Attached files

| file | filename |

|---|---|

| EX-32 - EXHIBIT 32 - GATX CORP | gatx-20180930xexhibit32.htm |

| EX-31.B - EXHIBIT 31B - GATX CORP | gatx-20180930xexhibit31b.htm |

| EX-31.A - EXHIBIT 31A - GATX CORP | gatx-20180930xexhibit31a.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

__________________________________________

FORM 10-Q

__________________________________________

x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2018

or

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number: 1-2328

GATX Corporation

(Exact name of registrant as specified in its charter)

New York | 36-1124040 |

(State of incorporation) | (I.R.S. Employer Identification No.) |

233 South Wacker Drive | |

Chicago, Illinois 60606-7147 | |

(Address of principal executive offices, including zip code) | |

(312) 621-6200 | |

(Registrant's telephone number, including area code) | |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

x | Large accelerated filer | ¨ | Smaller reporting company | ||

¨ | Non-accelerated filer | ¨ | Emerging growth company | ||

¨ | Accelerated filer | ||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

Common shares outstanding were 37.6 million at September 30, 2018.

GATX CORPORATION

FORM 10-Q

QUARTERLY REPORT FOR THE PERIOD ENDED SEPTEMBER 30, 2018

INDEX

Item No. | Page No. | |

Part I - FINANCIAL INFORMATION | ||

Item 1. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

Part II - OTHER INFORMATION | ||

Item 1. | ||

Item 1A. | ||

Item 2. | ||

Item 6. | ||

FORWARD-LOOKING STATEMENTS

Statements in this report not based on historical facts are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 and, accordingly, involve known and unknown risks and uncertainties that are difficult to predict and could cause our actual results, performance, or achievements to differ materially from those discussed. These include statements as to our future expectations, beliefs, plans, strategies, objectives, events, conditions, financial performance, prospects, or future events. In some cases, forward-looking statements can be identified by the use of words such as “may,” “could,” “expect,” “intend,” “plan,” “seek,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” “outlook,” “continue,” “likely,” “will,” “would”, and similar words and phrases. Forward-looking statements are necessarily based on estimates and assumptions that, while considered reasonable by us and our management, are inherently uncertain. Accordingly, you should not place undue reliance on forward-looking statements, which speak only as of the date they are made, and are not guarantees of future performance. We do not undertake any obligation to publicly update or revise these forward-looking statements.

A detailed discussion of the known material risks and uncertainties that could cause actual results and events to differ materially from such forward-looking statements is included in our Annual Report on Form 10-K for the year ended December 31, 2017, and in our other filings with the Securities and Exchange Commission ("SEC"). The following factors, in addition to those discussed under "Risk Factors", in our Annual Report on Form 10-K for the year ended December 31, 2017, could cause actual results to differ materially from our current expectations expressed in forward looking statements:

• exposure to damages, fines, criminal and civil penalties, and reputational harm arising from a negative outcome in litigation, including claims arising from an accident involving our railcars • inability to maintain our assets on lease at satisfactory rates due to oversupply of railcars in the market or other changes in supply and demand• a significant decline in customer demand for our railcars or other assets or services, including as a result of:◦ weak macroeconomic conditions◦ weak market conditions in our customers' businesses◦ declines in harvest or production volumes◦ adverse changes in the price of, or demand for, commodities◦ changes in railroad operations or efficiency◦ changes in supply chains◦ availability of pipelines, trucks, and other alternative modes of transportation◦ other operational or commercial needs or decisions of our customers• higher costs associated with increased railcar assignments following non-renewal of leases, customer defaults, and compliance maintenance programs or other maintenance initiatives• events having an adverse impact on assets, customers, or regions where we have a concentrated investment exposure• financial and operational risks associated with long-term railcar purchase commitments, including increased costs due to tariffs or trade disputes• reduced opportunities to generate asset remarketing income | • operational and financial risks related to our affiliate investments, including the Rolls-Royce & Partners Finance joint ventures (collectively the "RRPF affiliates")• the impact of changes to the Internal Revenue Code as a result of the Tax Cuts and Jobs Act of 2017 (the "Tax Act"), and uncertainty as to how this legislation will be interpreted and applied.• fluctuations in foreign exchange rates• failure to successfully negotiate collective bargaining agreements with the unions representing a substantial portion of our employees• asset impairment charges we may be required to recognize• deterioration of conditions in the capital markets, reductions in our credit ratings, or increases in our financing costs• competitive factors in our primary markets, including competitors with a significantly lower cost of capital than GATX• risks related to our international operations and expansion into new geographic markets, including the imposition of new or additional tariffs, quotas, or trade barriers• changes in, or failure to comply with, laws, rules, and regulations• inability to obtain cost-effective insurance • environmental remediation costs• inadequate allowances to cover credit losses in our portfolio• inability to maintain and secure our information technology infrastructure from cybersecurity threats and related disruption of our business | |

1

PART I - FINANCIAL INFORMATION

Item 1. Financial Statements

GATX CORPORATION AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS (Unaudited)

(In millions, except share data)

September 30 | December 31 | ||||||

2018 | 2017 | ||||||

Assets | |||||||

Cash and Cash Equivalents | $ | 254.5 | $ | 296.5 | |||

Restricted Cash | 4.1 | 3.2 | |||||

Receivables | |||||||

Rent and other receivables | 85.2 | 83.4 | |||||

Finance leases | 129.0 | 136.1 | |||||

Less: allowance for losses | (6.5 | ) | (6.4 | ) | |||

207.7 | 213.1 | ||||||

Operating Assets and Facilities | 9,262.9 | 9,045.4 | |||||

Less: allowance for depreciation | (2,965.0 | ) | (2,853.3 | ) | |||

6,297.9 | 6,192.1 | ||||||

Investments in Affiliated Companies | 478.5 | 441.0 | |||||

Goodwill | 83.6 | 85.6 | |||||

Other Assets | 191.1 | 190.9 | |||||

Total Assets | $ | 7,517.4 | $ | 7,422.4 | |||

Liabilities and Shareholders’ Equity | |||||||

Accounts Payable and Accrued Expenses | $ | 152.8 | $ | 154.3 | |||

Debt | |||||||

Commercial paper and borrowings under bank credit facilities | — | 4.3 | |||||

Recourse | 4,397.3 | 4,371.7 | |||||

Capital lease obligations | 11.6 | 12.5 | |||||

4,408.9 | 4,388.5 | ||||||

Deferred Income Taxes | 890.7 | 853.7 | |||||

Other Liabilities | 227.0 | 233.2 | |||||

Total Liabilities | 5,679.4 | 5,629.7 | |||||

Shareholders’ Equity | |||||||

Common stock, $0.625 par value: Authorized shares — 120,000,000 Issued shares — 67,325,950 and 67,083,149 Outstanding shares — 37,632,377 and 37,895,641 | 41.6 | 41.6 | |||||

Additional paid in capital | 703.6 | 698.0 | |||||

Retained earnings | 2,387.0 | 2,261.7 | |||||

Accumulated other comprehensive loss | (157.8 | ) | (109.6 | ) | |||

Treasury stock at cost (29,693,573 and 29,187,508 shares) | (1,136.4 | ) | (1,099.0 | ) | |||

Total Shareholders’ Equity | 1,838.0 | 1,792.7 | |||||

Total Liabilities and Shareholders’ Equity | $ | 7,517.4 | $ | 7,422.4 | |||

See accompanying notes to consolidated financial statements.

2

GATX CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (Unaudited)

(In millions, except per share data)

Three Months Ended September 30 | Nine Months Ended September 30 | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Revenues | |||||||||||||||

Lease revenue | $ | 271.9 | $ | 276.6 | $ | 816.1 | $ | 823.4 | |||||||

Marine operating revenue | 60.8 | 62.9 | 130.8 | 135.0 | |||||||||||

Other revenue | 17.0 | 20.1 | 57.6 | 65.7 | |||||||||||

Total Revenues | 349.7 | 359.6 | 1,004.5 | 1,024.1 | |||||||||||

Expenses | |||||||||||||||

Maintenance expense | 77.5 | 84.9 | 240.7 | 247.7 | |||||||||||

Marine operating expense | 39.4 | 38.9 | 89.5 | 89.8 | |||||||||||

Depreciation expense | 81.6 | 78.6 | 240.1 | 227.9 | |||||||||||

Operating lease expense | 11.8 | 15.8 | 37.5 | 46.8 | |||||||||||

Other operating expense | 8.5 | 8.5 | 26.2 | 25.9 | |||||||||||

Selling, general and administrative expense | 46.5 | 42.5 | 137.6 | 127.8 | |||||||||||

Total Expenses | 265.3 | 269.2 | 771.6 | 765.9 | |||||||||||

Other Income (Expense) | |||||||||||||||

Net gain on asset dispositions | 10.3 | 9.4 | 72.5 | 56.3 | |||||||||||

Interest expense, net | (42.6 | ) | (40.2 | ) | (124.7 | ) | (119.4 | ) | |||||||

Other expense | (3.8 | ) | (2.4 | ) | (14.9 | ) | (5.5 | ) | |||||||

Income before Income Taxes and Share of Affiliates’ Earnings | 48.3 | 57.2 | 165.8 | 189.6 | |||||||||||

Income taxes | (13.1 | ) | (20.4 | ) | (42.8 | ) | (60.3 | ) | |||||||

Share of affiliates’ earnings, net of taxes | 11.8 | 12.2 | 39.1 | 30.6 | |||||||||||

