Attached files

| file | filename |

|---|---|

| EX-99.1 - EX-99.1 - ASSOCIATED BANC-CORP | d758346dex991.htm |

| 8-K - 8-K - ASSOCIATED BANC-CORP | d758346d8k.htm |

ASSOCIATED BANC-CORP

2Q 2014 EARNINGS PRESENTATION

JULY 17, 2014

Exhibit 99.2 |

FORWARD-LOOKING STATEMENTS

Important

note

regarding

forward-looking

statements:

Statements made in this presentation which are not purely historical are

forward-looking statements, as defined in the Private Securities

Litigation Reform Act of 1995. This includes any statements regarding

management’s plans, objectives, or goals for future operations, products or

services,

and

forecasts

of

its

revenues,

earnings,

or

other

measures

of

performance.

Such

forward-looking

statements

may

be

identified

by

the

use

of

words

such

as

“believe”,

“expect”,

“anticipate”,

“plan”,

“estimate”,

“should”,

“will”,

“intend”,

“outlook”,

or

similar

expressions.

Forward-

looking statements are based on current management expectations and, by their

nature, are subject to risks and uncertainties. Actual results may differ

materially from those contained in the forward-looking statements.

Factors which may cause actual results to differ materially from those

contained in such forward-looking statements include those identified in the

Company’s most recent Form 10-K and subsequent SEC filings.

Such factors are incorporated herein by reference.

1 |

2014

SECOND QUARTER HIGHLIGHTS 2

Loan Growth drives Solid Earnings

•

Average loans of $16.6 billion were up $482 million, or 3% from the first

quarter Total average commercial loans grew $398 million from the first

quarter Credit card portfolio purchased on June 30, 2014 for $108

million •

Net interest income of $169 million was up $4 million, or 2% from the first

quarter Interest on Commercial loans was up $3 million, or 3% from the first

quarter •

Net interest margin of 3.08% compared to 3.12% in the first quarter

•

Quarterly dividend of $0.09 / common share, or 32% of second quarter

earnings •

Repurchased 1.7 million shares of common stock during the second

quarter

July 1st –

repurchased additional 1.6 million shares in accelerated program

•

Capital ratios remain strong and above Basel III targets

•

Noninterest income of $72 million was down $1 million compared to the first

quarter Core fee-based revenues grew $3 million from the first

quarter •

Noninterest expense of $168 million was flat compared to the first quarter

Efficiency ratio improved from the first quarter to 68%

•

Net income available to common shareholders of $45 million or $0.28 per

share •

Pretax income of $68 million was up $2 million, or 3% from the first quarter

•

Return on Tier 1 Common Equity of 9.6%

Net Interest Income

&

Net Interest Margin

Noninterest Income

&

Expenses

Capital

Balance Sheet

Net Income

&

ROT1CE |

LOAN

PORTFOLIO COMPOSITION 3

2Q 2014 Average Net Loan Change (+$482 mln)

Loan

Mix

–

2Q

2014

(Average)

($ in millions)

Home Equity & Installment

Commercial Real Estate

Residential Mortgage

Power & Utilities

Oil & Gas

Mortgage Warehouse

General Commercial Loans

Average Quarterly Loans ($ in billions)

$16.6

+4%

% Chg

+78%

+2%

+14%

(3%)

$15.7

+2%

$16.2

$14.6

$13.0

Total

Commercial &

Business

Lending

+6%

+8%

$4.2

$5.0

$5.9

$6.1

$6.5

$2.9

$3.3

$3.7

$3.9

$4.0

$2.7

$3.3

$3.7

$3.9

$4.1

$3.2

$3.0

$2.5

$2.2

$2.1

2Q 2011

2Q 2012

2Q 2013

1Q 2014

2Q 2014

Commercial & Business

Commercial Real Estate

Residential Mortgage

Home Equity & Installment

($67)

$48

$60

$74

$97

$119

$151

CRE Investor

18%

Construction

6%

Commercial

& Business

Lending

39%

Res Mtg

25%

Home Equity

10%

Installment

2% |

COMMERCIAL LINE UTILIZATION TRENDS

4

Line utilization increased in Commercial & Business Lending

Change from 1Q 14

Commercial Real

Estate (including

construction)

-

260 bps

Commercial &

Business Lending

+ 290 bps

50.0%

51.1%

48.6%

46.9%

48.8%

51.7%

56.5%

60.4%

61.1%

63.1%

64.2%

61.6%

45.0%

50.0%

55.0%

60.0%

65.0%

1Q 2013

2Q 2013

3Q 2013

4Q 2013

1Q 2014

2Q 2014

Commercial & Business Lending

Commercial Real Estate |

160,000 “Associated Bank”

branded card accounts

CREDIT CARD PORTFOLIO PURCHASE

5

Summary Details:

ASBC and US Bank will both participate on a pro-rata basis in all revenues,

credit losses, and growth going forward.

