Attached files

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2011

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _____________ to _______________.

Commission File No. 000-52346

TODA INTERNATIONAL HOLDINGS INC.

(Exact Name of Registrant as Specified in Its Charter)

| CAYMAN ISLANDS | N/A | |

|

(State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification No.) |

c/o Dalian TOFA New Materials Development Co, Ltd.

No. 18-2-401 Gangjing Garden, Dandong Street, Zhongshan District

Dalian, Liaoning Province, PRC 116001

(Address of Principal Executive Offices, including zip code)

011-86-(411) 8278-9758

(Registrant’s Telephone Number, Including Area Code)

Securities registered under Section 12(b) of the Exchange Act: None

Securities registered under Section 12(g) of the Exchange Act: Ordinary stock, par value $0.000256 per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (Section 229.405) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer," "accelerated filer” and "smaller reporting company" in Rule 12b-2 of the Exchange Act (check one):

| Large accelerated filer ¨ | Accelerated filer ¨ | |

| Non-accelerated filer ¨ | (Do not check if a smaller reporting company) | Smaller reporting company þ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

April 13, 2012, there were 27,780,000 shares of the registrant's ordinary stock, par value $0.000256 were outstanding.

TABLE OF CONTENTS

| Page | ||||

| PART I | ||||

| Item 1. | Business | 1 | ||

| Item 1A. | Risk Factors | 18 | ||

| Item 1B. | Unresolved Staff Comments | 36 | ||

| Item 2. | Properties | 36 | ||

| Item 3. | Legal Proceedings | 37 | ||

| Item 4. | Submission of Matters to a Vote of Security Holders | 37 | ||

| PART II | ||||

| Item 5. | Market for Registrant’s Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities | 38 | ||

| Item 6. | Selected Financial Data | 38 | ||

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 39 | ||

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 52 | ||

| Item 8. | Financial Statements and Supplementary Data | 52 | ||

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 52 | ||

| Item 9A. | Controls and Procedures | 52 | ||

| Item 9B. | Other Information | 54 | ||

| PART III | ||||

| Item 10. | Directors and Executive Officers of the Registrant | 55 | ||

| Item 11. | Executive Compensation | 58 | ||

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Shareholder Matters | 61 | ||

| Item 13. | Certain Relationships and Related Transactions | 61 | ||

| Item 14. | Principal Accountant Fees and Services | 63 | ||

| PART IV | ||||

| Item 15. | Exhibits and Financial Statement Schedules | 65 | ||

| SIGNATURES | 67 | |||

| EXHIBITS | ||||

The statements contained in this Annual Report on Form 10-K that are not historical facts are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 with respect to our financial condition, results of operations and business, which can be identified by the use of forward-looking terminology, such as “estimates,” “projects,” “plans,” “believes,” “expects,” “anticipates,” “intends,” or the negative thereof or other variations thereon, or by discussions of strategy that involve risks and uncertainties. Management wishes to caution the reader of the forward-looking statements that such statements, which are contained in this annual report, reflect our current beliefs with respect to future events and involve known and unknown risks, uncertainties and other factors, including, but not limited to, economic, competitive, regulatory, technological, key employee, and general business factors affecting our operations, markets, growth, services, products, licenses and other factors discussed in our other filings with the Securities and Exchange Commission ("SEC"), and that these statements are only estimates or predictions. No assurances can be given regarding the achievement of future results, as actual results may differ materially as a result of risks facing us, and actual events may differ from the assumptions underlying the statements that have been made regarding anticipated events.

These forward-looking statements are subject to numerous assumptions, risks and uncertainties that may cause our actual results to be materially different from any future results expressed or implied by us in those statements. Some of these risks are described in “Risk Factors” in Item 1A of this annual report.

These risk factors should be considered in connection with any subsequent written or oral forward-looking statements that we or persons acting on our behalf may issue. All written and oral forward looking statements made in connection with this annual report that are attributable to us or persons acting on our behalf are expressly qualified in their entirety by these cautionary statements. Given these uncertainties, we caution investors not to unduly rely on our forward-looking statements. We do not undertake any obligation to review or confirm analysts’ expectations or estimates or to release publicly any revisions to any forward-looking statements to reflect events or circumstances after the date of this document or to reflect the occurrence of unanticipated events. Further, the information about our intentions contained in this document is a statement of our intention as of the date of this document and is based upon, among other things, the existing regulatory environment, industry conditions, market conditions and prices, the economy in general and our assumptions as of such date. We may change our intentions, at any time and without notice, based upon any changes in such factors, in our assumptions or otherwise.

In this Annual Report on Form 10-K, we will refer to TODA International Holdings, Inc., a Cayman Islands exempted company, as "TODA," "Company," "we," "us," and "our."

PART I

Item 1. Business.

Overview

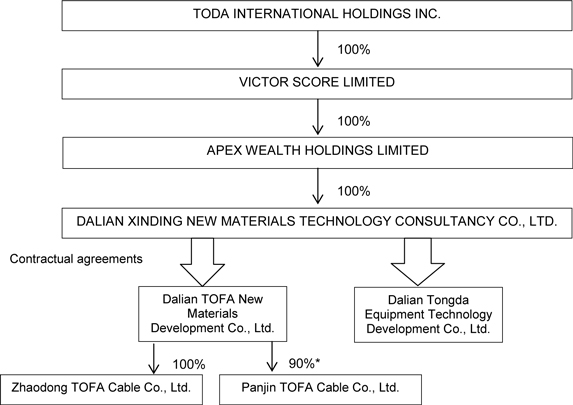

We were incorporated as Summit Growth Corporation on September 27, 2006 in the Cayman Islands as an exempted company. Since March 15, 2011, our principal place of business has been based in the People’s Republic of China (the “PRC” or “China”). Our name was changed to TODA International Holdings, Inc. as of May 16, 2011. Our headquarters are located at: c/o Dalian TOFA New Materials Development Co, Ltd., No. 18-2-401 Gangjing Garden, Dandong Street, Zhongshan District, Dalian, Liaoning Province, PRC 116001, Telephone: 011-86-(411) 8278-9758.

We are primarily engaged in the research and development, production and distribution of composite bimetallic materials, primarily copper-clad aluminum, or CCA, and its manufacturing equipment. We are also involved in the research and development of additional related production technologies and we provide consultancy services on such technologies to a number of entities, within and out of China. Due to PRC legal restrictions on foreign ownership and investment in businesses in China, we operate our business primarily through Dalian TOFA New Materials Development Co., Ltd. (“TOFA”) and Dalian Tongda Equipment Technology Development Co, Ltd. (“Tongda” and, collectively with TOFA, the “VIEs”), each a consolidated affiliated entity of TODA in China.

| 1 |

Organization

We are a holding company and parent of Victor Score Limited, a British Virgin Islands business company incorporated on May 13, 2010 (“Victor Score”). Victor Score is the parent company of Apex Wealth Holdings Limited, a Hong Kong limited liability company incorporated on February 12, 2010 (“Apex Wealth”). Apex Wealth is the parent of Dalian Xinding New Materials Technology Consultancy Co., Ltd., a wholly-owned foreign enterprise incorporated in China (“Dalian Xinding”) on August 18, 2010. None of Victor Score, Apex Wealth or Dalian Xinding conducts any independent business operations. Dalian Xinding entered into a series of contractual arrangements with each of the VIEs and their respective shareholders on October 12, 2010 (collectively, the “VIE Agreements”), pursuant to which Dalian Xinding effectively controls, and is able to derive substantially all of the economic benefits from, the VIEs. The VIE Agreements include a Loan Agreement, Equity Interest Pledge Agreement, Equity Interest Purchase Agreement, Business Operation Agreement and Lease Agreement.

