Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - Vertex Energy Inc. | Financial_Report.xls |

| EX-31.2 - EXHIBIT 31.2 - Vertex Energy Inc. | a3312015-ex312.htm |

| EX-32.1 - EXHIBIT 32.1 - Vertex Energy Inc. | a3312015-ex321.htm |

| EX-31.1 - EXHIBIT 31.1 - Vertex Energy Inc. | a3312015-ex311.htm |

| EX-32.2 - EXHIBIT 32.2 - Vertex Energy Inc. | a3312015-ex322.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

þ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal quarter ended March 31, 2015

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE TRANSITION PERIOD FROM _____________ TO _____________

Commission File Number 001-11476

———————

VERTEX ENERGY, INC.

(Exact name of registrant as specified in its charter)

———————

NEVADA | 94-3439569 |

(State or other jurisdiction of | (I.R.S. Employer Identification No.) |

incorporation or organization) | |

1331 GEMINI STREET, SUITE 250 HOUSTON, TEXAS | 77058 |

(Address of principal executive offices) | (Zip Code) |

Registrant's telephone number, including area code: 866-660-8156

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark whether the registrant is a large accelerated filer, and accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ¨ | Accelerated filer ý |

Non-accelerated filer ¨ | Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.

Yes ¨ No ý

State the number of shares of the issuer’s common stock outstanding, as of the latest practicable date: 28,181,761 shares of common stock issued and outstanding as of May 15, 2015.

TABLE OF CONTENTS

Page | |||

PART I | |||

Item 1. | Financial Statements | ||

Consolidated Balance Sheets (unaudited) | |||

Consolidated Statements of Operations (unaudited) | |||

Consolidated Statements of Equity (unaudited) | |||

Consolidated Statements of Cash Flows (unaudited) | |||

Notes to Consolidated Financial Statements (unaudited) | |||

Item 2 | Management’s Discussion and Analysis of Financial Condition and Results of Operations | ||

Item 3. | Quantitative and Qualitative Disclosures About Market Risk | ||

Item 4. | Controls and Procedures | ||

PART II | |||

Item 1. | Legal Proceedings | ||

Item 1A. | Risk Factors | ||

Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds | ||

Item 3. | Defaults Upon Senior Securities | ||

Item 4. | Mine Safety Disclosures | ||

Item 5. | Other Information | ||

Item 6. | Exhibits | ||

PART I – FINANCIAL INFORMATION

Item 1. Financial Statements

VERTEX ENERGY, INC. | ||||||||

CONSOLIDATED BALANCE SHEETS (Unaudited) | ||||||||

March 31, 2015 | December 31, 2014 | |||||||

ASSETS | ||||||||

Current assets | ||||||||

Cash and cash equivalents | $ | 3,680,841 | $ | 6,017,076 | ||||

Accounts receivable, net | 10,855,044 | 9,936,948 | ||||||

Current portion of notes receivable | 1,000,000 | 3,150,000 | ||||||

Inventory | 11,525,259 | 12,620,616 | ||||||

Prepaid expenses | 1,109,618 | 1,245,307 | ||||||

Costs in excess of billings | — | 779,285 | ||||||

Total current assets | 28,170,762 | 33,749,232 | ||||||

Noncurrent assets | ||||||||

Fixed assets, at cost | 60,157,402 | 59,919,721 | ||||||

Less accumulated depreciation | (4,754,911 | ) | (3,758,373 | ) | ||||

Net fixed assets | 55,402,491 | 56,161,348 | ||||||

Notes receivable | 8,308,000 | 8,308,000 | ||||||

Intangible assets, net | 18,077,020 | 18,512,960 | ||||||

Goodwill | 4,922,353 | 4,922,353 | ||||||

Deferred financing cost. net | 2,067,384 | 2,191,888 | ||||||

Deferred federal income tax | — | 9,495,000 | ||||||

Other assets | 481,450 | 481,450 | ||||||

Total noncurrent assets | 89,258,698 | 100,072,999 | ||||||

TOTAL ASSETS | $ | 117,429,460 | $ | 133,822,231 | ||||

LIABILITIES AND EQUITY | ||||||||

Current liabilities | ||||||||

Accounts payable and accrued expenses | $ | 22,645,753 | $ | 21,984,136 | ||||

Capital leases | 450,871 | 492,755 | ||||||

Current portion of long-term debt | 39,860,931 | 40,136,584 | ||||||

Derivative liability | 577,440 | — | ||||||

Revolving note | 1,437,500 | — | ||||||

Deferred revenue | 2,910,940 | 463,210 | ||||||

Total current liabilities | 67,883,435 | 63,076,685 | ||||||

Long-term liabilities | ||||||||

Long-term debt | 1,735,294 | 1,867,574 | ||||||

Contingent consideration | 6,069,000 | 6,069,000 | ||||||

Deferred federal income tax | — | 4,189,000 | ||||||

Total liabilities | 75,687,729 | 75,202,259 | ||||||

Commitments and contingencies | ||||||||

EQUITY | ||||||||

Preferred stock, $0.001 par value per share: | ||||||||

50,000,000 shares authorized | ||||||||

Series A Convertible Preferred stock, $0.001 par value, | ||||||||

5,000,000 authorized and 612,943 and 630,419 issued | ||||||||

and outstanding at March 31, 2015 and December 31, | ||||||||

2014, respectively | 613 | 630 | ||||||

Common stock, $0.001 par value per share; | ||||||||

750,000,000 shares authorized; 28,125,581 and 28,108,105 | ||||||||

issued and outstanding at March 31, 2015 and | ||||||||

December 31, 2014, respectively | 28,126 | 28,109 | ||||||

Additional paid-in capital | 46,683,686 | 46,595,472 | ||||||

F-1

Retained earnings (accumulated deficit) | (4,970,694 | ) | 11,995,761 | |||||

Total Equity | $ | 41,741,731 | $ | 58,619,972 | ||||

TOTAL LIABILITIES AND EQUITY | $ | 117,429,460 | $ | 133,822,231 | ||||

See accompanying notes to the consolidated financial statements

F-2

VERTEX ENERGY, INC. | ||||||||

CONSOLIDATED STATEMENTS OF OPERATIONS | ||||||||

THREE MONTHS ENDED MARCH 31, 2015 AND 2014 | ||||||||

(UNAUDITED) | ||||||||

Three Months Ended March 31, | ||||||||

2015 | 2014 | |||||||

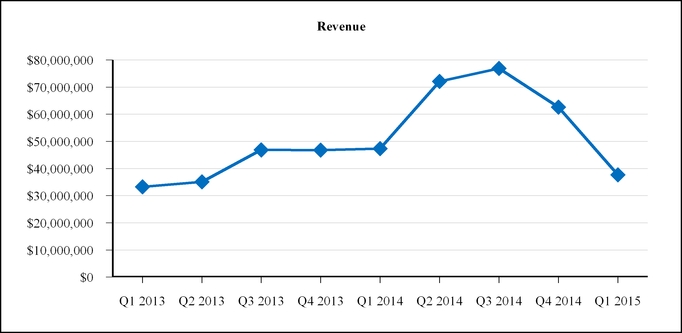

Revenues | $ | 37,684,339 | $ | 47,349,658 | ||||

Cost of revenues | 37,605,869 | 42,205,170 | ||||||

Gross profit | 78,470 | 5,144,488 | ||||||

Operating expenses: | ||||||||

Selling, general and administrative expenses (exclusive of acquisition related expenses) | 7,329,597 | 3,587,489 | ||||||

Acquisition related expenses | 157,678 | 600,412 | ||||||

Total operating expenses | 7,487,275 | 4,187,901 | ||||||

Income (loss) from operations | (7,408,805 | ) | 956,587 | |||||

Other income (expense): | ||||||||

Provision for doubtful accounts | (2,650,000 | ) | — | |||||

Other income | 8 | 370 | ||||||

Other expense | (70,478 | ) | — | |||||

Interest expense | (1,531,180 | ) | (75,811 | ) | ||||

Total other income (expense) | (4,251,650 | ) | (75,441 | ) | ||||

Income (loss) before income tax | (11,660,455 | ) | 881,146 | |||||

Income tax benefit (expense) | (5,306,000 | ) | — | |||||

Net income (loss) | $ | (16,966,455 | ) | $ | 881,146 | |||

Net loss attributable to non-controlling interest | $ | — | $ | (18,981 | ) | |||

Net income (loss) attributable to Vertex Energy, Inc. | $ | (16,966,455 | ) | $ | 862,165 | |||