Elan will continue to administer, service, and manage the portfolio for a fixed,

per account fee. The purchase premium will be amortized over 5 years.

55%

participation

45%

participation

ASBC acquired a 45% participation interest ($99 million) in a credit card portfolio

of customers who currently hold “Associated Bank”

branded credit card accounts for $108 million.

ASBC will forego referral fees it has been receiving from Elan/US Bank for new

accounts but expects that the net yield on the portfolio (net of losses and

premium amortization) will offset this foregone fee revenue.

Transaction is expected to result in less card based fee income but more net

interest income. Bottom line impact should not be material in 2014,

but will build value over time and contribute to earnings growth as the

portfolio grows. |

GROWING

NET INTEREST INCOME WHILE MARGIN COMPRESSES

6

Yield on Interest-earning Assets

Cost of Interest-bearing Liabilities

Net Interest Income & Net Interest Margin

($ in millions)

$160

$161

$167

$165

Net Interest Margin

$169

$1

<$1

<$1

0.41%

0.35%

0.31%

0.38%

0.29%

2Q 2013

3Q 2013

4Q 2013

1Q 2014

2Q 2014

$159

$159

$163

$164

$168

$1

$4

Net Interest Income Net of Interest Recoveries

Interest Recoveries

0.24%

0.23%

0.22%

0.19%

0.19%

2Q 2013

3Q 2013

4Q 2013

1Q 2014

2Q 2014

Interest Bearing Deposit Costs

Other Funding Costs

3.47%

3.42%

3.50%

3.36%

3.31%

3.16%

3.13%

3.23%

3.12%

3.08%

2Q 2013

3Q 2013

4Q 2013

1Q 2014

2Q 2014 |

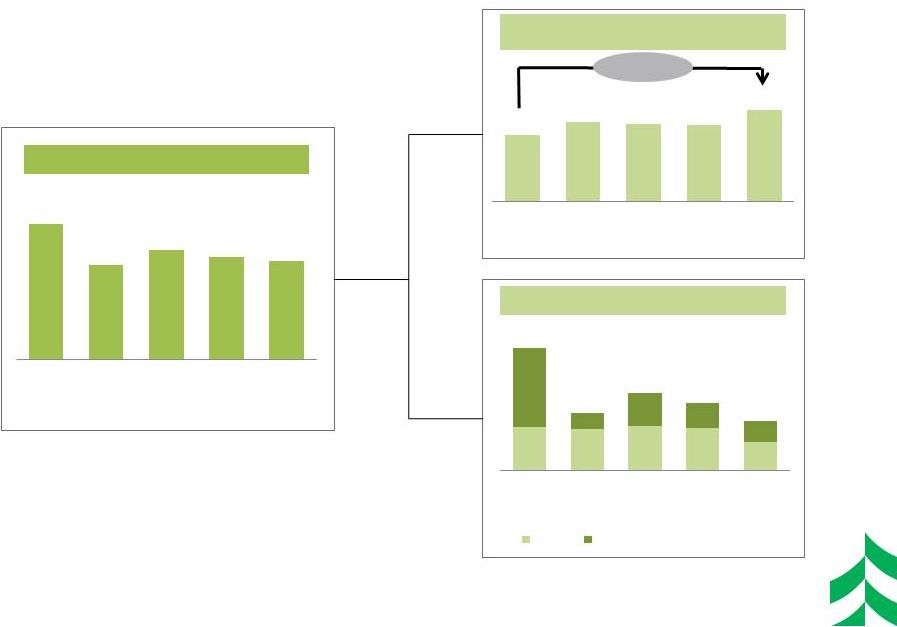

NONINTEREST INCOME TRENDS

($ IN MILLIONS)

7

Core

Fee-based

Revenue

Other

Noninterest

Income

Total Noninterest Income

1

–

Core

Fee-based

Revenue

=

Trust

service

fees

plus

Service

charges

on

deposit

accounts

plus

Card-based

and

other

nondeposit

fees

plus

Insurance

commissions plus Brokerage and annuity commissions. This is a non-GAAP

measure. Please refer to press release tables for more information.

