Attached files

| file | filename |

|---|---|

| 8-K - CURRENT REPORT - Vertex Energy Inc. | vtnr-8k_030420.htm |

| EX-99.1 - PRESS RELEASE OF VERTEX ENERGY, INC. - Vertex Energy Inc. | ex99-1.htm |

Exhibit 99.2

March 4, 2020 4Q19 Conference Call

Disclaimer This document may contain forward - looking statements including words such as “may,” “can,” “could,” “should,” “predict,” “aim,” “potential,” “continue,” “opportunity,” “intend,” “goal,” “estimate,” “expect,” “expectations,” “project,” “projections,” “plans,” “anticipates,” “believe,” “think,” “confident,” “scheduled,” or similar expressions, as well as information about management’s view of Vertex Energy’s future expectations, plans and prospects, within the safe harbor provisions under Private Securities Litigation Reform Act of 1995 . These statements involve known and unknown risks, uncertainties and other factors which may cause the results of Vertex Energy, its divisions and concepts to be materially different than those expressed or implied in such statements . These risk factors and others are included from time to time in documents Vertex Energy files with the Securities and Exchange Commission, including, but not limited to, its Form 10 - Ks, Form 10 - Qs and Form 8 - Ks , available at the SEC’s website at www . sec . gov . Other unknown or unpredictable factors also could have material adverse effects on Vertex Energy’s future results . The forward - looking statements included in this presentation are made only as of the date hereof . Vertex Energy cannot guarantee future results, levels of activity, performance or achievements . Accordingly, you should not place undue reliance on these forward - looking statements . Finally, Vertex Energy undertakes no obligation to update these statements after the date of this presentation, except as required by law, and also undertakes no obligation to update or correct information prepared by third parties that are not paid for by Vertex Energy . Industry Information Information regarding market and industry statistics contained in this presentation is based on information available to us that we believe is accurate . It is generally based on publications that are not produced for investment or economic analysis . 2

4Q19 RESULTS SUMMARY

Fourth Quarter 2019 Executive Summary 4 1 4 6 5 We exceeded the midpoint of fourth quarter Adj. EBITDA guidance by more than 40% 1 IMO 2020 product spread thesis unfolded as expected, positioning us to capitalize on improved realized margins 2 Strong performance at Marrero refinery driven by increased marine fuel sales and higher realized margins 3 Announced Bunker One USA supply - offtake agreement – anticipated pathway toward sustained profitable growth 4 Improved performance at Heartland refinery driven by increased demand for high - purity base oils 5 Pro - forma for Tensile Capital transaction, net cash positive as of 12/31/19 6

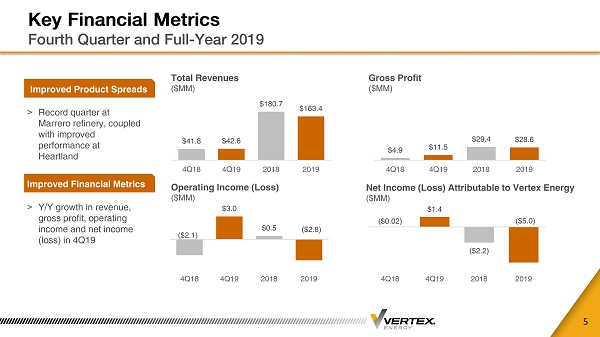

Key Financial Metrics Fourth Quarter and Full - Year 2019 5 Total Revenues ($MM) Gross Profit ($MM) Operating Income (Loss) ($MM) Net Income (Loss) Attributable to Vertex Energy ($MM) > Record quarter at Marrero refinery, coupled with improved performance at Heartland Improved Product Spreads $41.8 $42.6 $180.7 $163.4 4Q18 4Q19 2018 2019 $4.9 $11.5 $29.4 $28.6 4Q18 4Q19 2018 2019 ($2.1) $3.0 $0.5 ($2.8) 4Q18 4Q19 2018 2019 > Y/Y growth in revenue, gross profit, operating income and net income (loss) in 4Q19 Improved Financial Metrics ($0.02) $1.4 ($2.2) ($5.0) 4Q18 4Q19 2018 2019

