Attached files

| file | filename |

|---|---|

| EX-32.1 - CERTIFICATION - PEDEVCO CORP | ped_ex321.htm |

| EX-31.1 - CERTIFICATION - PEDEVCO CORP | ped_ex311.htm |

| EX-99.1 - RESERVES REPORT - PEDEVCO CORP | ped_ex991.htm |

| EX-23.2 - CONSENT - PEDEVCO CORP | ped_ex232.htm |

| EX-31.2 - CERTIFICATION - PEDEVCO CORP | ped_ex312.htm |

| EX-21.1 - SUBSIDIARIES - PEDEVCO CORP | ped_ex211.htm |

| EX-32.2 - CERTIFICATION - PEDEVCO CORP | ped_ex322.htm |

| EX-10.75 - AMENDMENT TO VESTING AGREEMENT - PEDEVCO CORP | ped_ex1075.htm |

| EX-23.1 - CONSENT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM - PEDEVCO CORP | ped_ex231.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

þ

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended December 31, 2015

|

o

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from to

Commission file number: 001-35922

PEDEVCO Corp.

(Exact Name of Registrant as Specified in Its Charter)

|

Texas

|

22-3755993

|

|

|

(State or other jurisdiction of incorporation or organization)

|

(IRS Employer Identification No.)

|

4125 Blackhawk Plaza Circle, Suite 201

Danville, California 94506

(Address of Principal Executive Offices)

(855) 733-2685

(Registrant’s Telephone Number,

Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

Common Stock, $0.001 par value per share NYSE MKT

Securities registered pursuant to Section 12(g) of the Act:

None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer

|

o

|

Accelerated filer

|

o

|

|

Non-accelerated filer

|

o

|

Smaller reporting company

|

þ

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No þ

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant as of June 30, 2015 based upon the closing price reported on such date was approximately $16,171,000. Shares of voting stock held by each officer and director and by each person who, as of June 30, 2015, may be deemed to have beneficially owned more than 10% of the outstanding voting stock have been excluded. This determination of affiliate status is not necessarily a conclusive determination of affiliate status for any other purpose.

As of March 25, 2016, 46,986,497 shares of the registrant’s common stock, $0.001 par value per share, were outstanding

Table of Contents

|

Page

|

|||

|

PART I

|

|||

|

Item 1.

|

Business

|

5 | |

|

Item 1A.

|

Risk Factors

|

29 | |

|

Item 1B.

|

Unresolved Staff Comments

|

61 | |

|

Item 2.

|

Properties

|

61 | |

|

Item 3.

|

Legal Proceedings

|

61 | |

|

Item 4.

|

Mine Safety Disclosures

|

61 | |

|

PART II

|

|||

|

Item 5.

|

Market For Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

62 | |

|

Item 6.

|

Selected Financial Data

|

64 | |

|

Item 7.

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

64 | |

|

Item 7A.

|

Quantitative and Qualitative Disclosure About Market Risk

|

74 | |

|

Item 8.

|

Financial Statements and Supplementary Data

|

74 | |

|

Item 9.

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

|

75 | |

|

Item 9A.

|

Controls and Procedures

|

75 | |

|

Item 9B.

|

Other Information

|

76 | |

|

PART III

|

|||

|

Item 10.

|

Directors, Executive Officers and Corporate Governance

|

77 | |

|

Item 11.

|

Executive Compensation

|

83 | |

|

Item 12.

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

|

90 | |

|

Item 13.

|

Certain Relationships and Related Transactions, and Director Independence

|

94 | |

|

Item 14.

|

Principal Accounting Fees and Services

|

98 | |

|

PART IV

|

|||

|

Item 15.

|

Exhibits and Financial Statement Schedules

|

99 | |

2

Forward Looking Statements

ALL STATEMENTS IN THIS DISCUSSION THAT ARE NOT HISTORICAL ARE FORWARD-LOOKING STATEMENTS. STATEMENTS PRECEDED BY, FOLLOWED BY OR THAT OTHERWISE INCLUDE THE WORDS "BELIEVES," "EXPECTS," "ANTICIPATES," "INTENDS,” "PROJECTS," "ESTIMATES,” "PLANS," "MAY INCREASE," "MAY FLUCTUATE" AND SIMILAR EXPRESSIONS OR FUTURE OR CONDITIONAL VERBS SUCH AS "SHOULD", "WOULD", "MAY" AND "COULD" ARE GENERALLY FORWARD-LOOKING IN NATURE AND NOT HISTORICAL FACTS. THESE FORWARD-LOOKING STATEMENTS WERE BASED ON VARIOUS FACTORS AND WERE DERIVED UTILIZING NUMEROUS IMPORTANT ASSUMPTIONS AND OTHER IMPORTANT FACTORS THAT COULD CAUSE ACTUAL RESULTS TO DIFFER MATERIALLY FROM THOSE IN THE FORWARD-LOOKING STATEMENTS. FORWARD-LOOKING STATEMENTS INCLUDE THE INFORMATION CONCERNING OUR FUTURE FINANCIAL PERFORMANCE, BUSINESS STRATEGY, PROJECTED PLANS AND OBJECTIVES. THESE FACTORS INCLUDE, AMONG OTHERS, THE FACTORS SET FORTH BELOW UNDER THE HEADING "RISK FACTORS." ALTHOUGH WE BELIEVE THAT THE EXPECTATIONS REFLECTED IN THE FORWARD-LOOKING STATEMENTS ARE REASONABLE, WE CANNOT GUARANTEE FUTURE RESULTS, LEVELS OF ACTIVITY, PERFORMANCE OR ACHIEVEMENTS. MOST OF THESE FACTORS ARE DIFFICULT TO PREDICT ACCURATELY AND ARE GENERALLY BEYOND OUR CONTROL. WE ARE UNDER NO OBLIGATION TO PUBLICLY UPDATE ANY OF THE FORWARD-LOOKING STATEMENTS TO REFLECT EVENTS OR CIRCUMSTANCES AFTER THE DATE HEREOF OR TO REFLECT THE OCCURRENCE OF UNANTICIPATED EVENTS. READERS ARE CAUTIONED NOT TO PLACE UNDUE RELIANCE ON THESE FORWARD-LOOKING STATEMENTS. REFERENCES IN THIS FORM 10-K, UNLESS ANOTHER DATE IS STATED, ARE TO DECEMBER 31, 2015. AS USED HEREIN, THE “COMPANY,” “WE,” “US,” “OUR” AND WORDS OF SIMILAR MEANING REFER TO PEDEVCO CORP. (D/B/A PACIFIC ENERGY DEVELOPMENT), WHICH WAS KNOWN AS BLAST ENERGY SERVICES, INC. UNTIL JULY 30, 2012, AND ITS WHOLLY-OWNED AND PARTIALLY-OWNED SUBSIDIARIES, BLAST AFJ, INC. PACIFIC ENERGY DEVELOPMENT CORP., CONDOR ENERGY TECHNOLOGY LLC (UNTIL DIVESTED EFFECTIVE JANUARY 1, 2015), WHITE HAWK PETROLEUM, LLC, PACIFIC ENERGY TECHNOLOGY SERVICES, LLC, PACIFIC ENERGY & RARE EARTH LIMITED, BLACKHAWK ENERGY LIMITED, RED HAWK PETROLEUM, LLC, AND PACIFIC ENERGY DEVELOPMENT MSL LLC, WHITE HAWK ENERGY, LLC, AND PEDEVCO ACQUISITION SUBSIDIARY, INC., UNLESS OTHERWISE STATED.

This Annual Report on Form 10-K (this “Annual Report”) may contain forward-looking statements which are subject to a number of risks and uncertainties, many of which are beyond our control. All statements, other than statements of historical fact included in this Annual Report, regarding our strategy, future operations, financial position, estimated revenues and losses, projected costs and cash flows, prospects, plans and objectives of management are forward-looking statements. When used in this Annual Report, the words “could,” “believe,” “anticipate,” “intend,” “estimate,” “expect,” “may,” “should,” “continue,” “predict,” “potential,” “project” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain such identifying words.

