Attached files

| file | filename |

|---|---|

| EX-32 - EXHIBIT 32.2 - BOTS, Inc./PR | exhibit322.htm |

| EX-32 - EXHIBIT 32.1 - BOTS, Inc./PR | exhibit321.htm |

| EX-31 - EXHIBIT 31.2 - BOTS, Inc./PR | exhibit312.htm |

| EX-31 - EXHIBIT 31.1 - BOTS, Inc./PR | exhibit311.htm |

|

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549

FORM 10-Q

[√] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE QUARTERLY PERIOD ENDED JULY 31, 2016

Commission file number: 333-175941 MCIG, INC. (Exact name of registrant as specified in its charter)

| |

|

NEVADA |

27-4439285 |

|

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

|

|

|

|

2831 St. Rose Parkway, Suite 200, Henderson, NV |

89052 |

|

(Address of principal executive offices) |

(Zip Code) |

|

Registrant’s telephone number, including area code |

570-778-6459 |

|

| |

|

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. [√] Yes [ ] No | |

|

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). [√] Yes [ ] No | |

|

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. | |

|

Large accelerated filer [ ] |

Accelerated filer [ ] |

|

Non-accelerated filer [ ] |

Smaller reporting company [√] |

|

(Do not check if smaller reporting company) |

|

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). | |

|

Yes [ ] No [√] | |

|

As of September 28, 2016, the Company had 331,655,154 shares of common stock, $0.0001 par value outstanding. | |

|

Transitional Small Business Disclosure Format Yes [ ] No [√] | |

|

| |

|

mCig, Inc.

|

|

|

TABLE OF CONTENTS

|

|

|

|

|

|

PART I. FINANCIAL INFORMATION |

|

|

Item 1. Financial Statements |

3 |

|

Condensed Consolidated Balance Sheets as of July 31, 2016 and April 30, 2016 (unaudited) |

4 |

|

Condensed Consolidated Statements of Operations for the three months ended July 31, 2016 and 2015 (unaudited) |

5 |

|

Condensed Consolidated Statements of Cash Flows for the three months ended July 31, 2016 and 2015 (unaudited) |

6 |

|

Notes to Condensed Consolidated Financial Statements (unaudited) |

7 |

|

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations |

14 |

|

Item 3. Quantitative and Qualitative Disclosures about Market Risk |

18 |

|

Item 4. Controls and Procedures |

18 |

|

PART II. OTHER INFORMATION |

|

|

Item 1. Legal Proceedings |

19 |

|

Item 1A. Risk Factors |

19 |

|

Item 2. Unregistered Sales of Equity Securities and Use of Proceeds |

19 |

|

Item 3. Defaults Upon Senior Securities |

19 |

|

Item 4. Mine Safety Disclosures |

19 |

|

Item 5. Other Information |

19 |

|

Item 6. Exhibits |

20 |

|

SIGNATURES |

21 |

|

2 | |

PART I – FINANCIAL INFORMATIONItem 1. Financial Statements

Interim Condensed Financial Statements and Notes to Interim Financial Statements

General

The accompanying unaudited condensed consolidated interim financial statements have been prepared in accordance with the instructions to Form 10-Q. Therefore, they do not include all information and footnotes necessary for a complete presentation of financial position, results of operations, cash flows, and stockholders’ equity in conformity with generally accepted accounting principles. Except as disclosed herein, there has been no material change in the information disclosed in the notes to the financial statements included in the Company’s annual report on Form 10-K for the year ended April 30, 2016. In the opinion of management, all adjustments considered necessary for a fair presentation of the results of operations and financial position have been included and all such adjustments are of a normal recurring nature. Operating results for the three months ended July 31, 2016 are not necessarily indicative of the results that can be expected for the year ending April 30, 2017.

3 |

|

mCig, Inc. | |||||

|

and SUBSIDIARIES | |||||

|

Consolidated Balance Sheets | |||||

|

(unaudited) | |||||

|

July 31, |

April 30, | ||||

|

2016 |

2016 | ||||

|

ASSETS | |||||

|

Current Assets |

|

|

| ||

|

Cash and cash equivalents |

$ 224,435 |

$ 80,542 | |||

|

|

Accounts Receivable, Net |

7,880 |

|

6,120 | |

|

Inventory |

25,325 |

7,268 | |||

|

|

Prepaid Expenses |

26,200 |

|

- | |

|

Total Current Assets |

283,840 |

93,930 | |||

|

Property, Plant and Equipment, Net |

6,251 |

|

1,334 | ||

|

Due From Related Party |

96,208 |

186,276 | |||

|

Cost Basis Investment |

67,500 |

|

67,500 | ||

|

Intangible Assets, Net |

270,183 |

488 | |||

|

Total Assets |

$ 723,982 |

|

$ 349,528 | ||

|

LIABILITIES AND STOCKHOLDERS' EQUITY | |||||

|

Current Liabilities |

|

|

| ||

|

|

Accounts Payable and Accrued Expenses |

$ 60,205 |

|

$ 45,385 | |

|

Note Payable, Current Portion |

25,000 |

- | |||

|

|

Due to Shareholder |

26,373 |

|

24,173 | |

|

Deferred Revenue |

85,702 |

6,502 | |||

|

|

|

Total Current Liabilities |

197,280 |

|

76,060 |

|

Noncurrent Liabilities |

|||||

|

|

|

Due to Related Party |

8,170 |

|

- |

|

Total Liabilities |

205,450 |

76,060 | |||

|

Stockholders' Equity |

|||||

|

Preferred stock, $0.0001 par value; 50,000,000 shares authorized; |

2,200 |

2,300 | |||

|

22,000,000 and 23,000,000 shares issued and outstanding, as | |||||

|

of July 31, 2016 and April 30, 2016, respectively. |

|||||

|

|

Common Stock, $0.0001 par value, voting; 560,000,000 shares |

32,858 |

|

30,631 | |

|

|

|

authorized; 328,587,913 and 306,314,216 shares issued, and |

|||

|

|

|

outstanding, as of July 31, 2016 and April 30, 2016, respectively. |

|||

|

Additional Paid In Capital |

7,330,308 |

6,916,635 | |||

|

|

Accumulated Deficit |

(6,820,535) |

|

(6,658,558) | |

|

Total Stockholders' Equity |

544,831 |

291,008 | |||

|

|

Non-Controlling Interest |

(26,299) |

|

(17,540) | |

|

Total Equity |

518,532 |

273,468 | |||

|

|

|

Total Liabilities and Stockholders' Equity |

$ 723,982 |

|

$ 349,528 |

|

See accompanying notes to unaudited consolidated financial statements.