Net Income | $ | 47.0 | $ | 49.0 | $ | 162.1 | $ | 159.9 | |||||||

Other Comprehensive Income, Net of Taxes | |||||||||||||||

Foreign currency translation adjustments | (4.7 | ) | 15.4 | (40.2 | ) | 74.0 | |||||||||

Unrealized gain on derivative instruments | 1.6 | 0.7 | 2.3 | 3.6 | |||||||||||

Post-retirement benefit plans | 5.3 | 1.4 | 9.1 | 4.1 | |||||||||||

Other comprehensive income (loss) | 2.2 | 17.5 | (28.8 | ) | 81.7 | ||||||||||

Comprehensive Income | $ | 49.2 | $ | 66.5 | $ | 133.3 | $ | 241.6 | |||||||

Share Data | |||||||||||||||

Basic earnings per share | $ | 1.25 | $ | 1.27 | $ | 4.29 | $ | 4.10 | |||||||

Average number of common shares | 37.7 | 38.6 | 37.8 | 39.0 | |||||||||||

Diluted earnings per share | $ | 1.22 | $ | 1.25 | $ | 4.21 | $ | 4.04 | |||||||

Average number of common shares and common share equivalents | 38.5 | 39.2 | 38.5 | 39.6 | |||||||||||

Dividends declared per common share | $ | 0.44 | $ | 0.42 | $ | 1.32 | $ | 1.26 | |||||||

See accompanying notes to consolidated financial statements.

3

GATX CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS (Unaudited)

(In millions)

Nine Months Ended September 30 | |||||||

2018 | 2017 | ||||||

Operating Activities | |||||||

Net income | $ | 162.1 | $ | 159.9 | |||

Adjustments to reconcile net income to net cash provided by operating activities: | |||||||

Depreciation expense | 253.3 | 238.5 | |||||

Change in accrued operating lease expense | (2.2 | ) | (21.2 | ) | |||

Net gains on sales of assets | (70.9 | ) | (48.4 | ) | |||

Deferred income taxes | 28.0 | 44.8 | |||||

Change in income taxes payable | (0.4 | ) | (4.9 | ) | |||

Share of affiliates’ earnings, net of dividends | (39.0 | ) | (22.0 | ) | |||

Other | 10.4 | (28.9 | ) | ||||

Net cash provided by operating activities | 341.3 | 317.8 | |||||

Investing Activities | |||||||

Additions to operating assets and facilities | (536.7 | ) | (422.4 | ) | |||

Investments in affiliates | — | (36.6 | ) | ||||

Portfolio investments and capital additions | (536.7 | ) | (459.0 | ) | |||

Purchases of leased-in assets | (66.6 | ) | (93.2 | ) | |||

Portfolio proceeds | 198.6 | 131.0 | |||||

Proceeds from sales of other assets | 28.5 | 24.3 | |||||

Proceeds from sale-leasebacks | 59.2 | 90.6 | |||||

Other | 2.7 | (0.2 | ) | ||||

Net cash used in investing activities | (314.3 | ) | (306.5 | ) | |||

Financing Activities | |||||||

Net proceeds from issuances of debt (original maturities longer than 90 days) | 297.1 | 297.5 | |||||

Repayments of debt (original maturities longer than 90 days) | (263.1 | ) | (301.5 | ) | |||

Net decrease (increase) in debt with original maturities of 90 days or less | (4.2 | ) | 11.1 | ||||

Stock repurchases | (37.4 | ) | (75.0 | ) | |||

Dividends | (52.7 | ) | (51.8 | ) | |||

Other | (3.6 | ) | (2.9 | ) | |||

Net cash used in financing activities | (63.9 | ) | (122.6 | ) | |||

Effect of Exchange Rate Changes on Cash and Cash Equivalents | (4.2 | ) | 3.1 | ||||

Net decrease in Cash, Cash Equivalents, and Restricted Cash during the period | (41.1 | ) | (108.2 | ) | |||

Cash, Cash Equivalents, and Restricted Cash at beginning of period | 299.7 | 311.1 | |||||

Cash, Cash Equivalents, and Restricted Cash at end of period | $ | 258.6 | $ | 202.9 | |||

See accompanying notes to consolidated financial statements.

4

GATX CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

NOTE 1. Description of Business

As used herein, "GATX," "we," "us," "our," and similar terms refer to GATX Corporation and its subsidiaries, unless indicated otherwise.

We lease, operate, manage, and remarket long-lived, widely-used assets, primarily in the rail market. We report our financial results through four primary business segments: Rail North America, Rail International, Portfolio Management, and American Steamship Company (“ASC”).

NOTE 2. Basis of Presentation

We prepared the accompanying unaudited consolidated financial statements in accordance with U.S. Generally Accepted Accounting Principles ("GAAP") for interim financial information and the instructions to Form 10-Q and Article 10 of Regulation S-X. Accordingly, our unaudited consolidated financial statements do not include all of the information and footnotes required for complete financial statements. We have included all of the normal recurring adjustments that we deemed necessary for a fair presentation. Certain prior year amounts have been reclassified to conform to the 2018 presentation.

Operating results for the nine months ended September 30, 2018 are not necessarily indicative of the results we may achieve for the entire year ending December 31, 2018. In particular, ASC's fleet is inactive for a significant portion of the first quarter of each year due to winter conditions on the Great Lakes. In addition, asset remarketing income does not occur evenly throughout the year. For more information, refer to the consolidated financial statements and footnotes in our Annual Report on Form 10-K for the year ended December 31, 2017.

New Accounting Pronouncements Adopted

Standard/Description | Effective Date and Adoption Considerations | Effect on Financial Statements or Other Significant Matters |

Revenue from Contracts with Customers In May 2014, the Financial Accounting Standards Board ("FASB") issued Accounting Standards Update ("ASU") 2014-09, Revenue from Contracts with Customers (Topic 606), which supersedes most current revenue recognition guidance, including industry-specific guidance. Subsequently, the FASB has issued updates which provide additional implementation guidance. The new guidance requires companies to recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration it expects to be entitled to in exchange for those goods or services. | We adopted this guidance in the first quarter of 2018 applying the modified retrospective approach. | We have completed our review of all revenue sources in scope for the new standard, and marine operating revenue is our largest component. In accordance with the new standard, the basis for determining revenue and expenses allocable to in-process shipments has been modified; however, the impact does not have a material impact on our financial statements. The net cumulative effect adjustment for this change was immaterial to retained earnings as of January 1, 2018. |

Financial Instruments In January 2016, the FASB issued ASU 2016-01, Financial Instruments - Overall (Topic 825): Recognition and Measurement of Financial Assets and Financial Liabilities, which modifies the accounting and reporting requirements for certain equity securities and financial liabilities. | We adopted the new guidance in the first quarter of 2018. | The application of this new guidance did not impact our financial statements or related disclosures. |

5

GATX CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) (Continued)

New Accounting Pronouncements Adopted (Continued)

Standard/Description | Effective Date and Adoption Considerations | Effect on Financial Statements or Other Significant Matters |

Income Taxes In October 2016, the FASB issued ASU 2016-16, Income Taxes (Topic 740): Intra-Entity Transfers of Assets Other Than Inventory, which modifies how an entity will recognize the income tax consequences of an intra-entity transfer of an asset when the transfer occurs. | We adopted the new guidance in the first quarter of 2018, applying the modified retrospective method. | The application of this new guidance had an immaterial impact on our financial statements and related disclosures, including the net cumulative effect adjustment recorded in retained earnings as of January 1, 2018. |

Compensation In March 2017, the FASB issued ASU 2017-07, Compensation - Retirement Benefits (Topic 715): Improving the Presentation of Net Periodic Pension Cost and Net Periodic Postretirement Benefit Cost, which modifies how an entity must present service costs and other components of net benefit cost. | We adopted the new guidance in the first quarter of 2018, applying the retrospective method. The optional practical expedient was elected. | Application of the new guidance had an immaterial impact on the presentation of our financial statements as certain components of our net periodic pension and other post-retirement benefits costs were reclassified to an alternative income statement line. |

Deferred Income Tax In December 2017, the FASB issued ASU 2017-15, Codification Improvements to Topic 995, U.S. Steamship Entities, which supersedes obsolete guidance in Topic 995 on unrecognized deferred taxes related to certain statutory reserve deposits. If an entity has unrecognized deferred income taxes related to statutory deposits made on or before December 15, 1992, the entity would be required to recognize the unrecognized income taxes in accordance with Topic 740. | We elected to early adopt this new guidance in the first quarter of 2018, applying the modified retrospective method. | The application of this new guidance had an immaterial impact on our financial statements and related disclosures, including the net cumulative effect adjustment recorded in retained earnings as of January 1, 2018. |

Accumulated Other Comprehensive Income In February 2018, the FASB issued ASU 2018-02, Income Statement Reporting - Reporting Comprehensive Income (Topic 220): Reclassification of Certain Tax Effects from Accumulated Other Comprehensive Income, which permits reclassification of certain stranded tax effects from the Tax Cuts and Jobs Act from Accumulated Other Comprehensive Income to Retained Earnings. The amount of the reclassification is calculated on the basis of the difference between the historical and newly enacted tax rates recorded for the applicable AOCI components. | We adopted the new guidance in the first quarter of 2018. | The application of this new guidance resulted in the reclassification of stranded tax effects resulting from the newly enacted Tax Act of $19.4 million from Accumulated Other Comprehensive Income to Retained Earnings. |