Pursuant to the terms of the Loan Agreement, Equity Interest Pledge Agreement and Equity Interest Purchase Agreement, Dalian Xinding effectively gained equity control of TOFA and Tongda.

| · | Under the Loan Agreement, each of the TOFA and Tongda shareholders received a loan from Dalian Xinding to pay off the debts arising from their capital contributions to TOFA and Tongda. |

For TOFA shareholders, Pi Jia Liu, Zong Li Li and Chuan-Tao Zheng, the aggregate amount of the loans is approximately $2.25 million (based on conversion rate of 1 RMB = $0.149849 on October 12, 2010). The individual loan amounts for Messrs. Liu, Li and Zheng are approximately $0.19 million, $0.35 million and $1.70 million, respectively.

For Tongda shareholders, Li Zhi Fei, Di Wang and Yu-Kai Wang (YK Wang), the aggregate amount of the loans is approximately $1.05 million (based on conversion rate of 1 RMB = $0.149849 on October 12, 2010). The individual loan amounts for Messrs. Fei, Di Wang and YK Wang are approximately $0.08 million, $0.43 million and $0.53 million, respectively.

Each of the loans contains the following additional material terms:

| · | Interest free |

| · | 10 year term |

| · | Repayment limited to transfer of all equity held in TOFA or Tongda, as applicable, to Dalian Xinding |

| · | Under the Equity Interest Pledge Agreement, each of the TOFA and Tongda shareholders pledged 100% of their equity interest in TOFA and Tongda to Dalian Xinding as collateral for their obligation under the Loan Agreement, Equity Interest Purchase Agreement and Business Operation Agreement. Messrs. Liu, Li and Zheng currently hold 8.6%, 15.7% and 75.7%, respectively, of the equity interest in TOFA. Messrs. Fei, D Wang and YK Wang currently hold 7.8%, 41.2% and 51.0%, respectively, of the equity interest in Tongda. |

As pledgee, Dalian Xinding has the right to sell the pledged equity pursuant to the law or through any other approach. If Dalian Xinding decides to enforce the pledge agreement, the pledgor shareholder must ensure that all of his rights as a shareholder are transferred to Dalian Xinding.

| · | Under the Equity Interest Purchase Agreement, Dalian Xinding has the right to purchase all or part of the TOFA and Tongda equity interest held by the shareholders at any time for a purchase price equal to the shareholder’s original investment price for the equity interest. For each of Messrs. Liu, Li and Zheng, the original investment price was approximately $22,477 for each percentage of equity interest held by him. For each of Messrs. Fei, D Wang and YK Wang, the original investment price was approximately $10,489 for each percentage of equity interest held by him. The total purchase price for the equity interests held by each of the TOFA and Tongda shareholders equals the amount of the Loan Agreements that they entered into with Dalian Xinding. |

| 2 |

Pursuant to the terms of the Business Operation Agreement, Dalian Xinding effectively gained management control of TOFA and Tongda.

| · | Without written consent of Dalian Xinding, neither TOFA nor Tongda can enter into or consummate a transaction that might significantly affect the assets, obligations, rights and operations of TOFA or Tongda. |

| · | Dalian Xinding is entitled to provide advice and guidance regarding hiring and firing employees, daily operations and financial management of TOFA and Tongda, and the management of TOFA and Tongda have agreed to accept such advice and guidance. |

| · | Dalian Xinding is entitled to recommend all candidates for directors and executive officers of TOFA and Tongda and TOFA and Tongda have agreed to appoint the candidates recommended by Dalian Xinding. |

| · | TOFA and Tongda have issued a letter of authorization that authorizes designated officers of Dalian Xinding to act as their proxies and exercise all rights of shareholders at any shareholders meetings of TOFA or Tongda pursuant to PRC law and the bylaws of TOFA and Tongda. |

Pursuant to the terms of the Lease Agreement, TOFA and Tongda have leased all of the property, plant and equipment of TOFA and Tongda to Dalian Xinding and Dalian Xinding possesses the right to use all of such property, plant and equipment during the lease term.

The following diagram sets forth the current ownership structure of the Company:

| * | the remaining 10% ownership of Panjin TOFA Cable Co., Ltd. is held by two minority shareholders of TODA. |

Each of TOFA and Tongda is a private limited company incorporated and headquartered in Dalian, Liaoning Province, China. Mr. Zheng, our Chairman of the Board, President and Chief Executive Officer, is the majority owner of TOFA, holding 75.7% of the equity interest in TOFA. Mr. YK Wang, our Chief Technology Officer and a director, is the majority owner of Tongda, holding 51.0% of the equity interest in Tongda. Zhaodong TOFA Cable Co., Ltd. (Zhaodong TOFA) was formed on November 18, 2011 and is a wholly-owned subsidiary of TOFA. Panjin TOFA Cable Co., Ltd. (“Panjin TOFA”) was formed on June 30, 2011 and is a majority owned subsidiary of TOFA. Two minority shareholders of TODA hold an aggregate 10% equity interest in Panjin TOFA.

History

From incorporation to March 15, 2011, the business of the Company, as Summit Growth Corporation, consisted solely of identifying and entering into a business combination with a privately held business or company, domiciled and operating in an emerging market that was seeking the advantages of being a publicly held corporation whose stock is eventually traded on a major United States stock exchange.

On March 15, 2011, the Company and its controlling shareholders entered into and consummated a share exchange with Victor Score and the Victor Score shareholders. Pursuant to the terms of a Share Exchange Agreement among the parties (the “Share Exchange Agreement”), all of the issued and outstanding shares of Victor Score were exchanged for shares of the Company.

| 3 |

In addition, the following actions occurred under the terms

of the Share Exchange Agreement:

| · | The Company issued an aggregate of 32,839,910 ordinary shares to 35 former Victor Score shareholders in exchange for 30,546.31 shares of Victor Score stock then held by them and 104,571.95 preference shares to Mr. Zheng in exchange for 19,453.69 shares of Victor Score stock then held by him. Upon effectiveness of the share exchange, the Company had 34,645,610 ordinary shares and 104,571.95 preference shares issued and outstanding. Mr. Zheng held 100% of the outstanding preference shares, or 23.19% of the voting power, of the Company. |

| · | As a condition to the closing of the share exchange, Mr. Joseph Rozelle resigned as a director of the Company, such resignation was effective on May 5, 2011, and Messrs. Zheng, YK Wang and Yu-Long Wang (YL Wang) were appointed to the board of directors of the Company, with Mr. Zheng being named Chairman of the Board. Mr. Zheng’s appointment was effective immediately and the appointments of Messrs. YK Wang and YL Wang were effective on May 5, 2011. |

| · | Also as a condition to the closing of the share exchange, Mr. Karl Brenza resigned as the President and Chief Executive Officer of the Company, Mr. Zheng was appointed Chief Executive Officer and President, Mr. Anthony Zhang was appointed Chief Financial Officer and Secretary, Mr. Pi-Jia Liu was appointed Chief Operating Officer and Mr. YK Wang was appointed Chief Technology Officer. |

As of May 16, 2011, we effected a one-for-two consolidation of our issued and outstanding ordinary shares and increased the amount of our authorized ordinary shares from 39,062,500 shares to 100,000,000 shares. The preference shares issued in connection with the share exchange were automatically converted into 10,457,195 ordinary shares upon effectiveness of the share consolidation.

As a result of the consummation of the share exchange and the one-for-two share consolidation, as of May 16, 2011, we had 27,780,000 ordinary shares and no preference shares of the Company's capital stock issued and outstanding.

