Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - SUNRISE REAL ESTATE GROUP INC | v305526_ex32-2.htm |

| EX-31.2 - EXHIBIT 31.2 - SUNRISE REAL ESTATE GROUP INC | v305526_ex31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - SUNRISE REAL ESTATE GROUP INC | v305526_ex31-1.htm |

| EX-32.1 - EXHIBIT 32.1 - SUNRISE REAL ESTATE GROUP INC | v305526_ex32-1.htm |

| EXCEL - IDEA: XBRL DOCUMENT - SUNRISE REAL ESTATE GROUP INC | Financial_Report.xls |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

For the fiscal year ended: December 31, 2011

¨ TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT

OF 1934

Commission file number: 000-32585

SUNRISE REAL ESTATE GROUP, INC.

(Name of Small Business Issuer in its Charter)

| Texas | 6351 | 75-2713701 | ||

| (State or Other Jurisdiction of Incorporation or Organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

No. 638, Hengfeng Road 25th Fl, Building A

Shanghai, PRC 200070

(Address of Principal Executive Offices) (Zip Code)

Issuer's telephone number: + 86-21-6167-2800

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: Common Stock, $0.01 par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes¨ No x

Check whether the issuer(1) filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the past 12 months (or for such shorter period that the issuer was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yesx No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes x No ¨

Check if there is no disclosure of delinquent filers in response to Item 405 of Regulation S-K is contained in this form, and no disclosure will be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by checkmark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act): Yes¨ No x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer¨ | Accelerated filer¨ | |||

| Non-accelerated filer¨ (Do not check if a smaller reporting company) | Smaller reporting company | x |

The aggregate market value of the common stock held by non-affiliates 12,334,803 shares was approximately $1,356,828, based on the average closing bid and ask price of $0.11 for the Common Stock on June 30, 2011.

The number of shares outstanding of the issuer's Common Stock, $0.01 par value, as of March 22, 2012 was 28,691,925 shares

SUNRISE REAL ESTATE GROUP, INC.

FORM 10-K

TABLE OF CONTENTS

| PART I | ||

| Item 1. | Description of Business | 2 |

| Item 2. | Description of Property | 17 |

| Item 3. | Legal Proceedings | 17 |

| Item 4. | Mine Safety Disclosures | 17 |

| PART II | ||

| Item 5. | Market for Common Equity and Related Stockholder Matters | 18 |

| Item 6. | Selected Financial Data | 18 |

| Item 7. | Management's Discussion and Analysis or Plan of Operation | 18 |

| Item 8. | Financial Statements | 26 |

| Item 9. | Changes In and Disagreements With Accountants on Accounting and Financial Disclosure | 42 |

| Item 9A. | Controls and Procedures | 42 |

| Item 9B. | Other Information | 42 |

| PART III | ||

| Item 10. | Directors, Executive Officers, Promoters, Control Persons and Corporate Governance; Compliance With Section 16(A) of the Exchange Act | 43 |

| Item 11. | Executive Compensation | 47 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 48 |

| Item 13. | Certain Relationships and Related Transactions and Director Independence | 49 |

| Item 14. | Principal Accountant Fees and Services | 50 |

| Item 15. | Exhibits | 51 |

| 1 |

PART I

ITEM 1. DESCRIPTION OF BUSINESS

Corporate History

The principal activities of the Company are real estate development and property brokerage services, real estate marketing services, property leasing services and property management services in the PRC.

Sunrise Real Estate Development Group, Inc. (“CY-SRRE”) was established in the Cayman Islands on April 30, 2004 as a limited liability company. CY-SRRE was wholly owned by Ace Develop Properties Limited, a corporation, (“Ace Develop”), of which Lin Chi-Jung, an individual, is the principal and controlling shareholder. Shanghai Xin Ji Yang Real Estate Consultation Company Limited (“SHXJY”) was established in the People’s Republic of China (the “PRC”) on August 14, 2001 as a limited liability company. SHXJY was originally owned by a Taiwanese company, of which the principal and controlling shareholder was Lin Chi-Jung. On June 8, 2004, all the fully paid up capital of SHXJY was transferred to CY-SRRE. On June 25, 2004 SHXJY and two individuals established a subsidiary, namely, Suzhou Xin Ji Yang Real Estate Consultation Company Limited (“SZXJY”) in the PRC, at which point in time, SHXJY held a 90% equity interest in SZXJY. SRRE and its subsidiaries and branches are sometimes hereinafter collectively referred to as “the Company.”

On August 9, 2005, SHXJY sold a 10% equity interest in SZXJY to a company owned by a director of SZXJY, and transferred a 5% equity interest in SZXJY to CY-SRRE. Following the disposal and the transfer, CY-SRRE effectively held an 80% equity interest in SZXJY. On November 24, 2006, CY-SRRE, SHXJY, a director of SZXJY and a third party established a subsidiary, namely, Suzhou Shang Yang Real Estate Consultation Company Limited (“SZSY”) in the PRC, with CY-SRRE holding a 12.5% equity interest, SHXJY holding a 26% equity interest and the director of SZXJY holding a 12.5% equity interest in SZSY. At the date of incorporation, SRRE and the director of SZXJY entered into a voting agreement that SRRE is entitled to exercise the voting right in respect of his 12.5% equity interest in SZSY. Following that, SRRE effectively holds 51% equity interest in SZSY. On September 24, 2007, CY-SRRE sold a 5% equity interest in SZXJY to a company owned by a director of SZXJY. Following the disposal, CY-SRRE effectively holds 75% equity interest in SZXJY. In January of 2012, SHXJY invested 24% and established a company in Linyi and acquired approximately 103,385 square meters for the purpose of developing into villa-style residential housings. In an agreement with Zhang Shu Qing, a majority shareholder of 51%, we have her 51% voting power and thus effectively have 75% of voting power.

LIN RAY YANG Enterprise Ltd. (“LRY”) was established in the British Virgin Islands on November 13, 2003 as a limited liability company. LRY was owned by Ace Develop, Planet Technology Corporation (“Planet Tech”) and Systems & Technology Corporation (“Systems Tech”). On February 5, 2004, LRY established a wholly owned subsidiary, Shanghai Shang Yang Real Estate Consultation Company Limited (“SHSY”) in the PRC as a limited liability company. On January 10, 2005, LRY and a PRC third party established a subsidiary, Suzhou Gao Feng Hui Property Management Company Limited (“SZGFH”), in the PRC, with LRY holding 80% of the equity interest in SZGFH. On May 8, 2006, LRY acquired 20% of the equity interest in SZGFH from the third party. Following the acquisition, LRY effectively holds 100% of the equity interest in SZGFH. In 2011 we established Wuhan Yuan Yu Long (WHYYL) and had a 49% ownership the purpose of this project company was for a development project in Wuhan.

SRRE was initially incorporated in Texas on October 10, 1996, under the name of Parallax Entertainment, Inc. (“Parallax”). On December 12, 2003, Parallax changed its name to Sunrise Real Estate Development Group, Inc. On April 25, 2006, Sunrise Estate Development Group, Inc. filed Articles of Amendment with the Texas Secretary of State, changing the name of Sunrise Real Estate Development Group, Inc. to Sunrise Real Estate Group, Inc., effective from May 23, 2006.

On August 31, 2004, Sunrise Real Estate Group, Inc. (“SRRE”), CY-SRRE and Lin Chi-Jung, an individual and agent for the beneficial shareholder of CY-SRRE, i.e., Ace Develop, entered into an exchange agreement under which SRRE issued 5,000,000 shares of common stock to the beneficial shareholder or its designees, in exchange for all outstanding capital stock of CY-SRRE. The transaction closed on October 5, 2004. Lin Chi-Jung is Chairman of the Board of Directors of SRRE, the President of CY-SRRE and the principal and controlling shareholder of Ace Develop.