Forward-looking statements may include statements about our:

|

●

|

business strategy;

|

|

●

|

reserves;

|

|

●

|

technology;

|

|

●

|

cash flows and liquidity;

|

|

●

|

financial strategy, budget, projections and operating results;

|

|

●

|

oil and natural gas realized prices;

|

|

●

|

timing and amount of future production of oil and natural gas;

|

|

●

|

availability of oil field labor;

|

|

●

|

the amount, nature and timing of capital expenditures, including future exploration and development costs;

|

|

●

|

availability and terms of capital;

|

|

●

|

drilling of wells;

|

|

●

|

government regulation and taxation of the oil and natural gas industry;

|

|

●

|

marketing of oil and natural gas;

|

|

●

|

exploitation projects or property acquisitions;

|

|

●

|

costs of exploiting and developing our properties and conducting other operations;

|

|

●

|

general economic conditions;

|

|

●

|

competition in the oil and natural gas industry;

|

|

●

|

effectiveness of our risk management activities;

|

|

●

|

environmental liabilities;

|

|

●

|

counterparty credit risk;

|

|

●

|

developments in oil-producing and natural gas-producing countries;

|

|

●

|

future operating results;

|

|

●

|

planned combination transaction with GOM Holdings, LLC;

|

|

●

|

estimated future reserves and the present value of such reserves; and plans, objectives, expectations and intentions contained in this Annual Report that are not historical.

|

3

All forward-looking statements speak only at the date of the filing of this Annual Report. The reader should not place undue reliance on these forward-looking statements. Although we believe that our plans, intentions and expectations reflected in or suggested by the forward-looking statements we make in this Annual Report are reasonable, we can give no assurance that these plans, intentions or expectations will be achieved. We disclose important factors that could cause our actual results to differ materially from our expectations under “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and elsewhere in this Annual Report. These cautionary statements qualify all forward-looking statements attributable to us or persons acting on our behalf. We do not undertake any obligation to update or revise publicly any forward-looking statements except as required by law, including the securities laws of the United States and the rules and regulations of the SEC.

Certain abbreviations and oil and gas industry terms used throughout this Annual Report are described and defined in greater detail under “Glossary of Oil and Natural Gas Terms” on page 26, and readers are encouraged to review that section.

Available Information

We are subject to the information and reporting requirements of the Securities Exchange Act of 1934, or the Exchange Act, under which we file periodic reports, proxy and information statements and other information with the United States Securities and Exchange Commission, or SEC. Copies of the reports, proxy statements and other information may be examined without charge at the Public Reference Room of the SEC, 100 F Street, N.E., Room 1580, Washington, D.C. 20549, or on the Internet at http://www.sec.gov. Copies of all or a portion of such materials can be obtained from the Public Reference Room of the SEC upon payment of prescribed fees. Please call the SEC at 1-800-SEC-0330 for further information about the Public Reference Room.

Financial and other information about PEDEVCO Corp. is available on our website (www.pacificenergydevelopment.com). Information on our website is not incorporated by reference into this report. We make available on our website, free of charge, copies of our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after filing such material electronically or otherwise furnishing it to the SEC.

4

PART I

We were originally incorporated in September 2000 as Rocker & Spike Entertainment, Inc. In January 2001 we changed our name to Reconstruction Data Group, Inc., and in April 2003 we changed our name to Verdisys, Inc. and were engaged in the business of providing satellite services to agribusiness. In June 2005, we changed our name to Blast Energy Services, Inc. (“Blast”) to reflect our new focus on the energy services business, and in 2010 we changed the direction of the Company to focus on the acquisition of oil and gas producing properties.

On July 27, 2012, we acquired through a reverse acquisition, Pacific Energy Development Corp., a privately held Nevada corporation, which we refer to as Pacific Energy Development. As described below, pursuant to the acquisition, the shareholders of Pacific Energy Development gained control of approximately 95% of the voting securities of our company. Since the transaction resulted in a change of control, Pacific Energy Development was the acquirer for accounting purposes. In connection with the merger, which we refer to as the Pacific Energy Development merger, Pacific Energy Development became our wholly-owned subsidiary and we changed our name from Blast Energy Services, Inc. to PEDEVCO Corp. Following the merger, we refocused our business plan on the acquisition, exploration, development and production of oil and natural gas resources in the United States, with a primary focus on oil and natural gas shale plays and a secondary focus on conventional oil and natural gas plays.

Business Operations

Overview

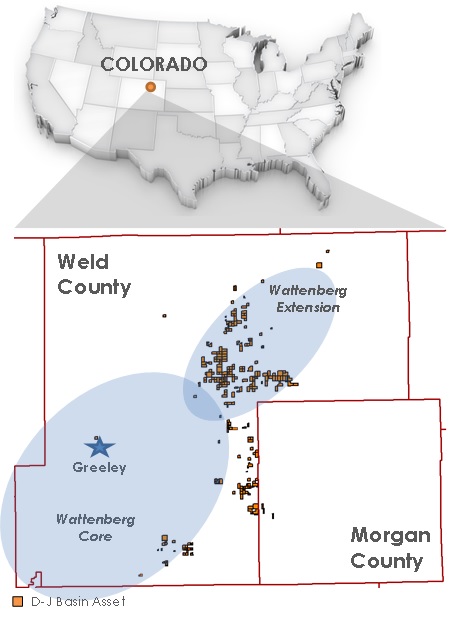

We are an energy company engaged primarily in the acquisition, exploration, development and production of oil and natural gas shale plays in the Denver-Julesberg Basin (“D-J Basin”) in Colorado, which contains hydrocarbon bearing deposits in several formations, including the Niobrara, Codell, Greenhorn, Shannon, J-Sand, and D-Sand. As of December 31, 2015, we held approximately 16,158 net D-J Basin acres located in Weld and Morgan Counties, Colorado through our wholly-owned subsidiary Red Hawk Petroleum, LLC (“Red Hawk”), which acreage is located in the Wattenberg and Wattenberg Extension areas of the D-J Basin, which we refer to as our “D-J Basin Asset.” As of December 31, 2015, we hold interests in 53 gross (15.6 net) wells in our D-J Basin Asset, of which 14 gross (12.5 net) wells are operated by Red Hawk and are currently producing, 17 gross (3.1 net) wells are non-operated, and 22 wells have an after-payout interest. The Company currently produces approximately 357 gross (287 net) barrels of oil equivalent per day (“Boepd”) from our D-J Basin Asset.

5

In February 2015, the Company sold to MIE Jurassic Energy Corp. (“MIEJ”), its then 80% partner in Condor Energy Technology LLC (“Condor”), the Company's (i) 20% interest in Condor, and (ii) approximately 972 net acres and interests in three wells located in the Company’s legacy, non-core Niobrara acreage located in Weld County, Colorado, that were directly held by the Company in Condor-operated wells. The assets sold included working interests in five Condor-operated wells that produced approximately 26 barrels of oil per day, net to the Company's interest, as of February 2015, as well as approximately 2,300 net acres to the Company's interest in non-core Niobrara areas. The Company and MIEJ also agreed to aggregate and restructure all liabilities owed by the Company to MIEJ and Condor, reducing our debt outstanding with MIEJ and Condor from approximately $9.4 million to $4.925 million, revising and extending the terms of the outstanding debt due to MIEJ, and reducing our senior debt by $500,000 through MIEJ’s direct repayment of principal due to our senior lenders. See greater details regarding this transaction below in “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources – Amendment to PEDCO-MIEJ Note and Condor-MIEJ Note.”

Also in February 2015, we expanded our D-J Basin position through the acquisition of additional acreage from Golden Globe Energy (US), LLC (“GGE”), which acquisition we refer to as the GGE Acquisition, which included approximately 12,977 additional net acres in the D-J Basin located almost entirely within Weld County, Colorado, including acreage located in the prolific Wattenberg core area, and interests in 53 gross wells with an estimated then-current net daily production of approximately 500 Boepd as of February 7, 2015. The majority of these assets were originally conveyed to GGE’s predecessor-in-interest, RJ Resources Corp., by us in March 2014 in connection with our acquisition of substantially all of the acreage, well interests and operations of Continental Resources, Inc. located in the D-J Basin (the “Continental Acquisition”), and are now included in our D-J Basin Asset. As partial consideration paid by the Company to GGE in the GGE Acquisition, the Company provided GGE with a one-year option to acquire all of the Company’s interests in Caspian Energy Inc., an Ontario, Canada company listed on the NEX board of the TSX Venture Exchange that holds exploration and production assets in Kazakhstan (“Caspian Energy”), comprised of 23,182,880 shares of common stock of Caspian Energy, for an option exercise price of $100,000. The option provided to GGE was not exercised and has expired.

