Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - WHITE FOX VENTURES, INC. | Financial_Report.xls |

| EX-32.1 - EXHIBIT 32.1 - WHITE FOX VENTURES, INC. | ex32_1.htm |

| EX-31.1 - EXHIBIT 31.1 - WHITE FOX VENTURES, INC. | ex31_1.htm |

| EX-32.2 - EXHIBIT 32.2 - WHITE FOX VENTURES, INC. | ex32_2.htm |

| EX-31.2 - EXHIBIT 31.2 - WHITE FOX VENTURES, INC. | ex31_2.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C.

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended: December 31, 2012

or

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from: _____________ to _____________

Commission file number 333-178624

DNA PRECIOUS METALS, INC.

(Exact name of registrant as specified in its charter)

| Nevada | 37-1640902 | |

| (State or other jurisdiction | (I.R.S. Employer | |

| of Incorporation) | Identification No.) |

| 9125 rue Pascal Gagnon, Suite 204 Saint Leonard, Quebec Canada HIP IZ4 |

| (Address of principal executive offices) |

Registrants telephone number including area code: (514) 852-2111

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| Common Stock, $0.001 par value | None | |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Acto Yesx No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act from their obligations under those Sections.

o Yesx No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

x Yes o No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

x Yes o No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

|

Large Accelerated Filer o

|

Non-accelerated Filer o

|

|

Accelerated Filer o

|

Smaller Reporting Company x|

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

o Yes x No

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant computed by reference to the price at which the common equity was last sold, or the average bid and asked price for such common equity, as of the last business day of the registrant's most recently completed second fiscal quarter was approximately $9,900,000 (Based on a sales price of $.25 per share, representing the sales price of the Company’s common stock on June 30, 2012.)

APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY

PROCEEDINGS DURING THE PRECEDING FIVE YEARS:

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

o Yes o No

APPLICABLE ONLY TO CORPPORATE ISSUERS

Indicate the number of shares outstanding of each of the issuer's classes of common stock as of the latest practicable date: 85, 528,000 of common stock, $0.001 par value as of March 1, 2013.

DOCUMENTS INCORPORATED BY REFERENCE

None.

2

Item 1. Business

DNA Precious Metals, Inc. (“we”, “us” “our” or the “Company”) is a Nevada corporation organized June 2, 2006. Our original name was Celtic Capital, Inc. On October 20, 2008, we changed our name to Entertainment Education Arts Inc. On May 12, 2010, we changed our name to DNA Precious Metals, Inc. to more accurately reflect our new business plan.

We are an exploration stage mining company whose business objective is to identify proven reserves of gold and silver, construct a mill, build out the Property’s infrastructure and place the mine into production. The Montauban Mining Project is located in the Montauban and Chavigny townships near Grondines-West in Portneauf County, Quebec, Canada (the “Property”). The Property does not contain any known ore reserves according to the definition of ore reserves under Industry Guide 7 promulgated by the Securities and Exchange Commission (“SEC”). Further work is required on the Property before a final determination as to the economic and legal feasibility of a mining venture can be made. There is no assurance that a commercially viable deposit will be proven through our exploration efforts. The funds expended on our properties may not be successful in leading to the delineation of ore reserves that meet the criteria established under SEC guidelines.

|

1.

|

MEASUREMENTS AND GLOSSARY

|

|

For ease of reference in

reviewing our business, we are providing you with conversion information and abbreviations. 1 acre |

= 0.4047 hectare

|

1 mile

|

= 1.6093 kilometers

|

|||||

|

1 foot

|

= 0.3048 meter

|

1 troy ounce

|

= 31.1035 grams

|

|||||

|

1 gram per metric ton

|

= 0.0292 troy ounce/

short ton

|

1 square mile

|

= 2.59 square kilometers

|

|||||

|

1 short ton (2000 pounds)

|

= 0.9072 ton

|

1 square kilometer

|

= 100 hectares

|

|||||

|

1 ton

|

= 1,000 kg or 2,204.6 lbs

|

1 kilogram

|

= 2.204 pounds or 32.151 troy oz

|

|||||

|

1 hectare

|

= 10,000 square meters

|

1 hectare

|

= 2.471 acres

|

|||||

3

The following abbreviations may be used herein:

|

Au

|

= gold

|

m2

|

= square meter

|

|||

|

G

|

= gram

|

m3

|

= cubic meter

|

|||

|

g/t

|

= grams per ton

|

Mg

|

= milligram

|

|||

|

Ha

|

= hectare

|

mg/m3

|

= milligrams per cubic meter

|

|||

|

Km

|

= kilometer

|

T or t

|

= ton

|

|||

|

Km2

|

= square kilometers

|

Oz

|

= troy ounce

|

|||

|

Kg

|

= kilogram

|

Ppb

|

= parts per billion

|

|||

|

M

|

= meter

|

Ma

|

= million years

|

GLOSSARY OF MINING TERMS

The following mining terms are used throughout this registration statement.

SEC Industry Guide 7 Definitions

|

exploration stage

|

An “exploration stage” prospect is one which is not in either the development or production stage.

|

|

development stage

|

A “development stage” project is one which is undergoing preparation of an established

Commercially mineable deposit for its extraction but which is not yet in production. This stage occurs after completion of a feasibility study.

|

|

mineralized

material

|

The term “mineralized material” refers to material that is not included in the reserve as it does not meet all of the criteria for adequate demonstration for economic or legal extraction.

|

|

probable reserve

|

The term “probable reserve” refers to reserves for which quantity and grade and/or quality are computed from information similar to that used for proven (measured) reserves, but the sites for inspection, sampling, and measurement are farther apart or are otherwise less adequately spaced. The degree of assurance, although lower than that for proven reserves, is high enough to assume continuity between points of observation.

|

4

|

production stage

|

A “production stage” project is actively engaged in the process of extraction and beneficiation of mineral reserves to produce a marketable metal or mineral product.

|

|

proven reserve

|

The term “proven reserve” refers to reserves for which (a) quantity is computed from dimensions revealed in outcrops, trenches, workings or drill holes; grade and/or quality are computed from the results of detailed sampling and (b) the sites for inspection, sampling and measurement are spaced so closely and the geologic character is so well defined that size, shape, depth and mineral content of reserves are well-established.

|

|

reserve

|

The term “reserve” refers to that part of a mineral deposit which could be economically and legally extracted or produced at the time of the reserve determination. Reserves must be supported by a feasibility study done to bankable standards that demonstrates the economic extraction. (“Bankable standards” implies that the confidence attached to the costs and achievements developed in the study is sufficient for the project to be eligible for external debt financing.) A reserve includes adjustments to the in-situ tons and grade to include diluting materials and allowances for losses that might occur when the material is mined.

|

Additional Definitions

|

alteration

|

Any change in the mineral composition of a rock brought about by physical or chemical means.

|

|

assay

|

A measure of the valuable mineral content.

|

|

dip

|

The angle that a structural surface, a bedding or fault plane, makes with the horizontal, measured perpendicular to the strike of the structure.

|

|

disseminated

|

Where minerals occur as scattered particles in the rock.

|

|

fault

|

A surface or zone of rock fracture along which there has been displacement.

|

|

feasibility study

|

A comprehensive study of a mineral deposit in which all geological, engineering, legal, operating, economic, social, environmental and other relevant factors are considered in sufficient detail that it could reasonably serve as the basis for a final decision by a financial institution to finance the development of the deposit for mineral production.