Key Financial Metrics Fourth Quarter and Full - Year 2019 6 Adjusted EBITDA ($MM) Free Cash Flow (1) ($MM) > Using free cash flow to invest in organic and inorganic growth opportunities, while maintaining a conservative net leverage profile; priority #1 UMO collections growth Capital Allocation (1) Free cash flow defined as Adjusted EBITDA less total capital expenditures in the period > IMO 2020 thesis unfolded as planned, resulting in y/y growth in EBITDA during 4Q19, as planned Strong 4Q19 Results ($1.6) $3.8 $7.3 $7.4 4Q18 4Q19 2018 2019 ($2.3) $3.4 $4.8 $3.4 4Q18 4Q19 2018 2019

Elevated Utilization at Both Marrero and Heartland Increased Sales of Middle Distillates and High Purity Base Oils 7 (1) Utilization defined as total refinery throughputs divided by nameplate capacity of the refinery Marrero Refinery Capacity Utilization Rate (1) > Incentivized to run at max capacity, given IMO - related widening in WTI - HSFO spreads Marrero Update Heartland Refinery Capacity Utilization Rate (1) 92% 98% 100% 91% 97% 95% 4Q17 4Q18 4Q19 2017 2018 2019 95% 109% 103% 67% 99% 101% 4Q17 4Q18 4Q19 2017 2018 2019 > Focused on producing increased volumes of high - purity base oils; focused on completing more than 30% expansion of the refinery by 2023 Heartland Update

Multi - Year Growth In Direct Collections Increased Weighting Toward Direct Collections 8 Growth In Direct Collections Reduced reliance on third - party supplies (UMO Gallons in Millions) 21.1 20.3 26.2 30.6 37.0 2015 2016 2017 2018 2019 > Total collections growth increased more than 20% y/y to 37.0 million gallons Collections Growth Higher Mix Of Direct Collections Direct collections as a percentage of total UMO volumes processed at the Marrero and Heartland refineries 32% 30% 33% 36% 45% 2015 2016 2017 2018 2019 > Nearly half of all collections are now direct, removing reliance on third - party supply Supply Mix Shift

Bridging To Improved Performance Balanced Benefit From Both Improved Sales Volumes, Wider Product Spreads 9 4Q18 vs. 4Q19 Adj. EBITDA Bridge Improved volume and margin at Marrero, plus improved volume at Heartland $3.9

MANAGEMENT OUTLOOK

Product Spreads Reverting Back Toward Long - Term Average High Sulfur Fuel Oil Continues To Trade At a Discount Below WTI NYMEX 11 USGC 3% High Sulfur Fuel Oil Less West Texas Intermediate Crude Oil ($/Barrel) High Sulfur Fuel Oil Has Been a Proxy for Used Motor Oil Pricing Source: Platts, company research; dates as of 3/2/20; orange bars are actuals; grey bars are the futures strip as of 3/2/20 4Q19 Avg: ($16) 1Q20 Avg: ($8) 2Q20 Avg: ($6) 4Q20 Avg: ($9) 3Q20 Avg: ($7) ($11) ($20) ($18) ($14) ($6) ($5) ($6) ($6) ($7) ($7) ($7) ($8) ($8) ($9) ($9) ($9) ($9) ($9) Oct-19 Nov-19 Dec-19 Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20 Jan-21 Feb-21 Mar-21 1Q21 Avg: ($9)

HSFO Has Not Tracked WTI Lower on a YTD 2020 Basis Seeing a Material Narrowing In 1Q20 Product Spreads vs. 4Q19 Levels 12 Absolute Price of West Texas Intermediate Crude Oil, High - Sulfur Fuel Oil and Ultra - Low Sulfur Diesel Oct - 19 to Feb - 20 Actuals; Mar - 20 to Jun - 20 Futures Strip ($ per barrel) $0.00 $10.00 $20.00 $30.00 $40.00 $50.00 $60.00 $70.00 $80.00 $90.00 Oct-19 Nov-19 Dec-19 Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Platts WTI Platts HSFO Platts ULSD

