Attached files

| file | filename |

|---|---|

| EX-32.1 - EXHIBIT 32.1 - TREDEGAR CORP | tg-ex321_20160330x10q.htm |

| EX-31.2 - EXHIBIT 31.2 - TREDEGAR CORP | tg-ex312_20160330x10q.htm |

| EX-31.1 - EXHIBIT 31.1 - TREDEGAR CORP | tg-ex311_20160330x10q.htm |

| EX-32.2 - EXHIBIT 32.2 - TREDEGAR CORP | tg-ex322_20160330x10q.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended March 31, 2016

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 1-10258

Tredegar Corporation

(Exact Name of Registrant as Specified in Its Charter)

Virginia | 54-1497771 | |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

1100 Boulders Parkway Richmond, Virginia | 23225 | |

(Address of Principal Executive Offices) | (Zip Code) | |

Registrant’s Telephone Number, Including Area Code: (804) 330-1000

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | x | Accelerated filer | ¨ | ||

Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | ||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The number of shares of Common Stock, no par value, outstanding as of April 28, 2016: 32,779,606.

PART I - FINANCIAL INFORMATION

Item 1. | Financial Statements. |

Tredegar Corporation

Consolidated Balance Sheets

(In Thousands, Except Share Data)

(Unaudited)

March 31, | December 31, | ||||||

2016 | 2015 | ||||||

Assets | |||||||

Current assets: | |||||||

Cash and cash equivalents | $ | 40,022 | $ | 44,156 | |||

Accounts and other receivables, net of allowance for doubtful accounts and sales returns of $3,076 in 2016 and $3,746 in 2015 | 98,717 | 94,217 | |||||

Income taxes recoverable | — | 360 | |||||

Inventories | 65,517 | 65,325 | |||||

Prepaid expenses and other | 7,282 | 6,946 | |||||

Total current assets | 211,538 | 211,004 | |||||

Property, plant and equipment, at cost | 775,517 | 754,678 | |||||

Less accumulated depreciation | (535,377 | ) | (523,363 | ) | |||

Net property, plant and equipment | 240,140 | 231,315 | |||||

Goodwill and other intangibles, net | 153,284 | 153,072 | |||||

Other assets and deferred charges | 30,801 | 27,869 | |||||

Total assets | $ | 635,763 | $ | 623,260 | |||

Liabilities and Shareholders’ Equity | |||||||

Current liabilities: | |||||||

Accounts payable | $ | 73,603 | $ | 84,148 | |||

Accrued expenses | 32,997 | 33,653 | |||||

Income taxes payable | 1,493 | — | |||||

Total current liabilities | 108,093 | 117,801 | |||||

Long-term debt | 107,000 | 104,000 | |||||

Deferred income taxes | 21,649 | 18,656 | |||||

Other noncurrent liabilities | 107,552 | 110,055 | |||||

Total liabilities | 344,294 | 350,512 | |||||

Commitments and contingencies (Notes 1 and 12) | |||||||

Shareholders’ equity: | |||||||

Common stock, no par value (issued and outstanding - 32,779,606 at March 31, 2016 and 32,682,162 at December 31, 2015) | 29,190 | 29,467 | |||||

Common stock held in trust for savings restoration plan (68,268 shares at March 31, 2016 and 67,726 shares at December 31, 2015) | (1,474 | ) | (1,467 | ) | |||

Accumulated other comprehensive income (loss): | |||||||

Foreign currency translation adjustment | (100,228 | ) | (112,807 | ) | |||

Loss on derivative financial instruments | (111 | ) | (373 | ) | |||

Pension and other post-retirement benefit adjustments | (93,057 | ) | (95,539 | ) | |||

Retained earnings | 457,149 | 453,467 | |||||

Total shareholders’ equity | 291,469 | 272,748 | |||||

Total liabilities and shareholders’ equity | $ | 635,763 | $ | 623,260 | |||

See accompanying notes to financial statements.

2

Tredegar Corporation

Consolidated Statements of Income

(In Thousands, Except Per Share Data)

(Unaudited)

Three Months Ended March 31, | |||||||

2016 | 2015 | ||||||

Revenues and other items: | |||||||

Sales | $ | 207,333 | $ | 234,171 | |||

Other income (expense), net | 770 | 108 | |||||

208,103 | 234,279 | ||||||

Costs and expenses: | |||||||

Cost of goods sold | 163,053 | 189,431 | |||||

Freight | 7,001 | 7,325 | |||||

Selling, general and administrative | 19,862 | 17,073 | |||||

Research and development | 4,977 | 3,885 | |||||

Amortization of intangibles | 956 | 1,083 | |||||

Interest expense | 1,085 | 885 | |||||

Asset impairments and costs associated with exit and disposal activities, net of adjustments | 672 | (52 | ) | ||||

Total | 197,606 | 219,630 | |||||

Income before income taxes | 10,497 | 14,649 | |||||

Income taxes | 3,216 | 4,779 | |||||

Net income | $ | 7,281 | $ | 9,870 | |||

Earnings per share: | |||||||

Basic | $ | 0.22 | $ | 0.30 | |||

Diluted | $ | 0.22 | $ | 0.30 | |||

Shares used to compute earnings per share: | |||||||

Basic | 32,654 | 32,482 | |||||

Diluted | 32,654 | 32,628 | |||||

Dividends per share | $ | 0.11 | $ | 0.09 | |||

See accompanying notes to financial statements.

3

Tredegar Corporation

Consolidated Statements of Comprehensive Income (Loss)

(In Thousands)

(Unaudited)

Three Months Ended March 31, | |||||||

2016 | 2015 | ||||||

Net income | $ | 7,281 | $ | 9,870 | |||

Other comprehensive income (loss): | |||||||

Foreign currency translation adjustment (net of tax of $40 in 2016 and tax benefit of $1,609 in 2015) | 12,579 | (34,653 | ) | ||||

Derivative financial instruments adjustment (net of tax of $156 in 2016 and tax benefit of $399 in 2015) | 262 | (662 | ) | ||||

Amortization of prior service costs and net gains or losses (net of tax of $855 in 2016 and $1,462 in 2015) | 2,482 | 2,522 | |||||

Other comprehensive income (loss) | 15,323 | (32,793 | ) | ||||

Comprehensive income (loss) | $ | 22,604 | $ | (22,923 | ) | ||

See accompanying notes to financial statements.

4

Tredegar Corporation

Consolidated Statements of Cash Flows

(In Thousands)

(Unaudited)

Three Months Ended March 31, | |||||||

2016 | 2015 | ||||||

Cash flows from operating activities: | |||||||

Net income | $ | 7,281 | $ | 9,870 | |||

Adjustments for noncash items: | |||||||

Depreciation | 6,952 | 8,129 | |||||

Amortization of intangibles | 956 | 1,083 | |||||

Deferred income taxes | 306 | (2,419 | ) | ||||

Accrued pension and post-retirement benefits | 2,891 | 3,129 | |||||

Gain on investment accounted for under the fair value method | (800 | ) | — | ||||

Loss on asset impairments and divestitures | 256 | — | |||||

Changes in assets and liabilities, net of effects of acquisitions and divestitures: | |||||||

Accounts and other receivables | (2,489 | ) | (14,782 | ) | |||

Inventories | 1,535 | (3,334 | ) | ||||

Income taxes recoverable/payable | 1,937 | 6,110 | |||||

Prepaid expenses and other | (824 | ) | (1,035 | ) | |||

Accounts payable and accrued expenses | (13,585 | ) | 4,251 | ||||

Other, net | 183 | 1,351 | |||||

Net cash provided by operating activities | 4,599 | 12,353 | |||||

Cash flows from investing activities: | |||||||

Capital expenditures | (7,974 | ) | (7,817 | ) | |||

Proceeds from the sale of assets and other | 676 | 504 | |||||

Net cash used in investing activities | (7,298 | ) | (7,313 | ) | |||

Cash flows from financing activities: | |||||||

Borrowings | 17,250 | 34,250 | |||||

Debt principal payments | (14,250 | ) | (30,500 | ) | |||

Dividends paid | (3,606 | ) | (2,939 | ) | |||

Debt financing costs | (2,450 | ) | (78 | ) | |||

Proceeds from exercise of stock options and other | — | 2,134 | |||||

Net cash used in financing activities | (3,056 | ) | 2,867 | ||||

Effect of exchange rate changes on cash | 1,621 | (2,808 | ) | ||||

Increase (decrease) in cash and cash equivalents | (4,134 | ) | 5,099 | ||||

Cash and cash equivalents at beginning of period | 44,156 | 50,056 | |||||

Cash and cash equivalents at end of period | $ | 40,022 | $ | 55,155 | |||

See accompanying notes to financial statements.

