the 2012 Equity Incentive Plan set to expire in 2022, the Board determined that it was appropriate to replace the 2012 Equity Incentive Plan. On July 27, 2020, the Board unanimously approved, and recommended that our stockholders approve, the Humanigen, Inc. 2020 Omnibus Incentive Compensation Plan (the “2020 Equity Plan”), to ensure that the Board and its compensation committee will be able to make the types of awards, and covering the number of shares, as necessary to meet the Company’s compensatory needs. On July 29, 2020, the 2020 Equity Plan was approved by written consent of the holders of approximately 63% of our outstanding shares of common stock on that date. Upon the “Effective Date” of the 2020 Equity Plan (as described below), an aggregate of 35,000,000 shares of our common stock will be reserved for issuance upon grants of awards made under the plan by the Board or its compensation committee. The 2020 Equity Plan will not become effective (such time, the “Effective Date”) until such time as we file an amendment to our certificate of incorporation with the Delaware Secretary of State to increase our authorized shares of common stock (described in more detail under Note 11—Subsequent Events). The 2020 Equity Plan will remain in effect until the tenth anniversary of the Effective Date, unless terminated earlier by the Board.

A summary of stock option activity for the six months ended June 30, 2020 under all of the Company’s options plans is as follows:

| Options | Weighted Average Exercise Price | |||||||

| Outstanding at January 1, 2020 | 15,881,721 | $ | 0.95 | |||||

| Granted | 1,719,395 | 0.54 | ||||||

| Exercised | (1,084,316 | ) | 0.65 | |||||

| Cancelled (forfeited) | - | - | ||||||

| Cancelled (expired) | (105 | ) | 11.68 | |||||

| Outstanding at June 30, 2020 | 16,516,695 | $ | 0.93 | |||||

| 14 |

The weighted average fair value of options granted during the six months ended June 30, 2020 was $0.40 per share.

The Company valued the options granted using the Black-Scholes options pricing model and the following weighted-average assumption terms for the six months ended June 30, 2020:

| Six months ended June 30, 2020 | |

| Exercise price | $0.38 - $1.20 |

| Market value | $0.38 - $1.20 |

| Expected term | 5 years |

| Expected volatility | 94.6% - 100.2% |

| Risk-free interest rate | 0.34% - 1.57% |

| Expected dividend yield | - % |

Stock-Based Compensation

The Company recorded stock-based compensation expense in the Condensed Consolidated Statements of Operations as follows:

| Three months ended June 30, | Six months ended June 30, | |||||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||

| General and administrative | $ | 295 | $ | 697 | $ | 506 | $ | 1,394 | ||||||||

| Research and development | 62 | $ | 32 | 116 | 32 | |||||||||||

| Total stock-based compensation | $ | 357 | $ | 729 | $ | 622 | $ | 1,426 | ||||||||

At June 30, 2020, the Company had $1.0 million of total unrecognized stock-based compensation expense, net of estimated forfeitures, related to outstanding stock options that will be recognized over a weighted-average period of 1.4 years.

8. License and Collaboration Agreements

Kite Agreement

On May 30, 2019, the Company entered into a collaboration agreement (the “Kite Agreement”) with Kite Pharmaceuticals, Inc., pursuant to which the Company and Kite are conducting a multi-center Phase 1b/2 study of lenzilumab with Kite’s Yescarta in patients with relapsed or refractory B-cell lymphoma, including diffuse large B-cell lymphoma (“DLBCL”). The primary objective of the Study is to determine the effect of lenzilumab on the safety of Yescarta.

Pursuant to the Kite Agreement, the Company shall supply lenzilumab to the collaboration for use in the study and will contribute up to approximately $8.0 million towards the out-of-pocket costs of the study, depending on the number of patients enrolled into the study.

Mayo Agreement

On June 19, 2019 the Company entered into an exclusive worldwide license agreement (the “Mayo Agreement”) with the Mayo Foundation for Medical Education and Research (“Mayo”) for certain technologies used to create CAR-T cells lacking GM-CSF expression through various gene-editing tools including CRISPR-Cas9 (GM-CSF knock-out). The license covers various patent applications and know-how developed by Mayo in collaboration with the Company. These licensed technologies complement and broaden the Company’s position in the GM-CSF neutralization space and expand the Company’s discovery platform aimed at improving CAR-T to include gene-edited CAR-T cells.

