Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - DELTA NATURAL GAS CO INC | Financial_Report.xls |

| EX-23 - EXHIBIT 23 - DELTA NATURAL GAS CO INC | dgas-2014630xkexhibit23.htm |

| EX-32.1 - EXHIBIT 32.1 - DELTA NATURAL GAS CO INC | dgas-2014630xex321.htm |

| EX-31.1 - EXHIBIT 31.1 - DELTA NATURAL GAS CO INC | dgas-2014630xex311.htm |

| EX-32.2 - EXHIBIT 32.2 - DELTA NATURAL GAS CO INC | dgas-2014630xex322.htm |

| EX-12 - EXHIBIT 12 - DELTA NATURAL GAS CO INC | dgas-2014630xkexhibit12.htm |

| EX-31.2 - EXHIBIT 31.2 - DELTA NATURAL GAS CO INC | dgas-2014630xex312.htm |

| EX-10.35 - EXHIBIT 10.35 - DELTA NATURAL GAS CO INC | dgas-2014630xexhibit1035.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

______________

FORM 10-K

______________

(Mark one)

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended June 30, 2014

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _______ to ________

Commission File No. 0-8788

______________

DELTA NATURAL GAS COMPANY, INC.

(Exact name of registrant as specified in its charter)

______________

Kentucky | 61-0458329 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

3617 Lexington Road, Winchester, Kentucky | 40391 |

(Address of principal executive offices) | (Zip code) |

859-744-6171

(Registrant's telephone number, including area code)

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered |

Common Stock $1 Par Value | NASDAQ |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes £ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15 (d) of the Act. Yes £ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes £ No x

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No £

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (Section 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. £

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer", "accelerated filer", and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer £ | Accelerated filer x |

Non-accelerated filer £ (Do not check if a smaller reporting company) | Smaller reporting company £ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes £ No x

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant's most recent completed second fiscal quarter. $155,037,002.

Indicate the number of shares outstanding of each of the registrant's classes of common stock, as of the latest practicable date. As of August 15, 2014, Delta Natural Gas Company, Inc. had outstanding 6,943,547 shares of common stock $1 par value.

DOCUMENTS INCORPORATED BY REFERENCE

The Registrant's definitive proxy statement, to be filed with the Commission not later than 120 days after June 30, 2014, is incorporated by reference in Part III of this Report.

TABLE OF CONTENTS

Page Number | ||||

1

PART I

Item 1. Business

References to “Delta”, “the Company”, “we”, “us” and “our” refer to Delta Natural Gas Company, Inc. and its consolidated subsidiaries, except as otherwise stated. We were incorporated under the laws of the Commonwealth of Kentucky on October 7, 1949. Unless otherwise stated, “2014”, “2013” and “2012” refers to the respective twelve month periods ending June 30.

General

Delta Natural Gas Company, Inc. (“Delta” or “the Company”) (Nasdaq: DGAS) distributes or transports natural gas to approximately 36,000 customers. Our distribution and transmission systems are located in central and southeastern Kentucky, and we own and operate an underground natural gas storage field in southeastern Kentucky. We transport natural gas to our industrial customers who purchase their natural gas in the open market. We also transport natural gas on behalf of local producers and customers not on our distribution system and sell liquids extracted from natural gas in our storage field and on our pipeline systems. We have three wholly-owned subsidiaries. Delta Resources, Inc. (“Delta Resources”) buys natural gas and resells it to industrial or large use customers on Delta's system. Delgasco, Inc. (“Delgasco”) buys natural gas and resells it to Delta Resources and to customers not on Delta's system. Enpro, Inc. (“Enpro”) owns and operates natural gas production properties and undeveloped acreage.

We seek to provide dependable, high-quality service to our customers while steadily enhancing value for our shareholders. Our efforts have been focused on developing a balance of regulated and non-regulated businesses to contribute to our earnings by profitably selling, transporting, producing and processing natural gas in our service territory.

We strive to achieve operational excellence through economical, reliable service with an emphasis on responsiveness to customers. We continue to invest in facilities for the distribution, transportation and storage of natural gas. We believe that our responsiveness to customers and the dependability of the service we provide afford us additional opportunities for growth. While we seek those opportunities, we will continue a conservative strategy of minimizing our exposure to market risk arising from fluctuations in the prices of natural gas.

We operate through two segments, a regulated segment and a non-regulated segment.

Our executive offices are located at 3617 Lexington Road, Winchester, Kentucky 40391. Our telephone number is (859) 744-6171. Our website is www.deltagas.com.

Regulated Operations

Distribution and Transportation

Through our regulated segment, we distribute natural gas to our retail customers in 23 predominantly rural counties. In addition, our regulated segment transports natural gas to industrial customers on our system who purchase their natural gas in the open market. Our regulated segment also transports natural gas on behalf of local producers and other customers not on our distribution system.

The economy of our service area is based principally on coal mining, farming and light industry. The communities we serve typically contain populations of less than 20,000. Our three largest service areas are Nicholasville, Corbin and Berea, Kentucky. In Nicholasville we serve approximately 8,000 customers, in Corbin we serve approximately 6,000 customers and in Berea we serve approximately 4,000 customers. Some of the communities we serve continue to expand, resulting in growth opportunities for us. Industrial parks have been developed in our service areas, which could result in additional growth in industrial customers.

The Kentucky Public Service Commission exercises regulatory authority over our retail natural gas distribution and transportation services. Their regulation of our business includes approving the rates we are permitted to charge our regulated customers. The impact of this regulation is further discussed in Note 14 of the Notes to Consolidated Financial Statements, in Item 8. Financial Statements and Supplementary Data and under “Regulatory Matters” in Item 1. Business.

2

Factors that affect our regulated revenues include the rates we charge our customers, economic conditions in our service areas, competition, the cost of natural gas and weather. Our current rate design lessens the impact weather has on our regulated revenues as our rates include both a fixed monthly customer charge and a volumetric rate which has a weather normalization provision that adjusts rates due to variations in weather. Market risk arising from fluctuations in the price of natural gas is mitigated through the natural gas cost recovery rate mechanism which permits us to pass through to our regulated customers changes in the price we must pay for our natural gas supply. However, increases in our rates may cause our customers to conserve or to use alternative energy sources.

Our regulated sales are seasonal and temperature-sensitive, since the majority of the natural gas we sell is used for heating. During 2014, 76% of the regulated volumes were sold during the heating season (December through April). Variations in the average temperature during the winter impact our volumes sold. The Kentucky Public Service Commission, through a weather normalization provision in our tariff, permits us to adjust the rates we charge our customers in response to winter weather that is warmer or colder than normal temperatures.

We compete with alternate sources of energy for our regulated distribution customers. These alternate sources include electricity, geo-thermal, coal, oil, propane, wood and solar.

Our larger regulated customers can obtain their natural gas supply by purchasing directly from interstate suppliers, local producers or marketers. Customers for whom we transport natural gas could by-pass our transportation system to directly connect to interstate pipelines or other transportation providers. Customers may undertake such a by-pass in order to seek lower prices for their natural gas and/or transportation services. Our larger customers who are in close proximity to alternative supply would be most likely to consider taking this action. Additionally, some of our industrial customers are able to switch to alternative sources of energy. These are competitive concerns that we continue to address by utilizing our non-regulated segment to offer these customers natural gas supply at competitive market-based rates.

Some natural gas producers in our service area can access pipeline delivery systems other than ours, which generates competition for our transportation services. We continue our efforts to purchase or transport natural gas that is produced in reasonable proximity to our transportation facilities through our regulated segment.

As an active participant in many areas of the natural gas industry, we plan to continue efforts to expand our natural gas transmission and distribution system and customer base. We continue to consider acquisitions of other natural gas systems, some of which are contiguous to our existing service areas, as well as expansion within our existing service areas.

Gas Supply

We maintain an active gas supply management program that emphasizes long-term reliability and the pursuit of cost-effective sources of natural gas for our customers. We purchase our natural gas from a combination of interstate and Kentucky sources. In our fiscal year ended June 30, 2014, we purchased approximately 99% of our natural gas from interstate sources.