Earnings (loss) per common share | ||||||||

Basic | $ | (0.60 | ) | $ | 0.04 | |||

Diluted | $ | (0.60 | ) | $ | 0.04 | |||

Shares used in computing earnings per share | ||||||||

Basic | 28,118,396 | 21,232,949 | ||||||

Diluted | 28,118,396 | 23,738,018 | ||||||

See accompanying notes to the consolidated financial statements

F-3

VERTEX ENERGY, INC. | ||||||||||||||||||||||||||||||

CONSOLIDATED STATEMENTS OF EQUITY | ||||||||||||||||||||||||||||||

FOR THE THREE MONTHS ENDED MARCH 31, 2015 | ||||||||||||||||||||||||||||||

Common Stock Shares | Common Stock $.001 Par | Series A Preferred Stock Shares | Series A Preferred Stock $.001 Par | Additional Paid-in Capital | Retained Earnings | Non-controlling Interest | Total Equity | |||||||||||||||||||||||

Balance on December 31, 2014 | 28,108,105 | $ | 28,109 | 630,419 | $ | 630 | 46,595,472 | $ | 11,995,761 | — | $ | 58,619,972 | ||||||||||||||||||

Issuance of stock options and warrants | — | — | — | — | 88,214 | — | — | 88,214 | ||||||||||||||||||||||

Conversion of preferred A stock to common | 17,476 | 17 | (17,476 | ) | (17 | ) | — | — | — | — | ||||||||||||||||||||

Net income (loss) | — | — | — | — | — | (16,966,455 | ) | — | (16,966,455 | ) | ||||||||||||||||||||

Balance on March 31, 2015 | 28,125,581 | $ | 28,126 | 612,943 | $ | 613 | $ | 46,683,686 | $ | (4,970,694 | ) | $ | — | $ | 41,741,731 | |||||||||||||||

F-4

VERTEX ENERGY, INC. | ||||||||

CONSOLIDATED STATEMENTS OF CASH FLOWS | ||||||||

THREE MONTHS ENDED MARCH, 2015 AND 2014 | ||||||||

(UNAUDITED) | ||||||||

Three Months Ended | ||||||||

March 31, 2015 | March 31, 2014 | |||||||

Cash flows from operating activities | ||||||||

Net income (loss) | $ | (16,966,455 | ) | $ | 881,146 | |||

Adjustments to reconcile net income to cash provided by operating activities | ||||||||

Stock based compensation expense | 88,214 | 51,224 | ||||||

Depreciation and amortization | 1,556,982 | 732,677 | ||||||

Payment-in-kind interest | 577,440 | — | ||||||

Gain on acquisition | — | — | ||||||

Loss on asset sale | 70,478 | — | ||||||

Deferred federal income tax | 5,306,000 | — | ||||||

Changes in operating assets and liabilities | ||||||||

Accounts receivable | (418,097 | ) | 297,587 | |||||

Allowance for doubtful accounts | 2,650,000 | — | ||||||

Inventory | 1,095,357 | 986,095 | ||||||

Prepaid expenses | (364,309 | ) | (728,644 | ) | ||||

Costs in excess of billings | 779,285 | — | ||||||

Accounts payable | 661,617 | 1,192,312 | ||||||

Deferred revenue | 2,447,730 | — | ||||||

Net cash provided by (used in) operating activities | (2,515,758 | ) | 3,412,397 | |||||

Cash flows from investing activities | ||||||||

Purchase of fixed assets | (312,659 | ) | (780,616 | ) | ||||

Proceeds from asset sales | 4,500 | — | ||||||

Net cash used in investing activities | (308,159 | ) | (780,616 | ) | ||||

Cash flows from financing activities | ||||||||

Proceeds from sale of stock | — | (3,500 | ) | |||||

Proceeds from note payable | — | 351,921 | ||||||

Proceeds from revolving note | 1,437,500 | — | ||||||

Origination of note payable | (449,818 | ) | (666,386 | ) | ||||

Notes receivable | (500,000 | ) | — | |||||

Proceeds from exercise of common stock options and warrants | — | 24,000 | ||||||

Net cash provided by (used in) financing activities | 487,682 | (293,965 | ) | |||||

Net change in cash and cash equivalents | (2,336,235 | ) | 2,337,816 | |||||

Cash and cash equivalents at beginning of the period | 6,017,076 | 2,678,628 | ||||||

Cash and cash equivalents at end of period | $ | 3,680,841 | $ | 5,016,444 | ||||

SUPPLEMENTAL INFORMATION | ||||||||

Cash paid for interest | $ | 953,115 | $ | 75,811 | ||||

NON-CASH INVESTING AND FINANCING TRANSACTIONS | ||||||||

Conversion of Series A Preferred Stock into common stock | $ | 17 | $ | 40 | ||||

Note payable for acquisition of E-Source interest | $ | — | $ | 854,050 | ||||

Additional paid in capital for acquisition of E-Source interest | $ | — | $ | 231,260 | ||||

See accompanying notes to the consolidated financial statements

F-5

VERTEX ENERGY, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

MARCH 31, 2015

(UNAUDITED)

NOTE 1. BASIS OF PRESENTATION AND NATURE OF OPERATIONS

The accompanying unaudited consolidated interim financial statements of Vertex Energy, Inc. (the “Company,” or “Vertex Energy”) have been prepared in accordance with accounting principles generally accepted in the United States of America and the rules of the Securities and Exchange Commission (“SEC”), and should be read in conjunction with the audited consolidated financial statements and notes thereto contained in the Company’s annual consolidated financial statements as filed with the SEC on Form 10-K/A on April 15, 2015 (the “Form 10-K”). In the opinion of management, all adjustments, consisting of normal recurring adjustments, necessary for a fair presentation of financial position and the results of operations for the interim periods presented have been reflected herein. The results of operations for interim periods are not necessarily indicative of the results to be expected for the full year. Certain prior period amounts have been reclassified to conform to current period presentation. Notes to the consolidated financial statements which would substantially duplicate the disclosure contained in the audited consolidated financial statements for the most recent fiscal year 2014 as reported in Form 10-K, have been omitted.

NOTE 2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Principles of consolidation

The consolidated financial statements include the accounts of the Company and its wholly-owned subsidiaries. All intercompany accounts and transactions have been eliminated in consolidation. The subsidiaries are as follows:

• | Cedar Marine Terminals, L.P. (“CMT”) operates a 19-acre bulk liquid storage facility on the Houston Ship Channel. The terminal serves as a truck-in, barge-out facility and provides throughput terminal operations. CMT is also the site of the Thermal Chemical Extraction Process ("TCEP"). |

• | Crossroad Carriers, L.P. (“Crossroad”) is a third-party common carrier that provides transportation and logistical services for liquid petroleum products, as well as other hazardous materials and product streams. |

• | Vertex Recovery, L.P. (“Vertex Recovery”) is a generator solutions company for the recycling and collection of used oil and oil-related residual materials from large regional and national customers throughout the U.S. It facilitates its services through a network of independent recyclers and franchise collectors. |

• | H&H Oil, L.P. (“H&H Oil”) collects and recycles used oil and residual materials from customers based in Austin, Baytown, San Antonio and Corpus Christi, Texas. |

• | E-Source Holdings, LLC (“E-Source”) provides dismantling and demolition services at industrial facilities throughout the Gulf Coast. |

• | Vertex Refining, LA, LLC is a used oil re refinery based in Marrero, Louisiana and also has assets in Belle Chasse, Louisiana. |

• | Vertex Refining, NV, LLC ("Vertex Refining") is a base oil marketing and distribution company with customers throughout the United States. |

• | Golden State Lubricant Works, LLC ("Golden State") operates an oil storage and blend facility based in Bakersfield, California. |

• | Vertex Refining, OH, LLC collects and re refines used oil and residual materials from customers throughout the Midwest. Refinery operations are based in Columbus, Ohio and has collection branches located in Norwalk, Ohio Zanesville, Ohio, Ravenswood, West Virginia, and Mt. Sterling, Kentucky. |

• | Vertex Energy Operating, LLC ("Vertex Operating"), a holding company for various of the subsidiaries described above. |

Accounts receivable

Accounts receivable represents amounts due from customers. Accounts receivable are recorded at invoiced amounts, net of reserves and allowances, and do not bear interest. The Company uses its best estimate to determine the required allowance for doubtful accounts based on a variety of factors, including the length of time receivables are past due, economic trends and conditions affecting its customer base, significant one-time events and historical write-off experience. Specific provisions are recorded for individual receivables when we become aware of a customer’s inability to meet its financial obligations. The Company reviews the adequacy of its reserves and allowances quarterly.

