Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - INDEPENDENT BANK CORP | d406431d8k.htm |

September 5, 2012

Christopher Oddleifson

President & Chief Executive Officer

Denis K. Sheahan

Chief Financial Officer

Exhibit 99.1 |

•

Main Sub:

Rockland Trust

•

Market:

Eastern Massachusetts

•

Loans:

$4.0 B

•

Deposits:

$4.1 B

•

$AUA:

$2.0 B

•

Market Cap:

$0.6 M

•

NASDAQ:

INDB

Who We Are

2 |

•

Strong fundamentals driving solid performance

•

Robust growth from new and existing customers

•

Expanding footprint into attractive markets

•

Aggressively promoting brand and new products

•

Investing for growth in high priority businesses

•

Disciplined risk management culture

•

Strong tangible and regulatory capital

Key Messages

3 |

Company Footprint*

4

Source: SNL Financial; Deposit/Market Share data as of June 30, 2011 including

pending transactions. (Includes Credit Unions) * Proforma to include the

pending acquisition of Central Bancorp. % of INDB Dep.

Rank

2011

1

16.7%

42%

Rank

2011

7

3.6%

17%

Rank

2011

4

10.2%

15%

Rank

2011

9

5.2%

13%

Rank

2011

23

1.0%

12%

Rank

2011

44

0.3%

1%

Barnstable County (Cape Cod)

Market Share

Plymouth County

Bristol County

Worcester County

Middlesex County

Norfolk County

78 Branches*

Commercial Lending

and Investment

Management Center |

•

Excellent loan and core deposit growth

•

Expanded breadth and depth of commercial franchise

•

Households grew by 7% in 1H12

•

Investment Management growth: Rev.

8% in 1H12

•

All capital ratios and TBV rose in past 12 months

•

Fitch upgrade and affirming of long-term issuer rating

•

New Market Tax Credits Award

(4 time)

•

Multiple 3 party recognition of excellence

Recent

Accomplishments

5

th

rd |

Strong Fundamentals

Driving Performance

6

•

Excellent loan growth

•

Core dep. up to 84%

•

Growing wealth mgmt.

•

Solid asset quality vs. peers

•

Strong capital

•

Core ROA near 1%

Diluted EPS

$1.43

$1.90

$2.12 $1.02 $0.99

+13%

+44%

* Loan fraud amounting to $4.0 million pre-tax

23.8

Operating Earnings

($ Mil.) |

Robust Core Business Generation

($ Mil.)

7

+11% CAGR

+8% CAGR

6/12 vs.

6/11

6/12 vs.

3/12

7%

13% annualized

23%

22% annualized

Comm’l Loan

$ Bal.

Home Equity

$ Bal.

Comm’l Loan Originations

Consumer Loan Originations

(Resi’s & Home Eq.) |

Strong Commercial and

Industrial Loan Growth

($

Bal.-mil.)

8

Yr. end

+27.0% CAGR

(24.6% ex acquisitions)

Adding High Quality Corporate Customers |

Attractive Balance Sheet Profile

(2Q12)

Very Focused On Containing Deposit Costs Shift

Towards Higher Yielding Assets TOTAL DEPOSITS

$4.1 B

AVG. COST: 0.28%

EARNING ASSETS

$4.7 B

Sec./ST Inv.

14%

Resi Mtges

9%

Home Eq

17%

Other

1%

Comm'l Loans

59%

Demand

Deposits

26%

Money

Market

20%

Savings/Now

38%

CD's

16% |

Net Interest Margin

Fairly steady over various rate cycles

Current low rate environment adding pressure

10 |

Investment Management –

High Priority Growth Business

11

•

Growing source of fee revenues

•

Strong feeder business from bank

•

Expanded investment offerings

•

Professionally managed

$ mil.

2006

2Q12

Assets

under

Admin.

816

$

+

145%

2,001

$

Revenues

6.1

$

+

121%

13.5

$

(2011)

7.4

$

(1H12) |

Asset Quality –

Well Managed

NPL/Loan %

1.07%

0.65%

0.76% 0.79% Peers

3.31%* Loss Rate

38bp

43bp

26bp 52bp

Peers 69bp*

Yr. end

* Source: FFIEC Peer Group 2; $3-10 Billion in Assets, March 31, 2012

Incl. 90 days + overdue

10.0

36.2

23.1

29.0

31.3

2009

2010

2011

2Q12

NPL’s

($

Mil.)

12.0

14.8

9.5

4.0

customer

fraud

6.0

2009

2010

2011

1H12

Net Chargeoffs

($

Mil.) |

Strong Loan Loss Reserves

13

Reflects Ben

Franklin loans

acquired at FV

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

1.60%

Reserves/Loans

Net Chargeoffs/Avg.

