Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - ROYAL HAWAIIAN ORCHARDS, L.P. | Financial_Report.xls |

| EX-32.1 - EXHIBIT 32.1 - ROYAL HAWAIIAN ORCHARDS, L.P. | ex32-1.htm |

| EX-31.1 - EXHIBIT 31.1 - ROYAL HAWAIIAN ORCHARDS, L.P. | ex31-1.htm |

| EX-23.1 - EXHIBIT 23.1 - ROYAL HAWAIIAN ORCHARDS, L.P. | ex23-1.htm |

| EX-11.1 - EXHIBIT 11.1 - ROYAL HAWAIIAN ORCHARDS, L.P. | ex11-1.htm |

| EX-21.1 - EXHIBIT 21.1 - ROYAL HAWAIIAN ORCHARDS, L.P. | ex21-1.htm |

| EX-10.27 - EXHIBIT 10.27 - ROYAL HAWAIIAN ORCHARDS, L.P. | ex10-27.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2014

1-9145

Commission File Number

ROYAL HAWAIIAN ORCHARDS, L.P.

(Exact name of registrant as specified in its charter)

|

STATE OF DELAWARE |

99-0248088 | |

|

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

688 Kinoole Street, Suite 121, Hilo, Hawaii 96720

(Address of principal executive offices)

Registrant’s telephone number, including area code: (808) 747-8471

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT: NONE

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT:

|

Title of Each Class |

Name of Each Exchange on Which Registered | |

|

Depositary Units Representing |

None (OTCQX) |

Indicate by check mark if the registrant is a well-known seasoned issuer as defined in Rule 405 of the Securities Act Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 of 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ☐ |

Accelerated filer ☐ | |

|

Non-accelerated filer ☐ |

Smaller reporting company ☒ | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Securities Exchange Act of 1934). Yes ☐ No ☒

The aggregate market value of registrant’s voting and non-voting equity (consisting of Class A Units) held by non-affiliates as of June 30, 2014, was $9,778,607 based on the last reported sales price on the OTCQX on that date of $2.92 per Unit.

The number of outstanding Class A Units as of March 27, 2015, was 11,100,000.

DOCUMENTS INCORPORATED BY REFERENCE

None.

| Page | ||

|

PART I | ||

|

ITEM 1. |

2 | |

|

ITEM 1A. |

5 | |

|

ITEM 1B. |

17 | |

|

ITEM 2. |

17 | |

|

ITEM 3. |

19 | |

|

ITEM 4. |

19 | |

|

PART II | ||

|

ITEM 5. |

MARKET FOR REGISTRANT’S UNITS, RELATED UNITHOLDER MATTERS AND ISSUER PURCHASES OF UNITS |

20 |

|

ITEM 6. |

20 | |

|

ITEM 7. |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

21 |

|

ITEM 7A. |

27 | |

|

ITEM 8. |

28 | |

|

ITEM 9. |

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE |

29 |

|

ITEM 9A. |

29 | |

|

ITEM 9B. |

29 | |

|

PART III | ||

|

ITEM 10. |

30 | |

|

ITEM 11. |

32 | |

|

ITEM 12. |

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED UNITHOLDER MATTERS |

36 |

|

ITEM 13. |

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE |

36 |

|

ITEM 14. |

37 | |

|

PART IV | ||

|

ITEM 15. |

40 | |

FORWARD-LOOKING STATEMENTS

Statements that are not historical facts contained in or incorporated by reference into this prospectus are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). The words “anticipate,” “goal,” “seek,” “project,” “strategy,” “future,” “likely,” “may,” “should,” “will,” “estimate,” “expect,” “plan,” “intend,” “target” and similar expressions and references to future periods, as they relate to us, are intended to identify forward-looking statements. Forward-looking statements include statements we make regarding:

|

|

● |

projections of revenues, expenses, income or loss; |

|

● |

our plans, objectives and expectations, including those relating to regulatory actions, business plans, products or services; |

|

● |

expected costs to produce kernel; |

|

● |

renewal of trademark; |

|

● |

ability to pass along increased costs; |

|

● |

improvement in gross margins; |

|

● |

future economic performance; |

|

● |

water needs of maturing orchards and effects on production of insufficient irrigation; |

|

● |

industry trends; |

|

● |

use of nut-in-shell inventories for manufacture of branded products; |

|

● |

relations with employees; |

|

● |

plans with respect to phase 2 of drying plant, including capacity and completion date; |

|

● |

assumptions impacting expenses and liabilities related to our pension obligations; |

|

● |

anticipated contributions to our pension plan; |

|

● |

lower yields and cash flows from newer orchards; |

|

● |

anticipated nut production; |

|

● |

expansion plans for the branded products segment, including gaining greater shelf space, increasing market share, the number of stores we expect to be in by the end of 2015 and introduction of new products; |

|

● |

anticipated increase in slotting fees and impact on results of operations; |

|

● |

estimated amount of working capital needed to fund expansion plans; |

|

● |

seasonality of nut production and sales of branded products; |

|

● |

our ability to engage third parties to process our nuts and the cost of such processing; |

|

● |

our ability to sell or find replacement buyers for nut production no longer subject to nut purchase contracts; |

|

● |

factors that influence consumer purchases; |

|

● |

consumer demands regarding food standards and their impact on our costs and operating results; |

|

● |

potential loss of shelf space; |

|

● |

reliance on two manufacturers; |

|

● |

delays in production or delivery of nuts; |

|

● |

use of herbicides, fertilizers and pesticides; |

|

● |

a lessor’s exercise of its contractual right to take back orchards; and |

|

● |

impact of new accounting rules. |

Forward-looking statements reflect our current views with respect to future events and are subject to certain risks, uncertainties and assumptions. Our actual results could differ materially from those in such statements. Factors that could cause actual results to differ from those contemplated by such forward-looking statements include, without limitation:

|

● |

the factors discussed in the “Risk Factors” section of this Annual Report on Form 10-K; |

|

● |

changing interpretations of accounting principles generally accepted in the U.S.; |

|

● |

outcomes of litigation, claims, inquiries or investigations; |

|

● |

world market conditions relating to macadamia nuts; |

|

● |

the weather and local conditions in Hawaii affecting macadamia nut production; |

|

● |

legislation or regulatory environments, requirements or changes adversely affecting our businesses; |

|

● |

general economic conditions; |

|

● |

geopolitical events and regulatory changes; |

|

● |

our ability to retain and attract skilled employees; |

|

● |

our success in finding purchasers for our macadamia nut production at acceptable prices; |

|

● |

increasing competition in the snack food market; |

|

● |

the availability of and our ability to negotiate acceptable agreements with third parties that are necessary for our business, including those with manufacturers, nut processors, co-packers, and distributors; |

|

● |

market acceptance of our products in the branded segment; |

|

● |

the availability and cost of raw materials; |

|

● |

changes in fuel and labor costs; |

|

● |

nonperformance by our largest customer; and |

|

● |

our success at managing the risks involved in the foregoing items. |

Forward-looking statements speak only as of the date on which such statements are made. We undertake no obligation to update any forward-looking statement, whether as a result of new information, future events or otherwise. All forward-looking statements are expressly qualified by these cautionary statements.

