Attached files

| file | filename |

|---|---|

| EX-31.1 - EXHIBIT 31.1 - CROSSROADS LIQUIDATING TRUST | a50805710ex31_1.htm |

| EX-31.2 - EXHIBIT 31.2 - CROSSROADS LIQUIDATING TRUST | a50805710ex31_2.htm |

| EX-32.1 - EXHIBIT 32.1 - CROSSROADS LIQUIDATING TRUST | a50805710ex32_1.htm |

| EX-32.2 - EXHIBIT 32.2 - CROSSROADS LIQUIDATING TRUST | a50805710ex32_2.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2013

OR

|

¨

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

FOR THE TRANSITION PERIOD FROM TO

COMMISSION FILE NUMBER: 0-53504

KEATING CAPITAL, INC.

(Exact name of registrant as specified in its charter)

|

Maryland

|

26-2582882

|

|

(State of Incorporation)

|

(I.R.S. Employer Identification Number)

|

|

5251 DTC Parkway, Suite 1100

Greenwood Village, CO 80111

(Address of principal executive offices)

(720) 889-0139

(Registrant’s telephone number, including area code)

|

|

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class Registered

|

Name of Each Exchange on Which Registered

|

|

|

Common stock, par value $0.001 per share

|

Nasdaq Capital Market

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨.

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨.

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “accelerated filer,” “large accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer ¨

|

Accelerated filer ¨

|

||

|

Non-accelerated filer x

|

Smaller reporting company ¨

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x.

The aggregate market value of the voting and non-voting common stock held by non-affiliates of the registrant as of the last business day of the registrant’s most recently completed second fiscal quarter was approximately $59.7 million based upon a closing price of $6.78 reported for such date on the Nasdaq Capital Market. Common shares held by each executive officer and director and by each person who owns 5% or more of the outstanding common shares have been excluded in that such persons may be deemed to be affiliates.

As of February 24, 2014, the number of outstanding shares of common stock of the registrant was 9,548,902.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement relating to the 2014 Annual Meeting of Stockholders, to be filed within 120 days after the close of the registrant’s year end, are incorporated by reference into Part III of this Annual Report on Form 10-K.

Keating Capital, Inc.

Annual Report on Form 10-K

For Fiscal Year Ended December 31, 2013

Table of Contents

|

Page

|

|||

|

Part I

|

|||

|

1

|

|||

| 23 | |||

| 42 | |||

| 42 | |||

| 42 | |||

| 42 | |||

|

Part II

|

|||

| 43 | |||

| 47 | |||

| 49 | |||

| 81 | |||

| 82 | |||

| 113 | |||

| 113 | |||

| 113 | |||

|

Part III

|

|||

| 114 | |||

| 114 | |||

| 114 | |||

| 114 | |||

| 114 | |||

|

Part IV

|

|||

| 115 | |||

| 118 | |||

PART I

In this annual report on Form 10-K, unless otherwise indicated, the “Company”, “we”, “us” or “our” refer to Keating Capital, Inc., and “Keating Investments” or “our investment adviser” refer to Keating Investments, LLC.

Item 1. Business

Overview

We are a closed-end, non-diversified investment company that has elected to be regulated as a business development company under the Investment Company Act of 1940, as amended (the “1940 Act”). As a business development company, we are required to comply with certain regulatory requirements. For instance, we generally have to invest at least 70% of our total assets in “qualifying assets,” including securities of private U.S. companies, cash, cash equivalents, U.S. government securities and high-quality debt investments that mature in one year or less. See “Regulation as a Business Development Company” below. Effective January 1, 2010, we elected to be treated for tax purposes as a regulated investment company, or a RIC, under Subchapter M of the Internal Revenue Code of 1986, as amended (the “Code”). We satisfied the RIC requirements for our 2013 taxable year, and we intend to operate so as to qualify as a RIC in 2014. See “— Material U.S. Federal Income Tax Considerations” below.

Our investment objective is to maximize capital appreciation. We seek to accomplish our capital appreciation objective by making investments in the equity and equity-linked securities of later stage, typically venture capital-backed, pre-IPO companies. Since our initial investment in January 2010, we have historically focused on venture capital-backed technology companies.

Our strategy is to evaluate and invest in companies prior to the valuation accretion that we believe occurs once private companies complete an initial public offering. We seek to capture this value accretion, or what we refer to as a private-public valuation arbitrage, by investing primarily in private, micro-cap and small-cap companies that meet our core investment criteria. Our investment strategy can be summarized as buy privately, sell publicly, capture the difference.

Based on our past experience–and representations made to us by our portfolio companies prior to our investments–we anticipate that, on average, it will take about two years after our initial investment for a portfolio company to complete its initial public offering, or IPO. Following a typical lockup restriction which prohibits us from selling our investment during a customary 180-day period following the IPO and an expected additional one-year period to sell our shares in the portfolio company in the public markets, we anticipate that, on average, the holding period for our portfolio company investments will be about four years. However, we may be able to sell our portfolio company positions prior to our targeted four-year holding period in cases where a portfolio company either completes an IPO sooner than we expected or, in lieu of an IPO, completes a strategic merger or sale prior to our targeted holding period.

Our Investment Adviser

We are externally managed by Keating Investments, an investment adviser that was founded in 1997 and is registered under the Investment Advisers Act of 1940, as amended, or the Advisers Act. As our investment adviser, Keating Investments is responsible for managing our day-to-day operations including, without limitation, identifying, evaluating, negotiating, closing, monitoring and servicing our investments. Keating Investments also provides us with the administrative services necessary for us to operate. Our investment activities are managed by Keating Investments pursuant to an investment advisory and administrative services agreement (the “Investment Advisory and Administrative Services Agreement”). Our investment adviser sources our investments through its principal office located in Greenwood Village, Colorado as well as through an additional office in Palo Alto, California.

We pay Keating Investments a fee for its investment advisory services under the Investment Advisory and Administrative Services Agreement consisting of two components–a base management fee and an incentive fee. See “— Investment Advisory and Administrative Services Agreement” below.

The managing member and principal owner of Keating Investments is Timothy J. Keating. Our investment adviser’s principals are Timothy J. Keating, our President, Chief Executive Officer and Chairman of our Board of Directors, Kyle L. Rogers, our Chief Investment Officer, and Frederic M. Schweiger, our Chief Financial Officer, Chief Operating Officer, Chief Compliance Officer, Treasurer, Secretary and a member of our Board of Directors. In addition, Keating Investments employs one other investment professional dedicated to portfolio company origination, due diligence and financial analysis.

Keating Investments has established an investment committee (“Investment Committee”) that must unanimously approve each new portfolio company investment that we make. Messrs. Keating, Rogers and Schweiger are the current members of the Investment Committee. However, as the managing member of Keating Investments, Mr. Keating has sole control over the appointment and removal of the members of the Investment Committee.