4 | |||||

|

mCig, Inc. | |||||||

|

and SUBSIDIARIES | |||||||

|

Consolidated Statements of Operations | |||||||

|

(unaudited) | |||||||

|

Three Months Ended July 31, | |||||||

|

2016 |

2015 | ||||||

|

Sales |

|

|

$ 254,702 |

|

$ 369,093 | ||

|

Total Cost of Sales |

181,401 |

242,129 | |||||

|

Gross Profit |

|

|

73,301 |

|

126,964 | ||

|

Operating Expenses: |

|

|

|

|

| ||

|

Selling, general, and administrative |

27,522 |

139,112 | |||||

|

Professional Fees |

|

|

13,100 |

|

3,681 | ||

|

Stock based compensation |

168,300 |

645,229 | |||||

|

Consultant Fees |

|

|

28,155 |

|

- | ||

|

Amortization and Depreciation |

8,168 |

2,070 | |||||

|

Total Operating Expenses |

|

|

245,245 |

|

790,092 | ||

|

Loss From Operations |

(171,944) |

(663,128) | |||||

|

Other Income (Expense) |

|

|

1,208 |

|

- | ||

|

Net Loss Before Non-Controlling Interest |

(170,736) |

(663,128) | |||||

|

Loss Attributable to Non-Controlling Interest |

|

|

(8,759) |

|

- | ||

|

Net Loss Attributable to Controlling Interest |

$ (161,977) |

$ (663,128) | |||||

|

Basic and Diluted (Loss) Per Share: |

|

|

|

|

| ||

|

Income(Loss) per share from Continuing Operations |

$ (0.00) |

$ (0.00) | |||||

|

Income(Loss) Per Share |

|

|

$ (0.00) |

|

$ (0.00) | ||

|

Weighted Average Shares Outstanding - Basic and Diluted |

320,316,968 |

280,311,306 | |||||

|

See accompanying notes to unaudited consolidated financial statements.

5 | |||||||

|

mCig, Inc. | ||||||

|

and SUBSIDIARIES | ||||||

|

Statements of Cash Flows | ||||||

|

(unaudited) | ||||||

|

For the Three Months Ended July 31, | ||||||

|

2016 |

2015 | |||||

|

Cash Flows From Operating Activities: |

|

|

| |||

|

Net (Loss) |

$ (170,736) |

$ (663,148) | ||||

|

Adjustments to Reconcile Net Loss to Net |

|

|

| |||

|

|

Cash Provided By (Used In) Operating Activities: |

|

|

| ||

|

Depreciation and Amortization |

8,168 |

2,070 | ||||

|

|

|

Common Stock Issued for Services |

168,300 |

|

340,501 | |

|

Loss on Impairment on Investments |

- |

304,728 | ||||

|

|

Decrease (Increase) in: |

|

|

| ||

|

Accounts Receivable, Net |

8,758 |

22,141 | ||||

|

|

|

Receivable Other |

- |

|

10,000 | |

|

Inventories |

8,550 |

(11,002) | ||||

|

|

|

Prepaid Expenses and Other Current Assets |

2,100 |

|

3,091 | |

|

Accounts Payable, Accrued Expenses and Taxes Payable |

1,898 |

(2,998) | ||||

|

Deferred Revenue |

47,326 |

6,053 | ||||

|

|

Total Adjustment to reconcile Net Income to Net Cash |

245,100 |

|

674,584 | ||

|

Net Cash Provided By Operating Activities |

74,364 |

11,436 | ||||

|

Cash Flows From Investing Activities: |

|

|

| |||

|

Increase (Decrease) in: |

||||||

|

|

|

Net cash received from acquisition |

44,280 |

|

- | |

|

Acquisition of property, plant and equipment |

(5,066) |

- | ||||

|

|

|

|

Net Cash Provided By investing activities |

39,214 |

|

- |

|

Cash Flows From Financing Activities: |

||||||

|

|

|

Borrowing from related party |

8,370 |

|

- | |

|

Advances from Related Party |

- |

8,500 | ||||

|

|

|

Repayments to Related Party |

- |

|

(6,201) | |

|

|

|

Repayment from Due to Related Party, net |

21,945 |

|

- | |

|

Proceeds from Related Party |

- |

2,850 | ||||

|

|

|

|

Net Cash Provided By Financing Activities |

30,315 |

|

5,149 |

|

Net Change in Cash |

143,893 |

16,585 | ||||

|

Cash at Beginning of Year |

80,542 |

|

102,691 | |||

|

Cash at End of Period |

$ 224,435 |

$ 119,276 | ||||

|

Supplemental Disclosure of Cash Flows Information: |

|

|

| |||

|

Cash paid for interest |

$ - |

$ - | ||||

|

|

|

Cash paid for income taxes |

$ - |

|

$ - | |

|

Non-cash Investing and Financing Activities: |

||||||

|

Prepaid expenses financed by notes payable |

$ 25,000 |

|

$ - | |||

|

Common stock issued for domain names |

$ 247,500 |

$ - | ||||

|

Conversion of preferred stock to common stock |

$ 1,000 |

|

$ - | |||

|

Inventory received for forgiveness of debt |

$ - |

$ 2,460 | ||||

|

See accompanying notes to unaudited consolidated financial statements.

6 | ||||||

|

MCIG, INC. Notes to Condensed Financial Statements (Unaudited)

Note 1 – Organization and Basis of Presentation

The accompanying unaudited financial statements of mCig, Inc., (the “Company”, “we”, “our”), have been prepared in accordance with accounting principles generally accepted in the United States of America and the rules of the Securities and Exchange Commission (“SEC”).