In May 2015, the Company entered into an Agreement and Plan of Reorganization (as amended to date, the “Reorganization Agreement”) with PEDEVCO Acquisition Subsidiary, Inc., a newly formed wholly-owned subsidiary of the Company (“Exchange Sub”), Dome Energy AB (“Dome AB”), and Dome Energy, Inc. a wholly-owned subsidiary of Dome AB (“Dome US”, and collectively with Dome AB, “Dome Energy”), which contemplated the Company’s acquisition of all of Dome Energy’s U.S. oil and gas assets in exchange for capital stock of the Company. On December 29, 2015, the Company and Dome Energy mutually agreed to terminate the Reorganization Agreement due to the continued downturn in oil prices and the challenging market environment. The Company has no further obligations or termination liabilities due or owing to Dome Energy as a result of the mutual termination.

Immediately following the termination of the Reorganization Agreement, on December 29, 2015, the Company entered into an Agreement and Plan of Reorganization (as amended to date, the “GOM Merger Agreement”) with White Hawk Energy, LLC (“White Hawk”) and GOM Holdings, LLC (“GOM”), a Delaware limited liability company. The GOM Merger Agreement provides for the Company’s acquisition of GOM through an exchange of certain of the shares of the Company’s common and preferred stock (the “Consideration Shares”), as described in greater detail in the Notes, for 100% of the limited liability company membership units of GOM (the “GOM Units”), with the GOM Units being received by White Hawk and GOM receiving the Consideration Shares, as described in greater detail in the Notes from the Company (the “GOM Merger”). On February 29, 2016, the parties entered into an amendment to the GOM Merger Agreement, which amended the merger agreement in order to provide GOM additional time to meet certain closing conditions contemplated by the GOM Merger Agreement. The parties entered into the Amendment to extend the deadline for closing the merger and the date after which either party could terminate the GOM Merger Agreement if the merger had not yet been consummated, from February 29, 2016 to no later than April 15, 2016.

We have listed below the total production volumes and total revenue, net to the Company, for the years ended December 31, 2015, 2014 and 2013 attributable to our D-J Basin Asset, including the calculated production volumes and revenues for our D-J Basin Asset held indirectly through Condor that would be net to our interest if reported on a consolidated basis.

|

For the Years Ended December 31,

|

||||||||||||

|

2015

|

2014(1)

|

2013(1)

|

||||||||||

|

Oil:

|

|

|

|

|||||||||

|

Total Production (Bbls)

|

117,365 | 57,753 | 16,065 | |||||||||

|

Average sales price (per Bbl)

|

$ | 41.13 | $ | 80.06 | $ | 90.30 | ||||||

|

Natural Gas:

|

||||||||||||

|

Total Production (Mcf)

|

343,967 | 94,981 | 13,560 | |||||||||

|

Average sales price (per Mcf)

|

$ | 1.54 | $ | 5.42 | $ | 5.95 | ||||||

|

Oil Equivalents:

|

||||||||||||

|

Total Production (Boe) (2)

|

174,693 | 73,583 | 18,325 | |||||||||

|

Average Daily Production (Boe/d)

|

479 | 202 | 50 | |||||||||

|

Average Production Costs (per Boe)(3)

|

$ | 6.63 | $ | 15.78 | $ | 27.36 | ||||||

_________________________

| (1) | Amounts reflect results for continuing operations and exclude results for discontinued operations related to non-core North Sugar Valley located in Matagorda County, Texas and White Hawk Petroleum, LLC assets located in McMullen County, Texas, sold or held for sale as of December 31, 2014 and 2013. |

| (2) | Assumes 6 Mcf of natural gas equivalents to 1 barrel of oil. |

| (3) | Excludes ad valorem and severance taxes. Represents lease operating expense per Boe using total production volumes of 174,693 Boe, 73,583 Boe, and 18,325 Boe for 2015, 2014 and 2013, respectively. |

6

Business Strategy

We believe that the D-J Basin shale play represents among the most promising unconventional oil and natural gas plays in the U.S. We plan to opportunistically seek additional acreage proximate to our currently held core acreage located in the Wattenberg and Wattenberg Extension areas of Weld County, Colorado. Our strategy is to be the operator, directly or through our subsidiaries and joint ventures, in the majority of our acreage so we can dictate the pace of development in order to execute our business plan. The majority of our capital expenditure budget for the next 12 calendar months will be focused on the development of our D-J Basin Asset. We plan to deploy approximately $35.6 million in capital expenditures in order to drill and complete, participate in the drilling and completion of, and/or acquire approximately 8.5 net wells in our D-J Basin Asset for the period from January 2016 to December 2016. We plan to fund our operations and business plan by utilizing projected cash flow from operations, the approximately $13.5 million gross ($11.0 million net, after origination-related fees and expenses, as further described in Part II, Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations-Liquidity and Capital Resources.”) available under our current senior debt facility, a $25 million debt facility we are seeking to close in April or May 2016, our cash on hand and proceeds from future potential debt and/or equity financings, which may include drilling partnerships. The availability of additional borrowings under the senior debt facility is subject to the Company providing matching funds for all amounts borrowed, which additional borrowed funds may only be used to fund development costs.

During 2015, the Company has focused on growth opportunities, while addressing the expected liquidity requirements arising from a significant decrease in oil and gas prices. The Company had the following significant events:

| ● | Acquired oil and gas assets from GGE, which increased the value of our assets by approximately $45,000,000, and our debt obligations by approximately $9,000,000, essentially doubling our proved reserves and net acreage held. In connection with the acquisition, we issued 3,375,000 shares of restricted common stock and 66,625 shares of Series A Convertible Preferred Stock, which are convertible on a 1,000:1 basis into common stock subject to a 9.9% ownership limitation. | |

| ● | Sold our ownership in Condor and working interests in the related oil and gas assets to MIEJ, recognizing a gain of approximately $275,000 and a net reduction in debt of approximately $2,000,000. | |

| ● | Entered into an agreement to merge with GOM, which, if consummated, is expected to result in significant additional proved reserves production, and provide greater resources to raise capital. | |

| ● | Restructured various debt obligations, to subordinate and defer until note maturity, approximately $4.5 million of principal and interest payments until April 2016, reducing current total cash pay requirements under the notes by approximately $500,000 to zero per month. In connection with the deferral, we issued 3 year warrants to purchase 1.55 million shares of common stock at exercise prices ranging from $0.75 to $1.50 per share. | |

| ● | Implemented general and administrative cost savings strategies (excluding non-cash items) which resulted in reducing annual G&A costs approximately $1,000,000 due to reduced legal fees and lower professional fees. |

Management is continually reviewing the recoverability of its oil and gas assets given the reduction of crude oil and natural gas prices during the year. Over the course of the year, we have identified acreage that we believe has a low probability of development in the near future and have not renewed such leases where appropriate and impaired the values as necessary. We believe that a significant portion of the effects of lower crude oil prices are now being offset by the continuing reduction of drilling and completion, collection, selling and LOE costs. We believe the leases we currently plan to develop in our 2016 development plan continue to be economic due to our estimates of total recoverable reserves, expected production rates and the continued reduction in development and operational costs through this year. The recoverability of our oil and gas assets is dependent on our ability to secure sufficient funds to develop our properties. If we are unable to have access to our credit facilities or alternative financing transactions, and crude oil prices stay at their current prices or go lower or if the new development and operational costs do not hold or such costs return to higher levels, Company management may deem it appropriate in the future to impair certain of our oil and gas properties in the event we determine we will not be able to fully develop our drilling program.