1

Our investment adviser’s principals have extensive experience in taking companies public, advising micro- and small-cap companies on capital markets strategies, and developing investor relations programs. Our investment adviser has managed our portfolio company investment activity since we made our first investment in January 2010. Through our investment adviser’s experience in taking companies public, we believe the principals of our investment adviser possess valuable insights on the trends affecting the IPO market, the factors that contribute to the completion of a successful IPO in the current market, key IPO pricing drivers, investor sentiment, and industries or sectors in and out of favor. Our investment adviser is able to use this experience and insight as part of its disciplined approach to investment assessment and adjust valuation expectations and portfolio composition as IPO market trends are identified.

Governance

Our Board of Directors monitors and performs an oversight role with respect to our business and affairs, including with respect to investment practices and performance, compliance with regulatory requirements and the services, expenses and performance of our service providers. Among other things, our Board of Directors approves the appointment of our investment adviser and officers, reviews and monitors the services and activities performed by our investment adviser and officers, approves the engagement, and reviews the performance of, our independent registered public accounting firm, and provides overall risk management oversight. Pursuant to the requirements under the 1940 Act and to satisfy the Nasdaq listing standards, our Board of Directors is composed of a majority of non-interested, independent, directors.

Our Board of Directors has established the Audit Committee, the Valuation Committee and the Nominating Committee to assist the Board of Directors in fulfilling its oversight responsibilities. Each of these committees is composed solely of non-interested, or independent, directors. The Audit Committee’s responsibilities include overseeing our accounting and financial reporting processes, our systems of internal controls over financial reporting, and audits of our financial statements. The Valuation Committee’s responsibilities include reviewing preliminary portfolio company investment valuations from our investment adviser and making recommendations to our Board of Directors regarding the valuation of each investment in our portfolio. The Nominating Committee’s responsibilities include identifying qualified individuals to serve on our Board of Directors, and to select, or recommend that the Board of Directors select, the Board nominees.

Our Investment Objective and Strategy

Our investment objective is to maximize capital appreciation. We seek to accomplish our capital appreciation objective by making investments in the equity and equity-linked securities of later stage, typically venture capital-backed, pre-IPO companies. We focus on acquiring equity securities that are typically a portfolio company’s most senior preferred stock at the time of our investment or, in cases where we acquire shares of common stock, the portfolio company typically has only common stock outstanding. However, to a lesser extent, we may also invest in convertible debt securities, such as convertible bridge notes, issued by a portfolio company typically seeking to raise capital to fund their operations until an IPO, sale/merger or next equity financing event. These bridge notes are typically subordinated to the portfolio company’s senior debt. We generally intend to hold our convertible debt securities, which we refer to as equity-linked securities, for the purpose of conversion into equity at a future date. In accordance with our investment objective, we seek to invest in equity and equity-linked securities of principally U.S.-based, private companies with an equity value typically between $100 million and $1 billion. We refer to companies with an equity value of between $100 million and less than $250 million as “micro-cap companies” and companies with an equity value of between $250 million and $1 billion as “small-cap companies.” Since our initial investment in January 2010, we have historically focused on venture capital-backed technology companies.

We specialize in making pre-IPO investments in emerging growth companies that are committed to and capable of becoming public, which we refer to as “pre-IPO” companies. We provide investors with the ability to participate in a publicly traded, closed-end fund that allows our stockholders to share in the potential value accretion that we believe typically occurs once a company transforms from private to public status, or what we refer to as the private-to-public valuation arbitrage. Our shares are listed on Nasdaq under the ticker symbol “KIPO.” Our strategy is to evaluate and invest in companies prior to the valuation accretion that we believe occurs once private companies complete an initial public offering. We seek to capture this value accretion by investing primarily in private, micro-cap and small-cap companies that meet our core investment criteria: they (i) generate annual revenue in excess of $20 million on a trailing 12-month basis and have growth potential; (ii) are committed to, capable of, and will benefit from becoming public companies; and (iii) create the potential to achieve a targeted 2x return on our investment within our expected investment horizon of four years. We may also pursue investments with a shorter expected investment horizon, where we believe the portfolio company may complete an IPO sooner than our targeted two-year period from our initial investment, in which case our targeted return may be correspondingly reduced. Our investment strategy can be summarized as buy privately, sell publicly, capture the difference.

2

By design, our fund has been structured as a high risk/high return investment vehicle. While we have discretion in the investment of our capital, we seek long-term capital appreciation through investments principally in equity or equity-linked securities that we believe will maximize our total return. Although our preferred stock investments typically carry a dividend rate, in some cases with a payment preference over other classes of equity, we do not expect dividends (whether cumulative or non-cumulative) to be declared and paid on our preferred stock investments, or on our common stock investments, since our portfolio companies typically prefer to retain profits, if any, in their businesses. Interest accrued under our equity-linked securities, such as convertible bridge notes, is generally not payable until maturity and, accordingly, does not generate current cash payments to us, nor are they held for that purpose. Accordingly, our equity and equity-linked investments are not expected to generate current income (i.e., dividends or interest income), which makes us different from other business development companies that primarily make debt investments from which they receive current yield in the form of interest income.

Our primary source of investment return will be generated from net capital gains, if any, realized on the sale of our portfolio company investments, which typically will occur after a portfolio company completes an IPO and after expiration of a customary 180-day post-IPO lockup restriction or, to a lesser extent, is acquired. We intend to maximize our potential for capital appreciation by taking advantage of the private-to-public valuation arbitrage, or the premium, that we believe is generally associated with having a more liquid asset, such as a publicly traded security. Typically, we believe investors place a premium on liquidity, or having the ability to sell stock more quickly and efficiently through an established stock exchange than through private transactions. Specifically, we believe that an exchange listing, if obtained, should generally provide our portfolio companies with greater visibility, marketability and liquidity than they would otherwise be able to achieve without such a listing. As a result, we believe that public companies typically trade at higher valuations than private companies with similar financial attributes. By going public and listing on an exchange, we believe that our portfolio companies have the potential to receive the benefit of this liquidity premium. There can be no assurance that our portfolio companies will trade at these higher valuations once they are public and listed on an exchange.

We target our investments in portfolio companies that we believe can complete this value transformation within our targeted four-year holding period, compared to private equity and venture capital funds which we believe typically take seven to 10 years. As a result, we may have low or negative returns in our initial years with any potential valuation accretion typically occurring in later years as our portfolio companies potentially are able to complete their IPOs and become publicly traded. However, there can be no assurance that we will be able to achieve our targeted return on any individual portfolio company investment if and when it goes public, or on the portfolio as a whole.