5

Tredegar Corporation

Consolidated Statement of Shareholders’ Equity

(In Thousands, Except Share and Per Share Data)

(Unaudited)

Accumulated Other Comprehensive Income (Loss) | |||||||||||||||||||||||||||

Common Stock | Retained Earnings | Trust for Savings Restoration Plan | Foreign Currency Translation | Gain (Loss) on Derivative Financial Instruments | Pension & Other Post-retirement Benefit Adjust. | Total Shareholders’ Equity | |||||||||||||||||||||

Balance at January 1, 2016 | $ | 29,467 | $ | 453,467 | $ | (1,467 | ) | $ | (112,807 | ) | $ | (373 | ) | $ | (95,539 | ) | $ | 272,748 | |||||||||

Net income | — | 7,281 | — | — | — | — | 7,281 | ||||||||||||||||||||

Other comprehensive income (loss): | |||||||||||||||||||||||||||

Foreign currency translation adjustment (net of tax of $40) | — | — | — | 12,579 | — | — | 12,579 | ||||||||||||||||||||

Derivative financial instruments adjustment (net of tax of $156) | — | — | — | — | 262 | — | 262 | ||||||||||||||||||||

Amortization of prior service costs and net gains or losses (net of tax of $855) | — | — | — | — | — | 2,482 | 2,482 | ||||||||||||||||||||

Cash dividends declared ($0.11 per share) | — | (3,606 | ) | — | — | — | — | (3,606 | ) | ||||||||||||||||||

Stock-based compensation expense | 297 | — | — | — | — | — | 297 | ||||||||||||||||||||

Issued upon exercise of stock options & other | (574 | ) | — | — | — | — | — | (574 | ) | ||||||||||||||||||

Tredegar common stock purchased by trust for savings restoration plan | — | 7 | (7 | ) | — | — | — | — | |||||||||||||||||||

Balance at March 31, 2016 | $ | 29,190 | $ | 457,149 | $ | (1,474 | ) | $ | (100,228 | ) | $ | (111 | ) | $ | (93,057 | ) | $ | 291,469 | |||||||||

See accompanying notes to financial statements.

6

TREDEGAR CORPORATION

NOTES TO THE CONSOLIDATED INTERIM FINANCIAL STATEMENTS

(Unaudited)

1. | In the opinion of management, the accompanying consolidated financial statements of Tredegar Corporation and its subsidiaries (“Tredegar,” “the Company,” “we,” “us” or “our”) contain all adjustments necessary to state fairly, in all material respects, Tredegar’s consolidated financial position as of March 31, 2016, the consolidated results of operations for the three months ended March 31, 2016 and 2015, the consolidated cash flows for the three months ended March 31, 2016 and 2015, and the consolidated changes in shareholders’ equity for the three months ended March 31, 2016. All such adjustments, unless otherwise detailed in the notes to the consolidated interim financial statements, are deemed to be of a normal, recurring nature. The financial position data as of December 31, 2015 that is included herein was derived from the audited consolidated financial statements provided in the Company’s Annual Report on Form 10-K/A for the year ended December 31, 2015 (“2015 Form 10-K”) but does not include all disclosures required by United States generally accepted accounting principles (“U.S. GAAP”). These financial statements should be read in conjunction with the consolidated financial statements and related notes included in the Company’s 2015 Form 10-K. The results of operations for the three months ended March 31, 2016, are not necessarily indicative of the results to be expected for the full year. |

2. | Plant shutdowns, asset impairments, restructurings and other charges are shown in the net sales and operating profit by segment table in Note 9, and unless otherwise noted below, are also included in “Asset impairments and costs associated with exit and disposal activities, net of adjustments” in the consolidated statements of income. |

Plant shutdowns, asset impairments, restructurings and other charges in the first quarter of 2016 include:

• | Pretax charges of $1.1 million associated with the consolidation of domestic PE Films’ manufacturing facilities, which includes severance and other employee-related costs of $0.3 million, asset impairments of $0.2 million, accelerated depreciation of $0.1 million (included in “Cost of goods sold” in the consolidated statements of income) and other facility consolidation-related expenses of $0.5 million ($0.4 million is included in “Cost of goods sold” in the consolidated statements of income); |

• | Pretax charges of $0.4 million associated with a non-recurring business development project (included in “Selling, general and administrative expense” in the consolidated statement of income and “Corporate expenses, net” in the statement of net sales and operating profit by segment); |

• | Pretax charges of $8,000 for severance and other employee-related costs associated with restructurings in PE Films; and |

• | Pretax charges of $7,000 associated with the shutdown of the aluminum extrusions manufacturing facility in Kentland, Indiana. |

Plant shutdowns, asset impairments, restructurings and other charges in the first quarter of 2015 include:

• | Pretax adjustment of $0.1 million to reverse previously accrued severance and other employee-related costs associated with restructurings in PE Films. |

• | Pretax charges of $15,000 associated with the shutdown of the aluminum extrusions manufacturing facility in Kentland, Indiana. |

Results in the first quarter 2016 include an unrealized gain on the Company’s investment in kaleo, Inc (“kaléo”), which is accounted for under the fair value method (included in “Other income (expense), net” in the consolidated statements of income), of $0.8 million ($0.6 million after taxes) (none in 2015). See Note 6 for additional information on investments.

7

A reconciliation of the beginning and ending balances of accrued expenses associated with “Asset impairments and costs associated with exit and disposal activities, net of adjustments” in the consolidated statements of income for the three months ended March 31, 2016 is as follows:

(In Thousands) | Severance | Asset Impairments | Other (a) | Total | |||||||||||

Balance at January 1, 2016 | $ | 1,462 | $ | — | $ | 405 | $ | 1,867 | |||||||

Changes in 2016: | |||||||||||||||

Charges | 294 | 256 | 592 | 1,142 | |||||||||||

Cash spent | (482 | ) | — | (619 | ) | (1,101 | ) | ||||||||

Charges against assets | — | (256 | ) | — | (256 | ) | |||||||||

Balance at March 31, 2016 | $ | 1,274 | $ | — | $ | 378 | $ | 1,652 | |||||||

(a) Other includes other facility consolidation-related costs associated with the consolidation of North American PE Films manufacturing facilities and other shutdown-related costs associated with the shutdown of the Company’s aluminum extrusions manufacturing facility in Kentland, Indiana. | |||||||||||||||

On July 7, 2015, the Company announced its intention to consolidate its domestic production for PE Films by restructuring the operations in its manufacturing facility in Lake Zurich, Illinois. Efforts to transition domestic production from the Lake Zurich manufacturing facility will require various machinery upgrades and equipment transfers to its other manufacturing facilities. Given PE Films’ focus on maintaining product quality and customer satisfaction, the Company anticipates that these activities will be completed in the middle of 2017. Total pre-tax cash expenditures associated with restructuring the Lake Zurich manufacturing facility are expected to be approximately $16-17 million over this period, and once complete, annual pre-tax cash cost savings are expected to be approximately $5-6 million.

The Company expects to recognize costs associated with the exit and disposal activities of approximately $5-6 million over the project period. Exit and disposal costs include severance charges and other employee-related expenses arising from the termination of employees of approximately $2-3 million and equipment transfers and other facility consolidation-related costs of approximately $2 million. During the same period of time, operating expenses will include the acceleration of approximately $3 million of non-cash depreciation expense for certain machinery and equipment at the Lake Zurich manufacturing facility. Total expenses associated with the North American facility consolidation project were $1.1 million in the first quarter of 2016 ($0.7 million included in “Asset impairments and costs associated with exit and disposal activities” and $0.4 million included in “Cost of goods sold” in the consolidated statement of income). Total expenses since the inception of the project were $3.3 million.

Total estimated cash expenditures of $16-17 million over the project period include the following:

• | Cash outlays associated with previously discussed exit and disposal expenses of approximately $5 million; |

• | Capital expenditures associated with equipment upgrades at other PE Films manufacturing facilities in the U.S. of approximately $11 million; |

• | Cash incentives of approximately $1 million in connection with meeting safety and quality standards while production ramps down at the Lake Zurich manufacturing facility; and |

• | Additional operating expenses of approximately $1 million associated with customer product qualifications on upgraded and transferred production lines. |

Cash expenditures for the North American facility consolidation project were $2.2 million in the first quarter of 2016, which includes $1.7 million for capital expenditures. Total cash expenditures since the inception of the project were $5.3 million, which includes $4.2 million for capital expenditures.

