Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - HOME BANCORP, INC. | v419939_8k.htm |

Exhibit 99.1

September 9, 2015 Raymond James 2015 U.S. Bank Conference

Forward Looking Statements Certain comments in this presentation contain certain forward looking statements (as defined in the Securities Exchange Act of 1934 and the regulations hereunder). Forward looking statements are not historical facts but instead represent only the beliefs, expectations or opinions of Home Bancorp, Inc. and its management regarding future events, many of which, by their nature, are inherently uncertain. Forward looking statements may be identified by the use of such words as: “believe”, “expect”, “anticipate”, “intend”, “plan”, “estimate”, or words of similar meaning, or future or conditional terms such as “wi ll” , “would”, “should”, “could”, “may”, “likely”, “probably”, or “possibly.” Forward looking statements include, but are not limit ed to, financial projections and estimates and their underlying assumptions; statements regarding plans, objectives and expectations with respect to future operations, products and services; and statements regarding future performance. Such statements are subject to certain risks, uncertainties and assumption, many of which are difficult to predict and generally a re beyond the control of Home Bancorp, Inc. and its management, that could cause actual results to differ materially from those expressed in, or implied or projected by, forward looking statements. The following factors, among others, could cause actual results to differ materially from the anticipated results or other expectations expressed in the forward looking statements: (1) economic and competitive conditions which could affect the volume of loan originations, deposit flows and real estate values; (2) the levels of non - interest income and expense and the amount of loan losses; (3) competitive pressure among depository institutions increasing significantly; (4) changes in the interest rate environment causing reduced interest margins; (5) gen era l economic conditions, either nationally or in the markets in which Home Bancorp, Inc. is or will be doing business, being less favorable than expected; (6) political and social unrest, including acts of war or terrorism ; (7) legislation or changes in regulatory requirements adversely affecting the business in which Home Bancorp, Inc. is engaged. Home Bancorp, Inc. undertakes no obligation to update these forward looking statements to reflect events or circumstances that occur after the date on which such statements were made; (8) the possibility that the proposed merger with Louisiana Bancorp, Inc. does not close when expected or at all because all conditions to closing are not received or satisfied on a timely basis or at all; (9 ) t he terms of the proposed merger may need to be modified to satisfy such conditions; (10) the anticipated benefits from the proposed merger are not realized in the time frame anticipated or at all as a result of changes in general economic and marke t conditions, interest rates, laws and regulations and their enforcement, and the degree of competition in our markets; (11) th e ability to promptly and effectively integrate the businesses of the companies; (12) the reaction of the companies’ customers to the merger, or (13) diversion of management time on merger - related issues . As used in this report, unless the context otherwise requires, the terms “we,” “our,” “us,” or the “Company” refer to Home Bancorp, Inc. and the term the “Bank” refers to Home Bank, a nationally chartered bank and wholly owned subsidiary of the Company. In addition, unless the context otherwise requires, references to the operations of the Company include the operations of the Bank. For a more detailed description of the factors that may affect Home Bancorp’s operating results or the outcomes described in these forward - looking statements, we refer you to our filings with the Securities and Exchange Commission, including our annual report on Form 10 - K for the year ended December 31, 2014. Home Bancorp assumes no obligation to update the forward - looking statements made during this presentation. For more information, please visit our website www.home24bank.com. 2

Our Company 3 • Headquartered in Lafayette, Louisiana – Bank founded in 1908 • National Bank Charter – Bank converted from Federal Savings Bank in 2015 • IPO completed in October 2008 • Ticker symbol: HBCP (NASDAQ Global) • Market Cap = $179 MM • Assets = $1.2 billion as of June 30, 2015 • Acquisition of Louisiana Bancorp (LABC) pending; closing date approaches

Significant Asset Growth Since IPO 4 200% asset increase CAGR = 17.6%* Statewide Bank • March 2010 • FDIC - a ssisted • Assets - $199MM Guaranty Savings Bank • July 2011 • Assets - $257MM • Cash @ 95% of book Britton & Koontz Bank • February 2014 • Assets - $301MM • Cash @ 88% of book Louisiana Bancorp • Assets - $348MM as of 6/30/2015 • Cash @ 126% of book *Asset growth after close of LABC acquisition is based on assets as of June 30, 2015