2

–

Other

Noninterest

Income

=

Total

Noninterest

Income

minus

Core

Fee-based

Revenue.

$29

$13

$19

$17

$12

$84

$71

$76

$74

$72

2Q

2013

3Q

2013

4Q

2013

1Q

2014

2Q

2014

$55

$58

$57

$57

$60

2Q

2013

3Q

2013

4Q

2013

1Q

2014

2Q

2014

+10%

$10

$10

$10

$10

$7

$19

$4

$8

$6

$5

2Q

2013

3Q

2013

4Q

2013

1Q

2014

2Q

2014

Other

Mortgage Banking Income (net)

1

2 |

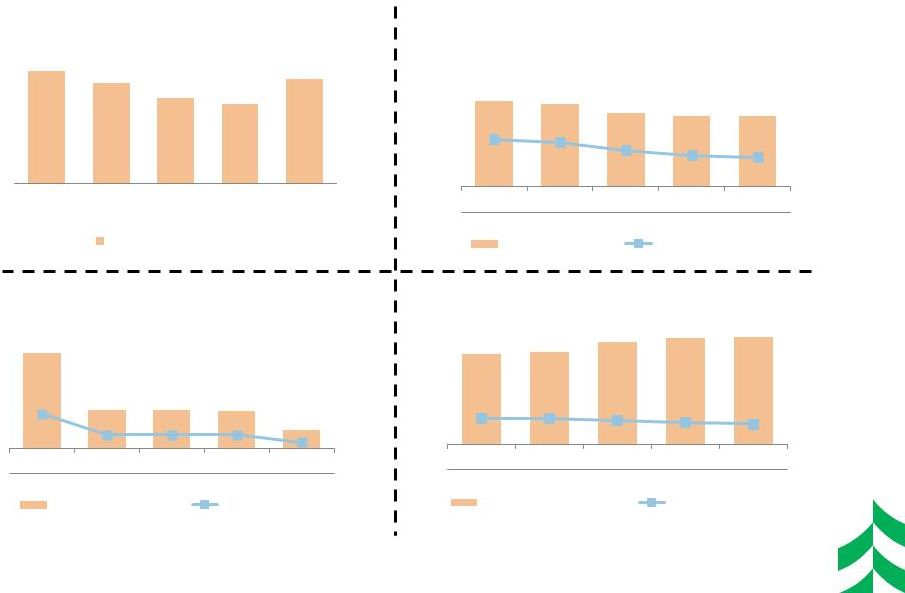

NONINTEREST EXPENSE TRENDS

($ IN MILLIONS)

8

Total Noninterest Expense

Personnel

Spend

/

FTE

Trend

Efficiency Ratio

67%

70%

73%

69%

68%

Other

Non-Personnel

Spend

Trend

1

–

Efficiency

ratio

=

Noninterest

expense,

excluding

amortization

of

intangibles,

divided

by

sum

of

taxable

equivalent

net

interest

income

plus

noninterest

income,

excluding investment securities gains, net, and asset gains, net. This is a

non-GAAP financial measure. Please refer to the appendix for a reconciliation of this.

2

–

FTE

= Average Full Time Equivalent Employees

3

–

Technology

Spend

=

Data

Processing

and

Equipment

expenses

4

–

Other

Non-Personnel

Spend

=

Total

Noninterest

Expense

less

Personnel

and

Technology

spend

3

4

$69

$67

$78

$70

$70

$169

$165

$179

$168

$168

2Q

2013

3Q

2013

4Q

2013

1Q

2014

2Q

2014

$100

$98

$101

$98

$98

4,790

4,699

4,584

4,517

4,431

2Q

2013

3Q

2013

4Q

2013

1Q

2014

2Q

2014

Personnel Spend

FTE

$19

$19

$19

$19

$21

$50

$49

$58

$51

$49

2Q

2013

3Q

2013

4Q

2013

1Q

2014

2Q

2014

Technology Spend

Other Non-Personnel

1

2 |

CREDIT

QUALITY INDICATORS ($ IN MILLIONS)