8

3. | The components of inventories are as follows: |

March 31, | December 31, | |||||||

(In Thousands) | 2016 | 2015 | ||||||

Finished goods | $ | 14,679 | $ | 13,935 | ||||

Work-in-process | 10,173 | 9,249 | ||||||

Raw materials | 20,338 | 22,149 | ||||||

Stores, supplies and other | 20,327 | 19,992 | ||||||

Total | $ | 65,517 | $ | 65,325 | ||||

4. | Basic earnings per share is computed by dividing net income by the weighted average number of shares of common stock outstanding. Diluted earnings per share is computed by dividing net income by the weighted average common and potentially dilutive common equivalent shares outstanding, determined as follows: |

Three Months Ended | |||||

March 31, | |||||

(In Thousands) | 2016 | 2015 | |||

Weighted average shares outstanding used to compute basic earnings per share | 32,654 | 32,482 | |||

Incremental dilutive shares attributable to stock options and restricted stock | — | 146 | |||

Shares used to compute diluted earnings per share | 32,654 | 32,628 | |||

Incremental shares attributable to stock options and restricted stock are computed under the treasury stock method using the average market price during the related period. For the three months ended March 31, 2016 and 2015, average out-of-the-money options to purchase shares that were excluded from the calculation of incremental shares attributable to stock options and restricted stock were 692,014 and 384,760, respectively.

5. | The following table summarizes the after-tax changes in accumulated other comprehensive income (loss) for the three months ended March 31, 2016: |

(In Thousands) | Foreign currency translation adjustment | Gain (loss) on derivative financial instruments | Pension and other post-retirement benefit adjustments | Total | |||||||||||

Beginning balance, January 1, 2016 | $ | (112,807 | ) | $ | (373 | ) | $ | (95,539 | ) | $ | (208,719 | ) | |||

Other comprehensive income (loss) before reclassifications | 12,579 | (342 | ) | — | 12,237 | ||||||||||

Amounts reclassified from accumulated other comprehensive income (loss) | — | 604 | 2,482 | 3,086 | |||||||||||

Net other comprehensive income (loss) - current period | 12,579 | 262 | 2,482 | 15,323 | |||||||||||

Ending balance, March 31, 2016 | $ | (100,228 | ) | $ | (111 | ) | $ | (93,057 | ) | $ | (193,396 | ) | |||

9

The following table summarizes the after-tax changes in accumulated other comprehensive income (loss) for the three months ended March 31, 2015:

(In Thousands) | Foreign currency translation adjustment | Gain (loss) on derivative financial instruments | Pension and other post-retirement benefit adjustments | Total | |||||||||||

Beginning balance, January 1, 2015 | $ | (47,270 | ) | $ | 656 | $ | (103,581 | ) | $ | (150,195 | ) | ||||

Other comprehensive income (loss) before reclassifications | (34,653 | ) | (682 | ) | — | (35,335 | ) | ||||||||

Amounts reclassified from accumulated other comprehensive income (loss) | — | 20 | 2,522 | 2,542 | |||||||||||

Net other comprehensive income (loss) - current period | (34,653 | ) | (662 | ) | 2,522 | (32,793 | ) | ||||||||

Ending balance, March 31, 2015 | $ | (81,923 | ) | $ | (6 | ) | $ | (101,059 | ) | $ | (182,988 | ) | |||

Reclassifications of balances out of accumulated other comprehensive income (loss) into net income for the three months ended March 31, 2016 are summarized as follows:

(In Thousands) | Amount reclassified from other comprehensive income | Location of gain (loss) reclassified from accumulated other comprehensive income to net income | |||

Gain (loss) on derivative financial instruments: | |||||

Aluminum future contracts, before taxes | $ | (984 | ) | Cost of sales | |

Foreign currency forward contracts, before taxes | 15 | Cost of sales | |||

Total, before taxes | (969 | ) | |||

Income tax expense (benefit) | (365 | ) | Income taxes | ||

Total, net of tax | $ | (604 | ) | ||

Amortization of pension and other post-retirement benefits: | |||||

Actuarial gain (loss) and prior service costs, before taxes | $ | (3,337 | ) | (a) | |

Income tax expense (benefit) | (855 | ) | Income taxes | ||

Total, net of tax | $ | (2,482 | ) | ||

(a) | This component of accumulated other comprehensive income is included in the computation of net periodic pension cost (see Note 8 for additional detail). |

10

Reclassifications of balances out of accumulated other comprehensive income (loss) into net income for the three months ended March 31, 2015 are summarized as follows:

(In Thousands) | Amount reclassified from other comprehensive income | Location of gain (loss) reclassified from accumulated other comprehensive income to net income | |||

Gain (loss) on derivative financial instruments: | |||||

Aluminum future contracts, before taxes | $ | (48 | ) | Cost of sales | |

Foreign currency forward contracts, before taxes | 15 | Cost of sales | |||

Total, before taxes | (33 | ) | |||

Income tax expense (benefit) | (13 | ) | Income taxes | ||

Total, net of tax | $ | (20 | ) | ||

Amortization of pension and other post-retirement benefits: | |||||

Actuarial gain (loss) and prior service costs, before taxes | $ | (3,984 | ) | (a) | |

Income tax expense (benefit) | (1,462 | ) | Income taxes | ||

Total, net of tax | $ | (2,522 | ) | ||

(a) | This component of accumulated other comprehensive income is included in the computation of net periodic pension cost (see Note 8 for additional detail). |

6. | In August 2007 and December 2008, the Company made an aggregate investment of $7.5 million in kaléo, a privately held specialty pharmaceutical company dedicated to building innovative solutions for serious and life-threatening medical conditions. The mission of kaléo is to provide products that empower patients to confidently take control of their medical conditions. Tredegar’s ownership interest on a fully diluted basis was approximately 19% at March 31, 2016, and the investment is accounted for under the fair value method. At the time of the initial investment, the Company elected the fair value option over the equity method of accounting since its investment objectives were similar to those of venture capitalists, which typically do not have controlling financial interests. |

The estimated fair value of the investment in kaléo (also the carrying value, which is included in “Other assets and deferred charges” in the consolidated balance sheets) was $19.4 million at March 31, 2016 and $18.6 million at December 31, 2015. In 2009, kaléo licensed exclusive rights to sanofi-aventis U.S. LLC (“Sanofi”) to commercialize an epinephrine auto-injector in the U.S. and Canada. Sanofi began manufacturing and distributing the epinephrine auto-injector, under the names Auvi-Q® in the U.S. and Allerject® in Canada, in 2013. Sanofi announced on October 28, 2015, a voluntary recall of all Auvi-Q and Allerject epinephrine injectors that were on the market. An unrealized gain of $0.8 million was recognized in the first quarter of 2016 (no unrealized gain (loss) in the first quarter of 2015). The change in the estimated fair value of the Company’s holding in kaléo in the first quarter of 2016 was primarily associated with the negotiated terms of the termination of Sanofi’s exclusive rights license for Auvi-Q and Allerject in North America and the return of such rights to kaléo.

Unrealized gains (losses) associated with this investment are included in “Other income (expense), net” in the consolidated statements of income and separately stated in the segment operating profit table in Note 9. Subsequent to its most recent investment (December 15, 2008), and until the next round of financing, the Company believes fair value estimates are based upon Level 3 inputs since there is no secondary market for its ownership interest. Accordingly, until the next round of financing or any other significant financial transaction, value estimates will primarily be based on assumptions relating to achieving product development and commercialization milestones, cash flow projections (projections of sales, costs, expenses, capital expenditures and working capital investment) and discounting of these factors for their high degree of risk. If kaléo does not meet its development and commercialization milestones or there are indications that the amount or timing of its projected cash flows or related risks are unfavorable versus the most recent valuation, or a new round of financing or other significant financial transaction indicates a lower enterprise value, then the Company’s estimate of the fair value of its ownership interest in kaléo is likely to decline. Adjustments to the estimated fair value of this investment will be made in the period upon which such changes can be quantified.