|

|

formation

|

A distinct layer of sedimentary rock of similar composition.

|

|

geochemistry

|

The study of the distribution and amounts of the chemical elements in minerals, ores, rocks, solids, water, and the atmosphere.

|

5

|

geophysics

|

The study of the mechanical, electrical and magnetic properties of the earth’s crust.

|

|

geophysical surveys

|

A survey method used primarily in the mining industry as an exploration tool, applying the methods of physics and engineering to the earth’s surface.

|

|

geotechnical

|

The study of ground stability.

|

|

grade

|

Quantity of metal per unit weight of host rock.

|

|

heap leach

|

A mineral processing method involving the crushing and stacking of an ore on an impermeable liner upon which solutions are sprayed to dissolve metals i.e. gold, copper etc.; the solutions containing the metals are then collected and treated to recover the metals.

|

|

host rock

|

The rock in which a mineral or an ore body may be contained.

|

|

in-situ

|

In its natural position.

|

|

lithology

|

The character of the rock described in terms of its structure, color, mineral composition, grain size and arrangement of tits component parts, all those visible features that in the aggregate impart individuality to the rock.

|

|

mapped or

geological mapping

|

The recording of geologic information including rock units and the occurrence of structural features, and mineral deposits on maps.

|

|

mineral

|

A naturally occurring inorganic crystalline material having a definite chemical composition.

|

|

mineralization

|

A natural accumulation or concentration in rocks or soil of one or more potentially economic minerals, also the process by which minerals are introduced or concentrated in a rock.

|

|

outcrop

|

That part of a geologic formation or structure that appears at the surface of the earth.

|

|

open pit or open

cut

|

Surface mining in which the ore is extracted from a pit or quarry, the geometry of the pit may vary with the characteristics of the ore body.

|

|

Ore

|

Mineral bearing rock that can be mined and treated profitably under current or immediately foreseeable economic conditions.

|

|

ore body

|

A mostly solid and fairly continuous mass of mineralization estimated to be economically mineable.

|

|

ore grade

|

The average weight of the valuable metal or mineral contained in a specific weight of ore i.e. grams per ton of ore.

|

|

oxide

|

Gold bearing ore which results from the oxidation of near surface sulfide ore.

|

6

|

preliminary

assessment

|

A study that includes an economic analysis of the potential viability of Mineral Resources taken at an early stage of the project prior to the completion of a preliminary feasibility study.

|

|

QA/QC

|

Quality Assurance/Quality Control is the process of controlling and assuring data quality for assays and other exploration and mining data.

|

|

quartz

|

A mineral composed of silicon dioxide, SiO2 (silica).

|

|

rock

|

Indurated naturally occurring mineral matter of various compositions.

|

|

sampling analytical

variance/precision

|

An estimate of the total error induced by sampling, sample preparation and analysis.

|

|

sediment

|

Particles transported by water, wind or ice.

|

|

sedimentary rock

|

Rock formed at the earth’s surface from solid particles, whether mineral or organic, which have been moved from their position of origin and re-deposited.

|

|

strike

|

The direction or trend that a structural surface, e.g. a bedding or fault plane, takes as it intersects the horizontal.

|

|

strip

|

To remove overburden in order to expose ore.

|

|

tailings

|

The residue from an ore crushing plant.

|

THE PROPERTY

The Montauban Property was acquired from Company 9215-8062 Quebec Inc. in exchange for the issuance of 5,000,000 shares of our common stock. The previous claim owner, Rocmec Mining Inc., exchanged its ten claims to Forage Magma Inc. for drilling equipments it needed at the time. Soon thereafter, Forage Magma Inc. sold those claims to 9215-8062 Quebec Inc. The ten claims were registered in the Quebec Government files directly from Forage Magma to 9215-8062 Quebec Inc.

No royalty payments are due in connection with the acquisition of the mining claims. We have paid the administrative fees with respect to the mining claims in Quebec through 2012. Thereafter, we will be required to pay every two years an administrative fee of $452 for all of the mining claims.

We are also required to allocate resources to each of the claims. The Quebec Ministry of Resources requires us to incur $19,750 in expenses directly related to the development of our mining claims.

7

We currently have a credit of approximately $76,800 which we can allocate amongst the ten mining claims. The credit is attributable to work that we have already completed on several of the mining claims

MINING HISTORY

The Montauban Tailings under study known as the “recent tailings” were produced by Anacon Lead Mines Ltd. between 1948 and 1955 and are situated within one kilometer northwest of the village. Reported production from this period amounts to over 87 M lbs of zinc, 34 M lbs of lead, close to 17,000 ounces of gold and over 2.6 M ounces of silver, extracted from a total of 1,375, 371 tons of ore processed.

GEOLOGY

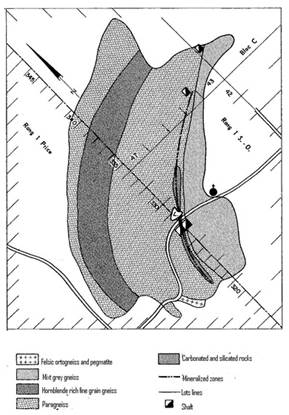

Regional geology is mostly comprised of three main rock groups: the basement crust, the supracrustal rocks and the intrusive rocks which were respectively identified as the Mekinac Group, the Montauban Group and the La Bostonnais Complex. The Montauban Deposit is a three-kilometer long mineralized formation with a geology that is fairly complex being located within an extensively folded sequence of amphibolite facies rocks that are sandwiched between intrusions of granodioritic to gabbroic composition. In the mine area, these metamorphic rocks strike roughly North-South and dip ±60° to the East and consist of migmatitic biotite gneiss, amphibolite, quartzofeldspathic biotite gneiss and quartzite.

DRILLING SUMMARY

A systematical sampling program was developed to provide an accurate and homogeneous grid of data to estimate the Montauban Tailings potential. A 24 holes percussion drilling campaign was performed totaling 143.1 meters. This percussion drilling campaign was completing a previous 25 holes drilled earlier. A total of 49 holes totaling 302.3 meters of drilling were completed. No proven or indicated reserves were identified.

PROPERTY DESCRIPTION AND LOCATION

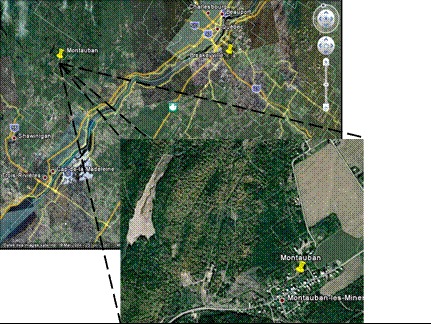

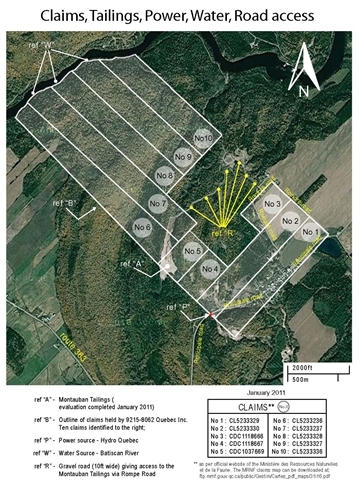

The Montauban Property is composed of 10 mining claims totaling 340.36 hectares located in the Montauban-les-Mines sector of the Notre-Dame-de-Montauban municipality, in the Montauban Township, Portneuf County, Province of Quebec. The property is located 120 km east of Quebec City and 80 km north of Trois-Rivières. The Montauban Tailings are located one kilometer west of Montauban-les-Mines with multiple land accesses. Manpower, water and electric power are easily available within the very same distance.

