Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - Marker Therapeutics, Inc. | tv499451_ex32-2.htm |

| EX-32.1 - EXHIBIT 32.1 - Marker Therapeutics, Inc. | tv499451_ex32-1.htm |

| EX-31.2 - EXHIBIT 31.2 - Marker Therapeutics, Inc. | tv499451_ex31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - Marker Therapeutics, Inc. | tv499451_ex31-1.htm |

UNITED STATES SECURITIES AND EXCHANGE

COMMISSION

Washington, D.C. 20549

FORM 10-Q

| x | Quarterly Report Under Section 13 or 15(d) of the Securities Exchange Act of 1934 for the quarterly period ended June 30, 2018 |

| ¨ | Transition Report Under Section 13 or 15(d) of the Securities Exchange Act of 1934 for the transition period from _____ to _____. |

Commission File Number: 001-37939

TAPIMMUNE INC.

(Name of registrant in its charter)

| NEVADA | 45-4497941 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

|

5 West Forsyth Street, Suite 200 Jacksonville, FL |

32202 | |

| (Address of principal executive offices) | (Zip Code) | |

| 904-516-5436 | ||

| (Issuer's telephone number) |

Indicate by check mark whether the registrant (1) filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, non-accelerated filer, a smaller reporting company, or an emerging growth company. See definition of “accelerated filer”, “large accelerated filer”, “smaller reporting company”, and “emerging growth company” in Rule 12b-2 of the Exchange Act (check one):

| ¨ | Large accelerated filer | ¨ | Accelerated filer |

| ¨ | Non-accelerated filer (Do not check | x | Smaller reporting company |

| if smaller reporting company) | ¨ | Emerging growth company | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

As of August 2, 2018, the Company had 13,710,544 shares of common stock issued and outstanding.

| PART I. | FINANCIAL INFORMATION |

| Item 1. | Financial Statements |

CONDENSED CONSOLIDATED BALANCE SHEETS

(UNAUDITED)

| June 30, | December 31, | |||||||

| 2018 | 2017 | |||||||

| ASSETS | ||||||||

| Current assets: | ||||||||

| Cash | $ | 7,782,962 | $ | 5,129,289 | ||||

| Prepaid expenses and deposits | 108,716 | 51,150 | ||||||

| Total current assets | 7,891,678 | 5,180,439 | ||||||

| Total assets | $ | 7,891,678 | $ | 5,180,439 | ||||

| LIABILITIES AND STOCKHOLDERS' EQUITY | ||||||||

| Current liabilities: | ||||||||

| Accounts payable and accrued liabilities | $ | 3,595,152 | $ | 1,508,312 | ||||

| Warrant liability | 147,000 | 9,000 | ||||||

| Promissory note | 5,000 | 5,000 | ||||||

| Total current liabilities | 3,747,152 | 1,522,312 | ||||||

| Total liabilities | 3,747,152 | 1,522,312 | ||||||

| COMMITMENTS AND CONTINGENCIES | ||||||||

| Stockholders' equity: | ||||||||

| Preferred stock - $0.001 par value, 5 million shares authorized at June 30, 2018 and December 31, 2017, respectively | ||||||||

| Series A, $0.001 par value, 1.25 million shares designated, 0 shares issued and outstanding as of June 30, 2018 and December 31, 2017, respectively | - | - | ||||||

| Series B, $0.001 par value, 1.5 million shares designated, 0 shares issued and outstanding as of June 30, 2018 and December 31, 2017, respectively | - | - | ||||||

| Common stock, $0.001 par value, 41.7 million shares authorized, 13.6 million and 10.6 million shares issued and outstanding as of June 30, 2018 and December 31, 2017, respectively | 13,624 | 10,616 | ||||||

| Additional paid-in capital | 170,287,725 | 161,067,538 | ||||||

| Accumulated deficit | (166,156,823 | ) | (157,420,027 | ) | ||||

| Total stockholders' equity | 4,144,526 | 3,658,127 | ||||||

| Total liabilities and stockholders' equity | $ | 7,891,678 | $ | 5,180,439 | ||||

See accompanying notes to these unaudited condensed consolidated financial statements.

| 1 |

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(UNAUDITED)

| For the three months ended | For the six months ended | |||||||||||||||

| June 30, | June 30, | |||||||||||||||

| 2018 | 2017 | 2018 | 2017 | |||||||||||||

| Revenues: | ||||||||||||||||

| Grant income | $ | 205,994 | $ | - | $ | 205,994 | $ | - | ||||||||

| Total revenues | 205,994 | - | 205,994 | - | ||||||||||||

| Operating expenses: | ||||||||||||||||

| Research and development | $ | 1,826,837 | $ | 1,202,725 | $ | 3,426,387 | $ | 2,191,817 | ||||||||

| General and administrative | 3,052,954 | 1,190,517 | 4,650,890 | 2,618,310 | ||||||||||||

| Total operating expenses | 4,879,791 | 2,393,242 | 8,077,277 | 4,810,127 | ||||||||||||

| Loss from operations | (4,673,797 | ) | (2,393,242 | ) | (7,871,283 | ) | (4,810,127 | ) | ||||||||

| Other income (expense): | ||||||||||||||||

| Change in fair value of warrant liabilities | (139,000 | ) | 7,500 | (138,000 | ) | 4,500 | ||||||||||

| Debt extinguishment gain | - | 492,365 | - | 492,365 | ||||||||||||

| Net loss | $ | (4,812,797 | ) | $ | (1,893,377 | ) | $ | (8,009,283 | ) | $ | (4,313,262 | ) | ||||

| Net loss per share, Basic and Diluted | $ | (0.41 | ) | $ | (0.22 | ) | $ | (0.71 | ) | $ | (0.51 | ) | ||||

| Weighted average number of common shares outstanding | 11,838,371 | 8,576,634 | 11,233,755 | 8,503,521 | ||||||||||||

See accompanying notes to these unaudited condensed consolidated financial statements.

| 2 |

CONDENSED CONSOLIDATED STATEMENT OF STOCKHOLDERS’ EQUITY

(UNAUDITED)

| Common Stock | Additional Paid- | Accumulated | Total Stockholders' | |||||||||||||||||

| Shares | Par value | in Capital | Deficit | Equity | ||||||||||||||||

| Balance at January 1, 2018 | 10,615,724 | $ | 10,616 | $ | 161,067,538 | $ | (157,420,027 | ) | $ | 3,658,127 | ||||||||||

| Issuance of common stock in private placement | 1,300,000 | 1,300 | 3,118,700 | - | 3,120,000 | |||||||||||||||

| Stock options exercised for cash | 10,416 | 10 | 18,115 | - | 18,125 | |||||||||||||||

| Stock warrants exercised for cash | 1,446,881 | 1,447 | 4,259,638 | - | 4,261,085 | |||||||||||||||

| Stock warrants cashless exercised | 118,425 | 118 | (118 | ) | - | - | ||||||||||||||

| Stock-based compensation | 132,825 | 133 | 1,096,339 | - | 1,096,472 | |||||||||||||||

| Fair value of repriced warrants as inducement | - | - | 727,513 | (727,513 | ) | - | ||||||||||||||

| Net loss | - | - | - | (8,009,283 | ) | (8,009,283 | ) | |||||||||||||

| Balance, June 30, 2018 | 13,624,271 | $ | 13,624 | $ | 170,287,725 | $ | (166,156,823 | ) | $ | 4,144,526 | ||||||||||

See accompanying notes to these unaudited condensed consolidated financial statements.