Interstate Natural Gas Supply

Our regulated segment acquires its interstate natural gas supply from gas marketers. We currently have commodity requirements agreements with Atmos Energy Marketing (“Atmos”) for our Columbia Gas Transmission Corporation (“Columbia Gas”), Columbia Gulf Transmission Corporation (“Columbia Gulf”), Tennessee Gas Pipeline (“Tennessee”) and Texas Eastern Transmission Corporation (“Texas Eastern”) supplied areas. Under these commodity requirements agreements, Atmos is obligated to supply the volumes consumed by our regulated customers in defined sections of our service areas. We are not obligated to purchase any minimum quantities from Atmos or purchase natural gas from them for any period longer than one month at a time. The natural gas we purchase under these agreements is priced at index-based prices, NYMEX or at mutually agreed-to fixed prices based on forward market prices. The index-based market prices are determined based on the prices published on the first of each month in Platts' Inside FERC's Gas Market Report for the indices that relate to the pipelines through which the natural gas will be transported, plus or minus an agreed-to fixed price adjustment per million British Thermal Units of natural gas purchased. Consequently, the price we pay for interstate natural gas is based on current market prices.

Our agreements with Atmos for the Columbia Gas, Columbia Gulf, Tennessee and Texas Eastern supplied service areas continue year to year unless canceled by either party by written notice at least sixty days prior to the annual anniversary date (April 30) of the agreement. In our fiscal year ended June 30, 2014, approximately 37% of our regulated natural gas supply was purchased under our agreements with Atmos.

3

Our regulated segment purchases natural gas from Midwest Energy Services, LLC (“Midwest”) for injection into our underground natural gas storage field and to supply a portion of our system. We are not obligated to purchase any minimum quantities from Midwest, nor are we required to purchase natural gas for any periods longer than one month at a time. The natural gas is priced at index-based market prices or at mutually agreed-to fixed prices based on forward market prices. Our agreement with Midwest may be terminated upon 30 days prior written notice by either party. In our fiscal year ended June 30, 2014, approximately 61% of our regulated natural gas supply was purchased under our agreement with Midwest.

We also purchase interstate natural gas from other natural gas marketers as needed at either current market prices, determined by industry publications, or at forward market prices.

Transportation of Interstate Natural Gas Supply

Our interstate natural gas supply is transported to us from market hubs, production fields and storage fields by Tennessee, Columbia Gas, Columbia Gulf and Texas Eastern.

Our agreements with Tennessee currently extend through October, 2019 and thereafter automatically renew for subsequent five-year terms unless Delta notifies Tennessee of its intent not to renew the agreements at least one year prior to the expiration of any renewal terms. We intend to renew our agreements with Tennessee. Subject to the terms of Tennessee's Federal Energy Regulatory Commission natural gas tariff, Tennessee is obligated under these agreements to transport up to 19,600 thousand cubic feet (“Mcf”) per day for us. During fiscal 2014, Tennessee transported for us a total of 1,100,000 Mcf, or approximately 23% of our regulated supply requirements, under these agreements. We have natural gas storage agreements with Tennessee under the terms of which we reserve a defined storage space in Tennessee's storage fields, which we have assigned to Atmos, and we reserve the right to withdraw daily natural gas volumes up to certain specified fixed quantities. These natural gas storage agreements renew on the same schedule as our transportation agreements with Tennessee.

Under our agreements with Columbia Gas and Columbia Gulf, Columbia Gas is obligated to transport, including utilization of our defined storage space as required, up to 12,600 Mcf per day for us, and Columbia Gulf is obligated to transport up to a total of 4,300 Mcf per day for us. During fiscal 2014, Columbia Gas and Columbia Gulf transported for us a total of 675,000 Mcf, or approximately 14% of our regulated natural gas supply requirements, under all of our agreements with them. Our transportation agreements with Columbia Gas and Columbia Gulf extend through 2015. After 2015, our agreement with Columbia Gas continues on a year-to-year basis unless terminated by one of the parties, but may be extended by mutual agreement.

Columbia Gulf also transported additional volumes under agreements it has with Midwest to a point of interconnection between Columbia Gulf and us where we purchase the natural gas to inject into our storage field. The amounts transported and sold to us under the agreements Columbia Gulf has with Midwest for fiscal 2014 constituted approximately 61% of our regulated gas supply. We are not a party to any of these separate transportation agreements on Columbia Gulf.

We have no direct agreement with Texas Eastern. However, Atmos has an arrangement with Texas Eastern to transport the natural gas to us that we purchase from Atmos to supply our customers' requirements in specific geographic areas. In our fiscal year ended June 30, 2014, Texas Eastern transported approximately 18,000 Mcf of natural gas to our system, which constituted less than 1% of our natural gas supply.

Kentucky Natural Gas Supply

We have an agreement with Vinland Energy Operations LLC (“Vinland”) to purchase natural gas on a year-to-year basis unless terminated by one of the parties. We purchased 45,000 Mcf from Vinland during fiscal 2014. The price for the natural gas we purchase from Vinland is based on the index price of spot gas delivered to Columbia Gas in the relevant region as reported in Platts' Inside FERC's Gas Market Report. Vinland delivers this natural gas to our customer meters directly from its own pipelines. In fiscal 2014, the natural gas we purchased from Vinland constituted less than 1% of our regulated natural gas supply.

Natural Gas in Storage

We own and operate an underground natural gas storage field that we use to store a significant portion of our natural gas supply needs. This storage capability permits us to purchase and store natural gas during the non-heating months and then withdraw and sell the natural gas during the peak usage months. We have a legal obligation to retire wells located at this underground natural gas storage facility. However, since we expect to utilize the storage facility as long as we provide natural gas to our customers, we have determined the wells have an indeterminate life and have therefore not recorded a liability associated with the cost to retire the wells.

4

Regulatory Matters

The Kentucky Public Service Commission exercises regulatory authority over our retail natural gas distribution and transportation services. Their regulation of our business includes approving the rates we are permitted to charge our regulated customers. We monitor our need to file requests with them for a general rate increase for our natural gas and transportation services. They have historically utilized cost-of-service ratemaking where our base rates are established to recover normal operating expenses, exclusive of gas costs, and a reasonable rate of return. We do not have any matters pending before the Kentucky Public Service Commission which would have a material impact on our results of operations, financial positions or cash flows.

We have a pipe replacement program which allows us to adjust our regulated rates annually to earn a return on capital expenditures incurred subsequent to our last rate case which are associated with the replacement of pipe and related facilities. The pipe replacement program is designed to additionally recover the costs associated with the mandatory retirement or relocation of facilities.

The Kentucky Public Service Commission allows us a natural gas cost recovery clause, which permits us to adjust the rates charged to our customers to reflect changes in our natural gas supply costs and any bad debt expense related to natural gas cost. Although we are not required to file a general rate case to adjust rates pursuant to the natural gas cost recovery clause, we are required to make quarterly filings with the Kentucky Public Service Commission. Under and over-recovered natural gas costs are collected or refunded through adjustments to customer bills beginning three months after the end of the quarter in which the actual natural gas costs were incurred.

Additionally, we have a weather normalization provision in our tariffs, approved by the Kentucky Public Service Commission, which provides for the adjustment of our rates to residential and small non-residential customers to reflect variations from thirty year average weather for our December through April billing cycles. These adjustments to customer bills are made on a real time basis such that there is no lag in collecting from or refunding to customers the related dollar amounts.

The Kentucky Public Service Commission also allows us a conservation and efficiency program for our residential customers. Through this program, we perform energy audits, promote conservation awareness and provide rebates on the purchase of certain high efficiency appliances. The program helps to align our interests with our residential customers' interests by reimbursing us for the margins on lost sales due to the program and providing incentives for us to promote customer conservation. Our rates are adjusted annually to recover the costs incurred under these programs, the reimbursement of margins on lost sales and the incentives provided to us.

