Attached files

| file | filename |

|---|---|

| 8-K - 8-K - Genesis Healthcare, Inc. | a15-16217_18k.htm |

| EX-23.1 - EX-23.1 - Genesis Healthcare, Inc. | a15-16217_1ex23d1.htm |

| EX-99.2 - EX-99.2 - Genesis Healthcare, Inc. | a15-16217_1ex99d2.htm |

| EX-23.2 - EX-23.2 - Genesis Healthcare, Inc. | a15-16217_1ex23d2.htm |

Exhibit 99.1

FC-GEN Operations Investment, LLC and Subsidiaries

Consolidated Financial Statements

December 31, 2014

Index to Consolidated Financial Statements

|

|

Page |

|

|

|

|

Report of Independent Registered Public Accounting Firm |

2 |

|

|

|

|

Consolidated Balance Sheets as of December 31, 2014 and 2013 |

3 |

|

|

|

|

Consolidated Statements of Operations for the years ended December 31, 2014, 2013 and 2012 |

4 |

|

|

|

|

Consolidated Statements of Comprehensive Income (Loss) for the years ended December 31, 2014, 2013 and 2012 |

5 |

|

|

|

|

Consolidated Statements of Stockholders’ Equity (Deficit) for the years ended December 31, 2014, 2013 and 2012 |

6 |

|

|

|

|

Consolidated Statements of Cash Flows for the years ended December 31, 2014, 2013 and 2012 |

7 |

|

|

|

|

Notes to Consolidated Financial Statements |

8 |

|

|

|

|

Quarterly Consolidated Financial Statements (Unaudited) |

39 |

|

|

|

|

Schedule II — Valuation and Qualifying Accounts |

40 |

|

|

|

|

Selected Financial Data |

41 |

|

|

|

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

42 |

Report of Independent Registered Public Accounting Firm

The Board of Directors and Stockholders

Genesis Healthcare, Inc.:

We have audited the accompanying consolidated balance sheets of FC-GEN Operations Investment, LLC and subsidiaries (the Company) as of December 31, 2014 and 2013, and the related consolidated statements of operations, comprehensive income (loss), stockholders’ equity (deficit), and cash flows for each of the years in the three-year period ended December 31, 2014. In connection with our audits of the consolidated financial statements, we also have audited financial statement schedule “Schedule II. Valuation and Qualifying Accounts.” These consolidated financial statements and financial statement schedule are the responsibility of the Company’s management. Our responsibility is to express an opinion on these consolidated financial statements and financial statement schedule based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of FC-GEN Operations Investment, LLC and subsidiaries as of December 31, 2014 and 2013, and the results of their operations and their cash flows for each of the years in the three-year period ended December 31, 2014, in conformity with U.S. generally accepted accounting principles. Also in our opinion, the related financial statement schedule, when considered in relation to the basic consolidated financial statements taken as a whole, presents fairly, in all material respects, the information set forth therein.

|

|

/s/ KPMG LLP |

|

|

|

|

Philadelphia, Pennsylvania |

|

|

July 24, 2015 |

|

FC-GEN OPERATIONS INVESTMENT, LLC AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

(IN THOUSANDS, EXCEPT SHARE AND PER SHARE DATA)

|

|

|

December 31, 2014 |

|

December 31, 2013 |

| ||

|

|

|

|

|

|

| ||

|

Assets: |

|

|

|

|

| ||

|

Current assets: |

|

|

|

|

| ||

|

Cash and equivalents |

|

$ |

87,548 |

|

$ |

61,413 |

|

|

Restricted cash and investments in marketable securities |

|

38,211 |

|

72,930 |

| ||

|

Accounts receivable, net of allowances for doubtful accounts of $133,530 in 2014 and $106,093 in 2013 |

|

605,830 |

|

659,164 |

| ||

|

Prepaid expenses |

|

72,873 |

|

51,898 |

| ||

|

Other current assets |

|

33,511 |

|

35,734 |

| ||

|

Deferred income taxes |

|

58,213 |

|

45,888 |

| ||

|

Total current assets |

|

896,186 |

|

927,027 |

| ||

|

Property and equipment, net of accumulated depreciation of $502,176 in 2014 and $325,490 in 2013 |

|

3,493,250 |

|

3,550,950 |

| ||

|

Restricted cash and investments in marketable securities |

|

108,529 |

|

50,065 |

| ||

|

Other long-term assets |

|

140,119 |

|

119,466 |

| ||

|

Deferred income taxes |

|

160,531 |

|

125,303 |

| ||

|

Identifiable intangible assets, net of accumulated amortization of $42,661 in 2014 and $27,969 in 2013 |

|

173,112 |

|

194,513 |

| ||

|

Goodwill |

|

169,681 |

|

169,681 |

| ||

|

Total assets |

|

$ |

5,141,408 |

|

$ |

5,137,005 |

|

|

Liabilities and Stockholders’ Deficit: |

|

|

|

|

| ||

|

Current liabilities: |

|

|

|

|

| ||

|

Current installments of long-term debt |

|

$ |

12,518 |

|

$ |

16,268 |

|

|

Capital lease obligations |

|

2,875 |

|

2,857 |

| ||

|

Financing obligations |

|

1,138 |

|

1,288 |

| ||

|

Accounts payable |

|

195,339 |

|

188,159 |

| ||

|

Accrued expenses |

|

125,000 |

|

156,460 |

| ||

|

Accrued compensation |

|

192,838 |

|

185,099 |

| ||

|

Self-insurance reserves |

|

130,874 |

|

135,552 |

| ||

|

Total current liabilities |

|

660,582 |

|

685,683 |

| ||

|

Long-term debt |

|

525,728 |

|

473,165 |

| ||

|

Capital lease obligations |

|

1,002,762 |

|

972,760 |

| ||

|

Financing obligations |

|

2,911,200 |

|

2,785,103 |

| ||

|

Deferred income taxes |

|

19,215 |

|

29,993 |

| ||

|

Self-insurance reserves |

|

355,344 |

|

263,455 |

| ||

|

Other long-term liabilities |

|

124,067 |

|

110,727 |

| ||

|

Commitments and contingencies |

|

|

|

|

| ||

|

Stockholders’ deficit: |

|

|

|

|

| ||

|

Class A common stock (par $0.001, 175,000,000 shares authorized, issued and outstanding 49,864,878 at December 31, 2014 and December 31, 2013) |

|

50 |

|

50 |

| ||

|

Additional paid-in capital |

|

143,492 |

|

161,452 |

| ||

|

Accumulated deficit |

|

(603,254 |

) |

(349,269 |

) | ||

|

Accumulated other comprehensive income |

|

515 |

|

1,068 |

| ||

|

Total stockholders’ deficit before noncontrolling interests |

|

(459,197 |

) |

(186,699 |

) | ||

|

Noncontrolling interests |

|

1,707 |

|

2,818 |

| ||

|

Total stockholders’ deficit |

|

(457,490 |

) |

(183,881 |

) | ||

|

Total liabilities and stockholders’ deficit |

|

$ |

5,141,408 |

|

$ |

5,137,005 |

|

See accompanying notes to the consolidated financial statements.