| 3 |

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(UNAUDITED)

| For the six months ended | ||||||||

| June 30, | ||||||||

| 2018 | 2017 | |||||||

| Cash Flows from Operating Activities: | ||||||||

| Net loss | $ | (8,009,283 | ) | $ | (4,313,262 | ) | ||

| Reconciliation of net loss to net cash used in operating activities: | ||||||||

| Changes in fair value of warrant liabilities | 138,000 | (4,500 | ) | |||||

| Stock-based compensation | 1,096,472 | 647,387 | ||||||

| Debt extinguishment gain | - | (492,365 | ) | |||||

| Changes in operating assets and liabilities: | ||||||||

| Prepaid expenses and deposits | (57,566 | ) | (109,032 | ) | ||||

| Accounts payable and accrued expenses | 2,086,840 | 336,135 | ||||||

| Net cash used in operating activities | (4,745,537 | ) | (3,935,637 | ) | ||||

| Cash Flows from Financing Activities: | ||||||||

| Proceeds from issuance of common stock and warrants in private placement, net of offering costs | 3,120,000 | 5,408,343 | ||||||

| Proceeds from exercise of stock warrants, net of offering costs | 4,261,085 | 638,666 | ||||||

| Proceeds from exercise of stock options | 18,125 | - | ||||||

| Net cash provided by financing activities | 7,399,210 | 6,047,009 | ||||||

| Net increase in cash | 2,653,673 | 2,111,372 | ||||||

| Cash at beginning of period | 5,129,289 | 7,851,243 | ||||||

| Cash at end of period | $ | 7,782,962 | $ | 9,962,615 | ||||

| For the six months ended | ||||||||

| June 30, | ||||||||

| 2018 | 2017 | |||||||

Supplemental schedule of non-cash financing activities: | ||||||||

Fair value of repriced warrants as inducement | $ | 727,513 | $ | 622,042 | ||||

Stock warrants cashless exercised | $ | 118 | $ | - | ||||

See accompanying notes to these unaudited condensed consolidated financial statements.

| 4 |

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2018

(Unaudited)

Note 1: Nature of Operations

TapImmune Inc. (the “Company” or “we”), a Nevada corporation incorporated in 1991, is a biotechnology company focusing on immunotherapy specializing in the development of innovative peptide and gene-based immunotherapeutics and vaccines for the treatment of oncology. Unlike other vaccine technologies that narrowly address the initiation of an immune response, TapImmune's approach broadly stimulates the cellular immune system by enhancing the function of killer T-cells and T-helper cells and by restoring antigen presentation in tumor cells allowing their recognition by the immune system.

NOTE 2: Basis of Presentation

The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with the accounting principles generally accepted in the United States of America (“U.S. GAAP”) for interim financial information and pursuant to the instructions to Form 10-Q and Article 8 of Regulation S-X of the Securities and Exchange Commission (“SEC”) and on the same basis as the Company prepares its annual audited consolidated financial statements. In the opinion of management, the accompanying unaudited condensed consolidated financial statements reflect all adjustments, consisting of normal recurring adjustments, considered necessary for a fair presentation of such interim results.

The results for the condensed consolidated statement of operations are not necessarily indicative of results to be expected for the year ending December 31, 2018 or for any future interim period. The condensed consolidated balance sheet at June 30, 2018 has been derived from unaudited financial statements; however, it does not include all of the information and notes required by U.S. GAAP for complete financial statements. The accompanying condensed consolidated financial statements should be read in conjunction with the consolidated financial statements for the year ended December 31, 2017, and notes thereto included in the Company’s annual report on Form 10-K filed on March 23, 2018.

NOTE 3: LIQUIDITY AND FINANCIAL CONDITION

The Company’s activities since inception have consisted principally of acquiring product and technology rights, raising capital, and performing research and development. Successful completion of the Company’s development programs and, ultimately, the attainment of profitable operations are dependent on future events, including, among other things, its ability to access potential markets; secure financing, develop a customer base; attract, retain and motivate qualified personnel; and develop strategic alliances and collaborations. From inception, the Company has been funded by a combination of equity and debt financings.

The Company expects to continue to incur substantial losses over the next several years during its development phase. To fully execute its business plan, the Company will need to complete certain research and development activities and clinical studies. Further, the Company’s product candidates will require regulatory approval prior to commercialization. These activities may span many years and require substantial expenditures to complete and may ultimately be unsuccessful. Any delays in completing these activities could adversely impact the Company. The Company plans to meet its capital requirements primarily through issuances of debt and equity securities and, in the longer term, revenue from product sales.

As of June 30, 2018, the Company had cash of approximately $7.8 million. Historically, the Company had net losses and negative cash flows from operations. Management intends to continue its research efforts and to finance operations of the Company through debt and/or equity financings. Management plans to seek additional debt and/or equity financing through private or public offerings. There can be no assurance that the Company will be successful in obtaining additional financing on favorable terms, or at all. The Company has no sources of revenue to provide incoming cash flows to sustain its future operations. The Company’s ability to pursue its planned business activities is dependent upon successful efforts to raise additional capital. These factors raise substantial doubt regarding the Company’s ability to continue as a going concern. The financial statements do not include any adjustments that might result from the outcome of these uncertainties.

| 5 |

Note 4: SIGNIFICANT ACCOUNTING POLICIES

There have been no material changes in the Company’s significant accounting policies to those previously disclosed in the Company’s annual report on Form 10-K, which was filed with the SEC on March 23, 2018.

New Accounting Pronouncements

From time to time, new accounting pronouncements are issued by the Financial Accounting Standards Board (“FASB”) or other standard setting bodies that we adopt as of the specified effective date. Unless otherwise discussed, we do not believe that the impact of recently issued standards that are not yet effective will have a material impact on our financial position or results of operations upon adoption.

Recent Accounting Pronouncements Adopted in the Year

Compensation-Stock Compensation

In May 2017, the FASB issued Accounting Standards Update (“ASU”) No. 2017-09, Compensation—Stock Compensation (Topic 718): Scope of Modification Accounting, which clarifies when to account for a change to the terms or conditions of a share-based payment award as a modification. Under the new guidance, modification accounting is required only if the fair value, the vesting conditions, or the classification of the award (as equity or liability) changes as a result of the change in terms or conditions. It is effective prospectively for the annual period beginning after December 15, 2017 and interim periods within that annual period. Early adoption is permitted. The Company adopted ASU 2017-09 on January 1, 2018; the adoption of ASU 2017-09 did not have a material impact on its financial condition or results of operations, as the Company has not had any modifications to share-based payment awards. However, if the Company does have a modification to an award in the future, it will follow the guidance in ASU 2017-09.

Revenue from Contracts with Customers

In May 2014, the FASB issued ASU No. 2014-09, “Revenue from Contracts with Customers (Topic 606)” (ASU 2014-09) as modified by ASU No. 2015-14, “Revenue from Contracts with Customers (Topic 606): Deferral of the Effective Date,” ASU 2016-08, “Revenue from Contracts with Customers (Topic 606): Principal versus Agent Considerations (Reporting Revenue Gross versus Net),” ASU No. 2016-10, “Revenue from Contracts with Customers (Topic 606): Identifying Performance Obligations and Licensing,” and ASU No. 2016-12, “Revenue from Contracts with Customers (Topic 606): Narrow-Scope Improvements and Practical Expedients.” The revenue recognition principle in ASU 2014-09 is that an entity should recognize revenue to depict the transfer of goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. In addition, new and enhanced disclosures will be required. Companies may adopt the new standard either using the full retrospective approach, a modified retrospective approach with practical expedients, or a cumulative effect upon adoption approach. The Company adopted the new standard effective January 1, 2018, using the modified retrospective approach. The only impact of the adoption of ASU 2014-09 was to reclassify the Company's grant income as revenue.

Recent Accounting Pronouncements Not Yet Adopted

Accounting for Certain Financial Instruments with Down Round Features

On July 13, 2017, the FASB has issued a two-part ASU, No. 2017-11, (i). Accounting for Certain Financial Instruments with Down Round Features and (ii) Replacement of the Indefinite Deferral for Mandatorily Redeemable Financial Instruments of Certain Nonpublic Entities and Certain Mandatorily Redeemable Noncontrolling Interests With a Scope Exception.

The ASU is effective for public business entities for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2018 and the interim periods within that annual period. Early adoption is permitted. The Company will be evaluating the impact of adopting this standard on the consolidated financial statements and disclosures.

Improvements to Nonemployee Share-Based Payment Accounting

In June 2018, the FASB issued ASU 2018-07 “Improvements to Nonemployee Share-Based Payment Accounting”, which simplifies the accounting for share-based payments granted to nonemployees for goods and services. Under the ASU, most of the guidance on such payments to nonemployees would be aligned with the requirements for share-based payments granted to employees. The amendments are effective for fiscal years beginning after December 15, 2019, and interim periods within fiscal years beginning after December 15, 2020. Early adoption is permitted, but no earlier than an entity’s adoption date of Topic 606. The Company is currently evaluating the impact of the new standard on its consolidated financial statements.

| 6 |

Note 5: NET LOSS PER SHARE APPLICABLE TO COMMON SHAREHOLDER

Basic loss per common share is computed by dividing net loss by the weighted average number of common shares outstanding during the reporting period. Diluted loss per common share is computed similarly to basic loss per common share except that it reflects the potential dilution that could occur if dilutive securities or other obligations to issue common stock were exercised or converted into common stock.