9

$310

$277

$235

$220

$288

2Q 2013

3Q 2013

4Q 2013

1Q 2014

2Q 2014

Potential Problem Loans

$217

$208

$185

$178

$179

1.38%

1.33%

1.17%

1.08%

1.05%

2Q 2013

3Q 2013

4Q 2013

1Q 2014

2Q 2014

Nonaccruals

Nonaccruals / Loans

$14

$5

$5

$5

$3

0.35%

0.14%

0.14%

0.14%

0.06%

2Q 2013

3Q 2013

4Q 2013

1Q 2014

2Q 2014

Net Charge Offs

NCOs / Avg Loans

127%

131%

145%

151%

152%

1.76%

1.74%

1.69%

1.63%

1.59%

2Q 2013

3Q 2013

4Q 2013

1Q 2014

2Q 2014

ALLL/ Nonaccruals

ALLL/ Total Loans |

EPS,

DIVIDENDS, AND CAPITAL DEPLOYMENT •

Current capital levels are in excess of

“well-capitalized”

regulatory benchmarks

Existing capital levels are already

above Basel III capital levels

$115 mm of remaining share

repurchase authorization

10

Tier 1 Common Equity Ratio

EPS and Dividends Paid & ROT1CE

Earnings & Dividends

per Common Share

Return on Tier 1

Common Equity

Definition of Tier 1 Common Equity:

Tier

1

Common

Equity

(T1CE),

a

non-GAAP

financial

measure,

is

used

by

banking

regulators,

investors

and

analysts

to

assess

and

compare

the

quality

and

composition of our capital with the capital of other financial services companies.

Management uses Tier 1 common equity, along with other capital measures, to assess

and

monitor

our

capital

position.

Tier

1

Common

Equity

is

Tier

1

capital

excluding

qualifying

perpetual

preferred

stock

and

qualifying

trust

preferred

securities.

$0.15

$0.24

$0.28

$0.28

12.61%

12.04%

11.49%

10.72%

2Q 2011

2Q 2012

2Q 2013

2Q 2014

$0.01

$0.05

$0.08

$0.09

2Q 2011

2Q 2012

2Q 2013

2Q 2014

6.1%

9.3%

9.9%

9.6% |

2014

SECOND HALF OUTLOOK 11

Asset Growth

Deposits / Funding

Mix

Margin

Noninterest

Income

Noninterest

Expense

Capital

Provision

•

Full year 2014 annual

average loan growth of approximately 8%

•

Mid single digit average deposit and slightly higher other

funding growth

•

NIM compression of a few basis points per quarter

•

Net interest income growth

•

Second half 2014 noninterest income in line with first half 2014

•

Total 2014 expenses expected to be flat compared to

2013 with a continued focus on efficiency initiatives

•

Continue to follow stated corporate priorities for capital

deployment

•

Provision based on expected loan growth and other factors

|

APPENDIX

12 |

RECONCILIATION AND DEFINITIONS OF

NON-GAAP ITEMS

13

2Q 2013

3Q 2013

4Q 2013

1Q 2014

2Q 2014

Efficiency Ratio Reconciliation:

Efficiency ratio (1)

69.01%

71.45%

73.70%

70.41%

69.70%

Taxable equivalent adjustment

(1.38)

(1.50)

(1.49)

(1.35)

(1.32)

Asset gains (losses), net

(0.01)

0.59

0.80

0.22

0.26

Other intangible amortization

(0.41)

(0.44)

(0.42)

(0.42)

(0.41)

Efficiency ratio, fully taxable equivalent (1)

67.21%

70.10%

72.59%

68.86%

68.23%

(1) Efficiency

ratio

is

defined

by

the

Federal

Reserve

guidance

as

noninterest

expense

divided

by

the

sum

of

net

interest

income

plus

noninterest

income, excluding investment securities gains / losses, net. Efficiency

ratio, fully taxable equivalent, is noninterest expense, excluding other

intangible amortization, divided by the sum of taxable equivalent net interest

income plus noninterest income, excluding investment securities gains /

losses, net and asset gains / losses, net. This efficiency ratio is presented on a taxable equivalent basis, which adjusts net interest

income for the tax-favored status of certain loans and investment

securities. Management believes this measure to be the preferred industry

measurement of net interest income as it enhances the comparability of net interest

income arising from taxable and tax-exempt sources and it excludes

certain specific revenue items (such as investment securities gains / losses, net and asset gains / losses, net). |