The Company prepares its condensed financial statements in accordance with accounting principles generally accepted in the United States of America. The accompanying interim unaudited condensed financial statements have been prepared in accordance with generally accepted accounting principles for interim financial information in accordance with the instructions to Form 10-Q and Article 8 of Regulation S-X. In management’s opinion, all adjustments (consisting of normal recurring adjustments) considered necessary for a fair presentation have been included.

Operating results for the three months ended July 31, 2016 are not necessarily indicative of the results that may be expected for the year ending April 30, 2017. Notes to the unaudited interim condensed financial statements that would substantially duplicate the disclosures contained in the audited condensed financial statements for the year ended April 30, 2016 have been omitted; this report should be read in conjunction with the audited condensed financial statements and the footnotes thereto for the fiscal year ended April 30, 2016 included within the Company’s Form 10-K as filed with the Securities and Exchange Commission.

Description of Business

The Company was incorporated in the State of Nevada on December 30, 2010 originally under the name Lifetech Industries, Inc. Effective August 2, 2013, the name was changed from "Lifetech Industries, Inc." to "mCig, Inc." reflecting the new business model.

All agreements related to the Lifetech business were terminated and closed as of April 30, 2014. It will not have any impact on the current and future operations because all of these agreements are related to the previous business directions of the Company.

Since 2013, the Company manufactures, markets, and distributes electronic cigarettes, vaporizers, and accessories under the mCig brand name in the United States. It offers electronic cigarettes and related products through its online store mcig.org, as well as through the company’s wholesale, distributor, and retail programs.

In FY 2016 the Company expanded its products and services to include construction management. The Company continues to look at strategic acquisitions and product and service developments for future growth.

Subsidiaries of the Company

The Company current business operations are conducted through three subsidiaries; Scalable Solutions, LLC, VitaCig, Inc., and mCig Internet Sales, Inc.

7 |

|

VitaCig, Inc. We distribute and wholesale the VitaCig product lines – affordable loose-leaf eCigs. Designed in the USA – with unique formulas, trade secrets, VitaCig provides a smoking experience by heating plant material, waxes, and oils delivering a smoother inhalation experience. On June 22, 2016 the Company acquired the business operations from VitaCig, Inc., in exchange for 172,500,000 shares of stock of VitaCig, Inc., owned by the Company and $68,123, which was a drawdown of the outstanding balance owed by VitaCig, Inc., to the Company. Scalable Solutions, LLC Scalable Solutions, LLC was organized by the Company on March 6, 2016, provides construction services in the cultivation and grow industry. Scalable began operations in December 2015, but was not officially incorporated until March 2016. The Company owns 80% of Scalable. Zoha Development, LLC maintains an option to acquire 40% of Scalable for a nominal fee. mCig Internet Sales, Inc. On June 1, 2016, the Company incorporated mCig Internet Sales, Inc., (“mCig Internet”) in order to consolidate all online retail sales from various websites and to provide streamlining of administrative and documentation services, consolidation of inventories, and support economy of scale. Note 2 – Summary of Significant Accounting Policies Principles of Consolidation The consolidated financial statements include the accounts of the Company, the wholly owned subsidiaries of mCig Internet Sales, Inc., and VitaCig, Inc., and the majority owned subsidiary of Scalable Solutions, LLC for the quarter ended July 31, 2016. Significant intercompany balances and transactions have been eliminated. Inventory Inventory consists of finished product, mCig products valued at the lower of cost or market valuation under the first-in, first-out method of costing. |

|

July 31, 2016 |

April 30, 2016 | |||||

|

Finished goods |

|

$ |

25,325 |

|

$ |

7,268 |

|

Total inventory |

|

$ |

25,325 |

|

$ |

7,268 |

|

Accounts Receivable The Company’s accounts receivable is primarily from its vendor tasked with accepting all credit card payments for purchases from its customers, and are held in escrow for potential chargebacks, and are reported at the amount due from the vendor. While the Company expects these receivables to be fully collectible it has created an allowance for doubtful accounts for the period, which is reported under Accounts Payable and Accrued Expenses. The Company did not report any accounts receivable from any of its wholesale customers.

Intangible Assets The Company’s intangible assets consist primarily of certain website development costs and domain urls, and are amortized over their useful life.

8 |

|

Basic and Diluted Net Loss Per Share The Company follows ASC Topic 260 to account for earnings per share. Basic earnings per share (“EPS”) calculations are determined by dividing net loss by the weighted average number of shares of common stock outstanding during the three months. Diluted earnings per share calculations are determined by dividing net income by the weighted average number of common shares and dilutive common share equivalents outstanding. During periods when common stock equivalents, if any, are anti-dilutive they are not considered in the computation.There is no potential dilutive security as of July 31, 2016 or April 30, 2016. Concentration of Credit Risk Financial instruments, which potentially subject us to concentrations of credit risk, consist principally of cash and trade receivables. Concentrations of credit risk with respect to trade receivables are limited due to the clients that comprise our customer base and their dispersion across different business and geographic areas. We estimate and maintain an allowance for potentially uncollectible accounts and such estimates have historically been within management's expectations.

We rely almost exclusively on one Chinese factory as our principle supplier, for the manufacturing of mCig’s. Therefore, our ability to maintain operations is dependent on this third-party manufacturer.

Our cash balances are maintained in accounts held by major banks and financial institutions located in the United States. The Company may occasionally maintain amounts on deposit with a financial institution that are in excess of the federally insured limit of $250,000. The risk is managed by maintaining all deposits in high quality financial institutions. The Company had no deposits in excess of federally insured limits at July 31, 2016 and April 30, 2016.

Cost-Basis Investments The Company’s non-marketable equity investment in Vapolution is recorded using the cost-basis method of accounting, and is classified within other long-term assets on the accompanying balance sheet as permitted by FASB ASC 325, “Cost Method Investments”. During the three months ended July 31, 2016 there were no impairment losses.

On September 30, 2015, the Company issued 2,500,000 shares of common stock valued at $67,500 for the second half of the Vapolution investment.

Equity-Basis Investments The Company accounts for its approximately 8% ownership of VitaCig, Inc., (Nevada) as an equity-basis investment. As of July 31, 2016 and April 30, 2016, there is no net book value of the ownership of VitaCig, as the pro-rata value after the Spin-off and the impairment of the investment in VitaCig.