11

In addition to the impact on valuation of the possible changes in assumptions, Level 3 inputs and projections from changes in business conditions, the fair market valuation of the Company’s interest in kaléo is sensitive to changes in the weighted average cost of capital used to discount cash flow projections for the high degree of risk associated with meeting development and commercialization milestones as anticipated. The weighted average cost of capital used in the fair market valuation of Tredegar’s interest in kaléo was 45% at both March 31, 2016 and December 31, 2015. At March 31, 2016, the effect of a 500 basis point decrease in the weighted average cost of capital assumption would have increased the fair value of the Company’s interest in kaléo by approximately $5 million, and a 500 basis point increase in the weighted average cost of capital assumption would have decreased the fair value of the Company’s interest by approximately $4 million.

Had the Company not elected to account for its investment under the fair value method, it would have been required to use the equity method of accounting. The condensed balance sheets for kaléo at March 31, 2016 and December 31, 2015 and condensed statements of operations for the three months ended March 31, 2016 and 2015, as reported to the Company by kaléo, are provided below:

(In Thousands) | March 31, 2016 | December 31, 2015 | March 31, 2016 | December 31, 2015 | ||||||||||||

Assets: | Liabilities & Equity: | |||||||||||||||

Cash & short-term investments | $ | 96,431 | $ | 91,844 | ||||||||||||

Restricted cash | 3,748 | 8,182 | ||||||||||||||

Other current assets | 19,063 | 9,070 | Other current liabilities | $ | 33,644 | $ | 10,261 | |||||||||

Property & equipment | 15,821 | 8,453 | Other noncurrent liabilities | 609 | 552 | |||||||||||

Patents | 2,867 | 2,811 | Long term debt, net | 142,868 | 142,696 | |||||||||||

Other long-term assets | 114 | 92 | Equity | (39,077 | ) | (33,057 | ) | |||||||||

Total assets | $ | 138,044 | $ | 120,452 | Total liabilities & equity | $ | 138,044 | $ | 120,452 | |||||||

Three Months Ended March 31, | |||||||

2016 | 2015 | ||||||

Revenues & Expenses: | |||||||

Revenues, net (a) | $ | (3,050 | ) | $ | 4,850 | ||

Cost of goods sold | (3,622 | ) | (2,330 | ) | |||

Expenses and other, net (b) | 541 | (14,384 | ) | ||||

Income tax benefit (expense) | (8 | ) | (4 | ) | |||

Net income (loss) | $ | (6,139 | ) | $ | (11,868 | ) | |

(a) Negative revenues during the first quarter of 2016 relate to the impact of product sales allowances on channel inventory following a product price reset during the quarter. (b) “Expenses and other, net” includes selling, general and administrative expense, research and development expense, gain on contract termination, interest expense and other income (expense), net. Excluding the gain, “Expenses and other, net” would have been a net deduction of $17.5 million in the first quarter of 2016. | |||||||

The Company’s investment in the Harbinger Capital Partners Special Situations Fund, L.P. (“Harbinger Fund”) had a carrying value (included in “Other assets and deferred charges”) of $1.7 million at March 31, 2016 and December 31, 2015. The carrying value at March 31, 2016 reflected Tredegar’s cost basis in its investment in the Harbinger Fund, net of total withdrawal proceeds received and unrealized losses. No withdrawal proceeds were received in the first three months of 2016 or 2015. The timing and amount of future installments of withdrawal proceeds, which commenced in August 2010, were not known as of March 31, 2016. Gains on the Company’s investment in the Harbinger Fund will be recognized when the amounts expected to be collected from any withdrawal from the investment are known, which will likely be when cash in excess of the remaining carrying value is received. Losses will be recognized when management believes it is probable that future withdrawal proceeds will not exceed the remaining carrying value.

7. | Tredegar uses derivative financial instruments for the purpose of hedging margin exposure from fixed-price forward sales contracts in Aluminum Extrusions and currency exchange rate exposures that exist as part of ongoing business operations (primarily in PE Films). These derivative financial instruments are designated as and qualify as cash flow hedges and are recognized in the consolidated balance sheet at fair value. The fair value of derivative instruments recorded on the consolidated balance sheets are based upon Level 2 inputs. If individual derivative instruments with the |

12

same counterparty can be settled on a net basis, the Company records the corresponding derivative fair values as a net asset or net liability.

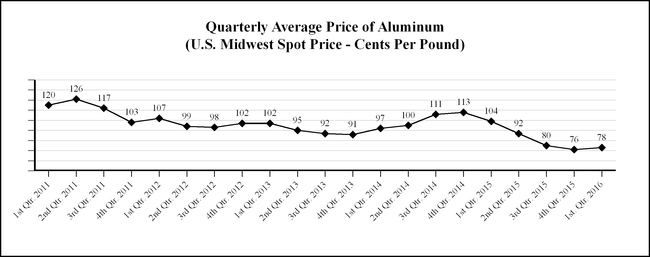

In the normal course of business, Aluminum Extrusions enters into fixed-price forward sales contracts with certain customers for the future sale of fixed quantities of aluminum extrusions at scheduled intervals. In order to hedge margin exposure created from the fixing of future sales prices relative to volatile raw material (aluminum) costs, Aluminum Extrusions enters into a combination of forward purchase commitments and futures contracts to acquire or hedge aluminum, based on the scheduled purchases for the firm sales commitments. The fixed-price firm sales commitments and related hedging instruments generally have durations of not more than 12 months, and the notional amount of aluminum futures contracts that hedged future purchases of aluminum to meet fixed-price forward sales contract obligations was $15.2 million (18.1 million pounds of aluminum) at March 31, 2016 and $16.6 million (18.9 million pounds of aluminum) at December 31, 2015.

The table below summarizes the location and gross amounts of aluminum futures contract fair values in the consolidated balance sheets as of March 31, 2016 and December 31, 2015:

March 31, 2016 | December 31, 2015 | ||||||||||

(In Thousands) | Balance Sheet Account | Fair Value | Balance Sheet Account | Fair Value | |||||||

Derivatives Designated as Hedging Instruments | |||||||||||

Asset derivatives: Aluminum futures contracts | Accrued expenses | $ | — | Accrued expenses | $ | 44 | |||||

Liability derivatives: Aluminum futures contracts | Accrued expenses | $ | (1,319 | ) | Accrued expenses | $ | (1,797 | ) | |||

Derivatives Not Designated as Hedging Instruments | |||||||||||

Asset derivatives: Aluminum futures contracts | Accrued expenses | $ | — | Accrued expenses | $ | — | |||||

Liability derivatives: Aluminum futures contracts | Accrued expenses | $ | — | Accrued expenses | $ | — | |||||

Net asset (liability) | $ | (1,319 | ) | $ | (1,753 | ) | |||||

In the event that a counterparty to an aluminum fixed-price forward sales contract chooses not to take delivery of its aluminum extrusions, the customer is contractually obligated to compensate Aluminum Extrusions for any losses on the related aluminum futures and/or forward contracts through the date of cancellation.

These derivative contracts involve elements of market risk that are not reflected on the consolidated balance sheet, including the risk of dealing with counterparties and their ability to meet the terms of the contracts. The counterparties to any forward purchase commitments are major aluminum brokers and suppliers, and the counterparties to any aluminum futures contracts are major financial institutions. Fixed-price forward sales contracts are only made available to the best and most credit-worthy customers. The counterparties to our foreign currency futures and zero-cost collar contracts are major financial institutions.

The effect on net income and other comprehensive income (loss) of derivative instruments classified as cash flow hedges and described in the previous paragraphs for the three month periods ended March 31, 2016 and 2015 is summarized in the table below:

(In Thousands) | Cash Flow Derivative Hedges | ||||||||||||||

Aluminum Futures Contracts | Foreign Currency Forwards | ||||||||||||||

Three Months Ended March 31, | |||||||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||||||

Amount of pre-tax gain (loss) recognized in other comprehensive income | $ | (550 | ) | $ | (1,094 | ) | $ | — | $ | — | |||||

Location of gain (loss) reclassified from accumulated other comprehensive income into net income (effective portion) | Cost of sales | Cost of sales | Cost of sales | Cost of sales | |||||||||||

Amount of pre-tax gain (loss) reclassified from accumulated other comprehensive income to net income (effective portion) | $ | (984 | ) | $ | (48 | ) | $ | 15 | $ | 15 | |||||

13

As of March 31, 2016, the Company expects $0.8 million of unrealized after-tax losses on derivative instruments reported in accumulated other comprehensive income (loss) to be reclassified to earnings within the next 12 months. For the three month periods ended March 31, 2016 and 2015, net gains or losses realized on previously unrealized net gains or losses from hedges that had been discontinued were not material.