In addition to regulation by the Kentucky Public Service Commission, we may obtain non-exclusive franchises from the cities in which we operate authorizing us to place our facilities in the streets and public grounds. No utility may obtain a franchise until it has obtained approval from the Kentucky Public Service Commission to bid on such franchise. We hold franchises in five of the cities we serve, and we continue to operate under the conditions of expired franchises in four other cities we serve. In the other cities and areas we serve, there are no governmental organizations authorized to grant franchises or the city governments do not require a franchise. We attempt to acquire or reacquire franchises whenever feasible. Without a franchise, a city could require us to cease our occupation of the streets and public grounds or prohibit us from extending our facilities into any new area of that city. To date, the absence of a franchise has not adversely affected our operations.

Non-Regulated Operations

Natural Gas Marketing

Our non-regulated segment includes three wholly-owned subsidiaries. Two of these subsidiaries, Delta Resources and Delgasco, purchase natural gas in the open market, including natural gas from Kentucky producers. We resell this natural gas to industrial customers on our distribution system and to others not on our system.

Factors that affect our non-regulated revenues include the rates we charge our customers, our supply cost for the natural gas we purchase for resale, economic conditions in our service areas, weather and competition.

Our larger non-regulated customers can obtain their natural gas supply by purchasing directly from interstate suppliers, local producers or marketers and arranging for alternate transportation of the natural gas to their plants or facilities. Additionally, some of our industrial customers are able to switch economically to alternative sources of energy. We continue to address these competitive concerns by offering these customers natural gas supply at competitive market based rates.

5

In our fiscal year ended June 30, 2014, approximately 94% of our non-regulated revenue was derived from our natural gas marketing activities. In our non-regulated segment, three customers each provided more than 5% of our operating revenues for 2014 and two customers each provided more than 5% for 2013 and 2012. Seminole Energy provided approximately $9,494,000, $17,866,000 and $12,450,000 of non-regulated revenues during 2014, 2013 and 2012, respectively. Atmos provided approximately $5,206,000, $5,390,000 and $6,815,000 of non-regulated revenues during 2014, 2013 and 2012, respectively. Greystone, LLC provided approximately $12,569,000 of non-regulated revenues during 2014. There is no assurance that revenues from these customers will continue at these levels.

Natural Gas Production

Our subsidiary, Enpro, produces natural gas that is sold to Delgasco for resale in the open market. Item 2. Properties further describes Enpro's oil and natural gas leases and production properties. Enpro produced a total of 80,000 Mcf of natural gas during 2014 which was approximately 1% of our non-regulated volumes sold.

Natural Gas Liquids

To improve the operations of our distribution, transmission and storage system, we operate a facility that is designed to extract liquids from the natural gas in our system. We sell these natural gas liquids at a price determined by a national unregulated market. In our fiscal year ended June 30, 2014, approximately 5% of our non-regulated revenue was derived from the sale of natural gas liquids.

Natural Gas Supply

Our non-regulated segment purchases natural gas from M & B Gas Services (“M&B”) and Midwest. Our underlying agreements with M&B and Midwest do not obligate us to purchase any minimum quantities from M&B or Midwest, nor to purchase natural gas from either company for any periods longer than one month at a time. The natural gas is priced at index-based market prices or at mutually agreed-to fixed prices based on forward market prices. Our agreements with both M&B and Midwest may be terminated upon 30 days prior written notice by either party. Any purchase agreements to supply our unregulated sales activities may have longer terms or multiple month purchase commitments. In our fiscal year ended June 30, 2014, 1% and 90% of our non-regulated natural gas supply was purchased under our agreements with M&B and Midwest, respectively.

Additionally, our non-regulated segment purchases natural gas from Atmos as needed. This spot gas purchasing arrangement is pursuant to an agreement with Atmos containing an “evergreen” clause which permits either party to terminate the agreement by providing not less than sixty days written notice. Our purchases from Atmos under this spot purchase agreement are generally month-to-month. However, we have the option of forward-pricing natural gas for one or more months. The price of natural gas under this agreement is based on current market prices. In our fiscal year ended June 30, 2014, approximately 9% of our non-regulated natural gas supply was purchased under our agreement with Atmos.

We also purchase intrastate natural gas from Kentucky producers as needed at either current market prices, determined by industry publications, or at forward market prices.

We anticipate continuing our non-regulated activities and intend to pursue and increase these activities wherever practicable.

Capital Expenditures

Capital expenditures during 2014 were $8.1 million and for 2015 are estimated to be $10.8 million. Our expenditures include system extensions as well as the replacement and improvement of existing transmission, distribution, gathering, storage and general facilities.

Financing

Our capital expenditures and operating cash requirements are met through the use of internally generated funds and a short-term bank line of credit. The current available line of credit is $40 million, all of which was available at June 30, 2014.

6

Our current bank line of credit extends through June 30, 2015 and will be utilized to meet capital expenditure and operating cash requirements. The amounts and types of future long-term debt and equity financings will depend upon our capital needs and market conditions.

We currently have long-term debt of $55,000,000 in the form of our Series A Notes. The Series A Notes are unsecured, bear interest at 4.26% per annum and mature on December 20, 2031. Accrued interest on the Series A Notes is payable quarterly and we are required to make a $1,500,000 principal reduction payment on the Series A Notes each December.

Employees

On June 30, 2014, we had 150 full-time employees. We consider our relationship with our employees to be satisfactory. Our employees are not represented by unions nor are they subject to any collective bargaining agreements.

Available Information

We make available free of charge on our Internet website http://www.deltagas.com under our “Investor Relations” tab, our Business Code of Conduct and Ethics, annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after we electronically file such material with, or furnish it to, the Securities and Exchange Commission (“SEC”). The SEC also maintains an Internet site http://www.sec.gov that contains reports, proxy and information statements and other information regarding Delta. The public may read and copy any materials the Company files with the SEC at the SEC's Public Reference Room at 100 F Street, NE, Washington, DC 20549. The SEC's phone number is 1-800-732-0330.

7

Consolidated Statistics | ||||||||||||||

For the Years Ended June 30, | 2014 | 2013 | 2012 | 2011 | 2010 | |||||||||

Average Regulated Customers Served | ||||||||||||||

Residential | 29,588 | 29,755 | 29,929 | 30,420 | 30,575 | |||||||||

Commercial | 4,861 | 4,906 | 4,890 | 4,949 | 4,957 | |||||||||

Industrial | 41 | 40 | 41 | 44 | 46 | |||||||||

Total | 34,490 | 34,701 | 34,860 | 35,413 | 35,578 | |||||||||

Operating Revenues ($000) (a) | ||||||||||||||

Regulated (b) | ||||||||||||||

Residential sales | 29,867 | 24,342 | 22,720 | 25,800 | 23,783 | |||||||||

Commercial sales | 20,294 | 15,849 | 14,026 | 16,672 | 15,894 | |||||||||

Industrial sales | 1,381 | 1,011 | 914 | 1,199 | 1,075 | |||||||||

On-system transportation | 5,416 | 5,237 | 4,780 | 4,830 | 4,421 | |||||||||

Off-system transportation | 3,747 | 3,800 | 3,595 | 3,670 | 3,650 | |||||||||

Other | 390 | 333 | 324 | 303 | 294 | |||||||||

Total regulated revenues | 61,095 | 50,572 | 46,359 | 52,474 | 49,117 | |||||||||

Non-regulated sales | 38,792 | 34,238 | 31,423 | 34,343 | 30,746 | |||||||||

Intersegment eliminations (c) | (4,041 | ) | (4,145 | ) | (3,704 | ) | (3,777 | ) | (3,441 | ) | ||||

Total | 95,846 | 80,665 | 74,078 | 83,040 | 76,422 | |||||||||

System Throughput (Million Cu. Ft.) (a) | ||||||||||||||

Regulated | ||||||||||||||

Residential sales | 1,814 | 1,659 | 1,331 | 1,737 | 1,756 | |||||||||

Commercial sales | 1,420 | 1,291 | 1,027 | 1,310 | 1,331 | |||||||||

Industrial sales | 117 | 107 | 90 | 120 | 111 | |||||||||

On-system transportation | 4,807 | 4,988 | 4,724 | 4,830 | 4,533 | |||||||||

Off-system transportation | 11,616 | 11,795 | 11,225 | 11,531 | 11,039 | |||||||||

Total regulated throughput | 19,774 | 19,840 | 18,397 | 19,528 | 18,770 | |||||||||

Non-regulated sales | 7,241 | 7,650 | 6,455 | 6,010 | 4,787 | |||||||||

Intersegment eliminations (c) | (7,096 | ) | (7,497 | ) | (6,326 | ) | (5,890 | ) | (4,692 | ) | ||||

Total | 19,919 | 19,993 | 18,526 | 19,648 | 18,865 | |||||||||

Average Annual Consumption Per | ||||||||||||||

Average Residential Customer | ||||||||||||||

(Thousand Cu. Ft.) | 61 | 56 | 44 | 57 | 57 | |||||||||

Lexington, Kentucky Degree Days | ||||||||||||||

Actual | 4,855 | 4,667 | 3,797 | 4,725 | 4,782 | |||||||||

Percent of 30 year average | 107 | 104 | 83 | 103 | 104 | |||||||||

(a) Additional financial information related to our segments can be found in Management's Discussion and Analysis of Financial Condition and Results of Operations and Note 15 of the Notes to Consolidated Financial Statements.