Part I

|

BUSINESS OF THE PARTNERSHIP |

Royal Hawaiian Orchards, L.P. (the “Partnership”) is a master limited partnership organized under the laws of the State of Delaware in 1986. The Partnership is managed by its sole general partner, Royal Hawaiian Resources, Inc. (the “Managing Partner”), which is a wholly owned subsidiary of the Partnership. On October 1, 2012, the Partnership changed its name from ML Macadamia Orchards, L.P. to Royal Hawaiian Orchards, L.P. to better enable the Partnership to brand its products. Royal Hawaiian was the original brand name used to market the macadamia nuts grown from 1946 until 1973 on the acreage that now comprises our orchards. Branded product sales are made through the Partnership’s wholly owned subsidiary Royal Hawaiian Macadamia Nut, Inc. (“Royal”). Unless the context otherwise requires, Royal Hawaiian Orchards, L.P. and its subsidiaries are referred to in this report as the Partnership and “we.”

Our principal executive offices are located at 688 Kinoole Street, Suite 121, Hilo, Hawaii 96720 and our telephone number is (808) 969-8057. Our Depositary Units Representing Class A Units of Limited Partnership Interests (“Units”) are currently traded on the OTCQX platform under the symbol “NNUTU.”

Overview

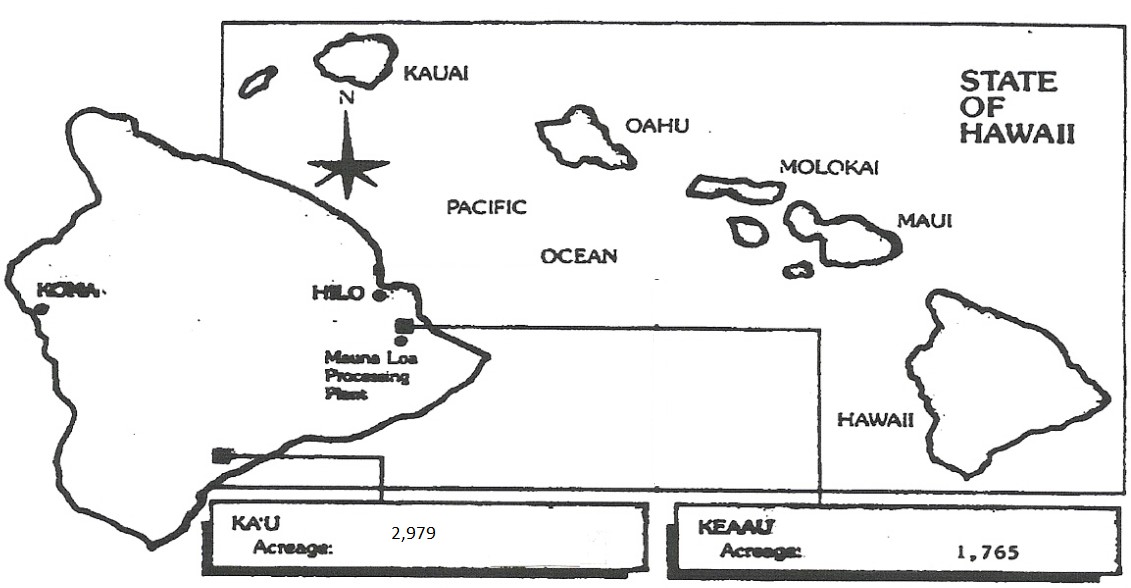

We are a vertically integrated producer, marketer and distributor of high-quality macadamia nut-based products. We are the largest macadamia nut farmer in Hawaii, farming approximately 4,744 tree acres of orchards that we own or lease in two locations on the island of Hawaii. We also farm approximately 1,047 tree acres of macadamia orchards in Hawaii for other orchard owners.

The Partnership was formed as an MLP in 1986 owning macadamia nut orchards on owned and leased land. Vertical integration of our business began in 2000 with the acquisition of farming operations from subsidiaries of C. Brewer and Company, Ltd. In 2012, we moved toward further vertical integration by beginning to manufacture and sell a line of macadamia snacks under the brand name ROYAL HAWAIIAN ORCHARDS®. In 2014, we completed construction of the first phase of our drying facility, which allows us more control over processing our nuts.

Business Segments

We have two business segments: orchards and branded products. The orchards segment includes our orchard, farming and processing operations. The branded products segment includes the development, manufacture and sale of branded products and the sale of processed kernel.

Information concerning industry segments is set forth in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and Note 3 to the Consolidated Financial Statements included in Part II, Item 8 of this Annual Report on Form 10-K.

Orchards Segment

The orchards segment grows and farms macadamia nuts for sale Wet-In-Shell (“WIS”), for sale to our branded products segment and on a contract basis for other orchard owners. The segment also includes the processing of macadamia nut to kernel for our branded products segment.

From 1986 through 2006 and from 2010 through the end of 2012, we sold all of our nut production to Mauna Loa Macadamia Nut Corporation (“Mauna Loa”), pursuant to various agreements with Mauna Loa. Since 2013, we have reduced the number of pounds that we have sold to Mauna Loa and as of January 1, 2015, only three long-term agreements remain, which represented approximately 21% and 16% of our production in 2014 and 2013, respectively.

Nuts to be retained by us for use in our branded products segment will be dried and then sent to a processor for shelling. In November 2014, the Partnership completed the construction of the first phase of its drying facility located in the Ka’u district of the Big Island, near our producing orchards, and we began drying a portion of our WIS nuts harvested from our orchards. The second, and last, phase of the drying plant will commence in 2015, giving us the ability to dry all of our nuts that are not sold WIS.

Competition. In addition to the State of Hawaii, mature macadamia nut orchards are located in Australia, Africa, and Central and South America. For the 2014 world crop, Hawaii supplied 9.0%, Australia supplied 30.6%, South Africa supplied 30.1% and other parts of Africa, and Latin and South America supplied the remaining 30.3%. In 2014, we supplied about 42% of the Hawaiian crop from its orchards. The orchards we farm for others supplied about 18% of the Hawaiian crop.

Macadamia Farming. Through June 30, 2014, we farmed approximately 5,070 tree acres of macadamia nut orchards. Following the termination of the lease for our Mauna Kea orchard effective June 30, 2014, owned or leased tree acreage decreased to 4,744 acres. Through December 30, 2014, the Partnership farmed 1,100 tree acres of macadamia orchards owned by others under farming contracts. Following the termination of a farming contract for orchards located in the area of the Mauna Kea orchard effective January 1, 2015, farming of macadamia orchards owned by others under farming contracts decreased to 1,047 acres.

All orchards are located in two separate regions on the island of Hawaii (“Keaau” and “Ka’u”). Because each region has different terrain and weather conditions, farming methods vary somewhat among the locations.

Branded Products Segment

In 2012, we commenced marketing branded products under the ROYAL HAWAIIAN ORCHARDS® brand name. As of December 2014, our branded products were in approximately 10,000 grocery, natural foods and mass merchant stores nationwide. Key elements of our branded product strategy are as follows:

Capitalize on the Health Benefits of Macadamia Nuts. Our strategy is to capitalize on consumers’ views of nuts as a healthy snack that can command prices above traditional mass-marketed products. According to research conducted by Mintel International, consumers view fruit and nuts as the number one and two healthiest snacks. Our products contain no artificial ingredients, contain no genetically modified organisms (“GMOs”), are gluten-free, and have no sulfites. We are leveraging the existing nutritional properties inherent in tree nuts in our line of macadamia-based healthy snacks. Our strategy is based on promoting the health benefits of macadamia nuts, which are similar to those of almonds, a food product that has achieved strong market positioning based on growing consumer awareness of associated wellness properties. As part of this strategy, the Partnership sells two product lines of better for you macadamia snacks under the brand name ROYAL HAWAIIAN ORCHARDS®.