FC-GEN OPERATIONS INVESTMENT, LLC AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

(IN THOUSANDS, EXCEPT PER SHARE DATA)

|

|

|

Year ended December 31, |

| |||||||

|

|

|

2014 |

|

2013 |

|

2012 |

| |||

|

|

|

|

|

|

|

|

| |||

|

Net revenues |

|

$ |

4,768,080 |

|

$ |

4,710,341 |

|

$ |

3,076,298 |

|

|

|

|

|

|

|

|

|

| |||

|

Salaries, wages and benefits |

|

2,904,094 |

|

2,898,860 |

|

1,946,383 |

| |||

|

Other operating expenses |

|

1,109,732 |

|

1,007,909 |

|

634,233 |

| |||

|

General and administrative costs |

|

147,030 |

|

152,555 |

|

107,997 |

| |||

|

Provision for losses on accounts receivable |

|

77,670 |

|

69,939 |

|

42,003 |

| |||

|

Lease expense |

|

131,898 |

|

131,231 |

|

35,367 |

| |||

|

Depreciation and amortization expense |

|

193,675 |

|

188,726 |

|

146,387 |

| |||

|

Interest expense |

|

442,724 |

|

426,975 |

|

323,641 |

| |||

|

Loss (gain) on early extinguishment of debt |

|

1,133 |

|

63 |

|

(1,777 |

) | |||

|

Investment income |

|

(3,399 |

) |

(4,150 |

) |

(3,782 |

) | |||

|

Other (income) loss |

|

(138 |

) |

450 |

|

(849 |

) | |||

|

Transaction costs |

|

13,353 |

|

5,878 |

|

29,755 |

| |||

|

Long-lived asset impairment |

|

31,399 |

|

9,999 |

|

— |

| |||

|

Equity in net loss (income) of unconsolidated affiliates |

|

416 |

|

691 |

|

(515 |

) | |||

|

|

|

|

|

|

|

|

| |||

|

Loss before income tax benefit |

|

(281,507 |

) |

(178,785 |

) |

(182,545 |

) | |||

|

Income tax benefit |

|

(44,022 |

) |

(9,179 |

) |

(11,633 |

) | |||

|

|

|

|

|

|

|

|

| |||

|

Loss from continuing operations |

|

(237,485 |

) |

(169,606 |

) |

(170,912 |

) | |||

|

Loss from discontinued operations, net of taxes |

|

(14,044 |

) |

(7,364 |

) |

(810 |

) | |||

|

|

|

|

|

|

|

|

| |||

|

Net loss |

|

(251,529 |

) |

(176,970 |

) |

(171,722 |

) | |||

|

Less net (income) loss attributable to noncontrolling interests |

|

(2,456 |

) |

(1,025 |

) |

448 |

| |||

|

Net loss attributable to FC-GEN Operations Investment, LLC |

|

$ |

(253,985 |

) |

$ |

(177,995 |

) |

$ |

(171,274 |

) |

|

|

|

|

|

|

|

|

| |||

|

Loss per common share: |

|

|

|

|

|

|

| |||

|

Basic and diluted: |

|

|

|

|

|

|

| |||

|

Weighted average shares outstanding for basic and diluted loss from continuing operations per share |

|

49,865 |

|

49,865 |

|

49,865 |

| |||

|

|

|

|

|

|

|

|

| |||

|

Basic and diluted net loss per common share: |

|

|

|

|

|

|

| |||

|

Loss from continuing operations attributable to FC-GEN Operations Investment, LLC |

|

$ |

(4.81 |

) |

$ |

(3.42 |

) |

$ |

(3.41 |

) |

|

Loss from discontinued operations, net of taxes |

|

(0.28 |

) |

(0.15 |

) |

(0.02 |

) | |||

|

Net loss attributable to FC-GEN Operations Investment, LLC |

|

$ |

(5.09 |

) |

$ |

(3.57 |

) |

$ |

(3.43 |

) |

See accompanying notes to the consolidated financial statements.

FC-GEN OPERATIONS INVESTMENT, LLC AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

(IN THOUSANDS)

|

|

|

Year ended December 31, |

| |||||||

|

|

|

2014 |

|

2013 |

|

2012 |

| |||

|

Net loss |

|

$ |

(251,529 |

) |

$ |

(176,970 |

) |

$ |

(171,722 |

) |

|

Net unrealized (loss) gain on marketable securities, net of tax |

|

(553 |

) |

(1,916 |

) |

34 |

| |||

|

Comprehensive loss |

|

(252,082 |

) |

(178,886 |

) |

(171,688 |

) | |||

|

Less: comprehensive (income) loss attributable to noncontrolling interests |

|

(2,456 |

) |

(1,025 |

) |

448 |

| |||

|

Comprehensive loss attributable to FC-GEN Operations Investment, LLC |

|

$ |

(254,538 |

) |

$ |

(179,911 |

) |

$ |

(171,240 |

) |

See accompanying notes to the consolidated financial statements.

FC-GEN OPERATIONS INVESTMENT, LLC AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY (DEFICIT)

(IN THOUSANDS)

|

|

|

|

|

|

|

|

|

|

|

Accumulated |

|

|

|

|

|

|

| |||||||

|

|

|

|

|

|

|

|

|

|

|

other |

|

|

|

|

|

Total |

| |||||||

|

|

|

Class A Common Stock |

|

Additional |

|

Accumulated |

|

comprehensive |

|

Stockholders’ |

|

Noncontrolling |

|

stockholders’ |

| |||||||||

|

|

|

Shares |

|

Amount |

|

paid-in capital |

|

deficit |

|

income (loss) |

|

deficit |

|

interests |

|

equity (deficit) |

| |||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

|

Balance at December 31, 2011 |

|

49,865 |

|

$ |

50 |

|

$ |

177,065 |

|

$ |

— |

|

$ |

2,950 |

|

$ |

180,065 |

|

$ |

57 |

|

$ |

180,122 |

|

|

Net loss |

|

— |

|

— |

|

— |

|

(171,274 |

) |

— |

|

(171,274 |

) |

(448 |

) |

(171,722 |

) | |||||||

|

Net unrealized gain on marketable securities, net of tax |

|

— |

|

— |

|

— |

|

— |

|

34 |

|

34 |

|

— |

|

34 |

| |||||||

|

Contributions by stockholders |

|

— |

|

— |

|

25,000 |

|

— |

|

— |

|

25,000 |

|

— |

|

25,000 |

| |||||||

|

Distributions to stockholders |

|

— |

|

— |

|

(35,274 |

) |

— |

|

— |

|

(35,274 |

) |

— |

|

(35,274 |

) | |||||||

|

Acquisition of noncontrolling interest |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

|

4,528 |

|

4,528 |

| |||||||

|

Consolidation of noncontrolling interests |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

|

15 |

|

15 |

| |||||||

|

Distributions to noncontrolling interests |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

|

(684 |

) |

(684 |

) | |||||||

|

Balance at December 31, 2012 |

|

49,865 |

|

$ |

50 |

|

$ |

166,791 |

|

$ |

(171,274 |

) |

$ |

2,984 |

|

$ |

(1,449 |

) |

$ |

3,468 |

|

$ |

2,019 |

|

|

Net loss |

|

— |

|

— |

|

— |

|

(177,995 |

) |

— |

|

(177,995 |

) |

1,025 |

|

(176,970 |

) | |||||||

|

Net unrealized loss on marketable securities, net of tax |

|

— |

|

— |

|

— |

|

— |

|

(1,916 |

) |

(1,916 |

) |

— |

|

(1,916 |

) | |||||||

|

Distributions to stockholders |

|

— |

|

— |

|

(5,339 |

) |

— |

|

— |

|

(5,339 |

) |

— |

|

(5,339 |

) | |||||||

|

Distributions to noncontrolling interests |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