6

GATX CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) (Continued)

New Accounting Pronouncements Not Yet Adopted

Standard/Description | Effective Date and Adoption Considerations | Effect on Financial Statements or Other Significant Matters |

Leases In February 2016, the FASB issued ASU 2016-02, Leases (Topic 842), which supersedes most current lease guidance. The FASB subsequently issued ASU 2018-10 and ASU 2018-11, Lease (Topic 842), for codification and targeted improvements to the standard. The new guidance requires companies to recognize most leases on the balance sheet and modifies accounting, presentation, and disclosure for both lessors and lessees. | The new guidance is effective for us in the first quarter of 2019 with early adoption permitted. We plan to adopt this guidance on January 1, 2019, using a modified retrospective transition method with a cumulative effect adjustment upon adoption, and we expect to utilize the package of optional practical expedients as provided in the standard. | We continue to assess the effect the new guidance will have on our consolidated financial statements and related disclosures. The adoption of the amended lease guidance will require us to recognize right of use assets and lease liabilities on our balance sheet attributable to operating leases for railcars, offices, and certain equipment. We are in the process of completing our analysis to determine applicable amounts. |

Credit Losses In June 2016, the FASB issued ASU 2016-13, Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments, which modifies how entities will measure credit losses. | The new guidance is effective for us in the first quarter of 2020, with early adoption permitted. | We are evaluating the effect the new guidance will have on our financial statements and related disclosures. |

Derivatives and Hedging In August 2017, the FASB issued ASU 2017-12, Derivatives and Hedging (Topic 815): Targeted Improvements to Accounting for Hedging Activities, which expands and refines hedge accounting for both financial and non-financial risk components, aligns the recognition and presentation of the effects of hedging instruments and hedge items in the financial statements, and includes certain targeted improvements to ease the application of current guidance related to the assessment of hedge effectiveness. | The update to the standard is effective for us beginning in the first quarter of 2019, with early adoption permitted in any interim period. | We do not expect the new guidance to have a significant impact on our financial statements or related disclosures. |

Compensation In June 2018, the FASB issued ASU 2018-07, Compensation - Stock Compensation (Topic 718): Improvements to Nonemployee Share-Based Payment Accounting, which modifies the accounting for nonemployee share-based payments. | The new guidance is effective for us in the first quarter of 2019, with early adoption permitted in any interim period. | We are evaluating the effect the new guidance will have on our financial statements and related disclosures. |

7

GATX CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) (Continued)

NOTE 3. Revenue

Adoption of Accounting Standards Codification Topic 606, “Revenue from Contracts with Customers”

In the first quarter of 2018, we adopted Topic 606 using the modified retrospective method with respect to applicable contracts existing as of January 1, 2018. As provided in the guidance, we recognize marine operating revenue in the amount that corresponds directly to the value transferred to the customer. Contract assets and liabilities related to our customer performance obligations are not material to our financial statements. Results for reporting periods beginning after January 1, 2018 are presented under Topic 606, while prior period amounts have not been adjusted and continue to be reported in accordance with appropriate accounting guidance. We recorded an immaterial cumulative adjustment to opening retained earnings, with the impact completely attributable to our marine operating revenue.

Revenue Recognition

Revenue is recognized when control of the promised goods or services is transferred to our customers, in an amount that reflects the consideration we expect to be entitled to in exchange for those goods or services.

We disaggregate revenue into three categories as presented on our income statement:

Lease Revenue

Lease revenue, which includes operating lease revenue and finance lease revenue, is our primary source of revenue which continues to be within the scope of existing lease guidance. Therefore, the adoption of Topic 606 had no impact on our recognition or presentation of lease revenue.

Operating Lease Revenue

We lease railcars and other operating assets under full-service and net operating leases. We price full-service leases as an integrated service that includes amounts related to executory costs, such as maintenance, insurance, and ad valorem taxes. We do not offer stand-alone maintenance service contracts and are unable to separate executory costs from full-service lease revenue. Operating lease revenue, including amounts related to executory costs, is recognized on a straight-line basis over the term of the underlying lease. As a result, we may not recognize lease revenue in the same period as maintenance and other executory costs, which we expense as incurred. Contingent rents are recognized when the contingency is resolved. Revenue is not recognized if collectability is not reasonably assured.

Finance Lease Revenue

In certain cases, we lease railcars and other operating assets that, at lease inception, are classified as finance leases. We recognize unearned income as lease revenue using the interest method, which produces a constant yield over the lease term. Initial unearned income is the amount that the original lease payment receivable and the estimated residual value of the leased asset exceeds the original cost or carrying value of the leased asset.

Marine Operating Revenue

We generate marine operating revenue through shipping services completed by our marine vessels. Upon adoption of Topic 606, marine operating revenue is recognized over time as the performance obligation is satisfied, beginning when cargo is loaded through its delivery and discharge. Revenue is recognized pro rata over the projected duration of each voyage, which is derived from our historical voyage data.

Other Revenue

Other revenue comprises customer liability repair revenue, utilization income, fee income, interest on loans, and other miscellaneous revenues. Select components of other revenue are within the scope of Topic 606 but based on our assessment, we determined that our

8

GATX CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) (Continued)

current revenue elements and timing for purposes of income recognition are consistent with applicable provisions in the new standard. The remaining items are considered lease components that continue to be within the scope of existing lease guidance.

NOTE 4. Fair Value Disclosure

The following tables show our assets and liabilities that are measured at fair value on a recurring basis (in millions):

Assets | Total September 30 2018 | Quoted Prices in Active Markets for Identical Assets (Level 1) | Significant Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | |||||||||||

Foreign exchange rate derivatives (1) | $ | 3.2 | $ | — | $ | 3.2 | $ | — | |||||||

Foreign exchange rate derivatives (2) | 0.2 | — | 0.2 | — | |||||||||||

Liabilities | |||||||||||||||

Interest rate derivatives (1) | 13.3 | — | 13.3 | — | |||||||||||

Foreign exchange rate derivatives (1) | 21.4 | — | 21.4 | — | |||||||||||

Foreign exchange rate derivatives (2) | 4.0 | — | 4.0 | — | |||||||||||

Assets | Total December 31 2017 | Quoted Prices in Active Markets for Identical Assets (Level 1) | Significant Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | |||||||||||

Foreign exchange rate derivatives (1) | $ | 1.2 | $ | — | $ | 1.2 | $ | — | |||||||

Liabilities | |||||||||||||||

Interest rate derivatives (1) | 4.7 | — | 4.7 | — | |||||||||||

Foreign exchange rate derivatives (1) | 27.7 | — | 27.7 | — | |||||||||||

Foreign exchange rate derivatives (2) | 6.9 | — | 6.9 | — | |||||||||||

_________

(1) | Designated as hedges. |

(2) | Not designated as hedges. |

We value derivatives using a pricing model with inputs (such as yield curves and foreign currency rates) that are observable in the market or that can be derived principally from observable market data.

Derivative instruments

Fair Value Hedges

We use interest rate swaps to manage the fixed-to-floating rate mix of our debt obligations by converting a portion of our fixed rate debt to floating rate debt. For fair value hedges, we recognize changes in fair value of both the derivative and the hedged item as interest expense. We had nine instruments outstanding with an aggregate notional amount of $500.0 million as of September 30, 2018 with maturities ranging from 2019 to 2022 and ten instruments outstanding with an aggregate notional amount of $550.0 million as of December 31, 2017 with maturities ranging from 2018 to 2022.

9

GATX CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) (Continued)

Cash Flow Hedges

We use interest rate swaps to convert floating rate debt to fixed rate debt. We use Treasury rate locks and swap rate locks to hedge our exposure to interest rate risk on anticipated transactions. We also use currency swaps to hedge our exposure to fluctuations in the exchange rates of the foreign currencies in which we conduct business. We had 8 instruments outstanding with an aggregate notional amount of $291.1 million as of September 30, 2018 that mature from 2018 to 2022 and five instruments outstanding with an aggregate notional amount of $285.6 million as of December 31, 2017 with maturities ranging from 2019 to 2022. Within the next 12 months, we expect to reclassify $2.9 million ($2.2 million after-tax) of net losses on previously terminated derivatives from accumulated other comprehensive income (loss) to interest expense or operating lease expense, as applicable. We reclassify these amounts when interest and operating lease expense on the related hedged transactions affect earnings.

Non-designated Derivatives

We do not hold derivative financial instruments for purposes other than hedging, although certain of our derivatives are not designated as accounting hedges. We recognize changes in the fair value of these derivatives in other (income) expense immediately.

Some of our derivative instruments contain credit risk provisions that could require us to make immediate payment on net liability positions in the event that we default on certain outstanding debt obligations. The aggregate fair value of our derivative instruments with credit risk related contingent features that are in a liability position as of September 30, 2018 was $34.7 million. We are not required to post any collateral on our derivative instruments and do not expect the credit risk provisions to be triggered.

In the event that a counterparty fails to meet the terms of an interest rate swap agreement or a foreign exchange contract, our exposure is limited to the fair value of the swap, if in our favor. We manage the credit risk of counterparties by transacting with institutions that we consider financially sound and by avoiding concentrations of risk with a single counterparty. We believe that the risk of non-performance by any of our counterparties is remote.