The following table sets forth the computation of net loss per share:

| Six Months Ended | Six Months Ended | |||||||||||||||

| June 30, | June 30, | |||||||||||||||

| 2018 | 2017 | 2018 | 2017 | |||||||||||||

| Numerator: | ||||||||||||||||

| Net loss | $ | (4,812,797 | ) | $ | (1,893,377 | ) | $ | (8,009,283 | ) | $ | (4,313,262 | ) | ||||

| Denominator: | ||||||||||||||||

| Weighted average common shares outstanding | 11,838,371 | 8,576,634 | 11,233,755 | 8,503,521 | ||||||||||||

| Net loss per share data: | ||||||||||||||||

| Basic and Diluted | $ | (0.41 | ) | $ | (0.22 | ) | $ | (0.71 | ) | $ | (0.51 | ) | ||||

The following securities, rounded to the thousand, were not included in the diluted net loss per share calculation because their effect was anti-dilutive for the periods presented:

| Six Months Ended | ||||||||

| June 30, | ||||||||

| 2018 | 2017 | |||||||

| Common stock options | 439,000 | 455,000 | ||||||

| Common stock purchase warrants | 4,871,000 | 6,544,000 | ||||||

| Potentially dilutive securities | 5,310,000 | 6,999,000 | ||||||

Note 6: WARRANT LIABILITY AND FAIR VALUE MEASUREMENTS

A summary of quantitative information with respect to valuation methodology and significant unobservable inputs used for the Company’s common stock purchase warrants that are categorized within Level 3 of the fair value hierarchy for the six months ended June 30, 2018 and 2017 is as follows:

| June 30, | June 30, | |||||||

| 2018 | 2017 | |||||||

| Stock price | $ | 9.43 | $ | 3.88 | ||||

| Exercise price | $ | 8.67 | $ | 1.20 | ||||

| Contractual term (years) | 1.32 | 1.03 | ||||||

| Volatility (annual) | 83 | % | 78 | % | ||||

| Risk-free rate | 1 | % | 1 | % | ||||

| Dividend yield (per share) | 0 | % | 0 | % | ||||

The foregoing assumptions are reviewed quarterly and are subject to change based primarily on management’s assessment of the probability of the events described occurring. Accordingly, changes to these assessments could materially affect the valuations.

| 7 |

Financial Liabilities Measured at Fair Value on a Recurring Basis

Financial liabilities measured at fair value on a recurring basis are summarized below and disclosed on the balance sheet under Warrant liability:

| Fair value measured at June 30, 2018 | |||||||||||||||

| Quoted prices in active | Significant other | Significant | |||||||||||||

| markets | observable inputs | unobservable inputs | Fair value at | ||||||||||||

| (Level 1) | (Level 2) | (Level 3) | June 30, 2018 | ||||||||||||

| Warrant liability | $ | - | $ | - | $ | 147,000 | $ | 147,000 | |||||||

| Fair value measured at December 31, 2017 | |||||||||||||||

| Quoted prices in active | Significant other | Significant | |||||||||||||

| markets | observable inputs | unobservable inputs | Fair value at | ||||||||||||

| (Level 1) | (Level 2) | (Level 3) | December 31, 2017 | ||||||||||||

| Warrant liability | $ | - | $ | - | $ | 9,000 | $ | 9,000 | |||||||

The fair value accounting standards define fair value as the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants. As such, fair value is determined based upon assumptions that market participants would use in pricing an asset or liability. Fair value measurements are rated on a three-tier hierarchy as follows:

| · | Level 1 inputs: Quoted prices (unadjusted) for identical assets or liabilities in active markets; |

| · | Level 2 inputs: Inputs, other than quoted prices included in Level 1, that are observable either directly or indirectly; and |

| · | Level 3 inputs: Unobservable inputs for which there is little or no market data, which require the reporting entity to develop its own assumptions. |

There were no transfers between Level 1, 2 or 3 during the six months ended June 30, 2018.

The following table presents changes in Level 3 liabilities measured at fair value for the six months ended June 30, 2018:

| Warrant | ||||

| Liability | ||||

| Balance - December 31, 2017 | $ | 9,000 | ||

| Change in fair value of warrant liability | 138,000 | |||

| Balance – June 30, 2018 | $ | 147,000 | ||

Note 7: STOCKHOLDERS’ EQUITY

2018 Common Stock Transactions

Common Stock Purchase Agreement

On May 14, 2018, the Company’s largest stockholder Eastern Capital Limited entered into a Common Stock Purchase Agreement with the Company pursuant to which it purchased 1,300,000 shares of common stock at a price per share of $2.40 providing gross proceeds to the Company of $3.12 million.

Exercise and Repricing of Warrants Held by Existing Institutional Investors

On May 14, 2018, certain institutional holders of outstanding warrants entered into Warrant Exercise Agreements with the Company that provide for an amendment to the exercise price of the warrants being exercised at $2.50 per share. Upon closing of the Warrant Exercise Agreements, such institutional holders immediately exercised warrants for 782,505 shares of common stock providing aggregate proceeds to the Company of approximately $2.0 million.

The fair value relating to the modification of exercise prices on the repriced and exercised warrants was treated as deemed dividend on the statement of stockholders’ equity of $728,000.

A weighted average summary of quantitative information with respect to valuation methodology and significant unobservable inputs used for the Company’s common stock purchase warrants that are included in the modification is as follows:

| 8 |

| Weighted Average Inputs | ||||||||

| Before | After | |||||||

| Modification | Modification | |||||||

| Exercise price | $ | 9.93 | $ | 2.50 | ||||

| Contractual term (years) | 2.37 | 2.37 | ||||||

| Volatility (annual) | 79 | % | 79 | % | ||||

| Risk-free rate | 1.5 | % | 1.5 | % | ||||

| Dividend yield (per share) | 0 | % | 0 | % | ||||

Exercise of Stock Warrants

During June 2018, shareholders exercised 782,800 shares of common stock pursuant to stock warrants providing aggregate proceeds to the Company of approximately $2.3 million. 118,425 of the stock warrants exercised were exercised on a cashless basis, resulting in a cancellation of 83,130 stock warrants.

Exercise of Stock Options

In January 2018, 10,416 shares of common stock were issued pursuant to stock option exercises at an exercise price equal to $1.74 per share.

Consulting Arrangements

During the six months ended June 30, 2018, the Company issued 132,825 shares of common stock as part of consulting agreements. The fair value of the common stock of approximately $644,000 was recognized as stock-based compensation, $563,000 in general and administrative expenses and $81,000 in research and development expenses.

Share Purchase Warrants

A summary of the Company’s share purchase warrants as of June 30, 2018 and changes during the period is presented below:

| Weighted Average | ||||||||||||||||

| Number of | Weighted Average | Remaining Contractual | Total Intrinsic | |||||||||||||

| Warrants | Exercise Price | Life (in years) | Value | |||||||||||||

| Balance - January 1, 2018 | 6,520,000 | $ | 6.11 | 3.16 | $ | 1,739,000 | ||||||||||

| Issued | - | - | - | - | ||||||||||||

| Cashless exercised | (118,000 | ) | 4.01 | - | - | |||||||||||

| Exercised for cash | (1,447,000 | ) | 2.95 | - | - | |||||||||||

| Expired or Cancelled | (84,000 | ) | 4.01 | - | - | |||||||||||

| Balance - June 30, 2018 | 4,871,000 | $ | 5.94 | 2.76 | $ | 20,417,000 | ||||||||||

Note 8: STOCK-BASED COMPENSATION

The Company recorded approximately $960,000 and $271,000 of stock-based compensation expense for the three months ended June 30, 2018 and 2017, respectively. The Company recorded approximately $1,096,000 and $647,000 of stock-based compensation expense for the six months ended June 30, 2018 and 2017, respectively.

At June 30, 2018, the total stock-based compensation cost related to unvested awards not yet recognized was $159,000. The expected weighted average period compensation costs to be recognized was 0.48 years. Future option grants will impact the compensation expense recognized.

$596,000 and $364,000 of stock-based compensation expenses for the three months ended June 30, 2018 were included in general and administrative expenses and research and development expenses, respectively, on the condensed consolidated statements of operations.