Favorable Balance Sheet Mix Change (% of assets) 5 2008 2009 2010 2011 2012 2013 2014 2Q 2015 Cash & Equivalents 9% 5% 6% 4% 4% 4% 3 % 3 % Investments 22% 23% 18% 16% 17% 16% 15% 15% Total Loans, net 63% 64% 63% 69% 70% 71% 74% 74% Other Assets 6% 8% 13% 11% 9% 9% 8% 8% Non Maturity Deposits 38% 41% 47% 46% 54% 56% 63% 66% CDs 29% 30% 32% 30% 26% 19% 18% 17% Borrowings & Other Liabilities 9% 4% 2% 10% 5% 10% 6% 4% Shareholders’ Equity 24% 25% 19% 14% 15% 14% 13% 13% • Strong organic loan growth • Relatively small investment portfolio • Core deposit growth has offset capital deployment

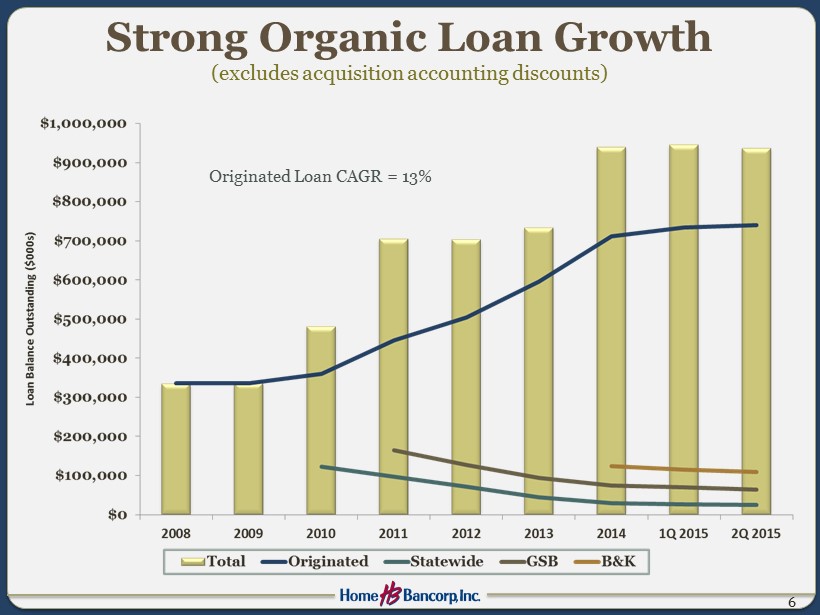

Strong Organic Loan Growth (excludes acquisition accounting discounts ) Originated Loan CAGR = 13% 6

7 In 2008, virtually 100% of Home Bank loans and deposits were located in Lafayette Market. Market Diversification as of June 30, 2015 Loans Deposits

Limited Direct Energy Exposure as of August 31, 2015 8 C&D $882 $0 $882 C&I 17,367 9,933 27,300 CRE 15,754 252 16,007 Total Balance $34,003 $10,185 $44,189 % of Total Loans 3.7% 1.1% 4.8% Average Loan Balance ($000s) $365 CRE - Average LTV 43% Substandard Loan Balance ($000s) $2,560 Outstanding Balance Unfunded Commitments Total Exposure Balance in ($000s)

