Attached files

| file | filename |

|---|---|

| 8-K - 8-K - EASTON-BELL SPORTS, INC. | esbi-8k_20140318.htm |

Transaction Summary

On

February

13,

2014,

Easton-Bell

Sports,

Inc.

reached

an

agreement

to

sell

the

assets

of

its

Easton

Baseball

/

Softball business to Bauer Performance Sports (“Bauer”) for $330MM

–

Closing expected in March / April 2014

Easton-Bell Sports, Inc. also announced that it is working towards an agreement

with a third party for the sale of its Easton Hockey business

–

Easton Hockey will be an Unrestricted Subsidiary until it is sold

Proceeds from the sale will be used in conjunction with a new financing to retire

the existing Easton-Bell Sports, Inc. 2016 Senior Secured Notes, the EB

Sports Corp. HoldCo Facility, and pay anticipated transaction fees and

expenses

–

$30MM of proceeds earmarked as unrestricted HoldCo cash to fund acquisitions or

capital structure changes The contemplated new financing includes the

following: –

$150MM

5-year

ABL

(undrawn

at

closing)

(1)

–

$205MM

7-year

1

st

Lien

Term

Loan

–

$105MM

8-year

2

nd

Lien

Term

Loan

The

contemplated new financing represents, on a pro forma basis, 1st Lien Debt / Pro

Forma Adj. EBITDA of 3.3x, Total Debt / Pro Forma Adj. EBITDA of 5.0x, and

Net Debt / Pro Forma Adj. EBITDA of 4.7x Upon completion of these

transactions, Easton-Bell Sports, Inc. will be renamed BRG Sports, Inc.

Note

1.ABL revolver may be additionally drawn for seasonal working capital needs

unrelated to funding the transaction Exhibit 99.1

|

Transaction Overview: Financing of BRG Sports

(5)

(3)

(7)

(4)

(2)

(6)

(2)

PF Capitalization | Credit Statistics

Pro Forma ($MM)

12/28/2013

Cash on Balance Sheet

19

New ABL Revolver ($150MM capacity)

0

New Term Loan (1st Lien)

205

New Term Loan (2nd Lien)

105

Total Debt

310

PF 2013E Adj. EBITDA

62

1st Lien Debt / PF Adj. EBITDA

3.3x

2nd Lien Debt / PF Adj. EBITDA

1.7x

Bank Debt / PF Adj. EBITDA

5.0x

Total Debt / PF Adj. EBITDA

5.0x

Net Debt / PF Adj. EBITDA

4.7x

Sources & Uses

Sources

Amount ($MM)

%

(1)

New ABL Revolver ($150MM capacity)

0

0

New 1st Lien Term Loan

205

32

New 2nd Lien Term Loan

105

16

Net Proceeds from Asset Sale

337

52

Total Sources

647

100

Uses

Amount ($MM)

%

(1)

Retire ABL Facility

23

4

Retire Senior Notes

350

54

Retire HoldCo Facility

145

22

HoldCo Unrestricted Cash Allocation

30

5

Partial Long-Term Incentive Payout

23

4

Transaction Costs, Financing Fees, and OID

52

8

Cash for Capitalizing Hockey

15

2

Cash for Restructuring Post-Transaction

9

1

Total Uses

647

100

Notes

1.

Figures may not add due to rounding

2.

ABL revolver may be additionally drawn for seasonal working capital needs unrelated to funding the

transaction

3.

Sale price of $330MM, adjusted for working capital, IP settlement, and escrowed proceeds 4.

Includes accrued interest of $3MM as of December 28, 2013 5.

Long-term incentive payments to Easton Sports, Inc. employees, former EBS management, group of

current BRG employees, and certain Board members

6.

Includes $10 million of financing fees and OID, bond breakage costs of $17 million ($350 million senior

notes outstanding x 4.875% call premium), and other transaction costs of $26 million

7.