Loans (annualized)

Reserves a Healthy Multiple of Loss Rate |

Strong Capital

14

(1)

Includes tax deductibility of certain goodwill

•

Strong internal capital generation

•

No external capital raising

•

No dividend cuts

(Year end)

Tier 1 Leverage %

Tangible Common %

(1)

Tangible Book Value

(1) |

Attentive to Shareholder Returns

15

Cash Dividends Per Share |

Business Opportunities

•

Expanded Commercial Presence

(Providence, Waltham)

•

Asset-Based Lending

•

Marketing

•

Mobile Banking

•

Image ATMs

Investing for Future Growth

16 |

Sustaining Business Momentum

17

Business Line

Focal Points

•

Expand Market Presence

•

Grow C&I Client Base

•

Expand Specialty Products, e.g. ABL

•

Continue to Drive Household Growth

•

Expand Electronic Banking Platform

•

Optimize Branch Network

•

Capitalize on Strong Market Demographics

•

Target COI Opportunity

•

Continue Strong Branch/Commercial Referrals

•

Continue Aggressive H.E. Marketing

Commercial

Retail Delivery

Investment Management

Home Equity |

Rockland Trust is the #1 ranked

New England bank in Customer

Satisfaction!

18 |

•

Attractive financial return

–

Highly accretive to earnings: +7% in 2013

–

IRR of 15.4%

–

Modest dilution to TBV and TCE/TA with short earn-back period

•

Significantly increases footprint in eastern Middlesex County, a

natural market extension with attractive demographics

–

Part

of

the

Boston

MSA

–

the

10

th

largest

MSA

by

population

in

the

U.S.

1

–

Largest population of any county in New England (~1.5 million) and third

highest

median

household

income

(~$78K)

1

•

Introduction of INDB operating model will provide:

–

Significant opportunity for improved efficiencies

–

Attractive platform for broader INDB product lines

Central Bancorp. (CEBK) Acquisition

Strategic Rationale

1

Source: SNL Financial

Source: SNL Financial; U.S. Bureau of Economic Analysis

19 |

Investment

Management

Commercial

Banking

Retail/

Consumer

•

$2 Bil. AUA

•

Wealth/Institutional

•

Sophisticated Products

•

Expanded presence

•

Knowledgeable bankers

Central Bancorp. Customer Base

Capitalizing on Rockland Trust Brand

•

Top-rated customer

satisfaction

•

Electronic banking

•

Home equity

INDB

Winning

Businesses

–

Major

Opportunities

20 |

Building Franchise Value

All Acquisitions Immediately Accretive

Deal Value: $40MM

12% Core Dep. Premium**

Fleet

Divest.

Aug ‘00

$336mm Deposits

$135mm Loans

16 Branches

Deal Value: $37MM

11% Core Dep. Premium**

Falmouth

Bancorp

Jul ‘04

$158mm Assets

$137mm Deposits

4 Branches

Deal Value: $105MM

17% Core Dep. Premium**

Slade’s Ferry

Bancorp

Mar ‘08

$610mm Assets

$409mm Deposits

9 Branches

Deal Value: $84.5MM

2% Core Dep. Premium**

Benjamin

Franklin Bancorp.

Apr ‘09

$998mm Assets

$653mm Deposits

11 Branches

Deal Value: $54.8MM

8% Core Dep. Premium**

Central

Bancorp.

4Q12*

$521mm Assets

$333mm Deposits

10 Branches

Disciplined Acquisitions

* Estimated closing

** Incl. CD’s <$100k |

2012 Outlook –

Key Expectations

Loan Growth

+6 – 7%

Led by commercial and home equity

Deposits

+5 – 6%

Continued core deposit growth

Net Chargeoffs

$15 – 17 MM

Provision $16 – 18 MM

1H margin of 3.81%

Lower over 2H

Non-Interest Inc.

Flattish

Invest. mgmt.

, Mort. rev.

NIE

+ 2 – 3%

Selective growth investing

Tax Rate

27.5%

vs. 27% in 2010

Net Int. Margin

FY: Mid 3.70s%

22 |

•

High quality franchise in attractive markets

•

Strong on-the-ground business volumes

•

Operating platform that can be leveraged further

•

Investing for growth in competitive strengths

•

Balance sheet equipped to deal with uncertainty

•

Grounded management team

•

Aligned

with

shareholders

–

insider

ownership

7%

•

Positioned to grow, build, and acquire to drive long-

term value creation

INDB –

Investment Merits

23 |

NASDAQ Ticker: INDB

www.rocklandtrust.com

Denis Sheahan -

CFO

Shareholder Relations:

Jennifer Kingston (781) 878-6100

Statements contained in this presentation that are not historical facts are

“forward-looking statements”

that are subject to risks and uncertainties which could cause actual results to

differ materially from those currently anticipated due to a number of

factors, which include, but are not limited to, factors discussed in

documents filed by the Company with the Securities and Exchange Commission

from time to time. |

Appendix |

•

Central, founded in 1915, is a $521

million asset bank headquartered in

the affluent Middlesex County

suburb of Boston, MA

•

Central operates 10 branches

across Middlesex County with top 10

deposit market share in each city

¹

•

Stock symbol: CEBK

•

Financial Profile:

–

Loans: $421mm

–

Deposits: $333mm

–

Tang. Comm. Equity: $33mm

–

LTM Net Income: $1.0mm

–

Cost of Deposits: 0.52%

–

NIM: 3.35%

–

Efficiency Ratio: 89.6%

–

LTM Net Chargeoffs: 0.23%

–

NPAs / Assets: 1.88%²

Note: Financial data as of December 31, 2011 or as of three months ended December

31, 2011, annualized Central full service branches located in Somerville

(1), Woburn (2), Arlington (1), Melrose (1), Burlington (1), Chestnut Hill

(1), Medford (1), and Malden (1); limited service high school branch in

Woburn (1) Overview of Central Bancorp

INDB (67)

CEBK (10)

(1)

Source: SNL Financial

(2)

Management December 31, 2011 Financial Statements, excluding

TDR’s |

•

7%

E.P.S.

accretive

in

2013,

7

–

8%

thereafter¹

•

IRR of 15.4%

•

5.8% TBV dilution and short earn-back period of 4.75 years

•

Strong pro forma capital levels at close with TCE / TA earn-back

period of 2.25 years

•

TCE / TA:

6.5%

•

Adjusted TCE / TA²:

•

Tier 1 Leverage:

8.0%

•

Tier 1 Capital:

10.4%

•

Total Risk Based Capital:

12.3%

Attractive Financial Transaction

(1)

Based on analyst consensus estimates

(2)

Pro

forma

to

include

the

tax

deductibility

of

goodwill

–

non-GAAP

measure

•

No additional capital raise

6.8% |

Loan Mix

Note: GAAP financial data as of June 30, 2012

($ in thousands)

Commercial & Industrial

$705,433

17.7%

$780

0.2%

$706,213

15.8%

Multifamily & CRE

1,912,563

48.0%

154,090

31.4%

2,066,653

46.3%

1-4 Family Residential

389,053

9.8%

323,897

66.1%

712,950

15.9%

Consumer & Other

973,740

24.5%

11,065

2.3%

984,805

22.0%

Total Loans

$3,980,789

100.0%

$489,832

100.0%

$4,470,621

100.0%

MRQ Yield on Loans

INDB

Combined

Central

4.46%

4.52%

4.47% |

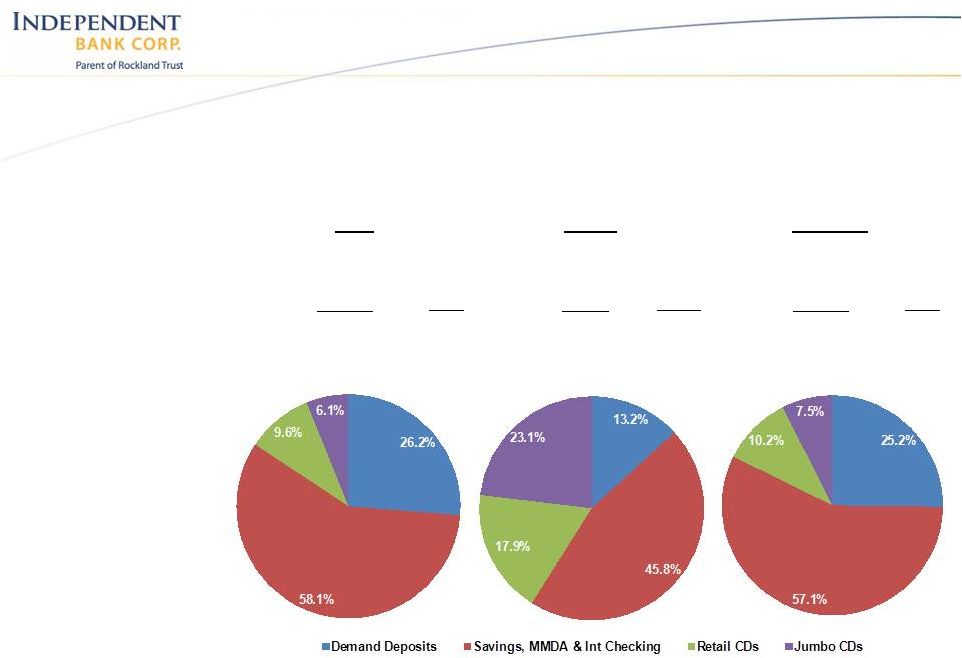

Deposit Mix

Note: GAAP financial data as of June 30, 2012

($ in thousands)

Demand Deposits

$1,070,279

26.2%

$47,039

13.2%

$1,117,318

25.2%

Savings, MMDA & Int Checking

2,368,319

58.1%

163,403

45.8%

2,531,722

57.1%

Retail CDs

390,242

9.6%

63,980

17.9%

454,222

10.2%

Jumbo CDs

249,293

6.1%

82,478

23.1%

331,771

7.5%

Total Deposits

$4,078,133

100.0%

$356,900

100.0%

$4,435,033

100.0%

MRQ Cost of deposits

0.27%

0.52%

0.29%

INDB

Central

Combined |