The following table shows the impacts of our derivative instruments on our statement of comprehensive income (in millions):

Three Months Ended September 30 | Nine Months Ended September 30 | |||||||||||||||||

Derivative Designation | Location of Loss (Gain) Recognized | 2018 | 2017 | 2018 | 2017 | |||||||||||||

Fair value hedges (1) | Interest expense | $ | 1.0 | $ | 0.6 | $ | 8.6 | $ | 1.5 | |||||||||

Cash flow hedges | Other comprehensive loss (effective portion) | 2.7 | (11.1 | ) | 8.4 | (34.8 | ) | |||||||||||

Cash flow hedges | Interest expense (effective portion reclassified from accumulated other comprehensive loss) | 1.1 | 1.7 | 3.3 | 5.1 | |||||||||||||

Cash flow hedges | Operating lease expense (effective portion reclassified from accumulated other comprehensive loss) | 0.1 | — | 0.1 | — | |||||||||||||

Cash flow hedges (2) | Other (income) expense (effective portion reclassified from accumulated other comprehensive loss) | (2.2 | ) | 10.1 | (10.3 | ) | 33.8 | |||||||||||

Non-designated | Other (income) expense | 3.0 | (2.0 | ) | (2.7 | ) | 4.1 | |||||||||||

_________

(1) | The fair value adjustments related to the underlying debt equally offset the amounts recognized in interest expense. |

(2) | Includes (income) expense on foreign currency derivatives that are substantially offset by foreign currency remeasurement adjustments on related hedged instruments, also recognized in Other (income) expense. |

10

GATX CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) (Continued)

Other Financial Instruments

The carrying amounts of cash and cash equivalents, restricted cash, rent and other receivables, accounts payable, and commercial paper and bank credit facilities approximate fair value due to the short maturity of those instruments. We estimate the fair values of fixed and floating rate debt using discounted cash flow analyses that are based on interest rates currently offered for loans with similar terms to borrowers of similar credit quality. The inputs we use to estimate each of these values are classified in Level 2 of the fair value hierarchy because they are directly or indirectly observable inputs.

The following table shows the carrying amounts and fair values of our other financial instruments (in millions):

September 30, 2018 | December 31, 2017 | ||||||||||||||

Carrying Amount | Fair Value | Carrying Amount | Fair Value | ||||||||||||

Liabilities | |||||||||||||||

Recourse fixed rate debt | $ | 3,998.4 | $ | 3,935.5 | $ | 3,971.2 | $ | 4,089.1 | |||||||

Recourse floating rate debt | 423.8 | 425.2 | 426.0 | 428.7 | |||||||||||

NOTE 5. Pension and Other Post-Retirement Benefits

The following table shows the components of our pension and other post-retirement benefits expense for the three months ended September 30, 2018 and 2017 (in millions):

2018 Pension Benefits | 2017 Pension Benefits | 2018 Retiree Health and Life | 2017 Retiree Health and Life | ||||||||||||

Service cost | $ | 2.0 | $ | 1.6 | $ | 0.1 | $ | — | |||||||

Interest cost | 3.7 | 3.8 | 0.2 | 0.2 | |||||||||||

Expected return on plan assets | (5.6 | ) | (5.9 | ) | — | — | |||||||||

Settlement expense | 2.1 | — | — | — | |||||||||||

Amortization of (1): | |||||||||||||||

Unrecognized prior service credit | — | — | (0.1 | ) | — | ||||||||||

Unrecognized net actuarial loss | 2.5 | 2.2 | — | — | |||||||||||

Net periodic cost | $ | 4.7 | $ | 1.7 | $ | 0.2 | $ | 0.2 | |||||||

11

GATX CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) (Continued)

The following table shows the components of our pension and other post-retirement benefits expense for the nine months ended September 30, 2018 and 2017 (in millions):

2018 Pension Benefits | 2017 Pension Benefits | 2018 Retiree Health and Life | 2017 Retiree Health and Life | ||||||||||||

Service cost | $ | 6.1 | $ | 4.9 | $ | 0.2 | $ | 0.1 | |||||||

Interest cost | 11.1 | 11.5 | 0.7 | 0.7 | |||||||||||

Expected return on plan assets | (16.7 | ) | (17.9 | ) | — | — | |||||||||

Settlement expense | 2.1 | 0.1 | — | — | |||||||||||

Amortization of (1): | |||||||||||||||

Unrecognized prior service credit | — | — | (0.2 | ) | (0.1 | ) | |||||||||

Unrecognized net actuarial loss (gain) | 7.6 | 6.9 | — | (0.2 | ) | ||||||||||

Net periodic cost | $ | 10.2 | $ | 5.5 | $ | 0.7 | $ | 0.5 | |||||||

________

(1) Amounts reclassified from accumulated other comprehensive loss.

In 2018, we adopted ASU 2017-07 which modifies how an entity must present service costs and other components of net benefit cost. See "Note 2. Basis of Presentation" for further details. In accordance with this new guidance, the service cost component of net periodic cost is recorded in the applicable operating expense line, including maintenance expense and selling, general and administrative expense in the Statements of Comprehensive Income; and the other components are recorded in other expense.

During the third quarter of 2018, we recorded a settlement accounting expense of $2.1 million attributable to certain lump-sum distributions made during the period.

NOTE 6. Share-Based Compensation

During the nine months ended September 30, 2018, we granted 320,100 non-qualified employee stock options, 61,490 restricted stock units, 58,440 performance shares, and 17,709 phantom stock units. For the three months and nine months ended September 30, 2018, total share-based compensation expense was $5.7 million and $15.4 million and the related tax benefits were $1.4 million and $3.9 million. For the three months and nine months ended September 30, 2017, total share-based compensation expense was $3.4 million and $10.6 million and the related tax benefits were $1.3 million and $4.1 million.

The estimated fair value of our 2018 non-qualified employee stock option awards and related underlying assumptions are shown in the table below.

2018 | |||

Weighted average estimated fair value | $ | 21.87 | |

Quarterly dividend rate | $ | 0.44 | |

Expected term of stock options and stock appreciation rights, in years | 4.5 | ||

Risk-free interest rate | 1.4 | % | |

Dividend yield | 2.5 | % | |

Expected stock price volatility | 27.9 | % | |

Present value of dividends | $ | 7.51 | |

NOTE 7. Income Taxes

On December 22, 2017, the Tax Act was enacted, which made broad and complex changes to the U.S. tax laws. In particular, the U.S. corporation income tax rate was reduced to 21% from 35%, and a new territorial tax system was implemented that will affect the future

12

GATX CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) (Continued)

U.S. taxation of earnings repatriated from our foreign subsidiaries and affiliates. Other provisions included an immediate deduction for qualified investments and limitations on the deductibility of interest expense and executive compensation. Due to our net operating loss position, these adjustments had no cash impact on our tax positions.

In 2017, we recorded a one-time non-cash net tax benefit of $315.9 million, which represented our provisional estimate of the impact of the Tax Act. This amount included a net benefit of $371.4 million associated with the re-measurement of our net deferred tax liability utilizing the lower U.S. tax rate. The Tax Act also imposed a one-time transitional repatriation tax of $57.2 million on certain undistributed earnings of our non-U.S. subsidiaries and affiliates.

We continue to evaluate the provisions of the Tax Act, and the ultimate impact may differ from this provisional estimate, due to, among other things, changes in interpretations and assumptions made by us, additional guidance that may be issued by the Internal Revenue Service and the U.S. Department of the Treasury, and actions that we may take. In addition, these estimates may change due to guidance provided by state taxing authorities and the completion of our 2017 U.S. and state income tax returns. No adjustments were made to our initial provisional estimate during the nine months ended September 30, 2018.

Our effective tax rate was 26% for the nine months ended September 30, 2018, compared to 32% for the nine months ended September 30, 2017. The difference in the effective rates for the current year compared to the prior year is primarily attributable to the reduction in the U.S. corporation income tax rate from 35% to 21%, as part of the Tax Act. Additionally, the effective tax rate was impacted by the mix of pre-tax income among domestic and foreign jurisdictions, which are taxed at different rates. Incremental tax benefits associated with share-based compensation were also recognized in each of the nine-month periods ended September 30, 2018 and 2017.

NOTE 8. Commercial Commitments

We have entered into various commercial commitments, such as guarantees, standby letters of credit, and performance bonds, related to certain transactions. These commercial commitments require us to fulfill specific obligations in the event of third-party demands. Similar to our balance sheet investments, these commitments expose us to credit, market, and equipment risk. Accordingly, we evaluate these commitments and other contingent obligations using techniques similar to those we use to evaluate funded transactions.

The following table shows our commercial commitments (in millions):

September 30 2018 | December 31 2017 | ||||||

Lease payment guarantees | $ | 2.7 | $ | 4.9 | |||

Standby letters of credit and performance bonds | 17.4 | 17.8 | |||||

Total commercial commitments (1) | $ | 20.1 | $ | 22.7 | |||

_______

(1) The carrying value of liabilities on the balance sheet for commercial commitments was $1.2 million at September 30, 2018 and $2.0 million at December 31, 2017. The expirations of these commitments range from 2019 to 2023. We are not aware of any event that would require us to satisfy any of our commitments.

Lease payment guarantees are commitments to financial institutions to make lease payments for a third party in the event they default. We reduce any liability that may result from these guarantees by the value of the underlying asset or group of assets.

