Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - Vertex Energy Inc. | Financial_Report.xls |

| EX-31.1 - EXHIBIT 31.1 - Vertex Energy Inc. | a6302014-ex311.htm |

| EX-10.25 - EXHIBIT 10.25 - Vertex Energy Inc. | ex1025tsa-omegaxmtb.htm |

| EX-32.1 - EXHIBIT 32.1 - Vertex Energy Inc. | a6302014-ex321.htm |

| EX-10.22 - EXHIBIT 10.22 - Vertex Energy Inc. | ex1022landlease-marreroter.htm |

| EX-10.23 - EXHIBIT 10.23 - Vertex Energy Inc. | ex1023myrtlegroveleasewexh.htm |

| EX-99.2 - EXHIBIT 99.2 - Vertex Energy Inc. | a6302014-ex992.htm |

| EX-32.2 - EXHIBIT 32.2 - Vertex Energy Inc. | a6302014-ex322.htm |

| EX-31.2 - EXHIBIT 31.2 - Vertex Energy Inc. | a6302014-ex312.htm |

| EX-10.24 - EXHIBIT 10.24 - Vertex Energy Inc. | ex1024omega-operationmanag.htm |

| EX-10.26 - EXHIBIT 10.26 - Vertex Energy Inc. | ex1026omegabangopurchasean.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

þ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal quarter ended June 30, 2014

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE TRANSITION PERIOD FROM _____________ TO _____________

Commission File Number 001-11476

———————

VERTEX ENERGY, INC.

(Exact name of registrant as specified in its charter)

———————

NEVADA | 94-3439569 |

(State or other jurisdiction of | (I.R.S. Employer Identification No.) |

incorporation or organization) | |

1331 GEMINI STREET, SUITE 250 HOUSTON, TEXAS | 77058 |

(Address of principal executive offices) | (Zip Code) |

Registrant's telephone number, including area code: 866-660-8156

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark whether the registrant is a large accelerated filer, and accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ¨ | Accelerated filer ¨ |

Non-accelerated filer ¨ | Smaller reporting company ý |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.

Yes ¨ No ý

State the number of shares of the issuer’s common stock outstanding, as of the latest practicable date: 25,042,210 shares of common stock issued and outstanding as of August 12, 2014.

TABLE OF CONTENTS

Page | |||

PART I | |||

Item 1. | Financial Statements | ||

Consolidated Balance Sheets (unaudited) | |||

Consolidated Statements of Operations (unaudited) | |||

Consolidated Statements of Cash Flows (unaudited) | |||

Notes to Consolidated Financial Statements (unaudited) | |||

Item 2 | Management’s Discussion And Analysis Of Financial Condition And Results Of Operations | ||

Item 3. | Quantitative And Qualitative Disclosures About Market Risk | ||

Item 4. | Controls and Procedures | ||

PART II | |||

Item 1. | Legal Proceedings | ||

Item 1A. | Risk Factors | ||

Item 2. | Unregistered Sales Of Equity Securities And Use Of Proceeds | ||

Item 3. | Defaults Upon Senior Securities | ||

Item 4. | Mine Safety Disclosures | ||

Item 5. | Other Information | ||

Item 6. | Exhibits | ||

PART I – FINANCIAL INFORMATION

Item 1. Financial Statements

VERTEX ENERGY, INC. | ||||||||

CONSOLIDATED BALANCE SHEETS (Unaudited) | ||||||||

June 30, 2014 | December 31, 2013 | |||||||

ASSETS | ||||||||

Current assets | ||||||||

Cash and cash equivalents | $ | 19,651,831 | $ | 2,678,628 | ||||

Accounts receivable, net | 13,952,805 | 11,714,813 | ||||||

Accounts receivable-related party | 9,335,321 | — | ||||||

Inventory | 16,412,448 | 8,540,459 | ||||||

Prepaid expenses | 3,530,682 | 1,161,721 | ||||||

Total current assets | 62,883,087 | 24,095,621 | ||||||

Noncurrent assets | ||||||||

Other assets | 2,925,096 | — | ||||||

Fixed assets, net | 46,725,108 | 15,091,176 | ||||||

Intangible assets, net | 16,733,683 | 15,172,816 | ||||||

Goodwill | 4,922,353 | 4,502,743 | ||||||

Deferred federal income tax | 5,684,000 | 5,684,000 | ||||||

Total noncurrent assets | 76,990,240 | 40,450,735 | ||||||

TOTAL ASSETS | $ | 139,873,327 | $ | 64,546,356 | ||||

LIABILITIES AND EQUITY | ||||||||

Current liabilities | ||||||||

Accounts payable and accrued expenses | $ | 26,004,141 | $ | 14,096,185 | ||||

Capital leases | 809,497 | — | ||||||

Current portion of long-term debt | 2,417,335 | 1,956,847 | ||||||

Total current liabilities | 29,230,973 | 16,053,032 | ||||||

Long-term liabilities | ||||||||

Long-term debt | 40,173,643 | 6,558,851 | ||||||

Contingent consideration | 5,385,250 | 3,220,250 | ||||||

Line of credit | 304,000 | — | ||||||

Deferred federal income tax | 378,000 | 378,000 | ||||||

Total liabilities | 75,471,866 | 26,210,133 | ||||||

Commitments and contingencies | ||||||||

EQUITY | ||||||||

Preferred stock, $0.001 par value per share: | ||||||||

50,000,000 shares authorized | ||||||||

Series A Convertible Preferred stock, $0.001 par value, | ||||||||

5,000,000 authorized and 675,558 and 1,319,002 issued | ||||||||

and outstanding at June 30, 2014 and December 31, | ||||||||

2013, respectively | 675 | 1,319 | ||||||

Common stock, $0.001 par value per share; | ||||||||

750,000,000 shares authorized; 25,019,450 and 21,205,609 | ||||||||

issued and outstanding at June 30, 2014 and | ||||||||

December 31, 2013, respectively | 25,019 | 21,206 | ||||||

Additional paid-in capital | 39,189,263 | 19,579,732 | ||||||

Retained earnings | 25,405,251 | 17,542,004 | ||||||

Total Vertex Energy, Inc. stockholders' equity | 64,620,208 | 37,144,261 | ||||||

Non-controlling interest | (218,747 | ) | 1,191,962 | |||||

Total equity | 64,401,461 | 38,336,223 | ||||||

TOTAL LIABILITIES AND EQUITY | $ | 139,873,327 | $ | 64,546,356 | ||||

See accompanying notes to the consolidated financial statements

F-1

VERTEX ENERGY, INC. | ||||||||||||||||

CONSOLIDATED STATEMENTS OF OPERATIONS | ||||||||||||||||

THREE AND SIX MONTHS ENDED JUNE 30, 2014 AND 2013 | ||||||||||||||||

(UNAUDITED) | ||||||||||||||||

Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

2014 | 2013 | 2014 | 2013 | |||||||||||||

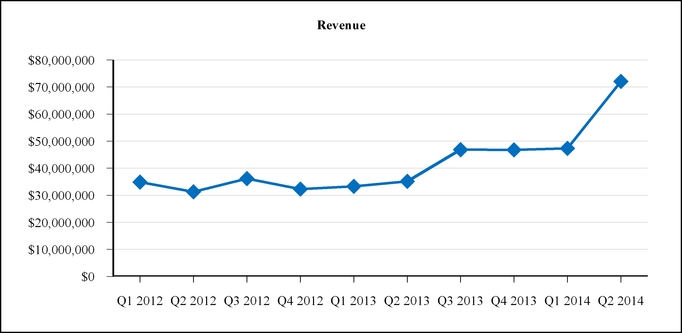

Revenues | $ | 72,079,622 | $ | 35,111,402 | $ | 119,429,280 | $ | 68,366,204 | ||||||||

Cost of revenues | 63,200,942 | 32,556,738 | 105,406,112 | 62,341,782 | ||||||||||||

Gross profit | 8,878,680 | 2,554,664 | 14,023,168 | 6,024,422 | ||||||||||||

Reduction of contingent liability | — | (1,850,000 | ) | — | (1,850,000 | ) | ||||||||||

Operating expenses: | ||||||||||||||||

Selling, general and administrative expenses (exclusive of acquisition related expenses) | 6,075,517 | 2,395,745 | 9,663,006 | 4,653,829 | ||||||||||||

Acquisition related expenses | 1,959,418 | — | 2,559,830 | — | ||||||||||||

Total operating expenses | 8,034,935 | 2,395,745 | 12,222,836 | 4,653,829 | ||||||||||||

Income from operations | 843,745 | 2,008,919 | 1,800,332 | 3,220,593 | ||||||||||||