Pursuant to the Mayo Agreement, the Company agreed to pay $200,000 to Mayo within six months of the effective date, or upon completion of a qualified financing, whichever is earlier. The Mayo Agreement also requires the payment of milestones and royalties upon the achievement of certain regulatory and commercialization milestones. The initial payment was accrued as expense in Research and development in June 2019. The Company paid the initial payment in June 2020 subsequent to the closing of the Private Placement.

| 15 |

Zurich Agreement

On July 19, 2019 the Company entered into an exclusive worldwide license agreement (the “Zurich Agreement”) with the University of Zurich (“UZH”) for technology used to prevent or treat Graft versus Host Disease (“GvHD”) through GM-CSF neutralization. The Zurich Agreement covers various patent applications filed by UZH which complement and broaden the Company’s position in the application of GM-CSF and expands the Company’s development platform to include improving allogeneic Hematopoietic Stem Cell Transplantation (“HSCT”).

Pursuant to the Zurich Agreement, the Company paid $100,000 to UZH in July 2019. The Zurich Agreement also requires the payment of milestones and royalties upon the achievement of certain regulatory and commercialization milestones. The license payment of $100,000 was recorded as expense in Research and development in July 2019.

9. Savant Arrangements

On June 30, 2016 the Company and Savant Neglected Diseases, LLC (“Savant”) entered into an Agreement for the Manufacture, Development and Commercialization of Benznidazole for Human Use (the “MDC Agreement”), pursuant to which the Company acquired certain worldwide rights relating to benznidazole (the “Compound”).

In addition, on the Effective Date the Company and Savant also entered into a Security Agreement (the “Security Agreement”), pursuant to which the Company granted Savant a continuing senior security interest in the assets and rights acquired by the Company pursuant to the MDC Agreement and certain future assets developed from those acquired assets.

On the Effective Date, the Company issued to Savant a five year warrant (the “Warrant”) to purchase 200,000 shares of the Company’s Common Stock, at an exercise price of $2.25 per share, subject to adjustment. As of June 30, 2020 the Warrant was exercisable for 100,000 shares at an exercise price of $2.25 per share. On July 20, 2020, the Company issued to Savant a total of 54,545 shares of its common stock pursuant to a “net exercise” of the Warrant by Savant. The Warrant is not, and is not expected to vest or become exercisable for any additional shares of the Company’s common stock.

As a result of the FDA granting accelerated and conditional approval of a benznidazole therapy manufactured by a competitor for the treatment of Chagas disease and awarding such competitor a neglected tropical disease PRV in August 2017, the Company ceased development of benznidazole and re-evaluated the final two vesting milestones and concluded that the probability of achievement of these milestones had decreased to 0%.

In July 2017, the Company commenced litigation against Savant alleging that Savant breached the MDC Agreement and seeking a declaratory judgement. Savant has asserted counterclaims for breaches of contract under the MDC Agreement and the Security Agreement. The dispute primarily concerns the Company’s right under the MDC Agreement to offset certain costs incurred by the Company in excess of the agreed upon budget against payments due Savant. See Note 10, below, for more information regarding the Savant litigation. The aggregate cost overages as of June 30, 2017 that the Company asserts are Savant’s responsibility total approximately $3.4 million, net of a $0.5 million deductible. The Company asserts that it is entitled to offset $2.0 million in milestone payments due Savant against the cost overages, such that as of June 30, 2017, Savant owed the Company approximately $1.4 million. As of June 30, 2019, the cost overages totaled $4.1 million such that Savant owed the Company approximately $2.1 million in cost overages. Such cost overages have been charged to Research and development expense as incurred. Recovery of such cost overages, if any, will be recorded as a reduction of Research and development expense in the period received.

The $2.0 million in milestone payments due Savant are included in Accrued expenses in the accompanying Condensed Consolidated Balance Sheets as of June 30, 2020 and December 31, 2019.