8. | The Company sponsors noncontributory defined benefit (pension) plans covering most employees. The plans for salaried and hourly employees currently in effect are based on a formula using the participant’s years of service and compensation or using the participant’s years of service and a dollar amount. The plan is closed to new participants, and based on plan changes announced in 2006, pay for active plan participants was frozen as of December 31, 2007. Beginning in the first quarter of 2014, with the exception of plan participants at one of Tredegar’s U.S. manufacturing facilities, the plan no longer accrued benefits associated with crediting employees for service, thereby freezing future benefits under the plan. |

The components of net periodic benefit cost for our pension and other post-retirement benefit programs reflected in consolidated results are shown below:

Pension Benefits | Other Post-Retirement Benefits | ||||||||||||||

Three Months Ended March 31, | Three Months Ended March 31, | ||||||||||||||

(In Thousands) | 2016 | 2015 | 2016 | 2015 | |||||||||||

Service cost | $ | 72 | $ | 144 | $ | 11 | $ | 12 | |||||||

Interest cost | 3,365 | 3,312 | 85 | 84 | |||||||||||

Expected return on plan assets | (3,978 | ) | (4,407 | ) | — | — | |||||||||

Amortization of prior service costs, gains or losses and net transition asset | 3,384 | 4,024 | (48 | ) | (40 | ) | |||||||||

Net periodic benefit cost | $ | 2,843 | $ | 3,073 | $ | 48 | $ | 56 | |||||||

Pension and other post-retirement liabilities were $100.4 million and $101.0 million at March 31, 2016 and December 31, 2015, respectively ($0.6 million included in “Accrued expenses” at March 31, 2016 and December 31, 2015, with the remainder included in “Other noncurrent liabilities” in the consolidated balance sheets). The Company’s required contributions are expected to be $6.1 million in 2016. There were no contributions to the pension plan in the first quarter of 2016. Tredegar funds its other post-retirement benefits (life insurance and health benefits) on a claims-made basis, which the Company anticipates will be consistent with amounts paid for the year ended December 31, 2015 or $0.1 million.

14

9. | The Company’s business segments are PE Films, Flexible Packaging and Aluminum Extrusions. Information by business segment is reported below. Tredegar had historically reported two business segments: Film Products and Aluminum Extrusions. In 2015, the Company divided Film Products into two separate reportable segments: PE Films and Flexible Packaging Films. All historical results for PE Films and Flexible Packaging Films have been separately presented to conform with the new presentation of segments. There are no accounting transactions between segments and no allocations to segments. Net sales (sales less freight) and operating profit from ongoing operations are the measures of sales and operating profit used by the chief operating decision maker for purposes of assessing performance. |

The following table presents net sales and operating profit by segment for the three-month periods ended March 31, 2016 and 2015:

Three Months Ended March 31, | |||||||

(In Thousands) | 2016 | 2015 | |||||

Net Sales | |||||||

PE Films | $ | 88,481 | $ | 106,357 | |||

Flexible Packaging Films | 26,377 | 26,844 | |||||

Aluminum Extrusions | 85,474 | 93,645 | |||||

Total net sales | 200,332 | 226,846 | |||||

Add back freight | 7,001 | 7,325 | |||||

Sales as shown in the Consolidated Statements of Income | $ | 207,333 | $ | 234,171 | |||

Operating Profit | |||||||

PE Films: | |||||||

Ongoing operations | $ | 10,235 | $ | 16,832 | |||

Plant shutdowns, asset impairments, restructurings and other | (1,135 | ) | — | ||||

Flexible Packaging Films: | |||||||

Ongoing operations | 2,032 | 785 | |||||

Plant shutdowns, asset impairments, restructurings and other | — | 67 | |||||

Aluminum Extrusions: | |||||||

Ongoing operations | 7,499 | 5,292 | |||||

Plant shutdowns, asset impairments, restructurings and other | (7 | ) | (15 | ) | |||

Total | 18,624 | 22,961 | |||||

Interest income | 37 | 89 | |||||

Interest expense | 1,085 | 885 | |||||

Gain on investment accounted for under fair value method | 800 | — | |||||

Stock option-based compensation costs | (37 | ) | 300 | ||||

Corporate expenses, net | 7,916 | 7,216 | |||||

Income before income taxes | 10,497 | 14,649 | |||||

Income taxes | 3,216 | 4,779 | |||||

Net income | $ | 7,281 | $ | 9,870 | |||

15

The following table presents identifiable assets by segment at March 31, 2016 and December 31, 2015:

(In Thousands) | March 31, 2016 | December 31, 2015 | |||||

PE Films | $ | 276,940 | $ | 270,236 | |||

Flexible Packaging Films | 155,000 | 146,253 | |||||

Aluminum Extrusions | 135,726 | 136,935 | |||||

Subtotal | 567,666 | 553,424 | |||||

General corporate | 28,075 | 25,680 | |||||

Cash and cash equivalents | 40,022 | 44,156 | |||||

Total | $ | 635,763 | $ | 623,260 | |||

10. | Tredegar recorded a tax expense of $3.2 million on pre-tax net income of $10.5 million in the first three months of 2016. The effective tax rate in the first three months of 2016 was 30.6%, compared to 32.6% in the first three months of 2015 and is expected to be 34% for the full year 2016. The significant differences between the U.S. federal statutory rate and the effective income tax rate for the three months ended March 31, 2016 and 2015 are as follows: |

Percent of Income Before Income Taxes | |||||

Three Months Ended March 31, | 2016 | 2015 | |||

Income tax expense at federal statutory rate | 35.0 | 35.0 | |||

Non-deductible expenses | 1.0 | 0.7 | |||

Income tax contingency accruals and tax settlements | 0.9 | 0.8 | |||

State taxes, net of federal income tax benefit | 0.6 | 1.2 | |||

Valuation allowance for foreign operating loss carry-forwards | 0.1 | (0.4 | ) | ||

Changes in estimates related to prior year tax provision | (0.2 | ) | (0.2 | ) | |

Foreign investment write-up | (0.3 | ) | — | ||

Research and development tax credit | (0.9 | ) | — | ||

Foreign rate differences | (0.9 | ) | (1.4 | ) | |

Unremitted earnings from foreign operations | (0.9 | ) | 1.0 | ||

Valuation allowance for capital loss carry-forwards | (1.1 | ) | (1.6 | ) | |

Domestic production activities deduction | (2.7 | ) | (2.5 | ) | |

Effective income tax rate | 30.6 | 32.6 | |||

The Brazilian federal statutory income tax rate is a composite of 34.0% (25.0% of income tax and 9.0% of social contribution on income). Terphane Holdings LLC’s (“Terphane”) manufacturing facility in Brazil is the beneficiary of certain income tax incentives that allow for a reduction in the statutory Brazilian federal income tax rate to 15.25% levied on the operating profit on certain of its products. The incentives have been granted for a 10-year period, which has a retroactive commencement date of January 1, 2015. No benefit was recognized from these tax incentives in the first three months of 2016 or 2015.

In connection with its capacity expansion project in Brazil, the Company paid certain social taxes associated with the purchase of machinery and equipment and construction of buildings and other long-term assets. Payments of these taxes in Brazil were included in “Net cash used in investing activities” given the nature of the underlying use of cash (e.g. the purchase of property, plant and equipment). The Company can recover tax credits associated with the purchase of machinery and equipment at different points over a period up to 24 months. Once the machinery and equipment was placed into service in the fourth quarter of 2014, the Company started applying these tax credits against various other taxes due in Brazil, with their recovery being reflected as cash received from investing activities, consistent with the classification of the original payments.

Income taxes in 2016 included a partial reversal of a valuation allowance of $0.1 million related to the expected limitations on the utilization of assumed capital losses on certain investments that were recognized in prior years. Income taxes in 2015 included the partial reversal of a valuation allowance of $0.2 million related to the expected limitations on the utilization of assumed capital losses on certain investments. The Company had a valuation allowance for excess capital losses from investments and other related items of $10.8 million at March 31, 2016. Tredegar continues to evaluate opportunities to utilize these loss carryforwards prior to their expiration at various dates in the

16

future. As events and circumstances warrant, allowances will be reversed when it is more likely than not that future taxable income will exceed deductible amounts, thereby resulting in the realization of deferred tax assets.