Also on August 31, 2004, SRRE, LRY and Lin Chi-Jung, an individual and agent for beneficial shareholders of LRY, i.e., Ace Develop, Planet Tech and Systems Tech, entered into an exchange agreement under which SRRE issued 10 million shares of common stock to the beneficial shareholders, or their designees, in exchange for all outstanding capital stock of LRY. The transaction was closed on October 5, 2004. Lin Chi-Jung is Chairman of the Board of Directors of SRRE, the President of LRY and the principal and controlling shareholder of Ace Develop. Regarding the 10 million shares of common stock of SRRE issued in this transaction, SRRE issued 8.5 million shares to Ace Develop, 750,000 shares to Planet Tech and 750,000 shares to Systems Tech.

As a result of the acquisition, the former owners of CY-SRRE and LRY hold a majority interest in the combined entity. Generally accepted accounting principles require in certain circumstances that a company whose shareholders retain the majority voting interest in the combined business be treated as the acquirer for financial reporting purposes. Accordingly, the acquisition has been accounted for as a “reverse acquisition” arrangement whereby CY-SRRE and LRY are deemed to have purchased SRRE. However, SRRE remains the legal entity and the Registrant for Securities and Exchange Commission reporting purposes. All shares and per share data prior to the acquisition have been restated to reflect the stock issuance as a recapitalization of CY-SRRE and LRY.

| 2 |

On January 21, 2011, we entered into a Share Purchase Agreement with Good Speed Services Limited (“Good Speed”) to issue 2.5 million shares for US $500,000. This agreement, subject to standard closing terms and conditions, was scheduled to close on or before March 20, 2011. On March 18, an extension was signed between SRRE and Good Speed to extend the closing date to on or before July 5, 2011. On June 24, 2011, we issued 2.5 million shares of common stock to Good Speed and received US $500,000.

On January 22, 2011 we entered into a Share Purchase Agreement with Better Time International Limited (“Better Time”) to issue 2.5 million shares for US $500,000. This agreement, subject to standard closing terms and conditions, was scheduled to close on or before March 20, 2011. On March 16 an extension was signed between SRRE and Better Time to extend the closing date to on or before July 1, 2011. On July 1, 2011, Sunrise and Better Time extended the closing date to on or before September 30, 2011. On September 30, 2011, we issued 2.5 million shares of common stock to Better Time and received US $500,000.

General Business Description

SRRE was incorporated on October 10, 1996 as a Texas corporation and was formerly known as Parallax Entertainment, Inc. SRRE has gone through a series of transactions leading to the completion of a reverse merger on October 5, 2004. Prior to the closing of the exchange agreements described in “Corporate History” above, SRRE was an inactive "shell" company. Following the closing, SRRE, through its two wholly owned subsidiaries, CY-SRRE and LRY, has engaged in the property brokerage services, real estate marketing services, property leasing services and property management services in the PRC.

The Company recognizes that in order to differentiate itself from the market, it should avoid direct competition with large-scale property developers who have their own marketing departments. Our objective is to develop a niche position with marketing alliances with medium size and smaller developers, and become their outsourcing marketing and sales agents.

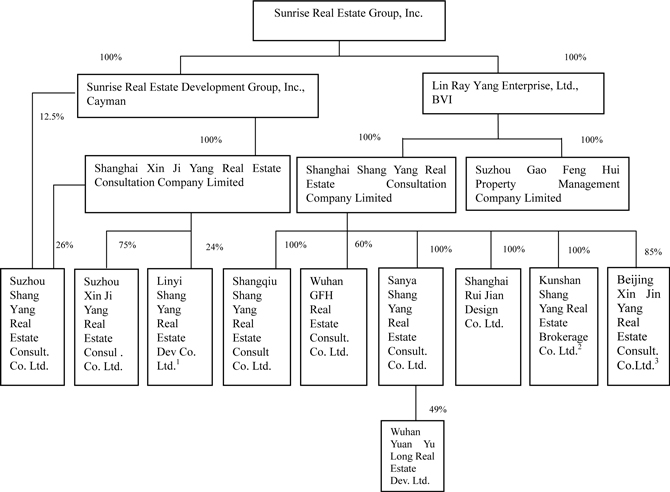

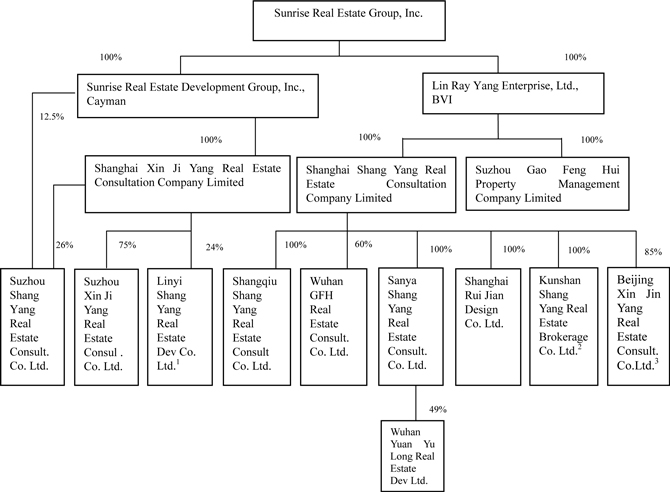

SRRE operates through a tier of wholly owned subsidiaries of Sunrise Real Estate Development Group, Inc., a Cayman Islands corporation ("CY-SRRE") and LIN RAY YANG Enterprise, Ltd., a British Virgin Islands company ("LRY"). Neither CY-SRRE nor LRY have operations but conduct operations in Mainland China through their respective subsidiaries that are based in the PRC. CY-SRRE operates through its wholly owned subsidiary, SHXJY. LRY operates through its two wholly owned subsidiaries, SHSY and SZGFH. SHXJY and SHSY are property agency business earning commission revenue from marketing and sales services to developers. The main business of SZGFH is to render property rental service, buildings management and maintenance service for office buildings. Our company organization chart is as follows:

| 3 |

Figure 1: Company Organization Chart

| 1. Established Linyi Shang Yang Real Estate Development Company Limited in January, 2012. |

| 2. Beijing Xin Jin Yang Real Estate Consultation Company Limited is currently in the process of being dissolved in 2012. |

| 3. Kunshan Shang Yang Real Estate Brokerage Company Limited is currently in the process of being dissolved in 2012. |

Our major business is agency sales, whereby our Chinese subsidiaries contracted with property developers to market and sell their newly developed property units. For these services we earned a commission fee calculated as a percentage of the sales prices. We have focused our sales on the whole China market, especially in secondary cities. To expand our agency business, we have established subsidiaries and branches in Shanghai, Suzhou, Beijing, Yangzhou, Chongqing, Quanjiao ,Hainan, Shangqiu, Chengdu, Wuhan, Kunshan, and Linyi.