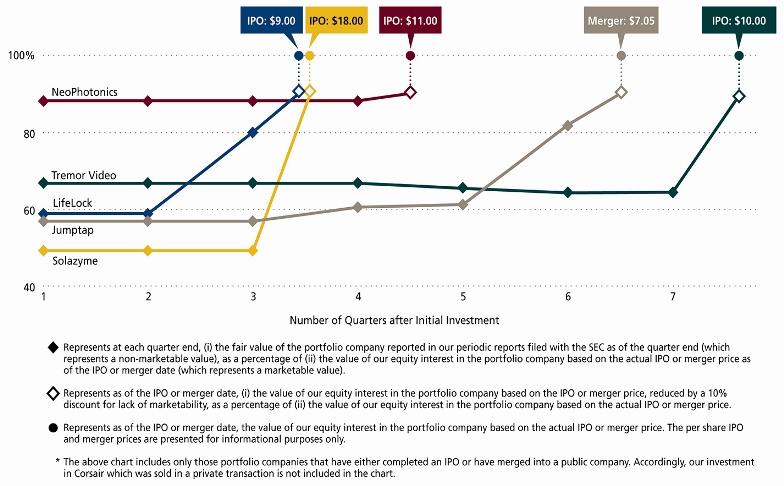

We continue to believe that public companies typically trade at higher valuations than private companies with similar financial attributes. The four portfolio companies that have completed IPOs (NeoPhotonics, Solazyme, LifeLock and Tremor Video) had unrealized returns at the time of their IPOs, based on their IPO price, of 1.8x, 2.0x, 1.7x and 1.5x our investment cost, respectively. However, the stock prices of each of these companies have changed since the IPO, and there is no assurance that we will be able to sell any of our portfolio company investments, following our lockup restrictions, at prices that will allow us to achieve our targeted 2x return on investment once the companies are publicly traded and assuming our targeted four-year investment horizon.

We have an IPO, event-driven strategy, and we attempt to generate returns by accepting the risks of owning illiquid securities of later stage private companies. We believe that investing in an issuer’s most senior equity securities and/or negotiating certain structural protections are ways to potentially mitigate the otherwise high risks associated with pre-IPO investing. However, the process of transforming from private to public ownership is subject to the uncertainties of the IPO process. If this process happened quickly and with certainty, we believe there would be less of an illiquidity discount available (and hence, less potential return) to us when we make our investments. Instead, the private-to-public transformation process takes time and is subject to market conditions, and we therefore incorporate a targeted four-year average holding period for each portfolio company into our strategy.

Because the equity and equity-linked securities of pre-IPO companies typically do not pay any current income, we may consider investments in qualified private and public companies that generate current yield in the form of interest income which can be used to offset some of our operating expenses. These investments typically will be in the form of debt instruments providing for the current payment of interest, which may be convertible into equity securities or have separate warrants exercisable for equity securities so that we have an opportunity to achieve long-term capital appreciation. To the extent that we make investments in public companies, we anticipate that the market capitalizations of these companies would typically be below $250 million and that we would be willing to generally accept a reduced level of potential capital appreciation in exchange for the payment of a current yield on our investments to offset some of our operating expenses. In addition to broadening our potential sources of return, we believe that the ability to generate current yield in the form of interest income on some of our investments may be attractive to our investors.

3

We believe that there are four critical factors that will drive the success of our pre-IPO investing strategy, differentiate us from other potential investors in later stage, venture-backed private companies, and potentially enable us to complete equity transactions in pre-IPO companies that we believe will meet our expected targeted return. First, we generally focus on companies with an equity value of typically between $100 million and $1 billion—companies we believe are better positioned to achieve our targeted return on our investment once the company is publicly traded. Second, we focus on prospective portfolio companies where we can purchase securities directly from an issuer or from a selling stockholder in a negotiated transaction and can obtain business and financial information on the portfolio company. Third, we focus on acquiring equity securities that are typically the issuer’s most senior preferred stock at the time of our investment or, in cases where we acquire shares of common stock, the issuer typically has only common stock outstanding. And lastly, we are focused on the acquisition of private securities at a valuation that creates the potential for our targeted return on our investment once the company is publicly traded. We believe that larger, highly-publicized, private companies may create the risk to a prospective investor of being either fully or, in certain cases, over-valued relative to publicly traded peers, which diminishes the opportunity for us to realize the potential value accretion that we believe exists when a private company completes an IPO.

Our portfolio companies are generally permitted to undertake subsequent financings in which they may issue equity securities or incur debt that ranks equally with, or senior to, the equity securities in which we invest. In such cases, debt securities may provide that the holders are entitled to receive payment of interest or principal before we are entitled to receive any distribution from the portfolio companies, and the holders of more senior classes of preferred stock would typically be entitled to receive full or partial payment in preference to any distribution to us.

We believe that investing in an issuer’s most senior equity securities and/or negotiating certain structural protections are ways to potentially mitigate the otherwise high risks associated with pre-IPO investing. We may seek to negotiate structural protections such as conversion rights which would result in our receiving shares of common stock at a discount to the IPO price upon conversion at the time of the IPO, or warrants that would result in our receiving additional shares for a nominal exercise price at the time of an IPO. In some circumstances, these structural protections will apply only if the IPO price is below stated levels. In some cases, our decision to pursue an investment opportunity will be dependent on obtaining some structural protections that are expected to enhance our ability to meet our targeted return on the investment. These structural protections are intended to provide some additional value protection in the event of an IPO. We view the potential value associated with these structural protections as an important component of our investment strategy. However, there can be no assurance that our investment adviser will succeed in negotiating structural protections for our future investments. Even if it succeeds in obtaining such protections, our ability to realize the potential value associated with these structural protections at the time of the IPO will depend on a number of factors including each portfolio company’s completion of an IPO, any adjustment to the special IPO conversion price that may be negotiated prior to or during the IPO process, the possible subsequent issuance of more senior securities that may impact the relative value of the structural protection, and fluctuations in the market price of each portfolio company’s common shares until such time as the common shares received upon conversion can be disposed of following the expiration of a customary 180-day post-IPO lockup period. Accordingly, the potential value associated with these structural protections would typically not be available unless each portfolio company completes an IPO. Further, even if an IPO is completed, the potential value associated with these structural protections would not be realized unless the market price of each portfolio company’s common shares equals or exceeds the IPO price at the time such shares are sold by us following the post-IPO lockup period.

See “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for additional information regarding the rights, preferences and limitations of the equity securities we hold in our private portfolio companies.

Investment Criteria

We have identified three core investment criteria that we believe are important in meeting our investment objective for pre-IPO companies. These core criteria provide the primary basis for making our investment decisions; however, we may not require each prospective portfolio company in which we choose to invest to meet all of these core criteria.

| ● |

High quality growth companies. We seek to invest primarily in micro-cap and small-cap companies that are already generating annual revenue in excess of $20 million on a trailing 12-month basis and which we believe have growth potential.

|

|

| ● |

Commitment to complete IPO. We seek to invest in public ready micro-cap and small-cap companies whose management teams are committed to, and capable of, becoming public companies, whose businesses we believe will benefit from status as public companies, and that we believe are capable of completing IPOs and obtaining exchange listings typically within two years after we complete our investments.

|

|

| ● |

Potential for return on investment. Because of the value differential which we believe exists between public and private companies as a result of the liquidity premium, or what we refer to as the private-to-public valuation arbitrage, as discussed above, we seek to make investments that create the potential to achieve a targeted 2x return on our investment once the company is publicly traded and within our expected investment horizon of four years. We may also pursue investments with a shorter expected investment horizon, where we believe the portfolio company may complete an IPO sooner than our targeted two-year period from our initial investment, in which case our targeted return may be correspondingly reduced.

|

4

We expect that the primary sources of our investment opportunities will be from our relationships with venture capital firms and investment banks.