On June 22, 2016 the Company reduced its ownership of VitaCig, Inc., to 57,500,000 through a Separation and Transfer Agreement where the Company acquired the business operations of VitaCig in exchange for selling back to the treasury of VitaCig, Inc., (Nevada) 172,500,000. As a condition to the action, the Company’s shares are non-dilutive for a period of 12 months.

Warranties Warranty reserves include management’s best estimate of the projected costs to repair or to replace any items under warranty, based on actual warranty experience as it becomes available and other known factors that may impact the Company’s evaluation of historical data. Management reviews mCig’s reserves at least quarterly to ensure that its accruals are adequate in meeting expected future warranty obligations, and the Company will adjust its estimates as needed. Initial warranty data can be limited early in the launch of a product and accordingly, the adjustments that are recorded may be material.. As a result, the products that can be returned as a warranty replacement are extremely limited. As a result, due to the Company’s warranty policy, the Company did not have any significant warranty expenses to report for the quarter ended July 31, 2016. Based on these actual expenses, the warranty reserve, as estimated by management as of July 31, 2016 and April 30, 2016 were at $0. Any adjustments to warranty reserves are to be recorded in cost of sales.

Segment Information In accordance with the provisions of SFAS No. 131, Disclosures about Segments of an Enterprise and Related Information, the Company is required to report financial and descriptive information about its reportable operating segments. The Company identifies its operating segments as divisions based on how management internally evaluates separate financial information, business activities and management responsibility. In addition to the corporate segment, the Company segments and the subsidiaries associated with each segment are as follows: |

|

Segment |

Subsidiary |

|

Construction |

Scalable Solutions, Inc. |

|

Internet Sales |

mCig Internet Sales, Inc. |

|

Wholesale |

VitaCig, Inc. |

| 9 |

|

Note 3. Going Concern

The Company's financial statements are prepared using generally accepted accounting principles, which contemplate the realization of assets and liquidation of liabilities in the normal course of business. Because the business is new and has a limited history and relatively few sales, no certainty of continuation can be stated. The accompanying financial statements for the three months ended July 31, 2016 and 2015 have been prepared assuming that the Company will continue as a going concern, which contemplates the realization of assets and satisfaction of liabilities in the normal course of business.

The Company has suffered losses from operations and has an accumulated deficit, which raise substantial doubt about its ability to continue as a going concern.

Management is taking steps to raise additional funds to address its operating and financial cash requirements to continue operations in the next twelve months. Management has devoted a significant amount of time in the raising of capital from additional debt and equity financing. However, the Company’s ability to continue as a going concern is dependent upon raising additional funds through debt and equity financing and generating revenue. There are no assurances the Company will receive the necessary funding or generate revenue necessary to fund operations. The financial statements contain no adjustments for the outcome of this uncertainty.

Note 4. Notes Payable

On June 15, 2016, the Company issued a convertible promissory note in the amount of $25,000 for future legal work. The note is due on June 14, 2017 and bears interest at 10% per annum. The loan becomes convertible 180 days after date of the note. The loan can then be converted into shares of the Company’s common stock at a rate of 80% multiplied by the market price, which is the average of the closing price on the preceding five (5) trading days. As of July 31, 2016, the note has not become convertible.

Note 5. Property, Plant and Equipment

During the three months ended July 31, 2016 the company acquired equipment for its Rollies operation, a service whereby the company provides onsite packing services at dispensaries where marijuana cigarettes are sold. The cost of the machine includes actual cost, transportation, travel for inspection and testing. The following is a detail of equipment at July 31, 2016 and April 30, 2016: |

|

July 31, 2016 |

April 30, 2016 | |||||

|

Office Furniture |

|

$ |

1,792 |

$ |

1,792 | |

|

Rollies Machine |

|

5,066 |

- | |||

|

Depreciation |

|

607 |

458 | |||

|

Total Property and Equipment |

|

$ |

6,251 |

$ |

1,334 | |

|

Note 6. Intangible Assets:

Intangible assets, net consisted of the following: |

|

July 31, 2016 |

April 30, 2016 | |||||

|

Website Designs |

|

$ |

22,591 |

|

$ |

22,591 |

|

Domains |

|

247,500 |

|

- | ||

|

VitaCig Intangibles |

|

|

30,124 |

|

|

- |

|

Total Intangible Assets |

|

|

300,215 |

|

|

22,591 |

|

Less: Amortization |

|

(30,032) |

|

(22,103) | ||

|

Current Intangible Assets |

|

$ |

270,183 |

|

$ |

488 |

|

10 |

|

Note 7. Business Segments

This summary reflects the Company's current segments, as described below.

Corporate

The parent company provides overall management and corporate reporting functions for the entire organization.

Construction

We develop, design, engineer, and construct modular buildings with unique and proprietary elements that assist cannabis growers in the market. Each modular building is uniquely designed for each customer. The Company began construction on its first contract in April 2016. We will continue to expand our offering in the construction and modular facilities in multiple facets as the industry continues to seek better and improved ways of production. Internet Sales

The Company tracks all retail sales through the Internet through the consolidation of all online retail sales from various websites. It provides streamlining of administrative and documentation services, consolidation of inventories, and supports economy of scale.

Wholesale The wholesale division works with mass distribution channels in eCig, wholesale CBD, marijuana cigarettes (Rollies), and all other operations not directly classified in the other reportable segments. Information concerning the revenues and operating income (loss) for the three months ended July 31, 2016 and 2015, and the identifiable assets for the segments in which the Company operates are shown in the following table: |