During 2005 and 2006, SZGFH entered into leasing agreements with certain buyers of the Sovereign Building underwriting project to lease the properties for them. These leasing agreements on these properties are for 62% of the floor space that was sold to third party buyers. In accordance with the leasing agreements, the owners of the properties can have a rental return of 8.5% and 8.8% per annum for a period of 5 years and 8 years, respectively. In regards to the leasing agreements, we have negotiated with the buyers and have lowered the annual rental return rate for the remaining leasing period from 8.5% for 5 years to 5.8%, and from 8.8% for 8 years to 6%. As of December 31, 2011, 68% of the buyers agreed upon the lowered rate and 25% of the buyers agreed to cancel the leasing agreements. The leasing period started in the second quarter of 2006, and the Company has the right to sublease the leased properties to cover these lease commitments in the leasing period. As of December 31, 2011, 104 sub-leasing agreements have been signed and the area of these sub-leasing agreements represented 67% of the total area with these lease commitments.

| 4 |

With a relatively short history and smaller capital base, we recognize that in order to differentiate ourselves from the market, we need to avoid direct competition with large-scale property developers, who have their own marketing departments. We plan to utilize our professional experience to carve a niche and position by developing marketing alliances with medium size and smaller developers. This strategic plan is designed to expand our activities beyond our existing revenue base, enabling us to assume higher investment risk and giving us flexibility in collaborating with partnering developers. The plan is aimed at improving our capital structure, diversifying our revenue base, creating higher values and equity returns.

In the past eleven years, we have established a reputation as a sales and marketing agency for new projects. With our accumulated expertise and experience, we intend to take a more aggressive role by participating in property investments. We plan to select property developers with outstanding qualifications as our strategic partners, and continue to build strength in design, planning, positioning and marketing services. Beginning 2012, we are developing our first development project in Wuhan and Linyi and have started the initial construction in the first quarter of 2012.

Business Activities

Our main operating subsidiaries, SHXJY and SHSY, have engaged in sales and marketing agency work for newly built property units. We also have developed a good network of landowners and earned the trust of developers, allowing us to explore opportunities in property investments.

In order to build a cushion against the cyclical nature of the real estate industry and have a more diversified revenue base, we established another operating subsidiary, SZGFH, to deal with property management and rental operations.

While our main operation is in agency sales, we are constantly seeking opportunities to branch out into real estate development. While we continue our efforts there are no assurance we will be able to obtain any development projects.

Commission Based Services

Commission based services refer to marketing and sales agency operations, which provide the following services:

a. Integrated Marketing Planning

b. Advertising Planning & Execution

c. Sales Planning and Execution

In this type of business, we sign a marketing and sales agency agreement with property developers to undertake the marketing and sales activities of a specific project. The scope of service varies according to clients' needs; it could be a full package of all the above services, a combination of any two of the above services or any single service.

A major part of our existing revenue comes from commission-based services. We secure these projects via bidding or direct appointments. As a result of our relationships with existing clients and our sales track record, we have secured a number of cases from prior clients on subsequent phases of projects.

Normally, before a developer retains us, we will evaluate and determine the Average Sales Value of a project. This value will be proposed to the developer, and the parties will determine and agree on an Average Sales Value as the basis of our agency agreement. The actual sales price of the project is generally priced higher than the Average Sales Value depending on market conditions. On average, we have been to sell the property at a small premium over Average Sales Value.

Our normal commission structure is a combination of the following:

a) Base Commission of 1.0% - 1.5% based on the Average sales value.

b) Surplus Commission of 10% - 30% based on the difference between Average Sales Value and actual sales price.

Our wholly owned subsidiaries, SHXJY and SHSY, engage in this sales and marketing phase of our business.

Real Estate Development

In mid 2011, we established a project company in Wuhan where we have 49% stake. During the fourth quarter of 2011, the project company was in the process of acquiring land and obtaining the appropriate license and certificate for the development project. In the first quarter of 2012, we began its initial construction. The land is approximately 27,950 square meters with an estimated development period of three years.. Proceeds from sales will fund the constructions of subsequent phases and we are currently in the process of applying for bank loans and other forms of funding, however, there are no assurance we will be able to obtain future financings.

| 5 |

In January 2012, we established Linyi Shang Yang Real Estate Development (“LYSY”) with 24% stake in the company. During the first quarter of 2012, we acquired approximately 103,385 square meters for the purpose of developing villa-style residential housing. Proceeds from sales will fund the constructions of subsequent phases and we are currently in the process of applying for bank loans and other forms of funding, however, there are no assurances we will be able to obtain future financings.

Mainland China's Property Sector

The industry's macro environment is opening up, and the property sector is gradually developing to be a more regulated market. Stable economic growth provides a solid and secure base for investment returns in the property sector.

GDP Growth of PRC for the period of 2007 through 2011

| GDP GROWTH | ||||||

| 2007 | 11.4 | % | ||||

| 2008 | 9.0 | % | ||||

| 2009 | 8.7 | % | ||||

| 2010 | 10.3 | % | ||||

| 2011 | 9.2 | % | ||||

| Source: National Bureau of Statistics of China | ||||||

Government regulation

On November 5, 2008, the State Council announced a two-year economic stimulus plan involving a total investment of RMB 4 trillion. The stimulus plan, which the State Council announced at a general meeting, is called the Ten Measures to Further Expand Domestic Demand and Promote Steady Economic Development (the Ten Measures). In the first measure, the government affirms its commitment to subsidizing low-rent housing, renovating poor and imperiled housing in rural areas, and providing housing for nomads. The National Development and Reform Commission (NDRC) announced on December 18, 2008, that the central government has distributed RMB10 billion for the construction of affordable housing.

The State Taxation Administration issued the Regulation of Land Value-added Tax Clearing and Administrating in May 2009, effective on June 1, 2009. It requires the developers to clear the land value-added tax, which have completed development projects and have finished sale, or have sold development projects under constructed, or have transferred the land use right to others.

On May 27 2009, the Chinese government issued the policy “Notice of the Fix Asset Investment Ratio” stating that economical housings and residential housing’s must provide at least 20% of the purchase price before bank loans. Other real estate project’s minimum payment, not including bank loans, shall be 30%. This is a decrease from the 35% minimum required since 2004 and a drop in level back in 1996. This policy signifies the government loosening of the real estate sector.

The Ministry of Finance, Ministry of Land and Resources, Ministry of Supervision, the Central Government, and five other agencies announced in “Notice Regarding to Improve Upon Land Sale and Receivable Management,” to increase the initial payment of land purchases to 50% of the purchase price and the entire purchase price must be paid in full within the year in Dec 2009. Prior to the increase, the increase, the initial payment was around 20% to 30%.

On January 1, 2010, the Ministry of Finance and the State Administration of Taxation re-imposed the business tax on total proceeds from the resale of certain residential properties held for less than five years. The China Banking Regulatory Authority withdrew its earlier policy and emphasized the minimum 40% down payment requirement for mortgages for second properties. On March 8, 2010, the Ministry of Land and Resources issued a circular to further strengthen the supervision on land supply, requiring a real estate developer to pay at least 50% of the land premium within one month and 100% within one year after the land use right contract is executed. On April 17, 2010, the State Council issued the Circular on Firmly Restraining Soaring Housing Prices in Certain Cities. According to this circular,

| • | A Down payment must be no less than 30% of the purchase price for first self-use housing unit purchases by a family with a gross construction area of more than 90 square meters.; |

| • | The minimum down payment for the second housing unit purchased by a family is increased from 40% to 50% and the loan interest rate must be no less than 110% of benchmark lending interest rate; |

| • | Down payment for the third or more housing unit purchased by any family and the loan interest rate must be further increased significantly based on the rate for the first and second housing units, as determined by commercial banks based on their assessment of the risks; |

| • | Commercial banks may suspend extending loans to families for their purchases of the third or more housing units in regions where commercial housing unit prices are too high or have risen too fast or supply of housing units is insufficient. The banks may also suspend extending loans to individuals for their purchase of housing units outside of their registered residence if they cannot furnish evidence of their tax or social insurance premium payment for at least one year locally in the region where the subject housing units are located; and |

| • | Local governments are allowed to limit the total number of housing units one can purchase in certain period in light of the local situation. |

| 6 |

On January 10th, 2010, the government established a notice of 11 measures to strengthen management of the real estate market to address the rising real estate prices. The measures call for an increasing supply of low-cost houses for low-income families and common residential houses, encouraging reasonably priced house buying while limiting purchases for speculation and investment, strengthening real estate project loan risk management and market supervision, speeding up construction of residential housing projects for low-income households, and specifying responsibilities of local governments.