(b) We implemented new regulated base rates, as approved by the Kentucky Public Service Commission in October, 2010, which were designed to generate additional annual revenue of $3,513,000.

(c) Intersegment eliminations represent the natural gas transportation costs from the regulated segment to the non-regulated segment at our tariff rates.

8

Item 1A. Risk Factors

The risk factors below should be carefully considered.

WEATHER CONDITIONS MAY CAUSE OUR REVENUES TO VARY FROM YEAR TO YEAR.

Our revenues vary from year to year, depending on weather conditions. We estimate that approximately 76% of our annual natural gas sales are temperature sensitive. As a result, mild winter temperatures can cause a decrease in the amount of natural gas we sell in any year, which would reduce our revenues and profits. The weather normalization provision in our tariff, approved by the Kentucky Public Service Commission, only partially mitigates this risk. Under our weather normalization provision in our tariff, we adjust our rates for our residential and small non-residential customers to reflect variations from thirty year average weather for our December through April billing cycles.

OUR ABILITY TO MEET CUSTOMERS' NATURAL GAS REQUIREMENTS MAY BE IMPAIRED IF CONTRACTED NATURAL GAS SUPPLIES AND INTERSTATE PIPELINE SERVICES ARE NOT AVAILABLE, ARE NOT DELIVERED IN A TIMELY MANNER OR IF FEDERAL REGULATIONS DECREASE OUR AVAILABLE CAPACITY.

We are responsible for acquiring sufficient natural gas supplies, interstate pipeline capacity and storage capacity to meet

current and future customers' annual and seasonal natural gas requirements. We purchase almost all of our natural gas supply from interstate sources and rely on interstate pipelines to transport natural gas to our system. The Federal Energy Regulatory Commission regulates the transportation of the natural gas we receive from interstate sources, and it could increase our transportation costs or decrease our available pipeline capacity by changing its regulatory policies. Additionally, federal legislation could restrict or limit drilling which could decrease the supply of available natural gas. A decrease in interstate pipeline capacity available to us or an increase in competition for interstate pipeline transportation service could reduce our normal interstate supply of natural gas. If we are not able to maintain a reliable and adequate natural gas supply and sufficient pipeline capacity to deliver that supply, we may be unable to meet our customers' requirements resulting in a loss of customers and decrease in profits.

OUR CUSTOMERS ARE ABLE TO BY-PASS OUR DISTRIBUTION AND TRANSMISSION SYSTEMS.

Our larger customers can obtain their natural gas supply by purchasing directly from interstate suppliers, local producers or marketers. Customers for whom we transport natural gas could by-pass our transportation system to directly connect to interstate pipelines or other transportation providers. Customers may undertake such by-passes in order to achieve lower prices for their natural gas and/or transportation services. Our larger customers who are in close proximity to alternative supply would be most likely to consider taking this action. This potential to by-pass our distribution and transportation systems creates a risk of the loss of large customers and thus could result in lower revenues and profits.

ACTIONS BY OUR REGULATORS COULD DECREASE FUTURE PROFITABILITY.

We are regulated by the Kentucky Public Service Commission. Our regulated segment generates a significant portion of our operating revenues. We face the risk that the Kentucky Public Service Commission may fail to grant us adequate and timely rate increases, may decrease our rates or may take other actions that would cause a reduction in our income from operations, such as limiting our ability to pass on to our customers our increased costs of natural gas. Such regulatory actions would decrease our revenues and our profitability. Additionally, our consolidated financial statements reflect the application of regulatory accounting standards by our regulated segment. Our regulated segment has recognized regulatory assets representing costs incurred in prior periods that are probable of recovery from customers in future rates. Disallowance of such costs in future proceedings before the Kentucky Public Service Commission could require us to write-off regulatory assets, which could have a material impact on our income and consolidated financial statements.

VOLATILITY IN PRICES COULD REDUCE OUR PROFITS.

Significant increases or lack of stability in the price of natural gas will likely cause our regulated retail customers to increase conservation or switch to alternate sources of energy. Any decrease in the volume of natural gas we sell that is caused by such actions will reduce our revenues and profits. Higher prices also make it more difficult to add new customers. Significant decreases in the price of natural gas will likely cause our non-regulated segment's gross margins to decrease. The price of natural gas liquids is determined by a national unregulated market, and decreases in the price could result in a decrease in our non-regulated gross margins.

9

DERIVATIVES LEGISLATION COULD ADVERSELY AFFECT OUR ABILITY TO HEDGE RISKS ASSOCIATED WITH OUR BUSINESS OR OTHERWISE HAVE A MATERIAL AND ADVERSE EFFECT ON OUR FINANCIAL POSITION, RESULTS OF OPERATIONS OR CASH FLOWS.

We currently use, and historically have used, forward commodity contracts, which meet the criteria of a derivative. The Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank Act”) adopted a comprehensive framework for the regulation of over-the-counter swaps (“OTC swaps”). The Dodd-Frank Act divides regulatory authority over swap agreements between the SEC and the Commodity Futures Trading Commission (“CFTC”) and requires that most OTC swaps be cleared through a registered clearing facility and traded on a designated exchange or swap execution facility. While the SEC and CFTC have adopted numerous regulations relating to OTC swaps, they are still in the process of rulemaking to address all of the requirements regarding OTC swaps under the Dodd-Frank Act. Current and future legal and regulatory requirements, restrictions and regulations imposed under the Dodd-Frank Act could increase the operational and transactional cost of derivatives contracts and could affect the number and/or creditworthiness of available counterparties, which could affect our ability to hedge our business risk.

INTERSTATE AND OTHER PIPELINES DELTA INTERCONNECTS WITH CAN IMPOSE RESTRICTIONS ON THEIR PIPELINE.

The pipelines interconnected to Delta's system are owned and operated by third parties who can impose restrictions on the quantity and quality of natural gas they will accept into their pipelines. To the extent natural gas on Delta's system does not conform to these restrictions, Delta could experience a decrease in volumes sold or transported to these pipelines.

FUTURE PROFITABILITY OF THE NON-REGULATED SEGMENT IS DEPENDENT ON A FEW INDUSTRIAL AND OTHER LARGE-VOLUME CUSTOMERS.

Our larger non-regulated customers are primarily industrial and other large-volume customers. Fluctuations in the natural gas requirements of these customers can have a significant impact on the profitability of the non-regulated segment.

A DECLINE IN THE LIQUIDS PRESENT IN OUR NATURAL GAS SUPPLY, OR LIQUIDS SALES PRICES, COULD REDUCE OUR NON-REGULATED REVENUES.

To improve the operations of our distribution, transmission and storage system, we operate a facility that is designed to extract liquids from the natural gas in our system. We are able to sell these liquids at a price determined by a national unregulated market. A reduction in the quantity of liquids present in our natural gas supply, or reductions in the prices we receive for such liquids sales, could result in a reduction of the earnings of our non-regulated segment.

WE RELY ON ACCESS TO CAPITAL TO MAINTAIN LIQUIDITY.