|

For the Three Months Ended July 31, 2016 |

|

|

Construction |

|

Internet Sales |

|

Wholesale |

|

Corporate |

|

Total |

|

Revenue |

$ 62,268 |

$ 92,462 |

$ 99,972 |

$ - |

$ 257,802 | ||||||

|

Segment Income (Loss) from Operations |

|

|

(43,797) |

|

16,055 |

|

14,782 |

|

(152,984) |

|

(165,944) |

|

Total Assets |

78,455 |

400,655 |

5,107 |

239,765 |

723,982 | ||||||

|

Capital Expenditures |

|

|

- |

|

247,500 |

|

5,066 |

|

(44,280) |

|

208,286 |

|

Depreciation and Amortization |

- |

7,500 |

90 |

578 |

8,168 | ||||||

|

For the Three Months Ended July 31, 2015 |

|

|

Construction |

|

Internet Sales |

|

Wholesale |

|

Corporate |

|

Total |

|

Revenue |

$ - |

$ 144,347 |

$ 224,746 |

$ - |

$ 369,093 | ||||||

|

Segment Loss from Operations |

|

|

- |

|

50,194 |

|

50,661 |

|

(763,983) |

|

(663,128) |

|

Total Assets |

- |

- |

- |

384,790 |

384,790 | ||||||

|

Capital Expenditures |

|

|

- |

|

- |

|

- |

|

- |

|

- |

|

Depreciation and Amortization |

- |

- |

- |

2,070 |

2,070 |

|

Note 8. Acquisition of VitaCig Business On June 22, 2016, the Company and VitaCig, Inc., entered into a Separation and Share Transfer Agreement whereby VitaCig transferred the assets and operations of the business of VitaCig, Inc., to Company in exchange for the return of 172,500,000 shares of VitaCig Common Stock to the treasury of VitaCig, Inc., and for a reduction of the amount owed to the Company in excess of $95,000. The purchase price of VitaCig was $68,123. The purchase price was derived from the amount of the reduction of the reduction in Due from VitaCig in excess of $95,000. In addition, the company returned 172,500,000 shares of VitaCig Common Stock which had no recorded net present value. The following table summarizes the estimated fair values of the assets acquired and the liabilities assumed, at the date of acquisition:11 |

|

Cash |

$ |

44,280 | |

|

Accounts Receivable |

|

|

10,517 |

|

Prepaid assets |

|

|

3,300 |

|

Inventory |

26,607 | ||

|

Intangible assets (domain, website, trademark, trade secrets) |

30,216 | ||

|

Total assets acquired |

|

114,920 | |

|

Current Liabilities |

12,923 | ||

|

Deferred Revenue |

31,874 | ||

|

Due to Related Party |

|

2,000 | |

|

Total liabilities assumed |

|

46,797 | |

|

Net assets acquired |

$ |

68,123 |

|

In accordance with ASC 805-10-50, the Company is providing the following unaudited pro-forma to present a summary of the combined results of the Company’s consolidated operations with the acquisition as if the acquisition had been completed as of the beginning of the reporting period. |

|

For three months ending July 31, | ||||||

|

CONSOLIDATED STATEMENTS of OPERATIONS: |

2016 |

2015 | ||||

|

Sales |

$ |

298,282 |

$ |

436,129 | ||

|

Cost of Sales |

|

215,097 |

|

286,615 | ||

|

Gross Profit |

83,185 |

149,514 | ||||

|

Operating Expenses |

|

243,119 |

|

832,174 | ||

|

(Loss) from Operations |

(159,934) |

(682,660) | ||||

|

Other Income / (Expense) |

1,208 |

- | ||||

|

Net Loss Before Non-Controlling Interest |

$ |

(158,726) |

$ |

(682,660) | ||

|

Loss Attributable to Non-Controlling Interest |

(8,759) |

- | ||||

|

Net Loss Attributable to Controlling Interest |

$ |

(149,967) |

$ |

(682,660) | ||

|

Note 9. Related Parties and Related Party Transactions

On May 1, 2016 the Company entered into a Line of Credit Agreement for up to $100,000 with Paul Rosenberg, the Chairman and CEO. The Company will utilize the Line of Credit as needed for day-to-day operations. During this quarter the company utilized $200 under the Line of Credit Agreement and $2,000 was assigned to the Line of Credit from the assumed liability of the VitaCig acquisition to Paul Rosenberg (see Note 8). During the period ended July 31, 2016, the Company had various transactions in which Paul Rosenberg, the Company's CEO and Chairman of the Board, personally paid expenses on behalf of the Company. As of July 31, 2016 and April 30, 2016, the Company borrowed $26,373 and $24,173, respectively, from Paul Rosenberg.

On May 2, 2016 the Company sold to Paul Rosenberg the bad inventory from the past several years that was written off the previous years at cost. Mr. Rosenberg paid for the bad inventory in cash. The Company had stored $20,730 worth of bad product it needed to destroy, which was not accounted for on its books and records. The Company booked the transaction as revenue.

On June 3, 2016 the Company entered into a Convertible Promissory Note with VitaCig, Inc., (VTCQ) in the amount of $95,000 which was accounted for by the reduction of the balance Due from Related Party. The terms of the Convertible Promissory Note include 8% annual interest, and a 25% reduction to the lowest conversion price of the preceding five days before election to convert.

Between May 1, 2016 and June 22, 2016, the Company received $21,945 which was paid towards the balance Due from Related Party leaving a balance owed of $68,123 on June 22, 2016, the date of acquisition. The Company purchased the VTCQ business for $68,123 on June 22, 2016 by writing off the remaining balance (excluding the Convertible Promissory Note of $95,000).

During the three months ended July 31, 2016, Scalable Solutions, LLC (Scalable) contracted Zoha Development, LLC (Zoha) to provide services to the construction division and paid Zoha $5,655 and has an outstanding balance owed of $10,000 at the end of the fiscal period ending July 31, 2016. The president of Scalable is a managing member of Zoha.

12 |

|

On June 7, 2016 the Company issued 2,500,000 shares of common stock ($75,000 in fair market value) to Paul Rosenberg for the acquisition of the domain url www.cbd.biz. See Note 5.

On June 8, 2016 Paul Rosenberg, the Company’s CEO and Chairman of the Board, converted 600,000 shares of Series A Preferred into 6,000,000 shares of common stock.

On June 22, 2016 the Company acquired the business of VitaCig, Inc., (VTCQ). See Note 7.

Note 10. Stockholders’ Equity Common Stock On June 7, 2016, the Company issued 2,941,176 shares of common stock for services and 7,500,000 shares of common stock in exchange for the purchase of three domain urls. The common stock issued for services was recorded as Stock Based Compensation in the amount of $98,000. The common stock issued for the purchase of the domain urls was recorded as an Intangible Asset in the amount of $247,500.