Receivable balances greater than 30 days past due are individually reviewed for collectability and if deemed uncollectible, are charged off against the allowance accounts after all means of collection have been exhausted and the potential for recovery is

F-6

considered remote. The Company does not have any significant off balance sheet credit exposure related to its customers. The allowance was $316,715 and $316,715 at March 31, 2015 and December 31, 2014, respectively.

Inventory

Inventories of products consist of feedstocks and refined petroleum products and are reported at the lower of cost or market. Cost is determined using the first-in, first-out (“FIFO”) method. The Company reviews its inventory commodities whenever events or circumstances indicate that the value may not be recoverable. The Company recognized an inventory impairment loss of $0 and $467,911 at March 31, 2015 and December 31, 2014, respectively.

Revenue recognition

Revenue for each of the Company’s divisions is recognized when persuasive evidence of an arrangement exists, goods are delivered, sales price is determinable, and collection is reasonably assured. Revenue is recognized upon delivery by truck and railcar of feedstock to its re-refining customers and upon product leaving the Company’s terminal facilities and third party processing facility via barge. Revenue is also recognized as recovered scrap materials are sold and projects are completed.

Income Taxes

The Company accounts for income taxes in accordance with the FASB ASC Topic 740. The Company records a valuation allowance against net deferred tax assets if, based upon the available evidence, it is more likely than not that some or all of the deferred tax assets will not be realized. The ultimate realization of deferred tax assets is dependent upon the generation of future taxable income and when temporary differences become deductible. The Company considers, among other available information, uncertainties surrounding the recoverability of deferred tax assets, scheduled reversals of deferred tax liabilities, projected future taxable income, and other matters in making this assessment.

As part of the process of preparing its consolidated financial statements, the Company is required to estimate its income taxes in each of the jurisdictions in which it operates. This process requires the Company to estimate its actual current tax liability and to assess temporary differences resulting from differing book versus tax treatment of items, such as deferred revenue, compensation and benefits expense and depreciation. These temporary differences result in deferred tax assets and liabilities, which are included within the Company’s consolidated statements of financial condition. Significant management judgment is required in determining the Company’s provision for income taxes, its deferred tax assets and liabilities and any valuation allowance recorded against its net deferred tax assets. In assessing the realization of deferred tax assets, management considers whether it is more likely than not that some portion or all of the deferred tax assets will be realized and, when necessary, valuation allowances are established. The ultimate realization of the deferred tax assets is dependent upon the generation of future taxable income during the periods in which temporary differences become deductible. Management considers the level of historical taxable income, scheduled reversals of deferred taxes, projected future taxable income and tax planning strategies that can be implemented by the Company in making this assessment. If actual results differ from these estimates or the Company adjusts these estimates in future periods, the Company may need to adjust its valuation allowance, which could materially impact the Company’s consolidated financial position and results of operations.

Tax contingencies can involve complex issues and may require an extended period of time to resolve. Changes in the level of annual pre-tax income can affect the Company’s overall effective tax rate. Significant management judgment is required in determining the Company’s provision for income taxes, its deferred tax assets and liabilities and any valuation allowance recorded against its net deferred tax assets. Furthermore, the Company’s interpretation of complex tax laws may impact its recognition and measurement of current and deferred income taxes.

The loss during the quarter ended March 31, 2015 put the Company in an accumulated loss position for the cumulative 12 quarters then ended. The Company did not have sufficient positive evidence to overcome the recent losses and determined it was more likely than not the deferred tax assets would not be realized as of March 31, 2015 and as a result the Company incurred deferred tax expense of $5,306,000 during the three month period ended March 31, 2015

Earnings per share

Diluted net income (loss) per share is computed by dividing the net income (loss) attributable to common shareholders by the weighted average number of common and common equivalent shares outstanding during the period. Common share equivalents included in the diluted computation represent shares issuable upon assumed exercise of stock options and warrants using the treasury stock and “if converted” method. For periods in which net losses are incurred, weighted average shares

F-7

outstanding is the same for basic and diluted loss per share calculations, as the inclusion of common share equivalents would have an anti-dilutive effect.

NOTE 3. GOING CONCERN

During the three month period ended March 31, 2015, an event of default occurred under our financing agreements (as described in Notes 5 and 8). Subsequent to March 31, 2015, we were able to obtain a waiver of the defaults under the credit agreements and to negotiate mutually agreed upon amendments to the credit agreements to bring the Company into compliance with such credit agreements. In the event further defaults occur under the credit agreements, the lenders may exercise any and all rights and remedies available to them under their respective agreements, including demanding immediate repayment of all amounts then outstanding or initiating foreclosure or insolvency proceedings. In the event we default upon our obligations under our credit facilities, our lenders demand repayment of such obligations and we are unable to obtain alternative financing to repay or refinance such obligations, our business will be materially and adversely affected, and we may be forced to sharply curtail or cease our operations.

These circumstances raise significant doubt as to our ability to operate as a going concern. The accompanying consolidated financial statements have been prepared on a going concern basis in in accordance with generally accepted accounting principles in the United States of America. As such, no adjustments have been made to the consolidated financial results for the recoverability of assets and classification of liabilities that might be necessary should the Company be unable to continue operating as a going concern. Recent financial performance was taken into consideration when evaluating the recoverability of our deferred tax asset (see Note 5).

NOTE 4. RELATED PARTIES

Effective October 3, 2014, the Company entered into a consulting agreement with its director, Timothy C. Harvey, pursuant to which Mr. Harvey agreed to provide consulting services to the Company in connection with overseeing the Company’s trading and selling of finished products and assisting the Company with finding the best markets for products from the Company’s facilities for a term of one year. In consideration for agreeing to provide services under the agreement, the Company agreed to pay Mr. Harvey $10,000 per month, and to grant him an option to purchase up to 75,000 shares of the Company's common stock at an exercise price of $6.615 per share, the mean between the highest and lowest quoted selling prices of the Company's common stock on October 2, 2014 (the day immediately preceding the approval by the Board of Directors of the agreement), which vest at the rate of 1/4th of such options per year, subject to Mr. Harvey’s continued consulting, employment or service as a director of the Company, which options were granted under the Company's 2013 Stock Incentive Plan.

NOTE 5. CONCENTRATIONS, SIGNIFICANT CUSTOMERS, COMMITMENTS AND CONTINGENCIES

At March 31, 2015 and 2014 and for each of the three months then ended, the Company’s revenues and receivables were comprised of the following customer concentrations:

Three months ended March 31, 2015 | Three months ended March 31, 2014 | |||||||

% of Revenues | % of Receivables | % of Revenues | % of Receivables | |||||

Customer 1 | 26% | 25% | —% | —% | ||||

Customer 2 | 14% | 13% | 21% | 17% | ||||

Customer 3 | 6% | —% | 15% | 9% | ||||

Customer 4 | 1% | —% | 42% | 32% | ||||

At March 31, 2015 and 2014 and for each of the three months then ended, the Company's segment revenues were comprised of the following customer concentrations:

% of Revenue by Segment | % Revenue by Segment | |||||||||||

Three months ended March 31, 2015 | Three months ended March 31, 2014 | |||||||||||

Black Oil | Refining | Recovery | Black Oil | Refining | Recovery | |||||||

Customer 1 | 100% | —% | —% | —% | —% | —% | ||||||

Customer 2 | 40% | 60% | —% | 79% | 21% | —% | ||||||

Customer 3 | —% | 100% | —% | —% | 100% | —% | ||||||

Customer 4 | 100% | —% | —% | 99% | —% | 1% | ||||||

The Company purchases goods and services from one company that represented 11% of total purchases for the three months ended March 31, 2015 and one company that represented 10% of total purchases for the three months ended March 31, 2014.

F-8

The Company has had various debt facilities available for use, of which there was $43,484,596 and $42,496,913 outstanding as of March 31, 2015 and December 31, 2014, respectively. See Note 8 for further details.

In February 2013, Bank of America agreed to lease the Company up to $1,025,000 of equipment to enhance the TCEP operation, which went into effect in April 2013. Under the current terms of the lease agreement, there are 60 monthly payments due of approximately $13,328.

The Company’s revenue, profitability and future rate of growth are substantially dependent on prevailing prices for petroleum-based products. Historically, the energy markets have been very volatile, and there can be no assurance that these prices will not be subject to wide fluctuations in the future. A substantial or extended decline in such prices could have a material adverse effect on the Company’s financial position, results of operations, cash flows, and access to capital and on the quantities of petroleum-based products that the Company can economically produce.