7

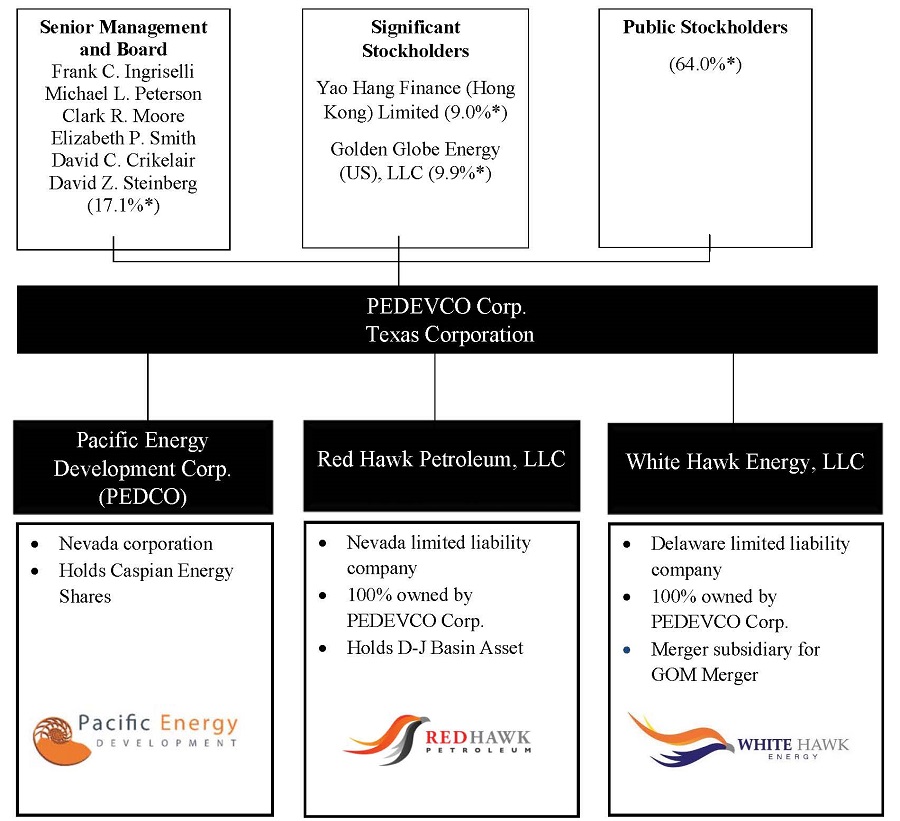

The following chart reflects our current organizational structure:

*Represents percentage of total voting power based on 46,986,497 shares of common stock and 66,625 shares of Series A Convertible Preferred Stock outstanding as of March 25, 2016, with beneficial ownership calculated in accordance with Rule 13d-3 under the Exchange Act. See “Part III, Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters.”

8

Competition

The oil and natural gas industry is highly competitive. We compete and will continue to compete with major and independent oil and natural gas companies for exploration opportunities, acreage and property acquisitions. We also compete for drilling rig contracts and other equipment and labor required to drill, operate and develop our properties. Most of our competitors have substantially greater financial resources, staffs, facilities and other resources than we have. In addition, larger competitors may be able to absorb the burden of any changes in federal, state and local laws and regulations more easily than we can, which would adversely affect our competitive position. These competitors may be able to pay more for drilling rigs or exploratory prospects and productive oil and natural gas properties and may be able to define, evaluate, bid for and purchase a greater number of properties and prospects than we can. Our competitors may also be able to afford to purchase and operate their own drilling rigs.

Our ability to drill and explore for oil and natural gas and to acquire properties will depend upon our ability to conduct operations, to evaluate and select suitable properties and to consummate transactions in this highly competitive environment. Many of our competitors have a longer history of operations than we have, and most of them have also demonstrated the ability to operate through industry cycles.

Competitive Strengths

We believe we are well positioned to successfully execute our business strategies and achieve our business objectives because of the following competitive strengths:

Management. We have assembled a management team at our Company with extensive experience in the fields of international and domestic business development, petroleum engineering, geology, petroleum field development and production, petroleum operations and finance. Several members of the team developed and ran what we believe were successful energy ventures that were commercialized at Texaco, Erin Energy Inc. (formerly CAMAC Energy Inc.), and Rosetta Resources. We believe that our management team is highly qualified to identify, acquire and exploit energy resources in the U.S. and abroad.

Our management team is headed by our Chairman and Chief Executive Officer, Frank C. Ingriselli, an international oil and gas industry veteran with over 37 years of experience in the energy industry, including as the President of Texaco International Operations Inc., President and Chief Executive Officer of Timan Pechora Company, President of Texaco Technology Ventures, and President, Chief Executive Officer and founder of Erin Energy Inc. (formerly CAMAC Energy Inc.). Our management team also includes President and Chief Financial Officer, Michael L. Peterson, who brings extensive experience in the energy, corporate finance and securities sectors, including as a Vice President of Goldman Sachs & Co., Chairman and Chief Executive Officer of Nevo Energy, Inc. (formerly Solargen Energy, Inc.), and a former director of Aemetis, Inc. (formerly AE Biofuels Inc.). In addition, our Executive Vice President and General Counsel, Clark R. Moore, has 10 years of energy industry experience, and formerly served as acting general counsel of Erin Energy Inc. (formerly CAMAC Energy Inc.).

Key Advisors. Our key advisors include South Texas Reservoir Alliance, LLC, which we refer to as STXRA, and other industry veterans. According to STXRA, the STXRA team has experience in drilling and completing horizontal wells, including over 100 horizontal wells with lengths exceeding 4,000 feet from 2010 to 2015, as well as experience in both slick water and hybrid multi-stage hydraulic fracturing technologies and in the operation of shale wells and fields. We believe that our relationship with STXRA, both directly and through our jointly-owned services company, Pacific Energy Technology Services, LLC, will supplement the core competencies of our management team and provide us with petroleum and reservoir engineering, petrophysical, and operational competencies that will help us to evaluate, acquire, develop, and operate petroleum resources into the future.

Significant acreage positions and drilling potential. We have accumulated interests in a total of approximately 16,158 net acres in our core D-J Basin Asset operating area, which we believe represents a significant unconventional resource play. The majority of our interests are in or near areas of considerable activity by both major and independent operators, although such activity may not be indicative of our future operations. Based on our current acreage position, we conservatively estimate there could be up to 202 potential gross drilling locations in our D-J Basin Asset acreage, on which we anticipate drilling and completing, and participating in the drilling and completion of, and/or acquiring approximately 16 additional total wells (equivalent to approximately 8.5 net wells to us) in our D-J Basin Asset through the end of 2016, leaving us a substantial drilling inventory for future years.

9

Marketing

The prices we receive for our oil and natural gas production fluctuate widely. The recent collapse in oil prices is among the most severe on record. The daily NYMEX WTI oil spot price went from a high of $107.62 per Bbl in 2014 to low of $34.73 per Bbl in 2015. The drop in crude oil pricing is due in large part to increased production levels, crude oil inventories and recessed global economic growth. Oil prices are also impacted by real or perceived geopolitical risks in oil producing regions, the relative strength of the U.S. dollar, weather and the global economy. Gas prices have been under downward pressure during 2015 due to excess supply leading to higher levels of gas in storage when compared to the 5-year average. We expect that depressed oil prices will lead to cuts in the exploration and production budgets to reduce incremental oil supply, which should ultimately restore equilibrium to the world oil market and rebalance oil prices. Decreases in these commodity prices adversely affect the carrying value of our proved reserves and our revenues, profitability and cash flows. Short-term disruptions of our oil and natural gas production occur from time to time due to downstream pipeline system failure, capacity issues and scheduled maintenance, as well as maintenance and repairs involving our own well operations. These situations can curtail our production capabilities and ability to maintain a steady source of revenue for our company. In addition, demand for natural gas has historically been seasonal in nature, with peak demand and typically higher prices during the colder winter months. See “Risk Factors” below.

Oil. Our crude oil is generally sold under short-term, extendable and cancellable agreements with unaffiliated purchasers. As a consequence, the prices we receive for crude oil move up and down in direct correlation with the oil market as it reacts to supply and demand factors. Transportation costs related to moving crude oil are also deducted from the price received for crude oil.

We are a party to a 12-month crude oil purchase contract with a third party buyer, pursuant to which the buyer purchases the crude oil produced from our 14 operated wells in our D-J Basin Asset, at a price per barrel equal to the average of the New York Mercantile Exchange’s (NYMEX) daily settle quoted price for Cushing/WTI for trade days only during a calendar month, applicable to product delivered during any such calendar month, less a per barrel differential of $4.75. The crude oil is purchased at the wellhead, and we do not bear any incremental transportation costs.

Natural Gas. Our natural gas is sold under both long-term and short-term natural gas purchase agreements. Natural gas produced by us is sold at various delivery points at or near producing wells to both unaffiliated independent marketing companies and unaffiliated mid-stream companies. We receive proceeds from prices that are based on various pipeline indices less any associated fees for processing, location or transportation differentials.

In connection with our Continental Acquisition in March 2014, we became a party to a Gas Purchase Contract, dated December 1, 2011, with DCP, pursuant to which we have agreed to sell, and DCP has agreed to purchase, all gas produced from six (6) of our D-J Basin Asset operated wells and surrounding lands located in Weld County, Colorado, at a purchase price equal to 83% of the net weighted average value for gas attributable to us that is received by DCP at its facilities sold during the month, less a $0.06/gallon local fractionation fee, for a period of ten years, terminating December 1, 2021.