Tredegar and its subsidiaries file income tax returns in the U.S., various states and jurisdictions outside the U.S. With few exceptions, Tredegar and its subsidiaries are no longer subject to U.S. federal, state or non-U.S. income tax examinations by tax authorities for years before 2012.

11. | On March 1, 2016, Tredegar entered into a $400 million five-year, secured revolving credit facility (“Credit Agreement”), with an option to increase that amount by $50 million. The Credit Agreement replaces the Company’s previous $350 million five-year, unsecured revolving credit facility that was due to expire on April 17, 2017. In connection with the refinancing, the Company borrowed $107 million under the Credit Agreement, which was used, together with available cash on hand, to repay all indebtedness under the previous revolving credit facility. |

Borrowings under the Credit Agreement bear an interest rate of LIBOR plus a credit spread and commitment fees charged on the unused amount under the Credit Agreement at various indebtedness-to-adjusted EBITDA levels as follows:

Pricing Under Credit Revolving Agreement (Basis Points) | ||||||

Indebtedness-to-Adjusted EBITDA Ratio | Credit Spread Over LIBOR | Commitment Fee | ||||

> 3.5x but <= 4.0x | 250 | 45 | ||||

> 3.0x but <= 3.5x | 225 | 40 | ||||

> 2.0x but <= 3.0x | 200 | 35 | ||||

> 1.0x but <= 2.0x | 175 | 30 | ||||

<= 1.0x | 150 | 25 | ||||

At March 31, 2016, the interest cost on debt borrowed under the Credit Agreement was priced at one-month LIBOR plus the applicable credit spread of 175 basis points.

The most restrictive covenants in the Credit Agreement include:

• | Maximum indebtedness-to-adjusted EBITDA (“Leverage Ratio:) of 4.00x; |

• | Minimum adjusted EBIT-to-interest expense of 2.50x; and |

• | Maximum aggregate distributions to shareholders over the term of the Credit Agreement of $100,000 plus, beginning with the fiscal quarter ended March 31, 2016, 50% of net income and, at a Leverage Ratio of equal to or greater than 3.00x, a limitation on such payments for the succeeding quarter at the greater of (i) $4 million and (ii) 50% of consolidated net income for the most recent fiscal quarter, and, at a Leverage Ratio of equal to or greater than 3.50x, the prevention of such payments for the succeeding quarter unless the fixed charge coverage ratio is equal to or greater than 1.20x. |

The Credit Agreement is secured by substantially all of the Company’s and its domestic subsidiaries’ assets, including equity in certain material first-tier foreign subsidiaries. As of March 31, 2016, Tredegar was in compliance with all financial covenants outlined in the Credit Agreement.

17

12. | In 2011, Tredegar was notified by U.S. Customs and Border Protection (“U.S. Customs”) that certain film products exported by Terphane to the U.S. since November 6, 2008 could be subject to duties associated with an antidumping duty order on imported PET films from Brazil. The Company contested the applicability of these antidumping duties to the films exported by Terphane, and it filed a request with the U.S. Department of Commerce (“Commerce”) for clarification about whether the film products at issue are within the scope of the antidumping duty order. On January 8, 2013, Commerce issued a scope ruling confirming that the films are not subject to the order, provided that Terphane can establish to the satisfaction of U.S. Customs that the performance enhancing layer on those films is greater than 0.00001 inches thick. The films at issue are manufactured to specifications that exceed that threshold. On February 6, 2013, certain U.S. producers of PET film filed a summons with the U.S. Court of International Trade to appeal the scope ruling from Commerce. If U.S. Customs ultimately were to require the collection of anti-dumping duties because Commerce’s scope ruling was overturned on appeal, or otherwise, indemnifications for related liabilities are specifically provided for under the purchase agreement pursuant to which the Company acquired Terphane. In December 2014, the U.S. International Trade Commission voted to revoke the anti-dumping duty order on imported PET films from Brazil. The revocation, as a result of the vote by the U.S. International Trade Commission, was effective as of November 2013. On February 20, 2015, certain U.S. producers of PET films filed a summons with the U.S. Court of International Trade to appeal the determination by the U.S. International Trade Commission. |

13. | In May 2014, the Financial Accounting Standards Board (“FASB”) and International Accounting Standards Board (“IASB”) issued their converged standard on revenue recognition. The revised revenue standard contains principles that an entity will apply to direct the measurement of revenue and timing of when it is recognized. The core principle of the guidance is that the recognition of revenue should depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which an entity expects to be entitled in exchange for those goods and services. To achieve that core principle, an entity will utilize a principle-based five-step approach model. The converged standard also includes more robust disclosure requirements which will require entities to provide sufficient information to enable users of financial statements to understand the nature, amount, timing and uncertainty of revenue and cash flows arising from contracts with customers. In March 2016, amended guidance was issued regarding clarifying the implementation guidance on principal versus agent considerations. The effective date of this revised standard is for annual reporting periods beginning after December 15, 2017, including interim periods within that reporting period. Early application is permitted as of annual reporting periods beginning after December 15, 2016, including interim reporting periods within that annual reporting period. The converged standard can be adopted either retrospectively or through the use of a practical expedient. The Company is still assessing the impact of this new guidance. |

In April 2015, the FASB issued new guidance requiring that debt issuance costs related to a recognized debt liability be presented in the balance sheet as a direct reduction from the carrying amount of that corresponding debt liability, consistent with debt discounts, rather than as a deferred charge (e.g. an asset). In August 2015, the FASB issued updated guidance that stated in the absence of authoritative guidance, debt issuance costs associated with line-of-credit arrangements could continue to be deferred and presented as an asset over the corresponding amortization period. The new guidance is effective for annual reporting periods beginning after December 15, 2015, including interim periods within that reporting period. The guidance requires that all prior period balance sheets be adjusted retrospectively. Deferred debt issuance costs associated with the Company’s Credit Agreement were $2.9 million and $0.7 million (included in “Other assets and deferred charges” in the consolidated balance sheet) at March 31, 2016 and December 31, 2015, respectively. The Company adopted this guidance this quarter but there was no impact to its consolidated balance sheet as its current debt issuance costs are associated with a revolving line of credit.

In July 2015, the FASB issued new guidance for the measurement of inventories. Inventories within the scope of the revised guidance should be measured at the lower of cost or net realizable value. The previous guidance dictated that inventory should be measured at the lower of cost or market, with market either replacement cost, net realizable value or net realizable value less an approximation of normal profit margin. Net realizable value is the estimated selling prices in the ordinary course of business, less reasonably predictable costs of completion, disposal and transportation. Subsequent measurement is unchanged for inventories measured using LIFO or the retail inventory method. The amended guidance is effective for fiscal years beginning after December 31, 2016, including the interim periods within those fiscal years. The amendments should be applied prospectively, with early adoption permitted. The Company is still assessing the impact of this revised guidance.

In January 2016, the FASB issued amended guidance associated with accounting for equity investments measured at fair value. The amended guidance requires all equity investments to be measured at fair value with changes in the fair value recognized through net income (other than those accounted for under equity method of accounting or those that result in consolidation of the investee). The amended guidance also require an entity to present separately in other comprehensive income the portion of the total change in the fair value of a liability resulting from a change in the

18

instrument-specific credit risk when the entity has elected to measure the liability at fair value in accordance with the fair value option for financial instruments. In addition the amendments in this update eliminate the requirement to disclose the fair value of financial instruments measured at amortized cost for entities that are not public business entities and the requirement to disclose the method(s) and significant assumptions used to estimate the fair value that is required to be disclosed for financial instruments measured at amortized cost on the balance sheet for public business entities. The amended guidance is effective for fiscal years beginning after December 31, 2017, including the interim periods within those fiscal years. The amendments should be applied by means of a cumulative-effect adjustment to the balance sheet as of the beginning of the fiscal year of adoption. The amendments related to equity securities without readily determinable fair values (including disclosure requirements) should be applied prospectively to equity investments that exist as of the date of adoption of the update. Early adoption is permitted under limited, specific circumstances. The Company is still assessing the impact of this new guidance.

In February 2016, the FASB issued a revised standard on lease accounting. Lessees will need to recognize virtually all of their leases on the balance sheet, by recording a right-of-use asset and lease liability. The revised standard requires additional analysis of the components of a transaction to determine if a right-to-use asset is embedded in the transaction that needs to be treated as a lease. Substantial additional disclosures are also required by the revised standard. The revised standard is effective for fiscal years beginning after December 31, 2018, including the interim periods within those fiscal years. The revised standard should be applied on a modified retrospective approach or through the use of a practical expedient, with early adoption permitted. The Company is still assessing the impact of this revised standard.