|

(1,675 |

) |

(1,675 |

) | |||||||

|

Balance at December 31, 2013 |

|

49,865 |

|

$ |

50 |

|

$ |

161,452 |

|

$ |

(349,269 |

) |

$ |

1,068 |

|

$ |

(186,699 |

) |

$ |

2,818 |

|

$ |

(183,881 |

) |

|

Net loss |

|

— |

|

— |

|

— |

|

(253,985 |

) |

— |

|

(253,985 |

) |

2,456 |

|

(251,529 |

) | |||||||

|

Net unrealized loss on marketable securities, net of tax |

|

— |

|

— |

|

— |

|

— |

|

(553 |

) |

(553 |

) |

— |

|

(553 |

) | |||||||

|

Distributions to stockholders |

|

— |

|

— |

|

(17,960 |

) |

— |

|

— |

|

(17,960 |

) |

— |

|

(17,960 |

) | |||||||

|

Distributions to noncontrolling interests |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

|

(3,567 |

) |

(3,567 |

) | |||||||

|

Balance at December 31, 2014 |

|

49,865 |

|

$ |

50 |

|

$ |

143,492 |

|

$ |

(603,254 |

) |

$ |

515 |

|

$ |

(459,197 |

) |

$ |

1,707 |

|

$ |

(457,490 |

) |

See accompanying notes to the consolidated financial statements.

FC-GEN OPERATIONS INVESTMENT, LLC AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

(IN THOUSANDS)

|

|

|

Year ended December 31, |

| |||||||

|

|

|

2014 |

|

2013 |

|

2012 |

| |||

|

|

|

|

|

|

|

|

| |||

|

Cash flows from operating activities: |

|

|

|

|

|

|

| |||

|

Net loss |

|

$ |

(251,529 |

) |

$ |

(176,970 |

) |

$ |

(171,722 |

) |

|

Adjustments to reconcile net loss to net cash provided by operating activities: |

|

|

|

|

|

|

| |||

|

Non-cash interest and leasing arrangements, net |

|

86,073 |

|

89,141 |

|

72,883 |

| |||

|

Other non-cash charges and (gains) |

|

3,947 |

|

2,853 |

|

(575 |

) | |||

|

Depreciation and amortization |

|

196,192 |

|

191,479 |

|

146,113 |

| |||

|

Provision for losses on accounts receivable |

|

78,552 |

|

71,538 |

|

42,159 |

| |||

|

Equity in net loss (income) of unconsolidated affiliates |

|

416 |

|

691 |

|

(515 |

) | |||

|

Provision for deferred taxes |

|

(58,293 |

) |

(25,693 |

) |

(9,811 |

) | |||

|

Long-lived asset impairment |

|

31,399 |

|

9,999 |

|

— |

| |||

|

Loss (gain) on early extinguishment of debt |

|

1,133 |

|

63 |

|

(1,777 |

) | |||

|

Changes in assets and liabilities: |

|

|

|

|

|

|

| |||

|

Transaction costs |

|

— |

|

(17,203 |

) |

(18,644 |

) | |||

|

Accounts receivable |

|

(33,568 |

) |

(109,844 |

) |

(45,290 |

) | |||

|

Accounts payable and other accrued expenses and other |

|

53,330 |

|

46,095 |

|

(2,849 |

) | |||

|

Net cash provided by operating activities |

|

107,652 |

|

82,149 |

|

9,972 |

| |||

|

Cash flows from investing activities: |

|

|

|

|

|

|

| |||

|

Capital expenditures |

|

(70,987 |

) |

(77,399 |

) |

(66,704 |

) | |||

|

Purchases of marketable securities |

|

(30,449 |

) |

(39,569 |

) |

(43,794 |

) | |||

|

Proceeds on maturity or sale of marketable securities |

|

30,188 |

|

26,227 |

|

36,758 |

| |||

|

Net change in restricted cash and equivalents |

|

(24,405 |

) |

4,235 |

|

(5,476 |

) | |||

|

Purchase of Sun, net of cash acquired |

|

— |

|

— |

|

(168,914 |

) | |||

|

Sale of hospice subsidiary |

|

— |

|

— |

|

75,306 |

| |||

|

Purchases of inpatient assets, net of cash acquired |

|

(1,878 |

) |

(12,200 |

) |

(5,175 |

) | |||

|

Sales of inpatient assets |

|

5,227 |

|

8,354 |

|

— |

| |||

|

Investment in joint ventures |

|

(2,309 |

) |

(6,182 |

) |

(2,000 |

) | |||

|

Other, net |

|

(1,062 |

) |

4,832 |

|

(2,900 |

) | |||

|

Net cash used in investing activities |

|

(95,675 |

) |

(91,702 |

) |

(182,899 |

) | |||

|

Cash flows from financing activities: |

|

|

|

|

|

|

| |||

|

Borrowings under revolving credit facility |

|

603,500 |

|

866,000 |

|

799,010 |

| |||

|

Repayments under revolving credit facility |

|

(549,000 |

) |

(828,000 |

) |

(714,010 |

) | |||

|

Proceeds from issuance of long-term debt |

|

960 |

|

15,095 |

|

317,322 |

| |||

|

Proceeds from tenant improvement draws under lease arrangements |

|

6,087 |

|

10,498 |

|

31,024 |

| |||

|

Repayment of long-term debt |

|

(17,947 |

) |

(35,085 |

) |

(226,024 |

) | |||

|

Debt issuance costs |

|

(7,915 |

) |

(746 |

) |

(21,335 |

) | |||

|

Distributions to noncontrolling interests |

|

(3,567 |

) |

(1,675 |

) |

(684 |

) | |||

|

Contributions by stockholders |

|

— |

|

— |

|

25,000 |

| |||

|

Distributions to stockholders |

|

(17,960 |

) |

(5,339 |

) |

(35,274 |

) | |||

|

Other, net |

|

— |

|

— |

|

(2,800 |

) | |||

|

Net cash provided by financing activities |

|

14,158 |

|

20,748 |

|

172,229 |

| |||

|

Net increase (decrease) in cash and equivalents |

|

26,135 |

|

11,195 |

|

(698 |

) | |||

|

Cash and equivalents: |

|

|

|

|

|

|

| |||

|

Beginning of period |

|

61,413 |

|

50,218 |

|

50,916 |

| |||

|

End of period |

|

$ |

87,548 |

|

$ |

61,413 |

|

$ |

50,218 |

|

|

Supplemental disclosure of cash flow information: |

|

|

|

|

|

|

| |||

|

Interest paid |

|

$ |

369,124 |

|

$ |

354,129 |

|

$ |

260,036 |

|

|

Taxes paid |

|

2,408 |

|

12,584 |

|

5,317 |

| |||

|

Non-cash financing activities: |

|

|

|

|

|

|

| |||

|

Capital leases |

|

$ |

13,096 |

|

$ |

(54,626 |

) |

$ |

680,909 |

|

|

Financing obligations |

|

80,284 |

|

43,934 |

|

21,282 |

| |||

|

Assumption of long-term debt |

|

— |

|

— |

|

113,340 |

| |||

See accompanying notes to the consolidated financial statements.