8

Figure I: Montauban Property Location Map

Pertinent data concerning the claims are presented in table I, these coming from the Quebec Government GESTIM website.

Table I: List of Claims

|

Claim #

|

Range

|

Lot

|

Area

|

Excess

Work |

|

1037669

|

1

|

42

|

12.55

|

$48,862.78

|

|

1118666

|

1

|

41

|

11.49

|

$0

|

|

1118667

|

1

|

41

|

12.32

|

$1,624.78

|

|

5233236

|

1

|

47

|

46.40

|

$23,900.91

|

|

5233237

|

1

|

46

|

48.80

|

$4,409.14

|

|

5233327

|

1

|

44

|

44.20

|

$0

|

|

5233328

|

1

|

45

|

43.30

|

$0

|

|

5233329

|

1

|

39

|

40.50

|

$0

|

|

5233330

|

1

|

40

|

40.50

|

$0

|

|

5233336

|

1

|

43

|

40.30

|

$0

|

|

Total

|

340.36

|

9

Figure II: Claim Reference Map

The Montauban Tailings are actually under the Government responsibility since the site was declared orphan. There are no environmental liabilities as such. However, the Company will have to obtain the necessary permits from the Authorities to realize any further field work having an impact on the environment, especially if remobilization of tailings is considered, as these are considered by the Authorities as toxic wastes.

ACCESS, CLIMATE, LOCAL INFRASTRUCTURES AND PHYSIOGRAPHY

The Montauban Municipality is accessible by route 363 from highway 40 linking Quebec City (120 km to the east) and Trois-Rivières (80 km to the southeast). Access to railway is also available less than 10 km to the northeast in Notre-Dame-des-Anges. The Montauban Tailings are located one kilometer west of Montauban-les-Mines with multiple land accesses.

From 1971 to 2000, Environment Canada Statistics reports daily average temperature of 18,8 °C in July and -14,2 °C for January. The extreme minimum temperature registered was of -45 °C (February 23, 1972) and the extreme maximum temperature reached 36,7 °C (August 1, 1975). The snow cover spreads from November to April, February being the month with the most important snow accumulation. The average yearly precipitation is 1138,8 mm, including rainfall (878,7 mm) and snowfall (260,2 mm). This data was collected at the Lac aux Sables station about 10 km to the northwest of Montauban.

10

Manpower, water and electric power are easily available within one-kilometer distance from the Montauban-les-Mines village. The region is rural, most of the farmers growing potatoes and corn. The equipment and personnel specialized in quarries are available within a 30 km radius from the Montauban Tailings in the surrounding municipalities (Notre-Dame-de-Montauban, St-Ubalde, Lac-aux-Sables, St-Casimir, St-Marc-des-Carrières and Ste-Thècle).

The area’s physiography is characterized by argilitic and sandy plateaus forming the foothills of the Laurentides. The Montauban Property is limited to the North West by the Batiscan River which is the main effluent in the area draining most of the Property towards the south to the St-Lawrence River. The topography consists of numerous small hills reaching an altitude of up to 220 m above the sea level from the valleys standing in average at 160 m elevation.

HISTORY

The mining history of the area began in 1910 with the discovery of the Pb-Zn Montauban Deposit by Mr. Elzéar Gauthier. The exploitation of the numerous base metal zones of the Montauban Mine were performed over the years by a series of successive owners: Mr. E. Gauthier (1910-1911), Mr. P. Tétreault (1911-1914), the Weedon Mining Company (1914-1915), the Zinc Company Ltd. (1915-1921), the Tetreault Estate (1921-1924), the British Metal Corporation (1925-1929), the Tetreault Estate (1929-1937), the Siscoe Metals Ltd./War Time Metals Corporation (1942-1944), Anacon Lead Mines Ltd. (1948-1956) and the Ghysleau Mining Corporation Ltd. (1957-1966). In 1966, most of the installations were decommissioned, and the mining rights on the Anacon Property expired in 1972.

In 1974, Muscocho Exploration Ltd. acquired the mining rights and performed over the following years numerous exploration programs leading to the definition of sufficient gold resources to start commercial gold production in 1983. The mine did produce gold and silver up to 1990 when production was stopped due to ore exhaustion. Over its production period, Muscocho processed 813,632 tonnes of ore producing 92,553 oz of gold and 323,376 oz of silver.

In 1981, a systematic sampling program was performed by Boville Resources Ltd. to evaluate the quantity and quality of mine tailings at Montauban-les-Mines, those tailings being the first period of exploitation between 1914 and 1944 located south of the access road to Montauban-les-Mines (Depatie (1982).

In 1999, Mirabel Resources Inc. performed a soil survey, a mag-VLF survey, some trenching and 18 diamond drill holes mostly on the south zone. In 2000-2001, more trenching and 17 short diamond drill holes were done on the north zone.

In 2003, Mirabel Resources Inc. performed limited gravimetrical tests on 4 samples equally split between core samples from former diamond drill holes and tailing samples of the “old tailings” taken close by the access road to Montauban-les-Mines (Bernard (2003)). The results showed that the gravimetric method gave good recoveries for the tailing samples but nothing significant for the rock samples.

The Montauban Tailings under study are known as the “recent tailings” located close to one kilometer north west of the village itself and that were produced from 1948 to 1955 by Anacon Lead Mines Ltd. Reported production from this period amounts to over 87 M lbs of zinc, 34 M lbs of lead, close to 17,000 ounces of gold and over 2.6 M ounces of silver, extracted from a total of 1,375,371 tons of ore processed.

11

GEOLOGY

Regional geology consists of three main rock groups: the basement crust, the supracrustal rocks and the intrusive rocks which were respectively identified as the Mekinac Group, the Montauban Group and the La Bostonnais Complex

The Montauban Group is composed of Helikian supracrustal rocks. Those are various gneiss, quartzites, amphibolites, metabasalts and calcosilicated rocks reaching less than 2 kilometers in thickness. The Montauban deposit is located in the upper part of this unit.

The Montauban Group is bordered to the East by the La Bostonnais Complex, an intrusive rocks complex formed of basic, tonalitic and felsic igneous rocks. To the West, the Montauban Group is in contact with the Mekinac Group mostly composed of charnockitic migmatites.

The Montauban Deposit is a three-kilometer long mineralized formation with a geology that is fairly complex being located within an extensively folded sequence of amphibolite facies rocks that are sandwiched between intrusions of granodioritic to gabbroic composition. In the mine area, these metamorphic rocks strike roughly North-South and dip ±60° to the East and consist of migmatitic biotite gneiss, amphibolite, quartzofeldspathic biotite gneiss and quartzite.

Locally, the Montauban mineralization is contained within a thin complex package of biotite gneiss, nodular sillimanite gneiss, cordierite-antophyllite gneiss, calc-silicate rocks and rocks as meta-exhalites (tourmalinite and, along strike iron formation and carbonate rocks).

The Montauban deposit is distributed within numerous different zones along the strike length of the mineralization, from South to North we have the zones: South, Tétreault, A, C, North and Montauban. All zones are zinc bearing with the exception of the South and North zones which are gold bearing.