The Company, in its normal course of business, is involved in various other claims and legal action. In the opinion of management, the outcome of these claims and actions will not have a material adverse impact upon the financial position of the Company.

For tax reporting purposes, we have NOLs of approximately $36.3 million as of March 31, 2015 that are available to reduce future taxable income. In determining the carrying value of our net deferred tax asset, the company considered all negative and positive evidence. The company has incurred a cumulative pre-tax loss of $9.8 million over a three year period ended March 31, 2015. As a result, we determined that a full valuation allowance for our deferred tax assets at March 31, 2015 of $5.3 million was appropriate.

NOTE 6. ACCOUNTS RECEIVABLE

Accounts receivable, net, consists of the following at:

March 31, 2015 | December 31, 2014 | |||

Accounts receivable | $11,171,759 | $10,253,663 | ||

Allowance for doubtful accounts | (316,715) | (316,715) | ||

Accounts receivable, net | $10,855,044 | $9,936,948 | ||

Accounts receivable represents amounts due from customers. Accounts receivable are recorded at invoiced amounts, net of reserves and allowances, and do not bear interest. The Company uses its best estimate to determine the required allowance for doubtful accounts based on a variety of factors, including the length of time receivables are past due, economic trends and conditions affecting its customer base, significant one-time events and historical write-off experience. Specific provisions are recorded for individual receivables when we become aware of a customer’s inability to meet its financial obligations. The Company reviews the adequacy of its reserves and allowances quarterly.

Receivable balances greater than 30 days past due are individually reviewed for collectability and if deemed uncollectible, are charged off against the allowance accounts after all means of collection have been exhausted and the potential for recovery is considered remote. The Company does not have any significant off balance sheet credit exposure related to its customers.

F-9

NOTE 7. NOTES RECEIVABLE

Current portion of notes receivable, net, consists of the following at:

March 31, 2015 | December 31, 2014 | |||

Accounts receivable | $5,346,452 | $4,846,452 | ||

Allowance for doubtful accounts | (4,346,452) | (1,696,452) | ||

Accounts receivable, net | $1,000,000 | $3,150,000 | ||

The current portion of notes receivable represents amounts due from Omega Holdings, LLC. Of the total notes receivable balance, $1,696,452 represents invoiced amounts that do not bear interest as of March 31, 2015. Based on management's assessment, the company recognized an allowance of $1,696,452 related to the receivable. The write off was necessary because the Company's receivable was unsecured and the amount that the Company may ultimately recover, if any, is not presently determinable.

As of March 31, 2015, $3,650,000 of the current notes receivable balance represents short-term loans that carry an interest rate of 9.5% per annum. No accrued interest is included in the balance. Based on managements assessment, the company recognized an allowance of $2,650,000 during three months ended March 31, 2015. The note is collateralized by insurance proceeds expected to be collected in 2015 and the allowance was a result of revised insurance proceed expectations.

The long-term notes receivable represents amounts due from Omega Holdings, LLC. The $8,308,000 due to Vertex is based on the purchase price allocated to the Nevada facility, which has not yet closed. The note is collateralized by assets at the Nevada facility and carries an interest rate of 9.5% per annum. No accrued interest is included in the account balance. The aggregate receivable balance has been classified as noncurrent because they are not expected to be collected within one year from the balance sheet date. The note is currently in default as of March 31, 2015.

NOTE 8. LINE OF CREDIT AND LONG-TERM DEBT

In September 2012, the Company entered into a credit agreement with Bank of America. Pursuant to the agreement, Bank of America agreed to loan the Company $8,500,000 in the form of a term loan and to provide the Company with an additional $10,000,000 in the form of a revolving line of credit.

In May 2014, the Company entered into an amended and restated credit agreement with Bank of America. The amended credit agreement amended and restated the prior credit agreement entered into with Bank of America in September 2012. Pursuant to the agreement, Bank of America agreed to loan the Company up to $20,000,000 in the form of a revolving line of credit, subject to certain terms and lending ratios, to be used for feedstock purchases and general corporate purposes. The line of credit bears interest at the option of the Company of either the lender's prime commercial lending rate then in effect between 1.25% and 2% per annum or the Bank of America LIBOR rate plus between 2.35% and 3% (both ranges dependent upon the Company's leverage ratio from time to time). Accrued and unpaid interest on the revolving note is due and payable monthly in arrears and all amounts outstanding under the revolving note are due and payable on May 2, 2017. The balance on the revolving line of credit was $0 at March 31, 2015.

The financing arrangement discussed above is secured by a first priority security interest in all of the assets and securities of our direct and indirect subsidiaries other than E-Source. The loan includes various covenants binding upon the Company, including, requiring that the Company comply with certain reporting requirements, provide notices of material corporate events and forecasts to Bank of America, and maintain certain financial ratios relating to debt leverage, consolidated EBITDA, maximum debt exposure, and minimum liquidity, including maintaining a ratio of quarterly consolidated EBITDA to certain fixed charges.

On May 2, 2014, the Company entered into a Credit and Guaranty Agreement with Goldman Sachs Bank USA. Pursuant to the agreement, Goldman Sachs Bank USA loaned the Company $40,000,000 in the form of a term loan. As set forth in the Credit Agreement, the Company has the option to select whether loans made under the Credit Agreement bear interest at (a) the greater of (i) the prime rate in effect, (ii) the weighted average of the rates on overnight Federal funds transactions with members of the Federal Reserve System plus ½ of 1%, (iii) the sum of (A) the Adjusted LIBOR Rate and (B) 1%, and (iv) 4.5% per annum; or (b) the greater of (i) 1.50% and (ii) the applicable ICE Benchmark Administration Limited interest rate, divided by (x) one minus, (y) the Adjusted LIBOR Rate. Interest on the Credit Agreement is payable monthly in arrears. Amortizing principal payments are due on the Credit Agreement Loan in the amount of $300,000 per fiscal quarter for June 30, 2014, September 30, 2014, December 31, 2014 and March 31, 2015, and $800,000 per fiscal quarter thereafter until maturity on May 2, 2019. The balance on the term loan was $39,100,000 at March 31, 2015.

F-10

The Goldman Sachs Bank USA financing arrangement is secured by all of the assets of the Company, but subordinate to the aforementioned Bank of America credit agreement. Amounts outstanding under this agreement have been recorded as current on the March 31, 2015 balance sheet.

On March 26, 2015, we, Vertex Operating, and substantially all of our other subsidiaries (other than E-Source), Goldman Sachs Specialty Lending Holdings, Inc. (“Lender”) and Goldman Sachs Bank USA, as Administrative Agent and Collateral Agent for Lender (“Agent”), entered into a Second Amendment to Credit and Guaranty Agreement (the “Second Amendment”). The Second Amendment amended that certain Credit and Guaranty Agreement entered into between the parties dated as of May 2, 2014 and amended by the First Amendment to Credit and Guaranty Agreement entered into on December 5, 2014 (the “First Amendment” and the Credit and Guaranty Agreement as amended and modified by the First Amendment and Second Amendment, the “Credit Agreement”).

During the third quarter of 2014, various events of default had occurred and were continuing under the Credit Agreement and the parties entered into the Second Amendment to among other things, provide for the waiver of the prior defaults and to restructure certain covenants and other financial requirements of the Credit Agreement and to allow for our entry into the MidCap Loan Agreement (described below).