Other income (expense) | ||||||||||||||||

Other income | 7 | 7,598 | 377 | 32,888 | ||||||||||||

Bargain purchase gain related to Omega acquisition | 6,481,051 | — | 6,481,051 | — | ||||||||||||

Other expense | (10,866 | ) | — | (10,866 | ) | (40,726 | ) | |||||||||

Interest expense | (657,235 | ) | (112,999 | ) | (733,046 | ) | (219,139 | ) | ||||||||

Total other income (expense) | 5,812,957 | (105,401 | ) | 5,737,516 | (226,977 | ) | ||||||||||

Income before income tax | 6,656,702 | 1,903,518 | 7,537,848 | 2,993,616 | ||||||||||||

Income tax benefit (expense) | — | (12,248 | ) | — | (18,751 | ) | ||||||||||

Net income | $ | 6,656,702 | $ | 1,891,270 | $ | 7,537,848 | $ | 2,974,865 | ||||||||

Net income attributable to non-controlling interest | 344,380 | — | 325,399 | — | ||||||||||||

Net income attributable to Vertex Energy, Inc. | $ | 7,001,082 | $ | 1,891,270 | $ | 7,863,247 | $ | 2,974,865 | ||||||||

Earnings per common share | ||||||||||||||||

Basic | $ | 0.31 | $ | 0.11 | $ | 0.36 | $ | 0.17 | ||||||||

Diluted | $ | 0.28 | $ | 0.10 | $ | 0.33 | $ | 0.15 | ||||||||

Shares used in computing earnings per share | ||||||||||||||||

Basic | 22,826,102 | 17,409,034 | 22,025,316 | 17,243,762 | ||||||||||||

Diluted | 24,847,456 | 19,887,288 | 23,879,500 | 19,798,989 | ||||||||||||

See accompanying notes to the consolidated financial statements

F-2

VERTEX ENERGY, INC. | ||||||||

CONSOLIDATED STATEMENTS OF CASH FLOWS | ||||||||

SIX MONTHS ENDED JUNE 30, 2014 AND 2013 | ||||||||

(UNAUDITED) | ||||||||

Six Months Ended | ||||||||

June 30, 2014 | June 30, 2013 | |||||||

Cash flows from operating activities | ||||||||

Net income | $ | 7,537,848 | $ | 2,974,865 | ||||

Adjustments to reconcile net income to cash provided by operating activities | ||||||||

Stock based compensation expense | 101,378 | 94,466 | ||||||

Depreciation and amortization | 1,800,950 | 1,069,035 | ||||||

Gain on acquisition | (6,481,051 | ) | — | |||||

Deferred federal income tax | — | 11,000 | ||||||

Reduction of contingent liability | — | (1,850,000 | ) | |||||

Changes in operating assets and liabilities | ||||||||

Accounts receivable | (2,237,992 | ) | (930,490 | ) | ||||

Accounts receivable-other | 950,000 | — | ||||||

Accounts receivable-related party | (1,027,321 | ) | — | |||||

Inventory | (3,679,989 | ) | (3,465,205 | ) | ||||

Prepaid expenses | (2,717,571 | ) | (45,451 | ) | ||||

Accounts payable | 9,464,956 | 3,669,339 | ||||||

Other assets | (79,806 | ) | — | |||||

Net cash provided by operating activities | 3,631,402 | 1,527,559 | ||||||

Cash flows from investing activities | ||||||||

Acquisition of Omega | (28,764,099 | ) | (67,972 | ) | ||||

Refund of asset acquisition | — | 675,558 | ||||||

Purchase of fixed assets | (2,635,882 | ) | (1,010,485 | ) | ||||

Net cash (used in) investing activities | (31,399,981 | ) | (402,899 | ) | ||||

Cash flows from financing activities | ||||||||

Line of credit (payments) proceeds, net | 304,000 | (750,000 | ) | |||||

Proceeds related to primary stock offering | 15,803,000 | — | ||||||

Proceeds from note payable | 40,509,906 | — | ||||||

Payments on note payable | (9,634,029 | ) | (922,873 | ) | ||||

Proceeds from exercise of common stock options and warrants | 211,062 | 37,501 | ||||||

Debt issue costs | (2,452,157 | ) | — | |||||

Net cash provided by (used in) financing activities | 44,741,782 | (1,635,372 | ) | |||||

Net change in cash and cash equivalents | 16,973,203 | (510,712 | ) | |||||

Cash and cash equivalents at beginning of the period | 2,678,628 | 807,940 | ||||||

Cash and cash equivalents at end of period | $ | 19,651,831 | $ | 297,228 | ||||

SUPPLEMENTAL INFORMATION | ||||||||

Cash paid for interest | $ | 733,046 | $ | 199,737 | ||||

Cash paid for income taxes | $ | — | $ | 21,249 | ||||

NON-CASH INVESTING AND FINANCING TRANSACTIONS | ||||||||

Conversion of Series A Preferred Stock into common stock | $ | 644 | $ | 168 | ||||

Note payable for acquisition of E-Source interest | $ | 854,050 | $ | — | ||||

Additional paid in capital for acquisition of E-Source interest | $ | 231,260 | $ | — | ||||

See accompanying notes to the consolidated financial statements

F-3

VERTEX ENERGY, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2014

(UNAUDITED)

NOTE 1. BASIS OF PRESENTATION AND NATURE OF OPERATIONS

The accompanying unaudited consolidated interim financial statements of Vertex Energy, Inc. (the “Company,” or “Vertex Energy”) have been prepared in accordance with accounting principles generally accepted in the United States of America and the rules of the Securities and Exchange Commission (“SEC”), and should be read in conjunction with the audited consolidated financial statements and notes thereto contained in the Company’s annual consolidated financial statements as filed with the SEC on Form 10-K on March 25, 2014 (the “Form 10-K”). In the opinion of management, all adjustments, consisting of normal recurring adjustments, necessary for a fair presentation of financial position and the results of operations for the interim periods presented have been reflected herein. The results of operations for interim periods are not necessarily indicative of the results to be expected for the full year. Certain prior period amounts have been reclassified to conform to current period presentation. Notes to the consolidated financial statements which would substantially duplicate the disclosure contained in the audited consolidated financial statements for the most recent fiscal year 2013 as reported in Form 10-K, have been omitted.

NOTE 2. CONCENTRATIONS, SIGNIFICANT CUSTOMERS, COMMITMENTS AND CONTINGENCIES

At June 30, 2014 and 2013 and for each of the six months then ended, the Company’s revenues and receivables were comprised of the following customer concentrations:

2014 | 2013 | |||||||

% of Revenues | % of Receivables | % of Revenues | % of Receivables | |||||

Customer 1 | 36% | 19% | —% | —% | ||||

Customer 2 | 16% | 3% | 54% | 40% | ||||

Customer 3 | 14% | 25% | —% | —% | ||||

Customer 4 | 11% | 9% | 8% | —% | ||||

Customer 5 | 7% | 9% | 10% | 30% | ||||

Customer 6 | —% | —% | 3% | 12% | ||||

The Company purchases goods and services from one company that represented 10% of total purchases for the six months ended June 30, 2014 and one company that represented 12% for the six months ended June 30, 2013.

The Company has had various debt facilities available for use, of which there was $43,704,475 and $8,515,698 outstanding as of June 30, 2014 and December 31, 2013, respectively. See Note 3 for further details.

In February 2013, Bank of America agreed to lease the Company up to $1,025,000 of equipment to enhance the Thermal Chemical Extraction Process (TCEP) operation, which went into effect in April 2013. Under the current terms of the lease agreement, there are 60 monthly payments of approximately $13,328.

The Company’s revenue, profitability and future rate of growth are substantially dependent on prevailing prices for petroleum-based products. Historically, the energy markets have been very volatile, and there can be no assurance that these prices will not be subject to wide fluctuations in the future. A substantial or extended decline in such prices could have a material adverse effect on the Company’s financial position, results of operations, cash flows, and access to capital and on the quantities of petroleum-based products that the Company can economically produce.

The Company, in its normal course of business, is involved in various other claims and legal action. In the opinion of management, the outcome of these claims and actions will not have a material adverse impact upon the financial position of the Company.

We intend to take advantage of any potential tax benefits related to net operating losses (“NOLs”) acquired as part of the Company's April 2009 merger with World Waste Technologies, Inc. ("World Waste"). As a result of the merger, we acquired approximately $42 million of net operating losses that may be used to offset taxable income generated by the Company in future periods.