Business

Description of Our Industry

The Composite Bimetallic Material Industry, Generally

The composite bimetallic material industry is part of the wire and cable industry. The wire and cable market broadly consists of two large categories: electrical, involving products that are used for electrical current carrying capabilities, and telecommunications, involving products that are used for signal carrying communications purposes. The global bimetallic wire industry is fast-growing and increasingly competitive. This is especially true in China where there is considerable fragmentation of manufacturers.

Traditionally, electrical conducting wires are made of copper because of its excellent conductivity, solderability and lower contact resistance. However, the weight of copper has been a disadvantage. Copper cladding over a core of steel or aluminum offers the surface corrosion resistance and solderability of a solid copper conductor at significantly less weight. As a result, composite bimetallic conductors are generally used as substitutes for solid copper conductors and offer the consumer the following advantages over solid copper - lighter weight per unit volume and high tensile strength - while maintaining the excellent conductivity of pure copper.

To produce the composite bimetallic material, aluminum rods or steel wires are wrapped concentrically with high quality copper ribbon; the two metals are then bound together using advanced clad welding technology. The clad welding enables the two metals to establish a very firm and strong metallurgical bond and makes the two become an inseparable one. The composite bimetallic material can be subject to wire-drawing and heat treatment processes just like single metal material. During the wire-drawing process, the outer copper cladding and the inner aluminum or steel core are proportionally decreased in diameter, thereby guaranteeing a constant ratio in the volume of copper per unit of composite bimetal.

| 4 |

In the 1970s, scientists in the US, Europe and Japan began researching and developing the first CCA materials. Their research concluded that CCA wire could be used effectively in much the same way as pure copper wire. This made CCA wire an excellent substitute for pure copper wire in terms of their applications, techniques involved and more importantly, costs. Since then, CCA wire and cable have been widely employed in the telecommunication, information technology, auto and, most recently, construction industries, which resulted in a tremendous decrease in the use of copper resources and project costs.

When compared to pure copper, composite bimetals have distinct advantages:

| · | Because of the “superficial effect” of high frequency signals, composite bimetals have the same electrical conductivity as pure copper when transmitting high frequency signals of 5 MHz or above; |

| · | The density of CCA wire is only 37% to 40% of pure copper wires, so for wires of the same weight and diameter, CCA wire will be 2.45 to 2.65 times longer than pure copper wire; |

| · | The copper outer layer makes it easy to weld; |

| · | The relative lighter weight of CCA to pure copper (ratio of 1:2.45 for wires of equal length) makes it easier to handle and saves on unit transportation cost; |

| · | Higher flexibility makes CCA easier to be processed than pure copper; |

| · | pure copper could cost about three times as much as CCA; and |

| · | Copper-clad steel, or CCS, wire is 1.6 to 2 times stronger than pure copper in terms of tensile strength when comparing wire of same weight and diameter, and, during signal transmission, has the same transmission parameters as pure copper; therefore, production costs of electrical wire and cable can be greatly reduced employing the composite bimetallic material while maintaining the strength of pure copper. |

Composite bimetallic wire can be further processed into enameled, tin-plated and silver-plated wire depending on the final application. Tin-plated composite bimetallic wire easily welded and can resist being sulphuretted. Silver- plated CCS wire has a higher conductivity for electricity and heat and better resistance to corrosion and oxidation. Therefore, these wires can be applied to a great variety of fields.

Aside from the more traditional use of composite bimetallic wire in the electrical and telecommunications business, composite bimetallic wire has found wide application in industries that have high-tech elements, such as the military, aerospace, automobile, computer and electronic appliance industries.

The Chinese Composite Bimetallic Metal Market

Prior to 1997, China did not have the capability to produce any composite bimetallic material. TOFA was one of the first companies to enter into the industry, spending time and energy researching the production of CCA material and succeeding in developing this product in China. TOFA was granted a national patent by the PRC Government for its proprietary technology used in the production of bimetallic wires with clad welding in 1997. The successful development of composite bimetallic material by local companies, including TOFA, was a landmark innovation in China. It has filled the vacuum in the production of this category of “new materials” in the country.

The successful development of composite bimetallic materials has significant meaning for China, reducing the cost of production of copper clad products and China’s reliance on imported composite bimetallic materials. This has also created an industry that helps to lower material or production costs for companies in downstream industries, and helps the country save millions of tons of copper resources per annum.

| 5 |

Because of the various advantages they have over pure copper products, the demand for composite bimetallic wire has been steadily increasing ever since they were introduced to the market. In 2005, Professor Dai, YaKang, a leading expert in the introduction and development of composite bimetals in China predicted, while participating in the Beijing Conference of the International Copper Association Ltd. (the “ICA Conference”), that 25% to 50% of the copper products market in China would gradually be replaced by composite bimetallic products by 2025. The International Wrought Copper Council (“IWCC”) has estimated that, at present, the annual demand for copper in China is in excess of 5 million tons. Based upon the statistics set forth by the IWCC, this demand increased at a rate of between 10% and 20% per year since 2000. Using a 25% assumed replacement rate, by 2025 the annual demand for CCA and CCS will be at least 1.25 million tons. Using the current wholesale price of approximately US$5,800 per ton, the domestic CCA and CCS market in China will conservatively be worth about US$7.25 billion per year by 2025.

Prior to 2005, the supply of CCA and CCS material for use in business in China was lagging the rest of the world because there were only a few manufacturers in China capable of producing composite bimetallic products. As a result of surging copper prices in early 2005, there was imminent need for the use of composite bimetals as replacements for pure copper material in a great variety of industries. This led to the rapid establishment of a number of companies that began producing composite bimetallic material and wires. However, due to a lack of access to proprietary technology and R&D capability, most of these producers operate on a rather small scale and produce composite bimetallic products that are used in the “lower end” markets, like those to be applied to home appliances. There are currently approximately 20 manufacturers that are of sufficient size, with production capacity, technological know-how and R&D capability to effectively compete on a national scale and less than five, including TOFA, are considered major players who have the ability to produce the kind of composite bimetallic products that are in great demand and could yield higher margin like the electricity and power cables on a larger scale, without the need to compete on price alone.

The Liaoning Province 2011 Government Work Report, published on January 27, 2011, provides that the local government is undertaking five industry-promoting programs designed to support Liaoning’s development. In connection with the “Industrial Project,” the government anticipates that “fixed asset investment” will surpass RMB 850 billion ($150 billion), with the investment in the power industry representing approximately 2% of the total. As a result, the Provincial Electricity Bureau’s solicitation of tenders for the supply of power cables could be worth US$3 billion every year. Although not all of the cables used will be made of composite bimetallic products, there is tremendous potential for growth in this area. In terms of total output, China produced about 5,000 tons of CCA and CCS wire in 2001, as compared to total production of 25,000 tons of CCA and CCS wire in 2006 and 40,000 tons in 2007.

In late 2008/early 2009, the Chinese State Council announced a US$590 billion stimulus package to support the Chinese economy in response to the financial turmoil of late 2008. Approximately US$30 billion of this stimulus money has been allocated to the advancement of the telecommunication industry, including the promotion of 3G mobile communication services, digital TV sets and next generation broadband. The 3G and 3G LTE Development Plan put forth by the Chinese State Council, provides that, with respect to radio and cellular technology, approximately RMB 400 billion will be invested in this sector over the next several years to build in excess of 400,000 base stations to provide services to approximately 15 million end users. This represents an annual increase of approximately 80,000 to 100,000 base stations throughout the country for the next three years. Based on TOFA’s experience, each base station needs between 500 and 800 meters of coaxial cable which equates to a minimum annual demand of 60,000 kilometers of coaxial cables. Each kilometer of coaxial cable uses approximately 500-700 kilograms of CCA, resulting in an annual demand of approximately 40,000 tons of CCA per year. Management believes that this will lead to a much higher demand for CCA wires and in fact that the whole composite bimetallic materials industry shall be significantly boosted.