In connection with our Continental Acquisition in March 2014, we also became a party to a Gas Purchase Agreement, dated April 1, 2012, as amended, with Sterling Energy Investments LLC, which we refer to as Sterling, pursuant to which we have agreed to sell, and Sterling has agreed to purchase, all gas produced from eight (8) of our D-J Basin Asset wells and surrounding lands located in Weld County, Colorado, at a purchase price equal to 85% of the revenue received by Sterling from the sale of gas after processing at Sterling’s plant that is attributable to us during the month, less a $0.50/Mcf gathering fee, subject to escalation, for a period of twenty years, terminating April 1, 2032.

We endeavor to ensure that title to our properties is in accordance with standards generally accepted in the oil and natural gas industry. Some of our acreage may be obtained through farmout agreements, term assignments and other contractual arrangements with third parties, the terms of which often will require the drilling of wells or the undertaking of other exploratory or development activities in order to retain our interests in the acreage. Our title to these contractual interests will be contingent upon our satisfactory fulfillment of these obligations. Our properties are also subject to customary royalty interests, liens incident to financing arrangements, operating agreements, taxes and other burdens that we believe will not materially interfere with the use and operation of or affect the value of these properties. We intend to maintain our leasehold interests by making lease rental payments or by producing wells in paying quantities prior to expiration of various time periods to avoid lease termination.

Oil and Gas Properties

We believe that the Wattenberg and Niobrara Shale plays represent among the most promising unconventional oil and natural gas plays in the U.S. We plan to continue to opportunistically seek additional acreage proximate to our currently held core acreage. Our strategy is to be the operator, directly or through our subsidiaries and joint ventures, in the majority of our acreage so we can dictate the pace of development in order to execute our business plan. The majority of our capital expenditure budget for the period from January 2016 to December 2016 will be focused on the development of these formations. However, if the Company consummates its merger with GOM, the Company will work with GOM to prepare a projected drilling and completion schedule and budget, with the final schedule and budget anticipated to be disclosed by the Company if the GOM Merger is consummated and once they are available, which could impact our current 2016 drilling and completion plans.

10

Unless otherwise noted, the following table presents summary data for our leasehold acreage in our core D-J Basin Asset as of December 31, 2015 and our drilling capital budget with respect to this acreage from January 1, 2016 to December 31, 2016. If commodity prices do not increase significantly, we may delay drilling activities. The ultimate amount of capital we will expend may fluctuate materially based on, among other things, market conditions, commodity prices, asset monetizations, the success of our drilling results as the year progresses, availability of capital and whether we consummate the GOM Merger. In the event the GOM Merger is consummated, the Company plans to expand this development plan to incorporate development of assets held by GOM, with the final schedule and budget anticipated to be disclosed by the Company once they are available.

11

|

Drilling Capital Budget

January 1, 2016 - December 31, 2016

|

||||||||||||||||||||||||

|

Current Core Assets:

|

Net Acres

|

Acre Spacing

|

Potential Gross -Drilling

Locations (1)

|

Net Wells

|

Gross Costs per Well (2)

|

Capital Cost to

the Company (2)

|

||||||||||||||||||

|

D-J Basin Asset

|

16,158 | 80 | 202 | |||||||||||||||||||||

|

Long lateral

|

6.4 | $ | 4,700,000 | $ | 30,080,000 | |||||||||||||||||||

|

Short lateral

|

2.1 | $ | 2,600,000 | $ | 5,557,510 | |||||||||||||||||||

|

Total Assets

|

16,158 | 202 | 8.5 | $ | 35,637,510 | |||||||||||||||||||

|

(1)

|

Potential gross drilling locations are conservatively calculated using 80 acre spacing, and not taking into account additional wells that could be drilled as a result of forced pooling in the Niobrara. Colorado, where the D-J Basin Asset is located, which allows for forced pooling, and which may create more potential gross drilling locations than acre spacing alone would otherwise indicate.

|

|

(2)

|

Costs per well are gross costs while capital costs presented are net to the Company’s working interests.

|

D-J Basin Asset

We directly hold all of our interests in the D-J Basin Asset through our wholly-owned subsidiary, Red Hawk. These interests are located in Weld County, Colorado. Red Hawk is currently the operator of 14 gross (12.5 net) wells located in our D-J Basin Asset. Our D-J Basin Asset acreage is shown in the map below.

Non-Core Assets

We own 23,182,880 shares of common stock of Caspian Energy, a Canadian publicly-traded company, representing approximately 5% of its common stock. Caspian Energy holds a 100% working interest in production and exploration licenses covering an approximate 380,000 acre oil and gas producing asset located in the Pre-Caspian Basin in Kazakhstan. As partial consideration paid by the Company to GGE in the GGE Acquisition, the Company provided GGE with a one-year option to acquire all of the Company’s interests in Caspian Energy for an option exercise price of $100,000. The option provided to GGE was not exercised and has expired, resulting in the retention of the 5% ownership described above.

12

Strategic Alliances

Golden Globe

On March 7, 2014, in connection with the Continental Acquisition, we entered into a $50 million 3-year term debt facility (the “Senior Notes”) with various investors including RJ Credit LLC, a subsidiary of a New York-based investment management group with more than $1 billion in assets under management specializing in resource investments. As part of the transaction, GGE (formerly Golden Globe Energy Corp.) (an affiliate of RJ Credit LLC) acquired an equal 13,995 net acre position in the assets we acquired from Continental (the “GGE Assets”), thereby making GGE an equal working interest partner with us in the development of these newly acquired assets, and allowing us to undertake a more aggressive drilling and development program. On February 23, 2015, we completed the acquisition of the GGE Assets from GGE in the GGE Acquisition, thereby reunifying the assets we originally acquired in the Continental Acquisition, and we assumed approximately $8.35 million of junior subordinated debt from GGE that GGE incurred to develop the GGE Assets subsequent to GGE’s acquisition of them from us in March 2014 and owed to RJ Credit LLC. GGE also currently holds approximately 9.9% of our issued and outstanding common stock, all of our issued and outstanding Series A Convertible Preferred Stock (which is convertible into 66.6 million shares of our common stock, subject to certain restrictions), and has the right to appoint two (2) designees to our Board of Directors, one of which must be an independent director as defined by applicable rules, and one of which directors, David Steinberg, was appointed to the Board of Directors in July 2015, as one GGE’s designees.

STXRA

On October 4, 2012, we established a technical services subsidiary, Pacific Energy Technology Services, LLC, which is 70% owned by us and 30% owned by South Texas Reservoir Alliance, LLC, which we refer to as STXRA, through which we plan to provide acquisition, engineering, and oil drilling and completion technology services in joint cooperation with STXRA in the United States. Pacific Energy Technology Services, LLC currently has no operations, only nominal assets and liabilities and limited capitalization.

STXRA is a consulting firm specializing in the delivery of petroleum resource acquisition services and practical engineering solutions to clients engaged in the acquisition, exploration and development of petroleum resources. In April 2011, we entered into an agreement of joint cooperation with STXRA in an effort to identify suitable energy ventures for acquisition by us, with a focus on plays in shale oil and natural gas bearing regions in the United States. According to information provided by STXRA, the STXRA team has experience in their collective careers of drilling and completing horizontal wells, including over 100 horizontal wells with lengths exceeding 4,000 feet from 2010 to 2015, as well as experience in both slick water and hybrid multi-stage hydraulic fracturing technologies and in the operation of shale wells and fields. We believe that our relationship with STXRA, both directly and through our jointly-owned Pacific Energy Technology Services LLC services company, will supplement the core competencies of our management team and provide us with petroleum and reservoir engineering, petrophysical, and operational competencies that will help us to evaluate, acquire, develop and operate petroleum resources in the future.

Our Core Areas

The majority of our capital expenditure budget for the period from January 2016 to December 2016 will be focused on the development of our core oil and natural gas properties located in the D-J Basin Asset. For additional information, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations-Liquidity and Capital Resources.”

D-J Basin Asset

As a result of the GGE Acquisition and the divestiture of legacy non-core Niobrara assets to MIEJ, as of December 31, 2015 we held 16,158 net acres in oil and natural gas properties related to our D-J Basin Asset. We currently own direct interests in 53 gross (15.6 net) wells in our D-J Basin Asset, of which 14 gross (12.5 net) wells are operated by Red Hawk and currently producing, 17 gross (3.1net) wells are non-operated and 22 wells have an after-payout interest.