FC-GEN Operations Investment, LLC and Subsidiaries

Notes to Consolidated Financial Statements

(1) General Information

Description of Business

FC-GEN Operations Investment, LLC (the Company) provides inpatient services through 414 skilled nursing, assisted living and behavioral health centers located in 28 states. These centers are operated by wholly owned subsidiaries of the Company. Revenues of the Company’s owned, leased and otherwise consolidated centers constitute approximately 85% of its revenues.

The Company also provides, through wholly owned subsidiaries, a range of rehabilitation therapy services, including speech pathology, physical therapy, occupational therapy and respiratory health services. These services are provided by rehabilitation therapists and assistants employed or contracted at substantially all of the centers operated by the Company, as well as by contract to healthcare facilities operated by others. After the elimination of intercompany revenues, the rehabilitation therapy services business constitutes approximately 13% of the Company’s revenues.

The Company also provides, through wholly owned subsidiaries, an array of other specialty medical services, including, management services, physician services, staffing services and other healthcare related services, which comprise the balance of the Company’s revenues.

Skilled Merger - Purchase and Contribution Agreement

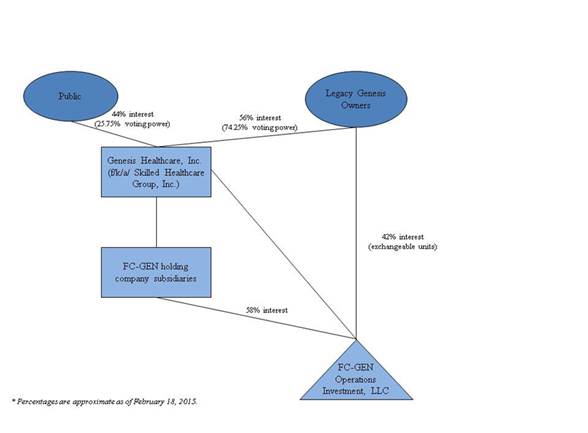

On August 18, 2014, Skilled Healthcare Group, Inc., a Delaware corporation (Skilled) entered into a Purchase and Contribution Agreement with the Company pursuant to which the businesses and operations of the Company and Skilled will be combined (the Combination). On February 2, 2015, the Company completed the Combination. See note 21 — “Subsequent Events.”

After completion of the transaction, the combined company now operates under the name Genesis Healthcare, Inc. and the Class A common stock of Skilled continues to trade on the NYSE under the symbol “GEN”. The current owners of the Company hold 74.25% of the economic interests in the combined entity post-transaction and the shareholders of Skilled hold the remaining 25.75% economic interest in the combined entity post-transaction. The Company obtained control over Skilled and, thus, is the accounting acquirer. Therefore, the transaction meets the definition of a reverse acquisition where the legal acquirer is the accounting acquiree. The acquisition method will be applied to the transaction based on Skilled’s stock price (level 1 valuation technique - quoted prices in active markets for identical assets or liabilities) as of the acquisition date. The consideration will be allocated to the legacy Skilled business that is being acquired on the acquisition date with any excess consideration over the fair value of the net assets acquired being recognized as goodwill. The Company’s assets and liabilities will remain at their historical costs.

Basis of Presentation

The accompanying consolidated financial statements have been prepared in accordance with U.S. generally accepted accounting principles. In the opinion of management, the consolidated financial statements include all necessary adjustments for a fair presentation of the financial position and results of operations for the periods presented.

(2) Summary of Significant Accounting Policies

Net Revenues and Accounts Receivable

The Company receives payments through reimbursement from Medicaid and Medicare programs and directly from individual residents (private pay), third-party insurers and long-term care facilities. The Company assesses collectibility on all accounts prior to providing services.

FC-GEN Operations Investment, LLC and Subsidiaries

Notes to Consolidated Financial Statements

The Company records revenue for inpatient services and the related receivables in the accounting records at the Company’s established billing rates in the period the related services are rendered. The provision for contractual adjustments, which represents the differences between the established billing rates and predetermined reimbursement rates, is deducted from gross revenue to determine net revenue. Retroactive adjustments that are likely to result from future examinations by third party payors are accrued on an estimated basis in the period the related services are rendered and adjusted as necessary in future periods based upon new information or final settlements.

The Company records revenue for rehabilitation therapy services and other ancillary services and the related receivables at the time services or products are provided or delivered to the customer. Upon delivery of products or services, the Company has no additional performance obligation to the customer.

Use of Estimates

The preparation of consolidated financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from these estimates. Significant items subject to such estimates and assumptions include the useful lives of fixed assets, allowances for doubtful accounts and provisions for contractual adjustments, deferred tax assets, fixed assets, goodwill, identifiable intangible assets, investments, as well as reserves for employee benefit obligations, self-insurance liabilities, income tax uncertainties, asset retirement obligations and other contingencies. These estimates and assumptions are based on management’s best estimates and judgment. Management evaluates its estimates and assumptions on an ongoing basis using historical experience and other factors, including the current economic environment. Management believes its estimates to be reasonable under the circumstances. The current economic environment has increased the degree of uncertainty inherent in these estimates and assumptions. As future events and their effects cannot be determined with precision, actual results could differ significantly from these estimates.

Cash and Equivalents

Short-term investments that have a maturity of ninety days or less at acquisition are considered cash equivalents. Investments in cash equivalents are carried at cost, which approximates fair value.

Restricted Cash and Investments in Marketable Securities

Restricted cash includes cash and money market funds principally held by the Company’s wholly owned captive insurance subsidiary, which is substantially restricted to securing outstanding claims losses. The restricted cash and investments in marketable securities balances at December 31, 2014 and 2013 were $146.7 million and $123.0 million, respectively.

Restricted investments in marketable securities, comprised of fixed interest rate securities, are considered to be available-for-sale and accordingly are reported at fair value with unrealized gains and losses, net of related tax effects, included within accumulated other comprehensive income, a separate component of stockholders’ equity. Fair values for fixed interest rate securities are based on quoted market prices.

A decline in the market value of any security below cost that is deemed other-than-temporary is charged to income, resulting in the establishment of a new cost basis for the security. Realized gains and losses for securities classified as available for sale are derived using the specific identification method for determining the cost of securities sold.

Allowance for Doubtful Accounts

The Company evaluates the adequacy of its allowance for doubtful accounts by estimating allowance requirement percentages for each accounts receivable aging category for each type of payor. The Company has developed estimated allowance requirement percentages by utilizing historical collection trends and its understanding of the nature and

FC-GEN Operations Investment, LLC and Subsidiaries

Notes to Consolidated Financial Statements

collectibility of receivables in the various aging categories and the various lines of the Company’s business. The allowance percentages are developed by payor type as the accounts receivable from each payor type have unique characteristics. The allowance for doubtful accounts also considers accounts specifically identified as uncollectible. Accounts receivable that Company management specifically estimates to be uncollectible, based upon the age of the receivables, the results of collection efforts, or other circumstances, are reserved in the allowance for doubtful accounts until written-off.

Prepaid Expenses and Other Current Assets

Prepaid expenses and other current assets principally consist of expenses paid in advance of the provision of services, inventories of nursing center food and supplies, non-trade receivables and $9.0 million and $9.3 million of escrowed funds held by third parties at December 31, 2014 and 2013, respectively, in accordance with loan and other contractual agreements.

Property and Equipment

Property and equipment are recorded at cost. Depreciation is calculated using the straight-line method over estimated useful lives of 20-35 years for buildings, building improvements and land improvements, and 3-15 years for equipment, furniture and fixtures and information systems. Depreciation expense on leasehold improvements and assets held under capital leases is calculated using the straight-line method over the lesser of the lease term or the estimated useful life of the asset. Expenditures for maintenance and repairs necessary to maintain property and equipment in efficient operating condition are charged to operations as incurred. Costs of additions and betterments are capitalized.