To the extent that internally generated cash coupled with short-term borrowings under our bank line of credit is not sufficient for our operating cash requirements and normal capital expenditures, we may need to obtain additional financing. Additionally, market disruptions may increase our cost of borrowing or adversely affect our access to capital markets. Such disruptions could include: economic downturns, the bankruptcy of an unrelated energy company, general capital market conditions, market prices for natural gas, terrorist attacks or the overall financial health of the energy industry. There is no guarantee we could obtain needed capital in the future.

POOR INVESTMENT PERFORMANCE OF PENSION PLAN HOLDINGS AND OTHER FACTORS IMPACTING PENSION PLAN COSTS COULD UNFAVORABLY IMPACT OUR LIQUIDITY AND RESULTS OF OPERATIONS.

Our cost of providing a non-contributory defined benefit pension plan is dependent upon a number of factors, such as the rates of return on plan assets, discount rates, the level of interest rates used to measure the required minimum funding level of the plan, future government regulation and our required or voluntary contributions made to the plan. Without sustained growth in the pension investments over time to increase the value of the plan assets and depending upon the other factors impacting our costs as listed above, we could be required to fund our plan with additional significant amounts of cash. Such cash funding obligations could have a material impact on our financial position, results of operations or cash flows.

10

WE ARE EXPOSED TO CREDIT RISKS OF CUSTOMERS AND OTHERS WITH WHOM WE DO BUSINESS.

Adverse economic conditions affecting, or financial difficulties of, customers and others with whom we do business could impair the ability of these customers and others to pay for our services or fulfill their contractual obligations or cause them to delay such payments or obligations. We depend on these customers and others to remit payments on a timely basis. Any delay or default in payment could adversely affect our cash flows, financial position or results of operations.

SUBSTANTIAL OPERATIONAL RISKS ARE INVOLVED IN OPERATING A NATURAL GAS DISTRIBUTION, TRANSPORTATION, LIQUIDS EXTRACTION AND STORAGE SYSTEM AND SUCH OPERATIONAL EVENTS COULD REDUCE OUR REVENUES AND INCREASE EXPENSES.

There are substantial risks associated with the operation of a natural gas distribution, transportation, liquids extraction and storage system, such as operational hazards and unforeseen interruptions caused by events beyond our control. These include adverse weather conditions, accidents, the breakdown or failure of equipment or processes, the performance of pipeline and storage facilities below expected levels of capacity and efficiency and catastrophic events such as explosions, fires, earthquakes, floods, landslides or other similar events beyond our control. These risks could result in injury or loss of life, extensive property damage or environmental pollution, which in turn could lead to substantial financial losses to us. In accordance with customary industry practice, we maintain insurance against some, but not all, of these risks. Liabilities incurred that are not fully covered by insurance could adversely affect our results of operations and financial condition. Additionally, interruptions to the operation of our natural gas distribution, transmission, liquids extraction or storage system caused by such events could reduce our revenues and increase our expenses.

WE MAY FACE CERTAIN REGULATORY AND FINANCIAL RISKS RELATED TO PIPELINE SAFETY LEGISLATION.

Increased regulatory oversight over pipeline operations and increased investment to inspect pipeline facilities, upgrade pipeline facilities, or control the impact of a breach of such facilities at the federal level could require additional operating expenses and capital expenditures to remain in compliance with any increased federal oversight. While we cannot predict with certainty the extent of these expenses and expenditures or when they might become effective, this could result in significant additional compliance costs to us and we may be unable to recover from our customers, through the regulatory process, all or some of these costs and an authorized rate of return on these costs.

HURRICANES, EXTREME WEATHER OR WELL-HEAD DISASTERS COULD DISRUPT OUR NATURAL GAS SUPPLY AND INCREASE NATURAL GAS PRICES.

Hurricanes, extreme weather or well-head disasters could damage production or transportation facilities, which could result in decreased supplies of natural gas, increased supply costs for us and higher prices for our customers. Such events could also result in new governmental regulations or rules that limit production or raise production costs.

OUR BORROWING ARRANGEMENTS INCLUDE VARIOUS FINANCIAL AND NEGATIVE COVENANTS AND A PREPAYMENT PENALTY THAT COULD RESTRICT OUR ACTIVITIES.

Our bank line of credit and Series A Notes contain financial covenants. A default on the performance of any single obligation incurred in connection with our borrowings, or a default on other indebtedness that exceeds $2,500,000, simultaneously creates an event of default with the bank line of credit and the Series A Notes. If we breach any of the financial covenants under these agreements, our debt repayment obligations under the bank line of credit and Series A Notes could be accelerated. For example, if we default we may not be able to refinance, repay all our indebtedness, pay dividends or have sufficient liquidity to meet our operating and capital expenditure requirements, all of which could result in a material adverse effect on our business, results of operations and financial condition.

OUR LONG-TERM DEBT ARRANGEMENTS LIMIT THE AMOUNT OF DIVIDENDS WE MAY PAY AND OUR ABILITY TO REPURCHASE OUR STOCK.

Under the terms of our 4.26% Series A Notes, the aggregate amount we may pay in dividends on our common stock and to repurchase our common stock is limited based on our cumulative net income and dividends paid. Consequently, as of June 30, 2014 our Series A Notes permit us to pay up to $22,778,000 in dividends and for the repurchase of our common stock. However, if we fail to generate sufficient net income in the future, our ability to continue to pay our regular quarterly dividend may be impaired and the value of our common stock would likely decline.

11

A SECURITY BREACH COULD DISRUPT OUR INFORMATION TECHNOLOGY SYSTEMS, INTERRUPT THE NATURAL GAS SERVICE WE PROVIDE TO OUR CUSTOMERS, COMPROMISE THE SAFETY OF OUR NATURAL GAS DISTRIBUTION, TRANSMISSION, LIQUIDS EXTRACTION AND STORAGE SYSTEMS OR EXPOSE CONFIDENTIAL PERSONAL INFORMATION.

Security breaches of our information technology infrastructure, including cyber-attacks and cyber-terrorism, could lead to information system disruptions or shutdowns, result in the interruption of our ability to provide natural gas to our customers or compromise the safety of our distribution, transmission, liquids extraction and storage systems. If such an attack or security breach were to occur, our business, results of operations and financial condition could be materially adversely affected. In addition, such an attack could affect our ability to service our indebtedness, our ability to raise capital and our future growth opportunities.

Additionally, a breakdown or a breach in our systems that results in the unauthorized release of individually identifiable customer, employee, vendor, investor or other sensitive data could have a material adverse effect on our reputation, operating results and financial condition. We could also be exposed to claims by persons harmed by such a breakdown or breach. Such a breakdown or breach could also materially increase the costs we incur to protect against such risks. There is no guarantee that the procedures that we have implemented to protect against unauthorized access to secured data are adequate to safeguard against all data security breaches.

FAILURE TO ATTRACT AND RETAIN AN APPROPRIATELY QUALIFIED WORKFORCE COULD UNFAVORABLY IMPACT OUR RESULTS OF OPERATIONS.

Certain situations, such as an aging workforce, mismatch of skill sets to complement future needs, or unavailability of a qualified workforce, may lead to increased operational risks and costs. As a result, we may be unable to hire enough individuals who are knowledgeable about the natural gas industry and/or face a lengthy time period associated with skill development and knowledge transfer. Failure to address this risk may result in increased operational and safety risks as well as increased costs. Even if we have reasonable plans in place to address succession planning and workforce training, we cannot control the future availability of qualified labor. If we are unable to successfully attract and retain an appropriately qualified workforce, our financial position or results of operations could be negatively affected.

NEW LAWS OR REGULATIONS COULD HAVE A NEGATIVE IMPACT ON OUR FINANCIAL POSITION, RESULTS OF OPERATIONS OR CASH FLOWS.

Changes in laws and regulations, including new accounting standards and tax laws, could change the way in which we are required to record revenues, expenses, assets and liabilities. Additionally, governing bodies may choose to re-interpret laws and regulations. These changes could have a negative impact on our financial position, cash flows, results of operations or access to capital.