On June 30, 2016, the Company issued 865,854 shares of common stock for services and was recorded as Stock Based Compensation in the amount of $35,500.

On July 31, 2016, the Company issued 966,667 shares of common stock for services and was recorded as Stock Based Compensation in the amount of $34,800.

Preferred Stock The Company has authorized 50,000,000 shares of preferred stock, at $0.0001 par value and 22,000,000 and 23,000,000 are issued and outstanding as of July 31, 2016 and April 30, 2016, respectively. Each share of the Preferred Stock has 10 votes on all matters presented to be voted by the holders of the Company’s common stock. All of the 23,000,000 shares of issued and outstanding preferred stock were granted to the Company’s Chief Executive Officer on September 23, 2013, which was valued at $2,300, the price of the common stock of $0.0001 exchanged in the transaction. The Company’s CEO currently owns 21,000,000 shares of Series A Preferred on July 31, 2016. On May 15, 2016, a shareholder elected to convert 400,000 shares of Series A Preferred Stock into 4,000,000 shares of common stock. On June 8, 2016, Paul Rosenberg, the Company’s CEO and Chairman of the Board, converted 600,000 shares of Series A Preferred Stock into 6,000,000 shares of common stock. Note 11. Subsequent Events

On September 1, 2016 the Company entered into an employment agreement with Michael Hawkins, the Chief Financial Officer and an employment agreement with Paul Rosenberg, the Chief Executive Officer of the Company (“employees”). Mr. Hawkins was the Interim Chief Financial Officer which agreement was scheduled to expire on September 6, 2016. Mr. Rosenberg has been the CEO since inception and served without an agreement. The terms of the Agreement are the same. The agreements call for $156,000 per year base salary with a three year term. Only $3,000 per month guaranteed to be paid in cash, while the remainder ($10,000 per month) is booked as a note due, which may be converted into shares of the company at the current price on April 30, of each year for all income earned. The initial year’s conversion option was accrued upon entering into the agreement. The employees earn annual bonuses based upon gross sales, net profits, and annual increases in sales and profits. The Company and employees may elect to convert a portion of this salary into equity of the company based upon the fair market value on April 30, of each year for the bonuses earned. In addition, each employee was issued a seven year warrant to acquire four percent (4%) of the Company Stock, based upon the issued and outstanding, fully diluted, as of September 1, 2016, at the fair market value on September 1, 2016 with 25% vested immediately and 25% on each subsequent year anniversary of employment. On August 15, 2016 the Company entered into an Asset Purchase Agreement with Gray Matter, LLC. The Agreement was consummated on September 1, 2016. The Company acquired all inventory and intellectual property in exchange for $35,000 in common stock. As a condition to this acquisition, the Company entered into a Consulting Agreement with John James Southard who became the President, mCig CBD Division. On August 31, 2016, the Company issued 1,067,241 shares of common stock for services and was recorded as Stock Based Compensation in the amount of $30,950. On September 1, 2016, the Company issued 2,000,000 shares of common stock for services and was recorded as Stock Based Compensation in the amount of $58,000. 13 |

|

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion should be read in conjunction with our condensed consolidated financial statements and related notes thereto included elsewhere in this Quarterly Report on Form 10-Q and the consolidated financial statements and related notes thereto in our Annual Report on Form 10-K for the year ended April 30, 2016.

Certain statements in this section contain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. All statements contained in this report and not clearly historical in nature are forward-looking, and the words “may,” “will,” “should,” “could,” “would,” “expects,” “plans,” “anticipates,” “believes,” “estimates,” “projects,” “predicts,” “intends,” “potential,” and similar expressions (as well as other words or expressions referencing future events, conditions or circumstances) generally are intended to identify forward-looking statements. Any statements in this report that are not historical facts are forward-looking statements. Actual results may differ materially from those discussed from time to time in the Company's Securities and Exchange Commission filings. The Company undertakes no obligation to update or revise any forward-looking statement for events or circumstances after the date on which such statement is made except as required by law.

Overview

mCig, Inc. (mCig) was incorporated in the State of Nevada on December 30, 2010 originally under the name Lifetech Industries, Inc. Effective August 2, 2013, the name was changed from "Lifetech Industries, Inc." to "mCig, Inc." reflecting the new business model. Since October 2013, we have positioned ourselves as a company focused on two long-term secular trends:

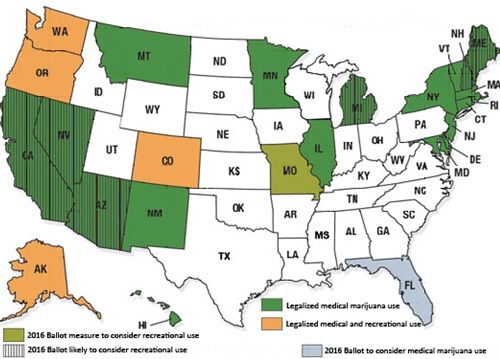

(1) the decriminalization and legalization of marijuana for medicinal or recreational purposes - legalizing medicinal and recreational marijuana usage is steadily on the rise not only domestically but also internationally. Marijuana has been decriminalized in over twenty countries, in over five continents. The following chart was created by the National Organization for the Reform of Marijuana Laws and depicts the current status (2016) of each state in the decriminalization and legalization of marijuana. |

|

Management believes that in 2016 it is very likely that many more states, will legalize the use and sale of recreational marijuana the way Washington, Oregon, Alaska and Colorado have.

(2) The adoption of electronic vaporizing cigarettes (commonly known as “eCigs”), as smokers move away from traditional cigarettes onto e-cigarettes. Smoking tobacco causes numerous health problems, including disease and death. Smoking becomes very addicting quickly, and the most difficult part is cessation. The Company contends that e-cigarettes offer a safer and healthier alternative to traditional tobacco cigarettes. E-cigarettes operate by heating a mixture of liquid nicotine and flavoring, which is then inhaled and exhaled in the same manner as a cigarette. However, e-cigarettes do not contain any tobacco or other dangerous additives. Scientific research has shown that the leading cause of cancer in smokers comes from the carcinogens in tobacco. As the movement towards personal health grows, smokers are trying to quit their harmful habits. 14 |

|

Since 2013, the Company manufactures, markets, and distributes electronic cigarettes, vaporizers, and accessories under the mCig brand name in the United States. It offers electronic cigarettes and related products through its online store mcig.org, as well as through the company’s wholesale, distributor, and retail programs.