Description of Our Business

Unless otherwise indicated, the following information relates only to the business and operations of our VIEs.

| 6 |

Our Variable Interest Entities

Dalian TOFA New Materials Development Co., Ltd.

TOFA was founded as a limited liability company on November 12, 1997. It is engaged in the development, manufacture and sale of composite materials, primarily copper-clad aluminum wire, for use in various industries in China. TOFA is a pioneer in the composite bimetallic materials industry in the PRC in terms of the production equipment and technology it employs, the quality of its products and its research and development capability.

Industrial data collected by TOFA suggests that it currently has a market share of approximately 30% of the high-end radio frequency (“RF”) cable CCA market segment in China. The “high-end RF cable CCA market segment” includes primarily telecommunications operators, and to a lesser extent, the power cable industry. In 2009, according to the most recent statistics available as published in the China Cable and Optical Device Industry Summary and 5 Year Plan 2011-2015, the telecommunications RF cable market accounted for the sale of approximately 400,000 kilometers (km) of copper and/or CCA material. Industry-wide, RF cables sold in 2009 consisted of approximately 60% of 7/8” Φ9.3-9.8 copper inner conductors and 40% of 1/2” Φ4.90 CCA inner conductors. The total sale of CCA inner conductors was, therefore, 160,000 km. Each km of CCA inner conductor contains 60 kg of CCA, using a total of 9,600 metric tons of CCA in 2009. Although we believe that these 2009 statistics present a conservative picture of the industry as of early 2011, assuming stagnant production in 2010 and taking into account TOFA’s sale of 7,074 metric tons of CCA for RF cables in 2011, at the end of 2011, TOFA is estimated to have sold approximately 30% of all high-end RF cable CCA in China in 2011.

Its proprietary clad-welding technology was first awarded a patent by the Chinese Government in 1997 and its CCA wire was recognized as a “State Level Major New Product” by five Ministries of the State Council of PRC within four years of inception. Since then, TOFA has secured six patents on its processes and products.

In 2000, the Company was invited by the China National Standardization Committee to be the principal party participating in the drafting of industrial standard SJ/T11223-2000 for the use of CCA and CCS wires in the electronic industry in China. The standard has been expanded and is now applicable to all production, manufacturing and use of CCA and CCS products in China. Manufacturers of composite bimetallic materials are also required to satisfy the International Standards certification ISO9001:2000, a quality management system where an organization:

| 1. | must demonstrate its ability to consistently provide product that meets customer and applicable regulatory requirements, and |

| 2. | aims to enhance customer satisfaction through the effective application of the system, including processes for continual improvement of the system and the assurance of conformity to customer and applicable regulatory requirements. |

TOFA meets these certification standards. Further, TOFA’s products are recognized within the wire and cable industry, both domestically and internationally, to be of very high quality and the “TTOFF” trademark under which TOFA markets its products is a sign of quality. With customers’ recognition for its brand and products, TOFA began to expand its production capacity and continued to develop more products and the related production technologies.

TOFA is beginning to enjoy the rewards of its efforts spent on product and technology development in the earlier days. Management believes that, as a result of its reputation, quality and product development capability, coupled with the increased demand for composite bimetallic products in China and an aggressive business development plan (discussed below), TOFA will continue to grow in the industry over the next two to three years.

| 7 |

Products and Services

TOFA currently produces a series of composite bimetallic materials from copper and aluminum. CCA is aluminum with a cladding of copper welded along the whole length of the material. Such material normally appears in the form of a wire and can be further drawn into fine wires with different diameters and/or further processed into wires with different coatings like silver, enamel or tin according to the requirements of their final applications or specifications of the customers.

The major products of TOFA include:

| · | CCA wire for use in telecommunication cables; |

| · | CCA wire for use in power cables; and |

| · | Raw material for electro-magnetic coils. |

The CCA wire produced by TOFA is either sold to end users or to intermediaries who further process the materials into finer wires or coated wires. Because of the unique characteristics of the CCA wire, namely the high conductivity, light weight and lower prices when compared to pure copper wires, management believes that there will be tremendous demands for the Company’s CCA wire products, especially in the telecommunications and power industries in China. At present, annual spending on copper products within the power industry in China is estimated to be US$71 billion, and about 30% of which is for power cables. Using current estimates, and assuming a 25% replacement of pure copper cables by CCA cables at a price equal to about 70% of the price for pure copper, we believe the market potential of CCA power cables could reach US$3.7 billion annually by 2025 (US$71 billion x 30% x 25% x 70%).

In 2006, TOFA began researching the development of a copper clad aluminum magnesium alloy (“CCAM”) braided material. The aluminum and magnesium alloy has a magnesium content of 0.8% to 1.5% that produces a bimetallic product with higher tensile strength that is used primarily in the production of high quality coaxial radiant electric cables. CCAM is a finer/thinner wire than the bimetallic wire currently produced by TOFA. Beginning in 2008, Shenzhen Tofa Complex Metal Material Co., Ltd., a company located in Shenzhen, China which is owned by Mr. Chuan-Tao Zheng, our President, Chief Executive Officer and Chairman of the Board of Directors (“Shenzhen Tofa”) began producing CCAM braided material, which it periodically sells to TOFA for those of TOFA’s customers that require it. At this time, TOFA does not intend to begin producing CCAM itself.

In 2008, TOFA expanded its product offerings to include CCS wire (which is similar to CCA although the aluminum is replaced by steel). Unlike CCS wire produced using traditional methods, TOFA’s CCS wire is eco-friendly and cost-effective to consumers for use in electronic, auto, home electrical appliances and IT industries. Management estimates that the annual demand for CCS products in China is about 80,000 to 100,000 tons, and the supply is mostly low price, low conductivity electro-plated products that are made using traditional processes. In general, the most significant negative factor impacting the environment in connection with the traditional production of CCS can be traced to the use of toxic materials to polish and weld the materials. The traditional CCS production process uses a significant amount of acid, alkali and highly toxic cyanide, all of which have a negative impact on the environment. Because of this, use of these substances has been widely restricted. In comparison, TOFA’s CCS production process depends completely on mechanical processes to polish copper, peel aluminum strips, coat welds and pull metals together to achieve metallurgical bonding. The entire process is completed without the use of acid, alkali or cyanide, resulting in minimal impact on the environment.

TOFA is confident that its eco-friendly CCS products will gradually replace the existing products in the market in three to five years’ time. At the current time, CCS sales by TOFA amount to less than 5% of its total revenues. However, TOFA is currently developing a high-yield CCS production line that it intends to launch within the next year. The new production line is expected to produce high quality CCS wire on a large scale, with high efficiency, low environmental impact and low cost. As a result, management believes that TOFA’s CCS wire will be an attractive alternative to the current norm – environmentally harmful CCS and electro-plating.

| 8 |

TOFA has focused on these products as its major revenue contributors because of the competitive advantage of its capability to produce CCA power cables and CCA boards and also because of the huge market potential. CCA electricity and power cables have an extremely large potential demand in China. For example, providing CCA electricity/power cables to a building in a city will, on the average, cost US$2.35 per square meter of gross floor area; and in Dalian alone, based on information reported in “The 2010 Real Estate Market Research Report for Dalian” published by the China Real Estate Information Corporation, there are approximately 6 million square meters of gross floor area being constructed every year. This means there is a potential demand of CCA electricity/power cables of US$14 million per annum. In August 2010, TOFA conducted a feasibility study on the replacement of traditional copper power cables by CCA power cables in the residential development projects in selected cities within Liaoning Province, followed by some trial marketing. The market was very receptive of CCA power cables because of their comparable conductivity characteristics to pure copper cables, coupled with the lighter weight and lower price of the products. In the year following the conclusion of this study and marketing effort, TOFA recorded US$47.0 million in sales of its products. Encouraged by these results, the management of TOFA is very confident that CCA cables will be applied to the new buildings and has begun talks with the various relevant government departments in some of the second tier cities like Fushun, Yingkou, Tieling and Anshan in Liaoning Province. TOFA regards this as a starting point as second tier cities, although smaller in scale, are also fast growing, and could shorten the time required to promote and market the CCA cables. Successfully securing orders for CCA cables in these cities will showcase the high qualities of their products to potential customers in other cities in the country, and would hopefully lead to more orders. With a proven track record from these second tier cities, TOFA will then begin to expand its presence in the CCA power cable market in first tier cities.