Such efforts by the government to slow down property price appreciation may reduce the activities in the real estate market and decrease real estate transaction volume, and prevent developers from raising capital they need or increase their costs to start new projects. There are no assurances that the PRC government will not adopt new measures in the future that may result in lower growth rates in the real estate industry. Frequent changes in government policies may also create uncertainty that could discourage investment in real estate. Our business may be materially and adversely affected as a result of decreased transaction volumes or real estate prices that may result from government policies.

In January 2011, the State Council released eight new measures to put downward pressure on property prices by:

1) Requiring local governments to set housing price targets in proportion with local income levels for 2011;

2) Requiring a business tax for housing sales within 5 years of purchase must be levied on total sales value;

properties;

3) Strengthening the management of land supply for housing

4) Imposing purchase restrictions in all large- & medium-sized cities. Families already owning a residential property are restricted to buy only one more, while those already owning two or more properties are prohibited to purchase additional properties;

5) Accelerating the construction of social security residential housings;

6) Providing that the down payment ratio for second-home purchases must not be less than 60%, up from 50%, with an interest rate at least 1.1 times of the benchmark rate;

7) Improving guidance for media's housing market coverage;

8) Providing for implementation & accountability for local governments over the housing price control targets.

In May 2011, the National Development and Reform Commission (“NDRC”) began the “one house, one price” policy which requires developers to enhance its disclosure of the residential properties’ offering prices and available supply volume. This policy is designed to prevent developers from posting false supply volume and prices to fuel speculative price volatility.

In July 2011, the China’s State Council declared that it will continue to implement tightening policies and expand the housing purchase restrictions to second and third-tier cities.

Environmental matters

There is a growing concern in regards to the global warming issues affecting the world today. The changing weather patterns and abnormal conditions may affect the construction and logistics of developers and this may indirectly cause inverse effect to our operation. Extreme weather conditions may delay in construction of properties; this then may delay the sale of these properties and therefore delaying our future revenue stream.

| 7 |

Employees

As of December 31, 2011, we had the following number of employees:

| Employees | ||

| SRRE | ||

| Administration Dept. | 1 | |

| Accounting Dept. | 2 | |

| Investor Relations Dept. | 2 | |

| SHXJY | ||

| Administration Dept. | 17 | |

| Accounting Dept. | 2 | |

| Research & Development Dept. | 5 | |

| Marketing Dept. | 12 | |

| Chongqing Branch of SHXJY | ||

| Accounting Dept. | 1 | |

| Marketing Dept. | 4 | |

| SZXJY | ||

| Administration Dept. | 11 | |

| Accounting Dept. | 3 | |

| Research & Development Dept. | 9 | |

| Advertising & Communication Planning Dept. | 5 | |

| Marketing Dept. | 48 | |

| SZSY | ||

| Marketing Dept. | 28 | |

| SZXJYB | ||

| Marketing Dept. | 7 | |

| SHSY | ||

| Administration Dept. | 9 | |

| Accounting Dept. | 3 | |

| Marketing Dept. | 1 | |

| SYSY | ||

| Marketing Dept. | 14 | |

| SZGFH | ||

| Administration Dept. | 2 | |

| Accounting Dept. | 3 | |

| Marketing Dept. | 4 | |

| SQSY | ||

| Marketing Dept. | 7 | |

| WHGFH | ||

| Marketing Dept. | 1 | |

| SHRJ | ||

| Administration Dept. | 1 | |

| Design Dept. | 9 | |

| Total | 211 |

None of our employees are represented by a labor union or bound by a collective bargaining unit. We believe that our relationship with its employees is satisfactory.

| 8 |

ITEM 1A. RISK FACTORS

RISK FACTORS

SRRE has identified a number of risk factors faced by the Company. These factors, among others, may cause actual results, events or performance to differ materially from those expressed in this 10-K or in press releases or other public disclosures. You should be aware of the existence of these factors.

RISKS RELATING TO THE GROUP

SRRE is a holding company and depends on its subsidiaries’ cash flows to meet its obligations.

SRRE is a holding company, and it conducts all of its operations through its subsidiaries. As a result, its ability to meet any obligations depends upon its subsidiaries’ cash flows and payment of funds as dividends, loans, advances or other payments. In addition, the payment of dividends or the making of loans, advances or other payments to SRRE may be subject to regulatory or contractual restrictions.

Our invoicing for commissions may be delayed.

Generally, we recognize our commission revenues after the contracts signed with developers are completed and confirmations are received from the developers. However, sometimes we do not recognize income even when we have rendered our services for any of the following reasons:

| a. | The developers have not received payments from potential purchasers who have promised to pay the outstanding sum by cash; |

| b. | The purchasers, who need to obtain mortgage financing to pay the outstanding balance due, are unable to obtain the necessary financing from their banks; |

| c. | Banks are sometimes unwilling to grant the necessary bridge loan to the developers in time due to the developers’ relatively low credit rating; |

| d. | The developers tend to be in arrears with sales commissions; therefore, do not grant confirmation to us to be able to invoice them accordingly. |

Development of new business may stretch our cash flow and strain our operation efficiency.

Business expansion and the need to integrate operations arising from the expansion may place a significant strain on our managerial, operational and financial resources, and will further contribute to a need to increase in our financial needs.

Risks associated with a Guaranteed Rental Return Promotion.

During the year of 2005 and 2006, SZGFH entered into leasing agreements with certain buyers of the Sovereign Building underwriting project to lease the properties for them. These leasing agreements on these properties are for 62% of the floor space that was sold to third party buyers. In accordance with the leasing agreements, the owners of the properties can have a rental return of 8.5% and 8.8% per annum for a period of 5 years and 8 years, respectively. In regards to the leasing agreements, we have negotiated with the buyers and have lowered the annual rental return rate for the remaining leasing period from 8.5% for 5 years to 5.8%, and from 8.8% for 8 years to 6%. As of December 31, 2011, 68% of the buyers agreed upon the lowered rate, 7% of the buyers did not agreed to a lowered rate and 25% of the buyers agreed to cancel the leasing agreements. The leasing period started in the second quarter, 2006, and the Company has the right to sublease the leased properties to cover these lease commitments in the leasing period.

We are continuing to promote this package. The return is guaranteed by SZGFH, whereby SZGFH’s principal activities are real estate leasing and property management services. However, we may not successfully sublease the targeted properties at prices higher than what we committed in the promotional package. Our failure to do so could adversely affect our financial condition.

Our acquisition of new property may involve risks.

These acquisitions involve several risks including, but not limited to, the following:

a. The acquired properties may not perform as well as we expected or ever become profitable.

b. Improvements to the properties may ultimately cost significantly more than we had originally estimated.

Additional acquisitions might harm our business.

As part of our business strategy, we may seek to acquire or invest in additional businesses, products, services or technologies that we think could complement or expand our business. If we identify an appropriate acquisition opportunity, we might be unable to negotiate the terms of that acquisition successfully, finance it, or integrate it into our existing business and operations. We may also be unable to select, manage or absorb any future acquisitions successfully. Furthermore, the negotiation of potential acquisitions, as well as the integration of an acquired business, would divert management time and other resources. We may have to use a substantial portion of our available cash to consummate an acquisition. If we complete acquisitions through exchange of our securities, our shareholders could suffer significant dilution. In addition, we cannot assure you that any particular acquisition, even if successfully completed, will ultimately benefit our business.

| 9 |

Our real estate investments are subject to numerous risks.