Critical Accounting Policies and Estimates

Our discussion and analysis of our financial condition and results of operations are based upon our financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States. The preparation of these financial statements requires us to make estimates and judgments that affect the reported amounts of assets, liabilities, revenues and expenses. On an ongoing basis, we evaluate our estimates, including those related to uncollectible receivables, inventory valuation, deferred compensation and contingencies.

We base our estimates on historical performance and on various other assumptions that we believe to be reasonable under the circumstances. These estimates allow us to make judgments about the carrying values of assets and liabilities that are not readily apparent from other sources.

We believe the following accounting policies are our critical accounting policies because they are important to the portrayal of our financial condition and results of operations and they require critical management judgments and estimates about matters that may be uncertain. If actual results or events differ materially from those contemplated by us in making these estimates, our reported financial condition and results of operations for future periods could be materially affected.

Revenue Recognition

Our revenue recognition policy is in accordance with generally accepted accounting principles, which requires the recognition of sales when there is evidence of a sales agreement, the delivery of goods has occurred, the sales price is fixed or determined and the collectability of revenue is reasonably assured.

The Company recognizes revenue for sales online either direct to consumer or through our Wholesaler, Distributor, Reseller (WDR) program. For online sales, revenue is recognized by the Company at the time of order fulfillment. Since mCig collects payment for each online order at the time of sale, the point of shipping revenue recognition method ensures that the Company recognizes the revenue collected within 24-48 hours after the order is received and the funds are collected.

Amounts billed or collected in excess of revenue recognized are recorded as deferred revenue.

Our operating results for the three months ended July 31, 2016 and 2015 are summarized as follows: |

|

Fiscal Quarter Ended April 30, | |||||||

|

2016 |

2015 | ||||||

|

Sales |

$ 254,702 |

$ 369,093 | |||||

|

Cost of Sales |

181,401 |

242,149 | |||||

|

Gross Profit |

73,301 |

126,944 | |||||

|

Total Operating Expenses |

245,245 |

790,092 | |||||

|

Other Income |

|

|

1,208 |

|

- | ||

|

Net Loss from Continuing Operations |

(170,736) |

(663,148) | |||||

| 15 |

|

Results of Operations

Revenue

Our revenue from operations for the three months ended July 31, 2016 was $254,702 compared to $369,093, a decrease of $114,391 or approximately 31%, from the three months ended July 31, 2015. This decrease is primarily a result of management’s decision to diversify, the inability to ship products before the end of the quarter, and the delays experienced in obtaining the required construction licenses needed to proceed.

Cost of Goods Sold

Our cost of goods sold for the three months ended July 31, 2016 was $181,401 compared to $242,149 for the three months ended July 31, 2015. The decrease is primarily due to the decrease in sales.

Gross Profit

Our gross profit for the three months ended July 31, 2016 was $73,301 compared to $126,964 for the three months ended July 31, 2015. The gross profit of $73,301 for the three months ended July 31, 2016 represents approximately 29% as a percentage of total revenue. The gross profit of $126,944 for the three months ended July 31, 2015 represents approximately 34% as a percentage of total revenue. This decrease in the gross profit is primarily attributed to the increase in wholesales and the inclusion of construction projects with flat rate cost+ contracts.

Operating Expenses

Our operating expenses decreased by $544,847 to $245,245 for the three months ended July 31, 2016, from $790,092 for the three months ended July 31, 2015.

The decrease was primarily due to the decrease in stock based compensation of $476,929, selling, general and administrative expenses of $111,560, and amortization and depreciation of $6,098, offset by an increase in consulting of $28,155 and professional fees of $9,419.

Our total operating expenses for the three months ended July 31, 2016 of $245,245 consisted of $27,522 of selling, general and administrative expenses, $13,100 of professional fees, consulting expense of $28,155, stock based compensation of $168,300, and $8,168 of amortization and depreciation expenses. Our general and administrative expenses consist of bank charges, telephone expenses, meals and entertainments, computer and internet expenses, postage and delivery, office supplies and other expenses.

Net Loss

Our net loss decreased by $492,412 to $170,736 for the three months ended July 31, 2016 from $663,148 for the three months ending July 31, 2015. The decrease in net loss compared to the prior period is primarily a result of the decrease in operating expenses of $544,847 and gross profit of $53,643.

Liquidity and Capital Resources

Introduction

During the three months ended July 31, 2016 we provided $74,364 in operating cash flows. Our cash on hand as of July 31, 2016 was $224,435.

Cash Requirements

We had cash available of $224,435 as of July 31, 2016. Based on our revenues, cash on hand and current monthly burn rate, around break-even, we believe that our operations are sufficient to fund operations through April 2017.

Sources and Uses of Cash

Operations

We had net cash provided by operating activities of $74,364 for the three months ended July 31, 2016, as compared to cash provided of $11,436 for the three months ended July 31, 2015.

16 |

|

Net cash provided by operations consisted primarily of the net loss of $170,736 offset by non-cash expenses of $176,468 consisting of depreciation and amortization of intangible assets of $8,168 and $168,300 in common stock issued for services. Additionally, changes in assets and liabilities consisted of increases of $8,758 in accounts receivable, prepaid expenses of $2,100, inventory of $8,550, accounts payable of $1,898, and deferred revenue of $47,326.

Investments

We had net cash provided in investing activities of $39,214 and $0 for the three months ended July 31, 2016 and July 31, 2015, respectively. Our investing activities consisted primarily of $44,280 in net cash received from acquisition, and the purchase of the Rollies Machine for $5,066.

Financing

We had net cash provided in financing activities of $30,315 for the three months ended July 31, 2016, as compared to net cash provided of $5,149 for the three months ended July 31, 2015. Our financing activities consisted borrowing from a related party of $8,370, repayment of advances to a related arty of $23,153, offset by interest due on note receivable of $1,208.

Off-Balance Sheet Arrangements

We have no off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on our financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources that we consider material.