A reconciliation of the non-GAAP measures presented to the comparable GAAP information can be found

on page 51 of this presentation |

...With Market Leading Positions

Leading Positions Across All Categories

Market Share (%)

Sources: 2013 NAERA data, Leisure Trends, Management Estimates

56%

62%

56%

42%

41%

Football Helmets

Reconditioning

Services

U.S. Mass Cycling

Accessories

Global Specialty

Cycling Helmets

U.S. Snow Helmets |

Riddell: The Football Specialty Company

A Leader in Football Equipment

Impressive and Continuous Growth

Broad Customer Base With Little Concentration

Premier developer, manufacturer and reconditioner

of football equipment, uniforms, and accessories

Leading market positions in each category

–

56% market share by sales in helmets

–

Meaningful share increases over the past five

years

–

Majority of players wear Riddell helmets

Record revenue and EBITDA performance

–

Share-driven unit growth and consistent ASP

increases

–

High gross margins with improvement through

innovation and reconditioning relocation

–

SG&A leverage despite R&D and marketing

investments

–

Strong free cash flow profile

Industry highly concentrated, only a few key players

–

Riddell, Schutt, and Rawlings

2013E Net Sales, %

$144

$160

$177

$203

$205

43.9%

43.3%

43.1%

44.5%

44.1%

Net Sales ($MM)

Gross Margin (%)

Institutional Sales

63%

Reconditioning

24%

Consumer

13%

A favorite among NFL professionals

2009

2010

2011

2012

2013E |

NFL-Related Litigation Summary

Case Overview

Since 2011, roughly 5,000 former NFL players have filed claims against the

NFL Only 25% of these plaintiffs have made a claim against Riddell

Although there is some overlap, the claims made against Riddell are different from

those made against the NFL The claims made in the cases naming Riddell

primarily relate to: Product Design

Product Manufacturing

Adequacy of Warnings

Riddell has denied liability in early court filings and will continue to vigorously

defend itself NFL players were not required to wear Riddell helmets, and not

all NFL players wore Riddell helmets It

is

possible

that

certain

cases

against

Riddell

will

proceed

to

“bellwether”

trials

Riddell

has

substantial

insurance

coverage

over

50+

years

for

the

NFL

player

claims

More than 80% of Riddell’s defense expenses are being paid by its

insurers |

NFL-Related

Litigation

Summary

(Cont’d)

Timeline

&

Process

–

A

proposed

settlement

was

reached

between

the

plaintiffs

and

the

NFL

in

late

summer

2013

–

Riddell is not a party to the proposed settlement between the plaintiffs and the

NFL –

Riddell is under no obligation to settle with the plaintiffs

–

If claims against Riddell are not resolved by settlement, the litigation will

proceed and the Judge will likely rule on pending procedural motions

–

Thereafter, depending on the outcome of the first round of motions, Riddell will

likely file a second round of motions, focused more on the deficiencies in

the plaintiffs' specific claims. –

After that, discovery about facts supporting the claims and defenses may be

exchanged by the parties, depending

on

the

Court’s

rulings

on

the

Riddell

defendants’

preliminary

motions

–

Therefore, Riddell is limited in what it can discuss on these matters

In

Summer

2013,

the

MDL

Judge

ordered

the

parties

to

participate

in

mediation

We do not expect any major milestones in the case involving Riddell until the

proposed settlement between plaintiffs and the NFL gets preliminarily

approved The

court

entered

a

“gag”

order

prohibiting

Riddell

and

its

counsel

from

publicly

discussing

the

mediation

process |

Multiple Lines of Defense

1

Product Liability Theory

Evidentiary Support / Statute of Limitations

Process and Timing

Insurance Coverage

2

3

4 |

2013E Net Sales, %

(2)

Action Sports: Global Cycling, Snow, and Powersports Leader

Stable Core Sales Base

A combination of two market-leading brands in Bell

and Giro

–

Helmets, accessories, footwear and apparel for

cycling, snowsports, and powersports

Segment also includes:

–

Blackburn cycling accessories

–

Easton cycling wheels and components

–

Exit from non-core Mass Fitness / Football

categories, Easton wheels quality issues

–

Unfavorable 2012/2013 seasonal weather

A Winning Combination

Notes

1.Reflects

core

operations

–

excludes

Mass

Fitness/Football

and

Easton

Cycling

2.Certain items with immaterial contribution not reflected in graph

Diversified by Both Brand and Category

Core Revenue

(1)

($MM)

Core Gross Margin

(1)

(%)

Mass Accessories

24%

Mass Helmets

9%

Mass Juvenile Licensed

9%

Specialty Cycling Helmets

9%

Powersports

7%

Specialty Cycling

Helmets

14%

Snow

Helmets

8%

Footwear

4%

Other Giro

4%

Easton

6%

Blackburn

6%

6%

6%

30%

Recent performance impacted by:

Giro

Bell

Blackburn

Easton

58% |

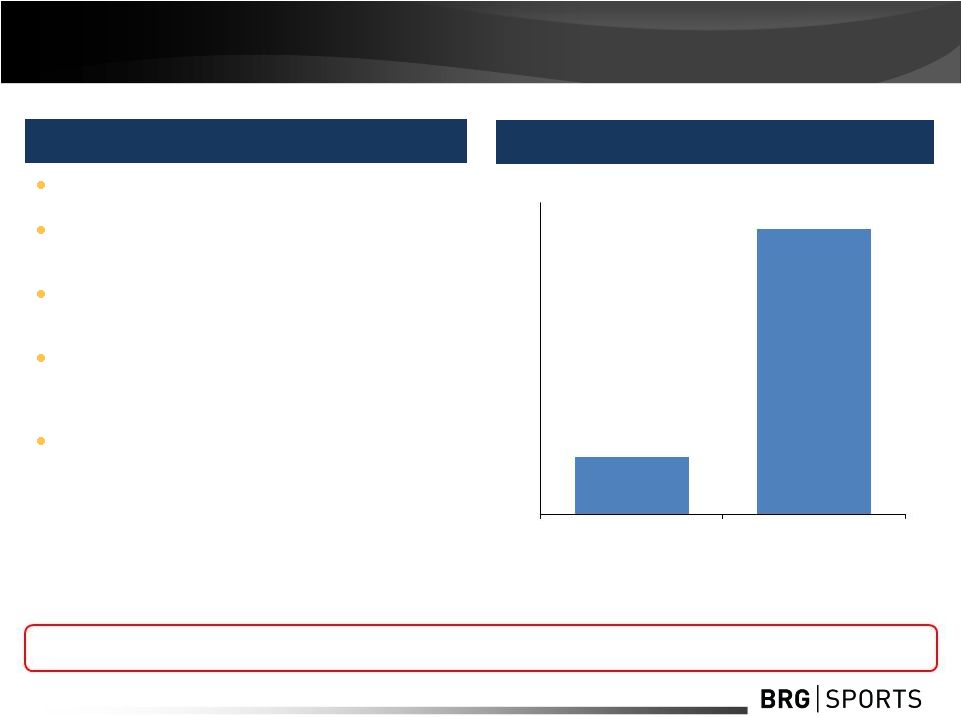

Significant Powersports Opportunity

45% Powersports 2011 to 2013E Net Sales CAGR

Highly confident 2014 growth will be even higher due

to last year’s re-acquisition of int’l distribution rights

Domestic door count could more than double in the

next few years

Co-branding arrangement with Harley-Davidson may

lead to a broader global opportunity with this

powerhouse brand

Snowmobile category expansion opportunity

Illustrative Potential if Market Share Approaches

Levels Bell Has in Other Categories

9%

40%

2013E Market Share

Illustrative 2018E Market Share

$MM

Poised for Growth

Powersports can easily exceed projections to be a $75M business in the next few

years Source: Management Estimates

$0

$20

$40

$60

$80

$100

$120 |

Stable Financial Performance

Net

Sales

(1)

Gross

Profit

and

Margin

(1)

PF

Adj.