12

MINERALIZATION

The base metal mineralization found in Montauban is massive to semi-massive sulphides, coarsely grained and mostly composed of sphalerite, galena, pyrrhotite, pyrite and chalcopyrite with minor quantities of cubanite, tetrahedrite and molybdenite.

The gold bearing mineralization is marginal and consists of disseminated pyrrhotite, galena, sphalerite and chalcopyrite with a large range of minor sulphides, sulphosalts and native minerals.

MONTAUBAN TAILINGS

The Montauban Tailings are covering a total area of 53,093 m² and amounts to a total volume of 250,750 m³. Since this volume is composed of tailings and that the water table is located within most of the blocks derived from each hole, the specific gravity of the material had to be evaluated to estimate the tonnage that is present on site. The estimation of the specific gravity was performed on the last drilling campaign 24 holes since no recovery evaluation is available from the first drilling campaign. Recovery of tailings in the sampling process averaged about 76% from the last percussion drilling campaign. Recoveries were ranging from 40 to 100 %, the lowest values being associated to the high water content of the deepest samples, the water table being at a depth of about 4,6 m (15 ft) within the pile of tailings. The averaged recovery was in the order of 81 % (68 samples) for the upper portion of the tailings and it dropped to below 64 % (27 samples) for the deeper portion (below the water table). The specific gravity is then estimated to be 1, 71 g/cm³.

13

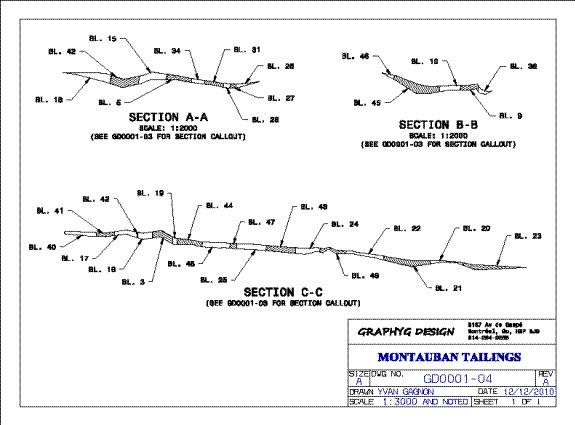

Montauban Tailings Hole Location Plan

The above graph shows the typical sections of the Montauban Tailings where it is clear that the drainage is towards the North (to the right on section C-C). It is also clear that the thickness is variable but not so thick compared to the value that should be reached if the whole production was to be still onsite. About 1.2 million tons were produced in the past; such a tonnage should be averaging over 13 meters in the Tailings pile. It is clear on site that an important fraction of the tailings was washed away through drainage.

14

Montauban Tailings Typical Sections

Figure X: Montauban Tailings View Looking South

15

A total of 49 blocks were defined from the two previous percussion drilling campaigns. The drilling pattern is essentially regular with a hole each and every 30 meter on average. The block volumes were calculated with the help of the computer modeling program that defined one polygon for each and every hole drilled. The perimeter of the tailings was mapped with the help of a GPS device, this perimeter is the limit where the surface meshing of the holes’ collars meets the meshing of the bottom of the holes. The block size is fairly regular averaging 8,740 tons, the smallest block being # 26 at 1 342 tons and the biggest one being # 21 at 24 334 tons.

To these metals one should add the mica content of the Montauban Tailings, the mica being mostly composed of the phlogopite type with some muscovite and minor amounts of biotite. The mica content is estimated to be at least 10 % of the total volume. The mica is an industrial mineral that is valued according to the market conditions.

DRILLING RESULTS

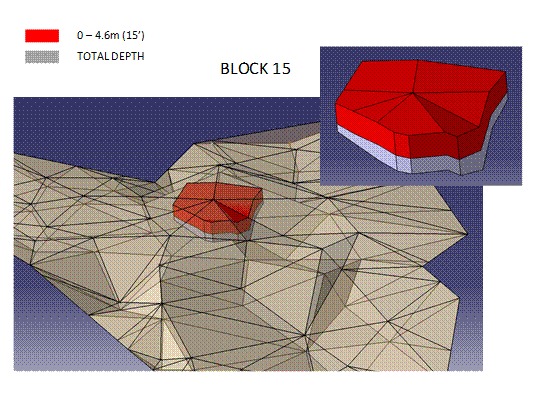

The distribution of metals within the tailings is not homogeneous. It was demonstrated with the 49 holes drilled on the Montauban Tailings that recoveries dropped from 81 to less than 64 % below the 4,6 m (15 ft) horizon, which is more or less the location of the water table within the Tailings. The impact is seen on metal content when gold is 67 % richer over this horizon, silver is up 73 %, Copper also up 63 %, and the winner being lead with a jump of 149 %. The only one being evenly distributed is the zinc.

Example of Block 15 Showing Richer Upper Portion of Montauban Tailings

16

MILL CONSTRUCTION

We are constructing a mill to process mining residues. Our focus will be to produce gold and silver concentrate in addition to a saleable mica product. By extracting mica and producing the gold and silver concentrate, we will reduce the sulphide content of the tailings thus lowering the environmental cost for the closure at the end of the operation.

Presently, there are no similar mills in the area surrounding our mining claims. The on-site mill facility is planned to be constructed initially with gravity separation equipment, consisting of spiral classifiers and Nelson concentrators in addition to other equipment. Test work to date has indicated that this configuration will effectively segregate the mica and produce a gold/silver concentrate. There is a risk that the plant as built will not effectively separate the values as designed and planned. There is also a risk that the process being used is not ideal or optimal and that a different process may enhance or increase recovery of values. We intend to continue testing to improve the recuperation and extraction process. We have incorporated flexibility into our mill building design to allow for alternative/additional precious metal extraction processes to be installed. Initial testing results indicate that recovery of mica, gold and silver is possible but economic feasibility has not been shown and there is the associated risk that the operation as planned will not be profitable either with respect to our own mining operations or refining tailings or other mining concentrates from other mining companies in close proximity to our operations.

Before gold and silver can be extracted from the tailings, the mica content must be removed. If we are able to produce a mica concentrate which corresponds to market standards, we will have an additional revenue stream with little incremental costs. There is a risk that there is no market for the mica product to be produced.

To keep expenditures as low as possible, we have used refurbished milling equipment when possible. Our larger expenses include the mill building, electrical distribution, pumps, pipe valves, spiral classifiers, Nelson concentrators, table separator, trommel, loader and a conveyor.

Special attention will be devoted to the potential of the surrounding area to produce more tailings, whether from the S-W extension of the actual deposit onto the adjoining property, or from the zone North of the access road (former exploitation), or again from the old tailings (on the Excel adjoining property). All these tailings will have to be neutralized in order to permanently close the site. The actual gross problematic is in the hands of the Government and it is highly probable that they would be interested in ruling it out with the least amount of expenses as possible. It should also be noted that the Government files are reporting that more than 2 million tones of tailings are located in numerous piles in the surroundings of the Montauban village).

We anticipate that the mill will be able to process 1,000 tons per day. By constructing our own mill we will be able to reduce transportation costs.

With this exception, the actual presence of tailings in Montauban, no environmental problems are reported for the Montauban Tailings (known as the recent tailings).