It is possible that the Company may be unable to use these NOLs in their entirety. The extent to which the Company will be able to utilize these carry-forwards in future periods is subject to limitations based on a number of factors, including the number of

F-4

VERTEX ENERGY, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2014

(UNAUDITED)

shares issued within a three-year look-back period, whether the merger is deemed to be a change in control, whether there is deemed to be a continuity of World Waste’s historical business, and the extent of the Company’s subsequent income. As of December 31, 2013, the Company had utilized approximately $11.25 million of these NOLs leaving approximately $30.75 million of potential NOLs of which we expect to utilize approximately $2.2 million for the six months ended June 30, 2014. The Company recorded a change in valuation allowance for the six months ended June 30, 2014 of approximately $748,000.

NOTE 3. NOTES PAYABLE

In September 2012, the Company entered into a credit agreement with Bank of America. Pursuant to the agreement, Bank of America agreed to loan the Company $8,500,000 in the form of a term loan and to provide the Company with an additional $10,000,000 in the form of a revolving line of credit.

In May 2014, the Company entered into an amended and restated credit agreement with Bank of America. The amended credit agreement amended and restated the prior credit agreement entered into with Bank of America in September 2012. Pursuant to the agreement, Bank of America agreed to loan the Company up to $20,000,000 in the form of a revolving line of credit, subject to certain terms and lending ratios, to be used for feedstock purchases and general corporate purposes. The line of credit bears interest at the option of the Company of either the lender's prime commercial lending rate then in effect between 1.25% and 2% per annum or the Bank of America LIBOR rate plus between 2.35% and 3% (both ranges dependent upon the Company's leverage ratio from time to time). Accrued and unpaid interest on the revolving note is due and payable monthly in arrears and all amounts outstanding under the revolving note are due and payable on May 2, 2017. The balance on the revolving line of credit was $0 at June 30, 2014.

The financing arrangement discussed above is secured by a first priority security interest in all of the assets and securities of our direct and indirect subsidiaries other than E-Source Holdings, LLC. The loan includes various covenants binding upon the Company, including, requiring that the Company comply with certain reporting requirements, provide notices of material corporate events and forecasts to Bank of America, and maintain certain financial ratios relating to debt leverage, consolidated EBITDA, maximum debt exposure, and minimum liquidity, including maintaining a ratio of quarterly consolidated EBITDA to certain fixed charges. The Company was in compliance with all aspects of the agreement at June 30, 2014.

On May 2, 2014, the Company entered into a Credit and Guaranty Agreement with Goldman Sachs Bank USA. Pursuant to the agreement, Goldman Sachs Bank USA loaned the Company $40,000,000 in the form of a term loan. As set forth in the Credit Agreement, the Company has the option to select whether loans made under the Credit Agreement bear interest at (a) the greater of (i) the prime rate in effect, (ii) the weighted average of the rates on overnight Federal funds transactions with members of the Federal Reserve System plus ½ of 1%, (iii) the sum of (A) the Adjusted LIBOR Rate and (B) 1%, and (iv) 4.5% per annum; or (b) the greater of (i) 1.50% and (ii) the applicable ICE Benchmark Administration Limited interest rate, divided by (x) one minus, (y) the Adjusted LIBOR Rate. Interest on the Credit Agreement is payable monthly in arrears. Amortizing principal payments are due on the Credit Agreement Loan in the amount of $300,000 per fiscal quarter for June 30, 2014, September 30, 2014, December 31, 2014 and March 31, 2015, and $800,000 per fiscal quarter thereafter until maturity on May 2, 2019. The balance on the term loan was $39,700,000 at June 30, 2014.

The Goldman Sachs Bank USA financing arrangement is secured by all of the assets of the Company, but subordinate to the aforementioned Bank of America credit agreement. The Credit Agreement contains customary representations, warranties, and covenants for facilities of similar nature and size as the Credit Agreement. The Credit Agreement also includes various covenants binding the Company including limits on indebtedness the Company may incur and maintenance of certain financial ratios relating to consolidated EBITDA and debt leverage. The Company was in compliance with all aspects of the agreement at June 30, 2014.

In August, 2013, the Company entered into a credit agreement with Texas Citizens Bank N.A. Pursuant to the agreement, Texas Citizens Bank agreed to loan E-Source Holdings $500,000 in the form of a revolving line of credit secured by E-Source held assets. The credit agreement carries an interest rate of 6.25% per annum. Accrued and unpaid interest on the revolving note is due and payable monthly in arrears and all amounts outstanding under the revolving note are due and payable on August 27, 2014. The balance on the line of credit was $304,000 at June 30, 2014.

On May 2, 2014, in connection with the closing of the Omega Refining acquisition, the Company assumed two capital leases totaling $3,154,860. Payments of $2,345,363 were made and the balance was $809,497 at June 30, 2014.

F-5

The Company has notes payable to various financial institutions, bearing interest at rates ranging from 5% to 6.35%, maturing from November 2015 to April 2023. The balance of the notes payable is $2,454,944 at June 30, 2014.

Effective January 1, 2014, the Company purchased an additional 19% ownership interest in E-Source Holdings, LLC ("E-Source") of which it had previously acquired 51%. In consideration for the additional interest the Company will pay $854,050 of which $200,000 was paid on April 11, 2014 and the remainder is to be paid monthly in $72,672 installments through December 31, 2014. The Company will also issue up to 207,743 shares of stock on January 31, 2015 based on certain EBITDA criteria being met for 2014 (reduced pro rata based on actual EBITDA). As of the date of the transaction, the estimated value of the stock to be issued of approximately $231,000 was recorded as additional paid in capital and a reduction of the non-controlling interest in accordance with ASC 810-10-45. The balance of the note payable is $436,033 at June 30, 2014.

NOTE 4. STOCK-BASED COMPENSATION

Stock-based compensation expense was $101,378 and $94,466 for the six months ended June 30, 2014 and 2013, respectively, for options previously awarded by the Company.

Stock option activity for the six months ended June 30, 2014 is summarized as follows:

Shares | Weighted Average Exercise Price | Weighted Average Remaining Contractual Life (in Years) | Grant Date Fair Value | |||||||||||

Outstanding at December 31, 2013 | 3,060,834 | $ | 5.89 | 6.07 | $ | 1,327,163 | ||||||||

Options granted | 150,000 | 7.55 | 10.00 | 304,915 | ||||||||||

Options forfeited/expired | (91,667 | ) | 10.78 | — | (29,335 | ) | ||||||||

Options exercised | (483,750 | ) | (0.68 | ) | — | (192,127 | ) | |||||||

Outstanding at June 30, 2014 | 2,635,417 | $ | 6.77 | 5.99 | $ | 1,410,616 | ||||||||

Vested at June 30, 2014 | 1,719,792 | $ | 8.43 | 4.72 | $ | 522,691 | ||||||||

Exercisable at June 30, 2014 | 1,719,792 | $ | 8.43 | 4.72 | $ | 522,691 | ||||||||

A summary of the Company’s stock warrant activity and related information for the six months ended June 30, 2014 is as follows:

Shares | Weighted Average Exercise Price | Weighted Average Remaining Contractual Life (in Years) | Grant Date Fair Value | |||||||||||

Outstanding at December 31, 2013 | 7,083 | $ | 2.72 | 1.57 | $ | 2,900 | ||||||||

Warrants exercised | (6,250 | ) | (1.75 | ) | — | (2,800 | ) | |||||||

Warrants cancelled/forfeited/expired | (833 | ) | (10.00 | ) | — | (100 | ) | |||||||

Warrants at June 30, 2014 | — | $ | — | — | $ | — | ||||||||

Vested at June 30, 2014 | — | $ | — | — | $ | — | ||||||||

Exercisable at June 30, 2014 | — | $ | — | — | $ | — | ||||||||

NOTE 5. EARNINGS PER SHARE

Basic earnings per share includes no dilution and is computed by dividing income available to common shareholders by the weighted average number of common shares outstanding for the periods presented. The calculation of basic earnings per share for the six months ended June 30, 2014 includes the weighted average of common shares outstanding. Diluted earnings per share reflect the potential dilution of securities that could share in the earnings of an entity, such as convertible preferred stock, stock options, warrants or convertible securities. The calculation of diluted earnings per share for the six months ended June 30, 2014 does not include options to purchase 906,000 shares due to their anti-dilutive effect.