$629,000 and $467,000 of stock-based compensation expenses for the six months ended June 30, 2018 were included in general and administrative expenses and research and development expenses, respectively, on the condensed consolidated statements of operations.

| 9 |

Note 9: grant income

During the six months ended June 30, 2018, the Company received $0.2 million of a grant awarded to Mayo Foundation from the U.S. Department of Defense for the Phase II Clinical Trial of TPIV200. The grant compensated the Company for clinical supplies manufactured and provided by the Company for the clinical study. In accordance with Accounting Standards Update No. 2014-09, “Revenue from Contracts with Customers (Topic 606)” issued by the Financial Accounting Standards Board, the Company recorded the $0.2 million of grant income as revenue.

| 10 |

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

This quarterly report on Form 10-Q contains forward-looking statements within the meaning of Section 21E of the Securities and Exchange Act of 1934, as amended, that involve risks and uncertainties. All statements other than statements relating to historical matters including statements to the effect that we “believe”, “expect”, “anticipate”, “plan”, “target”, “intend” and similar expressions should be considered forward-looking statements. Our actual results could differ materially from those discussed in the forward-looking statements as a result of a number of important factors, including factors discussed in this section and elsewhere in this quarterly report on Form 10-Q, and the risks discussed in our other filings with the Securities and Exchange Commission. Readers are cautioned not to place undue reliance on these forward-looking statements, which reflect management’s analysis, judgment, belief or expectation only as the date hereof. We assume no obligation to update these forward-looking statements to reflect events or circumstance that arise after the date hereof.

As used in this quarterly report: (i) the terms “we”, “us”, “our”, “TapImmune” and the “Company” mean TapImmune Inc. and its wholly owned subsidiary, GeneMax Pharmaceuticals Inc. which wholly owns GeneMax Pharmaceuticals Canada Inc., unless the context otherwise requires; (ii) “SEC” refers to the Securities and Exchange Commission; (iii) “Securities Act” refers to the Securities Act of 1933, as amended; (iv) “Exchange Act” refers to the Securities Exchange Act of 1934, as amended; and (v) all dollar amounts refer to United States dollars unless otherwise indicated.

The following should be read in conjunction with our unaudited condensed consolidated interim financial statements and related notes for the three and six months ended June 30, 2018 included in this quarterly report, as well as our Annual Report on Form 10-K for the year ended December 31, 2017 filed on March 23, 2018.

Company Overview

We are a clinical-stage immuno-oncology company specializing in the development of innovative peptide and gene-based immunotherapeutics and vaccines for the treatment of cancer and metastatic disease. We are actively advancing our clinical programs by expanding our Folate Receptor Alpha program (TPIV200) for breast and ovarian cancers and our HER2/neu peptide antigen program (TPIV110) in Phase II clinical trials. In parallel, we are developing a proprietary DNA expression technology named PolyStart™ to improve the ability of the cellular immune system to recognize and destroy diseased cells. We plan to complete the pre-clinical development of our PolyStart™ vaccine and move it into the clinic as an integral component of a prime-boost vaccine methodology.

We are a leader in the development of immunotherapies for women's cancers, with multiple Phase 2 and Phase 1b/2 clinical studies for the treatment of ovarian and breast cancer. The company's peptide or nucleic acid-based immunotherapeutic products comprise one or multiple naturally processed epitopes (NPEs) designed to comprehensively stimulate a patient's killer T-cells and helper T-cells, and to restore or further augment antigen presentation by using proprietary nucleic acid-based expression systems. Our technologies may be used as stand-alone medications or in combination with current treatment modalities.

Immuno-oncology has become the most rapidly growing sector in the pharmaceutical and biotech industry. The approval and success of checkpoint inhibitors, including ipilimumab and nivolumab (Yervoy® and Opdivo®, respectively, Bristol Myers Squibb), pembrolizumab (Keytruda®, Merck & Co.), avelumab (Bavencio®, EMD Serono), durvalumab (Imfinzi™, AstraZeneca), and atezolizumab (Tecentriq®, Genentech), together with the development and approval of CAR T-cell therapies sponsored by Novartis, Juno Therapeutics, and Kite Pharma, has provided much momentum in this sector. In addition, new evidence points to the increasing use of combination immunotherapies for the treatment of cancer. This has provided greater justification and opportunities for the successful development of T-cell vaccines in combination with other approaches.

On May 23, 2017, the U.S. Food and Drug Administration (“FDA”) approved expanded use of Keytruda for immunotherapy. The FDA granted accelerated approval to a treatment for patients whose cancers have a specific genetic feature (biomarker). This is the first time the FDA has approved a cancer treatment based on a common biomarker rather than the location in the body where the tumor originated.

We believe the strength of our science and development approaches is becoming more widely appreciated, particularly as our clinical program has now generated positive Phase I data using our two products in clinical programs in breast and ovarian cancers.

| 11 |

We continue to focus primarily on our Phase II triple-negative breast cancer trials using TPIV200 (which has achieved Fast Track and Orphan Drug Status), and are planning for the next Phase II HER2/neu breast cancer trial.

We expect to continue to prosecute our PolyStart™ patent filings and develop new PolyStart™ constructs to facilitate collaborative efforts in our current clinical indications. We will also evaluate those indications where others have already indicated interest in combination therapies.

We believe that these fundamental programs and corporate activities have positioned our company to capitalize on the acceptance of immunotherapy as a leading therapeutic strategy in cancer and infectious diseases.

We are continuously working on improving our product formulation and supply. TPIV200 and TPIV110 are both off-the-shelf, lyophilized products that only require reconstitution and mixing with GM-CSF at the clinical site before injection. We believe our off-the-shelf product may provide a significant competitive advantage over autologous products that require preparation for each patient. We also believe the investments we have made in the formulation work for both very stable products will result in commercially viable products consistent with typically high pharmaceutical profit margins.

The Phase I data produced for both TPIV200 and TPIV100 in collaboration with the Mayo Clinic are the driving force behind the high-value collaborations we have established and maintained with organizations such as Mayo Clinic, AstraZeneca, Memorial Sloan Kettering, and the U.S. Department of Defense. As we move forward into advanced Phase II studies, some of which incorporate collaborations with prestigious third-party organizations, we believe they will represent further independent validation of the potential of our technology.

Recent Developments

Merger Agreement

On May 15, 2018, we and our wholly owned subsidiary, (formed for purposes of the Merger) Timberwolf Merger Sub, Inc., a Delaware corporation (“Merger Sub”), and Marker Therapeutics, Inc., a Delaware corporation (“Marker”), entered into an Agreement and Plan of Merger and Reorganization (the “Merger Agreement”). Subject to the terms and conditions set forth in the Merger Agreement, MergerSub will merge with and into Marker (the “Merger”), with Marker surviving the Merger as a wholly owned subsidiary of TapImmune (the “Surviving Corporation”).

At the effective time of the Merger (the “Effective Time”), each outstanding share of Marker’s common stock will be converted into the right to receive (i) shares of TapImmune’s common stock, par value $0.001 per share (“TapImmune Common Stock”), in an amount equal to the exchange ratio calculated pursuant to the Merger Agreement (the “Stock Exchange Ratio”), and (ii) warrants to purchase TapImmune Common Stock, in an amount equal to the exchange ratio calculated pursuant to the Merger Agreement (the “Warrant Exchange Ratio”).

The Merger Agreement contains customary representations, warranties and covenants made by us and Marker, including covenants relating to obtaining the requisite approvals of the stockholders of TapImmune and Marker, indemnification of directors and officers, and TapImmune’s and Marker’s conduct of their respective businesses between the date of signing of the Merger Agreement and the closing of the Merger.

The issuance of TapImmune Common Stock and other transactions contemplated by the Merger Agreement are subject to approval by TapImmune’s stockholders. The Merger is subject to other customary closing conditions, including, among other things, the accuracy of the representations and warranties, subject generally to an overall material adverse effect qualification, compliance by the parties with their respective covenants and no existence of any law or order preventing the Merger and related transactions.

| 12 |

The Merger Agreement contains certain termination rights for both us and Marker and provides for the payment of a termination fee of $1,500,000 by us to Marker upon termination of the Merger Agreement under specified circumstances. In connection with a termination of the Merger Agreement under specified circumstances involving competing transactions, a willful, intentional and material breach of the non-solicitation obligations by us, a change in our board of directors’ recommendation of the Merger to the stockholders or other triggering events, we may be required to pay Marker reimbursement for certain fees and expenses up to $500,000. In connection with a termination of the Merger Agreement under specified circumstances involving the failure of Marker stockholders to approve the Merger Agreement within 24 hours of signing the Merger Agreement, intentional and material breach of the non-solicitation obligations by Marker or other triggering events, Marker may be required to pay our reimbursement for certain fees and expenses up to $500,000. The Merger Agreement may also be terminated by either us or Marker if the merger has not been consummated by September 15, 2018, subject to an extension of an additional 60 days if our proxy statement is being reviewed or commented upon by the SEC.