17

PROPERTY DEVELOPMENT

The Company has completed construction of all access roads to and from the new milling facility. The hydro power source to the milling facility totaling 1.3 kilometers has been completed. The main power line consists of 2,500 amperes total output power and has been brought inside the newly erected 16,000 sq/ft steel structure building.

We have hired 9216-9499 Quebec Inc. as the electrical contractor. In addition to the main power source line already completed, 9216-9499 Quebec Inc. has been hired to do all the electrical work inside the milling facility including the wiring of the entire building, installation of heating and air conditioning system, lighting supply, ventilation system installation and complete electrical set-up of all milling equipment. The contract price is $285,000CAD (approximately $279,300 U.S. based on an exchange ratio of $.98). The Contractor, 9216-9499 Quebec Inc., has received a retainer of $100,000 CAD ($98,000 U.S.) and has begun the preliminary work. The work is expected to be completed in the summer of 2013. At this time all the milling processing equipment is expected to be in place and ready for preliminary processing of the mining residues.

DNA hired Construction and Demolition Deschesnes was hired to complete the civil construction of the steel structure building. The total contract price is $470,000CAD (approximately $460,600 U.S.) of which $370,000 CAD (approximately $362,600 U.S.) has been paid to date. The remaining balance will be paid on completion of the work. The pouring of the cement interior floor of the steel structure building remains to be completed. This work has been temporarily delayed due to cold weather.

Also included in the price of the civil construction of the steel structure building was various equipment including lighting fixtures, 2,000 amperes electrical breaker system, heating system, air conditioning system, and back-up generator. This equipment will be installed by the electrical contractor and is included in the contract price.

DNA has purchased the Humphey Spirals necessary for the production of the mica product. In total, 128 spirals were purchased and is presently stored in three 40 foot containers. This equipment is necessary as a first step of the recovery of the precious metals as it will remove all the mica material through gravity separation. The successful extraction process of the gold and silver from the mining residues can only be obtained after the mica is removed from the mining residues.

POSSIBLE FURTHER ACTIVIITIES

We will also define further the local potential of other sources such as additional tailings or underground resources underneath the Property or close-by in the Montauban area.

SUBSEQUENT EVENTS

On March 4, 2013 754 2542 Canada Inc. executed an agreement with the Company whereby 754 2542 Canada agreed to accept 2.5 million shares of common stock in satisfaction of all amounts due and owing 754 2542 Canada Inc. pursuant to the promissory note executed between the parties and dated May 13, 2011. Despite the dilution that shareholders will experience as a result of this transaction, Management believes that the exchange of debt for equity is in the best interests of the Company as it will preserve much needed working capital.

18

Item 1A. Risk Factors

We are an exploration stage company and our business plan is unproven. We have generated no revenues from our operations and incurred operating losses since our inception.

We are an exploration stage company, our business plan is unproven, and we cannot assure you that we will ever achieve profitability or, if we achieve profitability, that it will be sustainable. We are subject to all of the risks inherent in a new business. We have not generated any revenues to date. At December 31, 2012 we had current assets in the amount of $603,360 and current liabilities totaling $310,784 and Long term liabilities totaled $502,550. We had a working capital surplus of $292,586 and deficits accumulated in the exploration stage of $1,773,047 as of December 31, 2012. We have a working capital surplus at December 31, 2011 of $458,516. We may require additional financing to become fully operational. We currently have no commitment for additional funding. There can be no assurance that we will be able to secure additional funding, or if available, available on terms acceptable to us.

We have no proven reserves.

The Property does not have known reserves of commercial gold or silver. Our long-term success will be related to the cost and success our exploration and mining programs. Mining for gold and silver and base metals is a highly speculative business, involving a high degree of risk. Few properties which are explored are ultimately developed into producing mines. There is no assurance that our exploration program will result in any discoveries of commercial quantities of gold or silver. There is also no assurance that, even if commercial quantities of gold or silver are discovered, a mine can be brought into commercial production. Production/discovery of gold and silver is dependent upon a number of factors, not the least of which is the technical skill of the exploration personnel involved. The commercial viability of a mine is also dependent upon a number of factors, many of which are beyond our control, such as the worldwide economy, the price of gold and silver, government regulations, including regulations relating to royalties, allowable production and environmental protection.

During our operations unexpected events may occur, including labor unrest, changes in government regulations, fires, floods, or earthquakes. It is not always possible to fully insure against such risks and we may decide not to take out insurance against such risks as a result of high premiums or for other reasons. Should such liabilities arise, they may impede our exploration activities, raise costs and otherwise reduce the commercial viability of the Property.

We may not identify proven reserves and our estimates may be inaccurate.

There is no certainty that any expenditures made in our exploration program will result in discoveries of commercially recoverable quantities of gold, silver or any base metal. Most exploration projects do not result in the discovery of commercially extractable deposits of gold or silver and no assurance can be given that any particular level of recovery will in fact be realized or that any identified leasehold interest will ever qualify as a commercially developed. Estimates of mineralization, reserves, deposits and production costs can also be affected by such factors as environmental regulations and requirements, weather, environmental factors, unforeseen technical difficulties, unusual or unexpected geological formations and work interruptions. Material changes in estimated reserves, exploration and mining costs may affect the economic viability of any project.

19

We will be required to locate mineral reserves for our long-term success.

Mines have limited lives based on proven and probable mineral reserves that are depleted in the course of production. To ensure continued viability we must offset depleted reserves by replacing and expanding our mineral reserves, through further exploration at the Property and/or the acquisition of new properties. Even if additional reserves are discovered, the process from exploration to production can take many years, during which the economic feasibility of production may change. Therefore, our ability to maintain or increase annual production of gold and other base or precious metals once mining activities commence, if at all, will be dependent almost entirely on our ability to bring new mines into production.

Mining is inherently dangerous and subject to conditions or events beyond our control, which could have a material adverse effect on our business.

Mining involves various types of risks and hazards, including:

|

•

|

environmental hazards;

|

|

|

•

|

power outages;

|

|

|

•

|

metallurgical and other processing problems;

|

|

|

•

|

unusual or unexpected geological formations;

|

|

|

•

|

flooding, fire, explosions, cave-ins, landslides and rock-bursts;

|

|

|

•

|

inability to obtain suitable or adequate machinery, equipment, or labor;

|

|

|

•

|

metals losses; and

|

|

|

•

|

periodic interruptions due to inclement or hazardous weather conditions.

|

These risks could result in damage to, or destruction of, mineral properties, production facilities or other properties, personal injury, environmental damage, delays in mining, increased production costs, monetary losses and possible legal liability.

Exploration for economic deposits of gold and silver is speculative.

Our business is very speculative since there is generally no way to recover any of the funds expended on exploration unless the existence of commercially exploitable reserves are established and the Company can exploit those reserves by either commencing mining operations, selling or leasing its interest in the property, or entering into a joint venture with a larger company that can further develop the property. Unless we can establish and exploit reserves before our funds are exhausted, we will have to discontinue operations.

Changes in the market price of gold, silver and other metals, which in the past has fluctuated widely, will affect the profitability of our operations and financial condition.