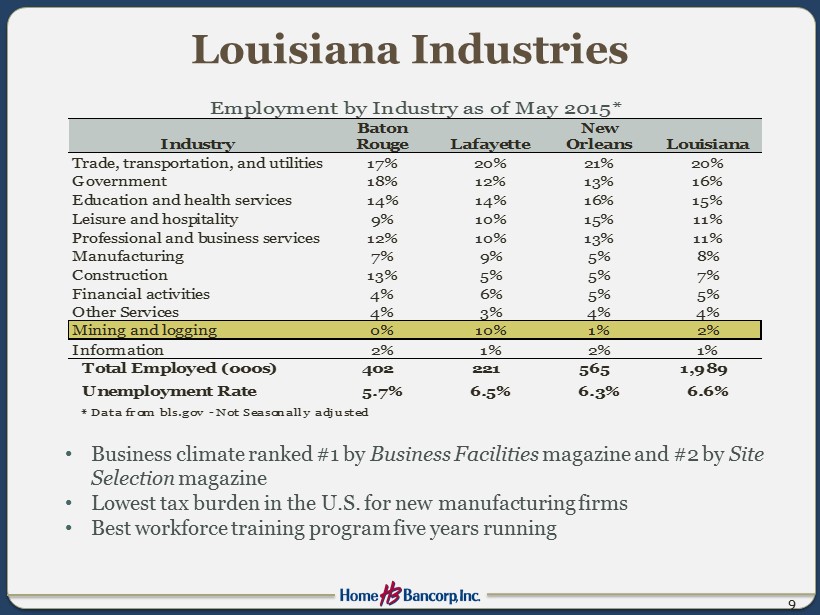

Louisiana Industries 9 • Business climate ranked #1 by Business Facilities magazine and #2 by Site Selection magazine • Lowest tax burden in the U.S. for new manufacturing firms • Best workforce training program five years running Trade, transportation, and utilities 17% 20% 21% 20% Government 18% 12% 13% 16% Education and health services 14% 14% 16% 15% Leisure and hospitality 9% 10% 15% 11% Professional and business services 12% 10% 13% 11% Manufacturing 7% 9% 5% 8% Construction 13% 5% 5% 7% Financial activities 4% 6% 5% 5% Other Services 4% 3% 4% 4% Mining and logging 0% 10% 1% 2% Information 2% 1% 2% 1% Total Employed (000s) 402 221 565 1,989 Unemployment Rate 5.7% 6.5% 6.3% 6.6% * Data from bls.gov - Not Seasonally adjusted Employment by Industry as of May 2015* Baton Rouge Lafayette New Orleans LouisianaIndustry

Loan Portfolio Composition as of June 30, 2015 10 B alance: $916 million Pro Forma estimate after close of LABC: $1.2 billion

Commercial Real Estate Portfolio as of June 30, 2015 11 Balance: $341 million

C&I Portfolio as of June 30, 2015 12 Balance: $115 million

Construction and Land Portfolio as of June 30, 2015 13 Balance: $94 million

1 - 4 Family First Mortgage Portfolio as of June 30, 2015 • Decline in overall loan composition since 2008 – 41% in 2008 – 26% in 2Q 2015 • Limited exposure to 30 year fixed - rate mortgages – $59MM, or 6%, of total loans as of 2 Q 2015 • Approximately 95% of LABC’s mortgages mature/reprice < 15 years (source: snl.com) 14 B alance: $233 million

Non Performing Assets / Assets • Originated NPAs historically low • Aggressively reducing acquired NPAs • Credit discounts on acquired loans • Excellent credit at LABC: 0.43% NPAs/Assets as of June 30, 2015 (source: snl.com) 15 Peer = BHCs $1 - $3 billion in assets. Peer data as of 3/31/2015. Source: ffiec.gov

16 Net Charge Offs / Average Loans • Credit discounts on acquired loans offset losses • Acquired loans performing better than anticipated since acquisition Low Net Charge Offs on Acquired Loans

• Credit coverage on acquired loans = 11.4% of outstanding balance 17 Credit Coverage as of June 30, 2015

• $193 MM, or 16% of Assets • 2.6 Year Effective Duration • 2.13% TE Yield in 2 nd Q 2015 • 22% of investments are variable rate 18 Investment Portfolio as of June 30, 2015 Current +100 +200 +300 Market Value / Book 0.9% -3.0% -6.1% -9.3% Avg Life / Reprice Term 3.1 3.5 3.8 4.1 Avg Life 4.0 4.5 4.8 5.2

Deposit Growth and Composition 19 • Favorable mix change while growing total deposits • 2Q 2015 cost on interest - bearing deposits = 0.37 % • 75 th percentile in non interest deposits / deposits • No non - relationship brokered deposits 2008 2Q 2015 Change DDA 19% 26% 7% MMDA 19% 24% 5% NOW 12% 21% 9% CD 44% 21% -23% Savings 6% 8% 2% Deposit Composition

Interest Rate Risk as of June 30, 2015 Change in Interest Rates (1) % Change in NII at 6/30/15 (2) +100 0.1% +200 - 0.1% +300 - 0.4% 20 1) Assumes an instantaneous and parallel shift in interest rates. 2) The actual impact of changes in interest rates will depend on many factors including but not limited to: the Company’s ability to maintain desired mix of interest - earning assets and interest - bearing liabilities, actual timing of asset and liability repricing , and competitor reaction to deposit and loan pricing. • Asset neutral • Low beta deposit growth