In March 2016, the FASB issued amended guidance associated with embedded derivatives in debt instruments. The current guidance requires that embedded derivatives be separated from the host contract and accounted for separately as derivatives if certain criteria are met, including the “clearly and closely related” criterion. The amended guidance clarifies the requirements for assessing whether contingent call (put) options that can accelerate the payment of principal on debt instruments are clearly and closely related to their debt hosts. An entity performing the assessment under the amendments is required to assess the embedded call (put) options solely in accordance with the four-step decision sequence. The amendments apply to all entities that are issuers of or investors in debt instruments (or hybrid financial instruments that are determined to have a debt host) with embedded call (put) options. The amended guidance is effective for fiscal years beginning after December 31, 2016, including the interim periods within those fiscal years. The revised standard should be applied on a modified retrospective approach, with early adoption permitted. The Company is still assessing the impact of this revised standard.

In March 2016, the FASB issued amended guidance to simplify the accounting for equity method investments. The amendments to the guidance eliminate the requirement that an entity retroactively adopt the equity method of accounting if an investment qualifies for use of the equity method as a result of an increase in the level of ownership or degree of influence. The amendments require that the equity method investor add the cost of acquiring the additional interest in the investee to the current basis of the investor’s previously held interest and adopt the equity method of accounting as of the date the investment becomes qualified for equity method accounting. The amendments require that the equity method investor add the cost of acquiring the additional interest in the investee to the current basis of the investor’s previously held interest and adopt the equity method of accounting as of the date the investment becomes qualified for equity method accounting. The amended guidance is effective for fiscal years beginning after December 31, 2016, including the interim periods within those fiscal years. The revised standard should be applied on a prospective basis, with early adoption permitted. The Company is still assessing the impact of this revised standard.

In March 2016, the FASB issued amended guidance to simplify several aspects of the accounting for share-based payment transactions, including the income tax consequences, classification of awards as either equity or liabilities, and classification on the statement of cash flows. The updated guidance is effective for fiscal years beginning after December 31, 2016, including the interim periods within those fiscal years. The updated standard can be applied on a retrospective or modified retrospective basis, with early adoption permitted. The Company is still assessing the impact of this updated standard.

19

Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations. |

Forward-looking and Cautionary Statements

Some of the information contained in this Quarterly Report on Form 10-Q (“Form 10-Q”) may constitute “forward-looking statements” within the meaning of the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995. When using the words “believe,” “estimate,” “anticipate,” “expect,” “project,” “likely,” “may” and similar expressions, Tredegar does so to identify forward-looking statements. Such statements are based on then current expectations and are subject to a number of risks and uncertainties that could cause actual results to differ materially from those addressed in the forward-looking statements. It is possible that actual results and financial condition may differ, possibly materially, from the anticipated results and financial condition indicated in or implied by these forward-looking statements. Accordingly, you should not place undue reliance on these forward-looking statements. Factors that could cause actual results to differ from expectations include, without limitation: we have an underfunded defined benefit (pension) plan to which we will be required to make contributions; our performance is influenced by costs incurred by our operating companies, including, for example, the cost of raw materials and energy; our substantial international operations subject us to risks of doing business in countries outside the U.S., which could adversely affect our consolidated financial condition, results of operations and cash flows; we may not be able to successfully identify, complete or integrate strategic acquisitions; acquired businesses, including Terphane Holdings LLC (“Terphane”) and AACOA, Inc. (“AACOA”), may not achieve the levels of revenue, profit, productivity, or otherwise perform as we expect; acquisitions, including our acquisitions of Terphane and AACOA, involve special risks, including without limitation, diversion of management’s time and attention from our existing businesses, the potential assumption of unanticipated liabilities and contingencies and potential difficulties in integrating acquired businesses and achieving anticipated operational improvements; PE Films is highly dependent on sales associated with its top five customers, the largest of which is The Procter & Gamble Company, and the loss or significant reduction of sales associated with one or more of these customers could have a material adverse effect on our business; growth of PE Films depends on its ability to develop and deliver new products at competitive prices; the failure of PE Films’ customers, who are subject to cyclical downturns, to achieve success or maintain market share could adversely impact its sales and operating margins; uncertain economic conditions in Brazil could adversely impact the financial condition, results of operations and cash flows of Flexible Packaging Films; and the other factors discussed in the reports Tredegar files with or furnishes to the SEC from time to time, including the risks and important factors set forth in additional detail in “Risk Factors” in Part I, Item 1A of Tredegar’s 2015 Annual Report on Form 10-K/A (the “2015 Form 10-K”) filed with the SEC. Readers are urged to review and consider carefully the disclosures Tredegar makes in its filings with the SEC, including the 2015 Form 10-K. Tredegar does not undertake, and expressly disclaims any duty, to update any forward-looking statement to reflect any change in management’s expectations or any change in conditions, assumptions or circumstances on which such statements are based, except as required by applicable law.

References herein to “Tredegar,” “the Company,” “we,” “us” and “our” are to Tredegar Corporation and its subsidiaries, collectively, unless the context otherwise indicates or requires.

Executive Summary

Tredegar is a manufacturer of polyethylene plastic films through its PE Films segment, polyester films through its Flexible Packaging segment and aluminum extrusions through its Aluminum Extrusions segment. PE Films is comprised of personal care materials, surface protection films, polyethylene overwrap films and films for other markets. Flexible Packaging Films produces polyester-based films for use in packaging applications that have specialized properties, such as heat resistance, strength, barrier protection and the ability to accept high-quality print graphics. Aluminum Extrusions produces high-quality, soft-alloy and medium-strength aluminum extrusions primarily for building and construction, automotive, consumer durables, machinery and equipment, electrical and distribution markets.

Tredegar had historically reported two business segments: Film Products and Aluminum Extrusions. In 2015, the Company divided Film Products into two separate reportable segments: PE Films and Flexible Packaging Films. All historical results for PE Films and Flexible Packaging Films have been separately presented to conform with the new presentation of segments.

First-quarter 2016 net income was $7.3 million ($0.22 per share) compared with net income of $9.9 million (30 cents per share) in the first quarter of 2015. Losses related to plant shutdowns, asset impairments, restructurings and other items are described in Note 2 on page 7. Net sales (sales less freight) and operating profit from ongoing operations are the measures of sales and operating profit used by the chief operating decision maker of each segment for purposes of assessing performance.

20

See the table in Note 9 on page 15 for a presentation of Tredegar’s net sales and operating profit by segment for the three months ended March 31, 2016 and 2015.

PE Films

A summary of operating results from ongoing operations for PE Films is provided below:

Three Months Ended | Favorable/ (Unfavorable) % Change | |||||||||

(In Thousands, Except Percentages) | March 31, | |||||||||

2016 | 2015 | |||||||||

Sales volume (lbs) | 37,886 | 43,046 | (12.0 | )% | ||||||

Net sales | $ | 88,481 | $ | 106,357 | (16.8 | )% | ||||

Operating profit from ongoing operations | $ | 10,235 | $ | 16,832 | (39.2 | )% | ||||

First-Quarter Results vs. Prior Year First Quarter Results

Net sales (sales less freight) in the first quarter of 2016 decreased by $17.9 million versus 2015 primarily due to:

• | The loss of business with PE Films’ largest customer related to various product transitions in personal care materials (approximately $6.0 million); |

• | Additional loss of business for the remaining portion of personal care materials and within polyethylene overwrap films (approximately $5.8 million); |

• | A decline in volume in surface protection films (approximately $2.6 million) that is believed to be the result of lower consumer demand for products with LCD screens in comparison to strong demand in the first quarter of 2015 and resulting in lower capacity utilization and inventory corrections by manufacturers in the supply chain; and |

• | The unfavorable impact from the change in the U.S. dollar value of currencies for operations outside of the U.S. (approximately $2.7 million). |

As noted above, current year sales volume has declined as a result of the wind down of shipments for certain personal care materials due to various previously announced product transitions and business lost, primarily with PE Films’ largest customer. In addition, efforts to consolidate domestic manufacturing facilities in PE Films commenced in the third quarter of 2015 (“North American facility consolidation”). This restructuring project is not expected to be completed until the middle of 2017, and once complete, annual pre-tax cash cost savings are expected to be approximately $5-6 million on cash-related expenditures and exit costs of approximately $17 million. The table below summarizes the pro forma operating profit from ongoing operations for the first quarters of 2016 and 2015, had the impact of the events noted above been fully realized:

Three Months Ended March 31, | ||||||

(In Thousands) | 2016 | 2015 | ||||

Operating profit from ongoing operations, as reported | $ | 10,235 | $ | 16,832 | ||

Contribution to operating profit from ongoing operations associated with product transitions & other losses before restructurings & fixed costs reduction | 1,543 | 4,952 | ||||

Operating profit from ongoing operations net of the impact of business that will be fully eliminated in future periods | 8,692 | 11,880 | ||||

Estimated future benefit of North American facility consolidation | 1,300 | 1,300 | ||||

Pro forma estimated operating profit from ongoing operations | $ | 9,992 | $ | 13,180 | ||

Net sales associated with lost business and product transitions that have yet to be fully eliminated were $4.7 million and $14.3 million in the first quarters of 2016 and 2015, respectively. As previously announced, PE Films anticipates additional exposure to product transitions and lost business in certain personal care materials, and the estimated additional exposure to future operating profit from ongoing operations relating to such is approximately $10 million annually, which would not likely occur until after 2017.