Our profitability and long-term viability depend, in large part, upon the market price of gold and other metals and minerals produced from our mineral properties. The market price of gold and other metals is volatile and is impacted by numerous factors beyond our control, including:

|

•

|

expectations with respect to the rate of inflation;

|

|

|

•

|

the relative strength of the U.S. dollar and certain other currencies;

|

|

|

•

|

interest rates;

|

|

•

|

global or regional political, financial, or economic conditions;

|

|

|

•

|

supply and demand for jewelry and industrial products containing metals; and

|

|

|

•

|

sales by central banks and other holders, speculators and producers of gold and other metals in response to any of the above factors.

|

20

A decrease in the market price of gold and other metals could affect the commercial viability of our Montauban Property and our anticipated development and production assumptions. Lower gold prices could also adversely affect our ability to finance future development at the Montauban Property, all of which would have a material adverse effect on our financial condition and results of operations. There can be no assurance that the market price of gold and other metals will remain at current levels or that such prices will improve.

Our estimates of resources are subject to uncertainty.

Estimates of resources are subject to considerable uncertainty. Such estimates are arrived at using standard acceptable geological techniques, and are based on the interpretations of geological data obtained from drill holes and other sampling techniques. Engineers use drilling results to derive estimates of cash operating costs based on anticipated tonnage and grades of ore to be mined and processed, the predicted configuration of the ore bodies, expected recovery rates of metal from ore, comparable facility and operating costs and other factors. Actual cash operating costs and economic returns on projects may differ significantly from the original estimates, primarily due to fluctuations in the current prices of metal commodities extracted from the deposits, changes in fuel costs, labor rates, changes in permit requirements, and unforeseen variations in the characteristics of the ore body. Due to the presence of these factors, there is no assurance that any geological reports will accurately reflect actual quantities of gold or silver that can be economically processed and mined by us.

The mineralization estimates are based on interpretation and assumptions and may yield less mineral production, if any, under actual conditions than is currently estimated.

We have relied on independent geologists to conduct drilling samples on the Property. When making determinations whether to continue any project, we must rely upon such estimated calculations as to the mineral reserves and grades of mineralization on the Property. Until ore is actually mined and processed, mineral reserves and grades of mineralization must be considered as estimates only.

These estimates are imprecise and depend upon geological interpretation and statistical inferences drawn from drilling and sampling analysis, which may prove to be unreliable. We cannot assure you that:

|

•

|

these estimates will be accurate;

|

|

|

•

|

reserve or other mineralization estimates will be accurate; or

|

|

|

•

|

this mineralization can be mined or processed profitably.

|

Any material changes in mineral reserve estimates and grades of mineralization may affect the economic viability of placing a property into production and a property’s return on capital. Because we have not started mining operations at the Property and have not commenced actual production, mineralization estimates may require adjustments or downward revisions based upon further drilling and/or actual production experience.

21

In addition, the grade of ore ultimately mined, if any, may differ from that indicated by our testing results to date. There can be no assurance that minerals recovered in small scale tests will be duplicated in large scale tests under on-site conditions or in production scale. Declines in market prices for gold and silver may render portions of our mineralization, reserve estimates uneconomic and result in reduced reported mineralization or adversely affect the commercial viability of the Property. Any material reductions in estimates of mineralization, or of our ability to extract this mineralization, could have a material adverse effect on our results of operations or financial condition.

Our exploration activities at the Montauban Property may not be successful, which could lead us to abandon our plans to develop the property and our investments in exploration.

Our long-term success depends on our ability to identify proven reserves and mine the Property and any other properties we may acquire, if any. Exploration activities are highly speculative in nature, which involves many risks and is frequently non-productive. These risks include unusual or unexpected geologic formations, and the inability to obtain suitable or adequate machinery, equipment or labor. The success of our exploration program is determined in part by the following factors:

|

•

|

the identification of potential gold mineralization based on surficial analysis;

|

|

|

•

|

availability of government-granted exploration permits;

|

|

|

•

|

the quality of our management and our geological and technical expertise; and

|

|

|

•

|

the capital available for exploration.

|

Substantial expenditures are required to establish proven and probable reserves through drilling and analysis, to develop metallurgical processes to extract metal, and to develop the mining and processing facilities and infrastructure at the Property. Whether a mineral deposit will be commercially viable depends on a number of factors, which include, without limitation, the particular attributes of the deposit, such as size, grade and proximity to infrastructure; metal prices, which fluctuate widely; and government regulations, including, without limitation, regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting of minerals and environmental protection. We may invest significant capital and resources in exploration activities and abandon such investments if we are unable to identify commercially exploitable mineral reserves. We cannot assure you that we will discover mineralized resources in sufficient quantities on the Property to commence commercial development.

Actual capital costs, operating costs, production and economic returns may differ significantly from those we have anticipated and there is no assurance that our development activities will result in profitable mining operations.

We plan to estimate operating and capital costs for the Property based on information available to us and that we believe to be accurate. However, costs for labor, regulatory compliance, energy, mine and plant equipment and materials needed for mine development and construction may fluctuate significantly. In light of these factors, actual costs related to our proposed mine development and construction may exceed any estimates we may make. We do not have an operating history upon which we can base estimates of future operating costs related to the Property. We intend to rely upon our analysis of the future economic feasibility of the project and any estimates that may be contained therein. Studies derive estimates of cash operating costs based upon, among other things:

22

|

●

|

anticipated tonnage, grades and metallurgical characteristics of the ore to be mined and processed; | |

|

●

|

anticipated recovery rates of gold and other metals from the ore; | |

|

●

|

cash operating costs of comparable facilities and equipment; and

|

|

|

●

|

anticipated climatic conditions.

|

Capital and operating costs, production and economic returns, and other estimates may differ significantly from actual costs, and there can be no assurance that our actual capital and operating costs will not be higher than anticipated or disclosed.

In addition, any calculations of cash costs and cash cost per ounce may differ from similarly titled measures of other companies and are not intended to be an indicator of projected operating profit.

There can be no assurance that we will be successful in establishing mining operations or profitably exploiting mineral deposits.

We are subject to all of the risks associated with establishing new mining operations and business enterprises including:

|

•

|

the timing and cost, which can be considerable, of the construction of mining

and processing facilities;

|

|

|

•

|

the ability to find sufficient gold reserves to support a mining operation;

|

|

|

•

|

the availability and costs of skilled labor and mining equipment;

|

|

|

•

|

the availability and cost of appropriate smelting and/or refining arrangements;

|

|

|

•

|

compliance with environmental and other governmental approval and permit requirements;

|

|

|

•

|

the availability of funds to finance construction and development activities;

|

|

|

•

|

potential opposition from non-governmental organizations, environmental groups, local groups or local inhabitants which may delay or prevent development activities; and

|

|

|

•

|

potential increases in construction and operating costs due to changes in the cost of fuel, power, materials, supplies, and other costs.

|

It is common in new mining operations to experience unexpected problems and delays during construction, development and mine start-up; delays in the commencement of mineral production often occur. Accordingly, we cannot assure you that our activities will result in profitable mining operations or that we will successfully establish mining operations or profitably extract gold or silver at the Property.

23

Historical production at the Property may not be indicative of the potential for future development.

We currently have no commercial production at the Property and have never recorded any revenues from gold or silver production. You should not rely on the fact that there were historical mining operations at the Property as an indication that we will ever have future successful commercial operations at the Property. We expect to continue to incur losses unless and until such time, if ever, as the Property enters into commercial production and generates sufficient revenues to fund our continuing operations. The development of new mining operations requires the commitment of substantial resources for operating expenses and capital expenditures, which may increase in subsequent years as needed consultants, personnel and equipment associated with advancing exploration, development and commercial production are added. The amount and timing of expenditures will depend on the progress of ongoing exploration and development, the results of consultants’ analysis and recommendations, the rate at which operating losses are incurred, the execution of any joint venture agreements with strategic partners and other factors, many of which are beyond our control.