10. Litigation

Savant Litigation

On July 10, 2017, the Company filed a complaint against Savant in the Superior Court for the State of Delaware, New Castle County (the “Delaware Court”). KaloBios Pharmaceuticals, Inc. v. Savant Neglected Diseases, LLC, No. N17C-07-068 PRW-CCLD. The Company asserted breach of contract and declaratory judgment claims against Savant arising under the MDC Agreement. See Note 9 - “Savant Arrangements” for more information about the MDC Agreement. The Company alleges that Savant has breached its MDC Agreement obligations to pay cost overages that exceed a budgetary threshold as well as other related MDC Agreement representations and obligations. In the litigation, the Company has alleged that as of June 30, 2017, Savant was responsible for aggregate cost overages of approximately $3.4 million, net of a $0.5 million deductible under the MDC. The Company asserts that it is entitled to offset $2.0 million in milestone payments due Savant against the cost overages, such that as of June 30, 2017 Savant owed the Company approximately $1.4 million.

| 16 |

On July 12, 2017, Savant removed the case to the Bankruptcy Court, claiming that the action is related to or arises under the Bankruptcy Case from which we emerged in July 2016. In re KaloBios Pharmaceuticals, Inc., No. 15-12628 (LSS) (Bankr. D. Del.). On July 27, 2017, Savant filed an Answer and Counterclaims. Savant’s filing alleges breaches of contracts under the MDC Agreement and the Security Agreement, claiming that the Company breached its obligations to pay the milestone payments and other related representations and obligations. On August 1, 2017, the Company moved to remand the case back to the Delaware Court (the “Motion to Remand”).

On August 2, 2017, Savant sent a foreclosure notice to the Company, demanding that it provide the Collateral as defined in the Security Agreement for inspection and possession on August 9, 2017, with a public sale to be held on September 1, 2017. The Company moved for a Temporary Restraining Order (the “TRO”) and Preliminary Injunction in the Bankruptcy Court on August 4, 2017. Savant responded on August 7, 2017. On August 7, 2017, the Bankruptcy Court granted the Company’s motion for a TRO, entering an order prohibiting Savant from collecting on or selling the Collateral, entering our premises, issuing any default notices to us, or attempting to exercise any other remedies under the MDC Agreement or the Security Agreement. On August 9, 2017, the parties have stipulated to continue the provisions of the TRO in full force and effect until further order of the appropriate court, which the Bankruptcy Court signed that same day (the “Stipulated Order”).

On January 22, 2018, Savant wrote to the Bankruptcy Court requesting dissolution of the TRO and the Stipulated Order. On January 29, 2018, the Bankruptcy Court granted the Motion to Remand and denied Savant’s request to dissolve the TRO and Stipulated Order, ordering that any request to dissolve the TRO and Stipulated Order be made to the Delaware Court.

On February 13, 2018 Savant made a letter request to the Delaware Court to dissolve the TRO and Stipulated Order. Also on February 13, 2018, the Company filed its Answer and Affirmative defenses to Savant’s Counterclaims. On February 15, 2018 the Company filed a letter opposition to Savant’s request to dissolve the TRO and Stipulated Order and requesting a status conference. A hearing on Savant’s request to dissolve the TRO and Stipulated Order was held before the Delaware Court on March 19, 2018. The Delaware Court denied Savant’s request to dissolve the TRO and Stipulated order, which remain in effect.

On April 11, 2018, the Company advised the Delaware Court that it would meet and confer with Savant regarding a proposed case management order and date for trial. On April 26, 2018 the Delaware Court so-ordered a proposed case management order submitted by the Company and Savant. The schedule in the case management order was modified by stipulation on August 24, 2018.

On April 8, 2019, the Company moved to compel Savant to produce documents in response to the Company’s document requests. The parties thereafter agreed to a discovery schedule through June 30, 2019, which the Superior Court so-ordered, and the parties produced documents to each other.

On June 4, 2019, Savant filed a complaint against the Company and Madison in the Delaware Court of Chancery (the “Chancery Action”) seeking to “recover as damages that amounts owed to it under the MDC Agreement, and to reclaim Savant’s intellectual property,” among other things. Savant also requested leave to move to dismiss the Company’s complaint on the grounds that the Company’s transfer of assets to Madison was champertous. On June 10, 2019, the Company requested by letter that the Superior Court hold a contempt hearing because the Chancery Action violated the TRO entered by the Bankruptcy Court, the terms of which have been extended by stipulation of the parties. On June 18, 2019, the Superior Court held a telephonic status conference. The parties agreed that the Chancery Action should be consolidated with the Superior Court action, after which the Superior Court would address the parties’ motions.

On July 22, 2019, the Company moved for contempt against Savant. Savant filed its opposition on July 29, 2019. On August 12, 2019, the Superior Court denied the Company’s motion for contempt.