Distribute Our Products through Retailers that Target Consumers who Desire Premium Healthy Snacks. We sell our products to national, regional and independent grocery and drug store chains, as well as mass merchandisers, club stores and other retail channels, that target consumers with healthy eating habits and the disposable income necessary to afford premium products. In accordance with this strategy, we seek to secure product placement in mainstream aisles. We believe this leads more consumers to purchase our products. Early reaction from retailers has been positive, and we estimate that as of December 31, 2014, we have products in retail distribution in approximately 10,000 stores in the United States and expect to be in 20,000 stores by the end of 2015.

Mitigate our Exposure to Fluctuating Commodity Prices. By pursuing a branded product strategy and continuing to farm macadamia nuts, we believe that we have a pricing advantage because we are able to produce nuts from our own orchards at a relatively fixed and currently favorable cost and do not have to compete to purchase nuts from third parties. Furthermore, we believe that if wholesale market prices for macadamia nuts decline below our actual production costs, we would be better positioned to profitably sell the nuts as branded products, thereby mitigating our exposure to fluctuating market prices.

Use of Co-packers. Royal has contracted with third-party manufacturers, also known as co-packers, in California to manufacture the ROYAL HAWAIIAN ORCHARDS® branded products. Utilizing co-packers provides us with the flexibility of producing different products and the ability to develop new products quickly and economically. We selected our co-packers based on production capabilities in producing products of these types.

Customers. Royal markets its retail products to wholesale customers directly and using food brokers, and markets to consumers through Royal’s e-commerce site. The food brokers represent multiple manufacturers and are paid a percentage of sales. Royal’s customers are mainly wholesale distributors, natural food and grocery stores and specialty retailers that purchase the products under payment terms approved by Royal based on their creditworthiness. Royal’s customers resell the macadamia nut products to end-consumers in retail outlets in the United States.

Marketing Strategy. Royal’s marketing strategy focuses on building brand awareness for its brand and line of better for you macadamia snacks using social media, grassroots marketing such as sampling, public relations and participation in community events and festivals. We launched a combination website and integrated e-commerce store at www.royalhawaiianorchards.com in 2012 and also sell our products on Amazon. Royal also uses Facebook and Twitter accounts and several other strategies to build its customer base. A key marketing strategy is consistent social media presence, where Royal can connect directly with potential target consumers.

Product Distribution. We developed a product distribution network to support sales growth and provide superior customer service in an efficient manner. Distribution of our products is performed either directly from our co-packers or through a third-party distribution center. We primarily use common carriers to deliver products from these distribution points to our customers.

Competition. The snack food market is highly competitive. Our products compete against food and snack products sold by many regional and national companies, some of which are substantially larger and have greater resources than the Partnership. We believe that additional competitors will enter the markets in which we operate. We also compete for shelf space of retail grocers, convenience stores, drug stores, mass merchandisers, natural food stores and club stores. As these retailers consolidate, the number of customers and potential customers declines and their purchasing power increases. We compete primarily on the basis of product quality, ability to satisfy specific consumer needs (including gluten-free needs), brand recognition, brand loyalty, service, marketing, advertising and price. Substantial advertising and promotional expenditures are required to maintain or improve a brand’s market position or to introduce a new product, and participants in our industry are engaging with new media, including customer outreach through social media and web-based vehicles, which require additional staffing and financial resources. Our largest principal competitors are Blue Diamond Growers, Diamond Foods, Paramount Farms and Mauna Loa, each of which has substantially greater market presence, longer operating histories, better distribution, and greater financial, marketing, capital and other resources than we have.

Environmental Matters. Our operations are subject to various federal, state and local environmental laws and regulations. We believe the Partnership is in compliance with all material environmental regulations affecting our facilities and operations and that expending resources for continued compliance will not have a material impact on our business, financial condition or results of operations.

Research and Development. We consider research and development of new products to be a significant part of our overall philosophy, and we are committed to developing new products that incorporate macadamia nuts. As we expand our snack nut product range, we believe we can gain greater shelf space in retail stores and increase our market share. We plan to introduce convenient, on-the-go, portion-sized packages that appeal to health-conscious consumers. We believe that our innovations differentiate our products from those of our competitors, leading to increased brand loyalty and higher consumer awareness. In addition to developing new products, we are focused on improving our existing products and are making incremental improvements based on customer feedback.

Trademarks and Patents. We market and sell our products primarily under the ROYAL HAWAIIAN ORCHARDS® brand, which is protected with trademark registration with the U.S. Patent and Trademark Office, as well as in various other jurisdictions. We expect to continue to maintain this trademark in effect. We have no patents.

Governmental Regulations

As an agricultural company, we are subject to extensive government regulation, including regulation of the manner in which we cultivate and fertilize as well as process our macadamia nuts. Furthermore, the branded products segment of our business subjects us to additional regulation regarding the manufacturing, distribution, and labeling of our products.

Manufacturers and marketers of food products are subject to extensive regulation by the Food and Drug Administration (“FDA”), the United States Department of Agriculture (“USDA”), and other national, state and local authorities. The Food, Drug and Cosmetic Act and the new Food Safety Modernization Act and their regulations govern, among other things, the manufacturing, composition and ingredients, packaging and safety of foods. Under these acts, the FDA regulates manufacturing practices for foods through its current “good manufacturing practices” regulations, imposes ingredient specifications and requirements for many foods, inspects food facilities and issues recalls for tainted food products. Additionally, the USDA has adopted regulations with respect to a national organic labeling and certification program.

Food manufacturing facilities and products are also subject to periodic inspection by federal, state and local authorities. State regulations are not always consistent with federal or other state regulations.

Seasonality

While sales of our branded products are anticipated to be only slightly seasonal, with the fourth quarter of the calendar year somewhat higher, macadamia nut production is very seasonal, with the largest quantities typically being produced and then inventoried from September through November, resulting in large inventories that will be converted into finished product and sold throughout the following year.

Significant Customers

Nut Sales. From 1986 through 2006 and from 2010 through the end of 2012, we sold all of our nut production to Mauna Loa pursuant to various agreements with Mauna Loa. On August 1, 2010, we assumed three long-term agreements expiring in 2029, 2078 and 2080 with Mauna Loa under which all macadamia nuts produced from the orchards acquired from International Air Service Co., Ltd. (“IASCO”), which represented approximately 21% and 16% of our production in 2014 and 2013, respectively, must be sold to and purchased by Mauna Loa at a predetermined price.

In addition, on January 31, 2011, we entered into three nut purchase contracts with Mauna Loa for the sale of the balance of our production (i.e., production from properties excluding the IASCO orchards), which represented approximately 79% and 84% of our production in 2014 and 2013, respectively, with approximately one-third of such production covered by a one-year agreement that expired December 31, 2012 (“ML Contract A”), one-third of such production covered by a two-year agreement that expired December 31, 2013 (“ML Contract B”), and one-third of such production covered by a three-year agreement that expired December 31, 2014 (“ML Contract C”) (collectively “ML Contracts”), each at a fixed price. The staggered expiration dates were designed to (i) normalize the effects of market price volatility by requiring annual renegotiation of pricing for only one-third of the non-IASCO volume and (ii) allow either party to exit the relationship gradually if it chose not to renew the expiring contracts.