Employees

TOFA currently employs 137 individuals, all of whom are full time employees.

Suppliers

TOFA obtains all of its raw materials from local copper ribbon manufacturers and aluminum and steel rod factories in China. TOFA enters into purchase contracts with the respective manufacturers or factories for the quantity of a particular metal that it anticipates will be required for production over a two month period. The purchase price of each individual metal closely resembles the price for delivery of the metal in the spot market in the Shanghai Futures Exchange. TOFA usually pays a deposit of about 30% of the purchase price at the time it enters into an order and the remainder is paid within 30 days of acceptance of delivery.

Because of the specific requirements with respect to the quality of the copper belts and aluminum rods, TOFA only sources raw materials from the list of qualified suppliers. There are three to four primary suppliers with whom TOFA has had a long term working relationship and a number of secondary suppliers that are available to fill in on an “as needed” basis. In 2011, TOFA’s major suppliers were:

| Raw Material | Supplier |

Percentage of Material Purchased Annually |

||||

| Copper ribbons | Anhui Yongjie Copper Co. Ltd. | 74 | % | |||

| Shanxi Chunlei Copper Co. Ltd. | 16 | % | ||||

| Aluminum rods | Jiangyin Hengli Electronic Co. Ltd | 86 | % | |||

Additionally, by early 2011, TOFA had replaced all of its existing production machinery with intelligent production machines made by Tongda. This is discussed in further detail below.

| 9 |

Sales and Marketing

TOFA has a sales team of 15 full-time staff to market its products to its customers in both the domestic and the international market. At present, about 80% of its bimetal composite materials are sold in China while the remaining 20% is marketed internationally, primarily in South Korea, Taiwan, Germany and the US. It has targeted reputable enterprises in the telecommunication, electricity and power, home electronic appliances, auto and IT industries to be its preferred clients. TOFA has successfully built up a client base of well-known and respected names. These include local companies and international companies located in the US, Germany, Taiwan and South Korea. TOFA’s diversified customer base has lowered its risk of reliance on a small number of clients to keep the business growing. TOFA’s largest customers in terms of net sales during the last three years were (amounts presented in US$ in thousands):

| Customer Name | 2009 | 2010 | 2011 | |||||||||

| Radio Frequency Systems GMBH | $ | 550 | $ | 2,896 | 6,701 | |||||||

| Jiangsu Hengxin Technology Co., Ltd. | 1,522 | 3,397 | 6,864 | |||||||||

| ShengYi Jianshe Group | 321 | 1,057 | 5,463 | |||||||||

| Hua Tong Technology Ltd. | 2,330 | 1,159 | 5,384 | |||||||||

Unit sales price of TOFA’s CCA products is determined according to a pre-agreed formula (which is equal to the sum of the average copper price for spot delivery on the Shanghai Futures Exchange multiplied by a factor of 30% to 40% (depending on the form of final output) plus the average aluminum price for spot delivery multiplied by a factor of 60% to 70% (again, depending on the form of final output) plus processing fees). This price is exclusive of packaging and transportation costs.

Competition

Based on customer feedback, internal marketing data related to the CCA market in China, our patented technology and expertise as evidenced by our participation as a principal party in the drafting of China’s industrial standards for the use of CCA and CCS wire in the electronic industry in China, we believe that the TOFA name is highly regarded by its customers and throughout the industry in China and recognized as a key player in the composite materials industry in China.

The following table sets forth TOFA’s primary competitors in the various industries where CCA is currently being applied in China, based solely on the experience of TOFA’s management, coupled with periodic discussions with industry experts:

| Industry | Company Name | |

| Telecommunications RF Cable* | Fushi Int’l (Dalian) Bimetal Wires & Cables Co. Ltd. (a subsidiary of Fushi Copperweld Inc.) | |

| Zhangjiagang Liangsheng Composite Bimetal Materials Co. | ||

| Suzhou Nanfang Xinda Bimetal Materials Co. Ltd. | ||

| Home Electrical Appliances** | Zhangjiagang Shingtian Metal Wires Co. Ltd. | |

| Suzhou Nanfang Xinda Bimetal Wires Co. Ltd. | ||

| Fushi Int’l (Dalian) Bimetal Wires & Cables Co. Ltd. | ||

| Electrical Power*** | Fushi Int’l (Dalian) Bimetal Wires & Cables Co. Ltd. |

| * | The total size for the telecommunications market is approximately 20,000 tons per annum, of which about 60% is the RF cable market. |

| ** | The total size of the home electrical appliance market is approximately 10,000 tons per annum. TOFA used to have a more robust presence in the home electrical appliances CCA market; however, because of the lower margin and generally longer credit period afforded to customers in this market, TOFA has begun switching its resources to concentrate on CCA products and market that yield higher returns like the telecommunication and power cables industries. |

| 10 |

| *** | The use of CCA cable for the electrical power industry in China is just beginning with annual demand estimated at 3,000 tons. |

This achievement is the result of extremely strong and aggressive dedication to research and development, as well as the quality of the products that it puts out. TOFA was the first Chinese company to enter the CCA industry in 1997 and its coating and welding processes were awarded the first patent in China’s CCA industry from the State Patent Office. TOFA has since been granted six patents for its CCA technology. No other company in China possesses such patented technology. Additionally, TOFA’s use of the intelligent, composite bimetallic material machinery developed and patented by Tongda for the production of its CCA wire (which is currently unique within China) enhances TOFA’s product and, by extension, its reputation. Further, the fact that it had been one of the principal parties to draft the industrial standards for the CCA wires for use in the electronic industry when such wires were introduced to the local market has also helped TOFA build a recognizable brand name. At present, it is also participating in drafting CCA wire industrial standards for use by all industries in China.

In fact, because of the rather high barrier to entry in terms of the production technologies required, our management believes that there are less than fifty players in the industry in the whole of China and among them, only twenty or so can be considered as having decent productions.

Of the top three or four players, Fushi Copperweld believes it is one of the largest bimetal producer in the world in terms of manufacturing capacity. Fushi has acquired manufacturing plants in the US and the UK, which have resulted in its gaining substantial market share in the international market. Despite having a smaller scale than Fushi Copperweld; TOFA management believes that it is very competitive because of its research and development capability, proprietary technologies and the brand name it has built up.

Research and Development; Intellectual Property Rights

TOFA has placed great emphasis on research and development since its formation in 1997. Having been a pioneer in the R&D of CCA wire from inception, TOFA now seeks to expand its reach by developing superior CCS wire and is exploring the development of CCA and CCS boards to complement its current business. Research and development costs are charged to expense as incurred. These costs mainly consist of remuneration for the staff and material costs. TOFA incurred $213,622 and $127,366 in research and development costs for the years ended December 31, 2011 and 2010, respectively.