EBITDA

(1)(2)(3)

and

Margin

Capital

Expenditures

(4)

$MM

$MM, Margins in %

Action Sports

Riddell

Total BRG Margin

$MM, Margins in %

$MM, Margins in %

Total BRG

Notes

1.Figures may not sum due to rounding

2.A reconciliation of the non-GAAP measures presented to the comparable GAAP

information can be found on page 51 of this presentation 3.Pro forma corporate

costs of $27MM in 2011, $31MM in 2012, and $22MM in 2013 allocated to Riddell and Action Sports based on annual revenue contribution

4.Capex adjusted for costs related to new distribution center (2012: $0.4MM; 2013E:

$3.6MM) and excess corporate project costs (2011: $6.4MM; 2012: $7.6MM; 2013E: $8.0MM)

64

57

62

12

12

13

546

556

533

193

202

195

177

203

205

327

353

369

116

111

105

91

90

76

29

33

42

23

23

33

2.2%

2.1%

2.4%

36.6%

36.3%

35.3%

11.7%

10.2%

11.8%

2011

2012

2013E

2011

2012

2013E

2011

2012

2013E

2011

2012

2013E |

Strong Cash Flow Generation

$MM

Conversion:

53.6%

33.0%

Run-Rate

Free

Cash

Flow

Bridge

(1)(2)

Notes

1.Illustratively based on 2013E PF Adj. EBITDA; figures may not sum due to

rounding 2.Assumed 42% tax rate for estimated taxes and tax-adjusted

interest. Estimated taxes calculated based on PF Adj. EBIT and pre-interest tax shield

3.Based on 2013E capex, net of costs related to new distribution center ($3.6MM) and

excess corporate project costs ($8.0MM) (2)

(2)

(3)

ILLUSTRATIVE

62

13

16

33

13

21

PF Adj. EBITDA

Maintenance Capex

Est. Taxes

Unlevered FCF

Tax-Adj. Interest

Levered FCF |

Net

Working Capital Dynamics Historical Monthly Net Working Capital

(1)

2012

2011

$MM

Preliminary

($MM, unless otherwise noted)

2011A

2012A

2013E

LTM Avg. Days of Sales Outstanding

95

95

92

LTM Avg. Inventory Turns

4.6x

4.3x

4.2x

LTM Avg. Days Payable Outstanding

48

49

49

LTM Avg. Working Capital ($)

(1)

$139

$145

$134

LTM Avg. Working Capital % of Sales

25.4%

26.1%

25.2%

Actual

Total BRG

Action Sports

Riddell

Note

1.Net working capital includes all current assets and liabilities except cash and

cash equivalents, revolving credit facility, current portion of long-term debt, and tax related items

Change from Peak to Trough (and vice versa)

2013

Cycling category builds

inventory in Q1 for Spring

sales push

Snow category inventory

builds through Summer with

bulk of sales booked from

Aug-Oct with fill-in orders

thereafter

Cycles reflect selling

seasons

Riddell sales increase

through August with A/R

collected once high school

football season begins

|

Product Liability Defense / Insurance

An Emphasis Within BRG

Product liability defense is a core competency of BRG Sports

–

We make great products; we fight frivolous cases and we win

“Ordinary course”

product liability suits are at an all-time low (Bell, Giro, and Riddell)

–

Helmet-related suits at Action Sports continue to decline, fitness (exited

category) contributed bulk of new suits in 2012 and 2013

Total premiums / defense / settlement expenses have remained flat at $9MM between

2011 and 2013 BRG Sports has not lost a product liability case at final

verdict in 10+ years BRG Sports maintains significant insurance for helmet

product liability –

2014 policy recently renewed with exact coverage as prior year

|

Pro

Forma Adjusted EBITDA Reconciliation $MM

(1)