Market Opportunity

We seek to invest in micro-cap and small-cap companies across a broad range of growth industries that we believe are being transformed by technological, economic and social forces. Since our initial investment in January 2010, we have historically focused on venture capital-backed technology companies.

We believe that an attractive market opportunity exists for us as a provider of pre-IPO financing to emerging growth companies that meet our investment criteria for the following reasons:

| ● | Companies staying private longer. The venture capital-backed companies that we typically target are staying private significantly longer than in the past. As a result, we believe there is a growing pipeline of more mature private companies that are currently able to satisfy investor demands for growth and prospects for near-term profitability. | |

| ● | Need for pre-IPO financing. As a result of the changing IPO market conditions over the last several years, we believe micro- and small-cap companies generally must demonstrate an ability to raise private capital prior to an IPO to be successful in the IPO process. We believe such pre-IPO financing evidences existing investors’ continuing commitment to the company, validates increased valuations to the extent new investors price the pre-IPO financing, and strengthens the company’s balance sheet as it prepares for the IPO process. | |

| ● | Favorable IPO market conditions. While capital markets volatility and the overall market environment may preclude our portfolio companies from completing an IPO and impede our exit from these investments, the U.S. IPO market in 2013 was the best year since 2000, when 406 IPOs were completed. In 2013, a total of 222 companies completed IPOs in U.S., compared to a total of 128 IPOs completed in 2012. The 222 IPOs completed in 2013 exceeded the 216 IPOs completed in 2004, the highest level of completed IPOs in the last 10 years. We believe there are three primary technical drivers that determine the overall number of completed IPOs: (i) volatility, (ii) recent IPO performance, and (iii) equity market trends. As of the end of 2013, we believe that each of the technical indicators were at favorable levels. | |

| ● | Non-controlling investment structure. We believe we can be a provider of choice for pre-IPO financing. Since we do not require board seats, observation rights, or other control provisions, we allow the current management and board to remain focused on executing the company’s business strategy. In addition to participating in financings led by other investors, we are able to act as a lead investor, in which case we would establish the price and other terms on our own behalf and on behalf of other investors. We believe that our willingness to lead an investment round may be attractive to certain existing venture capital investors, who may wish to avoid conflicts of interest presented by their board seats or other control rights. |

Our Investment Process

Investment Sourcing

We believe our investment adviser has developed a disciplined approach to source qualified pre-IPO investing opportunities from a highly developed network of investors, advisers, and private companies that are deeply involved in later stage venture capital and IPO transactions. We believe a very distinct “IPO ecosystem” exists, which is composed primarily of top tier venture capital firms, select investment banking firms, and a select group of law firms and accounting firms. Our investment adviser has developed relationships with many of these leading venture capital, investment banking, legal and accounting firms that it believes are important participants in this ecosystem.

Through these relationships, our investment adviser is able to gain valuable insights on the current IPO market and access to pre-IPO investment opportunities that currently, or may in the near-term, meet our investment criteria. We believe this approach will allow us to source the most attractive companies committed to going public. We typically do not pursue larger, well-publicized private company investments through anonymous bidding on the trading platforms of private secondary marketplaces. Instead, our investing strategy relies on the expertise of our investment adviser’s deal origination team to source opportunities that we can validate meet our investment criteria through our disciplined evaluation of company-provided business and financial information and access to management.

5

Based on the reputation we believe we have developed and our current pipeline of investment opportunities, we expect that the primary source of our future portfolio company investment opportunities will be from our relationships with venture capital firms and investment banks.

| ● |

Venture capital firms. We believe that a majority of our investment opportunities will come from venture capital firms with existing portfolio companies seeking later stage, pre-IPO financing. In addition to participating in financings led by other investors, we are able to act as a lead investor, in which case we would establish the price and other terms on our own behalf and on behalf of other investors.

|

|

| ● |

Investment banks. We also expect to source our investment opportunities from investment banks that are focused on emerging growth companies that meet our investment criteria. We have developed, and expect to continue building, relationships with the large, “bulge bracket,” investment banking firms and middle market firms that are recognized as leaders in these sectors.

|

We also have in the past and may in the future source investment opportunities from our direct outreach to private companies. We have implemented a proactive marketing program to communicate with our investment adviser’s established referral network and with companies that meet our investment criteria. We also maintain and continually update a database of emerging growth companies, which are typically venture capital-backed, that we believe currently satisfy, or will satisfy within the next year, our investment criteria. Our database has been compiled from opportunities identified by our referral network, from publicly available information, and from acquired sources.

Because of our relationships with participants in the later stage venture capital and IPO ecosystems, we believe we have access to a significant number of venture capital-backed companies which are committed to and capable of completing an IPO in the near- or long-term. We regularly monitor the progress of these private company opportunities in order to position us to participate or lead in their future private financing round before an IPO.

Portfolio Company Review and Approval

We use a disciplined approach to our initial investment assessment which relies primarily on the detailed financial and business information we receive about the company and our access to and discussions with management, both prior to and after our investment. Our investment adviser uses this company information to prepare our initial valuation analysis, leveraging its experience in taking companies public and its insights on current trends affecting the IPO market. We also use our initial discussions with our portfolio company management teams to discuss their commitment to completing an IPO and to determine which are best positioned to meet or exceed their performance targets following their IPOs and correspondingly achieve a market equity value comparable to their publicly traded peers.

Once we identify those private companies that we believe meet our minimum revenue threshold and have indicated a commitment to go public within our targeted time frame, we utilize an investment review and approval process focused on the following factors:

| ● |

Qualification. We obtain information from the company’s management and conduct a preliminary evaluation of the opportunity with a primary focus on understanding the business, historical and projected financial information, industry, competition and valuation to ascertain whether we believe the prospective portfolio company will be able to satisfy our targeted return on investment if and when the company becomes public. The results of this preliminary evaluation are presented to our investment adviser’s Investment Committee, and typically a decision is made whether to pursue the opportunity further based on the relative attractiveness of the opportunity, the expected investment horizon and our assessment of the potential return on our investment, and our core investment criteria, compared to other opportunities currently in our deal pipeline. The Investment Committee typically selects those portfolio company investment opportunities that meet our investment criteria and present the greatest potential for achieving our target return on investment.