Following the Merger, the board of directors of the Company will consist of six directors and will be comprised of (i) three members designated by Marker, and (ii) three members designated by us.

Common Stock Purchase Agreement

On May 18, 2018, we closed on the sale of 1,300,000 shares of common stock for $2.40 per share pursuant to a Common Stock Purchase Agreement with an existing accredited investor in a private placement under Rule 506 of Regulation D. Aggregate gross proceeds were approximately $3.1 million.

Exercise of Warrants Held by Existing Institutional Investors

Also on May 18, 2018, we and certain existing institutional investors, who are holders of various warrants to purchase shares of TapImmune common stock, closed on Warrant Exercise Agreements in which TapImmune agreed to reduce the exercise price for a portion of the investors’ previously purchased Series C, Series D, Series E and Series F warrants from $6.00, $9.00, $15.00 and $7.20, respectively per share to $2.50 per share, provided that the investors exercise such warrants for cash immediately, which they did, for 782,506 shares and aggregate proceeds of approximately $2.0 million. The shares of common stock underlying the exercised warrants are registered for resale under the Form S-3 Registration Statement (File no. 333-220538) declared effective by the SEC on December 29, 2017.

Private Placement

On June 8, 2018, in connection with, and in furtherance of, the Merger Agreement, we entered into Securities Purchase Agreements for a private placement with a select group of institutional and accredited investors (the “Purchasers”). Pursuant to the Securities Purchase Agreements, the Purchasers have agreed to purchase 17,500,000 shares of the Company’s common stock, par value $0.001, at $4.00 per share, for gross offering proceeds of $70 million. Each share of common stock will be issued with a warrant to purchase 0.75 additional shares of the Company’s common stock at an exercise price of $5.00 per share for an aggregate of 13,125,000 Warrants. In accordance with NASDAQ Stock Market Rule 5635, the completion of the issuance and sale of the common stock and Warrants pursuant to the Securities Purchase Agreements is subject to the approval of the private placement by the Company’s stockholders. The Warrants will be immediately exercisable upon issuance at closing and will have a term of five years. Subject to obtaining shareholder approval of the private placement, the issuance and sale of the common stock and Warrants pursuant to the Securities Purchase Agreements is expected to close concurrently with our merger with Marker.

Intellectual Property Strategies

A key component to success is having a comprehensive patent strategy that continually updates and extends patent coverage for key products. It is highly unlikely that early patents will extend through ultimate product marketing, so extending patent life is an important strategy for ensuring product protection.

We have three active patent families that we are supporting:

1. Filed patents on the PolyStart™ expression vector (owned by TapImmune and filed in 2014: this IP covers the use with TAP). We announced the allowance of this patent in February 2016.

2. Filed patents on HER2/neu Class II and Class I antigens: exclusive license from Mayo Foundation; and

3. Filed patents on Folate Receptor Alpha antigens: exclusive license from Mayo Foundation.

While doing the studies on the path to successful product development takes time, we believe we have put together a team that can deliver the highest quality data in the least amount of time. The strength of our product pipeline and access to leading scientists and institutions gives us a unique opportunity to make a major contribution to global health care.

| 13 |

With respect to the broader market, a major driver and positive influence on our activities has been the emergence and general acceptance of the potential of a new generation of immunotherapies that promise to change the standard of care for cancer. The immunotherapy sector has been greatly stimulated by the approval of Provenge® for prostate cancer and Yervoy™ for metastatic melanoma, progression of the areas of immune checkpoint inhibitors and adoptive T-cell therapy, as well as multiple other approaches reaching Phase II and Phase III status.

We believe that through our combination of technologies, we are well positioned to be a leading player in this emerging market. It is important to note that many of the late-stage immunotherapies currently in development do not represent competition to our programs, but instead offer synergistic opportunities to partner our antigen-based immunotherapeutics and the PolyStart™ expression system. Thus, the use of naturally processed T-cell antigens discovered using samples derived from cancer patients, plus our PolyStart™ expression technology to improve antigen presentation to T-cells, could not only produce an effective cancer vaccine in its own right, but could also enhance the efficacy of other immunotherapy approaches such as CAR-T and checkpoint inhibitors.

| 14 |

Products and Technology in Development-Clinical

TPIV200

Phase I Human Clinical Trials – Folate Alpha Breast and Ovarian Cancers – Mayo Clinic

Folate Receptor Alpha (“FRa”) is overexpressed in over 80% of breast cancers and in addition, over 90% of ovarian cancers, for which the only treatment options are surgery, radiation therapy and chemotherapy, leaving a very important and urgent clinical need for a new therapeutic. Time to recurrence is relatively short for ovarian cancer and survival prognosis is extremely poor after recurrence. In the United States alone, there are approximately 30,000 ovarian cancer patients and 40,000 triple-negative breast cancer patients newly diagnosed every year.

We have completed a 21-patient Phase I clinical trial for the FRa vaccine. Twenty-one patients with breast or ovarian cancer, who had undergone standard surgery and adjuvant treatment, were treated with one cycle of cyclophosphamide. Following this, patients were vaccinated intradermally with a mixture of the five FRa peptides adjuvanted with GM-CSF (now called TPIV200) on day one of a 28-day cycle for a maximum of six vaccination cycles. The vaccine was well-tolerated and safe and 20 out of 21 evaluable patients showed positive immune responses, providing a strong rationale for progressing to Phase II trials. Further, the data showed that 16 out of 16 patients in the observation stage still showed immune responses (Source: published online 15Mar2018; DOI: 10.1158/1078-0432.CCR-17-2499). We have developed a commercial quality lyophilized formulation of the peptides in a single vial for reconstitution and injection. Good Manufacturing Practice (“GMP”) manufacturing for the Phase II trials has been completed.

On July 27, 2015, we exercised our option agreement with Mayo Foundation with the signing of a worldwide exclusive license agreement to commercialize a proprietary Folate Receptor Alpha vaccine technology for all cancer indications. As part of this agreement, the IND from the Folate Receptor Alpha Phase I Trial was transferred from Mayo Foundation to us for amendment for Phase II Clinical Trials on our lead product.

On September 15, 2015, we announced that our collaborators at the Mayo Foundation had been awarded a grant of $13.3 million from the U.S. Department of Defense. This grant, commencing September 15, 2015, covers the costs for a 280-patient Phase II Clinical Trial of Folate Receptor Alpha Vaccine in patients with triple-negative breast cancer. We are working closely with Mayo Foundation on this clinical trial by providing clinical and manufacturing expertise, as well as providing GMP vaccine formulations. These vaccine formulations are being developed for multiple Phase II clinical programs in triple-negative breast and ovarian cancer in combination with other immunotherapeutics. This Phase II study of TPIV200 in the treatment of triple-negative breast cancer began enrolling patients in late 2017.

On December 9, 2015, we announced that we received Orphan Drug Designation from the U.S. Food & Drug Administration’s Office of Orphan Products Development (“OOPD”) for our cancer vaccine TPIV200 in the treatment of ovarian cancer. The TPIV200 ovarian cancer clinical program will now receive benefits including tax credits on clinical research and seven-year market exclusivity upon receiving marketing approval. TPIV200 is a multi-epitope peptide vaccine that targets Folate Receptor Alpha which is overexpressed in multiple cancers including over 90% of ovarian cancer cells.

On February 3, 2016, we announced that the U.S. FDA designated the investigation of multiple-epitope FRa Vaccine (TPIV200) for maintenance therapy in subjects with platinum-sensitive advanced ovarian cancer who achieved stable disease or partial response following completion of standard-of-care chemotherapy, as a Fast Track Development Program. We began enrolling a Phase II study in this indication in 2017.