APPENDIX

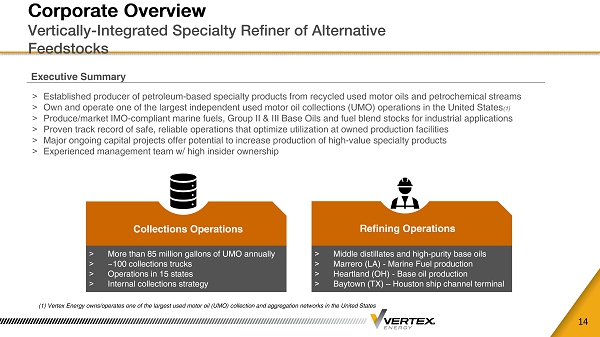

Corporate Overview Vertically - Integrated Specialty Refiner of Alternative Feedstocks 14 > More than 85 million gallons of UMO annually > ~100 collections trucks > Operations in 15 states > Internal collections strategy Collections Operations > Middle distillates and high - purity base oils > Marrero (LA) - Marine Fuel production > Heartland (OH) - Base oil production > Baytown (TX) – Houston ship channel terminal Refining Operations Executive Summary > Established producer of petroleum - based specialty products from recycled used motor oils and petrochemical streams > Own and operate one of the largest independent used motor oil collections (UMO) operations in the United States (1) > Produce/market IMO - compliant marine fuels, Group II & III Base Oils and fuel blend stocks for industrial applications > Proven track record of safe, reliable operations that optimize utilization at owned production facilities > Major ongoing capital projects offer potential to increase production of high - value specialty products > Experienced management team w/ high insider ownership (1) Vertex Energy owns/operates one of the largest used motor oil (UMO) collection and aggregation networks in the United Sta tes

Used Motor Oil Recycling Value Chain Direct and Third - Party UMO Collections Used As Refining Feedstock 15 UMO Generators Collectors Aggregators Processors Consumers Oil Change Shops, Car Dealerships 1.3 billion gal/ yr U.S. – fragmented industry Collect UMO to self - process or for sale Refined into higher - value finished products Consume middle distillates, base oils

We Own Advantaged Refining Assets In Strategic Markets Vertically Integrated Model Processes Collected UMO as Feedstock 16 > 4,800 bpd nameplate capacity > Feedstock: UMO > Production: Middle distillates > Opportunity: Demand for IMO - compliant marine fuel Marrero Refinery Marrero, Louisiana > 1,500 bpd nameplate capacity > Feedstock: UMO > Production: Group II+ base oil > Opportunity: Global transition to higher - purity base oils Heartland Refinery Columbus, Ohio > Waterfront facility w/ 100,000 barrels of storage on - site > Refining supply / distribution > Strategically located on the Houston ship channel Baytown Terminal Baytown, Texas Refining Operations Overview > Direct and third - party collections of UMO provide the feedstock for both Marrero and Heartland > Marrero and Heartland operating near peak utilization given strong demand for middle distillates and Group II base oils > Production slate includes middle distillates, base oils, asphalt, condensate and fuel oil

We Are Focused On High - Grading Our Production Slate Multi - Year Transition From Commodity To Branded Products 17 Realized Gross Margin Capture Product Portfolio Evolution Commodity Products Specialty Products Vacuum Gas Oil IMO Marine Fuels High Purity Base Oils Niche Lubricants

CAFE Standards Drive Demand For Higher Purity Base Oils Corporate Average Fleet Economy (CAFE) Standard Requires Lower Emissions 18 Executive Summary Drivers of Group II+/III Demand CAFE Standard Fuel Economy By Year 6% CAGR In Required MPG Fuel Economy > CAFE standard require increased fuel economy and lower emissions > Lower viscosity lubricants yield better fuel economy and lower emissions > High purity base oils are the primary base stock for premium synthetic lubricants used in CAFE - compliant higher performance engines > Base oil production from UMO is more efficient than from crude oil > Electrification of vehicle fleet a long - term factor, but not material to the forecast until after 2030 North American Base Oil Capacity Shift (1) Trend Toward Higher Viscosity Base Oil Capacity 2% 56% 21% 21% 6% 23% 54% 17% Re-refined Group I Group II and III Naphthenic 2008 2018 (1) Source: LNG Lubricants Industry Factbook (2018 - 2019) 35 41 55 CY 2017 CY 2021 CY 2025