Going Concern

Our financial statements are prepared using generally accepted accounting principles, which contemplate the realization of assets and liquidation of liabilities in the normal course of business. Because the business is relatively new and has a short history and relatively few sales, no certainty of continuation can be stated. The accompanying financial statements for the three months ended July 31, 2016 have been prepared assuming that we will continue as a going concern, which contemplates the realization of assets and satisfaction of liabilities in the normal course of business.

The Company has suffered losses from operations and has an accumulated deficit, which raises substantial doubt about its ability to continue as a going concern.

17 |

|

Item 3. Quantitative and Qualitative Disclosures about Market Risk

We are a smaller reporting company and therefore, we are not required to provide information required by this Item of Form 10-Q.

Item 4. Controls and Procedures Evaluation of Disclosure Controls and Procedures

Disclosure controls and procedures (as defined in Rules 13a-15(e) and 15d-15(e) under the Exchange Act) are designed to ensure that information required to be disclosed in reports filed or submitted under the Exchange Act is recorded, processed, summarized and reported within the time periods specified in SEC rules and forms. Disclosure controls and procedures are also designed to ensure that such information is accumulated and communicated to management, including the principal executive officer and principal financial officer, to allow timely decisions regarding required disclosures.

We carried out an evaluation, under the supervision and with the participation of management, including our principal executive officer and principal financial officer, of the effectiveness of the design and operation of our disclosure controls and procedures as of July 31, 2016. In designing and evaluating the disclosure controls and procedures, management recognizes that there are inherent limitations to the effectiveness of any system of disclosure controls and procedures, including the possibility of human error and the circumvention or overriding of the controls and procedures.

Accordingly, even effective disclosure controls and procedures can only provide reasonable assurance of achieving their desired control objectives. Additionally, in evaluating and implementing possible controls and procedures, management is required to apply its reasonable judgment. Based on the evaluation described above, our principal executive officer and principal financial officer concluded that our disclosure controls and procedures were not effective as of the end of the period covered by this report because we did not document our Sarbanes-Oxley Act Section 404 internal controls and procedures.

As funds become available to us, we expect to implement additional measures to improve disclosure controls and procedures such as implementing and documenting our internal controls procedures.

Changes in internal controls over financial reporting

There have been no changes in our internal control over financial reporting during the quarter ended July 31, 2016 that has materially affected, or is reasonably likely to materially affect, our internal control over financial reporting.

18 |

|

Limitations on the Effectiveness of Controls

A control system, no matter how well designed and operated, can provide only reasonable, not absolute, assurance that the control system’s objectives will be met. The Company’s management, including its Principal Executive Officer and its Principal Financial Officer, do not expect that the Company’s disclosure controls will prevent or detect all errors and all fraud. Further, the design of a control system must reflect the fact that there are resource constraints, and the benefits of controls must be considered relative to their costs. Because of the inherent limitations in all control systems, no evaluation of controls can provide absolute assurance that all control issues and instances of fraud, if any, within the Company have been detected. These inherent limitations include the realities that judgments in decision-making can be faulty, and that breakdowns can occur because of simple error or mistake. Controls can also be circumvented by the individual acts of some persons, by collusion of two or more people, or by management override of the controls. The design of any system of controls is based in part upon certain assumptions about the likelihood of future events, and there can be no assurance that any design will succeed in achieving its stated goals under all potential future conditions. Over time, controls may become inadequate because of changes in conditions or deterioration in the degree of compliance with associated policies or procedures. Because of the inherent limitations in a cost-effective control system, misstatements due to error or fraud may occur and not be detected.

PART II – OTHER INFORMATION Item 1. Legal Proceedings

From time to time, we may become involved in various lawsuits and legal proceedings that arise in the ordinary course of business. However, litigation is subject to inherent uncertainties and an adverse result in these or other matters may arise from time to time that may harm our business. Except as set forth below we are currently not aware of any such legal proceedings or claims that we believe will have a material adverse effect on our business, financial condition or operating results. Item 1A. Risk Factors

As a smaller reporting company, we are not required to provide the information required by this Item. Item 2. Unregistered Sales of Equity Securities and Use of Proceeds In the three months ended July 31, 2016, the Company did not issue any shares of common stock.

Item 3. Defaults Upon Senior Securities

There have been no events that are required to be reported under this Item. Item 4. Mine Safety Disclosures There have been no events that are required to be reported under this Item. Item 5. Other Information There have been no events that are required to be reported under this Item.

19 |

|

Item 6. Exhibits |

|

31.1 |

|

Certification of Principal Executive Officer pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 |

| |

|

|

|

|

| |

|

31.2 |

|

Certification of Principal Financial Officer pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 |

| |

|

|

|

|

| |

|

32.1 * |

|

Certification of Principal Executive Officer pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 |

| |

|

|

|

|

| |

|

32.2 * |

|

Certification of Principal Financial Officer pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 |

| |

|

|

|

|

| |

|

101.INS |

|

XBRL Instance Document | ||

|

|

|

| ||

|

101.SCH |

|

XBRL Taxonomy Extension Schema Document | ||

|

|

|

| ||

|

101.CAL |

|

XBRL Taxonomy Extension Calculation Linkbase Document | ||

|

|

|

| ||

|

101.DEF |

|

XBRL Taxonomy Extension Definition Linkbase Document | ||

|

|

|

| ||

|

101.LAB |

|

XBRL Taxonomy Extension Label Linkbase Document | ||

|

|

|

| ||

|

101.PRE |

|

XBRL Taxonomy Extension Presentation Linkbase Document | ||

|

|

|

* Furnished herewith.

| ||

|

|

||||

|

20 |

|

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned thereunto duly authorized.

|

|

|

mCig, Inc. | |

|

|

|

|

|

|

|

|

|

Dated: September 28, 2016 |

|

/s/ Paul Rosenberg |

|

|

By: |

Paul Rosenberg |

|

|

Its: |

Chief Executive Officer (Principal Executive Officer) |

|

|

|

|

|

|

|

|

|

Dated: September 28, 2016 |

|

/s/ Michael W. Hawkins |

|

|

By: |

Michael W. Hawkins |

|

|

Its: |

Chief Financial Officer (Principal Financial Officer) |

|

21 |