TOFA has been granted a total of six patents by the Chinese Government on their CCA wire products. The term of each of these patents runs from September 20, 2009 through September 19, 2019. They include:

| · | Conducting wires used grounding in lightning rods (ZL200520117626.7); |

| · | Ultra high-voltage grant span power transmission cable (ZL200520117631.8); |

| · | Conducting wires used for making braid and plug electronic components (ZL200520117628.6); |

| · | Bearing and trolley wire used for electrified railway (ZL200520117625.2); |

| · | High-voltage power cables of 66KV and below (ZL200520117629.0); and |

| · | Shaped wires used for high and low voltage distribution equipment (ZL200520117635.2). |

TOFA Subsidiaries

In June 2011, TOFA, together with two minority shareholders in TODA, formed Panjin TOFA Cable Co., Ltd. for the purpose of manufacturing CCA. Panjin TOFA is based at New Materials Industrial Park, Yuanlin Village, Chenjia Town, Panshan County, Panjin City, Liaoning Province and began production on June 30, 2011.

| 11 |

In November 2011, TOFA formed Zhaodong TOFA for the purpose of selling CCA. Zhaodong TOFA is currently in the process of renovating its facilities to be located at 2nd West Versailles Apartment, No.1 Runhong, Zhengyang Street, Zhaodong City, Suihua City, Heilongjiang Province and has not begun doing any business. We anticipate that the renovation of the Zhaodong TOFA facility will be completed and operations will commence in June 2012.

Dalian Tongda Equipment Technology Development Co., Ltd.

In 2008, Tongda was incorporated to engage in the research, development, production, manufacturing and distribution of intelligent composite bimetal materials manufacturing equipment. Tongda also provides consultancy services to customers with regard to such production technologies. All bimetallic composite materials production lines manufactured by Tongda employ a number of independent patented technologies that enable fully automated and intelligent control over raw material supply, clad-welding and finished product collection. The entire bimetallic composite material production process is monitored by a programmable logic controller (“PLC”) to ensure coordinated action of the various parts making up the production line. Tongda’s automated bimetallic composite materials production lines are the first of their kind to be introduced and marketed in the PRC.

Products and Services

Tongda produces a series of fully-automated, intelligent composite bimetal materials manufacturing equipment and facilities for the production of CCA wire and CCAM wire of various thicknesses (from 0.04 mm to 17 mm) and CCS wires with diameters less than 1.66 mm. Tongda is researching into production equipment that could produce CCS wires of diameters up to 7.5 mm, which requires more advanced technology to bond the constituent metals, and expects such equipment to be available in first half of 2013. The Tongda composite bimetal materials producing equipment is innovative in China as there was no domestically produced equipment of such kind in the market before. Apart from the automatic, intelligent composite bimetal materials manufacture equipment, Tongda also produces the following stand-alone machines and equipment used during the composite bimetal materials production process;

| · | wire-drawing machines; |

| · | metal feeding devices; |

| · | wire collection devices; |

| · | waste materials pressing machines; |

| · | copper belt connecting devices; |

| · | copper belt buffers; |

| · | inverted cleaning detection devices; |

| · | inverted bare wire devices; and |

| · | hydraulic cooling connecting devices. |

The availability of automated bimetallic composite material production lines and related equipment has made the manufacturing of the composite bimetal materials more cost effective and reduced total production time.

| 12 |

Traditionally, manufacturing of composite bimetallic materials was carried out via a number of discrete tasks - from cleaning of the raw metals, to loading the raw metals onto feeding wheels, to welding the raw metals into one wire, to collection of the finish products. These steps were each done on a separate machine and production was limited by the length of the ribbons and rods that could be input into the various machines. Tongda’s advanced design, which combines a built-in raw material feeding device, intelligent welding device and finished product collection device into one piece of equipment, makes it possible to produce high quality composite bimetal wires continuously. This is a breakthrough in the production mechanism in the industry in China. So, with the use of the intelligent production equipment from Tongda, the very complicated process of composite bimetal material production has become simplified.

When compared to the old generation equipment in Tongda’s internal testing process, the employment of the intelligent production lines from Tongda increases production efficiency by about 33% and lowers material wastage by 3%. Under the traditional system of manufacturing, raw material is lost in the feeding process and during the joining of one batch to the next for a continuous wire. Because of the high precision of the intelligent production lines, the copper ribbons used can be 20% thinner than those to be processed using the old machines. As a result, the material cost and hence the production cost is substantially lower.

The production process is more environmentally friendly. The intelligent design uses a mechanical peeling process to scratch off the outer layer of the aluminum rod, replacing the need to clean the surface of the metals with an alkali solution, thereby eliminating the waste water that would otherwise be generated from the cleaning of the raw materials. There is also a lower level of noise generated using Tongda’s intelligent production equipment when compared to the traditional bimetal materials production equipment.

Employees

Tongda currently employs 41 individuals, all of whom are full time employees.

Suppliers

To minimize the carrying and management costs, Tongda organizes its raw material purchases in such a way to keep inventory to a minimum. It keeps adequate supplies of those parts and raw materials required for the manufacture of two intelligent production lines, which require a delivery lead time of two months and above. With respect to the manufacture of its other machines and products, Tongda generally keeps only a small reserve of parts and raw materials and can easily order the materials required for production as an order comes in to the company. Tongda normally pays a deposit of 30% on signing a purchase order with its suppliers and settles in full when the supplies are received.

In 2011, Tongda’s major suppliers were:

|

Parts/ Raw Material |

Supplier |

Percentage of Material Purchased Annually |

||||

| Steel | Dalian Pengda Steel Material Co Ltd | 68 | % | |||

| Dalian Hongxingiso Steel Material Co Ltd | 30 | % | ||||

| Machinery and Parts | Dalian Weiyun Plastic Machinery Co Ltd | 43 | % | |||

| Dalian Shahekou Xudong Machines | 46 | % | ||||

| Dalian Bosheng Machinery Co Ltd | 11 | % | ||||

Sales and Marketing

Within China, Tongda has taken a very careful approach in choosing its customers for its intelligent bimetal materials production lines to avoid creating more competition within the high margin production area. As a result, a significant majority of these products are intended for the international market, with initial focus on South Korea. In 2010, Tongda entered into an agreement with a distribution agent in South Korea to exclusively market its products in that country. In addition, Tongda provides consultancy services to its South Korean customers, advising them on the overall strategy of their composite materials production and conducting turnkey projects for related production lines and equipment. Tongda plans to expand its overseas presence going forward.

| 13 |

To the extent that Tongda sells its bimetal materials production lines in China, it is anticipated that, with the exception of sales to TOFA, any sales are limited to companies producing CCA solely for use in home electronic appliances (so-called lower margin products) that would not compete with TOFA.

With respect to its other machines, such as its semi automatic bimetal material production equipment and peripheral devices, Tongda sells its products domestically to customers that do not constitute direct competition to TOFA. Sales of such equipment and devices contributes approximately 10% to the revenue of Tongda.

Tongda’s largest customers in terms of net sales since it began producing and selling its products were (amounts presented in US$ in thousands):

| Customer Name | 2009 | 2010 | 2011 | |||||||||

| Yixing Tongxin | $ | 730 | $ | 2,989 | $ | 11 | ||||||

| Zhejiang Detong | - | - | 1,312 | |||||||||

| Changzhou Mingtong | - | 1,014 | ||||||||||

| TOFA | 440 | 341 | - | |||||||||

| Tianjin Wanbo | 745 | 158 | ||||||||||

| Dongguang Zhaohong | - | - | 794 | |||||||||

| Shenzhen TOFA | - | 505 | - | |||||||||

| Saidelong | - | 1,642 | ||||||||||

With respect to intelligent composite bimetal production lines, customers pay a deposit equivalent to 50% of the purchase price on signing of the purchase contract. Another 40% of the purchase price is paid on delivery of the machinery, a further 5% is paid on satisfactory completion of a trial run and the balance is paid three months after installation. On completion of the trial run, a time locking program in the equipment is initiated as safeguard on the collection of the balance of the purchase price as required under the original contract.