|

|

| ● |

Analysis. Once the Investment Committee selects a portfolio company investment opportunity for further analysis, we will conduct research on the company’s prospects and industry, participate in additional discussions with the company’s management and existing investors, and prepare an internal investment memorandum which discusses our evaluation findings and recommendations, together with an internal valuation analysis outlining our acceptable valuation ranges for an investment. As part of our analysis, we typically have discussions with the company’s management and advisers, and we usually request access to the company’s major stockholders. These discussions generally are centered on a review of the company’s financial history and projections to understand key supporting assumptions, verification of the company’s commitment to go public and the timing thereof, and the primary considerations, metrics and milestone achievements being used by the company to justify its valuation. At this stage, we prepare an in-depth valuation analysis focused primarily on comparable private transactions, market multiples of public companies that we believe are most comparable, and a discounted cash flow analysis. Based on our comprehensive valuation assessment, the Investment Committee typically makes a decision whether to proceed with an investment and, if we are the lead investor, the terms and conditions that we will propose for further negotiation. Each new portfolio company investment that we make requires the unanimous approval of our investment adviser’s three-person Investment Committee.

|

6

| ● |

Terms. We believe that investing in an issuer’s most senior equity securities or negotiating investment terms that are expected to provide an enhanced return upon an IPO event is one important way to mitigate the otherwise high risks associated with pre-IPO investing. Examples of such structural protections include conversion rights which would result in our receiving shares of common stock at a discount to the IPO price upon conversion at the time of the IPO, or warrants that would result in our receiving additional shares for a nominal exercise price at the time of an IPO. In some circumstances, these structural protections will apply only if the IPO price is below stated levels. In some cases, our decision to pursue an investment opportunity will be dependent on obtaining some structural protections that are expected to enhance our ability to meet our targeted return on the investment.

|

|

| ● |

Due Diligence and Closing. Prior to closing an investment, we conduct further due diligence with a focus on verifying or validating the primary considerations used by our investment adviser’s Investment Committee in approving the investment, contacting where possible key suppliers, customers or industry sources, and verifying the company’s capitalization table and equity structure. The consummation of each investment will be subject to the satisfactory completion of our due diligence investigation, our confirmation and acceptance of the investment pricing and structure, and our review and acceptance of definitive agreements.

|

Our investment adviser’s principals have extensive experience negotiating, structuring and closing these specialized equity purchase transactions with issuers and selling stockholders. As part of its due diligence process, our investment adviser analyzes the complex capital structures which venture capital-backed, pre-IPO companies typically possess including multiple classes of common and preferred equity securities with differing rights with respect to voting, dividends, redemptions, liquidation, and conversion rights. Our investment adviser’s principals also have experience in negotiating matters relating to registration rights, restrictions of transfer, and other stockholder rights and restrictions.

Portfolio Company Monitoring and Managerial Assistance

We typically do not seek to take a control position in our investments through ownership, board seats, observation rights or other control features. Accordingly, we will typically not be in a position to control the management, operation and strategic decision-making of the companies we invest in. As a result, a portfolio company may make business decisions with which we disagree, and the stockholders and management of such a portfolio company may take risks or otherwise act in ways that are adverse to our interests. In addition, other stockholders, such as venture capital sponsors that have substantial investments in our portfolio companies, may have interests that differ from that of the portfolio company or its minority stockholders, which may lead them to take actions that could materially and adversely affect the value of our investment in the portfolio company. Due to the lack of liquidity for the equity investments that we will typically hold in our portfolio companies, we may not be able to dispose of our investments in the event that we disagree with the actions of a portfolio company or its substantial stockholders, including their decisions to delay their IPOs, and may therefore suffer a decrease in the value of our investments.

Nevertheless, as part of our portfolio company investment, we typically require information rights that give us access to the company’s quarterly and annual financial statements as well as the company’s annual budget. We also attempt to have dialogue, on at least a quarterly basis, with our private portfolio company management teams to review the company’s business prospects, financial results, and exit strategy plans. We monitor the financial trends of each portfolio company to assess the performance of individual companies as well as to evaluate overall portfolio quality and risk. We believe this is an important competitive advantage for us relative to those funds that do not have or require the same access to ongoing financial information that we insist upon.

We also use our ongoing discussions with our portfolio company management teams to monitor their continued commitment to completing an IPO and, when requested, to provide our insights on the current IPO market and what we believe are the key differentiators for successful IPOs. We also offer significant managerial assistance to our portfolio companies. We expect that this managerial assistance will likely involve consulting and advice on the going public process and public capital markets, including introducing certain portfolio company management teams to capital markets advisory firms that we believe can assist these management teams in: (i) selecting and structuring underwriting syndicates, (ii) developing the portfolio company’s IPO marketing message and plan, (iii) engaging the research analyst community, (iv) developing the appropriate valuation and go-to-market price range and advising on proper transaction size, (v) monitoring the quality of the roadshow audience and maximizing marketing effectiveness, (vi) monitoring bookbuilding and developing strategies for optimal pricing, and (vii) developing an optimal stockholder base and aftermarket trading. As a business development company, we are required to offer such managerial assistance.

7

Portfolio Composition and Follow-on Investments

We currently expect to have a portfolio of approximately 20 companies, taking into account our current portfolio composition and our current capital base. Based on our current capital base, the targeted size of our investments in new portfolio companies will be approximately $3 million, but we may invest more or less than this amount depending on the circumstances. We do not expect our $3 million targeted investment size to increase unless we are able to raise additional capital. It is also possible our targeted investment size may decrease over time if we are unable to raise additional capital. If our targeted investment size decreases, the number and types of opportunities in which we may be allowed to participate are likely to decline, and we may be unable to invest in opportunities that otherwise meet our investment criteria. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Financial Condition, Liquidity and Capital Resources.”

We generally expect that most of our portfolio company investments will represent approximately 5% of our gross assets measured at the time of investment depending on the size of our asset base and our investable capital. However, based on our investment adviser’s assessment of each portfolio company’s relative quality, fundamentals and valuation, we may make opportunistic portfolio company investments that could represent up to 25% of our gross assets measured at the time of investment. An individual portfolio company investment may be smaller than our targeted size and weighting at the time of the initial investment due to factors such as the size of investment made available to us and our cash available for investment. We expect that the size of our individual portfolio company investments and their weighting in our overall portfolio will fluctuate over time based on a variety of factors including, but not limited to additional follow-on investments in existing portfolio companies, sales of our interests in portfolio companies, unrealized appreciation or depreciation, or an increased asset base as a result of the possible issuance of additional equity.

We may also consider making follow-on investments in an existing private portfolio company that is seeking to raise additional capital in subsequent private equity financing rounds. Existing portfolio companies may elect, or be required, to raise additional capital prior to pursuing an IPO for any number of reasons including: (i) to fund additional spending in marketing and/or research and development to develop their business, (ii) to fund working capital deficiencies due to weaker than expected revenue growth or higher than expected operating expenses, (iii) to fund business acquisitions or strategic joint ventures, and (iv) to increase cash reserves in advance of an anticipated IPO. In evaluating follow-on investment opportunities, we typically assess a number of additional factors beyond the three core investment criteria we use in making our initial investment decisions. These additional factors may include: (i) the portfolio company’s continued commitment to an IPO, (ii) the achievement of pre-IPO milestones since our initial investment, (iii) the size of our portfolio company investment relative to our overall portfolio, (iv) any industry trends affecting the portfolio company or other portfolio investments in similar industries, (v) the impact of a follow-on investment on our diversification requirements so we can continue to qualify as a RIC for tax purposes, and (vi) the possible adverse consequences to our existing investment if we elect not to make a follow-on investment, such as the forced conversion of our preferred stock into common stock at an unfavorable conversion rate and the corresponding loss of any liquidation preferences or other rights and privileges that may be applicable to the securities we currently hold. Although we have de-emphasized the energy and recycling sectors as areas of interest, we may continue to evaluate and make investments in existing energy and recycling portfolio companies based on the foregoing factors.