WE MAY FACE CERTAIN REGULATORY AND FINANCIAL RISKS RELATED TO CLIMATE CHANGE LEGISLATION.

Future proposals to limit greenhouse gas emissions, measured in carbon dioxide equivalent units, could adversely affect our operating and service costs and demand for our product. In the past, the United States Congress has considered legislative proposals to limit greenhouse gas emissions and the United States Environmental Protection Agency has adopted regulations to limit carbon emissions. Future legislation and the implementation of existing regulations could increase utility costs and prices charged to utility customers. Unless we are able to timely recover the costs of such impacts from customers through the regulatory process, costs associated with any such regulatory or legislative changes could adversely affect our results of operations, financial condition and cash flows.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

We own our corporate headquarters in Winchester, Kentucky. We own eleven buildings used for field operations in the cities we serve.

12

We own approximately 2,500 miles of natural gas gathering, transmission, distribution and storage lines. These lines range in size up to twelve inches in diameter.

We hold leases for the storage of natural gas under 8,000 acres located in Bell County, Kentucky. We developed this property for the underground storage of natural gas.

We use all the properties described in the three paragraphs immediately above principally in connection with our regulated segment, as further discussed in Item 1. Business.

Through our wholly-owned subsidiary, Enpro, we produce natural gas as part of the non-regulated segment of our business. Enpro owns interests in oil and natural gas leases on 10,300 acres located in Bell, Knox and Whitley Counties. Thirty-five gas wells are producing from these properties. The remaining proved, developed natural gas reserves on these properties are estimated at 2.5 million Mcf. Also, Enpro owns the natural gas underlying 15,400 additional acres in Bell, Clay and Knox Counties. These properties have been leased to others for further drilling and development. We have performed no reserve studies on these properties. Enpro produced a total of 80,000 Mcf of natural gas during fiscal 2014 from all the properties described in this paragraph.

A producer plans to conduct further exploration activities on part of Enpro's developed holdings. Enpro reserves the option to participate in wells drilled by this producer and also retains certain working and royalty interests in any production from future wells.

Our assets have no significant encumbrances.

Item 3. Legal Proceedings

We are not currently a party to any legal proceedings that are expected to have a materially adverse impact on our liquidity, financial position or results of operations.

Item 4. Mine Safety Disclosures

None.

PART II

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

We have paid cash dividends on our common stock each year since 1964. The frequency and amount of future dividends will depend upon our earnings, financial requirements and other relevant factors, including limitations imposed by our Series A Notes as described in Note 10 of the Notes to Consolidated Financial Statements.

Our common stock is listed on NASDAQ and trades under the symbol “DGAS”. There were 1,482 record holders of our common stock as of August 26, 2014. The accompanying table sets forth, for the periods indicated, the high and low sales prices for the common stock on the NASDAQ stock market and the cash dividends declared per share.

13

Range of Stock Prices ($) | Dividends | |||||

High | Low | Per Share ($) | ||||

Quarter | ||||||

Fiscal 2014 | ||||||

First | 25.02 | 18.50 | .19 | |||

Second | 22.90 | 19.98 | .19 | |||

Third | 22.29 | 18.44 | .19 | |||

Fourth | 22.13 | 18.43 | .19 | |||

Fiscal 2013 | ||||||

First | 24.82 | 18.41 | .18 | |||

Second | 22.16 | 17.08 | .18 | |||

Third | 22.08 | 18.88 | .18 | |||

Fourth | 24.18 | 19.99 | .18 | |||

The sales prices shown above reflect prices between dealers and do not include markups or markdowns or commissions and may not necessarily represent actual transactions.

14

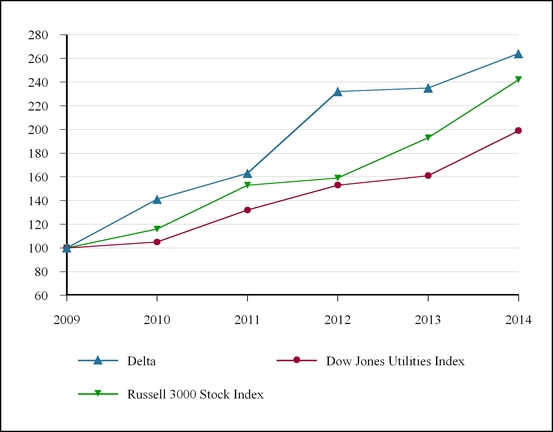

Comparison of Five-Year Cumulative Total Shareholder Return

The following graph sets forth a comparison of five year cumulative total shareholder returns (equal to dividends plus stock price appreciation) among our common shares, the Dow Jones Utilities Index and the Russell 3000 Stock Index during the past five fiscal years. Information reflected on the graph assumes an investment of $100 on June 30, 2009 in each of our common shares, the Dow Jones Utilities Index and the Russell 3000 Stock Index. Cumulative total return assumes quarterly reinvestment of dividends. The total shareholder returns shown are not necessarily indicative of future returns.

2009 | 2010 | 2011 | 2012 | 2013 | 2014 | ||||||

Delta | 100 | 141 | 163 | 232 | 235 | 264 | |||||

Dow Jones Utilities Index | 100 | 105 | 132 | 153 | 161 | 199 | |||||

Russell 3000 Stock Index | 100 | 116 | 153 | 159 | 193 | 242 | |||||

15

Item 6. Selected Financial Data

The following selected financial data is derived from the Company's audited consolidated financial statements and should be read in conjunction with those financial statements and notes thereto.

For the Years Ended June 30, | 2014 | 2013 | 2012 | 2011 | 2010 | ||||||

Summary of Operations ($) | |||||||||||

Operating revenues (a) | 95,845,871 | 80,664,837 | 74,078,322 | 83,040,251 | 76,422,068 | ||||||

Operating income (a) | 15,603,439 | 13,188,679 | 13,265,228 | 14,061,794 | 12,904,494 | ||||||

Net income (a)(b) | 8,275,128 | 7,200,776 | 5,783,998 | 6,364,895 | 5,651,817 | ||||||

Earnings per common share (a)(b) | |||||||||||

Basic and diluted | 1.19 | 1.05 | .85 | .95 | .85 | ||||||

Cash dividends declared per common share | .76 | .72 | .70 | .68 | .65 | ||||||

Weighted Average Number of Common Shares | |||||||||||

Basic | 6,918,725 | 6,843,455 | 6,777,186 | 6,707,224 | 6,652,320 | ||||||

Diluted | 6,918,725 | 6,843,455 | 6,777,186 | 6,712,804 | 6,652,320 | ||||||

Total Assets ($) | 186,025,161 | 183,930,015 | 182,895,363 | 174,896,239 | 168,632,420 | ||||||

Capitalization ($) | |||||||||||

Common shareholders' equity | 74,728,352 | 70,005,415 | 66,220,407 | 63,767,184 | 60,760,170 | ||||||

Long-term debt | 53,500,000 | 55,000,000 | 56,500,000 | 56,751,006 | 57,112,000 | ||||||

Total capitalization | 128,228,352 | 125,005,415 | 122,720,407 | 120,518,190 | 117,872,170 | ||||||

Short-Term Debt ($) (c) | 1,500,000 | 1,500,000 | 1,500,000 | 1,200,000 | 1,200,000 | ||||||

Other Items ($) | |||||||||||

Capital expenditures | 8,077,642 | 7,179,473 | 7,337,115 | 8,123,479 | 5,275,194 | ||||||

Total property, plant and equipment | 229,367,319 | 223,545,925 | 217,172,542 | 211,409,336 | 204,248,520 | ||||||

(a) | We implemented new regulated base rates as approved by the Kentucky Public Service Commission in October, 2010 and the rates were designed to generate additional annual revenue of $3,513,000, with a $1,770,000 increase in annual depreciation expense. |

(b) | In 2012, $877,000 of interest expense was accrued relating to a tax assessment. In 2013, the assessment was resolved and the previously accrued interest was reversed. |

(c) | Includes current portion of long-term debt. |

16

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations

Overview of 2014 and Future Outlook

Overview

The following is a discussion of the segments we operate, our corporate strategy for the conduct of our business within these segments and significant events that have occurred during 2014. Our Company has two segments: (i) a regulated natural gas distribution and transmission segment, and (ii) a non-regulated segment which participates in related activities, consisting of natural gas marketing, natural gas production and the sale of liquids extracted from natural gas.