We are subject to risks that generally relate to investments in real estate. The investment returns available from equity investments in real estate depend in large part on the amount of income earned and capital appreciation generated by the related properties, as well as the expenses incurred. In addition, a variety of other factors affect income from properties and real estate values, including governmental regulations, insurance, zoning, tax and eminent domain laws, interest rate levels and the availability of financing. For example, new or existing real estate zoning or tax laws can make it more expensive and/or time-consuming to develop real property or expand, modify or renovate properties. When interest rates increase, the cost of acquiring, developing, expanding or renovating real property increases and real property values may decrease as the number of potential buyers decrease. Similarly, as financing becomes less available, it becomes more difficult both to acquire and to sell real property. Finally, governments can, under eminent domain laws, take real property. Sometimes this taking is for less compensation than the owner believes the property is worth. Any of these factors could have a material adverse impact on results of our operations or financial condition. In addition, equity real estate investments, such as the investments we hold and any additional properties that we may acquire, are relatively difficult to sell quickly. If our properties do not generate sufficient revenue to meet operating expenses, including debt servicing and capital expenditures, our income will be reduced.

Competition, economic conditions and similar factors affecting us, and the real estate industry in general, could affect our performance.

Our properties and business are subject to all operating risks common to the real estate industry. These risks include:

a. Adverse effects of general and local economic conditions;

b. Increases in operating costs attributable to inflation and other factors; and

c. Overbuilding in certain property sectors.

These factors could adversely affect our revenues, profitability and results of operations.

Our business is susceptible to fluctuations in the real estate market of China, especially in certain areas of eastern China where a significant portion of our operations are concentrated, which may adversely affect our revenues and results of operations.

We conduct our real estate services business primarily in China. Our business depends substantially on the conditions of the PRC real estate market. Demand for private residential real estate in China has grown rapidly in the recent decade but such growth is often coupled with volatility in market conditions and fluctuation in real estate prices. Fluctuations of supply and demand in China’s real estate market are caused by economic, social, political and other factors. To the extent fluctuations in the real estate market adversely affect real estate transaction volumes or prices, our financial condition and results of operations may be materially and adversely affected.

As a significant portion of our operations is concentrated in Shanghai and Jiangsu Province, any decrease in demand or real estate prices or any other adverse developments in these regions may materially and adversely affect our total real estate transaction volumes and average selling prices, which may in turn adversely affect our revenues and results of operations. These economic uncertainties involve, among other things, conditions of supply and demand in local markets and changes in consumer confidence and income, employment levels, increase in mortgage interest rates and government regulations. These risks and uncertainties could periodically have an adverse effect on consumer demand for and the pricing of our homes, which could cause our operating revenues to decline. In addition, builders are subject to various risks, many of them outside the control of the homebuilder including competitive overbuilding, availability and cost of building lots, materials and labor, adverse weather conditions, cost overruns, changes in government regulations, and increases in real estate taxes and other local government fees. A reduction in our revenues could in turn negatively affect the market price of our securities.

Our business may be materially and adversely affected by government measures aimed at China’s real estate industry.

The real estate industry in China is subject to government regulations. Until 2009, the real estate markets in a number of major cities in China had experienced rapid and significant growth. Before the global economic crisis hit all the major economies worldwide in 2009, the PRC government had adopted a series of measures to restrain what it perceived as unsustainable growth in the real estate market. From 2003 to 2011, the PRC government introduced a series of specific administrative and credit-control measures including, but not limited to, setting minimum down payment requirements for residential and commercial real estate transactions, limiting availability of mortgage loans, and tightening governmental approval process for certain real estate transactions.

In cities such as Beijing and Shanghai, we have seen the effects of such policies and regulatory measures. The sales volumes for real properties in Beijing and Shanghai decreased significantly after the policy change. The sale prices for certain properties in such cities also weakened. The PRC government’s policy and regulatory measures on the PRC real estate sector could adversely affect the property purchasers’ ability to obtain mortgage financing or significantly increase the cost of mortgage financing and reduce market demand for properties. These factors may materially and adversely affect our business, financial condition, results of operations and prospects.

| 10 |

Despite the recent government measures aimed at maintaining the long-term stability of the real estate market, we cannot assure you that the PRC government will not continue to adopt new measures in the future that may result in short-term downward adjustments and uncertainty in the real estate market.

Our business may be materially and adversely affected as a result of decreased transaction volumes or real estate prices that may follow these adjustments or market uncertainty.

We operate in a highly competitive environment.

Our competitors may be able to adapt more quickly to changes in customer needs or to devote greater resources than we can to developing and expanding our services. Such competitors could also attempt to increase their presence in our markets by forming strategic alliances with other competitors, by offering new or improved services or by increasing their efforts to gain and retain market share through competitive pricing. As the market for our services matures, price competition and penetration into the market will intensify. Such competition may adversely affect our gross profits, margins and results of operations. There can be no assurance that we will be able to compete successfully with existing or new competitors.

We may be unable to effectively manage our growth.

We will need to manage our growth effectively, which may entail devising and effectively implementing business and integration plans, training and managing our growing workforce, managing our costs, and implementing adequate control and reporting systems in a timely manner. We may not be able to successfully manage our growth or to integrate and assimilate any acquired business operations. Our failure to do so could affect our success in executing our business plan and adversely affect our revenues, profitability and results of operations.

If we fail to successfully manage our planned expansion of operations, our growth prospects will be diminished and our operating expenses could exceed budgeted amounts.

Our ability to offer our services in an evolving market requires an effective planning and management process. We have expanded our operations rapidly since inception, and we intend to continue to expand them in the foreseeable future. This rapid growth places significant demand on our managerial and operational resources and our internal training capabilities. In addition, we have hired a significant number of employees and plan to further increase our total work force. This growth will continue to substantially burden our management team. To manage growth effectively, we must:

a. Implement and improve our operational, financial and other systems, procedures and controls on a timely basis.

b. Expand, train and manage our workforce, particularly our sales and marketing and support organizations.

We cannot be certain that our systems, procedures and controls will be adequate to support our current or future operations or that our management will be able to handle such expansion and still achieve the execution necessary to meet our growth expectations. Failure to manage our growth effectively could diminish our growth prospects and could result in lost opportunities as well as operating expenses exceeding the amount budgeted.

We may be unable to maintain internal funds or obtain financing or renew credit facilities in the future.

Adequate financing is one of the major factors, which can affect our ability to execute our business plan in this regard. We finance our business mainly through internal funds, bank loans or raising equity funds. There is no guarantee that we will always have internal funds available for future developments or we will not experience difficulties in obtaining financing and renewing credit facilities granted by financial institutions in the future. In addition, there may be a delay in equity fundraising activities. Although in 2011 we issued a total of 5,000,000 shares for an aggregate of $1,000,000 to two investors, our access to obtain debt or equity financing depends on the banks' willingness to lend and on conditions in the capital markets, and we may not be able to secure additional sources of financing on commercially acceptable terms, if at all.

We may need to raise additional capital that may not be available on terms favorable to us, if at all.