F-6

VERTEX ENERGY, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2014

(UNAUDITED)

The following is a reconciliation of the numerator and denominator for basic and diluted earnings per share for the six months ended June 30, 2014 and 2013:

2014 | 2013 | |||||||

Basic Earnings per Share | ||||||||

Numerator: | ||||||||

Net income available to common shareholders | $ | 7,863,247 | $ | 2,974,865 | ||||

Denominator: | ||||||||

Weighted-average shares outstanding | 22,025,316 | 17,243,762 | ||||||

Basic earnings per share | $ | 0.36 | $ | 0.17 | ||||

Diluted Earnings per Share | ||||||||

Numerator: | ||||||||

Net income available to common shareholders | $ | 7,863,247 | $ | 2,974,865 | ||||

Denominator: | ||||||||

Weighted-average shares outstanding | 22,025,316 | 17,243,762 | ||||||

Effect of dilutive securities | ||||||||

Stock options and warrants | 1,178,626 | 1,210,007 | ||||||

Preferred stock | 675,558 | 1,345,220 | ||||||

Diluted weighted-average shares outstanding | 23,879,500 | 19,798,989 | ||||||

Diluted earnings per share | $ | 0.33 | $ | 0.15 | ||||

NOTE 6. COMMON STOCK

The total number of authorized shares of the Company’s common stock is 750,000,000 shares, $0.001 par value per share. As of June 30, 2014, there were 25,019,450 common shares issued and outstanding.

Each share of the Company's common stock is entitled to equal dividends and distributions per share with respect to the common stock when, as and if declared by the Company's board of directors. No holders of any shares of the Company's common stock has a preemptive right to subscribe for any of the Company's securities, nor are any shares of the Company's common stock subject to redemption or convertible into other securities. Upon liquidation, dissolution or winding-up of the Company and after payment of creditors and preferred shareholders of the Company, if any, the assets of the Company will be divided pro rata on a share-for-share basis among the holders of the Company's common stock. Each share of the Company's common stock is entitled to one vote. Shares of the Company's common stock do not possess any cumulative voting rights.

During the six months ended June 30, 2014, a total of 643,444 shares of the Company's Series A Preferred Stock were converted into 643,444 shares of our common stock on a one-for-one basis. Warrants to purchase 6,250 shares of the Company's common stock were exercised for 6,250 shares of common stock with $10,937 of exercise price paid in cash. Options to purchase 483,750 shares of common stock were exercised for a net of 464,148 shares of common stock (when adjusting for a cashless exercise of 186,250 of such options and the payment, in shares of common stock, of an aggregate exercise price of $130,625, along with an exercise price of $200,125 paid in cash in connection with such exercises) and 464,148 shares of common stock were issued to the option holders in connection with such exercises. Additionally, in June 2014, 2,200,000 shares were sold in connection with an underwritten offering of the Company's common stock for net proceeds of $15,803,000 after deducting offering costs of $1,247,000 from the $17,050,000 raised. The shares have a par value per share of $0.001. In May 2014, 500,000 shares of our restricted common stock (valued at $3,266,000) were issued in connection with the initial closing of the Omega Refining acquisition.

In April 2014, the Company granted two employees Incentive Stock Options to purchase an aggregate of 150,000 shares of the Company's common stock, which have a term of ten years, an exercise price of $7.55 per share and vest at the rate of 1/4th of such options per year on each of the first four anniversaries of the grant date.

F-7

VERTEX ENERGY, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2014

(UNAUDITED)

NOTE 7. PREFERRED STOCK

The total number of authorized shares of the Company’s preferred stock is 50,000,000 shares, $0.001 par value per share. The total number of designated shares of the Company’s Series A Preferred Stock is 5,000,000 (“Series A Preferred”). The total number of designated shares of the Company’s Series B Preferred Stock is 2,000,000. As of June 30, 2014, there were 675,558 shares of Series A Preferred Stock issued and outstanding and no Series B Preferred shares issued and outstanding.

NOTE 8. SEGMENT REPORTING

The Company’s reportable segments include the Black Oil, Refining & Marketing and Recovery divisions. Segment information for the six months ended June 30, 2014 and 2013 is as follows:

SIX MONTHS ENDED JUNE 30, 2014 | ||||||||||||||||

Black Oil | Refining & Marketing | Recovery | Total | |||||||||||||

Revenues | $ | 72,449,922 | $ | 38,345,278 | $ | 8,634,080 | $ | 119,429,280 | ||||||||

Income (loss) from operations | $ | 1,137,078 | $ | 1,538,784 | $ | (875,530 | ) | $ | 1,800,332 | |||||||

SIX MONTHS ENDED JUNE 30, 2013 | ||||||||||||||||

Black Oil | Refining & Marketing | Recovery | Total | |||||||||||||

Revenues | $ | 42,692,716 | $ | 23,065,950 | $ | 2,607,538 | $ | 68,366,204 | ||||||||

Income from operations | $ | 784,537 | $ | 1,102,197 | $ | 1,333,859 | $ | 3,220,593 | ||||||||

THREE MONTHS ENDED JUNE 30, 2014 | ||||||||||||||||

Black Oil | Refining & Marketing | Recovery | Total | |||||||||||||

Revenues | $ | 48,878,522 | $ | 18,517,819 | $ | 4,683,281 | $ | 72,079,622 | ||||||||

Income (loss) from operations | $ | 1,116,688 | $ | 768,209 | $ | (1,041,152 | ) | $ | 843,745 | |||||||

THREE MONTHS ENDED JUNE 30, 2013 | ||||||||||||||||

Black Oil | Refining & Marketing | Recovery | Total | |||||||||||||

Revenues | $ | 19,493,407 | $ | 14,234,204 | $ | 1,383,791 | $ | 35,111,402 | ||||||||

Income (loss) from operations | $ | 1,091,268 | $ | 963,842 | $ | (46,191 | ) | $ | 2,008,919 | |||||||

NOTE 9. CONTINGENT CONSIDERATION

As part of the consideration paid related to the August 2012 acquisition of Vertex Holdings, L.P., if certain earnings targets are met, the Company has to pay the seller approximately $2,233,000 annually in each of 2013, 2014 and 2015. In 2013, it had been determined that the 2013 earnings target would not be met and the contingent consideration was reduced by $1,850,000, which represents the discounted cash flow for year one. It had also been determined that there was a 25% probability that the 2014 earnings target would not be met and the contingent consideration was reduced by $388,750, which represents 25% of the discounted cash flows for year two.

F-8

VERTEX ENERGY, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2014

(UNAUDITED)

As part of the consideration paid in connection with the acquisition of E-Source Holding, LLC, if certain targets are met, the Company has to pay the seller approximately $260,000 annually in 2014, 2015, 2016 and 2017. The Company has recorded contingent consideration of $748,000, which is the discounted cash flows of the earn-out payments. In addition, on January 31, 2015, 207,743 shares of the Company's stock will be issued as consideration for the additional equity interest if certain performance metrics are achieved for 2014. As of the date of the transaction, the estimated value of the stock to be issued of approximately $231,000 was recorded as additional paid in capital and a reduction of the non-controlling interest in accordance with ASC 810-10-45.

As part of the consideration paid in connection with the acquisition of Omega Holdings, the Company has agreed to pay the seller additional earn-out consideration in the event that certain EBITDA targets are met (a) during any twelve month period during the eighteen month period commencing on the first day of the first full calendar month following the May 2, 2014 initial closing date (which targets begin at $8,000,000 of EBITDA during such twelve month period) of up to 470,498 shares of common stock of the Company; and (b) during the calendar year ended December 31, 2015 (which targets begin at $9,000,000 of EBITDA) of up to 770,498 shares of common stock of the Company, in each case subject to adjustment for certain capital expenditures.

NOTE 10. ACQUISITION

Omega Refining Transaction

On May 2, 2014, the Company completed its acquisition of substantially all of the assets of Omega Refining, LLC (including the Marrero, Louisiana re-refinery and Omega’s Myrtle Grove complex in Belle Chaise, Louisiana) and ownership of Golden State Lubricant Works, LLC for the purpose of re-refining used lubricating oils into processed oils and other products for the distribution, supply and sale to end-customers with related products and support services. The purchase price paid at the closing was approximately $28,764,000 in cash, 500,000 shares of our restricted common stock (valued at $3,266,000) and the assumption of certain capital lease obligations and other liabilities relating to contracts and leases of Omega Refining in connection with the initial closing. We also agreed to provide Omega a loan in the amount of up to approximately $13.8 million.

The acquisition was accounted for under the purchase method of accounting, with the Company identified as the acquirer. Under the purchase method of accounting, the aggregate amount of consideration paid by the Company was allocated to Omega Refining's net tangible assets and intangible assets based on their estimated fair values as of May 2, 2014. The transaction resulted in a bargain purchase of $6,481,051 recognized in net income as an acquisition-date gain. The Omega purchase qualifies as a bargain purchase since the acquisition date amounts of the identifiable net asset acquired, excluding goodwill ($38.92 million), exceed the value of the consideration transferred ($32.44 million). The difference of $6.48 million is a gain as of the acquisition date. The bargain purchase resulted from the financial distress that Omega was in due to the large amount of debt held by Omega and the unexpected decrease in crack spreads that made the debt level overbearing. Evidence that a bargain purchase exists was seen in the common stock price of the Company, which increased from $3.82 (on March 19, 2014) when the transaction was announced) to $8.10 (on May 2, 2014 when the initial closing occurred). The Company retained an independent third party to assist management in determining the fair value of tangible and intangible assets transferred and liabilities assumed. The allocation of the purchase price is based on the best estimates of management.