Targeted Holding Periods and Portfolio Company Exits

We generally expect that our portfolio companies will be able to complete an IPO, on average, within approximately two years after the closing of our initial investment. After a typical lockup restriction which prohibits us from selling our investment during a customary 180-day period following the IPO, we expect that, on average, the holding period for our portfolio company investments will be approximately four years, compared to private equity and venture capital funds which we believe typically take seven to 10 years. In the venture capital and private equity industries, it is common for a portfolio's return to undergo a so-called "J-curve" pattern. This means that when reflected on a graph, the portfolio’s return would appear in the shape of the letter "J," with low or negative returns in early years and possible investment gains occurring in later years as valuations increase. In the context of the “J-curve” return pattern, our write-downs reflect our unrealized depreciation which may not be reversed on some investments. However, we are unable to reflect the potential value we believe may be realized if or when our private companies progress to and complete an IPO or other exit. This J-curve return pattern results from write-downs of portfolio investments that appear to be unsuccessful, prior to any potential write-ups and realized gains for portfolio investments that may prove to be successful.

While we have only a few discrete events to measure a portfolio company’s progress to an IPO–a registration statement publicly on file with the SEC, the completion of an IPO, and the disposition of our investment–which we refer to as “lagging” indicators, we believe that a number of our portfolio companies continue to prepare for and make progress towards an IPO. Our assessment of a portfolio company’s IPO preparation and progress is based on information our investment adviser may obtain in its quarterly update calls with our portfolio company management teams with respect to certain pre-IPO indicators, or what we refer to as “leading” indicators. These leading indicators include: (i) adding new members of senior management (e.g., a CFO with public company experience), (ii) meeting with investment banking firms and conducting a “bakeoff” to select underwriters, (iii) testing the waters by meeting with prospective institutional IPO investors, (iv) determining (and then achieving) the key operating milestones that need to be met to increase the probability of a successful IPO, (v) holding an IPO “organizational meeting” to begin preparation for the IPO process, (vi) drafting the IPO registration statement, and, in certain cases, (vii) confidentially filing a registration statement with the SEC. Due to the confidential nature of our investment adviser’s discussions with management, we are precluded from discussing the presence or absence of these “leading” indicators with respect to specific portfolio companies. Based on our assessment of these “leading” indicators, we believe that many of our portfolio companies are making progress toward an IPO that is consistent with our targeted time frames and holding periods.

8

In the event our portfolio companies fail to complete an IPO within our targeted two-year time frame, we may need to make additional investments in these portfolio companies, along with other existing investors, to fund their operations. In some cases, if we elect not to fund our pro rata share of these additional investments, there may be adverse consequences including the forced conversion of our preferred stock into common stock at an unfavorable conversion rate and the corresponding loss of any liquidation preferences or other rights and privileges that may be applicable to the securities we currently hold.

Although we have a targeted four-year holding period, our public company ownership structure eliminates the pressure to sell a portfolio company investment if a portfolio company’s IPO or merger/sale is delayed. Accordingly, we believe that we can be a patient investor in our portfolio companies, allowing them flexibility to access the IPO market when the timing and pricing may be best for the company and us. In the event the IPO markets become unfavorable to a specific industry or the broader market, we can be flexible as our portfolio companies wait for a market recovery or seek alternative exit strategies. However, there may be situations where our portfolio companies will not perform as planned and thus be unable to go public under any circumstances. There may also be situations where a specific industry or sector will no longer be attractive to IPO investors.

In such cases, we will consider whether the portfolio company has already passed, or is likely to exceed, our targeted two-year IPO completion period. If we believe the portfolio company will not complete an IPO within this period, our investment adviser has the discretion to consider a number of alternative strategies including (i) pursuing a sale of our interests to an existing investor, (ii) attempting to influence the portfolio company’s management to pursue a strategic merger or sale, and (iii) identifying potential third party investors interested in purchasing all or a portion of our interest. Our ability to liquidate our investments under any of these strategies will be highly uncertain, although we expect to have a greater chance of success if our investments contain structural protections. Nonetheless, depending on the circumstances, even if we are successful in liquidating an investment under these alternatives, we may not achieve our targeted return and, as for any investment, we may experience a loss on our investment.

There also can be no assurances that any of our private portfolio companies will complete an IPO within our targeted two-year time frame, or at all. Even if these portfolio companies are able to complete an IPO, we may not be able to dispose of our interests in these publicly traded portfolio companies within our targeted four-year holding period or at prices that would allow us to achieve our targeted 2x return on our investment, or any return at all. In cases where we have reduced our targeted return due to a shorter expected investment horizon, there can be no assurance that our portfolio company will be able to complete an IPO, or that we will be able to dispose of our investment, in this shorter time frame at our targeted return. There can be no assurance that we will be able to achieve our targeted return on our portfolio company investments if, as and when they go public.

See “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Targeted Holding Periods and Portfolio Company Exits” for additional information on the holding periods of our portfolio companies and the IPO progress of private portfolio companies.

Source of Returns

Our primary source of investment return will be generated from net capital gains, if any, realized on the sale of our portfolio company investments, which typically will occur after a portfolio company completes an IPO or, to a lesser extent, is acquired. We are typically prohibited from exiting investments in our publicly traded portfolio companies following their IPO until the expiration of the customary 180-day lockup period. These agreements, which we are usually required to enter into as part of our investment, prohibit us and other significant existing investors from selling stock in the portfolio company or hedging such securities during the customary 180-day period following an IPO. We may sell these securities at our discretion at any time following the lockup period based on our investment adviser’s business judgment. However, we will have no ability to mitigate the high volatility that is a typical characteristic of IPO aftermarket trading and is driven by such factors as overall market conditions, the industry conditions for the particular sector in which the portfolio company operates, the portfolio company’s performance, the relative size of the public float, and the potential selling activities of other pre-IPO investors and possibly management.

9

For our portfolio company investments where the lockup period following the IPO has expired and the stock becomes freely tradable, we typically do not begin selling automatically upon expiration of the lockup period. We expect to sell our positions over a period of time, typically during the one-year period following the expiration of our lockup, although we may sell more rapidly or in one or more block transactions. Factors that we may consider include, but are not limited to, the following:

| ● |

The target price determined by our investment adviser based on its business judgment and what it believes to be the portfolio company’s intrinsic value.

|

|

| ● |

The application of public company multiples and our proprietary analysis to a variety of operating metrics for each portfolio company. The primary operating metrics that we typically consider are revenue and earnings before interest, taxes, depreciation and amortization (“EBITDA”).

|

|

| ● |

Other factors that may be adversely or favorably affecting a particular portfolio company’s stock price, including overall market conditions, industry cyclicality, or issues specific to the portfolio company.

|

See “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Net Realized Gains” for additional information on the realized gains and losses for our portfolio company dispositions.