The amendments to the Credit Agreement effected by the Second Amendment include, but are not limited to:

• | Effecting various amendments to the Credit Agreement to substitute the name of MidCap Business Credit, LLC and the MidCap Loan Agreement (as described below) in place of Bank of America, NA (“BOA”), and the Company’s prior Credit Agreement with BOA. |

• | Increasing the interest rate of certain outstanding loans made under the terms of the Credit Agreement by up to 2% per annum, based on the leverage ratio of debt to consolidated EBITDA of the Company. |

• | Changing the calculation dates for certain fixed charge ratios required to be calculated pursuant to the terms of the Credit Agreement. |

• | Changing how certain debt leverage ratios are calculated under the terms of the Credit Agreement. |

• | Increasing the additional default interest payable upon the occurrence of an event of default under the Credit Agreement to 4% per annum (compared to 2% per annum for all other defaults) above the then applicable interest rate in the event we fail to make the Required Prepayment (as defined below). |

• | Providing that no quarterly amortization payments would be due under the terms of the Credit Agreement for the quarters ended March 31, 2015 and June 30, 2015 (previously amortization payments of $800,000 per quarter were due for both such quarters). |

• | Providing that we are not required to meet certain debt and leverage covenants for certain periods of fiscal 2015. |

• | Requiring that we raise at least $9.1 million by June 30, 2015 through the sale of equity, and that we are required to pay such funds directly to the Lender as a mandatory pre-payment of the amounts outstanding under the Credit Agreement (the “Required Payment”). |

• | Changing certain of the required prepayment terms of the Credit Agreement, which require us to prepay the amounts owed under the Credit Agreement in an amount equal to 100% of the extent total consolidated debt exceeds (x) total consolidated EBITDA (as calculated pursuant to the agreement) multiplied by (y) the maximum debt leverage ratios described in the Credit Agreement, provided that no prepayments in connection with such requirements are required to be made through December 31, 2015. |

• | Reducing the amount of allowable additional borrowings we can make under other debt agreements and facilities to $7 million in aggregate (including not more than $6 million under the MidCap Loan Agreement through December 31, 2015). |

• | Changing certain fixed charge, leverage ratios and consolidated EBITDA calculations, definitions, and requirements relating to covenants under the Credit Agreement. |

F-11

• | Changing the required amount of cash on hand and available borrowings under the MidCap Loan Agreement, We, are required to have at least (a)$750,000 after the date of the Second Amendment and prior to June 30, 2015, (b) $1.5 million at any time after June 30, 2015 and prior to December 31, 2015, (c) $2 million at any time after December 31, 2015 and prior to June 30, 2016, (d) $2.5 million at any time after June 30, 2016 and prior to December 31, 2016, and (e) $3 million at any time after December 31, 2016. |

The Lender also waived all of the prior defaults which the Lender had provided the Company notice of previously (which were all of the known defaults that existed at the time of the parties’ entry into the Second Amendment) and the Company and its subsidiaries provided a release in favor of the Lender and its representatives and assigns. We also agreed to pay the Agent a fee of $50,000 per year (including $50,000 paid upon our entry into the Second Amendment) as an administration fee; and pay the Agent certain prepayment fees in the event we prepay amounts outstanding under the Credit Agreement prior to March 26, 2018, provided no prepayment fee is due in connection with the Required Payment or certain other mandatory prepayments required under the terms of the Credit Agreement, subject to certain exceptions.

As additional consideration for the Lender agreeing to the terms of the Second Amendment, we granted Goldman, Sachs & Co., an affiliate of the Lender (such initial holder and its assigns, if any, the “Holder”) a warrant to purchase 1,766,874 shares of our common stock which was evidenced by a Common Stock Purchase Warrant (the “Lender Warrant”). The Lender Warrant expires on March 26, 2022 and has an exercise price equal to the lower of (x) $3.39583 per share; and (y) the lowest price per share at which we issue any common stock (or sets an exercise price for the purchase of common stock) between the date of our entry into the Lender Warrant and June 30, 2015. The Lender Warrant can be exercised by the Holder at any time after September 1, 2015, including pursuant to a cashless exercise. The Lender Warrant contains standard adjustment provisions in the event of stock splits, combinations, rights offerings, combinations and similar transactions. We are required to provide the Holder notice of certain corporate actions pursuant to the terms of the Lender Warrant. In the event that, prior to June 30, 2015, we prepay the amount owed under the Credit Agreement in an amount greater than $9.1 million (i.e., in an amount greater than the Required Payment) then the number of shares of common stock issuable upon exercise of the Lender Warrant is reduced by the pro rata amount by which the amount prepaid exceeds $9.1 million and is less than $15.1 million, provided that if prior to June 30, 2015 we prepay at least $6 million in addition to the Required Payment (i.e., we prepay at least $15.1 million of the amount owed under the Credit Agreement by June 30, 2015) the Lender Warrant automatically terminates and the Holder has no rights under such Lender Warrant. The Lender Warrant includes piggy-back registration rights (subject to certain exceptions) beginning after September 1, 2015. Additionally, beginning September 1, 2015, the Holder (subject to the terms of the Lender Warrant) can demand that we register the shares of common stock issuable upon exercise of the Lender Warrant in the event the Holder is unable to rely on Rule 144 of the Securities Act of 1933, as amended, which demand rights require that we file and obtain effectiveness of the applicable registration statement within 90 days after such demand (or 120 days after such demand in the event of a “full review” by the Securities and Exchange Commission), provided that if we are unable to meet the deadlines above, we are required to pay to the Holder on the first business day after the 90- or 120-day period, as applicable, and each 30th day thereafter (pro rata for any period of less than 30 days) until the registration statement is effective, an amount of damages equal to one percent (1%) of the exercise price of the Lender Warrant multiplied by the aggregate of (i) the total number of shares of common stock then issuable upon exercise of the Lender Warrant; and (ii) any previously exercised shares not sold by the Holder (the “Warrant Damages”). In the event any registration statement is declared effective and thereafter the Board of Directors determines in good faith that the use of the registration statement should be suspended, and any suspension or suspensions exist for more than 30 days in a row or 45 days in any year, Warrant Damages are payable to the Holder on each 30th day thereafter (pro rata for any period of less than 30 days), provided that no suspension shall continue for more than 90 days without the prior written consent of the Holder. The Lender Warrant also included standard indemnification rights and requirements for us to continue filing reports with the SEC in order for the Holder to use Rule 144 of the Securities Act of 1933, as amended, for the sale of the shares of common stock issuable upon exercise of the Lender Warrant.

On May 2, 2014, in connection with the closing of the Omega Refining acquisition, the Company assumed two capital leases totaling $3,154,860. Payments of $2,703,989 were made and the balance was $450,871 at March 31, 2015.

The Company financed insurance premiums through various financial institutions bearing interest rates from 4% to 4.52%. All such premium finance agreements have maturities of less than one year and have a balance of $299,316 at March 31, 2015.

Effective March 27, 2015, the Company, Vertex Operating and all of the Company’s other subsidiaries other than E-Source and Golden State, entered into a Loan and Security Agreement with MidCap Business Credit LLC (“MidCap” and the “MidCap Loan Agreement”). Pursuant to the MidCap Loan Agreement, MidCap agreed to loan us up to the lesser of (i) $7 million; and (ii) 85% of the amount of accounts receivable due to us which meet certain requirements set forth in the MidCap Loan Agreement (“Qualified Accounts”), plus the lesser of (y) $3 million and (z) 50% of the cost or market value, whichever is lower, of our raw material and

F-12

finished goods which have not yet been sold, subject to the terms and conditions of the MidCap Loan Agreement (“Eligible Inventory”), minus any amount which MidCap may require from time to time in order to over secure amounts owed to MidCap under the MidCap Loan Agreement, as long as no event of default has occurred or is continuing under the terms of the MidCap Loan Agreement. The requirement of MidCap to make loans under the MidCap Loan Agreement is subject to certain standard conditions and requirements.

The MidCap Loan Agreement contains customary representations, warranties, covenants, and events of default for facilities of similar nature and size as the MidCap Loan Agreement, and requirements for the Company to indemnify MidCap for certain losses.

We also entered into a Revolving Note (the “MidCap Note”) to evidence amounts borrowed from MidCap from time to time under the MidCap Loan Agreement. Interest on the MidCap Note accrues at a fluctuating rate equal to the aggregate of: (x) the prime rate then in effect, and (y) 1.75% per annum, or at such other rate mutually agreed on from time to time by the parties, based upon the greater of (i) any balance owing under the MidCap Note at the close of each day; or (ii) a minimum assumed average daily loan balance of $3 million. Interest is payable in arrears, on the first day of each month that amounts are outstanding under the MidCap Note. The balance on the revolving note was $1,437,500 at March 31, 2015.