We have no history as a company engaged in the mining business.

We have no history of earnings or cash flow from mining activities. If we identify proven reserves and are able to proceed to production, commercial viability will be affected by factors that are beyond our control such as the particular attributes of the deposit, the fluctuation in the prices of gold and silver, the cost of construction and operating a mining operation, the availability of economic sources for energy, government regulations including regulations relating to prices, royalties, restrictions on production, quotas on exploration as well as the costs of protection of the environment.

We face many operating hazards.

The development and operation of a mining property involves many risks, which even a combination of experience, knowledge and careful evaluation may not be able to overcome. These risks include, among other things, ground fall, flooding, environmental hazards and the discharge of toxic chemicals, explosions and other accidents. Such occurrences may result in work stoppages, delays in production, increased production costs, damage to or destruction of mines and other producing facilities, injury or loss of life, damage to property, environmental damage and possible legal liability for such damages.

A shortage of critical equipment, supplies and resources could adversely affect our operations.

We are dependent on equipment, supplies and resources to carry out our mining operations, including input commodities, drilling equipment and skilled labor. A shortage in the market for any of these factors could cause unanticipated cost increases and delays in delivery times, which could in turn adversely impact production schedules and costs.

Operations at the Property will require a significant amount of water. Successful mining and processing will require careful control of project water usage and efficient reclamation of project solutions in the process.

Current global financial conditions have made access to financing more difficult.

Since the fall of 2008 there has been severe deterioration in global credit and equity markets. This has resulted in the need for government intervention in major banks, financial institutions and insurers, and has also led to greater volatility, increased credit losses and tighter credit conditions. These unprecedented disruptions in the credit and financial markets have had a significant adverse impact on a number of financial institutions and have limited access to capital and credit for many companies. These disruptions could, among other things, make it more difficult for us to obtain, or increase our cost of obtaining, capital and financing for our operations.

24

We do not insure against all risks to which we may be subject in our planned operations.

Any insurance that we secure will in all likelihood not cover all of the potential risks associated with a mining company’s operations, and we may be unable to maintain insurance to cover these risks at economically feasible premiums. Insurance coverage may not be available or may not be adequate to cover any resulting liability. Moreover, we expect that insurance against certain hazards as a result of exploration and production may be prohibitively expensive to obtain for a company of our size and financial means.

We might also become subject to liability for pollution or other hazards which may not be insured against or which we may elect not to insure against because of premium costs or other reasons. Insurance against certain environmental risks, including potential liability for pollution or other hazards as a result of the disposal of waste products occurring from production, is not generally available to us or to other companies within the mining industry.

Losses from events that are not covered by our insurance policies may cause us to incur significant costs that could negatively affect our financial condition and ability to fund our activities on the Property. A significant loss could force us to terminate our operations.

Drilling operations are hazardous, raise environmental concerns and raise insurance risks.

We intend to conduct our business in a way that safeguards public health and the environment and in compliance with applicable laws and regulations. Environmental hazards may exist on properties in which we hold an interest which are unknown to us and may have been caused by prior owners. Changes to drilling and mining laws and regulations could require additional capital expenditures and increase operating and/or reclamation costs. Although we are unable to predict what additional legislation, if any, might be proposed or enacted, additional regulatory requirements could render certain operations uneconomic.

Local infrastructure may impact our exploration activities and results of operations.

Our activities depend, to one degree or another, on adequate infrastructure. Reliable roads, bridges and power and water supplies are important determinants that affect capital and operating costs. Unusual or infrequent weather phenomenon, sabotage or government or other interference in the maintenance of such infrastructure could adversely affect our activities.

Compliance with SEC reporting requirements can be costly.

We do not have any employees to segregate responsibilities and may be unable to afford increasing our staff or engaging outside consultants or professionals to overcome our lack of employees. During the course of our operations, we may identify other deficiencies that we may not be able to remedy in time to satisfy the requirements imposed by the Sarbanes-Oxley Act for compliance with that Section 404. If we fail to achieve and maintain the adequacy of our internal controls, we may not be able to ensure that we can conclude on an ongoing basis that we have effective internal controls over financial reporting in accordance with Section 404 of the Sarbanes-Oxley Act. Moreover, effective internal controls, particularly those related to revenue recognition, are necessary for us to produce reliable financial reports and are important to help prevent financial fraud. If we cannot provide reliable financial reports or prevent fraud, our business and operating results could be harmed, investors could lose confidence in our reported financial information.

25

We are subject to significant governmental regulations.

The Property is located in Quebec, Canada and is subject to extensive federal, provincial, and local laws and regulations governing various matters, including:

|

|

•

|

environmental protection;

|

|

•

|

management and use of toxic substances and explosives;

|

|

|

•

|

management of natural resources;

|

|

|

•

|

labor standards and occupational health and safety, including mine safety; and

|

|

|

•

|

historic and cultural preservation.

|

Noncompliance may result in civil or criminal fines or penalties or enforcement actions, including orders issued by regulatory or judicial authorities enjoining or curtailing operations or requiring corrective measures, installation of additional equipment or remedial actions, any of which could result in us incurring significant expenditures. We may also be required to compensate private parties suffering loss or damage by reason of a breach of such laws, regulations or permitting requirements. It is also possible that future laws and regulations will be more stringent which could cause additional expense, capital expenditures, restrictions on our operations and delays in the development of the Property.

Our activities are subject to environmental laws and regulations that may increase our costs of doing business and restrict our operations.

All of our exploration and potential development and production activities are in the province of Quebec, Canada and are subject to regulation by governmental agencies under various environmental laws. These laws address, among other things, emissions into the air, discharges into water, management of waste, management of hazardous substances, protection of natural resources, antiquities and endangered species and reclamation of lands disturbed by mining operations.

Additionally, our operations will result in emissions of greenhouse gases, which may be subject to increased regulation in the future. In general, environmental legislation is evolving and the trend has been towards stricter standards and enforcement, increased fines and penalties for non-compliance, more stringent environmental assessments of proposed projects and increasing responsibility for companies and their officers, directors and employees. Compliance with environmental laws and regulations requires significant capital outlays, and future changes in these laws and regulations may cause material changes or delays in our financial position, operations and future activities. More stringent regulation may cause us to re-evaluate our activities.

26

Land reclamation requirements for the Property may be burdensome.

Land reclamation requirements are generally imposed on mineral exploration companies (as well as companies with mining operations) in order to minimize long term effects of land disturbance.

Reclamation may include requirements to:

|

•

|

control dispersion of potentially deleterious effluents; and

|

|

|

•

|

reasonably re-establish pre-disturbance land forms and vegetation.

|

In order to carry out reclamation obligations we will have to allocate a portion of our financial resources that might otherwise be spent on further exploration and development programs. Unanticipated reclamation work will adversely impact our operations.

We may not be able to comply with permitting requirements.

We have obtained required permitting to commence production activities. Maintaining the permits may require us to comply with more stringent government regulation or new regulatory controls may be instituted which will require us to implement more stringent controls and procedures over our production activities. There can be no assurance that we will be able to comply with more stringent government regulations or that additional costs will be required to remain compliant. This may result in production delays and impact our budgeted resources.