Total depreciation expense from continuing operations for the years ended December 31, 2014, 2013 and 2012 was $184.3 million, $179.4 million, and $140.2 million, respectively.

Long-Lived Assets

The Company’s long-lived assets are reviewed for impairment whenever events or changes in circumstances indicate the carrying amount of an asset may not be recoverable. Recoverability of assets to be held and used is measured by comparison of the carrying amount of an asset to the future cash flows expected to be generated by the asset. If the carrying amount of an asset exceeds its estimated future undiscounted cash flows, an impairment charge is recognized to the extent the carrying amount of the asset exceeds the fair value of the asset. Assets to be disposed of are reported at the lower of the carrying amount or the fair value less costs to sell.

The Company performs an assessment of qualitative factors prior to the use of the two step quantitative method to determine if goodwill has been impaired. If such qualitative assessment does not indicate that it is more likely than not the fair value of the reporting is less than its carrying value, no further analysis is required. The Company performs its annual impairment assessment as of September 30, of each year or more frequently if adverse events or changes in circumstances indicate that the asset may be impaired. See note 19 — “Asset Impairment Charges.”

Self-Insurance Risks

The Company provides for self-insurance risks for both general and professional liability and workers’ compensation claims based on estimates of the ultimate costs for both reported claims and claims incurred but not reported. Estimated losses from asserted and incurred but not reported claims are accrued based on the Company’s estimates of the ultimate costs of the claims, which includes costs associated with litigating or settling claims, and the relationship of past reported incidents to eventual claims payments. All relevant information, including the Company’s own historical experience, the nature and extent of existing asserted claims and reported incidents, and independent actuarial analyses of this information is used in estimating the expected amount of claims. The reserves for loss for workers’ compensation risks are discounted based on actuarial estimates of claim payment patterns whereas the reserves for general and professional liability are recorded on an undiscounted basis. The Company also considers amounts that may be recovered from excess insurance carriers in estimating the ultimate net liability for such risks.

FC-GEN Operations Investment, LLC and Subsidiaries

Notes to Consolidated Financial Statements

Income Taxes

The Company is treated as a partnership for federal and state income tax purposes. Therefore, the consolidated financial statements do not include any provision for federal or state income taxes, except for the subsidiaries that continued to be treated as corporations for federal and state income tax purposes and for the few jurisdictions that tax partnership income. The Company’s financial results are allocated to the Company’s members. The Company’s members include these results on their separate tax returns.

For the Company’s subsidiaries treated as corporations for federal and state income tax purposes, the provision (benefit) for income taxes is based upon their annual reported income or loss for each respective accounting period. Deferred income taxes arise from the recognition of the tax consequences of temporary differences between the tax basis of assets and liabilities and their reported amounts in the consolidated financial statements. These temporary differences will result in taxable or deductible amounts in future years when the reported amounts of the assets are recovered or liabilities are settled. The Company also recognizes as deferred tax assets the future tax benefits from net operating loss (NOL) carryforwards. A valuation allowance is provided for these and other deferred tax assets if it is more likely than not that some portion or all of the net deferred tax assets will not be realized.

The Company records accrued interest and penalties associated with uncertain tax positions as income tax expense in the consolidated statement of operations.

Leases

Leasing transactions are a material part of the Company’s business. The following discussion summarizes various aspects of the Company’s accounting for leasing transactions and the related balances.

Capital Leases

Lease arrangements are capitalized when such leases convey substantially all the risks and benefits incidental to ownership. Capital leases are amortized over either the lease term or the life of the related assets, depending upon available purchase options and lease renewal features. Amortization related to capital leases is included in the consolidated statements of operations within depreciation and amortization expense.

Operating Leases

For operating leases, minimum lease payments, including minimum scheduled rent increases, are recognized as lease expense on a straight-line basis over the applicable lease terms and any periods during which the Company has use of the property but is not charged rent by a landlord. Lease terms, in most cases, provide for rent escalations and renewal options.

When the Company purchases businesses that have operating lease agreements, it recognizes the fair value of the lease arrangements as either favorable or unfavorable and records these amounts as other identifiable intangible assets or other long-term liabilities, respectively. Favorable and unfavorable leases are amortized to lease expense on a straight-line basis over the remaining term of the leases.

Sale/Leaseback Financing Obligation

Prior to recognition as a sale, or profit/loss thereon, sale/leaseback transactions are evaluated to determine if their terms transfer all of the risks and rewards of ownership as demonstrated by the absence of any other continuing involvement by the seller-lessee. A sale/leaseback transaction that does not qualify for sale/leaseback accounting because of any form of continuing involvement by the seller-lessee is accounted for as a financing transaction. Under the financing method: (1) the assets and accumulated depreciation remain on the consolidated balance sheet and continue to be depreciated over the remaining useful lives; (2) no gain is recognized; and (3) proceeds received by the Company from these transactions are recorded as a financing obligation.

FC-GEN Operations Investment, LLC and Subsidiaries

Notes to Consolidated Financial Statements

Asset Retirement Obligations

The fair value of a liability for an asset retirement obligation is recognized in the period when the asset is placed in service. The fair value of the liability is estimated using discounted cash flows. In subsequent periods, the retirement obligation is accreted to its future value or the estimate of the obligation at the asset retirement date. The accretion charge is reflected separately on the consolidated statement of operations. A corresponding retirement asset equal to the fair value of the retirement obligation is also recorded as part of the carrying amount of the related long-lived asset and depreciated over the asset’s useful life.

Recent Accounting Pronouncements

In April 2014, the FASB issued ASU No. 2014-08, Reporting Discontinued Operations and Disclosures of Disposals of Components of an Entity, (ASU 2014-08). This ASU requires an entity to report disposed components or components held-for-sale in discontinued operations if such components represent a strategic shift that has or will have a significant effect on operations and financial results. Additionally, expanded disclosure about discontinued operations and disposals of significant components that do not qualify for discontinued operations presentation will be required. The adoption of ASU 2014-08 is effective prospectively for disposals that occur within annual periods beginning on or after December 15, 2014, with early adoption permitted. The Company adopted ASU 2014-08 in the fourth quarter of 2014 and its adoption did not have a material impact on the consolidated financial statements.

In May 2014, the FASB issued ASU No. 2014-09, Revenue from Contracts with Customers, (ASU 2014-08). This ASU requires an entity to recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. To achieve this core principle, the guidance provides that an entity should apply the following steps: (1) identify the contract(s) with a customer; (2) identify the performance obligations in the contract; (3) determine the transaction price; (4) allocate the transaction price to the performance obligations in the contract; and (5) recognize revenue when, or as, the entity satisfies a performance obligation. The ASU is effective beginning in the first quarter of our fiscal year 2017. Early adoption is not permitted. The Company is currently evaluating the impact to the consolidated financial statements.

(3) Significant Transactions and Events

Sun Merger

Effective December 1, 2012, the Company completed the acquisition of Sun Healthcare Group, Inc. and its subsidiaries (Sun) (the Sun Merger). Upon consummation of the Sun Merger, each issued and outstanding share of Sun common stock and common stock equivalent was tendered for $8.50 in cash. The purchase price totaled $228.4 million before considering cash acquired in connection with the Sun Merger. The Company also assumed $88.8 million of long-term debt in the Sun Merger, of which $87.5 million was refinanced on December 3, 2012. The operating results of Sun have been included in the accompanying consolidated financial statements of the Company since December 1, 2012.