Competition

Tongda is the only private corporation in China that possesses the patented technology that it uses in the production of intelligent composite bimetal materials production lines. As a result, management is of the opinion that Tongda is a leader in the business and there is no domestic competition with respect to the production of intelligent composite bimetal materials manufacturing equipment in China.

As we discussed above, with the exception of sales to TOFA, the majority of Tongda’s intelligent composite bimetal production lines are intended for the international market or for lower margin producers of CCA wire. Internationally, we believe that our primary competition is Nexans Deutschland GmbH, a German subsidiary of French cable maker Nexans SA, that produces similar lines of products as our intelligent bimetal materials production equipment with clad welding technology. Fushi Int’l (Dalian) Bimetal Wires & Cables Co. Ltd. uses an intelligent production line licensed from Nexans by Fushi Copperweld, Inc. Outside of this competitor, we are not aware of any products that are currently available using similar intelligent technology.

Research and Development; Intellectual Property Rights

Since its inception in 2008, Tongda has devoted significant resources to the research and development of its hardware and production capabilities, understanding that the development of superior manufacturing was essential to its business strategy. Research and development costs are charged to expense as incurred. These costs mainly consist of remuneration for the staff and material costs. Tongda incurred $85,344 and $44,255 in research and development costs for the years ended December 31, 2011 and 2010, respectively. In the short span of time from incorporation to the present date, Tongda has already been granted ten patents by the Chinese authorities relating its products and production technology. In August 2008, Tongda also received ISO9001:2000 certification. Tongda’s patents include:

| 14 |

| · | Bimetal composite wires efficient production line (ZL200710012349.7) – the term of this patent runs from May 9, 2010 through May 8, 2020; |

| · | Copper ribbon supplier for bimetal composite wires production equipment using clad-welding technology (ZL200720012439.1) – the term of this patent runs from April 16, 2008 through April 15, 2018; |

| · | Bimetal wires blank continuous coated welding gun clamping device (ZL200810010173.6) – the term of this patent runs from May 17, 2010 through May 16, 2020; |

| · | Automatic degreasing device for copper belt used for bimetal composite wires blank coated welding production (ZL200720015302.1) – the term of this patent runs from August 6, 2008 through August 5, 2018; |

| · | Bimetal wires blank vertical molding wheel device (ZL200820010358.2) – the term of this patent runs from November 19, 2008 through November 18, 2018; |

| · | Drive with clutch function in bimetal wires blank coated welding drawing equipment (ZL200820010355.9) – the term of this patent runs from November 19, 2008 through November 18, 2018; |

| · | Bimetal wires blank coated welding equipment rapid replacement of tungsten rod device (ZL200820010414.2) – the term of this patent runs from November 19, 2008 through November 18, 2018; |

| · | Wire surface processor with peeling function (ZL200820199015.5) – the term of this patent runs from October 21, 2009 through October 20, 2019; |

| · | Wire surface treatment device (ZL200820189880.1) – the term of this patent runs from November 4, 2009 through November 3, 2019; and |

| · | Copper belt polishing machines (ZL200920166770.8) – the term of this patent runs from April 14, 2010 through April 13, 2020. |

Government Regulation applicable to TOFA and Tongda

TOFA and Tongda are subject to rules and regulations imposed by a wide range of governmental authorities and are diligent in maintaining an awareness of those rules. Their headquarters and manufacturing facilities are located in the PRC and as such, it is subject to various tax and business governance rules and regulations imposed by the PRC and its political subdivisions. Failure to comply with the various government regulations can have a negative impact on our company; therefore we are diligent in our compliance with these rules and regulations. We are in compliance with all material respects of such laws, regulations, rules, specifications and have obtained all material permits, approvals and registrations relating to human health and safety and the environment. In addition, third parties and governmental agencies in some cases have the power under such laws and regulations to require remediation of environmental conditions and, in the case of governmental agencies, to impose fines and penalties. We make capital expenditures from time to time to stay in compliance with applicable laws and regulations.

| 15 |

In 2011 and 2010, TOFA incurred expenses of $2,011 and $1,846, respectively, to comply with governmental regulations in China and $3,981 and $3,785, respectively, to comply with environmental regulations in China. During the same period, Tongda incurred expenses of $1,031 and $923, respectively, to comply with governmental regulations in China and $1,631 and $1,338, respectively, to comply with environmental regulations in China.

Environmental Compliance

As we conduct our manufacturing activities in China, we are subject to the requirements of PRC environmental laws and regulations on air emission, waste water discharge, solid waste and noise. The major environmental regulations applicable to us include the PRC Environmental Protection Law, the PRC Law on the Prevention and Control of Water Pollution and its Implementation Rules, the PRC Law on the Prevention and Control of Air Pollution and its Implementation Rules, the PRC Law on the Prevention and Control of Solid Waste Pollution, and the PRC Law on the Prevention and Control of Noise Pollution. We aim to comply with environmental laws and regulations and have received our ISO 14001:2004 Environmental Management System Certificate for environmental compliance. The ISO 14001:2004 standard is intended to help companies minimize the environmental impact of the production process. The standard includes a set of internationally accepted specifications for environmental management systems created by the International Organization for Standardization. The standards for certification include three major areas: (1) Management systems - systems development and integration of environmental responsibilities into a company's planning; (2) Operations - consumption of natural resources and energy; and (3) Environmental systems - measuring, assessing, and managing emissions, effluents, and other waste streams.

We do not believe that the costs and compliance with applicable environmental laws materially impact our business. The traditional electro-plating production process is a potential eco-hazard, releasing high levels of pollutants into the atmosphere. In Liaoning province alone, governmental regulators have forced the permanent closure of two metal material producers and the temporary shutdown of 34 more while they search for a way to reduce the level of harmful emissions from their facilities. Seven additional manufacturers have been ordered to reduce their level of emissions. Similar environmental crackdowns are being felt throughout other provinces in China. The Chinese government continues to introduce more stringent environmental regulations for the production of electro-plating with the goal of reducing or eliminating the production of harmful levels of acid and alkali residue, as well as toxic levels of cyanide. In the composite bimetallic material industry, this environmental liability is virtually eliminated. CCA and CCS wire saves a lot of the scarcity of copper resources and the coated welding production process does not pollute the environment.

Additionally, the production process for our intelligent composite bimetal materials manufacturing equipment is more environmentally friendly. The intelligent design uses a mechanical peeling process to scratch off the outer layer of the aluminum rod, replacing the need to clean the surface of the metals with an alkali solution, thereby eliminating the waste water that would otherwise be generated from the cleaning of the raw materials. There is also a lower level of noise generated using Tongda’s intelligent production equipment when compared to the traditional bimetal materials production equipment.

We are not subject to any admonitions, penalties, investigations or inquiries imposed by the environmental regulators, nor are we subject to any claims or legal proceedings to which we are named as defendant for violation of any environmental law or regulation. We do not have any reasonable basis to believe that there is any threatened claim, action or legal proceedings against us that would have a material adverse effect on our business, financial condition or results of operations.