The Partnership and Mauna Loa have not extended any of the ML Contracts. As a result, ML Contract A, ML Contract B and ML Contract C expired December 31, 2012, 2013, and 2014 respectively.

Under the IASCO agreements, we are paid based on WIS pounds at a price that is derived annually from a formula that factors in the Mauna Loa wholesale price of the highest year-to-date volume fancy and choice products sold in Hawaii and the USDA National Agricultural Statistics Service (“NASS”) reported price of WIS Hawaii macadamia nuts for the period of delivery. If the Final NASS Report for the year contains a price or moisture that varies from that used in the formula price calculations for nuts delivered during the year, then an adjustment is made between the parties. The NASS nut price for the crop year ended June 30, 2014 was $0.87 per WIS pound. In 2014, the Partnership recorded additional nut revenue of $89,000 on the production from the IASCO orchards delivered in 2013. In 2014 and 2013, the average price received from Mauna Loa per WIS pound amounted to $0.81 and $0.78, respectively. The price adjustment for 2014 production from the IASCO orchards will be calculated in the second quarter of 2015 when the NASS price of macadamia nuts is published.

On July 14, 2014, the Partnership entered into a Macadamia Nut Purchase Agreement (the “2014 Short-Term Agreement”) with Mauna Loa, effective July 1, 2014 through October 31, 2014, which required the Partnership to sell and Mauna Loa to purchase a minimum of 4 million pounds of WIS macadamia nuts adjusted to 20% moisture and 30% kernel recovery at $1.00 per pound. The Partnership sold 4 million pounds of WIS nuts under this contract and received $2.6 million. The 2014 Short-Term Agreement was in addition to ML Contract C, which expired on December 31, 2014.

Employees

As of December 31, 2014, the Partnership employed 269 people: 76 full-time employees; 186 seasonal employees; and seven part-time employees. Of the total, 21 are in farming supervision and management, 232 are in production, maintenance and agricultural operations, 14 are in accounting and administration, and 2 are in sales.

The Partnership is a party to two collective bargaining agreements with the International Longshore and Warehouse Union (“ILWU”) Local 142. These agreements cover all production, maintenance and agricultural employees of the Ka’u and Keaau Orchards. On June 20, 2013, the Partnership and the ILWU Local 142 agreed to two new three-year contracts, which are effective June 1, 2013 through May 31, 2016. Although the Partnership believes that relationships with its employees and the ILWU are good, there is no assurance that the Partnership will be able to extend these agreements on terms satisfactory to them when they expire.

Taxation

The Partnership has a grandfathered tax status, which allows it to be treated as a partnership for tax purposes, even though it is publically traded, provided that it pays a 3.5% federal tax on gross income from the active conduct of the trade and business of the Partnership. The Partnership will cease to be treated as a partnership for tax purposes if the Partnership engages in a substantially new line of business. A substantially new line of business conducted through a wholly owned corporate subsidiary of the Partnership is not deemed to be a new line of business for tax purposes. Accordingly, the Partnership manufactures, markets and sells its branded products through its wholly owned corporate subsidiary, Royal. The Partnership intends to maintain its status of being taxed as a partnership under the above-referenced provisions.

|

ITEM 1A. |

RISK FACTORS |

Our business, financial condition, and results of operations are subject to significant risks. We urge you to consider the following risk factors in addition to the other information contained in, or incorporated by reference into, this Form 10-K and our other periodic reports filed with the Securities and Exchange Commission (the “SEC”). If any of the following risks actually occur, our business, financial condition, results of operations or cash flows could be materially adversely affected.

ROYAL HAWAIIAN ORCHARDS® products were launched in November 2012 and have a limited retail distribution history. Our future ability to grow our revenues depends upon continued sell-in and sell-through sales of these new products.

Prior to November 2012, we had never pursued the sale of macadamia nut products to customers or the sale of nuts in kernel form to others for incorporation into their products. Any adverse developments with respect to the sale of ROYAL HAWAIIAN ORCHARDS® macadamia products could significantly reduce revenues and have a material adverse effect on our ability to achieve profitability and future growth. We cannot be certain that we will be able to continue to commercialize our macadamia products or that our products will be accepted in retail markets. Specifically, the following factors, among others, could affect continued market acceptance, revenues and profitability of ROYAL HAWAIIAN ORCHARDS® snack products:

|

● |

the introduction of competitive products into the healthy snack market; | |

|

● |

the level and effectiveness of our sales and marketing efforts; | |

|

● |

any unfavorable publicity regarding nut products or similar products; | |

|

● |

litigation or threats of litigation with respect to these products; | |

|

● |

the price of the product relative to other competing products; | |

|

● |

price increases resulting from rising commodity costs; | |

|

● |

regulatory developments affecting the manufacture, marketing or use of these products; and | |

|

● |

the inability to gain significant customers. |

There is no assurance that this effort will be successful or that we will receive a return on our investment.

We have historically depended on a single nut purchaser.

From 1986 through 2006 and from 2010 through 2012, we relied upon a single customer, Mauna Loa, to purchase all of the nuts that we produced under various nut purchase agreements, which required us to sell and Mauna Loa to buy all of our production of macadamia nuts at various prices. At December 31, 2012 and 2013, we and Mauna Loa did not extend ML Contract A and ML Contract B, respectively, and we retained part of our 2013 and 2014 crops previously covered by such contracts to support our own branded product development and marketing efforts. We entered into the 2014 Short-Term Agreement to sell 4.0 million pounds of WIS nuts to Mauna Loa from July 14, 2014 to October 31, 2014, representing approximately 46% of the crop that we had planned to retain, for $1.00 per adjusted WIS pound. Although we reduced the volume sold to Mauna Loa, Mauna Loa remains a significant customer, and any disruption of the Mauna Loa relationship could significantly adversely affect us if we are not able to find alternative purchasers of our nut production at comparable prices. We rely on Mauna Loa’s timely performance and payment under the nut purchase agreements. If Mauna Loa were to breach its obligation to pay for the macadamia nuts delivered, we would suffer substantial financial difficulty due to the loss of one of our major sources of revenue and cash flow, and we would need to seek another buyer for some or all of the nuts. Although we believe we could find other buyers for our nuts based on current market conditions, there could be delays or disruption in sales depending upon the available processing capacity and purchasing commitments of various buyers. If Mauna Loa were late in making payments to us, we could stop the delivery of macadamia nuts. However, if the WIS macadamia nuts are not husked and dried within a limited amount of time, they will deteriorate and have no commercial value. Accordingly, any cessation of shipments is only a short-term response. In order to preserve commercial value in our nut production if Mauna Loa were not making payments, we would need to process the nuts ordinarily purchased and processed by Mauna Loa. Although we have a drying facility, we may not have the extra capacity to dry the nuts that were to be purchased by Mauna Loa, and there can be no assurance that other Hawaiian processors could process the extra volume before the nuts deteriorate.

We are subject to risks relating to fixed-price and market-price nut purchase agreements.

There are three long-term agreements requiring Mauna Loa to purchase the nuts from the IASCO orchards. They expire in 2029, 2078 and 2080 and provide for market-determined prices. For the orchards other than the IASCO orchards, there was one fixed price nut purchase contract with Mauna Loa, ML Contract C, representing approximately 31% of our total production for 2014 that expired December 31, 2014. Although fixed-price contracts provide protection against adverse declines in market prices, fixed-price contracts can be disadvantageous because we may not be able to pass on unexpected cost increases as they arise or may find that the spot price for nuts materially exceeds this fixed price. On the other hand, a market-price mechanism subjects us to the risk of a decline in world macadamia nut prices, which may or may not result in a price that covers our cost of production.