Simultaneous with the Sun Merger, Sun’s hospice segment was sold to Life Choice Hospice, a provider of in-home hospice care, for approximately $85 million. Net cash sale proceeds of $75 million were used to repay the Term Loan Facility. The Company retained an approximate one-third interest in the sold hospice segment since it owned an approximate one-third interest in Life Choice Hospice’s parent company. Life Choice Hospice has since been merged into FC PAC Holdings, LLC. See note 15 — “Related Party Transactions.”

FC-GEN Operations Investment, LLC and Subsidiaries

Notes to Consolidated Financial Statements

Pro Forma Information

The acquired business contributed net revenues of $145.2 million and a net income of $0.7 million to the Company for the period from December 1, 2012 to December 31, 2012. The unaudited pro forma net effect of the Sun Merger assuming the acquisition occurred as of January 1, 2012 is as follows (in thousands, except per share amounts):

|

|

|

Pro Forma |

| |

|

|

|

Twelve months ended |

| |

|

|

|

December 31, 2012 |

| |

|

Revenues |

|

$ |

4,700,479 |

|

|

Loss attributable to FC-GEN Operations Investment, LLC |

|

(214,640 |

) | |

|

|

|

|

| |

|

Loss per share from continuing operations attributable FC-GEN Operations Investment, LLC: |

|

|

| |

|

Basic |

|

(4.30 |

) | |

|

Diluted |

|

(4.30 |

) | |

The unaudited pro forma financial data have been derived by combining the historical financial results of the Company and the operations acquired in the Sun Merger for the periods presented.

(4) Certain Significant Risks and Uncertainties

Revenue Sources

The Company receives revenues from Medicare, Medicaid, private insurance, self-pay residents, other third-party payors and long-term care facilities that utilize its rehabilitation therapy and other services. The Company’s inpatient services derives approximately 79% of its revenue from the Medicare and various state Medicaid programs.

The sources and amounts of the Company’s revenues are determined by a number of factors, including licensed bed capacity and occupancy rates of its inpatient facilities, the mix of patients and the rates of reimbursement among payors. Likewise, payment for ancillary medical services, including services provided by the Company’s rehabilitation therapy services business, vary based upon the type of payor and payment methodologies. Changes in the case mix of the patients as well as payor mix among Medicare, Medicaid and private pay can significantly affect the Company’s profitability.

It is not possible to quantify fully the effect of legislative changes, the interpretation or administration of such legislation or other governmental initiatives on the Company’s business and the business of the customers served by the Company’s rehabilitation therapy business. The potential impact of healthcare reform, which would initiate significant reforms to the United States healthcare system, including potential material changes to the delivery of healthcare services and the reimbursement paid for such services by the government or other third party payors, is uncertain at this time. Accordingly, there can be no assurance that the impact of any future healthcare legislation or regulation will not adversely affect the Company’s business. There can be no assurance that payments under governmental and private third-party payor programs will be timely, will remain at levels similar to present levels or will, in the future, be sufficient to cover the costs allocable to patients eligible for reimbursement pursuant to such programs. The Company’s financial condition and results of operations will be affected by the reimbursement process, which in the healthcare industry is complex and can involve lengthy delays between the time that revenue is recognized and the time that reimbursement amounts are settled.

Laws and regulations governing the Medicare and Medicaid programs are complex and subject to interpretation. The Company believes that it is in material compliance with all applicable laws and regulations and is not aware of any pending or threatened investigations involving material allegations of potential wrongdoing. While no such regulatory inquiries have been made, noncompliance with such laws and regulations can be subject to regulatory actions including fines, penalties, and exclusion from the Medicare and Medicaid programs.

FC-GEN Operations Investment, LLC and Subsidiaries

Notes to Consolidated Financial Statements

(5) Loss Per Share

The Company has a single class of common stock. Basic net loss per share was computed by dividing net loss by the weighted-average number of outstanding common shares for the period. Diluted earnings per share is computed by dividing loss plus the effect of assumed conversions (if applicable) by the weighted-average number of outstanding shares after giving effect to all potential dilutive common stock, including options, warrants, common stock subject to repurchase and convertible preferred stock, if any.

The computations of basic and diluted loss per share are consistent with any potentially dilutive adjustments to the numerator or denominator being anti-dilutive and therefore excluded from the dilutive calculation. A reconciliation of the numerator and denominator used in the calculation of basic and diluted net income per common share follows (in thousands, except per share data):

|

|

|

Year ended December 31, |

| |||||||

|

|

|

2014 |

|

2013 |

|

2012 |

| |||

|

|

|

|

|

|

|

|

| |||

|

Numerator: |

|

|

|

|

|

|

| |||

|

Loss from continuing operations |

|

$ |

(237,485 |

) |

$ |

(169,606 |

) |

$ |

(170,912 |

) |

|

Less: Net income (loss) attributable to noncontrolling interests |

|

2,456 |

|

1,025 |

|

(448 |

) | |||

|

Loss from continuing operations attributable to FC-GEN Operations Investment, LLC |

|

(239,941 |

) |

(170,631 |

) |

(170,464 |

) | |||

|

Loss from discontinued operations, net of income tax |

|

(14,044 |

) |

(7,364 |

) |

(810 |

) | |||

|

Net loss attributable to FC-GEN Operations Investment, LLC |

|

$ |

(253,985 |

) |

$ |

(177,995 |

) |

$ |

(171,274 |

) |

|

|

|

|

|

|

|

|

| |||

|

Denominator: |

|

|

|

|

|

|

| |||

|

Weighted average shares outstanding for basic and diluted net loss per share |

|

49,865 |

|

49,865 |

|

49,865 |

| |||

|

|

|

|

|

|

|

|

| |||

|

Basic and diluted net loss per common share: |

|

|

|

|

|

|

| |||

|

Loss from continuing operations attributable to FC-GEN Operations Investment, LLC |

|

$ |

(4.81 |

) |

$ |

(3.42 |

) |

$ |

(3.41 |

) |

|

Loss from discontinued operations, net of income tax |

|

(0.28 |

) |

(0.15 |

) |

(0.02 |

) | |||

|

Net loss attributable to FC-GEN Operations Investment, LLC |

|

$ |

(5.09 |

) |

$ |

(3.57 |

) |

$ |

(3.43 |

) |

(6) Segment Information

The Company has three reportable operating segments: (i) inpatient services; (ii) rehabilitation therapy services; and (iii) other services. For additional information on these reportable segments see note 1 — “General Information — Description of Business.”