Earnings from the regulated segment are primarily influenced by sales and transportation volumes, the rates we charge our customers and the expenses we incur. In order for us to achieve our strategy of maintaining reasonable long-term earnings, cash flow and stock value, we must successfully manage each of these factors. Regulated sales volumes are temperature-sensitive. Our regulated sales volumes in any period reflect the impact of weather, with colder temperatures generally resulting in increased sales volumes. The impact of winter temperatures on our revenues is partially reduced by our ability to adjust our winter rates for residential and small non-residential customers based on the degree to which actual winter temperatures deviate from historical average temperatures.

Our non-regulated segment markets natural gas to large-volume customers. We endeavor to enter sales agreements matching supply with estimated demand while providing an acceptable gross margin. The non-regulated segment also produces natural gas and sells liquids extracted from natural gas.

Consolidated earnings per common share for 2014 increased $0.14 per common share as compared to 2013. We experienced a winter that was colder than the preceding year resulting in increased volumes of natural gas sold. Additionally, sales of natural gas liquids increased, as compared to the prior year. Other factors which influenced our 2014 consolidated earnings per common share are further discussed in the Results of Operations.

Future Outlook

Future profitability of the regulated segment is contingent on the adequate and timely adjustment of the rates we charge our regulated customers. The Kentucky Public Service Commission sets these rates, and we monitor our need to file rate cases with the Kentucky Public Service Commission for a general rate increase for our regulated services. The regulated segment's largest expense is natural gas supply, which we are permitted to pass through to our customers. We manage remaining expenses through budgeting, approval and review.

Future profitability of the non-regulated segment is dependent on the business plans of some of our industrial and other large-volume customers and the market prices of natural gas and natural gas liquids, all of which are out of our control. We anticipate our non-regulated segment will continue to contribute to our consolidated net income in fiscal 2015. If natural gas prices increase, we would expect to experience a corresponding increase in our non-regulated segment gross margins related to our natural gas production and marketing activities. However, if natural gas prices decrease, we would expect a decrease in our non-regulated gross margins related to our natural gas production and marketing activities. The profitability of selling natural gas liquids is dependent on the amount of liquids extracted and the pricing for any such liquids, which is determined by a national unregulated market.

Liquidity and Capital Resources

Sources and Uses of Cash

Operating activities provide our primary source of cash. Cash provided by operating activities consists of net income adjusted for non-cash items, including depreciation, amortization, deferred income taxes, share-based compensation and changes in working capital. Our sales and cash requirements are seasonal. The largest portion of our sales occurs during the heating months (December - April), whereas significant cash requirements for the purchase of natural gas for injection into our storage field and capital expenditures occur during non-heating months. Therefore, when cash provided by operating activities is not sufficient to meet our capital requirements, our ability to maintain liquidity depends on our bank line of credit. The current bank line of credit with Branch Banking and Trust Company extends through June 30, 2015 and permits borrowings up to $40,000,000. There were no borrowings outstanding on the bank line of credit as of June 30, 2014 or June 30, 2013.

17

Cash and cash equivalents were $13,676,000 at June 30, 2014 compared with $10,360,000 at June 30, 2013 and $9,741,000 at June 30, 2012. These changes in cash and cash equivalents are summarized in the following table:

$(000) | 2014 | 2013 | 2012 | |||||

Provided by operating activities | 17,340 | 13,557 | 13,514 | |||||

Used in investing activities | (7,870 | ) | (7,108 | ) | (7,012 | ) | ||

Used in financing activities | (6,155 | ) | (5,829 | ) | (4,102 | ) | ||

Increase in cash and cash equivalents | 3,315 | 620 | 2,400 | |||||

In 2014, cash provided by operating activities increased $3,783,000 (28%), as compared to 2013, due to increased cash received from customers as a result of increased sales, partially offset by increased amounts paid for natural gas.

In 2013, there was not a significant change in cash provided by operating activities as compared to 2012.

Changes in cash used in investing activities result primarily from changes in the level of capital expenditures between years.

In 2014, there was not a significant change in cash used in financing activities, as compared to 2013.

In 2013, cash used in financing activities increased $1,727,000 (42%) , as compared to 2012, due to the first annual $1,500,000 repayment on our 4.26% Series A Notes.

Cash Requirements

Our capital expenditures result in a continued need for cash. These capital expenditures are being made for system extensions and for the replacement and improvement of existing transmission, distribution, gathering, storage and general facilities. We expect our capital expenditures for fiscal 2015 to be approximately $10.8 million.

The following is provided to summarize our contractual cash obligations for indicated periods after June 30, 2014:

Payments Due by Fiscal Year | |||||||||||||||

$(000) | 2015 | 2016 - 2017 | 2018 - 2019 | After 2019 | Total | ||||||||||

Interest payments (a) | 2,360 | 4,427 | 4,171 | 20,249 | 31,207 | ||||||||||

Long-term debt (b) | 1,500 | 3,000 | 3,000 | 47,500 | 55,000 | ||||||||||

Pension contributions (c) | 500 | 1,000 | 1,000 | 4,500 | 7,000 | ||||||||||

Natural gas purchases (d) | 140 | — | — | — | 140 | ||||||||||

Total contractual obligations (e) | 4,500 | 8,427 | 8,171 | 72,249 | 93,347 | ||||||||||

(a) | Our long-term debt, notes payable, customers' deposits and unrecognized tax positions all require interest payments. Interest payments are projected based on fiscal 2014 interest payments until the underlying obligation is satisfied. As of June 30, 2014, we have also accrued $5,000 of interest related to uncertain tax positions. These amounts have been excluded from the above table of contractual obligations as the timing of such payments is uncertain. |

(b) | See Note 10 of the Notes to Consolidated Financial Statements for a description of this debt. |

(c) | This represents currently projected contributions to the defined benefit plan through 2028, as recommended by our actuary. |

(d) | As of June 30, 2014, we had a contract which had a minimum purchase obligation. The contract term expires December, 2014. The remainder of our natural gas purchase contracts are either requirements-based contracts, or contracts with a minimum purchase obligation extending for a time period not exceeding one month. |

18

(e) | We have other long-term liabilities which include deferred income taxes ($40,538,000), regulatory liabilities ($1,165,000), asset retirement obligations ($3,261,000) and deferred compensation ($907,000). Based on the nature of these items their expected settlement dates cannot be estimated. |

All of our operating leases are year-to-year and cancelable at our option.

See Note 13 of the Notes to Consolidated Financial Statements for other commitments and contingencies.

Sufficiency of Future Cash Flows

Our ability to maintain liquidity, finance capital expenditures and pay dividends is contingent on the adequate and timely adjustment of the regulated rates we charge our customers. The Kentucky Public Service Commission sets these rates and we monitor our need to file for rate increases for our regulated segment. Our regulated base rates were most recently adjusted in our 2010 rate case and became effective in October, 2010. We expect that cash provided by operations will be sufficient to satisfy our operating and normal capital expenditure requirements and to pay dividends for the next twelve months and the foreseeable future. To the extent that internally generated cash is not sufficient to satisfy seasonal operating and capital expenditure requirements and to pay dividends, we rely on our bank line of credit.

In December, 2011, we refinanced our 5.75% Insured Quarterly Notes and 7% Debentures from the proceeds of a private debt financing. Under the Note Purchase and Private Shelf Agreement, we issued $58,000,000 of Series A Notes, for which the purchasers paid 100% of the face principal amount. The proceeds from the sale of the Series A Notes were used to fund the redemption of our 5.75% Insured Quarterly Notes Due April 1, 2021, which had an outstanding principal balance of $38,450,000, and our 7% Debentures Due February 1, 2023, which had an outstanding principal balance of $19,410,000.