We have opened multiple clinical sites and have completed enrollment of patients in a Phase II trial of our Folate Receptor Alpha cancer vaccine, TPIV200, in the treatment of triple-negative breast cancer, one of the most difficult-to-treat cancers representing a clear unmet medical need. The open-label, 80-patient clinical trial is designed to evaluate dosing regimens, efficacy, and immune responses in women with triple-negative breast cancer and is fully enrolled. Key data from the trial is expected to be included in a future New Drug Application submission to the FDA for marketing clearance. This trial is sponsored and conducted by TapImmune.

| 15 |

On April 21, 2016, we announced our participation in an ovarian cancer study sponsored by Memorial Sloan Kettering Cancer Center in New York City in collaboration with AstraZeneca Pharmaceuticals in ovarian cancer patients who are not responsive to platinum, a commonly used chemotherapy for ovarian cancer. This study, a Phase II study of TPIV200 is currently enrolling ovarian cancer patients and is designed to look at the effects of combination therapy with AstraZeneca’s checkpoint inhibitor durvalumab. The study will enroll 40 patients and is open-label. Because they are unresponsive to platinum, these patients have no real options left. If the combination therapy proves effective, we believe it would address a critical unmet need. TPIV200 has received Orphan Drug designation for use in the treatment of ovarian cancer. Although we have no business relationship with AstraZeneca, we are paying for one-half of the costs of the clinical study, in addition to providing our TPIV200 for the study.

A Company-sponsored Phase II study in platinum-sensitive ovarian cancer patients was initiated in 2017. This study is designed to evaluate TPIV200 with GM-CSF in a randomized, placebo-controlled fashion during the first maintenance period after primary surgery and chemotherapy. Patients at this stage of their treatment have the highest potential for an immunotherapeutic effect and no other approved treatment options. The study will enroll up to 120 patients over the next year and a half, with an interim analysis planned in the first half of 2019.

TPIV 100/110

Phase I Human Clinical Trials – HER2/neu+ Breast Cancer – Mayo Clinic

A Phase I study using TPIV 100 (four HER2/neu peptides adjuvanted with GM-CSF) was completed in 2015. Final safety analysis on all the patients treated is complete and shown to be safe. In addition, 19 out of 20 evaluable patients showed robust T-cell immune responses to the antigens in the vaccine composition providing a solid case for advancement to Phase II in 2017. An additional secondary endpoint incorporated into this Phase I Trial will be a two-year follow on recording time to disease recurrence in the participating breast cancer patients.

For Phase I(b)/II studies, we plan to add a Class I peptide, licensed from the Mayo Clinic (April 16, 2012), to the four Class II peptides, producing TPIV 110 (five peptide product). Management believes that the combination of Class I and Class II HER2/neu antigens, gives us the leading HER2/neu vaccine platform. We are amending the IND to incorporate the fifth peptide in the Phase I(b)/II study. Discussions with the FDA have resulted in a pre-clinical development project that should allow us to file the amended IND in mid-2018.

Products and Technology-Pre-clinical

Polystart

On February 7, 2017, we announced that we received a Notice of Allowance from the U.S. Patent and Trademark Office of our patent application titled, “Chimeric nucleic acid molecules with non-AUG initiation sequences and uses thereof,” which represents our first patent on our Polystart program. We anticipate additional patent filings in connection with our research and development in this area. We plan to develop Polystart as both a stand-alone therapy and as a ‘boost strategy’ to be used synergistically with our peptide-based vaccines for breast and ovarian cancers.

| 16 |

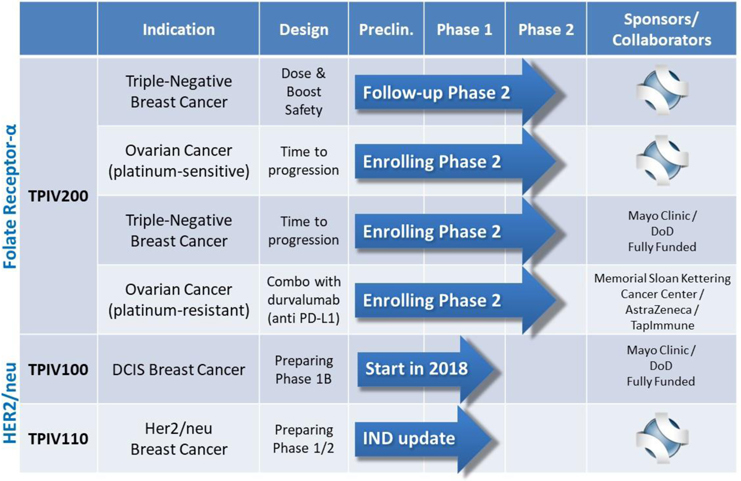

TapImmune’s Clinical Program Pipeline

Refer to the “Clinical Program Pipeline Status Updates” section below for latest updates on above clinical pipeline chart.

In addition to the exciting clinical developments, our peptide vaccine technology may be coupled with our recently developed in-house PolyStart™ nucleic acid-based technology, which is designed to make vaccines significantly more effective by producing four times the required peptides for the immune systems to recognize and act on.

Clinical Program Pipeline Status Updates

Completed GMP Manufacturing Scale Up and Second Clinical Lot of TPIV200; to Supply Additional Phase II Clinical Trials

We successfully completed a multi-gram production scale-up as well as GMP manufacturing of a second clinical lot of TPIV200. The vaccine supply will be used in the company’s ongoing Phase II study in platinum-sensitive ovarian cancer, as well as the planned 280-patient Phase II study sponsored by the Mayo Clinic and funded by the U.S. Department of Defense for treating triple-negative breast cancer. We also made various improvements to the vaccine manufacturing process, resulting in, what we believe to be, a superior formulation of the vaccine that is more amenable to large-scale manufacturing and commercialization.

Announcement of Publication of Clinical Trial Results for the TPIV200 Cancer Vaccine in Clinical Cancer Research

On March 15, 2018, we announced the publication of clinical data from a Phase I trial of TPIV200, our multi-epitope T-cell vaccine targeting Folate Receptor Alpha (“FRa”) in patients with ovarian and breast cancer. The results show that TPIV200 vaccination was well tolerated by all patients and over 90% developed robust and durable antigen-specific immune responses against FRa without regard for HLA type, which aligns with the intended mechanism of action of the vaccine.

| 17 |

Enrollment Completed: Phase II TPIV200 Trial in Triple-Negative Breast Cancer

We have completed enrollment and are now treating and following the patients in a Phase II trial of our Folate Receptor Alpha cancer vaccine, TPIV200, in the treatment of triple-negative breast cancer, one of the most difficult cancers to treat, representing a clear unmet medical need. The open-label, 80-patient clinical trial is designed to evaluate dosing regimens, pre-treatment, efficacy, and immune responses in women with triple-negative breast cancer. Key data from the trial is expected to be included in a future Biologics License Application submission to the FDA for marketing clearance. This trial is sponsored and conducted by TapImmune.

An independent Data Safety Monitoring Board (DSMB) reviews the safety every quarter in this ongoing Phase II study enrolling women with stage I-III triple-negative breast cancer who have completed initial surgery and chemo/radiation therapy. The randomized four-arm study is evaluating two doses of TPIV200 (a high dose and a low dose), each of which will be tested both with and without immune priming with cyclophosphamide prior to vaccination. Safety reviews are conducted quarterly and have shown no safety issues. The study completed enrollment at the end of 2017, with interim data expected in mid-2018. Details regarding this trial can be found at www.clinicaltrials.gov under identifier numbers NCT02593227 and FRV-002.

Enrolling Patients: Phase II TPIV200 Trial in Platinum-Sensitive Ovarian Cancer

We have opened multiple clinical sites and have enrolled half of the patients in a Phase II trial of TPIV200 for a 120-patient study on ovarian cancer patients who are responsive to platinum. We have received the FDA’s Fast Track designation to develop TPIV200 as a maintenance in women with Stage III and IV ovarian cancer who are in remission following their first round of successful platinum-based chemotherapy. This multi-center, double-blind efficacy study is sponsored and conducted by TapImmune. We expect to complete enrollment mid-2019. An interim analysis is planned based upon 50% patient progression, which we anticipate completing in the first half of 2019. Details regarding this trial can be found at www.clinicaltrials.gov under identifier numbers NCT02978222 and FRV-004. TPIV200 has also received Orphan Drug designation for use in the treatment of ovarian cancer.