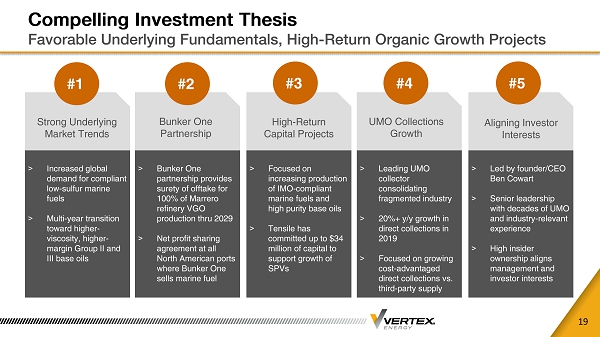

Compelling Investment Thesis Favorable Underlying Fundamentals, High - Return Organic Growth Projects 19 > Increased global demand for compliant low - sulfur marine fuels > Multi - year transition toward higher - viscosity, higher - margin Group II and III base oils Strong Underlying Market Trends > Bunker One partnership provides surety of offtake for 100% of Marrero refinery VGO production thru 2029 > Net profit sharing agreement at all North American ports where Bunker One sells marine fuel Bunker One Partnership > Leading UMO collector consolidating fragmented industry > 20%+ y/y growth in direct collections in 2019 > Focused on growing cost - advantaged direct collections vs. third - party supply UMO Collections Growth > Focused on increasing production of IMO - compliant marine fuels and high purity base oils > Tensile has committed up to $34 million of capital to support growth of SPVs High - Return Capital Projects y > Led by founder/CEO Ben Cowart > Senior leadership with decades of UMO and industry - relevant experience > High insider ownership aligns management and investor interests Aligning Investor Interests #1 #2 #3 #4 #5

TENSILE TRANSACTION OVERVIEW

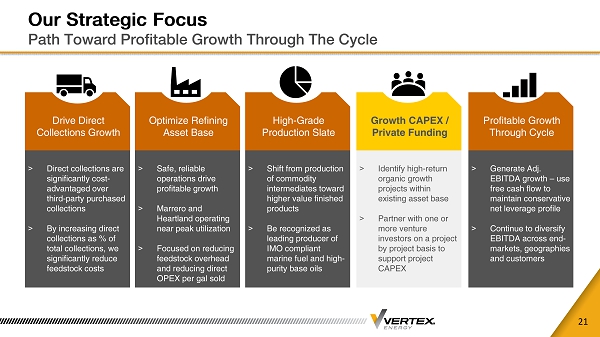

Our Strategic Focus Path Toward Profitable Growth Through The Cycle 21 > Direct collections are significantly cost - advantaged over third - party purchased collections > By increasing direct collections as % of total collections, we significantly reduce feedstock costs Drive Direct Collections Growth > Safe, reliable operations drive profitable growth > Marrero and Heartland operating near peak utilization > Focused on reducing feedstock overhead and reducing direct OPEX per gal sold Optimize Refining Asset Base > Shift from production of commodity intermediates toward higher value finished products > Be recognized as leading producer of IMO compliant marine fuel and high - purity base oils High - Grade Production Slate > Identify high - return organic growth projects within existing asset base > Partner with one or more venture investors on a project by project basis to support project CAPEX Growth CAPEX / Private Funding y > Generate Adj. EBITDA growth – use free cash flow to maintain conservative net leverage profile > Continue to diversify EBITDA across end - markets, geographies and customers Profitable Growth Through Cycle

22 Superior Project Economics Underpin Heartland Investment Anticipate 12 - 18 Month Payback Assuming Project Is On - Stream in 2023 Heartland Development Project projected to generate incremental EBITDA of $15 - $20 million in 2023 Combination of UMO Collections Growth, Refinery Optimization and Product Upgrades Drive The Model $2 million $2 to $3 million $5 to $7 million $8 to $10 million $17 to $22 million