We are also parties to standby letters of credit and performance bonds, which primarily relate to contractual obligations and general liability insurance coverages. No material claims have been made against these obligations, and no material losses are anticipated.

NOTE 9. Earnings per Share

We compute basic earnings per share by dividing net income available to our common shareholders by the weighted average number of shares of our common stock outstanding. We weight shares issued or reacquired for the portion of the period that they were outstanding. Our diluted earnings per share reflect the impacts of our potentially dilutive securities, which include our equity compensation awards.

13

GATX CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) (Continued)

The following table shows the computation of our basic and diluted net income per common share (in millions, except per share amounts):

Three Months Ended September 30 | Nine Months Ended September 30 | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Numerator: | |||||||||||||||

Net income | $ | 47.0 | $ | 49.0 | $ | 162.1 | $ | 159.9 | |||||||

Denominator: | |||||||||||||||

Weighted average shares outstanding - basic | 37.7 | 38.6 | 37.8 | 39.0 | |||||||||||

Effect of dilutive securities: | |||||||||||||||

Equity compensation plans | 0.8 | 0.6 | 0.7 | 0.6 | |||||||||||

Weighted average shares outstanding - diluted | 38.5 | 39.2 | 38.5 | 39.6 | |||||||||||

Basic earnings per share | $ | 1.25 | $ | 1.27 | $ | 4.29 | $ | 4.10 | |||||||

Diluted earnings per share | $ | 1.22 | $ | 1.25 | $ | 4.21 | $ | 4.04 | |||||||

NOTE 10. Accumulated Other Comprehensive Income (Loss)

The following table shows the change in components for accumulated other comprehensive loss (in millions):

Foreign Currency Translation Gain (Loss) | Unrealized Loss on Derivative Instruments | Post-Retirement Benefit Plans | Total | ||||||||||||

Balance at December 31, 2017 | $ | (10.5 | ) | $ | (15.5 | ) | $ | (83.6 | ) | $ | (109.6 | ) | |||

Change in component | 14.9 | (11.5 | ) | — | 3.4 | ||||||||||

Reclassification adjustments into earnings (1) | — | 9.3 | 2.5 | 11.8 | |||||||||||

Income tax effect | — | 0.7 | (0.6 | ) | 0.1 | ||||||||||

Reclassification adjustments into retained earnings (2) | — | (3.0 | ) | (16.4 | ) | (19.4 | ) | ||||||||

Balance at March 31, 2018 | $ | 4.4 | $ | (20.0 | ) | $ | (98.1 | ) | $ | (113.7 | ) | ||||

Change in component | (50.4 | ) | 18.0 | — | (32.4 | ) | |||||||||

Reclassification adjustments into earnings (1) | — | (15.2 | ) | 2.5 | (12.7 | ) | |||||||||

Income tax effect | — | (0.6 | ) | (0.6 | ) | (1.2 | ) | ||||||||

Balance at June 30, 2018 | $ | (46.0 | ) | $ | (17.8 | ) | $ | (96.2 | ) | $ | (160.0 | ) | |||

Change in component | (4.7 | ) | 2.8 | 4.6 | 2.7 | ||||||||||

Reclassification adjustments into earnings (1) | — | (1.0 | ) | 2.4 | 1.4 | ||||||||||

Income tax effect | — | (0.2 | ) | (1.7 | ) | (1.9 | ) | ||||||||

Balance at September 30, 2018 | $ | (50.7 | ) | $ | (16.2 | ) | $ | (90.9 | ) | $ | (157.8 | ) | |||

________

(1) | See "Note 4. Fair Value Disclosure" and "Note 5. Pension and Other Post-Retirement Benefits" for impacts of the reclassification adjustments on the statement of comprehensive income. |

(2) | As detailed in "Note 2. Basis of Presentation", we adopted ASU 2018-02, which permits reclassification of certain stranded tax effects related to the Tax Act from Accumulated Other Comprehensive Income to Retained Earnings. |

14

GATX CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) (Continued)

NOTE 11. Legal Proceedings and Other Contingencies

Various legal actions, claims, assessments and other contingencies arising in the ordinary course of business are pending against GATX and certain of our subsidiaries. These matters are subject to many uncertainties, and it is possible that some of these matters could ultimately be decided, resolved or settled adversely. For a full discussion of our pending legal matters, please refer to "Note 22. Legal Proceedings and Other Contingencies" of our consolidated financial statements in our Annual Report on Form 10-K for the year ended December 31, 2017.

NOTE 12. Financial Data of Business Segments

The financial data presented below depicts the profitability, financial position, and capital expenditures of each of our business segments.

We lease, operate, manage, and remarket long-lived, widely-used assets, primarily in the rail market. We report our financial results through four primary business segments: Rail North America, Rail International, Portfolio Management, and American Steamship Company (“ASC”).

Rail North America is composed of our operations in the United States, Canada, and Mexico, as well as an affiliate investment. Rail North America primarily provides railcars pursuant to full-service leases under which it maintains the railcars, pays ad valorem taxes and insurance, and provides other ancillary services.

Rail International is composed of our operations in Europe ("GATX Rail Europe" or "GRE"), India ("Rail India"), and Russia ("Rail Russia"). GRE leases railcars to customers throughout Europe pursuant to full-service leases under which it maintains the railcars and provides value-adding services according to customer requirements.

Portfolio Management is composed primarily of our ownership in a group of joint ventures with Rolls-Royce plc that lease aircraft spare engines, as well as five liquefied gas carrying vessels (the "Norgas Vessels") and assorted other marine assets. In prior years, Portfolio Management generated leasing, marine operating, asset remarketing, and management fee income through a collection of diversified wholly owned assets and joint venture investments. In 2015, we made the decision to exit the majority of the marine investments, excluding the Norgas Vessels, within our Portfolio Management segment, including six chemical parcel tankers, a number of inland marine vessels, and our 50% interest in the Cardinal Marine joint venture, all of which had been sold as of December 31, 2017.

ASC operates the largest fleet of US-flagged vessels on the Great Lakes, providing waterborne transportation of dry bulk commodities such as iron ore, coal, limestone aggregates, and metallurgical limestone.

Segment profit is an internal performance measure used by the Chief Executive Officer to assess the performance of each segment in a given period. Segment profit includes all revenues, pre-tax earnings from affiliates, and net gains on asset dispositions that are attributable to the segments, as well as expenses that management believes are directly associated with the financing, maintenance, and operation of the revenue earning assets. Segment profit excludes selling, general and administrative expenses, income taxes, and certain other amounts not allocated to the segments. These amounts are included in Other.

We allocate debt balances and related interest expense to each segment based upon predetermined debt to equity leverage ratios. The leverage levels are 5:1 for Rail North America, 3:1 for Rail International, 1:1 for Portfolio Management, and 1.5:1 for ASC. We believe that by using this leverage and interest expense allocation methodology, each operating segment’s financial performance reflects appropriate risk-adjusted borrowing costs.

15

GATX CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) (Continued)

The following tables show certain segment data for each of our business segments (in millions):

Rail North America | Rail International | Portfolio Management | ASC | Other | GATX Consolidated | ||||||||||||||||||

Three Months Ended September 30, 2018 | |||||||||||||||||||||||

Revenues | |||||||||||||||||||||||

Lease revenue | $ | 218.2 | $ | 52.3 | $ | 0.3 | $ | 1.1 | $ | — | $ | 271.9 | |||||||||||

Marine operating revenue | — | — | 3.1 | 57.7 | — | 60.8 | |||||||||||||||||

Other revenue | 15.2 | 1.8 | — | — | — | 17.0 | |||||||||||||||||

Total Revenues | 233.4 | 54.1 | 3.4 | 58.8 | — | 349.7 | |||||||||||||||||

Expenses | |||||||||||||||||||||||

Maintenance expense | 60.6 | 10.1 | — | 6.8 | — | 77.5 | |||||||||||||||||

Marine operating expense | — | — | 4.4 | 35.0 | — | 39.4 | |||||||||||||||||

Depreciation expense | 62.5 | 13.8 | 1.8 | 3.5 | — | 81.6 | |||||||||||||||||

Operating lease expense | 11.8 | — | — | — | — | 11.8 | |||||||||||||||||

Other operating expense | 7.1 | 1.3 | 0.1 | — | — | 8.5 | |||||||||||||||||

Total Expenses | 142.0 | 25.2 | 6.3 | 45.3 | — | 218.8 | |||||||||||||||||

Other Income (Expense) | |||||||||||||||||||||||

Net gain on asset dispositions | 9.6 | 0.5 | 0.2 | — | — | 10.3 | |||||||||||||||||

Interest (expense) income, net | (31.8 | ) | (8.9 | ) | (2.6 | ) | (1.5 | ) | 2.2 | (42.6 | ) | ||||||||||||

Other expense (income) | (1.2 | ) | 0.2 | — | (0.1 | ) | (2.7 | ) | (3.8 | ) | |||||||||||||

Share of affiliates' pre-tax income | 0.2 | — | 14.3 | — | — | 14.5 | |||||||||||||||||

Segment profit (loss) | $ | 68.2 | $ | 20.7 | $ | 9.0 | $ | 11.9 | $ | (0.5 | ) | $ | 109.3 | ||||||||||

Less: | |||||||||||||||||||||||

Selling, general and administrative expense | 46.5 | ||||||||||||||||||||||

Income taxes (includes $2.7 related to affiliates' earnings) | 15.8 | ||||||||||||||||||||||