The following information summarizes the allocation of the fair values assigned to the assets at the purchase date. The allocation of fair values are preliminary and are subject to change in the future during the measurement period.

F-9

VERTEX ENERGY, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2014

(UNAUDITED)

(in thousands) | ||||

Cash and cash equivalents | $ | 406 | ||

Accounts receivable | 950 | |||

Inventory | 4,192 | |||

Prepaid expenses | 71 | |||

Property, plant and equipment | 30,000 | |||

Deposits | 400 | |||

Bango secured note issued to Vertex | 8,308 | |||

Technology | 2,287 | |||

Non-compete agreements | 66 | |||

Total identifiable net assets | $ | 46,680 | ||

Less liabilities assumed, including contingent consideration | (7,763 | ) | ||

Gain on purchase | (6,481 | ) | ||

Total purchase price | $ | 32,436 | ||

The Company incurred $2,559,830 in costs associated with the Omega Refining acquisition. These included legal, accounting, environmental and investment banking.

The following table summarizes the cost of amortizable intangible assets related to the Omega Refining acquisition:

Estimated Cost (in thousands) | Useful life (years) | |||||

Non-Competes | $ | 66 | 1 | |||

Technology | $ | 2,287 | 15 | |||

Total | $ | 2,353 | ||||

The results of Omega Refining are included in the consolidated financial statements subsequent to May 2, 2014. The following schedule contains pro forma results from operations as if the acquisition had occurred on January 1, 2013. The pro forma results do not report actual results that would have occurred had the merger taken place on January 1, 2013 nor do they necessarily suggest future operating results.

Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

2014 | 2013 | 2014 | 2013 | |||||||||||||

Revenues | $ | 79,747,665 | $ | 68,597,653 | $ | 127,097,323 | $ | 140,850,582 | ||||||||

Income from operations | 498,141 | 335,135 | 1,454,728 | 3,899,588 | ||||||||||||

Net income | 6,284,339 | 116,145 | 7,165,485 | 3,346,949 | ||||||||||||

Net loss attributable to non-controlling interest | 344,380 | — | 325,399 | — | ||||||||||||

Net income attributable to Vertex Energy, Inc. | $ | 6,628,719 | $ | 116,145 | $ | 7,490,884 | $ | 3,346,949 | ||||||||

Earnings per common share | ||||||||||||||||

Basic | $ | 0.29 | $ | 0.01 | $ | 0.34 | $ | 0.19 | ||||||||

Diluted | $ | 0.27 | $ | 0.01 | $ | 0.31 | $ | 0.17 | ||||||||

F-10

VERTEX ENERGY, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2014

(UNAUDITED)

NOTE 11. SUBSEQUENT EVENTS

Subsequent to June 30, 2014, 22,760 shares of the Company's Series A Preferred Stock were converted into 22,760 shares of our common stock on a one-for-one basis.

Subsequent to June 30, 2014, the available credit on the Line of Credit is $20,000,000. As of August 12, 2014, the outstanding balance drawn on the line of credit is $0 leaving an available balance for draw downs of $20,000,000.

On May 2, 2014, we completed the Initial Closing (defined below) contemplated under that certain Asset Purchase Agreement entered into on March 17, 2014, and amended by the First Amendment dated April 14, 2014, Second Amendment dated April 30, 2014 and Third Amendment dated May 2, 2014 (as amended to date, the “Purchase Agreement”) by and among the Company, Vertex Refining LA, LLC and Vertex Refining NV, LLC (“Vertex Refining Nevada”), both wholly-owned subsidiaries of Vertex Operating, Omega Refining, LLC (“Omega Refining”), Bango Refining NV, LLC (“Bango Refining”) and Omega Holdings Company LLC (“Omega Holdings” and collectively with Omega Refining and Bango Refining, “Omega” or the “sellers”).

The acquisition is to close in two separate closings, the first of which relating to the acquisition of Omega Refining (including the Marrero, Louisiana re-refinery and Omega’s Myrtle Grove complex in Belle Chaise, Louisiana) and ownership of Golden State, as described above, closed on May 2, 2014 (the “Initial Closing”), and the second of which relating to the acquisition of Bango Refining and the Bango, Nevada plant, is expected to close on or around September 2014, subject to certain closing conditions being met prior to closing (the “Final Closing”). Vertex’s obligation to consummate the Final Closing is subject to among other things, compliance with certain provisions of the credit agreements described herein and that the Bango plant operated by Bango Refining be fully restored and operational, as well as the plant meeting certain used motor oil processing run rates and that there are no adverse claims or legal proceedings related to an accident that occurred at the Bango plant in December 2013.

The amount due at the Final Closing, in consideration for the acquisition of Bango Refining, will be the assumption of certain loans made pursuant to the Omega Secured Note (described below), the issuance of 1,500,000 shares of Vertex’s common stock of which 650,000 shares (with an agreed value of $3.2301 per share or approximately $2.1 million) will be held in escrow (the “Pledged Shares”) and used to satisfy indemnification claims and secure the repayment of the Omega Secured Note (defined below), and which amount is subject to adjustment in the event minimum inventory levels are not delivered at the Final Closing, and the assumption of certain capital lease obligations and other liabilities relating to contracts and leases of Bango Refining. A portion of the Pledged Shares will be released from escrow, subject to outstanding claims, on September 15, 2015, and the remainder will be released on the 18 month anniversary of the Final Closing. Subject to certain negotiated exceptions for excluded liabilities, taxes and other fundamental items, the sellers’ indemnification obligations are capped at $5 million.

The consideration payable in connection with the Final Closing is subject to customary adjustments prior to the Final Closing depending on certain criteria, including the amount of inventory delivered by the sellers at the Final Closing.

The sellers also have the right to earn additional earn-out consideration in the event certain EBITDA targets are met by (a) Vertex Refining NV, LLC during the years ended December 31, 2015 and 2016 (which targets begin at $3.5 million of EBITDA per year), of up to an aggregate of $6 million (payable in shares of the Company’s common stock equal to the volume-weighted average of the regular session closing prices per share of the Company’s common stock on the NASDAQ Capital Market for the ten (10) consecutive trading days prior to the applicable due date of such payments, provided, however, in no event shall the VWAP be less than $3.15 per share or more than $10.00 per share, as adjusted for any stock splits or recapitalizations); (b) Vertex Refining LA, LLC during any twelve month period during the eighteen month period commencing on the first day of the first full calendar month following the Initial Closing date (which targets begin at $8 million of EBITDA during such twelve month period) of up to 470,498 shares of common stock of the Company; and (c) Vertex Refining LA, LLC during the calendar year ended December 31, 2015 (which targets begin at $9 million of EBITDA) of up to 770,498 shares of common stock of the Company, in each case subject to adjustment for certain capital expenditures (collectively, the “Earn-Outs). Notwithstanding the above, the maximum number of shares of common stock to be issued pursuant to the Purchase Agreement cannot (i) exceed 19.9% of the outstanding shares of common stock outstanding on March 17, 2014, (ii) exceed 19.9% of the combined voting power of the Company on March 17, 2014, or (iii) otherwise exceed such number of shares of common stock that would violate applicable listing rules of the NASDAQ Stock Market in the event the Company’s stockholders do not approve the issuance of such shares (the “Share Cap”). In the event the number of shares to be issued under the Purchase Agreement exceeds the Share Cap, then the Company is required to instead pay any such additional consideration in cash or obtain the approval of the Company’s stockholders under applicable rules and requirements of the NASDAQ Capital Market for the additional issuance of shares.

F-11

VERTEX ENERGY, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2014

(UNAUDITED)

Finally, pursuant to the acquisition, (a) with certain exceptions related to sellers’ operation of Bango Refining between the Initial Closing and the Final Closing, the sellers agreed to enter into a non-competition agreement whereby they agreed not to compete against Vertex in connection with the acquired businesses, or to solicit active customers of the acquired businesses for a period of five years and (b) certain of the employees of the sellers agreed to enter into three year employment agreements with Vertex’s newly formed subsidiaries.