We may not be able to find buyers for our nuts that were previously sold to Mauna Loa pursuant to nut purchase agreements that have expired.

Our ML Contract A with Mauna Loa expired on December 31, 2012, ML Contract B expired on December 31, 2013 and ML Contract C expired on December 31, 2014. Production that we no longer sell to Mauna Loa (estimated to be 18.5 million pounds of WIS nuts in 2015) will be utilized to make our branded products for retail distribution or processed and sold. We believe that given the current market prices for macadamia nuts, we will be able to sell or find replacement buyers for the nut production that is no longer subject to a nut purchase contract. However, there is no assurance that we can find new buyers or that such new customers will be creditworthy and able to pay for nuts delivered. If there is not sufficient demand for our branded products and we are unable to secure buyers for the nuts from the expired contracts, sales will decrease and our results of operation and financial condition will be adversely impacted.

At this time, we do not have the capacity to dry all of our nuts or the ability to process any of our nut production, which could limit our ability to contract for timely processing of nuts at an acceptable quality and cost and could require us to sell a portion of our nuts in Hawaii at prices below those that could be obtained outside of Hawaii.

Macadamia nuts are harvested wet-in-shell and will rapidly deteriorate if they are not promptly dried. Once the nuts are husked and dried, they can be shipped to customers or processors that are not on the island of Hawaii. We completed construction of the first phase of our drying facility in November 2014, which has the capacity to dry 12 million WIS pounds. The second phase is scheduled to be completed in 2015. This will give us the flexibility to consider processors and purchasers for our nuts both on and off of the island of Hawaii. If the construction of the second phase of the drying facility is not completed in a timely manner, we will need to continue to have a processor on the island of Hawaii process or purchase some of our nuts. Our current inability to dry all of our nuts, which could require us to continue to utilize third party processors in Hawaii to process or buy nuts, could have a material adverse impact on the prices that we may be able to obtain for our nuts compared to the price we could obtain if we were able to ship the nuts outside of Hawaii, and we might not be able to sell our nuts at all. Such limitation could also reduce the amount of nuts available for our branded products. Either event would have a material adverse effect on our financial condition, business and results of operations. In addition, we will be contracting with other third parties to process our nuts, but there is no assurance that we will be able to contract for the timely processing of nuts at an acceptable quality and cost. Processing nuts outside of Hawaii could also subject the Partnership to risks of damage or loss of nuts in transit.

A disruption at any of our production facilities would significantly decrease production, which could increase our cost of sales and reduce our net sales and income from operations.

We plan to dry our nuts at our new drying plant and process and manufacture into products at third-party processor and manufacturing facilities. A temporary or extended interruption in operations at any of these facilities, whether due to technical or labor difficulties, destruction or damage from fire, flood or earthquake, infrastructure failures such as power or water shortages, raw material shortage or any other reason, whether or not covered by insurance, could interrupt our process and manufacturing operations, disrupt communications with our customers and suppliers and cause us to lose sales and write off inventory. Any prolonged disruption in the operations of these facilities would have a significant negative impact on our ability to manufacture and package our products on our own and may cause us to seek additional third-party arrangements, thereby increasing production costs or in the case of our drying facility, prevent us from having sufficient nuts for our branded products business. These third parties may not be as efficient as we and our current processors and manufacturers are and may not have the capabilities to process and package some of our products, which could adversely affect sales or operating income. Further, current and potential customers might not purchase our products if they perceive our lack of alternate manufacturing facilities to be a risk to their continuing source of products.

We are dependent on third-party manufacturers to manufacture all of our products, and the loss of a manufacturer or the inability of a manufacturer to fulfill our orders could adversely affect our ability to make timely deliveries of product.

We currently rely on and may continue to rely on two manufacturers to produce all of our branded products. If either manufacturer were unable or unwilling to produce sufficient quantities of our products in a timely manner or renew contracts with us, we would have to identify and qualify new manufacturers, and we may be unable to do so. Due to industry and customer requirements that manufacturers of food products be certified and/or audited for compliance with food safety standards, the number of qualified manufacturers is constrained. As we expand our operations, we may have to seek new manufacturers and suppliers or enter into new arrangements with existing ones. However, only a limited number of manufacturers may have the ability to produce a high volume of our products, and it could take a significant period of time to locate and qualify such alternative production sources. In addition, we may encounter difficulties or be unable to negotiate pricing or other terms as favorable as those that we currently enjoy.

There can be no assurance that we would be able to identify and qualify new manufacturers in a timely manner or that such manufacturers could allocate sufficient capacity to meet our requirements, which could materially adversely affect our ability to make timely deliveries of product. In addition, there can be no assurance that the capacity of our current manufacturers will be sufficient to fulfill our orders, and any supply shortfall could materially and adversely affect our business, results of operations, and financial condition. Currently, some of our products are produced by a single third-party source that maintains only one facility. The risks of interruption described above are exacerbated with respect to such single-source, single-facility manufacturer.

Our manufacturers are required to comply with quality and food production standards. The failure of our manufacturers to maintain the quality of our products could adversely affect our reputation in the market place and result in product recalls and product liability claims.

Our manufacturers are required to maintain the quality of our products and to comply with our product specifications and requirements for certain certifications for food safety from third-party organizations. In addition, our manufacturers are required to comply with all federal, state and local laws with respect to food safety. However, there can be no assurance that our manufacturers will continue to produce products that are consistent with our standards or in compliance with applicable laws and standards, and we cannot guarantee that we will be able to identify instances in which our manufacturers fail to comply with such standards or applicable laws. We would have the same issue with new suppliers. The failure of any manufacturer to produce products that conform to applicable standards could materially and adversely affect our reputation in the marketplace and result in product recalls, product liability claims and severe economic loss.

Any significant delays of shipments to or from our warehouses could adversely affect our sales.

Shipments to and from our warehouses could be delayed for a variety of reasons, including weather conditions, strikes, and shipping delays. Any significant delay in the shipments of product would have a material adverse effect on our business, results of operations and financial condition, and could cause our sales and earnings to fluctuate during a particular period or periods. We have from time to time experienced, and may in the future experience, delays in the production and delivery of product.

Our farming operations face a competitive labor market in Hawaii.

Our farming operations require a large number of workers, many on a seasonal basis. The labor market on the island of Hawaii is very competitive, and most of our employees are unionized under contracts that expire in May 2016. In the event that we are not able to obtain and retain both permanent and seasonal workers to conduct our farming operations, or in the event that we are not able to maintain satisfactory relationships with our unionized workers, the Partnership’s financial results could be negatively impacted.

Our operations rely on certain key personnel who are critical to our business.

Our future operating results depend substantially upon the continued service of key personnel and our ability to attract and retain qualified management and technical and support personnel. We cannot guarantee success in attracting or retaining qualified personnel. There may be only a limited number of persons with the requisite skills and relevant industry experience to serve in those positions. Our business, financial condition and results of operations could be materially adversely affected by the loss of any of our key employees, by the failure of any key employee to perform in his or her current position, or by our inability to attract and retain skilled employees.

Our farming operations are subject to environmental laws and regulations, and any failure to comply could result in significant fines or clean-up costs.