Net income | $ | 47.0 | |||||||||||||||||||||

Net Gain on Asset Dispositions | |||||||||||||||||||||||

Asset Remarketing Income: | |||||||||||||||||||||||

Net gains on disposition of owned assets | $ | 6.7 | $ | — | $ | — | $ | — | $ | — | $ | 6.7 | |||||||||||

Residual sharing income | 0.5 | — | 0.2 | — | — | 0.7 | |||||||||||||||||

Non-remarketing net gains (1) | 2.4 | 0.5 | — | — | — | 2.9 | |||||||||||||||||

$ | 9.6 | $ | 0.5 | $ | 0.2 | $ | — | $ | — | $ | 10.3 | ||||||||||||

Capital Expenditures | |||||||||||||||||||||||

Portfolio investments and capital additions | $ | 129.1 | $ | 40.4 | $ | — | $ | — | $ | 0.2 | $ | 169.7 | |||||||||||

Selected Balance Sheet Data at September 30, 2018 | |||||||||||||||||||||||

Investments in affiliated companies | $ | 3.7 | $ | — | $ | 474.8 | $ | — | $ | — | $ | 478.5 | |||||||||||

Identifiable assets | $ | 5,000.0 | $ | 1,357.3 | $ | 614.9 | $ | 303.5 | $ | 241.7 | $ | 7,517.4 | |||||||||||

__________

(1) Includes net gains from scrapping of railcars.

16

GATX CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) (Continued)

Rail North America | Rail International | Portfolio Management | ASC | Other | GATX Consolidated | ||||||||||||||||||

Three Months Ended September 30, 2017 | |||||||||||||||||||||||

Revenues | |||||||||||||||||||||||

Lease revenue | $ | 224.5 | $ | 50.3 | $ | 0.7 | $ | 1.1 | $ | — | $ | 276.6 | |||||||||||

Marine operating revenue | — | — | 3.8 | 59.1 | — | 62.9 | |||||||||||||||||

Other revenue | 17.9 | 2.0 | 0.2 | — | — | 20.1 | |||||||||||||||||

Total Revenues | 242.4 | 52.3 | 4.7 | 60.2 | — | 359.6 | |||||||||||||||||

Expenses | |||||||||||||||||||||||

Maintenance expense | 66.1 | 11.1 | — | 7.7 | — | 84.9 | |||||||||||||||||

Marine operating expense | — | — | 4.2 | 34.7 | — | 38.9 | |||||||||||||||||

Depreciation expense | 60.1 | 12.8 | 1.7 | 4.0 | — | 78.6 | |||||||||||||||||

Operating lease expense | 15.5 | — | — | 0.3 | — | 15.8 | |||||||||||||||||

Other operating expense | 7.3 | 1.1 | 0.1 | — | — | 8.5 | |||||||||||||||||

Total Expenses | 149.0 | 25.0 | 6.0 | 46.7 | — | 226.7 | |||||||||||||||||

Other Income (Expense) | |||||||||||||||||||||||

Net gain on asset dispositions | 8.1 | 1.0 | 0.3 | — | — | 9.4 | |||||||||||||||||

Interest (expense) income, net | (30.5 | ) | (8.5 | ) | (2.2 | ) | (1.4 | ) | 2.4 | (40.2 | ) | ||||||||||||

Other (expense) income | (0.9 | ) | 0.3 | — | — | (1.8 | ) | (2.4 | ) | ||||||||||||||

Share of affiliates' pre-tax income | 0.1 | — | 16.0 | — | — | 16.1 | |||||||||||||||||

Segment profit | $ | 70.2 | $ | 20.1 | $ | 12.8 | $ | 12.1 | $ | 0.6 | $ | 115.8 | |||||||||||

Less: | |||||||||||||||||||||||

Selling, general and administrative expense | 42.5 | ||||||||||||||||||||||

Income taxes (includes $3.9 related to affiliates' earnings) | 24.3 | ||||||||||||||||||||||

Net income | $ | 49.0 | |||||||||||||||||||||

Net Gain on Asset Dispositions | |||||||||||||||||||||||

Asset Remarketing Income: | |||||||||||||||||||||||

Net gains on disposition of owned assets | $ | 7.5 | $ | 0.1 | $ | — | $ | — | $ | — | $ | 7.6 | |||||||||||

Residual sharing income | 0.2 | — | 0.3 | — | — | 0.5 | |||||||||||||||||

Non-remarketing net gains (1) | 0.4 | 0.9 | — | — | — | 1.3 | |||||||||||||||||

$ | 8.1 | $ | 1.0 | $ | 0.3 | $ | — | $ | — | $ | 9.4 | ||||||||||||

Capital Expenditures | |||||||||||||||||||||||

Portfolio investments and capital additions | $ | 103.3 | $ | 22.9 | $ | 36.6 | $ | 0.8 | $ | 0.1 | $ | 163.7 | |||||||||||

Selected Balance Sheet Data at December 31, 2017 | |||||||||||||||||||||||

Investments in affiliated companies | $ | 6.8 | $ | — | $ | 434.2 | $ | — | $ | — | $ | 441.0 | |||||||||||

Identifiable assets | $ | 4,915.0 | $ | 1,332.9 | $ | 582.8 | $ | 286.7 | $ | 305.0 | $ | 7,422.4 | |||||||||||

__________

(1) Includes net gains from scrapping of railcars.

17

GATX CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) (Continued)

Rail North America | Rail International | Portfolio Management | ASC | Other | GATX Consolidated | ||||||||||||||||||

Nine Months Ended September 30, 2018 | |||||||||||||||||||||||

Revenues | |||||||||||||||||||||||

Lease revenue | $ | 655.3 | $ | 156.9 | $ | 0.8 | $ | 3.1 | $ | — | $ | 816.1 | |||||||||||

Marine operating revenue | — | — | 11.0 | 119.8 | — | 130.8 | |||||||||||||||||

Other revenue | 51.1 | 6.0 | 0.5 | — | — | 57.6 | |||||||||||||||||

Total Revenues | 706.4 | 162.9 | 12.3 | 122.9 | — | 1,004.5 | |||||||||||||||||

Expenses | |||||||||||||||||||||||

Maintenance expense | 192.8 | 33.8 | — | 14.1 | — | 240.7 | |||||||||||||||||

Marine operating expense | — | — | 12.9 | 76.6 | — | 89.5 | |||||||||||||||||

Depreciation expense | 185.8 | 41.7 | 5.5 | 7.1 | — | 240.1 | |||||||||||||||||

Operating lease expense | 37.5 | — | — | — | — | 37.5 | |||||||||||||||||

Other operating expense | 21.5 | 4.3 | 0.4 | — | — | 26.2 | |||||||||||||||||

Total Expenses | 437.6 | 79.8 | 18.8 | 97.8 | — | 634.0 | |||||||||||||||||

Other Income (Expense) | |||||||||||||||||||||||

Net gain on asset dispositions | 68.4 | 3.2 | 0.8 | 0.1 | — | 72.5 | |||||||||||||||||

Interest (expense) income, net | (93.1 | ) | (26.5 | ) | (7.6 | ) | (4.3 | ) | 6.8 | (124.7 | ) | ||||||||||||

Other expense | (3.3 | ) | (7.3 | ) | — | (0.2 | ) | (4.1 | ) | (14.9 | ) | ||||||||||||

Share of affiliates' pre-tax income | 0.5 | — | 47.6 | — | — | 48.1 | |||||||||||||||||

Segment profit | $ | 241.3 | $ | 52.5 | $ | 34.3 | $ | 20.7 | $ | 2.7 | $ | 351.5 | |||||||||||

Less: | |||||||||||||||||||||||

Selling, general and administrative expense | 137.6 | ||||||||||||||||||||||

Income taxes (includes $9.0 related to affiliates' earnings) | 51.8 | ||||||||||||||||||||||

Net income | $ | 162.1 | |||||||||||||||||||||

Net Gain on Asset Dispositions | |||||||||||||||||||||||

Asset Remarketing Income: | |||||||||||||||||||||||

Net gains on disposition of owned assets | $ | 60.8 | $ | — | $ | — | $ | 0.1 | $ | — | $ | 60.9 | |||||||||||

Residual sharing income | 0.9 | — | 0.8 | — | — | 1.7 | |||||||||||||||||

Non-remarketing net gains (1) | 6.7 | 3.2 | — | — | — | 9.9 | |||||||||||||||||

$ | 68.4 | $ | 3.2 | $ | 0.8 | $ | 0.1 | $ | — | $ | 72.5 | ||||||||||||

Capital Expenditures | |||||||||||||||||||||||

Portfolio investments and capital additions | $ | 414.7 | $ | 104.5 | $ | — | $ | 15.8 | $ | 1.7 | $ | 536.7 | |||||||||||

__________

(1) Includes net gains from scrapping of railcars.