We plan to deploy approximately $35.6 million in capital expenditures in order to drill and complete, participate in the drilling and completion of, and/or acquire approximately 8.5 net wells in our D-J Basin Asset for the period from January 2016 to December 2016. We plan to utilize the approximately $23.9 million new drilling facility with the $13.5 million drilling facility provided by GGE, a $25 million debt facility we are seeking to close in April or May 2016, cash on hand, proceeds from future equity offerings, internally generated cash flow, and future debt financings to develop this asset.

Based on publicly available information and information we have received from our oilfield service vendors, average drilling and completion costs for wells in our core area have significantly dropped during 2015 from between $4.3 million and $8.3 million per well in late 2014 and early 2015 to between $2.5 million and $5.0 million per well currently, with these wells having average estimated ultimate recoveries, or EURs, of 300,000 to 850,000 Boe per well and initial 30-day average production of 450 to 850 Boe per day per well in our areas of expected 2016 drilling development. The costs incurred, EURs and initial production rates achieved by others may not be indicative of the well costs we will incur or the results we will achieve from our wells.

13

Our Non-Core Areas

As described above, we hold an approximate 5% interest in Caspian Energy, which holds a 100% working interest in production and exploration licenses covering an approximate 380,000 acre oil and gas producing asset located in the Pre-Caspian Basin in Kazakhstan. In connection with our GGE Acquisition, we provided GGE a one-year option to acquire our interest in Caspian Energy for $100,000, described in greater detail below under “Item 13. Certain Relationships and Related Transactions, and Director Independence– Golden Globe Energy (US), LLC.” The option provided to GGE was not exercised and has expired, resulting in the Company retaining its ownership of the 5% interest in Caspian Energy.

Recent Developments

Debt Restructuring

On April 24, 2015, certain of our investors under our senior secured promissory notes issued to Senior Health Insurance Company of Pennsylvania (as successor-in-interest to BRe BCLIC Primary), BRe BCLIC Sub, BRe WINIC 2013 LTC Primary, BRe WNIC 2013 LTC Sub, HEARTLAND Bank, and RJ Credit LLC (“RJC”) (the “PEDEVCO Senior Loan Investors”), and BAM Administrative Services LLC, as agent for the investors, and any related collateral documents (collectively, the “PEDEVCO Senior Loan”), agreed to defer certain mandatory principal repayments and interest payments that would otherwise be payable by us to them in the months of May and June 2015, with such deferred amounts to be used by us solely to renew, extend, re-lease or otherwise acquire leases which will then become additional collateral under the PEDEVCO Senior Loan. The aggregate principal and interest that was deferred was approximately $524,000, which amount has been capitalized and added to the principal due under the PEDEVCO Senior Loan as of July 31, 2015 and is due upon maturity. The Company was also charged a one-time deferral fee of $354,000 which was added to the principal and due upon maturity. As consideration for the deferral, on September 10, 2015, we granted warrants exercisable for an aggregate of 349,111 shares of our common stock to the Senior Loan Investors with a fair value of approximately $40,000. Each warrant has a 3 year term and is exercisable on a cashless basis at an exercise price of $1.50 per share.

Subject to amendment on January 29, 2016 and March 7, 2016, on August 28, 2015, the Company initially entered into agreements with the holders of the Senior Notes to (i) defer until the maturity date of the Senior Notes the mandatory principal payments that would otherwise be due and payable by the Company on payment dates occurring during the six month period of August 1, 2015 through January 31, 2016, (ii) HEARTLAND Bank agreed to change the frequency of payment of accrued interest and mandatory principal repayments from monthly to semi-annually, with the next interest payment due February 1, 2016 and the next mandatory principal repayment due August 3, 2016, and with the Company agreeing to place an amount equal to 1/6th of the semi-annual principal and interest payments due into a sinking fund which the Company shall pay to HEARTLAND Bank every six months when due and owing, (iii) RJC agreed to defer all interest payments otherwise due and payable by the Company to RJC during the period commencing on August 1, 2015 through January 31, 2016 (the “Waiver Period”), which deferred interest is added to principal each month during the Waiver Period, (iv) certain other owners agreed to (a) defer until the maturity date of their Senior Notes 12/17ths of the interest payments that would otherwise be due and payable by the Company to them on payment dates occurring during the six month period of August 1, 2015 through January 31, 2016; and (b) have the Company pay in cash 5/17ths of such interest payments per month, with all deferred interest being added to principal each month until the maturity date of the Senior Notes, and (v) SHIP, BRe BCLIC Sub, BRe WINIC 2013 LTC Primary, BRe WNIC 2013 LTC Sub and RJC increased the interest rate under their Senior Notes from 15% to 17% per annum on all outstanding principal under the Senior Notes during the Waiver Period. These deferrals agreed upon with Investors (the “August-January Deferrals”) reduced the Company’s monthly cash interest payments and mandatory principal repayments from approximately $600,000 per month prior to these agreements, to approximately $100,000 per month during the Waiver Period after giving effect to the changes agreed upon under these agreements, thereby providing the Company with an estimated $500,000 per month in reduced cash flow requirements during the Waiver Period.

The purpose of these deferrals was to provide the Company with temporary relief from cash requirements to fully-focus and execute upon the contemplated merger with Dome, or another alternative transaction in the event the Company did not consummate the transaction with Dome.

As additional consideration for these agreements and related note amendments and deferrals, on September 10, 2015, the Company issued warrants exercisable on a cash-only basis for an aggregate of 1,201,004 shares of common stock to certain of the deferring Investors, proportionately based on their individual principal with a fair value of approximately $120,000. The warrants have a three year term and are exercisable on a cash-only basis at a price of $0.75 per share. In addition, in the event the aggregate total of principal and interest deferred exceeds $900,000 over the Waiver Period, within thirty days of February 1, 2016, and subject to NYSE MKT additional listing approval, the Company agreed to proportionately grant additional warrants such that the total aggregate number of shares of Company common stock exercisable under all warrants granted shall equal (x) the total principal and interest deferred by such Investors divided by (y) $0.75, provided that such obligations have been extended as discussed below. The Company estimates that up to an aggregate of approximately $4.5 million in total interest and principal payments may be deferred pursuant to these agreements through March 2016, in which event warrants exercisable solely on a cash basis for approximately an additional 4.8 million shares of Company common stock at an exercise price of $0.75 per share will be granted pro rata to the Investors (other than to HEARTLAND Bank) in May 2016. Through March 1, 2016, $4,051,000 of interest has been deferred. As of December 31, 2015, the amount of deferred interest and deferred principal was $2,527,000 and $519,000, respectively. The number of warrant shares to be issued as of December 31, 2015 is approximately 3.1 million. As the warrant value is minimal as of this date, no liability was accrued on the books.

14

In addition, the Company agreed to prepare and deliver to RJC a monthly budget in form and substance reasonably satisfactory to RJC, and such financial statements as RJC may reasonably request. The monthly budget is required to include a cash flow forecast and detail of all anticipated non-recurring expenses and non-cash budget items, and the Company is required to comply with the budgeted expenses set forth therein in all material respects, provided, however, that a variance of less than 10% with respect to the expenses, on an aggregate basis, is permitted.

On January 29, 2016, we entered into a Letter Agreement (the “Letter Agreement”) with the Investors and the Agent. The Letter Agreement extends by one (1) month, through February 29, 2016, the deferral of the payment of interest and principal due under the Notes (the “Deferral Extension”). The purpose of the Deferral Extension is to provide the Company with the financial resources and runaway it believes it needs to fully-focus upon and consummate the merger with GOM. Specifically, pursuant to the Letter Agreement, (i) all Investors agreed to further defer until the maturity date of their Notes the mandatory principal payments that would otherwise be due and payable by the Company to them on payment dates occurring through February 29, 2016, (ii) HEARTLAND Bank agreed to change the next scheduled semi-annual interest payment due from February 1, 2016 to March 1, 2016 (with interest due and payable thereafter on a semi-annual basis) and to change the next mandatory principal repayment due date to September 3, 2016, and the Company agreed to place an amount equal to 1/6th of the semi-annual principal and interest payments due into a sinking fund which the Company shall pay to HEARTLAND Bank every six months when due and owing, and (iii) Senior Health Insurance Company of Pennsylvania (“SHIP”) (as successor-in-interest to BRe BCLIC Primary), BRe BCLIC Sub, BRe WINIC 2013 LTC Primary, BRe WNIC 2013 LTC Sub, and RJC agreed to (a) defer until the maturity date of their Notes and the junior note held by RJC (the “RJC Junior Note”) all of the interest payments that would otherwise be due and payable by the Company to them in February 2016; (b) return the interest rate under each of their Notes to 15% per annum, and the interest rate under the RJC Junior Note to 12% cash pay per annum, effective January 31, 2016; and (c) delay the issuance of any “Subsequent Warrants” issuable pursuant thereto to within 30 days of March 1, 2016, subject to NYSE MKT additional listing approval.