On July 23, 2019, Savant moved for summary judgment on the issue of champerty. The Company filed its response and cross-motion for summary judgment on August 27, 2019. Savant filed its reply on September 10, 2019 and the Company filed its cross-reply on September 20, 2019. The motion is fully briefed, and was argued at a hearing on February 3, 2020. The court has not yet ruled on the motion.

| 17 |

On July 26, 2019, the Company moved to modify the previously agreed-upon discovery schedule to extend discovery through December 31, 2019, which the Superior Court granted. In subsequent orders, the discovery schedule was further extended until the end of June 2020.

On July 30, 2019, the Company filed a motion to dismiss Savant’s Chancery Action. Savant filed an amended complaint on September 4, 2019, and the Company filed its opening brief in support of its motion to dismiss on October 11, 2019. That motion is fully briefed and was argued at a hearing on February 3, 2020. The court has not yet ruled on the motion.

On August 19, 2019, Savant moved to dismiss the Company’s amended Superior Court complaint. On September 27, 2019, the Company filed an opposition to Savant’s motion and, in the alternative, requested leave to file a second amended complaint against Savant. Savant consented to the filing of the second amended complaint and withdrew their motion to dismiss. Savant filed a partial motion to dismiss against a co-defendant on October 30, 2019. That motion is fully briefed and was argued at a hearing on February 3, 2020. At the February 3, 2020 hearing, the Court reserved judgment on the parties’ reciprocal motions.

On November 18, 2019, the Court granted Savant’s Motion to Schedule a Preliminary Injunction hearing concerning the August 2017 TRO and Stipulated Order that are still in effect. On May 8, 2020, the Court granted the application for a preliminary injunction to the Company. The Stipulated Order is no longer in effect.

On May 22, 2020, upon the request of the parties, the Superior Court stayed both Delaware actions until July 29, 2020.

On July 24, 2020, the parties submitted a joint status report in the Delaware actions. The parties also requested a status conference with the Court to discuss moving the trial from October 2020 to some later time.

Private Placement Litigation

On June 15, 2020, a complaint was filed against Humanigen and Dr. Durrant in the Commercial Division of the Supreme Court of the State of New York. The plaintiffs comprise a group of 17 prospective investors introduced to Humanigen by Noble Capital Markets, Inc. (“Noble”), which had been engaged as a non-exclusive placement agent in connection with the Private Placement. The plaintiffs had indicated interest in purchasing shares of common stock in the Private Placement but, due to the strength of demand for shares from other prospective investors introduced to the company by J.P. Morgan Securities LLC, the lead placement agent for the Private Placement, the plaintiffs were not allocated any investment amount. The plaintiffs allege that the company and Dr. Durrant breached a contractual obligation to deliver shares of common stock to the plaintiffs. The plaintiffs seek to recover for losses due to alleged fraudulent misstatements and the company’s failure to deliver shares to them, and seek equitable relief in the form of specific performance.

On June 19, 2020, Noble filed a separate complaint against Humanigen in the Circuit Court of the Fifteenth Judicial Circuit in and for Palm Beach County, Florida, also arising from the Private Placement. Noble’s complaint alleges that Humanigen breached the terms of its engagement letters with Noble by refusing to pay it the sales commissions it would have earned had its prospective investors received the entire allocation of shares sought in the Private Placement, as opposed to the $4 million of shares actually allocated to Noble and its clients. Noble is seeking payment in full of the commission, damages for Humanigen’s alleged tortious interference with Noble’s business relationship with the investors it introduced to Humanigen but which were not allocated shares in the Private Placement, and attorneys’ fees.

The Company believes that the claims made in each complaint are without merit, and it is prepared to defend itself vigorously.

11. Subsequent Events

Appointment of Mr. Tousley as Chief Accounting and Administrative Officer, Corporate Secretary and Treasurer

On July 6, 2020, the Company entered into an employment agreement with David L. Tousley in connection with his appointment as the Company’s Chief Accounting and Administrative Officer, Corporate Secretary and Treasurer (the “Tousley Agreement”). The Tousley Agreement provides for an initial annual base salary for Mr. Tousley of $375,000 as well as eligibility for an annual bonus targeted at 40% of his base salary. In connection with his appointment, Mr. Tousley will be entitled to receive stock options to purchase 313,500 shares of the Company’s common stock within three business days following the Effective Date of the 2020 Equity Plan. Mr. Tousley is entitled to participate in the Company’s benefit plans available to other executives.

| 18 |

Under the Tousley Agreement, Mr. Tousley is entitled to receive certain benefits upon termination of employment under certain circumstances. If the Company terminates Mr. Tousley’s employment for any reason other than “Cause”, or if Mr. Tousley resigns for “Good Reason” (each as such term is defined in the Agreement), Mr. Tousley will receive twelve months of base salary then in effect and the amount of the actual bonus earned by Mr. Tousley under the Tousley Agreement for the year prior to the year of termination, pro-rated based on the portion of the year Mr. Tousley was employed by the Company during the year of termination, or if no bonus had been received, at minimum 50% of his target bonus.