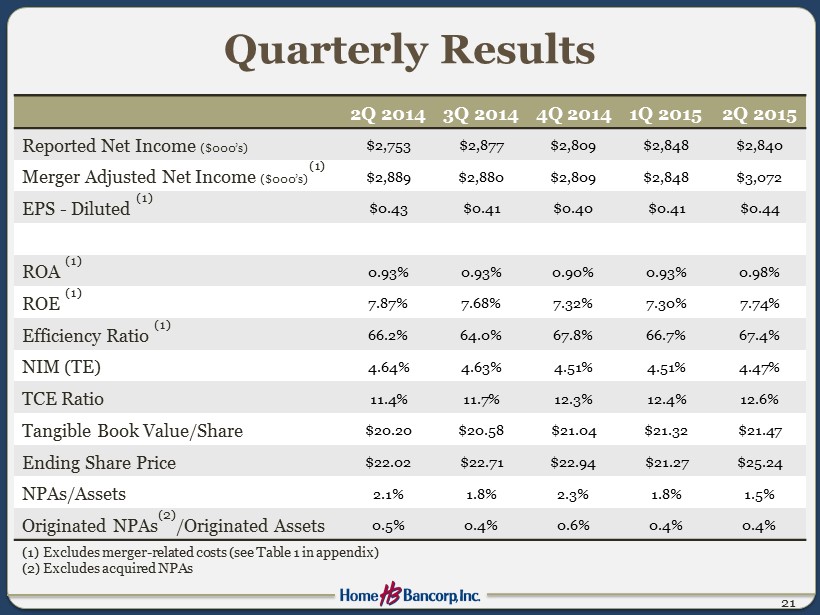

Quarterly Results 21 2Q 2014 3Q 2014 4Q 2014 1Q 2015 2Q 2015 Reported Net Income ($000’s) $ 2,753 $ 2,877 $2,809 $2,848 $2,840 Merger Adjusted Net Income ($000’s) (1) $ 2,889 $ 2,880 $2,809 $2,848 $3,072 EPS - Diluted (1) $ 0.43 $ 0.41 $0.40 $0.41 $0.44 ROA (1) 0.93% 0.93% 0.90% 0.93% 0.98% ROE (1) 7.87% 7.68% 7.32% 7.30% 7.74% Efficiency Ratio (1) 66.2% 64.0% 67.8% 66.7% 67.4% NIM (TE) 4.64% 4.63% 4.51% 4.51% 4.47% TCE Ratio 11.4% 11.7% 12.3% 12.4% 12.6% Tangible Book Value/Share $20.20 $20.58 $21.04 $21.32 $21.47 Ending Share Price $22.02 $22.71 $22.94 $21.27 $25.24 NPAs/Assets 2.1% 1.8% 2.3% 1.8% 1.5% Originated NPAs (2) /Originated Assets 0.5% 0.4% 0.6% 0.4% 0.4% (1) Excludes merger - related costs (see Table 1 in appendix) (2) Excludes acquired NPAs

Net Interest Margin (TE) 22 Outperformed peers by 92 basis points Peer = BHCs $1 - $3 billion in assets. Peer data as of 3/31/2015. Source: ffiec.gov

Net Interest Margin Drivers • Favorable asset mix – Loans = 74% of assets (74 th percentile) – Investments = 15% of assets (33 rd percentile) • Loan yield of 5.44% in 2015 (89 th percentile) – Loan discount accretion – Higher concentration in construction loans 23 • Maintained lower costs than peers even after capital was deployed • Favorable funding mix – Strong non interest deposit growth, 22% of assets (73 rd percentile) – Reduced CD funding 80 basis point spread 11 basis point spread

Non - Interest Income • New Retail and Mortgage leadership in 2014 • Restructured commercial and retail incentive plans to focus on new account acquisition 24 6/30/2015 YTD Composition Lagged peers by 17 basis points

Non - Interest Expense • Infrastructure for continued growth • Investments in commercial bankers across footprint • Considerable efficiencies gained in 2014 from B&K acquisition • Expect significant cost saves of 55% in LABC acquisition 25 6/30/2015 YTD Composition (1) Lagged peers by 28 basis points (1) Excludes merger - related costs (see Table 2 in appendix)

HBCP Ownership 26 Source: SNL (as reported through 8/27/2015) Top Institutional Holders Ownership % Firefly Value Partners LP 8.1% FJ Capital Management LLC 7.7% Jacobs Asset Management LLC 6.9% Fully Diluted Insider Ownership = 27%