Additionally, we were required to file and obtain effectiveness of a registration statement within 90 days following the Initial Closing (if the Securities and Exchange Commission did not review the filing) and 150 days following the Initial Closing (if the Securities and Exchange Commission did review the filing), registering the shares of common stock issuable in connection with the acquisition, which registration statement was declared effective on July 29, 2014.

The Final Closing remains subject to the satisfaction of certain customary closing conditions. The Purchase Agreement contains customary representations, warranties, covenants and indemnities by the parties thereto. Craig-Hallum Capital Group LLC is acting as exclusive financial advisor to the Company in connection with the acquisition and has provided a fairness opinion to the Board of Directors in connection with the transaction.

On July 30, 2014 the Company announced that it has begun due diligence of Heartland Group Holdings LLC ("Heartland") under the terms of a letter of intent which contemplates Vertex acquiring substantially all of the assets of Heartland for approximately $16.5 million, which includes an approximate $8 million dollar earnout achievable during the first 2 years.

Along with the Letter of Intent, Vertex also entered into a consulting agreement with Heartland to provide consulting services, which include advice and guidance related to Heartland petroleum’s collection operations, Heartland’s Re-refinery, the installation of new equipment there, and the implementation of operational changes at the re-refinery. The objective is to eventually facilitate the integration of all of Heartland's operations into Vertex’s platform, allowing for a smooth transition upon the closing of the transaction. Vertex has agreed to cover expenses throughout implementation of these changes and to reimburse Heartland for any operating losses recognized after July 16, 2014, subject to a cap of $500,000 if Vertex decides not to move forward with the closing, and which losses are reimbursable to Vertex if Heartland breaches the terms of the letter of intent.

The acquisition remains subject to due diligence, the negotiation of definitive purchase agreements, satisfaction of closing conditions, and receipt of required consents and approvals. The parties plan to enter into definitive purchase agreements by the end of September 2014, and tentatively plan to close the acquisition, subject to the negotiated conditions of closing being met by the end of October 2014.

F-12

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

This Report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. In some cases, you can identify forward-looking statements by the following words: “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “ongoing,” “plan,” “potential,” “predict,” “project,” “should,” or the negative of these terms or other comparable terminology, although not all forward-looking statements contain these words. Forward-looking statements are not a guarantee of future performance or results, and will not necessarily be accurate indications of the times at, or by, which such performance or results will be achieved. Forward-looking statements are based on information available at the time the statements are made and involve known and unknown risks, uncertainties and other factors that may cause our results, levels of activity, performance or achievements to be materially different from the information expressed or implied by the forward-looking statements in this Report. These factors include:

• | risks associated with our outstanding credit facilities, including amounts owed, restrictive covenants and security interests thereon; |

• | the level of competition in our industry and our ability to compete; |

• | our ability to respond to changes in our industry; |

• | the loss of key personnel or failure to attract, integrate and retain additional personnel; |

• | our ability to protect our intellectual property and not infringe on others’ intellectual property; |

• | our ability to scale our business; |

• | our ability to maintain supplier relationships and obtain adequate supplies of feedstocks; |

• | our ability to obtain and retain customers; |

• | our ability to produce our products at competitive rates; |

• | our ability to execute our business strategy in a very competitive environment; |

• | trends in, and the market for, the price of oil and gas and alternative energy sources; |

• | our ability to maintain our relationship with KMTEX, Ltd.; |

• | the impact of competitive services and products; |

• | our ability to maintain insurance; |

• | potential future litigation, judgments and settlements; |

• | rules and regulations making our operations more costly or restrictive; |

• | changes in environmental and other laws and regulations and risks associated with such laws and regulations; |

• | economic downturns both in the United States and globally; |

• | risk of increased regulation of our operations and products; |

• | negative publicity and public opposition to our operations; |

• | disruptions in the infrastructure that we and our partners rely on; |

• | an inability to identify attractive acquisition opportunities and successfully negotiate acquisition terms; |

• | our ability to effectively integrate acquired assets, companies, employees or businesses; |

• | liabilities associated with acquired companies, assets or businesses; |

• | interruptions at our facilities; |

• | our ability to complete pending acquisitions; |

• | required earn-out payments and other contingent payments we are required to make; |

• | unexpected changes in our anticipated capital expenditures resulting from unforeseen required maintenance, repairs, or upgrades; |

• | our ability to acquire and construct new facilities; |

• | our ability to effectively manage our growth; |

• | repayment of and covenants in our debt facilities; |

• | the lack of capital available on acceptable terms to finance our continued growth; and |

• | other risk factors included under “Risk Factors” below and in our Annual Report on Form 10-K. |

13

You should read the matters described in “Risk Factors” below and disclosed in the Company’s Annual Report on Form 10-K, filed with the Commission on March 25, 2014, and the other cautionary statements made in this Report as being applicable to all related forward-looking statements wherever they appear in this Report. We cannot assure you that the forward-looking statements in this Report will prove to be accurate and therefore prospective investors are encouraged not to place undue reliance on forward-looking statements. Other than as required by law, we undertake no obligation to update or revise these forward-looking statements, even though our situation may change in the future.

Please see the “Glossary of Selected Terms” incorporated by reference hereto as Exhibit 99.1, for a list of abbreviations and definitions used throughout this Report.

In this Quarterly Report on Form 10-Q, we may rely on and refer to information regarding the refining, re-refining, used oil and oil and gas industries in general from market research reports, analyst reports and other publicly available information. Although we believe that this information is reliable, we cannot guarantee the accuracy and completeness of this information, and we have not independently verified any of it.

Corporate History of the Registrant:

Vertex Energy, Inc. (the “Company,” “we,” “us,” and “Vertex”) was formed as a Nevada corporation on May 14, 2008. Pursuant to an Amended and Restated Agreement and Plan of Merger dated May 19, 2008, by and between Vertex Holdings, L.P. (formerly Vertex Energy, L.P.), a Texas limited partnership ("Holdings"), us, World Waste Technologies, Inc., a California corporation (“WWT” or “World Waste”), Vertex Merger Sub, LLC, a California limited liability company and our wholly-owned subsidiary ("Merger Subsidiary"), and Benjamin P. Cowart, our Chief Executive Officer, as agent for our shareholders (as amended from time to time, the “Merger Agreement”). Effective on April 16, 2009, World Waste merged with and into Merger Subsidiary, with Merger Subsidiary continuing as the surviving corporation and becoming our wholly-owned subsidiary (the "Merger"). In connection with the Merger, (i) each outstanding share of World Waste common stock was cancelled and exchanged for 0.10 shares of our common stock; (ii) each outstanding share of World Waste Series A preferred stock was cancelled and exchanged for 0.4062 shares of our Series A preferred stock; and (iii) each outstanding share of World Waste Series B preferred stock was cancelled and exchanged for 11.651 shares of our Series A preferred stock. Additionally, as a result of the Merger, the common stock of World Waste was effectively reversed one for ten (10) as a result of the exchange ratios set forth in the Merger, and unless otherwise noted, the impact of such effective reverse stock split, created by the exchange ratio set forth above, is retroactively reflected throughout this Report.

Finally, as a result of the Merger, as the successor entity of World Waste, we assumed World Waste’s filing obligations with the Securities and Exchange Commission and our common stock began trading on the Over-The-Counter Bulletin Board under the symbol “VTNR.OB” effective May 4, 2009. Subsequently, effective February 13, 2013, our common stock began trading on the NASDAQ Capital Market under the symbol “VTNR".

Material Acquisitions

Holdings:

Effective as of August 31, 2012, we acquired 100% of the outstanding equity interests of Vertex Acquisition Sub, LLC (“Acquisition Sub”), a special purpose entity consisting of substantially all of the assets of Holdings and real-estate properties of B & S Cowart Family L.P. (“B&S LP” and the “Acquisition”), both of which entities were owned and operated by related parties. Prior to closing the Acquisition, Holdings contributed to Acquisition Sub substantially all of its assets and liabilities relating to the business of transporting, storing, processing and re-refining petroleum products, crudes and used lubricants, including all of the outstanding equity interests in Holdings’ wholly-owned operating subsidiaries, Cedar Marine Terminals, L.P. (“CMT”), Crossroad Carriers, L.P. (“Crossroad”), Vertex Recovery, L.P. (“Vertex Recovery”) and H&H Oil, L.P. (“H&H Oil”, and collectively, the “Transferred Partnerships”), and B&S LP contributed real estate associated with the operations of H&H Oil.