The Tousley Agreement additionally provides that if Mr. Tousley resigns for Good Reason or the Company or its successor terminates his employment within the three month period prior to and the two year period following a change in control (as such term is defined in the Tousley Agreement), the Company must pay or cause its successor to pay Mr. Tousley a lump sum cash payment equal to one times (a) his annual salary as of the day before his resignation or termination plus (b) the aggregate bonus received by Mr. Tousley for the year immediately preceding the change in control or, if no bonus had been received, at minimum 50% of the target bonus. In addition, upon such a resignation or termination, all outstanding stock options held by Mr. Tousley will immediately vest and become exercisable.

Appointment of Dr. Chappell as Chief Scientific Officer

On July 6, 2020, the Company entered into an employment agreement with Dale Chappell in connection with his appointment as the Company’s Chief Scientific Officer (the “Chappell Agreement”). The Chappell Agreement provides for an initial annual base salary for Dr. Chappell of $410,000 as well as eligibility for an annual bonus targeted at 40% of his base salary. In connection with his appointment, Dr. Chappell will be entitled to receive stock options to purchase 668,800 shares of the Company’s common stock within three business days following the Effective Date of the 2020 Equity Plan. Dr. Chappell is entitled to participate in the Company’s benefit plans available to other executives.

Under the Chappell Agreement, Dr. Chappell is entitled to receive certain benefits upon termination of employment under certain circumstances. If the Company terminates Dr. Chappell employment for any reason other than “Cause”, or if Dr. Chappell resigns for “Good Reason” (each as such term is defined in the Chappell Agreement), Dr. Chappell will receive twelve months of base salary then in effect and the amount of the actual bonus earned by Dr. Chappell under the Chappell Agreement for the year prior to the year of termination, pro-rated based on the portion of the year Dr. Chappell was employed by the Company during the year of termination, or if no bonus had been received, at minimum 50% of his target bonus.

The Chappell Agreement additionally provides that if Dr. Chappell resigns for Good Reason or the Company or its successor terminates his employment within the three month period prior to and the two year period following a change in control (as such term is defined in the Chappell Agreement), the Company must pay or cause its successor to pay Dr. Chappell a lump sum cash payment equal to one times (a) his annual salary as of the day before his resignation or termination plus (b) the aggregate bonus received by Dr. Chappell for the year immediately preceding the change in control or, if no bonus had been received, at minimum 50% of the target bonus. In addition, upon such a resignation or termination, all outstanding stock options held by Dr. Chappell will immediately vest and become exercisable.

Appointment of Mr. Morris as Chief Financial Officer and Chief Operating Officer

On August 3, 2020, the Company announced the appointment of Timothy Morris as the Company’s Chief Operating Officer and Chief Financial Officer. In connection with his appointment as COO and CFO, Mr. Morris stepped down as a member of the Board, a position he had held since June 2016, and the size of the Board was reduced to five members.

The Company entered into an employment agreement with Mr. Morris in connection with his appointment (the “Morris Agreement”). The Morris Agreement provides for an initial annual base salary for Mr. Morris of $475,000 as well as eligibility for an annual bonus targeted at 50% of his base salary. In connection with his appointment, Mr. Morris will be entitled to receive stock options to purchase 756,580 shares of the Company’s common stock within three business days following the effective date of the Humanigen, Inc. 2020 Omnibus Incentive Compensation Plan. Mr. Morris is entitled to participate in the Company’s benefit plans available to other executives.

| 19 |

Under the Morris Agreement, Mr. Morris is entitled to receive certain benefits upon termination of employment under certain circumstances. If the Company terminates Mr. Morris’s employment for any reason other than “Cause”, or if Mr. Morris resigns for “Good Reason” (each as such term is defined in the Morris Agreement), Mr. Morris will receive his annual salary and the amount of the actual bonus earned by Mr. Morris under the Agreement for the year prior to the year of termination, pro-rated based on the portion of the year Mr. Morris was employed by the Company during the year of termination, or if no bonus had been received, 50% of his target bonus. In addition, upon such a resignation or termination, Mr. Morris will also be entitled to be reimbursed for certain monthly health plan continuation premiums for up to 12 months, and all outstanding stock options held by Mr. Morris will immediately vest and become exercisable.