On January 7, 2015, E-Source entered into a loan agreement with Texas Citizens Bank to consolidate various smaller debt obligations. The loan Agreement provides a term note in the amount of $2,201,372 that matures on January 7, 2020. Borrowings bear a fixed interest rate of 5.5% per annum and interest will be calculated from the date of each advance until repayment in full or maturity. The loan has 59 scheduled monthly payments of $42,126 which includes principal and interest. The loan is collateralized by all of the assets of E-Source. The balance on the term note was $2,131,326 at March 31, 2015

The Company's outstanding debt facilities as of March 31, 2015 are summarized as follows:

Creditor | Loan Type | Origination Date | Maturity Date | Loan Amount | Balance on March 31, 2015 | |||||||||

MidCap Business Credit, LLC | Revolving Note | March, 2015 | March, 2017 | $ | 7,000,000 | $ | 1,437,500 | |||||||

Goldman Sachs USA | Term Loan | May, 2014 | May, 2019 | 40,000,000 | 39,100,000 | |||||||||

Pacific Western Bank | Capital Lease | September, 2012 | August, 2017 | 520,219 | 450,871 | |||||||||

Texas Citizens Bank | Term Note | January, 2015 | January, 2020 | 2,201,372 | 2,131,326 | |||||||||

Ally | Auto Loan | September, 2013 | September, 2018 | 87,772 | 65,583 | |||||||||

Various institutions | Insurance premiums financed | Various | < 1 year | 1,789,481 | 299,316 | |||||||||

$ | 51,598,844 | $ | 43,484,596 | |||||||||||

Future contractual maturities of notes payable are summarized as follows:

Creditor | 2015 | 2016 | 2017 | 2018 | 2019 | Thereafter | ||||||||||||||||||

MidCap Business Credit, LLC | $ | 1,437,500 | $ | — | $ | — | $ | — | $ | — | $ | — | ||||||||||||

Goldman Sachs USA | 39,100,000 | — | — | — | — | — | ||||||||||||||||||

Pacific Western Bank | 130,769 | 186,947 | 133,154 | — | — | — | ||||||||||||||||||

Texas Citizens Bank | 289,309 | 412,986 | 436,896 | 461,892 | 488,317 | 41,927 | ||||||||||||||||||

Ally | 65,583 | — | — | — | — | — | ||||||||||||||||||

Various institutions | 299,316 | — | — | — | — | — | ||||||||||||||||||

Totals | $ | 41,322,477 | $ | 599,933 | $ | 570,050 | $ | 461,892 | $ | 488,317 | $ | 41,927 | ||||||||||||

NOTE 9. EARNINGS PER SHARE

Basic earnings per share includes no dilution and is computed by dividing income available to common shareholders by the weighted average number of common shares outstanding for the periods presented. The calculation of basic earnings per share for the three months ended March 31, 2015 includes the weighted average of common shares outstanding. Diluted earnings per share

F-13

reflect the potential dilution of securities that could share in the earnings of an entity, such as convertible preferred stock, stock options, warrants or convertible securities. The calculation of diluted earnings per share for the three months ended March 31, 2015 does not include options to purchase 1,073,166 shares and warrants to purchase 219,868 shares due to their anti-dilutive effect.

The following is a reconciliation of the numerator and denominator for basic and diluted earnings per share for the three months ended March 31, 2015 and 2014:

2015 | 2014 | |||||||

Basic Earnings per Share | ||||||||

Numerator: | ||||||||

Net income available to common shareholders | $ | (16,966,455 | ) | $ | 862,165 | |||

Denominator: | ||||||||

Weighted-average shares outstanding | 28,118,396 | 21,232,949 | ||||||

Basic earnings per share | $ | (0.60 | ) | $ | 0.04 | |||

Diluted Earnings per Share | ||||||||

Numerator: | ||||||||

Net income available to common shareholders | $ | (16,966,455 | ) | $ | 862,165 | |||

Denominator: | ||||||||

Weighted-average shares outstanding | 28,118,396 | 21,232,949 | ||||||

Effect of dilutive securities | ||||||||

Stock options and warrants | — | 1,225,727 | ||||||

Preferred stock | — | 1,279,342 | ||||||

Diluted weighted-average shares outstanding | 28,118,396 | 23,738,018 | ||||||

Diluted earnings per share | $ | (0.60 | ) | $ | 0.04 | |||

NOTE 10. COMMON STOCK

The total number of authorized shares of the Company’s common stock is 750,000,000 shares, $0.001 par value per share. As of March 31, 2015, there were 28,125,581 common shares issued and outstanding.

Each share of the Company's common stock is entitled to equal dividends and distributions per share with respect to the common stock when, as and if declared by the Company's board of directors. No holders of any shares of the Company's common stock has a preemptive right to subscribe for any of the Company's securities, nor are any shares of the Company's common stock subject

F-14

to redemption or convertible into other securities. Upon liquidation, dissolution or winding-up of the Company and after payment of creditors and preferred shareholders of the Company, if any, the assets of the Company will be divided pro rata on a share-for-share basis among the holders of the Company's common stock. Each share of the Company's common stock is entitled to one vote. Shares of the Company's common stock do not possess any cumulative voting rights.

During the three months ended March 31, 2015, a total of 17,476 shares of the Company's Series A Preferred Stock were converted into 17,476 shares of our common stock on a one-for-one basis.

During the three months ended March 31, 2015, the Company recognized contingently issuable warrants to purchase 1,766,874 shares of our common stock in connection with the amendments to the Credit Agreement with Goldman Sachs Bank USA (see Note 8). Management has determined that the warrants will more likely than not be canceled due to certain repayment provisions on or before June 30, 2015. Due to the down round feature of the warrant, the Company used the Black-Scholes model to value these warrants and have concluded that these are level 3 inputs. Management determined a discount factor on the grant date and on the balance sheet date based on available projections of cash to be used to make the mandatory repayments which resulted in a fair value derivative liability for the warrants of $577,440 at March 31, 2015.

NOTE 11. PREFERRED STOCK

The total number of authorized shares of the Company’s preferred stock is 50,000,000 shares, $0.001 par value per share. The total number of designated shares of the Company’s Series A Preferred Stock is 5,000,000 (“Series A Preferred”). The total number of designated shares of the Company’s Series B Preferred Stock is 2,000,000. As of March 31, 2015, there were 612,943 shares of Series A Preferred Stock issued and outstanding and no Series B Preferred shares issued and outstanding.

NOTE 12. SEGMENT REPORTING

The Company’s reportable segments include the Black Oil, Refining & Marketing and Recovery divisions. Segment information for the three months ended March 31, 2015 and 2014 is as follows:

THREE MONTHS ENDED MARCH 31, 2015 | ||||||||||||||||

Black Oil | Refining & Marketing | Recovery | Total | |||||||||||||

Revenues | $ | 24,913,976 | $ | 8,266,120 | $ | 4,504,243 | $ | 37,684,339 | ||||||||

Income (loss) from operations | $ | (7,893,676 | ) | $ | 55,049 | $ | 429,822 | $ | (7,408,805 | ) | ||||||

THREE MONTHS ENDED MARCH 31, 2014 | ||||||||||||||||

Black Oil | Refining & Marketing | Recovery | Total | |||||||||||||

Revenues | $ | 23,571,400 | $ | 19,827,459 | $ | 3,950,799 | $ | 47,349,658 | ||||||||

Income from operations | $ | 20,390 | $ | 770,575 | $ | 165,622 | $ | 956,587 | ||||||||

NOTE 13. CONTINGENT CONSIDERATION

As part of the consideration paid in connection with the acquisition of Vertex Holdings, L.P. in August 2012, if certain earning targets were met, the Company had to pay the seller approximately $2,233,000 annually in 2013, 2014 and 2015. The earn-out targets were not met for 2013 and the earn-out consideration was adjusted accordingly. In 2014, it was determined that the 2014 and 2015 earnings targets would not be met and the contingent consideration was reduced by $2,861,000, which represented 100% of the discounted cash flow for years two and three.

As part of the consideration paid in connection with the acquisition of certain assets from Omega Refining, LLC in May 2014, the Company agreed to pay the seller additional earn-out consideration in the event that certain EBITDA targets were met (a) during any twelve month period during the eighteen month period commencing on the first day of the first full calendar month following the May 2, 2014 initial closing date (which targets begin at $8,000,000 of EBITDA during such twelve month period) of up to 470,498 shares of common stock of the Company; and (b) during the calendar year ended December 31, 2015 (which targets begin at $9,000,000 of EBITDA) of up to 770,498 shares of common stock of the Company, in each case subject to adjustment for certain capital expenditures. In 2014, the contingent consideration was evaluated by management and reduced by $2,165,000, which represents 100% of the contingent liability related to the Omega Refining acquisition.

As part of the consideration paid in connection with the acquisition of 51% of E-Source, if certain targets were met, the Company had to pay the seller approximately $260,000 annually in 2014, 2015, 2016 and 2017. The Company recorded contingent consideration of $748,000, which was the discounted cash flows of the earn-out payments. Of this amount, $136,662 was paid in 2014 and the remaining $611,338 was written off. The write off was triggered because certain terms of the contingent consideration agreement were not met by the acquiree.