2012

2013

Preliminary GAAP Operating Income

$38.4

$26.7

Inclusion

/

(Removal)

of

Profits

for

Certain

Baseball/Softball

Business

Lines

(2)

(2.4)

(2.4)

Inclusion

of

Profits

for

Certain

Action

Sports

Business

Lines

(3)

5.0

-

Overhead

Absorption

of

Divested

/

Non

Borrower

Businesses

(4)

(12.3)

(12.2)

Non-Cash Stock Compensation

3.3

6.5

Standalone Operating Income

$32.1

$18.6

Other

Non-Recurring

and

Extraordinary

Charges,

Gains

and

Losses

(5)

0.4

16.2

Preliminary Adjusted Operating Income

(6)

$32.5

$34.8

Depreciation and Amortization

24.1

23.7

Preliminary Adjusted EBITDA

(6)

$56.6

$58.5

Pro Forma Adjustment

(7)

–

3.9

Pro Forma Adjusted EBITDA

(6)

$56.6

$62.4

Notes

1.

The financials presented for 2012 are derived from the audited subsidiary-level financials of the

Company. The financials presented for 2013 are derived from the preliminary, unaudited subsidiary-level financials of the

Company. The subsidiary-level audit for 2013 is underway. Figures may not sum due to

rounding.

2.

Revenues and expenses related to baseball / softball products sold through mass merchandisers were

historically booked through BRG Sports. This product line is being divested as part of the Easton operations being sold to

Bauer Performance Sports. Discontinued mass fitness and mass football product lines are included in

unadjusted figures. The financials presented for 2012 are derived from the audited subsidiary-level financials of the

Company. The financials presented for 2013 are derived from the preliminary, unaudited

subsidiary-level financials of the Company. The subsidiary-level audit for 2013 is underway.

3.

Certain revenues and expenses related to Easton wheels and components were historically booked through

Easton Sports. The accounting for this was changed to be included within BRG Sports in 2013.

4.

Represents corporate costs, including depreciation and amortization, allocated to the Easton Sports,

Inc. subsidiary as part of the audit process that are stranded post-divestiture and will remain with BRG Sports.

5.

Represents actual expenses historically permitted to be excluded pursuant to the Company’s Senior

Secured Credit Facilities. Such amount for 2013 includes (i) $9.7 million of expenses paid in connection with employee

severance, retention, relocation and contract termination, (ii) $2.2 million of expenses incurred in

conjunction with the divestiture of the Easton businesses, the refinancing and the acquisition of the Bell international powersports

rights, (iii) $1.3 million of extraordinary inventory write-offs and costs related to the exit from

certain product categories, (iv) $1.0 million of other extraordinary gains, losses or expenses, and (v) $1.9 million of additional

extraordinary items identified as part of Ernst & Young’s quality of earnings review; figures

may not sum due to rounding

6.

This presentation contains non-GAAP financial measures within the meaning of Regulation G

promulgated by the Securities and Exchange Commission. For purposes of Regulation G, a non-GAAP financial measure is a

numerical measure of a company's performance, financial position, or cash flows that either excludes or

includes amounts that are not normally excluded or included in the most directly comparable measure calculated and

presented in accordance with generally accepted accounting principles. Adjusted EBITDA, Pro Forma

Adjusted EBITDA, Adjusted Operating Income, and Adjusted Capital Expenditures, and any ratios derived therefrom, are

non-GAAP financial measures that exclude certain items such as asset impairments, restructuring

activities and other extraordinary gains/losses, in order to estimate our financial results and financial position on a going forward

basis. These measures should be considered in addition to results prepared in accordance with GAAP, but

are not a substitute for GAAP results.

7.

Includes full-year impact of cost reductions implemented and anticipated cost reduction initiatives

upon separation of the Easton businesses and the Financing. |