We paid the following consideration for 100% of the equity interests in Acquisition Sub (the “Purchase Price”): (i) to Holdings, (a) $14.8 million in cash and assumed debt; and (b) 4,545,455 million restricted shares of our common stock; and (ii) to B&S LP, $1.7 million cash consideration, representing the appraised value of certain real estate contributed by B&S LP to Acquisition Sub. Additionally, for each of the three one-year periods following September 11, 2012, the closing date of the transaction, Holdings will be eligible to receive earn-out payments of $2.23 million, up to $6.7 million in the aggregate (the “Earn-Out Payments”), contingent on the combined company achieving adjusted EBITDA targets of $10.75 million, $12.0 million and $13.5 million, respectively, in those periods. In 2013 it was determined that the 2013 earnings target would not be met and the contingent consideration was reduced by $1,850,000, which represents the discounted cash flow for year one. It was also determined

14

that there is a 25% probability that the 2014 earnings target will not be met and the contingent consideration was reduced by $388,750, which represents 25% of the discounted cash flow for year two.

We had numerous relationships and related-party transactions with Holdings and its subsidiaries prior to the closing of the Acquisition, including the lease of a storage facility, the subletting of office space, and agreements to operate the Thermal Chemical Extraction Process ("TCEP") (described below) facility and to transport and store feedstock and end products. The closing of the Acquisition eliminated these related-party transactions. The description of our operations below reflects the closing of the Acquisition, unless otherwise stated or the discussion requires otherwise.

E-Source:

Effective October 1, 2013 Vertex acquired a 51% interest in E-Source Holdings, LLC (“E-Source”), a company that leases and operates a facility located in Houston, Texas, and provides dismantling, demolition, decommission and marine salvage services at industrial facilities throughout the Gulf Coast. E-Source also owns and operates a fleet of trucks and other vehicles used for shipping and handling equipment and scrap materials. The consideration paid for the acquisition of E-Source was approximately $900,000 and the right of one of the sellers (the “Earn-Out Seller”) to earn additional earn-out payments of up to 15% of E-Source’s net income before taxes, in the event certain calendar year net income thresholds are met, in calendar years 2014 through 2017, as well as a commission of 20% of the net income before taxes associated with certain future planned projects of E-Source required to be completed prior to December 31, 2014, as long as such applicable seller remains an employee of E-Source during such applicable periods. Effective on March 14, 2014, we entered into an amendment to our acquisition agreement with the Earn-Out Seller, and mutually agreed that the lesser of (a) 20% and (b) $100,000, per calendar year of earn-out payments due the Earn-Out Seller, if any, will be payable in shares of our restricted common stock, based on the average of the five closing sales prices of the Company’s common stock on the first five trading days of each applicable calendar year (each a “Valuation”) for which the earn-out consideration relates, provided that the parties mutually agreed to use a valuation of $3.2922 per share (the “2014 Valuation Price”) for any earn-out payments relating to the 2014 calendar year and further agreed that in no event will any future calendar year Valuation be less than the 2014 Valuation Price. On March 26, 2014, but effective January 1, 2014, the Company acquired an additional 19% interest in E-Source for $854,050 in cash consideration and the right to receive stock consideration (on January 31, 2015) in the amount of 207,743 shares of stock subject to certain performance metrics being met during 2014.

E-Source leases and operates a plant located in Houston, Texas, and provides dismantling, demolition, decommission and marine salvage services at industrial facilities throughout the Gulf Coast. E-Source also owns and operates a fleet of trucks and other vehicles used for shipping and handling equipment and scrap materials.

Omega:

On May 2, 2014, we completed the Initial Closing (defined below) contemplated under the Asset Purchase Agreement entered into on March 17, 2014, and amended by the First Amendment dated April 14, 2014, Second Amendment dated April 30, 2014 and Third Amendment dated May 2, 2014 (as amended to date, the “Purchase Agreement”) by and among the Company, Vertex Refining LA, LLC and Vertex Refining NV, LLC (“Vertex Refining Nevada”), both wholly-owned subsidiaries of Vertex Operating, LLC (“Vertex Operating”), Omega Refining, LLC (“Omega Refining”), Bango Refining NV, LLC (“Bango Refining”) and Omega Holdings Company LLC (“Omega Holdings” and collectively with Omega Refining and Bango Refining, “Omega” or the “sellers”).

Pursuant to the Purchase Agreement, we agreed to acquire certain of Omega’s assets related to (1) the operation of oil re-refineries and, in connection therewith, purchasing used lubricating oils and re-refining such oils into processed oils and other products for the distribution, supply and sale to end-customers and (2) the provision of related products and support services. Specifically, the assets included Omega’s Marrero, Louisiana and Bango, Nevada, re-refineries (which re-refine approximately 80 million gallons of used motor oil per year). Additionally, the Marrero, Louisiana plant produces vacuum gas oil (VGO) and the Bango, Nevada plant produces base lubricating oils. Omega also operates Golden State Lubricants Works, LLC (“Golden State”), a strategic blending and storage facility located in Bakersfield, California, which is included in the acquisition. In connection with the acquisition, we also acquired certain of Omega’s prepaid assets and inventory.

The acquisition is to close in two separate closings, the first of which relating to the acquisition of Omega Refining (including the Marrero, Louisiana re-refinery and Omega’s Myrtle Grove complex in Belle Chaise, Louisiana) and ownership of Golden State, as described above, closed on May 2, 2014 (the “Initial Closing”), and the second of which relating to the acquisition of Bango Refining and the Bango, Nevada plant, is expected to close on or around September 2014, subject to certain closing

15

conditions being met prior to closing (the “Final Closing”). Vertex’s obligation to consummate the Final Closing is subject to among other things, compliance with certain provisions of the credit agreements described herein and that the Bango plant operated by Bango Refining be fully restored and operational, as well as the plant meeting certain used motor oil processing run rates and that there are no adverse claims or legal proceedings related to an accident that occurred at the Bango plant in December 2013.

The purchase price paid at the Initial Closing was approximately $28,764,000 in cash (which funds we raised pursuant to our entry into the Credit Agreements, described below under “Liquidity and Capital Resources”), 500,000 shares of our restricted common stock (valued at $3,266,000) and the assumption of certain capital lease obligations and other liabilities relating to contracts and leases of Omega Refining in connection with the Initial Closing. We also agreed to provide Omega a loan in the amount of up to approximately $13.8 million (described below).

The amount due at the Final Closing, in consideration for the acquisition of Bango Refining, will be the assumption of certain loans made pursuant to the Omega Secured Note (described below), the issuance of 1,500,000 shares of Vertex’s common stock of which 650,000 shares (with an agreed value of $3.2301 per share or approximately $2.1 million) will be held in escrow (the “Pledged Shares”) and used to satisfy indemnification claims and secure the repayment of the Omega Secured Note (defined below), and which amount is subject to adjustment in the event minimum inventory levels are not delivered at the Final Closing, and the assumption of certain capital lease obligations and other liabilities relating to contracts and leases of Bango Refining. A portion of the Pledged Shares will be released from escrow, subject to outstanding claims, on September 15, 2015, and the remainder will be released on the 18 month anniversary of the Final Closing. Subject to certain negotiated exceptions for excluded liabilities, taxes and other fundamental items, the sellers’ indemnification obligations are capped at $5 million.

In connection with the First Closing, Omega Refining and Bango Refining provided Vertex Refining Nevada a Secured Promissory Note (the “Omega Secured Note”) in the aggregate amount of $13,858,067, representing (a) a loan to Omega in the amount of approximately $7.56 million (representing the agreed upon value of the amount by which the consideration paid at the Initial Closing (which included consideration relating to the assets acquired at the Initial Closing and which will be acquired at the Final Closing) exceeded the value of assets acquired at the Initial Closing) (the “Purchase Price Loan”); (b) a $750,000 loan related to the delivery of a certain amount of used motor oil inventory at the Initial Closing (the “First Inventory Loan”); (c) a $1,400,000 loan related to the delivery of a certain amount of used motor oil inventory at the Final Closing (the “Second Inventory Loan” and along with the First Inventory Loan, the “Inventory Loans”); (d) a loan in a single advance of $3.15 million to satisfy accounts payable and other working capital related obligations of Omega after the Initial Closing, provided such loans are not required to be made until after June 16, 2014 (the “Draw Down Loan”) and (e) an additional loan of up to $1 million for capital expenditures, if mutually approved by us and Omega (the “Capital Expenditure Loan”). The Purchase Price Loan and the Draw Down Loan bear interest at the short-term federal rate as published by the Internal Revenue Service from time to time (currently 0.33% per annum) prior to October 30, 2014, and thereafter at 9.5% per annum, payable monthly in arrears and have a maturity date of March 31, 2015. The First Inventory Loan and the Draw Down Loan accrue interest at the rate of 9.5% per annum beginning on May 31, 2014, and are due and payable on March 31, 2015. Upon an event of default under any of the loans, the loans accrue interest at 18% per annum until paid in full. The Purchase Price Loan and the Draw Down Loan are due and payable in full on the earlier of March 31, 2015 and the date of the Final Closing, provided that both the Purchase Price Loan and Draw Down Loan (including accrued and unpaid interest thereon) will be deemed paid in full upon the Final Closing. The Omega Secured Note may be prepaid in whole or part from time to time without penalty.