Distributions

Quarterly Distribution Policy

On February 20, 2014, our Board of Directors adopted a quarterly distribution policy where we intend to pay regular quarterly distributions to our stockholders out of assets legally available for distribution. Under the quarterly distribution policy, our Board of Directors intends to pay regular quarterly distributions to our stockholders based on our estimated net capital gains (which are defined as our realized capital gains in excess of realized capital losses during the year, without regard to the long-term or short-term character of such gains or losses) for a given calendar year. Since our portfolio company investments typically do not generate current income (i.e., dividends or interest income), we do not expect the quarterly distributions to represent earnings from net investment income, which makes us different from other business development companies that primarily make debt investments and may pay dividends from their recurring interest income.

Under our quarterly distribution policy, we seek to maintain a consistent distribution level that may be paid in part or in full from net capital gains or a return of capital, or a combination thereof. If our actual net capital gains are less than the total amount of our regular quarterly distributions for the year, the difference will be distributed from our capital and will constitute a return of capital to our stockholders. Alternatively, if our actual net capital gains exceed the total amount of our regular quarterly distributions for a given year, our Board of Directors currently intends to adjust or make an additional distribution in December of each year so that our total distributions for any given year represent 100% of our actual net capital gains in that year. A return of capital is generally not taxable and, instead, reduces a stockholder's tax basis in his shares of Keating Capital. A return of capital does also not necessarily reflect our investment performance and generally does not reflect income earned. The tax character of a distribution is determined based upon our total net capital gains and distributions made with respect to a taxable year and, therefore, cannot be finally determined until after the close of the relevant taxable year.

Due to the uncertainty of our portfolio companies achieving a liquidity event through either an IPO or sale/merger and our ability to sell our positions at a gain following a liquidity event, we can give no assurance that we will be able to realize net capital gains during the year equal to the amount of our regular quarterly distributions. Furthermore, we can give no assurance that we will achieve our projected investment results that will allow us to pay a specified level of distributions, previously projected distributions for future periods, or year-to-year increases in distributions. Our ability to pay distributions will be based on our ability to invest our capital in securities of suitable portfolio companies in a timely manner, our portfolio companies achieving a liquidity event, and our ability to sell our publicly traded portfolio positions at a gain following a liquidity event. Accordingly, we can give no assurance that we will be able to realize any net capital gains from the sale of our portfolio company investments.

See “Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities – Distribution Policy” for additional information on our quarterly distribution policy.

Stock Distributions

On February 20, 2014, consistent with applicable tax rules, our Board of Directors determined that it intends to pay the regular quarterly distributions under our quarterly distribution policy in cash or our common stock at the election of stockholders, subject to a limitation that no more than 25% of the aggregate distribution will be paid in cash with the remainder paid in shares of our common stock. As a result of our stock distributions, you may be required to pay tax in excess of the cash portion of the dividend you receive.

10

Our Board believes there are a number of benefits from paying stock distributions and retaining cash for additional portfolio company investments, including the following: (i) that our increased cash resources would allow us to make investments in a greater number of portfolio companies at potentially larger investment amounts, (ii) that our increased capital base would have the effect of reducing our operating expenses as a percent of our net assets, and (iii) that a higher market capitalization and potentially greater liquidity may make our common stock more attractive to investors and help reduce or eliminate our stock price discount to net asset value over time. Based on our current stock price, we expect that stock distributions for the foreseeable future will be made at a price per share that is less than our net asset value per share, which will result in an immediate dilution of net asset value per share for all of our stockholders. We expect to continue to pay a portion of our distributions in shares of our common stock until such time as we have eliminated our stock price discount to net asset value and can successfully access the equity capital markets, or on an ongoing basis.

We intend to suspend our dividend reinvestment plan (“DRIP”) with respect to the entirety of any distribution which is paid in cash and shares of our common stock at the election of stockholders.

See “Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities – Distribution Policy” for additional information on our stock distributions and DRIP.

Capital Raising

As a business development company, we need the ability to raise additional capital for investment purposes on an ongoing basis. Accordingly, we expect to access the capital markets from time to time in the future to raise cash to fund additional investments. We intend to use the proceeds from these offerings to fund additional investments in portfolio companies consistent with our investment objective. However, we do not intend to raise additional equity capital in 2014 unless and until our stock price is at or above our net asset value per share. Nonetheless, we remain committed to distribute 100% of our net realized gains to our stockholders in accordance with the quarterly distribution policy adopted by our Board of Directions on February 20, 2014. Further, in an effort to preserve cash for additional portfolio company investments, we intend to pay our distributions in cash or in shares of our common stock at the election of stockholders, subject to a limitation that no more than 25% of the aggregate distribution will be paid in cash with the remainder paid in shares of our common stock. Capital for additional portfolio company investments will be provided from our available cash and the proceeds from our sale of existing portfolio company investments.

We may borrow additional funds to make investments, to the extent we determine that additional capital would allow us to take advantage of additional investment opportunities, if the market for debt financing presents attractively priced debt financing opportunities, or if our Board of Directors determines that leveraging our portfolio would be in our best interests and the best interests of our stockholders. While a debt offering could raise additional capital for investment, our investment adviser would need to carefully weigh the interest expense of the debt relative to the expected return on the invested capital. There is no assurance that any return from new investments funded by debt would cover the interest expense associated with the debt, which would adversely impact stockholders. Further, any interest expense associated with a debt offering would increase our operating expenses, which continue to be high compared to our peers because of our comparatively lower capital base. We do not currently anticipate issuing any preferred stock, although we could do so if our Board of Directors determines that it is in our best interest and the best interests of our stockholders. The costs associated with any borrowing or preferred stock issuance will be indirectly borne by our common stockholders.

Our ability to raise capital to fund additional investments provides a number of possible benefits to our stockholders, including the following:

Greater Number of and Larger Investment Opportunities May be Available with a Larger Capital Base. Our ability to raise additional capital through equity or debt offerings may help us generate additional deal flow. We believe additional capital could position us to attract greater deal flow and, at the same time, make larger investments in qualified portfolio companies and still satisfy the diversification requirements to maintain our status as a regulated investment company, or a RIC. Additionally, once our market capitalization reaches $100 million, we would achieve qualified institutional investor (“QIB”) status and, therefore, be eligible to participate in additional investment opportunities only available to QIBs.

Since we expect that most of our individual portfolio company investments will represent about 5% of our gross assets at the time of investment, an increase in our potential investment size (currently, about $3 million) would put us in a better position to act as lead investor and potentially negotiate structural protections that are expected to enhance our ability to meet our targeted return on our investments. We currently expect to have a portfolio of approximately 20 companies, each representing approximately 5% of our total assets. We believe an optimal investment size for each portfolio company is about $10 million.