We may need to raise additional capital in the future, and we cannot be certain that we will be able to obtain additional financing on favorable terms, if at all. If we cannot raise additional capital on acceptable terms, we may not be able to develop or enhance our services, take advantage of future opportunities or respond to competitive pressures or unanticipated requirements. To fully realize our business objectives and potential, we may require additional financing. We cannot be sure that we will be able to secure the financing we will require, or that it will be available on favorable terms. If we are unable to obtain any necessary additional financing, we will be required to substantially curtail our approach to implementing our business objectives. Additional financing may be debt, equity or a combination of debt and equity. If equity is used, it could result in significant dilution to our shareholders.

Our operations and growth prospects may be significantly impeded if we are unable to retain our key personnel or attract additional key personnel, particularly since experienced personnel and new skilled personnel are in short supply.

Competition for key personnel is intense. As a small company, our success depends on the service of our executive officers, and other skilled managerial and technical personnel, and our ability to attract, hire, train and retain personnel. There is always the possibility that certain of our key personnel may terminate their employment with us to work for one of our competitors at any time for any reason. There can be no assurance that we will be successful in attracting and retaining key personnel. The loss of services of one or more key personnel could have a material adverse effect on us and would materially impede the operation and growth of our business.

| 11 |

If our partnering developers experience financial or other difficulties, our business and revenues could be adversely affected.

As a service-based company, we greatly depend on the working relationships and agency contracts with its partnering developers. We are exposed to the risks that our partnering developers may experience financial or other difficulties, which may affect their ability or will to carry out any existing development projects or resell contracts, thus delaying or canceling the fulfillment of their agency contracts with us. Any of these factors could adversely affect our revenues, profitability and results of operations.

Our partnering developers are subject to extensive government regulation which could make it difficult for them to obtain adequate funding or additional funding. Various PRC regulations restrict developers’ ability to raise capital through external financings and other methods, including, but not limited to, the following:

| · | developers cannot pre-sell uncompleted residential units in a project prior to achieving certain development milestones specified in related regulations; |

| · | PRC banks are prohibited from extending loans to real estate companies to fund the purchase of land use rights; |

| · | developers cannot borrow from a PRC bank for a particular project unless we fund at least 35% of the total investment amount of that project using our own capital; |

| · | developers cannot borrow from a PRC bank for a particular project if we do not obtain the land use right certificate for that project; |

| · | property developers are strictly prohibited from using the proceeds from a loan obtained from a local bank to fund property developments outside of the region where the bank is located; and |

| · | PRC banks are prohibited from accepting properties that have been vacant for more than three years as collateral for a loan. |

If we fail to establish and maintain strategic relationships, the market acceptance of our services, and our profitability, may suffer.

To offer services to a larger customer base, our direct sales force depends on strategic partnerships, marketing alliances, and partnering developers to obtain customer leads and referrals. If we are unable to maintain our existing strategic relationships or fail to enter into additional strategic relationships, we will have to devote substantially more resources to the marketing of our services. We would also lose anticipated customer introductions and co-marketing benefits. Our success depends in part on the success of our strategic partners and their ability to market our services successfully. In addition, our strategic partners may not regard us as significant for their own businesses. Therefore, they could reduce their commitment to us or terminate their respective relationships with us, pursue other partnerships or relationships, or attempt to develop or acquire services that compete with our services. Even if we succeed in establishing these relationships, they may not result in additional customers or revenues.

We are subject to the risks associated with projects operated through joint ventures.

Some of our projects are operated through joint ventures in which we have controlling interests. We may enter into similar joint ventures in the future. Any joint venture investment involves risks such as the possibility that the joint venture partner may seek relief under Chinese insolvency laws, or have economic or business interests or goals that are inconsistent with our business interests or goals. While the bankruptcy or insolvency of our joint venture partner generally should not disrupt the operations of the joint venture, we could be forced to purchase the partner’s interest in the joint venture, or the interest could be sold to a third party. Additionally, we may enter into joint ventures in the future in which we have non-controlling interests. If we do not have control over a joint venture, the value of our investment may be affected adversely by a third party that may have different goals and capabilities than ours. It may also be difficult for us to exit a joint venture that we do not control after an impasse. In addition, a joint venture partner may be unable to meet its economic or other obligations, and we may be required to fulfill those obligations.

We are subject to the risks associated with projects operated through joint ventures.

Some of our projects are operated through joint ventures in which we have controlling interests. We may enter into similar joint ventures in the future. Any joint venture investment involves risks such as the possibility that the joint venture partner may seek relief under federal or state insolvency laws, or have economic or business interests or goals that are inconsistent with our business interests or goals. While the bankruptcy or insolvency of our joint venture partner generally should not disrupt the operations of the joint venture, we could be forced to purchase the partner’s interest in the joint venture, or the interest could be sold to a third party. Additionally, we may enter into joint ventures in the future in which we have non-controlling interests. If we do not have control over a joint venture, the value of our investment may be affected adversely by a third party that may have different goals and capabilities than ours. It may also be difficult for us to exit a joint venture that we do not control after an impasse. In addition, a joint venture partner may be unable to meet its economic or other obligations, and we may be required to fulfill those obligations.

| 12 |

We are subject to risks relating to acts of God, terrorist activity and war.

Our operating income may be reduced by acts of God, such as natural disasters or acts of terror, in locations where we own and/or operate significant properties and areas from which we draw customers and partnering developers. Some types of losses, such as from earthquake, hurricane, terrorism and environmental hazards, may be either uninsurable or too expensive to justify insuring against. Should an uninsured loss or a loss in excess of insured limits occur, we could lose all or a portion of the capital we have invested in any particular property, as well as any anticipated future revenue from such property. In that event, we might nevertheless remain obligated for any mortgage debt or other financial obligations related to the property. Similarly, wars (including the potential for war), terrorist activity (including threats of terrorist activity), political unrest and other forms of civil strife as well as geopolitical uncertainty have caused in the past, and may cause in the future, our results to differ materially from anticipated results.

We have limited business insurance coverage in China.

The insurance industry in China is still at an early stage of development. Insurance companies in China offer limited business insurance products. As a result, we do not have any business liability or disruption insurance coverage for our operations in China. Any business disruption, litigation or natural disaster might result in substantial costs and diversion of resources.

We may be affected by global climate change or by legal, regulatory, or market responses to such change.

There is a growing concern in regards to the global warming issues affecting the world today. The changing weather patterns and abnormal conditions may affect the construction and logistics of developers and this may indirectly cause inverse effect to our operation. Extreme weather conditions may delay in construction of properties; this then may delay the sale of these properties and therefore delaying our future revenue stream. There may be regulations in manufacturing materials for property construction and new building codes in response to global warming that may delay construction and/or create further expenses to the developers. These possible changes may indirectly affect our business.

Our real estate development operating results may not achieve our goals.

As there are many variables to developing a real estate project, we face the risk of running out of funds mid construction and may have to delay or be unable to continue developing the project. We may also run into market downturn and not be able to sell any of the housings we’ve developed. If any of the above happens, we may face an extreme cash shortage and will directly affect our business.

RISKS RELATING TO OUR SECURITIES

Our controlling shareholders could take actions that are not in the public shareholders’ best interests.

As of March 31, 2012, Ace Develop directly controls 15.7% of our outstanding common stock and Lin Chi-Jung, our Chairman, is the principal and controlling shareholder of Ace Develop. As of March 31, 2012, Robert Lin Investments directly controls 15.72% of our outstanding common stock and Lin Chao Chun, one of our directors, is the principal and controlling shareholder of Robert Lin Investments. Accordingly, pursuant to our Articles of Incorporation and bylaws, Ace Develop and Lin Chi-Jung, and Robert Lin Investments and Lin Chao Chun, by virtue of their controlling ownership of share interests, will be able to exercise substantial influence over our business by directly or indirectly voting at either shareholders meetings or the board of directors meetings in matters of significance to us and our public shareholders, including matters relating to:

a. Election of directors and officers;

b. The amount and timing of dividends and other distributions;

c. Acquisition of or merger with another company; and

d. Any proposed amendments to our Articles of Incorporation.