The repayment of the Omega Secured Note is guaranteed by Omega Holdings pursuant to a Guaranty Agreement and secured by a security interest granted pursuant to the terms of the Omega Secured Note and a Leasehold Deed of Trust, Security Agreement, Assignment of Leases and Rents and Fixture Filing. Additionally, we have the right to set-off any amount due upon an event of default against certain of the Pledged Shares and the earn-out consideration described below, of which a portion of such shares were pledged to secure the Omega Secured Note pursuant to a Pledge Agreement, subject to the terms of the Purchase Agreement.

The consideration payable in connection with the Final Closing is subject to customary adjustments prior to the Final Closing depending on certain criteria, including the amount of inventory delivered by the sellers at the Final Closing.

The sellers also have the right to earn additional earn-out consideration in the event certain EBITDA targets are met by (a) Vertex Refining NV, LLC during the years ended December 31, 2015 and 2016 (which targets begin at $3.5 million of EBITDA per year), of up to an aggregate of $6 million (payable in shares of the Company’s common stock equal to the volume-weighted average of the regular session closing prices per share of the Company’s common stock on the NASDAQ Capital Market for the ten (10) consecutive trading days prior to the applicable due date of such payments, provided, however, in no event shall the VWAP be less than $3.15 per share or more than $10.00 per share, as adjusted for any stock splits or recapitalizations); (b) Vertex Refining

16

LA, LLC during any twelve month period during the eighteen month period commencing on the first day of the first full calendar month following the Initial Closing date (which targets begin at $8 million of EBITDA during such twelve month period) of up to 470,498 shares of common stock of the Company; and (c) Vertex Refining LA, LLC during the calendar year ended December 31, 2015 (which targets begin at $9 million of EBITDA) of up to 770,498 shares of common stock of the Company, in each case subject to adjustment for certain capital expenditures (collectively, the “Earn-Outs). Notwithstanding the above, the maximum number of shares of common stock to be issued pursuant to the Purchase Agreement cannot (i) exceed 19.9% of the outstanding shares of common stock outstanding on March 17, 2014, (ii) exceed 19.9% of the combined voting power of the Company on March 17, 2014, or (iii) otherwise exceed such number of shares of common stock that would violate applicable listing rules of the NASDAQ Stock Market in the event the Company’s stockholders do not approve the issuance of such shares (the “Share Cap”). In the event the number of shares to be issued under the Purchase Agreement exceeds the Share Cap, then the Company is required to instead pay any such additional consideration in cash or obtain the approval of the Company’s stockholders under applicable rules and requirements of the NASDAQ Capital Market for the additional issuance of shares.

Finally, pursuant to the acquisition, (a) with certain exceptions related to sellers’ operation of Bango Refining between the Initial Closing and the Final Closing, the sellers agreed to enter into a non-competition agreement whereby they agreed not to compete against Vertex in connection with the acquired businesses, or to solicit active customers of the acquired businesses for a period of five years and (b) certain of the employees of the sellers agreed to enter into three year employment agreements with Vertex’s newly formed subsidiaries.

Additionally, we were required to file and obtain effectiveness of a registration statement within 90 days following the Initial Closing (if the Securities and Exchange Commission did not review the filing) and 150 days following the Initial Closing (if the Securities and Exchange Commission did review the filing), registering the shares of common stock issuable in connection with the acquisition, which registration statement was declared effective on July 29, 2014.

We obtained rights to certain material agreements and contracts of Omega Refining in connection with the Initial Closing, including obligations under Omega Refining’s capital leases and rights under a Terminaling Services Agreement dated May 1, 2008, originally between Omega Refining and Marrero Terminal LLC (the “Terminaling Agreement”) and a Second Used Motor Oil Buy/Sell Contract originally between Omega Refining and Thermo Fluids Inc. dated August 1, 2012 (the “Used Oil Contract”). Pursuant to the Terminaling Agreement, Marrero Terminal LLC agreed to provide certain terminaling services at the Marrero, Louisiana facility, subject to the terms of the agreement, including the use of tanks for storage in consideration for certain per barrel storage and throughput fees. The Terminaling Agreement has a term through April 30, 2018, subject to the right to extend such agreement pursuant to the terms thereof. Pursuant to the Used Oil Contract, we are required to purchase from Thermo Fluids Inc. an aggregate of a minimum of 26 million gallons of used motor oil through the end of the term of the agreement, December 31, 2014, with certain required minimum monthly and yearly volumes. We are required to pay Thermo Fluids Inc. consideration based on a discount to the average low posting of Platts U.S. Gulf Coast No. 6 Fuel Oil, plus in some cases additional consideration per barrel, for all used motor oil purchased pursuant to the agreement, subject to certain adjustments provided for in the agreement.

The Final Closing remains subject to the satisfaction of certain customary closing conditions. The Purchase Agreement contains customary representations, warranties, covenants and indemnities by the parties thereto. Craig-Hallum Capital Group LLC is acting as exclusive financial advisor to the Company in connection with the acquisition and has provided a fairness opinion to the Board of Directors in connection with the transaction.

Description of Business Activities:

We are an environmental services company that recycles industrial waste streams and off-specification commercial chemical products. Our primary focus is recycling used motor oil and other petroleum by-products. We are engaged in operations across the entire petroleum recycling value chain including collection, aggregation, transportation, storage, refinement, and sales of aggregated feedstock and re-refined products to end users. We operate in three divisions- the Black Oil, Refining and Marketing and Recovery divisions. Our Black Oil division collects and purchases used motor oil directly from third-party generators, aggregates used motor oil from an established network of local and regional collectors, and sells used motor oil to our customers for use as a feedstock or replacement fuel for industrial burners. Our Refining and Marketing division aggregates and manages the re-refinement of used motor oil and other petroleum by-products and sells the re-refined products to end customers. Our Recovery division is a generator solutions company for the proper recovery and management of hydrocarbon streams. We operate a refining facility that uses our proprietary TCEP technology and we also utilize third-party processing facilities.

We recently acquired a 70% interest in E-Source (as described above) a company that leases and operates a facility located in Houston, Texas, and provides dismantling, demolition, decommission and marine salvage services at industrial facilities throughout the Gulf Coast. E-Source also owns and operates a fleet of trucks and other vehicles used for shipping and handling

17

equipment and scrap materials. We also recently acquired Omega's Marrero, Louisiana re-refinery and Myrtle Grove complex in Belle Chasse, Louisiana and ownership of Golden State, as described above. The Marrero, Louisiana facility re-refines used motor oil and also produces vacuum gas oil. Golden State operates a strategic blending and storage facility located in Bakersfield, California.

Black Oil Division

Our Black Oil division is engaged in operations across the entire used motor oil recycling value chain including collection, aggregation, transportation, storage, refinement, and sales of aggregated feedstock and re-refined products to end users. We collect and purchase used oil directly from generators such as oil change service stations, automotive repair shops, manufacturing facilities, petroleum refineries, and petrochemical manufacturing operations. We collect and purchase used oil directly from generators such as oil change service stations, automotive repair shops, manufacturing facilities, petroleum refineries, and petrochemical manufacturing operations. We own a fleet of 13 collection vehicles which routinely visit generators to collect and purchase used motor oil. We also aggregate used oil from a diverse network of approximately 50 suppliers who operate similar collection businesses to ours.

We manage the logistics of transport, storage and delivery of used oil to our customers. We own a fleet of seven transportation trucks and more than 90 aboveground storage tanks with over 4.5 million gallons of storage capacity. These assets are used by both the Black Oil division and the Refining and Marketing division. In addition, we also utilize third parties for the transportation and storage of used oil feedstocks. Typically, we sell used oil to our customers in bulk to ensure efficient delivery by truck, rail, or barge. In many cases, we have contractual purchase and sale agreements with our suppliers and customers, respectively. We believe these contracts are beneficial to all parties involved because it ensures that a minimum volume is purchased from collectors and generators, a minimum volume is sold to our customers, and we are able to minimize our inventory risk by a spread between the costs to acquire used oil and the revenues received from the sale and delivery of used oil. We also use our proprietary TCEP technology to re-refine used oil into marine fuel cutterstock and a higher-value feedstock for further processing. In addition at our Marrero facility we produce a Vacuum Gas Oil (VGO) product that is sold to refineries as well as to the marine fuels market.

Refining and Marketing Division