We may experience difficulty attracting and retaining qualified management.

We are dependent on the services of our executive officers. We will have to hire other highly skilled and experienced consultants. Due to our relatively small size, the loss of these persons or our inability to attract and retain highly skilled employees may have a material adverse effect on our business or future operations. We do not maintain key-man life insurance on any of our officers or directors.

We compete with larger, better capitalized competitors in the mining industry.

The mining industry is intensely competitive in all of its phases, including financing, technical resources, personnel and property acquisition. It requires significant capital, technical resources, personnel and operational experience to effectively compete in the mining industry. Larger companies with significant resources have an advantage over us. Competition for resources at all levels is very intense, particularly affecting the availability of manpower, drill rigs, mining equipment and production equipment. As a result, we may be unable to maintain or acquire financing, personnel or technical resources.

There are differences in U.S. and Canadian practices for reporting reserves and resources.

Since our operations are in Canada, resource estimates disseminated outside the United States are not directly comparable to those made in filings subject to SEC reporting and disclosure requirements. These practices are different from the practices used to report reserve and resource estimates in reports and other materials filed with the SEC. It is Canadian practice to report measured, indicated and inferred resources, which are generally not permitted in filings with the SEC. In the United States, mineralization may not be classified as a “reserve” unless the determination has been made that the mineralization could be economically and legally produced or extracted at the time the reserve determination is made. United States investors are cautioned not to assume that all or any part of measured or indicated resources will ever be converted into reserves. Further, “inferred resources” have a great amount of uncertainty as to their existence and as to whether they can be mined legally or economically.

27

Our directors and officers may have conflicts of interest as a result of their relationships with other companies.

Our directors and officers may serve as officers or directors for other companies engaged in natural resource exploration and development. The directors and officers owe us a fiduciary obligation. We have not yet established a policy to deal with potential conflicts of interest.

Legislation, including the Sarbanes-Oxley Act of 2002, may make it difficult for us to retain or attract officers and directors.

We may be unable to attract and retain qualified officers, directors and members of board committees required to provide for our effective management as a result of rules and regulations which govern publicly-held companies. The Sarbanes-Oxley Act has resulted in a series of rules and regulations that increase responsibilities and liabilities of directors and executive officers. We are a small company with a limited operating history and no revenues. This may influence the decisions of potential candidates we may recruit as directors or officers. The perceived increased personal risk associated with these recent changes may deter qualified individuals from accepting these roles.

Risks Related To Our Securities

As an “emerging growth company” under the JOBS Act, we are permitted to rely on exemptions from certain disclosure requirements.

We qualify as an “emerging growth company” under the JOBS Act. As a result, we are permitted to, and intend to, rely on exemptions from certain disclosure requirements. For so long as we are an emerging growth company, we will not be required to:

Reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act;

|

●

|

Comply with all requirements that may be adopted by the Public Accounting Oversight Board regarding mandatory audit firm rotation or a supplement to the auditor’s report providing additional information about the audit and financial statements; | |

|

●

|

Submit certain execute compensation matters to shareholder advisory votes, such as “say-on-pay” and “say on frequency;” | |

|

●

|

Disclose certain executive compensation related items such as the correlation between executive compensation and performance. |

In addition, Section 107 of the JOBS Act also provides that an emerging growth company can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards. In other words, an emerging growth company can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We have elected to take advantage of the benefits of this extended transition period. Our financial statements may therefore not be comparable to those of companies that comply with such new or revised accounting standards.

We will remain an “emerging growth company” for up to five years, or until the earliest of (i) the last day of the first fiscal year in which our total annual gross revenues exceed $1 billion, (ii) the date that we become a “large accelerated filer” as defined in Rule 12b-2 under the Securities Exchange Act of 1934, which would occur if the market value of our ordinary shares that is held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter or (iii) the date on which we have issued more than $1 billion in non-convertible debt during the preceding three year period.

28

Our financial statements may not be comparable to those of companies that comply with new or revised accounting standards.

We have elected to take advantage of the benefits of the extended transition period that Section 107 of the JOBS Act provides an emerging growth company, as provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards. Our financial statements may therefore not be comparable to those of companies that comply with such new or revised accounting standards.

Our status as an “emerging growth company” under the JOBS Act OF 2012 may make it more difficult to raise capital when we need to do it.

Because of the exemptions from various reporting requirements provided to us as an “emerging growth company” and because we will have an extended transition period for complying with new or revised financial accounting standards, we may be less attractive to investors and it may be difficult for us to raise additional capital as and when we need it. Investors may be unable to compare our business with other companies in our industry if they believe that our financial accounting is not as transparent as other companies in our industry. If we are unable to raise additional capital as and when we need it, our financial condition and results of operations may be materially and adversely affected.

We will incur increased costs and demands upon management as a result of complying with the laws and regulations that affect public companies, which could materially adversely affect our results of operations, financial condition, business and prospects.

As a public company and particularly after we cease to be an “emerging growth company,” we will incur significant legal, accounting and other expenses that we did not incur as a private company, including costs associated with public company reporting and corporate governance requirements. These requirements include compliance with Section 404 and other provisions of the Sarbanes-Oxley Act of 2002, or the Sarbanes-Oxley Act, as well as rules implemented by the SEC and NASDAQ. In addition, our management team will also have to adapt to the requirements of being a public company. We expect that compliance with these rules and regulations will substantially increase our legal and financial compliance costs and will make some activities more time-consuming and costly.

The increased costs associated with operating as a public company will decrease our net income or increase our net loss, and may require us to reduce costs in other areas of our business or increase the prices of our products or services. Additionally, if these requirements divert our management’s attention from other business concerns, they could have a material adverse effect on our results of operations, financial condition, business and prospects.

However, for as long as we remain an “emerging growth company” as defined in the JOBS Act, we may take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies” including not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and shareholder approval of any golden parachute payments not previously approved. We may take advantage of these reporting exemptions until we are no longer an “emerging growth company.”

29

We will not be required to comply with certain provisions of the Sarbanes-Oxley Act for as long as we remain an “emerging growth company.”

Our independent registered public accounting firm is not required to formally attest to the effectiveness of our internal control over financial reporting until the later of the year following our first annual report required to be filed with the SEC, or the date we are no longer an “emerging growth company.” At such time, our independent registered public accounting firm may issue a report that is adverse in the event it is not satisfied with the level at which our controls are documented, designed or operating.

Reduced disclosure requirements applicable to emerging growth companies may make our common stock less attractive to investors.

As an “emerging growth company,” we may take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies” including not being required to comply with the auditor attestation requirements of section 404 of the Sarbanes-Oxley Act, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and shareholder approval of any golden parachute payments not previously approved. We cannot predict if investors will find our common stock less attractive because we may rely on these exemptions. If some investors find our common stock less attractive as a result, there may be a less active trading market for our common stock and our stock price may be more volatile.

In the event that your investment in our shares is for the purpose of deriving dividend income or in expectation of an increase in market price of our shares from the declaration and payment of dividends, your investment will be compromised because we do not intend to pay dividends.

We have never paid a dividend to our shareholders. We intend to retain cash for the continued development of our business. As a result, your return on investment will be solely determined by your ability to sell your shares in a secondary market.

The market valuation of our business may fluctuate due to factors beyond our control and the value of your investment may fluctuate correspondingly.