11

Additional Capital May Reduce our Operating Expenses Per Share. Additional capital that increases our total assets may reduce our operating expenses per share by spreading our fixed expenses over a larger asset base. We are currently operating at sub-scale based on our existing capital base. We also believe our investment adviser, with eight employees currently responsible for managing our day-to-day operations including, without limitation, identifying, evaluating, negotiating, closing, monitoring and servicing our investments, has the appropriate resources and infrastructure in place to cost effectively scale our operations. While the base management fee payable to our investment adviser will increase if we increase our total assets, we must also bear certain fixed expenses, such as certain administrative, governance, regulatory and compliance costs that do not generally vary based on our size. Further, as a public company, we incur legal, accounting and other expenses, including costs associated with the periodic reporting requirements applicable to a company whose securities are registered under the Exchange Act, as well as additional corporate governance requirements, including requirements under the Sarbanes-Oxley Act, and other rules implemented by the SEC, that do not generally vary based on our total assets. On a per share basis, these fixed expenses will be reduced when supported by a larger capital base.

Higher Market Capitalization and Greater Liquidity May Make our Common Stock More Attractive to Investors. If we increase our capital through the issuance of additional shares, our market capitalization and the amount of our publicly tradable common stock would increase, which may afford all holders of our common stock greater liquidity. A larger market capitalization may make our stock more attractive to a larger number of investors who have limitations on the size of companies in which they invest. The investment criteria of certain institutional investors typically include a minimum market capitalization (generally, $100 million). Furthermore, a larger number of shares outstanding may increase the Company’s trading volume, which could decrease the volatility in the secondary market price of our common stock.

We currently have a limited number of institutional investors that hold shares of our common stock. A higher market capitalization and greater liquidity could create an opportunity for institutional investors to acquire a larger position in open market purchases of our common stock that would otherwise be unavailable. Our ability to attract institutional ownership in our common stock could also attract additional coverage from analysts who serve these institutional investors.

Our Ability to Raise Additional Capital May Help Reduce or Eliminate our Stock Price Discount to Net Asset Value. Shares of business development companies, like us, may trade at a market price that is less than the value of the net assets attributable to those shares. The possibility that the shares of our common stock will trade at a discount from net asset value, or at premiums that are unsustainable over the long term, are risks separate and distinct from the risk that our net asset value will decrease. Since we initially listed our common stock on Nasdaq on December 12, 2011, our shares of common stock have typically traded at a discount to our net assets attributable to those shares. Our Board of Directors has been focused on the current discount between our stock price and net asset value, and we have taken active steps to try to eliminate this discount to net asset value over time. These steps have included purchases of our shares under our stock repurchase program that are accretive to net asset value as well as an investor relations program and corporate branding campaign designed to increase awareness and visibility for our stock, which includes presenting Keating Capital to the investment community at various investor conferences and holding one-on-one meetings with institutional investors. On February 20, 2014, our Board of Directors also adopted a quarterly distribution policy which we believe may help reduce or eliminate our stock price discount to net asset value over time. We believe it is important for us to demonstrate to the investment community that we can raise additional capital to make additional investments. However, we have no intention of raising equity capital in 2014 unless and until our stock price is at or above our net asset value per share. If we are successful in raising additional capital, we believe we are positioned to deliver returns and the potential for future dividends to stockholders, which we believe, in turn, will help reduce or eliminate our current stock price discount to net asset value over time.

Competition

A large number of entities compete with us to make the types of equity investments that we target as part of our business strategy. We compete for such investments with a large number of venture capital funds, other equity and non-equity based investment funds, investment banks and other sources of financing, including traditional financial services companies such as commercial banks and specialty finance companies. Many of our competitors are substantially larger than us and have considerably greater financial, technical and marketing resources than we do. In addition, some of our competitors may require less information than we do and/or have higher risk tolerances or different risk assessments, which could allow them to consider a wider variety of investments and establish more relationships than we can. Furthermore, many of our competitors are not subject to the regulatory restrictions that the 1940 Act imposes on us as a business development company and, as a result, such companies may be more successful in completing their investments. There can be no assurance that the competitive pressures we face will not have a material adverse effect on our business, financial condition, and results of operations. Also, as a result of this competition, we may not be able to take advantage of attractive investment opportunities from time to time, and we can offer no assurance that we will be able to identify and make investments that are consistent with our investment objective.

12

Employees

Currently, we do not have any employees. The management of our investment portfolio is the responsibility of our investment adviser, Keating Investments, and its Investment Committee, which currently consists of Messrs. Keating, Rogers and Schweiger. Keating Investments’ Investment Committee must unanimously approve each new investment that we make. The members of the Investment Committee are not employed by us, and receive no compensation from us in connection with their portfolio management activities. However, Messrs. Keating, Rogers and Schweiger, through their financial interests in, or management positions with, Keating Investments, are entitled to a portion of any investment advisory fees paid by us to Keating Investments pursuant to the Investment Advisory and Administrative Services Agreement.

Investment Advisory and Administrative Services Agreement

Organization of the Investment Adviser

Keating Investments is a Delaware limited liability company that is registered as an investment adviser under the Advisers Act and serves as our investment adviser. Timothy J. Keating is the principal owner and managing member of Keating Investments. Messrs. Keating, Rogers and Schweiger are Keating Investments’ principals and the members of its Investment Committee. Messrs. Keating, Rogers and Schweiger manage the day-to-day operations of our investment adviser and provide the services to us under the Investment Advisory and Administrative Services Agreement. Keating Investments may in the future provide similar investment advisory services to other entities in addition to us. In the event that Keating Investments provides investment advisory services to other entities, we expect that our management and our independent directors will attempt to resolve conflicts in a fair and equitable manner taking into account factors that would include the investment objective, amount of assets under management and available for investment in new portfolio companies, portfolio composition and return expectations of us and any other entity, and other factors deemed appropriate. However, in the event such conflicts do arise in the future, Keating Investments intends to allocate investment opportunities in a fair and equitable manner consistent with our investment objective and strategies and with the fiduciary duties owed to us so that we are not disadvantaged in relation to any other affiliate or client of Keating Investments. The principal address of Keating Investments is 5251 DTC Parkway, Suite 1100, Greenwood Village, Colorado 80111.

Management and Advisory Services

Subject to the overall supervision of our Board of Directors, Keating Investments manages our day-to-day operations and provides us with investment advisory services. Under the terms of the Investment Advisory and Administrative Services Agreement, as currently in effect, Keating Investments:

| ● |

Determines the composition of our portfolio, the nature and timing of the changes to our portfolio and the manner of implementing such changes;

|

|

| ● |

Determines which securities we will purchase, retain or sell;

|

|

| ● |

Identifies, evaluates and negotiates the structure of the investments we make; and

|

|

| ● |

Closes, monitors and services the investments we make.

|