21

Net of the impact of product transitions and business lost, pro forma estimated operating profit from ongoing operations in the first quarter of 2016 decreased by $3.2 million versus the first quarter of 2015. The decrease can be primarily attributed to:

• | The unfavorable lag in the pass-through of average resin costs in the first quarter of 2016 versus in 2015 of $2.0 million; |

• | Lower contribution to profits from surface protection films of $1.3 million, primarily due to lower volume and sales mix changes; and |

• | Higher research and development (“R&D”) expenses of $1.8 million to support new product opportunities offset by lower general, sales and administrative expenses of $1.8 million. |

The competitive dynamics in PE Films require continuous development of new materials through R&D to improve cost and performance for customers. The Company expects total R&D spending in 2016 to be higher than 2015 by approximately $4 million.

Restructuring

On July 7, 2015, the Company announced its intention to consolidate its domestic production for PE Films by restructuring the operations in its manufacturing facility in Lake Zurich, Illinois. Efforts to transition domestic production from the Lake Zurich manufacturing facility will require various machinery upgrades and equipment transfers to its other manufacturing facilities. Given PE Films’ focus on maintaining product quality and customer satisfaction, the Company anticipates that these activities will be completed in the middle of 2017. Total pre-tax cash expenditures associated with restructuring the Lake Zurich manufacturing facility are expected to be approximately $16-17 million over this period, and once complete, annual pre-tax cash cost savings are expected to be approximately $5-6 million.

The Company expects to recognize costs associated with the exit and disposal activities of approximately $5-6 million over the project period. Exit and disposal costs include severance charges and other employee-related expenses arising from the termination of employees of approximately $2-3 million and equipment transfers and other facility consolidation-related costs of approximately $2 million. During the same period of time, operating expenses will include the acceleration of approximately $3 million of non-cash depreciation expense for certain machinery and equipment at the Lake Zurich manufacturing facility. Total expenses associated with the North American facility consolidation project were $1.1 million in the first quarter of 2016 ($0.7 million included in “Asset impairments and costs associated with exit and disposal activities” and $0.4 million included in “Cost of goods sold” in the consolidated statement of income). Total expenses since the inception of the project were $3.3 million.

Total estimated cash expenditures of $16-17 million over the project period include the following:

• | Cash outlays associated with previously discussed exit and disposal expenses of approximately $5 million; |

• | Capital expenditures associated with equipment upgrades at other PE Films manufacturing facilities in the U.S. of approximately $11 million; |

• | Cash incentives of approximately $1 million in connection with meeting safety and quality standards while production ramps down at the Lake Zurich manufacturing facility; and |

• | Additional operating expenses of approximately $1 million associated with customer product qualifications on upgraded and transferred production lines. |

Cash expenditures for the North American facility consolidation project were $2.2 million in the first quarter of 2016, which includes $1.7 million for capital expenditures. Total cash expenditures since the inception of the project were $5.3 million, which includes $4.2 million for capital expenditures.

22

Capital Expenditures, Depreciation & Amortization

Capital expenditures in PE Films were $6.3 million in the first three months of 2016 compared to $4.4 million in the first three months of 2015. PE Films currently estimates that capital expenditures in 2016 will total approximately $35 million, including approximately $10 million for routine capital expenditures required to support operations. Capital spending for strategic projects in 2016 includes expansion of elastics capacity in Europe, expansion of surface protection films capacity in China, the North American facility consolidation and added capacity for the production of a new topsheet for feminine hygiene products. Depreciation expense was $3.4 million in the first three months of 2016 and $4.1 million in the first three months of 2015. Depreciation expense is projected to be approximately $14 million in 2016. Amortization expense was $29,000 in the first three months of 2016 and $40,000 in the first three months of 2015, and is projected to be approximately $0.1 million in 2016.

Flexible Packaging Films

The operations of Flexible Packaging Films, which is also referred to as Terphane, continue to be adversely impacted by competitive pressures that are primarily related to ongoing unfavorable economic conditions in its primary market of Brazil and excess global capacity in the industry. The Company believes that these conditions have shifted the competitive environment from a regional to a global landscape and have driven price convergence and lower product margins for Terphane in Brazil. While recent favorable anti-dumping rulings have been issued against China, Egypt and India, authorities in Brazil have initiated new investigations of dumping against Peru and Bahrain.

A summary of operating results from ongoing operations for Flexible Packaging Films is provided below:

Three Months Ended | Favorable/ (Unfavorable) % Change | |||||||||

(In Thousands, Except Percentages) | March 31, | |||||||||

2016 | 2015 | |||||||||

Sales volume (lbs) | 20,662 | 19,657 | 5.1 | % | ||||||

Net sales | $ | 26,377 | $ | 26,844 | (1.7 | )% | ||||

Operating profit from ongoing operations | $ | 2,032 | $ | 785 | 158.9 | % | ||||

First-Quarter Results vs. Prior Year First Quarter Results

Net sales in the first quarter of 2016 decreased 1.7% versus the first quarter of 2015 primarily due to lower pricing as a result of lower raw material prices partially offset by an increase in volume and a favorable mix.

Operating profit from ongoing operations in the first quarter of 2016 versus the first quarter of 2015 improved by $1.2 million, primarily due to the following:

• | Higher volume ($0.5 million benefit) and operating efficiencies ($0.8 million); |

• | The estimated lag in the pass through of lower raw material costs of $1.0 million in the first quarter of 2016 (none in 2015); |

• | Lower depreciation and amortization costs ($0.5 million benefit) and other costs and expenses ($1.6 million); |

• | Relief from duties on exports to the U.S. beginning in July 2015 as a result of the reinstatement of the GSP program, versus duties paid in the first quarter of 2015 of $0.3 million; and |

• | Foreign currency transaction losses of $1.7 million in the first quarter of 2016 versus foreign currency transaction gains of $1.8 million in the first quarter of 2015, associated with U.S. dollar denominated export sales in Brazil. |

Capital Expenditures, Depreciation & Amortization

Capital expenditures in Flexible Packaging Films were $0.7 million in the first three months of 2016 compared to $0.6 million in the first three months of 2015. Flexible Packaging Films currently estimates that capital expenditures in 2016 will total approximately $5 million, including approximately $3 million for routine capital expenditures required to support operations. Depreciation expense was $1.5 million in the first three months of 2016 and $1.9 million in the first three months of 2015. Depreciation expense is projected to be approximately $6 million in 2016. Amortization expense was $0.7 million in the first three months of 2016 and $0.8 million in the first three months of 2015, and is projected to be approximately $3 million in 2016.

23

Aluminum Extrusions

A summary of operating results from ongoing operations for Aluminum Extrusions is provided below:

Three Months Ended | Favorable/ (Unfavorable) % Change | |||||||||

(In Thousands, Except Percentages) | March 31, | |||||||||

2016 | 2015 | |||||||||

Sales volume (lbs) | 41,468 | 39,454 | 5.1 | % | ||||||

Net sales | $ | 85,474 | $ | 93,645 | (8.7 | )% | ||||

Operating profit from ongoing operations | $ | 7,499 | $ | 5,292 | 41.7 | % | ||||

First-Quarter Results vs. Prior Year First Quarter Results