18

GATX CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) (Continued)

Rail North America | Rail International | Portfolio Management | ASC | Other | GATX Consolidated | ||||||||||||||||||

Nine Months Ended September 30, 2017 | |||||||||||||||||||||||

Revenues | |||||||||||||||||||||||

Lease revenue | $ | 677.4 | $ | 139.8 | $ | 3.1 | $ | 3.1 | $ | — | $ | 823.4 | |||||||||||

Marine operating revenue | — | — | 21.8 | 113.2 | — | 135.0 | |||||||||||||||||

Other revenue | 60.0 | 4.7 | 1.0 | — | — | 65.7 | |||||||||||||||||

Total Revenues | 737.4 | 144.5 | 25.9 | 116.3 | — | 1,024.1 | |||||||||||||||||

Expenses | |||||||||||||||||||||||

Maintenance expense | 202.3 | 30.8 | — | 14.6 | — | 247.7 | |||||||||||||||||

Marine operating expense | — | — | 19.2 | 70.6 | — | 89.8 | |||||||||||||||||

Depreciation expense | 178.8 | 35.8 | 5.2 | 8.1 | — | 227.9 | |||||||||||||||||

Operating lease expense | 45.3 | — | — | 1.5 | — | 46.8 | |||||||||||||||||

Other operating expense | 21.7 | 3.5 | 0.7 | — | — | 25.9 | |||||||||||||||||

Total Expenses | 448.1 | 70.1 | 25.1 | 94.8 | — | 638.1 | |||||||||||||||||

Other Income (Expense) | |||||||||||||||||||||||

Net gain on asset dispositions | 42.6 | 2.6 | 11.1 | — | — | 56.3 | |||||||||||||||||

Interest (expense) income, net | (90.1 | ) | (24.5 | ) | (6.8 | ) | (3.9 | ) | 5.9 | (119.4 | ) | ||||||||||||

Other (expense) income | (4.1 | ) | (2.3 | ) | 2.3 | 0.8 | (2.2 | ) | (5.5 | ) | |||||||||||||

Share of affiliates' pre-tax income (loss) | 0.4 | (0.1 | ) | 39.9 | — | — | 40.2 | ||||||||||||||||

Segment profit | $ | 238.1 | $ | 50.1 | $ | 47.3 | $ | 18.4 | $ | 3.7 | $ | 357.6 | |||||||||||

Less: | |||||||||||||||||||||||

Selling, general and administrative expense | 127.8 | ||||||||||||||||||||||

Income taxes (includes $9.6 related to affiliates' earnings) | 69.9 | ||||||||||||||||||||||

Net income | $ | 159.9 | |||||||||||||||||||||

Net Gain on Asset Dispositions | |||||||||||||||||||||||

Asset Remarketing Income: | |||||||||||||||||||||||

Net gains on disposition of owned assets | $ | 39.5 | $ | 0.1 | $ | 1.8 | $ | — | $ | — | $ | 41.4 | |||||||||||

Residual sharing income | 0.5 | — | 9.3 | — | — | 9.8 | |||||||||||||||||

Non-remarketing net gains (1) | 4.5 | 2.5 | — | — | — | 7.0 | |||||||||||||||||

Asset impairments | (1.9 | ) | — | — | — | — | (1.9 | ) | |||||||||||||||

$ | 42.6 | $ | 2.6 | $ | 11.1 | $ | — | $ | — | $ | 56.3 | ||||||||||||

Capital Expenditures | |||||||||||||||||||||||

Portfolio investments and capital additions | $ | 333.7 | $ | 74.7 | $ | 36.6 | $ | 13.6 | $ | 0.4 | $ | 459.0 | |||||||||||

__________

(1) Includes net gains from scrapping of railcars.

19

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

OVERVIEW

We lease, operate, manage, and remarket long-lived, widely-used assets, primarily in the rail market. We report our financial results through four primary business segments: Rail North America, Rail International, Portfolio Management, and American Steamship Company (“ASC”).

The following discussion and analysis should be read in conjunction with the MD&A in our Annual Report on Form 10-K for the year ended December 31, 2017. We based the discussion and analysis that follows on financial data we derived from the financial statements prepared in accordance with U.S. Generally Accepted Accounting Standards ("GAAP") and on certain other financial data that we prepared using non-GAAP components. For a reconciliation of these non-GAAP components to the most comparable GAAP components, see “Non-GAAP Financial Measures” at the end of this item.

Operating results for the three and nine months ended September 30, 2018 are not necessarily indicative of the results we may achieve for the entire year ending December 31, 2018. In particular, ASC's fleet is inactive for a significant portion of the first quarter of each year due to winter conditions on the Great Lakes. In addition, asset remarketing income does not occur evenly throughout the year. For more information about our business, refer to our Annual Report on Form 10-K for the year ended December 31, 2017.

20

DISCUSSION OF OPERATING RESULTS

The following table shows a summary of our reporting segments and consolidated financial results (in millions, except per share data):

Three Months Ended September 30 | Nine Months Ended September 30 | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Segment Revenues | |||||||||||||||

Rail North America | $ | 233.4 | $ | 242.4 | $ | 706.4 | $ | 737.4 | |||||||

Rail International | 54.1 | 52.3 | 162.9 | 144.5 | |||||||||||

Portfolio Management | 3.4 | 4.7 | 12.3 | 25.9 | |||||||||||

ASC | 58.8 | 60.2 | 122.9 | 116.3 | |||||||||||

$ | 349.7 | $ | 359.6 | $ | 1,004.5 | $ | 1,024.1 | ||||||||

Segment Profit | |||||||||||||||

Rail North America | $ | 68.2 | $ | 70.2 | $ | 241.3 | $ | 238.1 | |||||||

Rail International | 20.7 | 20.1 | 52.5 | 50.1 | |||||||||||

Portfolio Management | 9.0 | 12.8 | 34.3 | 47.3 | |||||||||||

ASC | 11.9 | 12.1 | 20.7 | 18.4 | |||||||||||

109.8 | 115.2 | 348.8 | 353.9 | ||||||||||||

Less: | |||||||||||||||

Selling, general and administrative expense | 46.5 | 42.5 | 137.6 | 127.8 | |||||||||||

Unallocated interest (income) expense | (2.2 | ) | (2.4 | ) | (6.8 | ) | (5.9 | ) | |||||||

Other, including eliminations | 2.7 | 1.8 | 4.1 | 2.2 | |||||||||||

Income taxes ($2.7 and $3.9 QTR and $9.0 and $9.6 YTD related to affiliates' earnings) | 15.8 | 24.3 | 51.8 | 69.9 | |||||||||||

Net Income | $ | 47.0 | $ | 49.0 | $ | 162.1 | $ | 159.9 | |||||||

Net income, excluding tax adjustments and other items (non-GAAP) | $ | 47.0 | $ | 49.0 | $ | 167.9 | $ | 158.8 | |||||||

Diluted earnings per share | $ | 1.22 | $ | 1.25 | $ | 4.21 | $ | 4.04 | |||||||

Diluted earnings per share, excluding tax adjustments and other items (non-GAAP) | $ | 1.22 | $ | 1.25 | $ | 4.36 | $ | 4.01 | |||||||

Investment Volume | $ | 169.7 | $ | 163.7 | $ | 536.7 | $ | 459.0 | |||||||

21

The following table shows our return on equity ("ROE") for the trailing 12 months ended September 30:

2018 | 2017 | ||||

ROE (GAAP) | 30.5 | % | 13.4 | % | |

ROE, excluding tax adjustments and other items (non-GAAP) (1) | 13.0 | % | 14.4 | % | |

_________

(1) | See "Non-GAAP Financial Measures" at the end of this item for further details. |

Net income was $162.1 million, or $4.21 per diluted share, for the first nine months of 2018 compared to $159.9 million, or $4.04 per diluted share, in 2017. Results for the nine months ended September 30, 2018 included costs of approximately $5.8 million (after-tax) associated with the closure of a maintenance facility at Rail International, and results for the nine months ended September 30, 2017 included a net gain of approximately $1.1 million (after-tax) from the planned exit of the majority of Portfolio Management's marine investments (see "Non-GAAP Financial Measures" at the end of this item for further details). Excluding the impact of these items, net income increased $9.1 million compared to the prior year. The increase was driven by higher asset disposition gains and lower maintenance expense at Rail North America, higher lease revenue, resulting from more railcars on lease, and the positive impacts of foreign exchange rates, both at Rail International, and higher income from affiliates. These positive impacts were partially offset by lower lease revenue at Rail North America, due to lower lease rates and fewer railcars on lease, as well as lower residual sharing fees from our managed portfolio and lower marine operating results at our Portfolio Management segment.

Net income was $47.0 million, or $1.22 per diluted share, for the third quarter of 2018 compared to $49.0 million, or $1.25 per diluted share, in 2017. Net income decreased $2.0 million compared to the prior year. The decrease was largely due to lower lease revenue, as a result of lower lease rates and fewer railcars on lease at Rail North America, as well as lower affiliate income. These negative impacts were partially offset by lower maintenance expense at Rail North America, as well as higher lease revenue, resulting from more railcars on lease, and lower maintenance expense, both at Rail International.

Segment Operations

Segment profit is an internal performance measure used by the Chief Executive Officer to assess the performance of each segment in a given period. Segment profit includes all revenues, pre-tax earnings from affiliates, and net gains on asset dispositions that are attributable to the segments, as well as expenses that management believes are directly associated with the financing, maintenance, and operation of the revenue earning assets. Segment profit excludes selling, general and administrative expenses, income taxes, and certain other amounts not allocated to the segments. These amounts are included in Other.

We allocate debt balances and related interest expense to each segment based upon predetermined debt to equity leverage ratios. The leverage levels are 5:1 for Rail North America, 3:1 for Rail International, 1:1 for Portfolio Management, and 1.5:1 for ASC. We believe that by using this leverage and interest expense allocation methodology, each operating segment’s financial performance reflects appropriate risk-adjusted borrowing costs.