As part of the consideration paid for certain assets acquired from Warren Ohio Holdings Co., LLC. f/k/a Heartland Group Holdings, LLC (“Heartland”) in December 2014, the Company has agreed to pay the seller additional earn-out consideration of up to a maximum of $8,276,792, based on total EBITDA related to the operations acquired from Heartland during the twelve month period beginning on the first day of the first full calendar month commencing on or after the first anniversary of the closing (“Contingent Payments”). Any Contingent Payment due is payable 50% in cash and 50% in shares of the Company’s common stock. Additionally, the amount of any Contingent Payment is reduced by two-thirds of the cumulative total of required capital expenditures incurred at Heartland’s refining facility in Columbus, Ohio, which are paid or funded by Vertex OH after the closing, not to exceed $866,667, which capital expenditures are estimated to total $1.3 million in aggregate. The Company recorded contingent consideration of $6,069,000, which represents the fair value of the earn-out payment calculated at close. As of March 31, 2015, the contingent consideration was evaluated by management and it was determined that no adjustment was necessary.

F-15

NOTE 14. SUBSEQUENT EVENTS

On April 30, 2015, Vertex Refining, entered into a Lease With Option For Membership Interest Purchase (the “Bango Lease”) with Bango Oil, LLC (“Bango Oil”). Pursuant to the Bango Lease, we, through Vertex Refining, agreed to lease a used oil re-refining plant located on approximately 40 acres in Churchill County, Nevada (the “Bango Plant”). The Bango Plant produces base lubricating oils and all of the raw and finish products into and out of the Bango Plant are transported by either rail car or tanker trucks.

The Bango Plant was previously leased by Bango Refining NV, LLC (“Bango Refining”), a subsidiary of Omega Holdings Company LLC (“Omega”), with whom we entered into an Asset Purchase Agreement in March 2014, which was to close in two parts, the first of which relating to the acquisition of substantially all of the assets of Omega Refining, LLC, closed in May 2014, and the second of which relating to acquisition of the rights Omega and Bango Refining had to the Bango Plant, failed to close due to Omega’s inability to perform its closing deliveries under the Asset Purchase Agreement. The Bango Plant was previously leased by Bango Refining; however, the lease was recently terminated by Bango Oil and we were able to enter into the Bango Lease directly with Bango Oil instead of having to acquire the rights to the Bango Plant pursuant to the prior terms of the Asset Purchase Agreement, pursuant to which we were originally required to deliver 1.5 million shares to Omega and to forgive amounts due under the Secured Promissory Note described below. Bango Refining ceased operating the Bango Plant on April 30, 2015. As a result of its lease with Bango Oil, Vertex Refining has the right as of May 1, 2015 to operate the Bango Plant and is in the process of obtaining required operating permits.

The Bango Lease contains usual and customary covenants, representations, events of default and indemnification requirements for a commercial lease agreement of similar size and scope as the Bango Lease. The term of the Bango Lease continues until August 10, 2025, provided that as long as no event of default under the Bango Lease exists, we have the right to terminate the Bango Lease at any time, beginning six months after the start of the lease with twelve months prior notice to Bango Oil, provided further that Bango Oil can terminate the Bango Lease with thirty days prior notice to us during the twelve month notice period (i.e., after we have previously provided the twelve month notice of our intent to terminate the Bango Lease). Notwithstanding the above, we also have the right, during the first six months of the lease, to terminate the Bango Lease with five days written notice to Bango Oil in the event certain material improvements or equipment at the Bango Plant are physically removed by creditors of Omega, or such creditors obtain a preliminary injunction preventing the use of a material portion of such improvements or equipment, and in either case it interferes with our use of the plant.

No rent is due under the Bango Lease until January 1, 2016, at which time rent in the amount of $244,000 per month is due for the remainder of the term of the lease. We also have the option of paying rent which is due during 2016 in shares of our restricted common stock. Specifically, we have the right to issue shares of restricted common stock to Bango Oil equal to 110% of the rental payment due, based on the volume weighted average price (VWAP) of our common stock during the ten day period preceding the first of each applicable month, provided that if on the six month anniversary of the issuance of any stock issued in consideration for rent due, the value of the stock issued is less than 110% of the rental payment due, we are required to pay Bango Oil the difference in cash or issue Bango Oil additional shares of common stock equal to the difference in value. In addition to monthly rent, we are required to pay all taxes assessed on the property under the Bango Lease.

The Bango Lease also includes a purchase option, whereby, if no event of default exists on the Bango Lease, we have the option at any time during the term of the lease to purchase all of the equity interests of Bango Oil (the “Purchase Option”), effectively acquiring ownership of the Bango Plant. The initial consideration due to Bango Oil in connection with the Purchase Option is $8.5 million, provided that if the Purchase Option is not exercised by us prior to August 31, 2015, the amount due increases by $125,000 per month until July 1, 2016, and $3,000 per month thereafter, up to a maximum of $13 million, assuming we make timely rental payments under the lease (in the event we fail to timely make any rental payment due, the monthly increase in the purchase price for such applicable month increases by an additional $122,000).

We also continue to maintain a first priority security interest in certain personal property of Omega used at the plant pursuant to our prior agreements with Omega (which property we lease pursuant to the Personal Property Leases described below), including a Secured Promissory Note evidencing amounts we (through Vertex Refining) advanced to Omega at the first closing to permit it to deliver the Omega Refining assets purchased at the first closing free and clear of any liens, which funds were subsequently loaned to Bango Refining, in the aggregate amount of $14,358,067, which Omega failed to pay as of its due date on March 31, 2015, has failed to pay to date, and which Secured Promissory Note is currently in default. In the event we obtain title to such property which secures the repayment of the Secured Promissory Note through a foreclosure, we agreed to transfer certain assets which constitute fixtures to Bango Oil upon the termination of the Bango Lease, unless such termination is due to us exercising our rights under the Purchase Option. The value of the assets obtained are sufficient to cover the outstanding balance of the note. Notwithstanding the above, Vertex Refining entered into a Personal Property Lease with Omega Refining, LLC (“Omega Refining”)

F-16

and Bango Refining, LLC, both related parties of Omega on April 30, 2015 (the “Personal Property Lease”), whereby Vertex Refining agreed to lease all machinery, equipment and other tangible personal property located at the Bango Plant from Omega Refining and Bango Refining, for $220,000 per month, provided that until the Secured Promissory Note which Omega owes us is paid in full, Vertex Refining is able to accrue such payments and set them off against the amount due under the Secured Promissory Note. The Personal Property Lease terminates after 60 days unless Vertex Refining provides notice of its intent to renew for an additional 30 days. It is anticipated that Vertex Refining will acquire the leased personal property from Omega Refining and Bango Refining at the termination of the Personal Property Lease pursuant to Article 9 of the Uniform Commercial Code, with such acquisition occurring through an offset of a portion of the amount due Vertex Refining under the Secured Promissory Note.

Also on April 30, 2015, Vertex Refining and Vertex Operating, both our wholly-owned subsidiaries, entered into a Shared Services Agreement whereby Vertex Operating agreed to operate and provide support services at the Bango Plant for $80,000 per month through May 2, 2019.

In addition to the Bango Lease for the Bango Plant, Vertex Refining also entered into two Lease and Purchase Agreements (the “Equipment Leases”). The Equipment Leases provide the use of a rail facility and related equipment and a pre-fabricated metal building located at the plant. The Equipment Leases expires on December 31, 2016, subject to certain rights Vertex Refining has to terminate the leases earlier. The monthly rental costs for the leases are $16,300 and $3,800 per month, respectively, provided no rent is due for fiscal 2015. We also have the right pursuant to the Equipment Leases to pay the rent due under the Equipment Leases in shares of our restricted common stock, equal in value to 110% of the applicable rental payment due, based on the VWAP of our common stock during the ten day period preceding the first of each applicable month, provided that if on the six month anniversary of the issuance of any stock in lieu of cash payments, the value of the stock issued (based on the then 10 day VWAP) is less than 110% of the rental payment due, we are required to pay the lessor(s) the difference in cash or issue the lessor(s) additional shares of common stock equal to the difference in value. We also have the right under the Equipment Leases to acquire the applicable property/equipment subject to each Equipment Lease at any time prior to the expiration of the leases for $914,000 and $400,000, respectively, provided such amounts are discounted to $776,900 and $340,000, respectively, if the applicable purchase option is exercised prior to August 31, 2015. Finally, we have the right pursuant to the agreements to pay the purchase price associated with the purchase option in restricted common stock, equal in value to 110% of the amount due, based on the VWAP of our common stock during the ten day period preceding the purchase date, provided that if on the six month anniversary of the issuance of any stock in lieu of a cash payment, the value of the stock issued (based on the then 10 day VWAP) is less than 110% of the purchase price, we are required to pay the lessor(s) the difference in cash or issue the lessor(s) additional shares of common stock equal to the difference in value.