In addition, on the Monday of each week commencing on February 1, 2016 and thereafter, the Company agreed to deliver to the Agent: (a) an accounts receivable and accounts payable listing as of the close of business of the preceding week; (b) collection reports for the preceding week; (c) a compliance report with respect to the Budget which includes a comparison of all categories in the Budget with actual levels of expenditures and revenues generated for the preceding week together with an explanation of all variances from the Budget; and (d) a listing of all the Company’s and its subsidiaries’ (collectively, the “PEDEVCO Group Companies”) checks outstanding as of the end of the preceding week. For purposes of the Letter Agreement, the term, “Budget” means the PEDEVCO Group Companies’ budget for the ten (10) week period covered thereby in a form and substance satisfactory to the Agent, as such Budget may be modified, from time to time so long as such modifications have been agreed to by the Company and the Investors in their reasonable discretion. Furthermore, the Company agreed that at no time shall the PEDEVCO Group Companies’ disbursements exceed by more than 5% those amounts set forth in the Budget, and the Company agreed further to provide to the Agent a copy of (i) any selling memoranda (and any other similar marketing materials) for or relating to the sale of all or any equity or asset of any PEDEVCO Group Company (such sale, a “PEDEVCO Sale”), (ii) any loan memoranda (and any other similar marketing materials) for or relating to the borrowing of money by any PEDEVCO Group Company (such borrowing transaction, an “Additional PEDEVCO Loan”) or (iii) any executed letter of intent, purchase agreement, merger agreement or similar agreement relating to any PEDEVCO Sale or Additional PEDEVCO Loan, in each case within two (2) business days after (x) in the case of preceding clause (i) or (ii), the final preparation thereof or (y) in the case of preceding clause (iii), execution thereof by the parties thereto.

On March 7, 2016, the Company entered into a Letter Agreement, dated March 1, 2016 (the “March Letter Agreement”), with SHIP, BRe BCLIC Sub, BRe WINIC 2013 LTC Primary, BRe WNIC 2013 LTC Sub, and RJC (collectively, the “Original Lenders”), and the Agent, which extends the Deferral Extension by one (1) month, through March 31, 2016. Pursuant to the March Letter Agreement, the Original Lenders agreed to (i) further defer until the maturity date of their Senior Notes the mandatory principal payments that would otherwise be due and payable by the Company to them on payment dates occurring through March 31, 2016, (ii) defer until the maturity date of their Senior Notes and the RJC Junior Note all of the interest payments that would otherwise be due and payable by the Company to them in March 2016, with all interest amounts deferred being added to principal on the first business day of the month following the month in which such deferred interest is accrued; and (iii) delay the issuance of any “Subsequent Warrants” issuable pursuant thereto to within 30 days of April 1, 2016, subject to NYSE MKT additional listing approval.

15

The Company estimates that up to an aggregate of approximately $4.5 million in total interest and principal payments may be deferred pursuant to these agreements through March 2016, in which event warrants exercisable solely on a cash basis for approximately an additional 4.8 million shares of Company common stock at an exercise price of $0.75 per share will be granted pro rata to the Investors (other than to HEARTLAND Bank) in May 2016.

Wellbore Assignments to Dome Energy

On November 19, 2015, the Company entered into a Letter Agreement with Dome Energy pursuant to which Dome Energy agreed to fully fund the Company’s proportionate share of all working interest owner expenses with respect to eight (8) horizontal wells recently drilled and completed by a third party operator in the Wattenberg Area of Weld County, Colorado (the “Wattenberg Wells”). The Company assigned its interests in these Wattenberg Wells to Dome Energy effective November 19, 2015, which wells Dome Energy is now required to fully fund. This transaction was done in contemplation of the Company’s planned combination with Dome Energy (the “Reorganization”) pursuant to that certain Agreement and Plan of Reorganization entered into by and among PEDEVCO Corp., PEDEVCO Acquisition Subsidiary, Inc., Dome AB and Dome US on May 21, 2015, as amended to date (the “Reorganization Agreement”). Upon the closing of which these Wattenberg Wells would have become assets of the combined post-Reorganization company.

In connection with the assignment of these well interests to Dome Energy, Dome Energy has issued a contingent promissory note to the Company, dated November 19, 2015 (the “Dome Promissory Note”), with a principal amount of $250,000, which note is now due and payable by Dome AB to the Company as a result of the December 29, 2015 termination of the Reorganization Agreement. To guarantee prompt payment of the Dome Promissory Note, Dome AB deposited $250,000 into an escrow account.

Termination of Dome Merger

On December 29, 2015, the Company and Dome Energy terminated their pending merger due to the continued downturn in oil prices and the challenging market environment. The Company has no further obligations or termination liabilities due or owing to Dome Energy under the Reorganization Agreement as a result of the mutual termination of the transactions contemplated thereunder.

Entry into Merger Agreement with GOM Holdings, LLC

Immediately following the termination by the Company and Dome Energy of the Plan of Reorganization and the transactions contemplated thereby, on December 29, 2015, the Company entered into the GOM Merger Agreement with White Hawk Energy, LLC, a Delaware limited liability company and wholly-owned subsidiary of the Company (“Merger Sub”), and GOM. The GOM Merger Agreement provides for the Company’s acquisition of GOM through an exchange of certain of the shares of the Company’s common and preferred stock (the “Consideration Shares”), as described in greater detail below, for 100% of the limited liability company membership units of GOM (the “GOM Units”), with the GOM Units being received by Merger Sub and GOM receiving the Consideration Shares, as described in greater detail below from the Company (the “Merger”).

The Company and GOM are currently targeting a closing date (“Closing”) no later than April 15, 2016, subject to various closing conditions as described below and as set forth in greater detail in the GOM Merger Agreement. At the Closing of the Merger, (i) GOM will transfer the GOM Units to Merger Sub, solely in exchange for the Consideration Shares, and (ii) Merger Sub will continue as a wholly-owned subsidiary of the Company and will continue to carry on the business of GOM. In exchange for the transfer of GOM Units to Merger Sub, the Company will issue to the members of GOM, the Consideration Shares as follows: (x) an aggregate of 1,551,552 shares of the Company’s restricted common stock (the “Common Stock”) and 698,448 restricted shares of the Company’s to-be-designated Series B Convertible Preferred Stock (the “Series B Preferred” (described in greater detail below)), and (y) will assume approximately $125 million of subordinated debt from GOM’s existing lenders and a $30 million undrawn letter of credit backing certain offshore asset retirement obligations (the “GOM Debt”), which GOM Debt is anticipated to be restructured on terms and conditions mutually acceptable to the Company and GOM prior to the Closing of the Merger.

At or prior to Closing, we will file and cause to be effective a new Certificate of Designations of PEDEVCO Corp. Establishing the Designations, Preferences, Limitations, and Relative Rights of its Series B Convertible Preferred Stock (the “Certificate of Designation”), which will create 698,448 shares of newly-designated Series B Preferred, all of which will be issued to the members of GOM at Closing pro rata with their ownership of GOM. The Series B Preferred will (i) have a liquidation preference senior to all of the Company’s common stock and Series A Convertible Preferred Stock equal to $250 per share (the “Liquidation Preference”), (ii) accrue an annual dividend equal to 10% of the Liquidation Preference, payable annually from the date of issuance (the “Dividend”), (iii) vote together with the common stock on all shareholder matters, with each share having one (1) vote, and (iv) not be convertible into common stock of the Company until both the Shareholder Approval and NYSE MKT Approval are received (each as defined below). Upon the Company’s receipt of the Shareholder Approval and NYSE MKT Approval, (x) the Series B Preferred will automatically cease accruing Dividends and all accrued and unpaid Dividends will be automatically forfeited and forgiven in their entirety, (y) the Liquidation Preference of the Series B Preferred will be reduced to $0.001 per share from $250 per share, and (z) each share of Series B Preferred will be convertible into common stock on a 1,000:1 basis (the “Series B Conversion”), either (A) automatically upon the determination of the Company’s Board of Directors in its sole discretion (“Company Conversion”), or (B) at the option of the holder at any time (“Holder Conversion”), provided that no Holder Conversion is allowed to the extent the holder thereof would beneficially own more than 9.9% of the Company’s Common Stock or voting stock.