We use herbicides, fertilizers and pesticides, some of which may be considered hazardous or toxic substances. Various federal, state, and local environmental laws, ordinances and regulations regulate our properties and farming operations and could make us liable for costs of removing or cleaning up hazardous or toxic substances on, under, or in property that we currently own or lease, that we previously owned or leased, or upon which we currently or previously conducted farming operations. These laws could impose liabilities without regard to whether we knew of, or were responsible for, the presence of hazardous or toxic substances. The presence of hazardous or toxic substances, or the failure to properly clean up such substances when present, could jeopardize our ability to use, sell or collateralize certain real property and result in significant fines or clean-up costs, which could adversely affect our business, financial condition and results of operations. Future environmental laws could impact our farming operations or increase our cost of goods.

Our business is subject to seasonal fluctuations.

Because we experience seasonal fluctuations in production and thus sales from our orchards, our quarterly results fluctuate, and our annual performance has depended largely on results from two quarters. Our business is highly seasonal, reflecting the general pattern of peak production and consumer demand for nut products during the months of October, November and December. Historically, a substantial portion of our revenues occurred during our third and fourth quarters, and we generally experienced lower revenues during our first and second quarters together with losses. Weather conditions may delay harvesting from December into early January, which may result in a fiscal year with lower than normal revenues. With the launch of our branded products business, WIS revenue continues to be highly seasonal, while branded products revenue is more evenly distributed throughout the year.

Our branded products require us to carry additional inventory, which increases our working capital needs and our reliance on generating additional income from sales or obtaining additional external financing.

Although branded products revenues are more evenly distributed throughout the year, this change has required us to carry larger quantities of inventory, increasing our working capital needs. If we are unable to generate additional working capital from product sales or obtain external financing, we may not be able to build the inventory necessary to maintain a sufficient and consistent supply of our branded products to meet customer demands, which could have a material adverse effect on our business, results of operations, liquidity, financial condition and brand image.

The price at which we can sell our macadamia nuts may not always exceed our cost of goods sold.

During 2014, under our nut sale contracts with Mauna Loa, we received between 60.3 and 80.6 cents per WIS pound. During 2014, our costs to farm and produce these macadamia nuts, including depreciation of the trees, varied between 58.1 cents and 72.4 cents per WIS pound (depending on the orchard) or an average of approximately 67 cents per WIS pound (exclusive of the Mauna Kea orchards sold in June 2014). As our fixed price contracts with Mauna Loa have expired and have not been renewed, we will no longer have our price set and therefore will be subject to the risk of market pricing for those nuts not used in our branded products business. Macadamia orchards are required to be cultivated and farmed in order to maintain the trees, even in years where the price at which the macadamia nuts could be sold do not cover the cost of goods sold in any specific orchard. In such event, we could suffer losses from certain orchards, and our financial performance could be adversely affected. There is no assurance that the prices of macadamia nuts in the future will exceed the costs.

Additional regulation could increase our costs of production, and our business could be adversely affected.

As an agricultural company, we are subject to extensive government regulation, including regulation of the manner in which we cultivate, fertilize and process our macadamia nuts. Furthermore, processing and selling our branded products subject us to additional regulations regarding the manufacturing, distribution, and labeling of our products. There may be changes to the legal or regulatory environment, and governmental agencies and jurisdictions where we operate may impose new manufacturing, importation, processing, packaging, storage, distribution, labeling or other restrictions, which could increase our costs and affect our financial performance.

Many of our production costs are not within our control, and we may not be able to recover cost increases in the form of price increases from our customers.

We purchase water, electricity and fuel, fertilizer, pesticides, equipment and other products to conduct our farming operations and produce macadamia nuts. Transportation costs, including fuel and labor, also represent a significant portion of the cost of our nuts. These costs could fluctuate significantly over time due to factors that may be beyond our control. Our business and financial performance could be negatively impacted if there are material increases in the costs we incur that are not offset by price increases for the products sold.

We are subject to the risk of product liability claims.

The production and sale of food products for human consumption involves the risk of injury to consumers. This risk increases as we move from primarily a farming operation into the marketing and sale of branded products. Although we believe we have implemented practices and procedures in our operations to promote high-quality and safe food products, we cannot assure you that consumption of our products will not cause a health-related illness or injury in the future or that we will not be subject to claims or lawsuits relating to such matters.

We rely upon external financing which is secured by a pledge of all of our real and personal property. If we are unable to comply with the terms of our loan agreements, we could lose our assets.

We rely on external financing, currently being provided by an Amended and Restated Credit Agreement with American AgCredit, PCA (“AgCredit”), through a revolving credit facility and two term notes. This agreement contains various terms and conditions, including financial ratios and covenants, and is secured by all of the real and personal property of the Partnership. The first term loan matures on July 1, 2020. The second term loan matures on March 27, 2021. The revolving credit facility matures on March 27, 2017. This Amended and Restated Credit Agreement prohibits distributions to partners, other than tax distributions, without the prior consent of the lender. On multiple occasions during the last several years and as recently as the end of 2014, the Partnership has failed to comply with various covenants or financial ratios under its loan agreements but has been able to obtain waivers or modifications of the agreement to avoid a default. If we are unable to meet the terms and conditions of our loan agreements or to obtain waivers or modifications of such loan agreements, we could be in default under our loan agreements, and the lender would be able to accelerate the obligations and foreclose on the collateral securing the indebtedness. There is no assurance that we will be able to comply with our loan facilities or obtain waivers or modifications in the future to avoid a default.

We could lose the production from certain orchards due to early lease termination privileges held by the lessor.

We lease approximately 1,596 tree acres of land for our orchard operations. One of these leases, approximately 266 tree acres, has produced an average of 1.1 million WIS pounds over the past five years and terminates in 2019. Another of these leases terminates in 2034 but allows the lessor to purchase the trees from the Partnership at fair market value in 2019. This lease accounts for approximately 327 tree acres that have produced an average of 1.5 million WIS pounds over the past five years. We believe that this lessor may exercise his rights to take back these orchards in 2019. If that were to happen, we would lose approximately 593 tree acres or 12% of our production, which loss could have a material adverse effect on our operations.

We are involved in lawsuits regarding our performance under two of our leases, and we may not be successful.

From time to time, we have disagreements with persons who lease orchards to us regarding our performance under the applicable lease agreement. At this time, a lessor who owns the approximately 266 and 327 tree acres subject to the leases described above, which produced approximately 1 million field pounds and 931,000 field pounds in 2014, respectively, has commenced litigation in Hawaii, claiming that we have breached the leases, thereby allowing the lessor to terminate the leases. We have denied these allegations and filed cross-claims against the lessor in this suit, and we intend to vigorously defend this claim. Prior to the date of the lessor’s suit, we had filed a suit in California against the lessor asserting damages for breach of contract and other claims. See Item 3-Legal Proceedings, below. If the lessor is successful in pursuing this claim, we would lose both of these leases and the acreage and nut production associated therewith, which could adversely affect our financial condition and results of operations.

Diseases and pests can adversely affect nut production.

Macadamia trees are susceptible to various diseases and pests that can affect the health of the trees and resultant nut production. There are several types of fungal diseases that can affect flower and nut development. One of these is Phytophthora capsici, which affects the macadamia flowers and developing nuts, and another, Botrytis cinerea, causes senescence of the macadamia blossom before pollination is completed. These types of fungal disease are generally controllable with fungicides. Historically, these fungi have infested the reproductive plant parts at orchards located in Keaau during periods of persistent inclement weather. Tree losses may occur due to a problem known as Macadamia Quick Decline (“MQD”). Research at the University of Hawaii indicates that this affliction is due to Phytophthora capsici, which is associated with high moisture and poor drainage conditions. The Keaau Orchards are areas with high moisture conditions and may be more susceptible to the MQD problem. Afflicted trees in these regions are replaced with cultivars that are intolerant to MQD. The Partnership’s Keaau orchards experienced tree replacement of 1.4% in 2014 and 3.0% in 2013.