Our senior lender, Goldman Sachs Bank USA (“Goldman”), approved the entry by Vertex Refining into the Bango Lease and Equipment Leases, and also waived various events of default which had previously occurred under our senior credit facility with Goldman relating to various deliverables which we failed to make to Goldman as required pursuant to the terms of the credit facility and the fact that our auditor provided a ‘going concern’ opinion in our December 31, 2014 audited financial statements.

Each of the lessors under the Bango Lease and Equipment Leases also entered into an Acknowledgement and Confirmation Agreement with us, whereby they make various representations regarding their financial suitability to receive shares of our common stock, the restricted nature of the shares they may receive in lieu of cash consideration under the leases, and their status as an accredited investor, and agreed to not sell our stock short during the term of the leases which they are party to, and we agreed to not issue such investors securities representing more than 9.99% of our outstanding common stock. All of the parties also agreed that the aggregate shares of common stock issuable pursuant to all of the leases would not (i) exceed 19.9% of the outstanding shares of our common stock on April 30, 2015, (ii) exceed 19.9% of the combined voting power of the then outstanding voting securities of our common stock on April 30, 2015, or (iii) otherwise exceed such number of shares of common stock that would violate applicable listing rules of the NASDAQ Stock Market in the event our stockholders do not approve the issuance of the shares (collectively, the “Share Cap”).

Pursuant to the Heartland Purchase Agreement, the parties agreed to a true up of the inventory of the Acquired Business subsequent to closing on December 5, 2014. Pursuant to the true up, On April 5, 2015, the additional amount owed by the Company to Heartland for inventory at Closing (less amounts already paid for at Closing) was satisfied by issuing 56,180 shares of the Company’s restricted common stock.

F-17

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

This Report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. In some cases, you can identify forward-looking statements by the following words: “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “ongoing,” “plan,” “potential,” “predict,” “project,” “should,” or the negative of these terms or other comparable terminology, although not all forward-looking statements contain these words. Forward-looking statements are not a guarantee of future performance or results, and will not necessarily be accurate indications of the times at, or by, which such performance or results will be achieved. Forward-looking statements are based on information available at the time the statements are made and involve known and unknown risks, uncertainties and other factors that may cause our results, levels of activity, performance or achievements to be materially different from the information expressed or implied by the forward-looking statements in this Report. These factors include:

• | risks associated with our outstanding credit facilities, including amounts owed, restrictive covenants, security interests thereon and our ability to repay such facilities and amounts due thereon when due; |

• | the level of competition in our industry and our ability to compete; |

• | our ability to respond to changes in our industry; |

• | the loss of key personnel or failure to attract, integrate and retain additional personnel; |

• | our ability to protect our intellectual property and not infringe on others’ intellectual property; |

• | our ability to scale our business; |

• | our ability to maintain supplier relationships and obtain adequate supplies of feedstocks; |

• | our ability to obtain and retain customers; |

• | our ability to produce our products at competitive rates; |

• | our ability to execute our business strategy in a very competitive environment; |

• | trends in, and the market for, the price of oil and gas and alternative energy sources; |

• | our ability to maintain our relationship with KMTEX, Ltd.; |

• | the impact of competitive services and products; |

• | our ability to integrate acquisitions; |

• | our ability to complete acquisitions; |

• | our ability to maintain insurance; |

• | potential future litigation, judgments and settlements; |

• | rules and regulations making our operations more costly or restrictive; |

• | changes in environmental and other laws and regulations and risks associated with such laws and regulations; |

• | economic downturns both in the United States and globally; |

• | risk of increased regulation of our operations and products; |

• | negative publicity and public opposition to our operations; |

• | disruptions in the infrastructure that we and our partners rely on; |

• | an inability to identify attractive acquisition opportunities and successfully negotiate acquisition terms; |

• | our ability to effectively integrate acquired assets, companies, employees or businesses; |

• | liabilities associated with acquired companies, assets or businesses; |

• | interruptions at our facilities; |

• | our ability to complete pending and future acquisitions; |

• | required earn-out payments and other contingent payments we are required to make; |

• | unexpected changes in our anticipated capital expenditures resulting from unforeseen required maintenance, repairs, or upgrades; |

13

• | our ability to acquire and construct new facilities; |

• | certain events of default which have occurred under our debt facilities and previously been waived; |

• | our ability to effectively manage our growth; |

• | repayment of and covenants in our debt facilities; |

• | the lack of capital available on acceptable terms to finance our continued growth; and |

• | other risk factors included under “Risk Factors” below and in our Annual Report on Form 10-K and prior Form 10-Qs. |

You should read the matters described in “Risk Factors” below and disclosed in the Company’s Annual Report on Form 10-K/A, filed with the Commission on April 15, 2015 and the other cautionary statements made in this Report as being applicable to all related forward-looking statements wherever they appear in this Report. We cannot assure you that the forward-looking statements in this Report will prove to be accurate and therefore prospective investors are encouraged not to place undue reliance on forward-looking statements. Other than as required by law, we undertake no obligation to update or revise these forward-looking statements, even though our situation may change in the future.

Please see the “Glossary of Selected Terms” incorporated by reference hereto as Exhibit 99.1, for a list of abbreviations and definitions used throughout this Report.

In this Quarterly Report on Form 10-Q, we may rely on and refer to information regarding the refining, re-refining, used oil and oil and gas industries in general from market research reports, analyst reports and other publicly available information. Although we believe that this information is reliable, we cannot guarantee the accuracy and completeness of this information, and we have not independently verified any of it.

Corporate History of the Registrant:

Vertex Energy, Inc. (the “Company,” “we,” “us,” and “Vertex”) was formed as a Nevada corporation on May 14, 2008. Pursuant to an Amended and Restated Agreement and Plan of Merger dated May 19, 2008, by and between Vertex Holdings, L.P. (formerly Vertex Energy, L.P.), a Texas limited partnership ("Holdings"), us, World Waste Technologies, Inc., a California corporation (“WWT” or “World Waste”), Vertex Merger Sub, LLC, a California limited liability company and our wholly-owned subsidiary ("Merger Subsidiary"), and Benjamin P. Cowart, our Chief Executive Officer, as agent for our shareholders (as amended from time to time, the “Merger Agreement”). Effective on April 16, 2009, World Waste merged with and into Merger Subsidiary, with Merger Subsidiary continuing as the surviving corporation and becoming our wholly-owned subsidiary (the "Merger"). In connection with the Merger, (i) each outstanding share of World Waste common stock was cancelled and exchanged for 0.10 shares of our common stock; (ii) each outstanding share of World Waste Series A preferred stock was cancelled and exchanged for 0.4062 shares of our Series A preferred stock; and (iii) each outstanding share of World Waste Series B preferred stock was cancelled and exchanged for 11.651 shares of our Series A preferred stock. Additionally, as a result of the Merger, the common stock of World Waste was effectively reversed one for ten (10) as a result of the exchange ratios set forth in the Merger, and unless otherwise noted, the impact of such effective reverse stock split, created by the exchange ratio set forth above, is retroactively reflected throughout this Report.

Material Acquisitions

Effective as of August 31, 2012, we acquired 100% of the outstanding equity interests of Vertex Acquisition Sub, LLC (“Acquisition Sub”), a special purpose entity consisting of substantially all of the assets of Holdings and real-estate properties of B & S Cowart Family L.P. (“B&S LP” and the “Acquisition”), both of which entities were owned and operated by related parties. Prior to closing the Acquisition, Holdings contributed to Acquisition Sub substantially all of its assets and liabilities relating to the business of transporting, storing, processing and re-refining petroleum products, crudes and used lubricants, including all of the outstanding equity interests in Holdings’ wholly-owned operating subsidiaries, Cedar Marine Terminals, L.P. (“CMT”), Crossroad Carriers, L.P. (“Crossroad”), Vertex Recovery, L.P. (“Vertex Recovery”) and H&H Oil, L.P. (“H&H Oil”, and collectively, the “Transferred Partnerships”), and B&S LP contributed real estate associated with the operations of H&H Oil.

We paid the following consideration for 100% of the equity interests in Acquisition Sub (i) to Holdings, (a) $14.8 million