16

The Board of Directors of the Company and the Board of Managers of GOM have adopted and declared advisable the GOM Merger Agreement and the transactions contemplated by the GOM Merger Agreement, including the Merger, upon the terms and subject to the conditions set forth in the GOM Merger Agreement; and the Board of Directors has determined that the GOM Merger Agreement and the transactions contemplated by the GOM Merger Agreement are fair to, and in the best interests of, the Company and its stockholders.

The parties have made customary representations, warranties and covenants in the GOM Merger Agreement including, among others, covenants relating to (1) the conduct of each party’s business during the interim period between the execution of the GOM Merger Agreement and the consummation of the Merger, (2) GOM’s Board of Managers’ and members’ approval of the GOM Merger Agreement and the Merger, and (3) equity grants anticipated to be made to the post-Closing management team by the Company, contingent upon the Equity Plan Increase (described below), which grants will be mutually agreed upon by the Company and GOM prior to Closing. In addition, within 30 days of the Closing, (A) the Company has agreed to use commercially reasonable best efforts to file all the required documents with the SEC necessary to seek shareholder approval (the “Shareholder Approval”) of (i) the issuance of the shares of common stock in connection with the Series B Conversion, (ii) an increase of shares available for issuance under the Company’s 2012 Equity Incentive Plan equal to 12.0% of the Company’s issued and outstanding capital stock (calculated post-Closing, assuming conversion of all Company Series A Preferred and Series B Preferred into Common Stock) (the “Equity Plan Increase”), and (iii) such other matters that are required to be approved by the shareholders of the Company pursuant to applicable rules and requirements of the SEC and NYSE MKT or which in the reasonable determination of the Company, shall be approved by the stockholders of the Company; and (B) the Company agreed to use commercially reasonable best efforts to file all the required documents with the NYSE MKT necessary to obtain NYSE MKT approval of the listing of the Company upon the Series B Conversion (the “NYSE MKT Approval”), if and as necessary pursuant to applicable NYSE MKT rules and regulations. The approval of the shareholders of the Company is not required under applicable law for the closing of the Merger, nor is it a required condition to closing the Merger, and the Company does not intend to seek shareholder approval for the closing of the Merger, only for the Shareholder Approval, after the closing of the Merger, as described above.

The Merger is subject to customary closing conditions, including (1) approval of the agreement by the Board of Directors of the Company, the sole Manager and member of Merger Sub, the Board of Managers of GOM, and the members of GOM, (2) receipt of required regulatory approvals, (3) the absence of any law or order prohibiting the consummation of the Merger, (4) approval of the NYSE MKT for the issuance of the common stock and shares of common stock issuable upon conversion of the Series B Preferred to the members of GOM at Closing, and (5) the effectiveness of the Certificate of Designation. Each party’s obligation to complete the GOM Merger is also subject to certain additional customary conditions, including (a) subject to certain exceptions, the accuracy of the representations and warranties of the other party, (b) performance in all material respects by the other party of its obligations under the GOM Merger Agreement, (c) completion of the restructuring of each of the Company’s and GOM’s existing debt, respectively, to the other party’s satisfaction, and (d) each of the Company and GOM furnishing the other with evidence that each has entered into amended employment agreements with certain of each party’s employees as required and in forms acceptable to the other party. In addition, each of the Company and GOM agreed to pay all costs and expenses incurred by them in connection with the GOM Merger Agreement.

The GOM Merger Agreement also includes customary termination provisions for both the Company and GOM. Specifically, and subject to the terms of the GOM Merger Agreement, the agreement can be terminated by either party in the event the Closing has not occurred by April 15, 2016, or if any representation or warranty of the other party contained in the GOM Merger Agreement shall not be true in all material respects, subject to a right to cure by the breaching party.

The parties intend, for U.S. federal income tax purposes, that the Merger will qualify as a “reorganization” within the meaning of Section 368(a) of the Internal Revenue Code of 1986.

GOM is majority owned and controlled by Platinum Partners, an affiliate of Platinum Management (NY) LLC (“PM LLC”), a New York based investment firm which is the employer of Mr. David Z. Steinberg, who serves as one of the members of the Company’s Board of Directors. PM LLC is also an advisor to the entity which owns RJ Credit LLC (“RJC”), who has loaned the Company approximately $5.9 million to date in principal in connection with the Company’s March 2014 senior note funding. In connection with the March 2014 funding the Company also has the right, from time to time, subject to the terms and conditions of the Note Purchase Agreement relating to the March 2014 senior funding, to request additional loans from RJC, of up to an additional $13.5 million in funding.

17

PM LLC is also an advisor to the entity that owns GGE, a greater than 5% stockholder of the Company, from whom the Company acquired approximately 12,977 net acres of oil and gas properties and interests in 53 gross wells located in the Denver-Julesburg Basin, Colorado in February 2015, in connection with which the Company assumed approximately $8.35 million of subordinated notes payable owed by GGE to RJC, issued to GGE 3,375,000 restricted shares of the Company’s common stock (representing approximately 9.9% of our then outstanding shares of common stock), and issued to GGE 66,625 restricted shares of the Company’s then newly-designated Amended and Restated Series A Convertible Preferred Stock (the “Series A Preferred”), which can be converted into shares of the Company’s common stock on a 1,000:1 basis, subject to a 9.9% ownership blocker. GGE, as the sole holder of the Company’s Series A Preferred, has the right to appoint two designees to the Company’s Board of Directors for as long as GGE continues to hold 15,000 shares of Series A Preferred designated as “Tranche One Shares” under the Company’s Amended and Restated Certificate of Designations of PEDEVCO Corp. Establishing the Designations, Preferences, Limitations, and Relative Rights of its Series A Convertible Preferred Stock. Mr. Steinberg is one of the Series A Preferred shareholder designees to the Board of Directors in connection with such right, provided that GGE has not designated any further members of the Board of Directors at this time.

Vesting Agreements

In connection with the Company’s entry into the GOM Merger Agreement, on December 29, 2015, as amended on January 6, 2016, each of Messrs. Ingriselli, Peterson and Moore entered into Vesting Agreements with the Company (as amended, the “Vesting Agreements”), pursuant to which they each individually agreed that the future vesting of restricted common stock held by such officers from January 1, 2016 through June 1, 2016 (the “Delay Period”), including all restricted common stock that was subject to vesting on January 7, 2016 pursuant to the terms of prior vesting agreements entered into by such officers on May 21, 2015, shall be delayed until the 2nd trading day following the Company’s public announcement of the “Vesting Event,” defined as the later to occur of the receipt of (x) the Shareholder Approval and (y) the NYSE MKT Approval, upon which Vesting Event all vesting with respect to such shares shall be accelerated and all such shares shall be fully vested (the “Acceleration”). The aggregate number of shares of restricted common stock subject to the Delay Period is 1,354,000 shares, 519,000 of which are held by Mr. Ingriselli, 481,000 of which are held by Mr. Peterson, and 354,000 of which are held by Mr. Moore (collectively, the “Subject Shares”). The Acceleration will occur even if the executives are not then employees or directors of the Company on such date. Notwithstanding the above, in the event the GOM Merger Agreement is terminated or the Merger is not consummated by June 1, 2016 (unless otherwise agreed upon in writing by the parties to the GOM Merger Agreement), all the Subject Shares will vest on the 2nd trading day following the Company’s public disclosure of the termination of the Merger (in the event the GOM Merger Agreement is terminated prior to June 1, 2016), or, in the event the Merger is not terminated by, or consummated by, June 1, 2016, on June 1, 2016, and the original vesting terms for all future unvested stock will be reinstated to the terms in effect prior to the parties’ entry into the Vesting Agreements. Notwithstanding the above, nothing in the Vesting Agreements amends or waives any acceleration of vesting of unvested restricted stock or options currently provided under any executive officer’s current employment agreement with the Company, which provides for acceleration upon termination of such executive’s employment under certain circumstances detailed therein.

Amendment to the 2012 Equity Incentive Plan

At the Company’s Annual Meeting of Stockholders held on October 7, 2015 (the “Annual Meeting”), the Company’s stockholders approved an amendment to the Company’s 2012 Equity Incentive Plan (the “Plan”) to increase by 3,000,000, the number of shares of common stock reserved for issuance under the Plan to a total of 10,000,000 shares.

Approval of Conversion Rights of Series A Preferred Stock