FC-GEN Operations Investment, LLC and Subsidiaries

Notes to Consolidated Financial Statements

A summary of the Company’s segmented revenues follows:

|

|

|

Years Ended December 31, |

| |||||||||||||

|

|

|

2014 |

|

2013 |

|

2012 |

| |||||||||

|

|

|

Revenue |

|

Revenue |

|

Revenue |

|

Revenue |

|

Revenue |

|

Revenue |

| |||

|

|

|

(in thousands, except percentages) |

| |||||||||||||

|

|

|

|

| |||||||||||||

|

Revenues: |

|

|

|

|

|

|

|

|

|

|

|

|

| |||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||

|

Inpatient services: |

|

|

|

|

|

|

|

|

|

|

|

|

| |||

|

Skilled nursing facilities |

|

$ |

3,924,571 |

|

82.3 |

% |

$ |

3,847,857 |

|

81.7 |

% |

$ |

2,467,427 |

|

80.2 |

% |

|

Assisted living facilities |

|

107,034 |

|

2.2 |

% |

113,960 |

|

2.4 |

% |

77,335 |

|

2.5 |

% | |||

|

Administration of third party facilities |

|

10,297 |

|

0.2 |

% |

11,006 |

|

0.2 |

% |

10,743 |

|

0.3 |

% | |||

|

Elimination of administrative services |

|

(2,089 |

) |

0.0 |

% |

(2,146 |

) |

0.0 |

% |

(1,896 |

) |

-0.1 |

% | |||

|

Inpatient services, net |

|

4,039,813 |

|

84.7 |

% |

3,970,677 |

|

84.3 |

% |

2,553,609 |

|

83.0 |

% | |||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||

|

Rehabilitation therapy services: |

|

|

|

|

|

|

|

|

|

|

|

|

| |||

|

Total therapy services |

|

990,081 |

|

20.8 |

% |

993,459 |

|

21.1 |

% |

732,805 |

|

23.8 |

% | |||

|

Elimination intersegment rehabilitation therapy services |

|

(385,721 |

) |

-8.1 |

% |

(375,175 |

) |

-8.0 |

% |

(248,918 |

) |

-8.1 |

% | |||

|

Third party rehabilitation therapy services |

|

604,360 |

|

12.7 |

% |

618,284 |

|

13.1 |

% |

483,887 |

|

15.7 |

% | |||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||

|

Other services: |

|

|

|

|

|

|

|

|

|

|

|

|

| |||

|

Total other services |

|

154,011 |

|

3.2 |

% |

141,712 |

|

3.0 |

% |

53,713 |

|

1.7 |

% | |||

|

Elimination intersegment other services |

|

(30,104 |

) |

-0.6 |

% |

(20,332 |

) |

-0.4 |

% |

(14,911 |

) |

-0.5 |

% | |||

|

Third party other services |

|

123,907 |

|

2.6 |

% |

121,380 |

|

2.6 |

% |

38,802 |

|

1.3 |

% | |||

|

Total revenue |

|

$ |

4,768,080 |

|

100.0 |

% |

$ |

4,710,341 |

|

100.0 |

% |

$ |

3,076,298 |

|

100.0 |

% |

A summary of the Company’s condensed consolidated statement of operations follows:

|

|

|

Year ended December 31, 2014 |

| ||||||||||||||||

|

|

|

Inpatient |

|

Rehabilitation |

|

Other Services |

|

Corporate |

|

Eliminations |

|

Consolidated |

| ||||||

|

|

|

(In thousands) |

| ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

|

Net revenues |

|

$ |

4,041,902 |

|

$ |

990,081 |

|

$ |

153,397 |

|

$ |

614 |

|

$ |

(417,914 |

) |

$ |

4,768,080 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

|

Salaries, wages and benefits |

|

1,987,550 |

|

817,144 |

|

99,400 |

|

102,820 |

|

— |

|

3,006,914 |

| ||||||

|

Other operating expenses |

|

1,472,321 |

|

78,532 |

|

54,464 |

|

44,210 |

|

(417,915 |

) |

1,231,612 |

| ||||||

|

Lease expense |

|

130,005 |

|

176 |

|

821 |

|

896 |

|

— |

|

131,898 |

| ||||||

|

Depreciation and amortization expense |

|

165,105 |

|

11,055 |

|

917 |

|

16,598 |

|

— |

|

193,675 |

| ||||||

|

Interest expense |

|

393,521 |

|

4 |

|

19 |

|

49,678 |

|

(498 |

) |

442,724 |

| ||||||

|

Loss on extinguishment of debt |

|

— |

|

— |

|

— |

|

1,133 |

|

— |

|

1,133 |

| ||||||

|

Investment income |

|

(2,492 |

) |

— |

|

— |

|

(1,405 |

) |

498 |

|

(3,399 |

) | ||||||

|

Other income |

|

(47 |

) |

— |

|

(91 |

) |

— |

|

— |

|

(138 |

) | ||||||

|

Transaction costs |

|

— |

|

— |

|

— |

|

13,353 |

|

— |

|

13,353 |

| ||||||

|

Long-lived asset impairment |

|

31,399 |

|

— |

|

— |

|

— |

|

— |

|

31,399 |

| ||||||

|

Equity in net (income) loss of unconsolidated affiliates |

|

(1,284 |

) |

— |

|

— |

|

— |

|

1,700 |

|

416 |

| ||||||

|

(Loss) income before income tax benefit |

|

(134,176 |

) |

83,170 |

|

(2,133 |

) |

(226,669 |

) |

(1,699 |

) |

(281,507 |

) | ||||||

|

Income tax benefit |

|

— |

|

— |

|

— |

|

(44,022 |

) |

— |

|

(44,022 |

) | ||||||

|

(Loss) income from continuing operations |

|

$ |

(134,176 |

) |

$ |

83,170 |

|

$ |

(2,133 |

) |

$ |

(182,647 |

) |

$ |

(1,699 |

) |

$ |

(237,485 |

) |

FC-GEN Operations Investment, LLC and Subsidiaries

Notes to Consolidated Financial Statements

|

|

|

Year ended December 31, 2013 |

| ||||||||||||||||

|

|

|

Inpatient |

|

Rehabilitation |

|

Other Services |

|

Corporate |

|

Eliminations |

|

Consolidated |

| ||||||

|

|

|

(In thousands) |

| ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

|

Net revenues |

|

$ |

3,972,823 |

|

$ |

993,459 |

|

$ |

141,712 |

|

$ |

— |

|

$ |

(397,653 |

) |

$ |

4,710,341 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

|

Salaries, wages and benefits |

|

1,977,111 |

|

828,406 |

|

93,342 |

|

99,799 |

|

— |

|

2,998,658 |

| ||||||

|

Other operating expenses |

|

1,344,983 |

|

87,263 |

|

43,256 |

|

52,756 |

|

(397,653 |

) |

1,130,605 |

| ||||||

|

Lease expense |

|

129,296 |

|

198 |

|

843 |

|

894 |

|

— |

|

131,231 |

| ||||||

|

Depreciation and amortization expense |

|

160,954 |

|

10,607 |

|

1,027 |

|

16,138 |

|

— |

|

188,726 |

| ||||||

|

Interest expense |

|

378,461 |

|

10 |

|

525 |

|

48,515 |

|

(536 |

) |

426,975 |

| ||||||

|

Loss on extinguishment of debt |

|

63 |

|

— |

|

— |

|

— |

|

— |

|

63 |

| ||||||

|

Investment income |

|

(3,431 |

) |

— |

|

— |

|

(1,255 |

) |

536 |

|

(4,150 |

) | ||||||

|

Other loss |

|

— |

|

346 |

|

— |

|

104 |

|

— |

|

450 |

| ||||||

|

Transaction costs |

|

— |

|

— |

|

— |

|

5,878 |

|

— |

|

5,878 |

| ||||||

|

Long-lived asset impairment |

|

9,999 |

|

— |

|

— |

|

— |

|

— |

|

9,999 |

| ||||||

|

Equity in net (income) loss of unconsolidated affiliates |

|

(2,067 |

) |

— |

|

— |

|

1,066 |

|

1,692 |

|

691 |

| ||||||

|

(Loss) income before income tax benefit |

|

(22,546 |

) |

66,629 |

|

2,719 |

|

(223,895 |

) |

(1,692 |

) |

(178,785 |

) | ||||||

|

Income tax benefit |

|

— |

|

— |

|

— |

|

(9,179 |

) |

— |

|

(9,179 |

) | ||||||

|

(Loss) income from continuing operations |

|

$ |

(22,546 |

) |

$ |

66,629 |

|

$ |

2,719 |

|

$ |

(214,716 |

) |

$ |

(1,692 |

) |

$ |

(169,606 |

) |

|

|

|

Year ended December 31, 2012 |

| ||||||||||||||||

|

|

|

Inpatient |

|

Rehabilitation |

|

Other Services |

|

Corporate |

|

Eliminations |

|

Consolidated |

| ||||||

|

|

|

(In thousands) |

| ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

|

Net revenues |

|

$ |

2,555,505 |

|

$ |

732,805 |

|

$ |

53,713 |

|

$ |

— |

|

$ |

(265,725 |

) |

$ |

3,076,298 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

|

Salaries, wages and benefits |

|

1,316,333 |

|

600,293 |

|

29,759 |

|

70,174 |

|

— |

|

2,016,559 |

| ||||||

|

Other operating expenses |

|

817,205 |

|

103,159 |

|

21,595 |

|

37,823 |

|

(265,725 |

) |

714,057 |

| ||||||

|

Lease expense |

|

34,971 |

|

261 |

|

23 |

|

112 |

|

— |

|

35,367 |

| ||||||

|

Depreciation and amortization expense |

|

124,782 |

|

6,869 |

|

86 |

|

14,650 |

|

— |

|

146,387 |

| ||||||

|

Interest expense |

|

307,262 |

|

— |

|

12 |

|

16,370 |

|

(3 |

) |

323,641 |

| ||||||

|

Gain on extinguishment of debt |

|

(1,777 |

) |

— |

|

— |

|

— |

|

— |

|

(1,777 |

) | ||||||

|

Investment income |

|

(2,956 |

) |

— |

|

— |

|

(829 |

) |

3 |

|

(3,782 |

) | ||||||

|

Other income |

|

— |

|

— |

|

— |

|

(849 |

) |

— |

|

(849 |

) | ||||||

|

Transaction costs |

|

— |

|

— |

|

— |

|

29,755 |

|

— |

|

29,755 |

| ||||||

|

Equity in net (income) loss of unconsolidated affiliates |

|

(1,527 |

) |

— |

|

— |

|

(339 |

) |

1,351 |

|

(515 |

) | ||||||

|

(Loss) income before income tax benefit |

|

(38,788 |

) |

22,223 |

|

2,238 |

|

(166,867 |

) |

(1,351 |

) |

(182,545 |

) | ||||||

|

Income tax benefit |

|

— |

|

— |

|

— |

|

(11,633 |

) |

— |

|

(11,633 |

) | ||||||

|

(Loss) income from continuing operations |

|

$ |

(38,788 |

) |

$ |

22,223 |

|

$ |

2,238 |

|

$ |

(155,234 |

) |

$ |

(1,351 |

) |

$ |

(170,912 |

) |

The following table presents the segment assets as of December 31, 2014 compared to December 31, 2013 (in thousands):

|

|

|

December 31, 2014 |

|

December 31, 2013 |

| ||

|

Inpatient services |

|

$ |

4,381,044 |

|

$ |

4,213,835 |

|

|

Rehabilitation services |

|

322,268 |

|

372,241 |

| ||

|

Other services |

|

44,814 |

|

48,634 |

| ||

|

Corporate and eliminations |

|

393,282 |

|

502,295 |

| ||

|

Total assets |

|

$ |

5,141,408 |

|

$ |

5,137,005 |

|

FC-GEN Operations Investment, LLC and Subsidiaries

Notes to Consolidated Financial Statements

The following table presents the segment goodwill as of December 31, 2014 compared to December 31, 2013 (in thousands):

|

|

|

December 31, 2014 |

|

December 31, 2013 |

| ||

|

|

|

|

|

|

| ||

|

Inpatient services |

|

$ |

132,756 |

|

$ |

132,756 |

|

|

Rehabilitation services |

|

25,097 |

|

25,097 |

| ||

|

Other services |

|

11,828 |

|

11,828 |

| ||

|

Total goodwill |

|

$ |

169,681 |

|

$ |

169,681 |

|

(7) Restricted Cash and Investments in Marketable Securities

The current portion of restricted cash and investments in marketable securities principally represents an estimate of the level of outstanding self-insured losses the Company expects to pay in the succeeding year through its wholly owned captive insurance company. See note 17 — “Commitments and Contingencies — Loss Reserves For Certain Self-Insured Programs.”

Restricted cash and equivalents and investments in marketable securities at December 31, 2014 consist of the following (in thousands):

|

|

|

|

|

|

|

Unrealized losses |

|

|

| |||||||

|

|

|

Amortized |

|

Unrealized |

|

Less than |

|

Greater |

|

Fair value |

| |||||

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

|

Restricted cash and equivalents: |

|

|

|

|

|

|

|

|

|

|

| |||||

|

Cash |

|

$ |

35,791 |

|

$ |

— |

|

$ |

— |

|

$ |

— |

|

$ |

35,791 |

|

|

Money market funds |

|

599 |

|

— |

|

— |

|

— |

|

599 |

| |||||

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

|

Restricted investments in marketable securities: |

|

|

|

|

|

|

|

|

|

|

| |||||

|

Mortgage/government backed securities |

|

8,499 |

|

— |

|

(27 |

) |

— |

|

8,472 |

| |||||

|

Corporate bonds |

|

38,704 |

|

238 |

|

(4 |

) |

(60 |

) |

38,878 |

| |||||

|

Government bonds |

|

62,246 |

|

997 |

|

(19 |

) |

(224 |

) |

63,000 |

| |||||

|

|

|

$ |

145,839 |

|

$ |

1,235 |

|

$ |

(50 |

) |

$ |

(284 |

) |

146,740 |

| |

|

Less: Current portion of restricted investments |

|

|

|

|

|

|

|

|

|

(38,211 |

) | |||||

|

Long-term restricted investments |

|

|

|

|

|

|

|

|

|

$ |

108,529 |

| ||||

FC-GEN Operations Investment, LLC and Subsidiaries

Notes to Consolidated Financial Statements

Restricted cash and equivalents and investments in marketable securities at December 31, 2013 consist of the following (in thousands):

|

|

|

|

|

|

|

Unrealized losses |

|

|

| |||||||

|

|

|

Amortized |

|

Unrealized |

|

Less than |

|

Greater |

|

Fair value |

| |||||

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

|

Restricted cash and equivalents: |

|

|

|

|

|

|

|

|

|

|

| |||||

|

Cash |

|

$ |

11,386 |

|

$ |

— |

|

$ |

— |

|

$ |

— |

|

$ |

11,386 |

|

|

Money market funds |

|

1,072 |

|

— |

|

— |

|

— |

|

1,072 |

| |||||

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

|

Restricted investments in marketable securities: |

|

|

|

|

|

|

|

|

|

|

| |||||

|

Mortgage/government backed securities |

|

5,500 |

|

58 |

|

— |

|

— |

|

5,558 |

| |||||

|

Corporate bonds |

|

39,856 |

|

454 |

|

(160 |

) |

— |

|