Macadamia trees and production may also be affected by insects and other pests. The Southern Green Stink Bug disfigures the mature kernel and contributes to nut loss. The five-year historical nut loss due to the stink bug is 2.3%. Two natural enemies, a wasp and a fly, effectively keep nut losses at acceptable levels. An insect known as the Koa Seed Worm (“KSW”) causes full-sized nuts to fall that have not completed kernel development. The five-year average nut loss due to the KSW is 5.4%. The Tropical Nut Borer Beetle (“TNB”) bores through the mature macadamia shell and feeds on the kernel. Nut damage caused by the TNB is not recorded as a defect by Mauna Loa. However, field surveys in 2014 indicate that nut losses attributed to TNB is estimated to be around 1%. Damages caused by each insect may fluctuate when unfavorable environmental conditions affect the natural enemy population.

In March 2005 a new insect pest, the Macadamia Felted Coccid (“MFC”), or Eriococcus ironsidei, was detected on macadamia trees in the South Kona area on the island of Hawaii. The insect is originally from Australia, and it has the potential to become a serious problem on macadamia nut trees and cause leaf die-back, floret drop and in severe cases possible tree death. Surveys show that this pest is well distributed throughout the Partnership’s Ka’u orchards. Climatic conditions, particularly extremely dry weather, are conducive for increased pest activity. Due to good rainfall for most of 2014, tree damage from MFC is less than in previous years. We continue to work with other growers and the State of Hawaii to control this pest, but there is no assurance we will be successful, and if the insect infestation worsens, we could lose some of our macadamia nut trees. The MFC has not been detected in the orchards at the wetter locations of Keaau.

As indicated above, natural enemies are relied upon to manage insects that contribute to nut loss. Without these natural enemies, greater losses are possible. Pesticides may be available to manage these economic insect pests when treatment costs and nut loss justify their use, and when their use does not disrupt the natural enemy population.

Honey bees are placed in the orchards to supplement other insect pollinators during the flower season. In late 2008, the Hawaii Department of Agriculture identified the Varroa mite on feral honey bees near the port of Hilo, Hawaii. This mite is an ectoparasite that attaches to the body of honey bees and weakens them, and can result in the destruction of bee hives and colonies. The apiaries that place hives in the macadamia nut orchards must manage this pest with miticide in order to maintain healthy bee colonies and avoid the development of pest resistance to the miticide.

Increases in these diseases and pests or our inability to successfully control these diseases and pests could result in decreases in production, including loss of trees in affected orchards, which could have a material adverse effect on our business, financial condition and results of operations.

Our orchards are susceptible to natural hazards such as wildfires, rainstorms, floods and windstorms, which may adversely affect nut production.

Our orchards are located in areas on the island of Hawaii that are susceptible to natural hazards, including drought, wildfires, heavy rains, floods, and windstorms. Our orchards located in the Ka’u region are susceptible to wildfires due to recent drought conditions. In June and July 2012, a wildfire caused widespread damage to agricultural crops in the Ka’u region. The fire resulted in damage to irrigation pipes and approximately 24 tree acres of our macadamia nut orchards. Our orchards are also located in areas that are susceptible to heavy rainstorms. In November 2000, the Ka’u region was affected by flooding, resulting in some nut loss. Since the flood in 2000, heavy rain in the Ka’u region has not produced flooding of any consequence, but heavy rain and flooding continue to be potential risks that can affect our nut production. On August 7, 2014, tropical storm Iselle made landfall on the island of Hawaii with high winds and heavy rain resulting in some tree loss as well as increases in immature nut drop and mature nut loss due to storm run-off. In January 2015, another windstorm swept through the Ka’u region and caused a 1% loss of canopy to our orchards. Twenty-seven major windstorms have occurred on the island of Hawaii since 1961, and six of those caused material losses to our orchards. Most of our orchards are surrounded by windbreak trees, which provide limited protection. Younger trees that have not developed extensive root systems are particularly vulnerable to windstorms. The occurrence of any natural disaster affecting a material portion of our orchards could have a material adverse effect on our business, financial conditions and results of operations.

Our insurance may not be sufficient to reimburse us for crop losses.

We obtain tree insurance each year under a federally subsidized program. The tree insurance for 2015 provides coverage up to a maximum of approximately $14.8 million against catastrophic loss of trees due to wind, fire or volcanic activity. Crop insurance was purchased for the 2014-2015 crop season and provides coverage for up to a maximum of approximately $14.0 million against loss of nuts due to wind, fire, volcanic activity, earthquake, adverse weather, wildlife damage and failure of irrigation water supplies. There is no assurance that such insurance will cover all losses incurred by the Partnership or that such insurance will be available or purchased in the same amount in future periods.

Our orchards are subject to risks from active volcanoes.

Our orchards are located on the island of Hawaii, where there are two active volcanoes. To date, no lava flows from either volcano have affected or threatened the orchards, but the risk remains.

The amount and timing of rainfall can materially impact nut production.

The productivity of orchards depends in large part on moisture conditions. Inadequate rainfall can reduce nut yields significantly, whereas excessive rain without adequate drainage can foster disease and hamper harvesting operations. Although rainfall at the orchards located in the Keaau area has generally been adequate, the orchards located in the Ka’u area generally receive less rainfall and, as a result, a portion of the Ka’u orchards is presently irrigated. Irrigation can mitigate some of the effects of a drought, but it cannot completely protect a macadamia nut crop from the effect of a drought. Also, the timing of rainfall relative to key development stages in the growing season can impact nut production. Excessive rains during the flowering season affects pollination and nut set at the Keaau orchards where flowering and the rainy season coincide. During 2014, the Ka’u and Keaau areas recorded 160% and 104%, respectively, of the 20-year average annual rainfall. However, the rainfall for June through September 2013 was 65% of the 20-year average, and the rainfall for November 2013 through January 2014, which are key development months, was 44% of the 20-year average, and negatively impacted nut set and nut retention for the 2014 crop. Regardless of the timing, lack of adequate rainfall for prolonged periods of time will also negatively affect nut production.

We rely on irrigation water for our Ka’u orchards and orchards acquired from IASCO. If the capacities of those wells diminish or fail, we may not have an adequate water supply to irrigate our orchards, which could adversely affect our nut production.

With the May 2000 acquisition of the farming business, we acquired an irrigation well (the “Sisal Well”), which supplies water to our orchards in the Ka’u region. Historically, the quantity of water available from the Sisal Well has been generally sufficient to irrigate these orchards in accordance with prudent farming practices. The irrigated portion of the Ka’u II Orchards is expected to need greater quantities of water as the orchards mature. We anticipate that the amount of water available from the Sisal well will be generally sufficient, assuming average levels of rainfall, to irrigate the irrigated orchards in accordance with prudent farming practices for the next several years. If the amount of water provided by the Sisal Well becomes insufficient to irrigate the above-named orchards, we may need to incur additional costs to increase the capacity of the Sisal Well, drill an alternative well into the historical source that provides water to the Sisal Well or obtain water from other sources in order to avoid diminished yields.