The Morris Agreement additionally provides that if Mr. Morris resigns for Good Reason or the Company terminates his employment other than for Cause within the three month period prior to or the two year period following a change in control (as such term is defined in the Morris Agreement), the Company must pay or cause its successor to pay Mr. Morris a lump sum cash payment equal to one and one-half times (a) his annual salary plus (b) the aggregate bonus received by Mr. Morris for the year immediately preceding the change in control or, if no bonus had been received, 50% of the target bonus. In addition, upon such a resignation or termination, Mr. Morris will also be entitled to be reimbursed for certain monthly health plan continuation premiums for up to 18 months, and all outstanding stock options held by Mr. Morris will immediately vest and become exercisable.

Clinical Trial Agreement with the National Institute of Allergy and Infectious Diseases

On July 24, 2020, the Company entered into a clinical trial agreement (the “Clinical Trial Agreement”) with the National Institute of Allergy and Infectious Diseases (“NIAID”), part of the National Institutes of Health, which is part of the United States Government Department of Health and Human Services, as represented by the Division of Microbiology and Infectious Diseases. Pursuant to the Clinical Trial Agreement, lenzilumab will be an agent to be evaluated in the NIAID-sponsored Big Effect Trial (“BET”) in hospitalized patients with COVID-19.

BET will evaluate the combination of lenzilumab and Gilead’s investigational antiviral, remdesivir, on treatment outcomes versus placebo and remdesivir in hospitalized COVID-19 patients. The trial is expected to enroll 100 patients in each arm of the study with an interim analysis for efficacy after 50 patients have been enrolled in each arm.

Pursuant to the Clinical Trial Agreement, NIAID will serve as sponsor and will be responsible for supervising and overseeing BET. The Company will be responsible for providing lenzilumab to NIAID without charge and in quantities to ensure a sufficient supply of lenzilumab. The Clinical Trial Agreement imposes additional obligations on the Company that are reasonable and customary for clinical trial agreements of this nature, including in respect of compliance with data privacy laws and potential indemnification obligations.

Stockholder Action by Written Consent

On July 27, 2020, the Board unanimously approved and recommended, and on July 29, 2020, certain stockholders of the Company (the “Consenting Stockholders”) owning as of July 29, 2020 (the “Record Date”) approximately 63% of the Company's outstanding common stock, par value $0.001 per share (“common stock”), approved the following actions (each, an “Action” and collectively, the “Actions”) by written consent in lieu of a special meeting, in accordance with the applicable provisions of the Delaware General Corporation Law, the Company’s Amended and Restated Certificate of Incorporation, as amended (the “Charter”), and the Company’s Second Amended and Restated Bylaws:

| 1. | The approval of an amendment to Article IV of the Charter to increase the number of authorized shares of common stock from 225,000,000 to 750,000,000; |

| 2. | The approval of an amendment to Article IV of the Charter that will give the Board the discretion, until July 29, 2021, to effect a reverse stock split whereby each outstanding 2, 3, 4, 5, 6, 7, 8, 9 or 10 shares of our common stock may be combined, converted and changed into one share of common stock, with the final ratio (if any) as may be determined by and subject to final approval of the Board; and |

| 3. | The approval of the 2020 Equity Plan. |

The Company will prepare and cause to be sent or delivered to its stockholders of record as of the Record Date pursuant to Regulation 14C under the Securities Exchange Act of 1934 an information statement relating to the Actions (the “Information Statement”). In accordance with the rules and regulations of the Securities and Exchange Commission, the Actions will not become effective until at least 20 calendar days after we send the Information Statement to such stockholders. Furthermore, the Board retains sole discretion to implement or abandon a reverse stock split, based on its determination of whether effecting a reverse stock split is advisable and in the best interests of the Company and its stockholders. Therefore, a reverse stock split may not occur without further stockholder action, notwithstanding the approval provided by the Consenting Stockholders.

| 20 |

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations. |