Enrolling Patients: Phase II Mayo Clinic-U.S. DOD Trial of TPIV200 in Triple-Negative Breast Cancer

Patients are being enrolled in this Phase II study of TPIV200 in the treatment of triple-negative breast cancer, conducted by the Mayo Clinic and sponsored by the U.S. DOD. The 280-patient study is led by Dr. Keith Knutson of the Mayo Clinic in Jacksonville, Florida. Dr. Knutson is the inventor of the technology and a member of the Scientific Advisory Board at TapImmune. While we are supplying doses of TPIV200 for the trial and being reimbursed for the costs associated with manufacturing, the costs associated with conducting this study are being funded by a $13.3 million grant made by the DOD to the Mayo Clinic.

Enrolling Patients: Phase II Trial at Memorial Sloan Kettering of TPIV200 in Platinum-Resistant Ovarian Cancer

A Phase II study of TPIV200 in ovarian cancer patients who are not responsive to platinum, a commonly used chemotherapy for ovarian cancer, being sponsored by Memorial Sloan Kettering Cancer Center (“MSKCC”) in collaboration with AstraZeneca and TapImmune, has begun enrollment for a 40-patient study. The open-label study is designed to evaluate a combination therapy which includes our TPIV200 T-cell vaccine and AstraZeneca’s checkpoint inhibitor, durvalumab. Because they are unresponsive to platinum, these patients have no real remaining options. If the combination therapy proves effective, we believe it would address a critical unmet need. We successfully completed enrollment of the first safety cohort. This may enable MSKCC to increase the number of patients that can be enrolled and will subsequently increase the study’s enrollment rate. Currently more than 50% of patients have been enrolled. An interim analysis is planned in the second half of 2018. Details regarding this trial can be found at www.clinicaltrials.gov under identifier numbers NCT02764333.

Open IND with FDA for TPIV110 in 2018: Phase II Protocol Now in Preparation

We have enhanced the formulation of our second cancer vaccine product, TPIV110 (the five-peptide product), following very strong safety and immune responses from a Phase I Mayo Clinic study using TPIV100 (the four-peptide product). TPIV110 targets HER2/neu+, which makes it applicable to breast, ovarian, and colorectal cancers. The enhanced TPIV product adds a fifth antigen that should produce an even more robust immune response activating both CD4+ (helper) and CD8+ (killer) T-cells. We have participated in a pre-Investigational New Drug (“pre-IND”) meeting with the FDA and will file the amended IND containing the fifth peptide in mid-2018.

Mayo Clinic to Vaccinate Women With Ductal Carcinoma In Situ (DCIS) Using TapImmune TPIV100 HER2-targeted T-Cell Vaccine

On March 14, 2017, we announced that our partners at the Mayo Clinic received a grant from the U.S. Department of Defense to conduct a Phase IB study of our HER2-targeted vaccine candidate TPIV100 in an early form of breast cancer called DCIS. This is the second TapImmune vaccine to be tested in a fully funded study sponsored by the Mayo Clinic. Our collaborators at Mayo Clinic announced a $3.8 million grant which we believe would fully fund this trial. If the study is successful, our vaccine may eventually augment or even replace standard surgery and chemotherapy, and potentially could become part of a routine immunization schedule for preventing breast cancer in healthy women. The study is expected to enroll 40-45 women with DCIS and begin to commence such enrollment in mid-2018.

| 18 |

Results of Operations

In this discussion of the Company’s results of operations and financial condition, amounts, other than per-share amounts, have been rounded to the nearest thousand dollars.

Three Months Ended June 30, 2018 Compared to Three Months Ended June 30, 2017

We recorded a net loss of $4.8 million or ($0.41) basic and diluted per share during the three months ended June 30, 2018 compared to a net loss of $1.9 million or ($0.22) basic and diluted per share during the three months ended June 30, 2017. The change in net loss period over period was due to the following changes:

Revenue

Grant income

During the three months ended June 30, 2018, we received $206,000 of a grant awarded to Mayo Foundation from the US Department of Defense for the Phase II Clinical Trial of TPIV200. The grant compensated us for clinical supplies manufactured by us and provided for the clinical study.

Operating Expenses

Operating expenses incurred during the three months ended June 30, 2018 were $4.9 million compared to $2.4 million in the prior period. Significant changes in operating expenses are outlined as follows:

| · | Research and development costs during the three months ended June 30, 2018 were $1.8 million compared to $1.2 million during the prior year period. The three months ended June 30, 2018 had increased expenses from the prior period relating to our clinical trials. |

| · | General and administrative expenses increased to $3.1 million during the three months ended June 30, 2018 from $1.2 million during the prior year period. This was due to increased expenses relating to: |

| o | stock-based compensation for employees and outside consultants, |

| o | compensation expenses resulting from increased headcount, |

| o | expenses relating to the announced and proposed merger agreement, |

| o | investor relations expenses, and |

| o | increased legal, audit and other professional fees. |

Other Expense

Change in fair value of warrant liabilities

The change in fair value of warrant liabilities for the three months ended June 30, 2018 was $139,000 as compared to ($8,000) for the three months ended June 30, 2017. This increase by $139,000 for the three months ended June 30, 2018 is reflected by a corresponding expense in the condensed consolidated statement of operations.

Debt extinguishment gain

In 2003 we entered into a license agreement with a foreign based third-party for certain adenovirus technology. The license agreement was amended several times between inception and 2008 at which time it was amended and restated and had a fixed three-year term expiring in 2011. During such time, we did not pursue the technology and have not undertaken further work in the area covered by the technology license. Neither we nor the third-party took further actions under or pursuant to the license agreement. We carried a historical accrual of approximately $0.5 million under the amended license agreement related to certain obligations provided for in the license agreement. The license agreement was governed by the laws of a foreign jurisdiction. We sought and obtained legal advice related to such accrued obligations under the expired license agreement. We relied upon a judicial conclusion, as opined upon by outside legal counsel in the applicable foreign jurisdiction, that a court in such foreign jurisdiction would grant relief releasing us from liability under the license agreement, and in accordance with Accounting Standards Codification 405 “Extinguishment of Liabilities”, we recorded a debt extinguishment gain of $0.5 million and reduced the liability amount owed to $0 during the three months ended June 30, 2017.

| 19 |

Six Months Ended June 30, 2018 Compared to Six Months Ended June 30, 2017

We recorded a net loss of $8.0 million or ($0.71) basic and diluted per share during the six months ended June 30, 2018 compared to a net loss of $4.3 million or ($0.51) basic and diluted per share during the six months ended June 30, 2017. The change in net loss period over period was due to the following:

Revenue

Grant income

During the six months ended June 30, 2018, we received $206,000 of a grant awarded to Mayo Foundation from the US Department of Defense for the Phase II Clinical Trial of TPIV200. The grant compensated us for clinical supplies manufactured by us and provided for the clinical study.

Operating Expenses

Operating expenses incurred during the six months ended June 30, 2018 were $8.1 million compared to $4.8 million in the prior period. Significant changes in operating expenses are outlined as follows:

| · | Research and development costs during the six months ended June 30, 2018 were $3.4 million compared to $2.2 million during the prior year period. The six months ended June 30, 2018 had increased expenses from the prior period relating to our clinical trials. |

| · | General and administrative expenses increased to $4.7 million during the six months ended June 30, 2018 from $2.6 million during the prior year period. This was due to increased expenses relating to: |

| o | stock-based compensation for employees and outside consultants, |

| o | compensation expenses resulting from increased headcount, |

| o | expenses relating to the announced and proposed merger agreement, |

| o | investor relations expenses, and |

| o | increased legal, audit and other professional fees. |

Other Expense

Change in fair value of warrant liabilities

The change in fair value of warrant liabilities for the six months ended June 30, 2018 was $138,000 as compared to ($5,000) for the six months ended June 30, 2017. This increase by $138,000 for the six months ended June 30, 2018 is reflected by a corresponding expense in the condensed consolidated statement of operations.

Debt extinguishment gain

In 2003 we entered into a license agreement with a foreign based third-party for certain adenovirus technology. The license agreement was amended several times between inception and 2008 at which time it was amended and restated and had a fixed three-year term expiring in 2011. During such time, we did not pursue the technology and have not undertaken further work in the area covered by the technology license. Neither we nor the third-party took further actions under or pursuant to the license agreement. We carried a historical accrual of approximately $0.5 million under the amended license agreement related to certain obligations provided for in the license agreement. The license agreement was governed by the laws of a foreign jurisdiction. We sought and obtained legal advice related to such accrued obligations under the expired license agreement. We relied upon a judicial conclusion, as opined upon by outside legal counsel in the applicable foreign jurisdiction, that a court in such foreign jurisdiction would grant relief releasing us from liability under the license agreement, and in accordance with Accounting Standards Codification 405 “Extinguishment of Liabilities”, we recorded a debt extinguishment gain of $0.5 million and reduced the liability amount owed to $0 during the six months ended June 30, 2017.

| 20 |

Liquidity and Capital Resources

We have not generated any revenues since inception. We have financed our operations primarily through public and private offerings of our stock and debt including warrants and the exercises thereof.