Future sales of our common stock could adversely affect our stock price.

If our shareholders sell substantial amounts of our common stock in the public market, the market price of our common stock could be adversely affected. In addition, the sale of these shares could impair our ability to raise capital through the sale of additional equity securities.

| 13 |

We are listed on the OTCQB, which can be a volatile market.

Our common stock is quoted on the OTCQB, a quotation system for equity securities. It is a more limited trading market than the Nasdaq Capital Market, and timely and accurate quotations of the price of our common stock may not always be available. Investors may expect trading volume to be low in such a market. Consequently, the activity of only a few shares may affect the market and may result in wide swings in price and in volume.

We may be subject to exchange rate fluctuations.

A majority of our revenues are received, and a majority of our operating costs are incurred, in Renminbi. Because our financial statements are presented in U.S. Dollars, any significant fluctuation in the currency exchange rates between the Renminbi and the U.S. Dollar will affect our reported results of operations. We do not currently engage in currency-hedging transactions.

Trading of our common stock is limited, which may make it difficult for investors to sell their shares at times and prices that investors feel are appropriate.

Trading of our common stock has been extremely limited. This adversely effects the liquidity of our common stock, not only in terms of the number of shares that can be bought and sold at a given price, but also through delays in the timing of transactions and reduction in security analysts’ and the media’s coverage of us. This may result in lower prices for our common stock than might otherwise be obtained and could also result in a larger spread between the bid and asked prices for our common stock.

There is a limited market for our common stock and an active trading market for our common stock may never develop.

Trading in our common stock has been limited and has been characterized by wide fluctuations in trading prices, due to many factors that may have little to do with a company’s operations or business prospects.

Because it may be a “penny stock,” it will be more difficult for shareholders to sell shares of our common stock.

In addition, our common stock may be considered a “penny stock” under SEC rules because it has been trading on the OTC Bulletin Board at prices lower than $1.00. Broker-dealers who sell penny stocks must provide purchasers of these stocks with a standardized risk-disclosure document prepared by the SEC. This document provides information about penny stocks and the nature and level of risks involved in investing in the penny-stock market. A broker must also give a purchaser, orally or in writing, bid and offer quotations and information regarding broker and salesperson compensation, make a written determination that the penny stock is a suitable investment for the purchaser, and obtain the purchaser’s written agreement for the purchaser. Broker-dealers also must provide customers that hold penny stocks in their accounts with such broker-dealers a monthly statement containing price and market information relating to the penny stock. If a penny stock is sold to investors in violation of the penny stock rules, investors may be able to cancel the purchase and get the money back. The penny stock rules may make it difficult for investors to sell their shares of our stock, and because of these rules, there is less trading in penny stocks. Moreover, many brokers simply choose not to participate in penny-stock transactions. Accordingly, investors may not always be able to resell shares of our common stock publicly at times and at prices that investors feel are appropriate.

Our stock price is, and we expect it to remain, volatile, which could limit investors’ ability to sell stock at a profit.

Since the completion of the SRRE /CY-SRRE/LRY share exchange transactions the market price of our common stock has ranged from a high of $0.51 per share to a low of $0.01 per share in 2011. The volatile price of our stock makes it difficult for investors to predict the value of our investment, to sell shares at a profit at any given time, or to plan purchases and sales in advance. A variety of factors may affect the market price of our common stock. These include, but are not limited to:

a. Announcements of new technological innovations or new commercial services by our competitors or us;

b. Developments concerning proprietary rights;

c. Regulatory developments in Mainland China and foreign countries;

d. Period-to-period fluctuations in our revenues and other results of operations;

e. Economic or other crises and other external factors;

f. Changes in financial estimates by securities analysts; and

g. Sales of our common stock.

We will not be able to control many of these factors, and we believe that period-to-period comparisons of our financial results will not necessarily be indicative of our future performance.

The stock market in general has experienced extreme price and volume fluctuations that may have been unrelated and disproportionate to the operating performance of individual companies. These broad market and industry factors may seriously harm the market price of our common stock, regardless of our operating performance.

Because we have not paid and do not plan to pay cash dividends, investors will not realize any income from an investment in our common stock unless and until investors sell their shares at profit.

We did not pay cash dividends on our common stock in 2011, and we do not anticipate paying any cash dividends in the near future. Investors should not rely on an investment in our stock if they require dividend income. Further, investors will only realize income on an investment in our stock in the event they sell or otherwise dispose of their shares at a price higher than the price they paid for their shares. Such a gain would result only from an increase in the market price of our common stock, which is uncertain and unpredictable.

| 14 |

We intend to retain all of our earnings for use in our business and do not anticipate paying any cash dividends in the near future.

The payment of any future dividends will be at the discretion of the Board of Directors and will depend upon a number of factors, including future earnings, the success of our business activities, general financial condition, future prospects, general business conditions and such other factors as our Board of Directors may deem relevant.

RISKS RELATING TO THE REAL ESTATE INDUSTRY IN YANGTZE DELTA AND OTHER AREAS OF THE PRC

The real estate market in Yangtze Delta and other areas of the PRC is at an early stage of development.

We are subject to real estate market conditions in the PRC generally and Yangtze Delta in particular. Private ownership of property in the PRC is still at an early stage of development. Although there is a perception that economic growth in the PRC and the higher standard of living resulting from such growth will lead to a greater demand for private properties in the PRC, it is not possible to predict with certainty that such a correlation exists as many social, political, economic, legal and other factors may affect the development of the property market.The level of uncertainty is increased by the limited availability of accurate financial and market information as well as the overall low level of transparency in the PRC.

The PRC property market, including the Yangtze Delta property market, is volatile and may experience oversupply and property price fluctuations. The central and local governments frequently adjust monetary and other economic policies to prevent and curtail the overheating of the PRC and local economies, and such economic adjustments may affect the real estate market in Yangtze Delta and other parts of China. Furthermore, the central and local governments from time to time make policy adjustments and adopt new regulatory measures in a direct effort to control the over development of the real estate market in China, including Yangtze Delta. Such policies may lead to changes in market conditions, including price instability and an imbalance of supply and demand of residential properties, which may materially adversely affect our business and financial conditions. Also, there is no assurance that there will not be over development in the property sector in Yangtze Delta and other parts of China in the future. Any future over development in the property sector in Yangtze Delta and other parts of China may result in an oversupply of properties and a fall of property prices in Yangtze Delta or any of our other markets, which could adversely affect our business and financial condition. The lack of a liquid secondary market for residential property may discourage investors from acquiring new properties. The limited amount of property mortgage financing available to PRC individuals may further inhibit demand for residential developments.

Local government may issue further restrictive measures in the future.

In January, 2011, the Shanghai municipal government put forward a local restrictive policy. The policy prohibits residential housing purchases for 1) non-local residents, who are not able to provide a local tax payment or social security payment certificate over one year within the most recent two years, 2) local resident, who is already in possession of two residential units. The policy also limits residential housing purchases for 1) non-local residents, who are able to provide local tax payment certificate over one year, to only one unit, 2) local residents, who are already in possession of only one residential unit, to one additional residential unit.

We cannot assure you that the local government in Shanghai or Jiangsu Province will not issue further restrictive measures in the future. The local government’s restrictive regulations and measures could increase our operating costs in adapting to these regulations and measures, limit our access to capital resources or even restrict our business operations, which could further adversely affect our business and prospects.