Included in the assets we purchased from IASCO is an irrigation well (the “Palima Well”) that supplies water for the IASCO orchards, orchards owned by New Hawaii Macadamia Nut Co. (“NHMNC”), and trees owned by us on leased land from the State of Hawaii. Under a prior agreement with IASCO, NHMNC received a portion of the water pumped out of the Palima Well, and we, as the new owner of this well, are obligated to continue this service. The well provides supplemental irrigation and is generally sufficient, assuming average levels of rainfall, to sustain nut production at historical norms.

If insufficient irrigation water is available to the irrigated orchards, then diminished yields of macadamia nut production can be expected, which could have a material adverse effect on nut production.

Fluctuations in various food and supply costs as well as increased costs associated with product processing and transportation could materially adversely affect our business, financial condition and operating results.

Both we and our manufacturers obtain some of the key ingredients used in our products from third-party suppliers. As with most food products, the availability and cost of raw materials used in our products can be significantly affected by a number of factors beyond our control, such as general economic conditions, growing decisions, government programs (including government programs and mandates relating to ethanol), weather conditions such as frosts, drought, and floods, and plant diseases, pests and other acts of nature. Because we do not control the production of raw materials, we are also subject to delays caused by interruptions in production of raw materials based on conditions not within our control. Such conditions include job actions or strikes by employees of suppliers, weather, crop conditions, transportation interruptions, natural disasters, sustainability issues and boycotts of products or other catastrophic events.

There can be no assurance that we or our manufacturers will be able to obtain alternative sources of raw materials at favorable prices, or at all, should there be shortages or other unfavorable conditions. In some instances, we enter into forward purchase commitments to secure the costs of projected commodity requirements needed to produce our finished goods. These commitments are stated at a firm price, or as a discount or premium from a future commodity price, and are placed with our manufacturers or directly with ingredient or packaging suppliers. There can be no assurance that our pricing commitments will result in the lowest available cost for the commodities used in our products. Our key raw material is macadamia nuts. We currently obtain the macadamia nuts for our products solely from our production in Hawaii. The inability to obtain macadamia nuts due to poor weather or for any reason could have an adverse effect on our business. In addition, energy is required to process and produce our products. Transportation costs, including fuel and labor, also impact the cost of manufacturing our products. These costs fluctuate significantly over time due to factors that may be beyond our control.

Our inability or our manufacturers’ inabilities to obtain adequate supplies of raw materials for our products or energy at favorable prices, or at all, as a result of any of the foregoing factors or otherwise could cause an increase in our cost of sales and a corresponding decrease in gross margin, or cause our sales and earnings to fluctuate from period to period. Such fluctuations and decrease in gross margin could have a material adverse effect on our business, results of operations and financial conditions. There is no assurance that we would be able to pass along any cost increases to our customers in the form of price increases.

Our advertising is subject to regulation by the Federal Trade Commission under the Federal Trade Commission Act, which prohibits dissemination of false or misleading advertising.

The National Advertising Division of the Council of Better Business Bureaus, Inc., which we refer to as NAD, administers a self-regulatory program of the advertising industry to ensure truth and accuracy in national advertising. NAD monitors national advertising and entertains inquiries and challenges from competing companies and consumers. Should our advertising be determined to be false or misleading, we may have to pay damages, withdraw our campaign and possibly face fines or sanctions, which could have a material adverse effect on our sales and operating results.

Adverse publicity or consumer concern regarding the safety and quality of food products or health concerns, whether with our products or for food products in the same food group as our products, may result in the loss of sales.

We are highly dependent upon consumers’ perception of the safety, quality and possible dietary benefits of our products. As a result, substantial negative publicity concerning one or more of our products or other foods similar to or in the same food group as our products could lead to a loss of consumer confidence in our products, removal of our products from retailers’ shelves and reduced prices and sales of our products. Product quality issues, actual or perceived, or allegations of product contamination, even when false or unfounded, could hurt the image of our brands and cause consumers to choose other products. Furthermore, any product recall, whether our own or by a third party within one of our categories or due to real or unfounded allegations, could damage our brand image and reputation. Any of these events could have a material adverse effect on our business, results of operations and financial condition. If we conduct operations in a market segment that suffers a loss in consumer confidence as to the safety and quality of food products, our business could be materially adversely affected. The food industry has recently been subject to negative publicity concerning the health implications of GMOs, obesity, trans fat, diacetyl, artificial growth hormones, arsenic in rice and bacterial contamination, such as salmonella and aflatoxin. Consumers may increasingly require that foods meet stricter standards than are required by applicable governmental agencies, thereby increasing the cost of manufacturing such foods and ingredients. Developments in any of these areas, including, but not limited to, a negative perception about our formulations, could cause our operating results to differ materially from expected results. Any of these events could harm our sales, increase our costs and hurt our operating results, perhaps significantly.

We may experience increased competition for raw materials and from other producers of food products if the trend for non-GMO products continues, as well as increased regulation of our products, which could have a material adverse effect on our business.

Our products contain only non-GMO ingredients. The food industry has been experiencing a significant trend in which an increasing number of consumers are requiring only non-GMO ingredients in their foods. Legislation could require companies to move to non-GMO labeling or ingredients. Such industry trends or legislation could result in changes to our labeling, advertising or packaging. As additional retailers require or consider requiring all of their products to be non-GMO, we may face increased competition for sources of raw materials that are non-GMO. Such industry pressure may be particularly problematic in the United States, where most farmers produce genetically modified foods, making it difficult to source non-GMO ingredients and raw materials. There is also a risk of contamination of non-GMO farms by neighboring GMO farms. Although the trend toward non-GMO products could be positive for our sales, an increase in competition and regulatory requirements could have a material adverse effect on our business, financial conditions and results of operations.

As our business increases in size, we will need to locate and contract qualified co-packers with sufficient dedicated space for our non-GMO, gluten-free products, and there is no assurance that we will be able to do so.

We rely on a single co-packer for certain products. If demand for gluten-free products grows, we will need to increase our production through additional co-packers to ensure that we have sufficient supply to meet increasing demand. There is no assurance that we will be able to find available, qualified co-packers or that we will be able to negotiate contracts with them on commercially reasonable terms or at all.

Our business operations are subject to numerous laws and governmental regulations, exposing us to potential claims and compliance costs that could adversely affect our operations.

Manufacturers and marketers of food products are subject to extensive regulation by the FDA, the USDA, and other national, state and local authorities. For example, the Food, Drug and Cosmetic Act and the new Food Safety Modernization Act and their regulations govern, among other things, the manufacturing, composition and ingredients, packaging and safety of foods. Under these acts, the FDA regulates manufacturing practices for foods through its current “good manufacturing practices” regulations, imposes ingredient specifications and requirements for many foods, inspects food facilities and issues recalls for tainted food products. Additionally, the USDA has adopted regulations with respect to a national organic labeling and certification program.

Food manufacturing facilities and products are also subject to periodic inspection by federal, state and local authorities. State regulations are not always consistent with federal regulations or other state regulations.

Any changes in laws and regulations applicable to food products could increase the cost of developing and distributing our products and otherwise increase the cost of conducting our business, any of which could materially adversely affect our financial condition. In addition, if we fail to comply with applicable laws and regulations, including future laws and regulations, we may be subject to civil liability, including fines, injunctions, recalls or seizures, as well as potential criminal sanctions, any of which could have a material adverse effect on our business, financial condition, results of operations or liquidity.

We may be subject to significant liability should the consumption of any food products manufactured or marketed by us cause injury, illness or death.