The following table sets forth our cash and working capital as of June 30, 2018 and December 31, 2017:

| June 30, | December 31, | |||||||

| 2018 | 2017 | |||||||

| Cash | $ | 7,782,000 | $ | 5,129,000 | ||||

| Working Capital | $ | 4,144,000 | $ | 3,658,000 | ||||

Cash Flows

The following table summarizes our cash flows for the six months ended June 30, 2018 and 2017:

| Six Months Ended | ||||||||

| June 30, | ||||||||

| 2018 | 2017 | |||||||

| Net Cash provided by (used in): | ||||||||

| Operating activities | $ | (4,746,000 | ) | $ | (3,936,000 | ) | ||

| Financing activities | $ | 7,399,000 | $ | 6,047,000 | ||||

| Net increase in cash | $ | 2,653,000 | $ | 2,111,000 | ||||

| 21 |

Financings

Our financing activities during the six months ended June 30, 2018 were as follows:

Common Stock Purchase Agreement

On May 14, 2018, the Company’s largest stockholder Eastern Capital Limited entered into a Common Stock Purchase Agreement with the Company pursuant to which it purchased 1,300,000 shares of common stock at a price per share of $2.40 providing gross proceeds to the Company of $3.12 million.

Exercise and Repricing of Warrants Held by Existing Institutional Investors

On May 14, 2018, certain institutional holders of outstanding warrants entered into Warrant Exercise Agreements with the Company that provide for an amendment to the exercise price of the warrants being exercised at $2.50 per share. Upon closing of the Warrant Exercise Agreements, such institutional holders immediately exercised warrants for 782,505 shares of common stock providing aggregate proceeds to the Company of approximately $2.0 million.

The fair value relating to the modification of exercise prices on the repriced and exercised warrants was treated as deemed dividend on the statement of stockholders’ equity of $728,000.

Exercise of Stock Warrants

During June 2018, shareholders exercised warrants and acquired 782,800 shares of common stock providing aggregate proceeds to the Company of approximately $2.3 million. 118,425 of the stock warrants exercised were exercised on a cashless basis, resulting in a cancellation of 83,130 stock warrants.

Exercise of Stock Options

In January 2018, a former officer exercised 10,416 shares of common stock pursuant to stock options providing proceeds of $18,000.

Future Capital Requirements

As of June 30, 2018, we had working capital of $4.1 million, compared to working capital of $3.7 million as of December 31, 2017.

The discussion below excludes the closing of the proposed merger with Marker Therapeutics and the concurrent closing of the $70 million private placement.

We expect our expenses to continue at a similar pace through 2018 primarily to continue funding our in-process Phase II clinical trials. Two of our clinical studies are expected to be funded by a total of $17.1 million of grants made by the DOD to the Mayo Clinic. Our collaborators at Mayo Clinic announced a $3.8 million grant which we expect would fully fund a Phase II clinical trial in DCIS that we had planned for our HER2/neu+ vaccine.

Our capital requirements for 2018 and beyond will depend on numerous factors, including the success of our research and development, the resources we devote to develop and support our technologies and our success in pursuing strategic licensing and funded product development collaborations with external partners as well as other strategic initiatives we may determine to pursue. Subject to our ability to raise additional capital, we expect to incur substantial expenditures to further develop our technologies including continued increases in costs related to research, nonclinical testing and clinical studies and trials, as well as costs associated with our capital raising efforts and being a public company.

We believe our existing cash will fund our operations into the first quarter of fiscal 2019. We will require substantial additional capital to conduct research and development, to fund nonclinical testing and Phase II clinical trials of our licensed, patented technologies, and to begin cultivating collaborative relationships for the Phase II and future Phase III clinical testing. Our plans could include seeking both equity and debt financing, alliances or other partnership agreements with entities interested in our technologies, or other business transactions that could generate sufficient resources to ensure continuation of our operations and research and development programs.

We expect to continue to seek additional funding for our operations. Any such required additional capital may not be available on reasonable terms, if at all. If we were unable to obtain additional financing, we may be required to reduce the scope of, delay or eliminate some or all of our planned clinical testing and research and development activities, which could harm our business. The sale of additional equity or debt securities may result in additional dilution to our shareholders. If we raise additional funds through the issuance of debt securities or preferred stock, these securities could have rights senior to those holders of our common stock and could contain covenants that could restrict our operations. We also will require additional capital beyond our currently forecasted amounts.

| 22 |

Because of the numerous risks and uncertainties associated with research, development and commercialization of our product candidates, we are unable to estimate the exact amounts of our future working capital requirements. Our future funding requirements will depend on many factors, including, but not limited to:

| · | the number and characteristics of the product candidates we pursue; |

| · | the scope, progress, results and costs of researching and developing our product candidates, and conducting pre-clinical and clinical trials including the research and development expenditures we expect to make in connection with our license agreements with Mayo Foundation; |

| · | the amount and timing of transaction expenses we incur in connection with the pending Marker merger agreement; |

| · | strategic transactions we may undertake; |

| · | the timing of, and the costs involved in, obtaining regulatory approvals for our product candidates; |

| · | our ability to maintain current research and development licensing agreements and to establish new strategic partnerships and collaborations, licensing or other arrangements and the financial terms of such agreements; |

| · | our ability to achieve our milestones under our licensing arrangements and the payment obligations we may have under such agreements; |

| · | the costs involved in preparing, filing, prosecuting, maintaining, defending and enforcing patent claims, including litigation costs and the outcome of such litigation; and |

| · | the timing, receipt and amount of sales of, or royalties on, our future products, if any. |

We have based our estimates on assumptions that may prove to be wrong. We may need to obtain additional funds sooner or in greater amounts than we currently anticipate.

Various conditions outside of our control may detract from our ability to raise additional capital needed to execute our plan of operations, including overall market conditions in the international and local economies. We recognize that the United States economy has suffered through a period of uncertainty during which the capital markets have been impacted, and that there is no certainty that these levels will stabilize or reverse despite the optics of an improving economy. Any of these factors could have a material impact upon our ability to raise financing and, as a result, upon our short-term or long-term liquidity.

Critical Accounting Policies

The condensed consolidated financial statements are prepared in conformity with U.S. GAAP, which require the use of estimates, judgments and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent liabilities at the date of the financial statements, and the reported amounts of expenses in the periods presented. We believe that the accounting estimates employed are appropriate and resulting balances are reasonable; however, due to inherent uncertainties in making estimates, actual results could differ from the original estimates, requiring adjustments to these balances in future periods. The critical accounting estimates that affect the consolidated financial statements and the judgments and assumptions used are consistent with those described under Part II, Item 7 of our Annual Report on Form 10-K for the year ended December 31, 2017.

Going Concern

The below excludes the closing of the proposed merger with Marker Therapeutics and the concurrent closing of the $70 million private placement.

We have no sources of revenue to provide incoming cash flows to sustain our future operations. As outlined above, our ability to pursue our planned business activities is dependent upon our successful efforts to raise additional capital.

These factors raise substantial doubt regarding our ability to continue as a going concern. Our condensed consolidated financial statements have been prepared on a going concern basis, which implies that we will continue to realize our assets and discharge our liabilities in the normal course of business. Our financial statements do not include any adjustments to the recoverability and classification of recorded asset amounts and classification of liabilities that might be necessary should we be unable to continue as a going concern.

| 23 |

Off-Balance Sheet Arrangements

We have not entered into any off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on our financial condition, changes of financial condition, revenues, expenses, results of operations, liquidity, capital expenditures or capital resources that are material to investors.

| Item 3. | Quantitative and Qualitative Disclosures About Market Risk |

We are a smaller reporting company as defined by Rule 12b-2 of the Exchange Act and are not required to provide the information required under this item.

| Item 4. | Controls and Procedures |

| (a) | Evaluation of Disclosure Controls and Procedures |