We face increasing competition, which may adversely affect our revenues, profitability and results of operations.

In recent years, a large number of property companies have begun undertaking property sales and investment projects in Yangtze Delta and elsewhere in the PRC. Some of these property companies may have better track records and greater financial and other resources than we do. The intensity of the competition may adversely affect our business and financial position. In addition, the real estate market in Yangtze Delta and elsewhere in the PRC is rapidly changing. If we cannot respond to the changes in the market conditions more swiftly or effectively than our competitors do, our business and financial position will be adversely affected.

If the availability or attractiveness of mortgage financing were significantly limited, many of our prospective customers would not be able to purchase the properties, thus adversely affecting our business and financial position.

Mortgages are becoming increasingly popular as a means of financing property purchases in the PRC. An increase in interest rates may significantly increase the cost of mortgage financing, thus reducing the affordability of mortgages as a source of financing for residential property purchases. The PRC government has increased the down payment requirements and imposed certain other conditions that make mortgage financing unavailable or unattractive for some potential property purchasers. There is no assurance that the down payment requirements and other conditions will not be further revised. If the availability or attractiveness of mortgage financing is further significantly limited, many of our prospective customers would not be able to purchase the properties and, as a result, our business and future prospects would be adversely affected.

| 15 |

Our future prospects are heavily dependent on the performance of property sectors in specific geographical areas.

The properties we resell and intend to invest in are mainly based in Yangtze Delta. Our future prospects are, therefore, heavily dependent on the continued growth of the property sector around Yangtze Delta, and our business may be affected by any adverse developments in the supply and demand or housing prices in the property sector around Yangtze Delta.

The current level of property development and investment activity in Yangtze Delta and other markets is substantial. However, there is no assurance that such property resale and investment activity in Yangtze Delta or any of our other markets will continue at this level in the future or that we will be able to benefit from the future growth of these property markets.

Our revenues and operating income could be reduced by adverse conditions specific to our property locations.

The properties we resell and intend to invest in are concentrated geographically and are located predominately in Yangtze Delta. As a result, our business and our financial operating results may be materially affected by adverse economic, weather or business conditions in this area. Adverse conditions that affect these areas such as economic recession, changes in extreme weather conditions and natural disasters, may have an adverse impact on our operations.

RISKS RELATING TO THE PEOPLES REPUBLIC OF CHINA

All of our current prospects and deals are generated in Mainland China; thus all of our revenues are derived from our operations in the PRC. Accordingly, our business, financial condition, results of operations and prospects are subject, to a significant extent, to economic, political and legal developments in the PRC.

PRC economic, political policies and social conditions could adversely affect our business.

The economy of PRC differs from the economies of most developed countries in a number of respects, including the amount of government involvement, level of development, growth rate and control of foreign exchange and allocation of resources.

The PRC Government has been reforming the PRC economic system from planned economy to market oriented economy for more than 20 years, and has also begun reforming the government structure in recent years. These reforms have resulted in significant economic growth and social progress. Although we believe these reforms will have a positive effect on our overall and long-term development, we cannot predict whether any future changes in PRC’s political, economic and social conditions, laws, regulations and policies will have any adverse effect on our current or future business, results of operations or financial condition.

Changes in foreign exchange regulations may adversely affect our ability to pay dividends and could adversely affect our results of operations and financial condition.

Substantially all of our revenues and operating expenses are denominated in Renminbi. Conversion of Renminbi is under strict government regulation in the PRC. The Renminbi is currently freely convertible under the "current account", including trade and service related foreign exchange transactions and payment of dividends, but not under the "capital account", which includes foreign direct investment and loans. Under the existing foreign exchange regulations in the PRC, we will be able to pay dividends in foreign currencies without prior approval from the State Administration for Foreign Exchange by complying with certain procedural requirements. However, there is no assurance that the above foreign policies regarding payment of dividends in foreign currencies will continue in the future.

Fluctuation of the Renminbi could materially affect the value of, and dividends payable on, the common stock.

The value of the Renminbi is subject to changes in the PRC Government’s policies and depends to a large extent on China’s domestic and international economic and political developments, as well as supply and demand in the local market. Since 1994, the official exchange rate for the conversion of Renminbi to U.S. Dollars has generally been stable, and in 2005 the official exchange rate between U.S. Dollars and Renminbi had a little fluctuation. However, we cannot give any assurance that the value of the Renminbi will continue to remain stable against the U.S. Dollar or any other foreign currency. Since our income and profit are denominated in Renminbi, any devaluation of the Renminbi would adversely affect the value of, and dividends, if any, payable on, our shares in foreign currency terms.

Our operations could be adversely affected by changes in the political and economic conditions in the PRC. The PRC is our main market and accounted for all of our revenue. Therefore, we face risks related to conducting business in the PRC. Changes in the social, economic and political conditions of the PRC may adversely affect our business. Unfavorable changes in government policies, political unrest and economic developments may also have a negative impact on our operations.

Since the adoption of the “open door policy” in 1978 and the “socialist market economy” in 1993, the PRC government has been reforming and is expected to continue to reform its economic and political systems. Any changes in the political and economic policies of the PRC government may lead to changes in the laws and regulations or the interpretation of the same, as well as changes in the foreign exchange regulations, taxation and import and export restrictions, which may, in turn, adversely affect our financial performance. While the current policy of the PRC government seems to be one of imposing economic reform policies to encourage foreign investments and greater economic decentralization, we cannot assure that such a policy will continue to prevail in the future.

| 16 |

The PRC Legal System Embodies Uncertainties

The PRC legal system is a civil law system based on written statutes. Unlike common law systems, it is a system in which decided legal cases have little value as precedents. In 1979, the PRC Government began to promulgate a comprehensive system of laws and regulations governing economic matters in general. The overall effect of legislation over the past 28 years has significantly enhanced the protections afforded to various forms of foreign investment in Mainland China. Our PRC operating subsidiaries, wholly foreign-owned enterprises (“WFOEs”), are subject to laws and regulations applicable to foreign investment in the PRC in general and laws and regulations applicable to WFOEs in particular. However, these laws, regulations and legal requirements are constantly changing, and their interpretation and enforcement involve uncertainties. These uncertainties could limit the legal protections available to us and other foreign investors. In addition, we cannot predict the effect of future developments in the PRC legal system, including the promulgation of new laws, changes to existing laws or the interpretation or enforcement thereof, or the pre-emption of local regulations by national laws.

Our shareholders may not be able to enforce U.S. civil liabilities claims.

Our assets are located outside the United States and are held through subsidiaries incorporated under the laws of the Cayman Islands, British Virgin Islands and the PRC. Our current operations are conducted in the PRC. In addition, our directors and officers are residents of the PRC. As a result, it may be difficult for shareholders to implement service of process on these individuals. In addition, there is uncertainty as to whether the courts of China would recognize or enforce judgments of United States courts obtained against the Company or such persons predicated upon the civil liability provisions of the securities laws of the United States or any state thereof, or be competent to hear original actions brought in these countries against us or such persons predicated upon the securities laws of the United States or any state thereof.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. DESCRIPTION OF PROPERTY

We currently own our headquarter office space at No.638, Hengfeng Road,28th Floor, Shanghai, PRC. During 2011, our headquarter office was at Zhaojiabang Road, No. 333, 7th floor, Shanghai. We’ve also rented regional field support offices in various cities in Mainland China, namely Shanghai, Suzhou, Beijing, Yangzhou, Chongqing, Quanjiao, Hainan, Shangqiu, Chengdu, Linyi and Wuhan. We lease the facilities that house our regional field support offices. The average aggregate rental expense per month is $19,421.