Our Series A Notes are unsecured, bear interest at a rate of 4.26% per annum, which is payable quarterly, and mature on December 20, 2031. We are required to make an annual $1,500,000 principal payment on the Series A Notes each December. Any refinance of the Series A Notes, or any additional prepayments of principal, may be subject to a prepayment penalty.

With our bank line of credit agreement and Series A Notes, we have agreed to certain financial covenants. Noncompliance with these covenants can make the obligations immediately due and payable. We have agreed to the following financial covenants:

• | The Company must at all times maintain a tangible net worth of at least $25,800,000. |

• | The Company must at the end of each fiscal quarter maintain a total debt to capitalization ratio of no more than 70%. The total debt to capitalization ratio is calculated as the ratio of (i) the Company's total debt to (ii) the sum of the Company's shareholders' equity plus total debt. |

• | The Company must maintain a fixed charge coverage ratio for the twelve months ending each quarter of not less than 1.20x. The fixed charge coverage ratio is calculated as the ratio of (i) the Company's earnings adjusted for certain unusual or non-recurring items, before interest, taxes, depreciation and amortization plus rental expense to (ii) the Company's interest and rental expense. |

• | The Company may not pay aggregate dividends on its capital stock (plus amounts paid in redemption of its capital stock) in excess of the sum of $15,000,000 plus the Company's cumulative earnings after September 30, 2011 adjusted for certain unusual or non-recurring items. |

19

The following table shows the required and actual financial covenants under our Series A Notes as of June 30, 2014:

Requirement | Actual | |||||

Tangible net worth | no less than $25,800,000 | $ | 73,961,000 | |||

Debt to capitalization ratio | no more than 70% | 42 | % | |||

Fixed charge coverage ratio | no less than 1.20x | 8.79 | x | |||

Dividends paid | no more than $36,594,000 | $ | 13,816,000 | |||

Our 4.26% Series A Notes restrict us from:

• | with limited exceptions, granting or permitting liens on or security interests in our properties, |

• | selling a subsidiary, except in limited circumstances, |

• | incurring secured debt, or permitting a subsidiary to incur debt or issue preferred stock to any third party, in an aggregate amount that exceeds 10% of our tangible net worth, |

• | changing the general nature of our business, |

• | merging with another company, unless (i) we are the survivor of the merger or the survivor of the merger is another domestic company that assumes the 4.26% Series A Notes, (ii) there is no event of default under the 4.26% Series A Notes and (iii) the continuing company has a tangible net worth at least as high as our tangible net worth immediately prior to such merger, or |

• | selling or transferring assets, other than (i) the sale of inventory in the ordinary course of business, (ii) the transfer of obsolete equipment and (iii) the transfer of other assets in any 12 month period where such assets constitute no more than 5% of the value of our tangible assets and, over any period of time, the cumulative value of all assets transferred may not exceed 15% of our tangible assets. |

Without the consent of the bank that has extended to us our bank line of credit or terminating our bank line of credit, we may not:

• | merge with another entity; |

• | sell a material portion of our assets other than in the ordinary course of business, |

• | issue stock which in the aggregate exceeds thirty-five percent (35%) of our outstanding shares of common stock, or |

• | permit any person or group of related persons to hold more than twenty percent (20%) of the Company's outstanding shares of stock. |

Furthermore, the agreement governing our 4.26% Series A Notes contains a cross-default provision which provides that we will be in default under the 4.26% Series A Notes if we are in default on any other outstanding indebtedness that exceeds $2,500,000. Similarly, the loan agreement governing the bank line of credit contains a cross-default provision which provides that we will be in default under the bank line of credit if we are in default under our 4.26% Series A Notes and fail to cure the default within ten days of notice from the bank. We were in compliance with the covenants under our bank line of credit and 4.26% Series A Notes for all periods presented in the Consolidated Financial Statements.

Critical Accounting Policies and Estimates

Preparation of financial statements and related disclosures in compliance with generally accepted accounting principles requires the use of assumptions and estimates regarding future events, including the likelihood of success of particular investments or initiatives, estimates of future prices or rates, legal and regulatory challenges and anticipated recovery of costs. Therefore, the possibility exists for materially different reported amounts under different conditions or assumptions. We consider an accounting

20

estimate to be critical if (i) the accounting estimate requires us to make assumptions about matters that were reasonably uncertain at the time the accounting estimate was made and (ii) changes in the estimate are reasonably likely to occur from period to period.

These critical accounting estimates should be read in conjunction with the Notes to Consolidated Financial Statements. We have other accounting policies that we consider to be significant; however, these policies do not meet the definition of critical accounting estimates, because they generally do not require us to make estimates or judgments that are particularly difficult or subjective.

Regulatory Accounting

Our accounting policies reflect the effects of the rate-making process in accordance with regulatory accounting standards. Our regulated segment continues to be cost-of-service rate regulated, and we believe the application of regulatory accounting standards to that segment is appropriate. If, as a result of a change in circumstances, it is determined that the regulated segment no longer meets the criteria of regulatory accounting, that segment will have to discontinue regulatory accounting and write-off the respective regulatory assets and liabilities. Such a write-off could have a material impact on our consolidated financial statements.

The application of regulatory accounting standards results in recording regulatory assets and liabilities. Regulatory assets represent the deferral of incurred costs that are probable of future recovery in customer rates. In some cases, we record regulatory assets before approval for recovery has been received from the Kentucky Public Service Commission. We must use judgment to conclude that costs deferred as regulatory assets are probable of future recovery. We base this conclusion on certain factors, including changes in the regulatory environment, recent rate orders issued by the Kentucky Public Service Commission and the status of any potential new legislation. Regulatory liabilities represent revenues received from customers to fund expected costs that have not yet been incurred, or they represent probable future refunds to customers.

We use our best judgment when recording regulatory assets and liabilities; however, regulatory commissions can reach different conclusions about the recovery of costs, and those conclusions could have a material impact on our consolidated financial statements. We believe it is probable that we will recover the regulatory assets that have been recorded.

Pension

We have a non-contributory, defined benefit retirement plan covering all eligible employees hired prior to May 9, 2008. The net periodic benefit costs (“pension costs”) for our defined benefit plan as described in Note 6 of the Notes to Consolidated Financial Statements are dependent upon numerous factors resulting from actual plan experience and assumptions concerning future experience. These costs, for example, are impacted by employee demographics (including age, compensation levels and employment periods), the level of contributions we make to the plan and earnings on plan assets. Additionally, changes made to the provisions of the plan may impact current and future pension costs. Pension costs may also be significantly affected by changes in key actuarial assumptions, including anticipated rates of return on plan assets and the discount rates used in determining the projected benefit obligation and pension costs. For the years ended June 30, 2014, 2013 and 2012, we recorded pension costs for our defined benefit pension plan of $750,000, $980,000 and $481,000, respectively.

Changes in pension obligations associated with the above factors may not be immediately recognized as pension costs in the Consolidated Statements of Income, but may be deferred and amortized in the future over the average remaining service period of active plan participants. As of June 30, 2014, $5,824,000 of net losses have been deferred for amortization as pension costs into future periods.

Our pension plan assets are principally comprised of equity and fixed income investments. Differences between actual portfolio returns and expected returns will result in increased or decreased pension costs in future periods. Likewise, changes in assumptions regarding current discount rates and expected rates of return on plan assets could also increase or decrease pension costs in future periods.

In selecting our discount rate assumption we considered rates of return on high-quality fixed-income investments that are expected to be available through the maturity dates of the pension benefits. Our expected long-term rate of return on pension plan assets was 6% for 2014 and was based on our targeted asset allocation assumption for 2014 of approximately 70% equity investments and approximately 30% fixed income investments. Our targeted investment allocation for equity investments includes allocations to domestic, global and real estate markets. For additional diversification, we also invest in absolute return strategy mutual funds, which include both equity and fixed income securities. Our asset allocation is designed to achieve a moderate level of overall portfolio risk in keeping with our desired risk objective. We regularly review our asset allocation and periodically rebalance our investments to our targeted allocation as appropriate.

21

The funded status of our plan reflects investment gains or losses in the year in which they occur based on the market value of assets at the measurement date.