RAIL NORTH AMERICA

Segment Summary

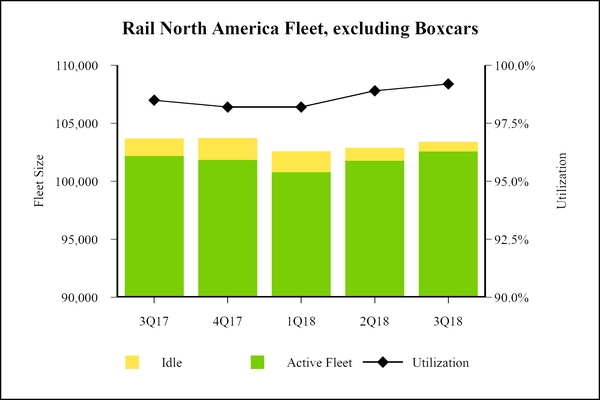

The operating environment for Rail North America continued to improve, as railroad car loadings increased and railroad velocity decreased relative to 2017. Despite absolute lease rates improving, revenue pressure continues. At September 30, 2018, Rail North America's wholly owned fleet, excluding boxcars, consisted of approximately 103,400 cars, and fleet utilization was 99.2% at September 30, 2018, compared to 98.9% at the end of the prior quarter, and 98.5% at September 30, 2017. Fleet utilization for our approximately 16,000 boxcars was 94.7% at September 30, 2018, compared to 92.8% at the end of the prior quarter, and 92.4% at September 30, 2017.

For the third quarter of 2018, an average of approximately 102,100 railcars, excluding boxcars, were on lease, compared to 101,300 in the prior quarter and 102,600 at September 30, 2017. The decrease in railcars on lease in the current year is largely due to railcars that

22

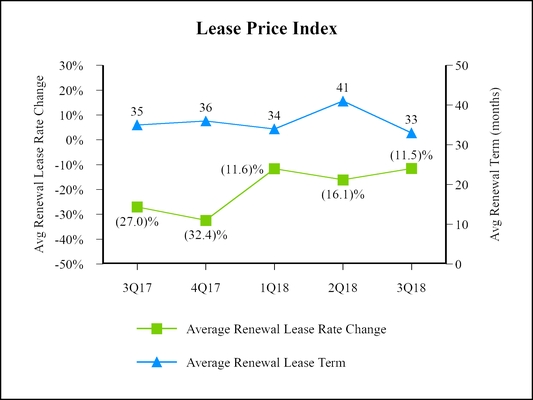

were sold or scrapped, consistent with our ongoing strategy to optimize the composition of our fleet. During the third quarter of 2018, the renewal rate change of the Lease Price Index (the "LPI", see definition below) was negative 11.5%, compared to negative 16.1% in the prior quarter and negative 27.0% in the third quarter of 2017. Lease terms on renewals for cars in the LPI averaged 33 months in the current quarter, compared to 41 months in the prior quarter, and 35 months in the third quarter of 2017. Additionally, the renewal success rate, which represents the percentage of expiring leases that were renewed with the existing lessee, was 82.9% in the current quarter, compared to 78.6% in the prior quarter, and 74.9% in the third quarter of 2017. Railcars returned by our customers may incur transitional costs, including additional repairs and related service prior to being leased to new customers, which may increase maintenance and associated expenses.

In 2014, we entered into a long-term supply agreement with Trinity Rail Group, LLC ("Trinity"), a subsidiary of Trinity Industries that took effect in mid-2016. Under the terms of that agreement, we may order up to 8,950 newly built railcars over a four-year period from March, 2016 through March, 2020. We may order either tank or freight cars; however, we expect that the majority of the order will be for tank cars. As of September 30, 2018, 7,715 railcars have been ordered, of which 5,095 railcars have been delivered. On May 24, 2018, we amended our long-term supply agreement with Trinity to extend the term to December 2023. We agreed to purchase an additional 4,800 tank cars (1,200 per year) beginning in January 2020 and continuing through the expiration of the extended term. Pricing will be on an agreed upon or cost-plus basis subject to certain adjustments and surcharges specified in the agreement.

On July 30, 2018, we entered into a multi-year railcar supply agreement with American Railcar Industries, Inc. ("ARI"), pursuant to which we will purchase 7,650 newly built railcars. The order encompasses a mix of tank and freight cars to be delivered over a five-year period, beginning in April 2019. ARI will deliver 450 railcars in 2019, with the remaining 7,200 to be delivered ratably over the four-year period of 2020 to 2023. The agreement also includes an option to order up to an additional 4,400 railcars subject to certain restrictions.

As of September 30, 2018, leases for approximately 5,400 tank cars and freight cars and approximately 1,100 boxcars are scheduled to expire over the remainder of 2018. These amounts exclude leases expiring in 2018 that have already been renewed or assigned to a new lessee.

23

The following table shows Rail North America's segment results (in millions):

Three Months Ended September 30 | Nine Months Ended September 30 | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Revenues | |||||||||||||||

Lease revenue | $ | 218.2 | $ | 224.5 | $ | 655.3 | $ | 677.4 | |||||||

Other revenue | 15.2 | 17.9 | 51.1 | 60.0 | |||||||||||

Total Revenues | 233.4 | 242.4 | 706.4 | 737.4 | |||||||||||

Expenses | |||||||||||||||

Maintenance expense | 60.6 | 66.1 | 192.8 | 202.3 | |||||||||||

Depreciation expense | 62.5 | 60.1 | 185.8 | 178.8 | |||||||||||

Operating lease expense | 11.8 | 15.5 | 37.5 | 45.3 | |||||||||||

Other operating expense | 7.1 | 7.3 | 21.5 | 21.7 | |||||||||||

Total Expenses | 142.0 | 149.0 | 437.6 | 448.1 | |||||||||||

Other Income (Expense) | |||||||||||||||

Net gain on asset dispositions | 9.6 | 8.1 | 68.4 | 42.6 | |||||||||||

Interest expense, net | (31.8 | ) | (30.5 | ) | (93.1 | ) | (90.1 | ) | |||||||

Other expense | (1.2 | ) | (0.9 | ) | (3.3 | ) | (4.1 | ) | |||||||

Share of affiliates' pre-tax income | 0.2 | 0.1 | 0.5 | 0.4 | |||||||||||

Segment Profit | $ | 68.2 | $ | 70.2 | $ | 241.3 | $ | 238.1 | |||||||

Investment Volume | $ | 129.1 | $ | 103.3 | $ | 414.7 | $ | 333.7 | |||||||

The following table shows the components of Rail North America's lease revenue (in millions):

Three Months Ended September 30 | Nine Months Ended September 30 | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Railcars | $ | 188.9 | $ | 195.9 | $ | 568.4 | $ | 591.8 | |||||||

Boxcars | 19.5 | 18.9 | 57.8 | 56.3 | |||||||||||

Locomotives | 9.8 | 9.7 | 29.1 | 29.3 | |||||||||||

Total | $ | 218.2 | $ | 224.5 | $ | 655.3 | $ | 677.4 | |||||||

Lease Price Index

Our LPI is an internally-generated business indicator that measures lease rate pricing on renewals for our North American railcar fleet, excluding boxcars. We calculate the index using the weighted average lease rate for a group of railcar types that we believe best represents our overall North American fleet, excluding boxcars. The average renewal lease rate change is reported as the percentage change between the average renewal lease rate and the average expiring lease rate, weighted by fleet composition. The average renewal lease term is reported in months and reflects the average renewal lease term of railcar types in the LPI, weighted by fleet composition.

24

Rail North America Fleet Data

The following table shows fleet activity for Rail North America railcars, excluding boxcars, for the quarter ended:

September 30 2017 | December 31 2017 | March 31 2018 | June 30 2018 | September 30 2018 | ||||||||||

Beginning balance | 104,007 | 103,692 | 103,730 | 102,597 | 102,890 | |||||||||

Cars added | 637 | 786 | 1,226 | 1,231 | 1,381 | |||||||||

Cars scrapped | (854 | ) | (600 | ) | (673 | ) | (720 | ) | (431 | ) | ||||

Cars sold | (98 | ) | (148 | ) | (1,686 | ) | (218 | ) | (420 | ) | ||||

Ending balance | 103,692 | 103,730 | 102,597 | 102,890 | 103,420 | |||||||||

Utilization rate at quarter end | 98.5 | % | 98.2 | % | 98.2 | % | 98.9 | % | 99.2 | % | ||||

Average active railcars | 102,555 | 102,078 | 101,208 | 101,330 | 102,056 | |||||||||

25

The following table shows fleet statistics for Rail North America boxcars for the quarter ended:

September 30 2017 | December 31 2017 | March 31 2018 | June 30 2018 | September 30 2018 | ||||||||||

Ending balance | 16,555 | 16,398 | 16,227 | 16,007 | 15,859 | |||||||||

Utilization | 92.4 | % | 92.6 | % | 93.5 | % | 92.8 | % | 94.7 | % | ||||

Comparison of the First Nine Months of 2018 to the First Nine Months of 2017

Segment Profit

In the first nine months of 2018, segment profit of $241.3 million increased 1.3% compared to $238.1 million in the same period in the prior year. The increase was driven by higher asset disposition gains and lower maintenance expense, partially offset by lower lease revenue and lower termination fees.

Revenues