Tax

Pursuant to the Provisional Regulation of China on Value Added Tax (“VAT”) and their implementing rules, all entities and individuals that are engaged in the sale of goods, the provision of repairs and replacement services and the importation of goods in China are generally required to pay VAT at a rate of 17.0% of the gross sales proceeds received, less any deductible VAT already paid or borne by the taxpayer. Further, when exporting goods, the exporter is entitled to a portion of or a full refund of the VAT that it has already paid or borne.

| 16 |

Foreign Currency Exchange

Under the PRC Regulations for the Control of Foreign Exchange (2nd Version), Part III – Control of Foreign Exchange on the Capital Account, which is applicable to us, the RMB is convertible for current account items, including the distribution of dividends, interest payments, trade and service-related foreign exchange transactions. Conversion of RMB for capital account items, such as direct investment, loan, security investment and repatriation of investment, however, is still subject to the approval of the PRC State Administration of Foreign Exchange, or SAFE. Foreign-invested enterprises may only buy, sell and/or remit foreign currencies at those banks authorized to conduct foreign exchange business after providing valid commercial documents and, in the case of capital account item transactions, obtaining approval from the SAFE. Capital investments by foreign-invested enterprises outside of are also subject to limitations, which include approvals by the Ministry of Commerce, the SAFE and the State Reform and Development Commission.

Dividend Distributions

Under the PRC regulations on the Implementation of Foreign-Invested Company Law, foreign-invested enterprises in China may pay dividends only out of their accumulated profits, if any, determined in accordance with the PRC accounting standards and regulations. In addition, a foreign-invested enterprise in China are required to set aside at least 10% of their after-tax profit based on the PRC accounting standards each year to its general reserves until the accumulative amount of such reserves reach 50% of its registered capital. These reserves are not distributable as cash dividends. The board of directors of a foreign-invested enterprise has the discretion to allocate a portion of its after-tax profits to staff welfare and bonus funds, which may not be distributed to equity owners except in the event of liquidation.

Development Strategies for TOFA and Tongda

| 1. | Concentrate on New Products |

Composite bimetallic wires are widely applied in the electricity/power, telecommunication, IT, auto, home electrical and electronic appliances industries; but different applications require very different specifications for the wires. We intend to move into the production of CCA wire for use in power cables. Management believes that we possess the technical expertise to develop, produce and install power cables that would be attractive to current and future clients.

| 2. | Diversify Production into New Materials and Product Lines |

TOFA intends to expand its composite bimetallic wire production of CCS wire. We believe that expansion in this area is an excellent complement to our existing business and will provide us access to international markets, including the US and Europe. Lead time of about 12 months is required for the installation of appropriate facilities before production can commence.

TOFA also intends to develop CCA boards to complement its existing product line. During power transmission, power cables are connected from the source to the end users via a number of transformers. Traditionally, a large number of copper boards are employed in the transformers as connecting bodies. With the development of CCA products, management believes that it would be advantageous to our customers to provide the option to replace heavy, expensive copper boards with lighter, more cost-effective CCA boards. Our employees have the technological know-how to develop attractive CCA boards and we intend to set up production facilities for CCA boards by the end of 2012.

At this time we are unable to estimate the cost associated with the development and expansion of these product lines.

| 17 |

| 3. | Closer Cooperation with Existing Customers |

With the availability of intelligent bimetallic wire production lines from Tongda, TOFA is in a position to offer closer cooperation to its customers. The operating model calls for TOFA to purchase and install Tongda’s intelligent production lines in premises adjacent to select customers who would guarantee a certain order quantity, and the CCA wires produced will all be sold to that customer. The purpose is to secure long term orders from the customers by providing them with guaranteed and timely supply of the CCA products.

| 4. | Further Research and Development |

To maintain its competitive edge, TOFA will continue to develop new products as well as its production technology. Tongda will expand its research into the manufacturing of intelligent production lines for CCS wires and for CCA boards.

| 5. | Expanding Market Share through Acquisitions |

We intend to locate a number of CCA manufacturers with good potential to be targets of acquisitions. Tongda will provide the targets with intelligent CCA production lines and will have them installed in their plants. In exchange, we will acquire a certain percentage of the equity interest, though not necessarily absolute majority, in the target.

Item 1A. Risk Factors.

Our business and an investment in our securities are subject to a variety of risks. You should carefully consider the risks described below before making any investment decision. The following risk factors describe the most significant events, facts or circumstances that we believe could have a material adverse effect upon our business, financial condition, results of operations, ability to implement our business plan, and the market price for our securities. Additional risks not presently known to us or that we currently believe are immaterial may also impair our business operations. Our business could be harmed by any of these risks. In assessing these risks, you should also refer to the other information contained in this Annual Report on Form 10-K, including our consolidated financial statements and related notes.

Risks Related to Our Business

Adverse capital and credit market conditions may significantly affect our ability to meet liquidity needs, access to capital and cost of capital.

The capital and credit markets have been experiencing extreme volatility and disruption in recent months, including, among other things, extreme volatility in securities prices, severely diminished liquidity and credit availability, ratings downgrades of certain investments and declining valuations of others. Governments have taken unprecedented actions intended to address extreme market conditions that have included severely restricted credit and declines in real estate values. In some cases, the markets have exerted downward pressure on availability of liquidity and credit capacity for certain issuers. While currently these conditions have not impaired our ability to utilize our current credit facilities and finance our operations, there can be no assurance that there will not be a further deterioration in financial markets and confidence in major economies such that our ability to access credit markets and finance our operations might be impaired. Adverse market conditions may limit our ability to replace, in a timely manner, maturing liabilities and access the capital necessary to operate and grow our business. As such, we may be forced to delay raising capital or bear an unattractive cost of capital which could decrease our profitability and significantly reduce our financial flexibility. Demand for our products is vulnerable to economic downturns. The worsening of economic condition could result in a decrease in or cancellation of orders for our products. We are unable to predict the duration and severity of the current disruption in financial markets and the global adverse economic conditions and the effect such events might have on our business. Our results of operations, financial condition, cash flows and capital position could be materially adversely affected by disruptions in the financial markets. Further, any decreased collectability of accounts receivable or early termination of sales contracts due to the current deterioration in economic conditions could negatively impact our results of operations.

| 18 |

We may encounter substantial competition in our business and our failure to compete effectively may adversely affect our ability to generate revenue.

The bimetallic industry is becoming increasingly competitive in China. The principal elements of competition in the bimetallic industry are, in our opinion, pricing, payment terms, product availability and quality. Our major competitors with substantially greater resources than us may be better able to successfully endure downturns in our industrial sector. In periods of reduced demand for our products, we can either choose to maintain market share by reducing our selling prices to meet the competition or maintain selling prices, which may sacrifice market share. Sales and overall profitability would be reduced under either scenario. In addition, we cannot assure you that additional competitors will not enter our markets, or that we will be able to compete successfully against existing or new competition.

We may not be able to effectively control and manage our growth.

If our business and markets continue to grow and develop as we expect, it will be necessary for us to finance and manage expansion in an orderly fashion. We may face challenges in managing expanding product offerings and in integrating acquired businesses with our own. Such eventualities will increase demands on our existing management and facilities. Failure to manage this growth and expansion could interrupt or adversely affect our operations, cause production backlogs, longer product development time frames and administrative inefficiencies.

Quarterly operating results may fluctuate due to factors beyond our control, including customer demand and raw materials pricing.

Our quarterly results of operations may fluctuate as a result of a number of factors, including fluctuation in the demand for our products and changes in the price of copper, which directly affects the prices of our products and may influence demand. Quarter-to-quarter comparisons of results of operations have been and will be impacted by the volume of such orders and shipments. In addition, our operating results each quarter could be adversely affected by the following factors, among others, such as variations in the mix of product sales, price changes in response to competitive factors, increases in raw material costs and other significant costs, increases in utility costs (particularly electricity), various types of insurance coverage and interruptions in plant operations. Some uses of our products are subject to seasonality factors which can affect our quarter to quarter results as well.

Fluctuating copper prices impact our business and operating results.