Total Return Since 2008 27 Source: SNL. Data as of 09/2/2015

Share Information 28 3Q 2014 4Q 2014 1Q 2015 2Q 2015 12 Months EPS – GAAP $0.41 $0.40 $0.41 $0.41 $1.63 EPS – Merger Adjusted (1) $0.41 $0.40 $0.41 $0.44 $1.66 Ending Share Price $22.71 $22.94 $21.27 $25.24 Dividend Yield 0.0% 1.2% 1.3% 1.3% P/ BV 107% 106% 97% 115% P/TBV 110% 109% 100% 118% Home Bancorp Price / Earnings Share price as of 9/2/2015 $24.80 2016 average analyst earnings estimate $2.37 P/E based on 2016 average estimates 10.5x (1) Excludes merger - related costs (see Table 1 in appendix) Peer Median Pricing: $1 - $3 billion in assets (as of 9/2/2015) P/TBV 132% P/EPS 14.5x

Tangible Common Equity Ratio 29 * Based on preliminary estimate of HBCP management

Capital Deployment Strategy • Acquisitions – Prior acquisitions (including LABC) have been cash transactions • Immediate ROE and EPS Impact (excluding merger costs) 30 2 nd Quarter Profitability Core ROA (1)(2) 1.02% TCE Leverage Multiplier 8.08 ROATCE 8.23% Leverage Impact of LABC 1.02% 10.42 10.62% Maintain Core ROA for illustration purposes Based on preliminary estimates of HBCP management of a 9.6% TCE Ratio at close Leverage increase boosts ROATCE 29% (1) Excludes merger - related costs (see Table 1 in appendix) (2) Adds back intangible asset amortization expense, tax effected ($173,000 *.65)

Capital Deployment Strategy • Organic Loan Growth • Cash Dividends – Announced company’s first dividend ($0.07/share) in 4 th Q 2014 – Raised dividend to $0.08/share in 3 rd Q 2015 • Share Repurchases (22% of IPO shares repurchased) – Buyback plan has approx. 38,000 shares remaining 31

Investment Perspective • Consistently superior organic asset quality • Deep customer relationships – 108 years • EPS - focused acquirer; experienced deal team • Strong capital base – Disciplined deployment – Well positioned for further acquisitions • Low direct energy exposure • Low trading multiple based on 2016 P/E estimate of 10.5x 32

Executive Leadership 33 Jason Freyou, Chief Operations Officer Joined Home Bank in 2015. Previously served as Chief Operations Officer for Teche Federal Bank. Darren Guidry, Chief Credit Officer Joined Home Bank in 1993. Previously served as Chief Lending Officer. Scott Ridley, Chief Banking Officer Joined Home Bank in 2013. Previously served as Group Executive for Louisiana Business Banking for Capital One Bank. Joseph Zanco, Chief Financial Officer Joined Home Bank in 2008. Previously served as Corporate Controller and Principal Accounting Officer for Iberiabank . John Bordelon, President and Chief Executive Officer Has led Home Bank since 1993. Previously served in various management and other positions since joining the Bank in 1981 . Former Chairman of the following organizations: Greater Lafayette Chamber of Commerce , University of Louisiana Alumni Association, Community Bankers of Louisiana, and Ragin Cajun Athletic Foundation

Appendix Non - GAAP Reconciliation 34 (dollars in thousands) 2010 2011 2012 2013 2014 2015 Reported non-interest expense 24,373$ 31,002$ 32,763$ 33,205$ 41,772$ 19,947$ Less: Merger-related expenses (1,000) (2,053) - (307) (2,286) (256) Non-GAAP noninterest expense 23,373$ 28,949$ 32,763$ 32,898$ 39,486$ 19,691$ TABLE 2 (dollars in thousands) 1Q 2014 2Q 2014 3Q 2014 4Q 2014 1Q 2015 2Q 2015 Reported non-interest expense 11,257$ 10,370$ 9,968$ 10,176$ 9,719$ 10,228$ Less: Merger-related expenses (1,955) (207) (124) - - (256) Non-GAAP non-interest expense 9,302$ 10,163$ 9,844$ 10,176$ 9,719$ 9,972$ Reported Net Income 1,433 2,753 2,877 2,809 2,848 2,840 Add: Merger-related expenses (after tax) 1,357 136 4 - - 232 Non-GAAP Net Income 2,790 2,889 2,881 2,809 2,848 3,072 Diluted EPS 0.21$ 0.40$ 0.41$ 0.40$ 0.41$ 0.41$ Add: Merger-related expenses 0.19 0.03 - - - 0.03 Non-GAAP EPS 0.40$ 0.43$ 0.41$ 0.40$ 0.41$ 0.44$ TABLE 1